FOREIGN DIRECT INVESTMENT J. Peter Neary University of Oxford and CEPR 5 February 2009

FOREIGN DIRECT INVESTMENT J. Peter Neary University of Oxford and CEPR 5 February 2009.

Dec 18, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

FOREIGN DIRECT INVESTMENT

J. Peter NearyUniversity of Oxford and CEPR

5 February 2009

2

“OLI” or “Eclectic” Paradigm of FDI• Dunning: Ownership; Location; Internalisation

• Focus on firms rather than factor movementsCompare Mundell (AER 1957)

Dominant View of FDI:• Mostly horizontal rather than vertical

• Determined by proximity-concentration trade-off [“L” versus “O”]

Paradoxical Implication:• Falls in trade costs should reduce FDI

• BUT: Many counter-examplese.g., in 1990s, trade costs fell yet FDI boomed

Resolution?

Introduction: FDI

3

Plan

• Horizontal FDI: The Proximity-Concentration Trade-Off

• Vertical FDI• Export-Platform FDI• Cross-Border Mergers and Acquisitions

4

Plan

• Horizontal FDI: The Proximity-Concentration Trade-Off

• Vertical FDI• Export-Platform FDI• Cross-Border Mergers and Acquisitions

5

2. Horizontal FDI: The Proximity-Concentration Trade-Off

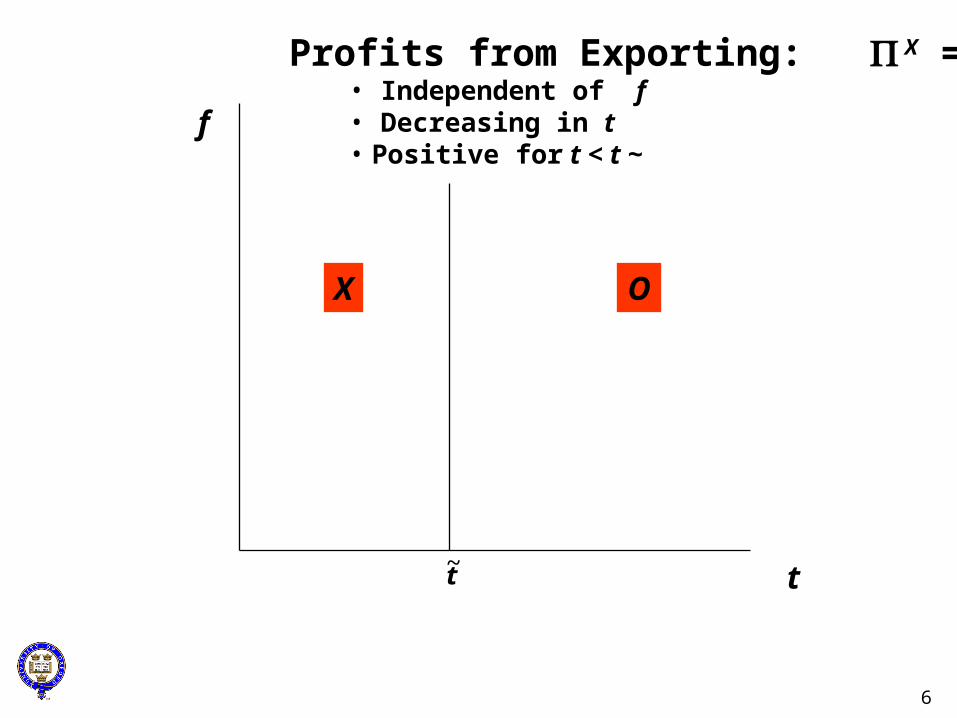

Simplest framework:• Partial equilibrium• Monopoly firm• How best to serve a foreign market?• External trade barrier: t (Tariffs, transport costs etc.)• Plant fixed costs: f• Operating profits from serving the market: (t), ' < 0

6

t

f

~t

Profits from Exporting: X = (t)• Independent of f • Decreasing in t • Positive for t < t ~

X O

7

t

f

(0)

Profits from FDI: F = (0) – f • Independent of t • Decreasing in f • Positive for f < (0)

~t

O

F

8

X O

FDI

t

f

(0)

Fig. 1: The Proximity-Concentration Trade-Off I:The Tariff-Jumping Motive

f (0)–(t)

~t

F – X = (t,f )(t,f )(0) – f – (t)

Tariff-jumping gain

[Increasing in t]

9

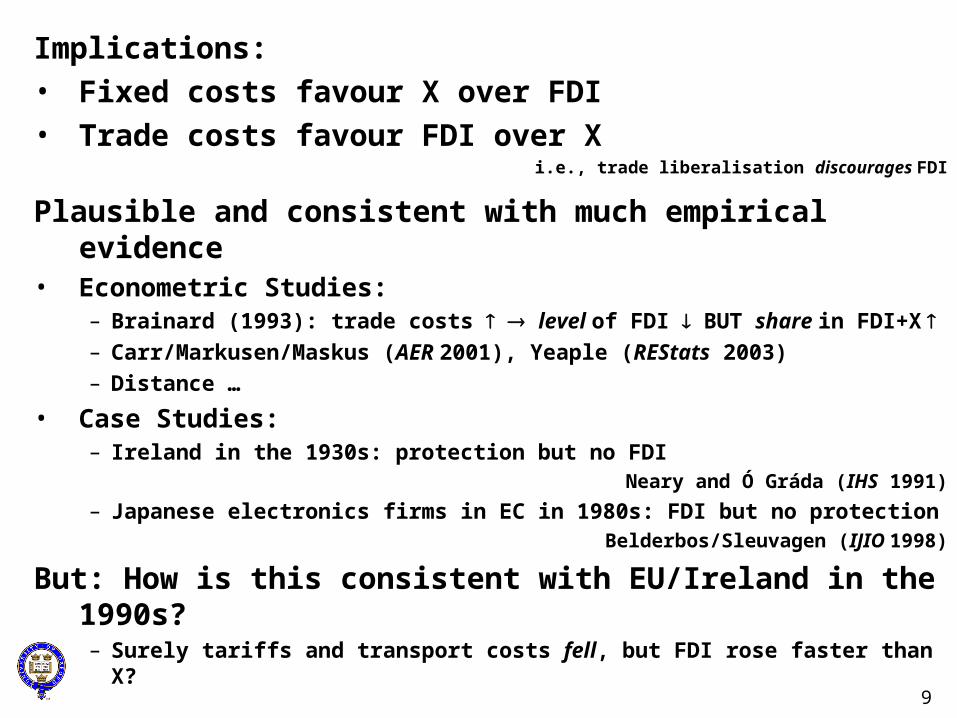

Implications:• Fixed costs favour X over FDI • Trade costs favour FDI over X

i.e., trade liberalisation discourages FDI

Plausible and consistent with much empirical evidence• Econometric Studies:

– Brainard (1993): trade costs level of FDI BUT share in FDI+X – Carr/Markusen/Maskus (AER 2001), Yeaple (REStats 2003)

– Distance …

• Case Studies:– Ireland in the 1930s: protection but no FDI

Neary and Ó Gráda (IHS 1991)

– Japanese electronics firms in EC in 1980s: FDI but no protectionBelderbos/Sleuvagen (IJIO 1998)

But: How is this consistent with EU/Ireland in the 1990s?– Surely tariffs and transport costs fell, but FDI rose faster than X?

10

Plan

• Horizontal FDI: The Proximity-Concentration Trade-Off

• Vertical FDI• Export-Platform FDI• Cross-Border Mergers and Acquisitions

11

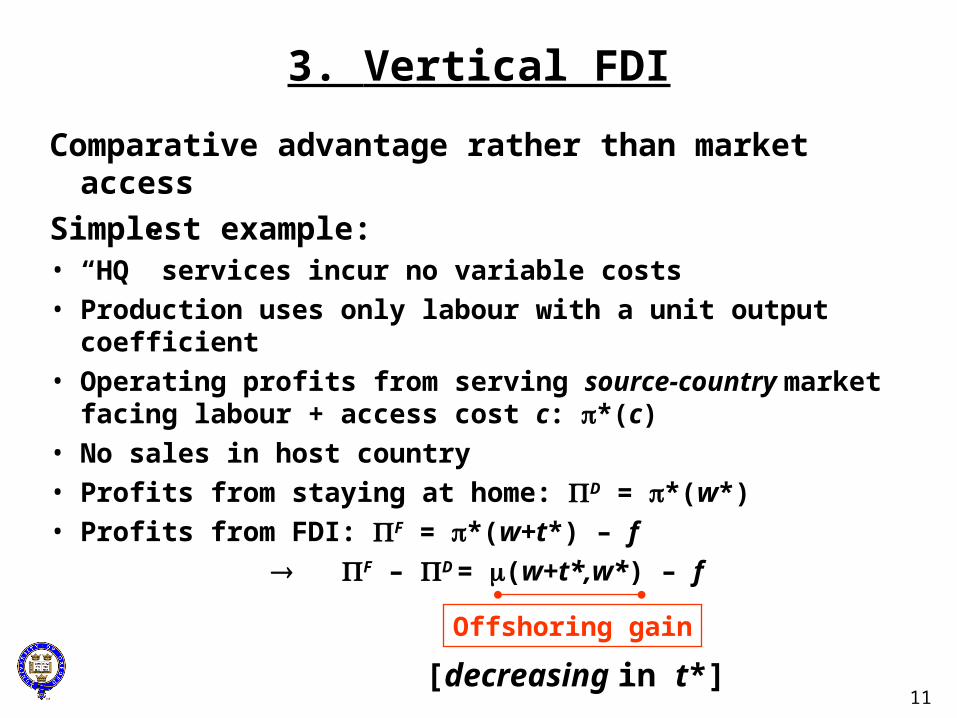

3. Vertical FDI

Comparative advantage rather than market access

Simplest example: • “HQ” services incur no variable costs

• Production uses only labour with a unit output coefficient

• Operating profits from serving source-country market facing labour + access cost c: *(c)

• No sales in host country

• Profits from staying at home: D = *(w*)

• Profits from FDI: F = *(w+t*) – f

F – D = (w+t*,w*) – f

Offshoring gain

[decreasing in t*]

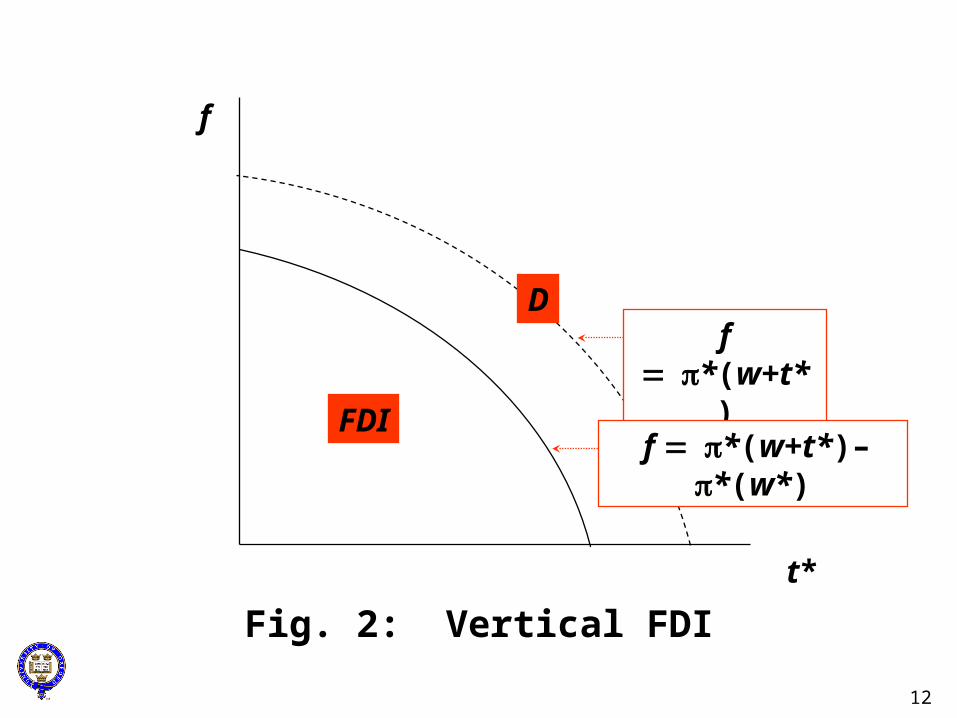

12

FDI

t*

f

Fig. 2: Vertical FDI

f *(w+t*)D

f *(w+t*)–*(w*)

13

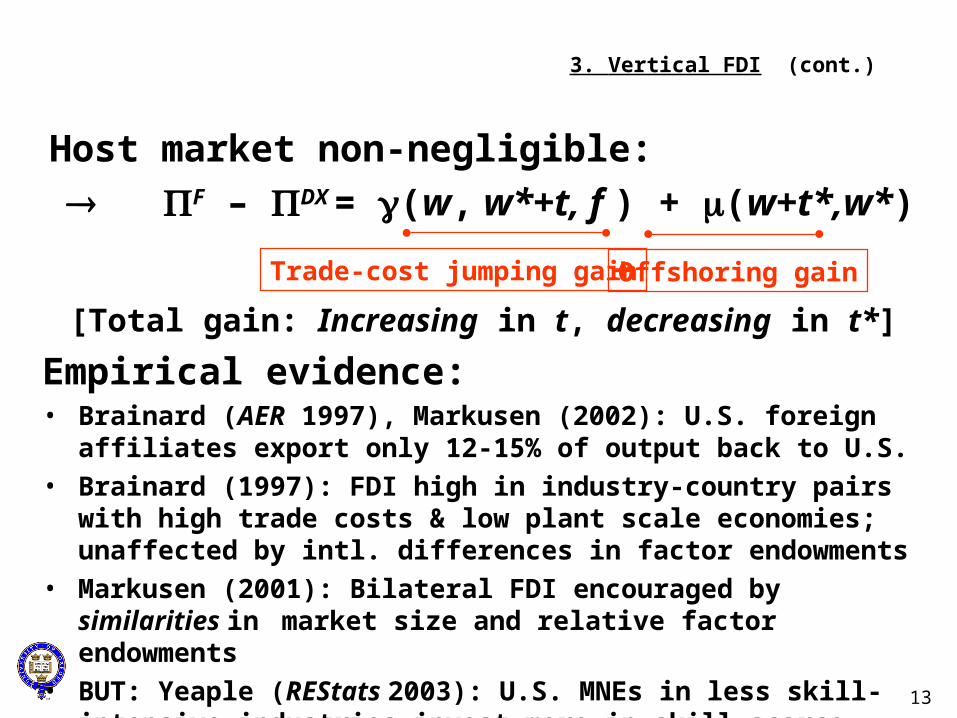

3. Vertical FDI (cont.)

Host market non-negligible:

F – DX = (w, w*+t, f ) + (w+t*,w*)

[Total gain: Increasing in t, decreasing in t*]

Empirical evidence: • Brainard (AER 1997), Markusen (2002): U.S. foreign affiliates export only

12-15% of output back to U.S.

• Brainard (1997): FDI high in industry-country pairs with high trade costs & low plant scale economies; unaffected by intl. differences in factor endowments

• Markusen (2001): Bilateral FDI encouraged by similarities in market size and relative factor endowments

• BUT: Yeaple (REStats 2003): U.S. MNEs in less skill-intensive industries invest more in skill-scarce countries

Trade-cost jumping gain Offshoring gain+

14

Plan

• Horizontal FDI: The Proximity-Concentration Trade-Off

• Vertical FDI• Export-Platform FDI• Cross-Border Mergers and Acquisitions

15

4. Export-Platform FDI

Suppose that host country is one of 2 identical countries in a potential economic union.

• Previous analysis still holds when intra-union barriers = t

Now: Suppose intra-union barriers are reduced to < t X = 2(t) [before: (t)]

F1 = (0) + () – f [before: (0) – f ]

F1 – X = (0) + () – f – 2(t)

= [(0) – f – (t)] + [() – (t)]

Tariff jumping gain

• FDI now more attractive relative to X

• Export-platform gain decreasing in trade cost

Export platform gain

16

t

(0)

(0)–()

f = (0)+()–2(t)f

~t

(0)+()

FDI (1)

X O

FDI (2)

Fig. 3: The Proximity-Concentration Trade-Off II:External Trade-Cost-Jumping + Export-Platform Motives

17

4. Export-Platform FDI (cont.)

Exports & FDI now complements:• For individual firms (though not across same frontier)

• In aggregate data

Empirical evidence: • Fits stylised facts of EU Single Market

e.g., “Celtic Tiger” boom: Barry (1999)

• Head/Mayer (REStats 2004): Japanese FDI in EU encouraged by GDP in host and adjacent regions

• Blonigen et al. (2004): U.S. FDI in EU: – discouraged by U.S. FDI in neighbouring countries

– encouraged by higher GDP in neighbouring countries

• Evidence on plant consolidation mixed:– Pavelin/Barry (ESR 2005) contra; Belderbos (1997) pro

18

Plan

• Horizontal FDI: The Proximity-Concentration Trade-Off

• Vertical FDI• Export-Platform FDI• Cross-Border Mergers and Acquisitions

19

5. Cross-Border Mergers and Acquisitions

So far: Greenfield FDI only

BUT: Cross-border M&As are quantitatively much more important

Now: Oligopoly model essential (almost) • No: Barba Navaretti/Venables (2003), Nocke/Yeaple (JIE 2007, RES 2008), Head/Ries (JIE

2007)

• Yes: Long/Vousden (RIE 1995), Falvey (WE 1998), Horn/Persson (JIE 2001), etc.

• Here: Neary (RES 2007)

Model of 2-country integrated market:• Cournot oligopoly

• Home: n firms with cost c; Foreign: n* with cost c*

• Absent mergers: “Cone of diversification” in {c, c*} space

20

Fig. 4: Equilibrium Production Patternsin Free Trade without FDI

c O: No home orforeign production

~c

F: Foreign production only

H: Homeproduction only

c*

HF: Homeand foreignproduction

~*c

(c,c*;n,n*)=0

*(c,c*;n,n*)=0

21

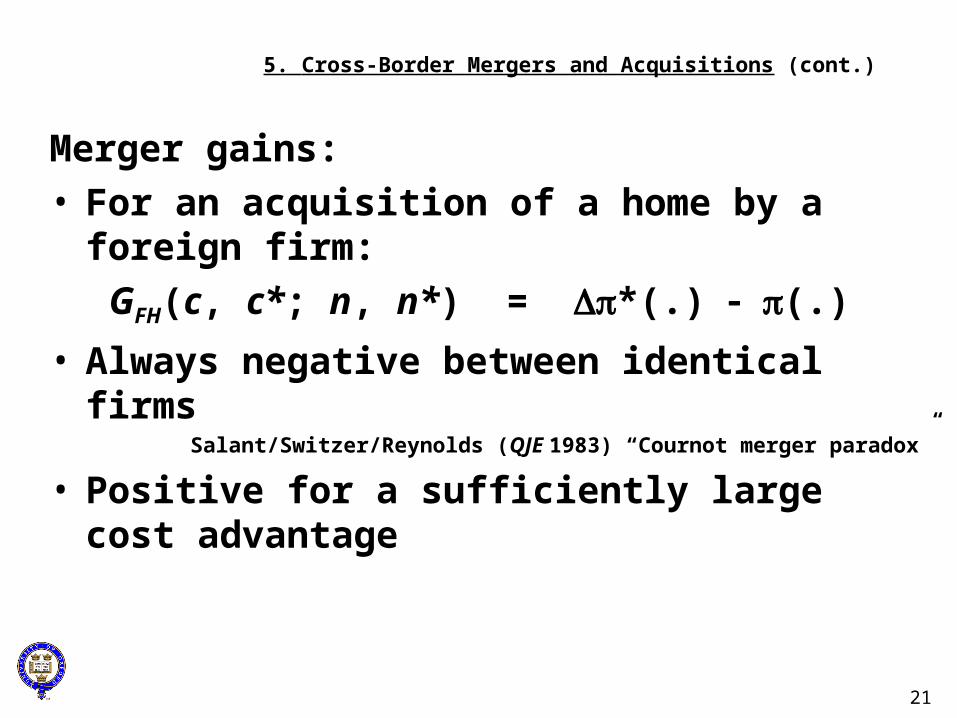

5. Cross-Border Mergers and Acquisitions (cont.)

Merger gains:• For an acquisition of a home by a foreign firm:

GFH(c, c*; n, n*) = *(.) (.)

• Always negative between identical firmsSalant/Switzer/Reynolds (QJE 1983) “Cournot merger paradox”

• Positive for a sufficiently large cost advantage

22

a–cQ R a–c*

GFH < 0

Fig. 5: The Components of Gainfrom a Cross-Border Acquisition by a Foreign Firm

GFH > 0

*

23

Fig. 6: Cross-Border Merger Incentives

Incentives for home firms to

take over foreign

c

c*

H

OF

HF

Incentives for foreign firms totake over home

=0

GFH=0

GHF=0

24

5. Cross-Border Mergers and Acquisitions (cont.)

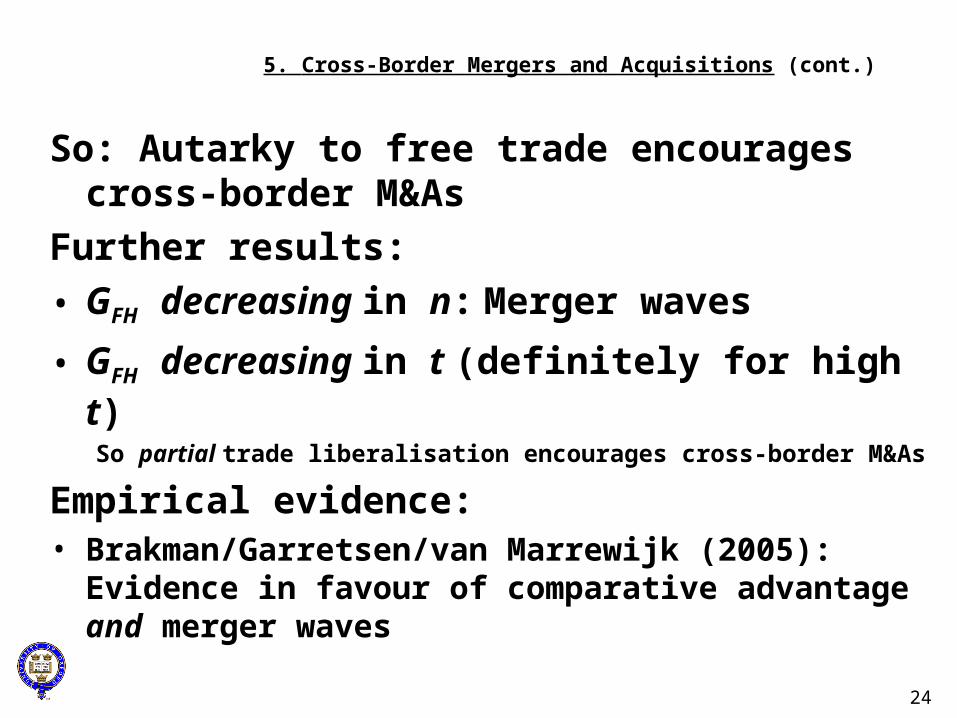

So: Autarky to free trade encourages cross-border M&As

Further results:

• GFH decreasing in n: Merger waves

• GFH decreasing in t (definitely for high t)So partial trade liberalisation encourages cross-border M&As

Empirical evidence: • Brakman/Garretsen/van Marrewijk (2005): Evidence in

favour of comparative advantage and merger waves

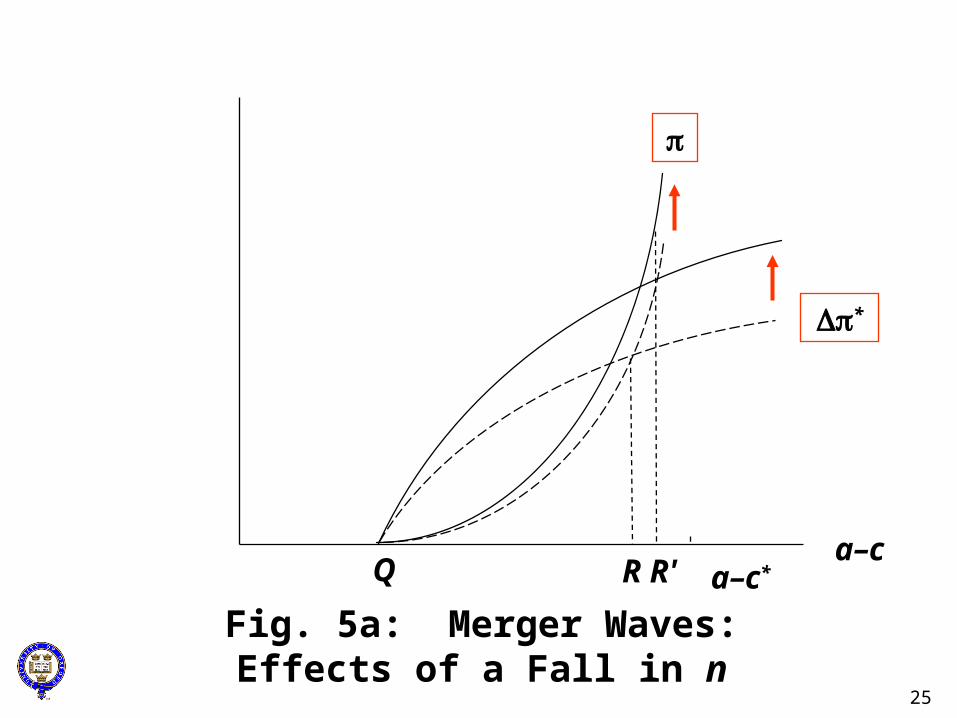

R'

25

a–c

Fig. 5a: Merger Waves:Effects of a Fall in n

*

Q R a–c*

26

Conclusion

Paradox resolved?• Vertical FDI may be quantitatively important after all• Export-Platform FDI encouraged by intra-bloc trade

liberalisation• Cross-border M&As encouraged by trade liberalisation

General conclusions:• Horizontal vs. vertical distinction useful (especially

pedagogically) but don’t expect too much of it• MNE’s engage in “complex integration strategies”

U.N. (1998); Yeaple (JIE 2003)

• Lots more work to be done!

Related Documents