IRA Compliance The material used in this text has been drawn from sources believed to be reliable. Every effort has been made to ensure the accuracy of the material, but the accuracy of this information is not guaranteed. The forms and laws are often changed without prior notice from the government. The IRA Compliance manual is sold with the understanding that the publisher and the editor are not engaging in the practice of law or accounting. April 2018 – The text is designed to address most IRA compliance issues. However, it may occasionally be necessary to refer to a more comprehensive text or other source to answer some questions. If you are unsure of an answer, consult a competent professional. #909 (V.2018.2) Ascensus ® and the Ascensus logo are registered trademarks of Ascensus, LLC. Copyright © 2018 Ascensus, LLC. All Rights Reserved. This material may not be reproduced in whole or in part in any form or by any means without written permission from the publisher. Copyright is not claimed on any material from official U.S. government sources. Printed in the United States of America. The IRA Compliance manual is updated regularly to incorporate new guidance issued throughout the year. For information on new guidance as it is released, visit www.ascensus.com or follow us on LinkedIn at www.linkedin.com/company/ascensus and Twitter @AscensusInc.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

IRA Compliance

The material used in this text has been drawn from sources believed to be reliable. Every effort has been made to ensure the accuracy of the material, but the accuracy of this information is not guaranteed. The forms and laws are often changed without prior notice from the govern ment. The IRA Compliance manual is sold with the understanding that the publisher and the editor are not engaging in the practice of law or accounting.

April 2018 – The text is designed to address most IRA compliance issues. However, it may occasionally be necessary to refer to a more comprehensive text or other source to answer some questions. If you are unsure of an answer, consult a competent professional.

#909 (V.2018.2)Ascensus® and the Ascensus logo are registered trademarks of Ascensus, LLC. Copyright © 2018 Ascensus, LLC. All Rights Reserved.

This material may not be reproduced in whole or in part in any form or by any means without written permission from the publisher.

Copyright is not claimed on any material from official U.S. government sources.

Printed in the United States of America.

The IRA Compliance manual is updated regularly to incorporate new guidance issued throughout the year.

For information on new guidance as it is released, visit www.ascensus.com or follow us on LinkedIn at www.linkedin.com/company/ascensus and Twitter @AscensusInc.

Table of Contents • i

Table of Contents

Chapter 1Origins of ComplianceIRA Compliance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1Financial Organization Penalties . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .3IRA Owner Penalty Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .5Financial Organization Responsibilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .6IRA Owner Responsibilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .8

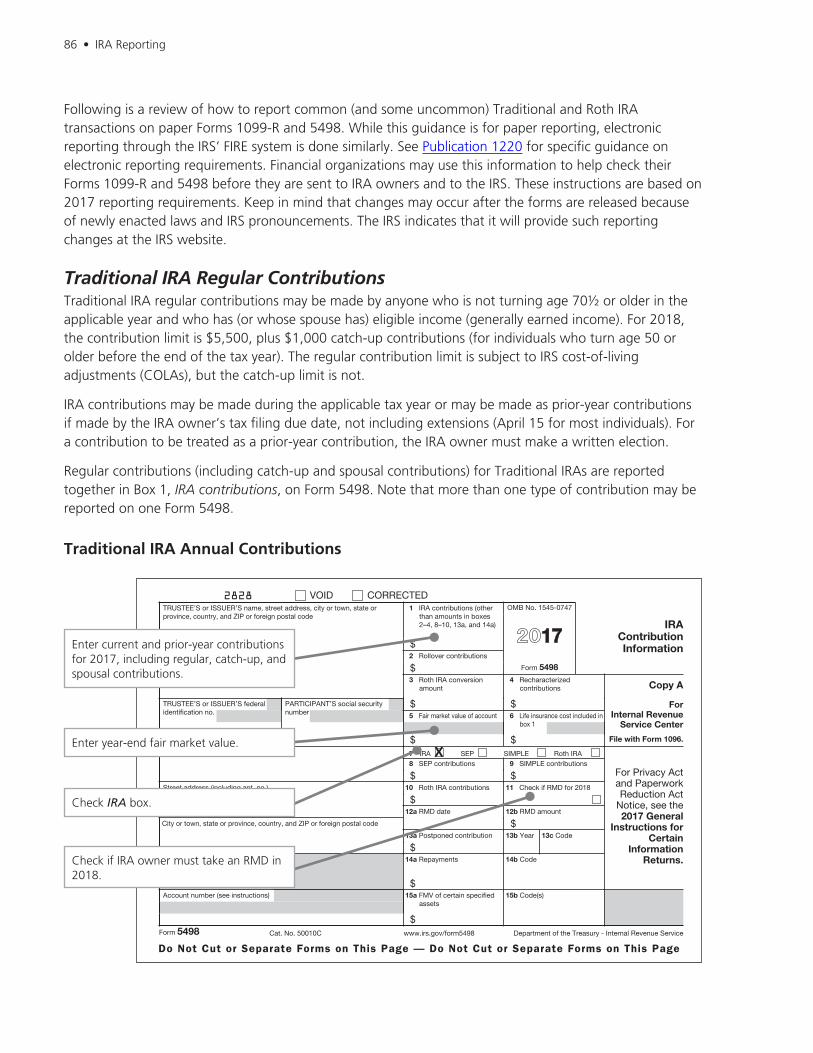

Chapter 2Opening an IRAOverview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9Trustees, Custodians, and Issuers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9IRA Opening Documents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .12Plan Agreement Contents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .14IRA Disclosure Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .18Customer Identification Program Requirements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .21Plan Agreement and Disclosure Statement Amendments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .23Beneficiary Designations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .41IRA Contribution Information. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .43IRA Opening Documents Log Sheet . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .43

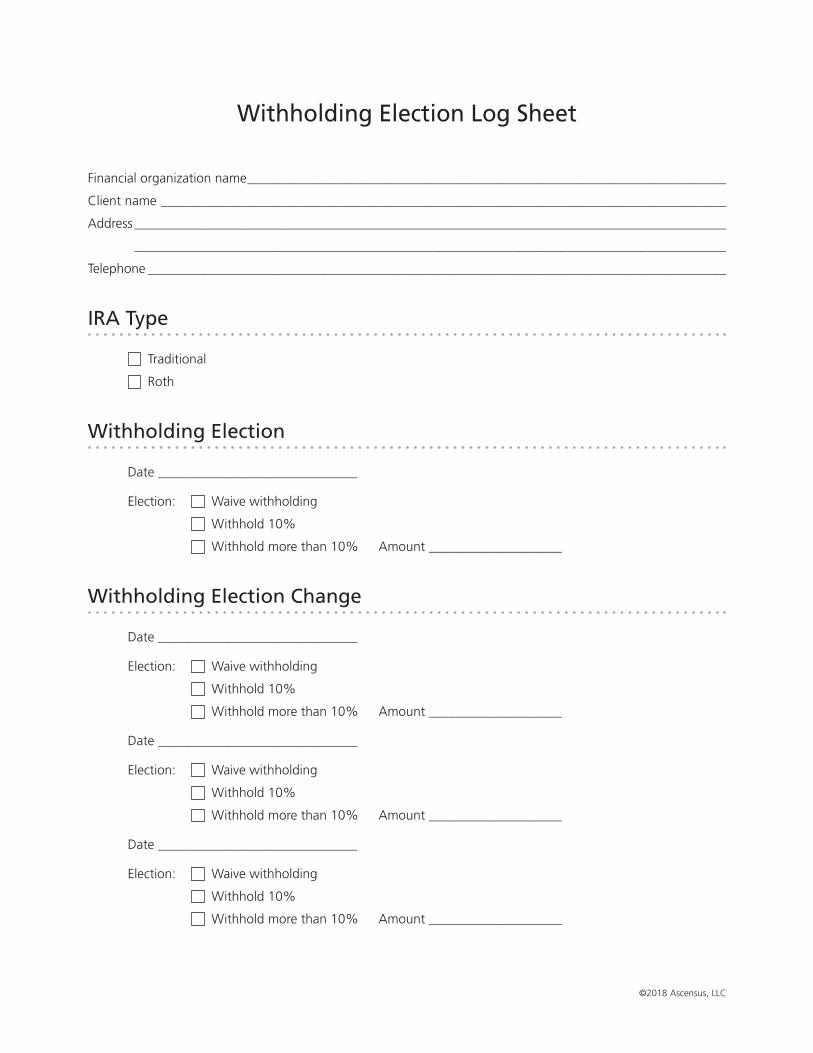

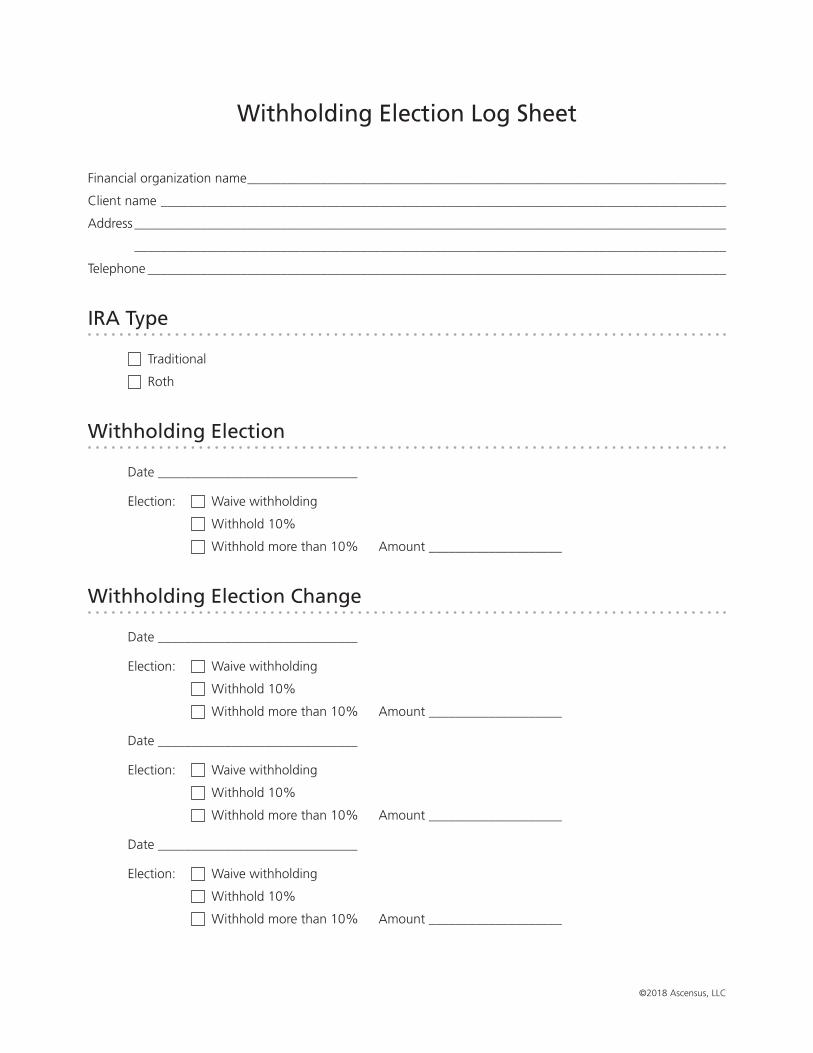

Chapter 3IRA WithholdingTraditional and Roth IRA Withholding . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .47Liability for Withholding. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .48Withholding for U.S. Citizens and Resident Aliens . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .48Withholding for Nonresident Aliens . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .57Withholding for Expatriates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .61Depositing and Reporting Withholding . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .62State Withholding . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .65Withholding Election Log Sheet . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .67

ii • Table of Contents

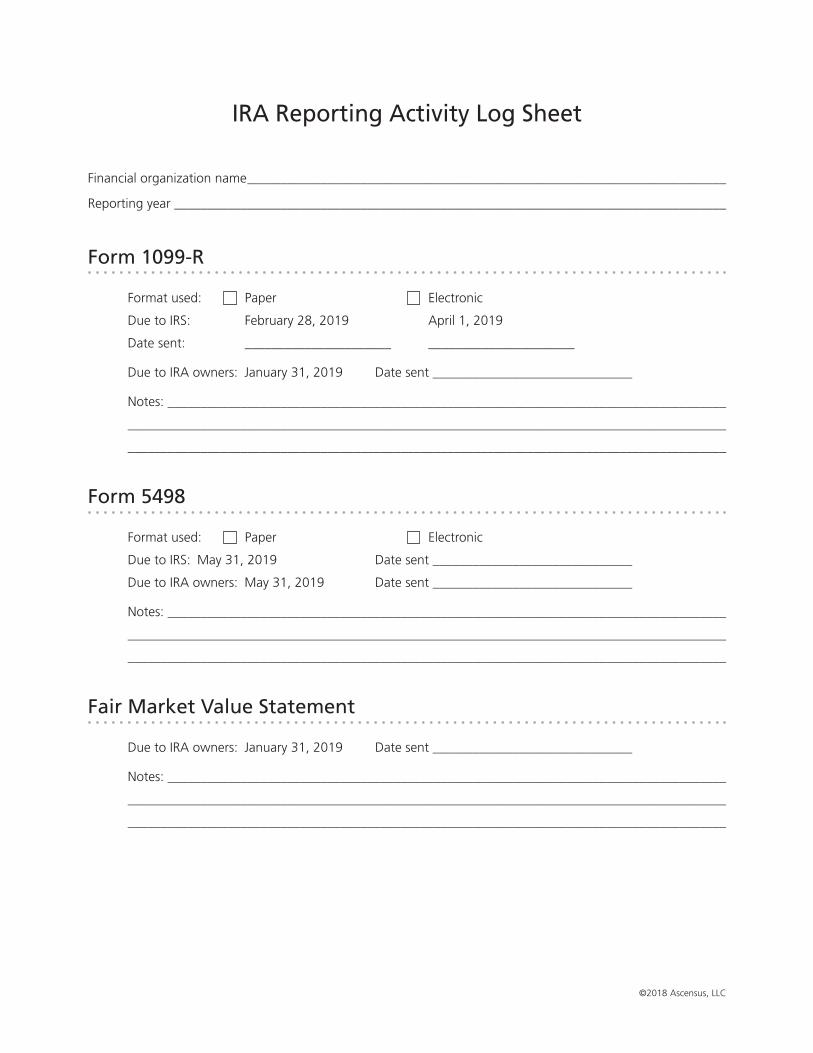

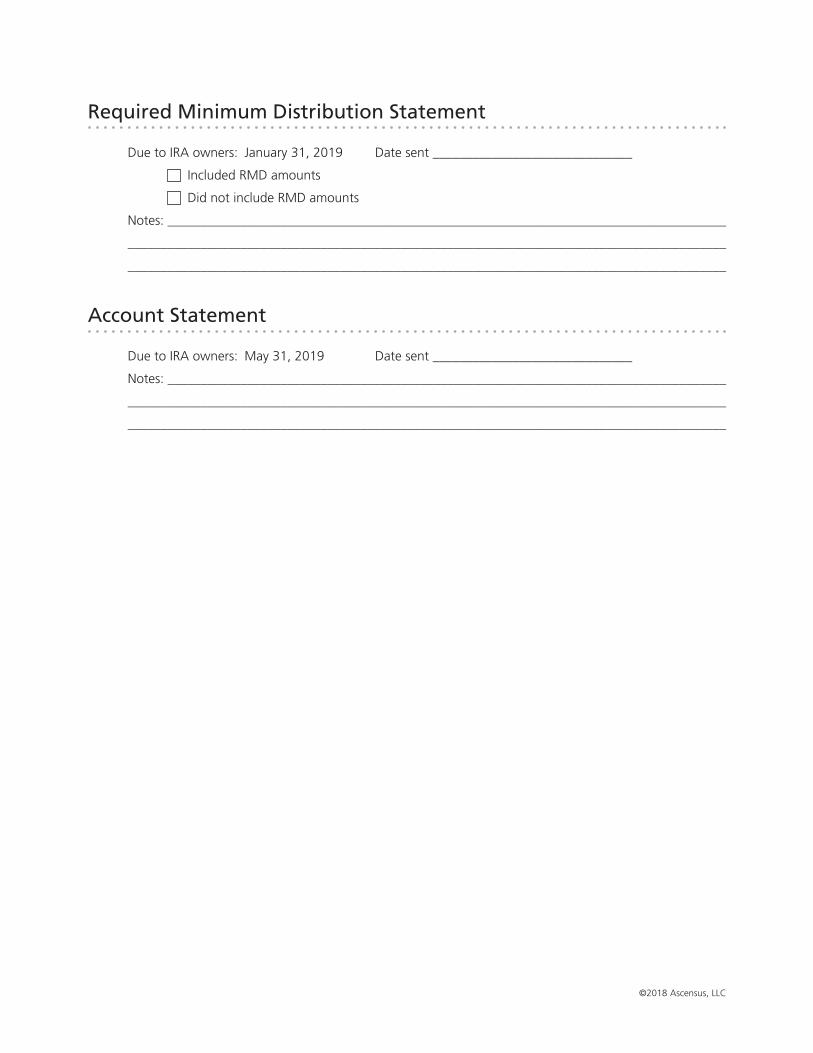

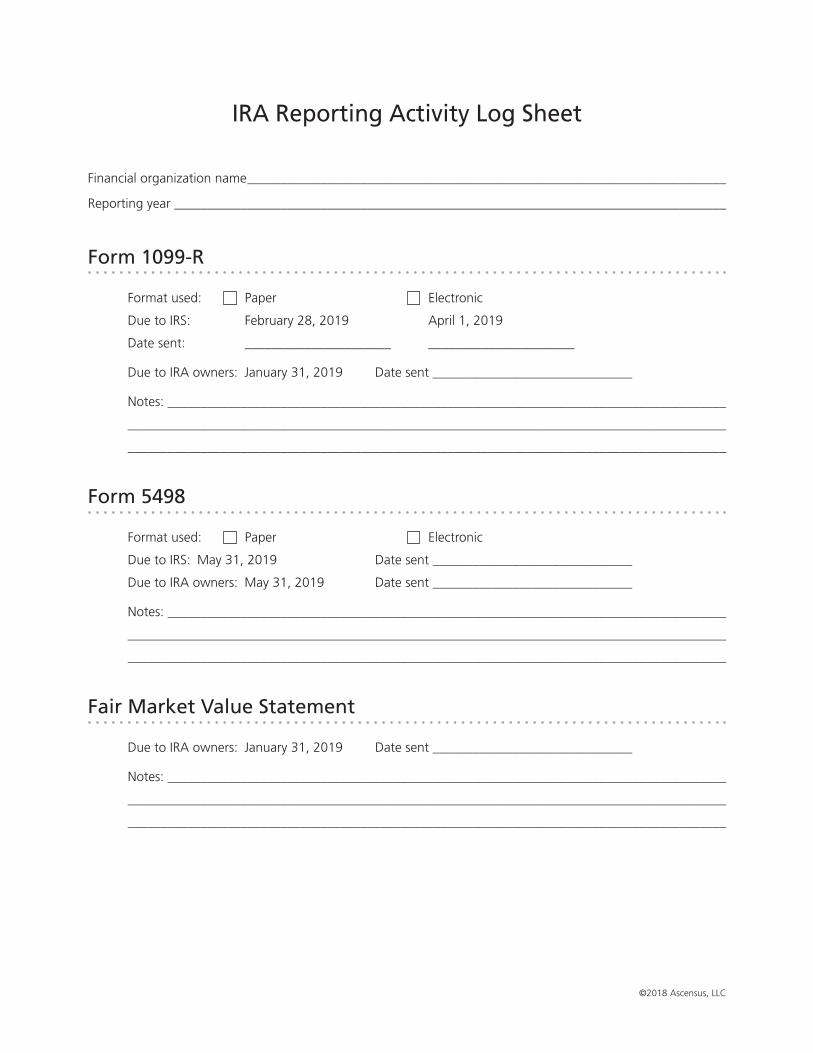

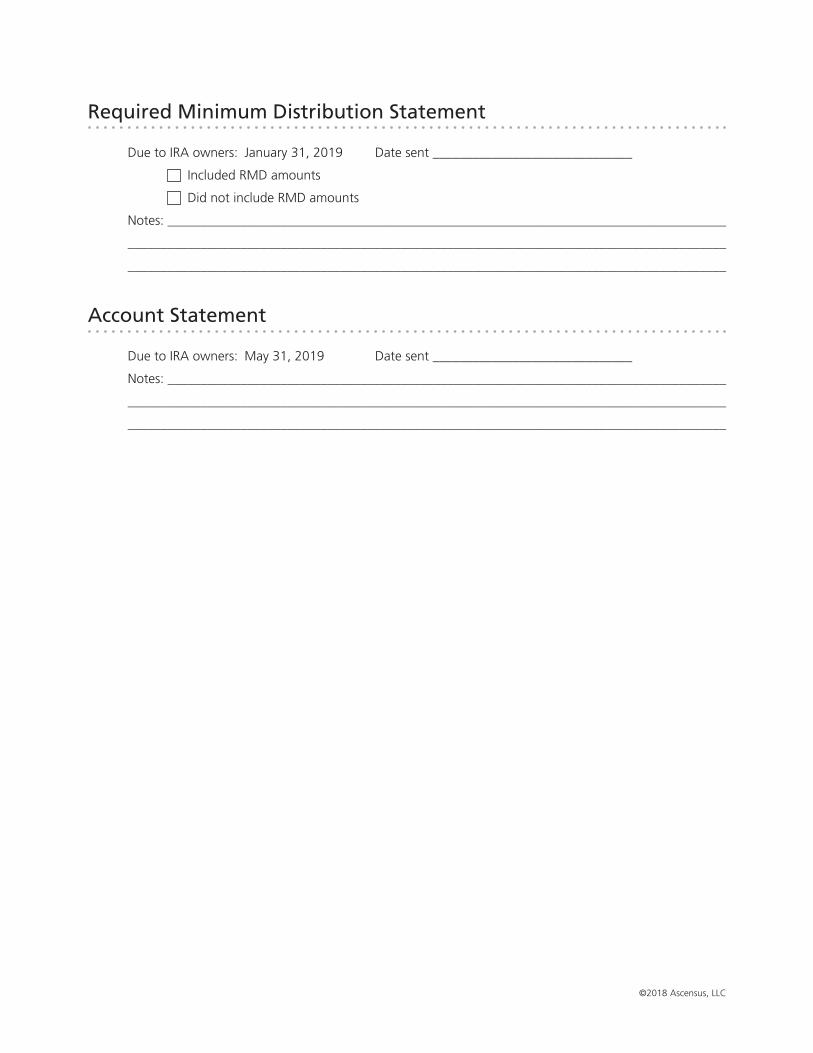

Chapter 4IRA ReportingIRA Reporting Requirements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .69Filing IRS Information Returns . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .71Form 5498 Contribution Reporting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .79Form 1099-R Distribution Reporting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .81IRA Contributions and Distributions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .85IRA-to-IRA Transfers and Rollovers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .94Retirement Plan Rollovers. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .99Recharacterizations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .103Conversions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .106Excess Contributions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .109Military and Disaster-Related Contributions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .115Endowment Contract IRAs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .120IRA Revocations or Account Closures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .121Mergers and Acquisitions. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .122Reporting Corrections . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .123Fair Market Value Statements. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .130Account Statements. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .131Required Minimum Distribution Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .133IRA Reporting Activity Log Sheet . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .134

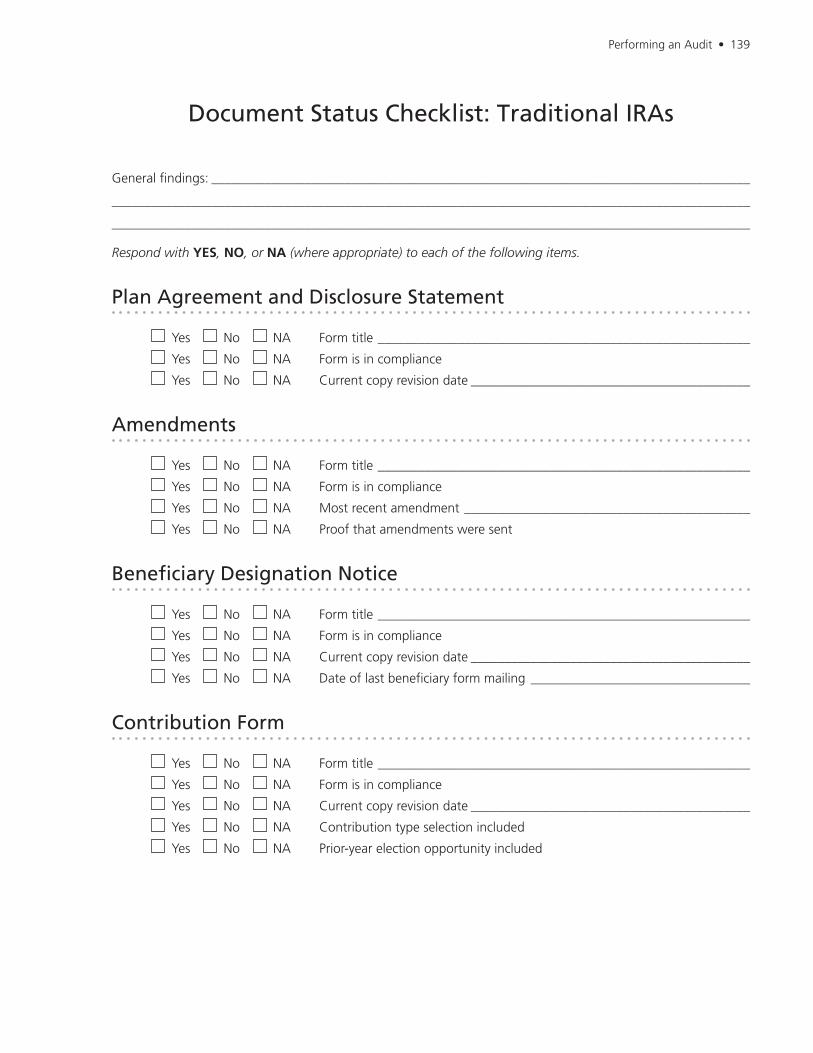

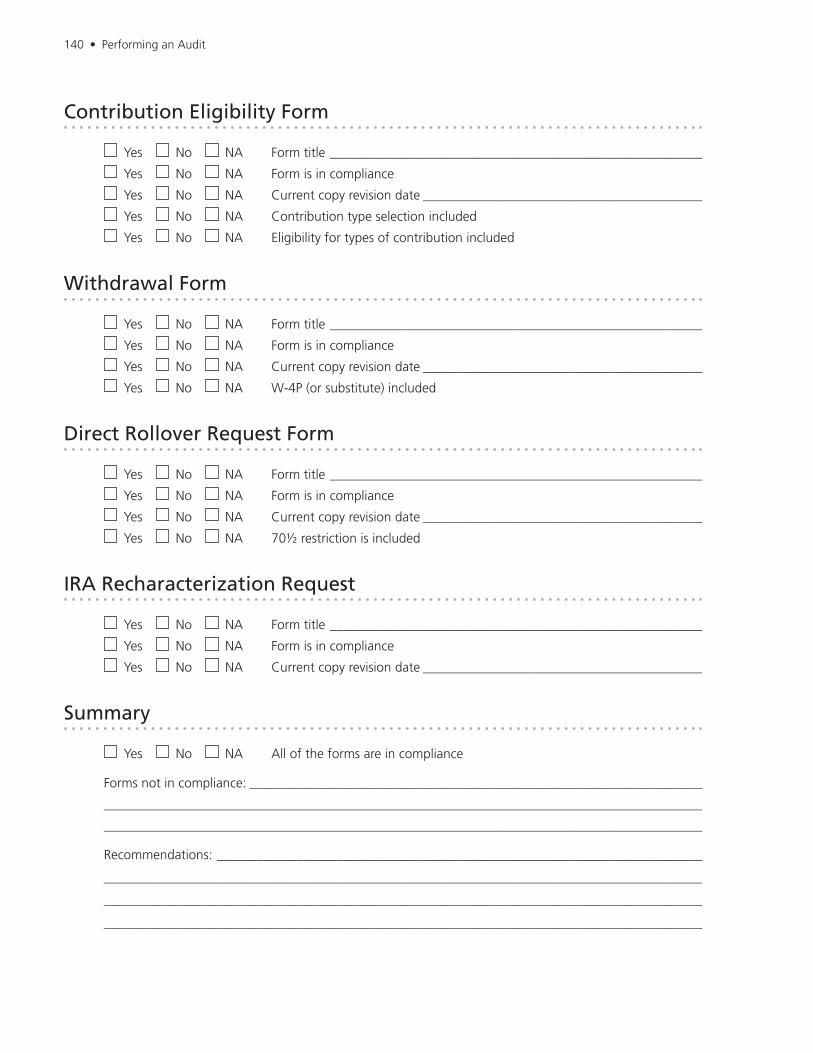

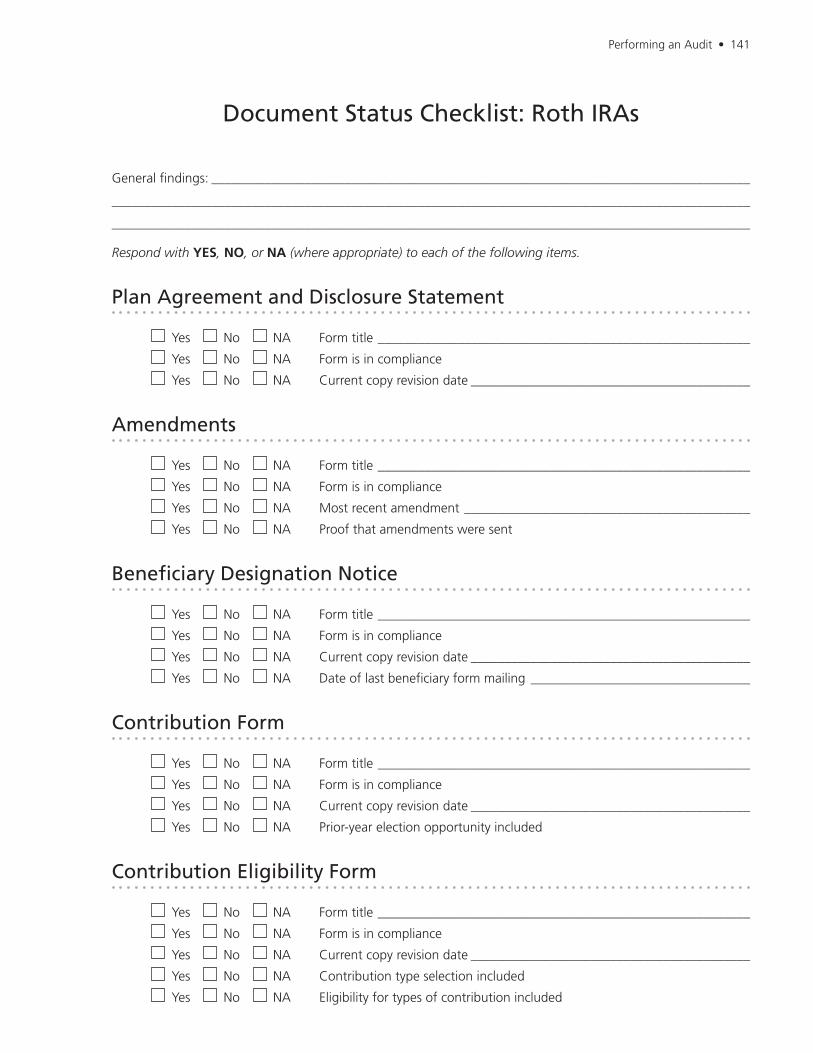

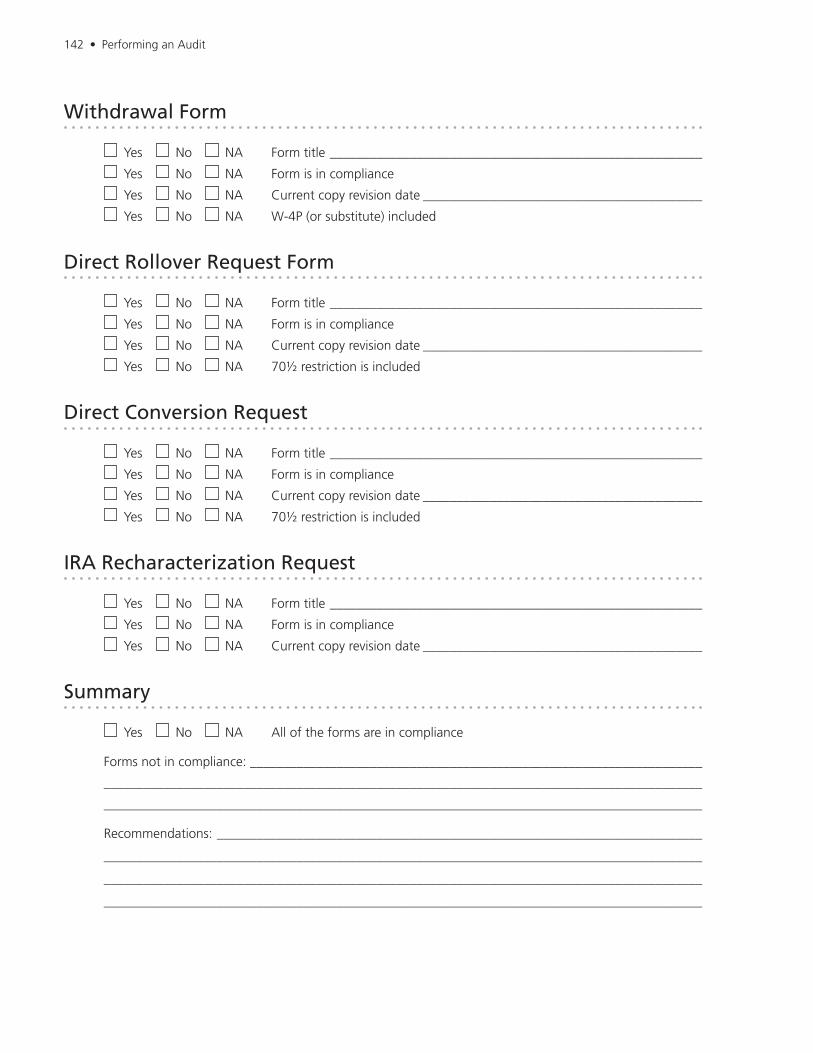

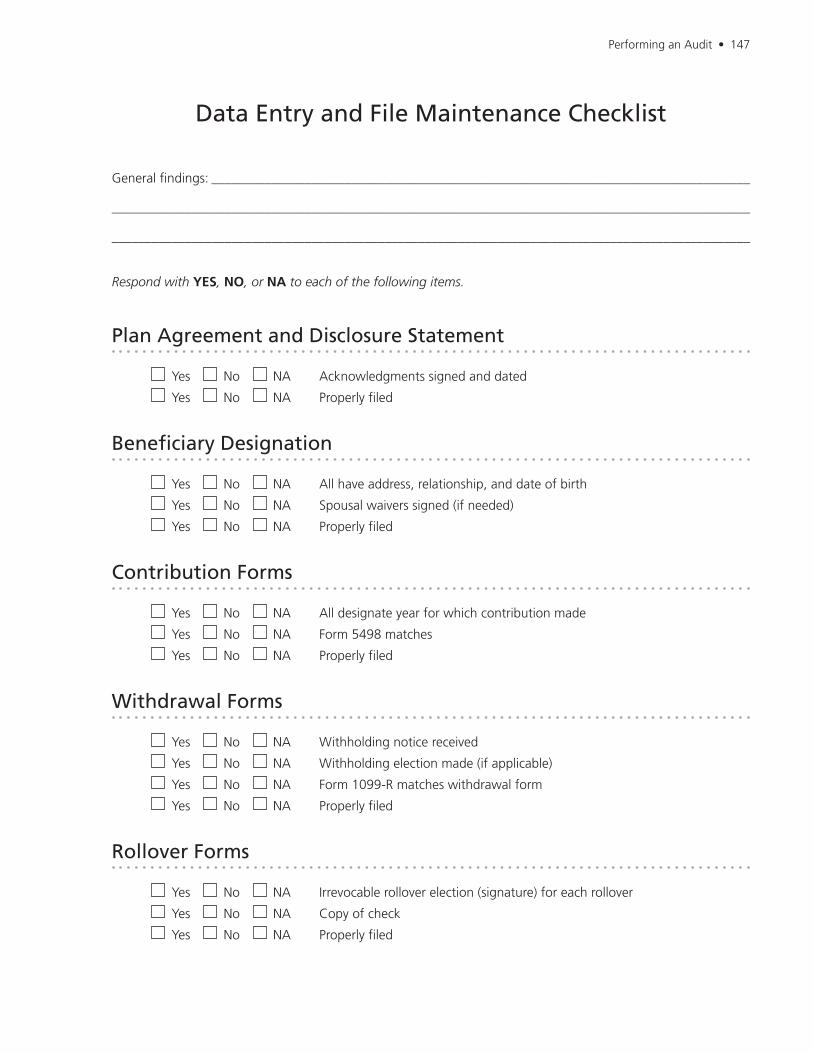

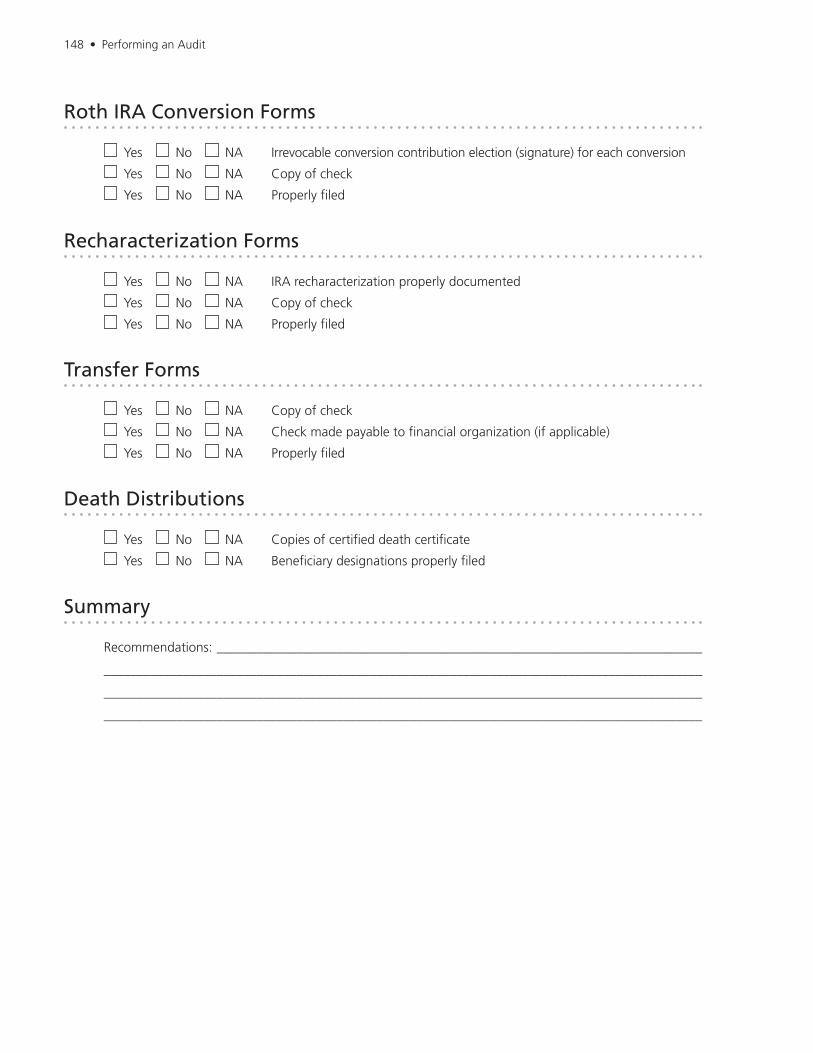

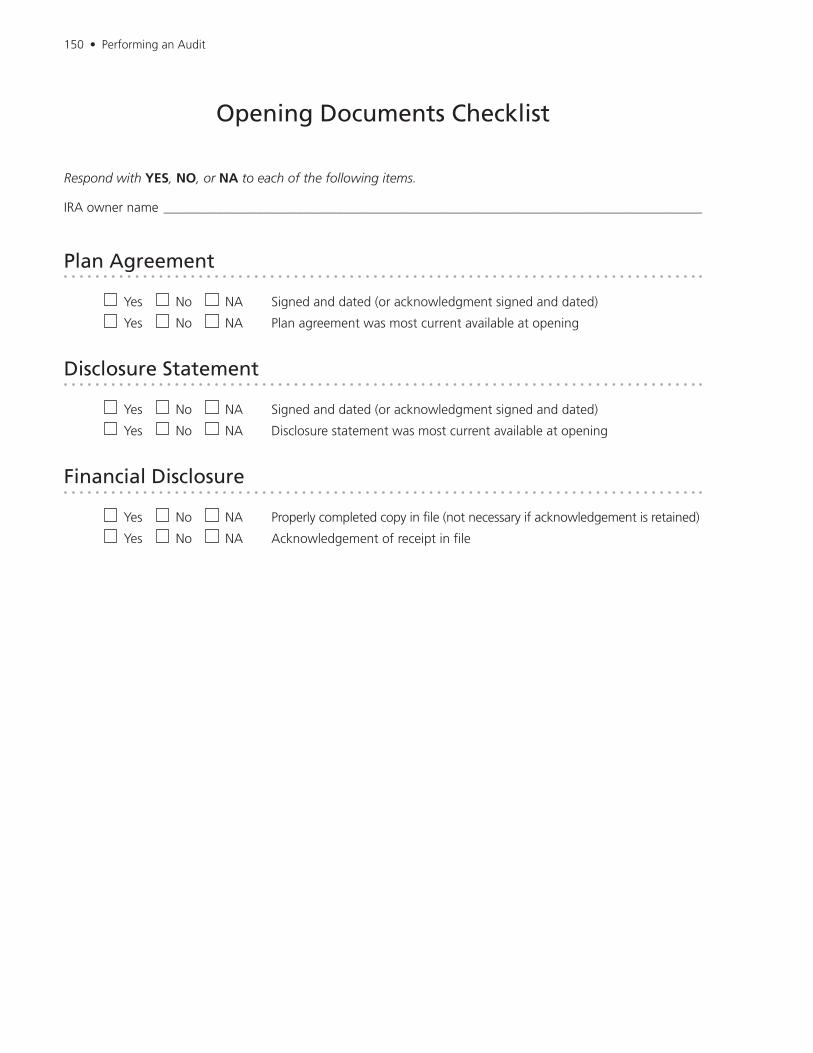

Chapter 5Performing an AuditOverview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .137Survey IRA Forms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .138Document Status Checklist: Traditional IRAs. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .139Document Status Checklist: Roth IRAs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .141Survey IRA Operations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .143Operational Procedures Status Checklist. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .144Data Entry and File Maintenance Checklist . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .147Survey IRA Owner Files. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .149Reviewing Opening Documents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .149Opening Documents Checklist . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .150Amendments Status Checklist . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .152Reviewing Reporting Issues . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .154Traditional and Roth IRA Contributions Checklist . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .155Traditional and Roth IRA Distributions Checklist . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .158Annual Statements Checklist . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .160Reviewing Withholding Requirements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .161Federal Withholding Requirements Checklist . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .162Common IRA Compliance Errors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .163Remedies for Compliance Problems . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .163

Table of Contents • iii

Chapter 6Miscellaneous Compliance ConcernsDesigning an Efficient IRA Department. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .165Procedure Manual . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .167IRA File Maintenance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .169Record Retention . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .171Importance of Training IRA Personnel . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .174Required Minimum Distributions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .175IRA Beneficiary Distribution Procedures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .181Traditional IRA Beneficiary Options. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .184Roth IRA Beneficiary Options . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .194

Chapter 7Handling Legal IssuesHandling Legal Issues . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .197Power of Attorney . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .198Guardianship . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .200Creditors of IRAs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .201Investment Protection for IRAs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .203Community and Marital Property . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .204Transfers Incident to Divorce or Legal Separation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .205Beneficiary Issues . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .207Missing IRA Owners and Beneficiaries . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .211Abandoned IRAs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .212Small Estate Administration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .214Minors as IRA Owners . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .214Mergers and Acquisitions. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .215Hold Harmless Language . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .216Final Fiduciary Rule. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .217Prohibited Transactions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .218Abusive Tax-Shelter Transactions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .225IRA Fees. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .226

Glossary of Terms

iv • Table of Contents

Importance of Compliance • v

Importance of ComplianceIndividual retirement arrangement (IRA) compliance is one of the most significant concerns for financial organizations that serve as IRA trustees, custodians, and issuers. If the IRS arrives to audit an IRA department, what will the examiners look for? Will they search for complete records of past transactions or assess present operations? What are the IRA administrator’s responsibilities? The IRA Compliance manual addresses relevant topics about Traditional and Roth IRA compliance with laws and related Treasury regulations.

The IRA Compliance manual focuses on Traditional and Roth IRAs—the most common types of individual retirement arrangements. Simplified employee pension (SEP) plans and savings incentive match plan for employees of small employers (SIMPLE) IRA plans are IRA-based employer-sponsored retirement plans. These employer plans are covered in the Ascensus IRA Reference Service and the IRA Fact Book.

Compliance Is More Than Avoiding Monetary PenaltiesThe Internal Revenue Code specifically addresses the financial organization’s responsibilities and potential penalties if those responsibilities are not met. As a result, most financial organizations equate compliance concerns with the potential monetary penalties. While the specific fines represent an integral part of IRA compliance, the overall issue of IRA compliance is much broader.

Legislative and Regulatory Changes to IRAsAlmost every year, Congress passes laws that affect retirement. The IRS periodically releases guidance in the form of Treasury regulations, revenue procedures, notices, publications, etc. Because of the volume and immediacy of newly mandated rules and procedures, IRA personnel must familiarize themselves with the newest guidance. The IRA Compliance manual contains the most up-to-date IRA information available at the time of its publication and covers how recent rule changes affect IRA compliance.

Using This Manual

Terms to NoteTo make understanding IRA compliance issues easier, the IRA Compliance manual may use simplified terms of which readers should be aware. Many different types of organizations offer IRAs, including banks, savings and loan associations, credit unions, insurance companies, brokerage firms. When this manual refers to IRA administrators or financial organizations, the term is inclusive of all types of organizations offering IRAs. Also note, entities that are not insurance companies often act in the capacity of either trustees or custodians, while insurance companies act in the capacity of issuers.

vi • Importance of Compliance

Scope and PurposeOrganizations offering IRAs do so in a constantly changing environment. Laws and rules change, organizations change, the industry continues to become more competitive, and many other intangible variables affect IRA programs. This manual is intended to explain IRA compliance issues from a federal law perspective. Because of substantial variations between state laws, IRA compliance concerns applicable to state-issued rules and regulations generally are not addressed. Financial organizations should consult with their legal advisors for any state law issues or changes that would affect their IRA programs.

Supporting IRS and DOL guidance (e.g., forms, Internal Revenue Code sections, DOL regulations) are sometimes referenced for additional background information. These items can be found by clicking on hyperlinks within this manual or are otherwise searchable at www.irs.gov or at www.dol.gov/agencies/ebsa.

NOTE: Hyperlinks to externally hosted forms at www.irs.gov generally go to the version identified by the IRS as the most current version of the form, unless there is some instructional value to linking to a specific year’s form. When linking out to an external IRS form, please verify that you’ve reached the version you intended, in case the IRS updates its URL addresses before the next update of this manual.

Origins of Compliance • 1

Chapter 1

Origins of ComplianceIRA Compliance

Financial Organization Penalties

IRA Owner Penalty Taxes

Financial Organization Responsibilities

IRA Owner Responsibilities

IRA Compliance

Financial organizations unfortunately do not have a single source to refer to for a complete list of all IRA compliance rules and regulations. Individual retirement arrangement (IRA) compliance is based on requirements from several sources, including the Internal Revenue Code (IRC), Treasury regulations, Internal Revenue Service (IRS) pronouncements, and other government directives.

Internal Revenue CodeThe Internal Revenue Code is created by Congress and is a compilation of federal laws governing the generation of revenue and includes laws that govern IRAs.

IRA owners are given the benefit of tax-deferred earnings, possible tax-free distributions, and, if eligible, income tax deductions for IRA contributions. To receive these tax benefits, IRA owners must follow certain rules regarding their IRAs. The rules address all aspects of the IRA, including IRA maintenance, deductions taken for the contributions, the timing of distributions, disbursements of dollars when the IRA owner dies, penalties for any IRA owner abuse in these areas, etc. The foundation for these rules is found in the Internal Revenue Code.

Some key sections in the Internal Revenue Code relating to IRAs are listed below.

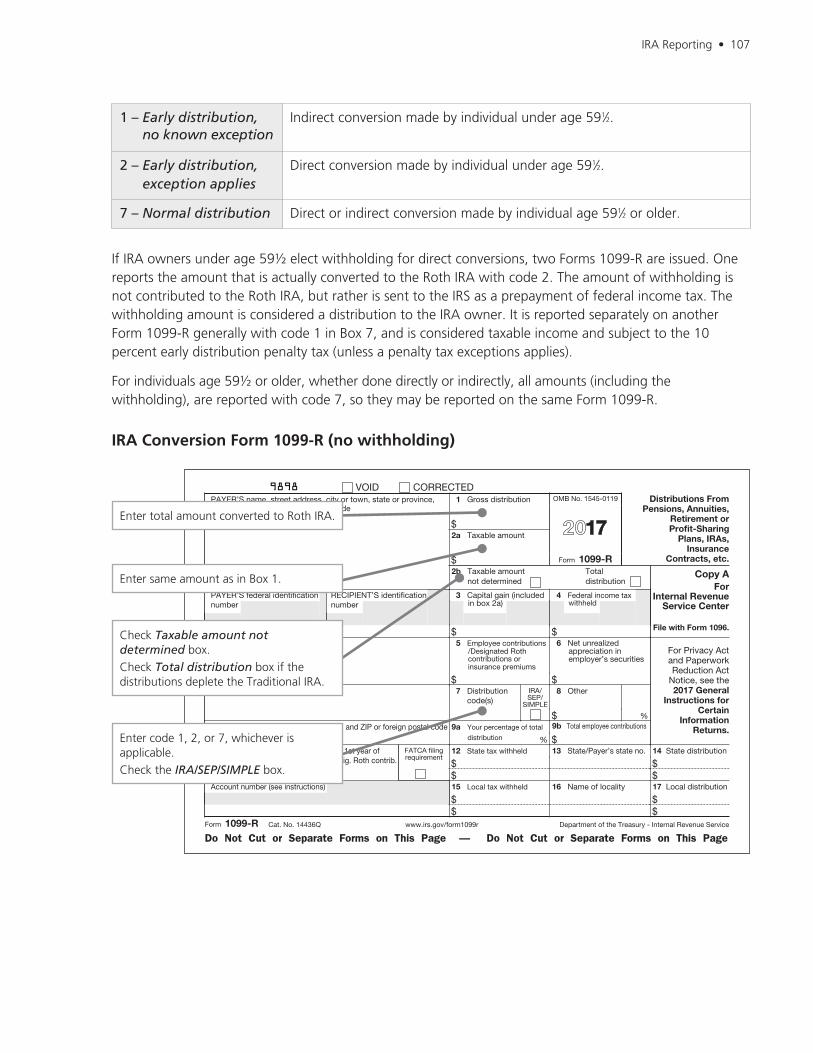

• IRC Sec. 72(t) contains details on the 10 percent early distribution penalty tax and the various exceptions to this penalty.

• IRC Sec. 219 cites contribution limits and authorizes the deductions allowed for certain types of IRA contributions.

• IRC Sec. 401(a)(9) outlines the general rules for required minimum distributions (RMDs) and beneficiary options.

• IRC Sec. 402 explains the rules for making rollover contributions from employer-sponsored retirement plans into IRAs.

• IRC Sec. 408 outlines the general rules applying to IRAs.

• IRC Sec. 408A contains the general rules for Roth IRAs.

2 • Origins of Compliance

Treasury RegulationsThe IRS is the government agency that is responsible for writing Treasury regulations that interpret and implement the Internal Revenue Code.

There are three types of Treasury regulations, each with a different degree of authority. Treasury regulations may be released in the form of final, temporary, and proposed regulations, each of which is explained next.

Final Regulations (Treas. Regs.)Final regulations remain in effect as long as the applicable legislation remains unchanged or until the IRS rewrites the regulations. Final Treasury regulations are released in Treasury Decisions.

Temporary Regulations (Temp. Treas. Regs.)Temporary regulations provide temporary guidance when taxpayers need immediate guidance, but more time is needed to develop final regulations. Temporary regulations have the same authority as final regulations, and generally are effective until replaced by final regulations.

Proposed Regulations (Prop. Treas. Regs.)Proposed regulations usually are issued during periods when final regulations are being developed in a certain area. After proposed regulations are released, the IRS considers comments from the public and may hold hearings to gather industry input before making the regulations final. The IRS indicates in the proposed regulations the extent to which they may be relied upon before final regulations are completed.

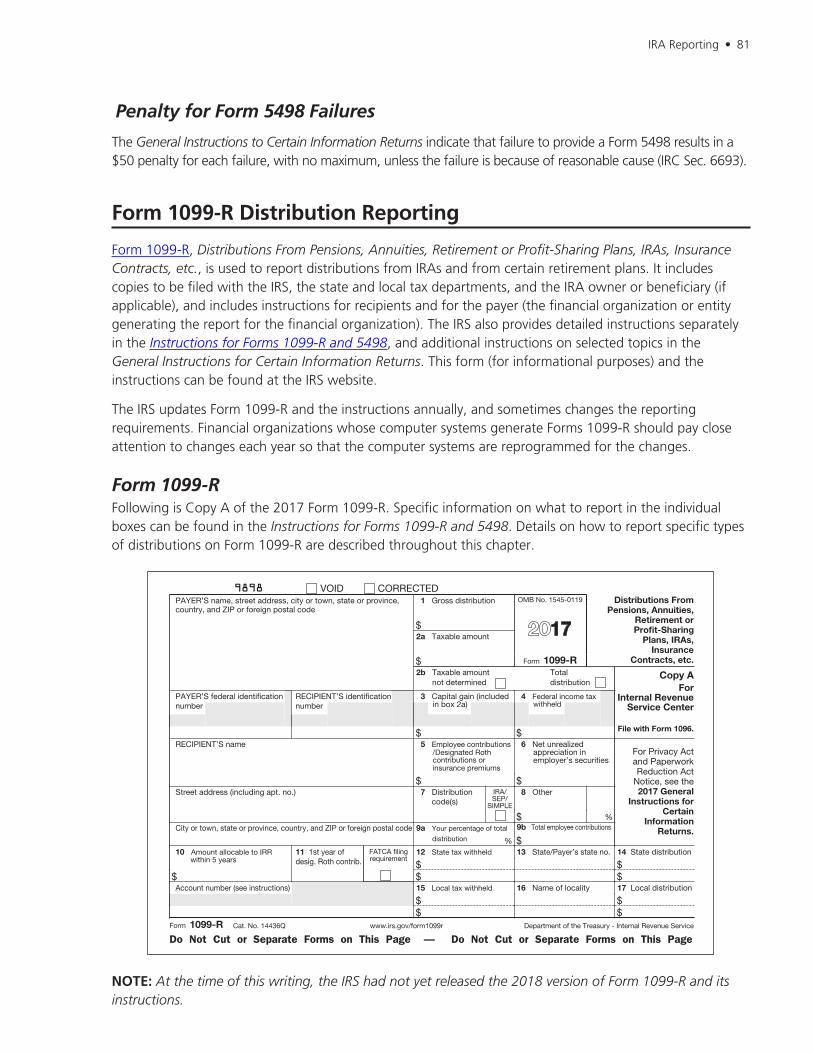

Each section of the Treasury regulations corresponds to a particular section of the Internal Revenue Code. For example, IRC Sec. 6081 is the basic authority for the Secretary to grant an extension of time for filing any tax-related information returns, such as Form 1099-R, Distributions From Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, etc., and Form 5498, IRA Contribution Information. Treas. Reg. 1.6081-1 provides more detail about the granting of filing extensions. Temporary Treasury regulations have similar numbering, except that the number sequence is followed by a “T.”

When the Treasury Department releases proposed regulations, the current method is that the release is given a six-digit identification number preceded by “REG” and followed by two digits denoting the year of drafting. Final regulations typically are released as Treasury Decisions (TD). For example, in January 2001, the IRS released the proposed Treasury regulations governing RMDs that were drafted in 2000. The initial release was identified as REG-130477-00 and REG-130481-00. Contained in this release, in addition to other sections, was Prop. Treas. Reg. 1.408-8 explaining RMD regulations specific to IRAs. The IRS released the final version of these regulations in TD 8987 in April 2002. The actual regulation citation, however, is Treas. Reg. 1.408-8.

Revenue RulingsThe IRS releases revenue rulings (Rev. Ruls.) as an interpretation of laws and Treasury regulations as applied to a specific set of facts. Revenue rulings may be relied on as the IRS’ official position on the specific set of facts. But the IRS reserves the right to restate any position by modifying or replacing a previously published ruling.

Revenue ProceduresRevenue procedures (Rev. Procs.) outline specific procedures necessary to comply with IRS rules and regulations.

Origins of Compliance • 3

IRS Announcements and NoticesThe IRS publishes announcements and notices in the Internal Revenue Bulletin. These pronouncements are published when taxpayers need immediate information on specific issues. The language in announcements and notices may appear later in revenue rulings or in procedures generated to explain the area covered in the announcement or notice in more detail. Taxpayers can rely on the information supplied in announcements and notices.

IRS PublicationsThe IRS annually releases publications designed to explain a variety of tax topics using layman’s terms. For example, IRS Publications 590-A, Contributions to Individual Retirement Arrangements (IRAs), and 590-B, Distributions from Individual Retirement Arrangements (IRAs), discuss essential IRA issues and are good resources for researching general IRA questions.

IRS FormsThe IRS publishes hundreds of forms and accompanying instructions every year. Often, the instructions to the forms contain information on certain rules or procedures that are not available from any other source. This is particularly true for procedures to satisfy reporting requirements.

Private Letter RulingsPrivate letter rulings (PLRs) are opinions written by the IRS in response to a written request from a taxpayer regarding a specific set of facts. A PLR may be relied upon only by the taxpayer who actually applied for the ruling. But a PLR gives some indication to all taxpayers about how the IRS views a particular issue.

Other ResourcesThe IRS uses the sources just discussed to inform IRA owners and financial organizations of how they must maintain IRAs. Compliance with these IRS rulings often depends on timely access to the information. Legislation and IRS pronouncements may come into play quickly. Additional information such as fact sheets and news releases may be found on some topics at the IRS website.

In this fluid environment, financial organizations need information immediately to coordinate operations that will accommodate the changes. Therefore, financial organizations should ensure their access to necessary information by using information sources or consulting services, regularly attending continuing education courses, and working closely with the organization’s advisors. In audit situations, the IRS does not view insufficient resources as a valid excuse for noncompliance.

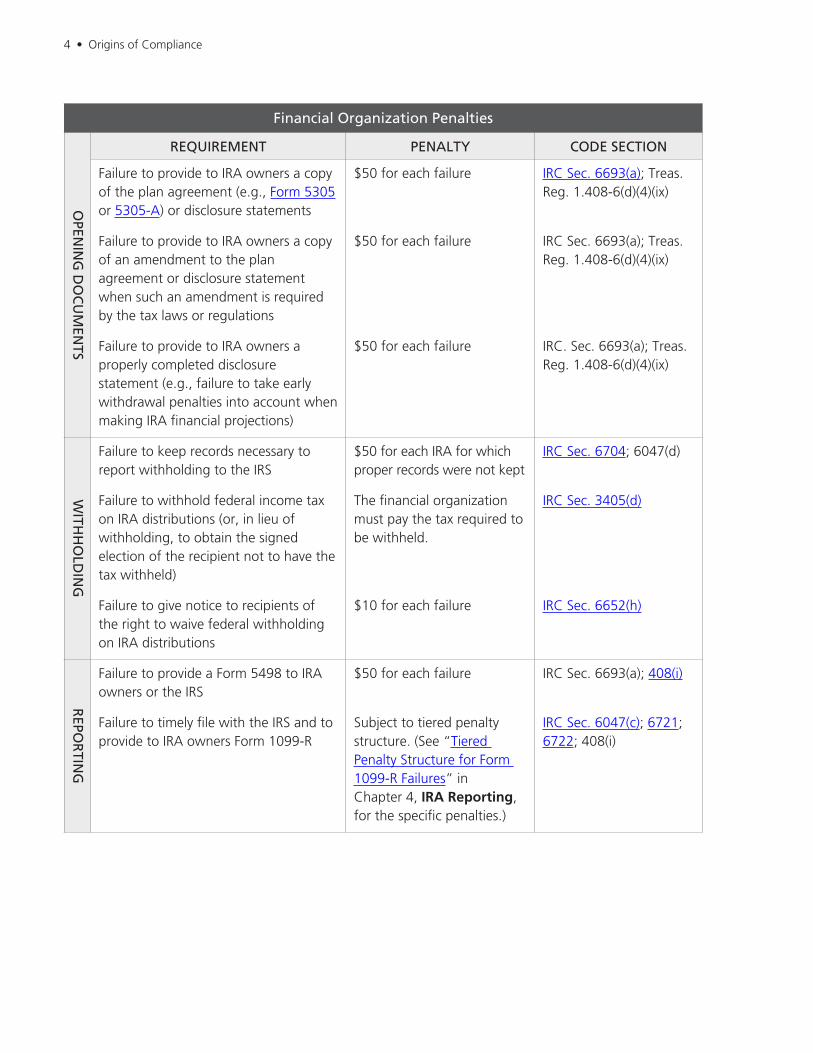

Financial Organization Penalties

Avoiding IRS penalties is not difficult if financial organization personnel make a serious effort to learn, to keep up to date on, and to adhere to the strict requirements. Seminars, technical reference books, procedure manuals, professional publications, checklists, and internal compliance reviews all aid personnel in establishing and maintaining a trouble-free IRA department.

Financial organizations generally are concerned about compliance for two primary reasons: to avoid the monetary penalties assessed for noncompliance and, of course, to avoid jeopardizing the tax-deferred status of their clients’ IRAs. With respect to penalties, there are three general areas in which financial organizations may be fined for noncompliance: IRA opening documents, withholding on IRA distributions, and reporting IRA transactions. Each particular compliance concern is discussed in detail in the following chapters. And a summary of the requirements, authorities, and applicable penalties for financial organization noncompliance follows.

4 • Origins of Compliance

Financial Organization Penalties

OPEN

ING

DO

CU

MEN

TS

REQUIREMENT PENALTY CODE SECTION

Failure to provide to IRA owners a copy of the plan agreement (e.g., Form 5305 or 5305-A) or disclosure statements

$50 for each failure IRC Sec. 6693(a); Treas. Reg. 1.408-6(d)(4)(ix)

Failure to provide to IRA owners a copy of an amendment to the plan agreement or disclosure statement when such an amendment is required by the tax laws or regulations

$50 for each failure IRC Sec. 6693(a); Treas. Reg. 1.408-6(d)(4)(ix)

Failure to provide to IRA owners a properly completed disclosure statement (e.g., failure to take early withdrawal penalties into account when making IRA financial projections)

$50 for each failure IRC. Sec. 6693(a); Treas. Reg. 1.408-6(d)(4)(ix)

WITH

HO

LDIN

G

Failure to keep records necessary to report withholding to the IRS

$50 for each IRA for which proper records were not kept

IRC Sec. 6704; 6047(d)

Failure to withhold federal income tax on IRA distributions (or, in lieu of withholding, to obtain the signed election of the recipient not to have the tax withheld)

The financial organization must pay the tax required to be withheld.

IRC Sec. 3405(d)

Failure to give notice to recipients of the right to waive federal withholding on IRA distributions

$10 for each failure IRC Sec. 6652(h)

REPO

RTIN

G

Failure to provide a Form 5498 to IRA owners or the IRS

$50 for each failure IRC Sec. 6693(a); 408(i)

Failure to timely file with the IRS and to provide to IRA owners Form 1099-R

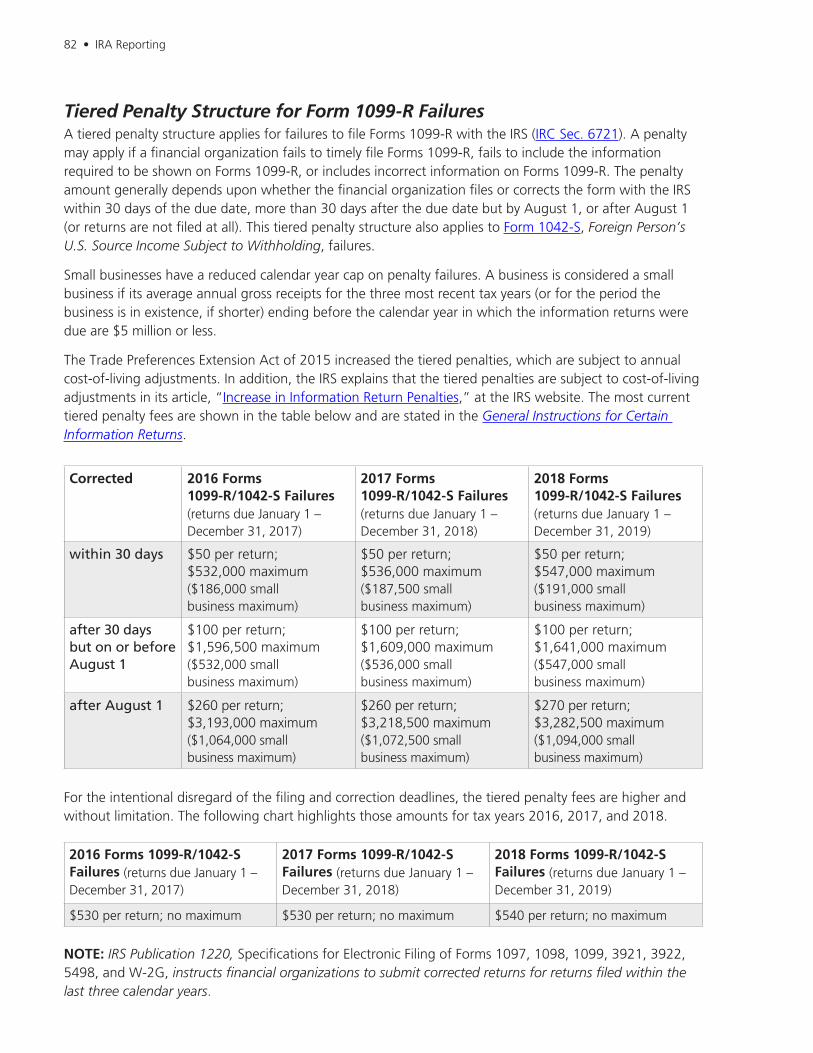

Subject to tiered penalty structure. (See “Tiered Penalty Structure for Form 1099-R Failures” in Chapter 4, IRA Reporting, for the specific penalties.)

IRC Sec. 6047(c); 6721; 6722; 408(i)

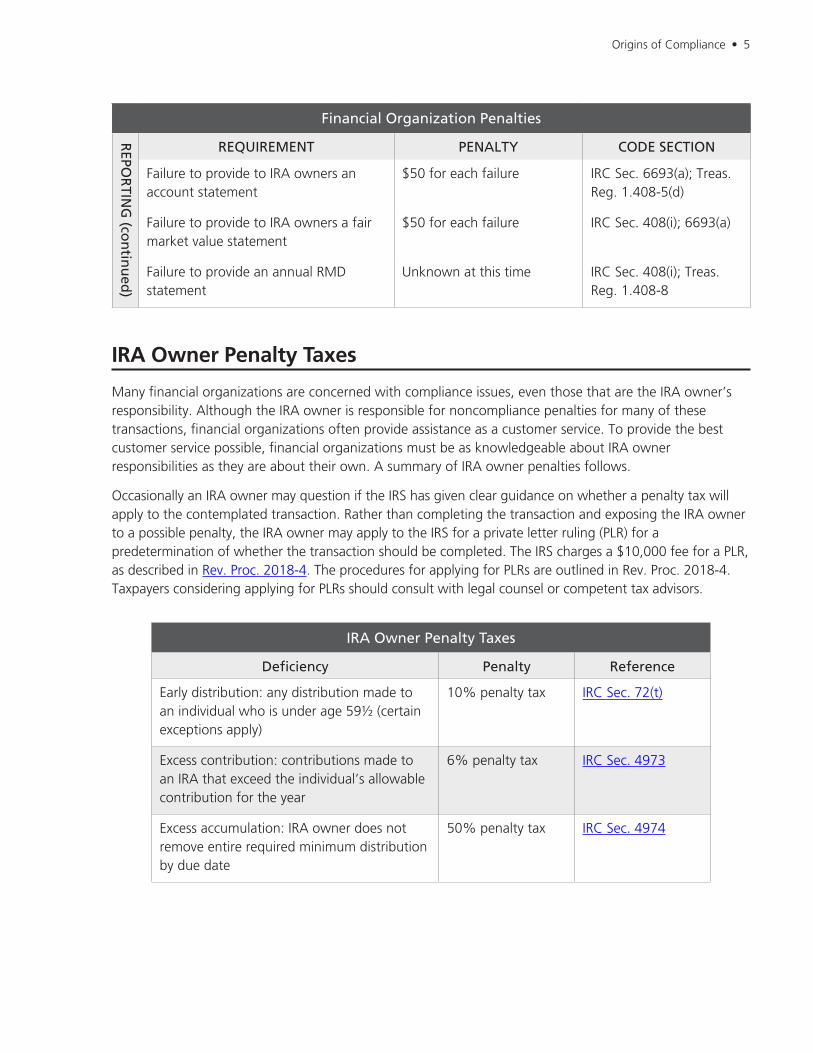

Origins of Compliance • 5

Financial Organization Penalties

REPO

RTIN

G (co

ntin

ued

)

REQUIREMENT PENALTY CODE SECTION

Failure to provide to IRA owners an account statement

$50 for each failure IRC Sec. 6693(a); Treas. Reg. 1.408-5(d)

Failure to provide to IRA owners a fair market value statement

$50 for each failure IRC Sec. 408(i); 6693(a)

Failure to provide an annual RMD statement

Unknown at this time IRC Sec. 408(i); Treas. Reg. 1.408-8

IRA Owner Penalty Taxes

Many financial organizations are concerned with compliance issues, even those that are the IRA owner’s responsibility. Although the IRA owner is responsible for noncompliance penalties for many of these transactions, financial organizations often provide assistance as a customer service. To provide the best customer service possible, financial organizations must be as knowledgeable about IRA owner responsibilities as they are about their own. A summary of IRA owner penalties follows.

Occasionally an IRA owner may question if the IRS has given clear guidance on whether a penalty tax will apply to the contemplated transaction. Rather than completing the transaction and exposing the IRA owner to a possible penalty, the IRA owner may apply to the IRS for a private letter ruling (PLR) for a predetermination of whether the transaction should be completed. The IRS charges a $10,000 fee for a PLR, as described in Rev. Proc. 2018-4. The procedures for applying for PLRs are outlined in Rev. Proc. 2018-4. Taxpayers considering applying for PLRs should consult with legal counsel or competent tax advisors.

IRA Owner Penalty Taxes

Deficiency Penalty Reference

Early distribution: any distribution made to an individual who is under age 59½ (certain exceptions apply)

10% penalty tax IRC Sec. 72(t)

Excess contribution: contributions made to an IRA that exceed the individual’s allowable contribution for the year

6% penalty tax IRC Sec. 4973

Excess accumulation: IRA owner does not remove entire required minimum distribution by due date

50% penalty tax IRC Sec. 4974

6 • Origins of Compliance

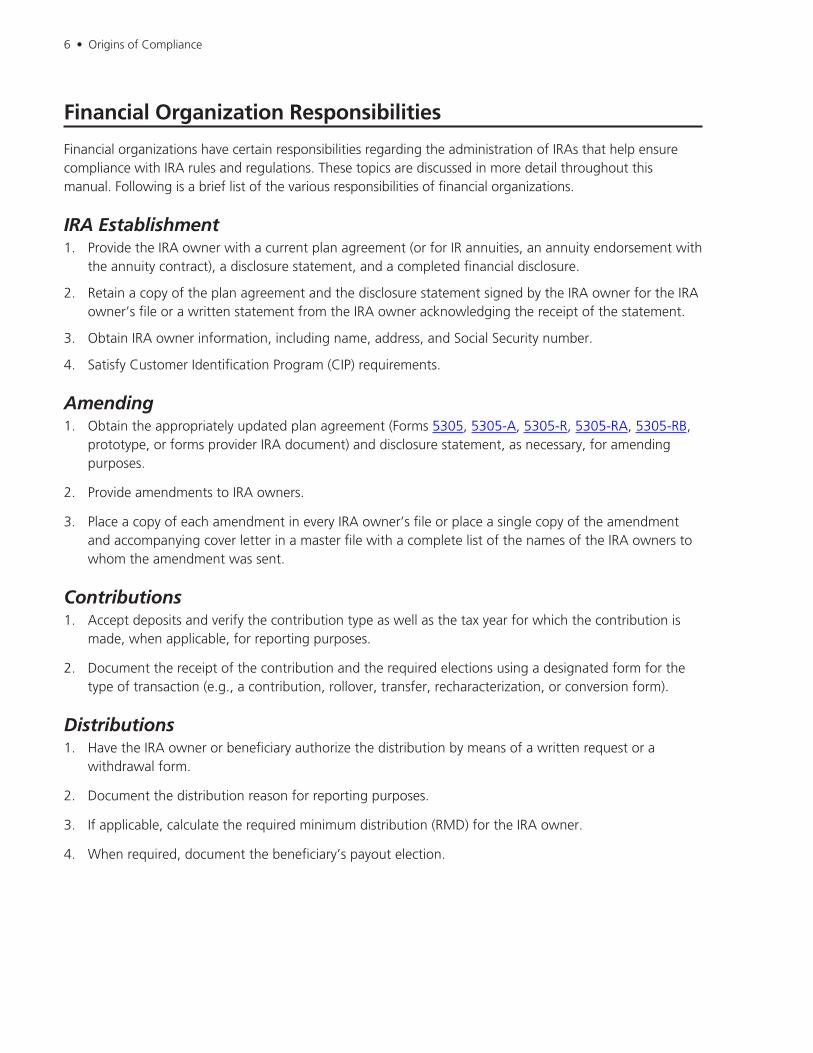

Financial Organization Responsibilities

Financial organizations have certain responsibilities regarding the administration of IRAs that help ensure compliance with IRA rules and regulations. These topics are discussed in more detail throughout this manual. Following is a brief list of the various responsibilities of financial organizations.

IRA Establishment1. Provide the IRA owner with a current plan agreement (or for IR annuities, an annuity endorsement with

the annuity contract), a disclosure statement, and a completed financial disclosure.

2. Retain a copy of the plan agreement and the disclosure statement signed by the IRA owner for the IRA owner’s file or a written statement from the IRA owner acknowledging the receipt of the statement.

3. Obtain IRA owner information, including name, address, and Social Security number.

4. Satisfy Customer Identification Program (CIP) requirements.

Amending1. Obtain the appropriately updated plan agreement (Forms 5305, 5305-A, 5305-R, 5305-RA, 5305-RB,

prototype, or forms provider IRA document) and disclosure statement, as necessary, for amending purposes.

2. Provide amendments to IRA owners.

3. Place a copy of each amendment in every IRA owner’s file or place a single copy of the amendment and accompanying cover letter in a master file with a complete list of the names of the IRA owners to whom the amendment was sent.

Contributions1. Accept deposits and verify the contribution type as well as the tax year for which the contribution is

made, when applicable, for reporting purposes.

2. Document the receipt of the contribution and the required elections using a designated form for the type of transaction (e.g., a contribution, rollover, transfer, recharacterization, or conversion form).

Distributions1. Have the IRA owner or beneficiary authorize the distribution by means of a written request or a

withdrawal form.

2. Document the distribution reason for reporting purposes.

3. If applicable, calculate the required minimum distribution (RMD) for the IRA owner.

4. When required, document the beneficiary’s payout election.

Origins of Compliance • 7

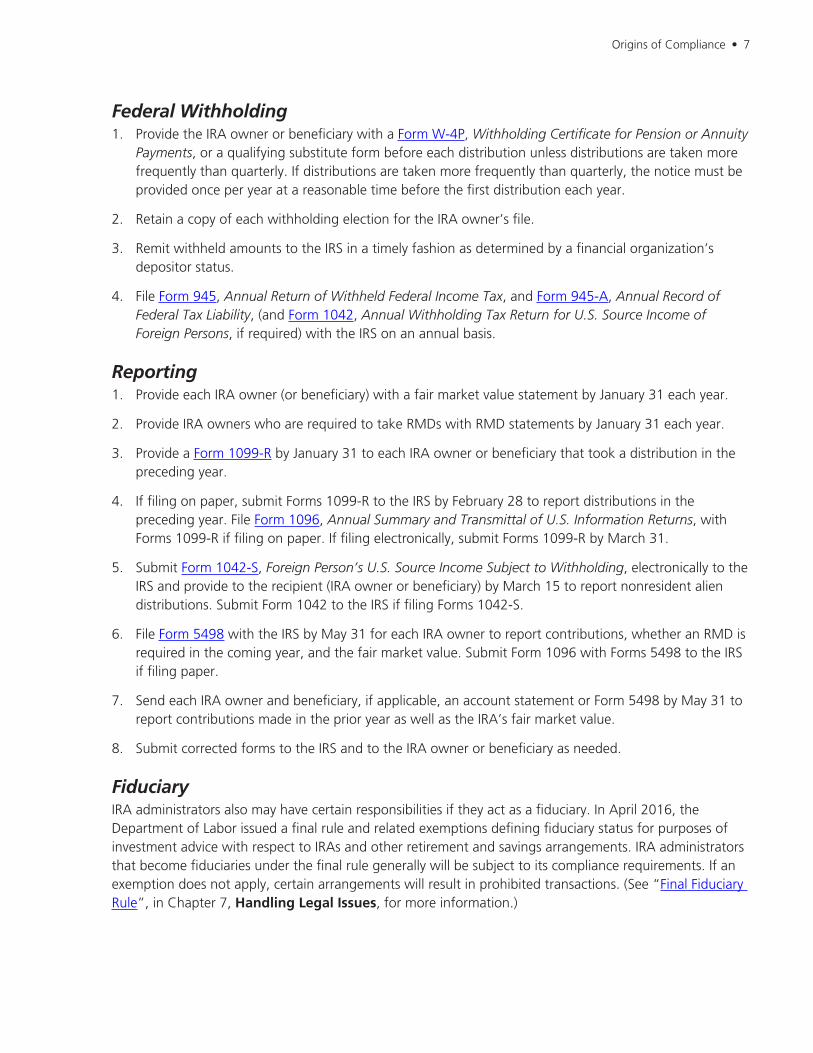

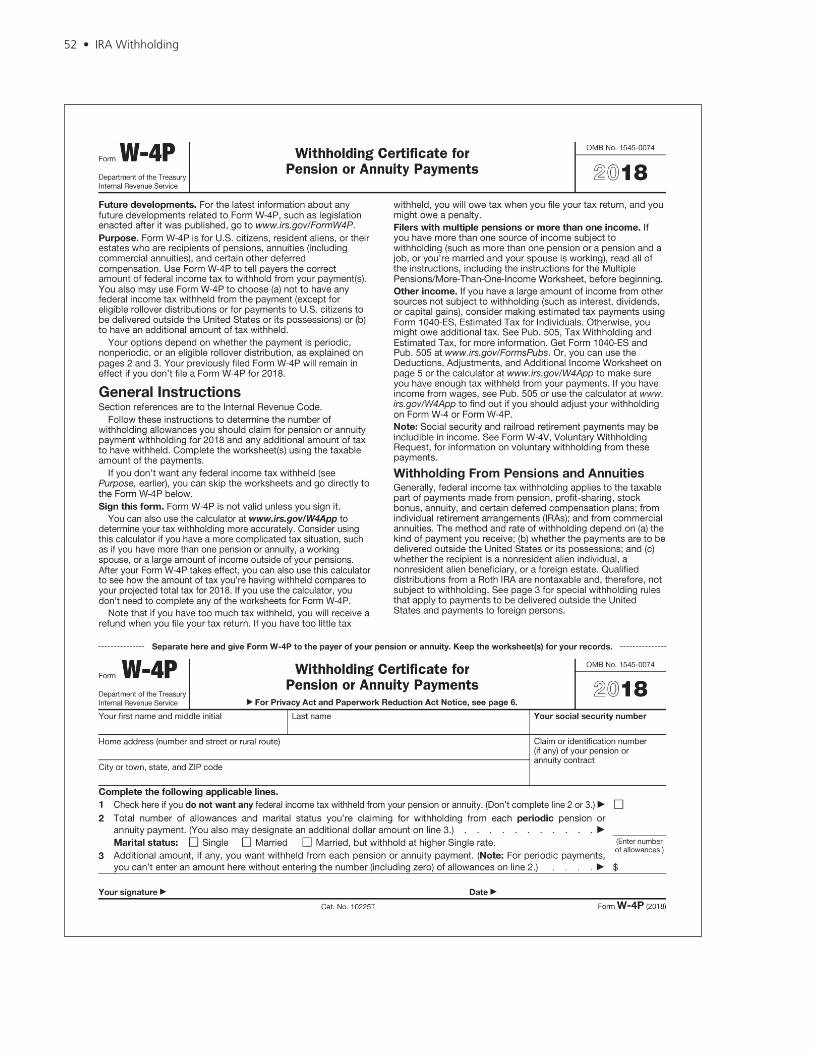

Federal Withholding1. Provide the IRA owner or beneficiary with a Form W-4P, Withholding Certificate for Pension or Annuity

Payments, or a qualifying substitute form before each distribution unless distributions are taken more frequently than quarterly. If distributions are taken more frequently than quarterly, the notice must be provided once per year at a reasonable time before the first distribution each year.

2. Retain a copy of each withholding election for the IRA owner’s file.

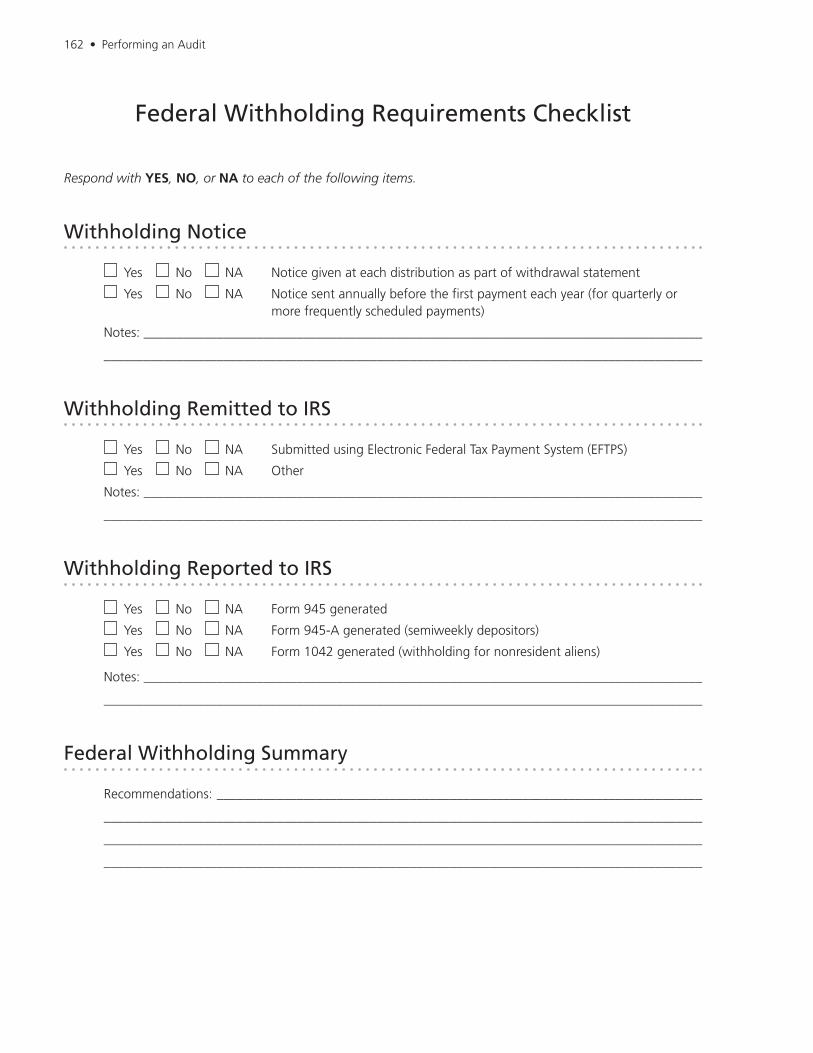

3. Remit withheld amounts to the IRS in a timely fashion as determined by a financial organization’s depositor status.

4. File Form 945, Annual Return of Withheld Federal Income Tax, and Form 945-A, Annual Record of Federal Tax Liability, (and Form 1042, Annual Withholding Tax Return for U.S. Source Income of Foreign Persons, if required) with the IRS on an annual basis.

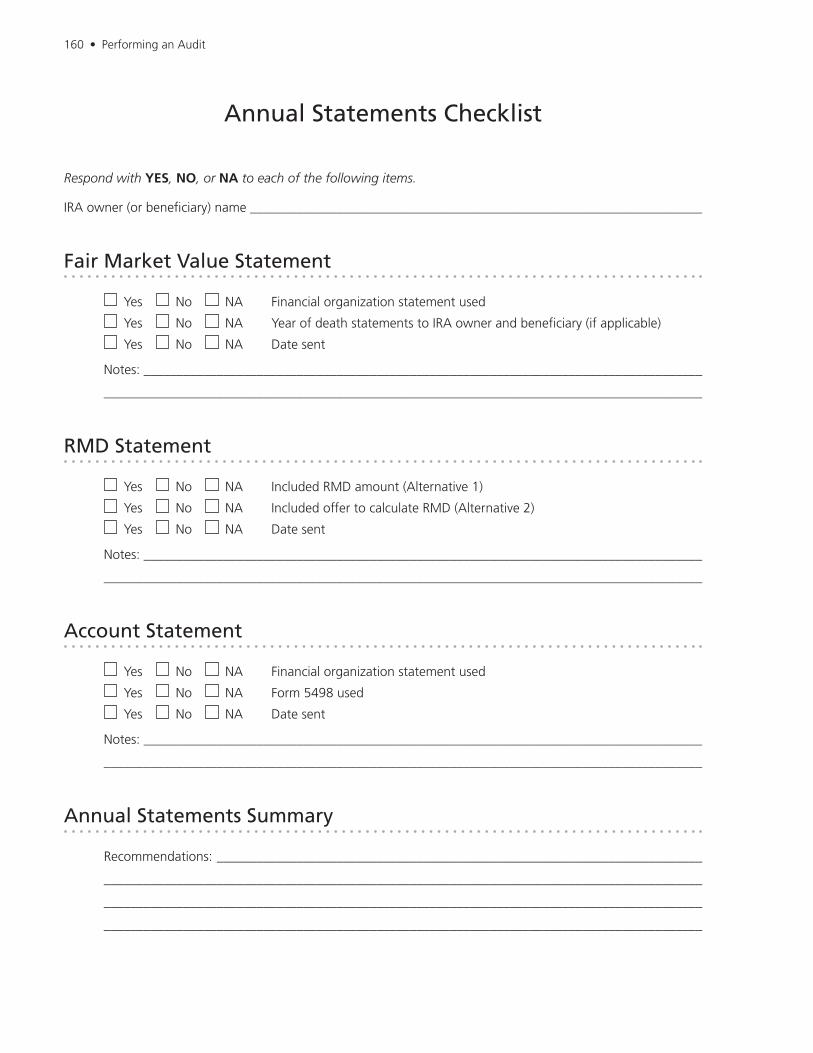

Reporting1. Provide each IRA owner (or beneficiary) with a fair market value statement by January 31 each year.

2. Provide IRA owners who are required to take RMDs with RMD statements by January 31 each year.

3. Provide a Form 1099-R by January 31 to each IRA owner or beneficiary that took a distribution in the preceding year.

4. If filing on paper, submit Forms 1099-R to the IRS by February 28 to report distributions in the preceding year. File Form 1096, Annual Summary and Transmittal of U.S. Information Returns, with Forms 1099-R if filing on paper. If filing electronically, submit Forms 1099-R by March 31.

5. Submit Form 1042-S, Foreign Person’s U.S. Source Income Subject to Withholding, electronically to the IRS and provide to the recipient (IRA owner or beneficiary) by March 15 to report nonresident alien distributions. Submit Form 1042 to the IRS if filing Forms 1042-S.

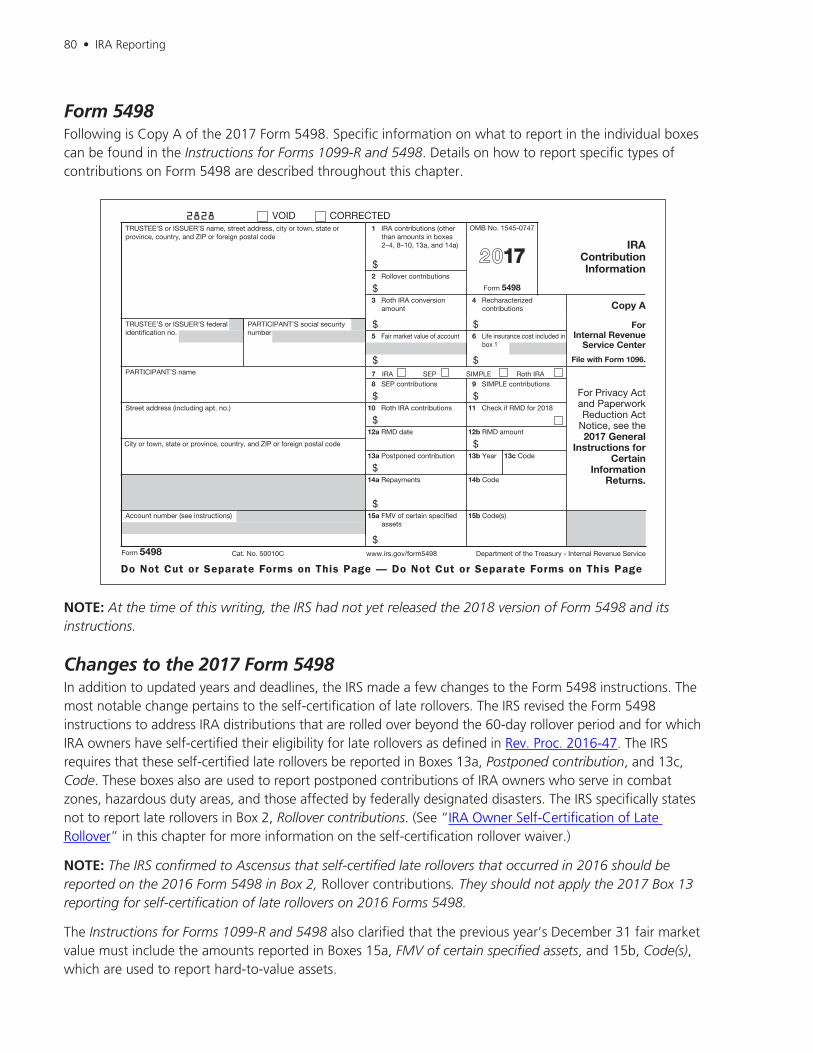

6. File Form 5498 with the IRS by May 31 for each IRA owner to report contributions, whether an RMD is required in the coming year, and the fair market value. Submit Form 1096 with Forms 5498 to the IRS if filing paper.

7. Send each IRA owner and beneficiary, if applicable, an account statement or Form 5498 by May 31 to report contributions made in the prior year as well as the IRA’s fair market value.

8. Submit corrected forms to the IRS and to the IRA owner or beneficiary as needed.

Fiduciary IRA administrators also may have certain responsibilities if they act as a fiduciary. In April 2016, the Department of Labor issued a final rule and related exemptions defining fiduciary status for purposes of investment advice with respect to IRAs and other retirement and savings arrangements. IRA administrators that become fiduciaries under the final rule generally will be subject to its compliance requirements. If an exemption does not apply, certain arrangements will result in prohibited transactions. (See “Final Fiduciary Rule”, in Chapter 7, Handling Legal Issues, for more information.)

8 • Origins of Compliance

IRA Owner Responsibilities

Taxpayers have certain responsibilities regarding the establishment, distribution, and reporting of IRAs. Sometimes, IRA administrators question whether they are obligated to assist IRA owners with some of these tasks. The following list clarifies the various responsibilities of IRA owners. As a demonstration of good customer service, most financial organizations use transaction forms that are designed to assist IRA owners with these responsibilities. Financial organizations should, however, direct IRA owners to see a competent tax advisor for specific questions about taxation and reporting.

IRA Establishment and Contributions1. Verify eligibility to establish an IRA and make regular contributions.

2. Provide the information that is necessary for reporting to the financial organization (name, Social Security number, etc.).

3. Submit customer information as required by the financial organization’s CIP.

4. Complete a beneficiary designation.

5. Provide a written irrevocable election if making a prior-year contribution.

6. Determine the eligibility for rollover, transfer, recharacterized, and conversion contributions.

7. Determine the deductibility of Traditional IRA contributions.

8. Correct excess contributions.

Distributions1. Provide a distribution request with a withholding election that includes the reason for the distribution.

2. If the financial organization extends an offer to calculate the RMD upon the request of the IRA owner rather than providing the RMD amount on the RMD statement, either request the RMD calculation from the financial organization or calculate the RMD.

3. Remove RMDs in a timely manner from Traditional IRAs.

Reporting and Penalty Taxes1. Report Traditional IRA contributions to the IRS on Form 1040, U.S. Individual Income Tax Return, and

Form 8606, Nondeductible IRAs (if applicable).

2. Record all distributions (taxable and nontaxable) on an individual federal income tax return. In addition, generally report all Roth IRA distributions, Roth IRA conversions, and partial recharacterizations on Form 8606, as well as any Traditional IRA distributions that include a return of basis (e.g., nondeductible contributions).

3. Remit penalties to the IRS along with Form 5329, Additional Taxes on Qualified Plans (Including IRAs) and Other Tax-Favored Accounts, when required.

Opening an IRA • 9

Chapter 2

Opening an IRAOverview

Trustees, Custodians, and Issuers

IRA Opening Documents

Plan Agreement Contents

IRA Disclosure Statements

Customer Identification Program Requirements

Plan Agreement and Disclosure Statement Amendments

Beneficiary Designations

IRA Contribution Information

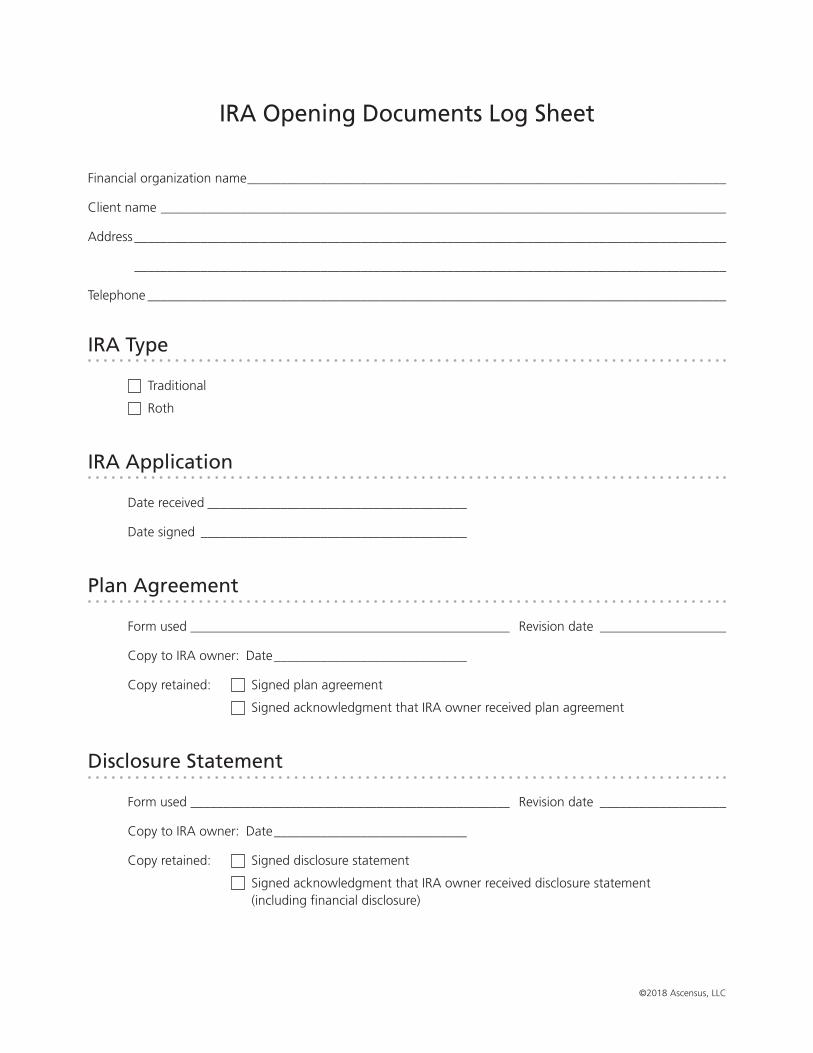

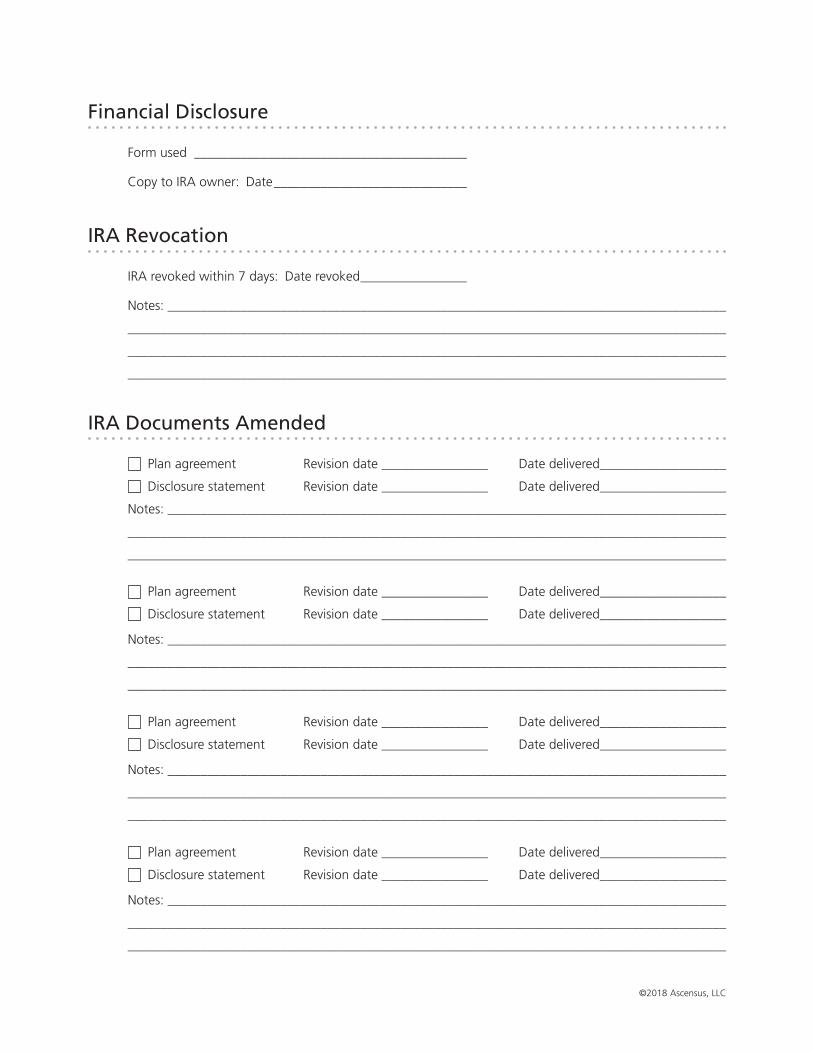

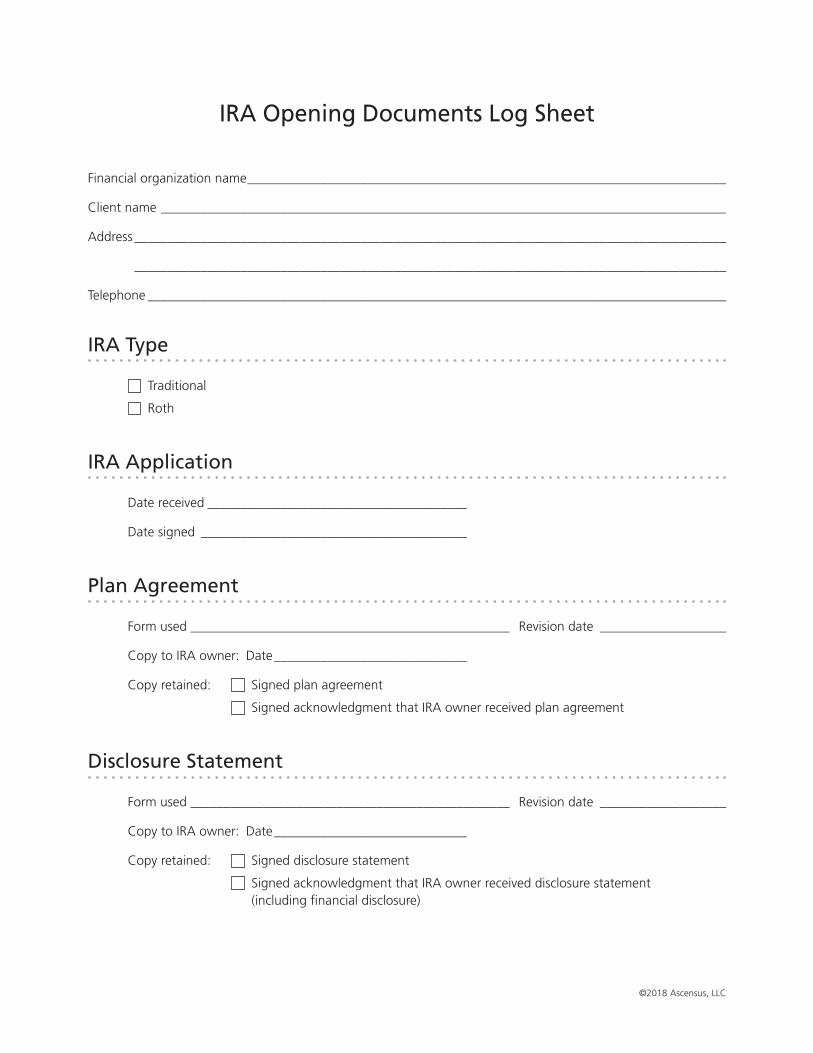

IRA Opening Documents Log Sheet

Overview

IRA compliance becomes important the moment an IRA is established. To ensure compliance, the financial organization must provide correct and current opening documents to the individual establishing the IRA.

Trustees, Custodians, and Issuers

IRA opening documents may differ by financial organization. IR accounts (IRC Sec. 408(a) and (h)) are IRAs established as trust or custodial accounts. A trustee or custodian holds the IRA assets under a plan agreement for the benefit of the IRA owner. The Traditional IR account opening document (i.e., the plan agreement) may be an IRS model Form 5305, Traditional Individual Retirement Trust Account, an IRS model Form 5305-A, Traditional Individual Retirement Custodial Account, or a prototype plan. The Roth IR account opening document (i.e., plan agreement) may be an IRS model Form 5305-R, Roth Individual Retirement Trust Account, an IRS model Form 5305-RA, Roth Individual Retirement Custodial Account, or a prototype plan. Forms providers, like Ascensus, often have specifically designed versions of these documents with added features or added explanations available to financial organizations.

10 • Opening an IRA

IR annuities (IRC Sec. 408(b)) are established through insurance companies. Insurance companies are “issuers” of IR annuities and they generally hold the IRA assets in annuities. The Traditional IR annuity opening document is referred to as an “endorsement,” and must be a prototype document. The endorsement, along with a state-approved insurance contract together make up the opening document. The Roth IR annuity opening document may be either an IRS model Form 5305-RB, Roth Individual Retirement Annuity Endorsement, with an annuity contract, or a prototype document with an annuity contract. IR accounts and annuities both operate under federal laws and applicable regulations, but there are some differences.

Trustee vs. CustodianWhat is the difference between a trustee and a custodian? The term “custodian” implies an entity whose role regarding the IRA is merely passive, meaning the organization takes title to the property and always acts upon the IRA owner’s direction. A financial organization that serves as a “trustee” may or may not have a passive role with respect to the IRAs it offers. If the organization does not have full trust powers under applicable state or federal laws, its role essentially is the same as a custodian’s. In some situations, a financial organization with full trust powers may offer “managed accounts” to IRA owners, for which the IRA trustee may choose to make investment decisions for the IRA and to allow a broader range of investment options within the IRA. But most financial organizations, even those with full trust powers, act as custodians. Trustees and custodians should check with their legal counsel if they are unsure about whether they should offer IRAs as a trustee or as a custodian.

The type of authority that a financial organization has will dictate the type of document it may use. Financial organizations with full trust powers may use IRS Form 5305 for Traditional IRAs or Form 5305-R for Roth IRAs (or a trustee IRA document from a forms provider). If a financial organization acts as a custodian, it may use Form 5305-A for Traditional IRAs or Form 5305-RA for Roth IRAs (or a custodial IRA document from a forms provider).

Regardless of whether a financial organization serves as a custodian or has trust powers, it has certain obligations as an IRA trustee or custodian as stated in tax laws and regulations. For example, both trustees and custodians have a duty to report, to withhold, and to provide an up-to-date plan agreement and disclosure statement to the IRA owner.

Nonbank Trustees and CustodiansAn entity not described as a bank (under IRC Sec. 408(n)) may be eligible to act as an IRA trustee or custodian if the IRS grants nonbank trustee or custodian powers to the entity. Rev. Proc. 2018-4 indicates that an entity applying for nonbank trustee or custodian powers must submit a written application to the IRS that demonstrates how the applicant intends to comply with the requirements of Treasury Regulation (Treas. Reg.) 1.408–2(e)(2) through (5), which defines some of the responsibilities of a nonbank trustee. An applicant must identify the specific accounts (e.g., Traditional or Roth IRAs) for which the entity desires to serve as a nonbank trustee or custodian.

Once approved, the nonbank trustee or custodian has the same obligations as stated in tax laws and regulations for IRAs administered by bank trustees and custodians (e.g., duty to report, to withhold, to provide up-to-date plan agreements and disclosure statements). A copy of the nonbank trustee/custodian approval letter must be given to IRA owners when they establish IRAs.

Opening an IRA • 11

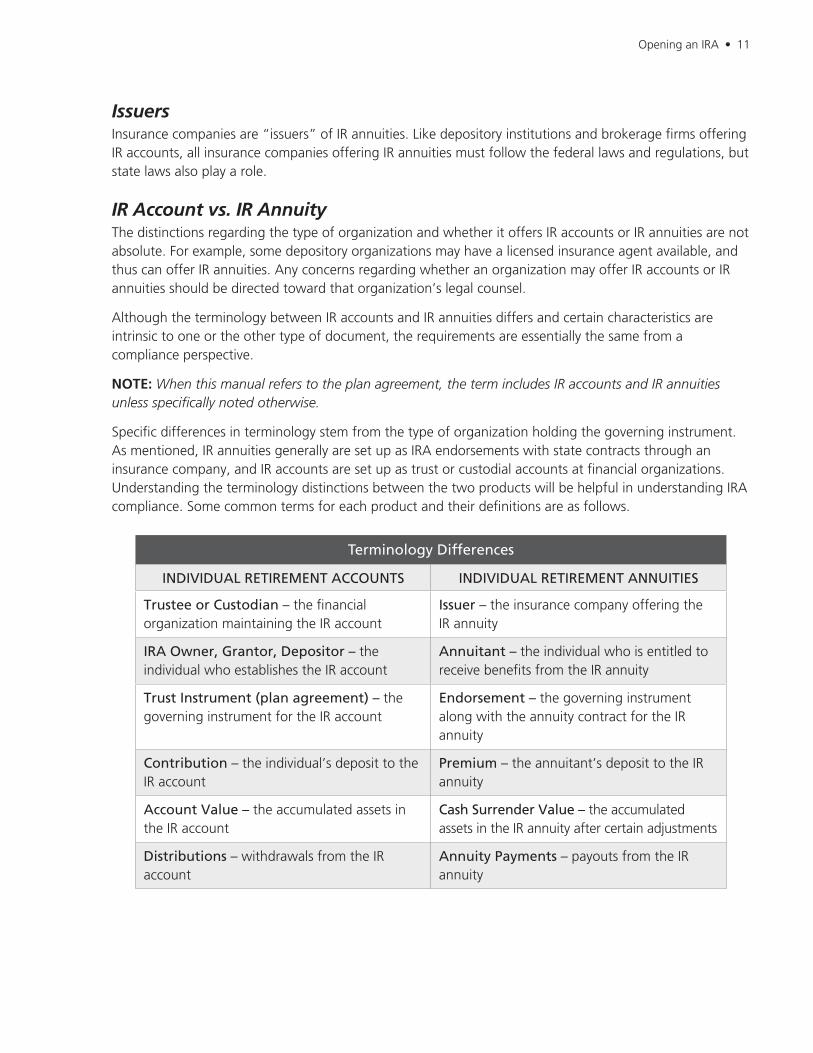

IssuersInsurance companies are “issuers” of IR annuities. Like depository institutions and brokerage firms offering IR accounts, all insurance companies offering IR annuities must follow the federal laws and regulations, but state laws also play a role.

IR Account vs. IR AnnuityThe distinctions regarding the type of organization and whether it offers IR accounts or IR annuities are not absolute. For example, some depository organizations may have a licensed insurance agent available, and thus can offer IR annuities. Any concerns regarding whether an organization may offer IR accounts or IR annuities should be directed toward that organization’s legal counsel.

Although the terminology between IR accounts and IR annuities differs and certain characteristics are intrinsic to one or the other type of document, the requirements are essentially the same from a compliance perspective.

NOTE: When this manual refers to the plan agreement, the term includes IR accounts and IR annuities unless specifically noted otherwise.

Specific differences in terminology stem from the type of organization holding the governing instrument. As mentioned, IR annuities generally are set up as IRA endorsements with state contracts through an insurance company, and IR accounts are set up as trust or custodial accounts at financial organizations. Understanding the terminology distinctions between the two products will be helpful in understanding IRA compliance. Some common terms for each product and their definitions are as follows.

Terminology Differences

INDIVIDUAL RETIREMENT ACCOUNTS INDIVIDUAL RETIREMENT ANNUITIES

Trustee or Custodian – the financial organization maintaining the IR account

Issuer – the insurance company offering the IR annuity

IRA Owner, Grantor, Depositor – the individual who establishes the IR account

Annuitant – the individual who is entitled to receive benefits from the IR annuity

Trust Instrument (plan agreement) – the governing instrument for the IR account

Endorsement – the governing instrument along with the annuity contract for the IR annuity

Contribution – the individual’s deposit to the IR account

Premium – the annuitant’s deposit to the IR annuity

Account Value – the accumulated assets in the IR account

Cash Surrender Value – the accumulated assets in the IR annuity after certain adjustments

Distributions – withdrawals from the IR account

Annuity Payments – payouts from the IR annuity

12 • Opening an IRA

IRA Opening Documents

To open a Traditional or Roth IRA, financial organizations must use IRA opening documents (i.e., plan agreements or IRA endorsements with annuity contracts) and disclosure statements that include financial disclosures. IRA administrators also often have the individuals sign beneficiary designations and contribution forms (if a contribution is being made) when opening IRAs.

The IRA plan agreement (or the application) is signed by the IRA owner and becomes the contract between the individual and the financial organization. In effect, the IRA plan agreement creates the IRA because without a signed agreement, the IRA does not exist.

The plan agreement contains the responsibilities of both the IRA owner and the financial organization.

Traditional IRAsAs previously noted, financial organizations can use government model forms or prototype plan agreements to open IRAs. Forms providers, like Ascensus, also may have available customized forms or forms kits (based on the IRS model documents or prototype documents) that also include the required disclosure statements.

IRS Model Forms 5305 and 5305-AIRA trustees and custodians may use the IRS model Form 5305 (trustees) or 5305-A (custodians) to offer Traditional IRAs. The IRS periodically updates these forms for law changes and IRS pronouncements. The latest revised Forms 5305 and 5305-A were released in September 2017, and carry an April 2017 revision date.

Forms 5305 and 5305-A or specially designed documents generally based off the IRS forms are used by most financial organizations as their plan agreements because they are the easiest to maintain. The IRS does not have a model form for Traditional IRA annuities, but does for Roth IRA annuities (Form 5305-RB).

The IRS model Traditional IRA forms include Articles I-VII with space provided for additional language to be included in Article VIII. Forms suppliers generating these plan agreements often customize Article VIII language to include special provisions, such as the right to charge fees, procedures for resignation of the trustee or custodian, and IRA investment restrictions. Except for Article VIII, the language of Forms 5305 and 5305-A usually will remain as the IRS drafted it. Articles I-III may not be altered in any way.

Prototype Plan AgreementSome financial organizations use a prototype plan agreement to offer IRAs. An IRA prototype generally is drafted by an attorney according to specific IRS guidelines and submitted to the IRS with IRS Form 5306, Application for Approval of Prototype or Employer Sponsored Individual Retirement Arrangement (IRA), for approval. Prototype documents generally are based on sample language drafted by the IRS, called a Listing of Required Modifications (LRMs). The LRM language may be modified slightly for prototype documents as long as all LRM topics are incorporated. The prototype often includes provisions giving the plan more flexibility than the IRS model agreements. The contents of an IRA prototype, however, are still bound by many of the standard requirements of Forms 5305 and 5305-A.

Financial organizations that apply for and receive IRS approval for the prototype document will receive opinion letters from the IRS. Financial organizations must provide individuals who establish IRAs with a copy of the opinion letter along with the other required documents.

Opening an IRA • 13

IR AnnuitiesInsurance companies issuing Traditional IR annuities also are bound by the general IRA requirements. As noted earlier, Traditional IR annuities currently can be opened only by using a prototype IRA endorsement. The prototype endorsement is coupled with an annuity (i.e., insurance) contract from the issuer to establish an IR annuity. IR annuity prototypes do not have to be submitted to or approved by the IRS, although an IRS submission is strongly recommended (using Form 5306).

A financial organization that offers IR annuities also must submit the IRA documentation to each state’s insurance commissioner for approval. IR annuity contracts must be state approved. Because insurance is a state-regulated product, an insurance provider can only sell its products, including IR annuities, within a state with the approval of the proper state insurance commissioner. Each state has the authority to set its own insurance standards. Each provider that seeks to operate in that state submits the proposed contract language to obtain approval to provide the product (e.g., IR annuity) in that state.

Roth IRAsFinancial organizations can use government model or prototype plan agreements to establish Roth IRAs. Forms providers also may have available customized forms or forms kits (based on the IRS model documents or prototype documents) that also include the required disclosure statements.

IRS Model Forms 5305-R, 5305-RA, and 5305-RBThe IRS offers model Roth IRA Forms 5305-R and 5305-RA that may be used to establish Roth IR accounts. The model forms are similar in content and form to the model IRS forms for establishing Traditional IRAs. The IRS also provides Form 5305-RB that may be used to establish Roth IR annuities. The latest revisions of these Roth IRA model forms were released in September 2017 and carry an April 2017 revision date.

According to the instructions to the model forms, a financial organization may make certain amendments to the provisions of the Roth IRA model forms in Article IX. For example, according to IRS Notice 98-49, a financial organization may amend the model forms to give a surviving spouse, who is the sole beneficiary of a Roth IRA, the option of not treating the Roth IRA as his own following the Roth IRA owner’s death. Roth IRAs generally have the same opening document requirements as Traditional IRAs (i.e., a plan agreement, disclosure statement, and financial disclosure).

Prototype DocumentsAs is the case with Traditional IRAs, financial organizations also may use Roth IRA prototype documents to establish Roth IRAs. Announcement 97-122 provides key guidance on prototype Roth IRA document issues. In addition, Rev. Proc. 98-59 (modified by Rev. Proc. 2010-48) contains the application procedures for obtaining IRS opinion letters for prototype Roth IRA documents.

The IRS prototype program accepts combination Traditional IRA/Roth IRA documents. Traditional IRA and Roth IRA assets may not be commingled in the same trust, however, so the document must clearly indicate whether the IRA that is being established is a Traditional or a Roth IRA. The IRS does not offer model Traditional IRA/Roth IRA combination forms.

Roth IR AnnuitiesFinancial organizations issuing Roth IR annuities have three document options: the IRS model Form 5305-RB, a prototype document, or a specially designed document from a forms provider (i.e., the endorsement). The endorsement is coupled with an annuity contract offered by the issuer.

14 • Opening an IRA

Inherited IRA Plan DocumentsThe Pension Protection Act of 2006 (PPA) provides that, effective January 1, 2007, beneficiaries of participants in eligible employer-sponsored retirement plans may directly roll over inherited plan assets to IRAs as long as the IRAs are established and maintained as “inherited” IRAs (IRC Sec. 402(c)(11), Notice 2008-30, Notice 2009-68). The Worker, Retiree, and Employer Recovery Act of 2008 required employer-sponsored retirement plans to begin offering this option for plan years beginning on or after January 1, 2010. Eligible retirement plans include qualified retirement plans under IRC Sec. 401(a), qualified annuity plans under 403(a), 403(b) plans, governmental 457(b) plans, and the U.S. government’s Thrift Savings Plan (TSP). Beneficiaries whose inherited 401(k), 403(b), governmental 457(b), or TSP accounts include designated Roth account assets may roll over the designated Roth assets to inherited Roth IRAs, but not to inherited Traditional IRAs. The government’s TSP began offering the designated Roth contribution option in 2012.

While spouse beneficiaries may roll over retirement plan assets to their own IRAs, they may also elect to directly or indirectly roll over the inherited assets to “inherited” IRAs. Unlike spouse beneficiaries, however, nonspouse beneficiaries may not directly or indirectly roll over inherited retirement plan assets to their own IRAs (i.e., IRAs not treated as inherited IRAs).

Little guidance has been issued regarding how inherited IRAs should be established. The IRS has informed Ascensus that it is not issuing specific model plan agreements for inherited IRAs. Ascensus recommends that financial organizations provide beneficiaries with plan agreements, disclosure statements, and financial disclosures upon establishing the inherited IRAs. Some forms providers, like Ascensus, may have specific “inherited IRA” plan documents available.

The IRS issued Notice 2007-7 to address certain PPA provisions. Notice 2007-7, Q&A 13, indicates that an inherited IRA must be established to identify both the nonspouse beneficiary and the deceased retirement plan participant, such as “Tom Smith as beneficiary of John Smith.” It also clarifies that a trust named as the beneficiary of a deceased retirement plan participant may complete a direct rollover to an IRA as long as the beneficiaries of the trust are “individuals” (i.e., persons). The inherited IRA must be established to identify the trust and the deceased retirement plan participant. (See Chapter 6, Miscellaneous Compliance Concerns, for more information on trust beneficiaries.)

Plan Agreement Contents

Every IRA professional should be familiar with the contents of the IRA plan agreement. The plan agreement lists the responsibilities of the IRA owner and the IRA trustee, custodian, or issuer (also referred to in this manual as the financial organization). Although the form of the opening document may vary depending on the type of IRA (Traditional or Roth) and on what version of the form the financial organization selects, the requirements generally are the same. To illustrate what provisions are found in a plan agreement, a summary of the contents of IRS Forms 5305 and 5305-A for Traditional IRAs follows.

Article IThe financial organization agrees not to accept more than the maximum annual amount ($5,500 for 2017 and for 2018, plus catch-up contributions, if eligible) in cash IRA contributions from an IRA owner for any tax year. The only exceptions are rollover, transfer, or simplified employee pension (SEP) contributions.

NOTE: The annual contribution limit applies in aggregate to all Traditional IRA and Roth IRA contributions made for a tax year. (IRC Sec. 408A(c)(2)).

Opening an IRA • 15

Article IIThe IRA owner’s interest in the IRA is nonforfeitable. The IRA owner has a right to all the IRA assets at any time as long as she is willing to pay any applicable taxes and penalties associated with the withdrawal.

Article IIICertain types of investments may not be held within an IRA. IRA assets may not be invested in life insurance contracts. IRA assets may not be commingled with any other property except in a common trust fund or a common investment fund within the meaning of IRC Sec. 408(a)(5).

IRA assets may not be invested in collectibles such as antiques, art, gold, silver, wines, etc. As a result of the Tax Reform Act of 1986, however, IRA owners are permitted to invest in certain gold and silver coins minted in the U.S. after 1985. Under the Technical and Miscellaneous Revenue Act of 1988, IRA owners also may invest in certain state issued coins. Under the Taxpayer Relief Act of 1997, effective January 1, 1998, certain platinum coins and certain gold, silver, platinum, or palladium bullion are allowed as an IRA investment as long as the bullion or coin(s) is in the possession of the financial organization (IRC Sec. 408(m)(3)).

Article IVIRA distributions must be made according to Internal Revenue Code requirements and final Treasury regulations once an IRA owner reaches his 70½ year. These required minimum distributions (RMDs) must begin by the IRA owner’s required beginning date of April 1 of the year following the IRA owner’s 70½ year. Article IV provides the formula for determining RMD amounts and lists the options an IRA owner has for taking these distributions.

An IRA owner who has two or more IRA plans may satisfy her RMD requirement by taking from one IRA the amount required to satisfy the RMD from another IRA.

Article IV also lists the options available to IRA beneficiaries upon the death of the IRA owner. These options also may be addressed in Article VIII.

Article VThe IRA owner agrees to supply the financial organization with the necessary information for reporting transactions to the IRS. The financial organization then agrees to do the required reporting.

Article VIArticles I through III of the plan agreement are the controlling articles in the IRA plan agreement.

Article VIIThe financial organization agrees to keep the plan agreement current by amending the plan agreement for law changes.

Article VIIIThe IRS does not draft Article VIII language for Forms 5305 and 5305-A (article IX in the Roth IRA model documents). Article VIII in these forms is left blank to allow the financial organization to add any provisions that comply with state law and the Internal Revenue Code. The IRS notes under Article VIII that the added language cannot imply that it has been reviewed or approved by the IRS.

16 • Opening an IRA

Fewer and fewer financial organizations feel the need to offer a prototype IRA because of the great flexibility offered by Article VIII. In the instructions to the model Forms 5305 and 5305-A, the IRS provides examples of some of the provisions that may be addressed in Article VIII or subsequent articles (all referred to as Article VIII in this discussion). Adding Article VIII language, while recommended, is not mandatory.

DefinitionsArticle VIII frequently begins with a list of definitions of the terms used in the section.

Investment PowersThe financial organization may add a provision to Article VIII enumerating the types of investments the financial organization will permit as IRA investments. Article VIII can include language granting the trustee or custodian specific powers necessary to manage the investments within the IRA or language giving the IRA owner exclusive control over investments.

Voting RightsIf a financial organization holds securities, it may wish to enter into a separate agreement with the IRA owner as to who will exercise voting rights for the stock.

Exculpatory ProvisionsThe financial organization may wish to state in Article VIII that it will rely on all information provided by the IRA owner and that any consequences resulting from doing so will be borne by the IRA owner. For instance, if an IRS report is incorrectly filed because of erroneous data provided by the IRA owner, the financial organization should not bear the expense of any fines relating to that incorrect report.

Another area of liability frequently addressed in Article VIII is the responsibility for investment performance. The financial organization typically is not responsible for the investment performance of the assets held by the IRA. Particularly where the IRA owners are allowed to self-direct or select their own investments, Article VIII should be enhanced to clarify that the financial organization will not be liable for the performance of investments selected by the IRA owner.

Amendment and TerminationArticle VIII may include language on how the plan will be amended and how either the IRA owner or the financial organization may terminate the agreement.

Removal of TrusteeA financial organization may, for various reasons, wish to resign as the trustee or custodian of an IRA. Conversely, an IRA owner may wish to remove a current trustee or custodian. (This operation generally is handled as a transfer or rollover.) Article VIII may contain a provision establishing both the financial organization’s and the IRA owner’s right to terminate the relationship at any time and also delineating the method of termination.

Trustee’s FeesMost financial organizations want the ability to initiate new fees and penalties, should it be necessary, after the IRA is opened. The procedures for introducing new fees could be addressed in Article VIII. For example, a financial organization could add language allowing additional fees (not described in the financial disclosure) to be imposed following 30 days notice to the IRA owner.

Opening an IRA • 17

Some plan agreements also add language permitting the financial organization to remove assets from the IRA to satisfy fees, including the liquidation of certain assets if cash is not available within the IRA.

State Law RequirementsState law also may affect IRAs. The financial organization may list specific laws that could affect the IRA owner’s maintenance of the IRA.

DistributionsA financial organization that wishes to modify the Article IV language governing distributions may do so in Article VIII.

Accepting Only CashFinancial organizations offering self-directed IRAs may wish to clarify the Article I requirement that only cash contributions will be accepted into the IRA except in the case of a rollover or transfer. The trustee generally will then purchase the investment for the IRA trust.

Excess Contribution TreatmentThe consequences of making excess contributions usually are handled in the IRA disclosure statement. But if the financial organization wishes to clarify its own procedure, the procedure may be explained in Article VIII.

Prohibited Transactions With the IRA ownerAlthough prohibited transactions are explained in the disclosure statement, information on the financial organization’s responsibility when an IRA prohibited transaction occurs may be described in Article VIII.

Most forms providers will draft extensive Article VIII language to assist the financial organizations that use their forms. This language will vary from provider to provider. Financial organizations should carefully check the Article VIII provisions to make sure the language meets their needs and does not mandate procedures that they are not prepared to follow.

Proof of Plan Agreement ReceiptThe IRS requires that an IRA owner receive a written document containing the terms and conditions of the plan agreement. The IRS may assess a monetary fine against the financial organization if it cannot offer proof that the IRA owner (either Traditional or Roth) received the plan agreement. The Internal Revenue Code states that a $50 penalty applies for each failure to provide a plan agreement (IRC Sec. 6693(a), Treas. Reg. 1.408-6(d)(4)(ix)).

To prove that the IRA owner received the document, the financial organization should have the IRA owner sign and date a copy of the plan agreement or an acknowledgment that he received a copy of the plan agreement. Often the acknowledgment is found as part of the signature section on the IRA application. The financial organization should retain the signed copy or acknowledgment in the IRA owner’s file as the required proof.

See “Electronic Signature” in Chapter 3, IRA Withholding, for laws regarding electronic signatures.

18 • Opening an IRA

Nonbank Trustee or Custodian Approval LetterWhen an entity is approved as a nonbank trustee or custodian, it will receive written notice of approval from the IRS that will specify the day on which approval is effective. The entity must not serve as a trustee or custodian before the effective date and cannot serve as an IRA trustee or custodian unless it has provided the IRA owner with a copy of the approval letter (Treas. Reg. 1.408-2(e)(7)(iii)). The approval letter, therefore, must be provided to the IRA owner on or before the IRA plan agreement is signed by the IRA owner and the trustee/custodian.

IRA Disclosure Statements

Each individual opening an IRA (either Traditional or Roth) must receive a disclosure statement in addition to the plan agreement. The disclosure statement consists of two parts: a nontechnical explanation of the IRA rules and a financial disclosure. Disclosure statement (and financial disclosure) requirements similar to those that apply to Traditional IRAs also apply to Roth IRAs.

Disclosure Statement Contents Treas. Reg. 1.408-6(d)(4)(iii) specifies the information that must be contained in a disclosure. Some of the key items that a disclosure statement must contain include the following.

• An explanation of the statutory requirements that pertain to an IRA

• An explanation of the tax consequences of establishing an IRA, including the deductibility of contributions, the tax treatment of distributions, the availability of income tax-free rollovers, and the tax status of IRAs

• An explanation of the limitations and restrictions on some IRA contributions

• An explanation of the circumstances under which an IRA owner may revoke the IRA

• A statement that a prohibited transaction will cause an IRA to lose its tax exemption, which results in the untaxed funds being included in gross income

• A statement that all or any portion of an IRA that is used as security for a loan is considered to be distributed, and that untaxed amounts are taxable in the year of distribution

• Statements explaining the reasons for and results of the early distribution, excess contribution, and excess accumulation penalties

• A statement explaining distributions, including required minimum distributions

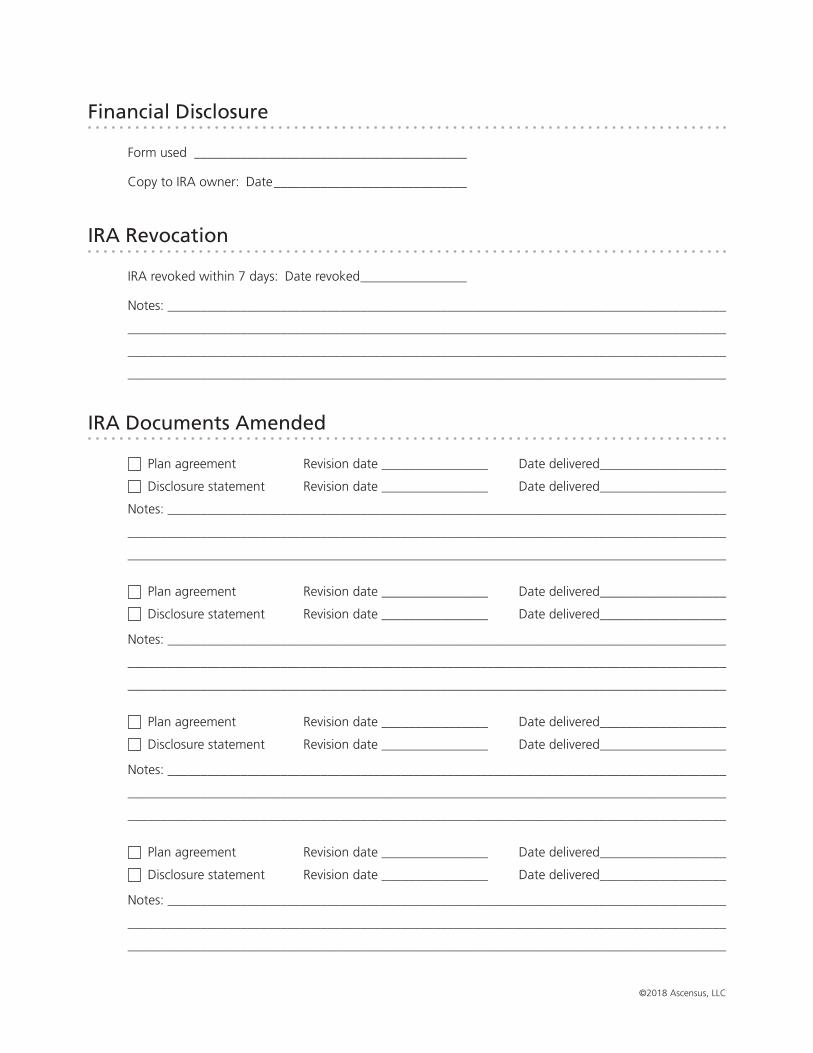

Right of RevocationBoth Roth and Traditional IRA owners generally must have the right to revoke a newly established IRA plan for seven calendar days following receipt of the IRA disclosure statement. The intent of the right of revocation is to give IRA owners time to compare IRAs offered through various financial organizations, as well as time to review the IRA provisions. A financial organization must distribute the disclosure statement to the IRA owner on or before the establishment of the IRA.

If the financial organization distributes the disclosure statement within seven days before the establishment of the IRA, the financial organization must permit the IRA owner to revoke the IRA for a period of seven days following the date of establishment (Treas. Reg. 1.408-6(d)(4)(ii)(A)(2)). The method of revocation, either written, oral, or both, must be described in the disclosure statement.

Opening an IRA • 19

See Chapter 4, IRA Reporting, for information on how to report IRA revocations.

IRA Owner Must Follow Proper Notice Procedures – If an individual revokes her IRA, she must notify the financial organization according to the procedures outlined in the disclosure statement. This information must be prominently displayed at the beginning of the disclosure statement. The disclosure statement will note whether the revocation must be written, delivered orally, or whether both written and oral notices are required. If a written notice is mailed, the procedure must note that it will be deemed mailed on the date of the postmark provided that the notice was properly mailed. If an oral notice is used, the procedure must permit a telephone call during business hours.

Entire Contribution Must Be Returned – Once the individual revokes the IRA using the proper procedures, he is entitled to a return of the entire contribution amount used to open the IRA. No adjustments may be made for sales commissions, administrative expenses, fluctuations in market value, etc. But a financial organization may establish a policy of returning earnings on a revoked IRA.

The IRA Financial DisclosureThe financial disclosure is an essential part of the disclosure statement and must reflect specific IRS assumptions (Treas. Reg. 1.408-6(d)(4)(v), (vi) and (vii)). Financial organizations have been fined by the IRS for providing improper financial projection information or for providing no information at all. The financial projections required by the IRS combine actual investment information with hypothetical assumptions. This projection informs IRA owners of the IRA’s projected growth, based on certain assumptions, and of any fees that may be charged or penalties that may be assessed against the IRA.

Financial Disclosure PurposeThe financial disclosure is completed when an IRA (either Traditional or Roth) initially is opened and is intended to be a consumer information device. Once the financial organization has entered the required information, the individual, ideally, may take the financial disclosure to compare to other financial organization’s fees and penalties and to secure the best investment for her IRA dollars.

Financial Disclosures When Growth Can Be ProjectedTo make the comparison between financial organizations’ IRAs easier for an individual, the IRS, in the Treasury regulations and Revenue Ruling 86-78, lists certain assumptions that must be used in every financial disclosure where (1) certain amounts are guaranteed over time, or (2) where a projection of growth in the IRA’s value can reasonably be made. If financial organizations can reasonably project the growth of the IRA assets, the assumptions for the financial disclosure are as follows.

• Contribution – When an individual establishes an IRA with a regular, spousal, or SEP contribution, the financial projection is based on an assumption that the IRA owner will make an annual $1,000 deposit on the first day of each year, regardless of the actual contribution made. When an individual establishes an IRA with a rollover or transfer contribution, the financial projection is based on an assumption that the IRA owner will make a one-time, $1,000 deposit on the first day of the year in which the contribution actually is made.

• Age Used – Financial organizations should base the financial disclosure on the age the IRA owner will attain in the year the disclosure is being completed.

• Investment Instrument – Use the type of investment instrument selected by the IRA owner.

• Term of Certificate – If a time deposit is the selected investment, use the actual length of the time deposit in projecting any loss of earnings penalty.

20 • Opening an IRA

• Interest Rate – Use an interest rate no greater than that which is currently in effect. The interest rate must remain the same for the entire projection.

• Compounding Method – Use the actual or a less frequent compounding method, if applicable.

• Loss of Earnings Penalty or Fee – Show the account value for each of the projected years, taking into consideration any applicable loss of earnings penalty or other fee that the financial organization would assess if the IRA owner received a distribution at the end of the year for which the projection is being made.

• First Five Years – Show the IRA’s value at the end of each of the first five years during which contributions are to be made.

• Account Value at Ages 60, 65, and 70 – Show the IRA’s value at the end of the years in which the IRA owner will attain ages 60, 65, and 70.

Financial Disclosures When Growth Cannot Be Projected – When an IRA owner chooses mutual funds, stocks, bonds, certain variable annuities, or similar investments as the initial investments within an IRA, an accurate earnings projection is not possible. Because the growth for these types of IRAs cannot be reasonably projected, these financial disclosures have different requirements.

• Give a general description of the investments associated with this type of IRA.

• Give a general description of the fees that the financial organization may apply to the IRA.

• Give a general description of how the financial organization computes the earnings on the available investments, including a statement that the IRA’s growth in value is neither guaranteed nor projected.

• Provide any other information that may aid the IRA owner, including all other investment information. This information must include any relationship between the financial organization and an affiliated brokerage firm, and the procedures to request an investment transaction.

Financial Disclosures for IR Annuities – An IR annuity can be invested in certain underlying investments allowed under the annuity contract. And depending on the type of annuity, different requirements apply for providing the financial disclosure. With a fixed annuity, the annuitant must receive a completed financial disclosure using the method when growth can be projected or when it cannot, as applicable. But with a variable annuity, financial organizations must provide a financial disclosure generally based on when the growth cannot reasonably be projected.

A fixed annuity earns interest at a rate determined by the insurance company or as described in the annuity contract. The initial rate of return is described and determined under the terms of the annuity contract. If the annual renewal rate differs from the initial guaranteed rate of interest, the renewal rate is either determined by the insurance company or described in the annuity contract. With a fixed annuity contract, the insurance company always agrees to pay a minimum guaranteed rate of return for the life of the contract.

With a variable annuity, the annuitant determines how the IR annuity assets are invested from a list of fund choices (sub-accounts) determined by the insurance company (like a mutual fund). Fund choices may range from fairly conservative funds to aggressive stock funds. It is a securities investment and, unlike a fixed annuity, there is no guaranteed rate of return. The account value can increase or decrease based on the performance of the investment funds selected under a particular contract.

Opening an IRA • 21

Proof of Disclosure Statement ReceiptAs described, the content of the entire disclosure statement and when the disclosure statement must be provided is specified in the Treasury regulations. The financial organization must be able to prove that an IRA owner has received a copy of the disclosure statement (including both the nontechnical explanation of the IRA rules and the financial projection) or be subject to a $50 per failure penalty (IRC Sec. 6693(a), Treas. Reg. 1.408-6(d)(4)(ix)).

To prove an IRA owner received a copy of the disclosure statement, the IRA administrator should have the IRA owner sign and date a copy of the statement and keep it in the IRA owner’s file. Alternatively, the IRA owner may sign a statement acknowledging receipt of the disclosure statement. This acknowledgment often is a part of the IRA application. When an individual acknowledges receiving the disclosure statement, the acknowledgment usually includes the financial disclosure.

Customer Identification Program Requirements