Sectoral Shocks in a Dependent Economy: Long-Run Adjustment and Short-Run Accommodation Author(s): J. Peter Neary and Douglas D. Purvis Source: The Scandinavian Journal of Economics, Vol. 84, No. 2, Proceedings of a Conference on Long-Run Effects of Short-Run Stabilization P olicy (1982), pp. 229-253 Published by: Wiley on behalf of The Scandinavian Journal of Economics Stable URL: http://www.jstor.org/stable/3439637 . Accessed: 04/07/2013 15:21 Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at . http://www.jstor.org/page/info/about/policies/terms.jsp . JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range of content in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new forms of scholarship. For more information about JSTOR, please contact [email protected]. . Wiley and The Scandinavian Journal of Economics are collaborating with JSTOR to digitize, preserve and extend access to The Scandinavian Journal of Economics. http://www.jstor.org

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

7/28/2019 Artículo Neary

http://slidepdf.com/reader/full/articulo-neary 1/26

Sectoral Shocks in a Dependent Economy: Long-Run Adjustment and Short-RunAccommodationAuthor(s): J. Peter Neary and Douglas D. PurvisSource: The Scandinavian Journal of Economics, Vol. 84, No. 2, Proceedings of a Conferenceon Long-Run Effects of Short-Run Stabilization Policy (1982), pp. 229-253

Published by: Wiley on behalf of The Scandinavian Journal of EconomicsStable URL: http://www.jstor.org/stable/3439637 .

Accessed: 04/07/2013 15:21

Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at .http://www.jstor.org/page/info/about/policies/terms.jsp

.JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range of

content in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new forms

of scholarship. For more information about JSTOR, please contact [email protected].

.

Wiley and The Scandinavian Journal of Economics are collaborating with JSTOR to digitize, preserve and

extend access to The Scandinavian Journal of Economics.

http://www.jstor.org

This content downloaded from 200.123.187.130 on Thu, 4 Jul 2013 15:21:12 PMAll use subject to JSTOR Terms and Conditions

7/28/2019 Artículo Neary

http://slidepdf.com/reader/full/articulo-neary 2/26

Scand.J.ofEconomics 4 (2), 229-253, 982

Sectoral hocksna Dependentconomy: ong-runAdjustmentndShort-runccommodation

J. PeterNearyUniversityollege,Dublin,reland

Douglas D. Purvis*Queen'sUniversity,ingston,ntario, anada

AbstractThispaper xamineshe llocationndstabilizationonsequencesf a resource oom nasmall peneconomy. oth he ntersectoralllocation fcapital ndtheprice fnon-tradedgoodsadjust luggishly;n contrast he nominalxchange ate djusts nstantaneouslyoensure hat he onditionsor ncoverednterestaritynthepresencefrationalxchange

rate xpectationsrealwaysmet.Theabilityfmonetaryolicy ostabilize he conomysexamined,nd t s shown hat, venwhennterventions ustifiednprinciple,olicy rrorswhichrisefromonfusingeal ndmonetaryhocksmayworsenmacroeconomicerform-ance.

I. Introduction

Despite, rperhaps ecauseof, he arge mountfresearchevoted o thestudy fmacroeconomictabilizationolicy, he1970sfailed o produce

anythingike consensus nthe ubject.Muchoftherecentiteratureasfocussed nprovidingxplanationsordeviations rom heclassicalnormofperpetual ull mployment,ndon analysingherobustnessfvariouspolicy rescriptionsnder lternativeationales or heuseof suchpolicy.Whileproponentsfthe"new Classicalmacroeconomics"aveputfor-ward n equilibriumnterpretationfthebusiness ycle nwhichnocon-structiveole existsfor"Keynesian"demandmanagement,thershaveinvokedwage-pricetickinesss a justificationor olicy ctivism.

However, hisfocuson short-runemandmanagementas distractedattentionrom he onger-runmplicationsf nterventionhroughts ffectson investmentndresource llocation. hispaper ttemptsoredresshebalancebyexploringhe nteractionsetweenxogenoushocks, hort-runstabilizationolicy, nd long-runesource llocationn a modelwhich

* We aregratefuloourdiscussant,ohn lemming,ootheronferencearticipants,ndtoNeilBruce,Willem uiter, arsCalmforsndSlobodanDjajicforhelpfulomments.hisresearch assupported,npart, ytheCommitteeor ocialScienceResearchn reland.

Scand. J. ofEconomics 1982

This content downloaded from 200.123.187.130 on Thu, 4 Jul 2013 15:21:12 PMAll use subject to JSTOR Terms and Conditions

7/28/2019 Artículo Neary

http://slidepdf.com/reader/full/articulo-neary 3/26

230 J. P. Neary and D. D. Purvis

combines rich roductiontructureith n explicitreatmentf money-market quilibriumnd rational xchange-ratexpectations. he modelwas introducedn Neary& Purvis1981)wheret was shown hat hereal

adjustmentftheeconomyrisingromluggishntersectoraleallocationofresourcesmplies hat henominalxchange atemay vershoottsnewlong-runaluefollowingn exogenous eal hock, venwhen llwages ndprices re perfectlylexible.nthepresentaperwe relax his ast ssump-tion nd thus re able to examine he nteractionetween hemacroeco-nomic ynamicsesultingromticky rices ndtheMarshallianynamicsarising romluggishactor eallocation.

While urfocus s on the ong-runffectsfstabilizationolicy,we do

not conceiveof interventions taking lace in a vacuumbutrather sevolvingn response o specific xogenousdisturbances.he dynamicresponse f the conomyhus eflectsoth he"natural" esponse ollow-ing he hock ndthe induced"responseo thepolicy.Althougholicy scharacterizeds intendingomitigateheeffectsf thedisturbances,heanalysis uggests ays nwhicht mightctuallyxacerbateucheffects.

Ourprocedures toanalyse wodifferentxogenous hockswhich avesimilar hort-runffects ut differentong-runmplicationsorresourceallocation. olicieswhich re appropriateor ne maynotbe appropriatefor he ther. et,since he mpactffectsresimilar,he womaybe hardto distinguishf the shocksthemselvesre not directlybservable; hisleadsus to a discussionfpolicy rrors. fthe wo hocksweconsider,hefirsts a purelymonetaryisturbancentheform f an equal percentageincrease n all foreignrices.The second s a "resourceboom" whichalters he ong-runllocation fresources;his ocus na "resource oom"underlieshe pecificsftherealmodel.

The allocation nd stabilizationonsequences fresource oomshavebeen nalysed lsewhere. orden& Neary 1982)usea three-sectorodel-resources, manufactures,nd non-tradedervices-to investigatehechannelswhereby resource oom an eadto a reductionfoutputn themanufacturingector, phenomenonftenabelled de-industrialization"or the "Dutchdisease". Two mainchannels re identified: resource-movement ffect,wherebythe boomingsectordirectly r indirectly ids

resourceswayfromhemanufacturingector,nd

spendingffecthich

squeezesprofitabilitynmanufacturingyraisinghedemand or ervicesandso loweringherealexchange ate therelative rice ftraded onon-tradedgoods). Buiter& Purvis 1981) arguethatde-industrializationnmanyountriess not ssociatedwith significantovementf abourntotheboomingector nd nstead tress hereal ppreciationrisingromheresource oom nconjunction ith ticky omestic rices. n theirmodelresourcesndmanufacturingo not ompete irectlyor actorsfproduc-tion inceresource utputs taken s exogenous; enceno labour-market

Scand. J. ofEconomics 1982

This content downloaded from 200.123.187.130 on Thu, 4 Jul 2013 15:21:12 PMAll use subject to JSTOR Terms and Conditions

7/28/2019 Artículo Neary

http://slidepdf.com/reader/full/articulo-neary 4/26

Sectoral hocks n a dependentconomy 231

pressuresmerge, nd deindustrializationccurs nstead hroughhefor-eign xchangemarket.'

The model used in thispaperretains hethree-sectorrameworkf

Corden& Nearybutmodifiesheunderlyingtructureo reflectheBuiter& Purvis iewthat hedirect abour-marketffectsrisingromxpansionof theresource ector re minimal.roductionftheresources assumedtorequire specific actornaddition ocapital, utnot abour.Manufac-turedgoods are producedusing capital and labour while services reproducedusingonly abour.Labour is freelymobilebetween he twosectors nwhich t is used,manufacturingndservices. n contrast,heallocation f capitalbetween hesectorsnwhichtis used,benzine nd

manufacturing,s fixedntheshort un ndvariable nly n the ongrun.Thisproductiontructures combined ith he ssumptionhat he cono-my s "dependent" nthesensethat t s a price aker n themarkets orboth raded oods;hence hedomestic emand epercussionsfthe xoge-nousshockshavedirectnfluencenly n the ervices ector.

Theplanof thepaper s as follows. ection Isketches hedetails ftherealmodel nd analyses ts short- nd long-runesponses o a resourceboom.Section II extends heanalysis o incorporatelowadjustmentn

the elativerice f ervices,while ectionV introducesmacroeconomicframeworkndexamines hedynamicshat risewhenboth hepriceofservices nd theallocation fcapital reslow toadjustwhile henominalexchange ate sallowed o float. ectionV then ocusses nthekeypolicyissues ndSectionVI presentsomeconclusions.

II. Resource llocationnd Marshallian djustment

in a DependentconomyIn this ectionweintroducehebasicproductionndconsumptionelation-shipsof therealpart f ourmodel, ndillustrateheresponses foutputandresource llocation o structuralhocks.Weexamine oth hort-ndlong-runesponsesntheMarshallianense hat omefactors fproductionarefixed ntheshort unbutvariablen the ongrun.However, nthissectionwe abstractrom hemacroeconomicistinctionetweenhortndlong un hat rises n thepresence fnominal rice tickinessy ssuming

perfectrice lexibility.

TheModelThemodel s characterized ythree ectors; heeconomy roduces nenon-tradedood (services) nd twotraded oods manufacturesnd the

' A thirdpproachstoemphasizehe ntermediateoods spect fresources,s isdone, orexample, yBruno& Sachs 1979) ndDjajic 1980).However,his annot ecentral othecase treated erewhere boomresultsrom domesticiscoveryf traded esource.

Scand. J. ofEconomics 1982

This content downloaded from 200.123.187.130 on Thu, 4 Jul 2013 15:21:12 PMAll use subject to JSTOR Terms and Conditions

7/28/2019 Artículo Neary

http://slidepdf.com/reader/full/articulo-neary 5/26

232 J.P. Neary ndD. D. Purvis

resource ood,benzine).We assume hat he conomys small n termsfworldmarketso that t takes heforeignurrencyrices fthe wo radedgoods, nd hence heir elative rice, s given.

The assumptionsoncerninghetechnologyf productionre intendedto reflect he stylized actsthatnon-tradedervices re highlyabour-intensive hileresource-extractiveectors se very ittleabour.Accord-ingly,heoutputf ervices, s, ispresumedorequirenlyabour,ndbyappropriatehoiceof unitsthe input-outputoefficients set equal tounity.2

Xs = Ls (1)

Thismeans hat hedomestic rice f ervicesmay eidentifiedhroughoutwith hewage rate:

Ps= W (2)Labour s also usedinconjunction ith apital o producemanufacturedgoods:

XM XM(KM,LM) (3)

Finally, enzines produced sing apital nda specific actor, :

XB = XB(KB, V) (4)

We assumethat abour s in fixed upply nd instantaneouslyobilebetween heservices ndmanufacturingectors. n this ectionwe alsoassume hat hefull mploymentonditioniven yequation5) is alwayssatisfied.3

LM+Ls = L (5)

While he services nd manufacturingectors huscompete irectlyorlabour, here s no such direct ink between heservices nd resourcesectors incethe atter oesnotuse labour.There re,ofcourse, ndirectlinks etweenervicesnd benzine hroughhemarketor apital,which sused n theproductionfboth enzinendmanufactures.owever, apital

is a fixednputntheshort

un,ndcanonlybe adjusted lowly hrough

time nresponse ochangesnitsperceived eturn. etailsof this djust-mentmechanismrepostponed ntilater.

Thedemand ideofthemodel s straightforward.incethecountrys aprice-takernworldmarkets ormanufacturedoods ndbenzine, omestic

2 See Kouri1979)for nearlier seofthis ssumption.3 In SectionII we replace his ssumptionith nespecifying"naturalevel"ofemploy-mentboutwhichctual mploymentanfluctuate.

Scand. J. ofEconomics 1982

This content downloaded from 200.123.187.130 on Thu, 4 Jul 2013 15:21:12 PMAll use subject to JSTOR Terms and Conditions

7/28/2019 Artículo Neary

http://slidepdf.com/reader/full/articulo-neary 6/26

Sectoral hocksn a dependentconomy 233

demand or hesegoodsplaysnorole ndeterminingheir rices routput.Incontrast,rice ndquantityn themarketor ervices re nfluencedydomestic emand. omestic emand or ervices, s, depends ponprices

and real ncomeYas shown nequation6) where he igns fthepartialderivativesreas shown:

CS= CS(PS, M, B,Y) (6)_ ? ? +

If services re net substitutes or manufacturesnd benzine, he twouncertainignswillbepositive; or oncreteness eassumehenceforward

that his s thecase.In later ectionswe willexaminemacroeconomichenomena singframeworknwhichnominal rices re determined.owever,weconfineourattentionnthis ection nd thenext o "real" variables.Henceonlyrelativerices redetermined;ationalncome ndexpenditurerealwaysequal, mplyingzerotrade alance talltimes. or thepresent echoosemanufacturedoodsas numeraire,nd defineherealexchange ate, r,astherelative rice fmanufacturesnterms fservices:

I=PM/PS = PM/W (7)

Movementsn therealexchange ate resimplyhe nverse fmovementsin therelative rice fservices r,equivalently,ntherealwagerate acedbythemanufacturingector.

Wewish oexamine owtheoutputfthe hree oods ndthe llocationoffactorsespondoa resource oom ntheform f nexogenousncreaseineither heworldpriceof benzine r intheavailable upply f V,the

specificactor sed ntheproductionfbenzine. o doso,wefirstxaminethedeterminationf equilibriumnd thensee howthatequilibriumsperturbedy a resource oom. Technical etails ndderivations aybefoundntheAppendix.)

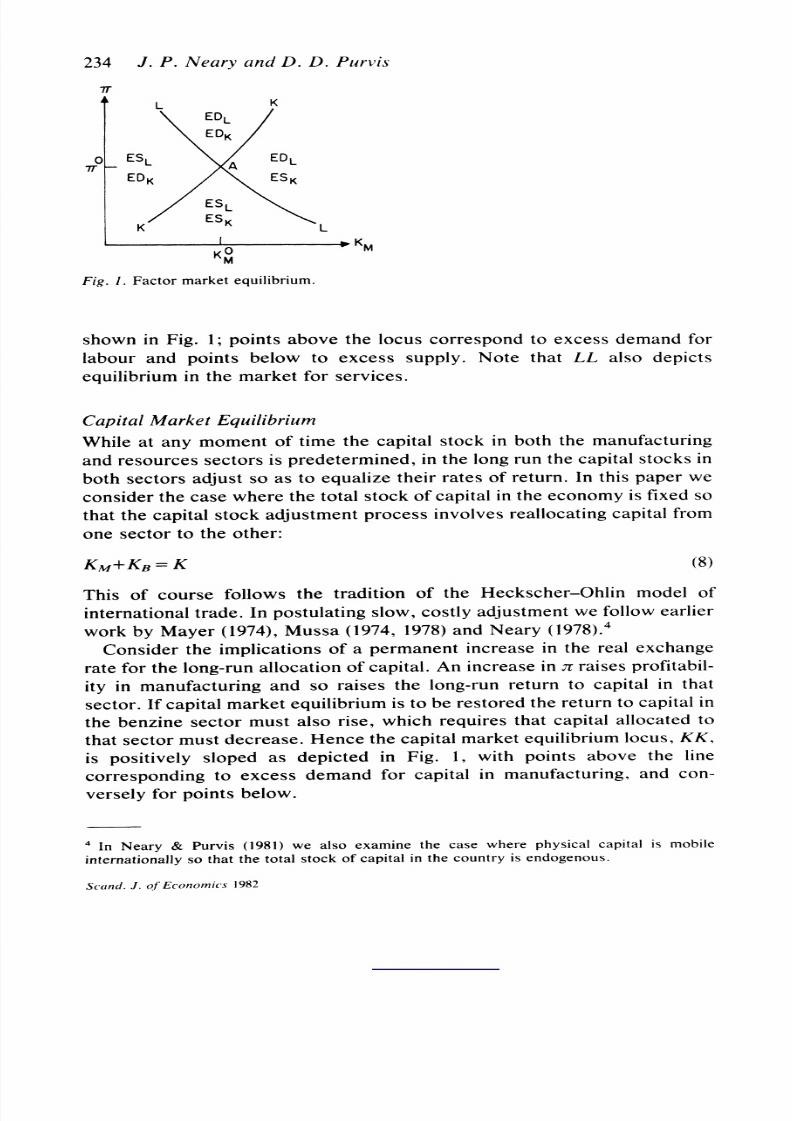

LabourMarket quilibriumIn Fig. 1 the combinationsf thereal exchange ateand the sectoralallocationfcapital onsistent ithabourmarketquilibriumredepictedbythe urve L. An ncreasenAr,which s a fall nthemanufacturingealwage, ncreases hedemand or abournthemanufacturingector.A risein r sequivalent oa fall nPs so that hedemand or ervices,ndhencefor abour n theservices ector,risesas well.An increase n :r leads,therefore,oan unambiguousncreasenthedemand or abour.A reduc-tionnthe apital tocknthemanufacturingectorwould, ta givenwage,leadtoa reductionnthedemand or abournthemanufacturingector.Hence the labourmarket quilibriumocus LL is negativelylopedas

Scand. J. ofEconomics 1982

This content downloaded from 200.123.187.130 on Thu, 4 Jul 2013 15:21:12 PMAll use subject to JSTOR Terms and Conditions

7/28/2019 Artículo Neary

http://slidepdf.com/reader/full/articulo-neary 7/26

234 J.P. Neary nd D. D. Purvis

7r

L KEDL

EDK

0 ESL \ EDL

EDK ESK

ESL

K ESKL. - - lo - wKM

KM

Fig. 1. Factormarketquilibrium.

shownn Fig. 1; points bovethe ocuscorrespondoexcessdemand orlabourand pointsbelow to excess supply.Note thatLL also depictsequilibriumnthemarketor ervices.

CapitalMarket quilibrium

While t anymomentftime hecapital tock n both he manufacturingandresourcesectorsspredetermined,nthe ong un he apital tocksnboth ectors djust o as toequalizetheir ates freturn.nthispaperweconsiderhe asewhere he otal tock fcapitalnthe conomysfixedothat he apital tock djustmentrocessnvolves eallocatingapital romone sector otheother:

KM+KB= K (8)

This of coursefollows he traditionf theHeckscher-Ohlin odelofinternationalrade. npostulatinglow, ostly djustmente followarlierwork yMayer1974),Mussa 1974,1978) ndNeary 1978).4

Consider he mplicationsfa permanentncreasen therealexchangerate or he ong-runllocationfcapital.An ncreasen rraisesprofitabil-ity n manufacturingnd so raisesthe ong-runeturno capital n thatsector.fcapitalmarketquilibriums toberestoredhe eturnocapitaln

thebenzine ectormust lso rise,which equireshat apital llocated othat ectormust ecrease.Hencethe apitalmarketquilibriumocus,KK,is positivelysloped as depicted in Fig. 1, withpoints above the line

correspondingo excess demandforcapital n manufacturing,nd con-versely orpoints elow.

4 In Neary & Purvis (1981) we also examine the case where physical capital is mobile

internationallyo thatthetotalstockofcapital in thecountrys endogenous.

Scand. J. ofEconomics 1982

This content downloaded from 200.123.187.130 on Thu, 4 Jul 2013 15:21:12 PMAll use subject to JSTOR Terms and Conditions

7/28/2019 Artículo Neary

http://slidepdf.com/reader/full/articulo-neary 8/26

7/28/2019 Artículo Neary

http://slidepdf.com/reader/full/articulo-neary 9/26

7/28/2019 Artículo Neary

http://slidepdf.com/reader/full/articulo-neary 10/26

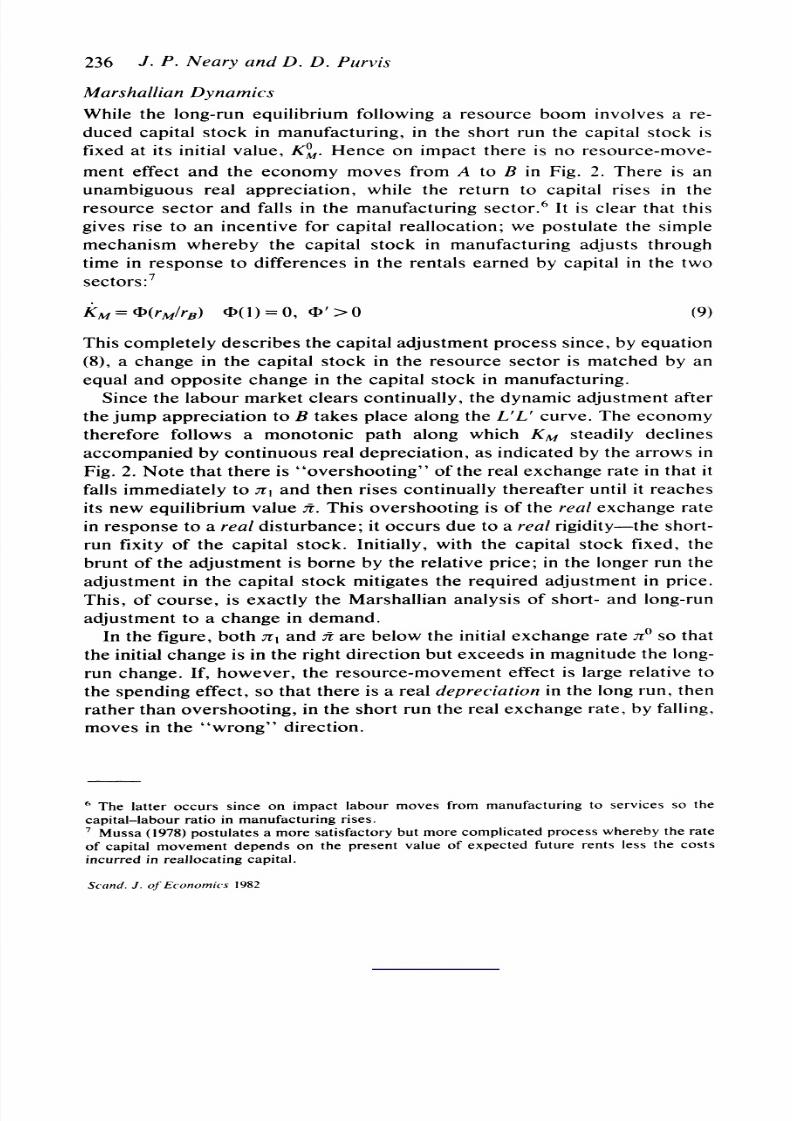

Sectoral hocks na dependentconomy 237

III. Marshallian djustmentithRelative Price Rigidities

In thepreviousection, ollowingeary& Purvis1981),

weconsideredheshort-ndlong-rundjustmento a sectoral hockunder heassumption

that omestic rices re nstantaneouslylexible.n thepresentectionweallowfor hepossibilityhat herelative rice f ervicesdjusts luggishlyinresponse o imbalances etween upply nd demand.Recallinghat nincrease ntherealexchange ate, sr,s equivalentoa fall n therelativeprice fservices,wemaywrite:

r=W(XSICs) I(1) = 0, '>0 (10)

Sincelabour s theonlyfactor sed intheservices ector, quation10)maybe interpreteds either labour-marketra services-marketdjust-mentmechanism.8husthepresence fnon-marketlearingn he ervicesmarkets equivalento a departurerom ull mploymentith hewagerateadjusting lowly o eliminate nder- r over-fullmployment.heparameter in equation 5) in the ast section hould hereforeow beinterpreteds the "natural"rateof fullemploymentather hanas a

bindingonstrainthich annot e exceeded nthe hort un. n order osimplifyhe nalysisweignore hefact hat eparturesromhis natural"levelmaycause either irmsr households o facequantityonstraints,forcinghem orecalculate heir ecisions nothermarketsnthemannerfamiliarrom lower's"dual-decisionypothesis". enceouranalysissstrictlypplicable nly ntheneighbourhoodffull mployment,lthoughfor he ssuesonwhichwewish ofocus his missionsnot crucial ne.9

While nthepresentectionwe allowfor luggishelative rice djust-

ment, hemodel s still realone in whichnominalmagnitudesre notdetermined.hedynamicvolutionf he ystemanthereforeeillustrat-ed in Fig. 3, whoseessential eaturesre identical o thoseof Fig. 2.However, he conomysno ongeronstrainedo ie onthe abour-marketequilibriumocus L'L'. Recallthatpoints bovethis ocuscorrespondoexcessdemand or ervices ndhence oupward ressurentheir rice,andconverselyorpoints elowthe ocus;theresultingendenciesor herealexchange ateto adjustare indicated ytheverticalrrows n the

diagram.As shown n theAppendixsee equationA.20), thesystemsglobally table;whetherrnot tgeneratesyclical djustmentathsde-

8 Theimplicationsfsluggishrice djustmentavebeenstudiednopen-economyodelsby, mong thers, ornbusch1976) nthe ontextfgoods-marketdjustmentndNomanJones1980) nthe ontextf abour-marketdjustment.9 This mountso gnoringhe ncomeffectsnthedemandor ervicesndmoneyausedbydeparturesromull-employment.heconsequencesf disequilibrium"pilloversnopeneconomies avebeen xplored yDixit 1978), iviatan1979) ndNeary1980).

Scand. J. ofEconomics 1982

This content downloaded from 200.123.187.130 on Thu, 4 Jul 2013 15:21:12 PMAll use subject to JSTOR Terms and Conditions

7/28/2019 Artículo Neary

http://slidepdf.com/reader/full/articulo-neary 11/26

238 J. P. Neary and D. D. Purvlis

L' ~~~~~~~~~K'

7r?_ v A n

A \ 1,~~~~

B

L'K

K KO MM M

Fig. 3. Simultaneous djustment f the capital stock and the real exchangerate.

pendson boththeparametersfthe ong-run odel ndon the relativeadjustmentpeedsembodiedn the djustmentquations 9) and 10).

Theresponse f theeconomy oa boom s now easilydeterminedrom

Fig. 3. Startingn nitialong-runquilibriumtpoint , theboomgives iseto excessdemand or ervices ndan incentiveo reallocateapital utofthemanufacturingector.However, nlike heflex-pricease analysedntheprevious ection, he economy oes notshiftmmediatelyo point .Rather,he conomytarts ff n a continuousath o the outh-westfA.Sluggish rice djustmentherefore itigatesheextento which herealexchange ateovershootsts ong-runalue.

When oth he abour ndcapitalmarketsdjust radually,he conomymaymovedirectlyrom to C as inthedotted ath n Fig.3,orcyclicallyas inthedashedpath.The slower s the peedofprice djustmentelativetothe peedofcapital eallocation,hemoreikelys thedirect ath.Hencein contrasto theDornbusch 1976)analysis f nominal vershootingnresponse omonetaryisturbances,tickyelative rices rovide "stabi-lizing" nfluencenthe real)exchange ate.'0

IV. MacroeconomicAdjustmentoMonetary nd Real ShocksInthepreviousectionwepostulated sluggishdjustment echanismortherealexchange ate, . Howeverno accountwas taken fthefact hatchangesn thisvariable eflecthangesnboth henominal rice fserv-

"' We have restricted ur discussion to the "plausible" case of long-run ppreciation. finstead, the long-run ffect s a rise in r, then nevitably here must be at least one turningpoint n rduring headjustment.

SC(and.J. ofEconomics 1982

This content downloaded from 200.123.187.130 on Thu, 4 Jul 2013 15:21:12 PMAll use subject to JSTOR Terms and Conditions

7/28/2019 Artículo Neary

http://slidepdf.com/reader/full/articulo-neary 12/26

Sectoral hocksna dependentconomy 239

ices,Ps, andthe nominal xchange ate,E, andthat hedeterminantsfthese wocomponentsrelikely obe very ifferent.hus, nstead f 7)wemaywrite:

EPf{P5 (I 1)

where f is thepriceofmanufacturesnforeignurrency,ssumed obeexogenouslyetermined.ollowing ornbusch1976),we assume hat henominal riceof domestic oodsmovesslowly o eliminatembalancesbetweenupplynddemand.Hence 10) is replaced y:

Ps=W(CsIXs); W(1)=0, II>0 (12)Bycontrast,henominalxchange ate s assumed obe determinedy

therequirementfstock quilibriumnthemarket or oreignxchange,nan environmenthere xchange-ratexpectationsreformed ationallyanddomestic nd foreignnterest-bearingssets are perfect ubstitutes.The latter ssumptionmplies hatdomestic ndforeignominalnterestrates relinked ytheuncoverednterestarityonditioniven yequa-tion 13).

i= if+E (13)

E isthe xpected roportionateate fchange f henominalxchange atewhich, iven he ssumptionfrationalxpectations,qualsthe ctual ateofchange.Equation 13) thusshowsthat hedomesticnterestatecanexceedtheforeignateonly fthere s an expecteddepreciationfthedomesticurrency.

Thedemand or ealbalancesdepends n real ncome ndthedomesticnominalnterestate:

MIP = WD(, ) (14)

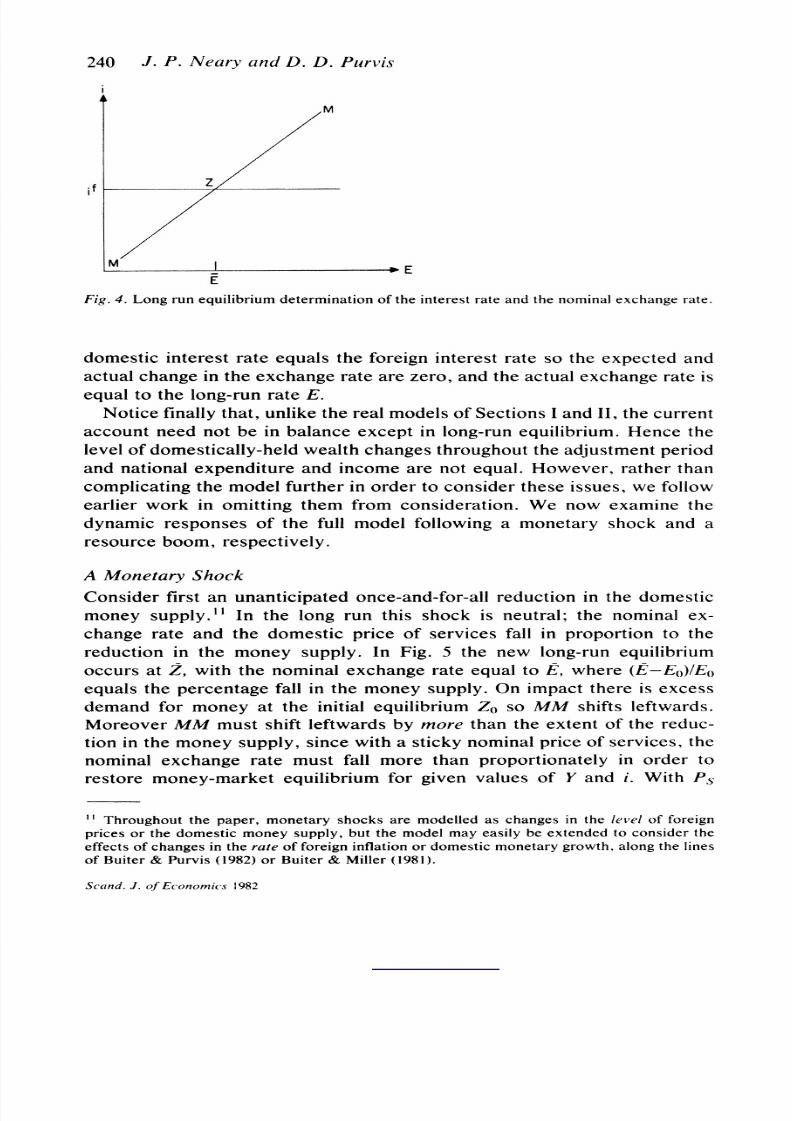

The price evel P is a linearly omogeneousunctionf all final-goodsprices ndhence ncreaseswith henominalxchange ate.An ncreasenthenominalxchange ate hus ivesrise o a fallnrealbalances; hismustbeaccompaniedy rise n or a fall nY norder ormonetaryquilibriumtobemaintained.hevaluesof andE whichreconsistent ithmonetaryequilibriumorgivenvaluesofM, Ps and Y are thusdepicted y thepositivelyloped ocusMM inFig.4. Inthe ong un heratio fE toPs isdeterminedytheconditionsor ealequilibriumutlinednSection andso,for givenM andwith eal ncome titsfull-employmentevel contin-gent ngiven aluesofthe xogenous ariables),hevalueofPs adjusts oensure hat quilibriumftherealandnominalectorss simultaneouslyattained.uch a long-runquilibriums illustratedypoint inFig.4: the

Scand. J. of Economics 1982

This content downloaded from 200.123.187.130 on Thu, 4 Jul 2013 15:21:12 PMAll use subject to JSTOR Terms and Conditions

7/28/2019 Artículo Neary

http://slidepdf.com/reader/full/articulo-neary 13/26

240 J. P. Neary and D. D. Purvis

ifZ/

M P.EE

Fig. 4. Longrun quilibriumeterminationf he nterestate nd henominalxchange ate.

domesticnterest ate quals theforeignnterestate o theexpected ndactual hangenthe xchange ate rezero, ndthe ctual xchange ate sequal to the ong-runateE.

Notice inallyhat, nlike herealmodels fSections and I, the urrent

accountneed notbe in balanceexcept n ong-runquilibrium. ence thelevel fdomestically-heldealth hanges hroughouthe djustmenteriodand national xpenditurend income re notequal. However, ather hancomplicatinghemodel urthernorder o consider hese ssues,we followearlierwork n omittinghem rom onsideration. e now examine hedynamic esponses f thefullmodelfollowing monetaryhockand aresource oom,respectively.

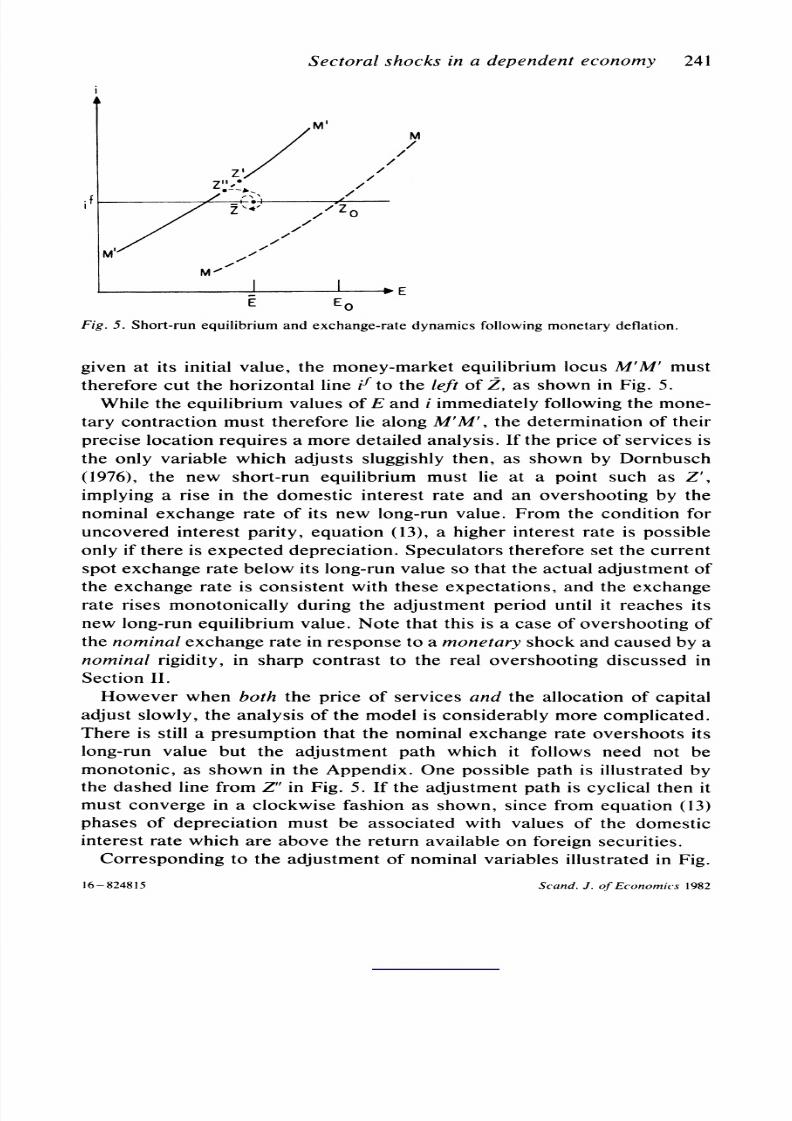

A MonetaryhockConsider irstn unanticipatednce-and-for-alleductionn thedomesticmoney upply." In thelongrun this shock s neutral; he nominal x-changerateand the domestic riceof services all n proportiono thereductionn themoney upply. n Fig. 5 thenewlong-runquilibriumoccurs tZ, with henominalxchange ate qualtoE, whereE-EO)/E1equalsthepercentageall n themoney upply.On impacthere s excessdemand ormoney t the nitial quilibriumOso MM shiftseftwards.

MoreoverMM must hifteftwardsymore han heextent fthereduc-tion n themoney upply,incewith sticky ominalrice fservices,henominal xchangeratemustfall morethanproportionatelyn order orestoremoney-marketquilibriumorgivenvaluesof Y and i. With s

'l Throughouthepaper,monetaryhocks re modelleds changesn the evelof foreignprices r thedomesticmoneyupply, ut hemodelmay asilybeextendedo considerheeffectsfchangesnthe ateofforeignnflationr domesticmonetaryrowth,long he inesofBuiter Purvis1982)or Buiter Miller1981).

Scand. J. ofEconomics 1982

This content downloaded from 200.123.187.130 on Thu, 4 Jul 2013 15:21:12 PMAll use subject to JSTOR Terms and Conditions

7/28/2019 Artículo Neary

http://slidepdf.com/reader/full/articulo-neary 14/26

Sectoral hocks n a dependentconomy 241

M

ZI

.1,

Z 0

M~~M-

E E E

Fig.5. Short-runquilibriumndexchange-rateynamicsollowing onetaryeflation.

given t its nitial alue,themoney-marketquilibriumocusM'M' mustthereforeutthehorizontaline ftothe eft fZ, as shownnFig.5.

While he quilibriumaluesofE and immediatelyollowinghemone-tary ontraction ust hereforeiealongM'M', thedeterminationf their

preciseocation equires more etailednalysis.ftheprice fservicesstheonlyvariablewhich djusts luggishlyhen, s shownbyDornbusch(1976), the new short-runquilibriummust ie at a pointsuch as Z',implying rise n thedomesticnterest ateand an overshootingythenominalxchange ateof itsnew ong-runalue. From hecondition oruncoverednterestarity,quation13),a highernterestate s possibleonlyf here s expected epreciation.peculatorshereforeetthe urrentspot xchange atebelow ts ong-runalue o that he ctual djustmentftheexchange ate s consistent ith hese xpectations,ndthe xchangeraterisesmonotonicallyuringheadjustmenterioduntiltreaches tsnew ong-runquilibriumalue. Note that his s a case ofovershootingfthenominalxchange ate nresponseo a monetaryhock ndcausedbynominal igidity,n sharp ontrasto the realovershootingiscussed nSection I.

Howeverwhenboth hepriceof services nd theallocation fcapitaladjust lowly,he nalysis f themodel s considerably ore omplicated.There s still presumptionhat henominalxchange ateovershootstslong-runalue but the adjustmentathwhich t followsneed not bemonotonic,s shownntheAppendix. nepossiblepath s illustratedythedashed inefrom " inFig.5. If the djustmentath s cyclical hentmust onvergena clockwise ashion s shown, incefromquation13)phasesof depreciationmustbe associatedwithvaluesof thedomesticinterestatewhich reabove thereturnvailable nforeignecurities.

Correspondingotheadjustmentf nominal ariablesllustratednFig.

16-824815 Scand. J. ofEconomics 1982

This content downloaded from 200.123.187.130 on Thu, 4 Jul 2013 15:21:12 PMAll use subject to JSTOR Terms and Conditions

7/28/2019 Artículo Neary

http://slidepdf.com/reader/full/articulo-neary 15/26

242 J. P. Nearly nd D. D. Purvis

5, real variables re also adjusting,incewith sticky omestic riceofservices he nitialmonetaryeflationas real effects. tZ" therelativepriceof serviceshas risen,giving ise to excess supply n that ector.

Accordingo equation12) thepriceof services tarts o fall; his n turntendsto raise real balancesand to reducethedomesticnterest ate.Correspondingo thehigher elative riceof servicess a rise n therealwage.Hence there s an incentiveo reallocate apitalfrom he abour-usingmanufacturingector o theresource ector, nd duringhe nitialstage fthe djustmentrocessXMfallsbelow tssteady-stateevel.

A Resource Boom

The long-runeal effects f a resourceboomwereanalysed n SectionII wherewesawthat he pendingffectf he oom endsoreduce he realexchange atewhereasthe resource-movementffect endsto raise it.There s anadditionalffect orkingn thenominalxchange ate hroughthemoney-marketquilibriumondition14); thiswe call the liquidityeffect.y raisingeal ncome,heboom equires fall nthedomesticricelevel n the ongrunwhich,with constanteal exchange ate, mpliesnominalppreciation. ence we takethis o be the"expected"outcome,

althoughs thefull xpressionor hechangenE (equationA.25) n theAppendix) hows,whether r notthis actually nsues dependson theparametersfthemodel.

Confiningttentiono thecase of nominalndrealappreciationnthelong un, he nduced hangesnnominal ariablesmay gainbe illustratedwith he idof Fig.5. When heprice f services djusts nstantaneously,Neary& Purvis1981) how hat henominal xchange atemay vershootits ong-runaluefollowedy steady epreciations capitalsreallocated

out ofthemanufacturingector.Thispossibilitys illustratedythe hort-run quilibriumtZ' inFig.5 where, nimpact,hedomesticnterestatehas risen.Butfromhe nterestarityonditionhis an occur nlyf hereis a simultaneousxpectationfdepreciationfthedomestic urrency.Rational peculators ill hereforeet thecurrentxchange atebelow tslong-runalue; f he ong-runxchange ate tself alls hen heremust eshort-runvershooting. henboththepriceof services nd thecapitalstock djust luggishly,nitial vershootingfboth he realandnominal

exchange ates sagain possibility,ithubsequentyclical r monotonicmovementowardshenew ong-runquilibrium.

V. Interactions etween ectoralAdjustmentand Macroeconomic olicy

So far urobjective as beentodevelop he ompletemodelnthe bsenceof ntervention.n thepresentectionwe turno the uestionfhowpolicy

Scand. J. ofEconomics 1982

This content downloaded from 200.123.187.130 on Thu, 4 Jul 2013 15:21:12 PMAll use subject to JSTOR Terms and Conditions

7/28/2019 Artículo Neary

http://slidepdf.com/reader/full/articulo-neary 16/26

Sectoral hocks n a dependent conomy 243

M /M/ /

///

f* /

M -

Ml

[ |I*EE E0

Fig. 6. Inappropriateesponse o a foreignrice hock.

rules ntendedo stabilize heeconomyn theshort unmayaffect tslonger-rundjustment.

Inappropriateesponses o Nominal xchangeRate MovementsWe beginby considering foreign ricedisturbance hich fproperlyperceived equires o response rom he uthorities.tartingn nitialong-run quilibriumtZO nFig. 6, suppose hat heworld rices fboth radedgoods increaseby an equi-proportionalmount. ftherewere no policyresponse, he new ong-runquilibriumtZ., with proportionateall ntheexchangerateto E,, would be attained nstantaneously. here would benorealchanges ven n the hort un, nd thedomesticurrencyrices f

allthree oodswould emainnchanged.incenochangenPs isrequired,nodynamicsre elicited.'2However henominalppreciationntailednmovingromO oZ, may

be resisted, erhaps n thefalsegrounds hat t willalso imply realappreciationeading o a loss incompetitivenessfthe domesticraded-goods sector.Such a view is incorrect,f course,since thenominalappreciations in response o a foreign ricerise,and so is merelyheprocess y which omestic ompetitivenessskeptn ine.However,f he

source fthefall nthenominalxchange ate snot learlydentified,hesituationmight e confusedwith newhere nominalppreciationoes

2 The new ong-runquilibriums attainednstantaneouslyecause n our model heonlyrolefor he xchange ate s toconvertoreignricesnto omesticurrencynitsndhenceonly heproduct fE andthe espectiveoreignricesmatters.f he xchangeate layednadditionalole, or xample nconvertingoreignenominatedssets nto omesticurrencyunitswhichhennfluencedeal pending,he esults ouldbesubstantiallyifferent.ee,forexample, alvo & Rodriguez1977)orPurvis1979).

Scand. J. ofEconomics 1982

This content downloaded from 200.123.187.130 on Thu, 4 Jul 2013 15:21:12 PMAll use subject to JSTOR Terms and Conditions

7/28/2019 Artículo Neary

http://slidepdf.com/reader/full/articulo-neary 17/26

244 J. P. Neary and D. D. Purvis

7T

L

I+

K

_M~77

K L

KM M

Fig.7. Realadjustmento nappropriateonetaryntervention.

harmhe ompetitiveosition fthedomesticxport ector. etusexam-ine the implicationsf usingmonetaryolicyto "offset" henominalappreciation.

Supposefirsthat hedomesticmoneyupplywereraised nproportionto theforeignricerise. This wouldmeanthat he ong-runquilibriumwouldremaintZO nFig.6 and the ong-runxchange atewould emainatE0. But n the hort unwith s given, herewouldbe anexcesssupplyofmoney t ZO.The MM curveshifts ighto M'M' and theshort-runequilibrium oves to a point uchas Z2. Dynamic djustmentnvolvesinstantaneousncreasesnE and Tfollowedyeitherontinuouspprecia-tion ombined ithncreasesn theprice fdomesticervicesas depictedinFig. 6) or by cyclical djustmentf all nominal ariables. he policymistake esultsn"importing"heforeignricencrease ince lldomesticprices rehighertZOthan t Z1 where heywere nfact nchanged),ndin a misallocation f resources uringheadjustmenteriod incebothnominal nd real exchangeratesdifferrom heir ong-runquilibriumvalues.The real adjustments illustratedn Fig. 7; the initial ndfinalequilibriareboth tA andthe hort-runquilibriummmediatelyollowingthemonetarynterventionsat B. It sclear hat heres at east neturningpointn the djustmentfKM,and nfact yclical djustmentfbothrandKM is also possible.

Analternativeorm fmonetarynterventionouldbe tosimplyix henominalxchange ate tEo inFig.6. Thiswould nvolve n instantaneousincreasenthemoneyupply roportionateothe mpactn thepricendexof therise n the raded-goodsrice i.e., a less-than-proportionatehangein M). Therewouldthen be excess demandfor services eading o acontinuous ise nPs matched ya rise n themoneyupply ufficientokeepreal balancesconstant.n terms fthe nominal ariables nFig. 6

S and. J. ofEconomics 1982

This content downloaded from 200.123.187.130 on Thu, 4 Jul 2013 15:21:12 PMAll use subject to JSTOR Terms and Conditions

7/28/2019 Artículo Neary

http://slidepdf.com/reader/full/articulo-neary 18/26

Sectoral shocks in a dependenteconomy 245

thererenodynamicss the conomyemains tZ0throughout.oweverreal djustmenttill nvolves n nstantaneousncrease nthe eal xchangerate ollowedyeither ontinuouseal ppreciationra clockwiseyclical

path.Theformerase is illustratednFig.7 where he hort-runquilibri-um s atpointC whichnvolves smaller ealdepreciationhanwhen hemoneyupplyncreasesnproportionotheforeignrice hock.

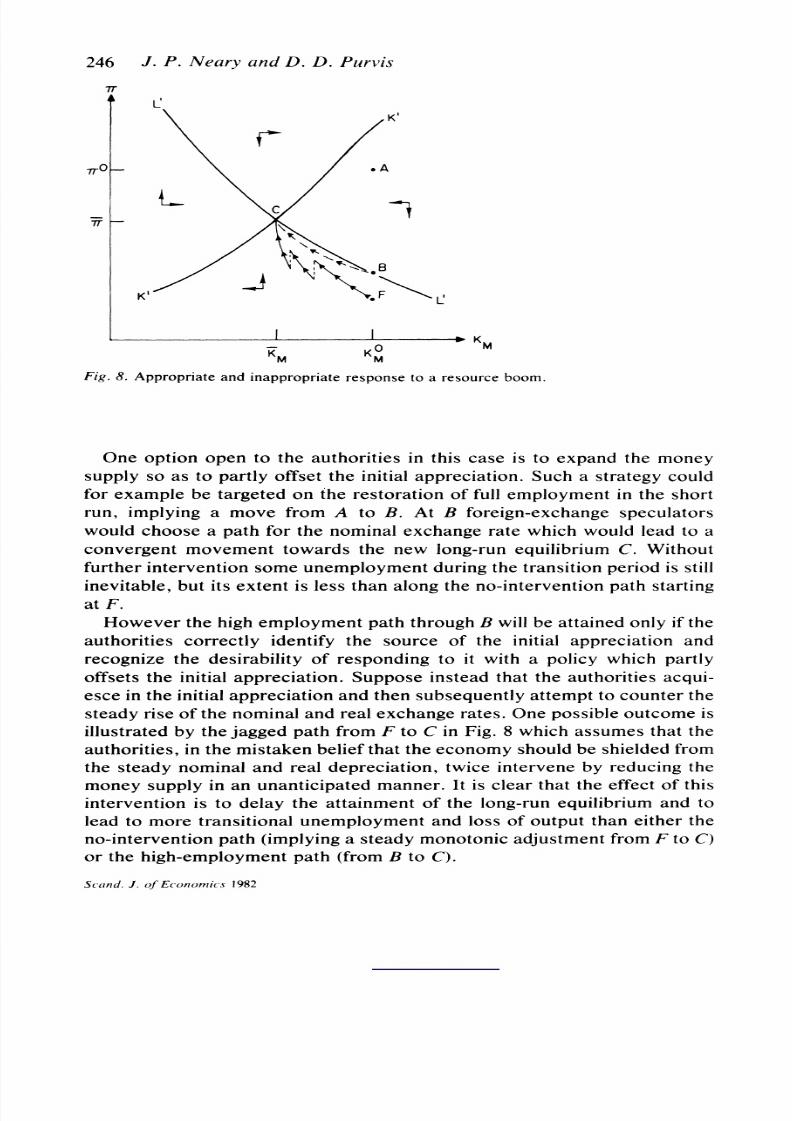

InappropriatePolicies and a Resource Boom

In thecase of a foreignricedisturbanceustconsidered,he ppropriateresponse nthepart fthemonetaryuthorities as toforegonterventionand lettheforeign-exchangearketdjustcompletelyo the shock.By

contrast,nthe ase ofa resource oom he luggishdjustmentfdomes-ticprices rovides rationaleorntervention:omeof he ransitionalossof output nd employmentouldbe avoidedby a monetaryxpansionwhichwouldmitigateheinitial ises n thereal and nominal xchangerates.'3This assumeshowever hat heauthoritiesorrectlydentifyhesource fthe nitialppreciation.fthey ail odo so then y nactionheyin effect olerate hetransitionalnemploymentttributableo thede-industrialisationffect f theboom.Worsestill, fmonetaryolicy s

targetedowards xchange-ratetabilityatherhan owards nternalal-ance itmayexacerbate hemedium-runosts of the boomanddelaytheattainmentf thenew ong-runquilibrium.4

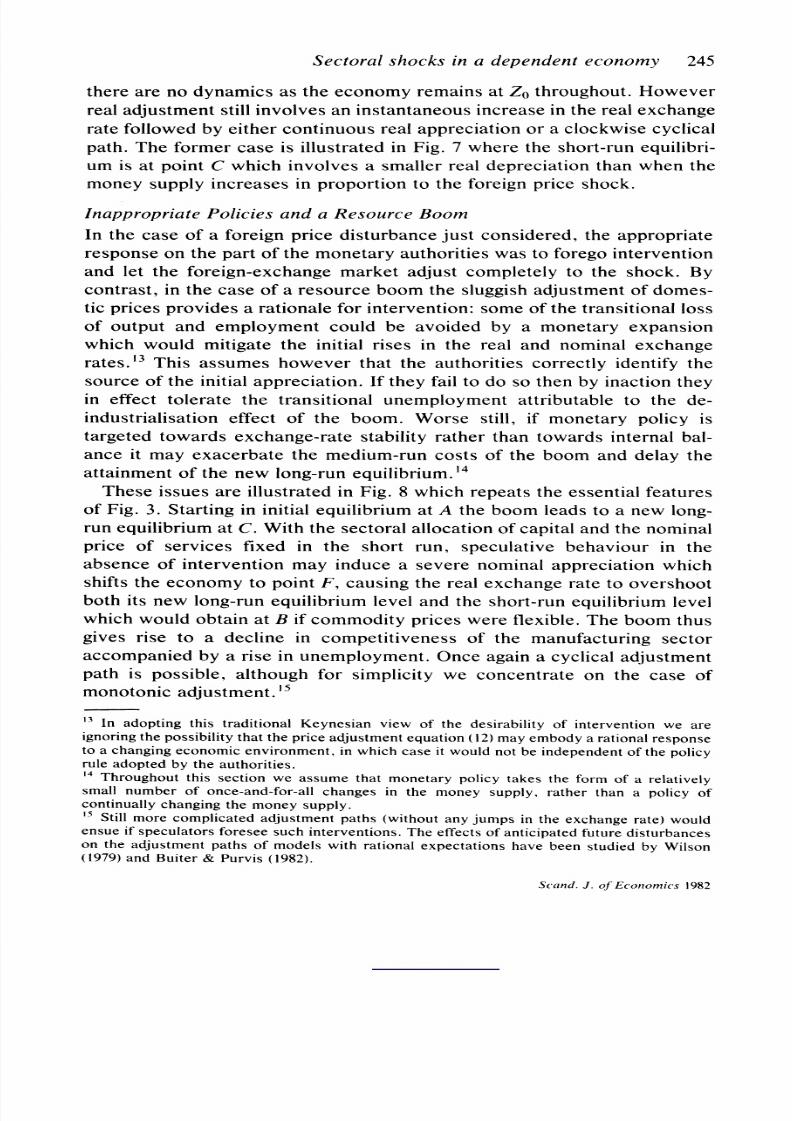

These ssuesare llustratednFig.8which epeats he ssential eaturesofFig.3. Startingn nitialquilibriumtA theboom eadstoa new ong-run quilibriumtC. With he ectoralllocation f apital ndthenominalpriceof servicesfixed n the shortrun,speculative ehaviour n theabsenceof nterventionay nduce severenominalppreciation hich

shiftshe conomy opoint , causing herealexchange ate oovershootboth tsnew ong-runquilibriumeveland the hort-runquilibriumevelwhichwould btain tB if ommodityriceswere lexible. heboom husgivesrise to a decline n competitivenessf themanufacturingectoraccompanied y a rise nunemployment.nceagain cyclical djustmentpath s possible, lthough orsimplicity e concentraten thecase ofmonotonicdjustment.'5

'3 In adoptingthis traditionalKeynesian view of the desirability f interventionwe areignoringhepossibility hat hepriceadjustmentquation 12) mayembody rational esponseto a changing conomicenvironment,nwhichcase itwould notbe independentfthepolicyruleadoptedbytheauthorities.14 Throughout his sectionwe assume thatmonetarypolicy takes the formof a relativelysmall numberof once-and-for-allhanges in the money supply, ratherthan a policy ofcontinually hanging hemoneysupply.'5 Stillmorecomplicatedadjustmentpaths (without ny umps in theexchangerate)wouldensue ifspeculatorsforeseesuch interventions.he effects fanticipated uture isturbanceson the adjustmentpaths of models withrationalexpectationshave been studiedby Wilson(1979) and Buiter& Purvis 1982).

Scand. J. ofEconomics 1982

This content downloaded from 200.123.187.130 on Thu, 4 Jul 2013 15:21:12 PMAll use subject to JSTOR Terms and Conditions

7/28/2019 Artículo Neary

http://slidepdf.com/reader/full/articulo-neary 19/26

246 J. P. Neary and D. D. Purvis

7r

j e L~~~~~~~~~~

K KA M

M M

Fig. 8. Appropriatend nappropriateesponse o a resource oom.

Oneoption pen to the authoritiesn this ase is to expand hemoneysupply o as to partly ffset he nitial ppreciation.uch a strategyouldfor xample e targeted ntherestorationf full mploymentn the hortrun, mplying move fromA to B. At B foreign-exchangepeculatorswould hoosea pathfor henominal xchange atewhichwould ead to aconvergent ovement owards he new long-runquilibrium . Withoutfurthernterventionomeunemploymenturinghe ransitioneriodsstillinevitable,ut tsextents less than long heno-interventionath tartingatF.

However hehigh mploymentath hroughwillbe attainednlyf heauthoritiesorrectlydentifyhe source of the initial ppreciationndrecognize he desirabilityf respondingo it with policywhichpartlyoffsetshe nitialppreciation.uppose nstead hat he uthoritiescqui-esceinthe nitialppreciationndthenubsequentlyttempto counterhesteady ise f henominal ndreal xchange ates.Onepossible utcomesillustratedytheaggedpath rom toC inFig.8 which ssumes hat heauthorities,nthemistaken eliefhat he conomyhould e shieldedromthe teadynominalndrealdepreciation,wice nterveney reducinghemoney upplyn anunanticipatedanner.t is clearthat he ffectfthisinterventions to delaythe attainmentf the ong-runquilibriumnd tolead tomore ransitionalnemploymentnd ossofoutputhan itherheno-interventionath implyingsteadymonotonicdjustmentrom toC)or thehigh-employmentath from toC).

Scand. J. ofEconomics 1982

This content downloaded from 200.123.187.130 on Thu, 4 Jul 2013 15:21:12 PMAll use subject to JSTOR Terms and Conditions

7/28/2019 Artículo Neary

http://slidepdf.com/reader/full/articulo-neary 20/26

Sectoral hocks n a dependentconomy 247

VI. Conclusion

In thispaperwe havepresented model n which omestic ricesdo notrespondnstantaneouslyo imbalances etweenupplynddemand.With-out examininghe microfoundationsf thisprice-stickiness,e haveassumed hat tprovides,nprinciple, justificationor overnmentnter-vention. oweverbecausedomestic actormarketso not djustmmedi-ately o exogenous hocks, isturbancesith imilarhort-runmpactsmayhavevery ifferentong-runffects. ence, s wehave hown,n nterven-tionist overnmenthich s unable o identifyhe ource fa disturbancemayrespond n a mannerwhich xacerbatesheeconomy's erformance

andslowsthereturno long-runquilibrium.Inour view t s therisk fpolicy onfusionsfthis ort atherhan heundesirabilityf activist olicyn tselfwhich onstituteshemajor bjec-tion o a strategyf"fine-tuning"hemacro-economy.his snot odenythatthe authoritiesan and shouldtake actionto offset he effects fsignificantndclearly dentifiablehocks.Butthey hould e conscious ftheneed fordifferentesponses o shockswhich avethe ameshort-runeffects.nparticular, hen nternationalapitalmovementsrevolatilend

exchange-ratexpectationsre formedn a rationalmanner,he uthoritiesshouldnot ttempto offsetmovementsn the xchange atewhich re anessential oncomitantfthe djustmentowards new ong-runealequi-librium. inally, lthough e have concentratedn this aper nmonetaryinterventionhich an only ffect he djustmentath, t s clearthat hesameprincipleslso apply ofiscal nterventionhich an also influencethe conomy's ong-runealequilibrium.'6

Appendix

Thisappendix resents heprincipal quations f themodel ndsketchesthederivationf theresults. urtheretails n theflexible-pricease maybefound nNeary& Purvis1981). Exceptwhere therwisendicated,llvariables re measured s naturalogarithms,enoted y ower-case ym-bols e.g., e=lnE), andexpressed n terms f deviations romheir aluesinthe nitial quilibrium.This s equivalent o choosing nits fmeasure-ment uchthat he nitial quilibriumevels of all variables re equal tounity.) xceptwherenoted, ll coefficientsre defined o bepositive.

16 Asnoted yDixit1978) ndNeary1980) his sonly he ase if he nterventionakes heformfgovernmenturchases fnon-tradedoods ince,withxogenouslyivenworld ricesof traded oods, nterventionn traded oodsmarketsffectivelyypasses hedomesticeconomy.

Scand. J. ofEconomics 1982

This content downloaded from 200.123.187.130 on Thu, 4 Jul 2013 15:21:12 PMAll use subject to JSTOR Terms and Conditions

7/28/2019 Artículo Neary

http://slidepdf.com/reader/full/articulo-neary 21/26

248 J. P. Neary nd D. D. Purvis

A.1. TheReal ModelThe demand or ervices,which s also that ector'sdemand or abour(since abour s theonlyfactor sed there), epends n prices ndrealincome:

CS = --SPS+?BPB+6MPM+91Y (A. 1)

Thecompensatedlasticitiesfdemand iobey hehomogeneityestriction(CB+ EM = 5), and thedomesticprices of tradedgoods are relatedto theirworld ricesbythenominalxchange ate :

ppfe i=BM (A.2)

Real income,y, is defined s nominalncomedeflated y theconsumerprice ndex,p:

P= /BPB+/MPM+#SPS (A.3)

where he/3's reexpenditurehares.In thepresent aperwe consider nlytwosourcesofchange n real

income: irst,n increase nV, the ndowmentf he pecific actor sed nthebenzine ector whose mpact epends n theshareofthat actor nnationalncomeOv); second,an increase n theworldrelative rice ofbenzinewhich aisesreal ncome n theassumptionhat enzines a netexport so that ts share n nationalproduct, B, exceeds its share nnationalxpenditure,B):

Y =V +(OB -B) rB (A.4)

We haveintroducedhesymbol rBodenote heterms ftrade, nd forlater se wedefineras therealexchange ate:

;rB=!P'-PfM = PB PM (A.5)

a PM-PS = e+p{m-W (A.6)

The demand orabour nmanufacturingepends n the uantityfcapital

located here ndon therealwagefacingmanufacturingirms:

im= kM-YM(W-PM) (A.7)

where M s thewageelasticityfthedemand or abournmanufacturing.This n turns related o the evelofemploymentn the ervices ector ythefull-employmentonstraintor abour:

ALM IM+ ALS IS =0 (A. 8)

Scandl(I.J. of Ecooinics 1982

This content downloaded from 200.123.187.130 on Thu, 4 Jul 2013 15:21:12 PMAll use subject to JSTOR Terms and Conditions

7/28/2019 Artículo Neary

http://slidepdf.com/reader/full/articulo-neary 22/26

Sectoral shocks in a dependent conomy 249

whereLj s theproportionffactor used n sector. From quation1) inthetext he evel ofemploymentn the services ectormaybe identifiedwith hat ector's utput.Henceequating emand ndsupply fservices

andsubstitutingromarlier quationsrecallinghatw=ps),weobtain nexpression or he abour-marketquilibriumocus,LL inFig.1, n ermsfkM, w ndexogenous hocks:

ALkM+Er+al = 0 (A.9)

where:

ALYM+CS >O; AL ALM/ALS (A. 0)

and

al-?l0vV? {CB+/1(0OB B)} JTB (A.11)

Inthedefinitionfthe xogenous isturbanceiven yequationA. 1)thecoefficientf TB is the ompensatedross-elasticityfdemand or erviceswith espect otheprice fbenzine, djusted or he erms-of-tradeffecton real ncome.

The capital-marketquilibriumocus is found n a similarmanner yrelatinghedemands or apitalfrom hebenzine ndmanufacturingec-torsbythefull-employmentonstraintor apital:

AKB B+AKMkM = 0 (A. 12)

Thedemand or apital nthebenzine ector epends n thestock f theresource vailablethere nd thereal rental acing hesectorwhere B

denotes herental lasticityfcapitaldemand):

kB= V- YB(rB-PB) (A. 13)

In long-runquilibriumherentalnthebenzine ectormust qualthat nmanufacturing;he atters related o thewagerate ytherequirementhattheprice fmanufactures ustustcoverunit osts:

PM= OLMW+OKMrM (A.14)

whereOij s theshare ffactor inthevalue ofoutputnsector. SettingrM=rB andcombininghese quationswithA.2) yields hecapital-marketequilibriumocus:

YB IKkM L7r+a2 =; AK AKM'IKB' OL OLMI0KM (A.15)

where:

a2 Y-1 V+2TB (A. 16)

Scand. J. of Economics 1982

This content downloaded from 200.123.187.130 on Thu, 4 Jul 2013 15:21:12 PMAll use subject to JSTOR Terms and Conditions

7/28/2019 Artículo Neary

http://slidepdf.com/reader/full/articulo-neary 23/26

250 J. P. Neary and D. D. Purvis

This s depicted y thepositivelylopedKK curve n Fig. 1.

A.2. Long-Run Comparative Statics and DisequilibriumDynamics

The ong-runquilibriumaluesofkM nd rmaybe found ysolvingA.9)and A.15):

A kM -(OLaI+Ea2) (A.17)

A -ft-B _AK I+AL2 (A 18)

where:

A=AALL+YBAKE > 0. (A. 19)

For givenvalues oftheexogenous ariables,he ttainmentf ong-runequilibriums broughtboutbythedynamic djustmentquations 9) and(10) in the text.These may be writtens a matrix ifferentialquation,where andV denote he speeds of adjustmentf thecapital nd labourmarkets,espectively:

[kM][ -

AKIYB T6iz] [kM-kM] (A.20)

The determinant f the coefficientmatrix n (A.20) is given by pTVy-' >0

and thetraceequals -{lpe+qAKy-'}<0. Since the trace nd determinantconditionsresatisfied,he ystemsgloballytable.

During he djustmenteriod, here refurtherncome ffectshat riseas capitalsreallocatedromesstomore roductivese; seeNeary 1982).

These second-orderffectsreneglectednour nalysis.Alternativelynecould consider hese incomeeffects s beinganticipatedo thattheircapitalized alueaugmentshe nitial isturbances measured ya,.

A.3. MoneyDemand and the NominalExchangeRate

Themoney-marketquilibriumondition12) maybe writtens follows:

m-p = ty-_6li (A.21)

(Notethat denotes he evel,not he ogarithm,fthe nterestate.)Using(A.2), A.5), and A.6), theprice ndexgivenn A.3) can be rewritten:

p = e+pM+/B aB /35J (A.22)

Notethatwith7rconstant, changenpf implies uniformhangentheforeign ricesofbothtradedgoods. Equations (A.21) and (A.22) maynowbe combinedtoobtaina relationship inking he ong-run alues ofe and r,

Scand. J. )f conlomli(cs 1982

This content downloaded from 200.123.187.130 on Thu, 4 Jul 2013 15:21:12 PMAll use subject to JSTOR Terms and Conditions

7/28/2019 Artículo Neary

http://slidepdf.com/reader/full/articulo-neary 24/26

Sectoral hocks na dependentconomy 251

substitutingory fromA.4) and recallinghat equals iJ' n long-runequilibrium:

e/37r + a3 = 0 (A.23)

where:

=~+O+1NIT__-"+f (A.24)

CombininghiswithA.6) and A. 18)yields nexpressionor he ong-run

valueofthenominalxchange ate:

The three hannelsby which he nominal xchange ate s affectedyexogenoushocks, ,, a2 anda3, correspondespectivelyo the pending,resource-movementnd iquidityffectsiscussedn the ext.

A.4. Exchange-RatexpectationsndSaddle-PointtabilityWritinghe exchangerate in logarithmicorm, heuncoverednterest

parityondition13)becomes:i =if+~~~~~~~~~~~~~(A.26)

When ombinedwithA.21) thisyields third ifferentialquation.Thedynamicystemmaybe writtens follows:

k -OY-IAK q!OO P0L iF k

PS VAL

_-iVE VEt~

PSP

(A.27)~J 0 613s 6(1l#s)JL_ -

Denotinghe coefficient atrixn (A.27) byA, we wishto solve for tscharacteristicoots,which re the olutions o the haracteristicquation:

flu)= I A+MII=MY3-a2 2+alu-a0=0 (A.28)

where hecoefficientsredefined s follows:

ao0=JA=qOVA >0 (A.29)

al = /npA-6[qOYBAA(-/3S)?+tp-] (A.30)

a2= trA (1-fl5)-qpy-' K-ip (A.31)

Sincethedeterminantspositivehe ystemA.27)must aveeitherneorthree ositive oots. incethe race fA (andso the um ftheroots)maybeeither ositivernegative, ecannot ule ut heunstableonfiguration

Scand. J.ofEconomics 1982

This content downloaded from 200.123.187.130 on Thu, 4 Jul 2013 15:21:12 PMAll use subject to JSTOR Terms and Conditions

7/28/2019 Artículo Neary

http://slidepdf.com/reader/full/articulo-neary 25/26

252 J. P. Nearyand D. D. Purvis

of llthree oots ositive.We focus,however,n themore nterestingasewhere nlyone root s positive.This givesrise to a typical addle-pointstructure:he ingle ositive oot ontributesdirectionf nstability,ut

exchange-ratepeculatorsreassumed ochoose an initial alueof e (andhenceof r) which nsures hat he modelconverges owards long-runequilibrium.

Inorder o solve A.27) we use a techniqueuggested yDixit1980).Heshows that fthe solution athsfor he three ariables re to lie on thestablemanifoldheymust atisfyhefollowingquation:

e(t)-e= u1kM(t)-kM} +u2{PS(t)-PS} (A.32)

where l andu2are elements f the normalized)eft haracteristicectorofA correspondingotheunstable ositiveharacteristicoot.They here-fore atisfyheequation:

[ul u2 -1][-A+,Il=[0 0 0]. (A.33)

where is thepositive oot f A.28). EquationA.33) maybe solved or l

andu2in terms fa:VALU2

U P= L (A.34)

YB K+/

u2- (A.35)

By evaluatingA.28)for =6 itcan be establishedhat/(8)spositive hich

implies hat >,i. Hence (A.34) and (A.35) showthatbothul andu2 arenegative.

Theseresultsmaybe usedtoestablish onditionsnderwhichnexoge-nous shockcauses the nominal xchange ate to overshootts long-runvalue.SincethevaluesofkM ndps are fixed ttheir nitialevels, A.32)implieshat:

e( e=ul(k-kM)+U2(PS-fis). (A.36)

where (0) is thevalue of theexchange ate mmediatelyollowingheshock.The ong-runalue ofkMs lowered ya resource oom ndthat fps also falls nless he pendingffectsdominant. ence, s wasassertedinthetext, heres a presumptionhat (O)-e is negative,mplyinginthecase where <0) that he nominal xchange ateovershoots. owever tdoesnot ppear obepossible oestablishhat his snecessarilyhe ase.

Using A.32), thesystem A.27) maybe reduced o a system ftwodifferentialquations in kM and ps:

Scand. J. ofEconomics 1982

This content downloaded from 200.123.187.130 on Thu, 4 Jul 2013 15:21:12 PMAll use subject to JSTOR Terms and Conditions

7/28/2019 Artículo Neary

http://slidepdf.com/reader/full/articulo-neary 26/26

Related Documents