{Page 1} INTRODUCTION Accounting serves the purpose of providing financial information relating a business. such information is provided to people who have interest in the organization , such as shareholders, managers, creditors, debenture holders, bankers, tax authorities and others, broadly speaking, on the basis of type of accounting information and the purpose for which such information is used, accounting may be divided into three categories: 1. Financial accounting (or General accounting), 2. Cost accounting, and 3. Management accounting FINANCIAL ACCOUNTING: Financial accounting is mainly concerned with recording business transaction in the books of account for the purpose presenting financial accounts to management, share holders, creditors, investors and tax authorities, etc. It is defined as “The art of recording, classifying and summarizing in a significant manner and in terms of money, transactions and events, which are in part at least, of a financial character and interpreting the results thereof”. The information supplied by financial accounting is summarized in the following two statements at the end of the accounting period, generally one year. Profit and loss account showing the net profit or loss during the period. Balance Sheet showing the financial position of the firm at the point of time. OBJECTIVE OF FINANCIAL ACCOUNTING: Financial accounting is to present a true and fair view of company’s income and financial position at regular intervals of one year mainly for use by parties who are external to business. COST ACCOUNTING: Cost accounting is a branch of accounting which specializes in providing information about the detailed cost of products or services being supplied by the undertaking. Compared with financial accounting, cost accounting is relatively a recent development. It has primarily developed to meet the needs of management. Profit and loss Account of balance sheet are presented to management by the financial accountant.

A FINANCIAL STATEMENT USING RATIO ANALYSIS AT MAHINDRA AND MAHINDRA LTD

Jul 17, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

{Page 1}

INTRODUCTION

Accounting serves the purpose of providing financial information relating a business. such information

is provided to people who have interest in the organization , such as shareholders, managers, creditors,

debenture holders, bankers, tax authorities and others, broadly speaking, on the basis of type of

accounting information and the purpose for which such information is used, accounting may be divided

into three categories:

1. Financial accounting (or General accounting),

2. Cost accounting, and

3. Management accounting

FINANCIAL ACCOUNTING:

Financial accounting is mainly concerned with recording business transaction in the books of account

for the purpose presenting financial accounts to management, share holders, creditors, investors and tax

authorities, etc.

It is defined as “The art of recording, classifying and summarizing in a significant manner and in terms

of money, transactions and events, which are in part at least, of a financial character and interpreting the

results thereof”.

The information supplied by financial accounting is summarized in the following two statements at the

end of the accounting period, generally one year.

Profit and loss account showing the net profit or loss during the period.

Balance Sheet showing the financial position of the firm at the point of time.

OBJECTIVE OF FINANCIAL ACCOUNTING:

Financial accounting is to present a true and fair view of company’s income and financial position at

regular intervals of one year mainly for use by parties who are external to business.

COST ACCOUNTING:

Cost accounting is a branch of accounting which specializes in providing information about the detailed

cost of products or services being supplied by the undertaking. Compared with financial accounting, cost

accounting is relatively a recent development. It has primarily developed to meet the needs of

management. Profit and loss Account of balance sheet are presented to management by the financial

accountant.

{Page 2}

The terms ‘costing’ and ‘cost accounting’ are often used interchangeably. The chartered institute of

Management Accountants (CIMA) of UK has defined costing as, “the techniques and process of

ascertaining costs”. Thus, costing simply means cost finding by any process or technique. It consists of

principles and rules which are used for determining:

(a) The cost of manufacturing a product; e.g., motor car, furniture, chemical steel, paper etc.

(b) The cost of providing a services; e.g., electricity, transport, education, etc.

Cost accounting information is mainly for internal use i.e. management. It is not to be provided to

external parties such as shareholder, creditors, potential investors, etc. neither do they have any claim on

this information, excepting government, to whom cost information may have to be submitted.

MANAGEMENT ACCOUNTING:

Meaning and Definitions

The terms ‘management accounting’ is the modern concept of accounts as a tool of management.

It is a board term and is concerned with all such accounting information that is useful to management. In

simple words, the term management accounting is applied to the provision of accounting information for

management activities such as planning, controlling and decision making, etc.

According to the Institute of Chartered Accountants of England, “any form of accounting which

enables a business to be conducted more efficiently” may be regarded as management accounting”.

Relationship of Management Accounting to Cost Accounting and Financial Accounting:

The three types of accounting, i.e., financial accounting, cost accounting and management accounting

are closely linked. The management accounting uses the principles and practices not only of cost

accounting but also of financial accounting. Information provided by financial accounting proves

extremely useful for management accounting. For example, profit and loss account and balance sheet

become the basis of ratio analysis and comparative financial statements, etc, which are used by the

management accounting as important tools of planning and control.

{Page 3}

Financial accounting records also become basis of preparing detailed cost computation and reports. Cost

accounting is a more detailed application of financial accounting and provides detailed cost information

about products, services, departments, etc. This information is used by management accounting for

planning, controlling and decision making purposes.

Fig. 1.1 shows the evolution of management accounting and its relationship to cost accounting and

financial accounting.

Fig.1.1. Relationship of financial, cost and management accounting.

PREPARING

PROFIT & LOSS

ACCOUNT AND

BALANCE SHEET

FINANCIAL

ACCOUNTING

ANALYSING

COST FOR

CONTROL AND

MAXIMISING

EFFICIENCY

COST

ACCOUNTING

ASSISTING

MANAGEMENT

FOR PLANNING,

DECISION

MAKING AND

CONTROL

MANAGEMENT

ACCOUNTING

{Page 4}

MANAGEMENT ACCOUNTANT – THE CONTROLLER

Management accountant plays a very important role in an organization. He analyses and interprets

accounting information and meets the informational needs of management at different levels. In an

organization, a management accountant generally performs a staff function i.e. advisory role. But if he is

permitted to participate in planning and decision making, he is a part of the management team and thus

becomes a part of the line function. It is very important that status of the management accountant in the

organization is clearly defined so that the scope of his work and responsibilities are accordingly

determined.

ORIGIN

The first basic principles of management accounting emerged during the period 1400 to 1600 in the

form of standards for materials, employee productivity, job cost system and budgets. But no

standardized management accounting was in practice until 1885 when Henry Metcalf published the

‘cost manufacture’. The real growth of management accounting was in 20 th century in USA due to the

emergence of large and integrated companies such as DuPont and general motors.

In fact the growth of management accounting is because of the need to overcome the limitations of

financial and cost accounting.

LIMITATIONS OF FINANCIAL ACCOUNTING:

Financial accounting is extremely useful to different categories of users. But it also suffers from the

following limitations.

1. Shows only overall performance. Financial accounting provides information about profit, loss,

cost etc., of the collective activities of the business as a whole. It does not give data regarding

costs by departments, products, processes and sales territories, etc.

2. Historical in nature. Financial accounting is historical, since the data are summarized only at

the end of the accounting period. There is no system of computing day to day cost and also

computing pre- determined costs.

{Page 5}

3. No performance appraisal. In financial accounting, there is no system of developing norms and

standards to appraise the efficiency in the use of materials, labour and other costs by comparing

the actual performance with what should have been accomplished during a given period of time.

4. No material control system. Generally, there is no proper system of control of materials losses

which may arise in the form of obsolescence, deterioration, excessive scrap and

misappropriation, etc.

5. No labour cost control. In financial accounting, there is no system of recording loss of labour

time; i.e., idle time. Labour cost is not recorded by jobs, processes or departments and as such no

system of incentives may be easily used to compensate workers for their above – standard

performance.

CHARACTERISTICS OR NATURE OF MANAGEMENT ACCOUNTING:

It is clear from the above definitions that management accounting is concerned with accounting data that

is useful in decision making. The main characteristics of management accounting are as follows:

1. Useful in decision making. The essential aim of management accounting is to assist

management in decision making and control. It is concerned with all such information which can

prove useful to management in decision making.

2. Financial and cost accounting information. Basic accounting information useful for

management accountings derived from cost accounting records.

3. Internal use. Information provided by management accounting is exclusively for use by

management for internal use. Such information is not to be given to parties external to the

business like shareholders, creditors, banks etc.

4. Purely optional. Management accounting is a purely voluntary technique and there is no

statutory obligation. Its adoption by any firm depends upon its utility and desirability.

5. Concerned with future. As management accounting is concerned with decision making, it is

related with future because decision is taken for future course of action and not the past.

{Page 6}

CHARACTERISTICS OR NATURE OF MANAGEMENT ACCOUNTING:

It is clear from the above definitions that management accounting is accounting is concerned with

accounting data that is useful in decision making. The main characteristics of management accounting as

follows:

* Useful in decision making. The essential aim of management accounting is to assist

management in decision making and control. It is concerned with all such information which can

prove useful to management in decision making.

* Financial and cost accounting information. Basic accounting information useful for

management accountings derived from financial and cost accounting records.

* Internal use. Information provided by management accounting is exclusively for use by

management for internal use. Such information is not to be given to parties external to the

business like shareholders, creditors, banks, etc.

* Purely optional. Management accounting is a purely voluntary technique and there is no

statutory obligation. Its adoption by any firm depends upon its utility and desirability.

* Concerned with future. As management accounting is concerned with decision making, it is

related with future because decisions are taken for future course of action and not the past.

SCOPE OF MANAGEMENT ACCOUNTING:

Management accounting has a very wide scope. It includes not only financial accounting and cost

accounting but all type of internal control, internal audit, tax accounting, office services, cost control and

other methods and control procedures. Thus scope of management accounting inter alia includes the

following:

1. FINANCIAL ACCOUNTING.

Financial accounting provides basic historical data which helps management to forecast and plan

its financial activities for the future period. Thus for an effective and successful management

accounting, there should be a proper and well designed financial accounting system.

{Page 7}

2. COST ACCOUNTING:

Many of the techniques of profit planning and decision-making like marginal costing, CVP

analysis and differential cost analysis are used by the management accounting.

3. BUDGETING AND FORECASTING:

In order to plan business activities for the future, forecasting and budgeting play a very

significant role. Forecasting helps in the preparation of budgets and budgeting helps management

accountant in exercising budgetary control.

4. TAX PLANNING:

In order to take advantage of various provisions of tax laws, management accountant has to

depend upon tax accounting and planning to minimize its tax liabilities and save more funds for

the business.

5. REPORTING TO MANAGEMENT:

For effective and timely decision, there should be a system of prompt and intelligent reporting

into management both routine and special reports are prepared for submission to top

management, middle order management and operating level management depending and their

requirements.

TOOLS AND TECHNIQUES USED IN MANAGEMENT ACCOUNTING

Management accounting uses a number of tools and techniques to help management in achieving

business goals. Some of the important tools and techniques are as follows:

1. Budgeting

2. Standard costing and variance analysis.

3. Marginal costing and costing volume profit analysis.

4. Ratio analysis.

5. Comparative financial statements

6. Differential cost analysis.

{Page 8}

FINANCIAL ACCOUNTING AND MANAGEMENT ACCOUNTING-COMPARISON

Financial accounting and management accounting are two major sub – systems of accounting

information system. Both are concerned with revenues and expenses, assets and liabilities and cash

flows. Both therefore involve financial statements. But the major differences between the two arise

because they serve different audiences. The main points of difference the two are as follows:

Basis Financial Accounting Management Accounting

1. External &

internal users

Financial accounting information is

mainly intended for external users

like investors, shareholders,

creditors, govt. authorities, etc,:

Management accounting

information meant for internal

users, i.e., management.

2. Accounting

method

It is based on double entry system

for recording business transactions.

It is not based on double entry

system.

3. Statement

requirements

Under company law and tax laws,

financial accounting is obligatory to

satisfy various statutory provisions.

Management accounting

provides detailed information

about individual products,

plants, departments or any other

responsibility centre.

4. Analysis of cost

& profit

Financial accounting shows the

profit/loss of the business as a

whole. It does not show the cost &

profit for individual products,

processes or departments are.

Management accounting

provides detailed information

about individual products,

plants, departments or any other

responsibility centre.

5. Past and future

data.

It is concerned with recording

transitions which have already taken

place, i.e., it represents past or

historical records.

It is future oriented and

concentrates on what is likely to

happen in future though it may

use past data for future

projections.

{Page 9}

COST ACCOUNTING AND MANAGENT ACCOUNTING:

An examination of the meaning and definitions of cost accounting and management accounting indicates

that the distinction between the two is quit vague. Some writers even consider these two areas as

synonymous while others distinguish between the two. horngren, a renowned author on the subject, has

gone to the extent of saying, “modern cost accounting is often called management accounting. Why?

Because cost accountings look at their organization through manager’s eyes”. Thus managerial aspects

of cost accounting are inseparable from management accounting. One point on which all agree is that

these two types of accounting do not have clear cut territorial boundaries. However, distinction between

cost accounting and management accounting may be made on the following point:

BASIS COST ACCOUNTING MANAGEMENT ACCOUNTING

1. Scope Scope of cost accounting is limited

to providing cost information for

managerial uses.

Scope of management accounting is

broader than that of cost accounting

as it provides all types of

information, i.e...Cost accounting

information for managerial uses.

2. Emphasis Main emphasis is on cost

ascertainment and cost control to

ensure maximum profit.

Main emphasis is on planning

controlling and decision-making to

maximize profit.

3. Technique

employed

Various technique used by cost

accounting include standard

costing and variance analysis,

marginal costing and cost volume

profit analysis, budgetary control,

uniform costing and inter-firm

comparison, etc.

Management accounting also uses

all these techniques used in cost

accounting but in addition it also

uses techniques like ratio analysis,

funds flow statement, statistical

analysis, operations research and

certain techniques from various

branches of knowledge like

mathematics, economics, etc.,

which so ever can help

management in its tasks.

{Page 10}

LIMITATION ON MANAGEMENT ACCOUNTING

Management accounting is very useful tool of management. However, it suffers from certain limitations

as stated below:

1) Based on historical data:

Management accounting helps management in making decisions for the future but it is mainly

based on the historical data supplied by financial accounting and cost accounting. This implies

that historical data is used for making future decisions. The accuracy and dependability of such

data will leave their mark on the quality of managerial decisions.

2) Lack of wide knowledge:

The management accountant should have knowledge of not only financial and cost accounting

but also many allied subjects like economics, management, taxation, statistical and mathematical

techniques etc. lack of knowledge of these subjects on the part of management accountant limits

the quality of management accounting.

3) Complicated approach:

Management accounting provides mass of data using various accounting and non-accounting

subjects for decision making purpose. But sometimes management avoided this complicated and

lengthy course of decision making and makes decisions based on intuition. This leads to

unscientific approach to decision making.

4) Not a substitute of management:

Management accounting only provides information to management for decision making but it is

not a substitute of management and administration.

5) Costly system:

The installation of management accounting system in an organization is costly affair as it

requires a wide net-work of management information system, rules and regulations. All this

requires heavy investment and small concerns may not be able to afford it.

{Page 11}

RATIO ANALYSIS

MEANING OF FINANCIAL STATEMENT:

The term financial statements refer to two basic statements which an accounting prepares at the end of

an accounting period for a business enterprise. These are:

1. Balance sheet (or Income statement of financial position ) which reflects the assets, Liabilities

and capital as on a certain date, and

2. Profit and Loss Account (or Income Statement) which shows the results of operations i.e. profit

or loss during a certain period.

RATIO ANALYSIS:

Ratio analysis is the process of determining and interpreting numerical relationship based on financial

statements. It is the technique of interpretation of financial statements with the help of accounting ratios

derived from the balance sheet and profit and loss account.

Ratio analysis is a very important tool of financial analysis. It is the process of establishing the

significant relationship between the items of financial statement to provide a meaningful understanding

of the performance and financial position of a firm. Ratio when calculated on the Basis of accounting

information are called ‘Accounting Ratio’.

DEFINITIONS:

Kennedy and Mc Mullah. “The relationship of one to another, expressed in simple term of

mathematical is known as ratio”

According to Accountant’s Handbook by Wixom, kell and Bedford, a ratio “is an expression of the

quantitative relationship between two numbers”.

{Page 12}

Ratio analysis is very powerful and most commonly used tool of analysis and interpretation of financial

statements. It concentrates on the inter-relation among the figures appearing in the financial statements.

Ratio analysis helps to analyze the part performance of a company and to make future projections. It

allows various interested parties like management, shareholders, potential investors, creditors,

government and other analysts to make an evaluation of the various aspects of company’s performance

from their own point of view and interest. For example, management and shareholders may be interested

in the company’s profitability while creditors and debenture holders may be interested in solvency of the

company.

BASIS OF COMPARISON:

Trend Analysis involves comparison of a firm over a period of time, that is, present ratios are compared

with past ratios for the same firm. It indicates the direction of change in the performance –

improvement, deterioration or constancy – over the years.

Inter-firm Comparison involves comparing the ratios of a firm with those of others in the same lines of

business or for the industry as a whole. It reflects the firm’s performance in relation to its competitors.

WAYS TO INTERPRET ACCOUNTING RATIOS:

Single absolute ratio.

Group ratio.

Historical comparison.

Inter-firm comparison.

Projected ratios.

CLASSIFICATION OF RATIOS:

Analysis of Short Term Financial Position or Test of Liquidity.

Analysis of Long Term Financial Position or Test of Solvency.

Activity Ratios.

Profitability Ratios.

{Page 13}

TEST OF LIQUIDITY:

The liquidity ratios are used to test the short term solvency or liquidity position of the business.

It enables to know whether short term liabilities can be paid out of short term assets.

It indicates whether a firm has adequate working capital to carry out routine business activity.

It is a valuable aid to management in checking the efficiency with which working capital is being

employed.

It is also of importance to shareholders and long term creditors in determining to some extent the

prospects of dividend and interest payment.

IMPORTANT RATIOS IN TEST OF LIQUIDITY:

1. Current ratio.

2. Quick ratio.

3. Absolute liquid ratio.

CURRENT RATIO

It is the most widely used of all analytical devices based on the balance sheet. It establishes relationship

between total current assets and current liabilities.

Current assets

Current ratio =

Current liabilities

IDEAL RATIO: 2:1

High ratio indicates under trading and over capitalization.

Low ratio indicates over trading and under capitalization.

ABSOLUTE LIQUIDITY RATIO

This ratio establishes a relationship between absolute liquid assets to quick liabilities.

Absolute liquid assets

Absolute liquid ratio=

Quick liabilities

{Page 14}

IDEAL RATIO: 1:2

It means that if the ratio is 1:2 or more than this the concern can be taken as liquid. If the ratio is less

than the standard of 1:2, it means the concern is not liquid.

Notes: - {Quick assets = Current asset-(inventories + prepaid expenses)

Quick Liabilities = Current liabilities – Bank overdraft

Absolute liquid assets include cash in hand, cash at bank, marketable securities, Temporary

investments.}

II. TEST OF SOLVENCY

Solvency indicates that position of an enterprise where it is capable of meeting long term

obligations.

When an organization's assets are more than its liabilities is known as solvent organization.

Long term solvency ratios denote the ability of the organization to repay the loan and interest.

IMPORTANT RATIOS IN TEST OF SOLVENCY:

Debt-equity ratio.

Proprietary ratio.

Solvency ratio.

Fixed assets to net worth ratio.

Current assets to net worth ratio.

Current liabilities to net worth ratio.

Capital gearing ratio.

Fixed assets ratio

Debt servicing ratio.

Dividend coverage ratio.

{Page 15}

DEBT EQUITY RATIO:

It is calculated to measure the relative claims of outsiders and the owners against the firm’s assets. This

ratio indicates the relationship between the outsider’s funds and the shareholders’ funds.

Outsider’s funds Debt equity ratio=

Shareholders’ funds

IDEAL RATIO: 2:1;

It means for every 2 shares there is 1 debt. If the debt is less than 2 times the equity, it means the

creditors are relatively less and the financial structure is sound. If the debt is more than 2 times the

equity, the state of long term creditors are more and indicate weak financial structure.

Notes: - {Components of Debt Equity Ratio Outsider’s funds include all debts/liabilities to outsiders,

whether long term or short term or whether in the form of debentures, bonds, mortgages or bills.

Shareholders’ funds consists of equity share capital, preference share capital, capital

reserves, revenue reserves and reserves representing accumulated profits and surpluses like

reserve for contingencies sinking funds. The accumulated losses and deferred expenses, if any

should be deducted from the total to find out shareholders’ funds, it is called net worth and the

ratio may be termed as debt to net worth ratio. }

PROPRIETARY RATIO OR NET WORTH RATIO:

It establishes relationship between the proprietors fund or shareholders funds and the total assets

Proprietary funds Capital employed

Proprietary ratio = or

Total assets Total liabilities

{Page 16}

IDEAL RATIO: 0.5:1

Higher the ratio betters the long term solvency (financial) position of the company. This ratio indicates

the extent to which the assets of the company can be lost without affecting the interest of the creditors of

the company

Notes:-

{Components of Proprietary Ratio: Shareholders’ funds or Proprietary funds are equity share

capital, preference share capital, undistributed profits, reserves and surpluses. Out of this amount

accumulated losses should be deducted. Total assets on other hand denote total resources of the

concern.}

SOLVENCY RATIO:

It expresses the relationship between total assets and total liabilities of a business. This ratio is a small

variant of equity ratio and can be simply calculated as 100-equity ratio

Total assets

Solvency ratio=

Total liabilities

No standard ratio is fixed in this regard. It may be compared with similar, such organizations to evaluate

the solvency position. Higher the solvency ratio, the stronger is its financial position and vice-versa.

FIXED ASSETS TO NET WORTH:

It is obtained by dividing the depreciated book value of fixed assets by the amount of proprietor’s funds.

Net fixed assets

Fixed assets to net worth ratio=

Net worth

{Page 17}

IDEAL RATIO: 0.75:1

A higher ratio, say, 100% means that there are no outside liabilities and all the funds employed are those

of shareholders. In such a case the return to shareholders would be lower rate of dividend and this is also

a sign of over capitalization.

This ratio shows the extent to which ownership funds are sunk into assets with relatively low turnover.

When the amount of proprietor's funds exceed the value of fixed assets, a part of the net working capital

is provided by the shareholders, provided there are no other non-current assets, and when proprietor’s

funds are less than the fixed assets, creditors obligation have been used to finance a part of fixed assets.

The Yardstick for this measure is 65% for industrial undertakings.

CURRENT ASSETS TO NET WORTH RATIO:

It is obtained by dividing the value of current assets by the amount of proprietor’s funds. The purpose of

this ratio is to show the percentage of proprietor’s fund investment in current assets.

Current assets

Current assets to net worth ratio=

Proprietor’s fund

A higher proportion of current assets to proprietor’s fund, as compared with the proportion of fixed

assets to proprietor’s funds are advocated, as it is an indicator of the financial strength of the business,

depending on the nature of the business there may be different ratios for different firms. This ratio must

be read along with the results of fixed assets to proprietor’s funds ratio.

CURRENT LIABILITIES TO NET WORTH:

It is expressed as a proportion and is obtained by dividing current liabilities by proprietor's fund.

Current liabilities

Current liabilities to net worth ratio = Net worth

{Page 18}

IDEAL RATIO: 1:3

This ratio indicates the relative contribution of short term creditors and owners to the capital of an

enterprise. If the ratio is high, it means it is difficult to obtain long term funds by the business.

CAPITAL GEARING RATIO:

It expresses the relationship between equity capital and fixed interest bearing securities and fixed

dividend bearing shares.

Fixed interest bearing securities + fixed dividend bearing shares CGR =

Equity shareholders funds

COMPONENTS OF FIXED INTEREST BEARING SECURITIES

COMPONENTS OF EQUITY SHAREHOLDERS FUNDS

Debentures

Long-term loans Long-term fixed deposits

Equity share capital

Accumulated reserves & profits Less losses and fictitious assets

INTERPRETATION OF CAPITAL GEARING RATIO:

* When fixed interest bearing securities and fixed dividend bearing shares are higher than equity

shareholders funds, the company is said to be ‘highly geared’.

* Where the fixed interest hearing securities and fixed dividend bearing shares share equal to

equity share capital it is said to be ‘evenly geared’.

* When the fixed interest bearing securities and fixed dividend bearing shares are lower than

equity share capital it is said to be ‘low geared’.

* If capital gearing is high, further rising of long term loans may be difficult and issue of equity

shares may be attractive and vice-versa.

{Page 19}

FIXED ASSETS RATIO:

It establishes the relationship between fixed assets and capital employed

Fixed assets

Fixed assets ratio=

Capital employed

IDEAL RATIO: 0.67:1

This ratio enables to know how fixed assets are financed i.e. by use of short term funds or by long term

funds. This ratio should not be more than 1.

FIXED CHARGES COVER OR DEBT SERVICE RATIO:

This ratio is determined by dividing net profit by fixed interest charges.

Net profit before deduction of interest and income tax

Debt service ratio =

Fixed interest charges

IDEAL RATIO: 6 OR 7 TIMES;

If the ratio is high it means there is higher margin of safety for the long term lenders and as such it is not

difficult for the business to obtain further long term funds and vice-versa.

This ratio indicates the financial ability of the enterprise to meet interest payment out of current earnings

DIVIDEND COVER RATIO:

It is the ratio between disposable profit and dividend. Disposable profit refers to profit left over after

paying interest on long term borrowing and income tax.

Net profit after interest and tax

Dividend cover ratio= Dividend declared

{Page 20}

This ratio indicates the ability of the business to maintain the dividend on shares in future. If this ratio is

higher is indicates that there is sufficient amount of retained profit. Even if there is slight decrease in

profit in the future it will not affect payment of dividend in future.

III. ACTIVITY RATIO:

Activity ratios indicate the performance of an organization.

This indicates the effective utilization of the various assets of the organization.

Most of the ratio falling under this category is based on turnover and hence these ratios are called

as turnover ratios.

IMPORTANT RATIOS IN ACTIVITY RATIO:

Stock turnover ratio.

Debtor’s turnover ratio.

Creditor’s turnover ratio.

Wording capital turnover ratio.

Fixed assets turnover ratio.

Current assets turnover ratio.

Total assets turnover ratio.

Sales to net worth ratio.

STOCK TURNOVER RATIO:

This ratio establishes the relationship between the cost of goods sold during a given period and the

average sock holding during that period. It tells us as to how many times stock has turned over (sold)

during the period. Indicates operational and marketing efficiency. Helps in evaluating inventory policy

to avoid over stocking.

{Page 21}

Cost of goods sold

Inventory turnover ratio =

Average stock

Cost of goods sold = sales - gross profit

= opening stock + purchases – closing stock

Opening stock + Closing stock

Average stock =

2

INTERPRETATION OF STOCK TURNOVER RATIO:

IDEAL RATIO: 8 times; a low inventory turnover may reflect dull business, over investment in

inventory, accumulation of stock and excessive quantities of certain inventory items in relation to

immediate requirements.

A high ratio may not be accompanied by a relatively high net income as; profits may be sacrificed in

obtaining a large sales volume (unless accompanied by a larger total gross profit). It may indicate under

investment in inventories. But generally, a high stock turnover ratio means that the concern is efficient

and hence it sells its goods quickly.

DEBTOR TURNOVER RATIO:

This ratio explains the relationship of net credit sales of a firm to its book debts indicating the rate at

which cash is generated by turnover of receivables or debtors.

The purpose of this ratio is to measure the liquidity of the receivables or to find out the period over

which receivables remain uncollected.

Net credit sales

Debtor turnover ratio =

Average Debtors

{Page 22}

Opening balance + closing balance

Average debtors =

2

Debtors include bills receivables along with book debts

Notes: - {when information about opening and closing balances of trade debtors is not

Available then the debtor turnover ratio can be calculated by dividing the total

Sales by the balances of debtors. Debtor turnover ratio = total sales/debtors}

AVERAGE COLLECTION PERIOD:

The average collection period represents the average number of days for which a firm has to wait before

its receivables are converted into cash

Number of working day in year

Average collection period =

Debtor turnover ratio

INTERPRETATION OF DEBTOR TURNOVER RATIO:

Ideal ratio: 10 to 12 times; debt collection period of 30 to 36 days is considered ideal.

A high debtor turnover ratio or low collection period is indicative of sound management policy.

The amount of trade debtors at the end of period should not exceed a reasonable proportion of

net sales. Larger the trade debtors greater the expenses of collection.

CREDITORS TURNOVER RATIO:

This ratio indicates the number of times the creditors are paid in a year. It is useful for creditors in

finding out how much time the firm is likely to take in repaying its trade creditors.

Net credit purchases

Creditors turnover ratio =

Average creditors

{Page 23}

Opening balance + closing balance

Average creditors =

2

Number of working days

Average payment period = Creditor’s turnover ratio

Notes: - {if information about credit purchases is not available, total purchases may be

Taken, if opening and closing balances of creditors are not given the balances of

Creditors may be taken. Trade creditors include sundry creditors and bills

Payable.}

INTERPRETATION OF CREDITOR TURNOVER RATIO:

Ideal ratio: 12 times; debt payment period of 30 days is considered ideal.

Very less creditor’s turnover ratio or a high debt payment period may indicate the firm’s inability

in meeting its obligation in time.

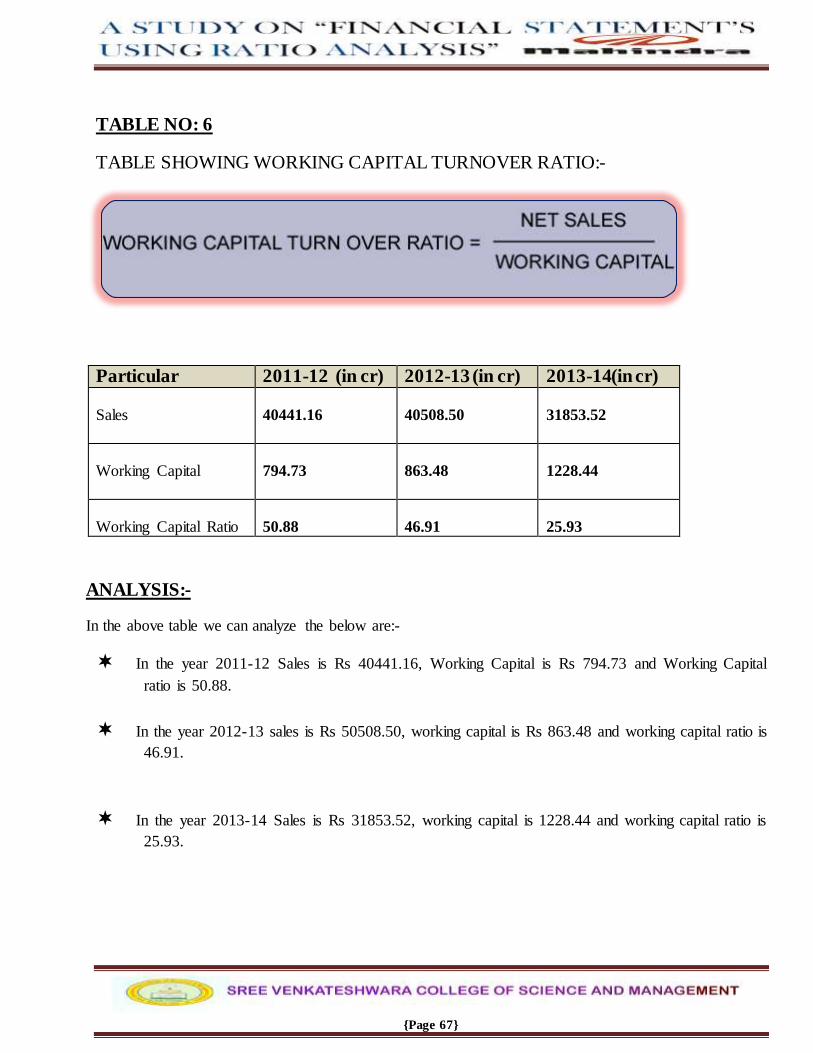

WORKING CAPITAL TURNOVER RATIO:

This ratio indicates the number of times the working capital is turned over in the course of the year.

Measures efficiency in the working capital usage. It establishes relationship between cost of sales and

working capital.

Cost of sales

Working capital turnover ratio = Average working capital

Opening + closing working capital

Average working capital = 2

If cost of sales is not given, then sales can be used. If opening working capital is not disclosed then

working capital at the yearend will be used.

Working capital turnover ratio= cost of sales (sales)/net working capital.

{Page 24}

INTERPRETATION OF WORKING CAPITAL TURNOVER RATIO:

* A higher ratio indicates efficient utilization of working capital and a low ratio indicates

inefficient utilization of working capital.

* But a very high ratio is not a good situation for any firm and hence care must be taken while

interpreting the ratio.

FIXED ASSETS TURNOVER RATIO:

This ratio establishes a relationship between fixed assets and sales.

Net sales Fixed assets turnover ratio =

Fixed assets

Ideal ratio: 5 times

A high ratio indicates better utilization of fixed assets.

A low ratio indicates under utilization of fixed assets.

TOTAL ASSET TURNOVER RATIO:

This ratio establishes a relationship between total assets and sales. This ratio enables to know the

efficient utilization of total assets of a business.

Net sales

Total assets turnover ratio = Total assets

Ideal ratio: 2 times

High ratio indicates efficient utilization and ratio less than 2 indicates under utilization.

IV. PROFITABILITY RATIO: Profitability ratios indicate the profit earning capacity of a business.

Profitability ratios are calculated either in relation to sales or in relation to investments.

Profitability ratios can be classified into two categories.

{Page 25}

a) General Profitability Ratios.

b) Overall Profitability Ratios.

GENERAL PROFITABILITY RATIOS:

Gross profit ratio.

Net profit ratio.

Operating ratio.

Operating profit ratio.

Expense ratio.

GROSS PROFIT RATIO:

It expresses the relationship of gross profit to net sales and is expressed in terms of percentage. This

ratio is a tool that indicates the degree to which selling price of goods per unit may decline without

resulting in losses.

Gross profit

Gross profit ratio = X 100

Net sales

A low gross profit ratio may indicate unfavorable purchasing; the instability of management to develop

sales volume thereby making it impossible to buy goods in large volume. Higher the gross profit ratio

betters the results.

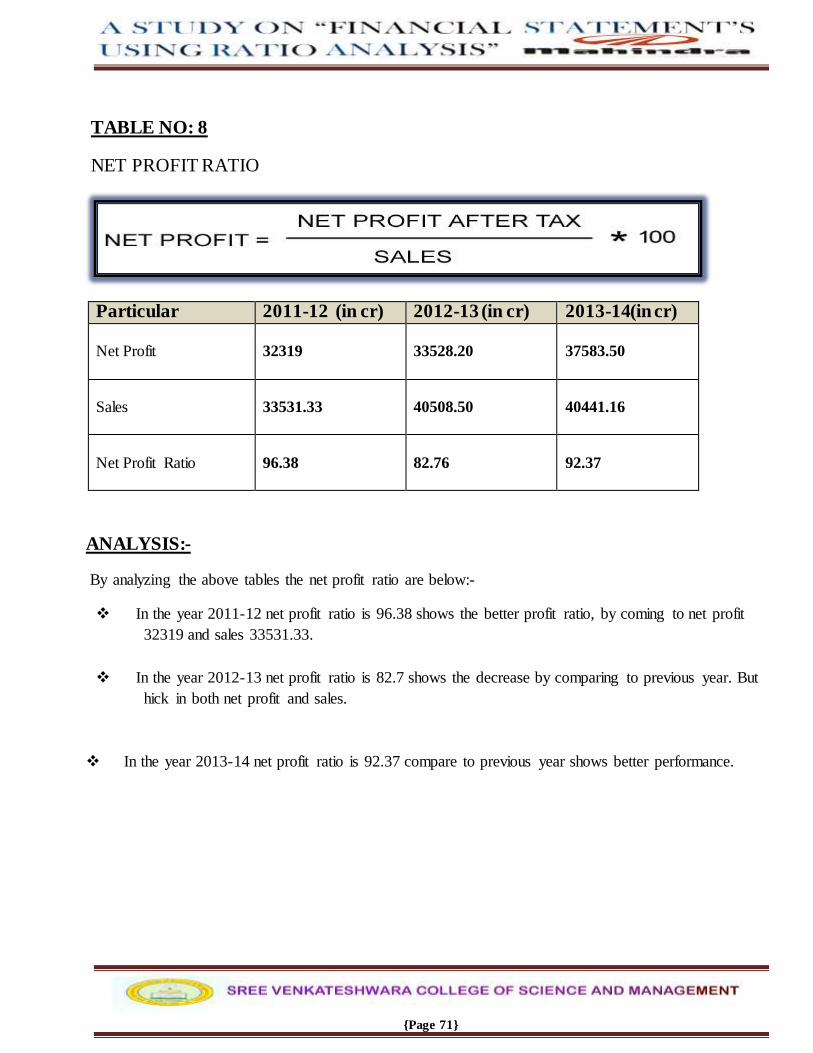

NET PROFIT RATIO:

It expresses the relationship between net profits after taxes to sales. Measure of overall profitability

useful to proprietors, as it gives an idea of the efficiency as well as profitability of the business to a

limited extent.

Net profit after taxes

Net profit ratio = X 100

Net sales

Higher the ratio better is the profitability

{Page 26}

OPERATING RATIO:

This ratio establishes a relationship between cost of goods sold plus other operating expenses and net

sales. This ratio is calculated mainly to ascertain the operational efficiency of the management in their

business operations.

Cost of goods sold + operating expenses

Operating ratio =

Net sales

Higher the ratio the less favorable it is because it would leave a smaller margin to meet interest,

dividend and other corporate needs. For a manufacturing concern it is expected to touch a percentage of

75% to 85%. This ratio is partial index of overall profitability.

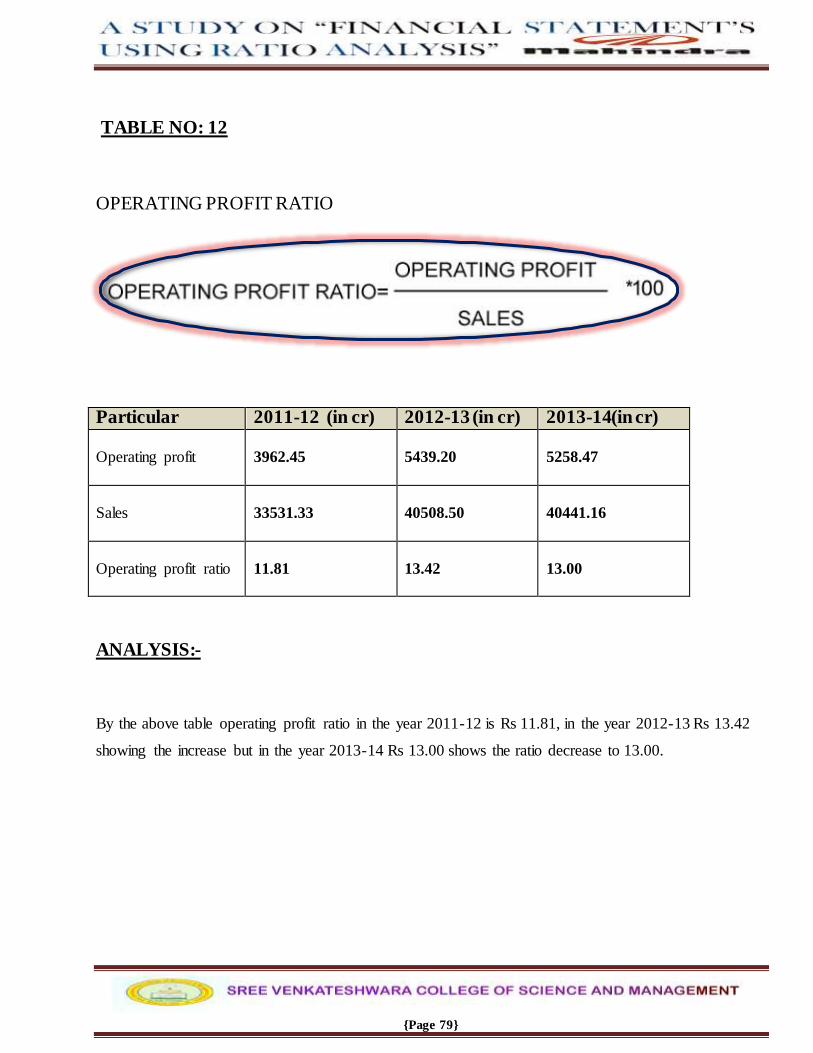

OPERATING PROFIT RATIO:

This ratio establishes the relationship between operation profit and net sales.

Operating profit

Operating profit ratio= X 100

Net sales

Operating profit ratio = 100 - operating ratio

Operating profit = Net sales – (cost of goods sold + Administrative and office expenses + selling and

distributive expenses.

EXPENSES RATIO:-

It establishes relationship between individual operation expenses and net sales revenue.

Cost of goods sold

1. Cost of goods sold ratio = X 100

Net sales

{Page 27}

Office and admin exp

2. Admin. And office exp ratio= X100

Net sales

Selling and dist. exp

3. Selling and distribution ratio= X 100

Net sales

Non operating expense

4. Non-operating expense ratio= X 100

Net sales

TEST OF OVERALL PROFITABILITY:

Return on shareholders’ investment or Net worth ratio.

Return on equity capital.

Return on capital employed.

Return on total resources.

Dividend yield ratio.

Preference dividend cover ratio.

Equity dividend cover ratio.

Price covering ratio.

Dividend payout ratio.

Earnings per share.

RETURN ON SHAREHOLDERS’ INVESTMENT:

Shareholders’ investment also called return on proprietor’s funds is the ratio of net profit to proprietor’s

funds. It is calculated by the prospective investor in the business to find out whether the investment

would be worth-making in terms of return as compared to the risk involved in the business.

Net profit (After tax and interest)

Return on shareholders’ investment= Proprietor’s funds

{Page 28}

RETURN ON SHAREHOLDERS’ INVESTMENT:

This ratio is of great importance to the present and prospective shareholders as well as the management

of the company. As this ratio reveals how well the resources of a firm are being used, higher the ratio,

better are the results. The return on shareholders’ investment should be compared with the return of

other similar firms in the same industry. The inter- firm comparison of this ratio determines whether

their investments in the firm are attractive or not as the investors would like to invest only where their

return is higher. Similarly, trend ratios can also be calculated for a number of years to get5 and idea of

the prosperity, growth of deterioration in the company’s profitability and efficiency.

RETURN ON EQUITY CAPITAL:

This ratio establishes the relationship between net profit available to equity shareholders and the amount

of capital invested by them. It is used to compare the performance of company's equity capital with

those of other companies, and thus help the investor in choosing a company with higher return on equity

capital.

Net profit – preference dividend

Return on equity capital =

Equity share capital (paid up)

RETURN ON CAPITAL EMPLOYED:

This ratio is the most appropriate indicator of the earning power of the capital employed in the business.

It also acts as a pointer to the management showing the progress or deterioration in the earning capacity

and efficiency of the business.

Net profit before taxes and interest on long – term loans and

debentures

Return on capital employed=

Capital employed

{Page 29}

IDEAL RATIO: 15%

If the actual ratio is equal ratio is equal to or above 15% it indicates higher productivity of the capital

employed and vice versa

Proprietors net capital employed = fixed assets + current assets – outside liabilities (both long and short

term)

SIGNIFICANCE OF THE RATIO:

* It is a prime test of the efficiency of business. It measures not only the overall efficiency of

business but also helps in evaluating the performance of various departments.

* The owners are interested in knowing the profitability of the business in relation to amounts

invested in it. A higher percentage of return on capital employed will satisfy the owners that their

money is profitably utilized.

RETURN OF TOTAL RESOURCES:

This ratio acts as a yardstick to assess the efficiency of the efficiency of the operations of the business as

it indicates the extent to which assets employed in the business are utilized to results in net profit.

Net profit

Return on total recourses = X 100

Total assets

DIVIDEND YIELD RATIO:

It refers to the percentage or ratio of dividend paid per share to the market price per share. This ratio

throws light on the effective rate of return on investment, which potential investors may hope to earn.

Dividend paid per equity share

Dividend yield ratio =

Market price per equity share

{Page 30}

PREFERENCE DIVIDEND COVERS:

It indicates how many times the preference dividend is covered by profits after tax. This ratio measures

the margin o safety for preference shareholders. Such investors normally expect their dividend to be

covered about 3 times by profits available for dividend purpose.

Profit after tax

Preference dividend cover =

Annual program me dividend

EQUITY DIVIDEND COVERS:

This ratio indicates the number of times the dividend is covered by the amount of profit available for

equity shareholders.

Net profit after tax - prefer dividend

Equity dividend cover =

Dividend paid on equity capital

Earning per equity share

=

Dividend per equity share

Ideal ratio: 2 times; i.e. for every Rs. 100 profits available for dividend, Rs. 50 is retained in

The business and Rs. 50 is distributed. Higher the ratio higher is extent

Of retained earnings and higher is the degree of certainty that dividend

Will be repeated in future.

PRICE EARNINGS RATIO:

It shows how many times the annual earnings the present shareholders are willing to pay to get a share.

This ratio helps investors to know the effect of earnings per share on the market price of the share. This

ratio when calculated for several years can be used as term analysis for predicting future price earnings

ratios and therefore, future stock prices.

{Page 31}

Average market price per share

Price earnings ratio =

Earnings per share

DIVIDEND PAYOUT RATIO:

This ratio indicates the proportion of earnings available which equity share holders actually receive in

the form of dividend.

Dividend paid per share

Payout ratio =

Earnings per share

An investor primarily interested should invest in equity share of a company with high payout ratio. A

company having low payout ratio need not necessarily be a bad company. A company having income

may like to finance expansion out of the income, thus low payout ratio. Investor interested in stock price

appreciation may well invest in such a company though the payout ratio is low.

EARNINGS PER SHARE:

This ratio indicates the earning per equity share. It establishes the relationship between net profit

available for equity shareholders and the number of equity shares.

Net profit available for equity share holders

Earnings per share =

Number of equity shares

{Page 32}

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@

{Page 33}

RESEARCH DESIGN:-

TITLE OF THE STUDY

A study on “financial position using ratio analysis” at Mahindra & Mahindra.

INTRODUCTION OF RATIOS:

Ratio analysis is a technique of analysis and interpretation of financial position. It is the process of

establishing and interpretation various for helping in making certain decisions, however ratio analysis is

not an end in itself. It is only a mean of better understanding of financial strengths and weakened of a

firm. Calculated of mere ratio does not serve4 any purpose unless several appropriate ratios are analyses

and interpreted. There are a number of ratios which can be calculated from the information given in the

financial position, but the analysis has to select the appropriate data and calculated only a few

appropriate ratios from the same keeping in mind.

STATEMENT OF PROBLEM:

{Page 34}

In the present global scenario financial position of an organization plays an important role on its

survival. So analyzing financial position of organization has becoming a little bit of difficult to financial

analysis. Financial position of an organization can be analyzed by using compound and discounting

techniques and ratio analysis plays an vital by analyzing the financial position of an organization this

study mainly focuses on the financial position through analyzing various ratio’s.

SCOPE OF THE STUDY:

The research study covers the area of ratios analysis and the research is restricted to the coverage of ratio

analysis concept and to respected organization study covers all the aspects of ratio analysis with respect

to the organization.

NEED OF THE STUDY:

The study has significant and provide benefits to various parties whim directly or indirectly

interest with the company.

It is beneficial to management of the company by providing crystal clear picture regarding

important aspects like liquidity, leverage, activity and profitability.

The study is also beneficial to employees and offers motivation by showing how actively they

are contributing for company’s growth.

The investors who are interested in investing company’s shares will also get benefited by setting

through the study and can easily take a decision whether to invest or not to invest the company’s

share.

OBJECTIVES OF THE STUDY:-

The objectives of the recent study known about the financial strength and weakness of MAHINDRA &

MAHINDRA through financial ratio analysis.

To evaluate the performance of the company by using ratio as yard stick and to measure the

efficiency of the company.

To understand the liquidity, profitability and efficiency position of the company during the study

period.

To make comparison between the ratios by using different periods.

{Page 35}

To study the present financial system at MAHINDRA & MAHINDRA.

To analyze the capital structure of the company with help of leverage ratio.

RESEARCH METHODOLOGY:-

Research methodology is a way to systematic search pertinent information on a specific topic and solves

the research problem research. It is a scientific investigation. It may be understood as a science of

studying how research is done science of studying how research is done scientifically. Research is a

systematized effort to gain new knowledge.

There are two sources of data:-

primary data

secondary data

1. PRIMARY DATA: - This data was collected through discussion with concerned officers using

the interview schedule.

2. SECONDARY DATA: - Secondary data refers to the data that has been complied by some

agency other than the user.

SECONDARY DATA’S ARE:-

Annual report of the company

Published financial statement of the company

Financial reports of the company

Text books

TOOLS AND TECHNIQUES:-

The tools and techniques used in the study are following ratio analysis for data analysis and

interpretation.

PLAN OF ANALYSIS:-

The primary data was collected through the interview schedule. This data was obtained to study the

procedure of the company relating to inventory and also includes various ratio analysis techniques used

by the company.

{Page 36}

The data collected secondary sources were processed and presented in the data analysis of various table

and explanations. The tables thus obtained were analyzed by calculating percentage’s, ratio’s and they

are followed by graphs in respect of current assets, current liability, sales, capital, net profit, gross profit

etc and thus to draw conclusion from the analysis done.

LIMITATIONS OF THE STUDY:-

Certain information was not revealed by the organization.

A thorough discussion with officials was not possible due to their busy schedule.

A study provides an insight into financial, personal, marketing and other aspects of MAHINDRA

& MAHINDRA every study will be bound with certain limitation.

One of the factors of the study was lack of availability of sample information most of the information

has been kept confidential and as such as not assed as art of policy of company.

{Page 37}

COMPANY PROFILE

MAHINDRA & MAHINDRA

HISTORY

Mahindra & Mahindra Limited (BSE: 500520) is part of the Indian Industrial Conglomerate Mahindra

Group based in Mumbai. The company was set up in 1945 in Ludhiana as Mahindra & Mohammed by

brothers K.C. Mahindra and J.C. Mahindra along with Malik Ghulam Mohammed.

After India gained independence and Pakistan was formed; Malik Ghulam Mohammed moved to

Pakistan where he became the nation's first finance minister.

{Page 38}

Now, with the Mahindra brothers as the whole sole of the company, its name was changed to Mahindra

& Mahindra in 1948. Initially set up to manufacture general-purpose utility vehicles, Mahindra &

Mahindra (M&M) was first known for assembly under license of the iconic Willis Jeep in India.

M&M introduced Jeeps to India and in no time they established themselves as the Jeep manufacturers

of India. The company later branched out into the manufacture of light commercial vehicles (LCVs) and

agricultural tractors, rapidly growing from being a manufacturer of army vehicles and tractors to an

automobile major with a growing global market presence.

At present, M&M is the leader in the utility vehicle segment in India with its flagship UV Scorpio.

FOUNDERS

{Page 39}

J.C.MAHINDRA K.C.MAHINDRA G. MOHAMMAD

CHAIRMAN

V.CHAIRMAN M.D

In recent times the company is engaged in spreading its reach beyond its traditional markets. They

entered into the two-wheeler segment by taking over the Kinetic Motors in India. M&M also has

controlling stake in REVA Electric Car Company. M&M has also been selected as the preferred bidder

for the acquisition of South Korea's sangYong Motor Company.

M&M is one of the leading tractor brands in the world. It is also the largest manufacturer of tractors in

India with sustained market leadership of over 25 years. It designs, develops, manufactures and markets

tractors as well as farm implements. Mahindra Tractors (China) Co. Ltd. manufactures tractors for the

growing Chinese market and is a hub for tractor exports to the USA and other nations. M&M has a

100% subsidiary, Mahindra USA, which assembles products for the American market.

MILESTONES OF M&M

KESHUB MAHINDRA

ANAND MAHINDRA

{Page 40}

M&M established its business connections in the USA through Mahindra Wallace.

It started steel trading on behalf of European suppliers

M&M was converted into a public limited company on June 15, 1955.

VISION AND MISSION

VISION:

To create a fully collaborative environment in which suppliers can deliver exactly what the

company needs, when it needs it, and at a competitive cost.

“We don’t have a group-wide mission statement. Our core purpose is what makes all of us want

to get up and come to work in the morning” -Anand Mahindra

MISSION:

To create India's largest automobile and automobile-related products distribution network by

providing dealers and customers with the largest choice of unique world-class products and

services.

RECENT /CURRENT VENTURES:

Mahindra Navistar Automotives Ltd. (MNAL), the commercial vehicle joint venture between

Mahindra & Mahindra Ltd. (M&M) and Navistar Inc. of USA, unveiled its 25 tone and 31 tone

trucks for the Indian market.

Mahindra & Mahindra Ltd announced the launch of the Maxximo, the world’s first mini-truck to

be powered by a 2-cylinder CRDe engine with DOHC technology and 4 valves per cylinder.

{Page 41}

PRODUCT OF MAHINDRA AND MAINDRA

MAHINDRA BOLERO

Mahindra Bolero is one of the most successful and popular utility vehicle of the Mahindra and Mahindra

Group. The car is robust in appearance and it has been elegantly designed, keeping in mind the

conditions of the Indian roads. Mahindra Bolero is also among the best fuel-efficient cars of India as the

manufacturer has equipped it with a 2500 cc diesel engine with5- speed transmission.

MAHINDRA SCORPIO

Mahindra & Mahindra Limited launched Mahindra Scorpio as its first Sports Utility Vehicle in India in

2002.

This SUV has redefined the expectations for the design of SUVs with its sturdy looks and powerful

performance, the sophisticated interior design adds to the further glory to the appearance.

{Page 42}

PERFORMANCE OF MAHINDRA XYLO:

Under the hood of Mahindra Xylo lies a 4-cylinder turbocharged, mEagle diesel engine, which generates

a power of 112bhp @ 3800 rpm and a peak torque of 24 kgm @ 1800-3000 rpm. The powerful engine is

developed on the NEF CRDe platform and is mated to 5-gears manual transmission. The car accelerates

from rest to 60 km/h in just 5.8 seconds.

{Page 43}

MILSTONE, AWARDS AND ACCOLADES:

M&M’s 61st year was studded with a number of noteworthy achievements, prestigious prizes and

glittering awards.

DUAL HONOURS FOR CHAIRMAN MR. KESHUB MAHINDRA

Chairman, Mr. Keshub Mahindra was awarded the “Business Visionary Award 2012” instituted by the

National Institute of Industrial Engineering (NITIE), Mumbai. Chairman, Mr. Keshub Mahindra was

{Page 44}

also awarded the prestigious IBS Kolkata Lifetime Achievement Award for his ‘unparalleled

contribution to industrial growth and social and economic development of the community’.

The Institute of Chartered Financial Analysts of India’s (ICFAI) India Business School (IBS) presented

it, Kolkata, at the Strategy Summit 2013, held in Kolkata.

SLEW OF HONOURS FOR MR. ANAND MAHINDRA

Mr. Anand Mahindra, VC & MD, Mahindra Group, received a number of prestigious awards in 2012-

13, including:

The prestigious CNBC Asia Business Leader of the Year Award for the Year 2012 as well as the

CNBC TV India “Business Leader of the Year Award”.

The ‘CEO of the Year’ award at the India Brand Summit 2012 co-sponsored by Business

Standard and ITM Business School in association with Times Now and DNA newspaper.

The LMA Entrepreneur of the Year 2013 award, instituted by the Ludhiana Management

Association (LMA).

The Most Inspiring Corporate Leader of the Year’ Award by NDTV Profit

The NDTV Profit – Car & Bike Award 2014 for Automobile Man of the Year.

Mr. Anand Mahindra was also nominated as a Member of the Council of the Executive Committee of

the National Sports Development Fund (NSDF) of the Govt. of India. He was featured in the list of 50

Most Influential Indians in Business Week’s edition dated August 13, 2013

HIGHEST CRISIL RATING FOR M&M

M&M has received the highest Governance & Value Creation rating, CRISIL GVC Level - I from

CRISIL for the ability to create value for all stakeholders, while adopting sound corporate governance

practices.

DUN & BRADSTREET AMERICAN EXPRESS CORPORATE AWARDS 2012

Mahindra & Mahindra was rated as the leading Indian company in the Automobile - Tractors sector in

the ‘Dun & Bradstreet – American Express Corporate Awards 2012’. The Automobile Sector comprises

{Page 45}

of three categories – Passenger Vehicles, Commercial Vehicles and Tractors. These awards recognize

the virtues of size and growth in the awards methodology. M&M ranked No. 1 in these two segments in

the premier Dun & Bradstreet India publication, India’s Top 500 Companies 2012.

MAHINDRA RECEIVES AMITY HR EXCELLENCE AWARD:

Mahindra & Mahindra was honored with the Amity HR Excellence Award at the Fourth Amity Global

HR Summit 2013 held at the Amity International Business School, Noida. The Amity HR Excellence

Award recognized Mahindra as one the most admired companies across the global on account of its

innovative strategies for Human Resources Management and Development.

GLOBAL HR EXCELLENCE AWARD FOR M&M;

Mahindra & Mahindra won the Global HR Excellence Award for Innovative HR practices

(Manufacturing Sector), in the Asia Pacific HRM Congress, held in Mumbai. These awards recognize

organizations and individuals who have embraced change, encouraged constructive challenges and

demonstrated entrepreneurial skills in the corporate world.

{Page 46}

{Page 47}

M&M WINS BOMBAY CHAMBER GOOD CORPORATE CITIZEN AWARD

2012-13

M&M was presented with the coveted Bombay Chamber Good Corporate Citizen Award 2012-13 at a

glittering ceremony held to celebrate the Chamber’s 172nd Foundation Day on September 21, 2012.

Mr. Bharat Doshi, Executive Director, M&M Ltd. and Mr. Rajeev Dubey, Member of the Group

Management Board and Chairman, Mahindra & Mahindra CSR Council, received the award on behalf

of the company.

This Award recognizes and honors conspicuous achievement by corporate organizations by way of

service to the civic community, in addition to outstanding operational performance. It takes into account

several parameters, including Business Performance, Corporate Interests, Employee Welfare, Customer

and Stakeholder Satisfaction and Social Investment.

GOLDEN PEACOCK AWARD FOR EXCELLENCE IN CORPORATE

GOVERNANCE

Mahindra & Mahindra won the coveted Golden Peacock Award for Excellence in Corporate

Governance 2006. This award validates the company’s ‘Best-in-Class’ corporate governance practices

and reflects its transparent and ethical dealings with stakeholders across the entire value chain. It

recognizes the Management’s commitment to the highest standards of corporate conduct and its

commitment to Corporate Social Responsibility as a distinct activity that helps build commendable

social values and adds to the ethical fiber of the organization.

{Page 48}

BEST AUTOMOTIVE MANUFACTURING SUPPLY CHAIN EXCELLENCE

AWARD

Mahindra & Mahindra has been awarded as the organization with the “Best Automotive Manufacturing

Supply Chain Excellence”. The awards were presented by India Times Mindscape (Times of India

Group) along with the Business India Group at the Express, Logistics & Supply Chain Awards held in

Mumbai on September 28, 2012. A. C. Neilson is accredited with the research for the award nominees

and winners.

HIGH RANKINGS FOR MAHINDRA;

M&M was ranked second in the prestigious e Most Trusted Car Company in India study conducted by

TNS. M&M scored 127 points, just seven points below the top ranking company, according to a TNS

communiqué.

M&M was ranked 14th in The Economic Times prestigious ‘ET 500’ list of top achieving

companies in India. The company has moved up four ranks from last year. To quote from the

‘ET 500’ write-up: “M&M’s ‘art-to-part’ strategy of diversification into the auto parts value

chain and its plans for new platforms for utility vehicles and joint venture with Renault for

Logan have led to a gain in ranks.”

M&M was ranked 22nd in Business India’s annual survey of the country’s top companies -

Super 100

{Page 49}

{Page 50}

{Page 51}

INTRODUCTION TO THE TOPIC

DATA ANALYSIS AND INTERPRETATION OF FINANCIAL STATEMENT

USING RATIO ANALYSIS:

Financial statements provide summarized view of the financial position and operation of the company.

Many parties are interested in financial statement analysis to know about the financial position of the

firm. They include investors, creditors, lenders, suppliers etc it is process of establishing the meaningful

relationship between the items of financial statements. To know financial position of the company with

the help of past and present performance of the company, Items include Balance sheet, Profit and loss

account, Reports and Explanatory notes.

THE FINANCIAL ANALYSIS AND INTERPRETATION:

The significance of financial statement not lies in their preparation but in their analysis and

interpretation. Therefore analysis and interpretation is an attempt to determine the importance of

financial statements. It increases the meaning of accounting data, to provide more understanding in

Layman’s language. That helps to forecast the future earnings, ability to pay dividend policy etc. the

analysis and interpretation are 2 terms complementary to each other. For interpretation analysis is

necessary. And analysis without interpretation is meaningless.

ANALYSIS : “A process of grouping or sub grouping of a given data for the purpose of developing

some relationships among the groups either for decisions or for future prediction”

The financial analysis involves the division of facts or information on the basis of some definite plans

and to classify them into groups on the basis of some conditions and presenting them in most

convenient, simple and understandable. Therefore analysis involves the following:

{Page 52}

Study and understanding of the data presented in the financial statements.

Collection of additional information necessary for interpretation.

presentation of the financial data in logical and simple manner

Grouping and sub grouping of the items given in the financial statements on the basis of common

characteristics.

Development relationship from one group to another group for further study.

The data provided in the financial statements is re arranged and methodically classified for

comparisons. For this purpose some standards are established for comparison such as:

a. Past year figures may be used as standard for comparison with the present year

figures.

b. Future year estimated figures may be used as standards.

c. Another progressive or successful firm’s figures may be used as standards.

d. Over all industry figures may be used as standards for a comparison.

The relationship can also be established from one item of statement to the other item of statement.

E.g.Net profit or gross profit to sales, current assets to current liabilities, cost of sales to inventory, fixed

assets to capital etc.

INTERPRETATION:

To interpret means to put the meaning of data in simple and understandable manner to a layman.

Interpretation can be made only after analysis. It is the explanation of the conclusion drawn from

analysis in simple terms. The interpretation involves the following.

1) Study of relationship among the items of financial statements.

2) Study of trend over a period or actual data with the standard data used for comparison

3) Conclusions or inferences are put in simple terms for easy and more understanding for a

common man.

{Page 53}

USES OR ADVANTAGES OF ANALYSIS:

1) It helps to determine financial strength or weakness of the business firm.

2) It highlights the significant facts and relations which cannot be understood by mere reading of

financial statements.

3) It is based on some logical and scientific method and is useful for decisions.

4) It is useful to understood multidirectional relationships of the various items of financial statements.

5) It minimizes the threat of wrong or delayed decisions.

6) It helps to evaluate correctness and accuracy of the decisions.

CLASSIFICATION OF RATIOS:

Ratio may be classified as given below:

A. Classification according to the nature of accounting statement from which the ratios are

derived

1. Balance Sheet Ratios. These ratios deal with the relationship between two items appearing in

the balance sheet, e.g., current ratio, liquid ratio, debt equity ratio, etc.

2. Profit and loss Account Ratios. This type of ratios show the relationship between two items

which are in the profit and loss account itself, e.g. gross profit ratio, net profit ratio, operating

ratio, etc.

3. Combined or Composite ratios. These ratios show the relationship between items one of which

is taken from profit and loss account and the other from the balance sheet, e.g., Ratio of return on

capital employed, debtor’s turnover ratio, stock turnover ratio, capital turnover ratio, etc.

B. Classification from the point of view of financial management or objective

1. Liquidity Ratios.

2. Capital Structure Ratios.

3. Turnover Ratios.

4. Profitability Ratios.

{Page 54}

1. LIQUIDITY RATIOS (short term solvency):

‘Liquidity’ means ability of a firm to meet its current liabilities. the liquidity ratios, therefore ,try to

establish a relationship between current liabilities, which are the obligations soon becoming due and

current assets, which presumably provide the source from which these obligations will be met. In other

words, the liquidity ratios answer the question : “will the company probably be able to meet its

obligations when they become due?” the failure of a company to meet its obligations due to lack of

adequate liquidity will result in bad credit ratings, loss of creditors confidence or even in law suits

against the company. The following ratios are commonly used to indicate the liquidity of business.

IMPORTANT LIQUIDITY RATIOS:

i. Current Ratio.

ii. Quick Ratio.

iii. Absolute liquid ratio.

1. CAPITAL STRUCTURE RATIOS OR GEARING RATIOS(long term solvency):

Capital structure ratios are also known as gearing ratios or solvency ratios or leverage ratios. These are

used to analyze the long term solvency of any particular business concern. There are two aspects of long

term solvency of a firm

(i) Ability to repay the principal amount when due, and

(ii) Regular payment of interest. In other words long term creditors like debenture holders,

financial institution etc. are interested in the security of their loan amount as well as the ability

of the company to meet interest costs. They, therefore, also consider the earning capacity of

the company to know whether it will be able to pay off interest on loan amount. Liquidity

ratios discussed earlier indicate short term financial strength whereas solvency ratios judge the

ability of a firm to pay off its long term liabilities. Important solvency ratios are discussed

below :

{Page 55}

IMPORTANT CAPITAL STRUCTURE RATIOS:

1. Debt equity ratio

2. Proprietary ratio.

3. Interest coverage ratio.

4. Debt to total funds ratio.

5. Capital gearing ratio.

3. TURNOVER RATIOS (Performance ratios or Activity Ratios):

Turnover ratios are used to indicate the efficiency with which assets and resources of the firm are

being utilized. These ratios are known as turnover ratios because they indicate the speed with which

assets are being converted or turnover over into sales. These ratios, thus express the relationship

between sales and various assets. A higher turnover ratio generally indicates better use of capital

resources which in turn has a favorable effect on the profitability of the firm.

IMPORTANT TURNOVER RATIOS:

1. Inventory turnover ratio

2. Debtors turnover ratio

3. Fixed assets turnover ratio

4. Working capital turnover ratio.

5. Capital turnover ratio.

6. Creditor’s turnover ratio.

4. PROFITABILITY RATIOS:

Every business should earn sufficient profits to survive and grow over a long period of time. In

fact efficiency of a business is measured in terms of profits. Profitability ratios are calculated to

measure the efficiency of a business.

{Page 56}

Profitability of a business may be measured in two ways:

1. Profitability in relation to sales.

2. Profitability in relation to investment.

Profitability in relation to sales indicated the amount of profit per rupee of sales. Similarly, profitability

in relation to investment indicates the amount of profit per rupee invested in assets. If a company is not

able to earn a satisfactory return on investment, it will not be able to pay a reasonable return to investors

and the survival of the company may be threatened.

IMPORTANT PROFITABILITY RATIOS:

1. Gross profit ratio.

2. Net profit ratio.

3. Operating ratio and expense ratios.

4. Return on investment

5. Return on equity.

6. Earnings per share (EPS).

7. Dividend payout ratio.

8. Dividend yield ratio.

9. Price earnings ratio.

{Page 57}

DATA ANALYSIS AND INTERPRETATION

RATIO ANALYSIS:

TABLE NO: 1

TABLE SHOWS THE CURRENT RATIO

Particular 2011-12 (in cr) 2012-13 (in cr) 2013-14(in cr) Current assets

8520.77

9798.79

12803.41

Current liabilities

8566.67

9567.60

10752.30

Current Ratio

99.46

102.41

121.10

ANALYSIS:-

By analyzing the above tables the current ratio are below:-

In the year 2011-12 Current ratio is 99.46, current assets is Rs 8520.77 and current liabilities is

Rs 8566.67.

In the year 2012-13 Current ratio is 102.41, current assets is Rs 9798.79 and current liabilities is

Rs 9567.60.

In the year 2013-14 Current ratio is 121.10, current assets is Rs 12803.41 and current liabilities is

Rs 10752.30.

{Page 58}

GRAPH: 1

GRAPH SHOWS THE CURRENT RATIO

INTERPRETATION:-

By interpreting above chart that in 2013-14 shows the good value of current ratio by comparing to

previous year .one thing we can comment is year by year shows increase in current ratio.

0

2000

4000

6000

8000

10000

12000

14000

current assets current liabilities current ratio

CURRENT RATIO

2011-12 2012-13 2013-14

{Page 59}

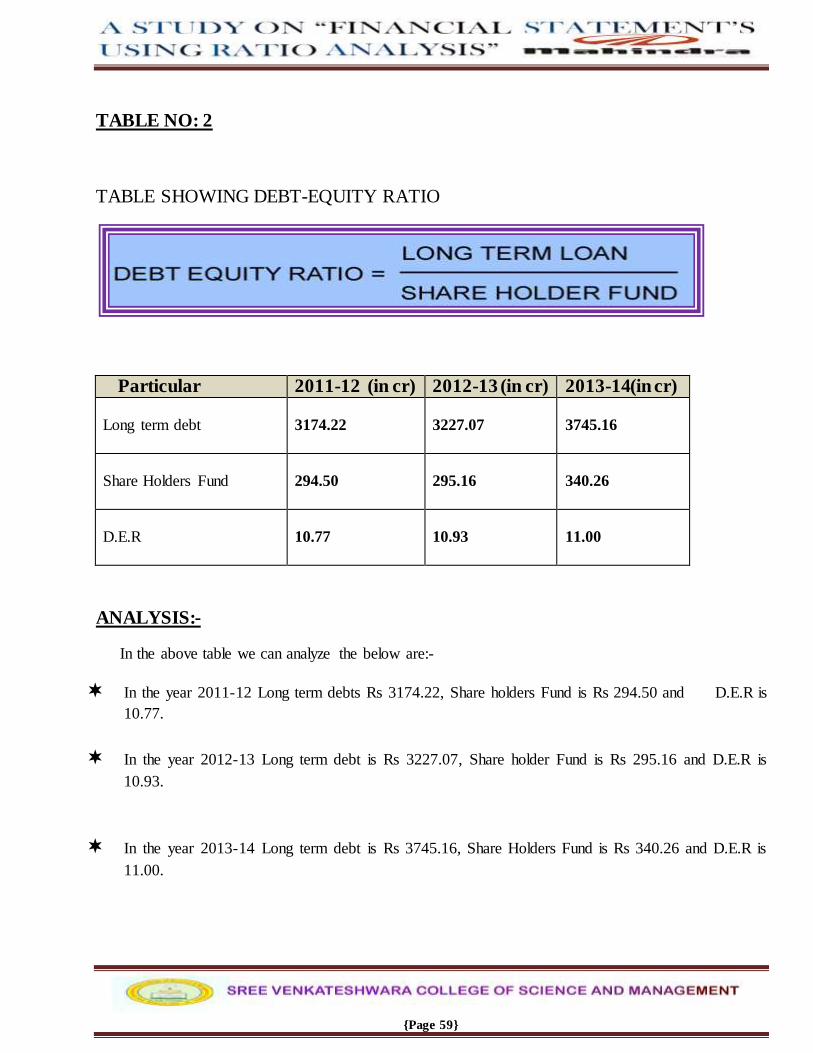

TABLE NO: 2

TABLE SHOWING DEBT-EQUITY RATIO

Particular 2011-12 (in cr) 2012-13 (in cr) 2013-14(in cr) Long term debt

3174.22

3227.07

3745.16

Share Holders Fund

294.50

295.16

340.26

D.E.R

10.77

10.93

11.00

ANALYSIS:-

In the above table we can analyze the below are:-

In the year 2011-12 Long term debts Rs 3174.22, Share holders Fund is Rs 294.50 and D.E.R is

10.77.

In the year 2012-13 Long term debt is Rs 3227.07, Share holder Fund is Rs 295.16 and D.E.R is

10.93.

In the year 2013-14 Long term debt is Rs 3745.16, Share Holders Fund is Rs 340.26 and D.E.R is

11.00.

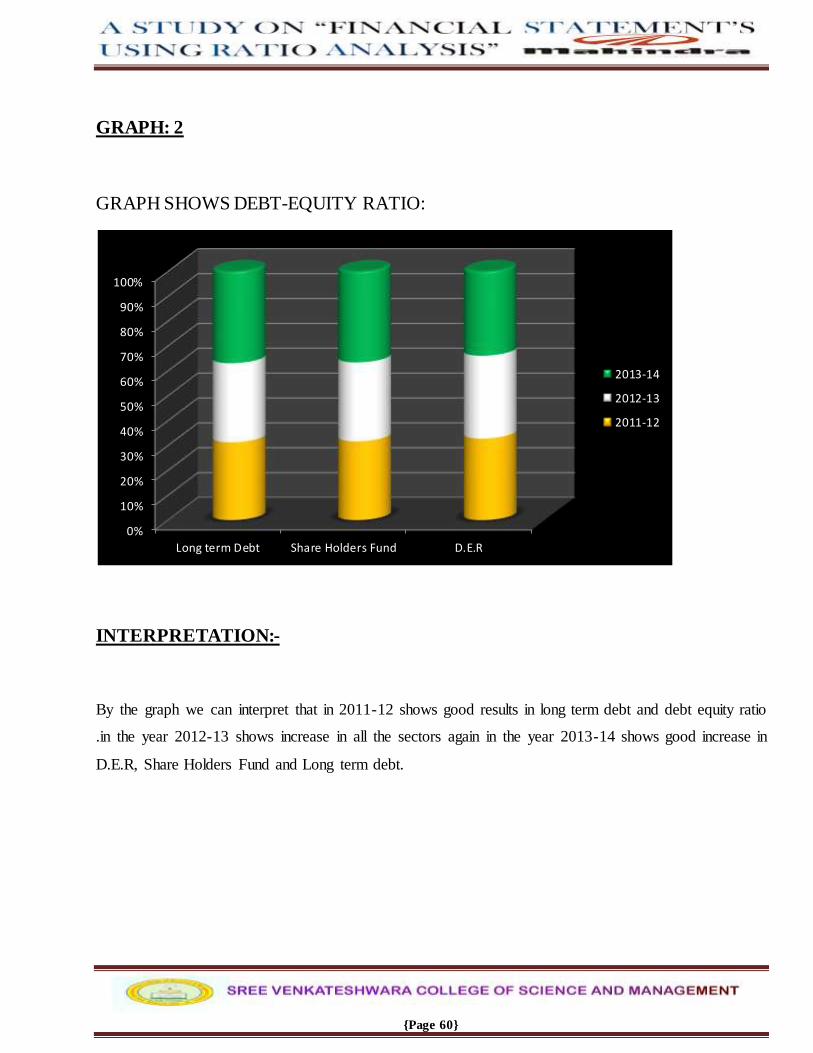

{Page 60}

GRAPH: 2

GRAPH SHOWS DEBT-EQUITY RATIO:

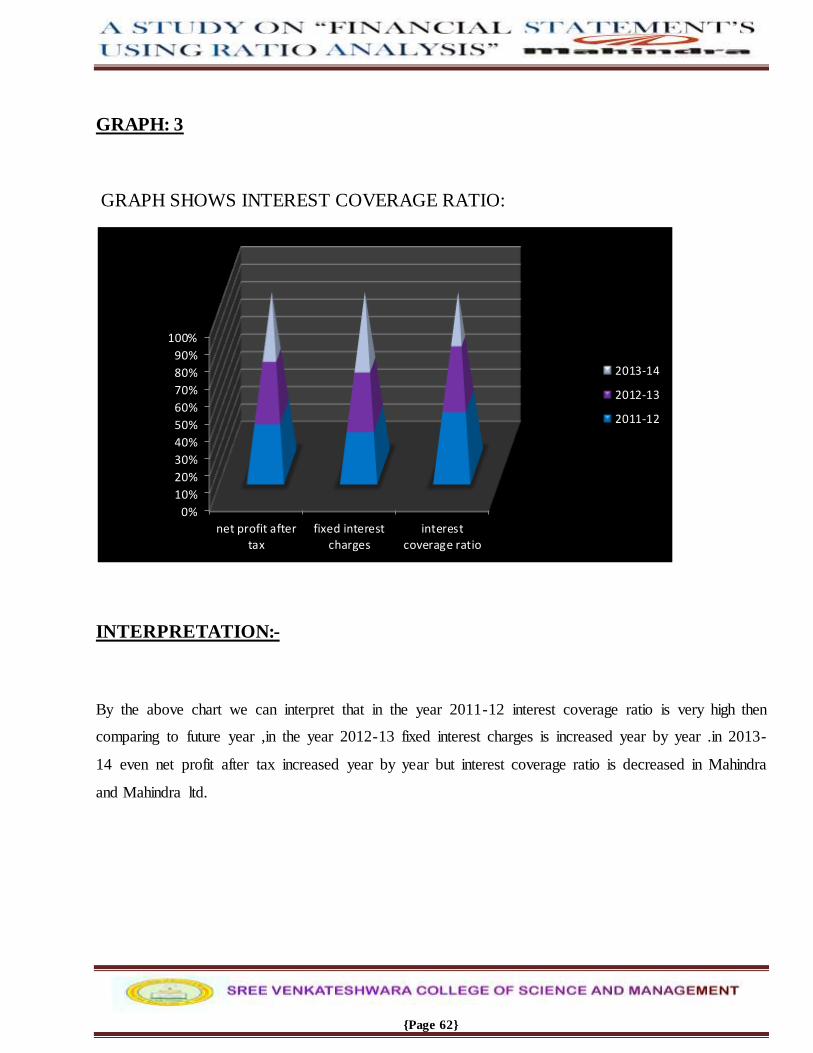

INTERPRETATION:-