Audit outcomes of local government IMFO 5 March 2015 MFMA 2012-13

Audit outcomes of local government IMFO 5 March 2015 MFMA 2012-13.

Dec 24, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Audit outcomes oflocal government

IMFO 5 March 2015

MFMA 2012-13

Our reputation promise/mission

The Auditor-General of South Africa (AGSA) has a constitutional mandate and, as the Supreme Audit

Institution (SAI) of South Africa, exists to strengthen our country’s democracy by enabling oversight, accountability and governance in the public sector through auditing, thereby building

public confidence.

2012-13MFMA

3

Financial statements

Fair presentation and reliability of information (no material misstatements)

Annual performance reports

Whether the reported information is reliable and credible (no material findings)

Compliance with legislation

Whether the auditee complied with key legislation on financial and performance management (no material non-compliance)

We audit … to determine …

Focus of our audits

2012-13MFMA

4

Auditees that received a financially unqualified opinion with findings are those that were able to produce financial statements without material misstatements but are struggling to:• align their performance reports to the predetermined objectives they committed to in

their annual performance plans• set clear performance indicators and targets to measure their performance against

their predetermined objectives• report reliably on whether they achieved their performance targets• determine which legislation they should comply with and implement the required

policies, procedures and controls to ensure they comply.

An unqualified opinion with no findings (clean audit) means the auditee was able to:• produce financial statements free of material misstatements.• report in a useful and reliable manner on performance as measured against

predetermined objectives in the annual performance plan.• comply with key legislation.

Adverse and disclaimed opinions mean the auditee was …• unable to provide sufficient supporting documentation for amounts in the financial

statements and achievements reported in the annual performance report.• not complying with key legislation.

Various categories of the audit outcomes

Auditees that received a financially qualified audit opinion with findings have the same challenges as those that were unqualified with findings but, in addition, they could not produce credible and reliable financial statements. There are material misstatements in their financial statements, which they could not correct before the financial statements were published.

Audit outcomes

Improved

Regressed

Stagnant or little progress

5

2012-13MFMA

Unqualified with no findings

Unqualified with findings

Qualified with findings

Adverse or disclaimer with findings

Audits outstandingFree State

MFMA PFMA

2 1

8

9

4

8

10

4

Limpopo MFMA PFMA

7

9

3

15

10

1

9

1

Mpumalanga

MFMA PFMA

5

11

4

3

8

25

KwaZulu-Natal

MFMA PFMA3

12 6

46 21

11 9

3

Gauteng MFMA PFMA

2 2

32

13

3

19

1

North West

MFMA PFMA

15 4

6

8

616

6

1

Northern Cape

MFMA PFMA

4

13

8

5

6

9

15

National government

PFMA

11928

132

53

Eastern Cape

MFMA PFMA2

131

21

6

18

15

14

Western Cape

MFMA PFMA1 1

18

5

12

18

1

6

2012-13MFMA

What is the status and progress of audit outcomes of local government?

… the key role players need to ...

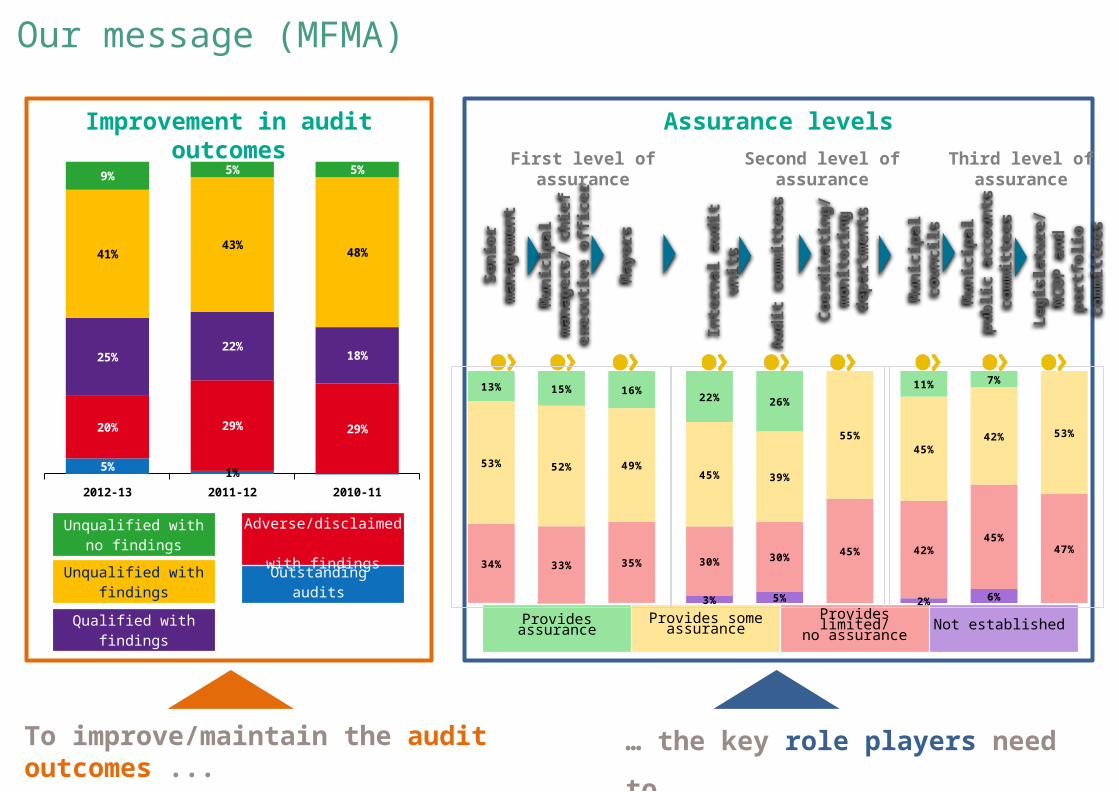

Improvement in audit outcomes

Outstanding audits

2012-13 2011-12 2010-11

5% 1%

20% 29% 29%

25%22%

18%

41%43%

48%

9% 5% 5%

To improve/maintain the audit outcomes ...

Unqualified with no findings

Unqualified with findings

Qualified with findings

Adverse/disclaimed with findings

Assurance levels

Provides assurance Provides some assurance Provides limited/no assurance Not established

Se

nio

r m

an

ag

em

en

t

Mu

nic

ipa

l m

an

ag

ers

/ c

hie

f e

xe

cu

tiv

e o

ffic

er

Ma

yo

rs

Inte

rna

l a

ud

it u

nit

s

Au

dit

co

mm

itte

es

Co

ord

ina

tin

g/

mo

nit

ori

ng

d

ep

art

me

nts

Mu

nic

ipa

l p

ub

lic

a

cc

ou

nts

c

om

mit

tee

s

Mu

nic

ipa

l c

ou

nc

ils

First level of assurance Second level of assurance Third level of assurance

Our message (MFMA)

34% 33% 35%

53% 52% 49%

13% 15% 16%

3% 5%

30% 30% 45%

45% 39%

55%

22% 26%

2% 6%

42%45%

47%

45%42% 53%

11% 7%

Le

gis

latu

re/

NC

OP

a

nd

po

rtfo

lio

c

om

mit

tee

s

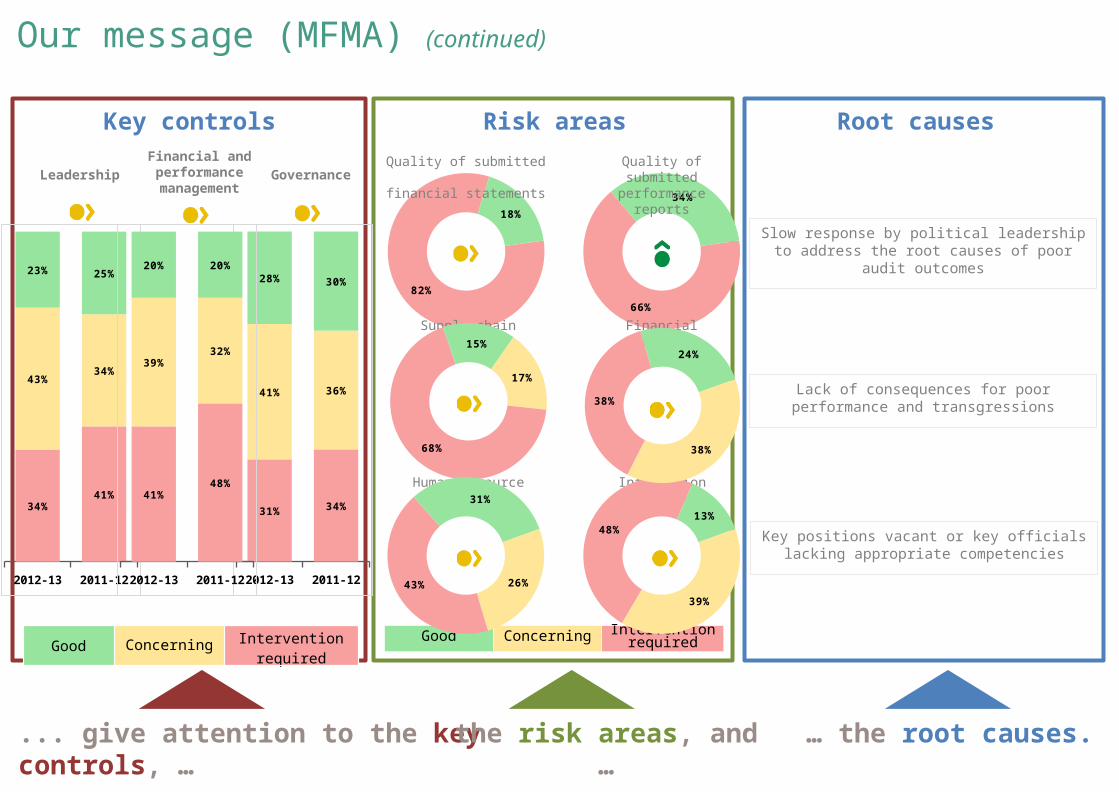

Key controls

LeadershipFinancial and performance management

Governance

Root causes

Slow response by political leadership to address the root causes of poor audit outcomes

... give attention to the key controls, …

Good Concerning Intervention required

the risk areas, and …

Lack of consequences for poor performance and transgressions

Key positions vacant or key officials lacking appropriate competencies

82%

18%

Quality of submitted financial statements

Supply chain management

Human resource management

Risk areas

66%

34%

Quality of submitted performance reports

Information technology

Financial health

Good Concerning Intervention required

Our message (MFMA) (continued)

… the root causes.

17%

68%

15%

39%

48%13%

2012-13 2011-12

34%41%

43%34%

23% 25%

2012-13 2011-12

31% 34%

41% 36%

28% 30%

2012-13 2011-12

41%48%

39%32%

20% 20%

38%

38%

24%

26%43%

31%

9

• Significant non-compliance with legislation by 88 of the auditees

• Slight improvement over 2011-12

90%

Status of compliance with legislation

With no findings

With findings

2012-13 2011-12 2010-11

90% (286) 95% (299) 93% (293)

10% (33) 5% (17) 7% (21)

2012-13MFMA

10

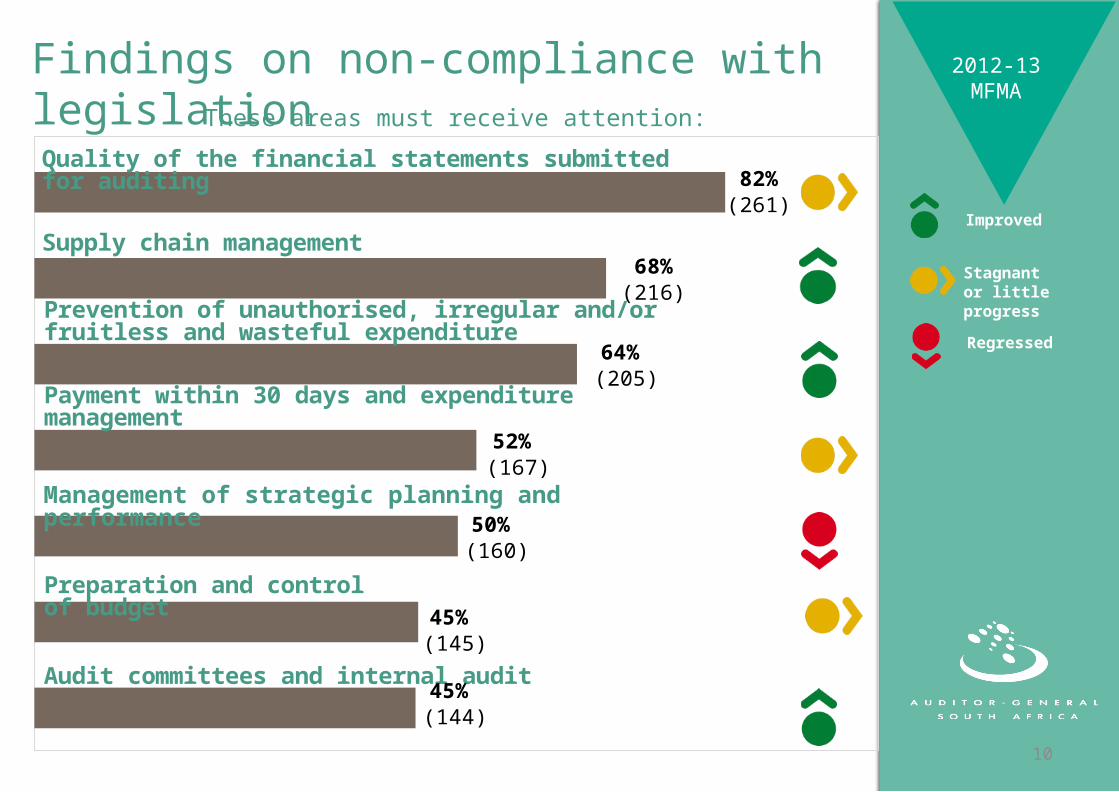

2012-13MFMAThese areas must receive attention:

Findings on non-compliance with legislation

Improved

Regressed

Stagnant or little progress

Quality of the financial statements submitted for auditing

Supply chain management

Prevention of unauthorised, irregular and/or fruitless and wasteful expenditure

Preparation and control of budget

Audit committees and internal audit

Payment within 30 days and expenditure management

82%(261)

68%(216)

64% (205)

52% (167)

50% (160)

45% (145)

45% (144)

Management of strategic planning and performance

2012-13MFMA

11

Quality of annual performance reports

With no findings

With findings

• The annual performance reports of only of auditees

were useful and reliable

• Improvement over 2011-12

34%

2012-13MFMA

2012-13 2011-12 2010-11

66% (212)75% (237) 73% (228)

34% (107)25% (79) 27% (86)

12

KwaZulu-Natal (1)• Umtshezi

Limpopo (1)• Waterberg District

Progressed to clean [17]

Eastern Cape (1)• Mandela Bay Development

Agency

Gauteng (1)• Sedibeng District

KwaZulu-Natal (7)• Msinga• Ntambanana• Okhahlamba• Ubuhlebezwe• uMhlathuze• uMzimkhulu• Uthungulu District

Northern Cape (1)• ZF Mgcawu District

Western Cape (7)• Breede Valley• Cape Town International

Convention Centre• City of Cape Town Metro• Knysna• Overstrand• Theewaterskloof• Witzenberg

2012-13MFMAClean audits Regressed from

clean audit to unqualified with

findings

Regressed from clean audit to

financially qualified

Movements in clean audits

KwaZulu-Natal (1)• ICC, Durban (Pty) Ltd

Retained [13]

Gauteng (2)• Johannesburg Fresh Produce

Market• Johannesburg Social Housing

Company

KwaZulu-Natal (4)• Durban Marine Theme Park

(Pty) Ltd• Safe City Pietermaritzburg• uThungulu Financing

Partnership• uThungulu House

Development Trust

Mpumalanga (1)• Ehlanzeni District

Western Cape (6)• George• Langeberg• Mossel Bay• Steve Tshwete• Swartland• West Coast District

Clean audits2012-13MFMA

13

2012-13MFMA

Characteristics of those that advanced to clean audits…• Basic accounting and daily disciplines in place

• Enforcing compliance with all legislation

• Employing staff with the required level of technical competence and experience

• Calling for information and reports regularly

• Allowing CFO to be in charge of the financial records and report thereon to the MM

• The monitoring of the financial improvement plan kept on the council’s quarterly meeting agenda

• The municipal manager reviewing management accounts with the CFO every month

• Effective combined assurance environment

2012-13MFMA

14

2012-13MFMA

2What assurances did the key role players provide and what vital actions and interactions should take place?

2012-13MFMA

2012-13MFMA

15

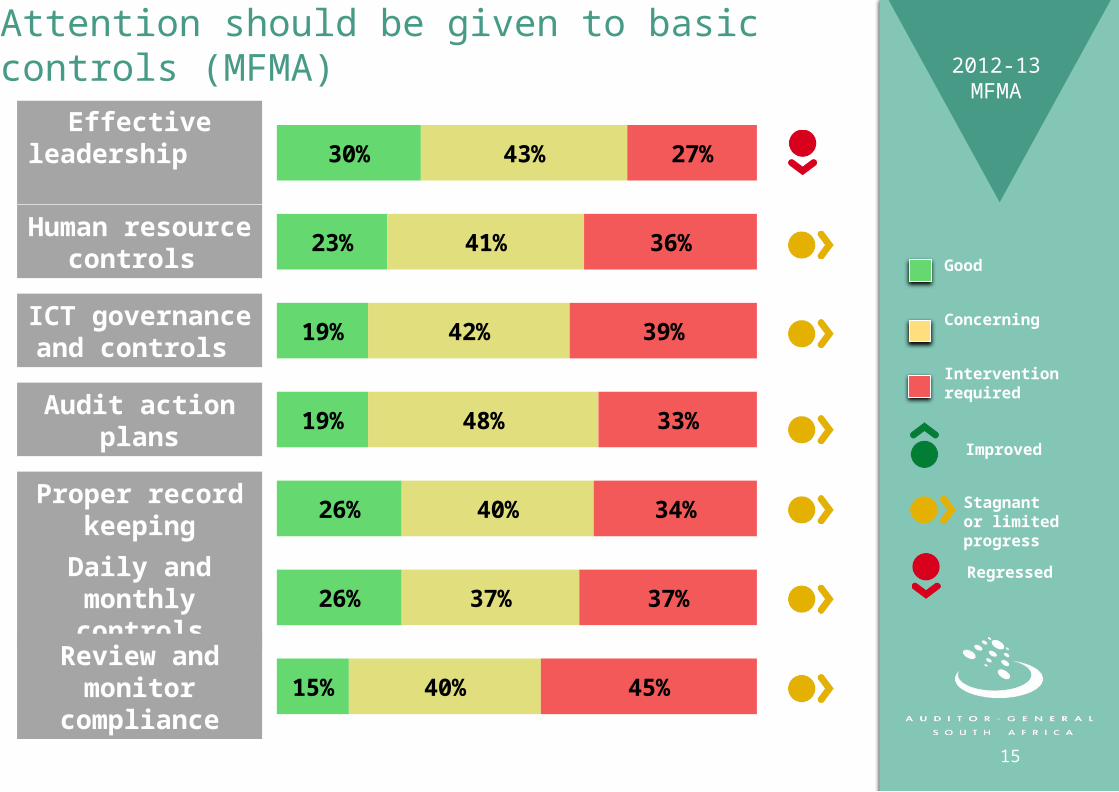

Attention should be given to basic controls (MFMA)

15%

26%

26%

19%

19%

23%

30%

40%

37%

40%

48%

42%

41%

43%

45%

37%

34%

33%

39%

36%

27%Effectiveleadership

Human resource controls

ICT governance and controls

Audit action plans

Daily and monthly controls

Review and monitor compliance

Proper record keeping

Good

Concerning

Intervention required

Improved

Regressed

Stagnant or limited progress

Understanding and monitoring of the municipal manager’s role are key to improving internal control environment

Role of the municipal manager

Robust financial and performance management

systems

Full and proper records of financial affairs

Effective, efficient and transparent systems for financial and risk management and internal controls

System of internal audit

Develop and implement policies – tariff, rates, credit control, debt collection and SCM

Appropriate management, accounting and information systems – assets, liabilities, revenue and expenditure

Effective, efficient, economical and transparent use of resources

Prevention of unauthorised, irregular and fruitless and wasteful expenditure and other losses

Oversight and accountability

Act with fidelity honesty, integrity and in best interest of municipalities

Manage and safeguard assets and liabilities

Take appropriate disciplinary steps against any official who commits act of financial misconduct or an offence

Disclose all material facts to council or mayor

Commitment and ethical behaviour

The role of the municipal manager is critical to ensure:

timely, credible information + accountability + transparency + service delivery

Executiveauthority

Required assurance levels

Extensive Extensive Extensive

Management’s assurance role• Senior management – take

immediate action to address specific recommendations and adhere to financial management and internal control systems

• Accounting officers/ authority – hold officials accountable on implementation of internal controls and report progress quarterly and annually

• Executive authority – monitor the progress of performance and enforce accountability and consequences

Management assuranceFirst level of assurance

SeniorManagement

Accountingofficers/authority

Combined assurance approach to oversight Oversight assurance

Second level of assurance

Coordinating /Monitoringinstitutions

Internalaudit

Auditcommittee

Extensive Extensive Extensive

Required assurance levels

Oversight’s assurance role• National Treasury/ DPSA – monitor

compliance with laws and regulations and enforce appropriate action

• Internal audit – follow up on management’s actions to address specific recommendations and conduct own audits on the key focus areas in the internal control environment and report on quarterly progress

• Audit committee – monitor risks andthe implementation of commitments on corrective action made by management as well as quarterly progress on the action plans

Independent assuranceThird level of assurance

Oversight(portfolio

committees/ councils)

Publicaccounts

committee

National Assembly

Extensive Extensive Extensive

Required assurance levels

Role of independent assurance• Oversight (portfolio committees)

– review and monitor quarterly progress on the implementation of action plans to address deficiencies

• Public accounts committee – exercise specific oversight on a regular basis on any report which it may deem necessary

• National Assembly – provide independent oversight on the reliability, accuracy and credibility of National and provincial government

Related Documents