ALL ABOUT MUTUAL FUNDS By - Dr. Y. P. Singh Lucknow (India)

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 1/183

ALL ABOUTMUTUAL FUNDS

By - Dr. Y. P. Singh

Lucknow (India)

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 2/183

Session 1: Concept,

Structure and RegulatoryFramework

• Introduction

• Sponsor-Trustee-AMC

• Other constituents

• Regulatory framework

• Mutual fund products• Merger and acquisitions

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 3/183

What Is a Mutual Fund?

A mutual fund is a pool of moneycollected from investors and isinvested according to statedinvestment objectives

Terms to know Mutual: the ownership of the fund is joint or mutual

Pool Investment objectives

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 4/183

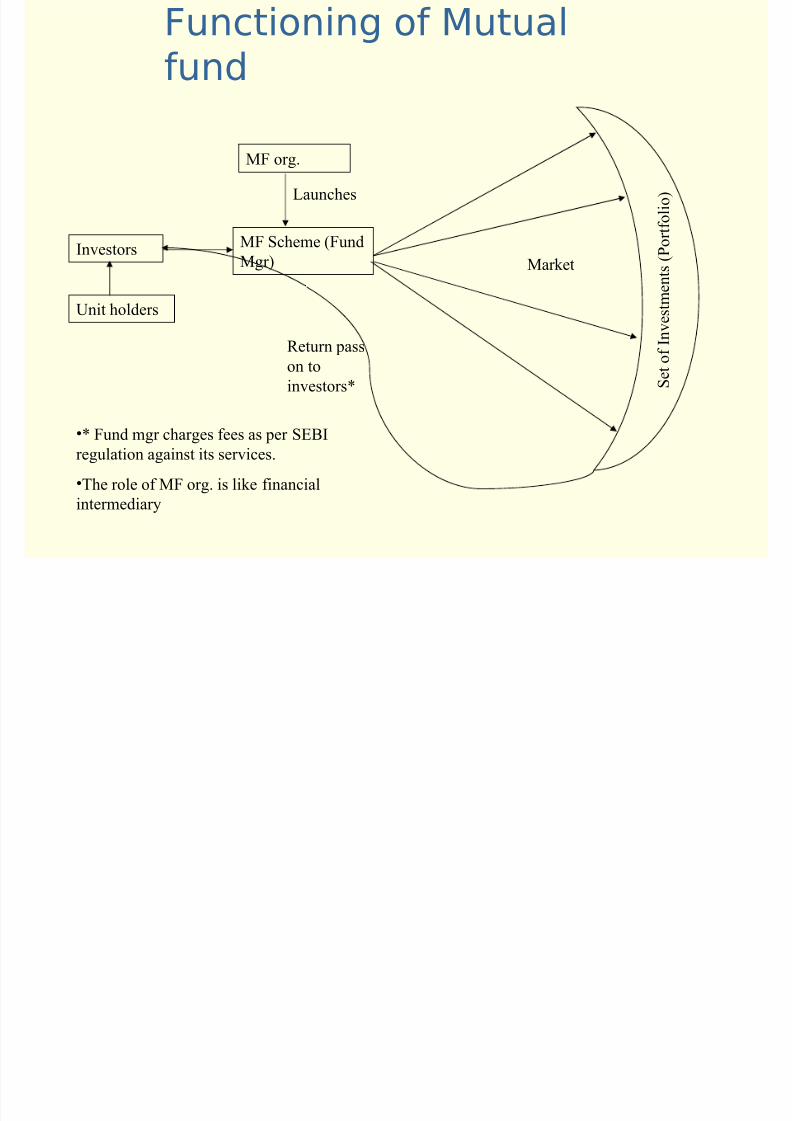

Functioning of Mutualfund

MF org.

MF Scheme (Fund

Mgr)

Launches

Unit holders

Investors

SetofInv

estments (

Portfolio)

•* Fund mgr charges fees as per SEBI

regulation against its services.

•The role of MF org. is like financial

intermediary

Return pass

on to

investors*

Market

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 5/183

Mutual Fund: Back ground

•Most appropriate investmentopportunity for small investors

•Birth of mutual funds – USA

•Good alternative to direct investing

•Size (AUM) in USA > Bank deposits

•Financial intermediary

•UTI only player between 1964-87

•Helps in the growth of capital markets

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 6/183

Characteristics of a MutualFund

• Investors own the mutual fund.

• Professional managers manage thefund for a fee.

• The funds are invested in a portfolio of marketable securities, reflecting theinvestment objective.

• Value of the portfolio and the value of

investors’ holdings, alters with changein market value of investments.

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 7/183

Advantages of MutualFunds to Investors

• Portfolio diversification

• Professional management• Reduction in risk

• Reduction in transaction cost

• Liquidity

• Convenience and flexibility

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 8/183

Disadvantages of MutualFunds

• No control over costs

•

No tailor-made portfolios• Issues relating to management of

a portfolio of mutual funds

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 9/183

Fund Structure &Constituents

• Mutual funds in US are setup asinvestment companies

• Mutual funds in UK are either unit trusts

(trust) or investment trust (companies)• Mutual funds in India are public trusts

under the Indian trust Act, 1882

• Mutual funds in India is a 3-tier structure Sponsor Trustee AMC

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 10/183

Sponsor

• Promoter of the the mutual fund

• Appoints AMC and also appointsthe trustees

• Criteria Financial services business 5-year track record 3-year profit making record At least 40% contribution to AMC

capital

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 11/183

Trustees

• Trustees represent the trust i.e. MF org. Trust has nophysical identity

• Fiduciary responsibility for investor funds

• Appointed by sponsor with SEBI approval

• Registered ownership of investments is with Trust

• Board of trustees or Trustee Company

appoints all other constituents• Trustees oversee the functioning of AMC

• Trustees approve each MF schemes floated by AMC

• Trustees receive fees for their services

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 12/183

Trustees

• At least 4 trustees 2/3 should be independent

• Trustees of one mutual fund cannot

be trustee of another mutual fundexcept in case of Independent trusteeafter Board approval of Both the MFs

• Right to seek regular information andremedial action

• All major decisions need trusteeapproval

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 13/183

Asset ManagementCompany• Responsible for operational aspects of

the mutual fund & can undertakefollowing businesses Asset mgt services

Portfolio Management Services Portfolio advisory services

• Investment management agreementwith trustees

• Registered with SEBI

• Rs. 10 crore of net worth to bemaintained at all times

• At least 1/2 of the board members to beindependent

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 14/183

Asset Management

Company• Appoints other constituents with

trustees approval

• Cannot have any other business

interest & can be changed /terminated Majority of trustees or At least 75% majority of unit holders

• Structured as a private limitedcompany Sponsor and associates hold capital

• AMC of one MF cannot be trustee of another MF

• Quarterly reporting to Trustees

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 15/183

Other Constituents

• Custodian Investment back-office: Safekeeping of

records & documents Registered with SEBI

• Registrar and Transfer agent Keeps Investors A/c’s & record of transactions:

purchase, redemption tranfer of units etc. Registered with SEBI

• Broker Purchase and sale of securities 5% limit per broker

• Banker Assist funds pay in & pay out obligations

• Auditor Separate auditor for AMC and mutual fund

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 16/183

Regulatory Framework• SEBI:

Apex regulator of capital markets. It is theprimary regulator of mutual funds in India.

SEBI has enacted SEBI (Mutual Fund)Regulations 1996 to regulate MF industry.

Mutual funds mandatorily required registeringwith SEBI.

Mutual funds have to send half-yearlycompliance report.

Inspects and regulates other constituents of mutual fund.

• RBI: Monetary authority of the country and also

the regulator of the banking system. It is involved only with bank-sponsoredmutual funds.

• MoF: Supervisor of RBI and SEBI Appellate authority under SEBI regulations.

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 17/183

Regulatory Framework

•

COMPANIES ACT: The AMC and the Trustee Company may bestructured as limited companies, which comeunder the regulatory purview of Company LawBoard (C L B),

Registrar of Companies (ROC) oversees thecompliance.

Department of Company Affairs (DCA) isresponsible for the formulation andamendments in laws relating to companies,including the Indian Companies Act. It has thepower to prosecute the directors.

• STOCK EXCHANGES: Regulatory role if the mutual fund is registered

with it.• PUBLIC TRUSTEE: Since the mutual funds are registered under

Indian Trusts Act, they come under regulatorypurview of the office of public trustee, which inturn reports to the commissioner.

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 18/183

Regulatory Framework• UTI:

UTI was governed by provisions of the UTI Act, 1963. UTI has, however, subjected itself voluntarily to theprovisions of the SEBI regulations in 1996.

All the UTI schemes, except the US 64, are under dualregulation of both SEBI and UTI Act.

The Board of Trustees operates it. The Board has nominees from MoF, RBI and other

institutions who subscribed to the initial corpus.

The Chairman is appointed by MoF, in consultation withIDBI, the principal investor in the corpus. UTI does not have a three-tier structure. Hence no AMC. All expenses borne by the schemes. UTI has powers to

take loans, other mutual funds can’t. Major Differences

• Assured return schemes

• Different accounting norms

• Ability to take and make loans

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 19/183

Self-regulatory Organisations(SROs)

• Derive powers from regulator

• Ability to make bye-laws

• Example : Stock exchanges

• Industry Associations Collective industry opinion Guidelines and recommendation Example: Association of Mutual Funds in

India

• AMFI is not yet a SEBI registered SRO

Regulatory Framework

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 20/183

Mutual Fund Products -classification:

Mutual fund products can be classified onvarious parameters: On the basis of maturity:

– Open ended funds - no maturity– Close ended funds – having maturity

On the basis of Investment

– Equity or growth fund– Debt or income fund– Balanced or hybrid fund

On the basis of investment objective– Equity diversified fund– ELSS / index funds

– Sectoral fund– Money market fund / gilt-edge fund– Gold fund– Exchange traded fund– Funds of fund etc.

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 21/183

Mutual Fund Products

• Open ended funds

Initial issue for a limited period Continuous sale and repurchase Size of the fund i.e. Unit capital

changes as investors enter and

exit NAV-based pricing

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 22/183

Mutual Fund Products

• Closed end funds Sale of units by fund only during

Initial Public Offer Listing on exchange and liquidity for

investors

Size of fund i.e. Unit capital remains

constant Price in the market is usually at a

discount

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 23/183

Equity Funds

• Pre-dominantly invest in equity markets Diversified portfolio of equity shares Select set based on some criterion

• Diversified equity funds that invest in the broad markets ELSS as a special case have the following features:

– 3 year lock in

– Minimum investment of 90% in equity marketsat all times

– Open or close ended

– Deduction u/s 80c for investments up to Rs.10000.

• Primary market funds• Small Cap funds

• Index funds which replicate an index• Sectoral funds which focus on a sector

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 24/183

Debt Funds

• Predominantly invest in the debt markets Diversified debt funds Select set based on some criterion

• Income funds or diversified debt funds-Diversified debt funds which invest in the

broad debt market• Gilt funds that invest only in Government

securities• Liquid and money market funds which

invest only in short term securities• Short term funds which invest in debt of

tenor higher than the money market funds.• Fixed term plans that invest in securities

and hold them to maturity, for a fixedperiod.

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 25/183

Balanced Funds

• Investment in more than oneasset class Debt and equity in comparable

proportions Pre-dominantly debt with some

exposure to equity Pre-dominantly equity with some

exposure to debt

• Education plans and children’splans are examples of balancedfunds

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 26/183

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 27/183

Basis for Classification

Investors choose funds based on theirobjective, risk appetite, time horizon andreturn expectations.

• Risk Sectoral funds are most risky; money

market funds are least risky• Tenor

Equity funds require a long investmenthorizon; liquid funds are for the short term

liquidity needs• Investment objective Equity funds suit growth objectives; debt

funds suit income objectives

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 28/183

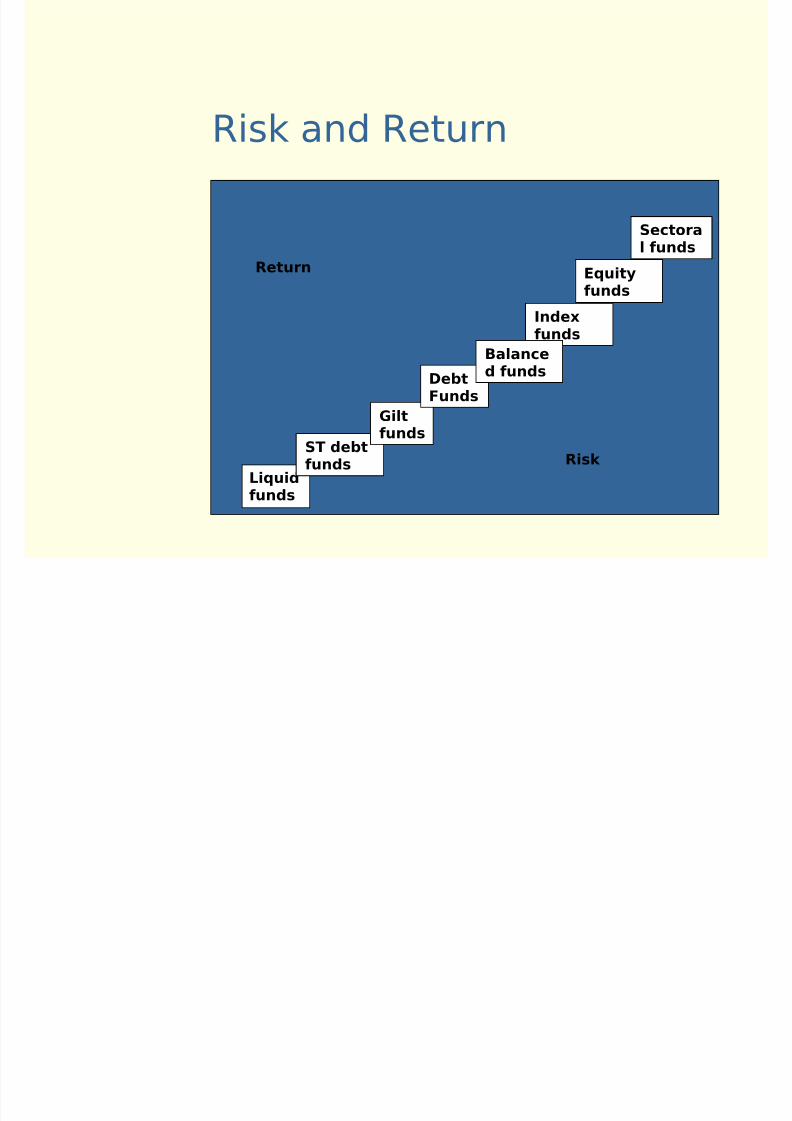

Risk and Return

Liquidfunds

ST debtfunds

Giltfunds

Debt

Funds

Indexfunds

Equityfunds

Sectoral funds

Balanced funds

Risk

Return

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 29/183

Mergers and Acquisitions

•

Scheme take over : If the schemes of one fund aretaken over by another fund, it is called as schemetake over. This requires SEBI and trustee approval.

• AMCs merger: If two AMCs merge, the stakes of sponsors changes and the schemes of both fundscome together. High court, SEBI and Trusteeapproval needed.

• AMC take-over : If one AMC or sponsor buys out theentire stake of another sponsor in an AMC, there is atake over of AMC. The sponsor who has sold out,exits the AMC. This needs high court approval aswell as SEBI and Trustee approval.

• Investors can choose to exit at NAV if they do notapprove of the transfer. They have a right to be

informed. No approval is required, in the case of open-ended funds.• For close-ended funds investor approval is required

for all cases of merger and take-over.

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 30/183

Session 2: Investing inMutual Funds:Understanding theProcess

• Offer Document• Investors/ unit holders rights

• Verification and Due Diligence

• Investing in a Fund Scheme

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 31/183

Offer Document/ KIM

• Legal offer from AMC to investor• Offer Document (OD) is the most important source

of information for investors.• Abridged version is called as Key Information

Memorandum (KIM).• Investors are required to read and understand the

offer document.• No recourse is available to investors for not reading

the OD or KIM• A glossary of important terms is included in the offer

document.• The cover page contains the details of the scheme

being offered and the names of sponsor, trustee and

AMC.• Mandatory disclaimer clause of SEBI should also be

on the cover page.• The borrowing restrictions on the mutual fund

should be disclosed. This includes the purposes andthe limits on borrowing.

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 32/183

Offer Document/ KIMContinue……

• OD is issued by the AMC on behalf of thetrustees.• KIM has to be compulsorily made available

along with the application form.• Close ended funds issue an offer document

at the time of the IPO.

• Open ended funds have to update OD atleastonce in 2 years.• Any change in scheme attributes calls for

updating the OD.• Addendums for financial data should be

submitted to SEBI and made available to

investors.• Trustees approve the contents of the OD andKIM.

• The format and content of the OD has to beas per SEBI Guidelines

• The AMC prepares the OD and is responsible

for the information contained in the OD.

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 33/183

• A scheme cannot make any guarantee of return,without stating the name of the guarantor, anddisclosing the networth of the guarantor.

• Information on existing schemes and financialsummary of existing schemes to be given for 3years.

• Information on transactions with associatecompanies to be provided for the past 3 years.• If any expense incurred is higher than what was

stated in the OD, for past schemes, explanationsshould be given.

• There is no information on other mutual funds,

their product or performance in the OD.• 3 years track record of investors’ complaints andredressal should be disclosed in the OD.

• Any pending cases or penalties against sponsorsor AMC should be disclosed in the OD.

• Investors’ rights are stated in the OD.

Offer Document/ KIMContinue……

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 34/183

Contents of OfferDocument• OD has to be submitted to SEBI prior to the launch of

the scheme.• The OD contains

Preliminary information on the fund and scheme Information on fund structure and constitution Fundamental attributes of the scheme Details of the offer

Fee structure and expenses Investor rights Information on income and expenses of existing

schemes• Risk factors, both standard and scheme-specific,

have to be disclosed• Factors common to all funds are called as standard

risk factors. These include market risk, noassurances of return, etc.

• Factors specific to a scheme are scheme-specific,risk factors in the Offer Document. These includerestrictions on liquidity such as lock-in period, risksof investing in the first scheme of a fund, etc.

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 35/183

Fundamental Attributes

Fundamental attributes of ascheme include:

Scheme type Objectives Investment pattern Fees and expenses

Liquidity conditions Accounting and valuation Investment restrictions, if any

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 36/183

Changes in FundamentalAttributes

• Investors approval is not neededbut Investors have right to be

informed• Public announcement by AMC

• Option to exit without load

• SEBI and Trustee approval

• New offer document

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 37/183

Unit Holder Rights/Investors

Investors have the right to inspecta number of documents. Theseare:

Trust deed Investment management agreement SEBI (MF) Regulations AMC Annual reports Unabridged offer document Annual reports of existing schemes

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 38/183

Unit Holder Rights

• Cannot sue the mutual fund• Complaints against AMC, sponsor

and BoT

•

75% unit holders can• wind up a scheme• seek AMC termination

• Prospective investor has no

rights• Right to redeem for fundamental

changes without exit load

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 39/183

Verification and DueDiligence

• Compliance Officer has to sign the duediligence certificate. He is usually anAMC employee.

• The due diligence certificate states that Information in the OD is according to

SEBI formats Information is verified and is true and fair

representation of facts

All constituents of the fund are SEBIregistered.

• SEBI does not approve or certify thecontents of the OD.

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 40/183

Investing in a Fund

Scheme• Units or amount

• Certificates and account statement

• Minimum amount• Initial offer and subsequent buying

• List of eligible investors Check eligibility with offer document Foreign investors not eligible (FII

Regulations)

• Documents for classes of investors

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 41/183

Distribution Channels

• Individual agents

• Institutional Distributors

Banks Distribution companies

• NBFCs Direct marketing channels

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 42/183

Individual Agents

• Wide network

• Certification AMFI registration No. (ARN) card

necessary before selling

• Commission structure Initial and Trail

• Loyalty and volume incentives

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 43/183

Institutional Distributors

• Banks HNIs and personal banking

• Distribution companies

NBFCs• Service and collection

• Advisory

• Direct Marketing Direct Service Agents Investor Service Centres e.g CAMS

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 44/183

Procedure

• Proof of purchase Certificate Account statement

• Application form- contents Single Joint holding Minor Nomination PAN number Tax status Folio number Bank details

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 45/183

Session 3: Accounting,

Valuation & Taxation

• Accounting

• NAV & Pricing• Accounting policies

• Valuation norms for mutual funds

• Taxation of mutual funds

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 46/183

Mutual Fund Accounting

• Knowledge of MF accounting vital

• Separate balance sheet for each scheme of aMF

• MFs to follow Accounting policies laid down by

SEBI (Mutual Fund) Regulations, 1996• Unit holdes’ subscriptions accounted

Not as liabilities or deposits But as Unit Capital at face value

• Investments made by the fund appear on assetside in the Balance sheet

• All assets of the scheme belongs to investors

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 47/183

NAV and Load

• Date on which NAV is calculated is called valuation date

• Open ended funds are required to compute and discloseNAV daily

• Close ended Funds can compute NAV’s every week NAVcalculation has to consider up to date transactions

• Sale and repurchase price are NAV-based

Cut-off time for NAV: The cut –off time for all mutualfund schemes except liquid fund schemes is 3 pm

For all valid applications received before the cut-off time, units are allotted /cancelled based on NAV at theend of the same day & after the cut-off time , NAV of the next business day.

The above rule does not apply to liquid fund schemes

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 48/183

NAV and Load• Load is a charge on the NAV

Entry load is charged on NAV and increasesthe sale price

Exit load is charged on NAV and reduces therepurchase price

•

Load is defined as a percentage• Load is primarily used to meet the expenses related

to sale and distribution of units.

• An exit load that varies with the holding period of aninvestor is called as CDSC (Contingent deferred sales

charge).• Loads are subject to SEBI Regulation and vary

depending on industry practice

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 49/183

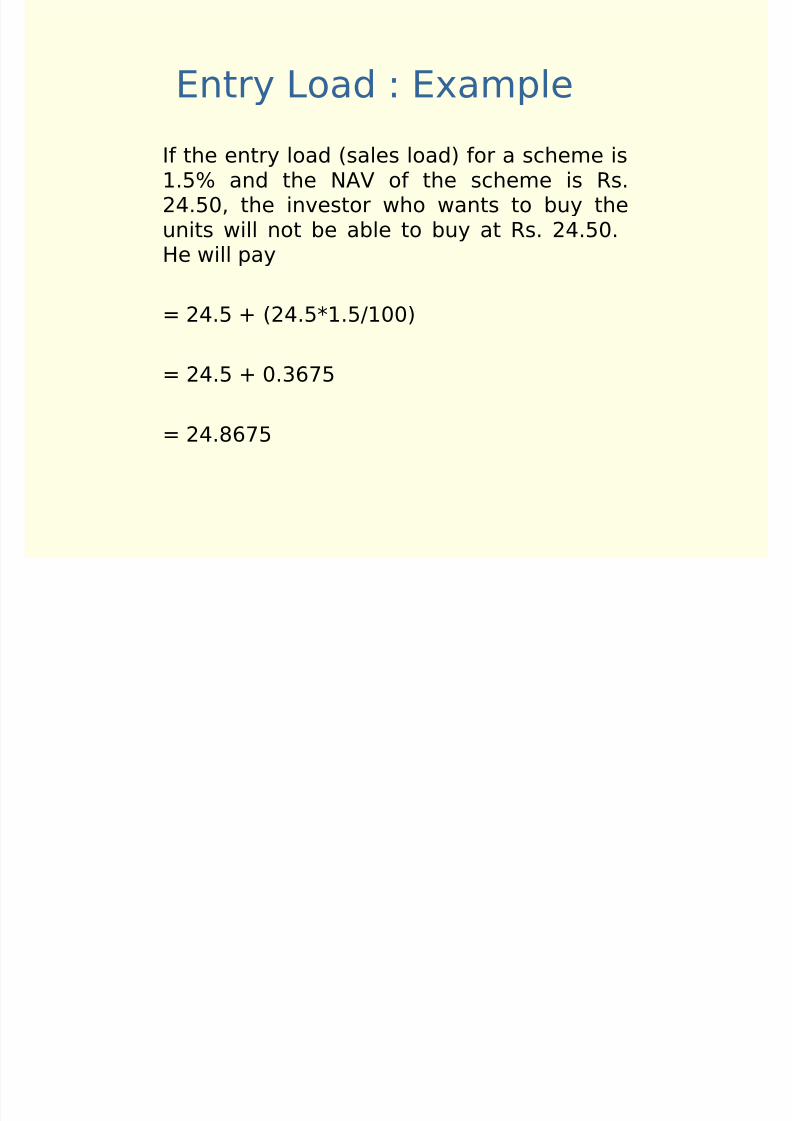

Entry Load : Example

If the entry load (sales load) for a scheme is1.5% and the NAV of the scheme is Rs.24.50, the investor who wants to buy theunits will not be able to buy at Rs. 24.50.He will pay

= 24.5 + (24.5*1.5/100)

= 24.5 + 0.3675

= 24.8675

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 50/183

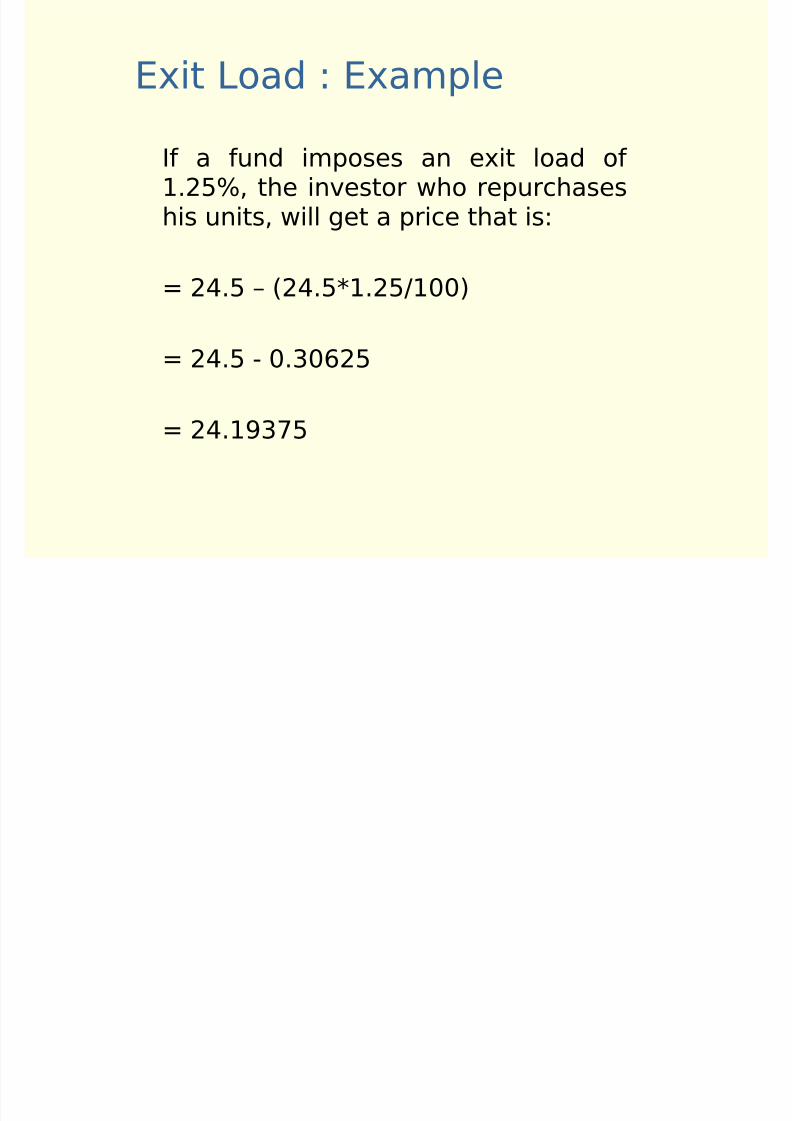

Exit Load : Example

If a fund imposes an exit load of 1.25%, the investor who repurchaseshis units, will get a price that is:

= 24.5 – (24.5*1.25/100)

= 24.5 - 0.30625

= 24.19375

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 51/183

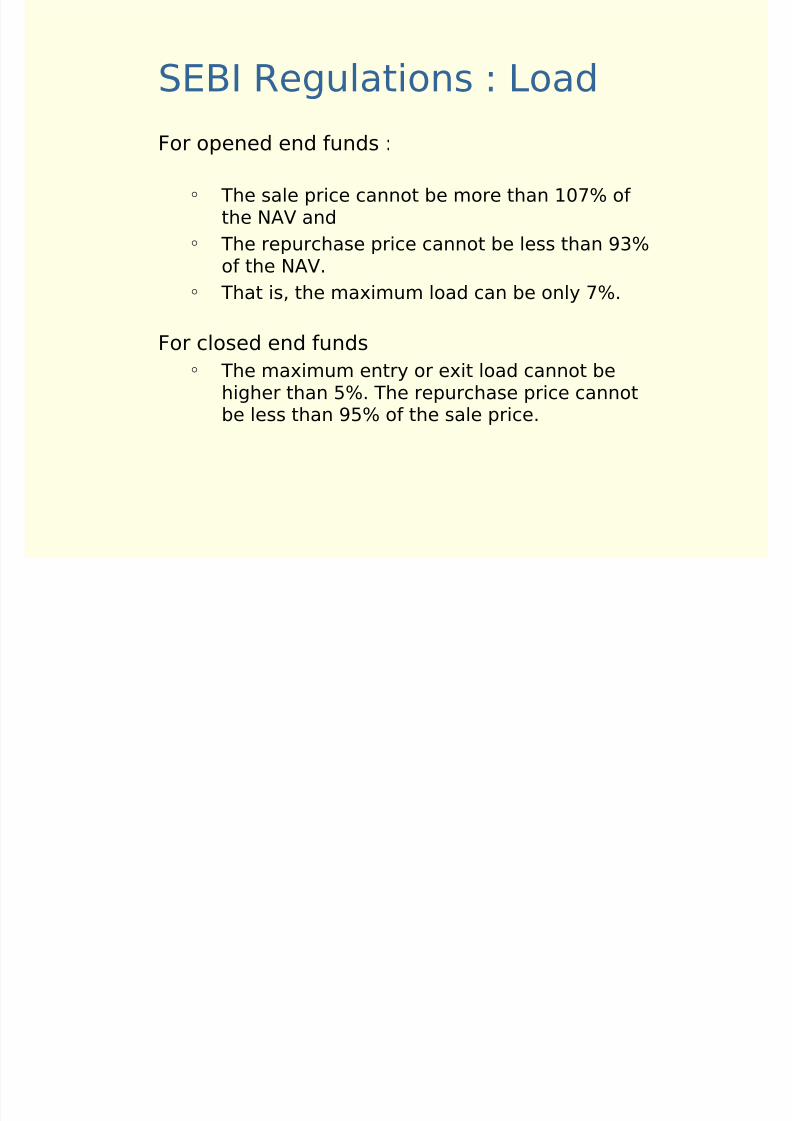

SEBI Regulations : Load

For opened end funds :

The sale price cannot be more than 107% of the NAV and

The repurchase price cannot be less than 93%

of the NAV. That is, the maximum load can be only 7%.

For closed end funds The maximum entry or exit load cannot be

higher than 5%. The repurchase price cannotbe less than 95% of the sale price.

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 52/183

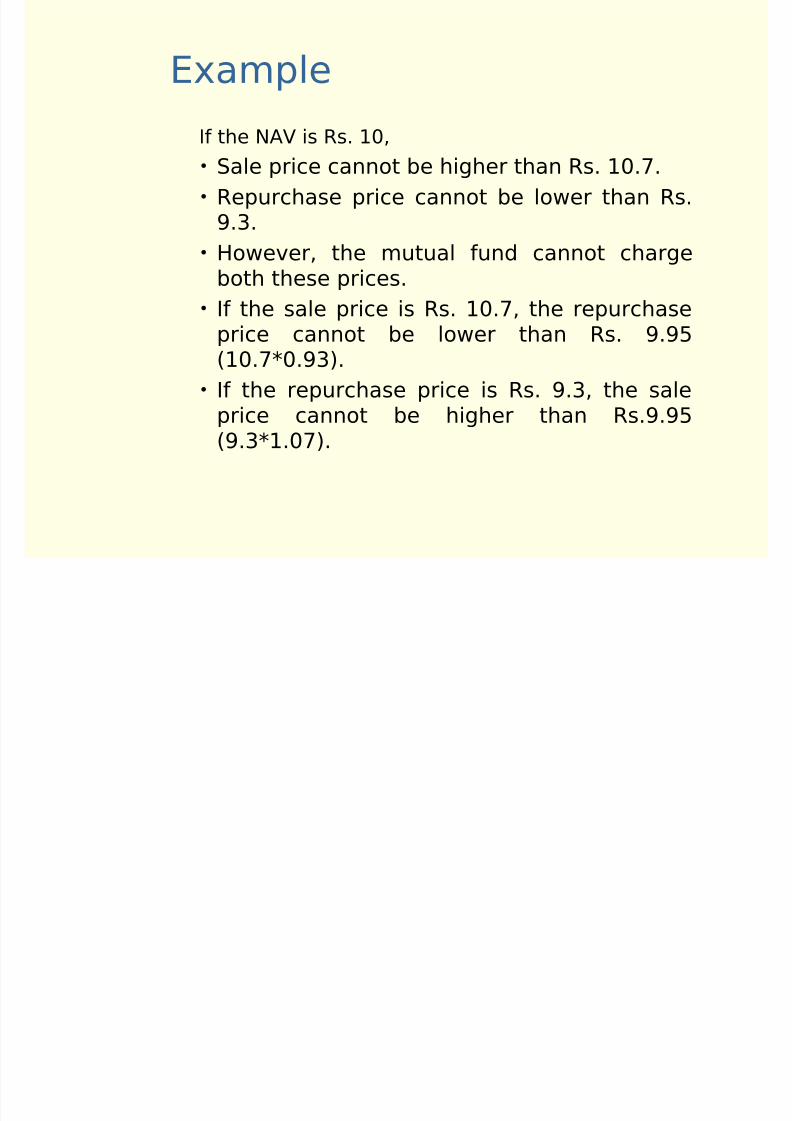

Example

If the NAV is Rs. 10,• Sale price cannot be higher than Rs. 10.7.

• Repurchase price cannot be lower than Rs.9.3.

• However, the mutual fund cannot chargeboth these prices.

• If the sale price is Rs. 10.7, the repurchaseprice cannot be lower than Rs. 9.95(10.7*0.93).

•

If the repurchase price is Rs. 9.3, the saleprice cannot be higher than Rs.9.95(9.3*1.07).

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 53/183

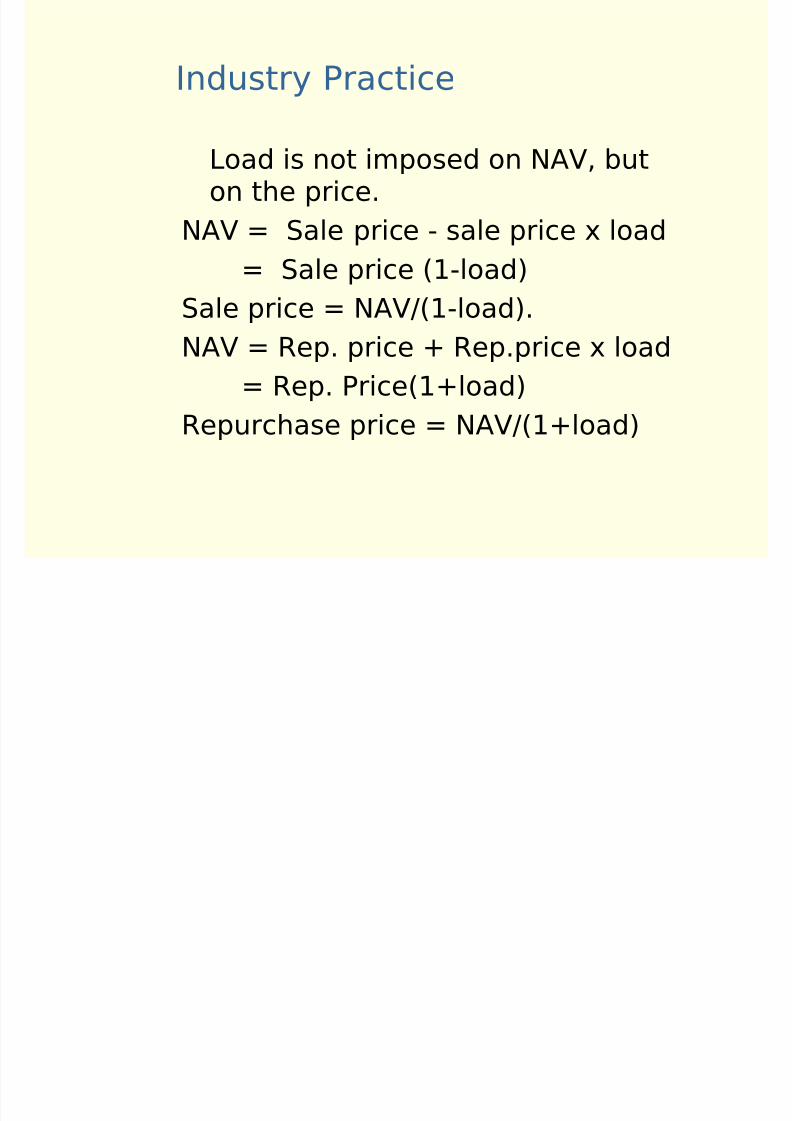

Industry Practice

Load is not imposed on NAV, buton the price.

NAV = Sale price - sale price x load

= Sale price (1-load)Sale price = NAV/(1-load).

NAV = Rep. price + Rep.price x load

= Rep. Price(1+load)Repurchase price = NAV/(1+load)

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 54/183

Example

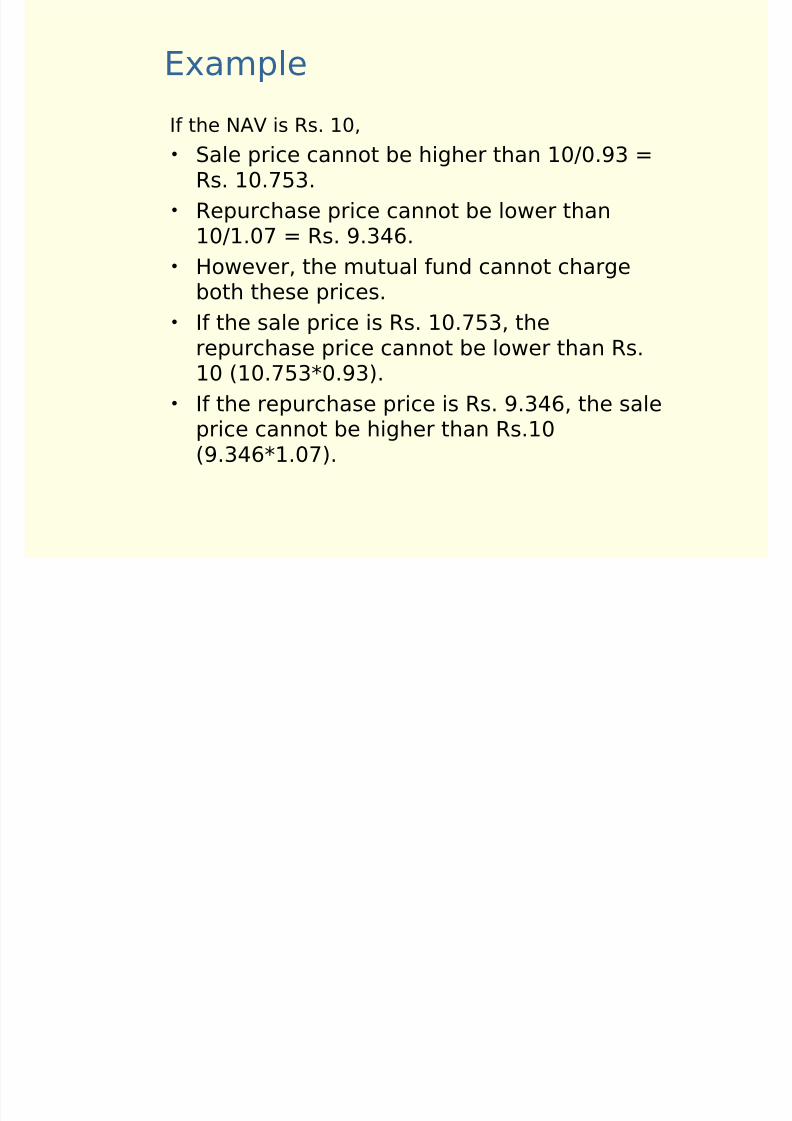

If the NAV is Rs. 10,

• Sale price cannot be higher than 10/0.93 =Rs. 10.753.

• Repurchase price cannot be lower than10/1.07 = Rs. 9.346.

• However, the mutual fund cannot chargeboth these prices.

• If the sale price is Rs. 10.753, therepurchase price cannot be lower than Rs.10 (10.753*0.93).

• If the repurchase price is Rs. 9.346, the saleprice cannot be higher than Rs.10(9.346*1.07).

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 55/183

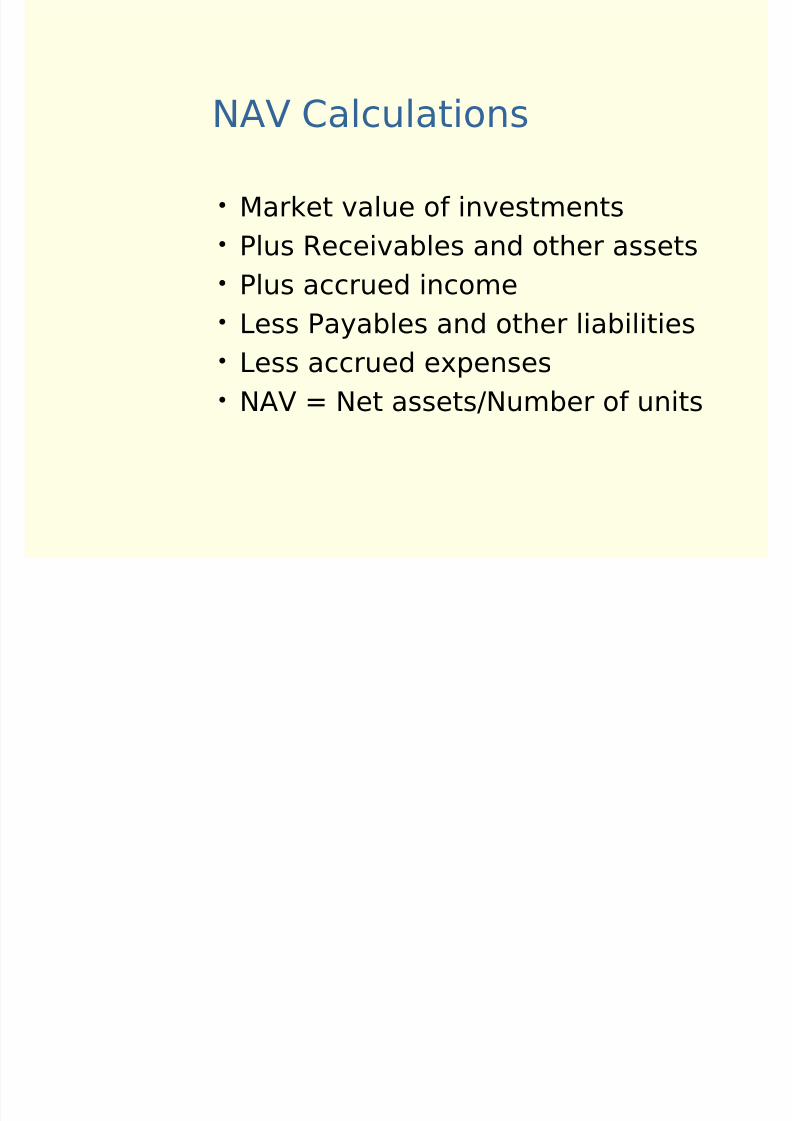

NAV Calculations

• Market value of investments

• Plus Receivables and other assets

• Plus accrued income

• Less Payables and other liabilities

• Less accrued expenses

• NAV = Net assets/Number of units

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 56/183

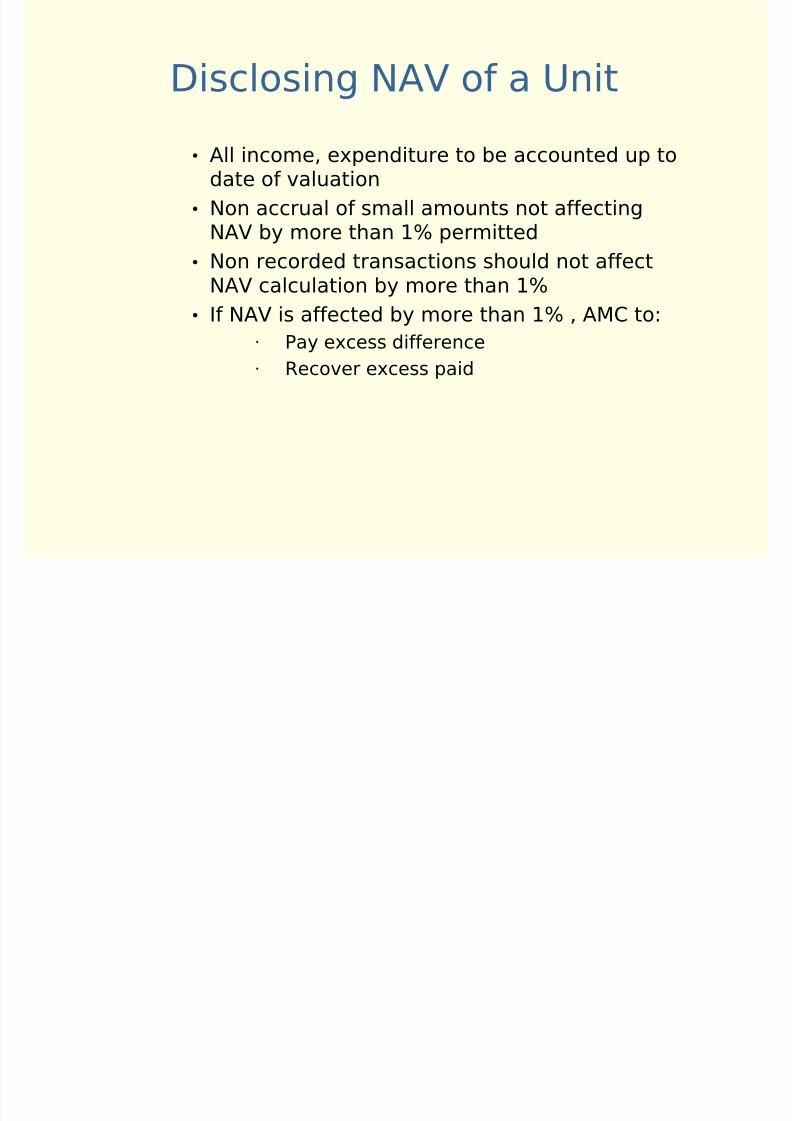

Disclosing NAV of a Unit

• All income, expenditure to be accounted up todate of valuation

• Non accrual of small amounts not affectingNAV by more than 1% permitted

• Non recorded transactions should not affectNAV calculation by more than 1%

• If NAV is affected by more than 1% , AMC to:• Pay excess difference

• Recover excess paid

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 57/183

Factors affecting NAV

NAV is affected by 4 set of factors:q Purchase & sale of

investment securities

q

Valuation of all investmentsecurities held

q Other assets and liabilities

q Units sold or redeemed

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 58/183

Sources of Income• Interest

• Dividend

• Profit from sale of investments• Other income

• Extra-ordinary income

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 59/183

Charges in MF

Mutual funds can recover two types of expenses:

• Initial issue expenses

• Recurring expenses

• Initial issue expenses: Expenses incurred

in floating schemes Effective April 04,2006 allowed up to 6% for

close ended funds only Close ended funds can not charge entry loads Open ended funds can recover initial expenses

through entry load

Initial issue expenses

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 60/183

Initial issue expenses

• Limit of 6% of initial resources raised under the scheme;excess expenses to be borne by AMC/sponsor

• CEF : Amortise on weekly basis until maturity• OEF : For an open-ended scheme, the initial issue

expenses are carried in the balance sheet of the fund as“deferred revenue expenses.” They are written off over aperiod not exceeding 5 years.

• A fund that does not charge any of the initial issue

expenses is called a no-load fund. AMCs can charge 1%higher investment management fee in this case.

• Open-ended fund should meet the expenses related tosales and distribution of schemes from the entry load andnot through initial issue expenses.

• In case of CEF, Investors exiting before expiry of period of

scheme will be charged unrecovered initial expenses• Conversion of CEF into OEF allowed only after recovery of

un-recovered initial expenses

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 61/183

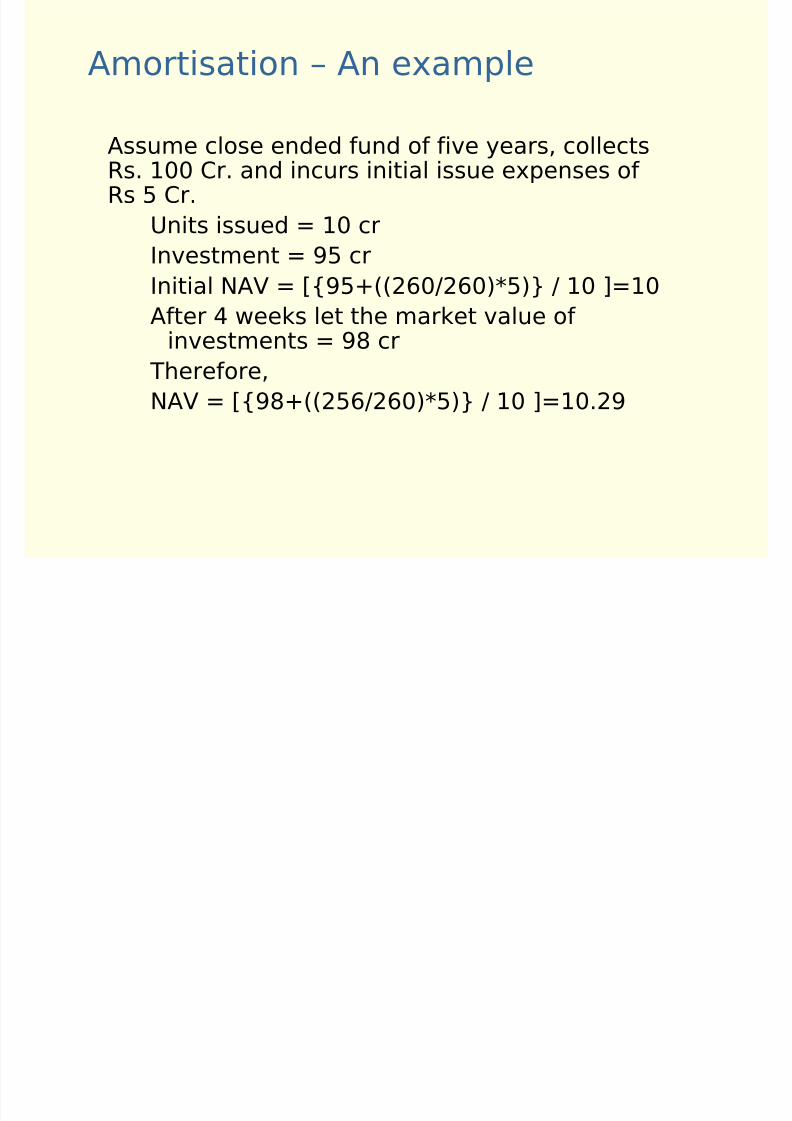

Amortisation – An example

Assume close ended fund of five years, collectsRs. 100 Cr. and incurs initial issue expenses of Rs 5 Cr.

Units issued = 10 cr

Investment = 95 cr

Initial NAV = [{95+((260/260)*5)} / 10 ]=10

After 4 weeks let the market value of investments = 98 cr

Therefore,

NAV = [{98+((256/260)*5)} / 10 ]=10.29

Impact of initial issue expenses on

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 62/183

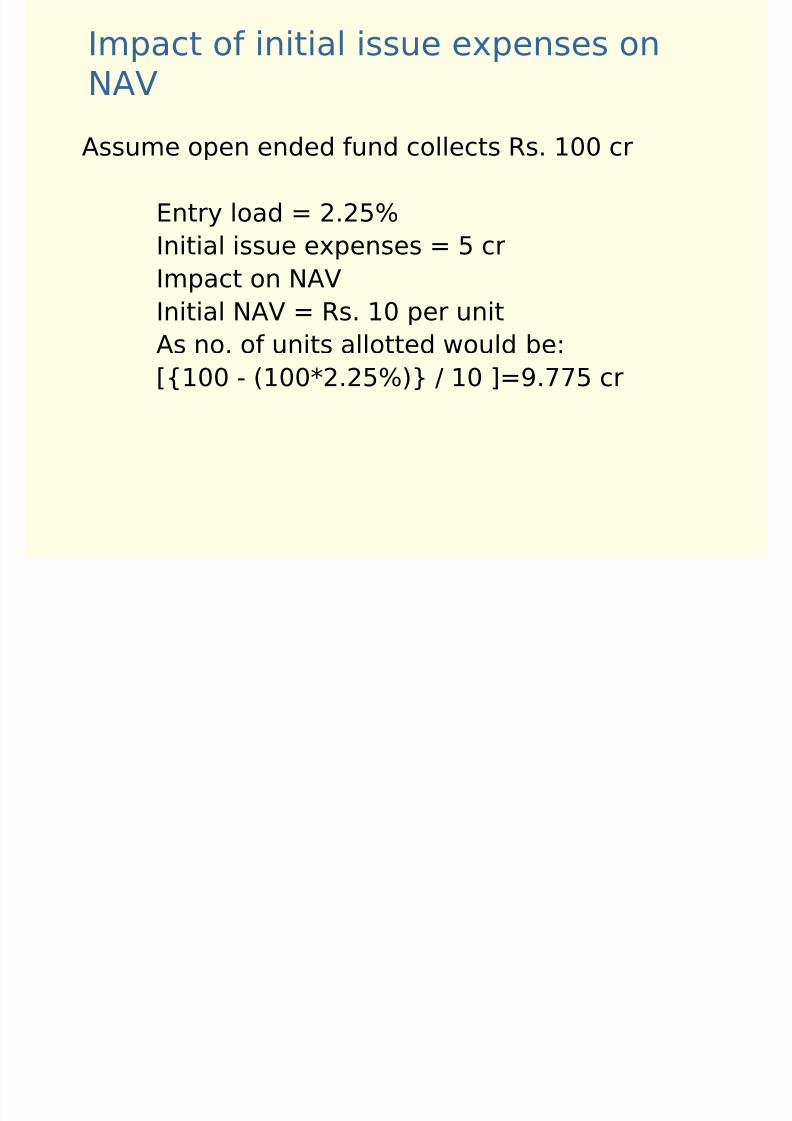

Impact of initial issue expenses onNAV

Assume open ended fund collects Rs. 100 cr

Entry load = 2.25%

Initial issue expenses = 5 cr

Impact on NAV

Initial NAV = Rs. 10 per unit

As no. of units allotted would be:

[{100 - (100*2.25%)} / 10 ]=9.775 cr

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 63/183

Recurring / OperatingExpenses

• Investment management fees

• Custodian’s fees

• Trustee Fees

• Registrar and transfer agent fees• Marketing and distribution expenses

• Other Operating expenses

• Audit fees

• Legal expenses• Costs of mandatory advertisements

and communications to investors

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 64/183

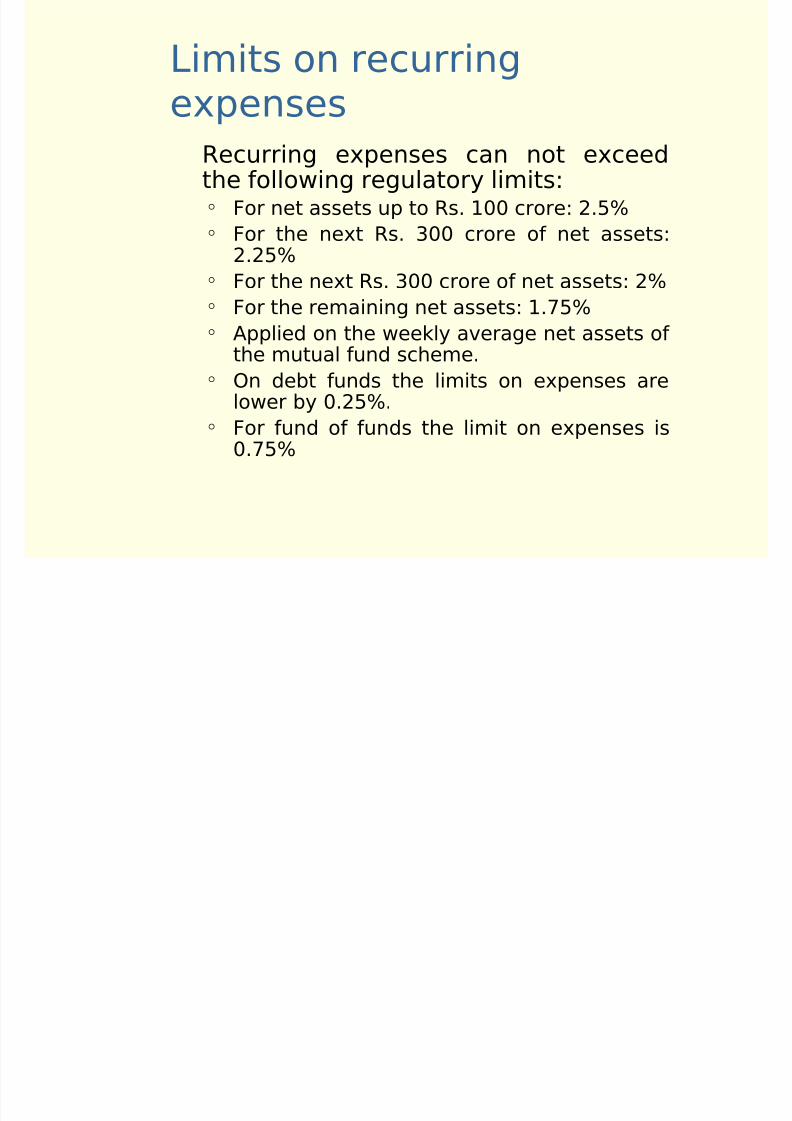

Limits on recurringexpenses

Recurring expenses can not exceedthe following regulatory limits: For net assets up to Rs. 100 crore: 2.5% For the next Rs. 300 crore of net assets:

2.25% For the next Rs. 300 crore of net assets: 2% For the remaining net assets: 1.75% Applied on the weekly average net assets of

the mutual fund scheme. On debt funds the limits on expenses are

lower by 0.25%. For fund of funds the limit on expenses is

0.75%

Investment (Asset) Management

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 65/183

Investment (Asset) ManagementFees

AMC charges Asset management fees: thelimits as per SEBI regulations are as follows: For the first Rs. 100 crore of net assets: 1.25% For net assets exceeding Rs. 100 crore: 1.00% 1% higher fee for no load funds

Asset management fees are not in addition to but a partof recurring expenses

Asset management fees are usually lower for debtfunds as compared to equity funds and are disclosed inOD

Balance of Deferred Revenue Expenses not included innet assets for computing investment management feeIn other words un-amortized portion added for NAVcalculation as other asset but no AMC fee on thisamount

h b

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 66/183

Expenses that cannot becharged

• Penalties and fines for infraction of laws.

• Interest on delayed payments to unit holders.

• Legal, marketing and publication expenses notattributable to any scheme.

• Expenses on investment and generalmanagement.

• Expenses on general administration, corporateadvertising and infrastructure costs.

• Expenses on fixed assets and softwaredevelopment expenses.

• Such other costs as may be prohibited by SEBI.

Disclosure and reporting

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 67/183

Disclosure and reportingrequirements

• AMC to prepare annual report and annualstatement of account for each scheme

• Annual statement of account to be audited byan auditor independent of the auditor of AMC

• Within 6 months of accounting year, Fund shall

–Publish scheme wise abridged summaryof report in newspapers

–Mail summary of report to all unit holders

–Forward to SEBI annual audited accounts,

half yearly unaudited accounts, Quarterlyportfolio statement

–Display the scheme wise annual reportson their website & on AMFI website

–Mail Annual reports to all unit holders

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 68/183

Accounting Policies

• Investments to be marked to market• Unrealized appreciation can’t be distributed

• Dividend/bonus recognized on the date shareis quoted ex-dividend/ex-bonus

• Average cost considered for determining

gain/loss on sale of shares• Purchase / Sale of investments recognized: On

the trade date , not on settlement date

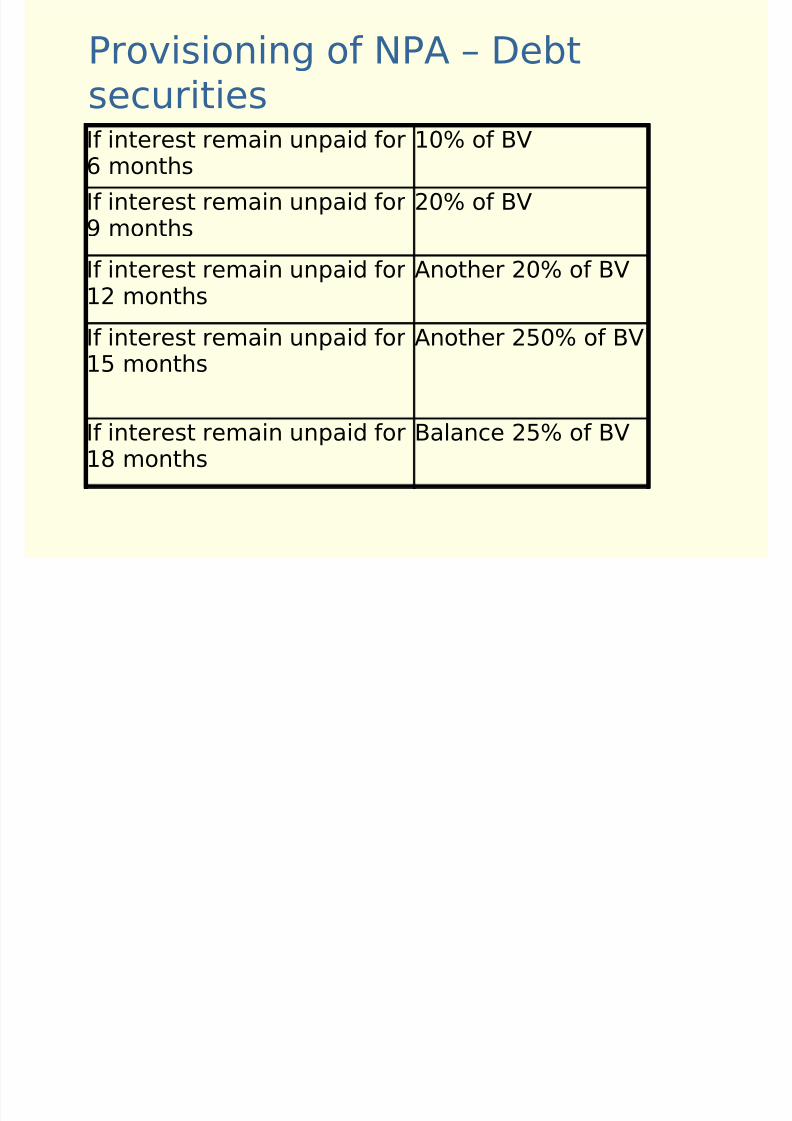

• Debt investments to be taken as NPA :

–If interest or principal amount remains

unpaid for more than 3 months–E.g. if interest due 30th June 2000 remainsunpaid on 1/10/2000 it becomes NPA on1/10/2000

Provisioning of NPA Debt

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 69/183

Provisioning of NPA – Debtsecurities

If interest remain unpaid for6 months

10% of BV

If interest remain unpaid for9 months

20% of BV

If interest remain unpaid for12 months

Another 20% of BV

If interest remain unpaid for15 months

Another 250% of BV

If interest remain unpaid for18 months

Balance 25% of BV

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 70/183

Valuation norms

for mutual funds

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 71/183

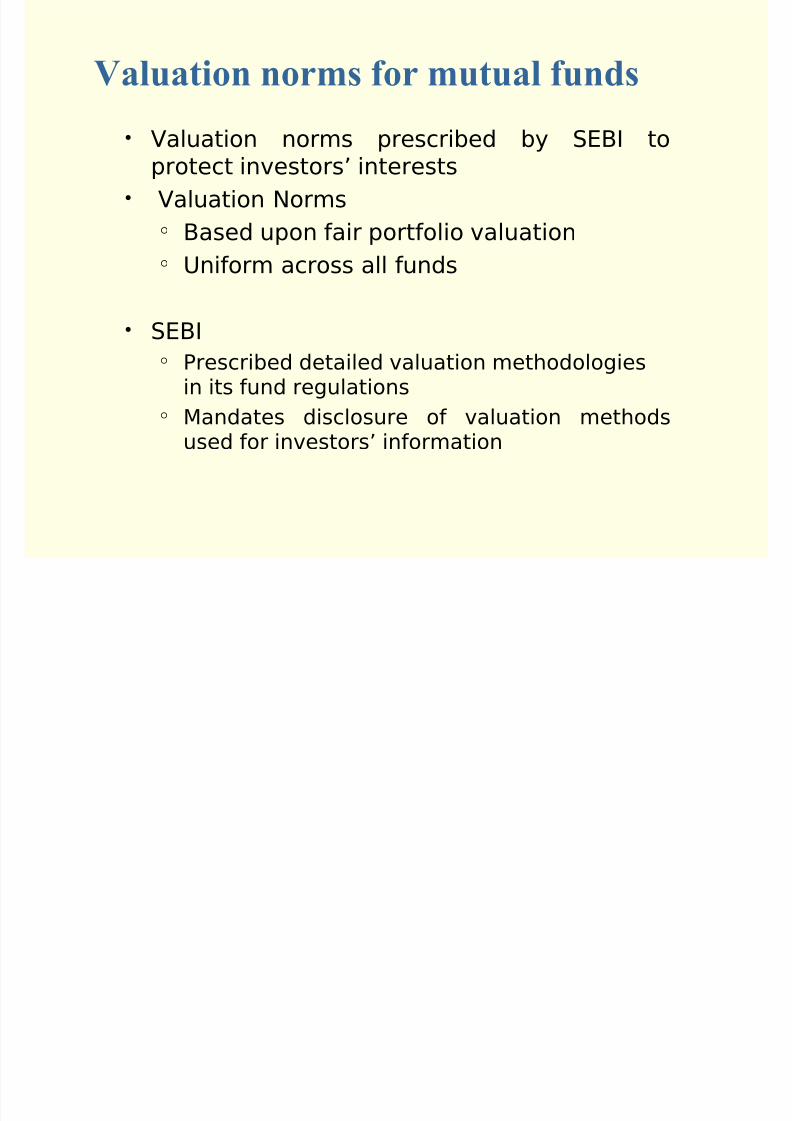

• Valuation norms prescribed by SEBI toprotect investors’ interests

• Valuation Norms Based upon fair portfolio valuation

Uniform across all funds

• SEBI Prescribed detailed valuation methodologies

in its fund regulations Mandates disclosure of valuation methods

used for investors’ information

Valuation norms for mutual funds

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 72/183

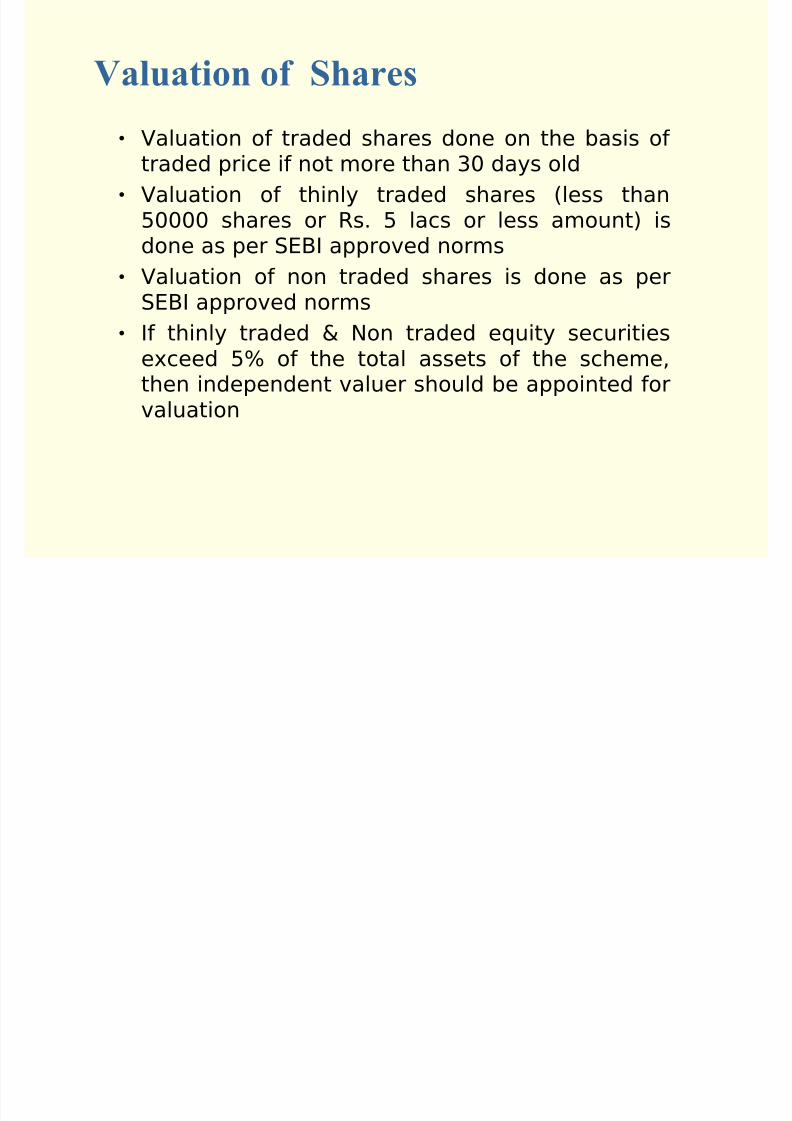

• Valuation of traded shares done on the basis of traded price if not more than 30 days old

• Valuation of thinly traded shares (less than50000 shares or Rs. 5 lacs or less amount) isdone as per SEBI approved norms

• Valuation of non traded shares is done as perSEBI approved norms

• If thinly traded & Non traded equity securitiesexceed 5% of the total assets of the scheme,then independent valuer should be appointed for

valuation

Valuation of Shares

V l ti f Sh

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 73/183

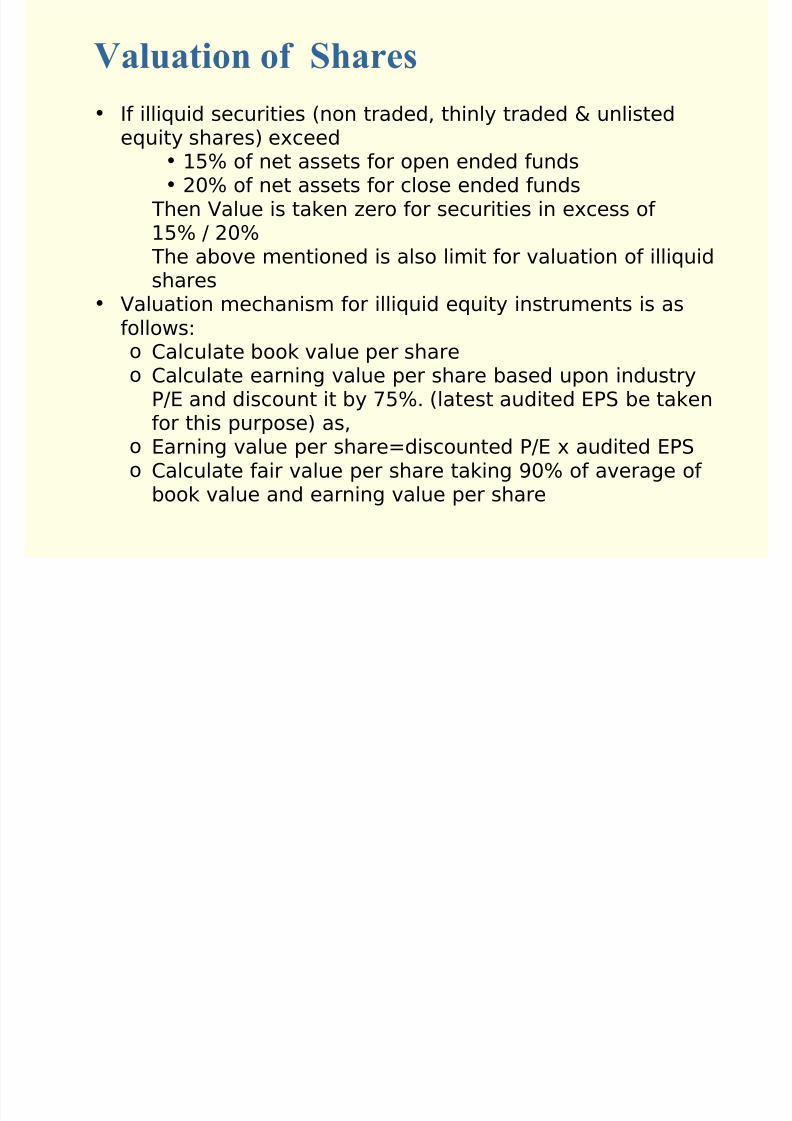

• If illiquid securities (non traded, thinly traded & unlisted

equity shares) exceed• 15% of net assets for open ended funds• 20% of net assets for close ended funds

Then Value is taken zero for securities in excess of 15% / 20% The above mentioned is also limit for valuation of illiquid

shares• Valuation mechanism for illiquid equity instruments is as

follows:o Calculate book value per shareo Calculate earning value per share based upon industry

P/E and discount it by 75%. (latest audited EPS be takenfor this purpose) as,

o Earning value per share=discounted P/E x audited EPSo Calculate fair value per share taking 90% of average of

book value and earning value per share

Valuation of Shares

V l ti A l

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 74/183

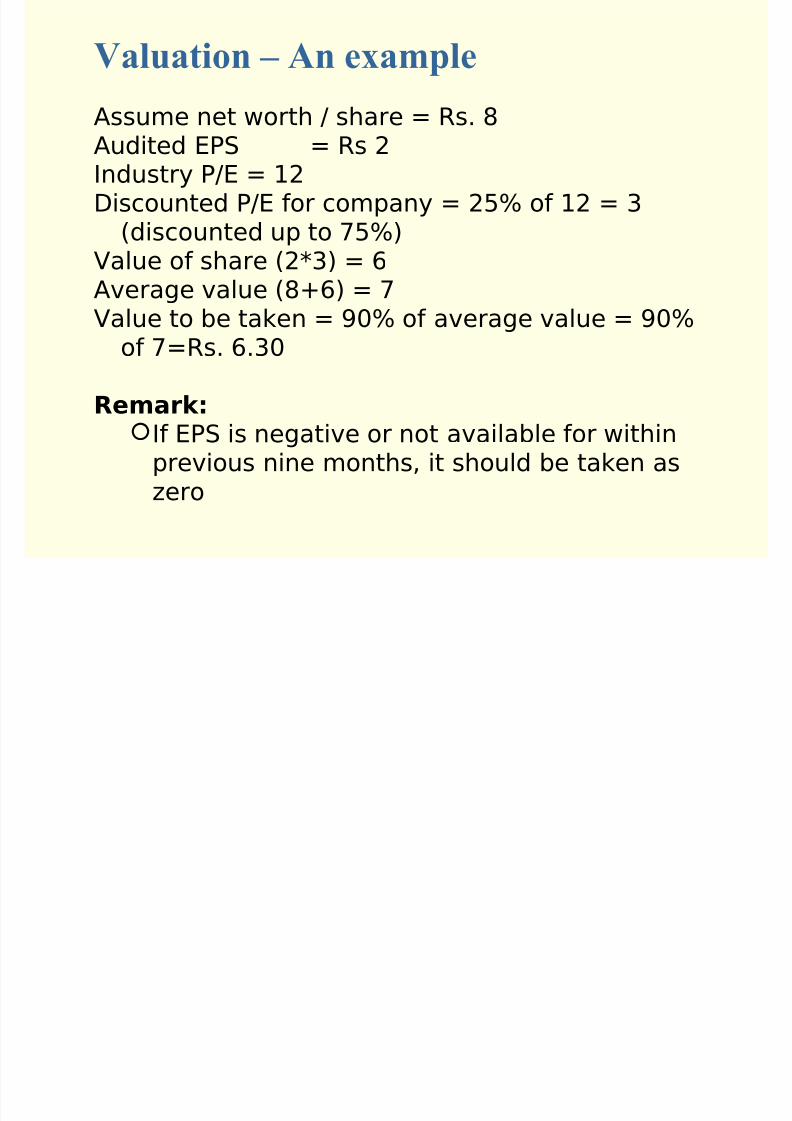

Assume net worth / share = Rs. 8

Audited EPS = Rs 2Industry P/E = 12Discounted P/E for company = 25% of 12 = 3

(discounted up to 75%)

Value of share (2*3) = 6Average value (8+6) = 7Value to be taken = 90% of average value = 90%

of 7=Rs. 6.30

Remark:If EPS is negative or not available for within

previous nine months, it should be taken aszero

Valuation – An example

Val ation of traded debt sec rities

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 75/183

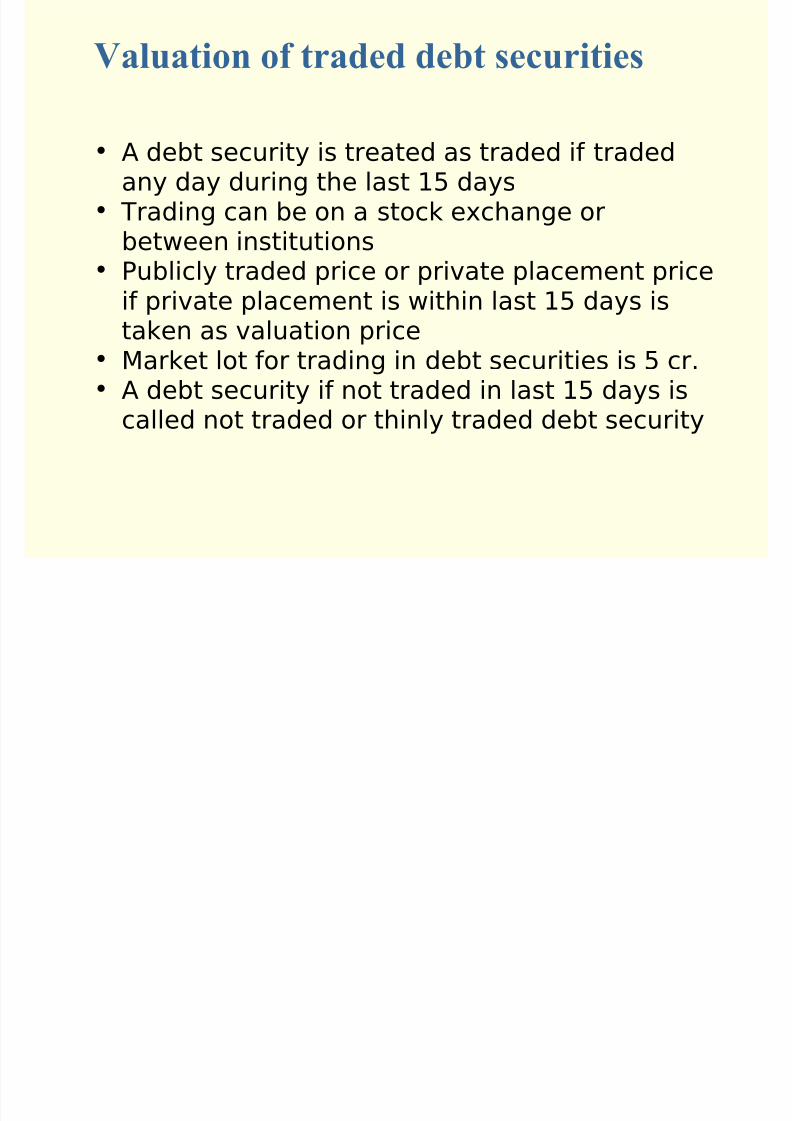

• A debt security is treated as traded if tradedany day during the last 15 days

• Trading can be on a stock exchange orbetween institutions

• Publicly traded price or private placement priceif private placement is within last 15 days istaken as valuation price

• Market lot for trading in debt securities is 5 cr.•

A debt security if not traded in last 15 days iscalled not traded or thinly traded debt security

Valuation of traded debt securities

Valuation of thinly traded and non

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 76/183

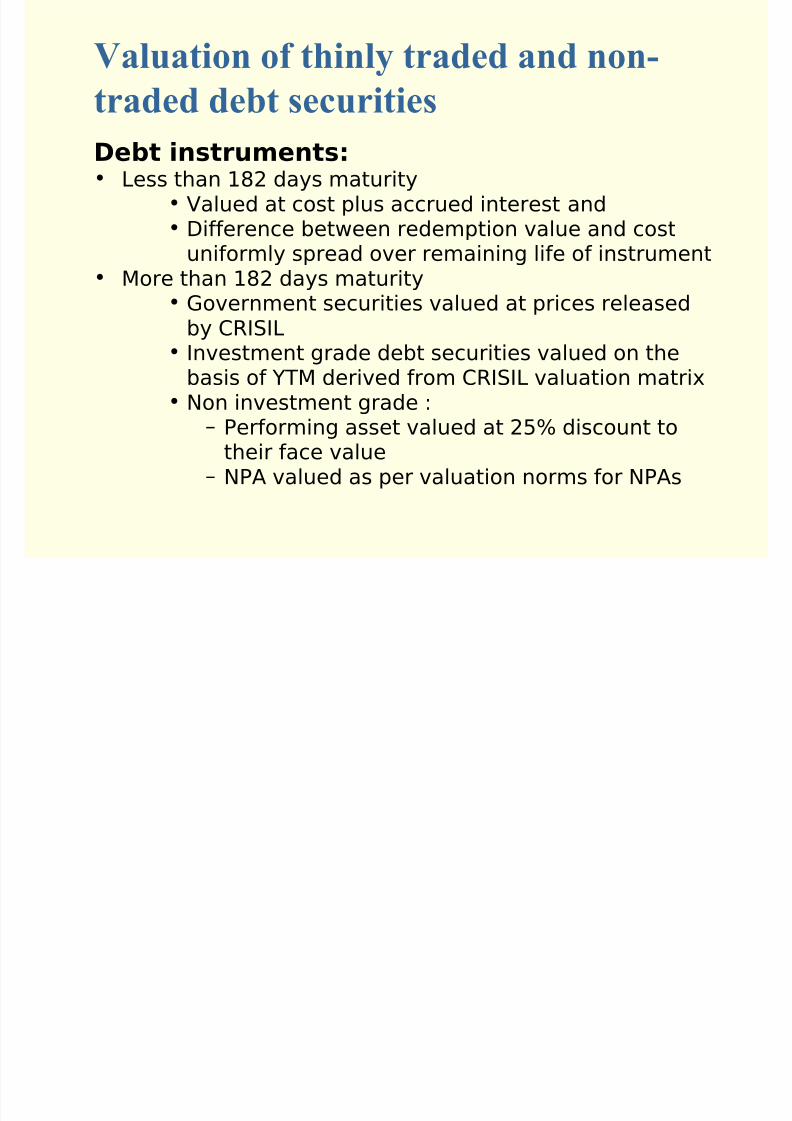

Debt instruments:• Less than 182 days maturity

• Valued at cost plus accrued interest and• Difference between redemption value and cost

uniformly spread over remaining life of instrument

• More than 182 days maturity• Government securities valued at prices released

by CRISIL• Investment grade debt securities valued on the

basis of YTM derived from CRISIL valuation matrix

• Non investment grade :– Performing asset valued at 25% discount to

their face value– NPA valued as per valuation norms for NPAs

Valuation of thinly traded and non-

traded debt securities

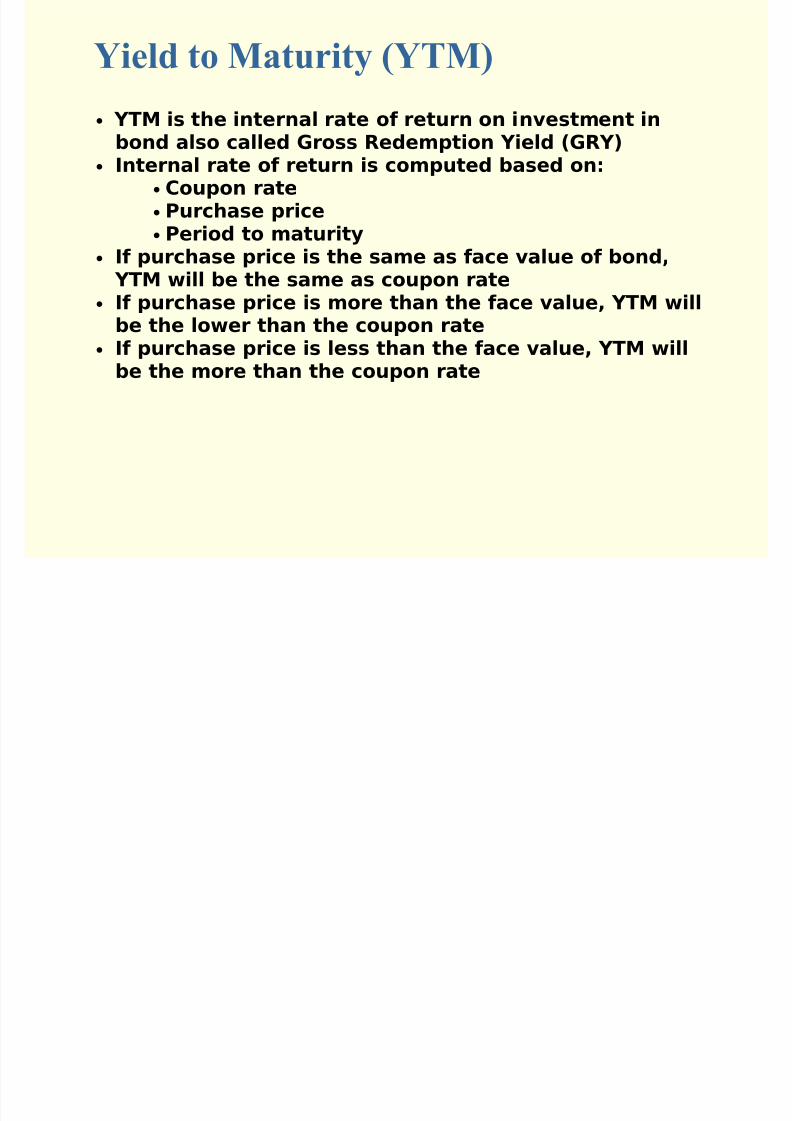

Yield to Maturity (YTM)

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 77/183

• YTM is the internal rate of return on investment in

bond also called Gross Redemption Yield (GRY)• Internal rate of return is computed based on:

•Coupon rate

•Purchase price

•Period to maturity

• If purchase price is the same as face value of bond,

YTM will be the same as coupon rate• If purchase price is more than the face value, YTM will

be the lower than the coupon rate

• If purchase price is less than the face value, YTM willbe the more than the coupon rate

Yield to Maturity (YTM)

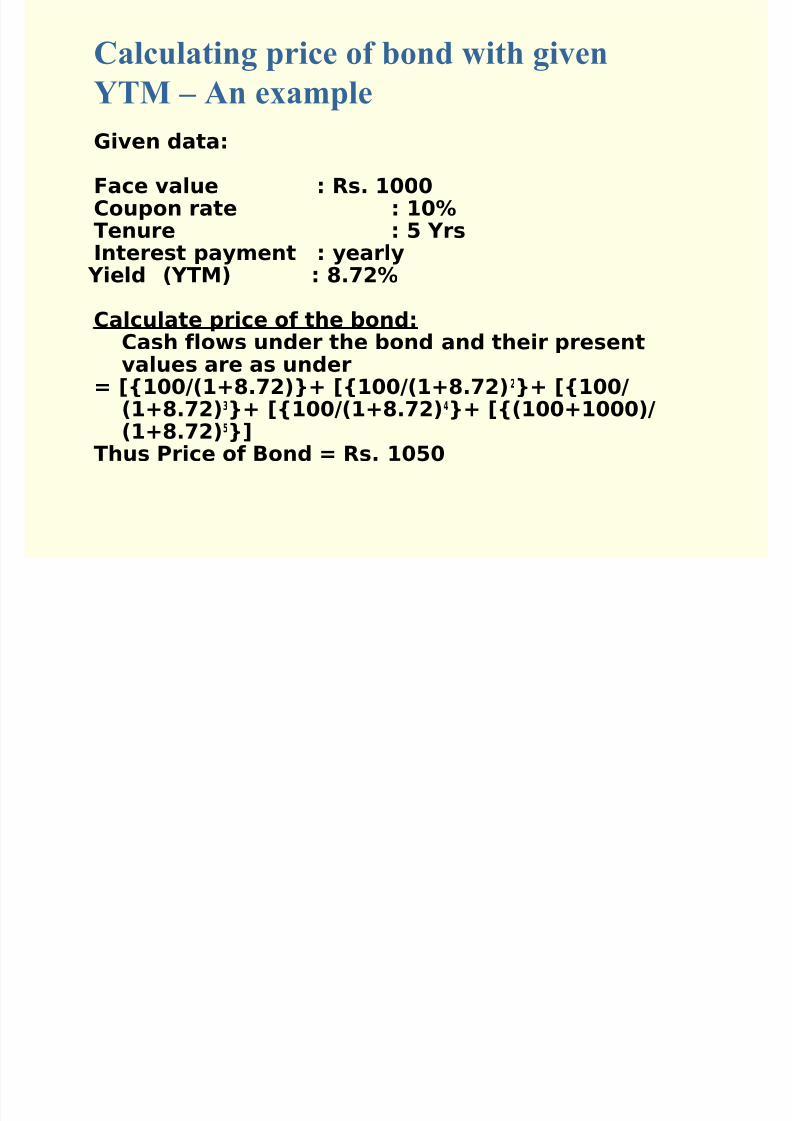

Calculating price of bond with given

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 78/183

Given data:

Face value : Rs. 1000Coupon rate : 10%Tenure : 5 YrsInterest payment : yearly

Yield (YTM) : 8.72%

Calculate price of the bond:Cash flows under the bond and their presentvalues are as under

= [{100/(1+8.72)}+ [{100/(1+8.72)2}+ [{100/

(1+8.72)3}+ [{100/(1+8.72)4}+ [{(100+1000)/(1+8.72)5}]

Thus Price of Bond = Rs. 1050

Calculating price of bond with given

YTM – An example

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 79/183

Taxation of mutualfunds

• Income for investors

–Dividend

–Capital gain

Taxation of MFs and

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 80/183

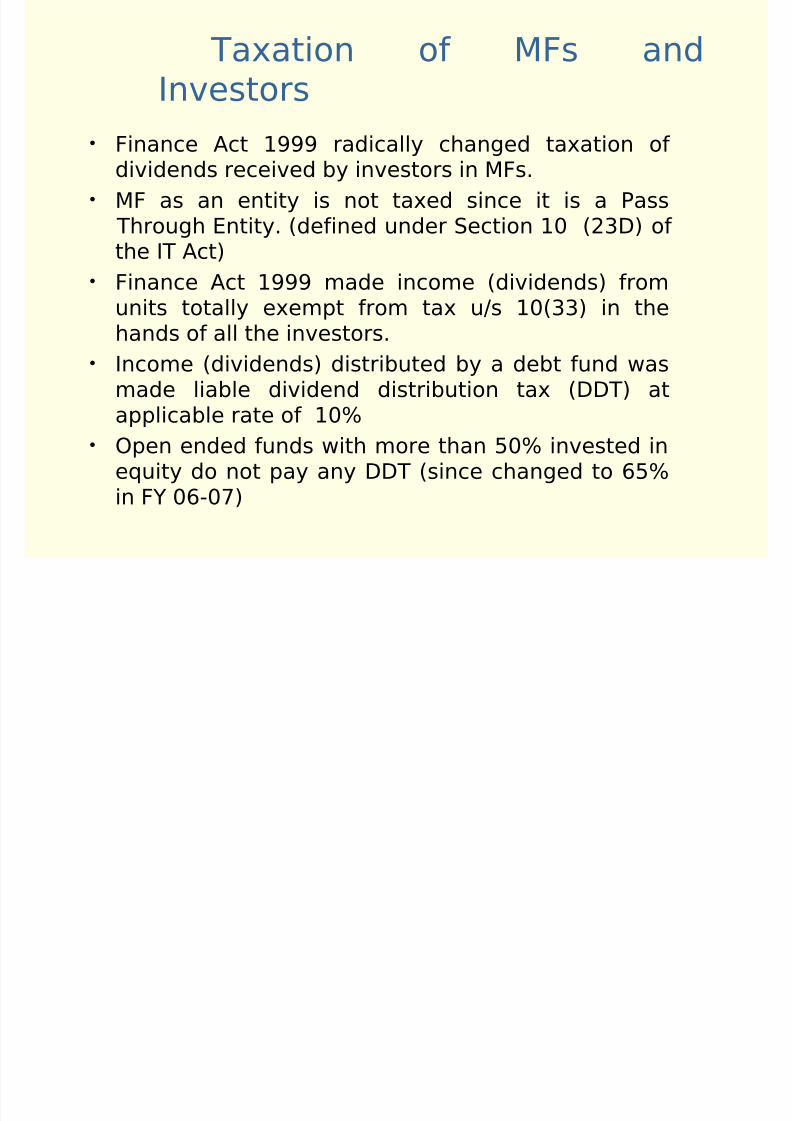

Taxation of MFs andInvestors

• Finance Act 1999 radically changed taxation of dividends received by investors in MFs.

• MF as an entity is not taxed since it is a Pass Through Entity. (defined under Section 10 (23D) of the IT Act)

• Finance Act 1999 made income (dividends) fromunits totally exempt from tax u/s 10(33) in thehands of all the investors.

• Income (dividends) distributed by a debt fund wasmade liable dividend distribution tax (DDT) atapplicable rate of 10%

• Open ended funds with more than 50% invested inequity do not pay any DDT (since changed to 65%in FY 06-07)

Taxation of MFs and

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 81/183

Investors

• Impact of DDT: Investor pays the tax indirectly, since NAV comes down to

the extend of tax paid by the fund DDT bears no relationship to the investor’s tax bracket. Dividend reinvested is also subject to DDT

In growth plans, DDT not applied, since no dividend isdistributed.

• Securities transaction tax (STT) is charged as applicable

• 80 C benefit for ELSS upto Rs. 1 lac

• Restriction on dividend stripping (Sec 94(7))

Within 3 months prior to record date of dividenddistribution and

Within 3 months after record date for dividenddistribution

Treatment of Capital Gains

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 82/183

Treatment of Capital Gains

• Long term: > 12 months

• Short term: < 12 months• Long term capital gains subject to indexation

benefit 20% +surcharge after indexation 10% + surcharge without indexation

• Short term capital gains taxed at normal tax ratesas applicable to investors.

• U/s 111(a) of IT Act: No long term gains tax on equity oriented schemes if STT

charged Short term capital gains tax at 10% on equity oriented

schemes if STT charged

• Indexation benefit on unlisted bonds not available

Treatment of Capital Gains

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 83/183

Treatment of Capital Gains

• No capital gain tax payable if entirecapital gain invested in capital gainbonds of NABARD, NHAI, REC under sec54 EC with a lock in of 3 years.

• Long term Capital gains exempt u/s 54ED if invested within 6 months in sharesof companies formed and registered inIndia with a lock in of 1 year.

Session 4: Capital Markets and

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 84/183

Session 4: Capital Markets andMutual Funds – Investment

management• Managing Equity portfolios

Equity investment options Equity markets: issue of concern Investment strategies Successful equity portfolio management Risk hedging techniques: use of equity derivatives

• Managing Debt portfolios Debt market securities- types and characteristics Risks of investing in debt securities /bonds Yield and duration Investment styles

• Investment restrictions

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 85/183

Managing Equity portfolios

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 86/183

Equity Investment

• Investment Options Equity shares Preference shares Convertibles: Debentures or

preference shares Equity Warrants: give holders option

to purchase specified number of

shares at predetermined rate.

E it M k t I f

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 87/183

Equity Markets: Issue of concern

• Concentration of marketcapitalization and liquidity (shares atBSE: Grp A-140, B1-1100, B2- 4500)

• High levels of volatility

• Information inadequacies: Disclosure of information Insider trading

• Lack of depth for large volumes

Investment Strategies: is aimed at

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 88/183

to produce capital appreciation & earningsand rewarding investors with superiorreturns

• Large cap, Mid cap and small cap

• P/E ratios & Dividend yield

•

Cyclical , Growth and value stocks• Active fund management style and

passive fund management style

• Fundamental analysis, Technical

analysis and quantitative analysis• Use of equity derivatives

Large cap, Mid cap and small

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 89/183

g p pcap• Large cap companies:

• High liquidity

• Low transaction costs

• Mid cap companies:• Moderate liquidity

• More transaction cost

• Small cap companies:• High profit potential

• High transaction costs

• High volatility

• There are different indices & benchmarksfor Large/ Mid / Small Cap

P/E ratios & Dividend yield and

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 90/183

Cyclical, Growth and value stocks• P/E ratios :

• Higher the P/E, greater the growth potential• Dividend yield :

• Lower the dividend yield, Higher the growth potential

• Cyclical stocks:• Earnings linked with market cycles i.e. macro economic

factors• Growth stocks:

• Low asset base

• High growth potential

• High P/E – Low dividend yield

• Value stocks:• Large Asset base

• Long term good track records

• Moderate P/E & Moderate dividend yield

Passive fund management style and

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 91/183

Active fund management style• Passive fund management style :

• Replicates a chosen index• Low fees• Low costs• Index linked returns

• Active fund management style :

• Aim for out -performance• Higher fees• Higher costs• Stock selection and timing:

– Growth investment strategy: Fund managerselects stocks of cos. Having potential of

above average rate of growth in earnings.– Value investment strategy: Fund manager

selects stocks of cos. With good track record,stability of earnings and are undervalued

Fundamental analysis, Technical

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 92/183

yanalysis and quantitative analysis

• Fundamental analysis :• Seeks where to invest

• Research inputs based upon fundamentals of thecompany and its profit potential

• Technical analysis :• Seeks when to invest

• Analysis of market price and volumes basedupon demand and supply position & past trendcharts

•

Quantitative analysis :• Helps in choosing asset class

• Analysis of sectors and industries based uponmacroeconomic factors

Equity portfolio management

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 93/183

organization structure

• Fund manager:– focuses on a certain location

– select stocks &

– fixes price range for purchase & sale

• Analysts:– researches companies and

– recommends buy & sell

• Dealers:

–collects market intelligence

– Places bye and sell orders with brokers

For Successful equity portfolio

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 94/183

q y pmanagement

• Set realistic returns based on abenchmark

• Be aware of the flexibility in managing aportfolio

• Decide on investment philosophy• Develop an investment strategy based

upon objectives & time horizons

• Avoid over diversification of portfolio &

have well diversified portfolio• Develop a flexible approach to investing

• Ensure risk hedging techniques

Risk hedging techniques: use of equity

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 95/183

g g q q yderivatives

• Mutual funds have been allowed to make useof futures & option contracts in equities for Portfolio risk management Portfolio rebalancing

• Since September 2005 SEBI has also allowedmutual funds to trade in derivative contracts, To enhance portfolio returns

To launch schemes which invest mainly infutures & options

What are equity derivatives?

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 96/183

What are equity derivatives?

• Equity derivatives instruments are specially designed contracts• They derive their value from an underlying assets

• They are traded separately in F&O segment of exchange• Main derivative instruments are:

• Futures,• options

• In a future contract :• You can buy & sell the underlying equity

• at a specified future date• at agreed price

• In option contract:• The buyer of option contract gets the right to buy (call)

or right to sell (put)• The underlying equity

• At agreed price• On a future date• Only if he exercises the option &• For the right he pays a price called premium.

• Option contracts are of two types viz: call option & put option

Equity derivatives as risk hedging tools

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 97/183

Equity derivatives as risk hedging tools

• If fund manager expects the equity market to decline:

He may not sell the equity in cash market rather He can sell the index future at the current future pricefor future delivery.

• If markets fall the equity portfolio will decline, But future contract will show a corresponding profit

since fund manager have sold future contract at ahigher price.

• This is called hedging portfolio risk with the use of futurecontracts.

• If market rise, instead of declining, the fund will not gainout of rise in the market prices as future contract will showcorresponding loss since fund manager has sold futurecontract at lower price.

• Other method of hedging investment portfolio is by buyinga put option (an option to sell the underlying equity at anagreed price) by paying premium.

• A fund manager has to decide whether to sell a futurecontract or to buy a put option depending upon the relativemerits of each.

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 98/183

Managing Debt portfolios

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 99/183

Debt securities: Other

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 100/183

Debt securities: Othertypes

Features based:

• Fixed rate / floating rate debt

securities• Coupon bonds / cumulative bonds

• Listed bonds / un-listed bonds

• Rated bonds / un-rated bonds

• Secured / unsecured bonds

M k t iti

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 101/183

Money market securities

• All debt securities maturingwithin one year are calledmoney market securities

•

Money market securities(instruments) are:• T-Bills

• CDs

• CPs• Call money

• Repos

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 102/183

Debt Markets• Tenor

short and long put and call options

• Interest payment Fixed and floating Periodic vs discounted

• Credit quality

Gilt, guaranteed, and others• Traded and non-traded

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 103/183

Price and Yield• Increase in rates reduces value of

existing bonds.

• Decrease in rates increases value of existing bonds

• Price and yield are inversely related

• The relationship between yield andtenor can be plotted as the yieldcurve.

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 104/183

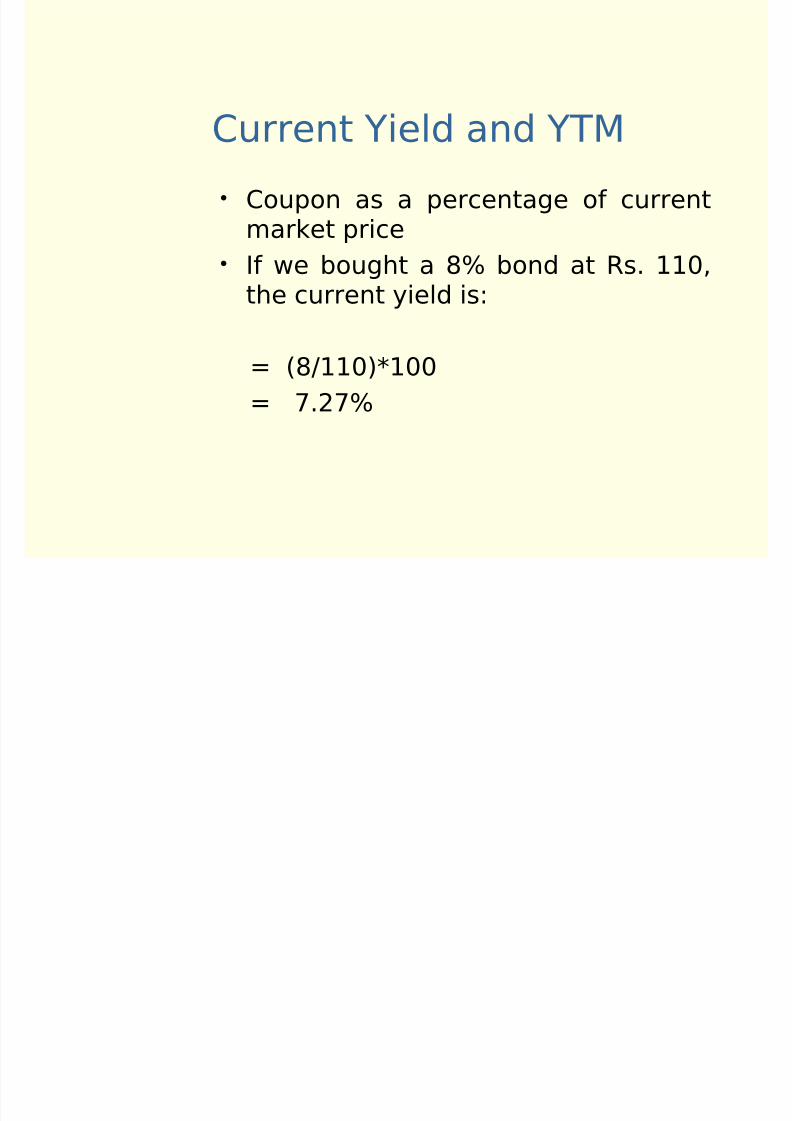

Current Yield and YTM• Coupon as a percentage of current

market price

•

If we bought a 8% bond at Rs. 110,the current yield is:

= (8/110)*100

= 7.27%

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 105/183

Credit Risk• Probability of default by the

borrower

• Change in credit rating: downgrade increases the yield

and decreases the price

upgrade decreases the yield andincreases the price.

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 106/183

Debt Portfolio

Management Styles• Buy and hold

Portfolio exposed to interest rate risk.

• Duration management increase duration if rates are expected to fall decrease duration if rates are expected to

rise

• Credit selection

invest in low grade bonds that are likely tobe upgraded.

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 107/183

Investment Restrictions• Invest only in marketable

securities.

• Investment only on delivery basis• A mutual fund under all its

schemes, cannot hold more than10% of the paid-up capital of a

company.

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 108/183

Investment Restrictions• Not more than 10% of its NAV in a single

company. Exceptions: Index Funds and Sectoral funds

• Rated investment grade issues of a singleissuer cannot exceed 15% of the net assets Can be extended to 20%, with the approval of

the trustees.

• Investment in unrated securities of one

company cannot exceed 10% of the netassets of a scheme and not more than 25%of net assets of a scheme can be in suchsecurities.

Investment in Sponsor

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 109/183

pCompany

A mutual fund scheme cannot investin unlisted securities of the sponsoror an associate or group company of the sponsor.

A mutual fund scheme cannot investin privately placed securities of thesponsor or its associates.

Investment by a scheme in listedsecurities of the sponsor or associate

companies cannot exceed 25% of thenet assets of the scheme

Oth Li it

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 110/183

Other Limits

• Mutual funds cannot make loans

• Mutual funds can borrow upto 20% of netassets for a period not exceeding 6 months.

• Derivatives can be used only after informing

investors

• Any change in investment objectives requiresinformation to investor, and provision of optionto exit at NAV, without exit load.

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 111/183

Session 5: Risk and

Return• Return Methods

Change in NAV

Total Return Total Return with dividend re-investment CAGR

• Risk

Standard deviation Beta and Ex-Marks

• Benchmark and comparison

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 112/183

Computing Returns• Sources of return

Dividend

Change in NAV• Return = Income earned for

amount invested over a givenperiod of time

• Standardise as % per annum

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 113/183

Alternate Methodologies• Computing return

Percentage change in NAV. Simple total return ROI or Total return with

dividend re-investment

Compounded rate of growth

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 114/183

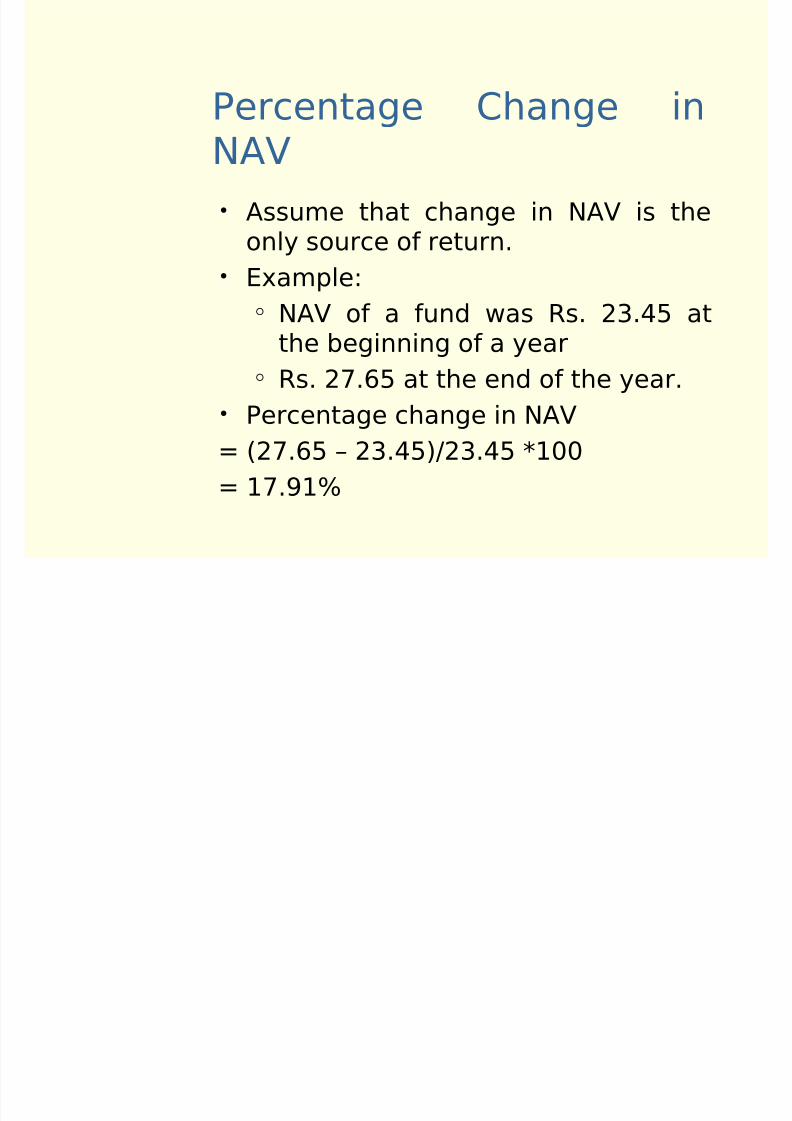

Percentage Change in

NAV• Assume that change in NAV is the

only source of return.

• Example: NAV of a fund was Rs. 23.45 at

the beginning of a year Rs. 27.65 at the end of the year.

• Percentage change in NAV

= (27.65 – 23.45)/23.45 *100

= 17.91%

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 115/183

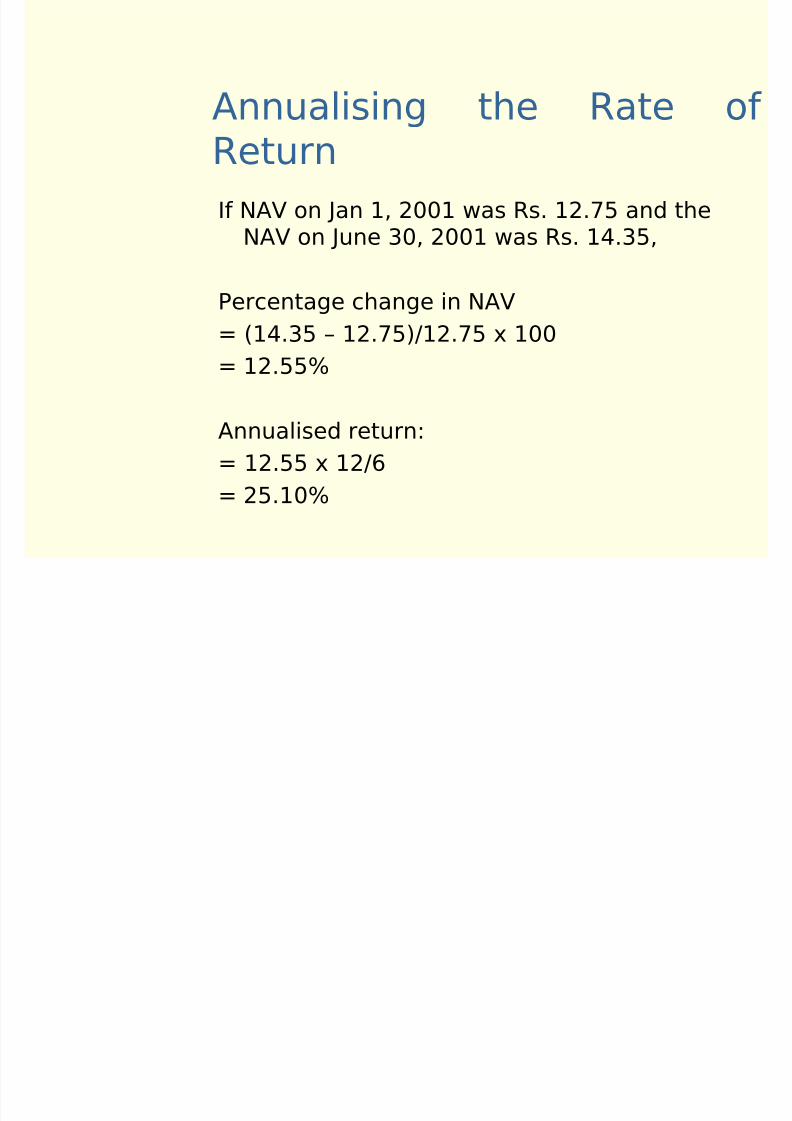

Annualising the Rate of

ReturnIf NAV on Jan 1, 2001 was Rs. 12.75 and the

NAV on June 30, 2001 was Rs. 14.35,

Percentage change in NAV

= (14.35 – 12.75)/12.75 x 100

= 12.55%

Annualised return:

= 12.55 x 12/6

= 25.10%

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 116/183

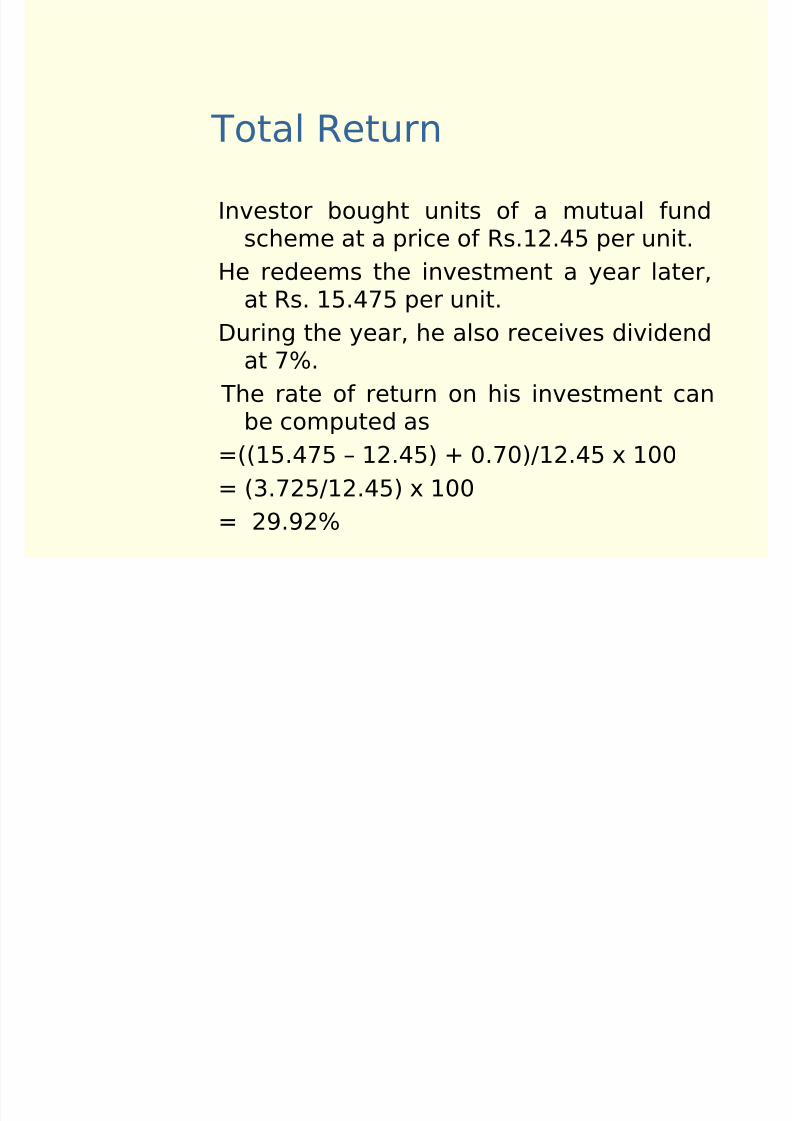

Total ReturnInvestor bought units of a mutual fund

scheme at a price of Rs.12.45 per unit.

He redeems the investment a year later,at Rs. 15.475 per unit.

During the year, he also receives dividendat 7%.

The rate of return on his investment canbe computed as

=((15.475 – 12.45) + 0.70)/12.45 x 100

= (3.725/12.45) x 100

= 29.92%

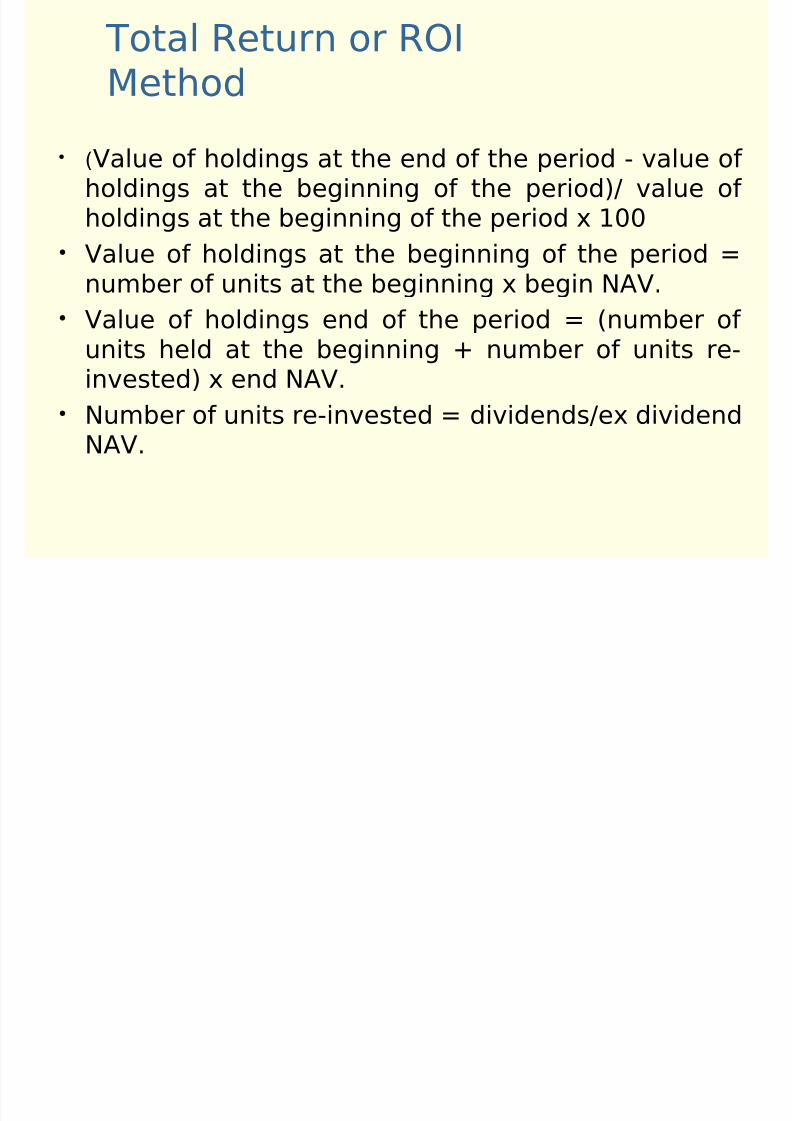

Total Return or ROIMethod

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 117/183

Method

• (Value of holdings at the end of the period - value of holdings at the beginning of the period)/ value of holdings at the beginning of the period x 100

• Value of holdings at the beginning of the period =

number of units at the beginning x begin NAV.• Value of holdings end of the period = (number of

units held at the beginning + number of units re-invested) x end NAV.

• Number of units re-invested = dividends/ex dividendNAV.

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 118/183

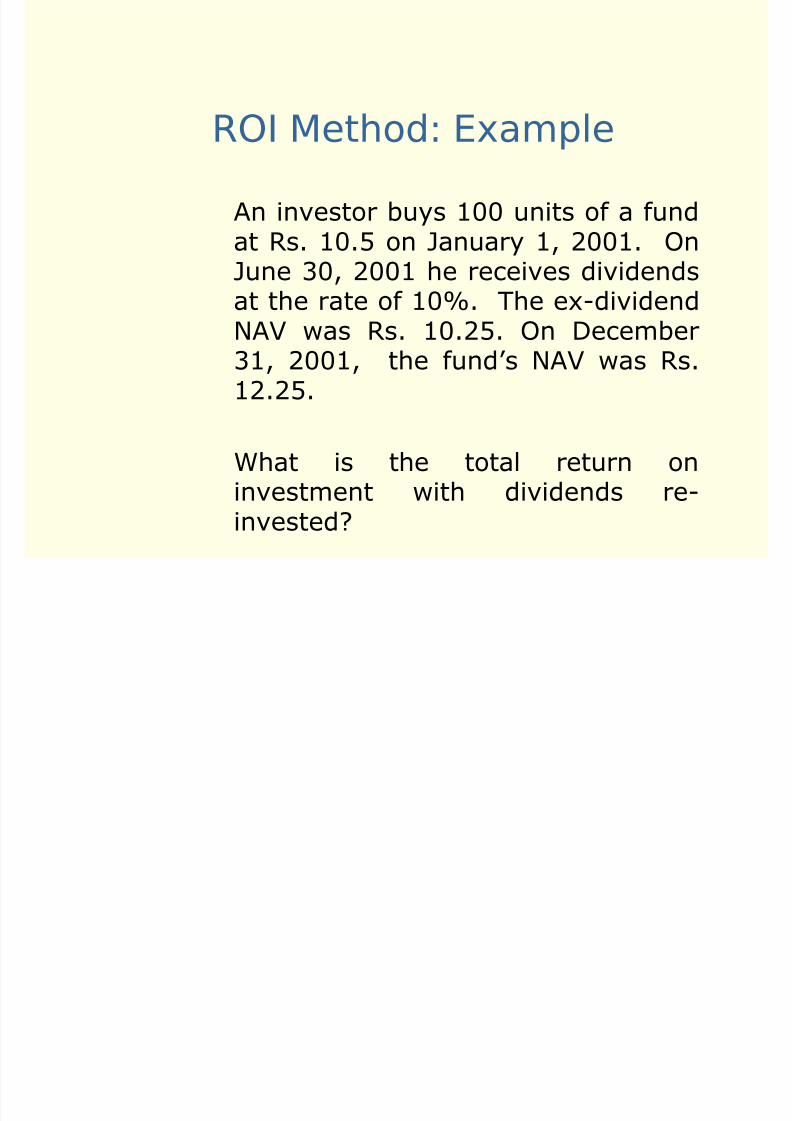

ROI Method: ExampleAn investor buys 100 units of a fundat Rs. 10.5 on January 1, 2001. On

June 30, 2001 he receives dividendsat the rate of 10%. The ex-dividendNAV was Rs. 10.25. On December31, 2001, the fund’s NAV was Rs.12.25.

What is the total return oninvestment with dividends re-invested?

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 119/183

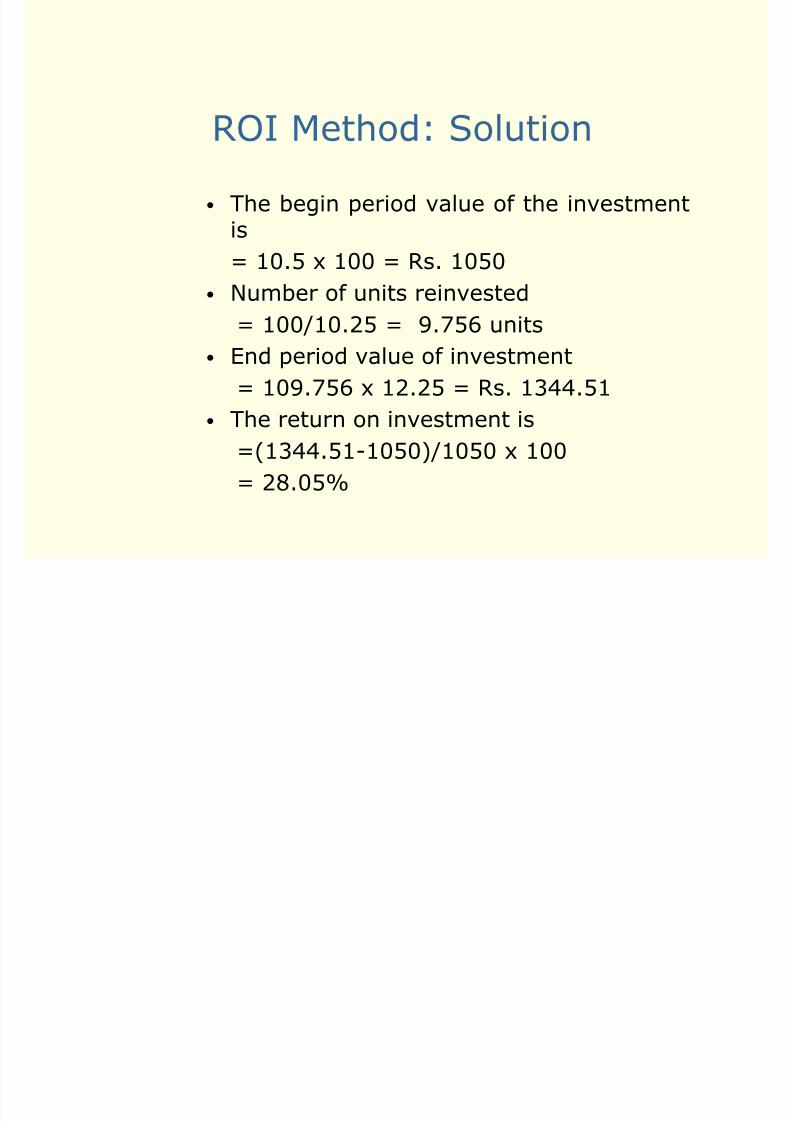

ROI Method: Solution

• The begin period value of the investmentis

= 10.5 x 100 = Rs. 1050

• Number of units reinvested

= 100/10.25 = 9.756 units

• End period value of investment

= 109.756 x 12.25 = Rs. 1344.51

• The return on investment is

=(1344.51-1050)/1050 x 100

= 28.05%

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 120/183

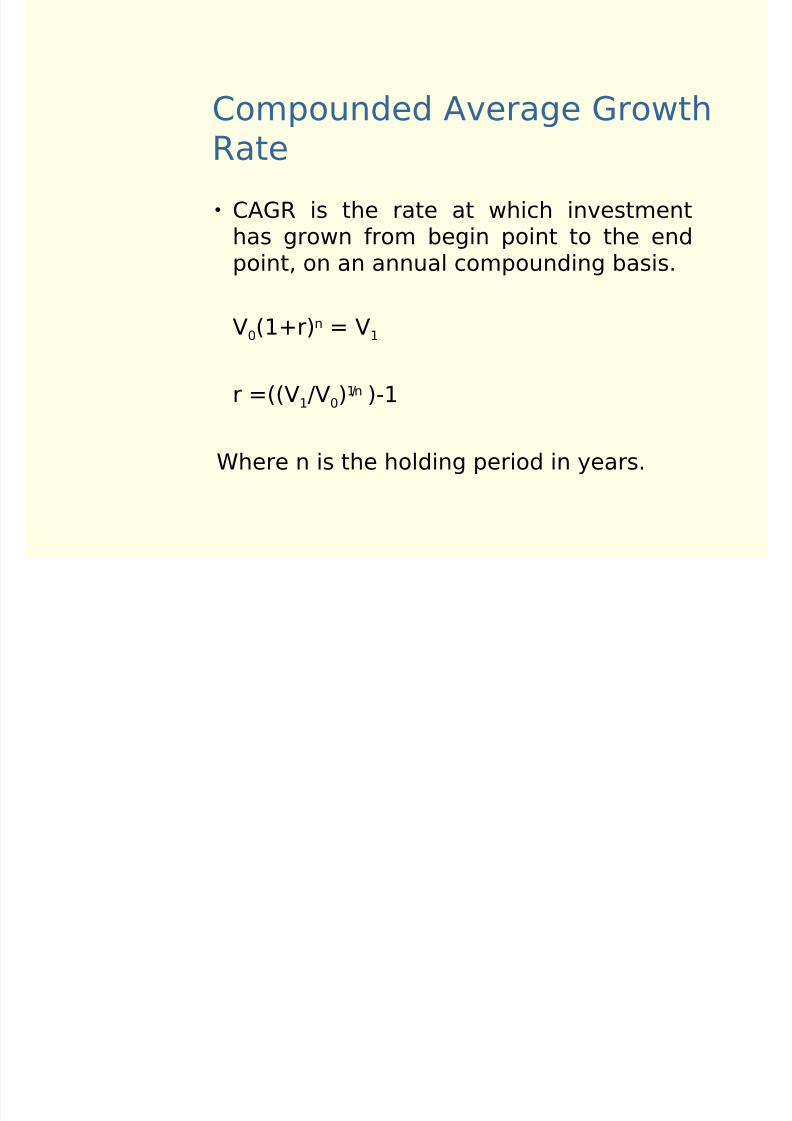

Compounded Average Growth

Rate

• CAGR is the rate at which investmenthas grown from begin point to the endpoint, on an annual compounding basis.

V0(1+r)n = V1

r =((V1/V0)1/n )-1

Where n is the holding period in years.

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 121/183

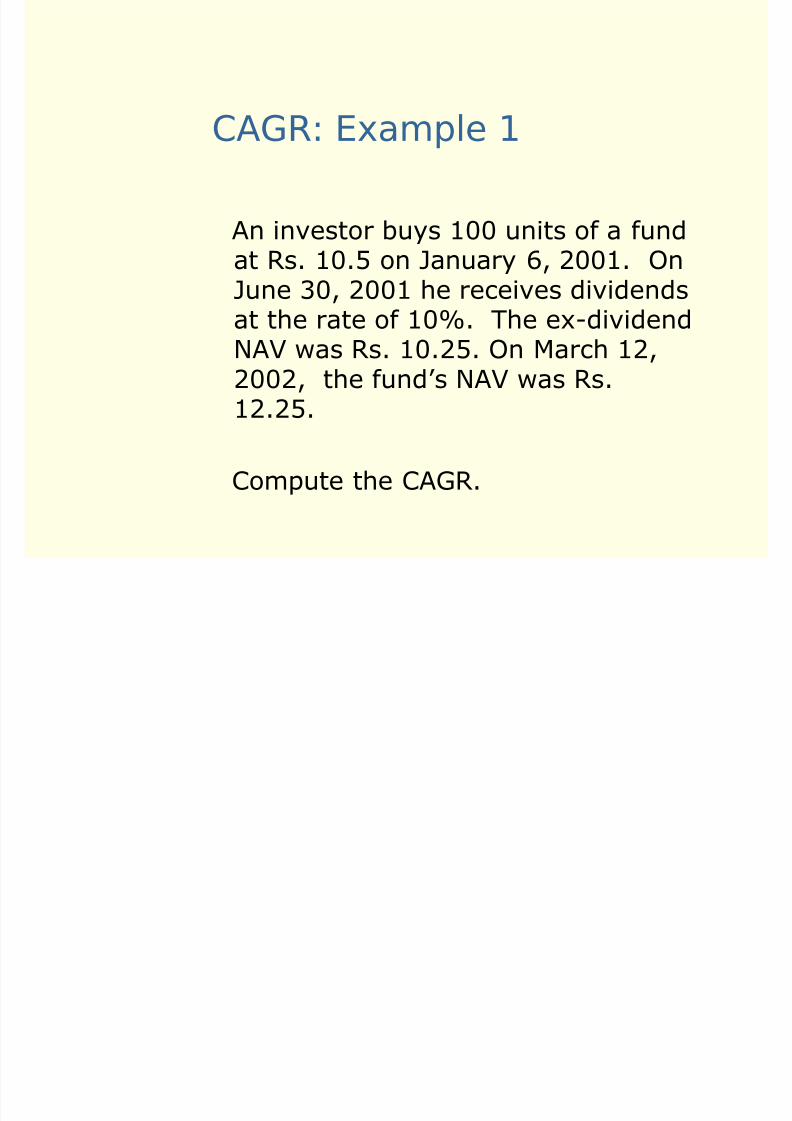

CAGR: Example 1

An investor buys 100 units of a fundat Rs. 10.5 on January 6, 2001. On

June 30, 2001 he receives dividendsat the rate of 10%. The ex-dividendNAV was Rs. 10.25. On March 12,2002, the fund’s NAV was Rs.

12.25.

Compute the CAGR.

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 122/183

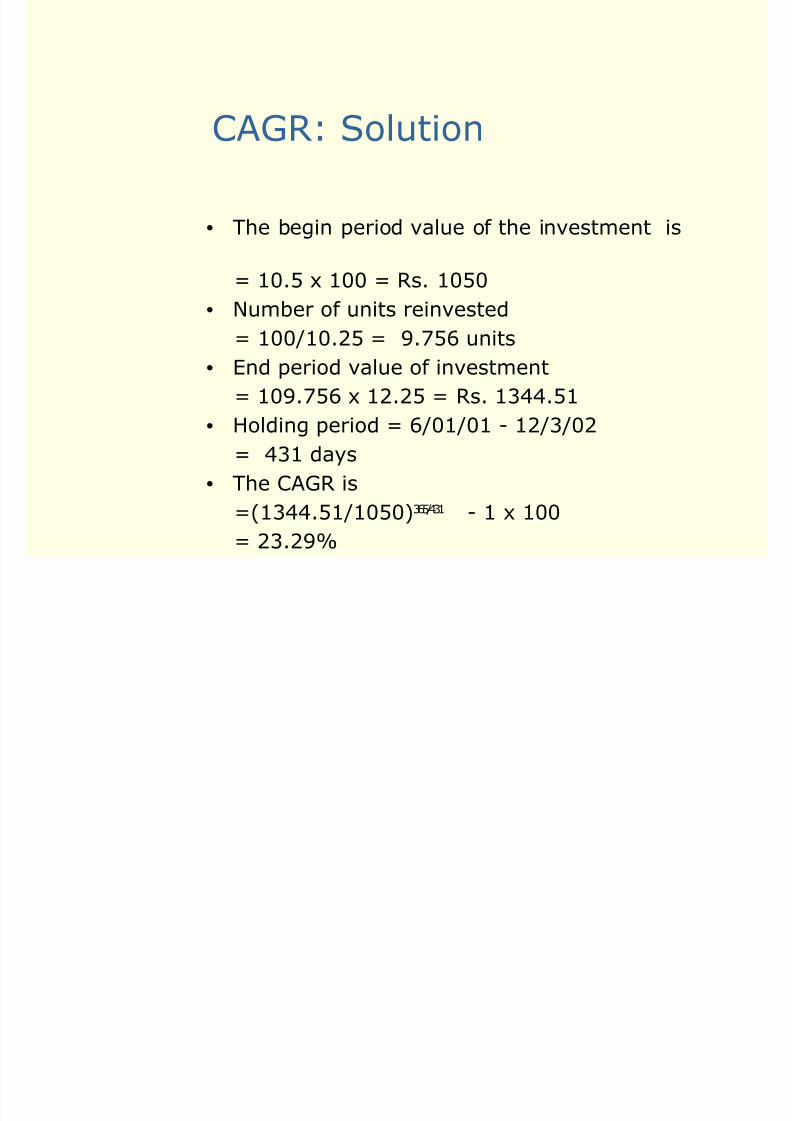

CAGR: Solution

• The begin period value of the investment is

= 10.5 x 100 = Rs. 1050• Number of units reinvested

= 100/10.25 = 9.756 units

• End period value of investment

= 109.756 x 12.25 = Rs. 1344.51

• Holding period = 6/01/01 - 12/3/02

= 431 days

• The CAGR is

=(1344.51/1050)365/431 - 1 x 100

= 23.29%

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 123/183

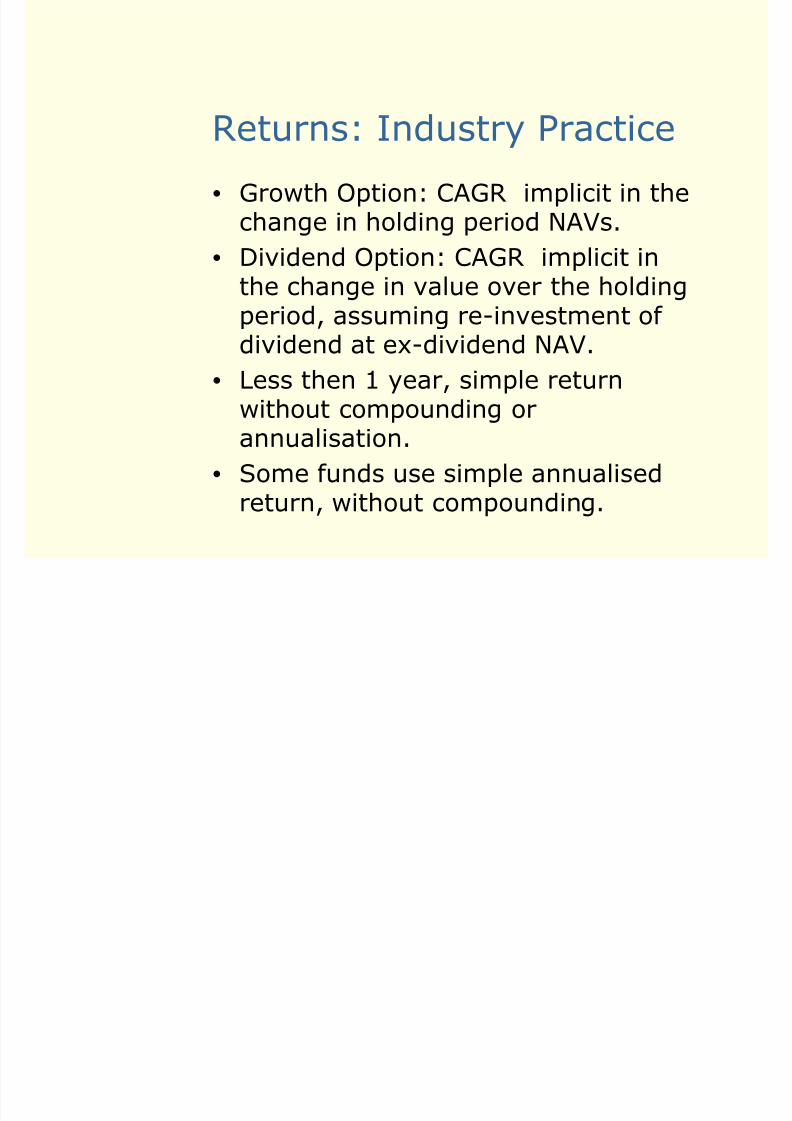

Returns: Industry Practice

• Growth Option: CAGR implicit in thechange in holding period NAVs.

• Dividend Option: CAGR implicit in

the change in value over the holdingperiod, assuming re-investment of dividend at ex-dividend NAV.

• Less then 1 year, simple return

without compounding orannualisation.

• Some funds use simple annualisedreturn, without compounding.

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 124/183

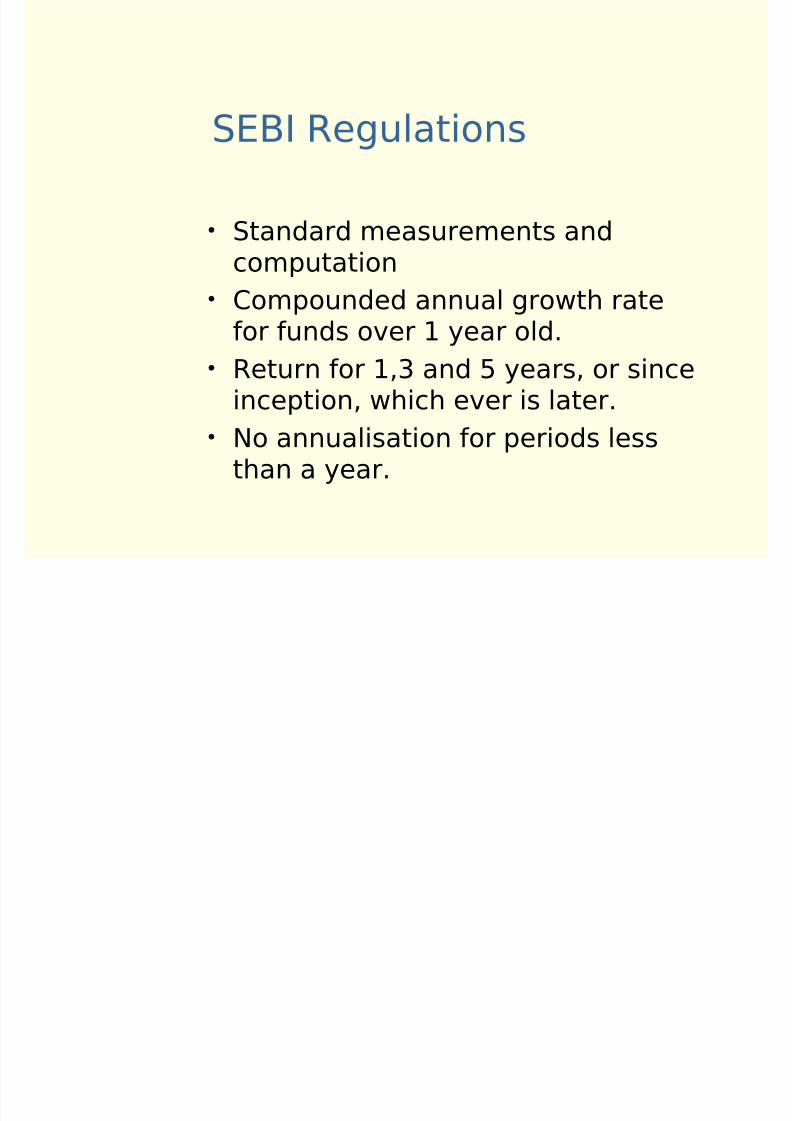

SEBI Regulations

• Standard measurements andcomputation

• Compounded annual growth ratefor funds over 1 year old.

• Return for 1,3 and 5 years, or since

inception, which ever is later.• No annualisation for periods less

than a year.

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 125/183

Risk in Mutual Fund

Returns• Risk arises when actual returns are

different from expected returns.

•

Historical average is a good proxyfor expected return.

• Standard deviation is an importantmeasure of total risk.

•

Beta co-efficient is a measure of market risk.

• Ex-marks is an indication of extent of correlation with market index.

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 126/183

Benchmarks

• Relative returns are important thanabsolute returns for mutual funds.

• Comparable passive portfolio is used asbenchmark.

• Usually a market index is used.

• Compare both risk and return, over thesame period for the fund and the

benchmark.• Risk-adjusted return, is the return per

unit of risk.

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 127/183

SEBI Guidelines

• Benchmark should reflect the assetallocation

• Same as stated in the offer document

• Growth fund with more than 60% in equityto use a broad based index.

• Bond fund with more than 60% in bonds touse a bond market index.

• Balanced funds to use tailor-made index• Liquid funds to use money market

instruments.

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 128/183

Other Measures of

Performance• Tracking error

Tracking error for index funds should be nil.

•

Credit quality Rating profile of portfolio should be studied

• Expense ratio Higher expense ratios hurt long term investors

• Portfolio turnover Higher for short term funds and lower for longer

term funds.

• Size and portfolio composition

Session 6: Financial

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 129/183

Session 6: FinancialPlanning and MutualFunds

• Concept of financial planning• Mapping life cycles and wealth

cycles of investors• Financial products

• Investment Strategies for Investors• Asset allocation

Concept of Financial Planning

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 130/183

p g

Financial planning process involves following

steps:

• Study client’s profile• Identifies all the financial needs of client• Translates the needs into monetarily

measurable goals e.g. Need of Rs. 30 lakhafter 5 yrs for purchase of house property• These goals can be short term, medium term

and long term• Recommend Asset mix (asset allocation) /

Portfolio under the framework of client's profile

• Implement recommendations and review theperformance time to time and suggestchanges in changed circumstances toaccomplish desired goals in time.

Assessing client’s profile

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 131/183

Parameters to assess:

•

Age, gender, physical status• Source of income & nature of income : steady or

fluctuating & Level of income

• Details of recurring expenses and life style (habits of spending) to assess all time liquidity need.

• Risk tolerance level or risk appetite• Tax status

• Current savings & Investments

• Details of Assets & Liabilities

• Family details & number of dependents

Note: Structured questionnaire should be used toassess client’s profile and risk tolerance level

Objective of Financial Planning

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 132/183

Objective of Financial Planning

The ultimate objective of financialplanning is to ensure that the right amountis available at right time to meet definedfinancial goal.

Thus financial planning comprises of :

• Defining financial goals

• Recommending and implementingappropriate assets mix

• Reviewing performances and makesuitable changes to achieve definedfinancial goals.

Who is a Financial Planner

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 133/183

Who is a Financial Planner(FP)?

• Is a person who uses the financialplanning process to help anotherperson determine how to meet his

or her financial goals• Key functions of a FP is to help

people identify their financialneeds, priorities and the products

that are most suitable to meettheir needs

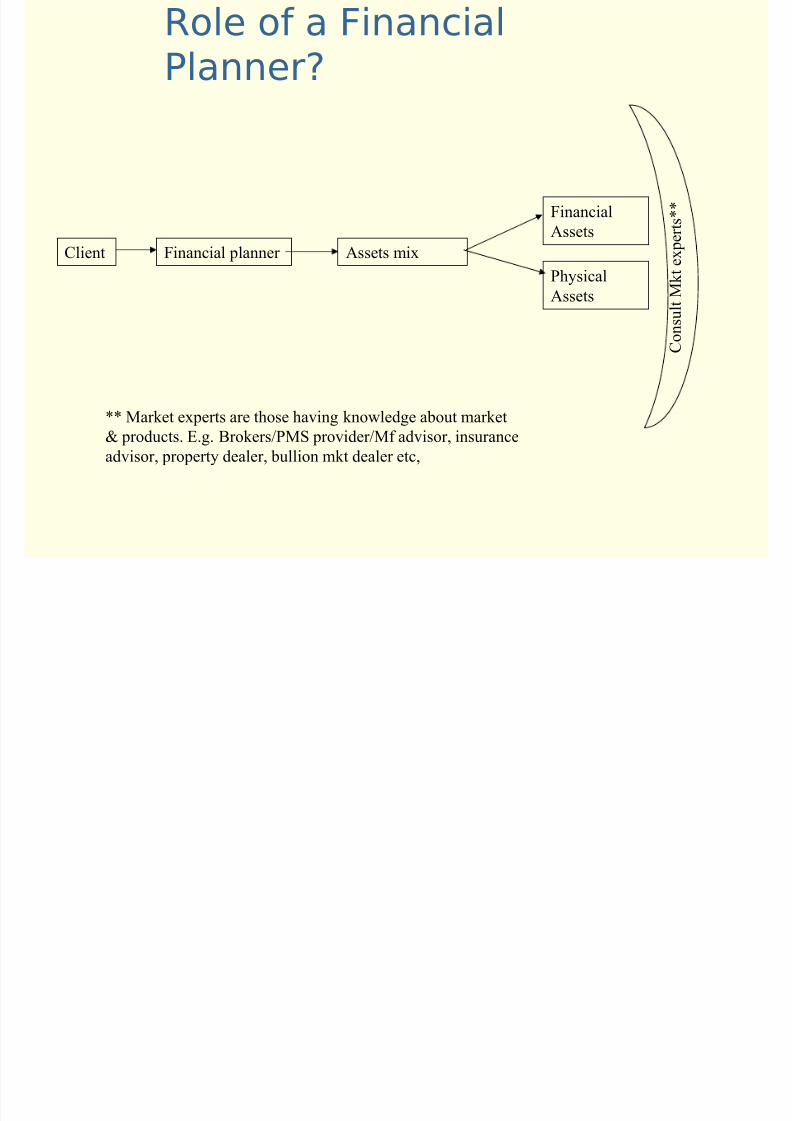

Role of a FinancialPlanner?

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 134/183

Financial planner Assets mix

Financial

Assets

PhysicalAssets

Client

ConsultM k

texpe

rts**

** Market experts are those having knowledge about market& products. E.g. Brokers/PMS provider/Mf advisor, insurance

advisor, property dealer, bullion mkt dealer etc,

Benefits of FinancialPlanning

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 135/183

• Financial planning provides directionand meaning to financial decisions

• Financial decisions comprises of

financing and investment decisions toattain financial goals

g

Importance of FinancialPlanning

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 136/183

• Financial goals are meant to fulfill human needswhich comprises of physical, social and spiritual

needs.• Physical need to remain fit and fine, social need to

fulfill family responsibility and spiritual need toattain peace & happiness which comes throughlove, affection, freedom and space which in turncomes from power/influence (intangible attribute)

and authority (tangible attribute) in society• The above mentioned needs involve cost viz.

survival cost (for basic need & reasonable std of living), social cost (for education, marriage,settlement etc. of family members) and protectioncost (for post retirement life and health care etc.)which in turn require sufficient liquidity,Investments, and variety of insurance.

• Financial planning helps in realizing above

Common mistakes inFinancial Planning (FP)

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 137/183

• Measurable financial goals are not set• Financial decisions made in isolation• FP is confused with investing• Financial plans are not re-evaluated

periodically• Considered relevant only for wealthy• FP is required only when clients get older

• FP is considered same as retirementplanning and estate planning

• FP is primarily tax planning• Only after a crisis FP is started• Expectation of unrealistic returns on

investments

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 138/183

MFs in Financial Planning

• Forms the core foundation andbuilding block for any type of FP

•

Variety of products available tosuit any need or combination of needs

• Barring life and property

insurance, rest of the productportfolio can be created out of bouquet of MFs

Wh h ld F d

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 139/183

• Strong potential demand for suchservices

• Limited supply of financial planners

• Ability to establish Long termrelationships

• Ability to build a profitable business

Why should a Fund

distributor become an FP

Att ib t f G d

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 140/183

Attributes of a Good

Financial PlannerUnderstands:

• The universe of investment products

• Risk-return attributes

• Tax and estate Planning

• Has the ability to convert life cycles of investors into need and preferencebased financial products

• Organised approach to work• Excellent communication and

interpersonal skills

Process of FP in Practice

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 141/183

• Step I: Establish and define therelationship with the client

• Step II: Gathering client’s data,

Define the client’s goals

• Step III: Analyze and evaluateclient’s financial status

• Step IV: Determine and shapethe client’s risk tolerance level

Process of FP in practice

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 142/183

p

• Step V: Ascertain client’s tax situation

• Step VI: Recommend the appropriateasset allocation and specificinvestments

• Step VII: Executing the plan & makingthe client invest

• Step VIII: Review the progress &portfolio rebalancing

Mapping life cycles and wealth cycles of investors

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 143/183

The life cycle stages of an investor can be

classified as follows:– Childhood stage

– Young unmarried stage

– Young married with children stage

– Married with older children stage

– Post-family/Pre-retirement stage

– Retirement stage The income level of investors, the saving potential,

the time horizon and the risk appetite of an investordepend on his life cycle.

Younger investors have higher income and saving

potential, take longer-term view and may be willing totake risks.

Older investors may have limited income and saving,shorter time horizon, and unwilling to risk theirsavings.

Life Cycle Stages

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 144/183

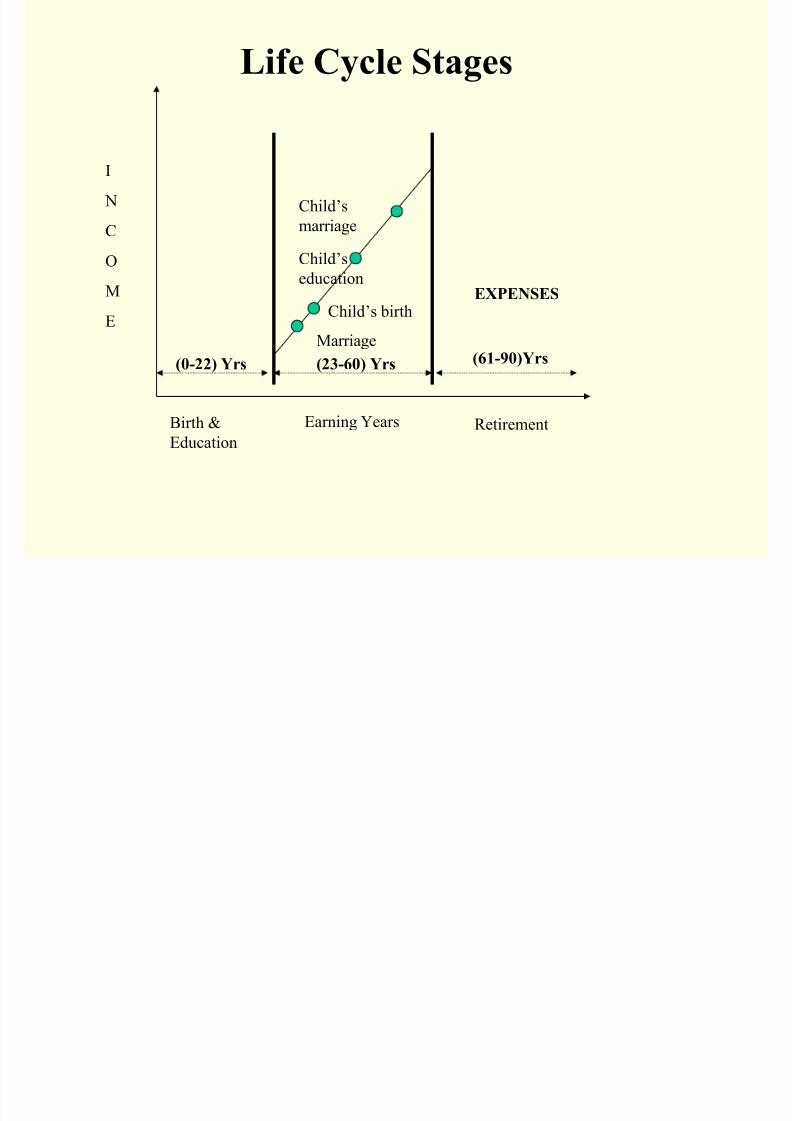

Birth &

Education

Earning Years Retirement

(0-22) Yrs (23-60) Yrs (61-90)Yrs

EXPENSES

Marriage

Child’s birth

Child’s

education

Child’s

marriage

I

N

C

O

M

E

Mapping life cycles and wealth cycles of investors

Continue

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 145/183

Continue……. There are 3 wealth cycle stages for investors:

• Accumulation stage is when investors are earning and havelimited need for investment income. They focus on savingand accumulating wealth for the long term. Equityinvestments are preferred in this stage.

• Transition stage is when financial goals are approaching.Investors still earn incomes, but have also draw on their

earnings. Investors choose balanced portfolios that haveboth debt and equity.

• Reaping stage or distribution stage in when investors needthe income from their investment, and cannot save further. They reap the benefits of their savings. They prefer debtinvestments and preserving of capital at this stage.

Mapping life cycles and wealth cycles of investors

Continue

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 146/183

Continue…….

• Inter generational fund transfer refers totransfer of wealth to an investor. Thepreferred investment avenue willdepend on the life cycle and wealth

cycle stage of the beneficiaries.• Sudden wealth surge refers to winningsin games and lotteries. Investors shouldbe advised to temporarily park theirfunds in money market investments andcreate a long-term plan after thinkingthrough the plan.

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 147/183

Investment Products:There are two broadcategories of products

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 148/183

categories of products

available:Physical Assets:

Gold ,Real Estate, Fine Arts, Commodities

Financial Assets:

• Bank Deposits, CPs, CDs• Corporate –Shares, Bonds, Debentures & Fixed

Deposits

• Government – G. Secs, PPF, RBI Relief Bondsand other post office savings-KVP,NSC etc.

• Financial Institutions – Bonds, Shares• Insurance Companies – Insurance Policies

Physical Assets:

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 149/183

• Individuals can invest in physical assets e.g. Gold andReal estate

• Govt. has permitted issue of gold bonds by banks

• Gold bonds represent securitization of gold where theyearn some returns and avoid risks associated withstorage of gold

• Investors are likely to be allowed to invest in goldlinked unit schemes

• Real estate MF are also in the offing which will offer theinvestors the twin benefits of Real estate investing & Mutual fund investing

Investment Products:Guaranteed and Non-

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 150/183

guaranteed Investments

Guaranteed Investments: Capital Protectionand interest rates are guaranteed by theborrower

• Bank deposits• Government savings instruments

Non Guaranteed Investments : Capitalprotection and Interest rates are Notguaranteed

• Mutual funds

• Equity investments

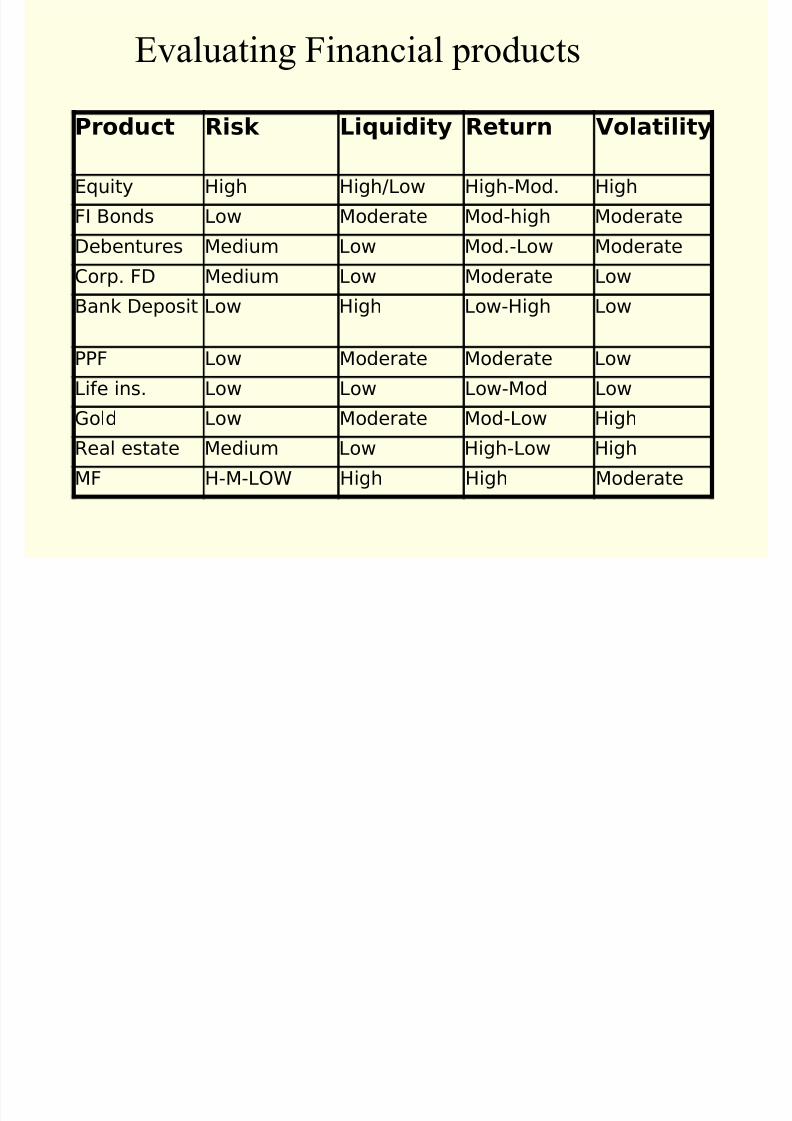

Evaluating Financial products

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 151/183

Product Risk Liquidity Return Volatility

Equity High High/Low High-Mod. High

FI Bonds Low Moderate Mod-high Moderate

Debentures Medium Low Mod.-Low Moderate

Corp. FD Medium Low Moderate LowBank Deposit Low High Low-High Low

PPF Low Moderate Moderate Low

Life ins. Low Low Low-Mod Low

Gold Low Moderate Mod-Low High

Real estate Medium Low High-Low High

MF H-M-LOW High High Moderate

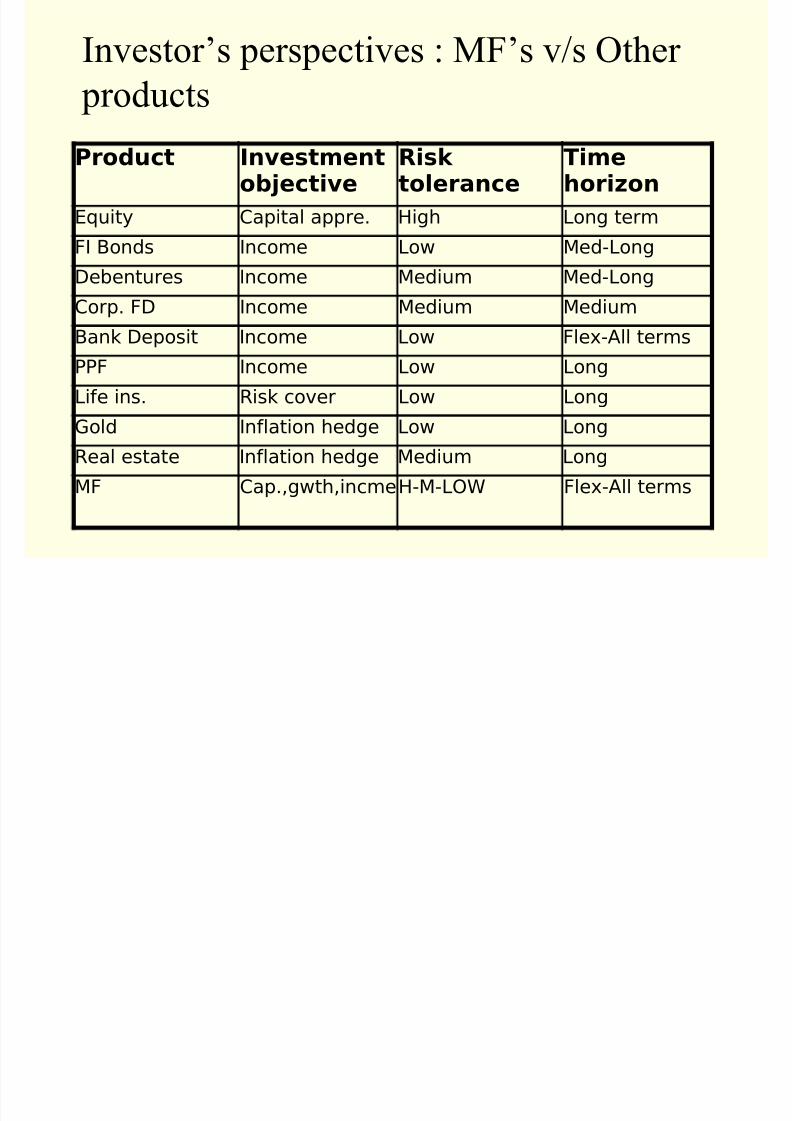

Investor’s perspectives : MF’s v/s Other

products

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 152/183

Product Investmentobjective

Risk tolerance

Timehorizon

Equity Capital appre. High Long term

FI Bonds Income Low Med-Long

Debentures Income Medium Med-LongCorp. FD Income Medium Medium

Bank Deposit Income Low Flex-All terms

PPF Income Low Long

Life ins. Risk cover Low Long

Gold Inflation hedge Low Long

Real estate Inflation hedge Medium Long

MF Cap.,gwth,incmeH-M-LOW Flex-All terms

products

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 153/183

Bank Deposits

• Available since a long period of time

• Large geographical network –transactions made easy & convenient

•

Fund transfer mechanism available• Perception of bank deposits being free of default; Deposits guaranteed up to Rs 1lakh per depositor

• Electronic facilities make it liquid and

easy to use

PPF

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 154/183

• 15 years deposit product madeavailable through banks.

• 9% p.a. interest payable onmonthly balances

• Minimum Rs. 100 & maximum Rs.60,000 p.a investment allowed.• Tax benefits u/s 80C under IT Act.

Limited by taxable income slabs.

•

Interest receipt and withdrawal of principal exempt from tax.• Limited liquidity available.

RBI Relief Bonds

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 155/183

• Issued by banks on behalf of theRBI

• Tenure of five years

• 8% p.a. interest payable

• Proposed to be converted tofloating rate instrument linked togovernment yields

• Option to receive or reinvest

interest• Interest income exempt from tax

Other Government

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 156/183

Other Government

Schemes• IVP & KVP issued by central

government & sold by post offices

• Interest is taxable

• Investor identity is protected andinvestment in cash is possible

Other Government

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 157/183

Other Government

Schemes• Post office savings and RD – gives

fixed rate of interest but are notliquid.

• These are governmentguaranteed deposits

• Attractive for their safety and

cash investment options

Instruments issued by

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 158/183

Instruments issued by

Companies

• Commercial Paper

• Debentures• Equity Shares

• Preference Shares

• Fixed Deposits

• Bonds of FI

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 159/183

How to Compare Products

• Compare products by nature of investments – Characteristics,benefits and risks.

• Current performance andsuitabilityon the basis of Taxability, age &risk profile of Investors.

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 160/183

Why MF is the Best Option

• Mutual funds combine theadvantages of each of theinvestment products

• Dispense the short comings of theother options

• Returns get adjusted for the

market movements

Investment Strategies forIn estors

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 161/183

Investors

Basic strategy:

• Harness the power of

compounding by choosing growthoption for long term

• Start early

•

Have realistic expectations• Invest regularly

Investment Strategies forInvestors

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 162/183

Continue…….• Buy and hold strategy which is preferred by many investors,

may not be beneficial because investors may not weed outpoor performing companies and invest in better performingcompanies , it is the fund manager who takes the decisionbut this strategy can be adopted for good mutual fundschemes

• Rupee-cost averaging (RCA) involves the following: A fixed amount is invested at regular intervals More units are bought when price is low and fewer units

are bought when price is high. Over a period of time, the average purchase price of the

investor’s holdings will be lower than if one tries to guessthe market highs and lows• RCA does not tell indicate when to sell or switch from one

scheme to another. This is a disadvantage.• Investors use the Systematic investment plan to implement

RCA.

Investment Strategies forInvestors

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 163/183

Continue…….• Value averaging involves the following:

A fixed amount is targeted as the desired value of theportfolio at regular intervals.

If markets have moved up, the units are sold and the targetvalue is restored.

If markets move down, additional units are bought at thelower prices.

Over a period of time, the average purchase price of theinvestors holdings will be lower than if one tries to guess themarket highs and lows

• Value averaging is superior to RCA, because it enablesthe investor to book profits and rebalance the portfolio.

• Investors can use the systematic withdrawal andautomatic withdrawal plans to implement value investing.• Investors can also use a money market fund and an

equity fund to implement value averaging.

Asset Allocation

8/8/2019 AMFI Advisory

http://slidepdf.com/reader/full/amfi-advisory 164/183

• Asset allocation is basic tool to translate financial

plans into action.