Published in ABA Tax Times, January 2022. © 2022 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868. An Online Publication of the ABA Tax Section Fall • January 2022 • Vol. 41 No. 1 CONTENTS FROM THE CHAIR Fire Is the Test of Gold ............................................. 1 PEOPLE IN TAX Interview with Jacob Puhl ........................................ 6 PRACTICE POINT A Primer on Charitable Trusts (Part II)........................ 9 AT COURT The IRS’s Procedural Battles in Micro-Captive Litigation.............................................................. 15 PRO BONO MATTERS A Sit-Down with Andrew VanSingel ......................... 24 YOUNG LAWYERS CORNER Revisiting the 100-Year-Old Debate on the Preferential Treatment of Capital Gains ..................................... 29 The Build Back Better Energy Tax Provisions ............ 37 IN REMEMBRANCE Remembering Doug Kahn ...................................... 40 SPECIAL FEATURES Tax Section Creates Fellowship and Fund to Advance Diversity and Inclusion........................................... 45 Tax Section Highlights from National Hispanic Heritage Month ................................................................. 46 TAX BITS Unallowable ......................................................... 49 IN THE STACKS Tax Section Publishes The Supreme Court, Federal and State Taxation, and the Constitution ....................... 50 SECTION NEWS & ANNOUNCEMENTS ................. 52 • Midyear Tax Meeting Goes Virtual, Features William Gale and Loretta Collins Argrett • End of Tax Connect and Next Steps for Committee Communication • Government Submissions Boxscore • Accepting Nominations for the 2022 Janet Spragens Pro Bono Award • Call for Applications: Diversity and Inclusion Scholarships to Virtual 2022 Midyear Tax Meeting • Get Social • Each One, Reach One • Virtual 2021 Fall Tax Meeting Materials Now Available • The Tax Lawyer—Fall 2021 Issue Now Available • The Practical Tax Lawyer—November 2021 Issue Now Available • Support the Section’s Public Service Efforts with a Contribution to the TAPS Endowment • Get Involved in ATT SECTION EVENTS & PROMOTIONS Section Meeting & CLE Calendar ............................. 59 Section CLE Products ............................................ 59 Sponsorship Opportunities ..................................... 60 SPONSORSHIP ACKNOWLEDGEMENTS Virtual 2021 Fall Tax Meeting................................. 61 Virtual 32nd Annual Philadelphia Tax Conference ..... 62 Thomson Reuters | Publishing Sponsor ................... 63

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Published in ABA Tax Times, January 2022. © 2022 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

An Online Publication of the ABA Tax Section Fall • January 2022 • Vol. 41 No. 1

CONTENTS

FROM THE CHAIRFire Is the Test of Gold ............................................. 1

PEOPLE IN TAXInterview with Jacob Puhl ........................................ 6

PRACTICE POINTA Primer on Charitable Trusts (Part II) ........................ 9

AT COURTThe IRS’s Procedural Battles in Micro-Captive Litigation .............................................................. 15

PRO BONO MATTERSA Sit-Down with Andrew VanSingel ......................... 24

YOUNG LAWYERS CORNERRevisiting the 100-Year-Old Debate on the Preferential Treatment of Capital Gains ..................................... 29

The Build Back Better Energy Tax Provisions ............ 37

IN REMEMBRANCERemembering Doug Kahn ...................................... 40

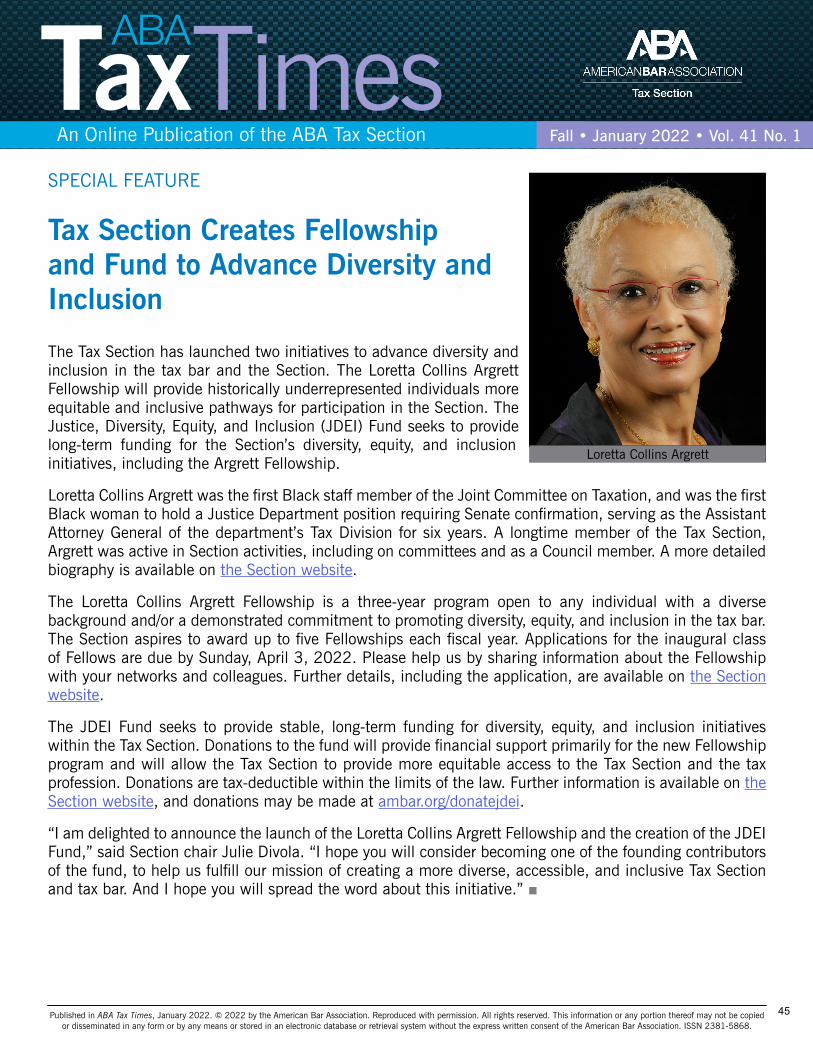

SPECIAL FEATURESTax Section Creates Fellowship and Fund to Advance Diversity and Inclusion ........................................... 45

Tax Section Highlights from National Hispanic Heritage Month ................................................................. 46

TAX BITSUnallowable ......................................................... 49

IN THE STACKSTax Section Publishes The Supreme Court, Federal and State Taxation, and the Constitution ....................... 50

SECTION NEWS & ANNOUNCEMENTS ................. 52

• Midyear Tax Meeting Goes Virtual, Features William Gale and Loretta Collins Argrett

• End of Tax Connect and Next Steps for Committee Communication

• Government Submissions Boxscore

• Accepting Nominations for the 2022 Janet Spragens Pro Bono Award

• Call for Applications: Diversity and Inclusion Scholarships to Virtual 2022 Midyear Tax Meeting

• Get Social

• Each One, Reach One

• Virtual 2021 Fall Tax Meeting Materials Now Available

• The Tax Lawyer—Fall 2021 Issue Now Available

• The Practical Tax Lawyer—November 2021 Issue Now Available

• Support the Section’s Public Service Efforts with a Contribution to the TAPS Endowment

• Get Involved in ATT

SECTION EVENTS & PROMOTIONSSection Meeting & CLE Calendar ............................. 59

Section CLE Products ............................................ 59

Sponsorship Opportunities ..................................... 60

SPONSORSHIP ACKNOWLEDGEMENTSVirtual 2021 Fall Tax Meeting ................................. 61

Virtual 32nd Annual Philadelphia Tax Conference ..... 62

Thomson Reuters | Publishing Sponsor ................... 63

Published in ABA Tax Times, January 2022. © 2022 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

ABA TAX TIMESFall • January 2022 • Vol. 41 No. 1

EDITORIAL BOARD

COUNCIL DIRECTORRoberta Mann

SUPERVISING EDITORLinda M. Beale

INTERVIEW EDITORSTameka E. LesterJeremiah Coder

PODCAST EDITORJames Creech

PRO BONO MATTERS EDITORSAndrew RobersonGina Ahn

AT COURT EDITORT. Keith Fogg

PRODUCTION EDITORSGregory Peacock Todd Reitzel

ASSOCIATE EDITORSJaye CalhounAndy HowlettGuinevere MooreDavid PrattDaniel M. ReachRobert S. SteinbergRobert W. Wood

HYPERTEXT CITATIONS & LINKS

As a service to our readers, ATT authors are encouraged to include hyperlinks to publicly available content within their articles. In addition, certain articles may also contain hypertext citation linking to Westlaw created with Drafting Assistant from Thomson Reuters. Thomson Reuters Legal is the Publishing Sponsor of the ABA Tax Section, and this software usage is implemented in connection with the Section’s sponsorship and marketing agreements with Thomson Reuters. Neither the ABA nor ABA Sections endorse non-ABA products or services. Check if you have access to Drafting Assistant by contacting your Thomson Reuters representative.

EDITORIAL POLICY

ABA Tax Times (ATT) is published at least four times a year featuring articles covering a wide range of tax topics and areas of tax practice, interviews with diverse tax practitioners, Committee reports, Tax Section comment submissions to the government, and other news and information of professional interest to Tax Section members and other readers.

ATT is presented in digital-only format and is distributed by e-mail to Tax Section members as a benefit of membership. To learn more about joining the ABA and the Tax Section, visit http://www.americanbar.org/groups/taxation/membership.html.

ABA Tax Times welcomes the submission of manuscripts from Tax Section members. ATT does not accept articles that have been published previously or are scheduled for publication elsewhere. Publication decisions will be based on editorial consideration of topical timeliness, legal accuracy, quality of writing, tone, and consistency with ATT’s editorial policy. ATT reserves the right to accept or reject any manuscript and to condition acceptance upon revision to conform to its criteria. Members interested in authoring an article are encouraged to contact Professor Linda M. Beale, ATT Supervising Editor, at [email protected].

ATT articles and reports reflect the views of the individuals or committees that prepare them and do not necessarily represent the position of the Tax Section, the American Bar Association, or the editors of ATT. The articles and other content published in ATT are intended for educational and informational purposes only and are not to be considered legal advice. Readers are responsible for seeking professional advice from their own legal counsel.

Authors of accepted articles must sign a standard ABA copyright release form, which gives the ABA exclusive rights to first publication. Authors retain the rights to republish their articles elsewhere (including on the SSRN network) after their articles appear in ATT, with appropriate citation to ATT.

Further information regarding the submission guidelines, including organization, hyperlinks, and article length, is available here: http://www.americanbar.org/groups/taxation/publications/abataxtimes_home/att_editorial.html.

Published in ABA Tax Times, January 2022. © 2022 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

An Online Publication of the ABA Tax Section Fall • January 2022 • Vol. 41 No. 1

FROM THE CHAIR

Fire Is the Test of Gold1

By Julie Divola, Pillsbury Winthrop Shaw Pittman, LLP, San Francisco, CA

Despite the challenges of the past year putting us through that test of fire, the Tax Section continues to thrive. We have done so thanks to the incredible creativity, hard work, dedication, resilience and teamwork of Section staff, Section leadership and Section members.

Fall Meeting

The Virtual 2021 Fall Meeting offered five days of superior educational programing, along with enhanced social networking opportunities. Thomas Barthold, Chief of Staff of the Joint Committee on Taxation, was our speaker for the plenary session, providing our members with much-needed insight into the workings of the legislative process (including the sometimes-inscrutable workings of budget reconciliation). An engaging selection of committee meetings greeted our members, who also benefited from refinements to the virtual meeting processes developed by the Section staff and our committees. We’re very proud of the result.

The Section is dedicated to getting back to in-person meetings as soon as it’s feasible to do so. Many of us found “our people” through the Tax Section and have missed the sense of community that comes with meeting in person. Even those who are less sentimental have missed the chance encounters and networking opportunities that are difficult to replicate in a virtual setting. However, the Section has also recognized that the virtual platform offers certain advantages, including the ability to reach, and become relevant to, younger and more diverse members as well as established attorneys in smaller practices that may find the time and cost of travel a deterrent to participation. Accordingly, as we shift back to in-person meetings, the Section will be working hard to structure these as hybrid meetings with robust virtual content.

Pro Bono and Public Service

The Tax Section serves as a national leader and innovator in the provision of pro bono legal services. Access to representation for low-income and other vulnerable taxpayers is fundamental to the Section’s mission to support the development of a fair and equitable tax system. With the ever-increasing complexity of tax laws, the significant role tax benefits have played as a lifeline to generally underserved populations during the pandemic, and the scarcity of government resources because of staffing and logistical challenges, pro bono programs are more important than ever. Members have consistently stepped up to the task of providing tax assistance. Filing season is set to begin on January 24, making this the perfect time to volunteer!

1 Martha Graham.

1

Published in ABA Tax Times, January 2022. © 2022 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

ABA TAX TIMESFall • January 2022 • Vol. 41 No. 1

The Section has a variety of programs intended to link tax attorneys with pro bono opportunities that are right for them. Pro bono programs supported by the Section include Assisting Elderly Taxpayers, Adopt-A-Base, Tax Court Calendar Call (representing Pro Se Taxpayers), Low Income Taxpayer Clinics (LITCs), Volunteer Income Tax Assistance (VITA) and Expanded and Advance Child Tax Credit assistance. The Section also provides free educational programming and acts as a vital resource to over 1,000 tax professionals who belong to the Section’s Pro Bono and Tax Clinics Community.

Through its Adopt-A-Base program, the Tax Section partners with the Armed Forces and the IRS to train service members who provide volunteer income tax assistance, such as tax return preparation, to other service members and their families throughout the country. The Adopt-A-Base 2022 filing season is now underway. In connection with this effort, the Section is recruiting volunteers to update information for the Military State Tax Guide for a selected state. This volunteer opportunity does not require any prior experience. The Section would like to receive the updated portions of the Guide by January 18. If you would like to sign up, please complete this very short information form.

Special thanks to Sheri Dillon, our Vice Chair for Pro Bono and Outreach and Meg Newman, the Section’s Chief Counsel, for their exemplary leadership, and thanks to our many members who are passionate in their pursuit of equal access to tax justice for all.

The Tax Section is currently accepting nominations for the 2022 Janet Spragens Pro Bono Award given to an individual or law firm for sustained and outstanding achievements in tax pro bono. Nominations will be accepted through February 15, 2022.

TAPS and Christine A. Brunswick Public Interest Tax Fellows

The Section’s Tax Assistance Public Service (TAPS) endowment fund provides a source of stable, long-term funding for our tax-related public service programs. The TAPS endowment fund primarily supports the Christine A. Brunswick Public Service Fellowship program, which provides two-year fellowships for recent law school graduates to work for non-profit organizations offering tax-related legal assistance to underserved communities. In Autumn 2021, Nirali Patel started as the 2021–2023 Christine A. Brunswick Public Service Fellow, working with the Greater Boston Legal Services on a project focused on misclassified employees. The continuing 2020–2022 Christine A. Brunswick Public Service Fellows are Shailana Dunn-Wall, who works with Legal Aid of Nebraska on a project focused on educating Nebraska residents about the benefits of the Earned Income Tax Credit and Terri Morris, who works with the Community Tax Law Project of Richmond, Virginia, on their Fight Against Financial Abuse project (where Terri provides advocacy and educates and engages local domestic violence survivors on tax issues related to financial abuse).

ABA Giving Day, a fundraising event spearheaded by the ABA Fund for Justice and Education, featured TAPS this year. With the help of a matching program with Tax Section leadership, over $50,000 was raised on ABA Giving Day for TAPS. Thanks to all the Section members who made that possible!

Government Relations

The Section provides leadership in simplifying and improving the tax system through unbiased, thoughtful and timely input into regulatory and legislative processes. Under the dedicated leadership of Kurt Lawson, Vice Chair, Government Relations, and Lisa Zarlenga, Chair of the Committee on Government Submissions, the Section has recently submitted numerous comment letters to the Internal Revenue Service. These have included comments on Voluntary Disclosure Practice and the Streamlined Compliance Procedures, Proposed

2

Published in ABA Tax Times, January 2022. © 2022 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

ABA TAX TIMESFall • January 2022 • Vol. 41 No. 1

Regulations with respect to the BBA Special Enforcement Matters, IRS Form 911, a proposed revenue ruling and a revenue procedure under Section 1504 regarding the ability of a professional corporation to join in the filing of a consolidated return, and Chief Counsel Memorandum 20214101F (concerning Research Credit Refund Claims). The Section also recently submitted comments to the Multistate Tax Commission on tax issues surrounding the application of sales and use taxes to digital goods and services. Please consider volunteering for a comments project. In addition to helping improve the tax system, it’s a perfect opportunity to get more involved in committee activities and to connect with like-minded practitioners. Also, I want to invite committee members to feel free to suggest comment projects to committee leaders—sometimes the people most connected to issues that are gaining momentum are committee members working on client matters who notice something others have missed.

Publications

The Section’s publications continue to provide a substantial member benefit and an important contribution to the tax bar through the committed leadership of Roberta Mann, Vice Chair, Publications. The Section’s publications include The Tax Lawyer, the ABA Tax Times and The Practical Tax Lawyer. These are a labor of love and are only possible thanks to the dedication and extraordinary contributions of the volunteer members who consistently go above and beyond, including Gilbert Rothenberg, Associate Editor-in-Chief, The Tax Lawyer; Matthew Schaefer, Associate Editor-in-Chief, State and Local Tax, The Tax Lawyer; Linda M. Beale, Supervising Editor, ABA Tax Times; and Jerald D. August, Editor-in-Chief, The Practical Tax Lawyer. Publication of The Tax Lawyer also relies on the extraordinary support of the Section’s educational affiliate, Northwestern University Pritzker School of Law Tax Program. Interested readers should consider submitting articles to one of the Section’s publications: the editors are always looking for good content.

The Section has recently published The Supreme Court, Federal and State Taxation, and the Constitution, Second Edition by Jasper L. Cummings, Jr., a comprehensive and illuminating look at the intersection of the U.S. Constitution and federal and state taxation going back to the earliest years of the nation.

Justice, Diversity, Equity and Inclusion (JDEI)

Our nation’s tax system has a meaningful impact on all of its people. In addition, the tax laws we enact, the interpretation of our tax laws, and the manner of their enforcement all reflect our nation’s values. The Tax Section is the largest national member organization of tax professionals. As such, it has an opportunity and a duty to ensure that bias in our tax laws is considered and addressed at every level. For these reasons, among many others, it’s critical that the members of the Tax Section, and the tax bar, represent our nation’s current and growing diversity.

In December, the Section launched two important JDEI initiatives: The Loretta Collins Argrett Fellowship and the Justice, Diversity, Equity, and Inclusion Fund (JDEI fund) endowment. The Loretta Collins Argrett Fellowship seeks to identify, engage, and bring historically underrepresented individuals into the Tax Section and create a more accessible, equitable, and inclusive pathway into Tax Section leadership.

The fellowship is a three-year program open to individuals with diverse backgrounds and/or who have a demonstrated commitment to promoting diversity, equity, and inclusion in the tax bar. The Section hopes to award up to five (5) three-year fellowships each fiscal year. Please help us get the word out to potential candidates. Applications for the inaugural class of Loretta Collins Argrett Fellows are due by Sunday, April 3, 2022. Thanks to Caroline Ciraolo, Vice-Chair of Membership, Diversity, and Inclusion, and Genevieve

3

Published in ABA Tax Times, January 2022. © 2022 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

ABA TAX TIMESFall • January 2022 • Vol. 41 No. 1

Borello, Director, Membership, Marketing, and Diversity, for their hard work and commitment in getting this across the finish line in 2021.

The JDEI Fund was created to provide stable, long-term funding for the Section’s JDEI initiatives and will provide financial support primarily for the new fellowship program.

Committees

The Section’s committees are its lifeblood and the vehicle through which the Section delivers high quality CLE sessions, prepares comments to the government on pending guidance, provides content for its many publications, offers targeted networking and mentorship opportunities, and much more. The Section has 36 substantive committees, covering practice areas such as Administrative Practice, Corporate Tax, Court Procedure and Practice, Employee Benefits, Foreign Activities of U.S. Taxpayers, Partnerships and LLCs, Pro Bono and Tax Clinics, Real Estate, S Corporations, Tax Accounting, Tax Policy, and U.S. Activities of Foreigners and Tax Treaties (to name a few), as well as special interest groups like Diversity, Teaching Tax and Young Lawyers. Committee involvement is the perfect vehicle for finding and networking with like-minded colleagues. If you are not an active member of one of the Section’s committees, I encourage you to consider the many areas covered and reach out to at least one committee. If you are interested in learning more about the committees in general, I encourage you to attend the Midyear Meeting’s Information and Networking Session: Connecting with Tax Section Committees for New and Veteran Members (described below).

Midyear Meeting

The Virtual 2022 Midyear Tax Meeting will be held January 31 to February 4 and will offer a full week of tax CLE, along with expanded networking opportunities on each day of the meeting. The Opening Plenary Session on Monday, January 31 at 10:30 Eastern Time will feature William G. Gale, Co-founder and Co-director, Tax Policy Center, who will focus his remarks on the lack of attention paid to race issues by mainstream public finance analysis in economics. Loretta Collins Argrett, the eponym of the Section’s new fellowship program, will also speak at the Opening Plenary Session. Her remarks will touch on her groundbreaking career and the importance of promoting diversity, equity and inclusion in the tax bar.

The Section continues to expand the networking opportunities at its virtual meetings. On January 31, the first day of the Midyear Meeting, at 4:30–5:30 p.m. Eastern Time, we’ll introduce a new Information and Networking Session: Connecting with Tax Section Committees for New and Veteran Members. During this session, Tax Section leaders will give an overview of how to get the most out of Tax Section meetings, committee membership and diversity efforts. In addition, representatives from many of the Section’s substantive committees will join participants in small breakout groups, which should allow participants to connect with the committees that interest them.

Gratitude

It’s impossible to write about the Tax Section without thanking the incredible staff and the volunteer leaders, including the Section Officers and committee leadership, who are the driving force behind it. The pandemic presents new challenges at every turn, and our amazing staff and leadership continue to rise to the occasion with energy, imagination, innovation and commitment. Toward the end of last year, we were delighted to promote Haydee Moore as the new Section Director of the Tax Section. As many of you know, Haydee did a

4

Published in ABA Tax Times, January 2022. © 2022 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

ABA TAX TIMESFall • January 2022 • Vol. 41 No. 1

wonderful job as the Section’s Director of Meetings. She’s now bringing that same extraordinary skillset to help us chart the Tax Section’s course into the future.

Thanks, too, for the loyalty and support of our members. We are fully committed to making the Section the best it can be. If you have ideas, comments, or suggestions, please feel free to reach out to me directly at [email protected]. ■

5

Published in ABA Tax Times, January 2022. © 2022 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

An Online Publication of the ABA Tax Section Fall • January 2022 • Vol. 41 No. 1

PEOPLE IN TAX

Interview with Jacob Puhl

By Jeremiah Coder, Washington, DC

Editor’s Note: Jacob Puhl (JP) is currently the Tax Policy Manager at Meta (formerly Facebook). He has been a legal intern at Treasury, a law clerk for the U.S. Senate, and a state and local tax (SALT) intern at KPMG. ATT interviewed him in mid-November to learn something about his decision to become a tax attorney.

ATT: Hi Jacob! You’ve been pretty consistent in being grounded in tax policy from the beginning of your career, with experience at Treasury, on the Hill, accounting firms, and now in-house. What got you

interested in tax in the first place?

JP: When I started law school, I was sure I wanted to go into finance or banking law, having spent the two years after college working at Morgan Stanley. But once I was a 2L and could actually take those

courses, I quickly realized they didn’t appeal to me. Meanwhile, I took Tax 1 as a suggested course for students interested in finance and I was instantly hooked. While there was still some “it depends” in tax, it felt more tangible than other courses and those first few tax cases are just fun! I quickly changed my spring semester to include other tax classes and fortunately ended up with a summer associate position in SALT at a Big 4 accounting firm.

ATT: What, if anything, surprises you most about the tax law profession?

JP: How little math is actually involved! Not that I’m afraid of the math, but especially in a policy role, the issue is more often about the bigger picture than a specific calculation.

ATT: How did you first get involved in the Tax Section?

JP: When I was at Georgetown working on my LLM and still unsure what kind of job I wanted after school, one of the best pieces of advice I got was to join the Tax Section and to attend events. So I did! It was a

great way to meet attorneys and hear the varied ways they used their law degrees in the field. It was also an amazing way to start building a network. And considering I ended up working in policy, it’s been really helpful to know people in a variety of areas. So I would highly recommend attending events to other tax lawyers and law students interested in tax!

Jacob Puhl

6

Published in ABA Tax Times, January 2022. © 2022 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

ABA TAX TIMESFall • January 2022 • Vol. 41 No. 1

ATT: Any significant mentors/influences in the profession?

JP: I haven’t had a formal mentor, but when I was an intern at Treasury, Bob Stack was a great resource: teaching interns a lot about tax policy; explaining how he got where he was in his career; and putting me

in contact with folks working in international tax in DC. We have had the chance to work together several times since then, including some overlapping time at Deloitte. And we still keep in touch: he recently gave me a collection of books to help fill our library while he downsizes.

I would also mention my first tax law professor, Donald Tobin, who made tax law exciting and accessible.

ATT: Did you have a perception of what in-house work would be like, and what’s been the biggest surprise you’ve encountered so far?

JP: I had heard that working in-house tends to be less specialized, so I expected to cover a more varied range of issues and need to brush up on things I hadn’t studied in years. However, it has been far broader

than I imagined! In a policy role, it’s often not enough to know the tax issue. You also have to understand the underlying political or technical issues that spill into tax, so a lot of the role is learning about those non-tax factors. And when you layer in our global footprint, the role often includes meeting with folks all over, though now these are all virtual – and often very early in the morning for me. Another surprise for an American: I never thought I would need to learn so much about VAT! So grateful for my overseas colleagues taking the time to teach me.

ATT: If you could make one change in the tax policy realm, what would it be and why?

JP: I think more tax policy should be accessible to non-tax folks, including non-lawyers. Tax is a unique area of the law in that basically every person interacts with it, yet many people don’t understand why

and how rules get made.

ATT: How has “globalization” of tax changed how some companies face international tax policy?

JP: Tax is in a period of rapid change just like the global economy. Most tax rules were written a century ago when businesses operated quite differently, and governments around the world are working to update

those rules. As more and more businesses of all sectors and sizes operate across borders, they are seeking workable, globally consistent rules aligned with best practices. Growth requires certainty and stability in the international tax system, so changes must be made in an international, collaborative context.

ATT: What do you think are important trends in tax policy that taxpayers and advisers will still be dealing with in 10 years?

JP: I may be partial, but I think taxation of the digitizing economy will continue to be an important issue over the decade. Tax is difficult enough without layering in evolving technologies and global economic

trends, so as more business takes place across borders electronically, I think policymakers will still be busy. In addition, the OECD Inclusive Framework member countries have agreed to work over the next few years to implement domestic rules for taxing the digitizing economy, which I think will have knock-on effects and influence non-member countries to develop similar regimes.

7

Published in ABA Tax Times, January 2022. © 2022 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

ABA TAX TIMESFall • January 2022 • Vol. 41 No. 1

ATT: When you’re not busy thinking about tax, what do you do to unwind? How important is it to maintain balance for mental health?

JP: My husband and I recently bought a historic home in Baltimore, so I spend a lot of time working on it and our gardens. It’s a lot of work but it’s been fun and really gratifying seeing it all come together! I think

a balance between work and personal life is essential, though it can be more difficult working from home. I also enjoy a nice long walk at the end of the day to separate the work day from the evening.

ATT: Do you have a favorite depiction of a lawyer in a movie or book?

JP: Since I’m sure others have said all the classics, I’ll go with Trevor Nelsson on NBC’s “Parks & Recreation.” ■

8

Published in ABA Tax Times, January 2022. © 2022 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

An Online Publication of the ABA Tax Section Fall • January 2022 • Vol. 41 No. 1

PRACTICE POINT

A Primer on Charitable Trusts (Part II)

By Thomas W. Bassett, VP, Tax Manager – East Region, Commerce Trust Company, St. Louis, MO

Part I of this article in the summer issue of ATT covered some of the basic terminology of charitable trusts and briefly discussed two types—the Charitable Remainder Trust

(CRT) and the Charitable Lead Trust (CLT). It also introduced readers to CRATs (charitable remainder annuity trusts) and CRUTs (charitable remainder unitrusts). As noted in that Part, CRUTs allow additional contributions to the trust after establishment and distribute a fixed percentage of the trust assets each year based on annual revaluations.

Depending on a client’s mix of assets and goals, there are some more specialized vehicles which might be relevant—including NICRUTs, NIMCRUTs (and “flip” variants of either), and Pooled Income Funds.

I. NICRUTs and NIMCRUTs

A NICRUT is a ‘net income charitable unitrust’, and a NIMCRUT is a ‘net income makeup charitable remainder unitrust’.

Each has some of the aspects of a standard CRUT as discussed in Part I. For example, each has a ‘valuation date’ and a ‘unitrust amount’ which the trustee will calculate, based on the fair market value of the trust’s assets on the valuation date.

However, that’s not the full story. A NICRUT typically distributes the lesser of (a) trust accounting income or (b) the unitrust amount. Trust accounting income, as expected, is a term of art: it’s a creature of state fiduciary statutes and may differ from one state to the next, even though all states have adopted some form of the Uniform Principal and Income Act first established by the Commission on Uniform State Laws in 1997.1

For example, if a settlor created a 5% CRAT for the benefit of a family member and contributed $1,000,000 of stock to the CRAT, the payout rate would be $50,000 per year to the income beneficiary. If the assets of the CRAT were solely stock in a non-dividend paying corporation, the trust wouldn’t have the cash to make the required $50,000 distribution.

In that case, it might be better to change the structure of the CRAT to a NICRUT. While the trustee would still need to value the assets of the trust to determine the unitrust amount (i.e., the fixed percentage to

1 See, e.g., Wikipedia Uniform Principal and Income Act. Although all 50 states have adopted some version of the act, it has not been uniformly adopted by the states. For example, one state may allocate investment fees 50% to income and 50% to corpus, while another state may have a different allocation method. Any expenses allocated to income reduce, dollar for dollar, the trust accounting income that would be distributed to an income beneficiary, so these differences matter!

9

Published in ABA Tax Times, January 2022. © 2022 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

ABA TAX TIMESFall • January 2022 • Vol. 41 No. 1

be paid to the income beneficiary), the NICRUT’s trust accounting income would be $0 (zero) in year(s) when the corporation made no dividend distributions. As a result, the required distribution amount for the NICRUT would also be $0.

A settlor would not typically fund a CRT with such non-dividend paying stock. But there are similar assets which generate little or no current income—such as forest land or undeveloped mineral resources. In those situations, a NICRUT would have no income during the development period and thus would not encounter the need to make required distributions when there was a cash shortfall.

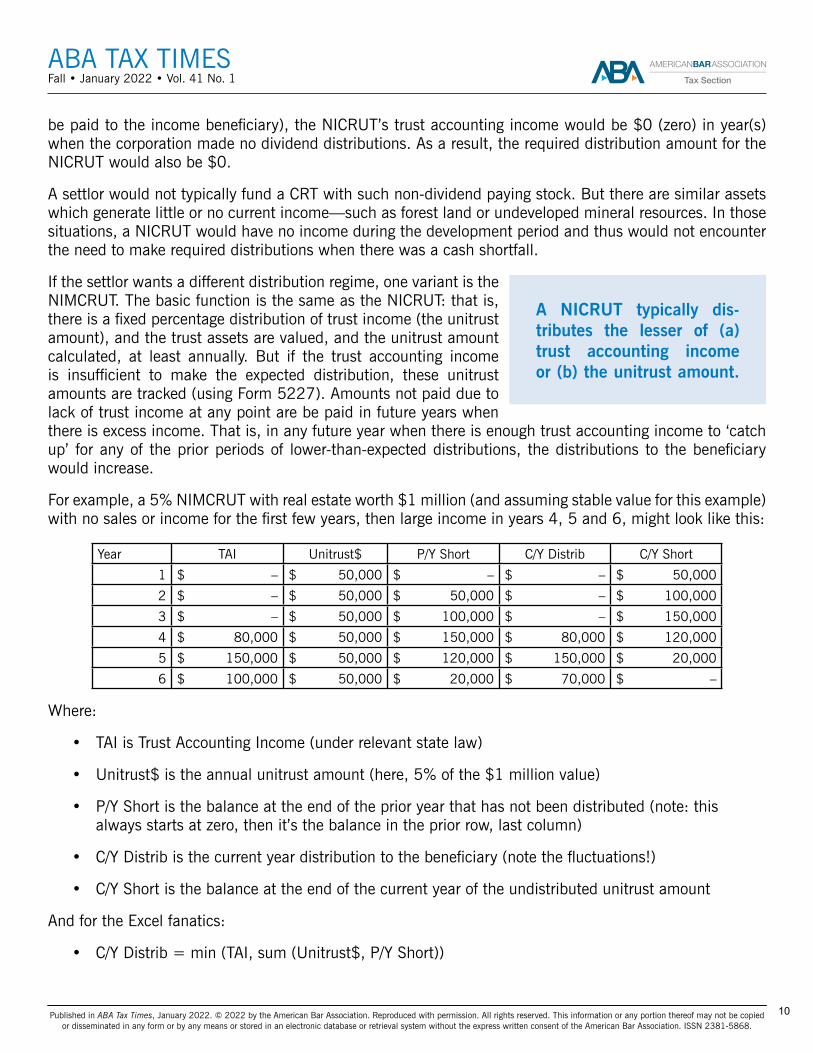

If the settlor wants a different distribution regime, one variant is the NIMCRUT. The basic function is the same as the NICRUT: that is, there is a fixed percentage distribution of trust income (the unitrust amount), and the trust assets are valued, and the unitrust amount calculated, at least annually. But if the trust accounting income is insufficient to make the expected distribution, these unitrust amounts are tracked (using Form 5227). Amounts not paid due to lack of trust income at any point are be paid in future years when there is excess income. That is, in any future year when there is enough trust accounting income to ‘catch up’ for any of the prior periods of lower-than-expected distributions, the distributions to the beneficiary would increase.

For example, a 5% NIMCRUT with real estate worth $1 million (and assuming stable value for this example) with no sales or income for the first few years, then large income in years 4, 5 and 6, might look like this:

Year TAI Unitrust$ P/Y Short C/Y Distrib C/Y Short

1 $ – $ 50,000 $ – $ – $ 50,000

2 $ – $ 50,000 $ 50,000 $ – $ 100,000

3 $ – $ 50,000 $ 100,000 $ – $ 150,000

4 $ 80,000 $ 50,000 $ 150,000 $ 80,000 $ 120,000

5 $ 150,000 $ 50,000 $ 120,000 $ 150,000 $ 20,000

6 $ 100,000 $ 50,000 $ 20,000 $ 70,000 $ –

Where:

• TAI is Trust Accounting Income (under relevant state law)

• Unitrust$ is the annual unitrust amount (here, 5% of the $1 million value)

• P/Y Short is the balance at the end of the prior year that has not been distributed (note: this always starts at zero, then it’s the balance in the prior row, last column)

• C/Y Distrib is the current year distribution to the beneficiary (note the fluctuations!)

• C/Y Short is the balance at the end of the current year of the undistributed unitrust amount

And for the Excel fanatics:

• C/Y Distrib = min (TAI, sum (Unitrust$, P/Y Short))

A NICRUT typically dis-tributes the lesser of (a) trust accounting income or (b) the unitrust amount.

10

Published in ABA Tax Times, January 2022. © 2022 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

ABA TAX TIMESFall • January 2022 • Vol. 41 No. 1

• C/Y Short = sum (Unitrust$, P/Y Short) – C/Y Distrib

At the close of year 6, the trust’s cumulative TAI is $330,000, of which $300,000 has been distributed to the beneficiary and $30,000 remains in the trust.

Note that there are a number of valuable features of the NICRUT and NIMCRUT. One distinctive feature is that the trust principal remains intact at all times (or increases), ensuring that when the trust period ends, the principal will pass to a charity for the purpose the settlor designated. In addition, because additional contributions may be made at any time (yielding a tax deduction for a portion of the value), the settlor has more precise tax management possibilities. The trust is confidential, and the assets are generally protected from creditors. Earnings that remain in the trust, of course, increase its value with tax-deferred compounding over time. The recipient charity can be changed at any time. Finally, administrative costs are generally lower than for a variety of other tax-reducing plans.

II. FLIP Variants

Both NICRUTs and NIMCRUTs can also have “flip” characteristics—that is, the language of the document specifies that the nature of the trust changes, with a different payout calculation, upon the occurrence of a particular event.

For example, assume that the settlor contributes a (former) family home to a CRT for the local college or university. That former residence might be vacant and not an income producing property, making it not a strong candidate for either a CRUT or CRAT. Nevertheless, the settlor might want the assurance of the cash flows of a CRUT.

Enter the flip. From the start, the CRT will be a NICRUT or NIMCRUT. The settlor will contribute the asset. Trust accounting income may be zero (or a nominal amount), entitling the beneficiary (often the settlor) to little or no income. But then the CRT sells the home.

The trust contains language such as the following:

1. The “Initial Term” of the trust means the term beginning on the date the trust is created and ending on the last day of the taxable year in which the Conversion Date occurs.

2. The “Conversion Date” means the date of the sale or exchange of the real property described on Schedule A which was contributed to the trust upon its creation.

3. In each taxable year of the trust during the Initial Term, the Unitrust Amount shall be equal to the lesser of (a) the trust income for the taxable year and (b) 7 percent of the net fair market value of the assets of the trust.

4. In each taxable year of the trust after the Initial Term, the Unitrust Amount shall be 7 percent of the net fair market value of the assets of the trust.

Both NICRUTs and NIMCRUTs can also have “flip” characteristics—that is, the language of the document spec-ifies that the nature of the trust chang-es, with a different payout calculation, upon the occurrence of a particular event.

11

Published in ABA Tax Times, January 2022. © 2022 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

ABA TAX TIMESFall • January 2022 • Vol. 41 No. 1

After the sale, the trust becomes a fairly standard CRUT, paying out 7 percent of the value of its assets to the beneficiary. In contrast, prior to that sale, the trust is a NICRUT, paying out the lesser of trust income or the 7 percent amount. That’s a “flip NICRUT” in action.

A similar example could be constructed for a flip NIMCRUT. The only difference is that the unitrust amounts prior to the Conversion Date would accumulate (similar to the accumulation in the prior NIMCRUT example in the first part, above). Those prior unpaid amounts would be taken into account for the distributions made after the Conversion Date.

Tax compliance for NICRUTs, NIMCRUTs, and the flip versions of them is similar to that for CRTs in general. Each of these trusts must file Form 5227 on a calendar-year basis and issue a Schedule K1 to the unitrust beneficiary or beneficiaries. Each accumulates income into different tranches. (See Part I of this article in the summer 2021 issue of ATT for a discussion of how those tranches fluctuate in amount during each tax year).

NICRUTs and NIMCRUTs use a few more lines on Form 5227 to reflect the calculations of trust accounting income. For the NIMCRUT, the return also tracks any amount undistributed from one year to the next.

III. Pooled Income Funds

Not every client situation warrants the creation of a full-blown independent trust, with the associated administrative costs of setting up trust accounts, finding a willing trustee, managing the trust’s investments, and the like.

Congress was sympathetic to this need and created the Pooled Income Fund.2 It’s similar to a charitable mutual fund where one or more donors contribute property (cash or marketable securities) to a common fund that is managed and administered by a qualified non-profit organization (often a college or university).

Instead of each donor having a separate annuity or unitrust calculation, the fund calculates a rate of return and that rate of return drives the annual distributions to the beneficiaries. After the death of each beneficiary, a share of the assets in the fund is then distributed to the charitable sponsor.

Pooled income fund deductions are computed using a valuation rate rather than the IRS discount rate. The applicable valuation rate depends on the age and investment history of the fund. The mandated valuation rate for gifts to ‘young’ funds originally funded in 2020 and 2021 is 2.2%.3 The valuation rate for gifts to older funds is the fund’s highest annual rate of return in the prior three years. This rate of return

must be computed as described in Treas. Regs. sections 1.642-6(c)(2)–(3). (The details for that calculation are far beyond the scope of this article.)

To illustrate, assume GreenAcres University has a long-established Pooled Income Fund. Donors Smith and Jones contribute cash to the fund: Smith donates $10,000 and Jones contributes $15,000. The fund would add

2 IRC § 642(c)(5).3 A good resource for Pooled Income Funds is the article at https://www.pgcalc.com/pooled-income-fund-valuation-rates.

The Pooled Income Fund [is] similar to a char-itable mutual fund where one or more donors contribute property (cash or marketable se-curities) to a common fund that is managed and administered by a qualified non-profit organization (often a college or university).

12

Published in ABA Tax Times, January 2022. © 2022 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

ABA TAX TIMESFall • January 2022 • Vol. 41 No. 1

those contributions to the pooled fund. Assume that the fund has one prior member who has 5 shares in the fund and that, based on their relative contributions, Smith is credited with 2 shares and Jones is credited with 3 shares in the pooled fund.

If the fund has $50,000 and earns 2%, it will have income of $1,000—i.e., $100 per share. That means Smith will receive a K1 from the fund listing $200 of income, and Jones will receive a K1 from the fund listing $300 of income, while the earlier member’s K1 will list the remaining $500.

IV. Conclusion

Charitable giving is widespread in the United States. Americans gave over $471 billion to charities in 2020, 5.1% more than they donated in 2019. Sixty-nine percent (69%) of that amount was donated by individuals—i.e., a total amount of $324 billion. That amount has grown in 5 of the past 6 years.4

A. Interesting Statistics on Form 5227

The IRS periodically releases Statistics of Income but has not updated these releases for Form 5227 in almost a decade.5 Their most recent summary provided the following information on filings:6

The number of Forms 5227 filed with the IRS has declined in recent years.

In Filing Year 2012, the IRS received 113,688 Forms 5227, down from 117,710 in 2011.

Charitable remainder unitrusts continued to be the most common split-interest trusts, accounting for more than three-quarters (80.3 percent) of returns filed in 2012.

Total investments reported increased 1.5 percent to $8.7 billion in 2012, with corporate stock remaining the largest investment category, accounting for 88 percent of total assets.

Trustees of split-interest trusts reported approximately $4.3 billion in charitable distributions, with charities established for public or societal benefit receiving $2.5 billion in distributions, 58 percent of the total.

The number of active pooled income funds declined rapidly in the data, likely reflecting the interest rate environment (which has not improved since the study period), as lower interest rates have an impact on the rates of returns used by these funds but can positively impact the charitable deduction claimed by the donor.

B. Other Funding Concerns

Some clients may ask about a Donor Advised Fund (DAF). While a DAF is often a public charity, which brings considerable simplicity (no separate tax return, no separate trust document is needed, etc.), that simplicity comes at a cost. DAF donors do not usually have any input on how the funds are managed by the DAF sponsor, and, more relevant to this article, DAF donors retain no interest in the DAF assets—there is no income stream for their retirements or for their surviving spouses.

4 https://www.nptrust.org/philanthropic-resources/charitable-giving-statistics/.5 Form 5227 is frequently called the “red-headed stepchild” by practitioners in the field.6 https://www.irs.gov/pub/irs-soi/12splitinteresttrustonesheet.pdf.

13

Published in ABA Tax Times, January 2022. © 2022 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

ABA TAX TIMESFall • January 2022 • Vol. 41 No. 1

Other clients may wish to have a split-interest trust survive beyond their generation to provide for members of the next generation. It’s very difficult to have a CRT qualify when there are young beneficiaries.

A Pooled Income Fund may solve some of these difficulties—a payment stream for the donor and/or family members is permitted, and there’s no 10 percent remainder requirement as there is for a CRT. Also, a donation to a Pooled Income Fund (particularly one that’s been in existence for many years) may provide a significant income tax deduction. However, such a fund usually has one charitable sponsor, so the donor won’t have the ability to pick/choose other charities to receive funds at the termination of the income interest.

C. Planning Opportunity7

A flip unitrust may also help with administrative issues for CRUTs formed late in the year. For example, if a donor creates a CRUT during December, the regulations require either (a) a distribution by December 31st of a pro-rated amount for the year or (b) a complex trustee election which is deemed to generate gain.

If, instead, the document is a flip NICRUT or flip NIMCRUT and there’s no income earned in the account for December, there’s no required distribution for the month. The ‘flip’ event can be “January 1 of the year following the funding of the trust”, which automatically changes the trust from an income-only trust to a ‘regular’ unitrust. This structure avoids the need to make a short-year calculation and distribution or the need to prematurely recognize gain. ■

7 Significant thanks are due to Larry Katzenstein of Thompson Coburn who presented this idea in a recent meeting of the Estate Planning Council of St. Louis.

14

Published in ABA Tax Times, January 2022. © 2022 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

An Online Publication of the ABA Tax Section Fall • January 2022 • Vol. 41 No. 1

AT COURT

The IRS’s Procedural Battles in Micro-Captive Litigation

By David J. Slenn, Shumaker, Loop & Kendrick, LLP, Tampa, FL

The ABA Tax Times Spring 2021 issue addressed the recent Tax Court opinion in Caylor Land v. Commissioner.1 Caylor represented the fourth straight IRS victory over abusive micro-captive transactions. Yet although the IRS has an unblemished record in the Tax Court against micro-captives on substantive grounds, it has faced numerous procedural battles in cases related to micro-captives.

These recent procedural battles include the Supreme Court’s decision in CIC Services v. Commissioner2 and a recent Tax Court case, Puglisi v. Commissioner.3 In CIC Services, the Supreme Court held the Anti-Injunction Act did not prevent a material advisor from challenging the validity of Notice 2016-66 (requiring reportable transaction reporting), thereby remanding the case to the district court. In Puglisi v. Commissioner, the taxpayers attempted to force the IRS to trial even though the IRS conceded all tax, interest and penalties associated with the taxpayers’ micro-captive deductions. As described in more detail below, the IRS recently filed a motion for summary judgment in CIC Services and a motion for decision in Puglisi.

I. Other Micro-Captive Cases of Interest

There are other pending cases worth noting but not covered in this article. The Delaware Department of Insurance is appealing a district court order granting an IRS petition to enforce a summons seeking certain Delaware micro-captive insurance company records.4 In addition, Moore Ingram Johnson & Steele LLP, a law firm that also provides captive management services, is appealing a Georgia district court order granting an IRS summons.5 Moore Ingram’s arguments on appeal involve the appropriateness of categorical privilege logging and whether collateral estoppel applies to privileged information that was at issue in two Kentucky district court privilege rulings. Moore Ingram’s oral argument begins with an observation about the IRS’s actions in the case as being part of a larger initiative to eliminate micro-captive insurance

1 Caylor Land & Dev., Inc. v. Comm’r of Internal Revenue, T.C. Memo. 2021-30 (2021).2 CIC Servs., LLC v. Internal Revenue Serv., 141 S. Ct. 1582 (U.S. May 17, 2021).3 Order, Puglisi, et. al. v. Comm’r of Internal Revenue, 4799-20, et. al. (U.S. Tax Court, Oct. 29, 2021).4 United States of America v. Delaware Department of Insurance, No. 21-3008 (3rd Cir. Nov. 1, 2021).5 United States of America v. Moore, Ingram, Johnson & Steele, LLP, No. 21-10341 (11th Cir. Feb. 2, 2021). In its Appellant’s Brief, the United States summarized the facts leading up to the appeal.

The IRS is investigating the Firm’s ‘captive insurance program’ – a kind of business transaction particularly susceptible to abusive tax avoidance schemes. To pursue its investigation, the IRS issued a summons to the Firm seeking documents related to that program. After the Firm withheld large volumes of responsive documents, the IRS petitioned the District Court for enforcement. As explained below, the District Court correctly rejected the Firm’s objections, other than its request not to be required to produce additional copies of materials it had already provided, and ordered that the summons be enforced.

United States of America v. Moore, Ingram, Johnson & Steele, LLP, 2021 WL 1526573 (11th Cir. Apr. 14, 2021).

15

Published in ABA Tax Times, January 2022. © 2022 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

ABA TAX TIMESFall • January 2022 • Vol. 41 No. 1

companies.6 Finally, in Celia R. Clark v. USA,7 an attorney who also provided captive management services in the first-decided micro-captive case, Avrahami v. Commissioner, is suing for a refund of section 6700 penalties and for improper disclosure of her return information under section 7431. The complaint also contains an allegation accusing the IRS of wrongful actions.

[It] has sought to destroy the microcaptive insurance industry. It has not done so by promulgating regulations, issuing revenue rulings, or providing affirmative guidance that taxpayers and tax practitioners could follow. Rather, the IRS has engaged in the unlawful “administrative repeal” of IRC Section 831(b), thwarting Congress’s intent by wrongfully penalizing taxpayers and practitioners in the microcaptive space, in a concerted effort to drive them out of that business.

The complaint further alleges that the IRS engaged in abusive tactics by allowing section 6700 penalties to accumulate against the plaintiff for years, “rather than provid[ing] clarity.”8

II. CIC Services v. Commissioner

A. Notice 2016-66 & the Administrative Procedures Act

In CIC Services, the IRS argued that CIC (a company that provides captive management services) was prohibited from challenging Notice 2016-66 under the Anti-Injunction Act. The Supreme Court ruled the Anti-Injunction Act did not bar the taxpayer’s challenge, thereby setting the stage for CIC and the IRS to battle once again in federal district court, this time over whether Notice 2016-66 was invalid due to, inter alia, the IRS’s failure to engage in the Administrative Procedures Act (APA) notice and comment rulemaking requirements.

The broader implication in this case is whether the IRS may issue notices requiring reporting obligations for reportable transactions (or a particular category of reportable transactions) without first engaging in the APA requirements. The IRS issued Notice 2016-66 describing a micro-captive transaction as a “transaction of interest” because the IRS and Treasury Department believe certain micro-captive transactions “have a potential for tax avoidance or evasion, but for which the IRS and Treasury lack enough information to determine whether the transaction should be identified specifically as a tax avoidance transaction.”9

On remand, CIC sought and obtained a preliminary injunction on September 21, 2021 enjoining the IRS from enforcing the Notice against CIC.10 Although the court granted the injunction, it was limited to CIC, as opposed to a national, outright injunction as to Notice 2016-66. On October 8, 2021, CIC requested that the court reconsider the scope of the injunction and issue a national, outright injunction as initially requested. While reconsideration of the national injunction matter is

6 Oral argument, Nov. 19, 2021 (audio recording).7 Celia R. Clark v. United States of America; The Internal Revenue Service, 9:21-cv-82056 (S.D. Fl. Nov. 11, 2021).8 Complaint and Demand for Jury Trial at 12.9 Preamble to the final section 1.6011-4 Regulations, 2007-38 I.R.B. 607, 72 F.R. 43146-01.10 CIC Servs., LLC v. Internal Revenue Serv., Dep’t of Treasury, No. 3:17-CV-110, 2021 WL 4481008 (E.D. Tenn. Sept. 21, 2021).

The broader implication in this case is whether the IRS may issue notices re-quiring reporting obligations for report-able transactions (or a particular cate-gory of reportable transactions) without first engaging in the APA requirements.

16

Published in ABA Tax Times, January 2022. © 2022 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

ABA TAX TIMESFall • January 2022 • Vol. 41 No. 1

pending, the IRS moved to dispose of the case on its merits through a motion for summary judgment (MSJ) on November 1, 2021.

B. IRS Motion for Summary Judgment

In its MSJ, the IRS acknowledged that the Court found CIC’s argument persuasive at first glance, but it suggested that a fuller examination of the issues should result in an IRS victory.

The MSJ addresses CIC’s three main arguments that the IRS violated the APA by not engaging in required notice and rulemaking requirements, engaged in arbitrary and capricious conduct by issuing Notice 2016-66, and did not comply with the Congressional Review Act.11 In its MSJ, the IRS argued that the Court focused on the wrong authorities for purposes of issuing its preliminary injunction. The IRS then argued that the notice and rulemaking requirements do not apply to Notice 2016-66 due to the scope of section 6707A and referencing Congressional enactments supporting the argument that notice and rulemaking were not required. The IRS also cited a recent Sixth Circuit opinion that found that IRS issuance of a notice regarding a listed transaction did not violate the APA. These arguments are discussed in more detail below.

1. Code Sections 6011 and 6707A & Treas. Reg. Section 1.6011-4

Section 6111 of the Code imposes reporting obligations on “material advisors.” When the court granted the injunction, it focused on section 6111(c), which authorizes the Secretary to “prescribe regulations which … provide such rules as may be necessary to carry out the purpose of this section.”12 Section 6111(c), however, is not the appropriate authority for issuing Notice 2016-66; instead, the relevant authorities for that notice’s issuance are section 6011 and Treas. Reg. section 1.6011-4. One only turns to section 6111 after a reportable transaction has been identified.

Section 6011 requires the filing of a return or statement when required by regulations.13 Treasury regulations promulgated under section 6011 provide the authority for the IRS to identify certain micro-captive transactions as “transactions of interest” through issuance of notices, as was done with certain micro-captive transactions through Notice 2016-66.14

11 CIC voluntarily dismissed its third cause of action alleging violation of the Congressional Review Act. See CIC Services, LLC’s Motion for Summary Judgment on its First Cause of Action, Partial Summary Judgment on its Second Cause of Action, and Voluntarily Dismissal of its Third Cause of Action (Dkt 97, Nov. 1, 2021) at 8.12 Memorandum Opinion and Order (Dkt 82, Sept. 21, 2021) at 10 n. 6. (emphasis added). The IRS notes in a footnote that it had mistakenly drawn the Court’s attention to section 6011 as the relevant source of authority in its response to the motion for preliminary injunction.13 I.R.C. § 6011(a) (stating that “[w]hen required by regulations prescribed by the Secretary any person made liable for any tax imposed by this title, or with respect to the collection thereof, shall make a return or statement according to the forms and regulations prescribed by the Secretary”).14 Treas. Reg. §1.6011-4(b)(6) (defining a transaction of interest as “a transaction that is the same as or substantially similar to one of the types of transactions that the IRS has identified by notice, regulation, or other form of published guidance as a transaction of interest”) (emphasis added).

The MSJ addresses CIC’s three main argu-ments that the IRS violated the APA by not en-gaging in required notice and rulemaking re-quirements, engaged in arbitrary and capricious conduct by issuing Notice 2016-66, and did not comply with the Congressional Review Act.

17

Published in ABA Tax Times, January 2022. © 2022 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

ABA TAX TIMESFall • January 2022 • Vol. 41 No. 1

In its MSJ, the IRS argues that the court should have considered the interplay between section 6707A and Treas. Reg. section 1.6011-4, which the Court did not focus on when it issued the injunction. Although section 6111 imposes reporting obligations on material advisors, one cannot be a material advisor unless an underlying reportable transaction has first been identified pursuant to section 6011 and the regulation promulgated under that section. The potential for penalties for failure to include reportable transaction information with a return is found in section 6707A. The IRS then described the exceptions under the APA and turned to the history of these Code and Regulation sections as support for its argument that it did not violate the APA when it issued Notice 2016-66.

2. Administrative Procedures Act

Generally, federal agencies must go through notice and comment rulemaking before promulgating a rule. This means the agency must notify the public of the proposed new rule, give the public an opportunity to comment on the new rule, and then address the comments received. The IRS argues it does not need to engage in notice and comment rulemaking when Congress expressed a clear intent that an agency may use another procedure or when issuing “interpretive” rules. The IRS argues that Notice 2016-66 falls under both exceptions to notice and comment rulemaking.

3. Notice 2016-16 & Congressional Intent

The IRS notes that notice and rulemaking was conducted in 2003 when the IRS finalized a regulation under section 6011 allowing it to identify potentially abusive transactions, including six categories of reportable transactions. Congress enacted section 6707A in 2004, which required reporting of transactions identified under section 6011, with the potential for penalties due to non-compliance. At that time, regulations were already in existence that authorized the IRS to identify listed transactions by “notice, regulation, or other form of published guidance.”15

The IRS notes that CIC did not challenge the section 6011 Treasury regulations identifying listed transactions and transactions of interest as reportable transactions. In its complaint, CIC challenged the IRS’s failure to engage in notice and rulemaking only as to Notice 2016-66. The IRS argues that a finding that Notice 2016-66 violated the APA would not make sense given the legislative history behind sections 6011 and 6707A, which in turn authorizes the Treasury Department to define a listed transaction and a reportable transaction.

The IRS also points to an amendment to the section 6011 regulations in 2007, where “transactions of interest” were added as a category of reportable transactions.16 The Treasury Decision publishing these regulations notes that “several commentators requested that the IRS and Treasury Department provide notice to taxpayers that the IRS and Treasury Department are considering designating a particular transaction as a transaction of interest and requesting comments prior to publishing guidance identifying a transaction as a transaction of interest.”17 As to this request for comments, the amendment provides “[t]he IRS and Treasury Department do not believe that the regulations should be amended to include language requiring the IRS and Treasury Department to provide advance notice for transactions of interest as suggested by the commentators. However, the IRS and Treasury Department may choose to publish advance notice and

15 Tax Shelter Regulations, 68 F.R. 10161-01 (March 4, 2003.)16 AJCA Modifications to the Section 6011 Regulations, 72 F.R. 43146-01 (Aug. 3, 2007).17 Treas. Dec. 9350.

18

Published in ABA Tax Times, January 2022. © 2022 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

ABA TAX TIMESFall • January 2022 • Vol. 41 No. 1

request comments in certain circumstances. The determination of whether to provide advance notice and a request for comments will be made on a transaction by transaction basis.”18

The IRS points to another amendment to section 6707A in 2010. By this time, it states, the IRS had already started to identify transactions of interest under the 2007 regulation, without notice and comment. Congress, the IRS notes, would have been aware of this since it expressly described how “listed transactions” and “transactions of interest” were identified by “publications issued by the Treasury Department.” The IRS cites the Technical Explanation of Tax Provisions in Senate Amendment 4594 to H.R. 5297. The Joint Committee on Taxation provided a summary of then-current law (i.e., as of 2010) which included statements indicating that transactions of interest were described in publications issued by the Treasury Department.

There are five categories of reportable transactions: listed transactions, confidential transactions, transactions with contractual protection, certain loss transactions and transactions of interest.

Transactions falling under the first and last categories of reportable transactions are transactions that are described in publications issued by the Treasury Department and identified as one of these types of transaction. A listed transaction is defined as a reportable transaction which is the same as, or substantially similar to, a transaction specifically identified by the Secretary as a tax avoidance transaction for purposes of the reporting disclosure requirements. A “transaction of interest” is one that is the same or substantially similar to a transaction identified by the Secretary as one about which the Secretary is concerned but does not yet have sufficient knowledge to determine that the transaction is abusive.19

4. Mann Construction, Inc. v. United States

The IRS then points to a recent decision in the Eastern District of Michigan involving a challenge to a notice20 issued with respect to a listed transaction. In Mann Construction, Inc. v. United States,21 the court was faced with “whether an IRS notice requiring disclosure of a potentially abusive transaction was issued without notice and comment in violation of the APA.”

The Mann court recounted the IRS’s struggle with a “new generation of tax shelters” during the 1990s, when Treasury developed a reporting regime but lacked the authority to penalize taxpayers for failure to disclose. The court noted the resolution of the issue.

18 Id.19 Technical Explanation of the Tax Provisions in Senate Amendment 4594 to H.R. 5297, the “Small Business Jobs Act of 2010,” Scheduled for Consideration by the Senate on September 16, 2010, 2010 WL 3712659, at *12 (emphasis added, internal references deleted).20 Notice 2007-83, 2007-45, I.R.B. 960, 2007 WL 3015114 (“Abusive Trust Arrangements Utilizing Cash Value Life Insurance Policies Purportedly to Provide Welfare Benefits”).21 Mann Constr., Inc. v. United States, No. 1:20-CV-11307, 2021 WL 1923412 (E.D. Mich. May 13, 2021).

The IRS argues that a finding that Notice 2016-66 violated the APA would not make sense given the legislative history behind sec-tions 6011 and 6707A, which in turn autho-rizes the Treasury Department to define a list-ed transaction and a reportable transaction.

19

Published in ABA Tax Times, January 2022. © 2022 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

ABA TAX TIMESFall • January 2022 • Vol. 41 No. 1

Congress addressed this problem in 2004 by passing the American Jobs Creation Act of 2004, Pub. L. 108-357, 118 Stat. 1418 (2004), which created I.R.C. § 6707A. Section 6707A laid the statutory foundation for the new reporting regime by establishing penalties for nondisclosure and defining “reportable transaction” and “listed transaction” by reference to Treasury regulations. See U.S.C. § 6707A. Since then, the IRS has identified many listed transactions by notice, in effect requiring taxpayers to disclose their participation or face substantial penalties under I.R.C. S 6707A. One of these revenue notices is IRS Revenue Notice 2007-83, the subject of controversy here.22

The Mann court ruled in favor of the IRS, dismissing the taxpayers’ complaint. Its holding noted the reference to section 6707A and identification of applicable transactions through various means.

Congress responded with section 6707A, which not only added penalties for the failure to disclose reportable transactions, but [also] defined “listed transaction” by reference to Treasury regulations that allow the IRS to identify listed transactions by “notice, regulation, or other form of published guidance.” 26 U.S.C. § 6707A; 26 C.F.R. § 1.6011-4. This reference is significant because revenue notices, like revenue rulings and procedures, are normally issued without the notice and comment required by the APA.23

5. Interpretive Rule Exception

Agencies are required to use notice and comment rulemaking to issue “legislative” rules, but not “interpretive” ones. In granting CIC Services’ request for a preliminary injunction, the court found Notice 2016-66 to be a legislative rule because CIC would not have to report micro-captive transactions without that notice. In its MSJ, the IRS argued that a legal effect (here, the filing requirement) is not the test for determining whether a rule is legislative or interpretive. Instead, the IRS asserted that the notice merely identifies a transaction of interest: the reporting requirement was not imposed by Notice 2016-66 but rather by the regulation that defines reportable transactions (i.e., Treas. Reg. section 1.6011-4) and the statutes that require material advisors to provide information on them or face penalties (i.e., sections 6011, 6111 and 6707A).

Although Notice 2016-66 identifies a transaction of interest, CIC did not challenge the regulatory concept of a transaction of interest as set forth in the defining regulation (Treas. Reg. section 1.6011-4(b)). In granting CIC’s injunction, the court homed in on the unlimited discretion the IRS has in identifying transactions of interest, “in contrast to the more clearly defined types of reportable transactions identified by the Secretary in 26 C.F.R. § 1.6011-4(b)(1)-(5).” It is worth noting that a “listed transaction” is defined in the regulations as “a transaction that is the same as or substantially similar to one of the types of transactions that the Internal Revenue Service (IRS) has determined to be a tax avoidance transaction and identified by notice, regulation, or other form of published guidance as a listed transaction.”24 Similarly, a “transaction of interest” is defined in the regulations as “a transaction that is the same as or substantially similar to one of the types of transactions that the IRS has identified by notice, regulation, or other form of published guidance as a transaction of interest.”25 It is not clear how a listed transaction, which results in heavier penalties, can be considered a “more clearly defined” type of reportable transaction than a transaction of interest, given these quite similar definitions in the regulations.

22 Id. at *1–2.23 Id. at *12 (emphasis added).24 Treas. Reg. § 1.6011-4(b)(2).25 Treas. Reg. § 1.6011-4(b)(5).

20

Published in ABA Tax Times, January 2022. © 2022 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

ABA TAX TIMESFall • January 2022 • Vol. 41 No. 1

6. Arbitrary and Capricious

CIC claimed that Notice 2016-66 was irrational and thus violated the APA. This was so, it said, because the IRS already had access to most of the information needed to assess the validity of captive insurance transactions and the scope of the Notice encompasses both legitimate and non-legitimate captive insurance transactions. The IRS countered that CIC’s position is inconsistent with its prior statements in which CIC conceded that captive insurance transactions have “a potential for tax avoidance or evasion.” Consequently, the IRS argues that it did not act arbitrarily or capriciously by taking the position that certain micro-captive transactions have the potential for tax avoidance or evasion.

C. IRS Notices as Prophylactic Measures

The IRS argues in its MSJ appeal not only on the legal basis but also from a public policy perspective.26 The IRS must be nimble enough to respect taxpayer rights but also identify transactions as potentially abusive at an early stage (and not “in the rear-view mirror”) to prevent widespread damage to taxpayers and the government alike.27 Once an abusive transaction takes hold, it can persist for years and cause extraordinary losses in tax revenue. For example, the IRS gave notice of syndicated conservation easements as a listed transaction in 2017,28 but by then the transaction had spread to the point where the number of transactions continued to rise after the 2017 listing.29