Pensions and Postretirement Benefits Revsine/Collins/Johnson/Mittelstaedt/Soffer: Chapter 14 Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Pensions and Postretirement

Benefits

Revsine/Collins/Johnson/Mittelstaedt/Soffer: Chapter 14

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education

Learning objectives

1. The rights and obligations in defined contribution and defined benefit plans.

2. The features of pension plan arrangements.

3. The components of pension expense and their relation to pension assets and pension liabilities.

4. How GAAP smooths the volatility inherent in pension estimates and forecasts.

5. The determinants of pension funding.

14-2

Learning objectives:Concluded

6. How to analyze and use the retirement benefit footnote disclosures.

7. Other postretirement benefits plan concepts and financial reporting rules.

8. What research tells us about the usefulness of the detailed pension and other postretirement benefits disclosures.

9. The key differences in defined benefit plan reporting among current U.S. GAAP and current IFRS requirements

14-3

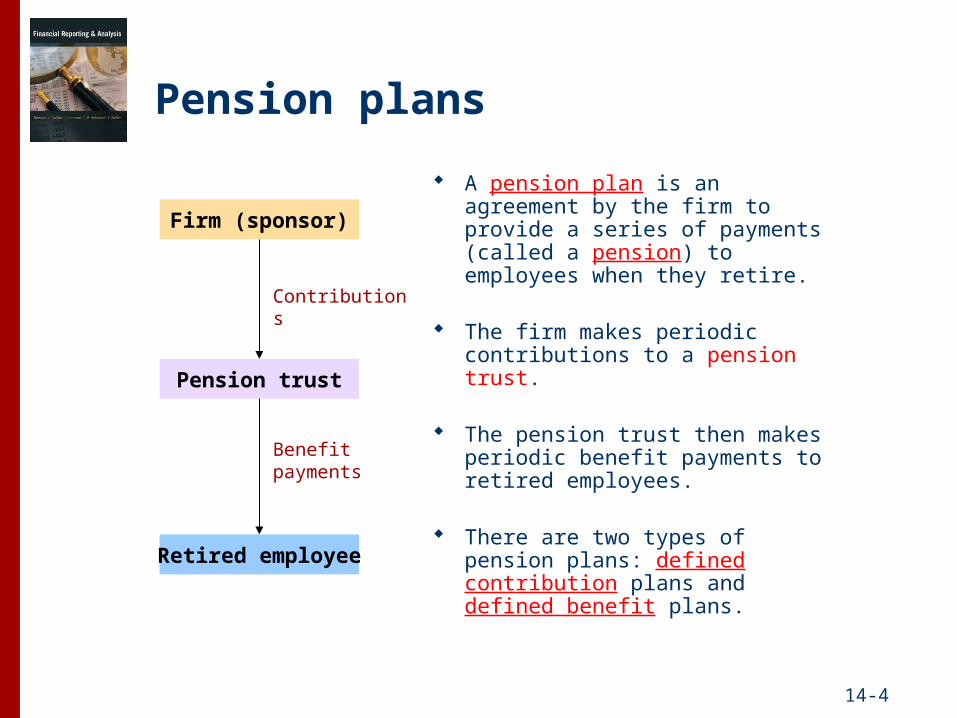

Pension plans

A pension plan is an agreement by the firm to provide a series of payments (called a pension) to employees when they retire.

The firm makes periodic contributions to a pension trust.

The pension trust then makes periodic benefit payments to retired employees.

There are two types of pension plans: defined contribution plans and defined benefit plans.

Firm (sponsor)

Pension trust

Retired employee

Contributions

Benefit payments

14-4

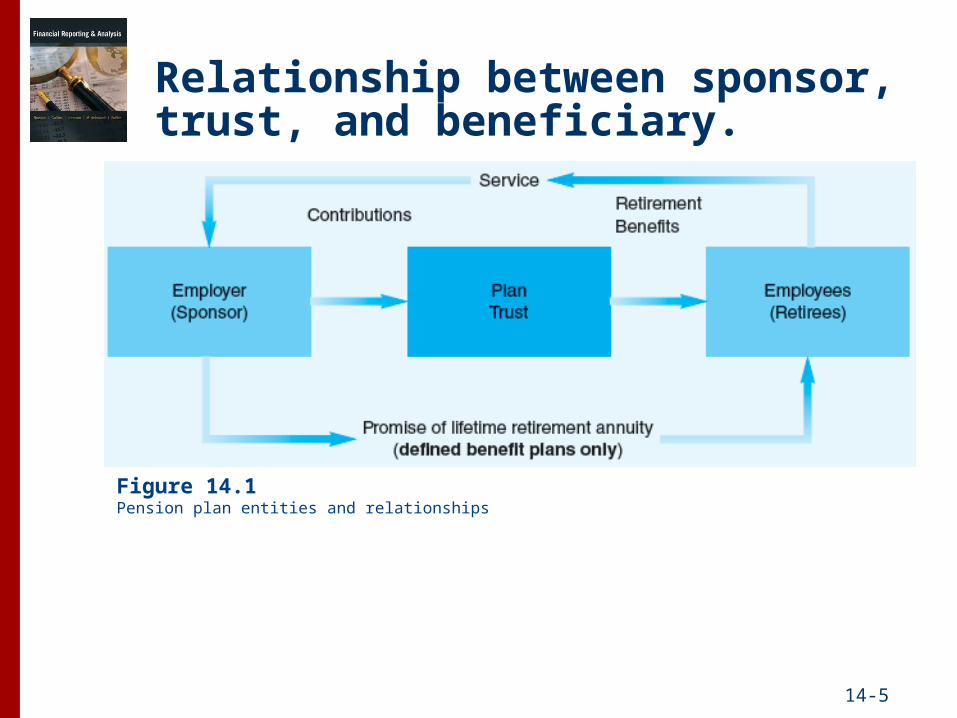

Relationship between sponsor, trust, and beneficiary.

Figure 14.1Pension plan entities and relationships

14-5

Pension plans:Defined contribution and defined benefit plans

Figure 14.2Assets by plan type

14-6

Defined benefit pension plans:Accounting complications

The plan specifies the benefit formula but not the benefit amount.

To determine the financial statement effects, the following factors must be considered:

1. The proportion of the workforce that will remain with the firm long enough to qualify for benefits under the plan (called vesting).

2. The rate at which employee salaries will rise until retirement.

3. The anticipated life expectancy of employees after retirement.

4. The discount rate used to reflect the present value of future benefits earned by employees in the current period.

5. What to do when actual experience differs from expectations.

14-7

Defined benefit pension plans:Five components of pension expense

Service cost (+)

Interest cost (+)

Expected returnon pension assets (-)

Recognized gainsor losses (- or +)

Recognized priorservice cost (- or +)

The increase in the discounted present value of the pension benefits due to an additional year’s employment.

Measures the growth in the pension liability that arises from the passage of time.

Dollar return management believes will be earned on pension investments.

Smoothing device that adjusts for the difference between the expected and actual return on pension assets.

Smoothing device that adjusts for the costs of retroactive changes in plan benefits.

14-8

Defined benefit pension plans:Component 1—Service cost

Service cost is the increase in the discounted present value of the pension benefits ultimately payable that is attributable to an additional year’s employment.

14-9

Defined benefit pension plans:Component 1—Service cost

14-10

Defined benefit pension plans:Component 2—Interest cost

The interest cost of $1,717 is computed by taking the PBO at the

beginning of the period (here $24,526) and multiplying it by the

discount rate (here 7%)

14-11

Defined benefit pension plans: Component 3—Expected return on plan assets

The 2015 expected return of $1,717 is computed by multiplying the beginning plan assets of $24,526 by

the expected long-term rate of return assumption of 7%. For this simplified example, we assume that the actual return equals

the expected return

14-12

Defined benefit pension plans:Relaxing the perfect certainty assumption

The previous example showed perfect certainty. Unforeseen pension events arise, examples include:

Higher or lower than anticipated employee turnover.

Higher or lower employee mortality before retirement.

Actual return on plan assets differs from the expected return.

Companies retroactively alter the level of benefits promised under the plan.

14-13

The Real World: Uncertainty Introduces Gains and Losses

GAAP requires that the same interest rate be used for computing both the service cost and the interest cost components of pensions expense. However, companies are free to choose some other rate for computing the expected rate of return on pension plan assets, and most do.

Uncertainty not only complicates the measurement of service cost and interest costs but also means that actual outcomes will likely differ from expectations.

14-14

The Real World: Uncertainty Introduces Gains and Losses

Figure 14.3Pension discount rate and expected long-term rate of return on plan assets 2005-2012

14-15

If gains and losses do not offset one another over time, the cumulative off-balance sheet deferred amounts will grow excessively large.

The role of Component 4 is to gradually reduce the cumulative deferred amounts.

Defined benefit pension plans:How Component 4 is measured

Cumulativedeferred net

gains or losses

• Actual versus expected return on plan assets

• Actuarial assumptions versus actual experience

• Changes in assumptions (e.g., discount rate)

14-16

Defined benefit pension plans:Computing Component 4—Step 1

On January 1, 2014, Dore Corporation has ($1,600,000) in AOCI – actuarial (gain) loss. The MRV of pension plan assets on that date is $10,000,000, and the PBO is $8,500,000. The estimated average remaining service period of active employees is 15 years.

14-17

Defined benefit pension plans:Computing Component 4—Step 2

On January 1, 2014, Dore Corporation has ($1,600,000) in AOCI – actuarial (gain) loss. The MRV of pension plan assets on that date is $10,000,000, and the PBO is $8,500,000. The estimated average remaining service period of active employees is 15 years.

14-18

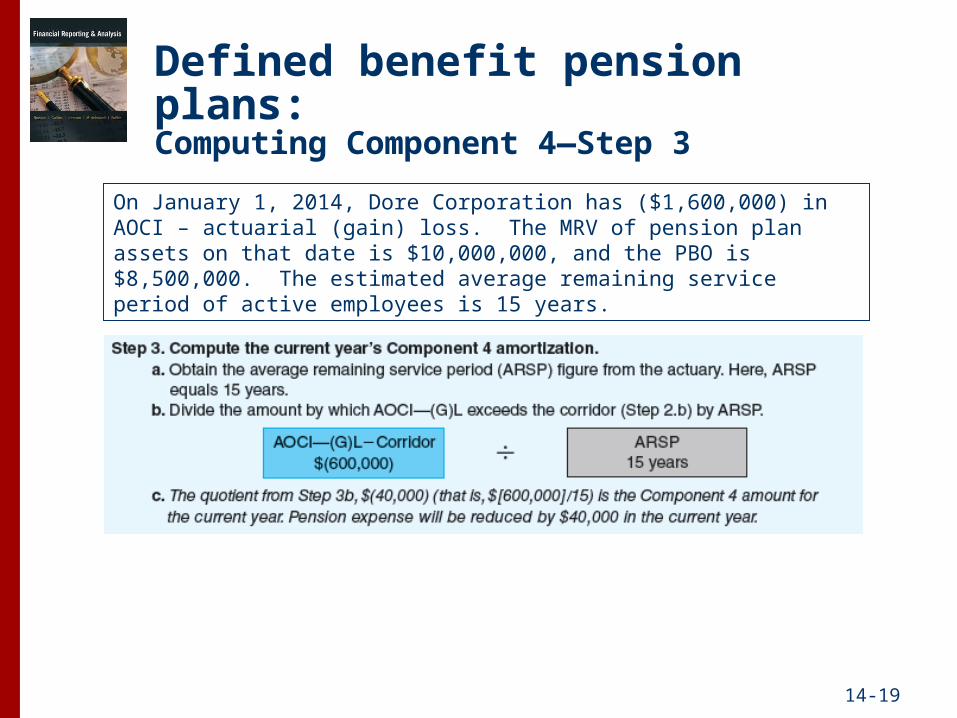

Defined benefit pension plans:Computing Component 4—Step 3

On January 1, 2014, Dore Corporation has ($1,600,000) in AOCI – actuarial (gain) loss. The MRV of pension plan assets on that date is $10,000,000, and the PBO is $8,500,000. The estimated average remaining service period of active employees is 15 years.

14-19

Defined benefit pension plans:Component 5—Prior service cost

Pension plans are frequently amended to provide increased benefits to employees.

When benefits are retroactively enhanced, it means prior pension expense was too low.

Similar to net actuarial losses, new prior service costs increase balance sheet liabilities and decrease OCI and AOCI.

14-20

Defined benefit pension plans:Determinants of Pension Funding

Funding decisions are influenced by income tax laws, protective pension legislation, the availability of cash, and other incentives.

Income tax laws

ERISA Firms with high marginal tax rates tend to

overfund their pension plans.

Competingcash needs

Firms with less stringent capital constraints and larger union membership tend to have higher funding ratios.

Contracting andpolitical cost incentives

Firms with more “precarious” debt/equity ratios tend to have lower funding ratios.

14-21

Case Study of Pension Recognition and Disclosure: General Electric

14-22

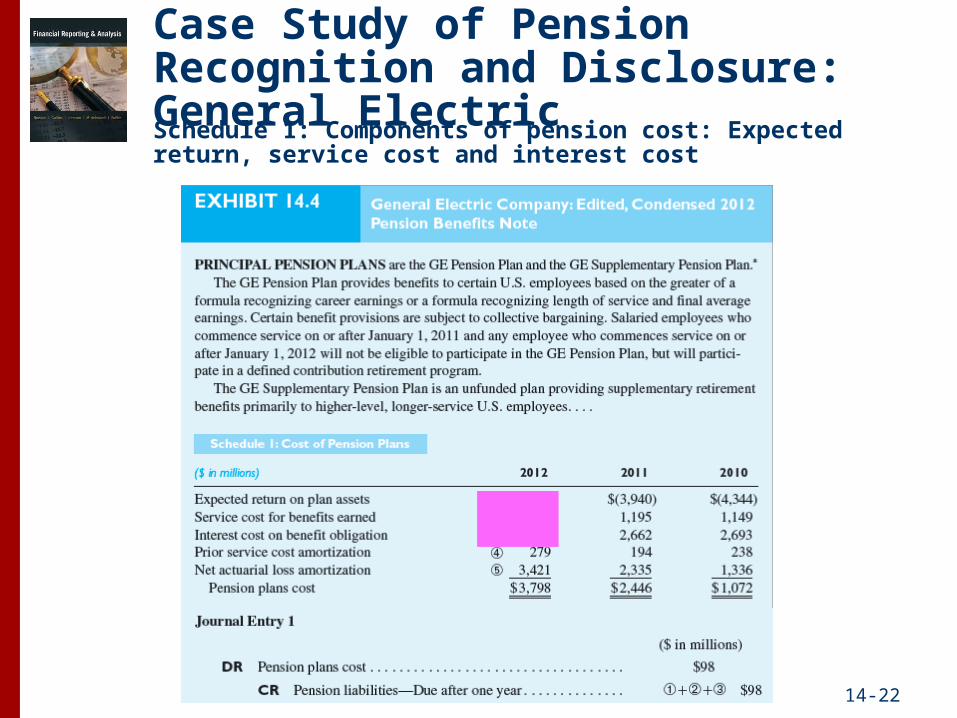

Schedule 1: Components of pension cost: Expected return, service cost and interest cost

Case Study of Pension Recognition and Disclosure: General Electric

14-23

Schedule 1: Components of pension cost: Expected return, service cost and interest cost

Case Study of Pension Recognition and Disclosure: General Electric

14-24

Schedules 2 and 3: Actuarial and accounting assumptions and the accumulated benefit obligation (ABO)

Case Study of Pension Recognition and Disclosure: General Electric

14-25

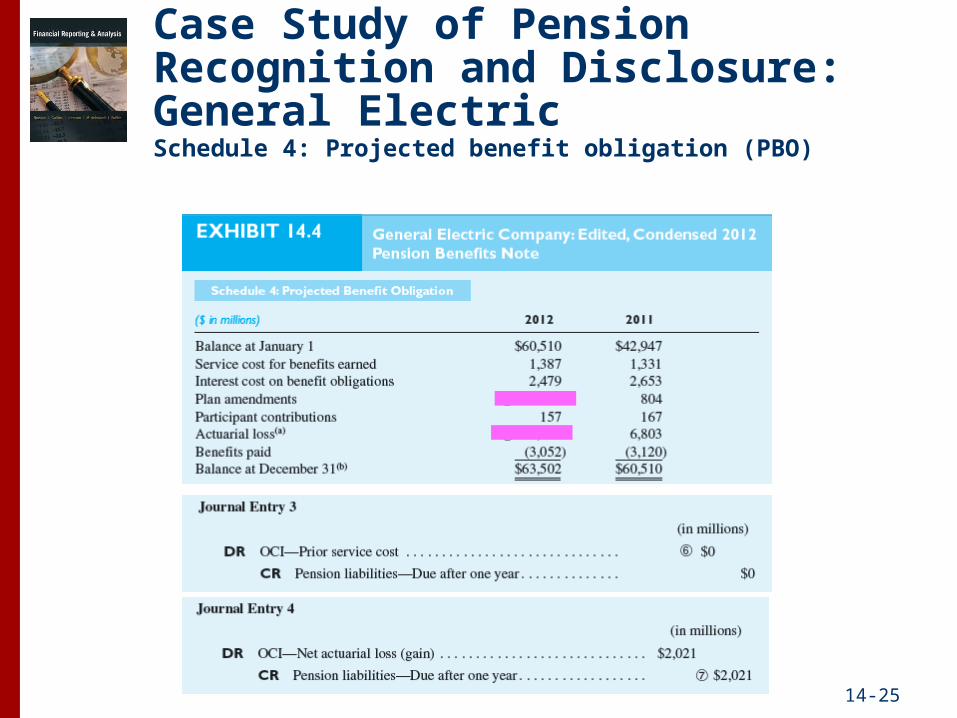

Schedule 4: Projected benefit obligation (PBO)

Case Study of Pension Recognition and Disclosure: General Electric

14-26

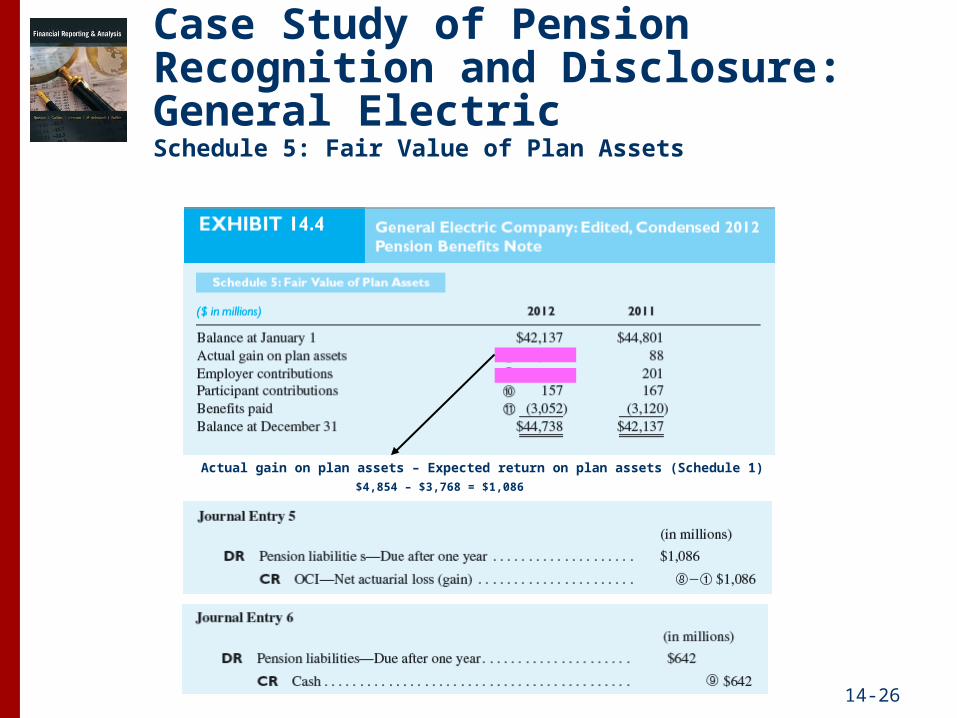

Schedule 5: Fair Value of Plan Assets

Actual gain on plan assets – Expected return on plan assets (Schedule 1) $4,854 – $3,768 = $1,086

Case Study of Pension Recognition and Disclosure: General Electric

14-27

Schedule 6 : Pension Asset (Liability)

$159 - $148 = $11

Case Study of Pension Recognition and Disclosure: General Electric

14-28

Pension recognition and disclosure:Funded status disclosure—Plan assets

Figure 14.6Causes of increases and decreases in plan assets

14-29

Pension recognition and disclosure: Funded status disclosure—PBO

Figure 14.7Causes of increases and decreases in PBO

14-30

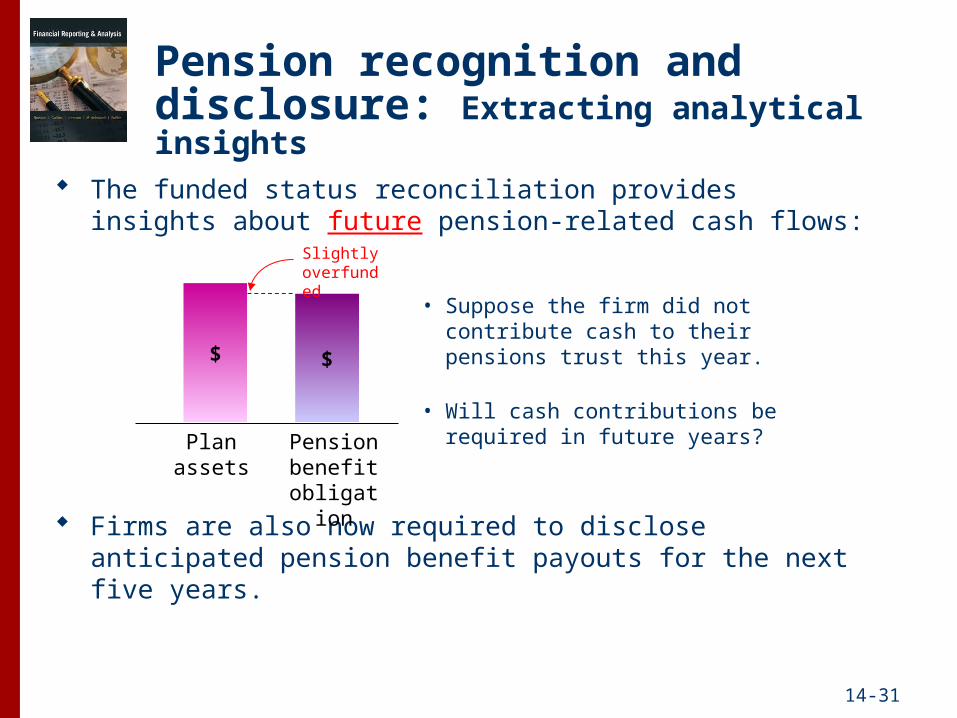

Pension recognition and disclosure: Extracting analytical insights

The funded status reconciliation provides insights about future pension-related cash flows:

Firms are also now required to disclose anticipated pension benefit payouts for the next five years.

$

Plan assets

Pension benefit

obligation

$

Slightly overfunded

• Suppose the firm did not contribute cash to their pensions trust this year.

• Will cash contributions be required in future years?

14-31

Defined benefit plans:Cash-balance plans

Many U.S. companies are replacing existing pension plans with a new cash-balance plan.

Cash balance plans are attractive to employers, but they are also controversial.

Employer

Employee

Trustee

Contributes fixed amount per year, say 5% of salary

Pays annuity benefit to employee

Interest earned at T-bond rate

14-32

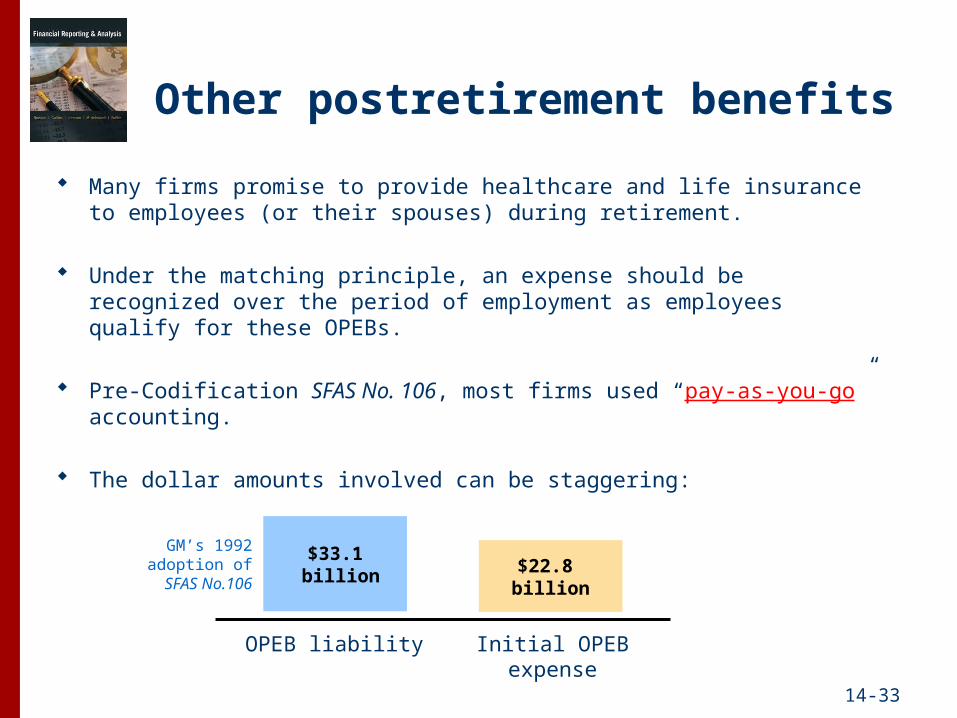

Other postretirement benefits

Many firms promise to provide healthcare and life insurance to employees (or their spouses) during retirement.

Under the matching principle, an expense should be recognized over the period of employment as employees qualify for these OPEBs.

Pre-Codification SFAS No. 106, most firms used “pay-as-you-go” accounting.

The dollar amounts involved can be staggering:

$22.8 billion

$33.1 billion

OPEB liability Initial OPEB expense

GM’s 1992 adoption of

SFAS No.106

14-33

Other postretirement benefits:General Electric footnote—part 1

14-34

Analytical Insights:Assessing OPEB Liability

Similar to pensions, the OPEB liability is riskier than many traditional forms of debt. Risk measures are defined as follows:

14-35

Evaluation of Pension and Postretirement Benefit Financial Reporting

Pension asset and liability measures in the notes are more closely associated with stock prices than are the measures recognized on the balance sheet.

Both note liabilities (ABO for pensions and APBO for OPEBS) are negatively correlated with stock prices.

Investors price the APBO as though it is measured with less reliability.

14-36

Global Vantage PointComparison of IFRS and GAAP Retirement Benefit Accounting

Difference GAAP IFRSActuarial Gains and Losses Follows FASB ASC Subtopic 715-30 IAS 19 requires that the discount

rate be used to compute the expected return on plan assets.

Prior Service Costs Recognize new prior services costs as part of OCI and recycle them into pension expense over the shorter of the average remaining work life or the period covered under the collective bargaining agreement

Called past service costs under IFRS. Under IAS – past service cost is recognized immediately

Balance sheet pension asset Service cost is part of operating activities, the finance component is part of finance costs within profit and loss, and actuarial gains and losses is part of OCI

14-37

Summary

In pension plan contracts, employees exchange current service for payments to be received during retirement.

Defined contribution pension plans specify amounts to be invested for the employee during the employee’s career, and the employee’s pension will be based on the value of those investments at retirement.

In the U.S., most new pension plans are defined contribution plans.

The accounting for defined contribution plans is straightforward. Defined benefit plans specify amounts to be received during retirement, thereby complicating the underlying economics of the exchange and the accounting.

14-38

Summary continued

Under ASC Topic 715, pension expense for defined benefit plans consists of service cost, interest cost, expected return on plan assets, and two other “smoothing” components.

The two smoothing mechanisms avoid year-to-year volatility in pension expense but make pension accounting exceedingly complex, because many pension related items are in AOCI.

Under pre-Codification SFAS 87, the balance sheet asset (liability) on the balance sheet differed from the actual funded status of the plan. Current GAAP, requires that the balance sheet asset (liability) equal the funded status of the plan.

14-39

Summary continued

Employer funding of defined benefit pension plans is influenced by tax law, labor law, union membership, and the employer’s financial needs.

The reporting rules for other postretirement benefit plans (OPEB) closely parallel pension accounting rules.

GAAP requires information about the expected future cash flows, future amortization amounts, and major classes of investments so that investors can make cash flow projections, assess risk, and evaluate return assumptions.

Academic research suggests that stock prices reflect pension and OPEB disclosures, but their impact may not be fully valued.

14-40

Summary concluded

Statement readers should be alert for these warning signals of earnings management:

1. A significant disagreement between any of the various pension and OPEB rates selected by a firm and the rates chosen by other firms in the industry.

2. A very large difference between the chosen expected rate of return on plan assets and the discount rate used.

3. An increase in the year-to-year expected rate of return on plan assets that seems unrelated to changes in market conditions.

4. A decrease in the assumed rate of increase in future compensation levels that cannot be explained by changing industry or labor market forces.

5. Rate of return assumptions that are inconsistent with prior investment experience or mix of equity and debt investments.

6. IAS 19 offers guidance that is markedly different from U.S. GAAP

14-41

Related Documents