TERMS OF USE Agricultural Foreign Trade Development: Annual Report is a publication of the Bureau of Agricultural Statistics (BAS), Department of Agriculture. The BAS reserves exclusive right to reproduce this publication in whatever form. Should any portion of this publication be included in a report/article, the title of the publication and the BAS should be cited as the source of the data. The BAS will not be responsible for any information derived from the processing of data contained in this publication. ISSN-2012-0370 Please direct technical inquiries to the Office of the Director Bureau of Agricultural Statistics Ben-Lor Building, 1184 Quezon Avenue Quezon City 1100, Philippines. Email: [email protected] Website: www.bas.gov.ph

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

AGRICULTURAL FOREIGN TRADE DEVELOPMENT

2 0 0 7 A N N U A L

Figure 32 WORLD PRICES OF MAIZE

JANUARY - DECEMBER 2006-2007

0.090

0.110

0.130

0.150

0.170

0.190

M o nth

20062007

Figure 31WORLD PRICES OF RICE (35% broken)

JANUARY - DECEMBER 2006-2007

0.255

0.275

0.295

0.315

0.335

0.355

M o nth

20062007

Figure 35WORLD PRICES OF COFFEE, ARABICA

JANUARY - DECEMBER 2006-2007

2.15

2.35

2.55

2.75

2.95

M o nth

20062007

Figure 36WORLD PRICES OF COFFEE, ROBUSTA

JANUARY - DECEMBER 2006-2007

1.20

1.40

1.60

1.80

2.00

M o nth

20062007

Figure 35WORLD PRICES OF BANANA

JANUARY - DECEMBER 2006-2007

0.45

0.55

0.65

0.75

0.85

0.95

M o nth

2006

2007

Figure 36WORLD PRICES OF RUBBER

JANUARY - DECEMBER 2006-2007

1.80

2.10

2.40

2.70

3.00

M o nth

2006

2007

TERMS OF USE Agricultural Foreign Trade Development: Annual Report is a publication of the Bureau of Agricultural Statistics (BAS), Department of Agriculture. The BAS reserves exclusive right to reproduce this publication in whatever form. Should any portion of this publication be included in a report/article, the title of the publication and the BAS should be cited as the source of the data. The BAS will not be responsible for any information derived from the processing of data contained in this publication.

ISSN-2012-0370

Please direct technical inquiries to the Office of the Director Bureau of Agricultural Statistics

Ben-Lor Building, 1184 Quezon Avenue Quezon City 1100, Philippines.

Email: [email protected]

Website: www.bas.gov.ph

53

AGRICULTURAL FOREIGN TRADE DEVELOPMENT

2 0 0 7 A N N U A L

i 52

FOREWORD

This is the 19th edition of the Agricultural Foreign Trade Development Report which is an annual publication of the Bureau of Agricultural Statistics (BAS). This edition presents statistics on the country’s agricultural trade performance in fiscal year 2007. The first part of this report contains the explanatory notes that describe the summary tables on Philippine agricultural trade. The next part presents the overall agricultural trade situation, trade with the country’s trading partners and consolidated tables on the volume and value of top ten agricultural exports and imports. The last part highlights the world prices of selected commodities.

This report is based on the 2004 Philippine Standard Commodity

Classification (PSCC) Code which defines products using 10-digit codes as compared with the 7-digit of the 1999 PSCC Code. For comparability of data, the formats established in the previous issues are maintained.

The agricultural trade statistics were provided by the National

Statistics Office (NSO) while the world price statistics were obtained from Bangko Sentral ng Pilipinas (BSP) and the World Bank.

To help us improve the BAS’ information support service to the client

and stakeholders in the agriculture sector, comments and suggestions from our readers will be greatly appreciated.

ROMEO S. RECIDE Director

Figure 25 WORLD PRICES OF COCONUT OIL JANUARY - DECEMBER 2006-2007

0.50

0.60

0.70

0.80

0.90

1.00

1.10

1.20

M o nth

20062007

Figure 29WORLD PRICES OF RICE (5% broken)

JANUARY - DECEMBER 2006-2007

0.280

0.290

0.300

0.310

0.320

0.330

0.340

0.350

0.360

0.370

M o nth

20062007

Figure 26 WORLD PRICES OF COPRA

JANUARY - DECEMBER 2006-2007

0.30

0.40

0.50

0.60

0.70

0.80

M o nth

20062007

Figure 27 WORLD PRICES OF SUGAR

JANUARY - DECEMBER 2006-2007

0.17

0.20

0.23

0.26

0.29

0.32

0.35

0.38

0.41

M o nth

20062007

Figure 30WORLD PRICES OF RICE (25% broken)

JANUARY - DECEMBER 2006-2007

0.260

0.270

0.280

0.290

0.300

0.310

0.320

0.330

0.340

0.350

M o nth

20062007

Figure 28WORLD PRICES OF SOYBEAN

JANUARY - DECEMBER 2006-2007

0.20

0.25

0.30

0.35

0.40

0.45

0.50

0.55

M o nth

20062007

AGRICULTURAL FOREIGN TRADE DEVELOPMENT

2 0 0 7 A N N U A L

iii 50

TABLE OF CONTENTS

Page

FOREWORD ……………………………………………………………………. i LIST OF TABLES ………………………………………………………………. iv LIST OF FIGURES ……………………………………………………………... vi HIGHLIGHTS ……………………………………………………………………. 1 STATISTICAL TABLES

OVERALL AGRICULTURAL TRADE ………………………………….… 9 EXPORTS …………………………………………………………………… 13 IMPORTS …………………………………………………………………… 22 TRADE WITH MAJOR TRADING PARTNERS ………………………… 30 WORLD PRICES …………………………………………………………... 49

2006

2007

2006

2007

2006

2007

Janu

ary

0.29

1

0.31

37.

450.

266

0.

287

7.62

0.26

3

0.27

96.

440.

103

0.

165

60.4

4Fe

brua

ry0.

302

0.

315

4.48

0.27

5

0.29

26.

090.

272

0.

285

4.95

0.10

7

0.17

765

.59

Mar

ch0.

304

0.

319

5.00

0.27

5

0.29

99.

050.

272

0.

293

7.48

0.10

5

0.17

161

.92

April

0.30

2

0.31

74.

700.

272

0.

296

9.02

0.27

0

0.29

17.

670.

108

0.

153

41.8

3M

ay0.

308

0.

318

3.12

0.27

6

0.29

67.

170.

273

0.

283

3.66

0.11

1

0.16

044

.87

June

0.31

3

0.32

33.

440.

281

0.

301

7.13

0.27

6

0.29

36.

160.

109

0.

165

51.0

5Ju

ly0.

316

0.

329

4.22

0.28

7

0.30

76.

970.

279

0.

297

6.50

0.11

4

0.14

728

.81

Augu

st0.

313

0.

328

4.73

0.28

4

0.30

77.

810.

278

0.

298

7.13

0.11

7

0.15

129

.65

Sept

embe

r0.

309

0.

325

5.11

0.28

3

0.30

68.

290.

276

0.

300

8.70

0.12

2

0.16

434

.83

Oct

ober

0.30

1

0.32

99.

370.

275

0.

313

14.0

50.

269

0.

311

15.6

80.

142

0.

164

15.4

5N

ovem

ber

0.29

6

0.34

215

.42

0.27

3

0.32

819

.92

0.26

4

0.32

623

.58

0.16

5

0.17

14.

10D

ecem

ber

0.30

4

0.36

118

.76

0.27

9

0.34

724

.63

0.27

3

0.34

627

.00

0.16

0

0.18

012

.38

Coc

onut

Oil

- (P

hilip

pine

s/In

done

sia)

, bul

k, c

.I.f R

otte

rdam

Cop

ra -

(Phi

lippi

nes/

Indo

nesi

a), b

ulk,

c.I.

f N.W

. Eur

ope

Suga

r-Int

erna

tiona

l Sug

ar A

gree

men

t (IS

A) F

OB

Car

ibbe

an P

ort.

Soyb

eans

(US)

, c.i.

f. R

otte

rdam

Ric

e (T

hai)

5% b

roke

n, w

hite

rice

(WR

), M

illed

, ind

icat

ive

pric

e ba

sed

on w

eekl

y su

rvey

s of

exp

ort t

rans

actio

ns,

gov

ernm

ent s

tand

ard,

f.o.

b. B

angk

okR

ice

(Tha

i) 25

% b

roke

n, W

R, m

illed,

indi

cativ

e su

rvey

pric

e, g

over

nmen

t sta

ndar

ds, f

.o.b

. Ban

gkok

Ric

e (T

hai)

35%

bro

ken,

WR

, mille

d, f.

o.b.

Ban

gkok

Mai

ze (U

S),

No.

2, y

ello

w, f

.o.b

. US

Gul

f Por

tsC

offe

e In

tern

atio

nal C

offe

e O

rgan

izat

ion

indi

cato

r pric

e, o

ther

mild

Ara

bica

s, a

vera

ge N

ew Y

ork

and

Bre

men

/Ham

burg

mar

kets

, ex-

dock

Cof

fee

Inte

rnat

iona

l Cof

fee

Org

aniz

atio

n in

dica

tor p

rice,

Rob

usta

s, a

vera

ge N

ew Y

ork

and

Le H

avre

/Mar

seill

es m

arke

ts, e

x-do

ckB

anan

a (C

entra

l and

Sou

th A

mer

ican

), m

ajor

bra

nds,

US

impo

rt pr

ice,

free

on tr

uck

US

Gol

f por

tsR

ubbe

r (an

y or

igin

), R

SS n

o. 1

, in

bale

s, R

ubbe

r Tra

ders

Ass

ocia

tion,

spo

t, N

ew Y

ork

Tabl

e 11

. (C

ontin

ued)

Gro

wth

R

ate

Year

/Mon

thG

row

th

Rat

e G

row

th

Rat

e

Ric

eG

row

th

Rat

e

Mai

ze (c

orn)

2007

5% B

roke

n20

0625

% B

roke

n35

% B

roke

n

AGRICULTURAL FOREIGN TRADE DEVELOPMENT

2 0 0 7 A N N U A L

Table No. Pages

1 SUMMARY OF PHILIPPINE AGRICULTURAL TRADE, 2006-2005 …… 9

1a PHILIPPINE AGRICULTURAL TRADE, BY QUARTER, 2006-2005 …… 10

2 AGRICULTURAL TRADE BALANCES WITH MAJOR TRADING PARTNERS OF THE PHILIPPINES, 2006 VS 2005 …………………… 12

3 QUANTITY AND VALUE OF PHILIPPINE AGRICULTURAL EXPORTSBY COMMODITY GROUP 2006-2005 …………………………………… 13

4 TOP TEN PHILIPPINE AGRICULTURAL EXPORTS, 2006 AND 2005 … 16

4a VALUE OF TOP TEN AGRICULTURAL EXPORTS, BY QUARTER 2006 & 2005 ………………………………………………… 17

5 MAJOR MARKETS OF TOP TEN PHILIPPINE AGRICULTURAL EXPORTS, 2006 ……………………………………… 20

6 QUANTITY AND VALUE OF PHILIPPINE AGRICULTURAL IMPORTSBY COMMODITY GROUP 2006 AND 2005 ……………………………… 22

7 TOP TEN AGRICULTURAL IMPORTS, 2006 AND 2005 ………………… 24

7a VALUE OF TOP TEN AGRICULTURAL IMPORTS, BY QUARTER 2006 AND 2005 …………………………………………… 25

8 MAJOR SUPPLIERS OF TOP TEN PHILIPPINE AGRICULTURALIMPORTS, 2006 ……………………………………………………………… 28

9 DISTRIBUTION OF PHILIPPINE AGRICULTURAL EXPORTSTO ASEAN MEMBER COUNTRIES, 2006 ……………………………… 30

49 iv

LIST OF TABLES

Janu

ary

0.56

90.

731

28.4

70.

373

0.48

429

.87

0.34

70.

241

-30.

470.

257

0.30

619

.07

Febr

uary

0.59

10.

763

29.1

00.

393

0.50

328

.15

0.39

80.

233

-41.

410.

257

0.32

526

.46

Mar

ch0.

575

0.76

933

.74

0.38

50.

509

32.2

10.

380

0.23

0-3

9.45

0.25

60.

322

25.7

8Ap

ril0.

578

0.82

843

.17

0.37

20.

553

48.5

20.

386

0.21

4-4

4.46

0.25

90.

320

23.4

6M

ay0.

583

0.89

453

.34

0.39

00.

592

51.7

90.

371

0.20

8-4

3.93

0.26

60.

334

25.5

6Ju

ne0.

575

0.97

970

.26

0.38

70.

653

68.7

30.

340

0.20

5-3

9.67

0.26

70.

361

35.2

1Ju

ly0.

583

0.92

959

.27

0.38

40.

613

59.6

50.

351

0.22

4-3

6.04

0.27

20.

376

38.1

5Au

gust

0.60

60.

910

50.1

70.

404

0.59

547

.28

0.29

80.

216

-27.

430.

262

0.38

546

.95

Sept

embe

r0.

609

0.93

052

.71

0.41

30.

614

48.6

10.

266

0.21

5-1

9.20

0.25

70.

426

65.7

6O

ctob

er0.

626

1.01

061

.34

0.41

10.

658

60.1

70.

257

0.22

0-1

4.08

0.27

30.

450

64.8

4N

ovem

ber

0.65

61.

131

72.4

10.

434

0.74

872

.35

0.26

00.

223

-14.

260.

300

0.48

963

.00

Dec

embe

r0.

732

1.15

357

.58

0.47

70.

765

60.2

80.

265

0.23

5-1

1.10

0.29

50.

515

74.5

1

Coc

onut

Oil

- (P

hilip

pine

s/In

done

sia)

, bul

k, c

.I.f R

otte

rdam

Cop

ra -

(Phi

lippi

nes/

Indo

nesi

a), b

ulk,

c.I.

f N.W

. Eur

ope

Sug

ar-In

tern

atio

nal S

ugar

Agr

eem

ent (

ISA

) FO

B C

arib

bean

Por

t.So

ybea

ns (U

S), c

.i.f.

Rot

terd

amR

ice

(Tha

i) 5%

bro

ken,

whi

te ri

ce (W

R),

Mill

ed, i

ndic

ativ

e pr

ice

base

d on

wee

kly

surv

eys

of e

xpor

t tra

nsac

tions

,

g

over

nmen

t sta

ndar

d, f.

o.b.

Ban

gkok

Ric

e (T

hai)

25%

bro

ken,

WR

, mille

d, in

dica

tive

surv

ey p

rice,

gov

ernm

ent s

tand

ards

, f.o

.b. B

angk

okR

ice

(Tha

i) 35

% b

roke

n, W

R, m

illed,

f.o.

b. B

angk

okM

aize

(US

), N

o. 2

, yel

low

, f.o

.b. U

S G

ulf P

orts

Cof

fee

Inte

rnat

iona

l Cof

fee

Org

aniz

atio

n in

dica

tor p

rice,

oth

er m

ild A

rabi

cas,

ave

rage

New

Yor

k an

d B

rem

en/H

ambu

rg m

arke

ts, e

x-do

ckC

offe

e In

tern

atio

nal C

offe

e O

rgan

izat

ion

indi

cato

r pric

e, R

obus

tas,

ave

rage

New

Yor

k an

d Le

Hav

re/M

arse

illes

mar

kets

, ex-

dock

Ban

ana

(Cen

tral a

nd S

outh

Am

eric

an),

maj

or b

rand

s, U

S im

port

pric

e,fre

e on

truc

k U

S G

olf p

orts

Rub

ber (

any

orig

in),

RS

S n

o. 1

, in

bale

s, R

ubbe

r Tra

ders

Ass

ocia

tion,

spo

t, N

ew Y

ork

Tabl

e 11

. W

OR

LD P

RIC

ES O

F SE

LEC

TED

CO

MM

OD

ITIE

S ( 2

006

- 200

7)($

per

kg.

)

Gro

wth

R

ate

Year

/Mon

thG

row

th

Rat

e G

row

th

Rat

e G

row

th

Rat

e 20

0620

0720

0620

0720

0620

0720

0620

07

Coc

onut

Oil

Cop

raSu

gar

Soyb

eans

AGRICULTURAL FOREIGN TRADE DEVELOPMENT

2 0 0 7 A N N U A L

Tabl

e 10

b. (C

ontin

ued)

IV.

Anim

al a

nd V

eget

able

Oil

and

Fats

0.00

0.00

0.00

0.00

2,08

3.17

150.

7927

1.34

18,3

50.2

8A.

Ani

mal

and

Veg

etab

le O

ils

447.

0324

7.76

9,28

7.00

a

nd F

ats

B. F

ixed

Veg

etab

le O

ils a

nd F

ats

1,63

6.14

150.

7923

.58

9,06

3.28

V. F

ertil

izer

Man

ufac

ture

d60

1.15

47.7

971

.34

2,55

8.36

VI.

Agric

ultu

ral C

hem

ical

s an

d M

ater

ials

17.3

17.

192.

5762

.36

38.3

37,

352.

9251

,751

.81

VII.

Agr

icul

tura

l Mac

hine

ry36

.11

551.

3817

4.11

1,14

4.52

19,5

27.7

5

TOTA

L VA

LUE

OF

AGR

ICU

LTU

RAL

IMPO

RTS

1,88

0.88

242.

2521

7.58

27.7

717

,286

.45

1,37

0.63

21,1

15.7

144

7,27

9.60

TOTA

L VA

LUE

OF

ALL

PHIL

IPPI

NE

IMPO

RTS

Sou

rce

of b

asic

dat

a: N

SO

57,9

95,7

52.4

73,

821.

0413

,142

.74

90,9

98.2

41,

151.

2213

9,33

4.50

150,

341.

1237

6,56

1.30

Port

ugal

Slov

akia

Slov

enia

Swed

en

Tota

l Phi

l. Ag

ricul

tura

l Im

port

s to

EU

EUR

OPE

AN U

NIO

N Spai

nU

K G

reat

B

ritai

n an

d N

. Ire

land

Item

Pola

nd

v 48

LIST OF TABLES (Continued)

Table No. Pages

9a DISTRIBUTION OF PHILIPPINE AGRICULTURAL EXPORTSTO AUSTRALIA, JAPAN, AND USA, 2006 ……………………………… 32

9b DISTRIBUTION OF PHILIPPINE AGRICULTURAL EXPORTSTO EU MEMBER COUNTRIES, 2006 …………………………………… 33

10 DISTRIBUTION OF PHILIPPINE AGRICULTURAL IMPORTSFROM ASEAN MEMBER COUNTRIES, 2006 …………………………… 39

10a DISTRIBUTION OF PHILIPPINE AGRICULTURAL IMPORTSFROM AUSTRALIA, JAPAN, AND USA, 2006 …………………………… 41

10b DISTRIBUTION OF PHILIPPINE AGRICULTURAL IMPORTSFROM EU MEMBER COUNTRIES, 2006 ………………………………… 43

11 WORLD PRICES OF SELECTED COMMODITIESJAN 2004-DEC 2006 ………………………………………………………… 49

AGRICULTURAL FOREIGN TRADE DEVELOPMENT

2 0 0 7 A N N U A L

Figure No. Pages

1 SHARE OF AGRICULTURAL AND NON-AGRICULTURAL EXPORTS TO TOTAL PHILIPPINE EXPORTS, 2006 ……………………………… 9

2 SHARE OF AGRICULTURAL AND NON-AGRICULTURAL IMPORTS TO TOTAL PHILIPPINE IMPORTS, 2006 ………………………………… 9

3 PHILIPPINE AGRICULTURAL EXPORTS, BY QUARTER 2006-2005 ………………………………………………… 11

4 PHILIPPINE AGRICULTURAL IMPORTS, BY QUARTER 2006-2005 ………………………………………………… 11

5 VALUE OF COCONUT OIL EXPORTS, BY QUARTER 2006-2005 ………………………………………………… 18

6 VALUE OF BANANA FRESH EXPORTS, BY QUARTER 2006-2005 ………………………………………………… 18

7 VALUE OF PINEAPPLE AND PINEAPPLE PRODUCT EXPORTS, BY QUARTER 2005-2006 ………………………………………………… 18

8 VALUE OF DESICCATED COCONUT EXPORTS, BY QUARTER 2005-2006 ………………………………………………… 18

9 VALUE OF TOBACCO MANUFACTURED EXPORTS, BY QUARTER 2005-2006 ………………………………………………… 18

10 VALUE OF TUNA EXPORTS, BY QUARTER 2005-2006 ………………… 18

11 VALUE OF SHRIMPS AND PRAWNS EXPORTS, BY QUARTER 2005-2006 ………………………………………………… 19

47 vi

LIST OF FIGURES

Tabl

e 10

b. (C

ontin

ued)

I. F

ood

and

Live

Ani

mal

s1,

226.

3123

5.06

217.

5825

.20

14,2

09.9

195

9.61

11,3

93.2

433

7,01

7.34

A. L

ive

Anim

als

257.

522,

834.

84B.

Mea

t and

Mea

t Pre

para

tions

1,51

0.19

222.

8815

,135

.42

C. D

airy

Pro

duct

s &

Bird

's E

ggs

1,10

0.86

25.2

079

3.33

326.

245,

036.

2372

,673

.70

D. F

ish

and

Fish

Pre

para

tions

95.1

654

7.35

4.99

1,12

0.27

E. C

erea

ls a

nd C

erea

l Pre

para

tions

22.0

515

.53

672.

3411

,466

.06

F. V

eget

able

s an

d Fr

uits

108.

0611

7.85

1,22

3.47

333.

6910

,736

.94

G. S

ugar

and

Sug

ar P

repa

ratio

ns82

0.20

179.

3915

,365

.57

H. C

offe

e, T

ea, C

ocoa

Spi

ces

217.

5848

3.10

0.23

425.

923,

836.

82

a

nd M

anuf

actu

res

ther

eof

I. F

eedi

ng S

tuff

for A

nim

als

5,06

1.56

604.

491,

803.

7642

,447

.37

(exc

ludi

ng u

nmille

d C

erea

ls)

J. M

isce

llane

ous

Edi

ble

Prod

ucts

17

.39

3,75

5.18

28.6

52,

456.

5216

1,40

0.35

and

Prep

arat

ions

II. T

obac

co a

nd T

obac

co M

anuf

actu

res

25.2

53,

198.

28

III. C

rude

Mat

eria

ls0.

000.

000.

000.

0037

9.63

0.00

857.

1014

,875

.78

A. O

il Se

eds

and

Ole

agin

ous

Frui

ts40

.75

43.2

5B.

Cru

de R

ubbe

r43

6.56

6,99

7.02

C. C

rude

Fer

tiliz

er45

.41

D. C

rude

Ani

mal

& V

e geta

ble

Mat

eria

ls

379.

6337

9.79

7,79

0.10

(i

nclu

ding

hid

es, s

kins

and

furk

ins,

raw

)

Tota

l Phi

l. Ag

ricul

tura

l Ex

port

s to

EU

EUR

OPE

AN U

NIO

N Spai

nU

K G

reat

B

ritai

n an

d N

. Ire

land

Item

Pola

ndPo

rtug

alSl

ovak

iaSl

oven

iaSw

eden

Tota

l Phi

l. Ag

ricul

tura

l Im

ports

to E

U

AGRICULTURAL FOREIGN TRADE DEVELOPMENT

2 0 0 7 A N N U A L

Tabl

e 10

b. (C

ontin

ued)

IV.

Ani

mal

and

Veg

etab

le O

il an

d Fa

ts58

.51

963.

2488

5.65

A. A

nim

al a

nd V

eget

able

Oils

and

Fat

s58

.51

8.45

816.

00

B. F

ixed

Veg

etab

le O

ils a

nd F

ats

954.

7969

.65

V. F

ertil

izer

Man

ufac

ture

d0.

844.

34

VI.

Agr

icul

tura

l Che

mic

als

and

Mat

eria

ls29

3.79

2,51

7.89

6,00

0.83

VII.

Agr

icul

tura

l Mac

hine

ry0.

255,

279.

274,

517.

94

TOTA

L VA

LUE

OF

AGR

ICU

LTU

RAL

IMPO

RTS

147.

920.

0697

,167

.73

14,3

65.7

762

.35

1,66

6.11

23.0

987

,696

.49

TOTA

L VA

LUE

OF

ALL

PHIL

IPPI

NE

IMPO

RTS

Sou

rce

of b

asic

dat

a: N

SO

EUR

OPE

AN U

NIO

NN

ethe

rland

s

2,20

8.75

10,7

42.6

51,

434,

988.

3621

9,84

4.17

110.

342,

351.

9130

7.78

481.

956.

30

Item

Gre

ece

Hun

gary

Irela

ndIta

lyLi

thun

iaLu

xem

bour

gM

alta

12 VALUE OF FERTILIZER MANUFACTURED EXPORTS,BY QUARTER 2005-2006 ………………………………………………… 19

13 VALUE OF MILK AND CREAM AND PRODUCTS EXPORTS, BY QUARTER 2005-2006 ………………………………………………… 19

14 VALUE OF SEAWEEDS AND CARAGEENAN EXPORTS, BY QUARTER 2005-2006 ………………………………………………… 19

15 VALUE OF RICE IMPORTS, BY QUARTER 2005-2006 ………………… 26

16 VALUE OF SOYABEAN OIL/CAKE MEAL IMPORTS, BY QUARTER 2005-2006 ………………………………………………… 26

17 VALUE OF WHEAT IMPORTS, BY QUARTER 2005-2006 ……………… 26

18 VALUE OF MILK AND CREAM AND PRODUCTS IMPORTS, BY QUARTER 2005-2006 ………………………………………………… 26

19 VALUE OF UNMANUFACTURED TOBACCO IMPORTS, BY QUARTER 2005-2006 ………………………………………………… 26

20 VALUE OF MEAT OF BOVINE ANIMALS IMPORTS, BY QUARTER 2005-2006 ………………………………………………… 26

21 VALUE OF UREA IMPORTS, BY QUARTER 2005-2006 ………………… 27

22 VALUE OF FOOD PREPARATIONS FOR INFANT USE IMPORTS, BY QUARTER 2005-2006 ………………………………………………… 27

23 VALUE OF NON-ALCOHOLIC CONCENTRATES IMPORTS, BY QUARTER 2005-2006 ………………………………………………… 27

LIST OF FIGURES (Continued) Figure No. Pages

vii 46

AGRICULTURAL FOREIGN TRADE DEVELOPMENT

2 0 0 7 A N N U A L

45 viii

LIST OF FIGURES (Continued) Figure No. Pages

24 VALUE OF PALM OIL IMPORTS, BY QUARTER 2005-2006 …………… 27

25 WORLD PRICES OF COCONUT OIL, JANUARY - DECEMBER 2005-2006 ……………………………………… 52

26 WORLD PRICES OF COPRA, JANUARY - DECEMBER 2005-2006 ……………………………………… 52

27 WORLD PRICES OF SUGAR, JANUARY - DECEMBER 2005-2006 ……………………………………… 52

28 WORLD PRICES OF SOYBEANS, JANUARY - DECEMBER 2005-2006 ……………………………………… 52

29 WORLD PRICES OF RICE (5% BROKEN), JANUARY 2005-DECEMBER 2006 ……………………………………… 52

30 WORLD PRICES OF RICE (25% BROKEN), JANUARY 2005-DECEMBER 2006 ……………………………………… 52

31 WORLD PRICES OF RICE (35% BROKEN), JANUARY 2005-DECEMBER 2006 ……………………………………… 53

32 WORLD PRICES OF MAIZE, JANUARY 2005-DECEMBER 2006 ……………………………………… 53

33 WORLD PRICES OF COFFEE, ARABICA, JANUARY- DECEMBER 2005-2006 ……………………………………… 53

34 WORLD PRICES OF COFFEE, ROBUSTA, JANUARY- DECEMBER 2005-2006 ……………………………………… 53

62.3

51,

666.

1111

.58

75,1

13.7

9

912.

3887

6.71

62.3

520

,127

.72

165.

6656

5.01

11.5

852

8.32

3,73

9.29

419.

93

16,2

45.4

6

1,66

6.11

31,5

33.3

1

11.7

0

0.00

0.00

11.5

11,

155.

24

11.5

141

5.83

739.

41

Luxe

mbo

urg

Mal

taN

ethe

rland

s

N U

NIO

NLi

thua

nia

I. F

ood

and

Live

Ani

mal

s72

.13

0.06

96,5

18.3

85,

377.

60

A. L

ive

Anim

als

0.06

B. M

eat a

nd M

eat P

repa

ratio

ns29

2.04

14.4

5C

. Dai

ry P

rodu

cts

& B

ird's

Egg

s4,

839.

5711

8.32

D. F

ish

and

Fish

Pre

para

tions

18.1

5E

. Cer

eals

and

Cer

eal P

repa

ratio

ns27

2.71

626.

14F.

Veg

etab

les

and

Frui

ts72

.13

45.4

11,

432.

55G

. Sug

ar a

nd S

ugar

Pre

para

tions

20.8

436

5.93

H. C

offe

e, T

ea, C

ocoa

Spi

ces

129.

9410

3.86

and

Man

ufac

ture

s th

ereo

f I.

Fee

ding

Stu

ff fo

r Ani

mal

s1,

224.

67

(e

xclu

ding

unm

illed

Cer

eals

)J.

Mis

cella

neou

s E

dibl

e P

rodu

cts

90,9

17.8

71,

473.

53

an

d P

repa

ratio

ns

II. T

obac

co a

nd T

obac

co M

anuf

actu

res

75.5

429

7.05

III. C

rude

Mat

eria

ls0.

000.

000.

0022

6.93

A. O

il S

eeds

and

Ole

agin

ous

Frui

tsB

. Cru

de R

ubbe

r12

9.98

C. C

rude

Fer

tiliz

erD

. Cru

de A

nim

al &

Veg

etab

le M

ater

ials

96

.95

(i

nclu

ding

hid

es, s

kins

and

furk

ins,

raw

)

Tabl

e 10

b. (C

ontin

ued)

EUR

Item

Gre

ece

Hun

gary

Irela

ndIta

lyEU

RO

PEAN

UN

ION

AGRICULTURAL FOREIGN TRADE DEVELOPMENT

2 0 0 7 A N N U A L

Tabl

e 10

b. (C

ontin

ued)

IV.

Anim

al a

nd V

eget

able

Oil

and

Fats

1,27

7.24

8,63

4.21

983.

053,

043.

08

A. A

nim

al a

nd V

eget

able

Oils

and

Fat

s66

8.32

3,21

5.69

979.

692,

845.

55

B. F

ixed

Veg

etab

le O

ils a

nd F

ats

608.

925,

418.

523.

3619

7.53

V. F

ertil

izer

Man

ufac

ture

d19

3.45

23.8

71,

615.

58

VI.

Agric

ultu

ral C

hem

ical

s an

d M

ater

ials

68.5

23,

337.

3610

.72

1,35

6.32

170.

9313

,251

.54

17,2

56.2

3

VII.

Agr

icul

tura

l Mac

hine

ry24

.96

778.

3041

0.86

9.27

1,48

9.83

5,11

0.95

TOTA

L VA

LUE

OF

AGR

ICU

LTU

RAL

IMPO

RTS

1,95

4.01

36,6

22.4

138

3.48

554.

2638

,430

.86

101.

072,

091.

5759

,083

.93

64,7

87.2

2

TOTA

L VA

LUE

OF

ALL

PHIL

IPPI

NE

IMPO

RTS

Sou

rce

of b

asic

dat

a: N

SO

1,29

1,94

1.12

Fran

ceG

erm

any

30,2

48.9

232

0,43

0.14

880.

4999

,442

.45

68,7

40.6

514

7.93

164,

633.

7062

6,82

5.78

Item

Aust

riaB

elgi

umC

ypru

sC

zech

R

epub

licD

enm

ark

Esto

nia

Finl

and

EUR

OPE

AN U

NIO

N

ix 44

LIST OF FIGURES (Continued)) Figure No. Pages

35 WORLD PRICES OF BANANA, JANUARY- DECEMBER 2005-2006 ……………………………………… 53

36 WORLD PRICES OF RUBBER, JANUARY- DECEMBER 2005-2006 ……………………………………… 53

AGRICULTURAL FOREIGN TRADE DEVELOPMENT

2 0 0 7 A N N U A L

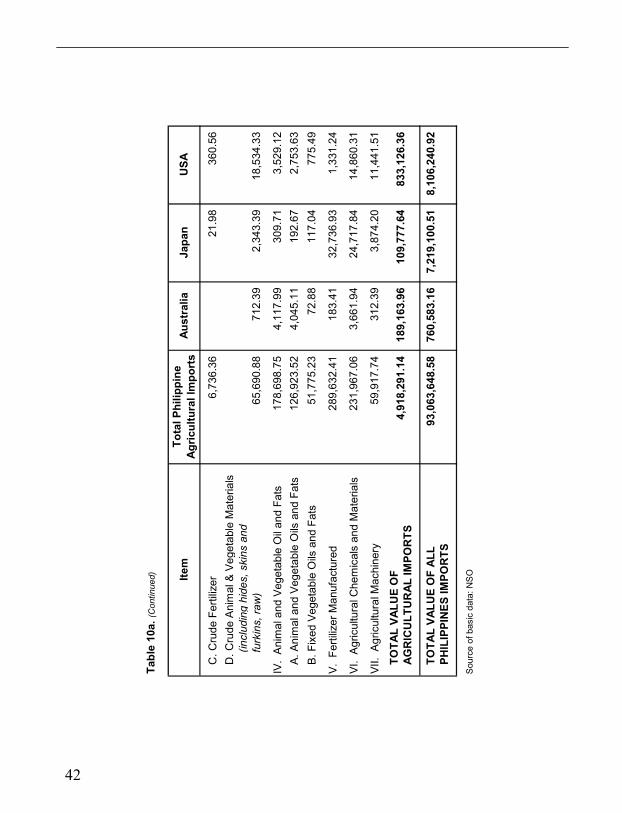

C. C

rude

Fer

tiliz

er6,

736.

36

21.9

8

360.

56

D

. Cru

de A

nim

al &

Ve g

etab

le M

ater

ials

(inc

ludi

ng h

ides

, ski

ns a

nd

fu

rkin

s, ra

w)

65,6

90.8

8

71

2.39

2,

343.

39

18,5

34.3

3

IV.

Anim

al a

nd V

eget

able

Oil

and

Fats

178,

698.

75

4,

117.

99

30

9.71

3,52

9.12

A.

Ani

mal

and

Veg

etab

le O

ils a

nd F

ats

126,

923.

52

4,

045.

11

19

2.67

2,75

3.63

B.

Fix

ed V

eget

able

Oils

and

Fat

s51

,775

.23

72.8

8

11

7.04

775.

49

V. F

ertil

izer

Man

ufac

ture

d28

9,63

2.41

183.

41

32,7

36.9

3

1,33

1.24

VI.

Agric

ultu

ral C

hem

ical

s an

d M

ater

ials

231,

967.

06

3,

661.

94

24

,717

.84

14

,860

.31

VII.

Agr

icul

tura

l Mac

hine

ry59

,917

.74

312.

39

3,87

4.20

11

,441

.51

TOTA

L VA

LUE

OF

AGR

ICU

LTU

RAL

IMPO

RTS

TOTA

L VA

LUE

OF

ALL

93,0

63,6

48.5

8

76

0,58

3.16

7,

219,

100.

51

8,10

6,24

0.92

PH

ILIP

PIN

ES IM

POR

TS

Sou

rce

of b

asic

dat

a: N

SO

833,

126.

36

10

9,77

7.64

189,

163.

96

4,91

8,29

1.14

USA

Tabl

e 10

a. (C

ontin

ued) Ite

mTo

tal P

hilip

pine

Ag

ricul

tura

l Im

port

sAu

stra

liaJa

pan

HIGHLIGHTS

42

AGRICULTURAL FOREIGN TRADE DEVELOPMENT

2 0 0 7 A N N U A L

IV. A

nim

al a

nd V

eget

able

Oil

a

nd F

ats

0.00

40,8

69.1

685

,446

.37

0.00

0.00

8,41

8.83

1,43

9.05

203.

9213

6,37

7.33

A. A

nim

al a

nd V

eget

able

Oils

and

Fat

s25

,783

.39

65,8

28.4

23,

541.

751,

181.

9420

3.92

96,5

39.4

2B

. Fix

ed V

eget

able

Oils

and

Fat

s15

,085

.77

19,6

17.9

54,

877.

0825

7.11

39,8

37.9

1

V.

Ferti

lizer

Man

ufac

ture

d21

,832

.18

14,1

97.5

10.

113,

936.

8972

9.43

1,46

9.03

42,1

65.1

5

VI.

Agric

ultu

ral C

hem

ical

s an

d M

ater

ials

16,7

91.0

37,

691.

435,

728.

1018

,805

.90

7,36

0.51

56,3

76.9

7

VII.

Agr

icul

tura

l Mac

hine

ry67

8.88

2,16

5.18

3,34

0.61

2,29

9.60

151.

218,

635.

48

TOTA

L VA

LUE

OF

AG

RIC

ULT

UR

AL IM

POR

TS9.

3922

1,56

3.38

183,

581.

972,

198.

0412

0.67

94,2

95.6

836

3,83

9.21

553,

210.

791,

418,

819.

13

TOTA

L VA

LUE

OF

ALL

PHIL

IPPI

NE

IMPO

RTS

no im

port

data

from

Lao

s, B

rune

i and

Sar

awak

Sou

rce

of b

asic

dat

a: N

SO

13,4

50,8

59.9

2

3,

023.

296,

411,

299.

832,

402,

510.

6790

6,45

8.07

Indo

nesi

aVi

etna

m

547.

011,

357,

153.

732,

318,

501.

862,

827.

88

Thai

land

Sing

apor

e

Tota

l Phi

lippi

ne

Agric

ultu

ral

Impo

rts

to

ASEA

N

Tabl

e 10

. (C

ontin

ued)

ITEM

Cam

bodi

a

A S

E A

N

Saba

hM

yanm

arM

alay

sia

1 40

OVERALL AGRICULTURAL TRADE SITUATION 1. A relatively weaker performance characterized the country’s 2007

agricultural foreign trade. Growth rate of imports (8.25%) was higher than that of exports (3.35%) and this widened trade deficit by 18.51% or US$1,750.22 million.

• The total Philippine exports in 2007 reached US$50,465.72 million.

The share of agricultural exports to total Philippine exports increased by 6.30% from the previous year’s record.

• The country realized earnings amounting to US$3,168.07 million from

agricultural exports . This marked a 13.90% growth compared with the last year’s level. The fourth quarter of 2007 recorded the highest level of exportation at US$913.10 million and this indicated a 33.74% increase over the 2006 level.

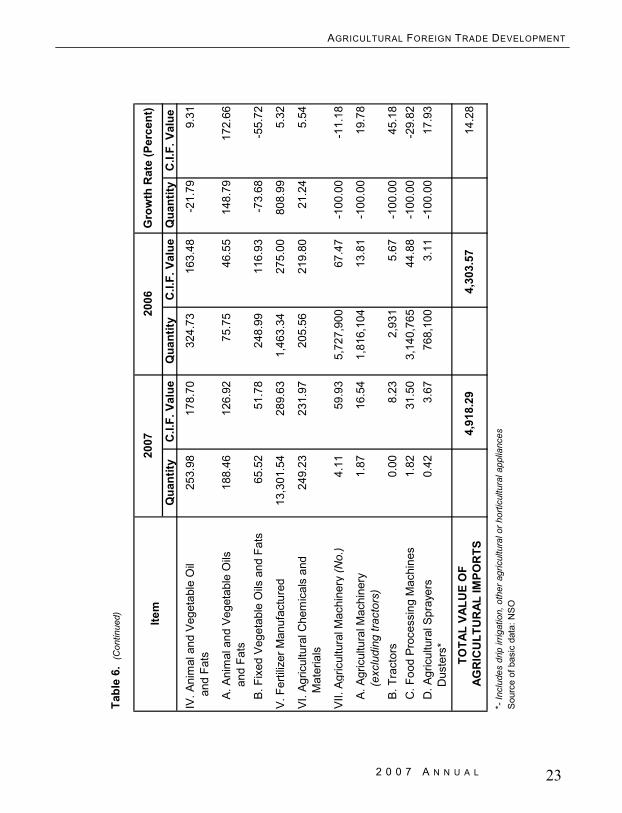

• Agricultural import expenditures amounted to US$4,918.29 million or

14.28% higher than in 2006. Agricultural imports contributed 8.48% to the country’s total import expenditures. This represented an increase of 6.54% from the 2006 record.

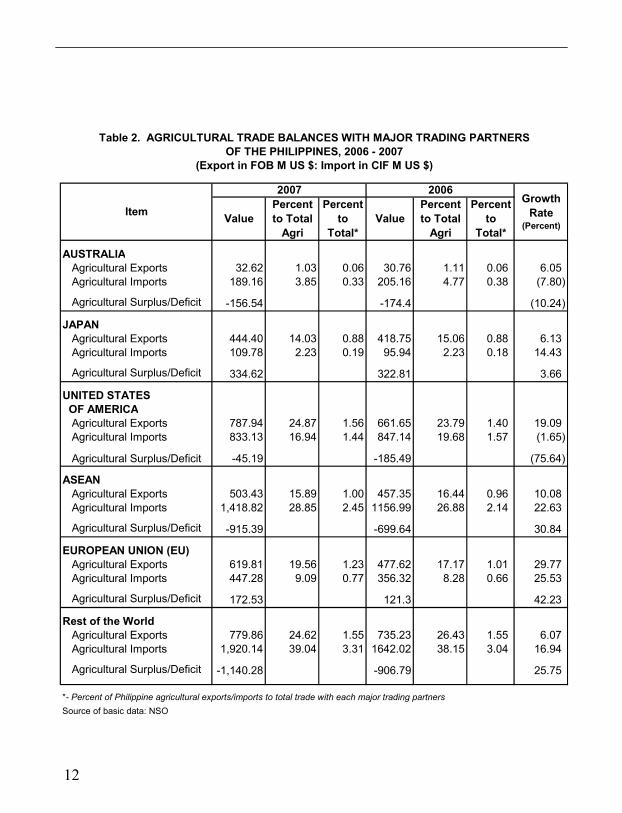

2. Trade surpluses with Japan and European Union (EU) countries

were maintained in an increasing rate, whereas deficits were noted with the rest of the country’s trading partners.

• The country’s trade with European Union posed a surplus of

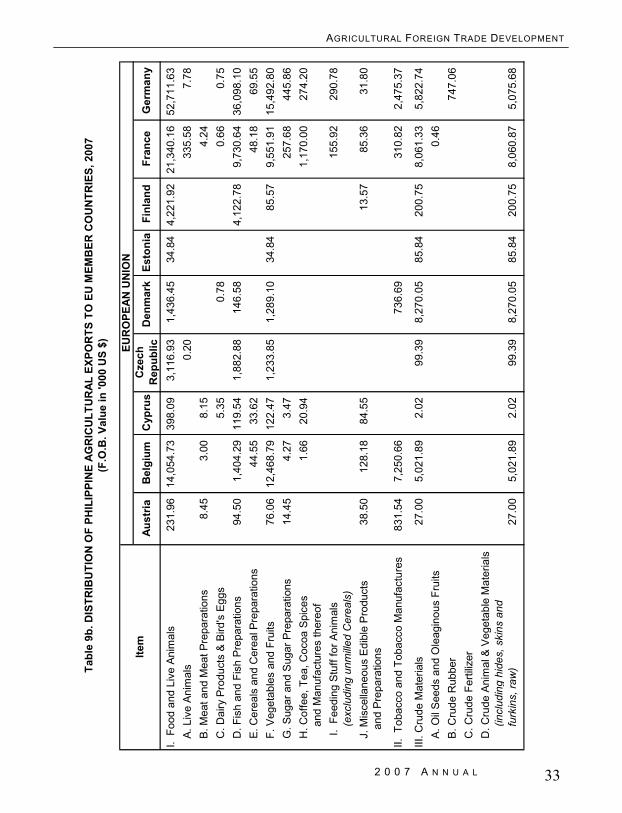

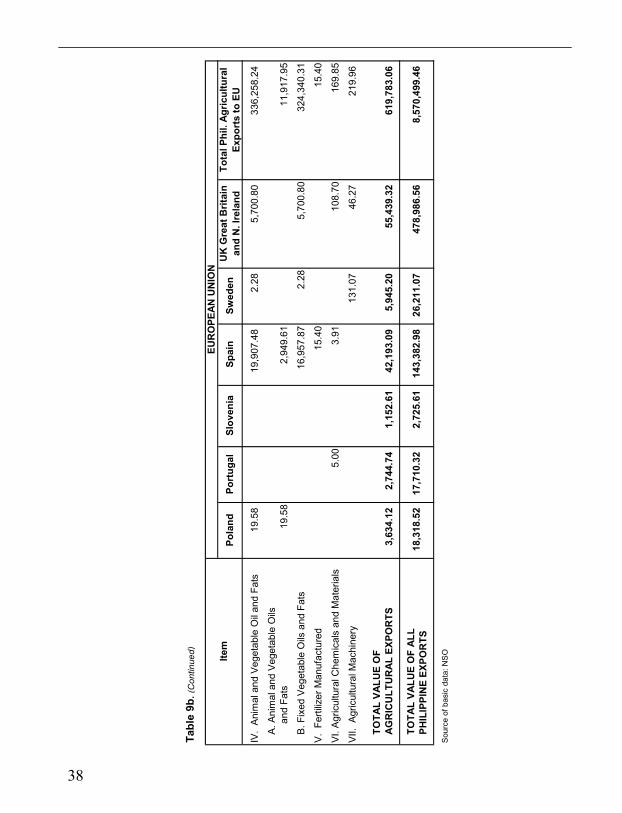

US$172.53 million in 2007. There was a significant increase of 42.23% from last year’s US$121.30 million. During the period, agricultural exports (US$ 619.81 million) outpaced imports (US$447.18 million) .

• Agricultural trade with Japan posted the largest surplus of US$334.62

million with 3.66% increase over last year’s value. Japan was the leading market for Philippine fresh banana and shrimps and prawns which comprised 44.39% and 45.28%, respectively of the country’s agricultural exports. It was also the top supplier of rubber, accounting for 21.94% of the country’s total rubber import data.

AGRICULTURAL FOREIGN TRADE DEVELOPMENT

2 0 0 7 A N N U A L

39 2

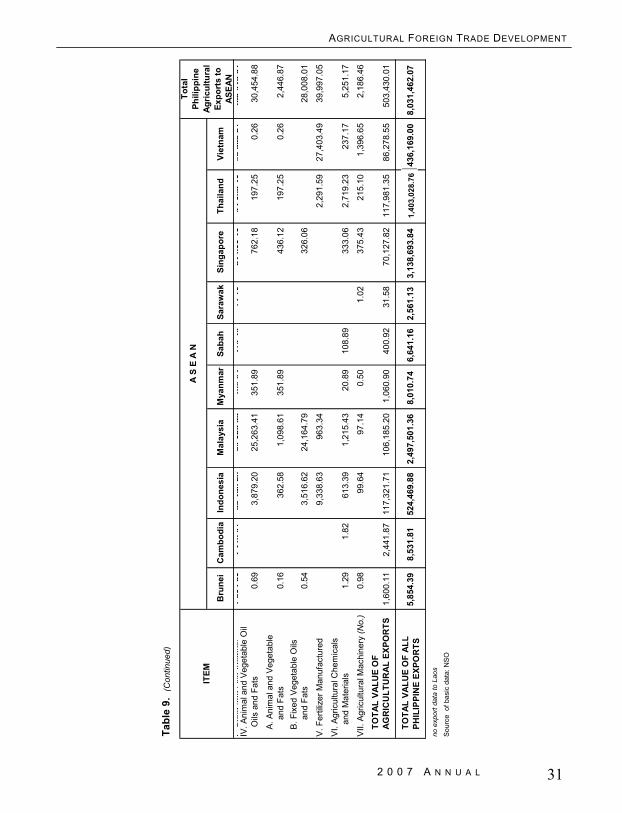

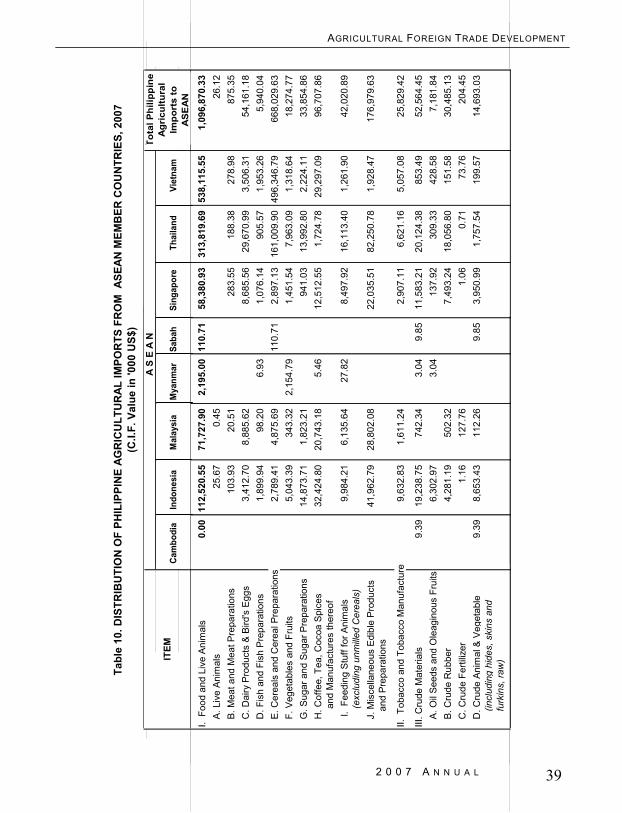

• There was still a wide imbalance in the Philippine agricultural trade with the ASEAN countries. This year’s trade deficit of US$915.39 million was 30.84% higher than last year’s deficit of US$699.64.

• The country’s exchange of commodities with USA and Australia

recorded decreases in trade deficits by 10.24% and 75.64%, respectively. Trade with the rest of the world was characterized by higher import expenses which negated the increase in export receipts. The net effect was a wider gap in agricultural trade balance at 25.75%.

3. Agricultural Exports

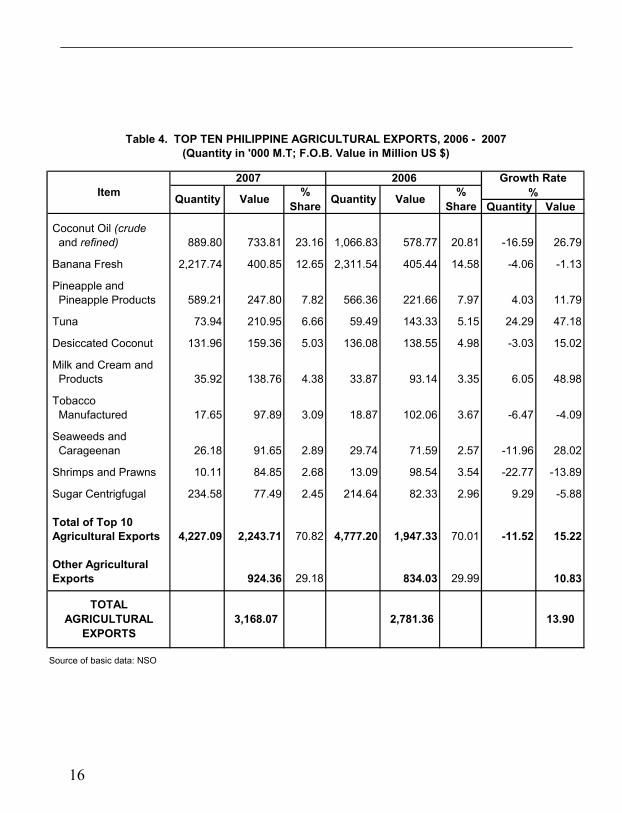

Most of the top 10 export commodities registered gains in export earnings compared with last year’s proceeds.

• Milk and cream and their by-products and tuna led the major gainers

among agricultural exports with 48.98% and 47.18% increases, respectively. These effected the rise of milk and cream and their by-products from 8th placer in the previous year to 6th placer this year. Tuna maintained its position in the fourth rank. Indonesia remained to be the country’s top destination of milk and cream and their by-products with 48.95% share in the total value of the country’s exports for this product. On the other hand, 32.79% of the Philippine tuna export went to USA.

• Crude and refined coconut oil continued as the country’s top

agricultural exports. There was a 26.79% increase in its exports value, a turn-around from the last year’s negative growth of 11.94%. The highest volume of exportation was recorded during the last quarter of the year. The major markets were Netherlands with 41.71% share and USA with 36.79%.

• Export earnings from seaweeds and carageenan increased by

28.02%, that is, from US$ 71.59 million in 2006 to US$ 91.65 million in 2007. This brought the item to the 8th place which displaced fertilizer, manufactured in the top 10 list of agricultural imports. The major destination countries included USA (17.49%), Denmark (8.91%), France (8.60%), Belgium (5.46%) and Thailand (5.25%).

Tabl

e 10

. DIS

TRIB

UTI

ON

OF

PHIL

IPPI

NE

AGR

ICU

LTU

RAL

IMPO

RTS

FR

OM

ASE

AN M

EMB

ER C

OU

NTR

IES,

200

7(C

.I.F.

Val

ue in

'000

US$

)

108

428

380

448

116

504

0.00

0.00

112,

520.

5571

,727

.90

2,19

5.00

110.

7125

.67

0.45

ratio

ns10

3.93

20.5

1s

Egg

s3,

412.

708,

885.

62at

ions

1,89

9.94

98.2

06.

93re

para

tions

2,78

9.41

4,87

5.69

110.

715,

043.

3934

3.32

2,15

4.79

para

tions

14,8

73.7

11,

823.

21pi

ces

32,4

24.8

020

,743

.18

5.46

reof

mal

s9,

984.

216,

135.

6427

.82

erea

ls)

Prod

ucts

41

,962

.79

28,8

02.0

8

Man

ufac

ture

s9,

632.

831,

611.

24

0.00

9.39

19,2

38.7

574

2.34

3.04

9.85

nous

Fru

its6,

302.

973.

044,

281.

1950

2.32

1.16

127.

76

tabl

e 9.

398,

653.

4311

2.26

9.85

and

Cam

bodi

aB

rune

i

A S

E A

N

Saba

hM

yanm

arM

alay

sia

Indo

nesi

aS

I. F

ood

and

Live

Ani

mal

sA

. Liv

e A

nim

als

B. M

eat a

nd M

eat P

repa

ratio

nsC

. Dai

ry P

rodu

cts

& B

ird's

Egg

sD

. Fis

h an

d Fi

sh P

repa

ratio

nsE

. Cer

eals

and

Cer

eal P

repa

ratio

nsF.

Veg

etab

les

and

Frui

tsG

. Sug

ar a

nd S

ugar

Pre

para

tions

H. C

offe

e, T

ea, C

ocoa

Spi

ces

and

Man

ufac

ture

s th

ereo

f I.

Fee

ding

Stu

ff fo

r Ani

mal

s

(e

xclu

ding

unm

illed

Cer

eals

)J.

Mis

cella

neou

s E

dibl

e P

rodu

cts

and

Pre

para

tions

II. T

obac

co a

nd T

obac

co M

anuf

actu

res

III. C

rude

Mat

eria

lsA

. Oil

See

ds a

nd O

leag

inou

s Fr

uits

B. C

rude

Rub

ber

C. C

rude

Fer

tiliz

erD

. Cru

de A

nim

al &

Ve g

etab

le

(incl

udin

g hi

des,

ski

ns a

nd

furk

ins,

raw

)

BIT

EM

720

780

892

58,3

80.9

331

3,81

9.69

538,

115.

551,

096,

870.

3326

.12

283.

5518

8.38

278.

9887

5.35

8,68

5.56

29,6

70.9

93,

506.

3154

,161

.18

1,07

6.14

905.

571,

953.

265,

940.

042,

897.

1316

1,00

9.90

496,

346.

7966

8,02

9.63

1,45

1.54

7,96

3.09

1,31

8.64

18,2

74.7

794

1.03

13,9

92.8

02,

224.

1133

,854

.86

12,5

12.5

51,

724.

7829

,297

.09

96,7

07.8

6

8,49

7.92

16,1

13.4

01,

261.

9042

,020

.89

22,0

35.5

182

,250

.78

1,92

8.47

176,

979.

63

2,90

7.11

6,62

1.16

5,05

7.08

25,8

29.4

2

11,5

83.2

120

,124

.38

853.

4952

,564

.45

137.

9230

9.33

428.

587,

181.

847,

493.

2418

,056

.80

151.

5830

,485

.13

1.06

0.71

73.7

6

204.

453,

950.

991,

757.

5419

9.57

14,6

93.0

3

Viet

nam

Thai

land

Sing

apor

e

Tota

l Phi

lippi

ne

Agric

ultu

ral

Expo

rts

to

ASEA

N

Tota

l Phi

lippi

ne

Agr

icul

tura

l Im

port

s to

A

SE

AN

Thai

land

Sing

apor

eCa

mbo

dia

Saba

hM

yanm

arM

alay

sia

Indo

nesi

aVi

etna

m

AGRICULTURAL FOREIGN TRADE DEVELOPMENT

2 0 0 7 A N N U A L

Tabl

e 9b

. (Con

tinue

d)

IV.

Anim

al a

nd V

eget

able

Oil

and

Fats

19.5

819

,907

.48

2.28

5,70

0.80

336,

258.

24

A. A

nim

al a

nd V

eget

able

Oils

and

Fat

s19

.58

2,94

9.61

11,9

17.9

5

B. F

ixed

Veg

etab

le O

ils a

nd F

ats

16,9

57.8

72.

285,

700.

8032

4,34

0.31

V. F

ertil

izer

Man

ufac

ture

d15

.40

15.4

0

VI. A

gric

ultu

ral C

hem

ical

s an

d M

ater

ials

5.00

3.91

108.

7016

9.85

VII.

Agr

icul

tura

l Mac

hine

ry13

1.07

46.2

721

9.96

TOTA

L VA

LUE

OF

AGR

ICU

LTU

RAL

EXP

OR

TS3,

634.

122,

744.

741,

152.

6142

,193

.09

5,94

5.20

55,4

39.3

261

9,78

3.06

TOTA

L VA

LUE

OF

ALL

PHIL

IPPI

NE

EXPO

RTS

Sou

rce

of b

asic

dat

a: N

SOIte

mEU

RO

PEAN

UN

ION

Pola

ndPo

rtug

alSl

oven

iaSp

ain

Swed

enU

K G

reat

Brit

ain

and

N. I

rela

ndTo

tal P

hil.

Agric

ultu

ral

Expo

rts

to E

U

18,3

18.5

2

17,7

10.3

2

2,72

5.61

143,

382.

98

26,2

11.0

7

478,

986.

56

8,

570,

499.

46

3 38

Income from four (4) major export commodities declined in 2007. Reductions ranged from 1.13% (Banana Fresh) to 13.89% (Shrimps and Prawns).

• Export earnings from fresh banana declined by 1.13%. From

US$405.44 million in 2006, export revenues decreased to US$400.85 million in 2007. The three (3) major markets which registered reductions in export transactions with the Philippines included United Arab Emirates by 31.97%, Taiwan by 21.21% and Iran by 18.15%.

• Exportation of manufactured tobacco slid from US$102.06 million

during the previous year to US$97.89 million in 2007. Major markets were Thailand (64.77%), Korea (7.36%), Vietnam (7.35%), Singapore (4.12%) and Hongkong (3.44%).

• Export receipts from shrimps and prawns which amounted to

US$84.85 million were down by 13.89% from last year’s receipts of US$98.54 million. The highest volume of exports was registered during the 1st quarter while the lowest was in the 4th quarter of the year. Destination points were Japan, Korea, USA, Canada and Guam.

• Export earnings from centrifugal sugar which amounted to US$77.49

million, declined by 5.88% from last year’s income of US$82.33 Foreign markets were USA, Indonesia, Japan, United Arab Emirates and France.

4. Agricultural Imports

Increased import expenditures were registered for most of the top 10 import commodities.

• For this year, rice was the top agricultural import displacing wheat. The

country spent US$653.51 million for rice and registered a 27.31% increase from the 2006 level. The bulk or 75.75% of the Philippine rice imports were again sourced from Vietnam. The highest value of importation for 2007 was registered on the second quarter.

AGRICULTURAL FOREIGN TRADE DEVELOPMENT

2 0 0 7 A N N U A L

Tabl

e 9b

. (Con

tinue

d)

I. F

ood

and

Live

Ani

mal

s2,

481.

732,

702.

541,

152.

6117

,574

.05

5,14

1.06

38,4

89.1

123

1,28

8.00

A. L

ive

Ani

mal

s 0.

0311

2.05

300.

28B.

Mea

t and

Mea

t Pre

para

tions

5.72

3.95

108.

41C

. Dai

ry P

rodu

cts

& Bi

rd's

Egg

s77

.62

225.

34D

. Fis

h an

d Fi

sh P

repa

ratio

ns37

1.55

2,64

0.09

1,08

6.78

10,8

79.2

72,

784.

406,

517.

4670

,821

.41

E. C

erea

ls a

nd C

erea

l Pre

para

tions

2.06

67.9

28.

4653

4.70

3,16

8.62

F. V

eget

able

s an

d Fr

uits

2,06

6.16

35.3

030

.45

6,15

2.12

2,14

3.20

28,3

21.1

314

2,95

0.10

G. S

ugar

and

Sug

ar P

repa

ratio

ns36

.34

61.0

11,

356.

713,

778.

95H

. Cof

fee,

Tea

, Coc

oa S

pice

s 0.

370.

0845

.83

292.

08

a

nd M

anuf

actu

res

ther

eof

I. F

eedi

ng S

tuff

for A

nim

als

44.0

235

.38

202.

6931

5.00

1,70

4.18

(exc

ludi

ng u

nmille

d C

erea

ls)

J. M

isce

llane

ous

Edib

le P

rodu

cts

25.0

922

9.58

143.

911,

204.

687,

938.

70

an

d Pr

epar

atio

ns

II. T

obac

co a

nd T

obac

co M

anuf

actu

res

178.

1866

9.59

97.0

23,

193.

57

III. C

rude

Mat

eria

ls1,

132.

8137

.20

4,51

4.07

1.20

10,9

97.4

246

,603

.08

A. O

il Se

eds

and

Ole

agin

ous

Frui

ts0.

46B.

Cru

de R

ubbe

r83

2.74

C. C

rude

Fer

tiliz

er0.

00D

. Cru

de A

nim

al &

Ve g

etab

le M

ater

ials

(inc

ludi

ng h

ides

, ski

ns a

nd

fu

rkin

s, ra

w)

1,13

2.81

37.2

04,

514.

07

1.20

10,9

97.4

2

45,7

69.8

7

Swed

enU

K G

reat

Brit

ain

and

N. I

rela

ndIte

mEU

RO

PEAN

UN

ION

Tota

l Phi

l. Ag

ricul

tura

l Ex

port

s to

EU

Pola

ndPo

rtug

alSl

oven

iaSp

ain

37 4

• Importation of milk and cream and products increased by 42.24%. From US$413.41 million in 2006, it went up to US$588.02 million with the biggest importation recorded during the 4th quarter. The major sources were New Zealand, Australia, United States of America, Thailand and Netherlands

• The increase in the foreign disbursement for meat of bovine animals

displaced urea in the 6th place in the major agricultural imports. In 2007, importation of meat of bovine animals reached US$138.35 million, an increase of 19.38% from 2006. India, Brazil, Australia, USA and New Zealand were the major sources of imports.

The country realized a remarkable increase in importation of rubber and coffee displacing maize and palm oil from the list of top 10 imports.

• Coffee which was not formerly included in the top ten agricultural

imports landed on the 10th place in 2007. The country spent US$69.47 million for this commodity, about 90% higher than in the previous year. Vietnam supplied about 41.10% and Indonesia brought in 35.34%.

• Importation of rubber reached US$87.57 million in 2007; it increased

by 17.96% compared to previous year’s level. The country’s major suppliers were Japan, Thailand, USA, Korea and Singapore.

• Despite the decrease in the import expenses for wheat by 19.30%, this

commodity remained in the list of top imports. The biggest importation was registered in the fourth quarter of the year. Wheat imports were mostly coming from the USA with 71.88% of the total importation. Other suppliers were Canada, China, Australia and Pakistan.

5. World Price Trends

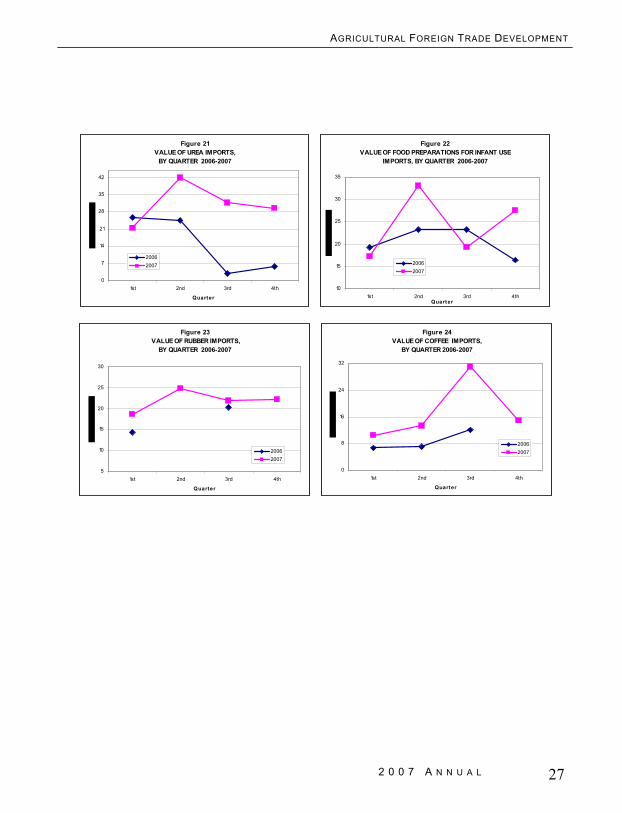

• Coconut oil and Copra. World prices of coconut oil and copra

showed similar patterns. World prices were going-up during the first half of the year. These started to go down in July but recovered in September until the end of the year. The lowest and highest prices were registered in January and December, respectively.

AGRICULTURAL FOREIGN TRADE DEVELOPMENT

2 0 0 7 A N N U A L

Tabl

e 9b

. (Con

tinue

d)

IV.

Ani

mal

and

Veg

etab

le O

il an

d Fa

ts31

,435

.06

40.5

727

2,57

1.82

A. A

nim

al a

nd V

eget

able

Oils

and

Fat

s11

9.77

2,61

4.47

B. F

ixed

Veg

etab

le O

ils a

nd F

ats

31,3

15.3

040

.57

269,

957.

35

V. F

ertil

izer

Man

ufac

ture

d

VI. A

gric

ultu

ral C

hem

ical

s an

d M

ater

ials

0.80

31.2

02.

16

VII.

Agr

icul

tura

l Mac

hine

ry29

6.29

3.96

TOTA

L VA

LUE

OF

AGR

ICU

LTU

RAL

EXP

OR

TS2,

628.

2499

7.01

1,97

8.38

46,5

28.5

844

4.90

614.

851.

8044

7.27

311,

595.

56

TOTA

L VA

LUE

OF

ALL

PHIL

IPPI

NE

EXPO

RTS

Sou

rce

of b

asic

dat

a: N

SOItem

EUR

OPE

AN U

NIO

NG

reec

eH

unga

ryIre

land

Italy

Latv

iaLi

thun

iaLu

xem

bour

gM

alta

Net

herla

nds

16,4

80.7

2

78,1

28.7

6

69,8

11.4

8

202,

842.

77

660.

81

1,37

0.15

3,

013.

66

22,1

46.1

2

4,14

9,52

2.31

5 36

• Sugar. A downtrend in international sugar prices was exhibited in the first half of 2007 and it registered its lowest level in June at US$0.205/kg. Prices recovered in the second half with the highest price posted at US$ 0.235/kg in December.

• Soybean. Better world prices were accorded to soybean throughout

the year. The highest quotation was registered at US$0.515/kg in December.

• Rice. For this year, similar trend was noted for the international prices of rice regardless of the percentage broken. Prices were higher than in the previous year. Surges were more pronounced towards the end of the year with the highest quotation noted in December.

• Maize. International price of maize fluctuated during the first nine months of 2007. The highest price was recorded in December at US$0.180/kg while the lowest at US$0.147/kg was noted in July. Rising prices were sustained from October until the end of the year.

• Coffee Arabica. Prices of coffee, Arabica in the world market

generally increased in 2007 and the highest quotation was registered at US$21.39/kg in October.

• Coffee Robusta. In 2007, monthly prices of coffee, robusta were

higher compared with last year’s quotations. These ranged from US$1.698/kg in March to US$ 2.043/kg in June.

• Banana. World prices of banana dropped in the first five (5) months of

the year compared with the previous year’s quotation. Prices recovered in June until the end of the year at a decreasing rate. Lowest prices were noted in March, April and December.

• Rubber. Generally, prices were higher compared with 2006. Surges of

about 40% were noted in the last two (2) months of the year.

AGRICULTURAL FOREIGN TRADE DEVELOPMENT

2 0 0 7 A N N U A L

Tabl

e 9b

. (C

ontin

ued)

IV.

Ani

mal

and

Veg

etab

le O

il an

d Fa

ts2,

299.

4110

2.10

2.30

26.6

04,

150.

24

A. A

nim

al a

nd V

eget

able

Oils

and

Fat

s2,

299.

4126

.53

3,88

8.58

B. F

ixed

Veg

etab

le O

ils a

nd F

ats

V.

Ferti

lizer

Man

ufac

ture

d10

2.10

2.30

0.07

261.

67

VI.

Agr

icul

tura

l Che

mic

als

and

Mat

eria

ls5.

846.

250.

035.

96

VII.

Agr

icul

tura

l Mac

hine

ry0.

518.

86

TOTA

L VA

LUE

OF

AGR

ICU

LTU

RAL

EXP

OR

TS1,

090.

5028

,632

.53

400.

113,

216.

3210

,551

.54

120.

684,

425.

5129

,738

.91

65,1

74.8

0

TOTA

L VA

LUE

OF

ALL

PHIL

IPPI

NE

EXPO

RTS

Sou

rce

of b

asic

dat

a: N

SO

Ger

man

y

69,1

87.9

1

666,

284.

79

1,82

9.40

72

,497

.80

32

,598

.05

2,

312.

77

79,7

31.3

8

265,

398.

84

2,14

9,34

6.68

Item

EUR

OPE

AN U

NIO

N

Aust

riaB

elgi

umC

ypru

sC

zech

R

epub

licD

enm

ark

Esto

nia

Finl

and

Fran

ce

7 34

STATISTICALTable

2 0 0 7 A N N U A L

I. Food and Live Animals 2,021,344.83 27,223.28 383,656.11 446,087.87 A. Live Animals 3,390.96 1,024.62 855.03 B. Meat and Meat Preparations 19,720.83 142.09 13,321.69 210.97 C. Dairy Products & Bird's Eggs 140,709.58 162.89 249.47 1,546.98

D. Fish and Fish Preparations 470,076.58 2,278.59 68,210.16 137,603.84 E. Cereals and Cereal Preparations 70,464.15 4,808.35 3,584.66 9,704.09 F. Vegetables and Fruits 1,025,838.09 15,604.46 274,174.77 209,539.46 G. Sugar and Sugar Preparations 132,359.44 742.83 10,422.19 65,520.92 H. Coffee, Tea, Cocoa Spices 14,270.43 515.25 4,022.19 2,425.37

and Manufactures thereof I. Feeding Stuff for Animals 49,634.14 68.77 4,117.98 255.00

(excluding unmilled Cereals)J. Miscellaneous Edible Products 94,880.83 2,900.05 4,528.38 18,426.21

and PreparationsII. Tobacco and Tobacco Manufactures 140,871.97 1,505.25 451.82 6,842.63 III. Crude Materials 165,652.92 2,495.49 8,057.57 17,816.11

A. Oil Seeds and Oleaginous Fruits 131.86 56.83 B. Crude Rubber 42,093.38 307.28 150.18 C. Crude Fertilizer 509.75 3.20 9.06 D. Crude Animal & Vegetable Materials (including hides, skins and furkins, raw) 122,909.62 2,495.49 7,690.26 17,656.87

IV. Animal and Vegetable Oil and Fats 769,159.41 34.74 50,957.43 314,657.80 A. Animal and Vegetable Oils and Fats 3,505.76 3.37 583.18 8,583.78 B. Fixed Vegetable Oils and Fats 734,108.64 31.37 50,374.25 306,074.02

V. Fertilizer Manufactured 53,640.66 588.50 22.79 VI. Agricultural Chemicals and Materials 9,885.67 745.41 73.55 584.98 VII. Agricultural Machinery 7,509.95 31.85 1,173.03 1,948.43

TOTAL VALUE OF AGRICULTURAL EXPORTS

TOTAL VALUE OF ALLPHILIPPINE EXPORTS

Source of basic data: NSO

JAPAN AND USA, 2007 (F.O.B. Value in '000 US$)

Item

Table 9a. DISTRIBUTION OF PHILIPPINE AGRICULTURAL EXPORTS TO AUSTRALIA,

Total Philippine

Agricultural Australia Japan USA

3,168,065.41 32,624.52 444,392.30 787,937.82

32,981,329.35 528,414.46 7,304,148.30 8,546,805.06

9 32

OVERALL AGRICULTURAL TRADE S

2007/2006 2006/2005

Agricultural Exports 3,168.07 2,781.36 2,691.19 13.90 3.35

Total Exports 50,465.72 47,410.12 41,254.68 6.45 14.92

Percent of Agricultural Exports Total Exports 6.30 5.87 6.52 7.33 -9.97

Agricultural Imports 4,918.29 4,303.57 3,975.62 14.28 8.25

Total Imports 57,995.75 54,077.99 49,487.42 7.24 9.28

Percent of Agricultural Imports 8.48 7.96 8.03 6.54 -0.87 to Total Imports

Agricultural Trade Surplus/Deficit -1,750.22 -1,522.21 -1,284.43 14.98 18.51

P- preliminarySource of Basic Data: National Statistics Office (NSO)

Table 1. SUMMARY OF PHILIPPINE AGRICULTURAL TRADE, 2005 - 2007(Export Value in F.O.B. M US$; Import Value in C.I.F. M US$)

Growth Rate 2006 2005Item 2007P

F igure 1 SH A R E OF A GR IC ULT UR A L A N D N ON -A GR IC ULT UR A L EXP OR T S T O T OT A L

P H ILIP P IN E EXP OR T S, 2006

Non-Agricultural

94%

Agricultural6%

F igure 2 SH A R E OF A GR IC ULT UR A L A N D N ON -A GR IC ULT UR A L IM P OR T S T O T OT A L

P H ILIP P IN E IM P OR T S, 2006

Agricultural8%

Non-Agricultural

92%

Figure 1SHARE OF AGRICULTURAL AND

NON-AGRICULTURAL EXPORTS TO TOTAL PHILIPPINE IMPORTS, 2007

Figure 2 SHARE OF AGRICULTURAL AND

NON-AGRICULTURAL IMPORTS TO TOTAL PHILIPPINE IMPORTS, 2007

AGRICULTURAL FOREIGN TRADE DEVELOPMENT

2 0 0 7 A N N U A L

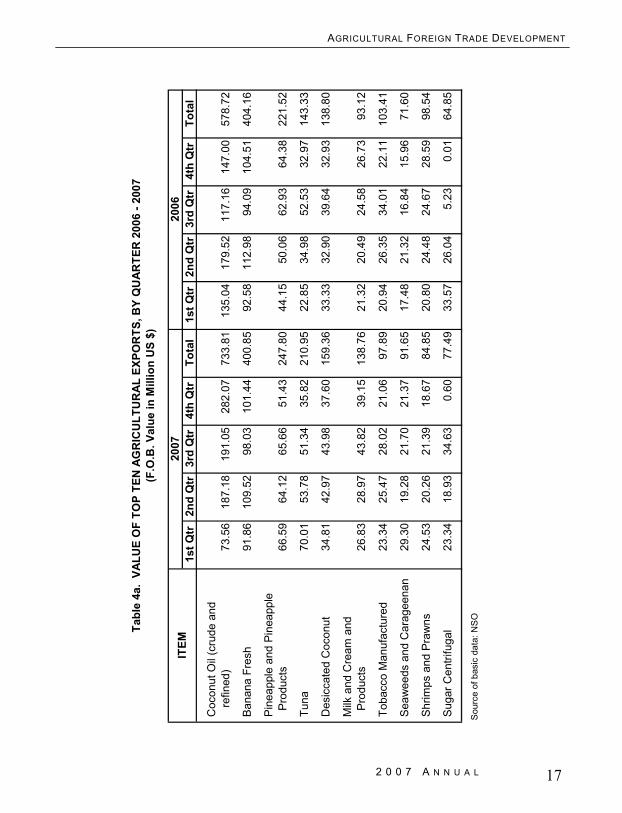

31 10

1st Qtr 2nd Qtr 3rd Qtr 4th Qtr TOTAL

Agricultural Exports 606.07 806.93 841.97 913.10 3,168.07

Percent to Annual Agricultural Exports 19.13 25.47 26.58 28.82

Agricultural Imports 973.06 1,267.06 1,282.88 1,395.29 4,918.29

Percent to Annual Agricultural Imports 19.78 25.76 26.08 28.37

Agricultural Trade Surplus/Deficit

1st Qtr 2nd Qtr 3rd Qtr 4th Qtr TOTAL

Agricultural Exports 621.49 760.40 716.73 682.74 2,781.36

Percent to Annual Agricultural Exports 22.34 27.34 25.77 24.55

Agricultural Imports 1,087.76 1,173.04 1,095.33 947.33 4,303.46

Percent to Annual Agricultural Imports 25.28 27.26 25.45 22.01

Agricultural Trade Surplus/Deficit

Source of Basic Data: National Statistics Office (NSO)

Table 1a. PHILIPPINE AGRICULTURAL TRADE, BY QUARTER 2006 - 2007 (Export Value in F.O.B. M US$; Import Value in C.I.F. M US$)

Item

2006

2007

Item

(366.99) (460.13) (440.91) (482.19)

(466.27) (412.64) (264.59) (378.60)

Bru

nei

Cam

bodi

aIn

done

sia

Mal

aysi

aM

yanm

arSa

bah

Sara

wak

Sing

apor

eTh

aila

ndVi

etna

m

IFo

odan

dLi

veA

nim

als

158

258

231

047

9539

060

5486

999

104

4227

424

1278

5308

838

4280

938

4599

667

296

439

51IV

. Ani

mal

and

Veg

etab

le O

il

Oils

and

Fat

s0.

693,

879.

2025

,263

.41

351.

8976

2.18

197.

250.

2630

,454

.88

A. A

nim

al a

nd V

eget

able

a

nd F

ats

0.16

362.

581,

098.

6135

1.89

436.

1219

7.25

0.26

2,44

6.87

B. F

ixed

Veg

etab

le O

ils

a

nd F

ats

0.54

3,51

6.62

24,1

64.7

932

6.06

28,0

08.0

1

V. F

ertil

izer

Man

ufac

ture

d9,

338.

6396

3.34

2,29

1.59

27,4

03.4

939

,997

.05

VI.

Agric

ultu

ral C

hem

ical

s

and

Mat

eria

ls1.

291.

8261

3.39

1,21

5.43

20.8

910

8.89

333.

062,

719.

2323

7.17

5,25

1.17

VII.

Agr

icul

tura

l Mac

hine

ry (N

o.)

0.98

99.6

497

.14

0.50

1.02

375.

4321

5.10

1,39

6.65

2,18

6.46

TOTA

L VA

LUE

OF

AGR

ICU

LTU

RA

L EX

POR

TS1,

600.

112,

441.

8711

7,32

1.71

106,

185.

201,

060.

9040

0.92

31.5

870

,127

.82

117,

981.

3586

,278

.55

503,

430.

01

TOTA

L VA

LUE

OF

ALL

PHIL

IPPI

NE

EXPO

RTS

no e

xpor

t dat

a to

Lao

s

Sour

ce o

f bas

ic d

ata:

NSO

Tabl

e 9.

(C

ontin

ued)

1,40

3.02

8.76

Tota

l Ph

ilipp

ine

Agric

ultu

ral

Expo

rts

to

ASEA

N

ITEM

A S

E A

N

436,

169.

008,

031,

462.

075,

854.

398,

531.

8152

4,46

9.88

2,49

7,50

1.36

8,01

0.74

6,64

1.16

2,56

1.13

3,13

8,69

3.84

1,40

3,02

8.76

AGRICULTURAL FOREIGN TRADE DEVELOPMENT

2 0 0 7 A N N U A L

11 30

Bru

nei

Cam

bodi

aIn

done

sia

Mal

aysi

aM

yanm

arSa

bah

Sara

wak

Sing

apor

eTh

aila

ndVi

etna

m

I. F

ood

and

Live

Ani

mal

s1,

582.

582,

310.

4795

,390

.60

54,8

69.9

910

4.42

274.

2412

.78

53,0

88.3

842

,809

.38

45,9

96.6

729

6,43

9.51

A. L

ive

Anim

als

(No.

)20

9.02

2.00

568.

239.

061.

6813

.85

1.77

805.

61B.

Mea

t and

Mea

t

Pre

para

tions

109.

305.

370.

7244

.71

609.

1871

7.12

1,48

6.40

C. D

airy

Pro

duct

s an

d

Bird

's E

ggs

15.1

468

,884

.28

34,9

36.6

170

.57

595.

247,

456.

064,

189.

2811

6,14

7.18

D. F

ish

& Fi

sh P

repa

ratio

ns85

.99

0.45

1,16

5.81

2,77

5.80

223.

5515

,178

.03

13,3

23.4

62,

541.

0035

,294

.09

E. C

erea

ls a

nd C

erea

l

Pre

para

tions

185.

033.

805,

872.

806,

759.

080.

5341

.36

1,58

1.73

10,0

48.6

937

6.58

24,8

69.6

0F.

Veg

etab

les

and

Frui

ts43

2.88

2.14

5,66

1.92

1,66

4.79

4.41

7.36

30,4

26.3

42,

538.

276,

487.

1747

,225

.28

G. S

ugar

and

Sug

ar

P

repa

ratio

ns93

.41

2,29

2.81

9,14

9.83

2,91

5.39

2.20

594.

134,

749.

3922

,585

.10

42,3

82.2

6H

. Cof

fee,

Tea

, Coc

oa,

Spi

ces

and

Man

ufac

ture

s

th

ereo

f47

.85

819.

3832

2.84

387.

101,

019.

2222

.36

2,61

8.75

I. Fe

edin

g St

uff f

or A

nim

als

(exc

ludi

ng u

nmill

ed C

erea

ls)

28.3

521

9.06

26.4

10.

5493

2.51

335.

458,

298.

340.

00J.

Mis

cella

neou

s E

dibl

e 40

3.96

9.27

3,23

4.63

5,26

6.64

2.50

5.45

4.88

3,33

4.74

2,72

7.89

779.

7215

,769

.68

Prod

ucts

and

Pre

para

tions

II. T

obac

co a

nd T

obac

co

M

anuf

actu

res

14.5

712

1.13

3,60

2.87

3,46

4.54

583.

208,

107.

2963

,422

.58

5,67

2.50

84,9

88.6

8

III. C

rude

Mat

eria

ls8.

454,

397.

3820

,311

.35

17.7

917

.78

7,46

1.48

6,32

6.22

5,57

1.81

44,1

12.2

6

A. O

il Se

eds

& O

leag