DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. 13 April 2017 Asia Pacific/Japan Equity Research Automobiles & Components Auto, Auto Parts, Industrial & Consumer Electronics, Electronic Components Sector The Credit Suisse Connections Series leverages our exceptional breadth of macro and micro research to deliver incisive cross-sector and cross-border thematic insights for our clients. Research Analysts Masahiro Akita 81 3 4550 7361 [email protected] Koji Takahashi 81 3 4550 7884 [email protected] Hideyuki Maekawa 81 3 4550 9723 [email protected] Akinori Kanemoto 81 3 4550 7363 [email protected] Mika Nishimura 81 3 4550 7369 [email protected] Yoshiyasu Takemura 81 3 4550 7358 [email protected] Takuma Tsuji 81 3 4550 9815 [email protected] CONNECTIONS SERIES Automotive technology insights: Electrification, Automation, Informatization: Vol.4 Electrification update Figure 1: Auto electrification market coming into its own Source: Continental Automotive GmbH ■ Summary: We note an ever-increasing need for electrification in the auto sector since the publication of our first Connection Series report, Automotive technology insights: Electrification, Automation, Informatization: Vol.1 Electrification in 2014. Automakers are moving rapidly to shift resources toward electrification technology due partly to issues such as the need to meet near- and medium-term environmental regulations and Volkswagen’s emissions scandal. With the market actually coming into its own recently, we renew our focus on auto electrification technology and provide an update on the latest trends. ■ Key points: Having reviewed our outlook for the auto electrification market, we forecast the market to reach ¥35tn by 2030. Our outlook also points to a 31% weighting for electrified vehicles by 2030. As for market growth factors, we focus on (1) the adoption of 48V systems, particularly by automakers from Europe and the US, (2) stepped-up PHEV/EV launches by automakers including from Japan, and (3) potential electrification of auxiliary devices in tandem with the increase in voltage used in vehicles. We regard the present as a good opportunity to ride the auto electrification wave and lock-in value-added in both auto and non-auto sectors. ■ Auto electrification stocks under our coverage: Auto: Toyota Motor (7203), Nissan Motor (7201), Honda Motor (7267) Auto parts: Denso (6902), Aisin Seiki (7259), GS Yuasa (6674) Industrial electronics: Hitachi (6501) Electronic components: Nidec (6594), Murata Mfg. (6981), Rohm (6963) Consumer electronics: Panasonic (6752)

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

13 April 2017 Asia Pacific/Japan Equity Research

Automobiles & Components

Auto, Auto Parts, Industrial & Consumer Electronics, Electronic Components Sector

The Credit Suisse Connections Series leverages our exceptional breadth of macro and micro research to deliver incisive cross-sector and cross-border thematic insights for our clients.

Research Analysts Masahiro Akita 81 3 4550 7361

Koji Takahashi 81 3 4550 7884

Hideyuki Maekawa 81 3 4550 9723

Akinori Kanemoto 81 3 4550 7363

Mika Nishimura 81 3 4550 7369

Yoshiyasu Takemura 81 3 4550 7358

Takuma Tsuji 81 3 4550 9815

CONNECTIONS SERIES

Automotive technology insights: Electrification, Automation, Informatization: Vol.4 Electrification update Figure 1: Auto electrification market coming into its own

Source: Continental Automotive GmbH

■ Summary: We note an ever-increasing need for electrification in the auto sector since the publication of our first Connection Series report, Automotive technology insights: Electrification, Automation, Informatization: Vol.1 Electrification in 2014. Automakers are moving rapidly to shift resources toward electrification technology due partly to issues such as the need to meet near- and medium-term environmental regulations and Volkswagen’s emissions scandal. With the market actually coming into its own recently, we renew our focus on auto electrification technology and provide an update on the latest trends.

■ Key points: Having reviewed our outlook for the auto electrification market, we forecast the market to reach ¥35tn by 2030. Our outlook also points to a 31% weighting for electrified vehicles by 2030. As for market growth factors, we focus on (1) the adoption of 48V systems, particularly by automakers from Europe and the US, (2) stepped-up PHEV/EV launches by automakers including from Japan, and (3) potential electrification of auxiliary devices in tandem with the increase in voltage used in vehicles. We regard the present as a good opportunity to ride the auto electrification wave and lock-in value-added in both auto and non-auto sectors.

■ Auto electrification stocks under our coverage: Auto: Toyota Motor (7203), Nissan Motor (7201), Honda Motor (7267) Auto parts: Denso (6902), Aisin Seiki (7259), GS Yuasa (6674) Industrial electronics: Hitachi (6501) Electronic components: Nidec (6594), Murata Mfg. (6981), Rohm (6963) Consumer electronics: Panasonic (6752)

13 April 2017

Auto, Auto Parts, Industrial & Consumer Electronics, Electronic Components Sector 2

Table of contents Electrification, automation, and informatization 3

Automotive technology trends mainly in three fields ................................................ 3

Renewing focus on electrification technology 4

Auto electrification market coming into its own ........................................................ 4

Ideal approach for engine load reduction and linear control .................................... 5

HEVs, PHEVs, EVs, and FCEVs take pride of place among technologies to reduce

engine loading .......................................................................................................... 8

Environmental regulations drive auto technology trends ......................................... 9

Auto electrification market outlook ......................................................................... 13

Electrification market trends (1): 48V systems seen as stopgap ahead of 2021

CO2 regulations...................................................................................................... 17

Electrification market trends (2): Full-fledged launch of PHEVs, EVs starting ....... 20

Electrification market trends (3): A good outlook for electrification as it spreads to

auxiliary equipment ................................................................................................ 23

Increase in electronics bodes well for Japan’s tech sector .................................... 27

Electrified vehicle developments by automaker 30

Valuations growing as electrified vehicle model launches speed up ..................... 30

Toyota Motor .......................................................................................................... 33

Nissan Motor .......................................................................................................... 36

Honda Motor ........................................................................................................... 38

Other Japanese automakers .................................................................................. 40

Overseas automakers ............................................................................................ 42

Electrification supply chain trend 45

Denso ..................................................................................................................... 45

Aisin Seiki ............................................................................................................... 46

Hitachi ..................................................................................................................... 49

Nidec ...................................................................................................................... 49

Murata Manufacturing ............................................................................................ 53

Rohm ...................................................................................................................... 58

Panasonic ............................................................................................................... 62

GS Yuasa ............................................................................................................... 62

13 April 2017

Auto, Auto Parts, Industrial & Consumer Electronics, Electronic Components Sector 3

Electrification, automation, and informatization Automotive technology trends mainly in three fields Cross-sector report series on electronics, automation, and informatization Trends in automotive technology are increasingly focused on the three areas of electrification, automation, and informatization as offering ways to boost environmental performance and enhance user safety and comfort. In addition to researching these three areas, we are conducting cross-sector research aimed at highlighting the important trends within automotive supply chains, while also focusing on specific individual stocks in sectors such as industrial electronics, electronic components, and consumer electronics that are playing critical roles in automotive technology. This—the fourth report in a series of cross-sector Connections reports that examine sectors relating to the three growth areas of electrification, automation, and informatization as they are applied in the automotive field—follows our initial offering, Automotive technology insights: Electrification, Automation, Informatization: Vol.1 Electrification, which focused on electrification technologies, and our second report, Automotive technology insights: Electrification, Automation, Informatization: Vol.2 Automation, which focused on automation technologies, and Automotive technology insights: Electrification, Automation, Informatization: Vol.3 Informatization. In this installment, we update the latest trend toward Electrification.

Delivering increased environmental performance, safety, and comfort A typical vehicle consists of 20,000 to 30,000 parts, all of which are designed to deliver the environmental performance, safety, and comfort demanded either by users or automakers. The evolution of automobiles can be viewed in terms of the continuous improvement of the various systems and modules that make up the powertrain, drivetrain, brake and chassis, and body (exterior and interior) of the vehicle to deliver increased levels of satisfaction for these three elements.

Non-automotive sector supplying high-value-added products in three fields In automotive supply chains, it is the value added to specific parts, systems, and modules that is exerting the major influence on technical trends. The key value creators and drivers of these trends are the companies capable of supplying parts, systems and modules vital to the increasing use of electronics, automation, and informatization by automakers. As the value added via these three trends grows, industrial electronics, electronic components, and consumer electronics players within other non-automotive sectors are seeing their scope of operations increasingly spread out into the automotive sphere. This is almost self-evident, given the increasing adoption of computers, sensors, and electric motors in passenger vehicles. We see players outside of the automotive sector leading some of the shift in auto-related technical value creation, which in turn should generate increasing growth potential for such companies from auto-related operations.

13 April 2017

Auto, Auto Parts, Industrial & Consumer Electronics, Electronic Components Sector 4

Renewing focus on electrification technology Auto electrification market coming into its own We provide an update on the latest trends in the area of auto electrification in a follow up to Vol.1 of this series We note an ever-increasing need for electrification in the auto sector since the publication of our first Connection Series report, Automotive technology insights: Electrification, Automation, Informatization: Vol.1 Electrification in 2014. With the rollout of ZEV regulations in California in 2018 and the EU’s 2021 CO2 emissions regulations, moves toward stricter environmental regulations continue to gain momentum in key markets. As highlighted by China’s NEV policy, the need for compliance with environmental regulations is also growing in the emerging markets. In addition to meeting near- and medium-term environmental regulations, issues such as Volkswagen’s emissions scandal have prompted not only Japanese automakers but also those from the EU and the US to rapidly shift resources toward auto electrification. With the market actually coming into its own recently, we think it is worth renewing our focus on auto electrification technology.

Figure 2: Auto electrification market coming into its own

Source: Continental Automotive GmbH

Focusing on switch to 48V systems, full-fledged launches of PHEVs, EVs, electrification of auxiliary equipment Having revised our electrification market forecasts we expect the market to expand to around ¥35tn in 2030. We think electrified vehicles will account for 31% of all cars on the road in that year. Among the factors supporting electrification market expansion, we are focusing on (1) adoption of 48V systems, especially by European and US carmakers, (2) full-fledged launches of PHEVs and EVs, including by Japanese carmakers, and (3) electrification of auxiliary equipment due to the adoption of higher-voltage electrical systems in automobiles. Systems that use 48V are mild hybrid systems that use 48V power supplies. Adoption of 48V systems by carmakers, especially European and US companies, has suddenly taken off ahead of achievement of the 2021 CO2 emission target in Europe of 95g/km. In parallel, carmakers, including Japanese companies, have started

13 April 2017

Auto, Auto Parts, Industrial & Consumer Electronics, Electronic Components Sector 5

to ramp up PHEV and EV launches, which is a radical way of meeting the target. Typical recent examples with regard to Japanese makers include the launch of the remodeled Toyota Prius PHV and the company's announcement that it will set up an EV business planning department. In terms of the impact of this on supply chains, we note the trend toward electrification of secondary auxiliary equipment due to the shift to higher voltage systems. As such systems generate surplus power, we see substantial scope to replace actuators that have to date depended on engine power with electric actuators, with which linear control is possible. We see golden opportunities for auto and non–auto sector companies to tap added value by riding the electrification wave.

Ideal approach for engine load reduction and linear control Key applications are powertrain electrification, X-by-Wire, and boosting efficiency of auxiliary systems Electrification of automotive parts, systems and modules is proving relentless. In broad terms, the advantages are linear control and reduction of engine load. Engine load reduction is a way of mitigating dependence on the energy produced by the engine. In this area, electronic components are being used to replace traditional hydraulic or other mechanical systems. The most developed systems for engine load reduction can be found in the powertrains used in HEV/EV/FCEV vehicles, 48V systems categorized in mild-hybrids, or idling stop systems (ISS).

Linear control of motorized systems is also growing in importance as demand increases for parts, systems and modules with more advanced specifications. The prime example of this is “X-by-Wire” applications that use electrical signals to control the throttle, brakes or steering. Other linear control applications include using the technology to boost the efficiency of various types of auxiliary components. Converting pumps, air-conditioning compressors and other auxiliary parts from mechanical to electronic control not only saves the energy produced by the engine for use in the drivetrain, but also enables more efficient control. This enhances environmental performance as well as safety and comfort, which we think implies that this trend is likely to persist.

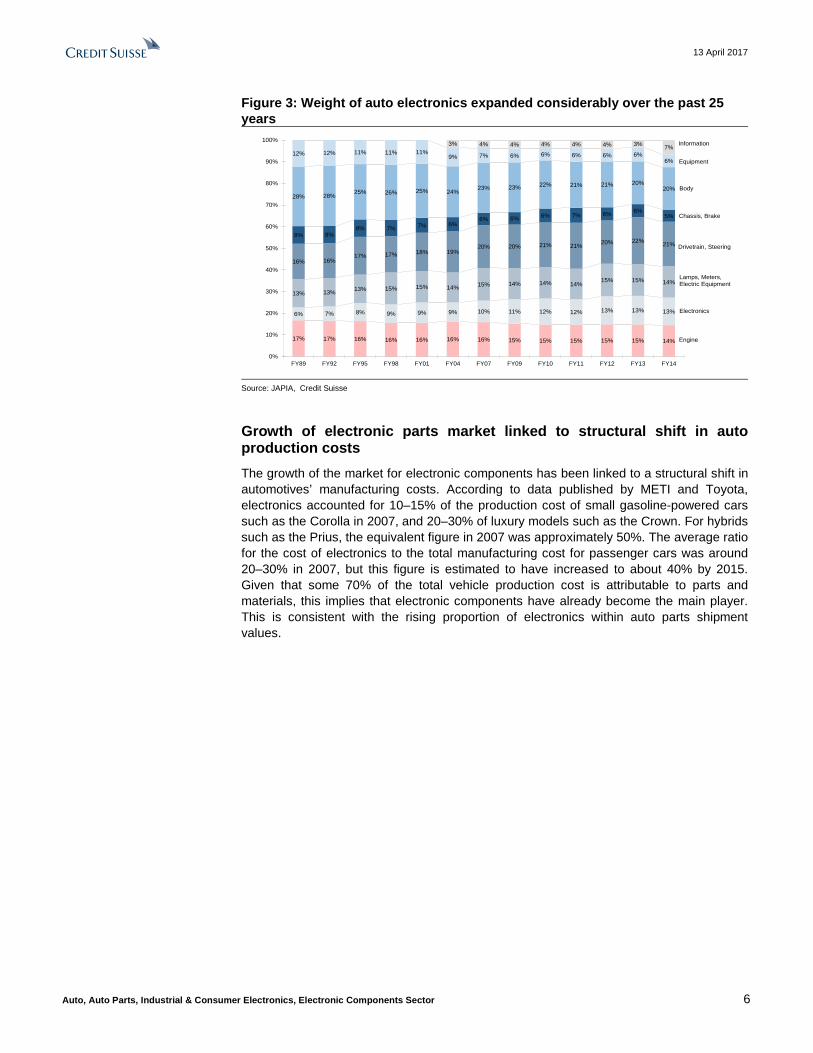

Data confirm expansion of market for electronic components We can track the long-term trends in automotive technology using the shipment value data published by the Japan Auto Parts Industries Association (JAPIA). The trend toward more use of electronic components can be seen between FY3/90 and FY3/15 by the increasing contribution of electronics to overall auto parts shipment value. Accounting for just 6% of auto parts shipments by value in FY3/90, electronics had grown to 13% by FY3/15. Note that the other sector registering significant growth is drivetrain and steering components. Body components are the sector that has lost out most noticeably.

We believe the gap in value-added between auto parts suppliers is due largely to the type of components they handle or technology domain to which their system belongs. Furthermore, amid the transformation in auto technology trends, there could also be a change in the value-added accepted by automakers in a specific technology domain. The increasingly limited scope to tack on additional costs to the sales price means automakers could discontinue technology that they see as contributing little in the way of value-added or cost reductions associated with such technology. Resulting in conclusion in which, suppliers’ topline/profit growth would be determined by whether they belong in the specific technology domain with growth or already mature market, regardless of auto or non-auto sector, and by their intensity of involvement with adding values to their products.

13 April 2017

Auto, Auto Parts, Industrial & Consumer Electronics, Electronic Components Sector 6

Figure 3: Weight of auto electronics expanded considerably over the past 25 years

Source: JAPIA, Credit Suisse

Growth of electronic parts market linked to structural shift in auto production costs The growth of the market for electronic components has been linked to a structural shift in automotives’ manufacturing costs. According to data published by METI and Toyota, electronics accounted for 10–15% of the production cost of small gasoline-powered cars such as the Corolla in 2007, and 20–30% of luxury models such as the Crown. For hybrids such as the Prius, the equivalent figure in 2007 was approximately 50%. The average ratio for the cost of electronics to the total manufacturing cost for passenger cars was around 20–30% in 2007, but this figure is estimated to have increased to about 40% by 2015. Given that some 70% of the total vehicle production cost is attributable to parts and materials, this implies that electronic components have already become the main player. This is consistent with the rising proportion of electronics within auto parts shipment values.

17% 17% 16% 16% 16% 16% 16% 15% 15% 15% 15% 15% 14%

6% 7% 8% 9% 9% 9% 10% 11% 12% 12% 13% 13% 13%

13% 13% 13% 15% 15% 14% 15% 14% 14% 14%15% 15% 14%

16% 16%17% 17% 18% 19%

20% 20% 21% 21% 20% 22% 21%8% 8%

8% 7% 7% 6%6% 6% 6% 7% 6% 6%

5%

28% 28% 25% 26% 25% 24% 23% 23% 22% 21% 21% 20%20%

12% 12% 11% 11% 11%9% 7% 6% 6% 6% 6% 6%

6%

3% 4% 4% 4% 4% 4% 3% 7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY89 FY92 FY95 FY98 FY01 FY04 FY07 FY09 FY10 FY11 FY12 FY13 FY14

Information

Equipment

Body

Chassis, Brake

Drivetrain, Steering

Lamps, Meters,Electric Equipment

Electronics

Engine

13 April 2017

Auto, Auto Parts, Industrial & Consumer Electronics, Electronic Components Sector 7

Figure 4: Electronic components generate a rising proportion of auto manufacturing costs

Source: METI, Toyota Motor, Credit Suisse

Historical overview of automotive electronics Now growing rapidly, the market for electronics used in automotive applications originated in the 1960s with the introduction of limited electronic parts such as lights, starters, alternators, voltage regulators and igniters. The 1970s saw the passage of the Muskie Act in the US to control exhaust emissions; fresh demand for greater fuel efficiency in response to the twin oil shocks; and the introduction of more electronics in the engine field as computing power increased. Adoption of electronic technologies started to take off in the 1980s and 1990s with the development of innovative advances such as electronically controlled automatic transmissions, anti-lock braking systems (ABS), electronically controlled suspension, electronic power steering, airbags, electric windows, and powered seating controls. These technologies were aimed at enhancing the basic vehicular functions of moving, steering and braking, as well as improving the safety and comfort of users. Since 2000, we have seen acceleration in the introduction of automotive electronics, led by the development of HEV (hybrids), EV (pure-electric vehicles), PHEV (plug-in hybrids), and FCEV (fuel cell electric vehicles).

10ー15

20-30

50

20-30

40

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Small GasolineCar (Corolla)

Luxury GasolineCar (Crown)

HV (Prius) 2007 Average 2015 Average

Electronic Components Other Components

13 April 2017

Auto, Auto Parts, Industrial & Consumer Electronics, Electronic Components Sector 8

Figure 5: Automotive electronics/motorization technology progress

Source: JSAE, Credit Suisse

HEVs, PHEVs, EVs, and FCEVs take pride of place among technologies to reduce engine loading Electrification of powertrains critical if environmental standards are to be met We think automakers must redouble their commitment to technological development supporting improved fuel efficiency, keeping as a yardstick the EU’s 95g/km average CO2 emission target for 2021. To lower fuel consumption and achieve greater fuel efficiency, we think automakers will need to take a multi-pronged approach. In our view the main approaches are likely to be "improving internal combustion engines," "improving energy efficiency,” “reducing the engine weight,” and “reducing the engine load.” Reducing the engine load is primarily a means of curbing the vehicle’s reliance on energy produced by the engine; for the most part, we think this will be achieved by electrifying systems that have traditionally been mechanical (often hydraulic). Among technologies geared toward reducing the engine’s load, powertrain electrification—delivering eco-friendly cars such as HEVs, EVs (including PHEVs), and FCEVs—is likely to retain pride of place for the time being. We believe powertrain electrification is critical if automakers are to remain compliant with environmental regulations.

13 April 2017

Auto, Auto Parts, Industrial & Consumer Electronics, Electronic Components Sector 9

Figure 6: Key technology areas involved in fuel efficiency

Source: JSAE, Credit Suisse

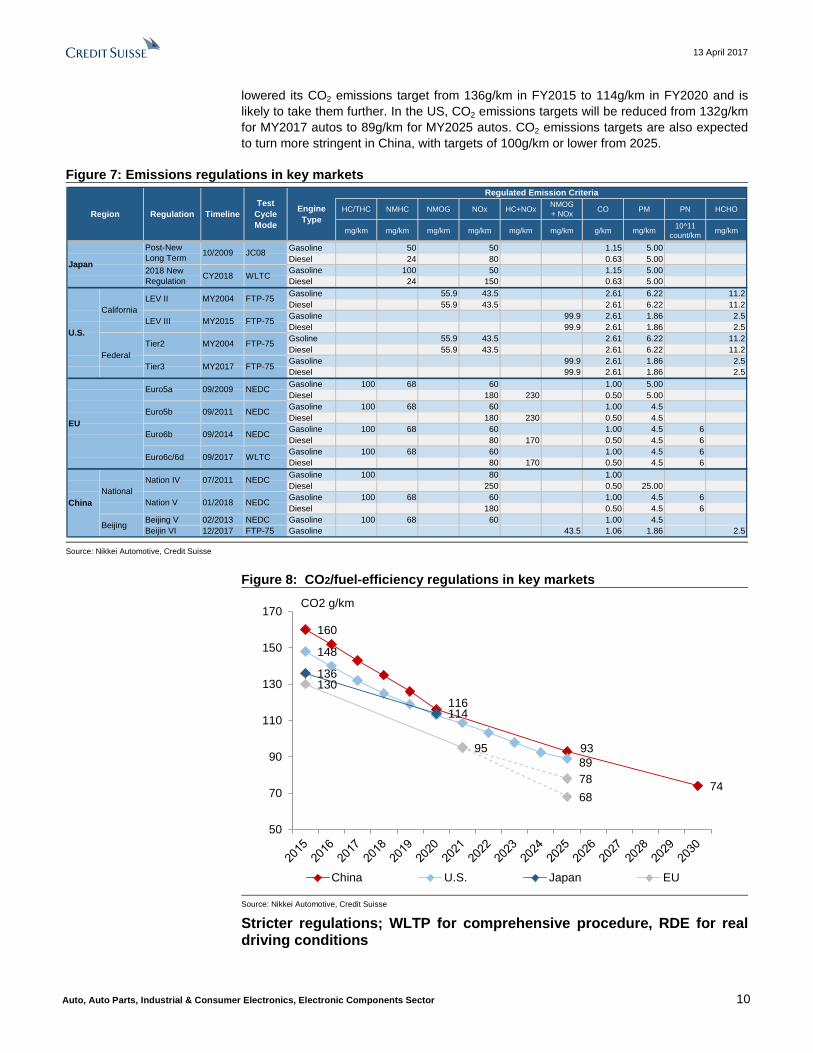

Environmental regulations drive auto technology trends Emissions regulations and CO2/fuel-efficiency regulations Environmental regulations tend to exert a significant influence on auto technology trends and can be broadly divided into two categories: (1) emissions regulations aimed at reducing nitrogen oxides (NOx) and particulate matter (PM) as seen in Euro regulations, tier regulations in the US, and Post New Long-term Emission Regulations in Japan, and (2) CO2 emissions/fuel-efficiency regulations as seen in Europe’s EC 443/2009 and Japan’s fuel-efficiency standards based on the Energy Savings Act. Emissions regulations are intended for reducing NOx, HC, CO, and PM in auto emissions, a by-product of internal combustion in autos. Japan, Europe, and the US lean toward tighter emissions regulations, and China and other emerging economies are following.

With the rollout of Euro 3 regulations in Europe, Tier 2 regulations in the US, and the new short-term emissions requirements in Japan, emissions regulations have grown increasingly stringent since 2000. Euro regulations, which consist of six levels up to Euro 6, require pollutants to be effectively reduced to less than half of the permitted levels of 2000. Regulations have also been tightened in the US with MY2017 autos coming under EPA’s Tier 3; in California, the California Air Resources Board (CARB) has introduced LEV III regulations starting with MY2015 autos. After starting with the new short-term emissions requirements in 2009, Japan moved to the new long-term emissions regulations and eventually to the Post New Long-Term Emission Regulations. Faced with alarming levels of air pollution, China put emissions IV regulations in force at the national level starting 2011 and has also introduced the new Beijing V emissions standard for the capital city.

In CO2/fuel-efficiency regulations, the EU's CO2 emissions targets have emerged as leading indicators—Europe aims to reduce CO2 from 130g/km in 2015 to 95g/km in 2021, and in addition to setting its 2025 CO2 emissions target at 68–78g/km, it will also seek to keep CO2 emissions reductions at similar levels in 2030 and beyond. Japan has also

13 April 2017

Auto, Auto Parts, Industrial & Consumer Electronics, Electronic Components Sector 10

lowered its CO2 emissions target from 136g/km in FY2015 to 114g/km in FY2020 and is likely to take them further. In the US, CO2 emissions targets will be reduced from 132g/km for MY2017 autos to 89g/km for MY2025 autos. CO2 emissions targets are also expected to turn more stringent in China, with targets of 100g/km or lower from 2025.

Figure 7: Emissions regulations in key markets

Source: Nikkei Automotive, Credit Suisse

Figure 8: CO2/fuel-efficiency regulations in key markets

Source: Nikkei Automotive, Credit Suisse

Stricter regulations; WLTP for comprehensive procedure, RDE for real driving conditions

HC/THC NMHC NMOG NOx HC+NOx NMOG+ NOx CO PM PN HCHO

mg/km mg/km mg/km mg/km mg/km mg/km g/km mg/km 10^11 count/km mg/km

Gasoline 50 50 1.15 5.00Diesel 24 80 0.63 5.00Gasoline 100 50 1.15 5.00Diesel 24 150 0.63 5.00Gasoline 55.9 43.5 2.61 6.22 11.2Diesel 55.9 43.5 2.61 6.22 11.2Gasoline 99.9 2.61 1.86 2.5Diesel 99.9 2.61 1.86 2.5Gsoline 55.9 43.5 2.61 6.22 11.2Diesel 55.9 43.5 2.61 6.22 11.2Gasoline 99.9 2.61 1.86 2.5Diesel 99.9 2.61 1.86 2.5Gasoline 100 68 60 1.00 5.00Diesel 180 230 0.50 5.00Gasoline 100 68 60 1.00 4.5Diesel 180 230 0.50 4.5Gasoline 100 68 60 1.00 4.5 6Diesel 80 170 0.50 4.5 6Gasoline 100 68 60 1.00 4.5 6Diesel 80 170 0.50 4.5 6Gasoline 100 80 1.00Diesel 250 0.50 25.00Gasoline 100 68 60 1.00 4.5 6Diesel 180 0.50 4.5 6

Beijing V 02/2013 NEDC Gasoline 100 68 60 1.00 4.5Beijin VI 12/2017 FTP-75 Gasoline 43.5 1.06 1.86 2.5

Region Regulation TimelineTest

Cycle Mode

Engine Type

Regulated Emission Criteria

Post-New Long Term2018 New Regulation

10/2009

CY2018

JC08

WLTCJapan

U.S.

California

Federal

LEV II

LEV III

Tier2

Tier3

MY2004

MY2015

MY2004

MY2017

FTP-75

FTP-75

FTP-75

FTP-75

EU

ChinaNational

Beijing

Euro5a

Euro5b

Euro6b

Euro6c/6d

Nation IV

Nation V

09/2011

NEDC

NEDC

07/2011

WLTC

09/2014

NEDC

09/2009

01/2018

NEDC

09/2017

NEDC

160

116

93

74

148

89

136

114

130

95

7868

50

70

90

110

130

150

170

China U.S. Japan EU

CO2 g/km

13 April 2017

Auto, Auto Parts, Industrial & Consumer Electronics, Electronic Components Sector 11

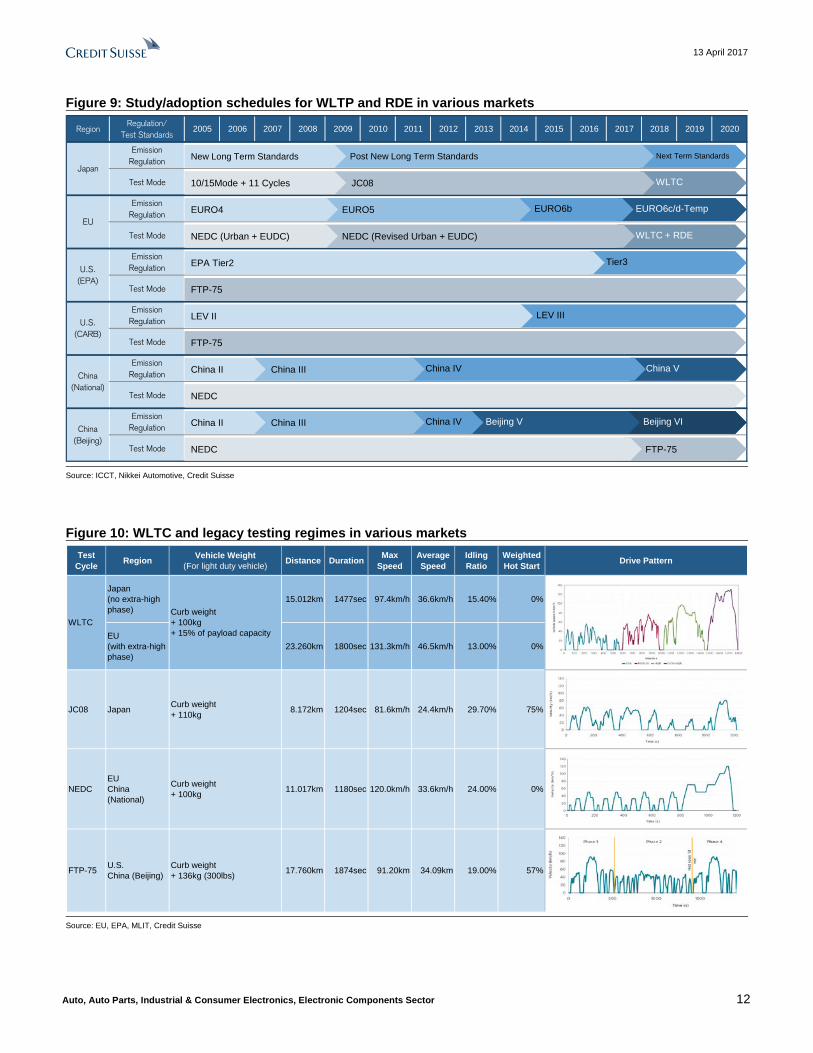

Environmental regulations such as emissions and CO2/fuel-efficiency regulations tend to vary by country. Each country has established its own measures for checking compliance to these regulations and has separate test procedures for measuring vehicles’ environmental performance. For example, test procedures include the New European Driving Cycle (NEDC) in Europe, JC08 in Japan, and FTP-75 in the US. Automakers are forced to bear an enormous burden in development man-hours and costs to meet regulations and test procedures in each market, and we believe this was one of the key impetus for the recent VW diesel scandal. However, we already see moves, particularly in Europe and Japan, toward the introduction of the Worldwide harmonized Light Vehicles Test Procedure (WLTP), which aims to reduce the burden of automakers through the establishment of uniform test procedures worldwide.

WLTP aims to be a comprehensive test procedure that can be used across the globe as it incorporates driving conditions in individual countries or markets. Another salient point of WLTP versus previous test procedures is its easily enforceable standards that mimic real driving conditions. The Working Party on Pollution and Energy (GRPE), a part of the United Nations Economic Commission for Europe, took the lead in establishing specifics for the Worldwide-harmonized Light-duty Test Cycle (WLTC), the specific test mode of WLTP. Europe, Japan, US, China, India, and South Korea are currently considering its adoption. WLTC is due for rollout in Europe starting September 2017 and during 2018 in Japan.

Furthermore, an introduction of RDE (Real Driving Emissions) is in preparation, aiming to capture the so-called “off-cycle mode” outside the previously used testing cycles. RDE involves using vehicles fitted with PEMS (portable emissions measurement system) devices to measure environmental performance under actual driving conditions. Relative to the conventional bench testing approach, RDE on-road vehicle testing results in a dramatic increase in the number of variables involved in the testing process. In turn, this makes it far more difficult to develop defeat devices that could rig such tests. The EU has taken the lead in developing the RDE concept, which is expected to be incorporated into the Euro 6d-TEMP emissions standard that is due to be implemented in September 2017 at the same time as the Euro 6c emissions regulations. In Japan, the Ministry of Land, Infrastructure, Transport and Tourism (MLIT) and the Ministry of the Environment (MOE) plan to consider revising the emissions testing methodology for diesel-powered vehicles based on an RDE feasibility study, using statistical sampling to compare on-road test results against the data produced by the conventional bench testing approach.

13 April 2017

Auto, Auto Parts, Industrial & Consumer Electronics, Electronic Components Sector 12

Figure 9: Study/adoption schedules for WLTP and RDE in various markets

Source: ICCT, Nikkei Automotive, Credit Suisse

Figure 10: WLTC and legacy testing regimes in various markets

Source: EU, EPA, MLIT, Credit Suisse

RegionRegulation/

Test Standards2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Emission Regulation

Test Mode

Emission Regulation

Test Mode

Emission Regulation

Test Mode

Emission Regulation

Test Mode

Emission Regulation

Test Mode

Emission Regulation

Test Mode

Japan

EU

U.S.(EPA)

U.S.(CARB)

China(National)

China(Beijing)

FTP-75

Beijing VI

EURO6c/d-Temp

WLTC

Next Term StandardsPost New Long Term StandardsNew Long Term Standards

JC0810/15Mode + 11 Cycles

EURO6bEURO5EURO4

WLTC + RDENEDC (Revised Urban + EUDC)NEDC (Urban + EUDC)

Tier3EPA Tier2

FTP-75

LEV IIILEV II

FTP-75

China VChina IVChina IIIChina II

Beijing VChina IVChina IIIChina II

NEDC

NEDC FTP-75

Beijing VI

EURO6c/d-Temp

WLTC

Next Term StandardsPost New Long Term StandardsNew Long Term Standards

JC0810/15Mode + 11 Cycles

EURO6bEURO5EURO4

WLTC + RDENEDC (Revised Urban + EUDC)NEDC (Urban + EUDC)

Tier3EPA Tier2

FTP-75

LEV IIILEV II

FTP-75

China VChina IVChina IIIChina II

Beijing VChina IVChina IIIChina II

NEDC

NEDC

Test Cycle Region Vehicle Weight

(For light duty vehicle) Distance Duration Max Speed

Average Speed

Idling Ratio

Weighted Hot Start Drive Pattern

Japan(no extra-high phase)

15.012km 1477sec 97.4km/h 36.6km/h 15.40% 0%

EU(with extra-high phase)

23.260km 1800sec 131.3km/h 46.5km/h 13.00% 0%

JC08 Japan Curb weight+ 110kg 8.172km 1204sec 81.6km/h 24.4km/h 29.70% 75%

NEDCEUChina (National)

Curb weight+ 100kg 11.017km 1180sec 120.0km/h 33.6km/h 24.00% 0%

FTP-75 U.S.China (Beijing)

Curb weight + 136kg (300lbs) 17.760km 1874sec 91.20km 34.09km 19.00% 57%

WLTCCurb weight+ 100kg + 15% of payload capacity

13 April 2017

Auto, Auto Parts, Industrial & Consumer Electronics, Electronic Components Sector 13

Auto electrification market outlook Auto electrification market likely to reach ¥35tn by 2030 We update our outlook for the auto electrification market. We forecast the market to reach ¥35tn in 2030. We expect progress in powertrain electrification spurred by stricter environmental regulations to drive growth in the auto electrification market. In addition to growth in core components such as motors and batteries as a result of the higher penetration of various types of electric vehicles—including HEVs, PHEVs, EVs, and FCEVs—we also look at secondary effects including greater electrification in auxiliary equipment due to greater voltage and electric capacitance per vehicle. Using CO2 regulatory guidelines in various markets, we forecast volume trends for legacy autos with internal combustion engines (ICE), 48V HEVs (mild-hybrid autos using 48V electric power), full-hybrid vehicles (HEV), plug-in hybrid vehicles (PHEV), electric vehicles (EV), and fuel cell electric vehicles (FCEV). We include legacy integrated starter generator (ISG) systems running on 12V electric power as an HEV. We calculate the potential market size in 2030 based on estimated electric unit price per vehicle in each of the above categories.

Our outlook shows the market share held by electrified vehicles’ (48V HEV, HEV, PHEV, EV, and FCEV) rising to 31% in 2030. By type, we see growth in 48V HEV mild hybrids heading into 2020 and forecast market growth for EV and PHEV as stricter regulations come into force heading towards 2030. We see a growing need for 48V HEVs as the most efficient means for attaining the EU’s 2021 emission guideline (CO2 95g/km). We also anticipate a boost in the electrification of auxiliary equipment in conjunction with the jump in automotive battery voltage from 12V to 48V. Assuming the EU’s CO2 emission guideline is lowered to 60g/km heading towards 2030, we think it will be difficult to meet regulatory requirements just through expansion of 48V HEVs. We accordingly foresee greater impetus for the adoption of PHEVs and EVs after reasonable progress in 48V HEVs. In light of the above, we anticipate demand growth for high-value-added electric components including high-output motors and batteries.

Figure 11: Auto electrification market to reach ¥35tn in 2030; proportion of electrified vehicles likely to reach 31%

Source: IHS, Marklines, LMC Automotive, Credit Suisse estimates

0%

5%

10%

15%

20%

25%

30%

35%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Auto Electrification Market (LHS) Electrification rate (RHS)

Biilion Yen

13 April 2017

Auto, Auto Parts, Industrial & Consumer Electronics, Electronic Components Sector 14

Figure 12: Global volume outlook for electrified vehicles

Figure 13: Electrified vehicle ratio and fleet-average CO2 emissions

Source: IHS, Marklines, LMC Automotive, Credit Suisse estimates Source: IHS, Marklines, LMC Automotive, Credit Suisse estimates

Spotlight on HEV in the Japanese auto electrification market Among developed nations, the Japanese auto market probably boasts the best fleet average CO2 emission levels at present, which we attributable to a predominately high ratio of mini-vehicles and HEV in the Japanese market. Another factor contributing to Japan’s favorable fleet average CO2 emissions is the prevalence of mild hybrids among mini-vehicles, where we see a notably high use of ISG systems running on 12V. Japan’s fleet average CO2 emissions, derived from the fuel efficiency in each passenger vehicle category (weighted average CO2 emission for the entire vehicle sales volume) is estimated at around 109g/km. However, Japan’s CO2 target was 137g/km in 2015 and is set to 114g/km for 2020. We think targets at this the level, which appear rather lax compared with those in the EU, can be easily met with the model mix currently available in the market. Thus, while Japan continues to see a high ratio of mini-vehicles and HEVs, there appears to be little incentive for it to pursue extreme levels of auto electrification. We estimate that the proportion of electrified vehicles in Japan will rise to 49% in 2030, but expect HEVs including mild hybrids using legacy 12V ISG systems to account for a full 42% of the total.

Figure 14: Hybrid vehicles accounting for almost all of Japan’s electrified

Figure 15: Japanese market ahead of CO2 guidelines due to a high HEV/mini-vehicle ratio

Source: IHS, Marklines, LMC Automotive, Credit Suisse estimates Source: IHS, Marklines, LMC Automotive, Credit Suisse estimates

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

FCEV EV PHEV HEV 48V-HEV

Thousand Units

0%

5%

10%

15%

20%

25%

30%

35%

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

Global Weighted Fleet Average CO2 (LHS) Electrified Vehicle Ratio (RHS)

CO2 g/km Electrified Vehicle Ratio

0

500

1,000

1,500

2,000

2,500

FCEV EV PHEV HEV 48V-HEV

Thousand Units

0%

10%

20%

30%

40%

50%

60%

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

Japan Fleet Average CO2 (LHS) Japan Regulated CO2 Guideline (LHS)Japan Electrified Vehicle Ratio (RHS)

CO2 g/km Electrified Vehicle Ratio

13 April 2017

Auto, Auto Parts, Industrial & Consumer Electronics, Electronic Components Sector 15

North American CO2 emission guidelines to tighten in stages coinciding with ZEV regulations; large models to take large proportion of market with PHEV/EV Due in part to the popularity of pickup trucks, the North American market has a predominately high ratio of large vehicles over other developed nations, but it is also estimated to have highest fleet average CO2 emission levels. In the North American market, D segment and above (excluding electrified vehicles) represent nearly half of all new sales. Auto electrification remains at modest levels, accounting for just a few percent. The CO2 regulatory value in the US was 150g/km (CO2 equivalent) in 2015, in line with the market’s skew toward large vehicles. However, given plans to tighten carbon emissions to 93g/km by 2025 in the US, emission regulations in this market could turn stricter than those in Japan. Furthermore, the state of California plans to expand Zero Emission Vehicle (ZEV) regulations to cover almost all automakers after 2018. The regulation will make it mandatory for automakers have a certain proportion of unit sales in ZEVs or purchase carbon credits to offset the shortfall. Only EVs and FCEVs with zero tailpipe pollution qualify as ZEV, but as it may be difficult to meet the standard through these vehicles alone, we see a likelihood of PHEV being added to the ZEV list. Still, legacy HEVs do not qualify as ZEVs. We think this situation will inevitably lead to growth in PHEV and EV weightings over time. While certain issues remain such as electrification of the popular pickup trucks, we expect a sustained growth in auto electrification centered on PHEVs and EVs.

Figure 16: Compliance with ZEV regulations could lead to PHEV/EV growth

Figure 17: North American fleet-averageCO2 emissions and regulatory guidelines

Source: IHS, Marklines, LMC Automotive, Credit Suisse estimates Source: IHS, Marklines, LMC Automotive, Credit Suisse estimates

With the strictest CO2 regulations, EU should see gradual growth in 48V and PHEV The EU, which has the strictest CO2 regulations globally, has set the average CO2 emissions target at 95g/km. While the market leads others in the adoption of electrified vehicles such as PHEVs and EVs, we also note progress in the development of 48V HEVs (mild hybrids using 48V electric power) to replace the existing ICE-based vehicles for attaining the region’s 2021 CO2 regulatory value. The region apparently lags in full hybrid vehicles such as those rolled out by Toyota and Honda, but we believe the objective here is to rollout 48V HEVs, a less expensive option, as a bridge strategy until 2021 regulations take effect rather than matching Japan on the technology side. While 48V HEV’s improvement in fuel efficiency ratios is lower than that of full hybrids, the technology is likely to gain focus as an effective method for achieving regulatory compliance as it keeps down additional costs at less than half. However, Europe is considering a CO2 regulatory guideline of 60g/km by 2030. We believe it will be difficult to meet the regulatory norm in

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

FCEV EV PHEV HEV 48V-HEV

Thousand Units

0%

5%

10%

15%

20%

25%

30%

35%

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

NA Fleet Average CO2 (LHS) NA Regulated CO2 Guideline (LHS)NA Electrified Vehicle Ratio (RHS)

CO2 g/km Electrified Vehicle Ratio

13 April 2017

Auto, Auto Parts, Industrial & Consumer Electronics, Electronic Components Sector 16

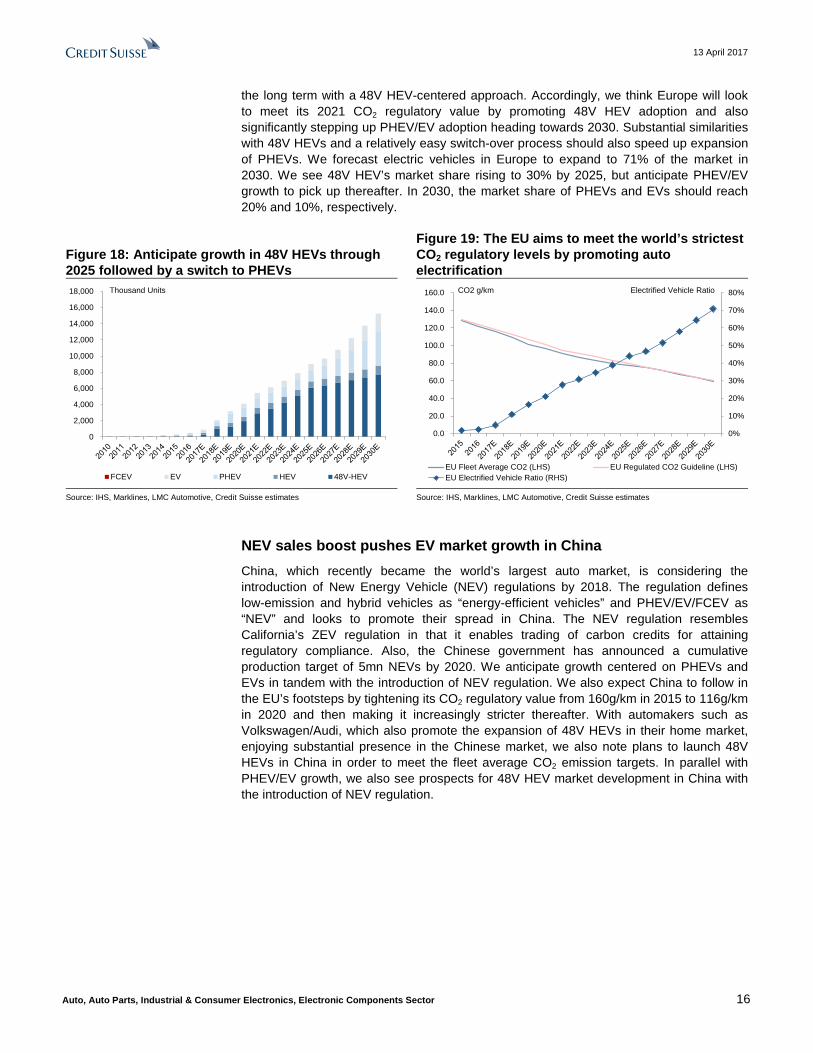

the long term with a 48V HEV-centered approach. Accordingly, we think Europe will look to meet its 2021 CO2 regulatory value by promoting 48V HEV adoption and also significantly stepping up PHEV/EV adoption heading towards 2030. Substantial similarities with 48V HEVs and a relatively easy switch-over process should also speed up expansion of PHEVs. We forecast electric vehicles in Europe to expand to 71% of the market in 2030. We see 48V HEV’s market share rising to 30% by 2025, but anticipate PHEV/EV growth to pick up thereafter. In 2030, the market share of PHEVs and EVs should reach 20% and 10%, respectively.

Figure 18: Anticipate growth in 48V HEVs through 2025 followed by a switch to PHEVs

Figure 19: The EU aims to meet the world’s strictest CO2 regulatory levels by promoting auto electrification

Source: IHS, Marklines, LMC Automotive, Credit Suisse estimates Source: IHS, Marklines, LMC Automotive, Credit Suisse estimates

NEV sales boost pushes EV market growth in China China, which recently became the world’s largest auto market, is considering the introduction of New Energy Vehicle (NEV) regulations by 2018. The regulation defines low-emission and hybrid vehicles as “energy-efficient vehicles” and PHEV/EV/FCEV as “NEV” and looks to promote their spread in China. The NEV regulation resembles California’s ZEV regulation in that it enables trading of carbon credits for attaining regulatory compliance. Also, the Chinese government has announced a cumulative production target of 5mn NEVs by 2020. We anticipate growth centered on PHEVs and EVs in tandem with the introduction of NEV regulation. We also expect China to follow in the EU’s footsteps by tightening its CO2 regulatory value from 160g/km in 2015 to 116g/km in 2020 and then making it increasingly stricter thereafter. With automakers such as Volkswagen/Audi, which also promote the expansion of 48V HEVs in their home market, enjoying substantial presence in the Chinese market, we also note plans to launch 48V HEVs in China in order to meet the fleet average CO2 emission targets. In parallel with PHEV/EV growth, we also see prospects for 48V HEV market development in China with the introduction of NEV regulation.

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

FCEV EV PHEV HEV 48V-HEV

Thousand Units

0%

10%

20%

30%

40%

50%

60%

70%

80%

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

EU Fleet Average CO2 (LHS) EU Regulated CO2 Guideline (LHS)EU Electrified Vehicle Ratio (RHS)

CO2 g/km Electrified Vehicle Ratio

13 April 2017

Auto, Auto Parts, Industrial & Consumer Electronics, Electronic Components Sector 17

Figure 20: EV growth likely in China following the introduction of NEV regulation

Figure 21: CO2 regulatory guidelines to gain momentum after 2020

Source: IHS, Marklines, LMC Automotive, Credit Suisse estimates Source: IHS, Marklines, LMC Automotive, Credit Suisse estimates

Electrification market trends (1): 48V systems seen as stopgap ahead of 2021 CO2 regulations Likely to be developed as high-cost-performance electrification option Development of 48V systems is getting off the ground in Europe, ahead of the 2021 CO2 emissions target of 95g/km coming into force. Such systems feature 48V power sources in addition to the 12V batteries previously fitted in automobiles. This makes it possible to improve performance and fuel economy by allotting spare power to engine assist motors, auxiliary equipment, and the like. Although the improvement in fuel economy is not as great as in HEVs and PHEVs, which have power sources of 200V or higher, 48V systems have attracted attention for their low additional costs. Since they use a voltage below the hazardous level of 60V, fitting them and ensuring their safety is easy. The pace at which cars with such systems are launched will likely pick up ahead of the 2021 fuel efficiency regulations coming into force. Renault, Audi, and other automakers have already commercialized 48V systems in Europe. Other makers (Daimler, BMW, Groupe PSA, and Ford) are due to launch models featuring 48V systems in 2017. We understand automakers are considering also launching models with 48V systems in the Chinese and North American markets. We expect 3.78mn vehicles to have 48V systems in 2021, rising to 8.60mn in 2025.

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

FCEV EV PHEV HEV 48V-HEV

Thousand Units

0%

5%

10%

15%

20%

25%

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

China Fleet Average CO2 (LHS) China Regulated CO2 Guideline (LHS)China Electrified Vehicle Ratio (RHS)

CO2 g/km Electrified Vehicle Ratio

13 April 2017

Auto, Auto Parts, Industrial & Consumer Electronics, Electronic Components Sector 18

Figure 22: 48V greatly improves fuel economy in small/midsize cars

Figure 23: Higher voltage enables electrification of auxiliary equipment

Source: Science & Technology, Credit Suisse estimates Source: Company Data, Science & Technology, Credit Suisse estimates

48V systems offer additional benefits besides better fuel economy, driving performance due to ISG Although individual 48V systems vary from maker to maker, they all basically comprise a 48V battery, a 48V integrated starter generator (ISG), a DC-DC converter, and an inverter. When the vehicle decelerates, power generated by the alternator is stored in the battery. When it accelerates, the starter motor assists the engine. In contrast to full hybrid systems, 48V systems are simple, requiring only the addition of a relatively small capacity battery and converter, and replacement of the starter motor with an ISG. By using an ISG, 48V systems offer other additional benefits than better fuel economy and driving performance. For one, fitting a high-voltage 48V battery generates surplus power making it possible to electrify auxiliary equipment that previously depended on engine power. Mechanical actuators that previously operated via connection with the engine (air conditioner compressors, turbochargers, water pumps, can oil pumps) can be fully electrified, which also helps reduce loss of engine output. In addition, we believe adoption of systems associated with driving performance (electric stabilizers, large-model electric power steering systems, and active suspension), which was difficult with predecessor 12V systems, will likely increase. Demand should therefore increase for electronic parts (motors and passive components) and for high-value-added automotive semiconductors compatible with high-voltage systems.

0%

10%

0 1200 2400

Suitable Segment for 48V Mild Hybrid

Suitable for StrongHybrids

Acceptable Segmentfor 48V or Strong HV

Engine Displacement (cc)

Fuel

Effi

cien

cy Im

prov

emen

t (%

)

0.1

1

10

100

1000

10 100 1,000 10,000 100,000Electrical Load (W)

Ope

ratio

nal T

ime

(Sec

)

Strong HVMotor

Generator

Car Audio

Elec. Air Compressor

LCDMonitor

Active Suspension

ElectricCompressor

Mild HVIntegrated

Motor Generator

ElectricStabilizerABS

LargeEPS

Power Window

WiperMotor

SmallEPS

Lamps

48V >100V

13 April 2017

Auto, Auto Parts, Industrial & Consumer Electronics, Electronic Components Sector 19

Figure 24: 48V system configuration

Source: Science & Technology, Credit Suisse

Trend toward higher-voltage systems likely to continue as 48V systems alone cannot keep pace with environmental regulations in the long term The structure of 48V systems resembles mild hybrid systems (130V). However, they are far superior in cost performance. Compared to other vehicles with the same performance engine, full hybrid systems improve fuel economy by around 40%. Use of a 48V system achieves an improvement of only around 15%. However, the additional cost can be kept down to around one-third that of a full hybrid system. Such systems are therefore expected to be rolled out in small and mid-size cars, where the demand is for low prices. However, while it is easy to equip a vehicle with a 48V system and such systems boast high cost performance, there is a view that the maximum improvement in fuel economy of 15% will not be sufficient to meet environmental regulations from 2025. For this reason, 48V systems are being seen as a bridging measure ahead of 2021 regulations. To meet even tighter environmental standards a shift is expected toward higher-voltage electrified cars (PHEVs, EVs), favoring PHEVs, which have many structural similarities but do not require the major powertrain changes needed in full hybrid systems.

48V systems developed mainly by European and US makers, but Japanese suppliers should also benefit from the movement toward higher voltage European and US mega-suppliers (Bosch, Continental, Delphi, Schaeffler, and Valeo) are developing 48V systems. Japanese manufacturers are strongly associated with full hybrid systems, but have not adopted a clear stance on the adoption of 48V systems. In 2001, Toyota Motor (7203) launched the Crown Hybrid featuring a 42V power supply in the Japanese market. However, sales missed expectations and in due course full hybrid cars such as the Prius and Aqua took over the primary role. We see little demand for a shift to 48V in the Japanese market given its high proportion of HEVs and mini-vehicles and its maintenance of high average levels of fuel economy. However, we think some Japanese

DC-DCConverter

Inverter

48V Driven ProductsElectric Turbo/Super ChargerElectric CompressorABS (Antilock Brake System)Large EPS (Electric Power Steering)Eletric Stabilizer, etc

12V Driven UnitsLampsSmall EPS (Electric Power Steering)Power WindowWiper MotorsCluster Panels, etc

12V Battery

48V Battery

Integrated Starter Generator (48V E-Motor/ Alternator)

Torque Assist

13 April 2017

Auto, Auto Parts, Industrial & Consumer Electronics, Electronic Components Sector 20

suppliers will likely benefit from higher value-added and growth in the ratio of vehicles fitted with 48V systems arising from the shift to higher voltage systems in the global market. As discussed later, growth in the number of motors used will likely impact manufacturers such as Nidec (6594), while Denso (6902) and Aisin Seiki (7259), which make electrical auxiliary equipment, should feel an impact as well.

Electrification market trends (2): Full-fledged launch of PHEVs, EVs starting Stricter CO2 standards effective from 2021 should spur growth in PHEV/EV demand The auto industry developed 48V systems as a bridge to meet the EU’s CO2 standards scheduled to take effect in 2021. More radical electrified vehicle innovations will be needed to comply with even stricter environmental standards expected to be imposed in the future. Electrified vehicles (i.e., 48V HEVs, HEVs, PHEVs, EVs and FCEVs) currently account for an estimated 4% share of the global automobile market. One reason for their low share, besides the cost of equipping vehicles with electric power units, is that recharging infrastructure (for, e.g., EVs, FCEVs) is not yet adequately available. With CO2 standards slated to continue to be progressively tightened beyond the 2021 target, we expect demand for PHEVs, currently the most fuel-efficient vehicles, and EVs, which will likely benefit from government incentives, to grow sharply from 2021. We forecast global unit-demand for PHEVs at 2.5mn in 2021 and 9.8mn in 2030, up from a mere 210,000 in 2015. For EVs, our corresponding 2021 and 2030 forecasts are 2.7mn and 7.89mn, respectively, up from 290,000 in 2015.

Automakers rushing to roll out PHEVs, the most fuel-efficient ICE vehicles PHEVs are hybrid vehicles that are equipped with both internal combustion engines (ICE) and electric powertrains and can recharge their batteries from an external power source. PHEVs are equipped with larger batteries and have a much greater all-electric range than HEVs. Meanwhile, their ICEs enable PHEVs to circumvent EVs’ continuous driving range limitations. Fuel efficiency conversion methods for PHEVs differ internationally, but PHEVs are currently considered the most fuel efficient ICE-equipped vehicles. Being more marketable than EVs, which are dependent solely on external power sources and have continuous-driving-range limitations, PHEVs will likely grow in prevalence. In this report, PHEVs include extended-range EVs equipped with ICEs used exclusively for recharging to extend driving range.

Automakers are expediting development of PHEV models in preparation for future tightening of CO2 standards. Japanese automakers, particularly Toyota and Honda, have been expanding their HEV model lines. Recently, however, they have started to place priority on PHEVs also. Toyota’s new Prius PHV has a maximum all-electric range of 68.2km, a drastic improvement from its predecessor’s 26.4km range. Its HEV-mode fuel efficiency is 37.2km/l, better than the smaller Toyota Aqua (a.k.a. Prius c) HEV’s 33.8km/l. Under the US’s combined fuel economy standard, the new Prius PHV is rated at 56km per gasoline liter equivalent. Honda announced that it will roll out a CR-V PHEV around November 2017 in conjunction with the CR-V’s upcoming full model change. In the SUV space, Mitsubishi Motors (7211)’ Outlander PHEV has an all-electric range of 60km and an impressive HEV-mode fuel efficiency of 19.2km/l. Among US automakers, GM offers the Volt, an extended-range EV. The Volt has an all-electric range of 53mi (approx. 85km) and maximum driving range of about 420mi (approx. 672km) on a full tank of gas, both of which are vastly better than the original Volt’s corresponding specs. European automakers also are starting to focus on PHEV models. While they seem to be laggards in developing

13 April 2017

Auto, Auto Parts, Industrial & Consumer Electronics, Electronic Components Sector 21

the full hybrid systems in which Toyota and Honda Excel, they apparently aim to make up for lost time by accelerating development of PHEVs, which pose less of a challenge than full hybrids.

US/European automakers are focusing on PHEVs in response to fuel efficiency conversion formulas Formulas used to calculate PHEV fuel consumption differ internationally, partly reflecting that PHEVs do not consume any fuel when used for short-distance driving. In Japan, PHEVs’ combined fuel efficiency was previously calculated by multiplying their conventional fuel efficiency by a coefficient that adjusts for the battery-powered share of distance driven. This method was abandoned in 2014. The original Prius PHV’s HEV-mode fuel efficiency was 31.6km/l (JC08 mode) but its combined fuel efficiency was an astounding 61.0km/l. As PHEV models became more varied (e.g., extended-range EVs), combined fuel efficiency was likewise abandoned because it no longer accurately reflected all PHEVs’ actual fuel efficiency. Currently, PHEVs in Japan have both EV- and HEV-mode fuel efficiency ratings. In Europe, by contrast, PHEVs’ improvement in fuel efficiency over ICE-equipped vehicles is calculated by multiplying conventional ICE-equipped vehicles’ CO2 emissions by a CO2-reduction coefficient, using the formula F = (De + Dav)/Dav, where F is the CO2-reduction coefficient, De is the vehicle’s all-electric range and Dav is the average distance between battery recharges (Dav is statutorily set at 25km). For example, assume that Mercedes-Benz hypothetically develops a PHEV version of a full-sized S-class sedan with CO2 emissions of 180g/km. Given an all-electric range (De) of 40km, the PHEV model’s CO2-reduction coefficient would be 2.6, which would yield a CO2 emissions rating of 69g/km, well below Europe’s 2021 CO2 emissions limit of 95g/km. From this example, it is readily apparent that this CO2 emissions formula is one reason why European automakers are focusing on PHEVs. In the US, PHEVs’ fuel efficiency is calculated by a formula similar to Japan’s old combined fuel efficiency formula. The US formulas is based on an EV-mode utility rate. In European and North American markets, PHEVs are advantageous to automakers in terms of compliance with CO2 emission standards. The PHEV market segment should continue to grow rapidly.

EVs boast zero emissions but have limitations EVs are vehicles powered solely by electric motors and with no internal combustion engine or power source other than an external charger. We define them narrowly in this report as pure electric vehicles, meaning that we exclude plug-in hybrids (PHEVs) and other variations. EVs available at present include the mass-market Nissan Leaf and Tesla Model X and Model S. EVs’ exclusive reliance on electric power means that they generate no exhaust emissions, but it also limits their driving range and requires long charging times. The Leaf has a 30kWh battery, and while it takes just 30 minutes to charge to 80% of full capacity using a 50kW fast charger (the largest widely available in Japan at present), its range is just 280km even on a full charge. The Tesla Model X ups this to 414km on the back of a 90kWh battery, but the battery is exceptionally pricey and requires triple the charging time of the Leaf’s. Another impediment to EV penetration has been the fact that charging infrastructure remains a work in progress worldwide. There were around 190,000 public charging stations globally as of 2015 (ICCT estimate), and while this was around triple the number in 2013, just 27,000 or so of these have fast chargers. As all of this suggests, EVs are currently well suited to frequent short-distance driving in cities but remain slightly too inflexible to accommodate a broader range of usage environments.

China a possible game changer near term; longer-term demand hinges on performance and government policy The fact that EVs generate zero emissions has governments worldwide offering generous subsidies for EV buyers. Japan and other developed countries offer subsidies for the required charging systems, and EVs also have the highest purchase subsidies of any

13 April 2017

Auto, Auto Parts, Industrial & Consumer Electronics, Electronic Components Sector 22

clean energy vehicle—including ¥330,000 for the Leaf in Japan, or around 10% of the total price. China, now the world's largest EV market, pays around ¥1mn per vehicle and plans to continue this policy through 2020. This has us expecting continued growth in the market through 2020 centered on China, but we think demand could shift toward PHEVs from 2021 as Chinese subsidies taper off and in view of their ease-of-use and compatibility with conventional internal combustion vehicles. That said, we do see a possibility of EV sales continuing to rise sharply depending on where vehicle performance and government subsidies go from here. Battery makers are working to improve battery efficiency and are also making steady improvements in charging time. Chademo, an organization working to promote fast-charging standards for EVs, revised its charger standards in March 2017 to allow commercialization of fast chargers of up to 150kW, triple the current level. Standardization efforts aimed at accommodating larger capacity batteries are also in progress worldwide beginning with Europe's combined standards.

Figure 25: Buildout of fast-charger stations a work in progress

Figure 26: Number of charging stations up sharply in China

Source: ICCT, Credit Suisse Source: ICCT, Credit Suisse

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000

2007 2008 2009 2010 2011 2012 2013 2014 2015

Fast Charger Slow Charger

EV Charging Spots

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000

2007 2008 2009 2010 2011 2012 2013 2014 2015Others Japan/Korea China Europe North America

EV Charging Spots

13 April 2017

Auto, Auto Parts, Industrial & Consumer Electronics, Electronic Components Sector 23

Figure 27: Major models for electrified vehicles

Source: Company data, Credit Suisse estimates

Electrification market trends (3): A good outlook for electrification as it spreads to auxiliary equipment Shift to higher voltages not only for primary motors

With reliance on electric motor power increasing as automakers strive to achieve compliance with environmental regulations, we think electrification of automotive components will likely accelerate due to expansion of the supporting battery capacity. As power supply voltages rise from 12V to 48V and then to 200–270V for HEVs and 300–400V for PHEVs, the added value of auto batteries that support this will naturally increase, but in tandem with this expanding capacity, the rise in voltage should also promote electrification of auxiliary equipment. Engine peripherals that used to depend on engine power can be electrified and this re-allocation of spare power is opening up possibilities for components that formerly could not be handled by 12V power supplies but now can.

Electrification Type

Brand Model Engine Main Motor (ISG) Peak Output

Official Fuel Economy EV Driving Range

Battery Capacity

Audi SQ7 4.0L Turbodiesel - 7.2L/100km - 0.47kWh

Daimler S-Class 2.0L I4 Gasoline 15kW TBA - 0.9kWh

Ford Focus 1.5L Turbodiesel 10kW 88g/km (CO2) - 0.5kWh

Renault Scenic 1.5L Turbodiesel 10kW 92g/km (CO2) - 0.5kWh

Chevloret Malibu Hybrid 1.8L I4 Gasoline 55kW 46mpg - 1.5kWh

Honda Fit 1.5L I4 Gasoline 22kW 36.4km/L - 0.86kWh

Hyundai Ioniq Hybrid 1.6L I4 Gasoline 32kW 58mpg - 1.6kWh

Toyota Prius 1.8L I4 Gasoline 53kW 40.8km/L - 0.75kWh

BYD Tang 2.0L I4 Gasoline 110kW x 2 117mpg 100km 18.4kWh

Chevloret Volt 1.5L I4 Gasoline 110kW x 2 42mpg 85km 18.5kWh

Mitsubishi Oulander 2.0L I4 Gasoline 60kW x 2 19.2km/L (in HV only) 60km 12.0kWh

Toyota Prius PHV 1.8L I4 Gasoline 53kW + 23kW 37.2km/L (in HV only) 68km 8.8kWh

BMW i3 (94Ah) N/A 125kW - 190km 33.0kWh

BYD e6 N/A 90kW - 300km 61.4kWh

Nissan Leaf N/A 80kW - 280km 30kWh

Tesla Model S (85kWh) N/A 310kW - 480km 85kWh

Daimler B-Fuel Cell N/A 100kW - 385km 3.7kg @700 bar

Honda Clarity Fuel Cell N/A 130kW - 750km 141L

Hyundai Tucson FCEV N/A 100kW - 424km 140L

Toyota Mirai N/A 113kW - 650km 122L

*FCEV listed in terms of hydrogen tank for capacity, and max driving range with full tank.*Fuel economy listed per the regional regulated value and testing mode.*Includes some models being before launch, using the preliminary figures from the automakers

48V System

HEV

PHEV

FCEV

EV

13 April 2017

Auto, Auto Parts, Industrial & Consumer Electronics, Electronic Components Sector 24

Substantial scope for electrification of engine and driving components

Engines are surrounded by numerous components—including oil pumps, water pumps, exhaust gas recirculation (EGR) valves associated with engine air intakes and exhausts, variable valve timing (VVT) units, turbochargers, and A/C compressors—that mediate engine power or are driven by oil pressure or other means generated by engine power. Because these components are connected to the engine they cause loss of engine power, and because they depend on engine turnover they cannot be easily turned on and off. Using electric motors to run these parts enables efficient control and reduces the load on the engine, thereby enabling automakers to boost fuel economy.

An automotive oil pump is an actuator that generates powertrain lubrication, cooling, or pneumatic pressure to drive other auxiliary components. By making these electrically driven, it becomes possible to control them without relying on engine rpms and also to use idling stop systems, all of which can sharply improve fuel efficiency. Electrification has similar benefits for water pumps, including for use in cooling the inverters required in an electrified vehicle. Electrification of exhaust gas recirculation (EGR), variable valve timing (VVT), and turbo/superchargers can further improve the fuel efficiency of an internal combustion engine. In particular, electric turbochargers join integrated starter generators (ISG) as a key component for 48V systems. Conventional turbochargers are driven by engine exhaust (superchargers rely on the engine's crankshaft), but an electric turbocharger uses a motor to rotate the compressor. This reduces turbo lag and exhaust pressure loss caused by fluctuations in exhaust gas energy and improves the engine’s responsiveness. This allows engine down-sizing and down-speeding and makes a major contribution to improved fuel efficiency. The bottleneck in electrifying these components has been the amount of voltage required, but this now looks set to be remedied with the development of high-voltage vehicles. Higher voltages could also facilitate electrification of automotive air-conditioning compressors in support of reduced engine loads.

We also believe there is still substantial scope for electrification of suspension systems to improve driving performance. More cars are being fitted with electric power steering systems (EPS), but we still room for growth as the global installment of EPS is roughly at 60%. Fuel efficiency could see 2–4% improvement by electrifying the power steering, which in the past was driven by hydraulics generated from engines. As voltages rise, more cars will include such features as electric driving brakes and parking brakes, electrically controlled suspensions, electric active stabilizers, and electric four-wheel drive. We expect these systems to improve vehicle range, to assist stable driving, and to contribute indirectly to improved fuel economy. Stabilizers act as anti-rolling, or anti-swaying system while cars in turns or on unstable roads. With electrification, the stabilizers be controlled by motors and reduction gears instead of the rigidity of the physical stabilizer bars, in terms give more flexibility and smooth control for vehicle stability. By adopting power supplies with higher voltage above 48V, the electrified active stabilizers could see more usage in larger vehicles. Electric 4WD system, notably installed on new Toyota Prius, equips an independent driving motor on vehicle’s rear axle. Traditional 4WDs used power transfer unit (or transfer case) to split the output force from transmission to front and rear axles, whereas the electric 4WD units generates its own force to avoid any engine loss to establish 4WD. Along with the active stabilizer, both units require higher electrical loads, however we anticipate higher installation as the overall vehicle power source becomes higher.

13 April 2017

Auto, Auto Parts, Industrial & Consumer Electronics, Electronic Components Sector 25

Expecting electrification of auxiliary equipment to lead to a large increase in the number of motors

We expect a large increase in the number of motors in use due to electrification of auxiliary equipment. We estimate that cars today have around 45 motors on average (excluding the primary motor). Low-price vehicles have around 25, while electrified cars and high-class vehicles can have over 130. The difference is thus substantial. Electric motors are already used for basic functions such as starting the engine, locking doors, and operating windscreen wipers. However, use of electric motors for the functions mentioned above including in engine-related and driving components, is still rare. We think the shift to higher voltage systems will push accelerated use of motors in these components. Motors used in engine and driving-related parts need to be powerful. As this area covers mid- to large-capacity motors, we believe high-price-band motors are likely to see increased use overall. We forecast the market for vehicle equipped motors, excluding the main driving unit, would grow from ¥3.5tn in 2015 to ¥5.5tn in 2020, and ¥10tn in 2030. The average installation of the motors per vehicle is forecasted to grow from 44 pieces in 2015 to 79 pieces in 2030.

Figure 28: Substantial scope for electrification of engine/driving components

Source: Credit Suisse

Figure 29: Major scope for electrification of engine/running components

Figure 30: Electrification of engine/running components sharply improves fuel efficiency

Note: Motors shipment price basis Source: Marklines, IHS, Credit Suisse estimates

Source: ICCT, Credit Suisse estimates

Fuel Efficiency:Improve

Engine-loss

Fuel Efficiency:Idling Stop

Specificallydemanded for

HEV/EV

ImproveDriveability

Safety andOthers

Valvetrain EGR e-EGR x

Valvetrain Variable Valve Timing e-VVT x

Valvetrain Valve Lifter Control e-Valve Control x

Valvetrain Turbocharger Electric Turbo x x

Powertrain Water Pump Electric Water Pump x x

Powertrain Engine Oil Pump Electric Oil Pump x x x

Drivetrain Transmission Oil Pump Electric Oil Pump x x x

Drivetrain 4WD (Transfer/PTU) E-4WD Unit x x x

Chassis/Brakes Power Steering EPS x x

Chassis/Brakes Steering Lock E-Steering Lock x

Chassis/Brakes Vacuum Pump Electric Vacuum Pump x x

Chassis/Brakes Brakes Regenerative Brakes x

Chassis/Brakes Parking Brakes Electronic Parking Brake x

Chassis/Brakes Rear Steering Active Rear Steering x x

Chassis/Brakes Stabilizer Electronic Active Stabilizer x x

Auxiliary AC Compressor Electronic Compressor x x

Advantages from Electrification

System Component Electrified Version

0

1,000

2,000

3,000

4,000

5,000

6,000

Drivetrain Support Suspension BrakesSteerings Hydraulic Control Temperature Control

Billion JPY

7.5%7.0%

6.5%6.0%

3.5%

2.0%1.5%

0.0%

2.0%

4.0%

6.0%

8.0%

13 April 2017

Auto, Auto Parts, Industrial & Consumer Electronics, Electronic Components Sector 26

Battery performance being improved to increase vehicle voltage We expect increased vehicle electrification (48V HEV, HEV, PHEV, EV) to drive steady growth in demand for the high-output batteries that power these vehicles. The amount of battery capacity required by electrified vehicles varies widely, from 0.25kWh for 48V HEVs to 100kWh for EVs, but the global market for next-generation automotive batteries totaled upward of 37GWh as of 2016. We expect this to reach 167GWH in 2020 and 255GWH in 2025 in tandem with increased vehicle electrification. Battery prices per kWh very widely but currently average around ¥20,000 by our estimate.

At present, electrified vehicles generally use either nickel-metal hydride (NiMH) or lithium-ion (Li-ion) batteries. Li-ion batteries account for the majority due to their superiority in terms of charge capacity and charge/discharge current, but battery makers are working to develop everything from new basic materials to new basic technologies in an effort to improve EVs’ driving range and charge performance. A key issue is the need for higher capacity batteries to enable longer driving distances. With onboard space limited, battery makers are looking into materials with higher energy density as they race to develop higher-performance batteries. Increased EV penetration also hinges on battery costs being reduced. Battery makers aim to lower the average cost per kWh from ¥20,000 ($160–$240) at present to less than $150.

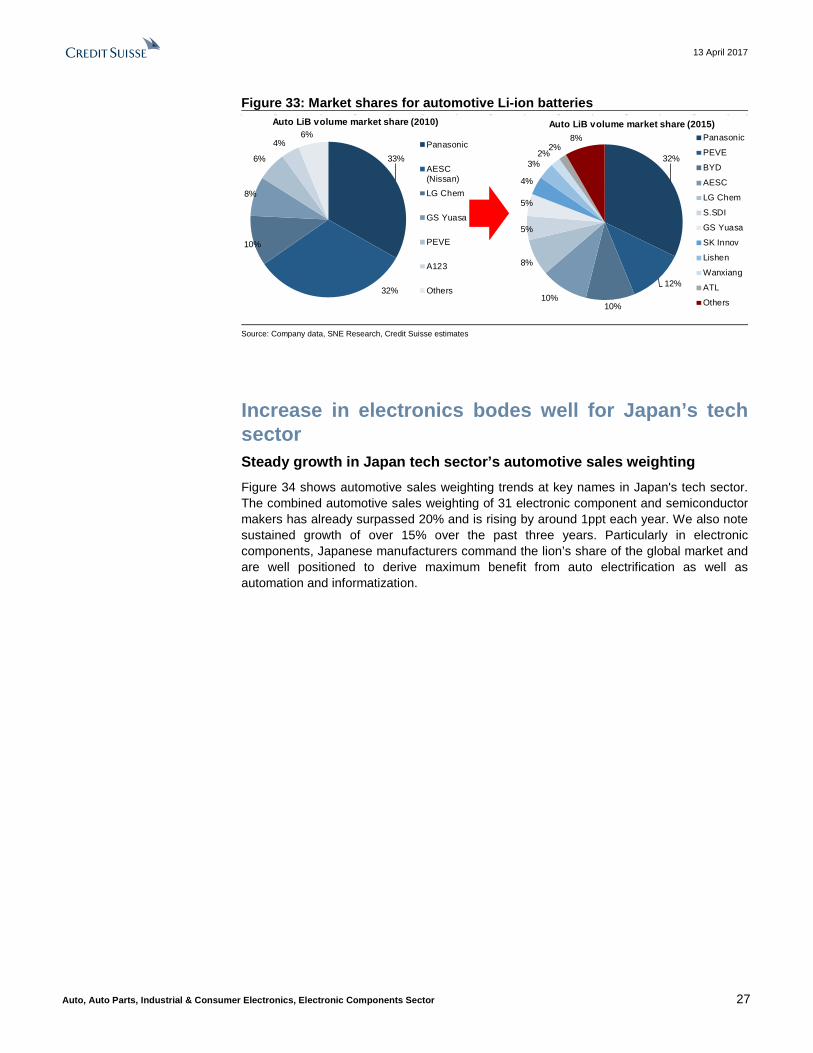

Growth in the number of electrified vehicles also implies coming economies of scale for the battery makers. However, the market for automotive Li-ion batteries has become substantially more crowded in recent years, making for an exceptionally competitive operating environment. The number of suppliers rose from just seven in 2010 to over 20 in 2015. The leaders are currently Panasonic (which supplies Tesla), Toyota’s Primearth EV Energy (PEVE), Nissan’s Automotive Energy Supply Corporation (AESC), and EV maker BYD, which makes its own batteries in house. We think this reflects current market shares and battery capacities for electrified vehicles and see potential for changes as automakers launch more such models.

Figure 31: Outlook for automotive battery market Figure 32: Number of competitors in automotive battery market

Source: Marklines, IHS, LMC Automotive, Credit Suisse estimates Source: Company data, SNE Research, Credit Suisse estimates

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000 Market Size in Mwh

0

5

10

15

20

25

CY2009 CY2015

Auto LiB

Number of competitors in mass-production (estimate)

6-7

20+

13 April 2017

Auto, Auto Parts, Industrial & Consumer Electronics, Electronic Components Sector 27

Figure 33: Market shares for automotive Li-ion batteries

Source: Company data, SNE Research, Credit Suisse estimates

Increase in electronics bodes well for Japan’s tech sector Steady growth in Japan tech sector’s automotive sales weighting Figure 34 shows automotive sales weighting trends at key names in Japan's tech sector. The combined automotive sales weighting of 31 electronic component and semiconductor makers has already surpassed 20% and is rising by around 1ppt each year. We also note sustained growth of over 15% over the past three years. Particularly in electronic components, Japanese manufacturers command the lion’s share of the global market and are well positioned to derive maximum benefit from auto electrification as well as automation and informatization.

32%

12%

10%10%

8%

5%

5%

4%

3%2%

2%8%

Auto LiB volume market share (2015)Panasonic

PEVE

BYD

AESC

LG Chem

S.SDI

GS Yuasa

SK Innov

Lishen

Wanxiang

ATL

Others

33%

32%

10%

8%

6%

4%6%

Auto LiB volume market share (2010)

Panasonic

AESC(Nissan)

LG Chem

GS Yuasa

PEVE

A123

Others

13 April 2017

Auto, Auto Parts, Industrial & Consumer Electronics, Electronic Components Sector 28

Figure 34: Japan tech sector: Automotive-related sales and weightings at major companies

Source: Company data, Credit Suisse

Acceleration in topline growth Figure 34 shows long-term trends in automotive-related sales and weightings at a smaller number (18) of Japanese electronic component and semiconductor makers. Due to growth in smartphone-related sales in FY13–15, growth in automotive sales weightings slowed slightly, although sales growth accelerated. Combined sales at the 18 companies has grown by 10% per year on average over the past 10 years, versus 14% per year over the past five years.

Average(FY12) (FY13) (FY14) (FY15) (FY12) (FY13) (FY14) (FY15) (FY13) (FY14) (FY15) FY13-15 (FY12) (FY13) (FY14) (FY15)