ANNUAL REPORT 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ANNUALREPORT

2016

“Our company is sustained by the strength of its relationships with all key stakeholders. These relationships are as strong as ever, because our stakeholders recognise and understand the value of our company.

Our stakeholders understand the temporary nature of the industry crisis. They recognise the stability and strength with which we are meeting all our obligations; and they see the same bright future that lies ahead.”

“Our company is sustained by the strength of its relationships with all key stakeholders. These relationships are as strong as ever, because our stakeholders recognise and understand the value of our company.

Our stakeholders understand the temporary nature of the industry crisis. They recognise the stability and strength with which we are meeting all our obligations; and they see the same bright future that lies ahead.”

HIS MAJESTY

SULTAN QABOOS BIN SAID

HIS MAJESTY

SULTAN QABOOS BIN SAID

CONTENTS

Renaissance Services SAOGP.O. Box 1676, P.C. 114, Muttrah, Sultanate of OmanTel.: +968 2479 6636 Fax: +968 2479 6639www.renaissance-oman.com

RENAISSANCEThe Renaissance Group is an Omani multinational listed on the Muscat Securities Market (MSM30) as “Renaissance Services SAOG”. The group contains two businesses. Topaz operates a modern and diverse fleet of 100 off-shore support vessels for the oil and gas sector, primarily located in the Caspian and MENA markets. The Topaz vision is to be the global local quality champion and top five OSV player, with profitability in the top quartile. Renaissance is an Omani company offering strategic facilities management solutions for businesses in a wide range of sectors and geographies. We provide contract services, IFM and run the Renaissance Village brand, which is our uniquely designed workforce accommodation solution. Clients include government, universities and hospitals, ports, industry, onshore and offshore hydrocarbon development, and the military.

The Renaissance vision is to deliver world-class services to a worldwide market.

Board of Directors 6

Financial Highlights 8

Chairman’s Report 10

Chief Executive’s Report 20

Auditors’ Report on Corporate Governance 31

Report on Corporate Governance 32

Auditors’ Report on Financial Statements 40

Financial Statements 46

VALUESSAFETY – HSE, no harm to people, no harm to the environment

SERVICE – customers really do come first, standards, performance, unique solutions

INTEGRITY – governance, honesty, ethics

EFFICIENCY – best in class competitiveness with world-class competition, performance

CARING – nurturing our people, family culture, helping communities

CONTENTS

Renaissance Services SAOGP.O. Box 1676, P.C. 114, Muttrah, Sultanate of OmanTel.: +968 2479 6636 Fax: +968 2479 6639www.renaissance-oman.com

RENAISSANCEThe Renaissance Group is an Omani multinational listed on the Muscat Securities Market (MSM30) as “Renaissance Services SAOG”. The group contains two businesses. Topaz operates a modern and diverse fleet of 100 off-shore support vessels for the oil and gas sector, primarily located in the Caspian and MENA markets. The Topaz vision is to be the global local quality champion and top five OSV player, with profitability in the top quartile. Renaissance is an Omani company offering strategic facilities management solutions for businesses in a wide range of sectors and geographies. We provide contract services, IFM and run the Renaissance Village brand, which is our uniquely designed workforce accommodation solution. Clients include government, universities and hospitals, ports, industry, onshore and offshore hydrocarbon development, and the military.

The Renaissance vision is to deliver world-class services to a worldwide market.

Board of Directors 6

Financial Highlights 8

Chairman’s Report 10

Chief Executive’s Report 20

Auditors’ Report on Corporate Governance 31

Report on Corporate Governance 32

Auditors’ Report on Financial Statements 40

Financial Statements 46

VALUESSAFETY – HSE, no harm to people, no harm to the environment

SERVICE – customers really do come first, standards, performance, unique solutions

INTEGRITY – governance, honesty, ethics

EFFICIENCY – best in class competitiveness with world-class competition, performance

CARING – nurturing our people, family culture, helping communities

BOARD OF DIRECTORS

A N N U A L R E P O R T 2 0 1 66

Colin RutherfordDirector

Saleh bin Nasser Al HabsiDirector

Sunder GeorgeDirector

Samir J FancyChairman

7A N N U A L R E P O R T 2 0 1 6

HH Sayyid Tarik bin Shabib bin TaimurDirector

Yeshwant C DesaiDirector

Ali bin Hassan SulaimanDeputy Chairman

USD Million

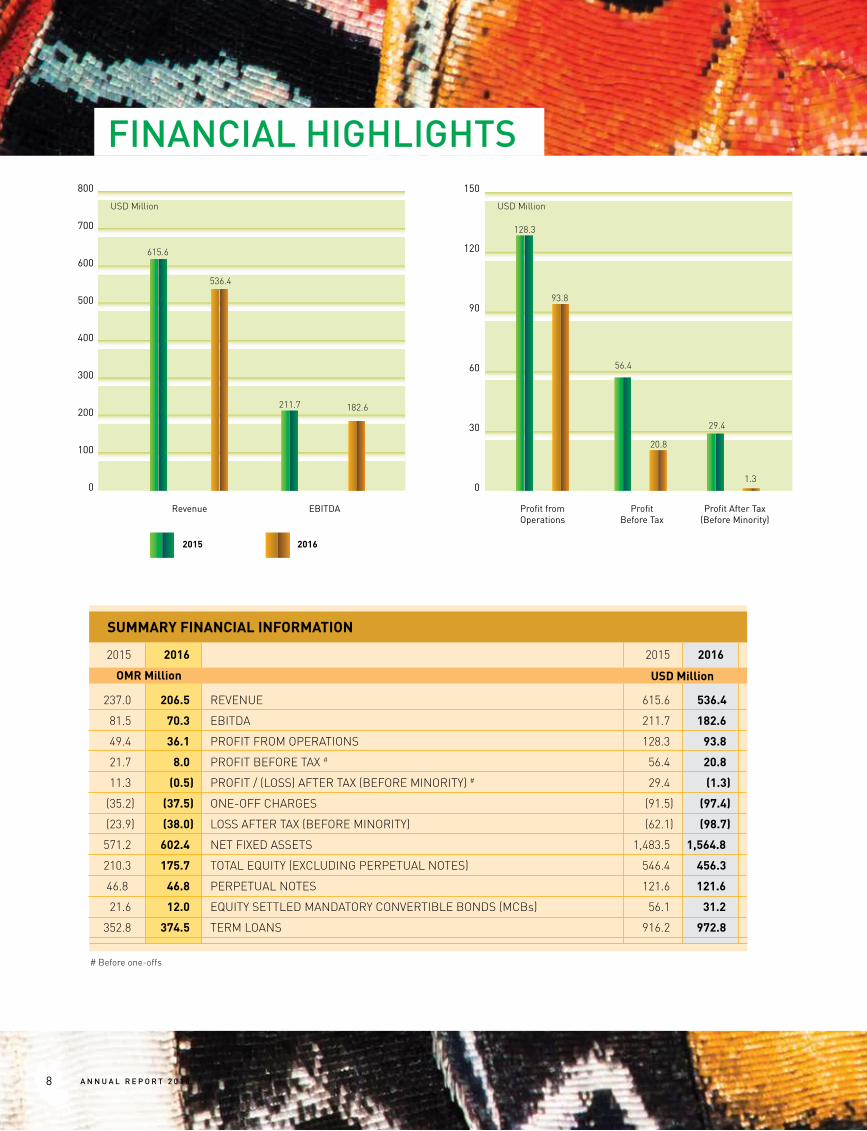

SUMMARY FINANCIAL INFORMATION

Revenue EBITDA

# Before one-offs

Profit fromOperations

ProfitBefore Tax

Profit After Tax(Before Minority)

USD Million USD Million

Gearing Total Liabilities/Net Worth

2.23

1.621.58

1.29

93.8

20.8

1.3

128.3

56.4

29.4

536.4

182.6

615.6

211.7

2015 2016 2015 2016

237.0 206.5 REVENUE 615.6 536.4

81.5 70.3 EBITDA 211.7 182.6

49.4 36.1 PROFIT FROM OPERATIONS 128.3 93.8

21.7 8.0 PROFIT BEFORE TAX # 56.4 20.8

11.3 (0.5) PROFIT / (LOSS) AFTER TAX (BEFORE MINORITY) # 29.4 (1.3)

(35.2) (37.5) ONE-OFF CHARGES (91.5) (97.4)

(23.9) (38.0) LOSS AFTER TAX (BEFORE MINORITY) (62.1) (98.7)

571.2 602.4 NET FIXED ASSETS 1,483.5 1,564.8

210.3 175.7 TOTAL EQUITY (EXCLUDING PERPETUAL NOTES) 546.4 456.3

46.8 46.8 PERPETUAL NOTES 121.6 121.6

21.6 12.0 EQUITY SETTLED MANDATORY CONVERTIBLE BONDS (MCBs) 56.1 31.2

352.8 374.5 TERM LOANS 916.2 972.8

OMR Million

20162015

0

100

200

300

400

500

600

700

800

0

30

60

90

120

150

0.0

0.5

1.0

1.5

2.0

2.5

Ratio

SIGNIFICANT RATIOS

2015 2016

GEARING* 1.29 1.62

TOTAL LIABILITIES/NET WORTH* 1.58 2.23

RETURN ON CAPITAL EMPLOYED (%) # 5.69 4.13

* MCBs are considered as part of equity# Continuing operations before one-offs

FINANCIAL HIGHLIGHTS

A N N U A L R E P O R T 2 0 1 68

USD Million

SUMMARY FINANCIAL INFORMATION

Revenue EBITDA

# Before one-offs

Profit fromOperations

ProfitBefore Tax

Profit After Tax(Before Minority)

USD Million USD Million

Gearing Total Liabilities/Net Worth

2.23

1.621.58

1.29

93.8

20.8

1.3

128.3

56.4

29.4

536.4

182.6

615.6

211.7

2015 2016 2015 2016

237.0 206.5 REVENUE 615.6 536.4

81.5 70.3 EBITDA 211.7 182.6

49.4 36.1 PROFIT FROM OPERATIONS 128.3 93.8

21.7 8.0 PROFIT BEFORE TAX # 56.4 20.8

11.3 (0.5) PROFIT / (LOSS) AFTER TAX (BEFORE MINORITY) # 29.4 (1.3)

(35.2) (37.5) ONE-OFF CHARGES (91.5) (97.4)

(23.9) (38.0) LOSS AFTER TAX (BEFORE MINORITY) (62.1) (98.7)

571.2 602.4 NET FIXED ASSETS 1,483.5 1,564.8

210.3 175.7 TOTAL EQUITY (EXCLUDING PERPETUAL NOTES) 546.4 456.3

46.8 46.8 PERPETUAL NOTES 121.6 121.6

21.6 12.0 EQUITY SETTLED MANDATORY CONVERTIBLE BONDS (MCBs) 56.1 31.2

352.8 374.5 TERM LOANS 916.2 972.8

OMR Million

20162015

0

100

200

300

400

500

600

700

800

0

30

60

90

120

150

0.0

0.5

1.0

1.5

2.0

2.5

Ratio

SIGNIFICANT RATIOS

2015 2016

GEARING* 1.29 1.62

TOTAL LIABILITIES/NET WORTH* 1.58 2.23

RETURN ON CAPITAL EMPLOYED (%) # 5.69 4.13

* MCBs are considered as part of equity# Continuing operations before one-offs

9A N N U A L R E P O R T 2 0 1 6

CHAIRMAN’SREPORT

A N N U A L R E P O R T 2 0 1 610

OverviewOn behalf of the Board of Directors, I present the audited accounts for Renaissance Services SAOG, for the financial period ending 31 December 2016.

I want to focus on four subjects:

Impairment: The impact of impairment on our 2015 and 2016 results.

Stability: The underlying financial strength of the business to steer the company safely through 2017 meeting all our financial obligations.

Relationships: The sustaining strength of our relationships with all stakeholders.

Future: The company’s USD 1.6 billion contract backlog and two major projects driving growth with positive impact from 2018.

This will explain the losses of 2015 and 2016. It will describe the prudent path we are taking through 2017; and it will confirm the prospect of why we look forward to a positive future.

Financial performance Rial Million USD Million

2016 2015 2016 2015

Continuing Operations (before one-off charges)

Revenue 206.5 237.0 536.4 615.6

EBITDA 70.3 81.5 182.6 211.7

Operating profit 36.1 49.4 93.8 128.3

Net profit/(loss) after tax from continuing operations (before one-off charges) (0.5) 11.3 (1.3) 29.4

One-off charges (Note 1) (37.5) (35.2) (97.4) (91.4)

Net loss after tax from continuing operations (38.0) (23.9) (98.7) (62.1)

Discontinued operations

Loss from discontinued operations (Note 2) (1.2) (6.1) (3.1) (15.8)

Net loss after tax for the year (39.2) (30.0) (101.8) (77.9)

Net loss for the year after minority interest (42.1) (34.8) (109.4) (90.4)

11A N N U A L R E P O R T 2 0 1 6

Note 1 – Details of one-off charges are as follows: The following one-off charges for 2016 relate to Topaz.

Rial Million USD Million

2016 2015 2016 2015

Provision for impairment of vessels (net of tax adjustment) (36.5) (27.3) (94.8) (70.9)

Increase in derivative liability (1.0) (4.7) (2.6) (12.2)

Unamortised arrangement fees write-off - (3.2) - (8.3)

Total (37.5) (35.2) (97.4) (91.4)

Note 2 - Loss from discontinued / discontinuing operations

is as follows:

Rial Million USD Million

2016 2015 2016 2015

Marine Engineering Division

(1.0) (3.2) (2.6) (8.3)

RS Angola - (2.9) - (7.5)

National Hospitality Institute

(0.2) - (0.5) -

Total (1.2) (6.1) (3.1) (15.8)

The global Offshore Support Vessel (OSV) Company

TOPAZ (BEFORE ONE-OFFS)

Rial Million USD Million

2016 2015 2016 2015

Revenue 108.7 139.5 282.3 362.3

Operating profit 27.2 39.9 70.6 103.6

Net profit/(loss) after tax (2.8) 8.0 (7.3) 20.8

Net loss after minority interest (11.4) (0.6) (29.7) (1.6)

Topaz is directly exposed to the ongoing oil price crisis that has adversely affected the entire OSV industry. But the company is sustained by long-term stable contracts, which have been further extended; and has won major new contracts that ensure a significant upturn in performance from 2018.

Our Services Business: Integrated Facilities Management (IFM); Soft FM; Hard FM; and Accommodation Solutions.

A N N U A L R E P O R T 2 0 1 612

RENAISSANCE

Rial Million USD Million

2016 2015 2016 2015

Revenue 97.8 97.6 254.0 253.5

Operating profit 9.1 9.4 23.6 24.4

Net profit after tax 6.0 5.4 15.6 14.0

Net profit after minority interest 6.1 5.4 15.8 14.0

Our services business has maintained top line and improved bottom line. The company’s strategy is to diversify the range of its services, sectors and geography. While this reduces exposure to the oil & gas industry, the sector remains the dominant player in our portfolio. So this business is also not immune to the oil price crisis and the significant increase in cost of doing business in our dominant home market of Oman. The company is focused on growth and efficiency to mitigate and out-pace further cost impacts to come.

IMPAIRMENT

Oil, like all commodities, is cyclical. Any boom or bust cycle in oil price directly impacts the offshore support vessel (OSV) industry. The current oil price crisis that started with steep decline in 2014 has stabilised in recent weeks following production cutback agreement between OPEC and non-OPEC producers. While a current oil price

above USD 50 offers some respite, it cannot change the negative impact on OSV fleet owners and operators over the last two years. While Topaz has fared better than its peers, it has not been immune.

The global OSV fleet numbers about 3,500 vessels, and today about 1,300 of those vessels are laid up and out of work. This is because oil and gas producers have cut back sharply on capex for exploration and construction, while the industry adjusts to a new price range per barrel. Topaz has a fleet of 100 vessels, and today 11 of those are out of work, while many others are competing for short-term contracts in a very difficult spot market. While this is better than the OSV industry as a whole, it nevertheless has a direct negative impact on revenue and profit.

Topaz is able to mitigate the impact due to its largely young fleet, focused primarily in longer-term contracts in the production cycle of the oil industry. But vessels on shorter-term contracts and under-utilised assets are affected.

The crisis has wiped billions of dollars in value of the global OSV fleet; and some of the older tonnage may never return to the industry. Topaz is not in that situation, but for the second year running we had to make a material impairment. Following a one-off charge of Rials 27.3 million (USD 70.9 million) in 2015, we have taken a further one-off charge of Rials 36.5 million (USD 94.8 million) in 2016.

13A N N U A L R E P O R T 2 0 1 6

While we do not take these charges lightly, we draw some solace from being in a far better position than most industry peers. While the loss of value hurts, it is not a cash loss and Topaz EBITDA achievement of USD 145 million underwrites the strength and allows the company to meet all of its financial commitments throughout the prolonged crisis.

This particular bust cycle in oil price has had unprecedented negative impact on the industry – more so than even lower price cycles. This is because when the oil price ranged from USD 100-147 a barrel, the industry embarked on major expansion and development of previously uneconomic oilfields. Readjustment has been painful.

We expect 2017 to be another challenging year. As oil price stabilises, we expect vessel utilisation to improve paving the way for improvement in rates. So whilst we feel further major impairment in 2017 unlikely, we cannot rule out any impact at this stage. But we have reason for cautious optimism while markets reprice oil for the future. The underlying reality is that oil supplies shall have to meet increasing demand at the right price over the years ahead.

STABILITY

The company has been sustained throughout this crisis by a solid foundation of stability: A strong balance sheet; sustainable healthy cash flows; long-term financing arrangements matched with our long-term asset profile; Rials 30 million cash in the balance sheet; fully funded capex programmes; and well managed low counter-party risk.

Central to this financial stability has been the actions taken in anticipation of strong headwinds arising from declining oil prices. The company has in place long-term financial arrangements aligned with our cash flows, our requirements and our obligations. This includes long-term facilities at competitive rates.

All our capex obligations are fully funded, either through equity and loans in place, or through inherent contract terms. This includes the entire capex requirement as we invest for growth in the TCO Project for Topaz and the Renaissance Village Duqm.

While getting paid is a rising concern in the market place, we have been able to sustain the collection of our receivables through the quality and stability of our client-base.

Chairman’s Report

A N N U A L R E P O R T 2 0 1 614

During the year, the company has successfully concluded its negotiations with Standard Chartered Private Equity regarding 9.8% shares held by them in Topaz. The new structure reduces the guaranteed IRR from existing 12% to 8% and extends the deadline within which the liquidity event may occur from 3 to 5/6 years, in return for granting an additional 3.7% equity position in Topaz. This outcome reflects the solid partnership and collaboration between the shareholders allowing the group to tide over the business cycle and protect value in the company.

RELATIONSHIPS

The company is also sustained by the strength of its relationships with all key stakeholders: our clients and customers; our shareholders and bondholders; our bankers and other financial institutions; our professional advisors – legal, auditing, commercial, industry; government, official agencies and institutions; suppliers and service providers; the communities in which we serve; and, of course, our own people.

Our relationships remain as strong as ever, because all of these people recognise and understand the value of our company and our two principal businesses. They understand the temporary nature of the industry crisis; they recognise the stability and strength with which we are meeting all our contractual, legal and financial obligations; and they see the same bright future that lies ahead.

On behalf of the Board of Directors I would like to record our appreciation for all these relationships and their confidence and belief in our company.

FUTURE

We have been sailing under dark skies for these last two years; but we have always had a clear eye on a bright future. This is not based on unfounded optimism; but rather on the relevance and potential of the businesses and markets in which we operate – backed up by a contract backlog of USD 1.6 billion. We also have two major flagship projects in place where the full benefits shall start to flow in 2018.

15A N N U A L R E P O R T 2 0 1 6

As reported earlier this year, Topaz has secured a contract to supply and operate vessels for the Tengizchevroil (TCO) project. The total TCO contract is worth in excess of USD 550 million to Topaz over a minimum contract period of three years commencing in Q2 2018.

This important contract win has opened many opportunities for Topaz with formidable customers such as Chevron and ExxonMobil, and has opened up strategic paths for achieving the company strategy of a more diversified marine platform over the longer term.

Further opportunity lurks as this highly fragmented industry consolidates. The Topaz OSV fleet is poised to be one of the strongest out of this crisis: modern, relevant, efficient, fit and ready to serve its clients. Where relevant to our strategy the right opportunities will be thoughtfully considered. Value abounds, but risk mitigation has to be the key to any inorganic action in this very difficult environment. The company remains vigilant to opportunity within these parameters.

On 1 February 2017, we and our partners opened the first phase of the Renaissance Village Duqm. The 16,000-bed facility for accommodating workforces in the SEZAD, shall be fully open in April 2017. Of course, during 2017 we expect a slower and gradual occupancy build-up. Whereas in 2018 we anticipate high occupancy as major Duqm projects get underway. Like the PAC

Projects in Oman’s oilfields, Renaissance Village Duqm is a world-class facility that allows SEZAD, Duqm and Oman to show the world how to look after workforces at high standards, but affordable competitive rates through the economies of scale. Renaissance Village facilities already generate sustainable annual revenues > USD 75 million, and as Duqm occupancy grows into 2018, we can expect the brand to at least double that.

MR. YESHWANT C. DESAI

Mr. Yeshwant C. Desai has advised that he will retire at the end of his current term and will not offer himself for re-election at the Annual General Meeting (AGM).

He has been a Director of the Board of Renaissance since 2001 and is currently the Chairman of the Audit & Internal Controls Committee. He has also served as the Chairman of the Compensation Committee in the past.

On behalf of the Board and Management, I express our deepest appreciation for the exceptional efforts Mr. Desai extended to the company over the past 16 years, guiding the group’s growth and mentoring its Board with his wisdom and experience.

OUTLOOK

Of course, there shall be more challenging times in 2017 and it will be another difficult year. There is always a time lag between improving oil price and new investment in the industry. So we remain in our stable and resilient mode for this year. However we are already thinking and acting ahead of the curve of current reality. Our secured growth contracts and projects provide us a future to look forward to in 2018 and beyond.

TRIBUTE

On behalf of the Board of Directors, I would like to express our sincere gratitude to His Majesty Sultan Qaboos bin Said for his leadership and support to create a business environment that enables our company to thrive and prosper in our home market, and compete with the very best in markets abroad.

Samir J. FancyChairman

Chairman’s Report

A N N U A L R E P O R T 2 0 1 616

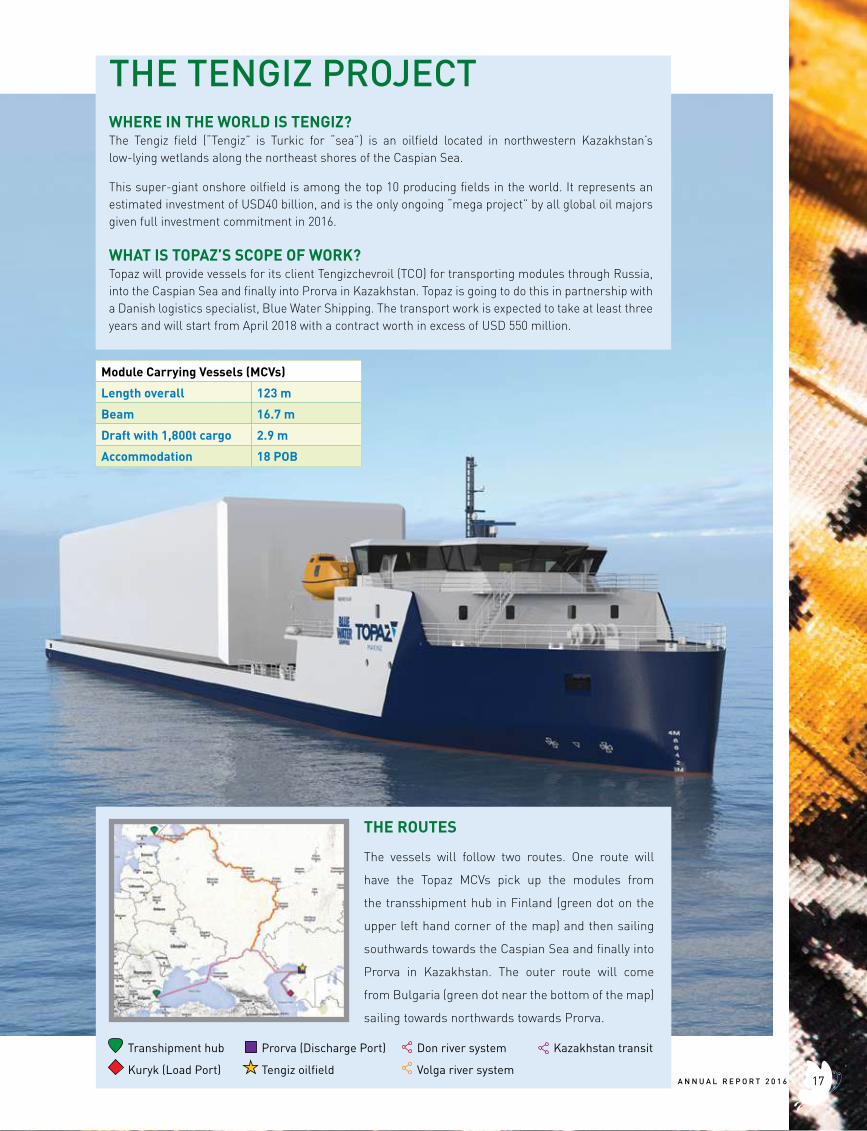

THE ROUTES

The vessels will follow two routes. One route will

have the Topaz MCVs pick up the modules from

the transshipment hub in Finland (green dot on the

upper left hand corner of the map) and then sailing

southwards towards the Caspian Sea and finally into

Prorva in Kazakhstan. The outer route will come

from Bulgaria (green dot near the bottom of the map)

sailing towards northwards towards Prorva.

Transhipment hub

Kuryk (Load Port)

Prorva (Discharge Port)

Tengiz oilfield

Don river system

Volga river system

Kazakhstan transit

WHERE IN THE WORLD IS TENGIZ?The Tengiz field (“Tengiz” is Turkic for “sea”) is an oilfield located in northwestern Kazakhstan’s low-lying wetlands along the northeast shores of the Caspian Sea.

This super-giant onshore oilfield is among the top 10 producing fields in the world. It represents an estimated investment of USD40 billion, and is the only ongoing “mega project” by all global oil majors given full investment commitment in 2016.

WHAT IS TOPAZ’S SCOPE OF WORK?Topaz will provide vessels for its client Tengizchevroil (TCO) for transporting modules through Russia, into the Caspian Sea and finally into Prorva in Kazakhstan. Topaz is going to do this in partnership with a Danish logistics specialist, Blue Water Shipping. The transport work is expected to take at least three years and will start from April 2018 with a contract worth in excess of USD 550 million.

Module Carrying Vessels (MCVs)

Length overall 123 m

Beam 16.7 m

Draft with 1,800t cargo 2.9 m

Accommodation 18 POB

THE TENGIZ PROJECT

17A N N U A L R E P O R T 2 0 1 6

RENAISSANCE FACILITIES MANAGEMENT SERVICES

A N N U A L R E P O R T 2 0 1 618

19A N N U A L R E P O R T 2 0 1 6

CHIEFEXECUTIVE’SREPORT

A N N U A L R E P O R T 2 0 1 620

CEO Report 2016We expect the challenges of 2016 to continue in 2017. Through the coming year we plan prudent efficiency measures and new growth initiatives to improve upon 2016 performance. But we can only forecast more significant improvements in 2018 and 2019; arising principally from two innovative game changing drivers: growth in our strategic investment of RENAISSANCE VILLAGE DUQM in RENAISSANCE; and by realisation of the USD550 million Tengizchevroil (TCO) contract in TOPAZ.

RS GROUP Consolidated

Rial million2015

Audited2016

Audited

Revenue 237.0 206.5

EBITDA 81.5 70.3

PAT (30.0) (39.2)

PATMI (34.8) (42.1)

The group’s consolidated loss performance has been affected by one-off impairment charges on vessels in the Topaz offshore support vessel (OSV) fleet of Rials 36.5 million; following similar charges of Rials 27.3 million last year.

TOPAZTopaz performance excluding one-off charges

Rial million2015

Audited2016

Audited

Revenue 139.5 108.7

Operating Profit 39.9 27.2

PAT 8.0 (2.8)

PATMI (0.6) (11.4)

In recent years the group has restructured, with Topaz operating as an independently managed entity with its own governance structure. As such, Renaissance Board Members and Executive Management carry out fiduciary responsibilities by, with and through our respective roles on the subsidiary Topaz Board and Committees. Topaz Executive Management also attend all Renaissance Board meetings and Audit Committee meetings, to ensure a transparent flow of information, guidance and direction.

From the Renaissance perspective, we continue to offer full support to the Topaz Executive Management Team and appreciate its achievements throughout the oil price crisis that has affected the global OSV industry over the past two years. In spite of the crisis, Topaz continues to out-perform its peers. Topaz has renewed and extended all major long-term contracts, that provide stability and sustainable cash-flows to meet all

21A N N U A L R E P O R T 2 0 1 6

Chief Executive’s Report

the company’s obligations; and has won an innovative substantial contract with Tengizchevroil (TCO) that ensures additional positive growth for the company from 2018.

For further details on this and all other Topaz matters, my colleague the Topaz CEO, produces a detailed report within the Topaz Annual Report, which may be read via the link on the Renaissance website [Link: http://www.topazworld.com/en/investors/reports-presentations]

RENAISSANCE

Rial million 2015Audited

2016Audited

Revenue 97.6 97.8

Operating Profit 9.4 9.1

PAT 5.4 6.0

PATMI 5.4 6.1

While we have seen some improved bottom line performance in 2016 in the RENAISSANCE services businesses, this has been tempered by reduced revenue in the oil & gas sector as the industry adjusts to the re-pricing of oil. Also, the cost of doing business has increased in the oil-reliant economies in which we operate; including our dominant home market of Oman.

For 2017 we are working to increase revenues with targeted new business in contract services, increasing occupancy in Renaissance Villages PDO, a full year of the EMIRATES TASTE business in UAE, and opening the new RENAISSANCE VILLAGE DUQM. This shall be partially offset by a downturn of revenue in Norway, where a number of rigs are laid up, reducing demand for our services.

If we realise our targets for increased revenue in 2017, we do not expect this to be matched by a corresponding ratio increase in PAT. We anticipate increased profitability across all businesses except Norway; and the RENAISSANCE VILLAGE DUQM has planned P&L loss in a year of occupancy build-up, before making an anticipated significant growth contribution in 2018.

In 2017 we anticipate further increases in cost of doing business in our home market of Oman. The impact of mandatory 3% increment for Omani employees, the change in visa fees for expats, and the proposed 3% increase in corporate tax rate to 15%, shall impact costs by Rials 700K in 2017. We may expect other increases from other government departments that charge for a service or administrative process; as well as further reduction in subsidies for utilities and fuel, as the government seeks to increase revenue and reduce costs. We also anticipate an inflationary impact on cost of food commodities this year.

In addition to these external cost pressures, we have also planned an increase in employment costs as we seek to strengthen and enlarge the leadership team, at various levels, for growth and succession; with additional resources in HR, Operations and Business Development.

Increased costs shall of course temper our growth trajectory in what we see as a transition year, while the RENAISSANCE VILLAGE DUQM grows to full-scale operations. However, we remain confident in our ability to grow the business in these difficult times. The same cost pressures that challenge us, also afflict our clients and potential clients. RENAISSANCE offers services that have a proven track record of maintaining or improving standards while driving down costs and creating efficiencies for our clients. In these difficult times our role and potential is significant in the lives of our customer base.

A N N U A L R E P O R T 2 0 1 622

SUSTAINABILITYRENAISSANCE commitment to sustainability underwrites our values and provides the platform of stability and purpose upon which we may drive continuous improvement in service, standards, performance, growth and value.

For further details on our progress and plans in our ENVIRONMENT, SOCIAL RESPONSIBILITY, GOVERNANCE (ESG) agenda and our commitment to QHSE and IN-COUNTRY VALUE (ICV), please refer to our separate Sustainability Report. [Link: http://www.renaissanceoman.com/en/sustainability/]

RENAISSANCE VILLAGE DUQMA top priority for the company in 2017 is opening our flagship RENAISSANCE VILLAGE DUQM project and populating it with clients and customers from Duqm’s permanent workforces and temporary project workforces. The facility is also an ideal solution for short-term business visitors or work teams requiring accommodation for single night or short-term project durations.

This 16,000-bed facility fulfils SEZAD’s and Oman’s vision to show the world how to look after workforces well, without compromising competitiveness of projects. Staying at the Duqm facility is more cost-effective than building short-term Temporary Portacabin Accommodation for the duration of a project. This is achieved by the longevity, permanence and economy of scale of our Duqm facility.

Visibility for high occupancy is positive from 2018, when some major projects get underway. So the challenge is to attract maximum possible occupancy during the build-up phase of 2017. We plan to do this, not just by the compelling imperative of the economic argument, but by the quality of services to our clients and the customers who stay with us. We offer a lifestyle, not a basic camp experience – but at the same, or lesser, cost.

More details on the RENAISSANCE VILLAGE DUQM offering may be seen at the following link: [Link: http://www.duqmvillage.com/duqm.html]

STRATEGY IMPLEMENTATIONTo achieve or exceed our plans, our strategy remains unchanged.

To continuously strengthen our capability, reputation and delivery of service solutions in the following categories:

SOFT FM: Contract Services

HARD FM: O&M

IFM: Turnkey solutions for clients’ non-core activities (but uniquely, avoiding margins on margins, due to our ability to provide most of the Soft and Hard FM outsource solutions in-house)

ACCOMMODATION SOLUTIONS: Renaissance Villages (formerly PAC) – workforce, military, student and other turnkey accommodation solutions

To grow through diversifying the spread of services, sectors and geographies in which we operate.

To deliver superior customer experiences through our operating mantra: SAFE, EFFICIENT, GREEN, LOCAL.

So far our major progress remains concentrated in our traditional core competencies of SOFT FM Contract Services and ACCOMMODATION SOLUTIONS with the Renaissance Village brand. We have had success in IFM with significant contracts with BP Khazzan and Al Mouj. We continue to seek greater opportunity as we demonstrate and strengthen our capabilities in both IFM and HARD FM O&M.

While we are seeing slow but gradual progress in diversification of services and sectors; we have had only limited success in geographical expansion through the small, but strategically important, acquisition of EMIRATES TASTE in Abu Dhabi, UAE. The integration of this new acquisition continues in 2017 as an important focus to ensure the business provides a platform for further growth.

23A N N U A L R E P O R T 2 0 1 6

In 2017 we anticipate 85% of Revenue and 87% of PAT to come from Oman. A number that is likely to grow in subsequent years with higher occupancy growth in RENAISSANCE VILLAGE DUQM. So, we are directing more focus and resources to ensure greater geographical expansion in neighbouring markets.

We continue to work at growing our HARD FM capability and building on our breakthrough into services in the Utilities sector. We have been competing for major waste management opportunities, in JV with international expertise, but so far without success. We still believe this is a potential growth area for the company.

While we would have wished to have greater success in our diversification efforts, we shall continue to vigorously pursue opportunity in our traditional areas of competence. What we have achieved is the establishment of an IFM track record, and we are now pre-qualified and actively bidding on a much larger stage of IFM and HARD FM opportunities. We are learning lessons from each new diversification effort and experience; and these shall translate into new success in time.

STRATEGIES FOR GROWTHWhile we have plans and initiatives in play for all aspects of our business, it is appropriate we provide some headline comments on our strategies for growth within the context of our overall strategy.

Growth through contract tendering

This is what improves our ROE as pure services business requires minimum capital investment, when we provide the services within client-owned facilities. Margins are usually very tight in this type of business – and this is a factor across all GCC markets. We have identified some specific major tender targets for 2017. If successful, there would be some positive impact in 2017, with full benefit flowing into the years that follow.

Growth through supplementary services

In each of our contracts and in our Renaissance Villages, we make every effort to provide other supplementary services either to the client or the individual customers, within the confines of the facility. This enhances the offering to our customer-base as well as bringing increased revenue to our business.

Chief Executive’s Report

A N N U A L R E P O R T 2 0 1 624

Growth through value innovation

One example of value innovation is our ACCOMMODATION SOLUTIONS in the form of the Renaissance Village brand. These deliver higher standards at lower costs through economies of scale. But an independent survey conducted by Shell some years ago also proved that these permanent facilities deliver additional tangible and intangible value, including: less consumption of water and electricity through quality of permanent infrastructure; better safety performance and lower downtime of absence through sickness.

We have Renaissance Villages which we own 100% in the oilfields; and RENAISSANCE VILLAGE DUQM which we own 51% with valued strategic partners investing in the balance 49%.

We are developing a win-win formula for future initiatives where up to 100% of the property (PROPCO) may be owned by investors; while securing longevity for RENAISSANCE as the operator (OPCO) in exchange for our intellectual property in developing the concept from design to operation.

We are also working on developing the thinking of some clients in terms of how they outsource their services in packaged cyclical tendering for individual services; rather than considering the full IFM cost-efficiency approach. In this regard, we are uniquely placed to offer solutions due to our ability to deliver at both the IFM level and self-perform at the SOFT & HARD FM levels; so avoiding margins on margins for our clients.

We are also looking at how we may innovate the delivery of some of our services; migrating from physical energy (people) to mechanical energy (plant, equipment and technology) to drive both standards and efficiency; and upgrade the attractiveness of jobs for Omanis.

Growth through investment

Of course some of the accommodation projects shall require investment for growth. We are looking at potential expansion of our RENAISSANCE VILLAGE DUQM in the years ahead, as well as a complimentary Beach Club Facility.

Our investment in Warehousing, Cold Storage and Logistics capability in our Central Stores in Mabela is already paying dividends in driving down our costs, increasing our buying-power and enhancing our logistics and supplies offering. The investment in Warehousing and Cold Storage in Duqm is also intended to create scale and value in this capability in the future.

Growth through merger & acquisition (M&A)

This same approach is taken in the prospect of achieving further growth through merger and/or acquisition, beyond the recent EMIRATES TASTE acquisition. Again, we continue to react to opportunities when they arise; but we do not have any specific M&A target in view at this time.

Growth through diversification

This is of course an integral part of the overall strategy (to diversify our services, our sectors and our geography). We are continuing to compete for utility services, waste management and HARD FM opportunities. Oil & Gas, Healthcare, Education, Defence and Industry are sectors in which we excel; and these shall remain a core part of our growing client base. We are exploring in what ways we may provide more services and add greater value in other key sectors, including: Ports & Airports; Logistics; Manufacturing; Tourism; and Agriculture & Fisheries.

ORGANISATION CAPABILITY TO EXECUTE THE STRATEGYA strategic HR focus is essential to ensure we have the leadership and skill sets at every level of the organisation to execute our strategy. We are seeking to make some important new appointments in 2017, aligned with our diversification and growth ambitions.

In addition to our ISO 9001, HACCP and ISO 22000 certification, for 2017 we have planned ISO 14001 certification for our Environment impact processes and OHSAS 18001 to further strengthen our Safety system.

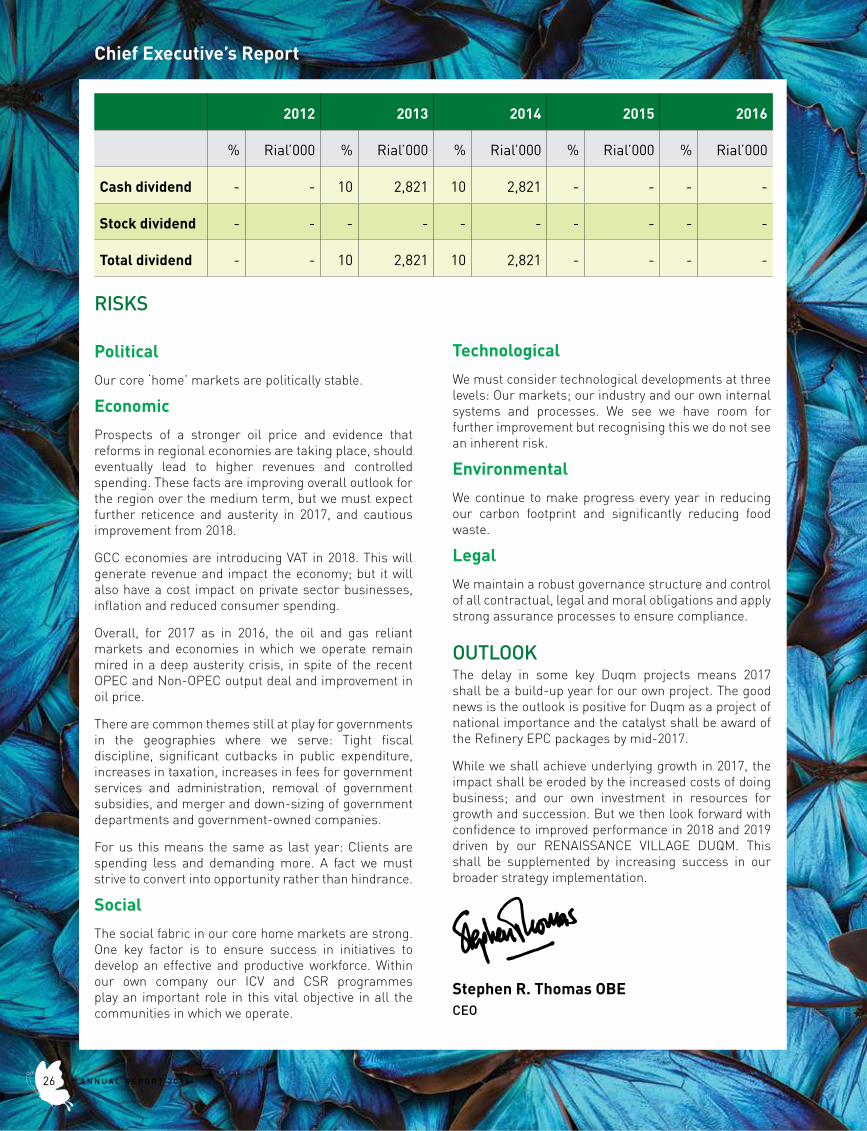

DIVIDEND RECORDThe Renaissance Dividend Policy is based on the proposition that cash is returned to shareholders in the form of higher dividend pay-outs when there are no credible value creating opportunities to invest in the business.

In 2016 our Board is proposing no dividend, as it is important to maintain the cash position of the company through this period of uncertainty in oil markets. We look forward to restoring a practice of regular dividend payments, as soon as practicable.

25A N N U A L R E P O R T 2 0 1 6

Chief Executive’s Report

2012 2013 2014 2015 2016

% Rial’000 % Rial’000 % Rial’000 % Rial’000 % Rial’000

Cash dividend - - 10 2,821 10 2,821 - - - -

Stock dividend - - - - - - - - - -

Total dividend - - 10 2,821 10 2,821 - - - -

RISKS

Political

Our core ‘home’ markets are politically stable.

Economic

Prospects of a stronger oil price and evidence that reforms in regional economies are taking place, should eventually lead to higher revenues and controlled spending. These facts are improving overall outlook for the region over the medium term, but we must expect further reticence and austerity in 2017, and cautious improvement from 2018.

GCC economies are introducing VAT in 2018. This will generate revenue and impact the economy; but it will also have a cost impact on private sector businesses, inflation and reduced consumer spending.

Overall, for 2017 as in 2016, the oil and gas reliant markets and economies in which we operate remain mired in a deep austerity crisis, in spite of the recent OPEC and Non-OPEC output deal and improvement in oil price.

There are common themes still at play for governments in the geographies where we serve: Tight fiscal discipline, significant cutbacks in public expenditure, increases in taxation, increases in fees for government services and administration, removal of government subsidies, and merger and down-sizing of government departments and government-owned companies.

For us this means the same as last year: Clients are spending less and demanding more. A fact we must strive to convert into opportunity rather than hindrance.

Social

The social fabric in our core home markets are strong. One key factor is to ensure success in initiatives to develop an effective and productive workforce. Within our own company our ICV and CSR programmes play an important role in this vital objective in all the communities in which we operate.

Technological

We must consider technological developments at three levels: Our markets; our industry and our own internal systems and processes. We see we have room for further improvement but recognising this we do not see an inherent risk.

Environmental

We continue to make progress every year in reducing our carbon footprint and significantly reducing food waste.

Legal

We maintain a robust governance structure and control of all contractual, legal and moral obligations and apply strong assurance processes to ensure compliance.

OUTLOOKThe delay in some key Duqm projects means 2017 shall be a build-up year for our own project. The good news is the outlook is positive for Duqm as a project of national importance and the catalyst shall be award of the Refinery EPC packages by mid-2017.

While we shall achieve underlying growth in 2017, the impact shall be eroded by the increased costs of doing business; and our own investment in resources for growth and succession. But we then look forward with confidence to improved performance in 2018 and 2019 driven by our RENAISSANCE VILLAGE DUQM. This shall be supplemented by increasing success in our broader strategy implementation.

Stephen R. Thomas OBECEO

A N N U A L R E P O R T 2 0 1 626

CEO’s Message – Sustainability Report 2016

RENAISSANCE commitment to sustainability underwrites our values and provides the platform of stability and purpose upon which we may drive continuous improvement in service, standards, performance, growth and value.

In this report we aim to provide our stakeholders with a transparent overview of our progress and plans in our ENVIRONMENT, SOCIAL RESPONSIBILITY, GOVERNANCE (ESG) agenda; as well as our absolute commitment to QHSE and IN-COUNTRY VALUE (ICV) as intrinsic to our culture and way of doing business.

We have again asked the EY team to assist us in preparing this report, to ensure an independent view of our performance and how we stand up to measurement within the GRI framework.

People, Planet and Profits are not mutually exclusive – at RENAISSANCE we know they can and must be mutually beneficial, complementary and inter-dependent.

Stephen R. Thomas OBECEO

27A N N U A L R E P O R T 2 0 1 6

RENAISSANCE VILLAGE DUQM

A N N U A L R E P O R T 2 0 1 628

29A N N U A L R E P O R T 2 0 1 6

Sohar International Urea and Chemical Industries

Renaissance Customers include the following

Chief Executive’s Report

A N N U A L R E P O R T 2 0 1 630

31A N N U A L R E P O R T 2 0 1 6

REPORT ON CORPORATE GOVERNANCECorporate governance is an internal system encompassing policies, processes and people, which serves the needs of shareholders and other stakeholders, by directing and controlling management activities with good business savvy, objectivity, accountability and integrity. Sound corporate governance is not only about structure and clarity in management and areas of responsibility, but it also encourages good transparency so that shareholders can understand and monitor the development of the company.

The Board and the Management of Renaissance Services SAOG (the “Company”) are committed to adopt the best practices of corporate governance that promote ethical standards and individual integrity. The Company will continue to focus on its resources, strengths and strategies for creating, safeguarding and enhancing shareholders’ value while at the same time protecting the interests of its stakeholders.

This report illustrates how the Principles of Corporate Governance and the provisions of the Code of Corporate Governance, set out in the Capital Market Authority’s (CMA) Code of Corporate Governance for companies listed on the Muscat Securities Market (MSM), and the Provisions for Disclosure stipulated in the Executive Regulations of the Capital Market Law, are adhered to by the Company.

The Company believes that the Code prescribes a minimum framework for governance of a business. The Company’s philosophy is to develop this minimum framework and institutionalise its principles as an ingredient of its corporate culture. This will lay the foundation for further development of a model of governance with superior governance practices, which are vital for growing a successful business. The Company recognises that transparency, disclosure, financial controls and accountability are the pillars of any good system of corporate governance.

In accordance with the Provision for Disclosure stipulated in the Executive Regulation of the Capital Market Law, Deloitte & Touche (M.E.) has issued a separate Factual Findings Report on the Company’s Corporate Governance Report for the year ended 31 December 2016.

1. New Code of Corporate GovernanceThe Capital Market Authority circulated a new Code of Corporate Governance (the ‘Code’) for public joint stock companies, which came into force and effect as of July 2016. The new Code replaced the 2003 Code of Corporate Governance for Public Listed Companies (‘the Old Code’).

The Company has applied the principles of the Code

and is fully compliant with its provisions.

Since the introduction of the Code, the Company has implemented the following provisions including but not limited to:

- Updated existing/developed new company policies to ensure compliance with the Code;

- Renamed the Board Sub-Committees;- Pre-approved all related party transactions in the

ordinary course of business by the Audit and Internal Controls Committee and Board;

- Complied with the provisions of the Code relating to conduct of Board meetings;

- Measured the performance of the Board Sub-committees in 2016;

- Initiated the process of appointing an independent consultant to develop criteria for measuring the performance of the Board and Sub-committees in 2017;

- Conducted corporate governance training for the Board and Executive Management.

As of the date of this report, the provisions of the Code relating to the independence of the Directors do not apply. The CMA issued guidance on the provisions relating to the independence of Directors, clarifying that these provisions will only apply upon election of a new Board. As the Board of Directors were last elected in March 2014, the provisions will apply from March 2017 at the next Board elections. All Board members are therefore currently considered independent until a new Board has been elected in March 2017, at which point the new Board of Directors will be constituted in accordance with the provisions in the Code relating to independence of Directors.

2. Company’s PhilosophyThe Company upholds a governance philosophy that aims at enhancing long term shareholder value while at the same time adheres to the law and observes the ethical standards of the business environment within which it operates.

According to the Company’s governance paradigm the management assumes accountability to the Board, and the Board assumes accountability to the Shareholders. The Board’s role is to be an active participant and a decision-maker in fostering the overall success of the Company by enhancing shareholder value, selecting and evaluating the top management team, approving and overseeing the corporate strategy and management’s business plan, and acting as a resource for management in matters of planning and policy.

A N N U A L R E P O R T 2 0 1 632

The Board monitors corporate performance against the strategic and business plans, and evaluates on a regular basis whether those plans pay off in terms of operating results.

In order that it can effectively discharge its governance responsibilities, the Board ensures that all Board members are non-executive.

Furthermore, the Board accesses independent legal and expert advice of professionals who also assist the management. The Board also encourages active participation and decision making on the part of shareholders in General Meeting proceedings.

The Board maintains a positive and ethical work environment that is conducive to attracting, retaining and motivating a diverse group of top quality employees at all levels. The Board, through the Nomination and Remuneration Committee, reviews and decides the parameters for assessment and compensation of key personnel.

The Board abides by ethical behaviour principles at all times. It ensures that the Company complies with all laws and regulations and has developed a Code of Ethics that promotes these values among its employees. The Company has also developed a comprehensive number of policies to ensure compliance with the requirements of the new Code of Corporate Governance, as well as updated its policies in existence prior to the introduction of the new code. These policies include, but are not limited to, Audit and Internal Controls Committee Policy, Rules for Related Party Transactions, Disclosure Guidelines, Corporate Social Responsibility Policy, Conflict of Interest Policy, Board Secretarial Duties, Auditor Consultancy Policy and a number of other policies.

3. Board of Directors During 2016, the Board consisted of seven Directors. Five Directors on the Board are Shareholders / representatives of Shareholders and two Directors are non-shareholder Directors.

3.1 The Composition and Category of Directors and Board Meeting Attendance

Sr. No Name of Director Position Category

No. of Board meetings held

during the year

No. of Board meetings attended

Whether attended last AGM

1 Samir J Fancy Chairman Independent Non-Executive Shareholder 5 5 Yes

2 Ali bin Hassan Sulaiman

Deputy Chairman

Independent Non-Executive Shareholder 5 5 Yes

3 Sayyid Tarik bin Shabib bin Taimur Director Independent Non-Executive

Shareholder 5 3 No

4 Sunder George Director Independent Non-Executive Non-Shareholder 5 5 Yes

5 Yeshwant C Desai* Director Independent Non-Executive Non-Shareholder 5 5 Yes

6 Colin Rutherford Director Independent Non-Executive Shareholder 5 3 No

7 Saleh bin Nasser Al Habsi Director Independent Non-Executive,

Representative of a Shareholder 5 5 No

The above Board members were elected on the 26th of March 2014 for a tenure of three years which will expire in March 2017. The Company will hold elections for members of the new Board of Directors at the AGM in March 2017.

*Mr Yeshwant Desai has expressed an intention not to offer himself for re-appointment as a Director at the forthcoming AGM in March 2017, having served on the Renaissance Board for many years. Mr Desai will continue to serve on the Renaissance Board until the new Board is elected, and will formally retire as a member of the Board at the AGM in March 2017.

3.2 Statement of the Names & Profiles of Directors and Top Management The Renaissance Board brings together core competencies of Directors with vision, strategic insight, and industry knowledge, who provide direction to the executive management.

33A N N U A L R E P O R T 2 0 1 6

Samir J Fancy - ChairmanMr. Samir J Fancy is the Chairman of the Board of Directors since 1996. He has held senior positions and undertaken leading roles such as:• Founder and Vice Chairman of Tawoos Group since

1983, and Chairman of Tawoos Group since 2005• Chairman of Topaz Energy & Marine SAOG since

foundation and up to its acquisition by the Company in May 2005

• Chairman of Amani Financial Services SAOC since 1997

• Chairman of Topaz Energy & Marine Ltd• Director of Renaissance Duqm Holding SAOC• Director of Renaissance Duqm Accommodation

Company SAOC• Director of Renaissance International Ltd• Director of Samena Capital• Director of BUE Marine Ltd• He has acted as a Director of National Bank of Oman,

Muscat Finance Company and Vision Insurance in the past

Ali bin Hassan Sulaiman - Deputy Chairman Mr. Ali bin Hassan Sulaiman is a member of the Board of Directors of the Company since 1996 and is Deputy Chairman since March 2010. He is a founder of Ali and Abdul Karim Group and director in the following companies:

• Topaz Energy & Marine SAOG for several years up to its acquisition by the Company in May 2005

• Majan Glass Co SAOG• Topaz Energy & Marine Ltd• Renaissance Duqm Holding SAOC• Renaissance Duqm Accommodation Company SAOC

HH Sayyid Tarik bin Shabib bin Taimur - DirectorHH Sayyid Tarik bin Shabib bin Taimur is a member of the Board of Directors of the Company since 1996. Other positions held by him include the following: • Founder and Director of Tawoos Group• Chairman of Marina Bander Al Rowdha SAOG for

six years until its takeover by the Government of the Sultanate of Oman in April 2003

• Chairman of Renaissance Duqm Holding SAOC• Chairman of Renaissance Duqm Accommodation

Company SAOC• Chairman of National Hospitality Institute SAOG

(now SAOC) since 1995• Director of Amani Financial Services SAOC

Sunder George - DirectorMr. Sunder George is a member of the Board of Directors of the Company since 2001. He has extensive experience in Banking & Finance and has held several senior executive positions in Oman & abroad until he retired from Bank Muscat on 31 December 2012 as its

Deputy Chief Executive. He was Chief Adviser to the Bank for a year until the end of 2013. Sunder George sits on the Board of Directors of the following Companies: • Topaz Energy & Marine Ltd• Director of Bank Muscat

Yeshwant C Desai - DirectorMr. Yeshwant C Desai is a member of the Board of Directors of the Company since 2001 and is the Chairman of the Audit and Internal Controls Committee and also Chairman of the Nomination and Remuneration Committee. He has had a successful career and extensive experience in Banking & Finance and has held senior executive positions in Oman & abroad, which include:

• Ex-CEO of Bank Muscat SAOG• Director of Topaz Energy & Marine SAOG for several

years up to its acquisition by the Company in May 2005

• Ex-Director of Topaz Energy & Marine Ltd

Colin Rutherford – DirectorMr. Colin Rutherford has been a member of the Board since 2005 and was formerly Chairman of BUE Marine Holdings Limited prior to its acquisition by Renaissance Group SAOG. He has diverse experience of public and private companies having served on many international Boards. He is a Chartered Accountant and former Corporate Financier, and currently enjoys the following positions within his portfolio:• Executive Chairman and CEO of Teachers Media PLC• Non-Executive Director and Audit Committee

Chairman of Mitchells & Butlers PLC• Non-Executive Chairman of Brookgate Limited• Colin holds further positions in retail, specialist

building products and real estate, amongst others

Saleh bin Nasser Al Habsi - DirectorMr. Saleh Al Habsi is the General Manager of the Pension Fund of the Ministry of Defence. He holds an MBA and M.Sc in Finance from the University of Maryland (USA) and BSBA and BA from Boston University (USA). He also attended a senior executive programme at London Business School and High Performance Boards Programme at IMD, Switzerland. Mr. Al Habsi is also member of the Board of GrowthGate Capital, a regional private equity company and also a former member of the Board of Al Suwadi Power Company SAOG. Previously, he served as Chairman of Muscat Fund, Deputy Chairman of Gulf Custody Company Oman SAOC. He was a Board member of Bank Dhofar SAOG, Board member of National Bank of Oman and Al Omaniya Financial Services SAOG.

Stephen R Thomas OBE – Chief Executive OfficerMr. Stephen R Thomas joined Tawoos Group as General Manager of Tawoos Industrial Services Co LLC in 1988. He took over as Chief Executive Officer of Renaissance

Report on Corporate Governance

A N N U A L R E P O R T 2 0 1 634

Services SAOG in 1998. In the 2010 United Kingdom New Year’s Honours List, Mr. Thomas was appointed an Officer of the Most Excellent Order of the British Empire (OBE) for services to business abroad and services to the community in Oman. He also held senior positions in the Group including the following positions:• Director of Renaissance Hospitality Services

SAOG since foundation and until its merger with Renaissance Services SAOG in April 2002

• Founder and former Chairman of Oman Society for Petroleum Services (“OPAL”)

• Director of Topaz Energy & Marine Ltd

3.3 Membership of Other Boards/ Board Committees (SAOG Companies in Oman)

Sr. No Name of Director

Directorship in other

SAOG companies

Membership in Board

Committees of other

companies1 Samir J Fancy -

2 Ali bin Hassan Sulaiman 1 -

3HH Sayyid Tarik bin Shabib bin Taimur

- -

4 Sunder George 1 -5 Yeshwant C Desai - -6 Colin Rutherford - -

7 Saleh bin Nasser Al Habsi - -

3.4 Number & Dates of Meetings of the Board of Directors

The Board held five meetings during 2016 on the following dates:-

14 January 2016, 24 February 2016, 11 May 2016, 11 August 2016, and 7 November 2016.

4. Audit and Internal Controls Committee & Other Sub-committees

The Audit and Internal Controls Committee is a sub-committee of the Board comprising of three Directors, all of whom are independent, non-executive directors.

4.1 Brief Description & Terms of Reference The functions of the Audit and Internal Controls Committee are as follows:• Recommend to the Board the appointment and

removal of the Statutory Auditors and determine their independence, fee and terms of engagement for approval by the Shareholders.

• Review the audit plan and results of the audit in conjunction with the Statutory Auditors and provide its comments and consider whether Statutory

Auditors have full access to all relevant documents • Following up on the work of the Statutory Auditors

and approving any non-audit services which they are assigned during the audit process.

• Overseeing the preparation of the financial statements including:

- Reviewing the annual and quarterly financial statements prior to publication.

- Reviewing the reservations and qualifications of the external auditors in the draft financial statements.

- Discussing the accounting principles in general focusing on any changes in accounting policies and principles that had taken place and their impact on the financial position of the Company

- Ensuring compliance with disclosure requirements prescribed by the CMA.

• Consideration and follow up of the comments of the Statutory Auditor on the annual and quarterly financial statements and providing opinion and recommendation to the Board.

• Consideration and review of the Internal Audit function in general and submitting an annual report outlining its opinions and recommendations with particular reference to reviewing the scope of internal audit plan for the year, reports of internal auditors pertaining to critical areas, efficacy of internal auditing and whether the internal auditors have full access to relevant documents.

• Oversee the adequacy and sufficiency of internal control systems either through consideration of the internal and external Audit Reports or by appointing an independent consultant and any following up remedial action.

• Review any non-compliance with disclosure requirements prescribed by CMA.

• Oversee the Company’s financial reporting process and the disclosure of its financial information to ensure accuracy, sufficiency and credibility of the financial statements.

• Consideration of the adopted accounting policies and principles and providing opinion and recommendation to the Board.

• Serve as a channel of communication between Statutory & Internal Auditors and the Board.

• Developing a risk management plan and following up on its implementation. The plan should include the key risks which the Company is exposed to, their probability, mechanisms for detecting, measuring and monitoring these risks and any mitigation mechanisms.

• Developing and reviewing risk management policies taking into account the business, any changes in market conditions and the Company’s investment and expansion tendencies and approach.

• Guiding the Board and Executive Management on risk management matters.

35A N N U A L R E P O R T 2 0 1 6

• Reporting periodically, or as directed by the Board, on the risk status and management.

• Review proposed related party transactions and providing appropriate recommendations to the Board.

• Validating and verifying the overall efficiency of Executive Management in implementing operational directives and guidelines set up by the Board.

• Creating policies for safeguarding the Company’s human, material and intellectual resources and assets.

• Seek the assistance of any other entity on a consultancy basis to assist it to perform its duties.

4.2 Composition of Audit and Internal Controls Committee and Meetings Attendance

In 2016, the Audit Committee of the Company was renamed ‘Audit and Internal Controls Committee’ in accordance with the requirements of the Code of Corporate Governance. The Committee comprises of three non-executive Directors. During 2016, the Committee held four meetings on 23 February 2016, 10 May 2016, 10 August 2016 and 06 November 2016 respectively. The following table shows the composition of the Audit and Internal Controls Committee and the meetings attendance:-

Sr. No

Name of Director Position

Meetings held during

the year

Meetings attended

during the year

1 Yeshwant C Desai Chairman 4 4

2 Ali bin Hassan Sulaiman Member 4 4

3 Sunder George Member 4 4

During its meetings in 2016, the Audit and Internal Controls Committee discussed and approved the annual internal audit plan, and recommended the appointment of the Statutory Auditors for the year 2017. It also reviewed and recommended the audited and quarterly accounts and looked into certain specific areas of the Company’s operations and reported on these to the Board. Further, the Audit and Internal Controls Committee also reviewed all related party transactions before submitting to the Board for approval.

4.3 The Nomination and Remuneration CommitteeThe Nomination and Remuneration Committee, formerly known as the ‘Compensation Committee’ was originally formed as a Board Committee to lay down and update the parameters for assessment and compensation of key personnel, undertake their performance assessment and report to the Board on the compensation and personnel policies. Following the implementation of the Code of Corporate Governance in July 2016, the Compensation Committee was formally renamed as the ‘Nomination and Remuneration Committee’ and its policy charter outlining the functions of the committee was updated to incorporate the requirements of the new code. These duties include assisting the Board with finding suitable Directors to sit on the Board, succession planning for Board members

and senior executive management, drawing up job descriptions for board members and formulating a policy for remuneration of senior executives.

The committee, which consists of the following directors, held two meetings on 31 March 2016 and 21 December 2016:

Sr. No

Name of Director Position

Meetings held

during the year

Meetings attended

during the year

1 Ali bin Hassan Sulaiman Chairman 2 2

2HH Sayyid Tarik bin Shabib bin Taimur

Member 2 1

3 Samir J Fancy Member 2 1

4 Yeshwant C Desai*

Member (Former) 2 1

5 Colin Rutherford**

Member (Former) 2 1

* Since the introduction of the Code of Corporate Governance, Mr Yeshwant Desai has stepped down as a member of the Nomination and Remuneration Committee as he was serving as the Chairman of the Audit and Internal Controls Committee. As per the new requirement introduced by the Code, the Chairman of the Audit and Internal Controls Committee cannot serve as a Chairman or member of any other Sub-committee of the Board. Yeshwant Desai attended one Nomination and Remuneration Committee meeting in 2016 and was replaced by HH Sayyid Tarik bin Shabib bin Taimur.

**Mr Colin Rutherford stepped down from the Nomination and Remuneration Committee and was replaced by Samir J Fancy. Colin Rutherford attended one Nomination and Remuneration Committee meeting in 2016.

5. Process of Nomination of the DirectorsIn nominating and screening candidates to fill a casual vacancy, the Board, assisted by the Nomination and Remuneration Committee, seeks candidates with the skills and capacity to provide strategic insight and direction, encourage innovation, conceptualize key trends and evaluate strategic decisions. The Board focuses on professionalism, integrity, accountability, performance standards, leadership skills, professional business judgment, financial literacy and industry knowledge as core competencies of the candidates. While nominating competent candidates, the Board ensures that the shareholders retain the power of electing any candidate, irrespective of his candidature being recommended by the Board or otherwise, and that any shareholder has the full right of nominating himself.

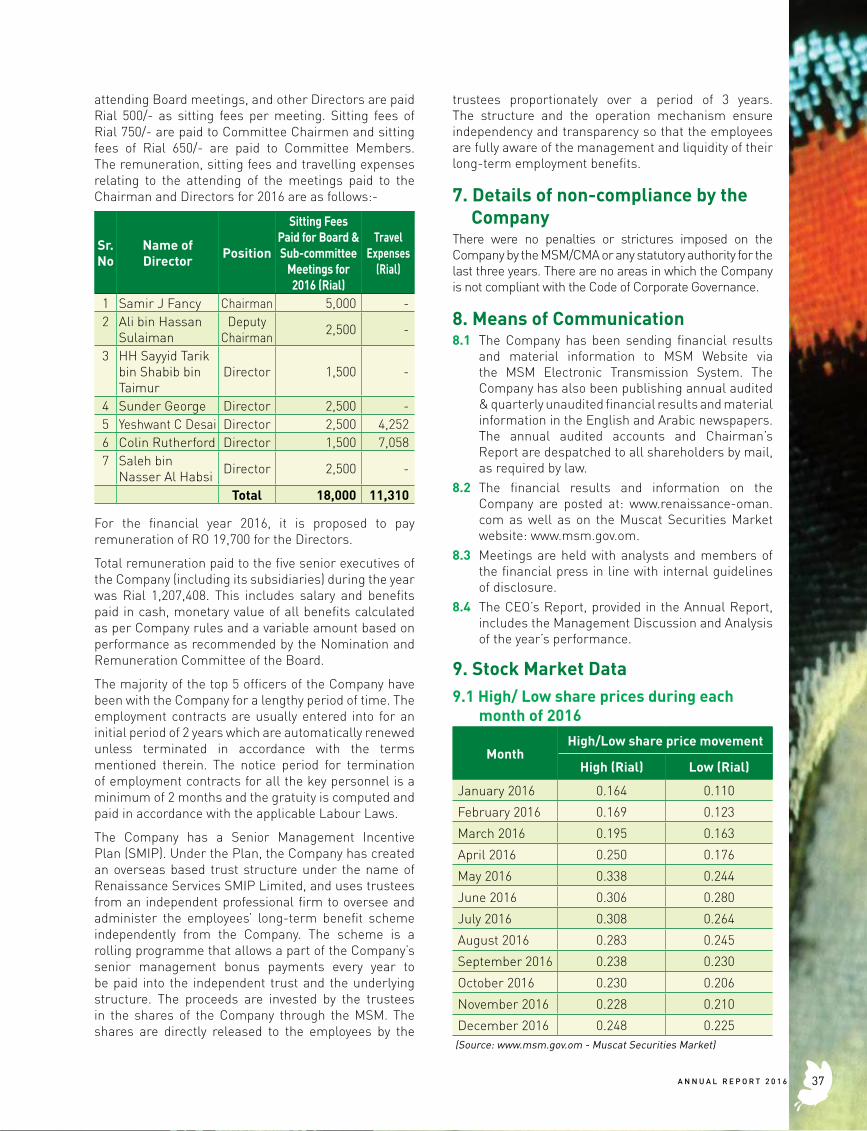

6. Remuneration MattersAs per the approval accorded by the AGM held on 31March 2016, the Chairman is paid Rial 1,000/- for

Report on Corporate Governance

A N N U A L R E P O R T 2 0 1 636

attending Board meetings, and other Directors are paid Rial 500/- as sitting fees per meeting. Sitting fees of Rial 750/- are paid to Committee Chairmen and sitting fees of Rial 650/- are paid to Committee Members. The remuneration, sitting fees and travelling expenses relating to the attending of the meetings paid to the Chairman and Directors for 2016 are as follows:-

Sr. No

Name of Director Position

Sitting Fees Paid for Board & Sub-committee

Meetings for 2016 (Rial)

Travel Expenses

(Rial)

1 Samir J Fancy Chairman 5,000 -2 Ali bin Hassan

SulaimanDeputy

Chairman 2,500 -

3 HH Sayyid Tarik bin Shabib bin Taimur

Director 1,500 -

4 Sunder George Director 2,500 -5 Yeshwant C Desai Director 2,500 4,2526 Colin Rutherford Director 1,500 7,0587 Saleh bin

Nasser Al Habsi Director 2,500 -

Total 18,000 11,310

For the financial year 2016, it is proposed to pay remuneration of RO 19,700 for the Directors.

Total remuneration paid to the five senior executives of the Company (including its subsidiaries) during the year was Rial 1,207,408. This includes salary and benefits paid in cash, monetary value of all benefits calculated as per Company rules and a variable amount based on performance as recommended by the Nomination and Remuneration Committee of the Board.

The majority of the top 5 officers of the Company have been with the Company for a lengthy period of time. The employment contracts are usually entered into for an initial period of 2 years which are automatically renewed unless terminated in accordance with the terms mentioned therein. The notice period for termination of employment contracts for all the key personnel is a minimum of 2 months and the gratuity is computed and paid in accordance with the applicable Labour Laws.

The Company has a Senior Management Incentive Plan (SMIP). Under the Plan, the Company has created an overseas based trust structure under the name of Renaissance Services SMIP Limited, and uses trustees from an independent professional firm to oversee and administer the employees’ long-term benefit scheme independently from the Company. The scheme is a rolling programme that allows a part of the Company’s senior management bonus payments every year to be paid into the independent trust and the underlying structure. The proceeds are invested by the trustees in the shares of the Company through the MSM. The shares are directly released to the employees by the

trustees proportionately over a period of 3 years. The structure and the operation mechanism ensure independency and transparency so that the employees are fully aware of the management and liquidity of their long-term employment benefits.

7. Details of non-compliance by the Company

There were no penalties or strictures imposed on the Company by the MSM/CMA or any statutory authority for the last three years. There are no areas in which the Company is not compliant with the Code of Corporate Governance.

8. Means of Communication 8.1 The Company has been sending financial results

and material information to MSM Website via the MSM Electronic Transmission System. The Company has also been publishing annual audited & quarterly unaudited financial results and material information in the English and Arabic newspapers. The annual audited accounts and Chairman’s Report are despatched to all shareholders by mail, as required by law.

8.2 The financial results and information on the Company are posted at: www.renaissance-oman.com as well as on the Muscat Securities Market website: www.msm.gov.om.

8.3 Meetings are held with analysts and members of the financial press in line with internal guidelines of disclosure.

8.4 The CEO’s Report, provided in the Annual Report, includes the Management Discussion and Analysis of the year’s performance.

9. Stock Market Data9.1 High/ Low share prices during each

month of 2016

MonthHigh/Low share price movement

High (Rial) Low (Rial)

January 2016 0.164 0.110

February 2016 0.169 0.123

March 2016 0.195 0.163

April 2016 0.250 0.176

May 2016 0.338 0.244

June 2016 0.306 0.280

July 2016 0.308 0.264

August 2016 0.283 0.245

September 2016 0.238 0.230

October 2016 0.230 0.206

November 2016 0.228 0.210

December 2016 0.248 0.225 (Source: www.msm.gov.om - Muscat Securities Market)

37A N N U A L R E P O R T 2 0 1 6

9.2 Renaissance Share Price movement in comparison to the MSM Index and MSM Services Index.

4,500

4,900

5,300

5,700

6,100

6,500

6,900

0.025

0.075

0.125

0.175

0.225

0.275

0.325

0.375

MSM

Inde

x

Shar

e P

rice

(in

Ria

l)

RS Closing price MSM Index

2800

3000

3200

3400

3600

0.040

0.090

0.140

0.190

0.240

0.290

0.340

0.390

MSM

Ser

vice

s In

dex

Shar

e P

rice

(in

Ria

l)

RS Closing Price MSM Service Index

9.3 Distribution of Shareholding as on 31 December 2016Source of Statistics: Muscat Clearing & Depository (SAOC)

Sr. No Category Number of Shareholders No of shares % Shareholding

1 Less than 100,000 shares 3,965 14,702,083 4.92%

2 100,000 – 200,000 shares 32 4,434,652 1.48%

3 200,001 – 500,000 shares 41 13,072,622 4.38%

4 500,001 – 2,987,7767 shares 35 48,350,290 16.18%

5 1% - 1.99% of share capital 7 27,054,552 9.06%

6 2% - 9.99% of share capital 11 148,625,451 49.74%

7 10% of share capital & above 1 42,538,025 14.24%

Total 4,092 298,777,675 100%

Report on Corporate Governance

A N N U A L R E P O R T 2 0 1 638

9.4 The Company has issued 423,141,678 mandatory convertible bonds (MCBs) at Rial 0.102 each on 25 July 2012 and listed on Muscat Securities Market (MSM) on 6 August 2012. The MCBs carry a coupon rate of 3.75% per annum and shall be converted at face value (Rial 0.100) through conversion into shares of the Company at the conversion price. In accordance with the issue prospectus, the conversion would be carried out in three tranches, 33.33% at the end of third and fourth year each and 33.34% at the end of fifth year, commencing from the third anniversary and ending on the fifth anniversary from the issue date.

However, in order to safeguard the interests of all stakeholders including MCB holders, the Company offered a repurchase option to MCB holders wishing to tender their MCBs to the Company prior to the first conversion date. To date, the Company has repurchased the first tranche of MCBs in July 2015, the second tranche in September 2015 and third tranche in July 2016 from MCB holders who offered to tender their MCBs.

Following the repurchase of the third tranche, the remaining 80,824,189 MCB’s are held by those MCB holders who chose not to participate in the repurchase scheme. These MCBs will be converted into shares in July 2017.

10. Professional Profile of the Statutory Auditors

Deloitte (Deloitte Touche Tohmatsu Limited), a UK private company limited by guarantee (“DTTL”) is a globally connected network of member firms in more than 150 countries and territories and each of its member firms are legally separate and independent entities. Deloitte employs more than 220,000 professionals globally.

Deloitte & Touche (M.E.) is a member firm of Deloitte Touche Tohmatsu Limited and is a leading professional services firm established in the Middle East region with uninterrupted presence since 1926. It provides audit, tax, consulting, and financial advisory services through 26 offices in 15 countries with more than 3,300 partners, directors and staff. It is a Tier 1 Tax advisor in the GCC region since 2010 (according to the International Tax Review World Tax Rankings). It has also received numerous awards in the last few years which include best employer in the Middle East, best consulting firm, the Middle East Training & Development Excellence Award by the Institute of Chartered Accountants in England and Wales (ICAEW), as well as the best CSR integrated organisation.

10.1 Audit Fees paid to the AuditorsDuring the year 2016, aggregate professional fees in the amount of Rial 198,232 were paid by the Company to Deloitte in respect of services provided for audit.

11. Confirmation by the Board of Directors

Renaissance is committed to conducting business legally and professionally under the highest standards of business ethics and moral code. This same high standard is expected and required of all Renaissance subsidiary companies and people working at every level throughout the group.

The Board of Directors confirms its accountability for the preparation of the financial statements in accordance with the applicable standards and rules.

The Board of Directors confirms that it has reviewed the efficiency and adequacy of the internal control systems of the Company. The Board is pleased to inform shareholders that adequate and efficient internal controls are in place, and that they are in full compliance with the internal rules and regulations.

The Board of Directors also confirms that there are no material matters that affect the continuation of the Company, and its ability to continue its operations during the next financial year.

_________________ ________________ Chairman Director

39A N N U A L R E P O R T 2 0 1 6

A N N U A L R E P O R T 2 0 1 640

41A N N U A L R E P O R T 2 0 1 6

A N N U A L R E P O R T 2 0 1 642

43A N N U A L R E P O R T 2 0 1 6

A N N U A L R E P O R T 2 0 1 644

45A N N U A L R E P O R T 2 0 1 6

RENAISSANCE SERVICES SAOG AND ITS SUBSIDIARY COMPANIES

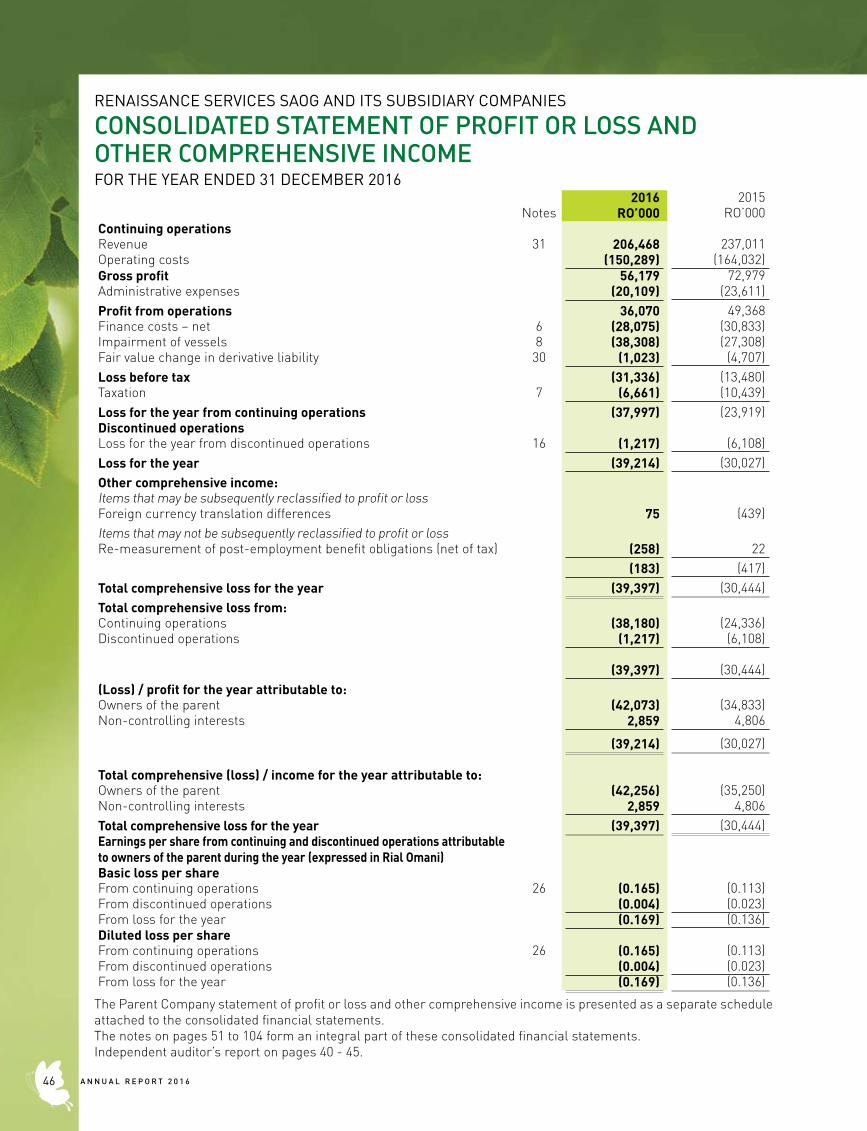

CONSOLIDATED STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOMEFOR THE YEAR ENDED 31 DECEMBER 2016

2016 2015Notes RO’000 RO’000

Continuing operationsRevenue 31 206,468 237,011 Operating costs (150,289) (164,032)Gross profit 56,179 72,979Administrative expenses (20,109) (23,611) Profit from operations 36,070 49,368Finance costs – net 6 (28,075) (30,833)Impairment of vessels 8 (38,308) (27,308)Fair value change in derivative liability 30 (1,023) (4,707)Loss before tax (31,336) (13,480)Taxation 7 (6,661) (10,439)Loss for the year from continuing operations (37,997) (23,919)Discontinued operationsLoss for the year from discontinued operations 16 (1,217) (6,108)Loss for the year (39,214) (30,027)Other comprehensive income:Items that may be subsequently reclassified to profit or lossForeign currency translation differences 75 (439)Items that may not be subsequently reclassified to profit or lossRe-measurement of post-employment benefit obligations (net of tax) (258) 22

(183) (417)Total comprehensive loss for the year (39,397) (30,444)Total comprehensive loss from:Continuing operations (38,180) (24,336)Discontinued operations (1,217) (6,108)

(39,397) (30,444)(Loss) / profit for the year attributable to: Owners of the parent (42,073) (34,833)Non-controlling interests 2,859 4,806

(39,214) (30,027)

Total comprehensive (loss) / income for the year attributable to:Owners of the parent (42,256) (35,250)Non-controlling interests 2,859 4,806Total comprehensive loss for the year (39,397) (30,444)Earnings per share from continuing and discontinued operations attributable to owners of the parent during the year (expressed in Rial Omani)Basic loss per shareFrom continuing operations 26 (0.165) (0.113)From discontinued operations (0.004) (0.023)From loss for the year (0.169) (0.136)Diluted loss per shareFrom continuing operations 26 (0.165) (0.113)From discontinued operations (0.004) (0.023)From loss for the year (0.169) (0.136)

The Parent Company statement of profit or loss and other comprehensive income is presented as a separate schedule attached to the consolidated financial statements.The notes on pages 51 to 104 form an integral part of these consolidated financial statements.Independent auditor’s report on pages 40 - 45.

A N N U A L R E P O R T 2 0 1 646

RENAISSANCE SERVICES SAOG AND ITS SUBSIDIARY COMPANIES

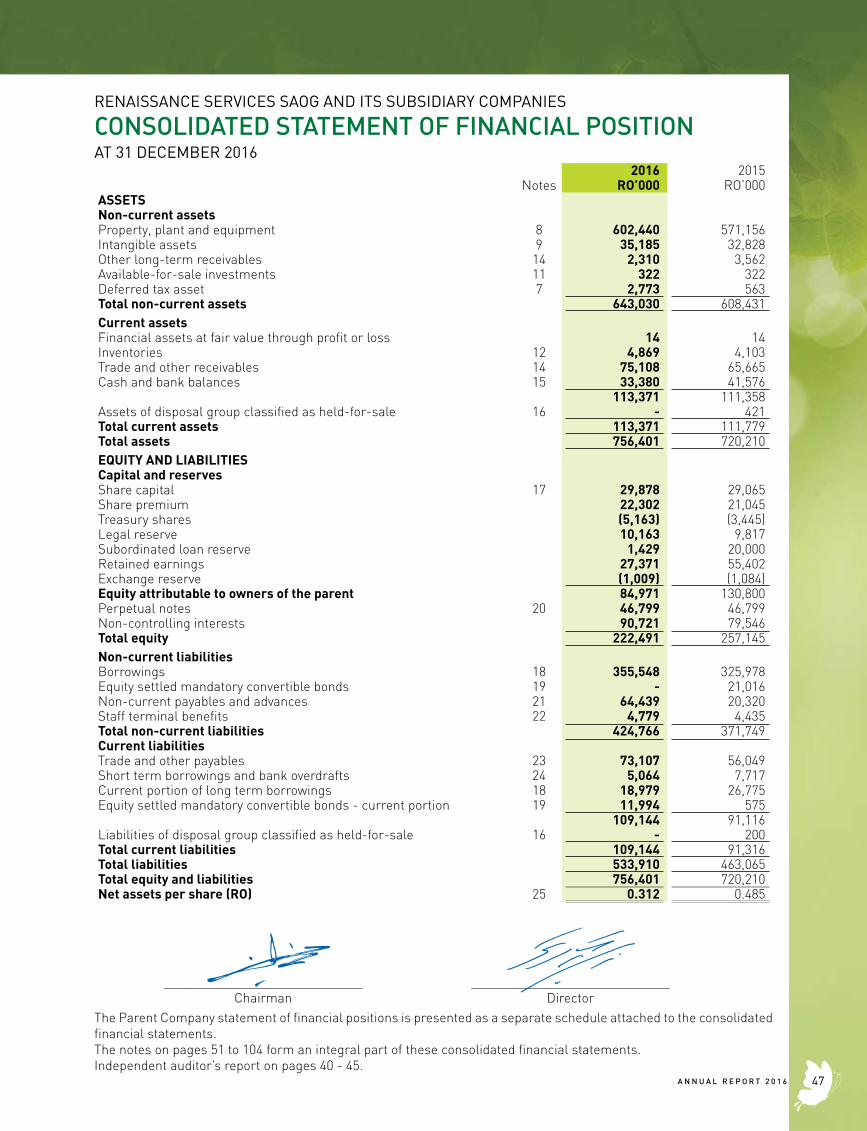

CONSOLIDATED STATEMENT OF FINANCIAL POSITIONAT 31 DECEMBER 2016

2016 2015Notes RO’000 RO’000