Finance McGraw-Hill Primis ISBN: 0-390-32000-5 Text: Corporate Finance, Sixth Edition Ross-Westerfield-Jaffe Corporate Fiance David Whitehurst UMIST Volume 2 McGraw-Hill/Irwin =>?

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Finance

McGraw−Hill Primis

ISBN: 0−390−32000−5

Text: Corporate Finance, Sixth EditionRoss−Westerfield−Jaffe

Corporate Fiance

David Whitehurst

UMIST

Volume 2

McGraw-Hill/Irwin���

Finance

http://www.mhhe.com/primis/online/Copyright ©2003 by The McGraw−Hill Companies, Inc. All rights reserved. Printed in the United States of America. Except as permitted under the United States Copyright Act of 1976, no part of this publication may be reproduced or distributed in any form or by any means, or stored in a database or retrieval system, without prior written permission of the publisher. This McGraw−Hill Primis text may include materials submitted to McGraw−Hill for publication by the instructor of this course. The instructor is solely responsible for the editorial content of such materials.

111 FINA ISBN: 0−390−32000−5

This book was printed on recycled paper.

Finance

Volume 2

Ross−Westerfield−Jaffe • Corporate Finance, Sixth Edition

Back Matter 903

Appendix A: Mathematical Tables 903Appendix B: Solutions to Selected End−of−Chapter Problems 919Glossary 923Name Index 939Subject Index 942End Papers 959

iii

Ross−Westerfield−Jaffe: Corporate Finance, Sixth Edition

Back Matter Appendix A: Mathematical Tables

903© The McGraw−Hill Companies, 2002

Mathematical Tables

AP

PE

ND

IXA

Ross−Westerfield−Jaffe: Corporate Finance, Sixth Edition

Back Matter Appendix A: Mathematical Tables

904 © The McGraw−Hill Companies, 2002

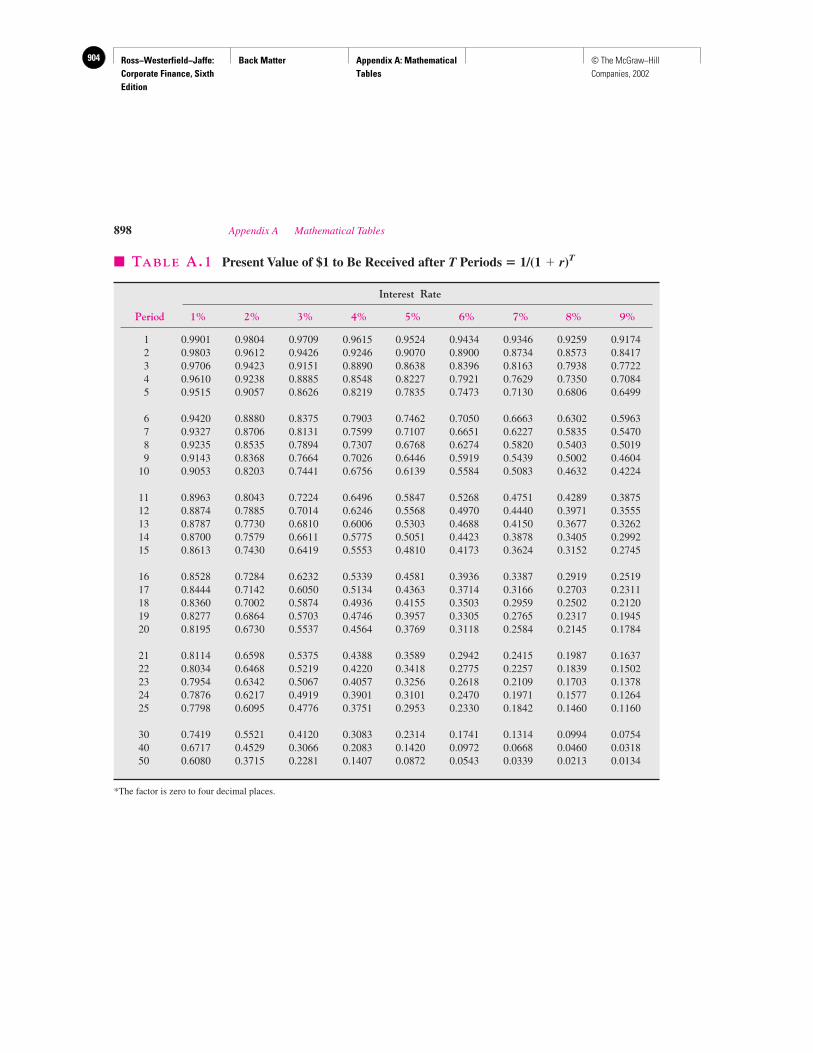

898 Appendix A Mathematical Tables

� TABLE A.1 Present Value of $1 to Be Received after T Periods � 1/(1 � r)T

Interest Rate

Period 1% 2% 3% 4% 5% 6% 7% 8% 9%

1 0.9901 0.9804 0.9709 0.9615 0.9524 0.9434 0.9346 0.9259 0.91742 0.9803 0.9612 0.9426 0.9246 0.9070 0.8900 0.8734 0.8573 0.84173 0.9706 0.9423 0.9151 0.8890 0.8638 0.8396 0.8163 0.7938 0.77224 0.9610 0.9238 0.8885 0.8548 0.8227 0.7921 0.7629 0.7350 0.70845 0.9515 0.9057 0.8626 0.8219 0.7835 0.7473 0.7130 0.6806 0.6499

6 0.9420 0.8880 0.8375 0.7903 0.7462 0.7050 0.6663 0.6302 0.59637 0.9327 0.8706 0.8131 0.7599 0.7107 0.6651 0.6227 0.5835 0.54708 0.9235 0.8535 0.7894 0.7307 0.6768 0.6274 0.5820 0.5403 0.50199 0.9143 0.8368 0.7664 0.7026 0.6446 0.5919 0.5439 0.5002 0.4604

10 0.9053 0.8203 0.7441 0.6756 0.6139 0.5584 0.5083 0.4632 0.4224

11 0.8963 0.8043 0.7224 0.6496 0.5847 0.5268 0.4751 0.4289 0.387512 0.8874 0.7885 0.7014 0.6246 0.5568 0.4970 0.4440 0.3971 0.355513 0.8787 0.7730 0.6810 0.6006 0.5303 0.4688 0.4150 0.3677 0.326214 0.8700 0.7579 0.6611 0.5775 0.5051 0.4423 0.3878 0.3405 0.299215 0.8613 0.7430 0.6419 0.5553 0.4810 0.4173 0.3624 0.3152 0.2745

16 0.8528 0.7284 0.6232 0.5339 0.4581 0.3936 0.3387 0.2919 0.251917 0.8444 0.7142 0.6050 0.5134 0.4363 0.3714 0.3166 0.2703 0.231118 0.8360 0.7002 0.5874 0.4936 0.4155 0.3503 0.2959 0.2502 0.212019 0.8277 0.6864 0.5703 0.4746 0.3957 0.3305 0.2765 0.2317 0.194520 0.8195 0.6730 0.5537 0.4564 0.3769 0.3118 0.2584 0.2145 0.1784

21 0.8114 0.6598 0.5375 0.4388 0.3589 0.2942 0.2415 0.1987 0.163722 0.8034 0.6468 0.5219 0.4220 0.3418 0.2775 0.2257 0.1839 0.150223 0.7954 0.6342 0.5067 0.4057 0.3256 0.2618 0.2109 0.1703 0.137824 0.7876 0.6217 0.4919 0.3901 0.3101 0.2470 0.1971 0.1577 0.126425 0.7798 0.6095 0.4776 0.3751 0.2953 0.2330 0.1842 0.1460 0.1160

30 0.7419 0.5521 0.4120 0.3083 0.2314 0.1741 0.1314 0.0994 0.075440 0.6717 0.4529 0.3066 0.2083 0.1420 0.0972 0.0668 0.0460 0.031850 0.6080 0.3715 0.2281 0.1407 0.0872 0.0543 0.0339 0.0213 0.0134

*The factor is zero to four decimal places.

Ross−Westerfield−Jaffe: Corporate Finance, Sixth Edition

Back Matter Appendix A: Mathematical Tables

905© The McGraw−Hill Companies, 2002

Appendix A Mathematical Tables 899

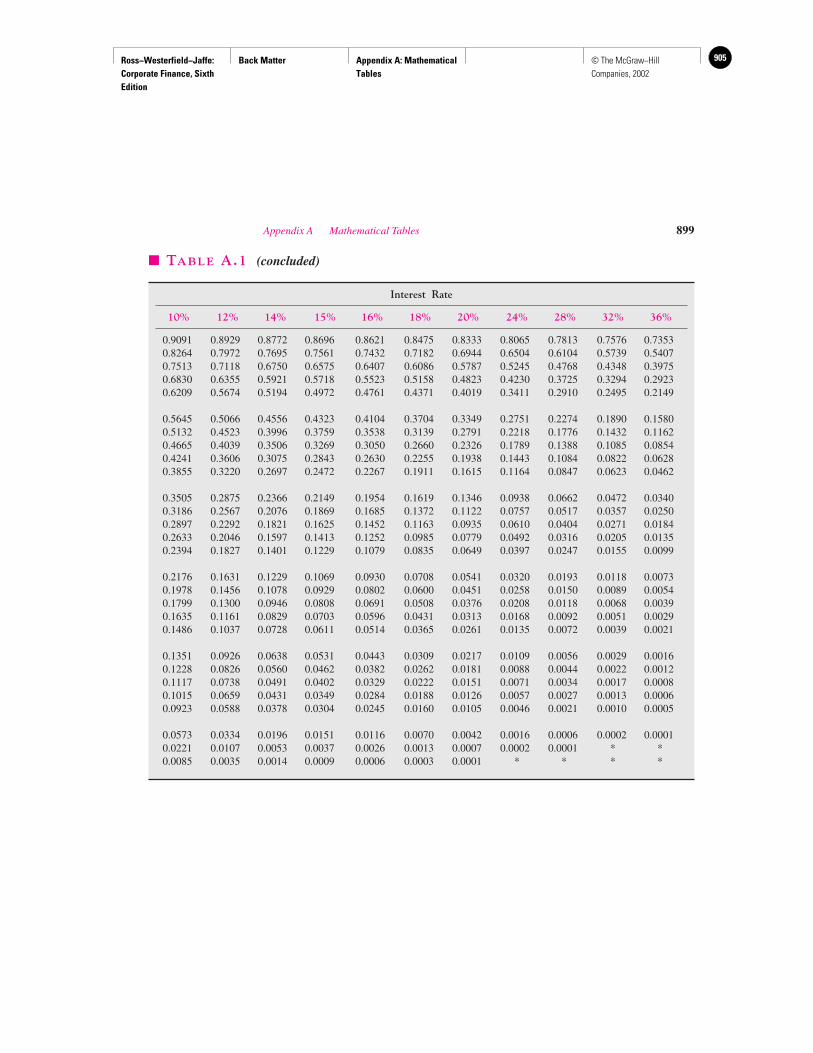

� TABLE A.1 (concluded)

Interest Rate

10% 12% 14% 15% 16% 18% 20% 24% 28% 32% 36%

0.9091 0.8929 0.8772 0.8696 0.8621 0.8475 0.8333 0.8065 0.7813 0.7576 0.73530.8264 0.7972 0.7695 0.7561 0.7432 0.7182 0.6944 0.6504 0.6104 0.5739 0.54070.7513 0.7118 0.6750 0.6575 0.6407 0.6086 0.5787 0.5245 0.4768 0.4348 0.39750.6830 0.6355 0.5921 0.5718 0.5523 0.5158 0.4823 0.4230 0.3725 0.3294 0.29230.6209 0.5674 0.5194 0.4972 0.4761 0.4371 0.4019 0.3411 0.2910 0.2495 0.2149

0.5645 0.5066 0.4556 0.4323 0.4104 0.3704 0.3349 0.2751 0.2274 0.1890 0.15800.5132 0.4523 0.3996 0.3759 0.3538 0.3139 0.2791 0.2218 0.1776 0.1432 0.11620.4665 0.4039 0.3506 0.3269 0.3050 0.2660 0.2326 0.1789 0.1388 0.1085 0.08540.4241 0.3606 0.3075 0.2843 0.2630 0.2255 0.1938 0.1443 0.1084 0.0822 0.06280.3855 0.3220 0.2697 0.2472 0.2267 0.1911 0.1615 0.1164 0.0847 0.0623 0.0462

0.3505 0.2875 0.2366 0.2149 0.1954 0.1619 0.1346 0.0938 0.0662 0.0472 0.03400.3186 0.2567 0.2076 0.1869 0.1685 0.1372 0.1122 0.0757 0.0517 0.0357 0.02500.2897 0.2292 0.1821 0.1625 0.1452 0.1163 0.0935 0.0610 0.0404 0.0271 0.01840.2633 0.2046 0.1597 0.1413 0.1252 0.0985 0.0779 0.0492 0.0316 0.0205 0.01350.2394 0.1827 0.1401 0.1229 0.1079 0.0835 0.0649 0.0397 0.0247 0.0155 0.0099

0.2176 0.1631 0.1229 0.1069 0.0930 0.0708 0.0541 0.0320 0.0193 0.0118 0.00730.1978 0.1456 0.1078 0.0929 0.0802 0.0600 0.0451 0.0258 0.0150 0.0089 0.00540.1799 0.1300 0.0946 0.0808 0.0691 0.0508 0.0376 0.0208 0.0118 0.0068 0.00390.1635 0.1161 0.0829 0.0703 0.0596 0.0431 0.0313 0.0168 0.0092 0.0051 0.00290.1486 0.1037 0.0728 0.0611 0.0514 0.0365 0.0261 0.0135 0.0072 0.0039 0.0021

0.1351 0.0926 0.0638 0.0531 0.0443 0.0309 0.0217 0.0109 0.0056 0.0029 0.00160.1228 0.0826 0.0560 0.0462 0.0382 0.0262 0.0181 0.0088 0.0044 0.0022 0.00120.1117 0.0738 0.0491 0.0402 0.0329 0.0222 0.0151 0.0071 0.0034 0.0017 0.00080.1015 0.0659 0.0431 0.0349 0.0284 0.0188 0.0126 0.0057 0.0027 0.0013 0.00060.0923 0.0588 0.0378 0.0304 0.0245 0.0160 0.0105 0.0046 0.0021 0.0010 0.0005

0.0573 0.0334 0.0196 0.0151 0.0116 0.0070 0.0042 0.0016 0.0006 0.0002 0.00010.0221 0.0107 0.0053 0.0037 0.0026 0.0013 0.0007 0.0002 0.0001 * *0.0085 0.0035 0.0014 0.0009 0.0006 0.0003 0.0001 * * * *

Ross−Westerfield−Jaffe: Corporate Finance, Sixth Edition

Back Matter Appendix A: Mathematical Tables

906 © The McGraw−Hill Companies, 2002

900 Appendix A Mathematical Tables

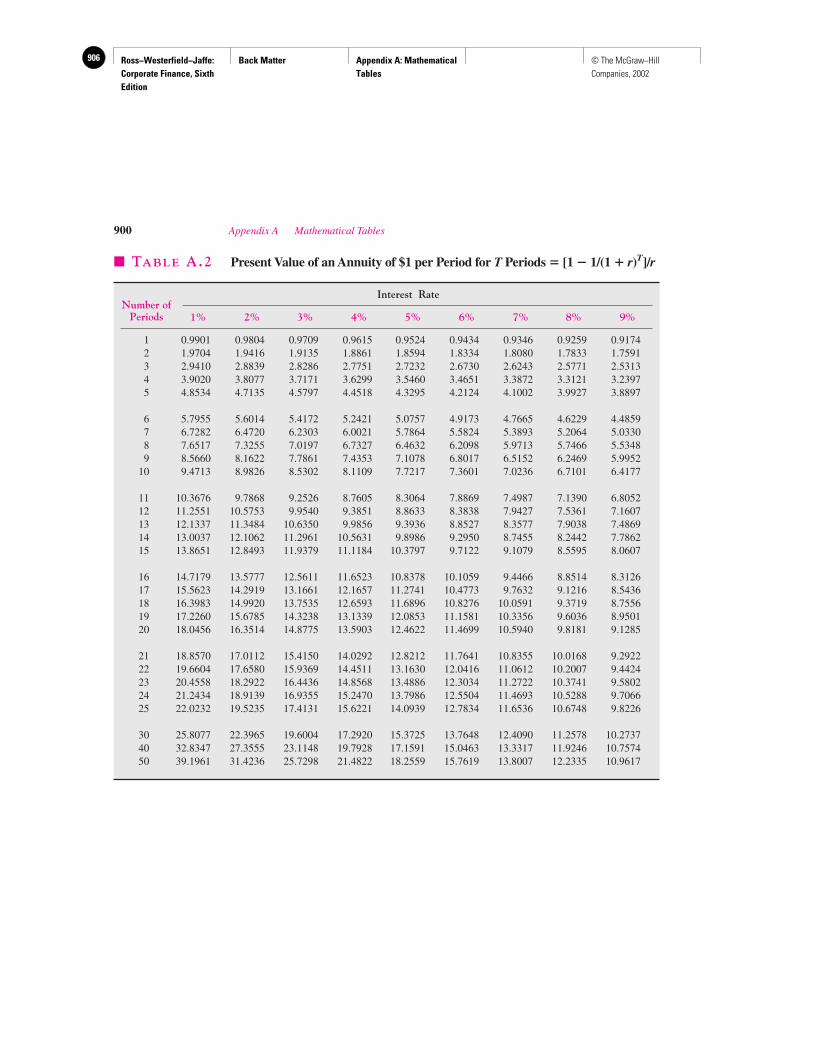

� TABLE A.2 Present Value of an Annuity of $1 per Period for T Periods � [1 � 1/(1 � r)T]/r

Interest Rate

1% 2% 3% 4% 5% 6% 7% 8% 9%

1 0.9901 0.9804 0.9709 0.9615 0.9524 0.9434 0.9346 0.9259 0.91742 1.9704 1.9416 1.9135 1.8861 1.8594 1.8334 1.8080 1.7833 1.75913 2.9410 2.8839 2.8286 2.7751 2.7232 2.6730 2.6243 2.5771 2.53134 3.9020 3.8077 3.7171 3.6299 3.5460 3.4651 3.3872 3.3121 3.23975 4.8534 4.7135 4.5797 4.4518 4.3295 4.2124 4.1002 3.9927 3.8897

6 5.7955 5.6014 5.4172 5.2421 5.0757 4.9173 4.7665 4.6229 4.48597 6.7282 6.4720 6.2303 6.0021 5.7864 5.5824 5.3893 5.2064 5.03308 7.6517 7.3255 7.0197 6.7327 6.4632 6.2098 5.9713 5.7466 5.53489 8.5660 8.1622 7.7861 7.4353 7.1078 6.8017 6.5152 6.2469 5.9952

10 9.4713 8.9826 8.5302 8.1109 7.7217 7.3601 7.0236 6.7101 6.4177

11 10.3676 9.7868 9.2526 8.7605 8.3064 7.8869 7.4987 7.1390 6.805212 11.2551 10.5753 9.9540 9.3851 8.8633 8.3838 7.9427 7.5361 7.160713 12.1337 11.3484 10.6350 9.9856 9.3936 8.8527 8.3577 7.9038 7.486914 13.0037 12.1062 11.2961 10.5631 9.8986 9.2950 8.7455 8.2442 7.786215 13.8651 12.8493 11.9379 11.1184 10.3797 9.7122 9.1079 8.5595 8.0607

16 14.7179 13.5777 12.5611 11.6523 10.8378 10.1059 9.4466 8.8514 8.312617 15.5623 14.2919 13.1661 12.1657 11.2741 10.4773 9.7632 9.1216 8.543618 16.3983 14.9920 13.7535 12.6593 11.6896 10.8276 10.0591 9.3719 8.755619 17.2260 15.6785 14.3238 13.1339 12.0853 11.1581 10.3356 9.6036 8.950120 18.0456 16.3514 14.8775 13.5903 12.4622 11.4699 10.5940 9.8181 9.1285

21 18.8570 17.0112 15.4150 14.0292 12.8212 11.7641 10.8355 10.0168 9.292222 19.6604 17.6580 15.9369 14.4511 13.1630 12.0416 11.0612 10.2007 9.442423 20.4558 18.2922 16.4436 14.8568 13.4886 12.3034 11.2722 10.3741 9.580224 21.2434 18.9139 16.9355 15.2470 13.7986 12.5504 11.4693 10.5288 9.706625 22.0232 19.5235 17.4131 15.6221 14.0939 12.7834 11.6536 10.6748 9.8226

30 25.8077 22.3965 19.6004 17.2920 15.3725 13.7648 12.4090 11.2578 10.273740 32.8347 27.3555 23.1148 19.7928 17.1591 15.0463 13.3317 11.9246 10.757450 39.1961 31.4236 25.7298 21.4822 18.2559 15.7619 13.8007 12.2335 10.9617

Number ofPeriods

Ross−Westerfield−Jaffe: Corporate Finance, Sixth Edition

Back Matter Appendix A: Mathematical Tables

907© The McGraw−Hill Companies, 2002

Appendix A Mathematical Tables 901

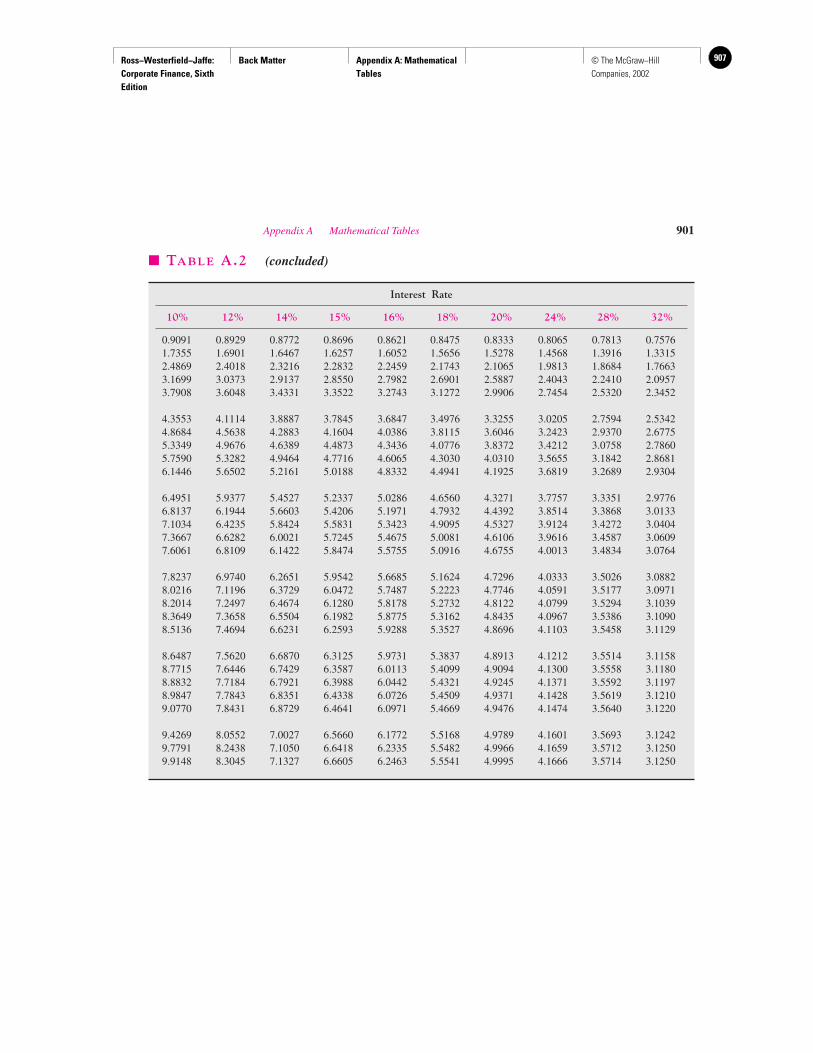

� TABLE A.2 (concluded)

Interest Rate

10% 12% 14% 15% 16% 18% 20% 24% 28% 32%

0.9091 0.8929 0.8772 0.8696 0.8621 0.8475 0.8333 0.8065 0.7813 0.75761.7355 1.6901 1.6467 1.6257 1.6052 1.5656 1.5278 1.4568 1.3916 1.33152.4869 2.4018 2.3216 2.2832 2.2459 2.1743 2.1065 1.9813 1.8684 1.76633.1699 3.0373 2.9137 2.8550 2.7982 2.6901 2.5887 2.4043 2.2410 2.09573.7908 3.6048 3.4331 3.3522 3.2743 3.1272 2.9906 2.7454 2.5320 2.3452

4.3553 4.1114 3.8887 3.7845 3.6847 3.4976 3.3255 3.0205 2.7594 2.53424.8684 4.5638 4.2883 4.1604 4.0386 3.8115 3.6046 3.2423 2.9370 2.67755.3349 4.9676 4.6389 4.4873 4.3436 4.0776 3.8372 3.4212 3.0758 2.78605.7590 5.3282 4.9464 4.7716 4.6065 4.3030 4.0310 3.5655 3.1842 2.86816.1446 5.6502 5.2161 5.0188 4.8332 4.4941 4.1925 3.6819 3.2689 2.9304

6.4951 5.9377 5.4527 5.2337 5.0286 4.6560 4.3271 3.7757 3.3351 2.97766.8137 6.1944 5.6603 5.4206 5.1971 4.7932 4.4392 3.8514 3.3868 3.01337.1034 6.4235 5.8424 5.5831 5.3423 4.9095 4.5327 3.9124 3.4272 3.04047.3667 6.6282 6.0021 5.7245 5.4675 5.0081 4.6106 3.9616 3.4587 3.06097.6061 6.8109 6.1422 5.8474 5.5755 5.0916 4.6755 4.0013 3.4834 3.0764

7.8237 6.9740 6.2651 5.9542 5.6685 5.1624 4.7296 4.0333 3.5026 3.08828.0216 7.1196 6.3729 6.0472 5.7487 5.2223 4.7746 4.0591 3.5177 3.09718.2014 7.2497 6.4674 6.1280 5.8178 5.2732 4.8122 4.0799 3.5294 3.10398.3649 7.3658 6.5504 6.1982 5.8775 5.3162 4.8435 4.0967 3.5386 3.10908.5136 7.4694 6.6231 6.2593 5.9288 5.3527 4.8696 4.1103 3.5458 3.1129

8.6487 7.5620 6.6870 6.3125 5.9731 5.3837 4.8913 4.1212 3.5514 3.11588.7715 7.6446 6.7429 6.3587 6.0113 5.4099 4.9094 4.1300 3.5558 3.11808.8832 7.7184 6.7921 6.3988 6.0442 5.4321 4.9245 4.1371 3.5592 3.11978.9847 7.7843 6.8351 6.4338 6.0726 5.4509 4.9371 4.1428 3.5619 3.12109.0770 7.8431 6.8729 6.4641 6.0971 5.4669 4.9476 4.1474 3.5640 3.1220

9.4269 8.0552 7.0027 6.5660 6.1772 5.5168 4.9789 4.1601 3.5693 3.12429.7791 8.2438 7.1050 6.6418 6.2335 5.5482 4.9966 4.1659 3.5712 3.12509.9148 8.3045 7.1327 6.6605 6.2463 5.5541 4.9995 4.1666 3.5714 3.1250

Ross−Westerfield−Jaffe: Corporate Finance, Sixth Edition

Back Matter Appendix A: Mathematical Tables

908 © The McGraw−Hill Companies, 2002

902 Appendix A Mathematical Tables

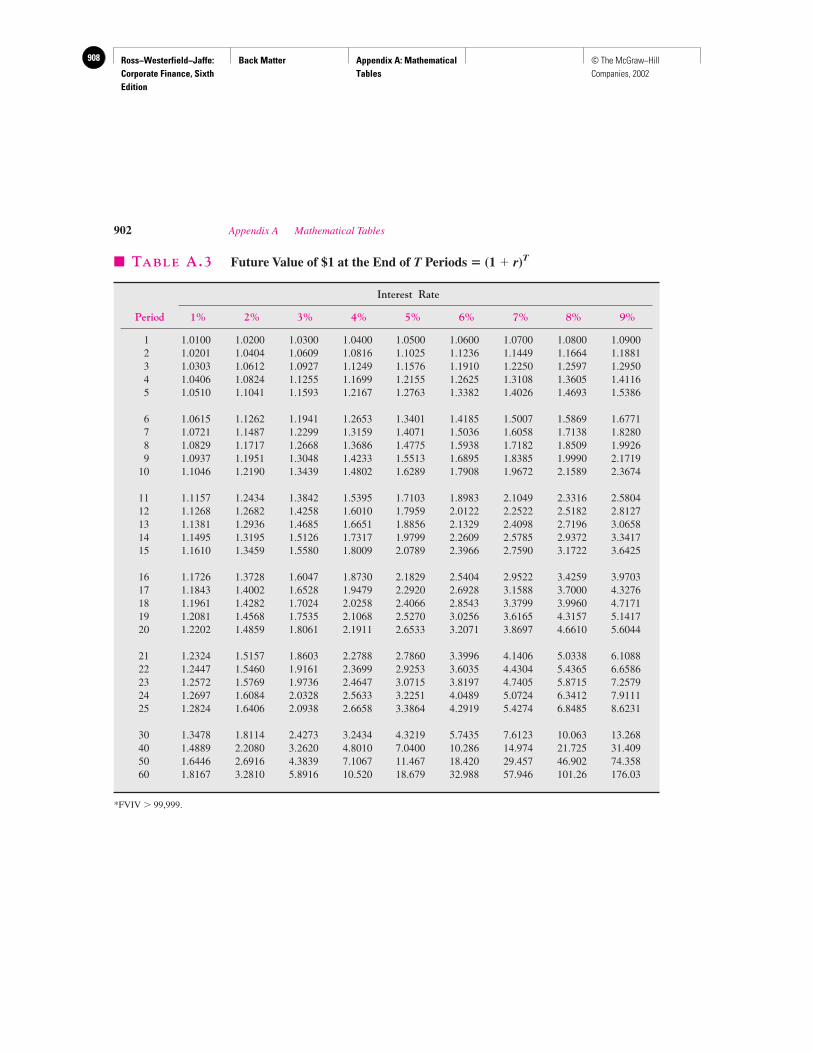

� TABLE A.3 Future Value of $1 at the End of T Periods � (1 � r)T

Interest Rate

Period 1% 2% 3% 4% 5% 6% 7% 8% 9%

1 1.0100 1.0200 1.0300 1.0400 1.0500 1.0600 1.0700 1.0800 1.09002 1.0201 1.0404 1.0609 1.0816 1.1025 1.1236 1.1449 1.1664 1.18813 1.0303 1.0612 1.0927 1.1249 1.1576 1.1910 1.2250 1.2597 1.29504 1.0406 1.0824 1.1255 1.1699 1.2155 1.2625 1.3108 1.3605 1.41165 1.0510 1.1041 1.1593 1.2167 1.2763 1.3382 1.4026 1.4693 1.5386

6 1.0615 1.1262 1.1941 1.2653 1.3401 1.4185 1.5007 1.5869 1.67717 1.0721 1.1487 1.2299 1.3159 1.4071 1.5036 1.6058 1.7138 1.82808 1.0829 1.1717 1.2668 1.3686 1.4775 1.5938 1.7182 1.8509 1.99269 1.0937 1.1951 1.3048 1.4233 1.5513 1.6895 1.8385 1.9990 2.1719

10 1.1046 1.2190 1.3439 1.4802 1.6289 1.7908 1.9672 2.1589 2.3674

11 1.1157 1.2434 1.3842 1.5395 1.7103 1.8983 2.1049 2.3316 2.580412 1.1268 1.2682 1.4258 1.6010 1.7959 2.0122 2.2522 2.5182 2.812713 1.1381 1.2936 1.4685 1.6651 1.8856 2.1329 2.4098 2.7196 3.065814 1.1495 1.3195 1.5126 1.7317 1.9799 2.2609 2.5785 2.9372 3.341715 1.1610 1.3459 1.5580 1.8009 2.0789 2.3966 2.7590 3.1722 3.6425

16 1.1726 1.3728 1.6047 1.8730 2.1829 2.5404 2.9522 3.4259 3.970317 1.1843 1.4002 1.6528 1.9479 2.2920 2.6928 3.1588 3.7000 4.327618 1.1961 1.4282 1.7024 2.0258 2.4066 2.8543 3.3799 3.9960 4.717119 1.2081 1.4568 1.7535 2.1068 2.5270 3.0256 3.6165 4.3157 5.141720 1.2202 1.4859 1.8061 2.1911 2.6533 3.2071 3.8697 4.6610 5.6044

21 1.2324 1.5157 1.8603 2.2788 2.7860 3.3996 4.1406 5.0338 6.108822 1.2447 1.5460 1.9161 2.3699 2.9253 3.6035 4.4304 5.4365 6.658623 1.2572 1.5769 1.9736 2.4647 3.0715 3.8197 4.7405 5.8715 7.257924 1.2697 1.6084 2.0328 2.5633 3.2251 4.0489 5.0724 6.3412 7.911125 1.2824 1.6406 2.0938 2.6658 3.3864 4.2919 5.4274 6.8485 8.6231

30 1.3478 1.8114 2.4273 3.2434 4.3219 5.7435 7.6123 10.063 13.26840 1.4889 2.2080 3.2620 4.8010 7.0400 10.286 14.974 21.725 31.40950 1.6446 2.6916 4.3839 7.1067 11.467 18.420 29.457 46.902 74.35860 1.8167 3.2810 5.8916 10.520 18.679 32.988 57.946 101.26 176.03

*FVIV � 99,999.

Ross−Westerfield−Jaffe: Corporate Finance, Sixth Edition

Back Matter Appendix A: Mathematical Tables

909© The McGraw−Hill Companies, 2002

Appendix A Mathematical Tables 903

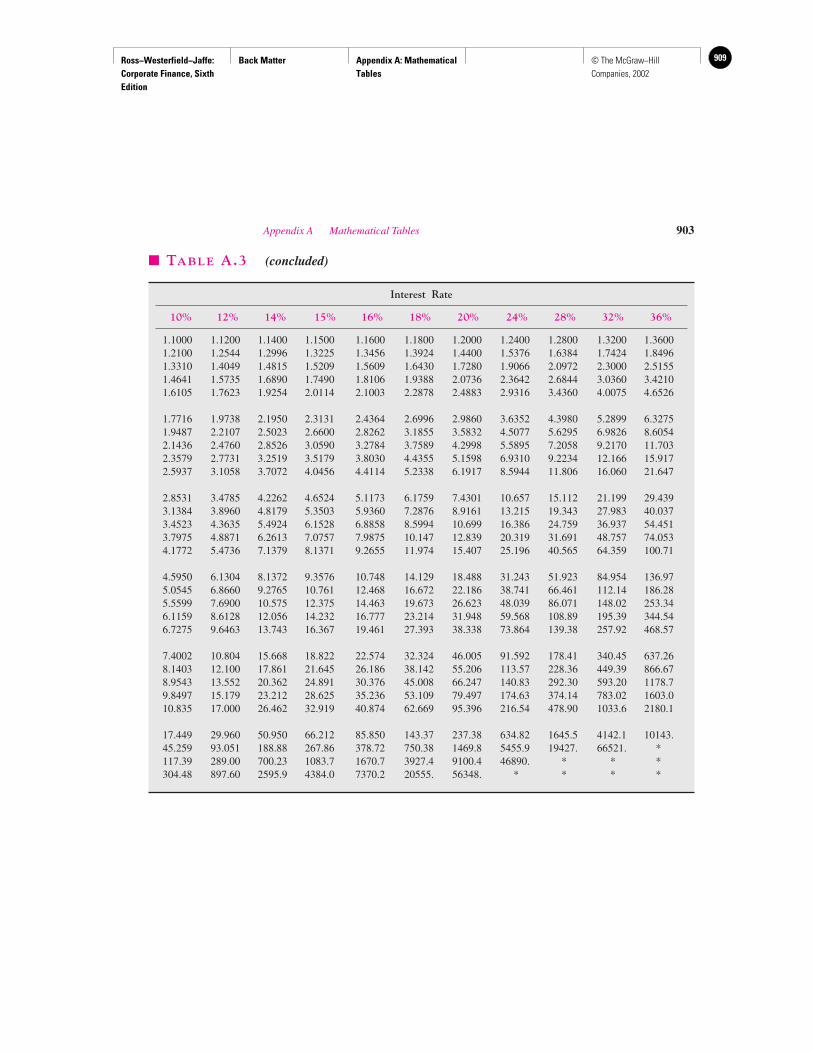

� TABLE A.3 (concluded)

Interest Rate

10% 12% 14% 15% 16% 18% 20% 24% 28% 32% 36%

1.1000 1.1200 1.1400 1.1500 1.1600 1.1800 1.2000 1.2400 1.2800 1.3200 1.36001.2100 1.2544 1.2996 1.3225 1.3456 1.3924 1.4400 1.5376 1.6384 1.7424 1.84961.3310 1.4049 1.4815 1.5209 1.5609 1.6430 1.7280 1.9066 2.0972 2.3000 2.51551.4641 1.5735 1.6890 1.7490 1.8106 1.9388 2.0736 2.3642 2.6844 3.0360 3.42101.6105 1.7623 1.9254 2.0114 2.1003 2.2878 2.4883 2.9316 3.4360 4.0075 4.6526

1.7716 1.9738 2.1950 2.3131 2.4364 2.6996 2.9860 3.6352 4.3980 5.2899 6.32751.9487 2.2107 2.5023 2.6600 2.8262 3.1855 3.5832 4.5077 5.6295 6.9826 8.60542.1436 2.4760 2.8526 3.0590 3.2784 3.7589 4.2998 5.5895 7.2058 9.2170 11.7032.3579 2.7731 3.2519 3.5179 3.8030 4.4355 5.1598 6.9310 9.2234 12.166 15.9172.5937 3.1058 3.7072 4.0456 4.4114 5.2338 6.1917 8.5944 11.806 16.060 21.647

2.8531 3.4785 4.2262 4.6524 5.1173 6.1759 7.4301 10.657 15.112 21.199 29.4393.1384 3.8960 4.8179 5.3503 5.9360 7.2876 8.9161 13.215 19.343 27.983 40.0373.4523 4.3635 5.4924 6.1528 6.8858 8.5994 10.699 16.386 24.759 36.937 54.4513.7975 4.8871 6.2613 7.0757 7.9875 10.147 12.839 20.319 31.691 48.757 74.0534.1772 5.4736 7.1379 8.1371 9.2655 11.974 15.407 25.196 40.565 64.359 100.71

4.5950 6.1304 8.1372 9.3576 10.748 14.129 18.488 31.243 51.923 84.954 136.975.0545 6.8660 9.2765 10.761 12.468 16.672 22.186 38.741 66.461 112.14 186.285.5599 7.6900 10.575 12.375 14.463 19.673 26.623 48.039 86.071 148.02 253.346.1159 8.6128 12.056 14.232 16.777 23.214 31.948 59.568 108.89 195.39 344.546.7275 9.6463 13.743 16.367 19.461 27.393 38.338 73.864 139.38 257.92 468.57

7.4002 10.804 15.668 18.822 22.574 32.324 46.005 91.592 178.41 340.45 637.268.1403 12.100 17.861 21.645 26.186 38.142 55.206 113.57 228.36 449.39 866.678.9543 13.552 20.362 24.891 30.376 45.008 66.247 140.83 292.30 593.20 1178.79.8497 15.179 23.212 28.625 35.236 53.109 79.497 174.63 374.14 783.02 1603.010.835 17.000 26.462 32.919 40.874 62.669 95.396 216.54 478.90 1033.6 2180.1

17.449 29.960 50.950 66.212 85.850 143.37 237.38 634.82 1645.5 4142.1 10143.45.259 93.051 188.88 267.86 378.72 750.38 1469.8 5455.9 19427. 66521. *117.39 289.00 700.23 1083.7 1670.7 3927.4 9100.4 46890. * * *304.48 897.60 2595.9 4384.0 7370.2 20555. 56348. * * * *

Ross−Westerfield−Jaffe: Corporate Finance, Sixth Edition

Back Matter Appendix A: Mathematical Tables

910 © The McGraw−Hill Companies, 2002

904 Appendix A Mathematical Tables

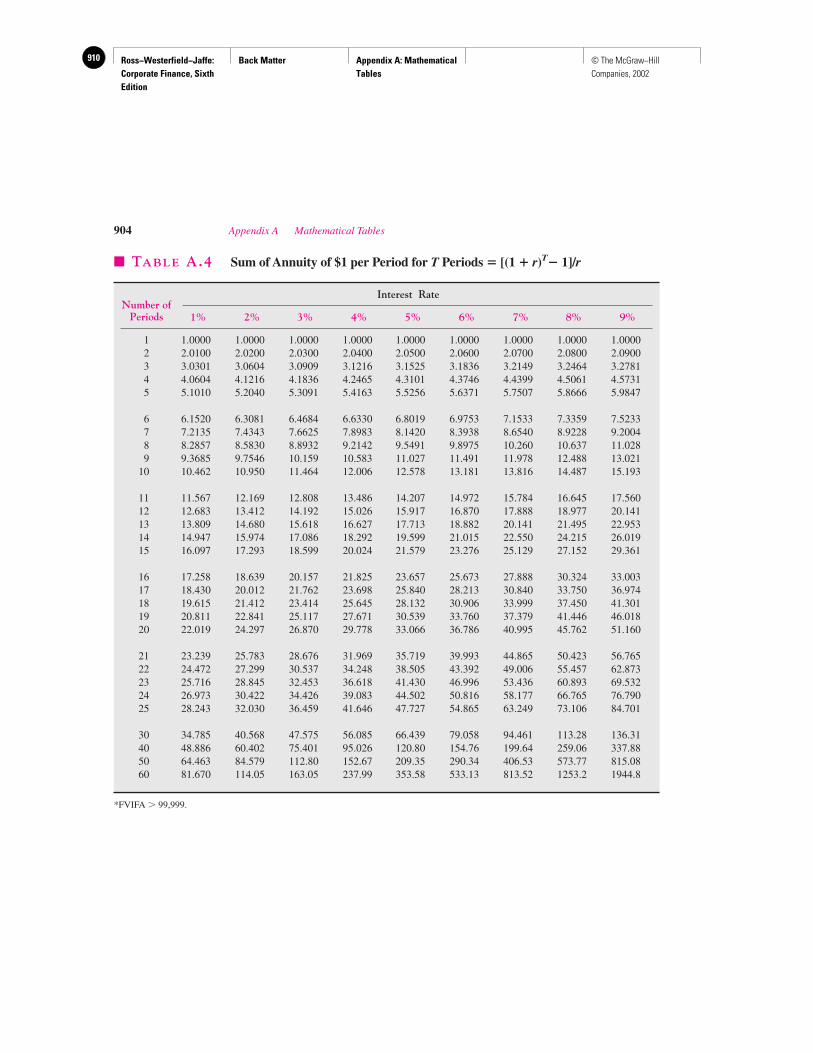

� TABLE A.4 Sum of Annuity of $1 per Period for T Periods � [(1 � r)T� 1]/r

Interest Rate

1% 2% 3% 4% 5% 6% 7% 8% 9%

1 1.0000 1.0000 1.0000 1.0000 1.0000 1.0000 1.0000 1.0000 1.00002 2.0100 2.0200 2.0300 2.0400 2.0500 2.0600 2.0700 2.0800 2.09003 3.0301 3.0604 3.0909 3.1216 3.1525 3.1836 3.2149 3.2464 3.27814 4.0604 4.1216 4.1836 4.2465 4.3101 4.3746 4.4399 4.5061 4.57315 5.1010 5.2040 5.3091 5.4163 5.5256 5.6371 5.7507 5.8666 5.9847

6 6.1520 6.3081 6.4684 6.6330 6.8019 6.9753 7.1533 7.3359 7.52337 7.2135 7.4343 7.6625 7.8983 8.1420 8.3938 8.6540 8.9228 9.20048 8.2857 8.5830 8.8932 9.2142 9.5491 9.8975 10.260 10.637 11.0289 9.3685 9.7546 10.159 10.583 11.027 11.491 11.978 12.488 13.021

10 10.462 10.950 11.464 12.006 12.578 13.181 13.816 14.487 15.193

11 11.567 12.169 12.808 13.486 14.207 14.972 15.784 16.645 17.56012 12.683 13.412 14.192 15.026 15.917 16.870 17.888 18.977 20.14113 13.809 14.680 15.618 16.627 17.713 18.882 20.141 21.495 22.95314 14.947 15.974 17.086 18.292 19.599 21.015 22.550 24.215 26.01915 16.097 17.293 18.599 20.024 21.579 23.276 25.129 27.152 29.361

16 17.258 18.639 20.157 21.825 23.657 25.673 27.888 30.324 33.00317 18.430 20.012 21.762 23.698 25.840 28.213 30.840 33.750 36.97418 19.615 21.412 23.414 25.645 28.132 30.906 33.999 37.450 41.30119 20.811 22.841 25.117 27.671 30.539 33.760 37.379 41.446 46.01820 22.019 24.297 26.870 29.778 33.066 36.786 40.995 45.762 51.160

21 23.239 25.783 28.676 31.969 35.719 39.993 44.865 50.423 56.76522 24.472 27.299 30.537 34.248 38.505 43.392 49.006 55.457 62.87323 25.716 28.845 32.453 36.618 41.430 46.996 53.436 60.893 69.53224 26.973 30.422 34.426 39.083 44.502 50.816 58.177 66.765 76.79025 28.243 32.030 36.459 41.646 47.727 54.865 63.249 73.106 84.701

30 34.785 40.568 47.575 56.085 66.439 79.058 94.461 113.28 136.3140 48.886 60.402 75.401 95.026 120.80 154.76 199.64 259.06 337.8850 64.463 84.579 112.80 152.67 209.35 290.34 406.53 573.77 815.0860 81.670 114.05 163.05 237.99 353.58 533.13 813.52 1253.2 1944.8

*FVIFA � 99,999.

Number ofPeriods

Ross−Westerfield−Jaffe: Corporate Finance, Sixth Edition

Back Matter Appendix A: Mathematical Tables

911© The McGraw−Hill Companies, 2002

Appendix A Mathematical Tables 905

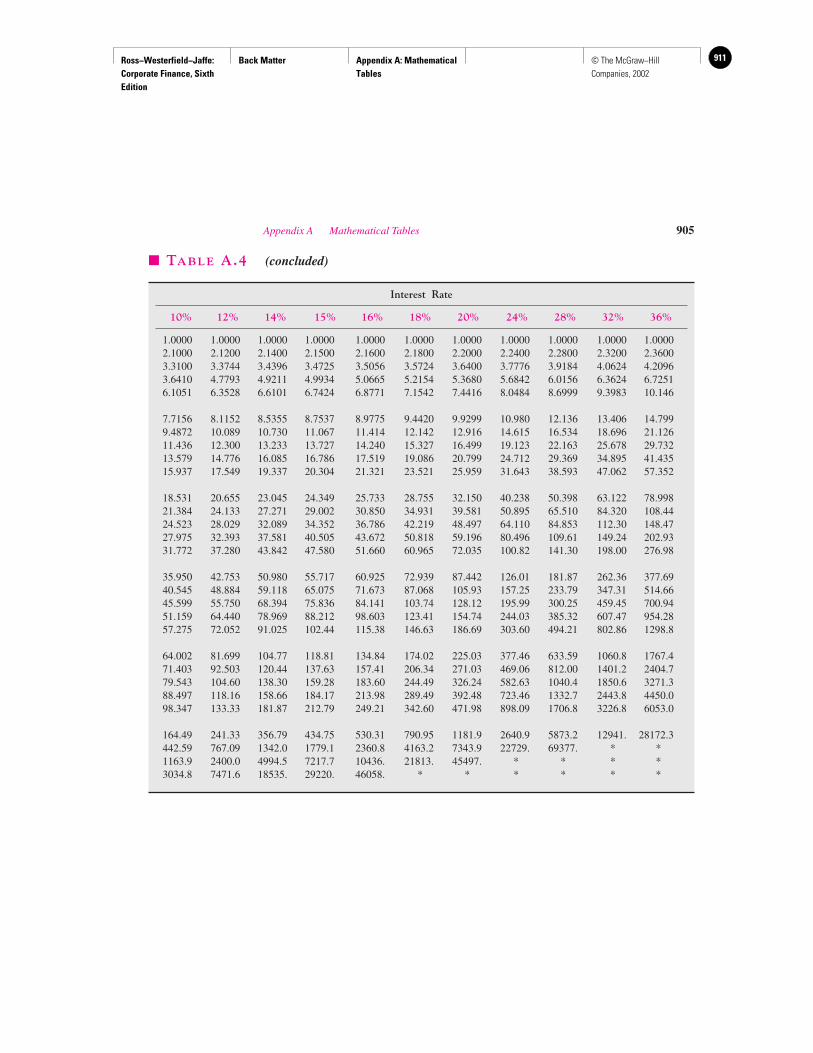

� TABLE A.4 (concluded)

Interest Rate

10% 12% 14% 15% 16% 18% 20% 24% 28% 32% 36%

1.0000 1.0000 1.0000 1.0000 1.0000 1.0000 1.0000 1.0000 1.0000 1.0000 1.00002.1000 2.1200 2.1400 2.1500 2.1600 2.1800 2.2000 2.2400 2.2800 2.3200 2.36003.3100 3.3744 3.4396 3.4725 3.5056 3.5724 3.6400 3.7776 3.9184 4.0624 4.20963.6410 4.7793 4.9211 4.9934 5.0665 5.2154 5.3680 5.6842 6.0156 6.3624 6.72516.1051 6.3528 6.6101 6.7424 6.8771 7.1542 7.4416 8.0484 8.6999 9.3983 10.146

7.7156 8.1152 8.5355 8.7537 8.9775 9.4420 9.9299 10.980 12.136 13.406 14.7999.4872 10.089 10.730 11.067 11.414 12.142 12.916 14.615 16.534 18.696 21.12611.436 12.300 13.233 13.727 14.240 15.327 16.499 19.123 22.163 25.678 29.73213.579 14.776 16.085 16.786 17.519 19.086 20.799 24.712 29.369 34.895 41.43515.937 17.549 19.337 20.304 21.321 23.521 25.959 31.643 38.593 47.062 57.352

18.531 20.655 23.045 24.349 25.733 28.755 32.150 40.238 50.398 63.122 78.99821.384 24.133 27.271 29.002 30.850 34.931 39.581 50.895 65.510 84.320 108.4424.523 28.029 32.089 34.352 36.786 42.219 48.497 64.110 84.853 112.30 148.4727.975 32.393 37.581 40.505 43.672 50.818 59.196 80.496 109.61 149.24 202.9331.772 37.280 43.842 47.580 51.660 60.965 72.035 100.82 141.30 198.00 276.98

35.950 42.753 50.980 55.717 60.925 72.939 87.442 126.01 181.87 262.36 377.6940.545 48.884 59.118 65.075 71.673 87.068 105.93 157.25 233.79 347.31 514.6645.599 55.750 68.394 75.836 84.141 103.74 128.12 195.99 300.25 459.45 700.9451.159 64.440 78.969 88.212 98.603 123.41 154.74 244.03 385.32 607.47 954.2857.275 72.052 91.025 102.44 115.38 146.63 186.69 303.60 494.21 802.86 1298.8

64.002 81.699 104.77 118.81 134.84 174.02 225.03 377.46 633.59 1060.8 1767.471.403 92.503 120.44 137.63 157.41 206.34 271.03 469.06 812.00 1401.2 2404.779.543 104.60 138.30 159.28 183.60 244.49 326.24 582.63 1040.4 1850.6 3271.388.497 118.16 158.66 184.17 213.98 289.49 392.48 723.46 1332.7 2443.8 4450.098.347 133.33 181.87 212.79 249.21 342.60 471.98 898.09 1706.8 3226.8 6053.0

164.49 241.33 356.79 434.75 530.31 790.95 1181.9 2640.9 5873.2 12941. 28172.3442.59 767.09 1342.0 1779.1 2360.8 4163.2 7343.9 22729. 69377. * *1163.9 2400.0 4994.5 7217.7 10436. 21813. 45497. * * * *3034.8 7471.6 18535. 29220. 46058. * * * * * *

Ross−Westerfield−Jaffe: Corporate Finance, Sixth Edition

Back Matter Appendix A: Mathematical Tables

912 © The McGraw−Hill Companies, 2002

906 Appendix A Mathematical Tables

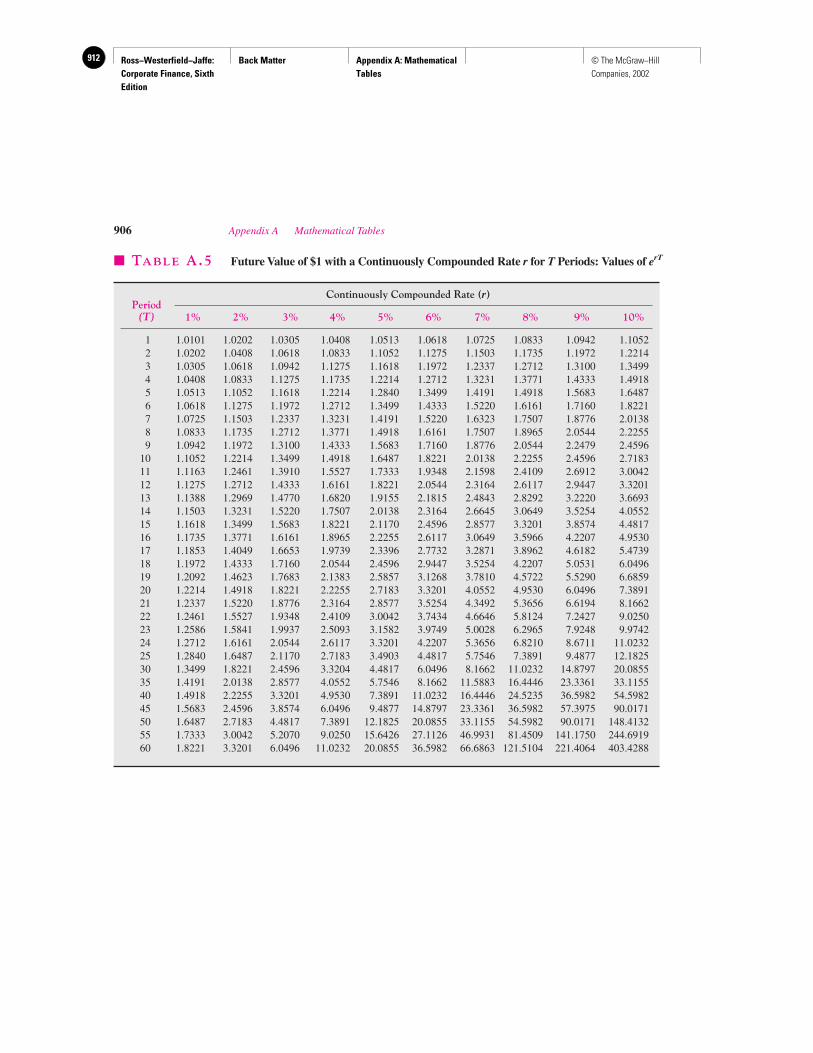

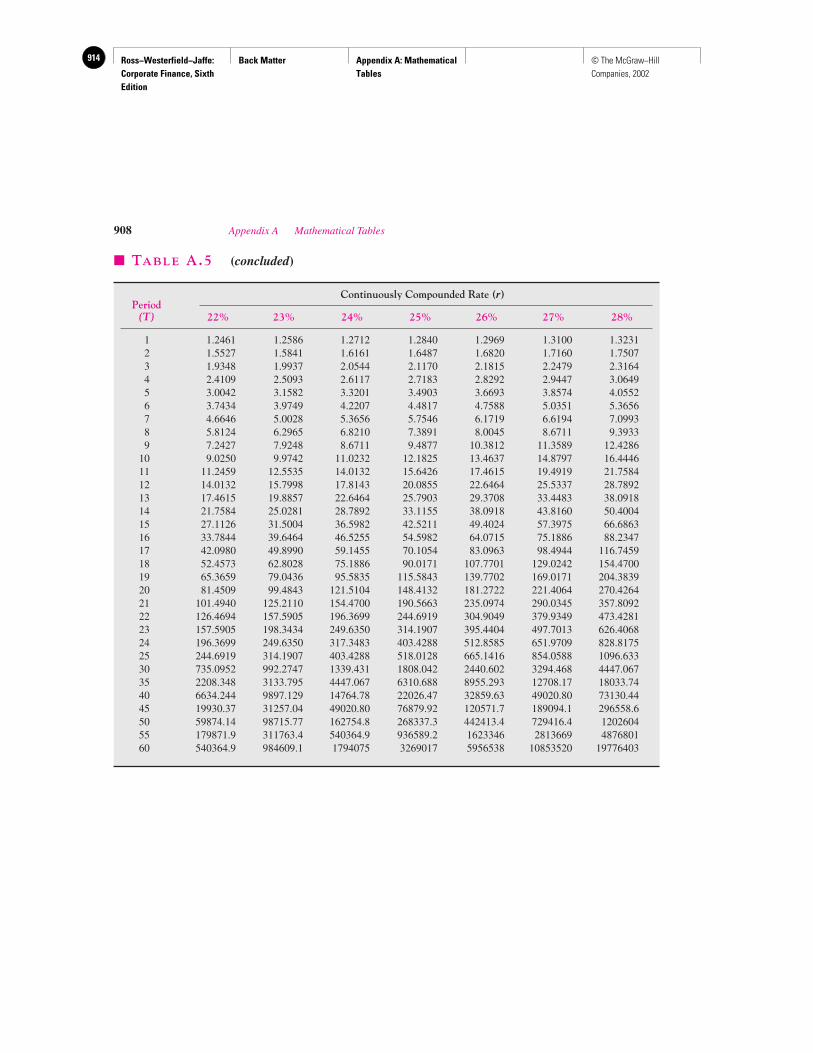

� TABLE A.5 Future Value of $1 with a Continuously Compounded Rate r for T Periods: Values of erT

Continuously Compounded Rate (r)

1% 2% 3% 4% 5% 6% 7% 8% 9% 10%

1 1.0101 1.0202 1.0305 1.0408 1.0513 1.0618 1.0725 1.0833 1.0942 1.10522 1.0202 1.0408 1.0618 1.0833 1.1052 1.1275 1.1503 1.1735 1.1972 1.22143 1.0305 1.0618 1.0942 1.1275 1.1618 1.1972 1.2337 1.2712 1.3100 1.34994 1.0408 1.0833 1.1275 1.1735 1.2214 1.2712 1.3231 1.3771 1.4333 1.49185 1.0513 1.1052 1.1618 1.2214 1.2840 1.3499 1.4191 1.4918 1.5683 1.64876 1.0618 1.1275 1.1972 1.2712 1.3499 1.4333 1.5220 1.6161 1.7160 1.82217 1.0725 1.1503 1.2337 1.3231 1.4191 1.5220 1.6323 1.7507 1.8776 2.01388 1.0833 1.1735 1.2712 1.3771 1.4918 1.6161 1.7507 1.8965 2.0544 2.22559 1.0942 1.1972 1.3100 1.4333 1.5683 1.7160 1.8776 2.0544 2.2479 2.4596

10 1.1052 1.2214 1.3499 1.4918 1.6487 1.8221 2.0138 2.2255 2.4596 2.718311 1.1163 1.2461 1.3910 1.5527 1.7333 1.9348 2.1598 2.4109 2.6912 3.004212 1.1275 1.2712 1.4333 1.6161 1.8221 2.0544 2.3164 2.6117 2.9447 3.320113 1.1388 1.2969 1.4770 1.6820 1.9155 2.1815 2.4843 2.8292 3.2220 3.669314 1.1503 1.3231 1.5220 1.7507 2.0138 2.3164 2.6645 3.0649 3.5254 4.055215 1.1618 1.3499 1.5683 1.8221 2.1170 2.4596 2.8577 3.3201 3.8574 4.481716 1.1735 1.3771 1.6161 1.8965 2.2255 2.6117 3.0649 3.5966 4.2207 4.953017 1.1853 1.4049 1.6653 1.9739 2.3396 2.7732 3.2871 3.8962 4.6182 5.473918 1.1972 1.4333 1.7160 2.0544 2.4596 2.9447 3.5254 4.2207 5.0531 6.049619 1.2092 1.4623 1.7683 2.1383 2.5857 3.1268 3.7810 4.5722 5.5290 6.685920 1.2214 1.4918 1.8221 2.2255 2.7183 3.3201 4.0552 4.9530 6.0496 7.389121 1.2337 1.5220 1.8776 2.3164 2.8577 3.5254 4.3492 5.3656 6.6194 8.166222 1.2461 1.5527 1.9348 2.4109 3.0042 3.7434 4.6646 5.8124 7.2427 9.025023 1.2586 1.5841 1.9937 2.5093 3.1582 3.9749 5.0028 6.2965 7.9248 9.974224 1.2712 1.6161 2.0544 2.6117 3.3201 4.2207 5.3656 6.8210 8.6711 11.023225 1.2840 1.6487 2.1170 2.7183 3.4903 4.4817 5.7546 7.3891 9.4877 12.182530 1.3499 1.8221 2.4596 3.3204 4.4817 6.0496 8.1662 11.0232 14.8797 20.085535 1.4191 2.0138 2.8577 4.0552 5.7546 8.1662 11.5883 16.4446 23.3361 33.115540 1.4918 2.2255 3.3201 4.9530 7.3891 11.0232 16.4446 24.5235 36.5982 54.598245 1.5683 2.4596 3.8574 6.0496 9.4877 14.8797 23.3361 36.5982 57.3975 90.017150 1.6487 2.7183 4.4817 7.3891 12.1825 20.0855 33.1155 54.5982 90.0171 148.413255 1.7333 3.0042 5.2070 9.0250 15.6426 27.1126 46.9931 81.4509 141.1750 244.691960 1.8221 3.3201 6.0496 11.0232 20.0855 36.5982 66.6863 121.5104 221.4064 403.4288

Period(T)

Ross−Westerfield−Jaffe: Corporate Finance, Sixth Edition

Back Matter Appendix A: Mathematical Tables

913© The McGraw−Hill Companies, 2002

Appendix A Mathematical Tables 907

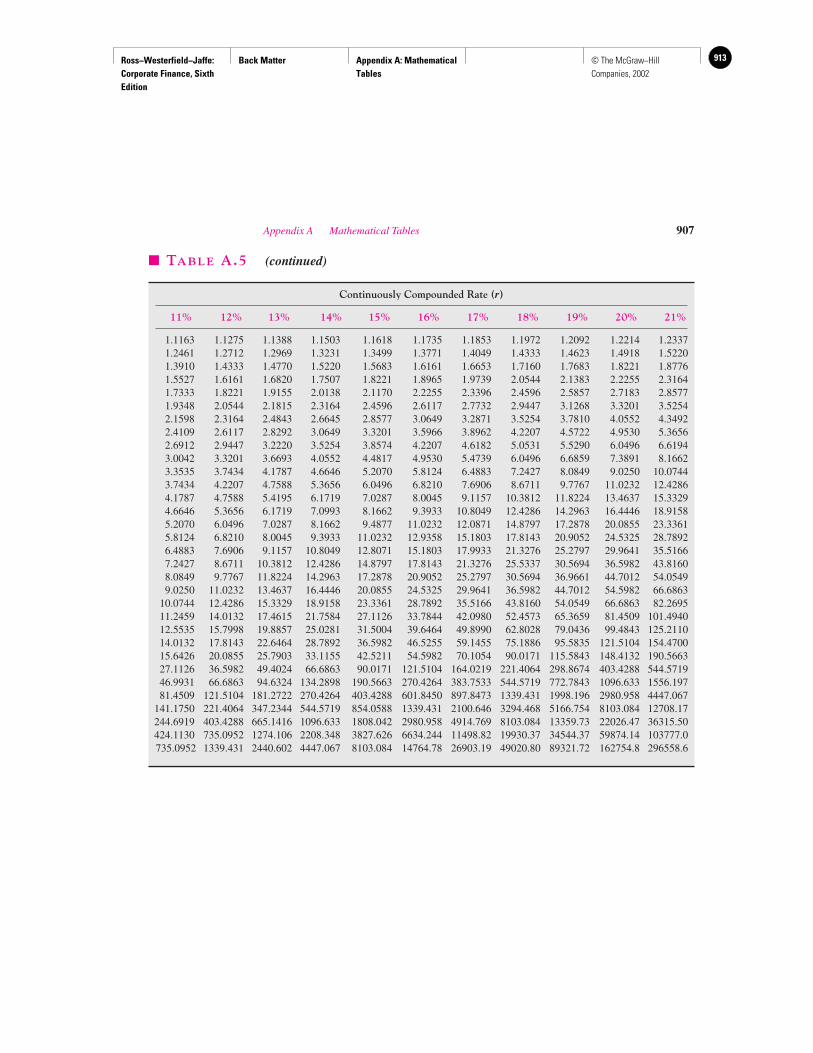

� TABLE A.5 (continued)

Continuously Compounded Rate (r)

11% 12% 13% 14% 15% 16% 17% 18% 19% 20% 21%

1.1163 1.1275 1.1388 1.1503 1.1618 1.1735 1.1853 1.1972 1.2092 1.2214 1.23371.2461 1.2712 1.2969 1.3231 1.3499 1.3771 1.4049 1.4333 1.4623 1.4918 1.52201.3910 1.4333 1.4770 1.5220 1.5683 1.6161 1.6653 1.7160 1.7683 1.8221 1.87761.5527 1.6161 1.6820 1.7507 1.8221 1.8965 1.9739 2.0544 2.1383 2.2255 2.31641.7333 1.8221 1.9155 2.0138 2.1170 2.2255 2.3396 2.4596 2.5857 2.7183 2.85771.9348 2.0544 2.1815 2.3164 2.4596 2.6117 2.7732 2.9447 3.1268 3.3201 3.52542.1598 2.3164 2.4843 2.6645 2.8577 3.0649 3.2871 3.5254 3.7810 4.0552 4.34922.4109 2.6117 2.8292 3.0649 3.3201 3.5966 3.8962 4.2207 4.5722 4.9530 5.36562.6912 2.9447 3.2220 3.5254 3.8574 4.2207 4.6182 5.0531 5.5290 6.0496 6.61943.0042 3.3201 3.6693 4.0552 4.4817 4.9530 5.4739 6.0496 6.6859 7.3891 8.16623.3535 3.7434 4.1787 4.6646 5.2070 5.8124 6.4883 7.2427 8.0849 9.0250 10.07443.7434 4.2207 4.7588 5.3656 6.0496 6.8210 7.6906 8.6711 9.7767 11.0232 12.42864.1787 4.7588 5.4195 6.1719 7.0287 8.0045 9.1157 10.3812 11.8224 13.4637 15.33294.6646 5.3656 6.1719 7.0993 8.1662 9.3933 10.8049 12.4286 14.2963 16.4446 18.91585.2070 6.0496 7.0287 8.1662 9.4877 11.0232 12.0871 14.8797 17.2878 20.0855 23.33615.8124 6.8210 8.0045 9.3933 11.0232 12.9358 15.1803 17.8143 20.9052 24.5325 28.78926.4883 7.6906 9.1157 10.8049 12.8071 15.1803 17.9933 21.3276 25.2797 29.9641 35.51667.2427 8.6711 10.3812 12.4286 14.8797 17.8143 21.3276 25.5337 30.5694 36.5982 43.81608.0849 9.7767 11.8224 14.2963 17.2878 20.9052 25.2797 30.5694 36.9661 44.7012 54.05499.0250 11.0232 13.4637 16.4446 20.0855 24.5325 29.9641 36.5982 44.7012 54.5982 66.6863

10.0744 12.4286 15.3329 18.9158 23.3361 28.7892 35.5166 43.8160 54.0549 66.6863 82.269511.2459 14.0132 17.4615 21.7584 27.1126 33.7844 42.0980 52.4573 65.3659 81.4509 101.494012.5535 15.7998 19.8857 25.0281 31.5004 39.6464 49.8990 62.8028 79.0436 99.4843 125.211014.0132 17.8143 22.6464 28.7892 36.5982 46.5255 59.1455 75.1886 95.5835 121.5104 154.470015.6426 20.0855 25.7903 33.1155 42.5211 54.5982 70.1054 90.0171 115.5843 148.4132 190.566327.1126 36.5982 49.4024 66.6863 90.0171 121.5104 164.0219 221.4064 298.8674 403.4288 544.571946.9931 66.6863 94.6324 134.2898 190.5663 270.4264 383.7533 544.5719 772.7843 1096.633 1556.19781.4509 121.5104 181.2722 270.4264 403.4288 601.8450 897.8473 1339.431 1998.196 2980.958 4447.067

141.1750 221.4064 347.2344 544.5719 854.0588 1339.431 2100.646 3294.468 5166.754 8103.084 12708.17244.6919 403.4288 665.1416 1096.633 1808.042 2980.958 4914.769 8103.084 13359.73 22026.47 36315.50424.1130 735.0952 1274.106 2208.348 3827.626 6634.244 11498.82 19930.37 34544.37 59874.14 103777.0735.0952 1339.431 2440.602 4447.067 8103.084 14764.78 26903.19 49020.80 89321.72 162754.8 296558.6

Ross−Westerfield−Jaffe: Corporate Finance, Sixth Edition

Back Matter Appendix A: Mathematical Tables

914 © The McGraw−Hill Companies, 2002

908 Appendix A Mathematical Tables

� TABLE A.5 (concluded)

Continuously Compounded Rate (r)

22% 23% 24% 25% 26% 27% 28%

1 1.2461 1.2586 1.2712 1.2840 1.2969 1.3100 1.32312 1.5527 1.5841 1.6161 1.6487 1.6820 1.7160 1.75073 1.9348 1.9937 2.0544 2.1170 2.1815 2.2479 2.31644 2.4109 2.5093 2.6117 2.7183 2.8292 2.9447 3.06495 3.0042 3.1582 3.3201 3.4903 3.6693 3.8574 4.05526 3.7434 3.9749 4.2207 4.4817 4.7588 5.0351 5.36567 4.6646 5.0028 5.3656 5.7546 6.1719 6.6194 7.09938 5.8124 6.2965 6.8210 7.3891 8.0045 8.6711 9.39339 7.2427 7.9248 8.6711 9.4877 10.3812 11.3589 12.4286

10 9.0250 9.9742 11.0232 12.1825 13.4637 14.8797 16.444611 11.2459 12.5535 14.0132 15.6426 17.4615 19.4919 21.758412 14.0132 15.7998 17.8143 20.0855 22.6464 25.5337 28.789213 17.4615 19.8857 22.6464 25.7903 29.3708 33.4483 38.091814 21.7584 25.0281 28.7892 33.1155 38.0918 43.8160 50.400415 27.1126 31.5004 36.5982 42.5211 49.4024 57.3975 66.686316 33.7844 39.6464 46.5255 54.5982 64.0715 75.1886 88.234717 42.0980 49.8990 59.1455 70.1054 83.0963 98.4944 116.745918 52.4573 62.8028 75.1886 90.0171 107.7701 129.0242 154.470019 65.3659 79.0436 95.5835 115.5843 139.7702 169.0171 204.383920 81.4509 99.4843 121.5104 148.4132 181.2722 221.4064 270.426421 101.4940 125.2110 154.4700 190.5663 235.0974 290.0345 357.809222 126.4694 157.5905 196.3699 244.6919 304.9049 379.9349 473.428123 157.5905 198.3434 249.6350 314.1907 395.4404 497.7013 626.406824 196.3699 249.6350 317.3483 403.4288 512.8585 651.9709 828.817525 244.6919 314.1907 403.4288 518.0128 665.1416 854.0588 1096.63330 735.0952 992.2747 1339.431 1808.042 2440.602 3294.468 4447.06735 2208.348 3133.795 4447.067 6310.688 8955.293 12708.17 18033.7440 6634.244 9897.129 14764.78 22026.47 32859.63 49020.80 73130.4445 19930.37 31257.04 49020.80 76879.92 120571.7 189094.1 296558.650 59874.14 98715.77 162754.8 268337.3 442413.4 729416.4 120260455 179871.9 311763.4 540364.9 936589.2 1623346 2813669 487680160 540364.9 984609.1 1794075 3269017 5956538 10853520 19776403

Period(T)

Ross−Westerfield−Jaffe: Corporate Finance, Sixth Edition

Back Matter Appendix A: Mathematical Tables

915© The McGraw−Hill Companies, 2002

Appendix A Mathematical Tables 909

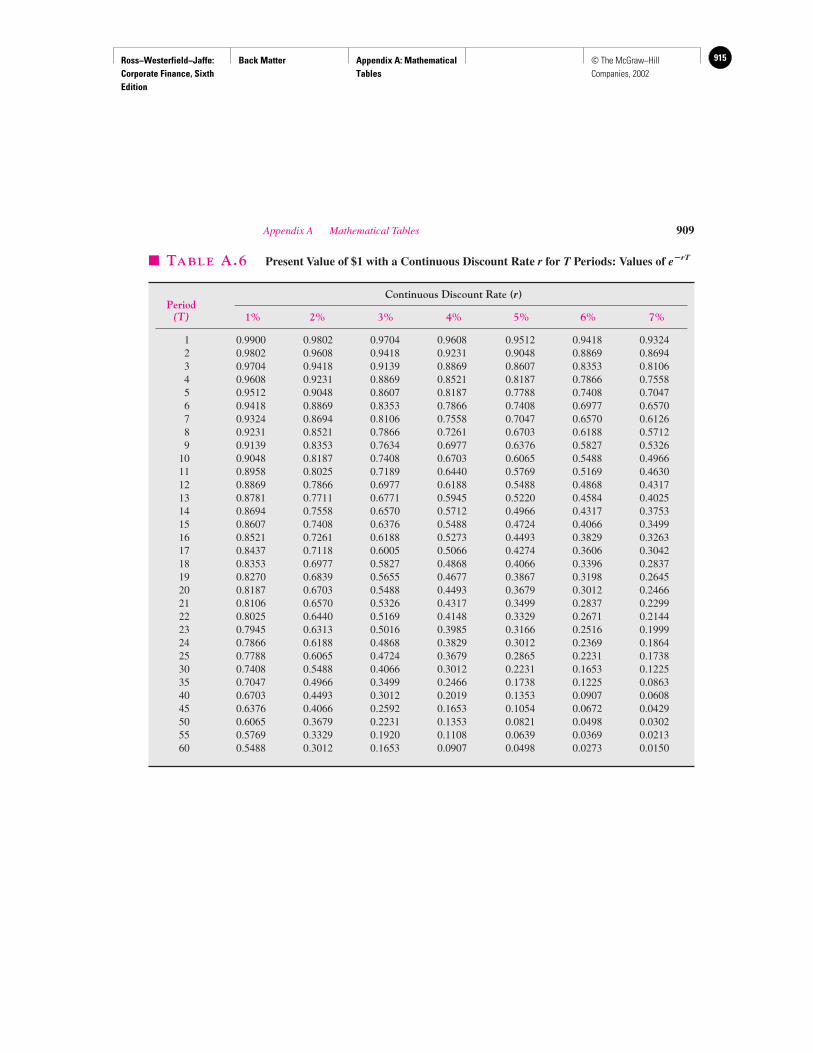

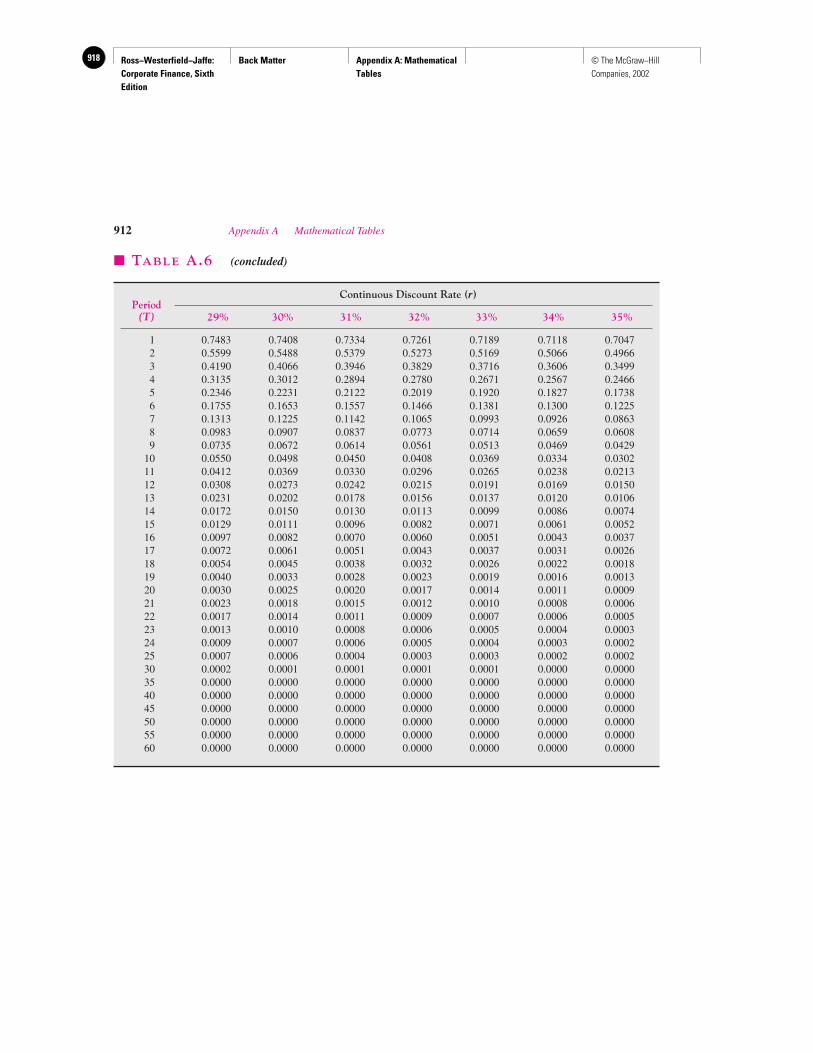

� TABLE A.6 Present Value of $1 with a Continuous Discount Rate r for T Periods: Values of e�rT

Continuous Discount Rate (r)

1% 2% 3% 4% 5% 6% 7%

1 0.9900 0.9802 0.9704 0.9608 0.9512 0.9418 0.93242 0.9802 0.9608 0.9418 0.9231 0.9048 0.8869 0.86943 0.9704 0.9418 0.9139 0.8869 0.8607 0.8353 0.81064 0.9608 0.9231 0.8869 0.8521 0.8187 0.7866 0.75585 0.9512 0.9048 0.8607 0.8187 0.7788 0.7408 0.70476 0.9418 0.8869 0.8353 0.7866 0.7408 0.6977 0.65707 0.9324 0.8694 0.8106 0.7558 0.7047 0.6570 0.61268 0.9231 0.8521 0.7866 0.7261 0.6703 0.6188 0.57129 0.9139 0.8353 0.7634 0.6977 0.6376 0.5827 0.5326

10 0.9048 0.8187 0.7408 0.6703 0.6065 0.5488 0.496611 0.8958 0.8025 0.7189 0.6440 0.5769 0.5169 0.463012 0.8869 0.7866 0.6977 0.6188 0.5488 0.4868 0.431713 0.8781 0.7711 0.6771 0.5945 0.5220 0.4584 0.402514 0.8694 0.7558 0.6570 0.5712 0.4966 0.4317 0.375315 0.8607 0.7408 0.6376 0.5488 0.4724 0.4066 0.349916 0.8521 0.7261 0.6188 0.5273 0.4493 0.3829 0.326317 0.8437 0.7118 0.6005 0.5066 0.4274 0.3606 0.304218 0.8353 0.6977 0.5827 0.4868 0.4066 0.3396 0.283719 0.8270 0.6839 0.5655 0.4677 0.3867 0.3198 0.264520 0.8187 0.6703 0.5488 0.4493 0.3679 0.3012 0.246621 0.8106 0.6570 0.5326 0.4317 0.3499 0.2837 0.229922 0.8025 0.6440 0.5169 0.4148 0.3329 0.2671 0.214423 0.7945 0.6313 0.5016 0.3985 0.3166 0.2516 0.199924 0.7866 0.6188 0.4868 0.3829 0.3012 0.2369 0.186425 0.7788 0.6065 0.4724 0.3679 0.2865 0.2231 0.173830 0.7408 0.5488 0.4066 0.3012 0.2231 0.1653 0.122535 0.7047 0.4966 0.3499 0.2466 0.1738 0.1225 0.086340 0.6703 0.4493 0.3012 0.2019 0.1353 0.0907 0.060845 0.6376 0.4066 0.2592 0.1653 0.1054 0.0672 0.042950 0.6065 0.3679 0.2231 0.1353 0.0821 0.0498 0.030255 0.5769 0.3329 0.1920 0.1108 0.0639 0.0369 0.021360 0.5488 0.3012 0.1653 0.0907 0.0498 0.0273 0.0150

Period(T)

Ross−Westerfield−Jaffe: Corporate Finance, Sixth Edition

Back Matter Appendix A: Mathematical Tables

916 © The McGraw−Hill Companies, 2002

910 Appendix A Mathematical Tables

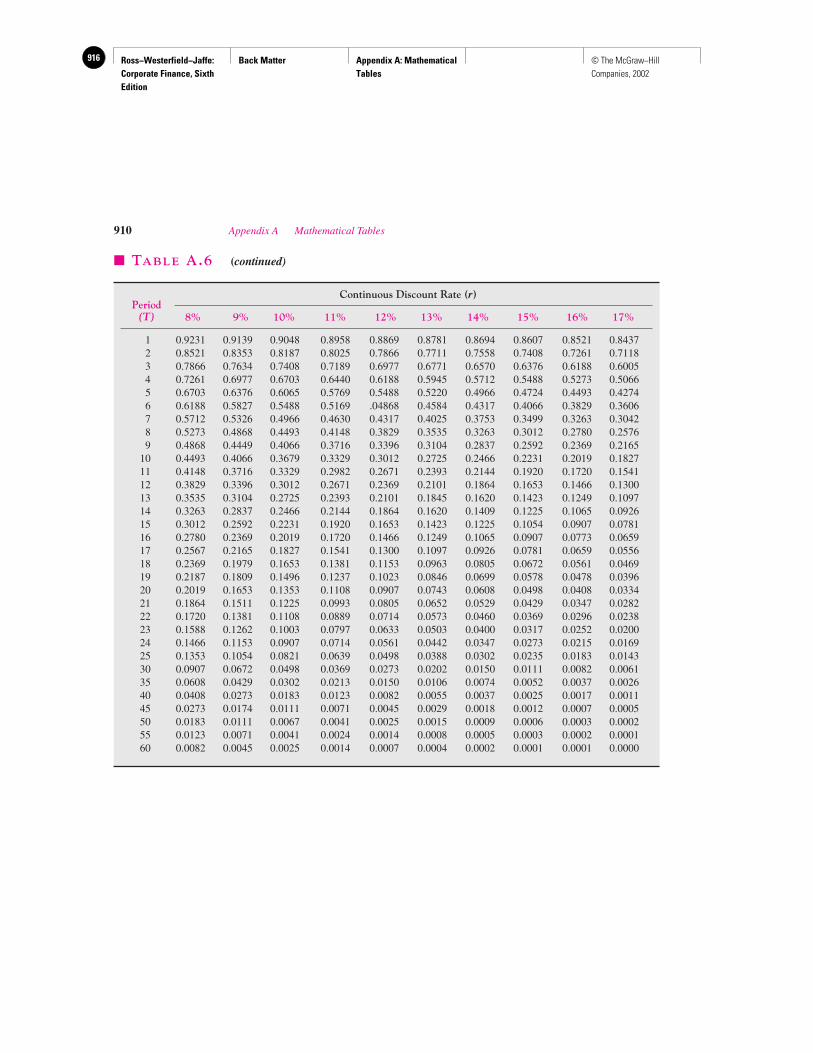

� TABLE A.6 (continued)

Continuous Discount Rate (r)

8% 9% 10% 11% 12% 13% 14% 15% 16% 17%

1 0.9231 0.9139 0.9048 0.8958 0.8869 0.8781 0.8694 0.8607 0.8521 0.84372 0.8521 0.8353 0.8187 0.8025 0.7866 0.7711 0.7558 0.7408 0.7261 0.71183 0.7866 0.7634 0.7408 0.7189 0.6977 0.6771 0.6570 0.6376 0.6188 0.60054 0.7261 0.6977 0.6703 0.6440 0.6188 0.5945 0.5712 0.5488 0.5273 0.50665 0.6703 0.6376 0.6065 0.5769 0.5488 0.5220 0.4966 0.4724 0.4493 0.42746 0.6188 0.5827 0.5488 0.5169 .04868 0.4584 0.4317 0.4066 0.3829 0.36067 0.5712 0.5326 0.4966 0.4630 0.4317 0.4025 0.3753 0.3499 0.3263 0.30428 0.5273 0.4868 0.4493 0.4148 0.3829 0.3535 0.3263 0.3012 0.2780 0.25769 0.4868 0.4449 0.4066 0.3716 0.3396 0.3104 0.2837 0.2592 0.2369 0.2165

10 0.4493 0.4066 0.3679 0.3329 0.3012 0.2725 0.2466 0.2231 0.2019 0.182711 0.4148 0.3716 0.3329 0.2982 0.2671 0.2393 0.2144 0.1920 0.1720 0.154112 0.3829 0.3396 0.3012 0.2671 0.2369 0.2101 0.1864 0.1653 0.1466 0.130013 0.3535 0.3104 0.2725 0.2393 0.2101 0.1845 0.1620 0.1423 0.1249 0.109714 0.3263 0.2837 0.2466 0.2144 0.1864 0.1620 0.1409 0.1225 0.1065 0.092615 0.3012 0.2592 0.2231 0.1920 0.1653 0.1423 0.1225 0.1054 0.0907 0.078116 0.2780 0.2369 0.2019 0.1720 0.1466 0.1249 0.1065 0.0907 0.0773 0.065917 0.2567 0.2165 0.1827 0.1541 0.1300 0.1097 0.0926 0.0781 0.0659 0.055618 0.2369 0.1979 0.1653 0.1381 0.1153 0.0963 0.0805 0.0672 0.0561 0.046919 0.2187 0.1809 0.1496 0.1237 0.1023 0.0846 0.0699 0.0578 0.0478 0.039620 0.2019 0.1653 0.1353 0.1108 0.0907 0.0743 0.0608 0.0498 0.0408 0.033421 0.1864 0.1511 0.1225 0.0993 0.0805 0.0652 0.0529 0.0429 0.0347 0.028222 0.1720 0.1381 0.1108 0.0889 0.0714 0.0573 0.0460 0.0369 0.0296 0.023823 0.1588 0.1262 0.1003 0.0797 0.0633 0.0503 0.0400 0.0317 0.0252 0.020024 0.1466 0.1153 0.0907 0.0714 0.0561 0.0442 0.0347 0.0273 0.0215 0.016925 0.1353 0.1054 0.0821 0.0639 0.0498 0.0388 0.0302 0.0235 0.0183 0.014330 0.0907 0.0672 0.0498 0.0369 0.0273 0.0202 0.0150 0.0111 0.0082 0.006135 0.0608 0.0429 0.0302 0.0213 0.0150 0.0106 0.0074 0.0052 0.0037 0.002640 0.0408 0.0273 0.0183 0.0123 0.0082 0.0055 0.0037 0.0025 0.0017 0.001145 0.0273 0.0174 0.0111 0.0071 0.0045 0.0029 0.0018 0.0012 0.0007 0.000550 0.0183 0.0111 0.0067 0.0041 0.0025 0.0015 0.0009 0.0006 0.0003 0.000255 0.0123 0.0071 0.0041 0.0024 0.0014 0.0008 0.0005 0.0003 0.0002 0.000160 0.0082 0.0045 0.0025 0.0014 0.0007 0.0004 0.0002 0.0001 0.0001 0.0000

Period(T)

Ross−Westerfield−Jaffe: Corporate Finance, Sixth Edition

Back Matter Appendix A: Mathematical Tables

917© The McGraw−Hill Companies, 2002

Appendix A Mathematical Tables 911

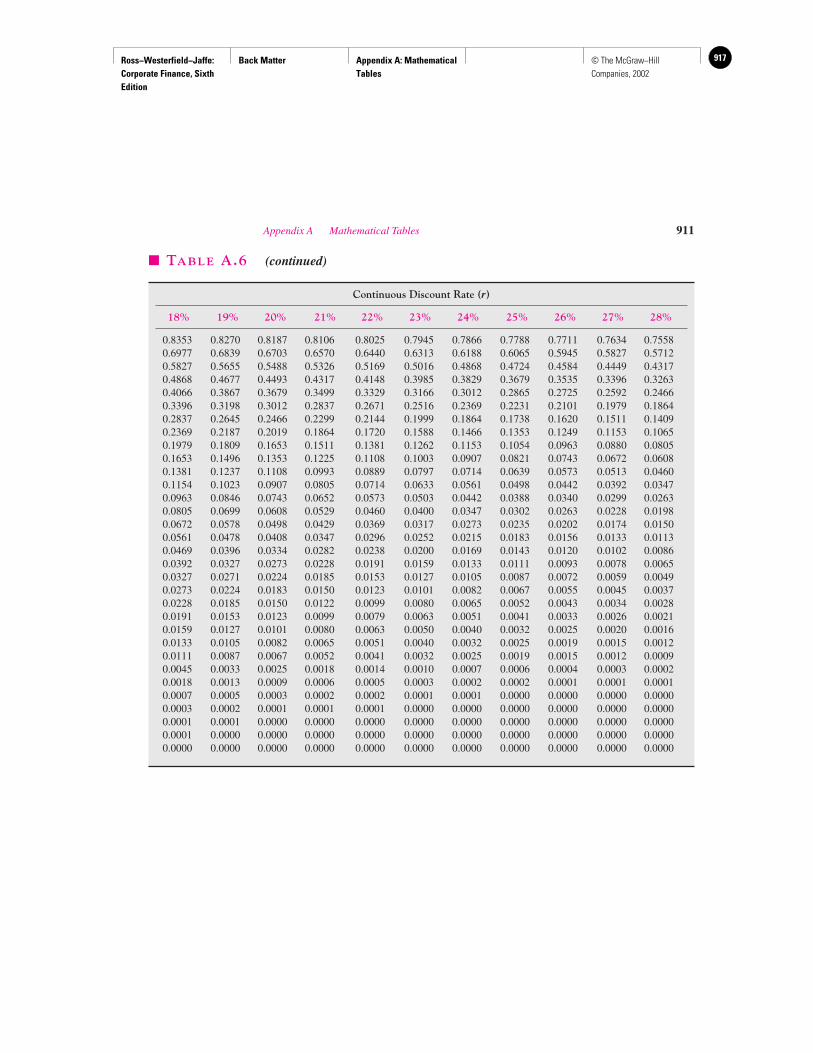

� TABLE A.6 (continued)

Continuous Discount Rate (r)

18% 19% 20% 21% 22% 23% 24% 25% 26% 27% 28%

0.8353 0.8270 0.8187 0.8106 0.8025 0.7945 0.7866 0.7788 0.7711 0.7634 0.75580.6977 0.6839 0.6703 0.6570 0.6440 0.6313 0.6188 0.6065 0.5945 0.5827 0.57120.5827 0.5655 0.5488 0.5326 0.5169 0.5016 0.4868 0.4724 0.4584 0.4449 0.43170.4868 0.4677 0.4493 0.4317 0.4148 0.3985 0.3829 0.3679 0.3535 0.3396 0.32630.4066 0.3867 0.3679 0.3499 0.3329 0.3166 0.3012 0.2865 0.2725 0.2592 0.24660.3396 0.3198 0.3012 0.2837 0.2671 0.2516 0.2369 0.2231 0.2101 0.1979 0.18640.2837 0.2645 0.2466 0.2299 0.2144 0.1999 0.1864 0.1738 0.1620 0.1511 0.14090.2369 0.2187 0.2019 0.1864 0.1720 0.1588 0.1466 0.1353 0.1249 0.1153 0.10650.1979 0.1809 0.1653 0.1511 0.1381 0.1262 0.1153 0.1054 0.0963 0.0880 0.08050.1653 0.1496 0.1353 0.1225 0.1108 0.1003 0.0907 0.0821 0.0743 0.0672 0.06080.1381 0.1237 0.1108 0.0993 0.0889 0.0797 0.0714 0.0639 0.0573 0.0513 0.04600.1154 0.1023 0.0907 0.0805 0.0714 0.0633 0.0561 0.0498 0.0442 0.0392 0.03470.0963 0.0846 0.0743 0.0652 0.0573 0.0503 0.0442 0.0388 0.0340 0.0299 0.02630.0805 0.0699 0.0608 0.0529 0.0460 0.0400 0.0347 0.0302 0.0263 0.0228 0.01980.0672 0.0578 0.0498 0.0429 0.0369 0.0317 0.0273 0.0235 0.0202 0.0174 0.01500.0561 0.0478 0.0408 0.0347 0.0296 0.0252 0.0215 0.0183 0.0156 0.0133 0.01130.0469 0.0396 0.0334 0.0282 0.0238 0.0200 0.0169 0.0143 0.0120 0.0102 0.00860.0392 0.0327 0.0273 0.0228 0.0191 0.0159 0.0133 0.0111 0.0093 0.0078 0.00650.0327 0.0271 0.0224 0.0185 0.0153 0.0127 0.0105 0.0087 0.0072 0.0059 0.00490.0273 0.0224 0.0183 0.0150 0.0123 0.0101 0.0082 0.0067 0.0055 0.0045 0.00370.0228 0.0185 0.0150 0.0122 0.0099 0.0080 0.0065 0.0052 0.0043 0.0034 0.00280.0191 0.0153 0.0123 0.0099 0.0079 0.0063 0.0051 0.0041 0.0033 0.0026 0.00210.0159 0.0127 0.0101 0.0080 0.0063 0.0050 0.0040 0.0032 0.0025 0.0020 0.00160.0133 0.0105 0.0082 0.0065 0.0051 0.0040 0.0032 0.0025 0.0019 0.0015 0.00120.0111 0.0087 0.0067 0.0052 0.0041 0.0032 0.0025 0.0019 0.0015 0.0012 0.00090.0045 0.0033 0.0025 0.0018 0.0014 0.0010 0.0007 0.0006 0.0004 0.0003 0.00020.0018 0.0013 0.0009 0.0006 0.0005 0.0003 0.0002 0.0002 0.0001 0.0001 0.00010.0007 0.0005 0.0003 0.0002 0.0002 0.0001 0.0001 0.0000 0.0000 0.0000 0.00000.0003 0.0002 0.0001 0.0001 0.0001 0.0000 0.0000 0.0000 0.0000 0.0000 0.00000.0001 0.0001 0.0000 0.0000 0.0000 0.0000 0.0000 0.0000 0.0000 0.0000 0.00000.0001 0.0000 0.0000 0.0000 0.0000 0.0000 0.0000 0.0000 0.0000 0.0000 0.00000.0000 0.0000 0.0000 0.0000 0.0000 0.0000 0.0000 0.0000 0.0000 0.0000 0.0000

Ross−Westerfield−Jaffe: Corporate Finance, Sixth Edition

Back Matter Appendix A: Mathematical Tables

918 © The McGraw−Hill Companies, 2002

912 Appendix A Mathematical Tables

� TABLE A.6 (concluded)

Continuous Discount Rate (r)

29% 30% 31% 32% 33% 34% 35%

1 0.7483 0.7408 0.7334 0.7261 0.7189 0.7118 0.70472 0.5599 0.5488 0.5379 0.5273 0.5169 0.5066 0.49663 0.4190 0.4066 0.3946 0.3829 0.3716 0.3606 0.34994 0.3135 0.3012 0.2894 0.2780 0.2671 0.2567 0.24665 0.2346 0.2231 0.2122 0.2019 0.1920 0.1827 0.17386 0.1755 0.1653 0.1557 0.1466 0.1381 0.1300 0.12257 0.1313 0.1225 0.1142 0.1065 0.0993 0.0926 0.08638 0.0983 0.0907 0.0837 0.0773 0.0714 0.0659 0.06089 0.0735 0.0672 0.0614 0.0561 0.0513 0.0469 0.0429

10 0.0550 0.0498 0.0450 0.0408 0.0369 0.0334 0.030211 0.0412 0.0369 0.0330 0.0296 0.0265 0.0238 0.021312 0.0308 0.0273 0.0242 0.0215 0.0191 0.0169 0.015013 0.0231 0.0202 0.0178 0.0156 0.0137 0.0120 0.010614 0.0172 0.0150 0.0130 0.0113 0.0099 0.0086 0.007415 0.0129 0.0111 0.0096 0.0082 0.0071 0.0061 0.005216 0.0097 0.0082 0.0070 0.0060 0.0051 0.0043 0.003717 0.0072 0.0061 0.0051 0.0043 0.0037 0.0031 0.002618 0.0054 0.0045 0.0038 0.0032 0.0026 0.0022 0.001819 0.0040 0.0033 0.0028 0.0023 0.0019 0.0016 0.001320 0.0030 0.0025 0.0020 0.0017 0.0014 0.0011 0.000921 0.0023 0.0018 0.0015 0.0012 0.0010 0.0008 0.000622 0.0017 0.0014 0.0011 0.0009 0.0007 0.0006 0.000523 0.0013 0.0010 0.0008 0.0006 0.0005 0.0004 0.000324 0.0009 0.0007 0.0006 0.0005 0.0004 0.0003 0.000225 0.0007 0.0006 0.0004 0.0003 0.0003 0.0002 0.000230 0.0002 0.0001 0.0001 0.0001 0.0001 0.0000 0.000035 0.0000 0.0000 0.0000 0.0000 0.0000 0.0000 0.000040 0.0000 0.0000 0.0000 0.0000 0.0000 0.0000 0.000045 0.0000 0.0000 0.0000 0.0000 0.0000 0.0000 0.000050 0.0000 0.0000 0.0000 0.0000 0.0000 0.0000 0.000055 0.0000 0.0000 0.0000 0.0000 0.0000 0.0000 0.000060 0.0000 0.0000 0.0000 0.0000 0.0000 0.0000 0.0000

Period(T)

Ross−Westerfield−Jaffe: Corporate Finance, Sixth Edition

Back Matter Appendix B: Solutions to Selected End−of−Chapter Problems

919© The McGraw−Hill Companies, 2002

Solutions to SelectedEnd-of-Chapter Problems

AP

PE

ND

IXB

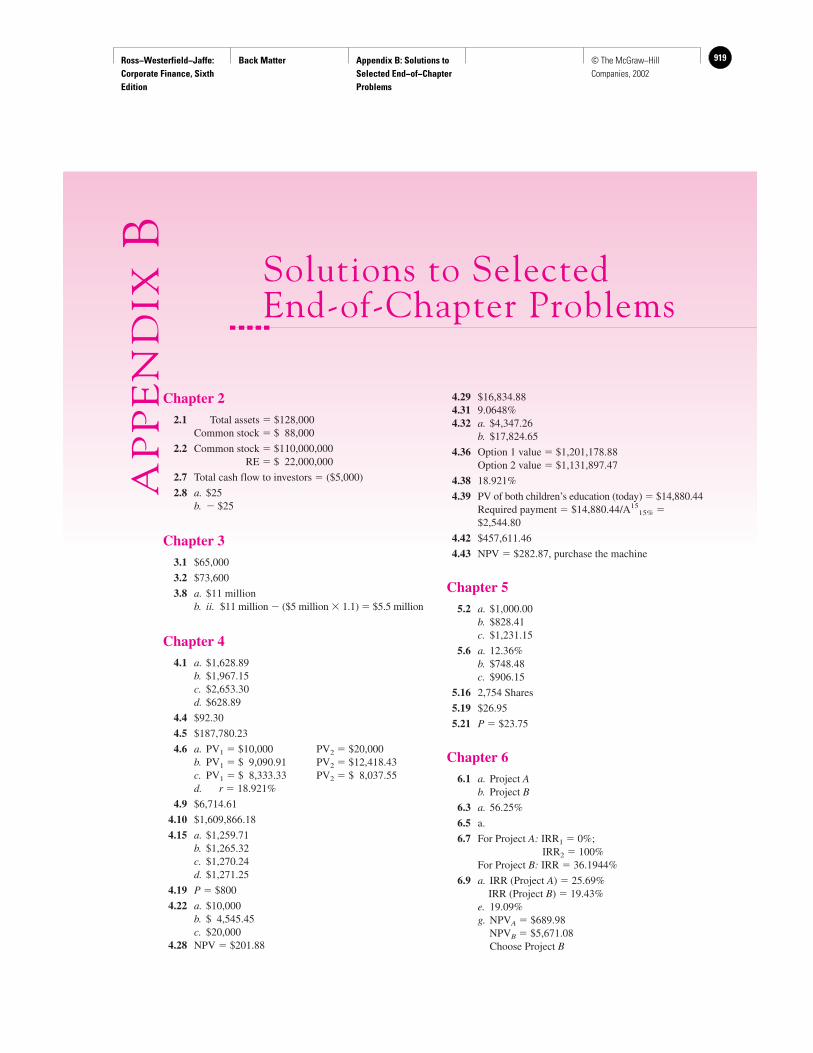

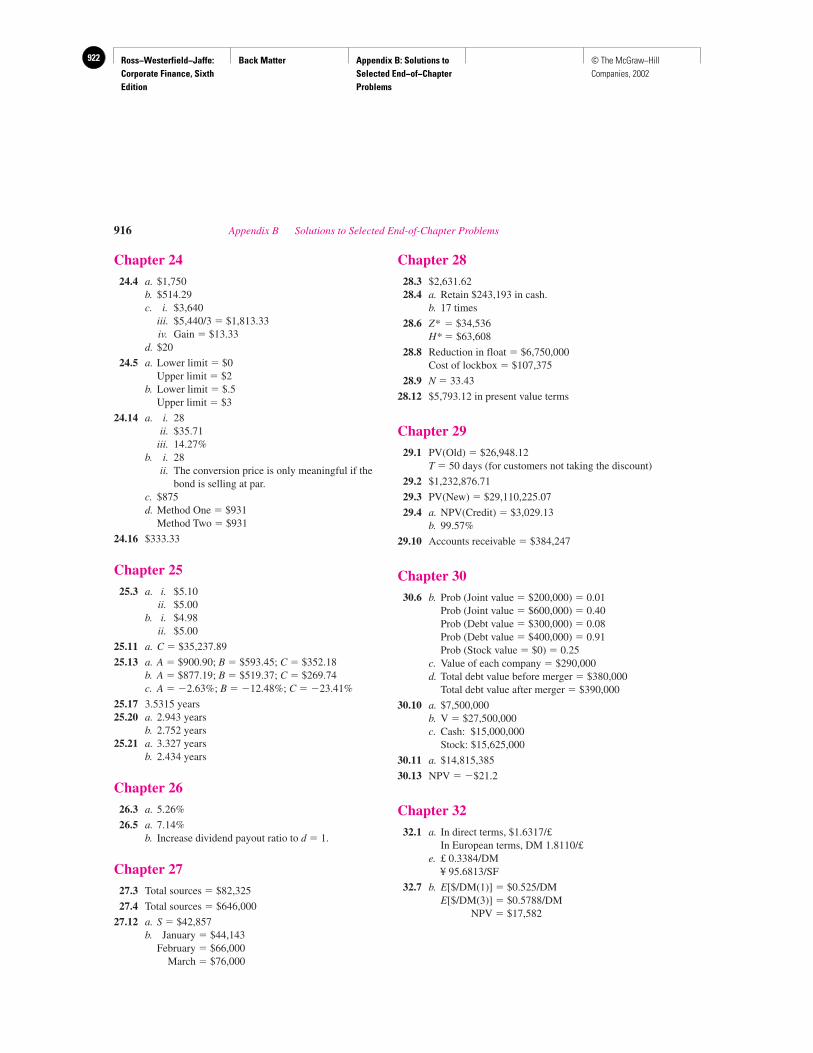

Chapter 22.1 Total assets � $128,000

Common stock � $ 88,000

2.2 Common stock � $110,000,000RE � $ 22,000,000

2.7 Total cash flow to investors � ($5,000)

2.8 a. $25b. � $25

Chapter 33.1 $65,000

3.2 $73,600

3.8 a. $11 millionb. ii. $11 million � ($5 million � 1.1) � $5.5 million

Chapter 44.1 a. $1,628.89

b. $1,967.15c. $2,653.30d. $628.89

4.4 $92.30

4.5 $187,780.23

4.6 a. PV1 � $10,000 PV2 � $20,000b. PV1 � $ 9,090.91 PV2 � $12,418.43c. PV1 � $ 8,333.33 PV2 � $ 8,037.55d. r � 18.921%

4.9 $6,714.61

4.10 $1,609,866.18

4.15 a. $1,259.71b. $1,265.32c. $1,270.24d. $1,271.25

4.19 P � $800

4.22 a. $10,000b. $ 4,545.45c. $20,000

4.28 NPV � $201.88

4.29 $16,834.884.31 9.0648%4.32 a. $4,347.26

b. $17,824.65

4.36 Option 1 value � $1,201,178.88Option 2 value � $1,131,897.47

4.38 18.921%

4.39 PV of both children’s education (today) � $14,880.44Required payment � $14,880.44/A15

15% �$2,544.80

4.42 $457,611.46

4.43 NPV � $282.87, purchase the machine

Chapter 55.2 a. $1,000.00

b. $828.41c. $1,231.15

5.6 a. 12.36%b. $748.48c. $906.15

5.16 2,754 Shares

5.19 $26.95

5.21 P � $23.75

Chapter 66.1 a. Project A

b. Project B

6.3 a. 56.25%

6.5 a.

6.7 For Project A: IRR1 � 0%;IRR2 � 100%

For Project B: IRR � 36.1944%

6.9 a. IRR (Project A) � 25.69%IRR (Project B) � 19.43%

e. 19.09%g. NPVA � $689.98

NPVB � $5,671.08Choose Project B

Ross−Westerfield−Jaffe: Corporate Finance, Sixth Edition

Back Matter Appendix B: Solutions to Selected End−of−Chapter Problems

920 © The McGraw−Hill Companies, 2002

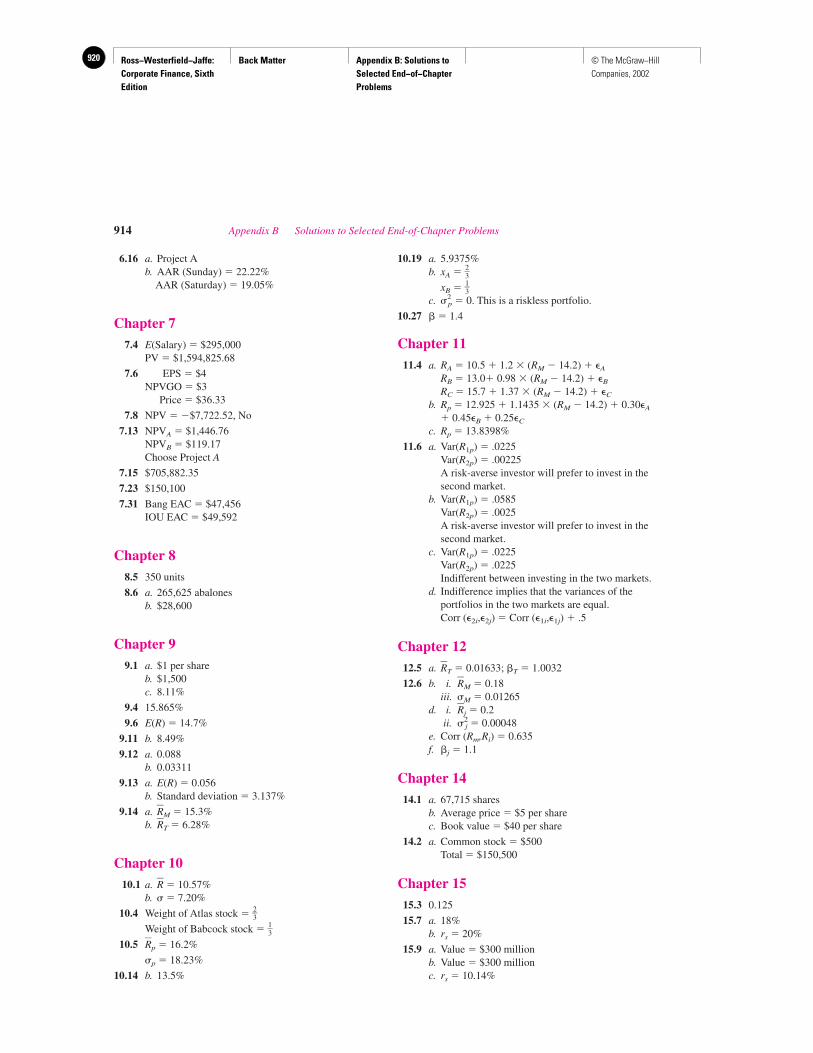

6.16 a. Project Ab. AAR (Sunday) � 22.22%

AAR (Saturday) � 19.05%

Chapter 77.4 E(Salary) � $295,000

PV � $1,594,825.68

7.6 EPS � $4NPVGO � $3

Price � $36.33

7.8 NPV � �$7,722.52, No

7.13 NPVA � $1,446.76NPVB � $119.17Choose Project A

7.15 $705,882.35

7.23 $150,100

7.31 Bang EAC � $47,456IOU EAC � $49,592

Chapter 88.5 350 units

8.6 a. 265,625 abalonesb. $28,600

Chapter 99.1 a. $1 per share

b. $1,500c. 8.11%

9.4 15.865%

9.6 E(R) � 14.7%

9.11 b. 8.49%

9.12 a. 0.088b. 0.03311

9.13 a. E(R) � 0.056b. Standard deviation � 3.137%

9.14 a. R�M � 15.3%b. R�T � 6.28%

Chapter 1010.1 a. R� � 10.57%

b. � � 7.20%

10.4 Weight of Atlas stock � 23

Weight of Babcock stock � 13

10.5 R�p � 16.2%

�p � 18.23%

10.14 b. 13.5%

10.19 a. 5.9375%b. xA � 2

3

xB � 13

c. �2p � 0. This is a riskless portfolio.

10.27 � � 1.4

Chapter 1111.4 a. RA � 10.5 � 1.2 � (RM � 14.2) � A

RB � 13.0� 0.98 � (RM � 14.2) � B

RC � 15.7 � 1.37 � (RM � 14.2) � C

b. Rp � 12.925 � 1.1435 � (RM � 14.2) � 0.30A

� 0.45B � 0.25C

c. Rp � 13.8398%

11.6 a. Var(R1p) � .0225Var(R2p) � .00225A risk-averse investor will prefer to invest in thesecond market.

b. Var(R1p) � .0585Var(R2p) � .0025A risk-averse investor will prefer to invest in thesecond market.

c. Var(R1p) � .0225Var(R2p) � .0225Indifferent between investing in the two markets.

d. Indifference implies that the variances of theportfolios in the two markets are equal.Corr (2i,2j) � Corr (1i,1j) � .5

Chapter 1212.5 a. R�T � 0.01633; �T � 1.0032

12.6 b. i. R�M � 0.18iii. �M � 0.01265

d. i. R�j � 0.2ii. �2

j � 0.00048e. Corr (Rm,Ri) � 0.635f. �j � 1.1

Chapter 1414.1 a. 67,715 shares

b. Average price � $5 per sharec. Book value � $40 per share

14.2 a. Common stock � $500Total � $150,500

Chapter 1515.3 0.125

15.7 a. 18%b. rs � 20%

15.9 a. Value � $300 millionb. Value � $300 millionc. rs � 10.14%

914 Appendix B Solutions to Selected End-of-Chapter Problems

Ross−Westerfield−Jaffe: Corporate Finance, Sixth Edition

Back Matter Appendix B: Solutions to Selected End−of−Chapter Problems

921© The McGraw−Hill Companies, 2002

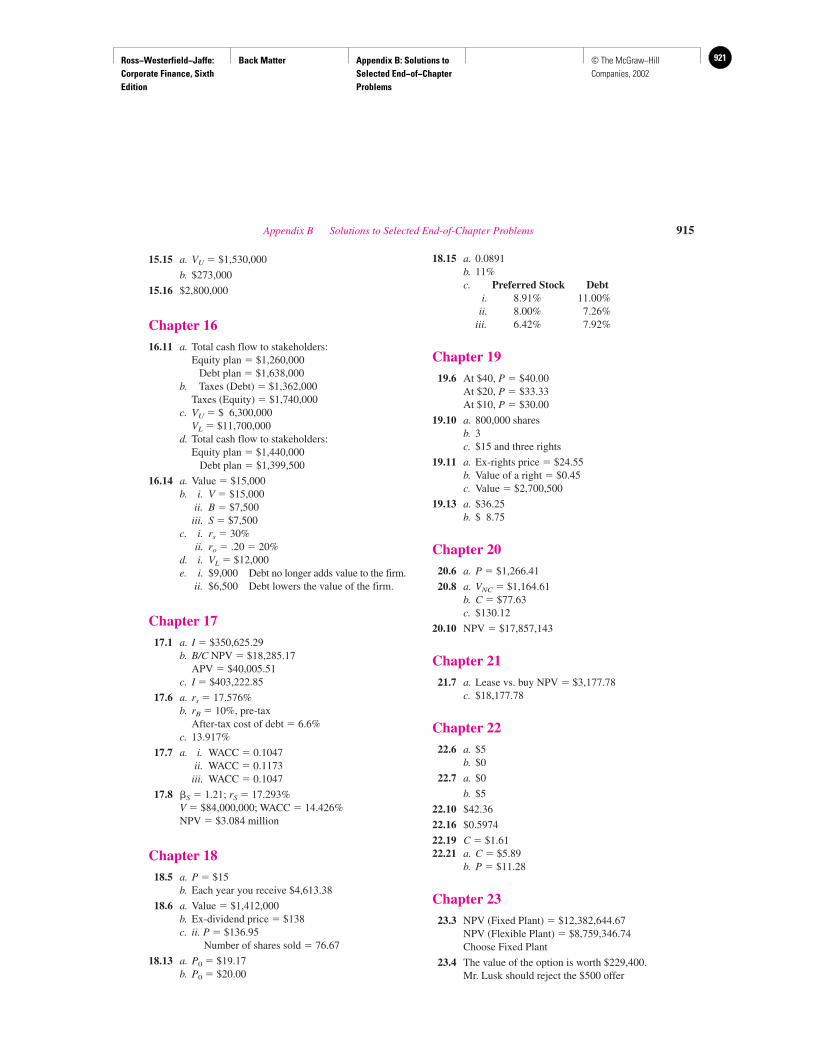

15.15 a. VU � $1,530,000

b. $273,000

15.16 $2,800,000

Chapter 1616.11 a. Total cash flow to stakeholders:

Equity plan � $1,260,000Debt plan � $1,638,000

b. Taxes (Debt) � $1,362,000Taxes (Equity) � $1,740,000

c. VU � $ 6,300,000VL � $11,700,000

d. Total cash flow to stakeholders:Equity plan � $1,440,000

Debt plan � $1,399,500

16.14 a. Value � $15,000b. i. V � $15,000

ii. B � $7,500iii. S � $7,500

c. i. rs � 30%ii. ro � .20 � 20%

d. i. VL � $12,000e. i. $9,000 Debt no longer adds value to the firm.

ii. $6,500 Debt lowers the value of the firm.

Chapter 1717.1 a. I � $350,625.29

b. B/C NPV � $18,285.17APV � $40,005.51

c. I � $403,222.85

17.6 a. rs � 17.576%b. rB � 10%, pre-tax

After-tax cost of debt � 6.6%c. 13.917%

17.7 a. i. WACC � 0.1047ii. WACC � 0.1173iii. WACC � 0.1047

17.8 �S � 1.21; rS � 17.293%V � $84,000,000; WACC � 14.426%NPV � $3.084 million

Chapter 1818.5 a. P � $15

b. Each year you receive $4,613.38

18.6 a. Value � $1,412,000b. Ex-dividend price � $138c. ii. P � $136.95

Number of shares sold � 76.67

18.13 a. P0 � $19.17b. P0 � $20.00

18.15 a. 0.0891b. 11%c. Preferred Stock Debt

i. 8.91% 11.00%ii. 8.00% 7.26%

iii. 6.42% 7.92%

Chapter 1919.6 At $40, P � $40.00

At $20, P � $33.33At $10, P � $30.00

19.10 a. 800,000 sharesb. 3c. $15 and three rights

19.11 a. Ex-rights price � $24.55b. Value of a right � $0.45c. Value � $2,700,500

19.13 a. $36.25b. $ 8.75

Chapter 2020.6 a. P � $1,266.41

20.8 a. VNC � $1,164.61b. C � $77.63c. $130.12

20.10 NPV � $17,857,143

Chapter 2121.7 a. Lease vs. buy NPV � $3,177.78

c. $18,177.78

Chapter 2222.6 a. $5

b. $0

22.7 a. $0

b. $5

22.10 $42.36

22.16 $0.5974

22.19 C � $1.6122.21 a. C � $5.89

b. P � $11.28

Chapter 2323.3 NPV (Fixed Plant) � $12,382,644.67

NPV (Flexible Plant) � $8,759,346.74Choose Fixed Plant

23.4 The value of the option is worth $229,400. Mr. Lusk should reject the $500 offer

Appendix B Solutions to Selected End-of-Chapter Problems 915

Ross−Westerfield−Jaffe: Corporate Finance, Sixth Edition

Back Matter Appendix B: Solutions to Selected End−of−Chapter Problems

922 © The McGraw−Hill Companies, 2002

Chapter 2424.4 a. $1,750

b. $514.29c. i. $3,640

iii. $5,440/3 � $1,813.33iv. Gain � $13.33

d. $20

24.5 a. Lower limit � $0Upper limit � $2

b. Lower limit � $.5Upper limit � $3

24.14 a. i. 28ii. $35.71

iii. 14.27%b. i. 28

ii. The conversion price is only meaningful if thebond is selling at par.

c. $875d. Method One � $931

Method Two � $931

24.16 $333.33

Chapter 2525.3 a. i. $5.10

ii. $5.00b. i. $4.98

ii. $5.00

25.11 a. C � $35,237.89

25.13 a. A � $900.90; B � $593.45; C � $352.18b. A � $877.19; B � $519.37; C � $269.74c. A � �2.63%; B � �12.48%; C � �23.41%

25.17 3.5315 years25.20 a. 2.943 years

b. 2.752 years25.21 a. 3.327 years

b. 2.434 years

Chapter 2626.3 a. 5.26%

26.5 a. 7.14%b. Increase dividend payout ratio to d � 1.

Chapter 2727.3 Total sources � $82,325

27.4 Total sources � $646,000

27.12 a. S � $42,857b. January � $44,143

February � $66,000March � $76,000

Chapter 2828.3 $2,631.6228.4 a. Retain $243,193 in cash.

b. 17 times

28.6 Z* � $34,536H* � $63,608

28.8 Reduction in float � $6,750,000Cost of lockbox � $107,375

28.9 N � 33.43

28.12 $5,793.12 in present value terms

Chapter 2929.1 PV(Old) � $26,948.12

T � 50 days (for customers not taking the discount)

29.2 $1,232,876.71

29.3 PV(New) � $29,110,225.07

29.4 a. NPV(Credit) � $3,029.13b. 99.57%

29.10 Accounts receivable � $384,247

Chapter 3030.6 b. Prob (Joint value � $200,000) � 0.01

Prob (Joint value � $600,000) � 0.40Prob (Debt value � $300,000) � 0.08Prob (Debt value � $400,000) � 0.91Prob (Stock value � $0) � 0.25

c. Value of each company � $290,000d. Total debt value before merger � $380,000

Total debt value after merger � $390,000

30.10 a. $7,500,000b. V � $27,500,000c. Cash: $15,000,000

Stock: $15,625,000

30.11 a. $14,815,385

30.13 NPV � �$21.2

Chapter 3232.1 a. In direct terms, $1.6317/£

In European terms, DM 1.8110/£e. £ 0.3384/DM

¥ 95.6813/SF

32.7 b. E[$/DM(1)] � $0.525/DME[$/DM(3)] � $0.5788/DM

NPV � $17,582

916 Appendix B Solutions to Selected End-of-Chapter Problems

Ross−Westerfield−Jaffe: Corporate Finance, Sixth Edition

Back Matter Glossary 923© The McGraw−Hill Companies, 2002

Glossary

AAR Average accounting return.

ACRS Accelerated cost recovery system.

APT Arbitrage pricing theory.

Absolute priority rule (APR) Establishes priority ofclaims under liquidation.

Accelerated cost recovery system (ACRS) A system usedto depreciate assets for tax purposes. The current system, en-acted by the 1986 Tax Reform Act, is very similar to theACRS established in 1981. The current system specifies thedepreciable lives (recovery periods) and rates for each of sev-eral classes of property.

Accounting insolvency Total liabilities exceed total assets.A firm with negative net worth is insolvent on the books.

Accounting liquidity The ease and quickness with whichassets can be converted to cash.

Accounts payable Money the firm owes to suppliers.

Accounts receivable Money owed to the firm by customers.

Accounts receivable financing A secured short-term loanthat involves either the assigning of receivables or the factor-ing of receivables. Under assignment, the lender has a lien onthe receivables and recourse to the borrower. Factoring in-volves the sale of accounts receivable. Then the purchaser,called the factor, must collect on the receivables.

Accounts receivable turnover Credit sales divided by av-erage accounts receivable.

Additions to net working capital Component of cash flowof firm, along with operating cash flow and capital spending.

Advance commitment A promise to sell an asset before theseller has lined up purchase of the asset. This seller can offsetrisk by purchasing a futures contract to fix the sales price.

Agency costs Costs of conflicts of interest among stock-holders, bondholders, and managers. Agency costs are thecosts of resolving these conflicts. They include the costs ofproviding managers with an incentive to maximize share-holder wealth and then monitoring their behavior, and the costof protecting bondholders from shareholders. Agency costsare borne by stockholders.

Agency theory The theory of the relationship betweenprincipals and agents. It involves the nature of the costs of re-solving conflicts of interest between principals and agents.

Aggregation Process in corporate financial planning wherebythe smaller investment proposals of each of the firm’s opera-tional units are added up and in effect treated as a big picture.

Aging schedule A compilation of accounts receivable bythe age of account.

American Depository Receipt (ADR) A security issued inthe United States to represent shares of a foreign stock, en-abling that stock to be traded in the United States.

American option An option contract that may be exercisedanytime up to the expiration date. A European option may beexercised only on the expiration date.

Amortization Repayment of a loan in installments.

Angels Individuals providing venture capital.

Annualized holding-period return The annual rate of re-turn that when compounded T times, would have given thesame T-period holding return as actually occurred from pe-riod 1 to period T.

Annuity A level stream of equal dollar payments that lastsfor a fixed time. An example of an annuity is the coupon partof a bond with level annual payments.

Annuity factor The term used to calculate the present valueof the stream of level payments for a fixed period.

Annuity in advance An annuity with an immediate initialpayment.

Annuity in arrears An annuity with a first payment onefull period hence, rather than immediately. That is, the firstpayment occurs on date 1 rather than on date 0.

Appraisal rights Rights of shareholders of an acquiredfirm that allow them to demand that their shares be purchasedat a fair value by the acquiring firm.

Arbitrage Buying an asset in one market at a lowerprice and simultaneously selling an identical asset in another market at a higher price. This is done with no costor risk.

Arbitrage pricing theory (APT) An equilibrium assetpricing theory that is derived from a factor model by usingdiversification and arbitrage. It shows that the expected re-turn on any risky asset is a linear combination of variousfactors.

Arithmetic average The sum of the values observed di-vided by the total number of observations—sometimes re-ferred to as the mean.

Assets Anything that the firm owns.

Assets requirements A common element of a financialplan that describes projected capital spending and the pro-posed uses of net working capital.

Ross−Westerfield−Jaffe: Corporate Finance, Sixth Edition

Back Matter Glossary924 © The McGraw−Hill Companies, 2002

Auction market A market where all traders in a certaingood meet at one place to buy or sell an asset. The NYSE isan example.

Autocorrelation The correlation of a variable with itselfover successive time intervals.

Availability float Refers to the time required to clear acheck through the banking system.

Average accounting return (AAR) The average projectearnings after taxes and depreciation divided by the averagebook value of the investment during its life.

Average collection period Average amount of time re-quired to collect an account receivable. Also referred to asdays sales outstanding.

Average cost of capital A firm’s required payout to thebondholders and the stockholders expressed as a percentageof capital contributed to the firm. Average cost of capital iscomputed by dividing the total required cost of capital by thetotal amount of contributed capital.

Average daily sales Annual sales divided by 365 days.

Balance sheet A statement showing a firm’s accountingvalue on a particular date. It reflects the equation, Assets �Liabilities � Stockholders’ equity.

Balloon payment Large final payment, as when a loan isrepaid in installments.

Banker’s acceptance Agreement by a bank to pay a givensum of money at a future date.

Bankruptcy State of being unable to pay debts. Thus theownership of the firm’s assets is transferred from the stock-holders to the bondholders.

Bankruptcy costs See Financial distress costs.

Bargain-purchase-price option Gives lessee the option topurchase the asset at a price below fair market value when thelease expires.

Basic IRR rule Accept the project if IRR is greater than thediscount rate; reject the project if IRR is less than the discountrate.

Bearer bond A bond issued without record of the owner’sname. Whoever holds the bond (the bearer) is the owner.

Best-efforts underwriting An offering in which an under-writer agrees to distribute as much of the offering as possibleand to return any unsold shares to the issuer.

Beta coefficient A measure of the sensitivity of a security’sreturn to movements in an underlying factor. It is a measuredsystematic risk.

Bidder A firm or person that has made an offer to take overanother firm.

Black-Scholes call pricing equation An exact formula forthe price of a call option. The formula requires five vari-ables: the risk-free interest rate, the variance of the underlyingstock, the exercise price, the price of the underlying stock, andthe time to expiration.

Blanket inventory lien A secured loan that gives the lendera lien against all the borrower’s inventories.

Bond A long-term debt of a firm. In common usage, theterm bond often refers to both secured and unsecured debt.

Book cash A firm’s cash balance as reported in its financialstatements. Also called ledger cash.

Book value per share Per-share accounting equity value ofa firm. Total accounting equity divided by the number of out-standing shares.

Borrow To obtain or receive money on loan with the prom-ise or understanding of returning it or its equivalent.

Break-even analysis Analysis of the level of sales at whicha project would make zero profit.

Bubble theory (of speculative markets) Security pricessometimes move wildly above their true values.

Business failure The risk that the firm’s stockholders bearif the firm is financed only with equity.

Buying the index Purchasing the stocks in the Standard &Poor’s 500 in the same proportion as the index to achieve thesame return.

CAPM Capital asset pricing model.

CAR Cumulative abnormal return.

Call option The right—but not the obligation—to buy afixed number of shares of stock at a stated price within a spec-ified time.

Call premium The price of a call option on common stock.

Call price of a bond Amount at which a firm has the rightto repurchase its bonds or debentures before the stated matu-rity date. The call price is always set at equal to or more thanthe par value.

Call protected Describes a bond that is not allowed to becalled, usually for a certain early period in the life of the bond.

Call provision A written agreement between an issuingcorporation and its bondholders that gives the corporation theoption to redeem the bond at a specified price before the ma-turity date.

Callable Refers to a bond that is subject to be repurchasedat a stated call price before maturity.

Capital asset pricing model (CAPM) An equilibrium as-set pricing theory that shows that equilibrium rates of ex-pected return on all risky assets are a function of their covari-ance with the market portfolio.

Capital budgeting Planning and managing expendituresfor long-lived assets.

Capital gains The positive change in the value of an asset.A negative capital gain is a capital loss.

Capital market line The efficient set of all assets, bothrisky and riskless, which provides the investor with the bestpossible opportunities.

Capital markets Financial markets for long-term debt andfor equity shares.

918 Glossary

Ross−Westerfield−Jaffe: Corporate Finance, Sixth Edition

Back Matter Glossary 925© The McGraw−Hill Companies, 2002

Capital rationing The case where funds are limited to a fixeddollar amount and must be allocated among competing projects.

Capital structure The mix of the various debt and equitycapital maintained by a firm. Also called financial structure.The composition of a corporation’s securities used to financeits investment activities; the relative proportions of short-termdebt, long-term debt, and owners’ equity.

Capital surplus Amounts of directly contributed equitycapital in excess of the par value.

Carrying costs Costs that increase with increases in thelevel of investment in current assets.

Carrying value Book value.

Cash budget A forecast of cash receipts and disbursementsexpected by a firm in the coming year. It is a short-term fi-nancial planning tool.

Cash cow A company that pays out all earnings per share tostockholders as dividends.

Cash cycle In general, the time between cash disbursementand cash collection. In net working capital management, itcan be thought of as the operating cycle less the accountspayable payment period.

Cash discount A discount given for a cash purchase. Onereason a cash discount may be offered is to speed up the col-lection of receivables.

Cash flow Cash generated by the firm and paid to creditorsand shareholders. It can be classified as (1) cash flow fromoperations, (2) cash flow from changes in fixed assets, and(3) cash flow from changes in net working capital.

Cash flow after interest and taxes Net income plus depreciation.

Cash-flow time line Line depicting the operating activitiesand cash flows for a firm over a particular period.

Cash offer A public equity issue that is sold to all interestedinvestors.

Cash transaction A transaction where exchange is imme-diate, as contrasted to a forward contract, which calls for fu-ture delivery of an asset at an agreed-upon price.

Cashout Refers to situation where a firm runs out of cashand cannot readily sell marketable securities.

Certificates of deposit Short-term loans to commercialbanks.

Change in net working capital Difference between networking capital from one period to another.

Changes in fixed assets Component of cash flow that equalssales of fixed assets minus the acquisition of fixed assets.

Characteristic line The line relating the expected return ona security to different returns on the market.

Clearing The exchanging of checks and balancing of ac-counts between banks.

Clientele effect Argument that stocks attract clientelesbased on dividend yield or taxes. For example, a tax clientele

effect is induced by the difference in tax treatment of dividendincome and capital gains income; high tax-bracket individu-als tend to prefer low-dividend yields.

Coinsurance effect Refers to the fact that the merger of twofirms decreases the probability of default on either’s debt.

Collateral Assets that are pledged as security for paymentof debt.

Collateral trust bond A bond secured by a pledge of com-mon stock held by the corporation.

Collection float An increase in book cash with no immedi-ate change in bank cash, generated by checks deposited by thefirm that have not cleared.

Collection policy Procedures followed by a firm in at-tempting to collect accounts receivable.

Commercial draft Demand for payment.

Commercial paper Short-term, unsecured promissorynotes issued by corporations with a high credit standing. Theirmaturity ranges up to 270 days.

Common equity Book value.

Common stock Equity claims held by the “residual own-ers” of the firm, who are the last to receive any distribution ofearnings or assets.

Compensating balance Deposit that the firm keeps withthe bank in a low-interest or non-interest-bearing account tocompensate banks for bank loans or services.

Competitive offer Method of selecting an investmentbanker for a new issue by offering the securities to the under-writer bidding highest.

Composition Voluntary arrangement to restructure a firm’sdebt, under which payment is reduced.

Compound interest Interest that is earned both on the ini-tial principal and on interest earned on the initial principal inprevious periods. The interest earned in one period becomesin effect part of the principal in a following period.

Compound value Value of a sum after investing it over oneor more periods. Also called future value.

Compounding Process of reinvesting each interest pay-ment to earn more interest. Compounding is based on the ideathat interest itself becomes principal and therefore also earnsinterest in subsequent periods.

Concentration banking The use of geographically dis-persed collection centers to speed up the collection of ac-counts receivable.

Conditional sales contract An arrangement whereby thefirm retains legal ownership of the goods until the customerhas completed payment.

Conflict between bondholders and stockholders Thesetwo groups may have interests in the corporation that conflict.Sources of conflict include dividends, dilution, distortion ofinvestment, and underinvestment. Protective covenants workto resolve these conflicts.

Glossary 919

Ross−Westerfield−Jaffe: Corporate Finance, Sixth Edition

Back Matter Glossary926 © The McGraw−Hill Companies, 2002

Conglomerate acquisition Acquisition in which the ac-quired firm and the acquiring firm are not related, unlike ahorizontal or a vertical acquisition.

Consol A bond that carries a promise to pay a coupon forever;it has no final maturity date and therefore never matures.

Consolidation A merger in which an entirely new firm iscreated.

Consumer credit Credit granted to consumers. Tradecredit is credit granted to other firms.

Contingent claim Claim whose value is directly dependenton, or is contingent on, the value of its underlying assets. Forexample, the debt and equity securities issued by a firm derivetheir value from the total value of the firm.

Contingent pension liability Under ERISA, the firm is li-able to the plan participants for up to 30 percent of the networth of the firm.

Continuous compounding Interest compounded continu-ously, every instant, rather than at fixed intervals.

Contribution margin Amount that each additional prod-uct, such as a jet engine, contributes to after-tax profit of thewhole project: (Sales price � Variable cost) � (1 � Tc),where Tc is the corporate tax rate.

Conversion premium Difference between the conversionprice and the current stock price divided by the current stockprice.

Conversion price The amount of par value exchangeablefor one share of common stock. This term really refers to thestock price and means the dollar amount of the bond’s parvalue that is exchangeable for one share of stock.

Conversion ratio The number of shares per $1,000 bond(or debenture) that a bondholder would receive if the bondwere converted into shares of stock.

Conversion value What a convertible bond would be worthif it were immediately converted into the common stock at thecurrent price.

Convertible bond A bond that may be converted into an-other form of security, typically common stock, at the optionof the holder at a specified price for a specified period of time.

Corporation Form of business organization that is createdas a distinct “legal person” composed of one or more actualindividuals or legal entities. Primary advantages of a corpora-tion include limited liability, ease of ownership, transfer, andperpetual succession.

Correlation A standardized statistical measure of the de-pendence of two random variables. It is defined as the covari-ance divided by the standard deviations of two variables.

Cost of equity capital The required return on the com-pany’s common stock in capital markets. It is also called theequity holders’ required rate of return because it is what eq-uity holders can expect to obtain in the capital market. It is acost from the firm’s perspective.

Coupon The stated interest on a debt instrument.

Covariance A statistical measure of the degree to whichrandom variables move together.

Credit analysis The process of determining whether acredit applicant meets the firm’s standards and what amountof credit the applicant should receive.

Credit instrument Device by which a firm offers credit,such as an invoice, a promissory note, or a conditional salescontract.

Credit period Time allowed a credit purchaser to remit thefull payment for credit purchases.

Credit scoring Determining the probability of defaultwhen granting customers credit.

Creditor Person or institution that holds the debt issued bya firm or individual.

Cross rate The exchange rate between two foreign curren-cies, neither of which is generally the U.S. dollar.

Crown jewels An antitakeover tactic in which major assets—the crown jewels—are sold by a firm when facedwith a takeover threat.

Cum dividend With dividend.

Cumulative abnormal return (CAR) Sum of differencesbetween the expected return on a stock and the actual returnthat comes from the release of news to the market.

Cumulative dividend Dividend on preferred stock thattakes priority over dividend payments on common stock.Dividends may not be paid on the common stock until all pastdividends on the preferred stock have been paid.

Cumulative probability The probability that a drawingfrom the standardized normal distribution will be below a par-ticular value.

Cumulative voting A procedure whereby a shareholdermay cast all of his or her votes for one member of the boardof directors.

Current asset Asset that is in the form of cash or that is ex-pected to be converted into cash in the next 12 months, suchas inventory.

Current liabilities Obligations that are expected to requirecash payment within one year or the operating period.

Current ratio Total current assets divided by total currentliabilities. Used to measure short-term solvency of a firm.

Date of payment Date that dividend checks are mailed.

Date of record Date on which holders of record in a firm’sstock ledger are designated as the recipients of either divi-dends or stock rights.

Dates convention Treating cash flows as being received onexact dates—date 0, date 1, and so forth—as opposed to theend-of-year convention.

Days in receivables Average collection period.

Days sales outstanding Average collection period.

De facto Existing in actual fact although not by officialrecognition.

920 Glossary

Ross−Westerfield−Jaffe: Corporate Finance, Sixth Edition

Back Matter Glossary 927© The McGraw−Hill Companies, 2002

Dealer market A market where traders specializing in par-ticular commodities buy and sell assets for their own account.The OTC market is an example.

Debenture An unsecured bond, usually with maturity of 15 years or more. A debt obligation backed by the generalcredit of the issuing corporation.

Debt Loan agreement that is a liability of the firm. An obli-gation to repay a specified amount at a particular time.

Debt capacity Ability to borrow. The amount a firm canborrow up to the point where the firm value no longer increases.

Debt displacement The amount of borrowing that leasingdisplaces. Firms that do a lot of leasing will be forced to cutback on borrowing.

Debt ratio Total debt divided by total assets.

Debt service Interest payments plus repayments of princi-pal to creditors, that is, retirement of debt.

Decision trees A graphical representation of alternativesequential decisions and the possible outcomes of those decisions.

Declaration date Date on which the board of directorspasses a resolution to pay a dividend of a specified amount toall qualified holders of record on a specified date.

Dedicated capital Total par value (number of shares issuedmultiplied by the par value of each share). Also called dedi-cated value.

Deed of trust Indenture.

Deep-discount bond A bond issued with a very lowcoupon or no coupon and selling at a price far below parvalue. When the bond has no coupon, it is also called a pure-discount or original-issue-discount bond.

Default risk The chance that interest or principal will notbe paid on the due date and in the promised amount.

Defeasance A debt-restructuring tool that enables a firm toremove debt from its balance sheet by establishing an irrevo-cable trust that will generate future cash flows sufficient toservice the decreased debt.

Deferred call A provision that prohibits the company fromcalling the bond before a certain date. During this period thebond is said to be call protected.

Deferred nominal life annuity A monthly fixed-dollarpayment beginning at retirement age. It is nominal becausethe payment is fixed in dollar amount at any particular time,up to and including retirement.

Deferred taxes Noncash expense.

Deficit The amount by which a sum of money is less thanthe required amount; an excess of liabilities over assets, oflosses over profits, or of expenditure over income.

Deliverable instrument The asset in a forward contractthat will be delivered in the future at an agreed-upon price.

Denomination Face value or principal of a bond.

Depreciation A noncash expense, such as the cost of plantor equipment, charged against earnings to write off the cost ofan asset during its estimated useful life.

Depreciation tax shield Portion of an investment that canbe deducted from taxable income.

Dilution Loss in existing shareholders’ value. There are sev-eral kinds of dilution: (1) dilution of ownership, (2) dilution ofmarket value, and (3) dilution of book value and earnings, aswith warrants and convertible issues. Firms with significantamounts of warrants or convertible issues outstanding are re-quired to report earnings on a “fully diluted” basis.

Direct lease A lease under which a lessor buys equipmentfrom a manufacturer and leases it to a lessee.

Disbursement float A decrease in book cash but no imme-diate change in bank cash, generated by checks written by the firm.

Discount If a bond is selling below its face value, it is saidto sell at a discount.

Discount rate Rate used to calculate the present value offuture cash flows.

Discounted payback period rule An investment decisionrule in which the cash flows are discounted at an interest rateand the payback rule is applied on these discounted cash flows.

Discounting Calculating the present value of a futureamount. The process is the opposite of compounding.

Distribution A type of dividend paid by a firm to its own-ers from sources other than current or accumulated retainedearnings.

Diversifiable risk A risk that specifically affects a singleasset or a small group of assets. Also called unique or unsys-tematic risk.

Dividend Payment made by a firm to its owners, either incash or in stock. Also called the “income component” of thereturn on an investment in stock.

Dividend growth model A model wherein dividends areassumed to be at a constant rate in perpetuity.

Dividend payout Amount of cash paid to shareholders ex-pressed as a percentage of earnings per share.

Dividend yield Dividends per share of common stock di-vided by market price per share.

Dividends per share Amount of cash paid to shareholdersexpressed as dollars per share.

Double-declining balance depreciation Method of accel-erated depreciation.

DuPont system of financial control Highlights the factthat return on assets (ROA) can be expressed in terms of theprofit margin and asset turnover.

Duration The weighted average time of an asset’s cashflows. The weights are determined by present value factors.

EAC Equivalent annual cost.

Glossary 921

Ross−Westerfield−Jaffe: Corporate Finance, Sixth Edition

Back Matter Glossary928 © The McGraw−Hill Companies, 2002

EBIT Earnings before interest and taxes.

EMH Efficient market hypothesis.

ERISA Employee Retirement Income Security Act of 1974.

Economic assumptions Economic environment in whichthe firm expects to reside over the life of the financial plan.

Effective annual interest rate The interest rate as if it werecompounded once per time period rather than several timesper period.

Efficient market hypothesis (EMH) The prices of se-curities fully reflect available information. Investors buy-ing bonds and stocks in an efficient market should expectto obtain an equilibrium rate of return. Firms should expectto receive the “fair” value (present value) for the securitiesthey sell.

Efficient set Graph representing a set of portfolios thatmaximize expected return at each level of portfolio risk.

End-of-year convention Treating cash flows as if they oc-cur at the end of a year (or, alternatively, at the end of a pe-riod), as opposed to the date convention. Under the end-of-year convention, the end of year 0 is the present, end of year1 occurs one period hence, and so on.

Equilibrium rate of interest The interest rate that clearsthe market. Also called market-clearing interest rate.

Equity Ownership interest of common and preferred stock-holders in a corporation. Also, total assets minus total liabili-ties, or net worth.

Equity kicker Used to refer to warrants because they usu-ally are issued in combination with privately placed bonds.

Equity share Ownership interest.

Equivalent annual cost (EAC) The net present value ofcost divided by an annuity factor that has the same life as theinvestment.

Equivalent loan The amount of the loan that makes leasingequivalent to buying with debt financing in terms of debt ca-pacity reduction.

Erosion Cash-flow amount transferred to a new projectfrom customers and sales of other products of the firm.

Eurobanks Banks that make loans and accept deposits inforeign currencies.

Eurobond An international bond sold primarily in coun-tries other than the country in whose currency the issue isdenominated.

Eurocurrency Money deposited in a financial center out-side of the country whose currency is involved.

Eurodollar A dollar deposited in a bank outside the UnitedStates.

Eurodollar CD Deposit of dollars with foreign banks.

European Currency Unit (ECU) An index of foreign ex-change consisting of about 10 European currencies, originallydevised in 1979.

European option An option contract that may be exercisedonly on the expiration date. An American option may be ex-ercised any time up to the expiration date.

Event study A statistical study that examines how the re-lease of information affects prices at a particular time.

Ex rights or ex dividend Phrases used to indicate that astock is selling without a recently declared right or dividend.The ex-rights or ex-dividend date is generally four businessdays before the date of record.

Exchange rate Price of one country’s currency for another’s.

Exclusionary self-tender The firm makes a tender offer fora given amount of its own stock while excluding targetedstockholders.

Ex-dividend date Date four business days before the dateof record for a security. An individual purchasing stock beforeits ex-dividend date will receive the current dividend.

Exercise price Price at which the holder of an option canbuy (in the case of a call option) or sell (in the case of a putoption) the underlying stock. Also called the striking price.

Exercising the option The act of buying or selling the un-derlying asset via the option contract.

Expectations hypothesis (of interest rates) Theory thatforward interest rates are unbiased estimates of expected fu-ture interest rates.

Expected return Average of possible returns weighted bytheir probability.

Expiration date Maturity date of an option.

Extension Voluntary arrangements to restructure a firm’sdebt, under which the payment date is postponed.

Extinguish Retire or pay off debt.

Face value The value of a bond that appears on its face.Also referred to as par value or principal.

Factor A financial institution that buys a firm’s accounts re-ceivables and collects the debt.

Factor model A model in which each stock’s return is gener-ated by common factors, called the systematic sources of risk.

Factoring Sale of a firm’s accounts receivable to a financialinstitution known as a factor.

Fair market value Amount at which common stock wouldchange hands between a willing buyer and a willing seller,both having knowledge of the relevant facts. Also called mar-ket price.

Feasible set Opportunity set.

Federal agency securities Securities issued by corpora-tions and agencies created by the U.S. government, such asthe Federal Home Loan Bank Board and GovernmentNational Mortgage Association (Ginnie Mae).

Field warehouse financing A form of inventory loan inwhich a public warehouse company acts as a control agent tosupervise the inventory for the lender.

922 Glossary

Ross−Westerfield−Jaffe: Corporate Finance, Sixth Edition

Back Matter Glossary 929© The McGraw−Hill Companies, 2002

Financial Accounting Standards Board (FASB) The gov-erning body in accounting.

Financial distress Events preceding and including bank-ruptcy, such as violation of loan contracts.

Financial distress costs Legal and administrative costs ofliquidation or reorganization (direct costs); an impaired abil-ity to do business and an incentive toward selfish strategiessuch as taking large risks, underinvesting, and milking theproperty (indirect costs).

Financial intermediaries Institutions that provide the mar-ket function of matching borrowers and lenders or traders.Financial institutions may be categorized as depository, con-tractual savings, and investment-type.

Financial lease A long-term noncancelable lease, generallyrequiring the lessee to pay all maintenance fees.

Financial leverage Extent to which a firm relies on debt.Financial leverage is measured by the ratio of long-term debtto long-term debt plus equity.

Financial markets Markets that deal with cash flows overtime, where the savings of lenders are allocated to the financ-ing needs of borrowers.

Financial requirements In the financial plan, financingarrangements that are necessary to meet the overall corporateobjective.

Financial risk The additional risk that the firm’s stockholdersbear when the firm is financed with debt as well as equity.