1 Chapter 20 Accounting for Pensions and Postretirement Benefits 1 Annual reports: Coca Cola (pages 4, 106) Learning Objectives 1. Distinguish between accounting for employer’s pension plan and accounting for pension fund 2. Types of pension plans and their characteristics 3. Alternative measures for valuing pension obligation 4. List components of pension expense 5. Use a worksheet for employer’s pension plan entries 6. Describe amortization of prior service costs 7. Accounting for unexpected gains and losses 8. Corridor approach to amortizing gains and losses 9. Requirements for reporting pension plans 2 Investments Learning Objective 1 Distinguish between accounting for employer’s pension plan and accounting for pension fund 4 Nature of Pension Plans Employer provides benefits To retired employees As compensation for services employees provided while working Form of delayed compensation 5 Nature of Pension Plans 6 Contributions Retired Employees Payments Assets & Liabilities Pension Plan Administrator Employer

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Chapter 20

Accounting for Pensions and Postretirement Benefits

1

Annual reports: Coca Cola (pages 4, 106)

Learning Objectives

1. Distinguish between accounting for employer’s pension plan and accounting for pension fund

2. Types of pension plans and their characteristics 3. Alternative measures for valuing pension obligation 4. List components of pension expense 5. Use a worksheet for employer’s pension plan entries 6. Describe amortization of prior service costs 7. Accounting for unexpected gains and losses 8. Corridor approach to amortizing gains and losses 9. Requirements for reporting pension plans

2

Investments Learning Objective 1

§ Distinguish between accounting for employer’s pension plan and accounting for pension fund

4

Nature of Pension Plans

§ Employer provides benefits § To retired employees § As compensation for services

employees provided while working § Form of delayed compensation

5

Nature of Pension Plans

6

Contributions

Retired Employees

Payments Assets & Liabilities

Pension Plan Administrator Employer

2

Accounting for Employer and Pension Plan Administrator

7

Pension Plan Administrator Employer

Contributions

Topic of Chapter 20 is accounting for employer

Pension Plan Administrator

§ Receives contributions § Plans and executes investment strategy § Pays beneficiaries

8

Learning Objective 2

§ Identify types of pension plans and their characteristics

9

Two Types of Pension Plans

§ Defined Contribution Plan § Defined Benefit Plan

10

Defined Contribution Plan

§ Employer contribution limited § Employer payment based on formula

§ Employee age, service, salary; Profits § After payment employer has no further

obligation § Plan administrator pays retirees

§ Based on value of plan assets § Depends contributions, investment growth

11

Defined Contribution Plan

§ Accounting simple § Employer makes contribution each year § Employer’s annual cost is amount paid § No pension asset or liability

12

Description Debit Credit Pension Expense 150,000 Cash 150,000 Annual payment to defined contribution plan

Defined contribution plans not covered in ACTG 162

3

Defined Benefit Plan

§ Benefits fixed by contract § Employer contribution not limited § Payments to retirees determined by

§ Compensation near retirement § Years of service

§ Future benefits and plan assets function of many uncertain variables

§ Accounting complex 13

Actuary

§ Estimates interest rates, rates of return § Calculates projected benefit obligation

(PBO) liability § Calculates employer contributions

14

Actuarial Services

§ Actuaries determine employer contribution by estimating § Future salaries § Mortality rates § Employee turnover § Early retirement frequency § Interest rates on borrowing § Rate of return on investments

15

Estimates

§ All estimates are wrong § Some estimates are useful § To be useful an estimate must

§ Be reasonable § Make financial statements more

meaningful (than without an estimate)

16

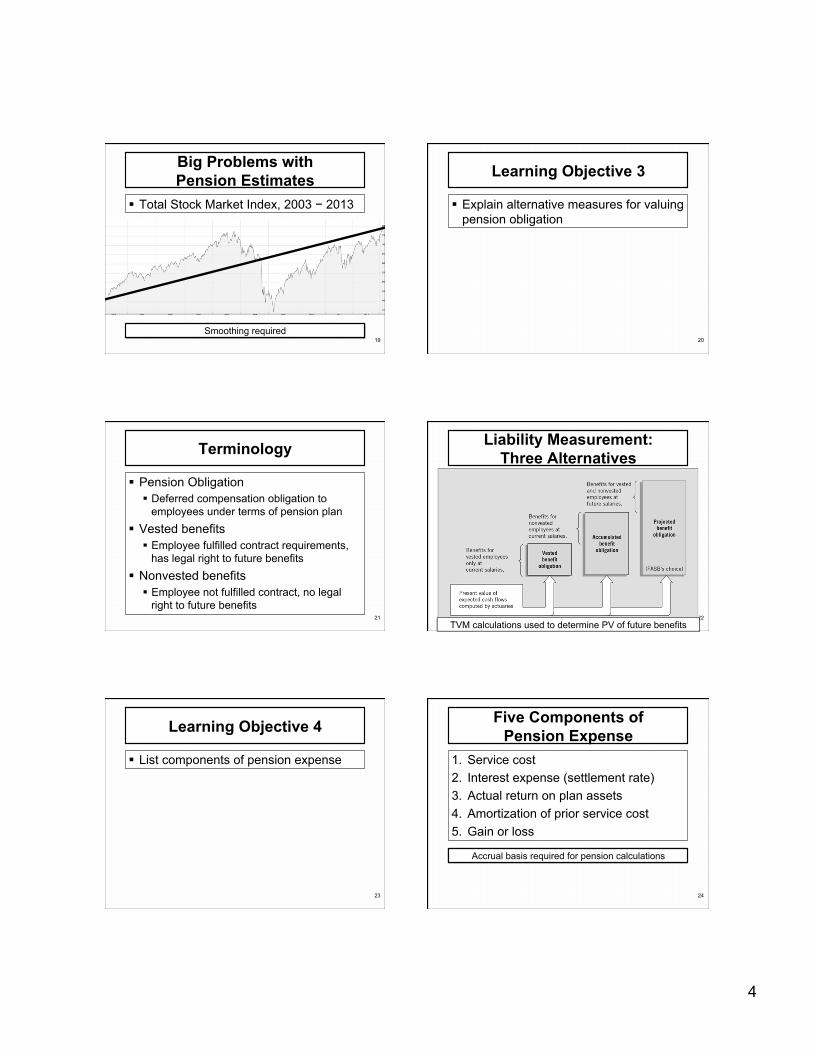

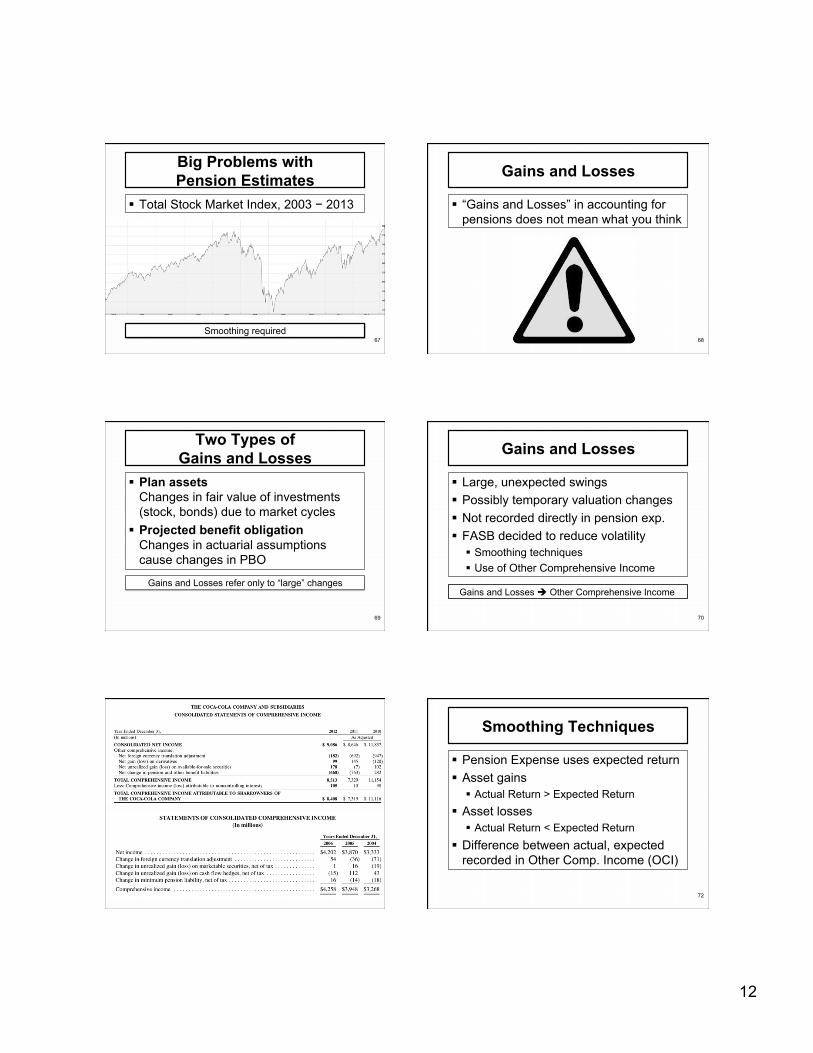

Big Problems with Pension Estimates

§ Estimates for very long periods § Actual performance may differ

significantly from estimate § Wide swings in actual performance

§ Over several years stock market portfolio may go down 40% then up 90%

§ Quarterly reporting required

17

Smoothing required

Big Problems with Pension Estimates

§ Total Stock Market Index, 2003 2013

18

4

Big Problems with Pension Estimates

§ Total Stock Market Index, 2003 − 2013

19 Smoothing required

Learning Objective 3

§ Explain alternative measures for valuing pension obligation

20

Terminology

§ Pension Obligation § Deferred compensation obligation to

employees under terms of pension plan § Vested benefits

§ Employee fulfilled contract requirements, has legal right to future benefits

§ Nonvested benefits § Employee not fulfilled contract, no legal

right to future benefits 21

Liability Measurement: Three Alternatives

22 TVM calculations used to determine PV of future benefits

Learning Objective 4

§ List components of pension expense

23

Five Components of Pension Expense

1. Service cost 2. Interest expense (settlement rate) 3. Actual return on plan assets 4. Amortization of prior service cost 5. Gain or loss

24

Accrual basis required for pension calculations

5

Service Costs

§ Present value of new benefits earned by employees during period

25

Service Costs + 1

Interest on Liability

§ Interest on projected benefit obligation § Actuary selects “settlement rate”

26

Service Costs + 1 Interest on Liability + 2

Settlement rate based rates of return on high quality, fixed income investments whose cash flows match timing and amount of expected benefit payments

Actual Return on Plan Assets

§ Increase (decrease) in plan assets from § Interest and dividends received § Realized, unrealized changes in fair value

27

Service Costs + 1 Interest on Liability + 2 Actual Return on Plan Assets ± 3

Actual Return on Plan Assets

28

Actual Return on Plan Assets Fair value plan assets, ending $ 900

− Fair value plan assets, beginning 600 Increase (decrease) in plan assets 300 Contributions to plan $ 500

− Benefits paid from plan 400 Net change from plan activity 100 Actual return on plan assets $ 200

Increase subtracted from [decreases] pension expense Decrease added to [increases] pension expense

Actual Return on Plan Assets

29

Service Costs + 1 Interest on Liability + 2 Actual Return on Plan Assets ± 3

30

6

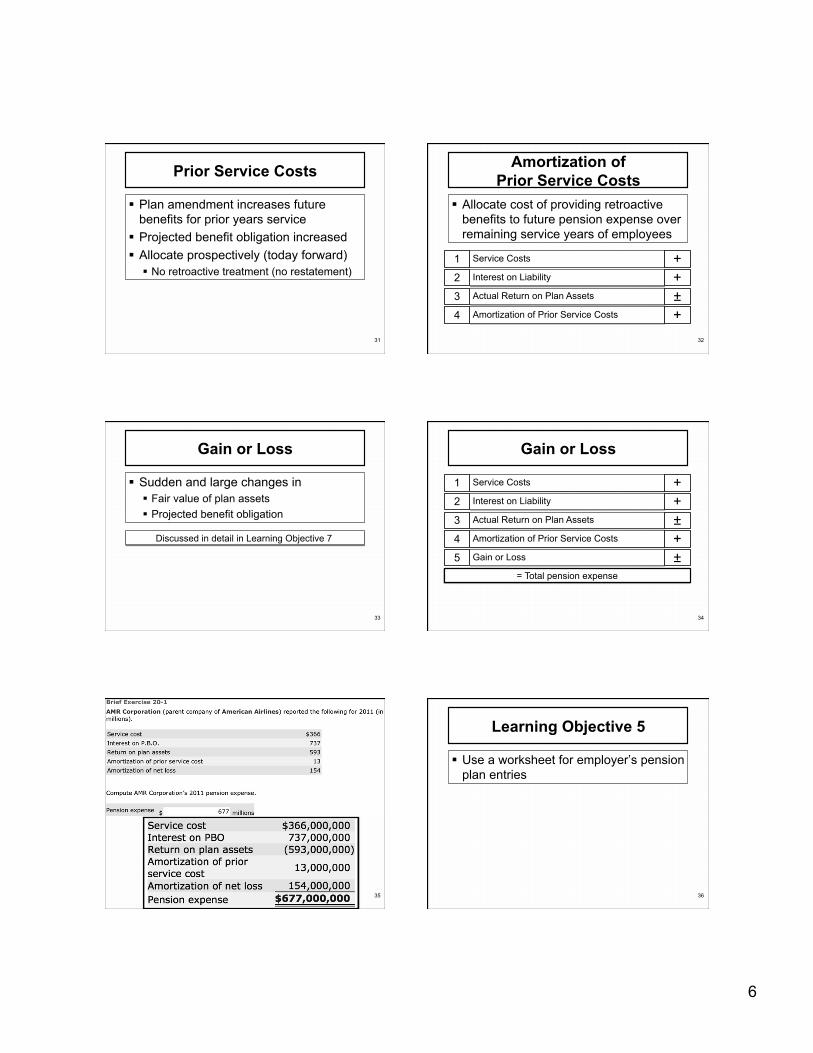

Prior Service Costs

§ Plan amendment increases future benefits for prior years service

§ Projected benefit obligation increased § Allocate prospectively (today forward)

§ No retroactive treatment (no restatement)

31

Amortization of Prior Service Costs

§ Allocate cost of providing retroactive benefits to future pension expense over remaining service years of employees

32

Service Costs + 1 Interest on Liability + 2 Actual Return on Plan Assets ± 3 Amortization of Prior Service Costs + 4

Gain or Loss

§ Sudden and large changes in § Fair value of plan assets § Projected benefit obligation

33

Discussed in detail in Learning Objective 7

Gain or Loss

34

Service Costs + 1

= Total pension expense

Interest on Liability + 2 Actual Return on Plan Assets ± 3 Amortization of Prior Service Costs + 4 Gain or Loss ± 5

35

Learning Objective 5

§ Use a worksheet for employer’s pension plan entries

36

7

Pension Work Sheet

37

Entries create required journal entry Maintain balances

Pension Work SheetGENERAL JOURNAL ENTRIES MEMO RECORD

Prior Pension ProjectedPension Service Asset / Benefit Plan

Items Expense Cash Costs (PSC) Gain/Loss Liability Obligation Assets

Other Comprehensive Income (OCI)

Pension Work Sheet

§ Enter beginning balances on first line § Record activity for period as line items § For each line debits = credits

38

Calculation of Pension Asset (Liability) Ending Plan Assets $ 307,500

− Ending Projected Benefit Obligation 318,000 Ending Pension Asset (Liability) $ (10,500)

Pension Work Sheet: Case 1

39

January 1, 2012 Plan assets $280,000 Projected benefit obligation $280,000

Activity During 2012 Service cost $27,500 Settlement rate 10% Actual return on plan assets $25,000 Expected return on plan assets $25,000 Contributions $20,000 Benefits paid $17,500

Pension Work Sheet: Case 1

40

January 1, 2012 Plan assets $280,000 Projected benefit obligation $280,000

Activity During 2012 Service cost $27,500 Settlement rate 10% Actual return on plan assets $25,000 Expected return on plan assets $25,000 Contributions $20,000 Benefits paid $17,500

Because plan assets = projected benefit obligation no pension asset or liability at beginning of year

Pension Work Sheet: Case 1

41

January 1, 2012 Plan assets $280,000 Projected benefit obligation $280,000

Activity During 2012 Service cost $27,500 Settlement rate 10% Actual return on plan assets $25,000 Expected return on plan assets $25,000 Contributions $20,000 Benefits paid $17,500

Because actual return = expected return no “unexpected gain or loss” (explained later)

Pension Work Sheet: Case 1

Pension Projected Pension Asset / Benefit Plan

Items Expense Cash PSC Gain/Loss Liability Obligation Assets Jan. 1, 2010 0 (280,000) 280,000

Service costs 27,500 (27,500)

Interest costs 28,000 (28,000)

Actual return (25,000) 25,000

Contributions (20,000) 20,000

Benefits paid 17,500 (17,500)

Journal entry 30,500 (20,000) (10,500)

Dec. 31, 2010 - - (10,500) (318,000) 307,500

MEMO RECORD GENERAL JOURNAL ENTRIES OCI

($280,000 x 10%)

January 1, 2012 Plan assets $280,000 Projected benefit obligation $280,000

8

Pension Projected Pension Asset / Benefit Plan

Items Expense Cash PSC Gain/Loss Liability Obligation Assets Jan. 1, 2010 0 (280,000) 280,000

Service costs 27,500 (27,500)

Interest costs 28,000 (28,000)

Actual return (25,000) 25,000

Contributions (20,000) 20,000

Benefits paid 17,500 (17,500)

Journal entry 30,500 (20,000) (10,500)

Dec. 31, 2010 - - (10,500) (318,000) 307,500

MEMO RECORD GENERAL JOURNAL ENTRIES OCI

Service cost $27,500 Settlement rate 10% Actual return on plan assets $25,000 Expected return on plan assets $25,000 Contributions $20,000 Benefits paid $17,500

($280,000 x 10%)

Pension Projected Pension Asset / Benefit Plan

Items Expense Cash PSC Gain/Loss Liability Obligation Assets Jan. 1, 2010 0 (280,000) 280,000

Service costs 27,500 (27,500)

Interest costs 28,000 (28,000)

Actual return (25,000) 25,000

Contributions (20,000) 20,000

Benefits paid 17,500 (17,500)

Journal entry 30,500 (20,000) (10,500)

Dec. 31, 2010 - - (10,500) (318,000) 307,500

MEMO RECORD GENERAL JOURNAL ENTRIES OCI

Service cost $27,500 Settlement rate 10% Actual return on plan assets $25,000 Expected return on plan assets $25,000 Contributions $20,000 Benefits paid $17,500

($280,000 x 10%)

Pension Projected Pension Asset / Benefit Plan

Items Expense Cash PSC Gain/Loss Liability Obligation Assets Jan. 1, 2010 0 (280,000) 280,000

Service costs 27,500 (27,500)

Interest costs 28,000 (28,000)

Actual return (25,000) 25,000

Contributions (20,000) 20,000

Benefits paid 17,500 (17,500)

Journal entry 30,500 (20,000) (10,500)

Dec. 31, 2010 - - (10,500) (318,000) 307,500

MEMO RECORD GENERAL JOURNAL ENTRIES OCI

($280,000 x 10%)

Description Debit Credit Pension expense 30,500 Cash 20,000 Pension asset / liability 10,500 AJE: Record pension expense, cash paid, change in pension asset/liab.

Plug

Pension Work Sheet: Case 1

Pension Projected Pension Asset / Benefit Plan

Items Expense Cash PSC Gain/Loss Liability Obligation Assets Jan. 1, 2010 0 (280,000) 280,000

Service costs 27,500 (27,500)

Interest costs 28,000 (28,000)

Actual return (25,000) 25,000

Contributions (20,000) 20,000

Benefits paid 17,500 (17,500)

Journal entry 30,500 (20,000) (10,500)

Dec. 31, 2010 - - (10,500) (318,000) 307,500

MEMO RECORD GENERAL JOURNAL ENTRIES OCI

($280,000 x 10%)

Difference between Projected Benefit Obligation, Plan Assets must equal ending balance in Pension Asset / Liability account

($10,500) net liability

47

Brief Exercise 20-3 At January 1, 2014, Hennein Company had plan assets of $294,000 and a projected benefit obligation of the same amount. During 2014, service cost was $32,370, the settlement rate was 10%, actual and expected return on plan assets were $25,760, contributions were $21,990, and benefits paid were $21,550. Prepare a pension worksheet for Hennein Company for 2014.

48

9

49 50

51 52

Learning Objective 6

§ Amortization of prior service costs

53

Prior Service Costs

§ Plan amendment increases future benefits for prior years service

§ Projected benefit obligation increased § Allocate cost of providing retroactive

benefits to future pension expense over remaining service years of employees

54

10

Amortization of Prior Service Cost

§ Prospective change (today forward) § Not retroactive or in year of change only

§ Amortization methods § FASB prefers years of service method

§ Like units-of-production method § (Years in current period / Total years)

§ SFAS No. 158 allows straight line method

55

Prior Service Cost è Other Comprehensive Income

Pension Work Sheet: Case 2 On January 1, 2012 Projected benefit obligation (before change) $560,000 Plan assets 546,200 Pension liability 13,800 Prior service benefits granted in 2012 120,000

56

During 2012 Settlement rate 9% Service cost 58,000 Contributions (funding) 65,000 Actual return on plan assets 52,280 Benefits paid to retirees 40,000 Prior service cost amortization for 2012 17,000

Pension Projected Pension Gain / Asset / Benefit Plan

Items Expense Cash PSC Loss Liability Obligation Assets Dec. 31, 2010 (13,800) (560,000) 546,200 PSC 120,000 (120,000) Bal. Jan. 1, 2010 (680,000) 546,200 Service costs 58,000 (58,000) Interest costs 61,200 (61,200) Asset Return (52,280) 52,280 Amort. PSC 17,000 (17,000) Contributions (65,000) 65,000 Benefits paid 40,000 (40,000) Journal entry 83,920 (65,000) 103,000 (121,920) AOCI -12/31/2011 - Dec. 31, 2012 103,000 - (135,720) (759,200) 623,480

MEMO RECORD GENERAL JOURNAL ENTRIES OCI

($135,720) liability

On January 1, 2012 Projected benefit obligation (before change) $560,000 Plan assets 546,200 Pension liability 13,800 Prior service benefits granted in 2012 120,000

Pension Projected Pension Gain / Asset / Benefit Plan

Items Expense Cash PSC Loss Liability Obligation Assets Dec. 31, 2010 (13,800) (560,000) 546,200 PSC 120,000 (120,000) Bal. Jan. 1, 2010 (680,000) 546,200 Service costs 58,000 (58,000) Interest costs 61,200 (61,200) Asset Return (52,280) 52,280 Amort. PSC 17,000 (17,000) Contributions (65,000) 65,000 Benefits paid 40,000 (40,000) Journal entry 83,920 (65,000) 103,000 (121,920) AOCI -12/31/2011 - Dec. 31, 2012 103,000 - (135,720) (759,200) 623,480

MEMO RECORD GENERAL JOURNAL ENTRIES OCI

($135,720) liability

During 2012 Settlement rate 9% Service cost 58,000 Contributions (funding) 65,000

Pension Projected Pension Gain / Asset / Benefit Plan

Items Expense Cash PSC Loss Liability Obligation Assets Dec. 31, 2010 (13,800) (560,000) 546,200 PSC 120,000 (120,000) Bal. Jan. 1, 2010 (680,000) 546,200 Service costs 58,000 (58,000) Interest costs 61,200 (61,200) Asset Return (52,280) 52,280 Amort. PSC 17,000 (17,000) Contributions (65,000) 65,000 Benefits paid 40,000 (40,000) Journal entry 83,920 (65,000) 103,000 (121,920) AOCI -12/31/2011 - Dec. 31, 2012 103,000 - (135,720) (759,200) 623,480

MEMO RECORD GENERAL JOURNAL ENTRIES OCI

During 2012 Actual return on plan assets 52,280 Benefits paid to retirees 40,000 Prior service cost amortization for 2012 17,000

Pension Projected Pension Gain / Asset / Benefit Plan

Items Expense Cash PSC Loss Liability Obligation Assets Dec. 31, 2010 (13,800) (560,000) 546,200 PSC 120,000 (120,000) Bal. Jan. 1, 2010 (680,000) 546,200 Service costs 58,000 (58,000) Interest costs 61,200 (61,200) Asset Return (52,280) 52,280 Amort. PSC 17,000 (17,000) Contributions (65,000) 65,000 Benefits paid 40,000 (40,000) Journal entry 83,920 (65,000) 103,000 (121,920) AOCI -12/31/2011 - Dec. 31, 2012 103,000 - (135,720) (759,200) 623,480

MEMO RECORD GENERAL JOURNAL ENTRIES OCI

($135,720) liability

Description Debit Credit Pension expense 83,920 Other comprehensive income 103,000 Cash 65,000 Pension asset / liability 121,920 AJE: Record pension expense, cash paid, change in pension asset/liab.

Plug

11

Pension Projected Pension Gain / Asset / Benefit Plan

Items Expense Cash PSC Loss Liability Obligation Assets Dec. 31, 2010 (13,800) (560,000) 546,200 PSC 120,000 (120,000) Bal. Jan. 1, 2010 (680,000) 546,200 Service costs 58,000 (58,000) Interest costs 61,200 (61,200) Asset Return (52,280) 52,280 Amort. PSC 17,000 (17,000) Contributions (65,000) 65,000 Benefits paid 40,000 (40,000) Journal entry 83,920 (65,000) 103,000 (121,920) AOCI -12/31/2011 - Dec. 31, 2012 103,000 - (135,720) (759,200) 623,480

MEMO RECORD GENERAL JOURNAL ENTRIES OCI

($135,720) liability

Difference between Projected Benefit Obligation, Plan Assets must equal ending balance in Pension Asset / Liability account

62

63 64

Learning Objective 7, 8

§ Explain accounting for unexpected gains and losses

§ Explain corridor approach to amortizing gains and losses

65

Five Components of Pension Expense

66

Service Costs + 1

= Total pension expense

Interest on Liability + 2 Actual Return on Plan Assets ± 3 Amortization of Prior Service Costs + 4 Gain or Loss ± 5

12

Big Problems with Pension Estimates

§ Total Stock Market Index, 2003 − 2013

67 Smoothing required

Gains and Losses

§ “Gains and Losses” in accounting for pensions does not mean what you think

68

Two Types of Gains and Losses

§ Plan assets Changes in fair value of investments (stock, bonds) due to market cycles

§ Projected benefit obligation Changes in actuarial assumptions cause changes in PBO

69

Gains and Losses refer only to “large” changes

Gains and Losses

§ Large, unexpected swings § Possibly temporary valuation changes § Not recorded directly in pension exp. § FASB decided to reduce volatility

§ Smoothing techniques § Use of Other Comprehensive Income

70

Gains and Losses è Other Comprehensive Income

71

Smoothing Techniques

§ Pension Expense uses expected return § Asset gains

§ Actual Return > Expected Return § Asset losses

§ Actual Return < Expected Return § Difference between actual, expected

recorded in Other Comp. Income (OCI)

72

13

Smoothing Techniques

§ PBO liability gains § Unexpected decreases in liability balance

§ PBO liability losses § Unexpected increases in liability balance

§ Deferred in same OCI account

73

Gains and Losses

§ Record in net gain or loss account § Difference between expected return and

actual return on plan assets § Gains (Losses) from changes in Projected

Benefit Obligation (PBO)

74

Pension Work Sheet: Case 3

75

January 1, 2011 Plan assets $200,000 Projected benefit obligation $250,000 Plan Asset (Liability) $ 50,000

Estimates for Year Ended December 31, 2011 Settlement rate (interest on PBO) 10% Expected rate of return (growth in plan assets) 10% Average remaining service life (in years) 15

Pension Work Sheet: Case 3

76

2011 2012 2013 Annual service cost $16,000 $19,000 $26,000 Actual return on plan assets 18,000 22,000 24,000 Expected return on plan assets* 20,000 22,000 26,560 Annual funding (contributions) 16,000 40,000 48,000 Benefits paid 14,000 16,400 21,000 Prior service cost (amended, 1/1/12) 160,000 Amortization of prior service cost 54,400 41,600 Change in PBO actuarial assumptions; ending balance as of 12/31/2013 520,000

*Beg bal plan assets × Expected rate of return = Expected return

77

Pension ProjectedPension Gain / Asset / Benefit Plan

Items Expense Cash PSC Loss Liability Obligation AssetsBal. Jan. 1, 2011 (50,000) (250,000) 200,000 Service costs 16,000 (16,000) Interest 25,000 (25,000) Return on assets (18,000) 18,000 Unexpected loss (2,000) 2,000 Contributions (16,000) 16,000 Benefits paid 14,000 (14,000) Journal entry 21,000 (16,000) 2,000 (7,000) AOCI - 12/31/10 - Dec. 31, 2011 - 2,000 (57,000) (277,000) 220,000

OCIGENERAL JOURNAL ENTRIES MEMO RECORD

($57,000)

January 1, 2011 Plan assets $ 200,000 Projected benefit obligation $ 250,000 Plan Asset (Liability) $ (50,000)

78

Pension ProjectedPension Gain / Asset / Benefit Plan

Items Expense Cash PSC Loss Liability Obligation AssetsBal. Jan. 1, 2011 (50,000) (250,000) 200,000 Service costs 16,000 (16,000) Interest 25,000 (25,000) Return on assets (18,000) 18,000 Unexpected loss (2,000) 2,000 Contributions (16,000) 16,000 Benefits paid 14,000 (14,000) Journal entry 21,000 (16,000) 2,000 (7,000) AOCI - 12/31/10 - Dec. 31, 2011 - 2,000 (57,000) (277,000) 220,000

OCIGENERAL JOURNAL ENTRIES MEMO RECORD

2011 Annual service cost $16,000 Actual return on plan assets 18,000 Expected return on plan assets* 20,000 Annual funding (contributions) 16,000 Benefits paid 14,000

($57,000)

Expected Return = $200,000 × 10%

14

79

Pension ProjectedPension Gain / Asset / Benefit Plan

Items Expense Cash PSC Loss Liability Obligation AssetsBal. Jan. 1, 2011 (50,000) (250,000) 200,000 Service costs 16,000 (16,000) Interest 25,000 (25,000) Return on assets (18,000) 18,000 Unexpected loss (2,000) 2,000 Contributions (16,000) 16,000 Benefits paid 14,000 (14,000) Journal entry 21,000 (16,000) 2,000 (7,000) AOCI - 12/31/10 - Dec. 31, 2011 - 2,000 (57,000) (277,000) 220,000

OCIGENERAL JOURNAL ENTRIES MEMO RECORD

2011 Annual service cost $16,000 Actual return on plan assets 18,000 Expected return on plan assets* 20,000 Annual funding (contributions) 16,000 Benefits paid 14,000

Use expected return on plan assets to calc pension expense. Difference between expected return and actual return

plugged to unexpected gain/loss.

($57,000) 80

Pension ProjectedPension Gain / Asset / Benefit Plan

Items Expense Cash PSC Loss Liability Obligation AssetsBal. Jan. 1, 2011 (50,000) (250,000) 200,000 Service costs 16,000 (16,000) Interest 25,000 (25,000) Return on assets (18,000) 18,000 Unexpected loss (2,000) 2,000 Contributions (16,000) 16,000 Benefits paid 14,000 (14,000) Journal entry 21,000 (16,000) 2,000 (7,000) AOCI - 12/31/10 - Dec. 31, 2011 - 2,000 (57,000) (277,000) 220,000

OCIGENERAL JOURNAL ENTRIES MEMO RECORD

($57,000)

Description Debit Credit Pension expense 21,000 OCI – Gain (loss) 2,000 Cash 16,000 Pension asset / liability 7,000 AJE: Record pension expense, cash paid, change in pension asset/liab.

Plug

2012 Prior service cost (amended, 1/1/12) 160,000 Annual service cost $19,000 Actual return on plan assets 22,000 Expected return on plan assets* 22,000 Annual funding (contributions) 40,000 Benefits paid 16,400 Amortization of prior service cost 54,400

Pension ProjectedPension Gain / Asset Benefit Plan

Items Expense Cash PSC Loss Liability Obligation AssetsBal. Jan. 1, 2012 2,000 (57,000) (277,000) 220,000 Prior service costs 160,000 (160,000) Adj Bal., 1/1/12 (437,000) 220,000 Service costs 19,000 (19,000) Interest 43,700 (43,700) Return on assets (22,000) 22,000 Amort. of PSC 54,400 (54,400) Contributions (40,000) 40,000 Benefits paid 16,400 (16,400) Journal entry 95,100 (40,000) 105,600 (160,700) AOCI - 12/31/11 2,000 Dec. 31, 2012 105,600 2,000 (217,700) (483,300) 265,600

GENERAL JOURNAL ENTRIESOCI

MEMO RECORDPension Projected

Pension Gain / Asset Benefit PlanItems Expense Cash PSC Loss Liability Obligation Assets

Bal. Jan. 1, 2012 2,000 (57,000) (277,000) 220,000 Prior service costs 160,000 (160,000) Adj Bal., 1/1/12 (437,000) 220,000 Service costs 19,000 (19,000) Interest 43,700 (43,700) Return on assets (22,000) 22,000 Amort. of PSC 54,400 (54,400) Contributions (40,000) 40,000 Benefits paid 16,400 (16,400) Journal entry 95,100 (40,000) 105,600 (160,700) AOCI - 12/31/11 2,000 Dec. 31, 2012 105,600 2,000 (217,700) (483,300) 265,600

GENERAL JOURNAL ENTRIESOCI

MEMO RECORD

Description Debit Credit Pension expense 95,100 OCI – Prior service cost 105,600 Cash 40,000 Pension asset / liability 160,700 AJE: Record pension expense, cash paid, change in pension asset/liab.

Plug

Pension ProjectedPension Gain / Asset / Benefit Plan

Items Expense Cash PSC Loss Liability Obligation AssetsBal. Dec. 31, 2012 105,600 2,000 (217,700) (483,300) 265,600 Service costs 26,000 (26,000) Interest 48,330 (48,330) Return on assets (24,000) 24,000 Unexpected loss (2,560) 2,560 Amort. of PSC 41,600 (41,600) Contributions (48,000) 48,000 Benefits paid 21,000 (21,000) Liability gain (16,630) 16,630 Journal entry 89,370 (48,000) (41,600) (14,070) 14,300 AOCI - 12/31/12 105,600 2,000 Dec. 31, 2013 64,000 (12,070) (203,400) (520,000) 316,600

GENERAL JOURNAL ENTRIESOCI

MEMO RECORD

2013 Annual service cost $26,000 Actual return on plan assets 24,000 Expected return on plan assets* 26,560 Annual funding (contributions) 48,000 Benefits paid 21,000 Amortization of prior service cost 41,600 Change in PBO actuarial assumptions; end balance 12/31/2013 520,000

Pension ProjectedPension Gain / Asset / Benefit Plan

Items Expense Cash PSC Loss Liability Obligation AssetsBal. Dec. 31, 2012 105,600 2,000 (217,700) (483,300) 265,600 Service costs 26,000 (26,000) Interest 48,330 (48,330) Return on assets (24,000) 24,000 Unexpected loss (2,560) 2,560 Amort. of PSC 41,600 (41,600) Contributions (48,000) 48,000 Benefits paid 21,000 (21,000) Liability gain (16,630) 16,630 Journal entry 89,370 (48,000) (41,600) (14,070) 14,300 AOCI - 12/31/12 105,600 2,000 Dec. 31, 2013 64,000 (12,070) (203,400) (520,000) 316,600

GENERAL JOURNAL ENTRIESOCI

MEMO RECORD

2013 Annual service cost $26,000 Actual return on plan assets 24,000 Expected return on plan assets* 26,560 Annual funding (contributions) 48,000 Benefits paid 21,000 Amortization of prior service cost 41,600 Change in PBO actuarial assumptions; end balance 12/31/2013 520,000

Change in actuarial assumptions of PBO as of Dec 31, 2013 creates new ending balance. Plug OCI gain (loss) to balance.

15

Gains and Losses

§ Record in net gain or loss account § Difference between expected return and

actual return on plan assets § Gains (Losses) from changes in Projected

Benefit Obligation (PBO) § Amortize amount in excess of corridor

to pension expense over average remaining service period of active employees expected to receive benefits

85

Corridor Amortization

§ FASB invented corridor approach for amortizing accumulated net gain or loss balance when it gets too large

§ Amortize accumulated net gain or loss greater than 10% of larger of beginning balance of § Projected benefit obligation § Fair value of plan assets

86

87

Calculation for Asset Gain or Loss

88

Gains and Losses

89

January 1, 2012 Plan assets $ 3,300,000 Projected benefit obligation $ 3,100,000 AOCI, Pension Loss $ 465,000 Remaining employee service life 7.5 years

Gains and Losses

§ Corridor amortization of loss

90

AmortizationProjected benefit obligation (3,100,000)$ Plan assets 3,300,000 3,300,000$ Corridor percentage 10%Corridor amount 330,000 Accumulated loss 465,000 Excess loss subject to amortization 135,000 Average remaining service 7.5 Amortized to pension expense 18,000$

16

Five Components of Pension Expense

91

Service Costs + 1

= Total pension expense

Interest on Liability + 2 Actual Return on Plan Assets ± 3 Amortization of Prior Service Costs + 4 Gain or Loss ± 5

92

93 94

Learning Objective 9

§ Describe requirements for reporting pension plans in financial statements

95

Financial Statements

96

Financial Statements Income Statement Pension Expense Balance Sheet Net Funded Status (asset/liability) OCI / AOCI Gain (Loss) OCI / AOCI Prior Service Cost

17

Pension Plans Notes

§ Calculation of Pension Expense § Reconcile PBO, fair value plan assets § Rates and estimates

§ Settlement rate § Expected return on plan assets § Increase in compensation over time

97

Pension Plans Notes

§ Table allocating pension plan assets § Equity securities § Debt securities § Real estate § Other assets

98

Pension Plans Notes

§ Expected benefit payments for each of next five fiscal years

§ Estimate of expected contributions to plan during next year

99

Pension Plans Notes

§ Nature and amount of changes in plan assets and benefit obligations recognized in net income and in other comprehensive income of each period

§ Accumulated amount of changes in plan assets and benefit obligations that have been recognized in OCI

100

Pension Plans Notes

§ Estimated net actuarial gains (losses) and prior service costs and credits that will be amortized from AOCI to net income over next fiscal year

101 102

18

103 104

Aggregation of Pension Plans

§ More than one pension plan § Overfunded plans (asset balances)

§ Combined, listed as one pension asset § Underfunded plans (liability balances)

§ Combined, listed as one pension liability

105 106

End of Chapter

107

Appendix 20A

§ Accounting for postretirement benefits § LO 10: Identify differences between

pensions and postretirement healthcare benefits

§ LO 11: Contrast accounting for pensions to accounting for other postretirement benefits

108

19

Postretirement Benefits

§ In December 1990, FASB issued rules on “Employers’ Accounting for Postretirement Benefits Other Than Pensions”

§ Rules cover for healthcare and other “welfare benefits” provided to retirees, their spouses, dependents, and beneficiaries

109

Postretirement Benefits

§ Other welfare benefits include § Life insurance offered outside a pension

plan § Medical, dental, and eye care § Legal and tax services § Tuition assistance § Day care § Housing assistance

110

Postretirement Benefits

§ Differences between pension benefits and healthcare benefits

111

Postretirement Benefits

§ Measuring future payments for healthcare benefit plans more difficult than for pension plans § Many postretirement plans do not set a

limit on healthcare benefits § Levels of healthcare benefit use and

healthcare costs are difficult to predict § Increased longevity, unexpected illnesses,

new medical technologies cause changes in healthcare utilization

112

Attribution Period

§ Period of time over which postretirement benefit cost accrue

113

Obligations Under Postretirement Benefits

§ Expected postretirement benefit obligation (EPBO) is actuarial present value as of a particular date of all benefits a company expects to pay after retirement to employees and their dependents

114

20

Postretirement Expense

§ Service Cost § Interest Cost § Actual Return on Plan Assets § Amortization of Prior Service Costs § Gains and Losses

115

Work Sheet: Case 4

§ January 1, 2012 § Adopt healthcare benefit plan § Plan assets fair value, $0 § Accumulated postretirement benefit

obligation (APBO), $0

116

Work Sheet: Case 4

§ During 2012 § Service cost, $54,000 § Funding contributions, $38,000 § Benefit payments, $28,000 § Actual and expected returns on plan

assets, $0 § Interest cost on APBO, $0 § No prior service cost

117

Work Sheet: Case 4

118

Description Debit Credit Postretirement expense 54,000 Cash 38,000 Postretirement asset / liability 16,000 AJE: Record postretirement exp, cash paid, change in asset/liability

Plug

Gains and Losses

§ Gains and losses represent changes in APBO or value of plan assets

§ Gains and losses are recorded in OCI (other comprehensive income) § Corridor Approach § Amortization Methods

119

Work Sheet: Case 5

§ January 1, 2013 § Accumulated postretirement benefit

obligation (APBO), $26,000 § Plan assets fair value, $10,000 § Postretirement liability, $16,000

120

21

Work Sheet: Case 5

§ During 2013 § Discount rate, 8% § Average remaining service, 25 years

121

2013 Service cost 26,000 Actual return on plan assets 600 Expected return on plan assets 800 Funding contributions 18,000 Benefit payments 5,000 Increase in APBO due to change in actuarial assumptions 60,000

Work Sheet: Case 5 2013

Service cost 26,000 Actual return on plan assets 600 Expected return on plan assets 800

Work Sheet: Case 5 2013

Funding contributions 18,000 Benefit payments 5,000 Increase in APBO due to change in actuarial assumptions 60,000

Description Debit Credit Postretirement expense 27,280 OCI – Gain (Loss) 60,200 Cash 18,000 Postretirement asset / liability 69,480 AJE: Record postretirement exp, cash paid, change in asset/liability

Plug

Amortization of Gains and Losses in 2014

125

JE Needed 126

22

127

Learning Objective 3

§ Explain alternative measures for valuing pension obligation

128

129

Description Debit Credit Cash 3,960,000 Bonds payable 4,000,000 Issued bonds at 99: $4,000,000 × 99% = $3,960,000

Description Debit Credit Fair value adjustment 150,000 Unrealized holding gain (loss) [OCI] 150,000 AJE: Impairment loss, write down value of asset, reduce net income

Plug

Description Debit Credit Payroll tax expense 5,000 SUTA taxes payable 1,500

130

Liability – stock appreciation plan

15,000 20,000

0

55,000 50,000

Year 1

Year 2

Year 3

Payout

Debt investments

108,111

106,732

676

703

Purchase

Period 1

Period 2

131

Calculation of equity reclassified Shares distributed 300,000 Par value $10 Equity reclassified 3,000,000

Related Documents