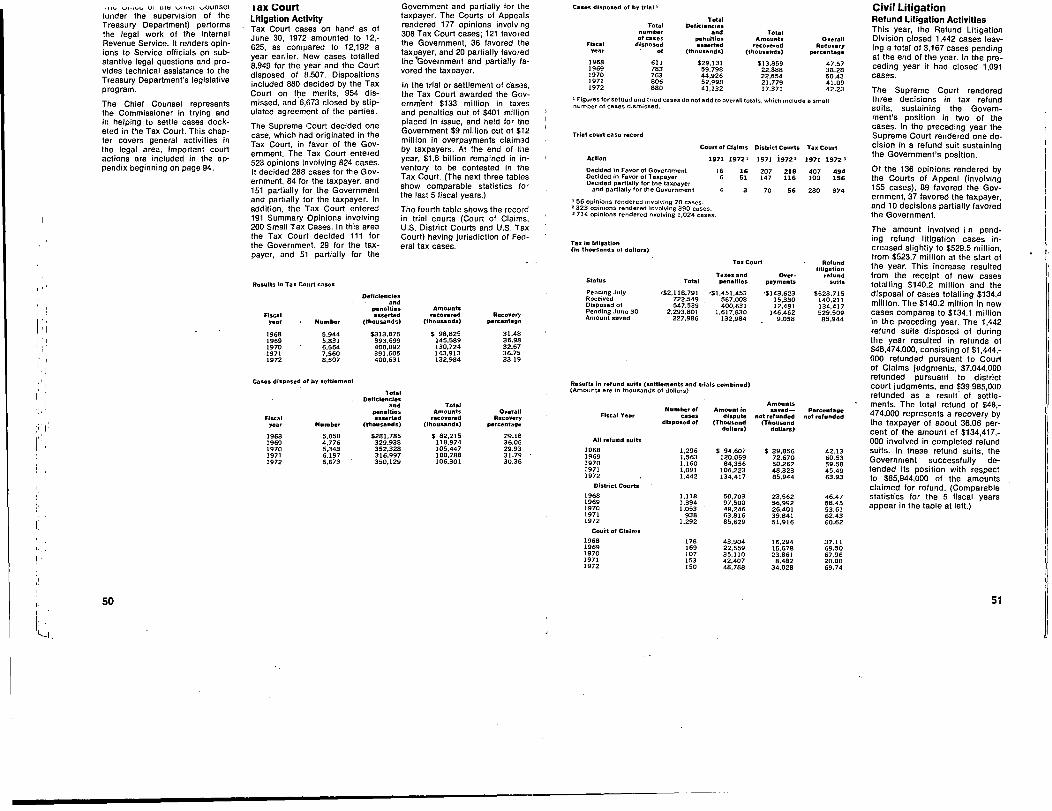

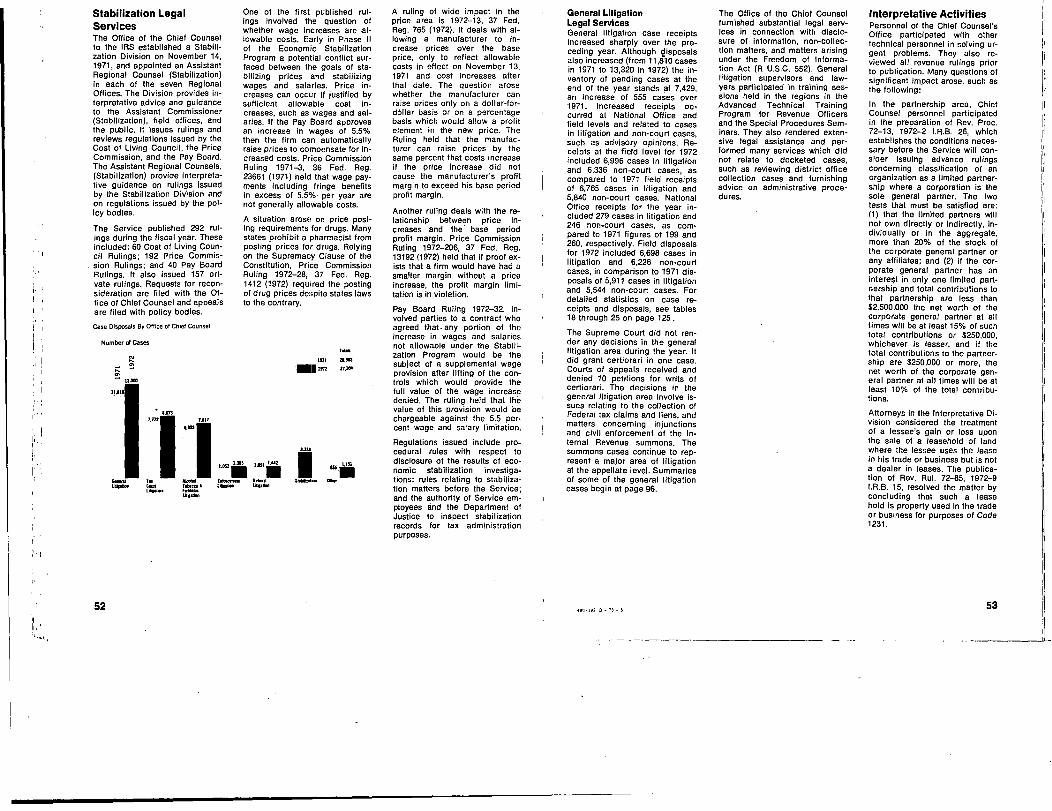

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

I

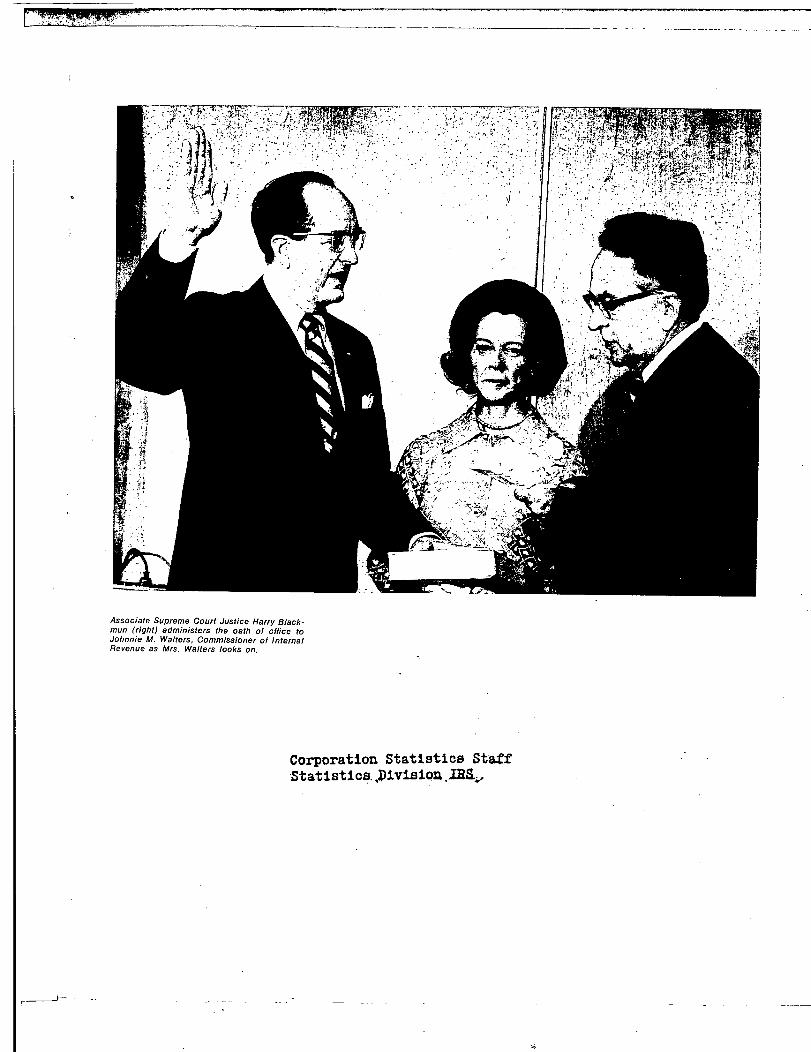

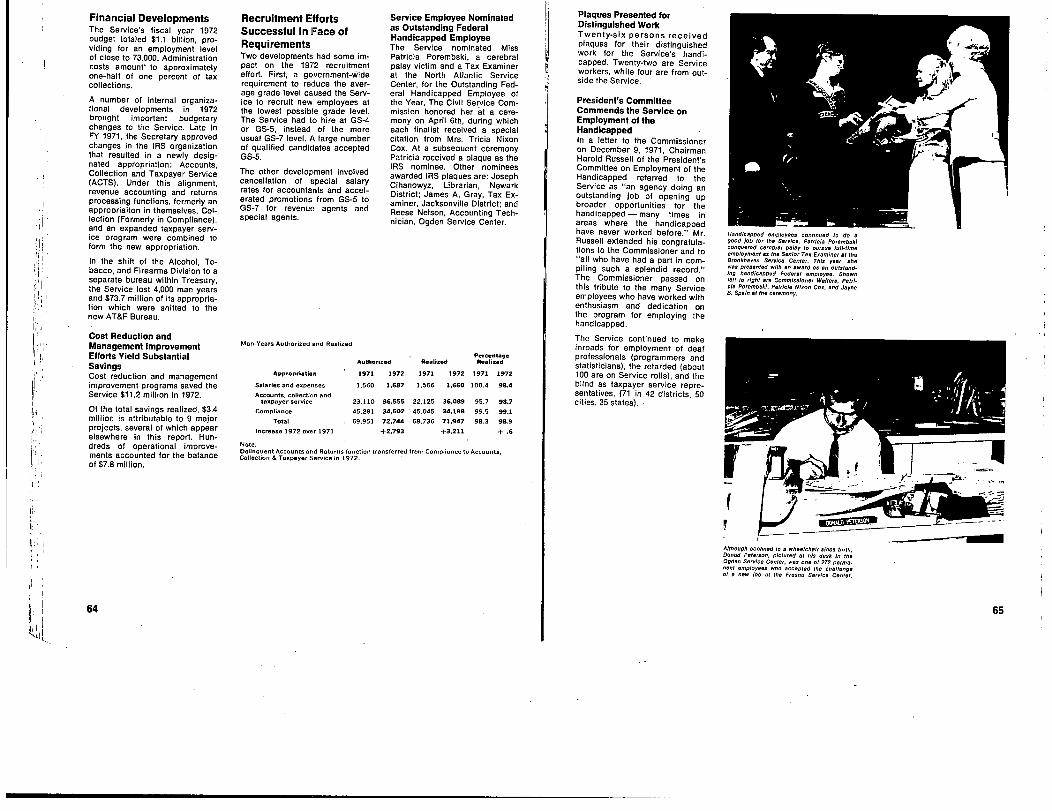

Associate Supreme Court Justice Harry Black-mun (right) administers the oath of office toJohnnie M. Walters, Commissioner of InternalRevenue as Mrs . Walters looks on.

Corporation Statistics StaffStatistics. 'Divisiou .m.,

1;

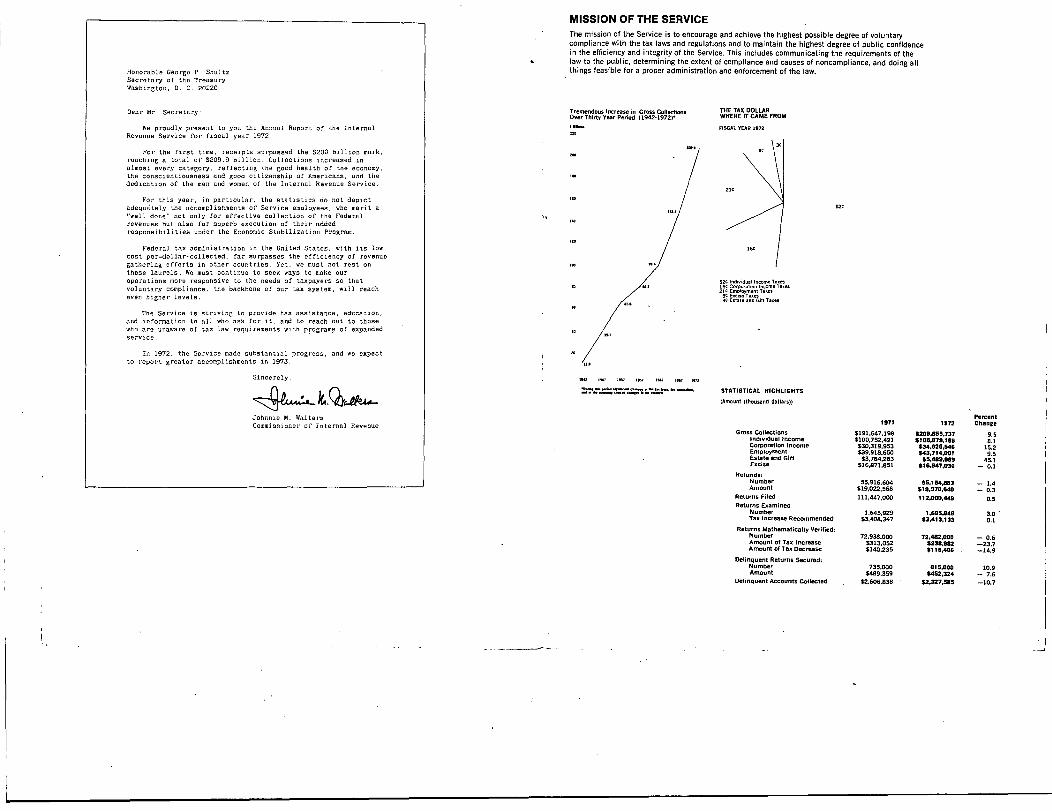

Honorable George P . ShultzSecretary of the Treasury

Washirgton . D . C . 2022 0

Dear Mr . Secretary :

We proudly present to you the Annual Report of the InternalRevenue Service for fiscal year 1972 .

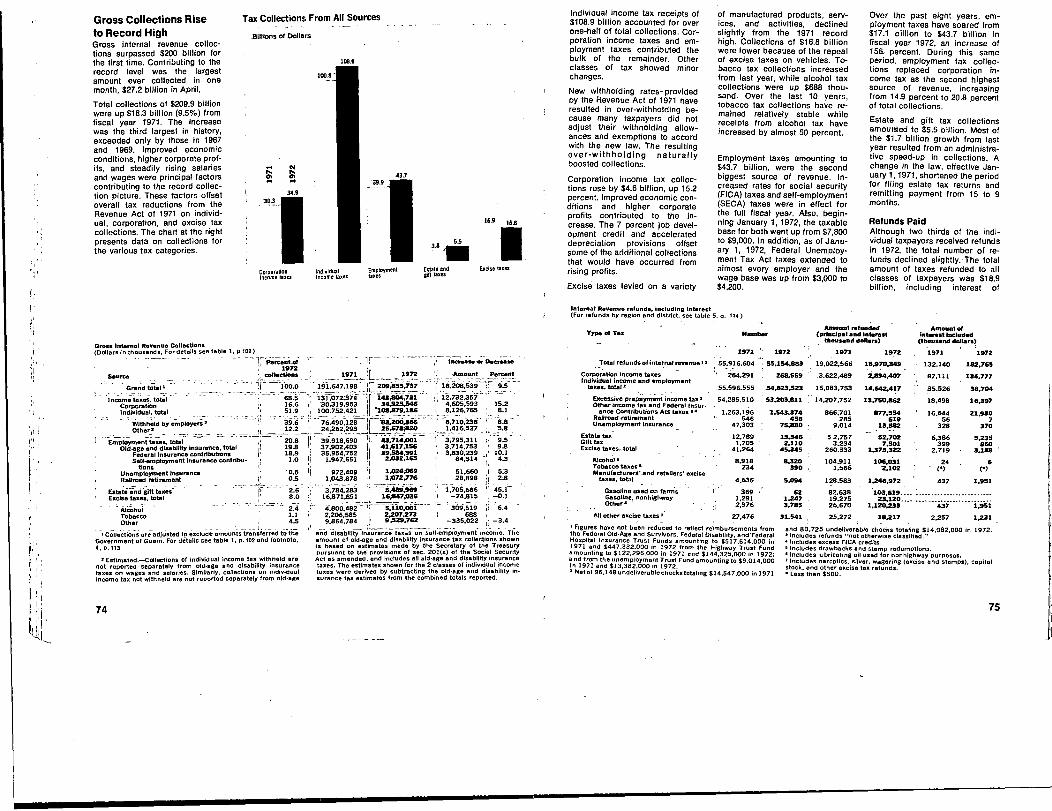

For the first time . receipts surpassed the $200 billion mark,reaching a total of S209 .9 billion . Collections increased inalmost every category, reflecting the good health of the economy,the conscientiousness and good citizenship of Americans, and thededication of the men and women of the Internal Revenue Service .

For this year . in particular . the statistics do not depict

adsqudtely the accomplishments of Service employees, who merit a

"well done" not only for effective collection of the Federalrevenues but also for superb execution of their addedresponsibilities under the Economic Stabilization Program .

Federal tax administration in the United States, with its lowcost per-dollar-collected, fir surpasses the efficiency of revenuegathering efforts in other countries . Yet, we must not rest onthese laurels . We must continue to seek ways to make ouroperations more responsive to the needs of taxpayers so that

voluntary compliance, the backbone of our tax system, will reacheven higher levels .

The Service is striving to provide tax assistance, education,and information to all who ask for it, and to reach out to thosewho are unaware of tax law requirements with pFograms of expandedservic e

In 1972, the Service made substantial progress . and we expectto report greater accomplishments in 1973 .

Sincerely ,

Johnnie M . WaltersCommissioner of Internal Revenue

MISSION OF THE SERVICEThe mission of the Service is to encourage and achieve the highest possible degree of voluntarycompliance with the tax laws and regulations and to maintain the highest degree of public confidencein the efficiency and integrity of the Service . This includes communicating the requirements of thelaw to the public, determining the extent of compliance and causes of noncompliance, and doing allthings feasible for a proper administration and enforcement of the law .

Tremendous Increase in Gross CollectionsOver Thirty Year Period (1942-1972)-

1 .

.I.

- - 11. 1- 1- .1. .1n

THE TAX DOLLARWHERE IT CAME FROM

IFISCsn- YEAR 1972

5. rdn,idn.l In... T.-

Eiic". T .-

3C Eanst, and Gin T-

STATISTICAL HIGHLIGHTS

(Amount (thousand dollars))

WC

Percent1971 1972 Chang e

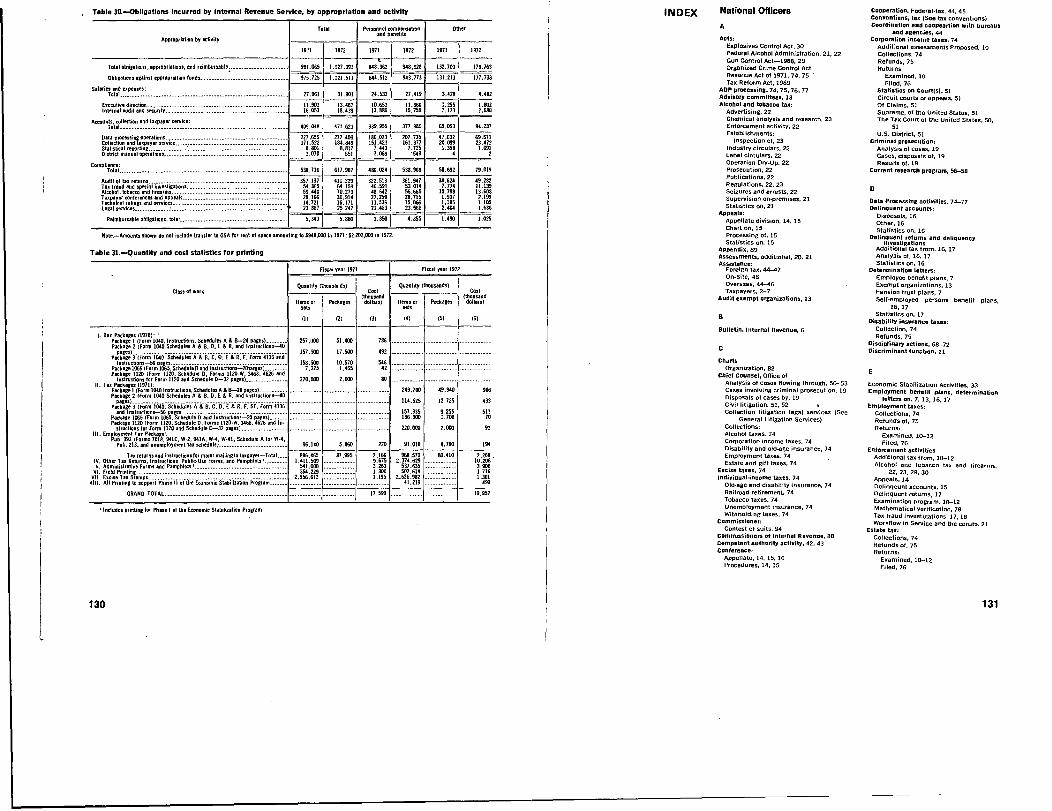

Gross Collections $191 .647.198 $209,835,737 9.5Individual Income $100,752.421 $10SX79.186 8 .1Corporation Income $30,319,953 $3,11,925.546 15 .2Employm m S39,918.650 $43,714.001 9 .5Estate end Gift $3,784.283 $5,489,969 45 .1Exci se

$16,871,851 $16 .047,036 - 0 .1Rotunda-,

gumbin, 55,916,604 55,154,883 - 1.4Amount $19,022,568 $11111970.6.40 - 0.3

Returns Filed 111,447,000 112,000,449 0.5Returns Examined

Number 164592 1695,11148 30

Tax Increases Recommended $3 :408:3479 $3,413 133 D'AReturns Mathematically Verified :

Number 72,938.000 72,482,000 - 0.6Amount of Tax Increase $313,052 $238,982 -23.7Amount of Tax Decrease $140 .235 $110,408 -14.9

Delinquent Returns Secured :Num r 735,DOO 815,000 10.9Amount $489,359 $452,324 - 7.6

Delinquent Accounts Collected . $2.606,838 $2.327,505 -10.7

REPORT ON OFFICERS

Informing and Assisting TaxpayersEnforcement Activities / 9Special Enforcement Activities / 25Economic Stabilization Activities / 33International Activities / 41Legislative and Legal Activities / 49Planning Activities / 5 5Internal Management and Support Activities / 63Receipts, Refunds and Returns Filed / 73

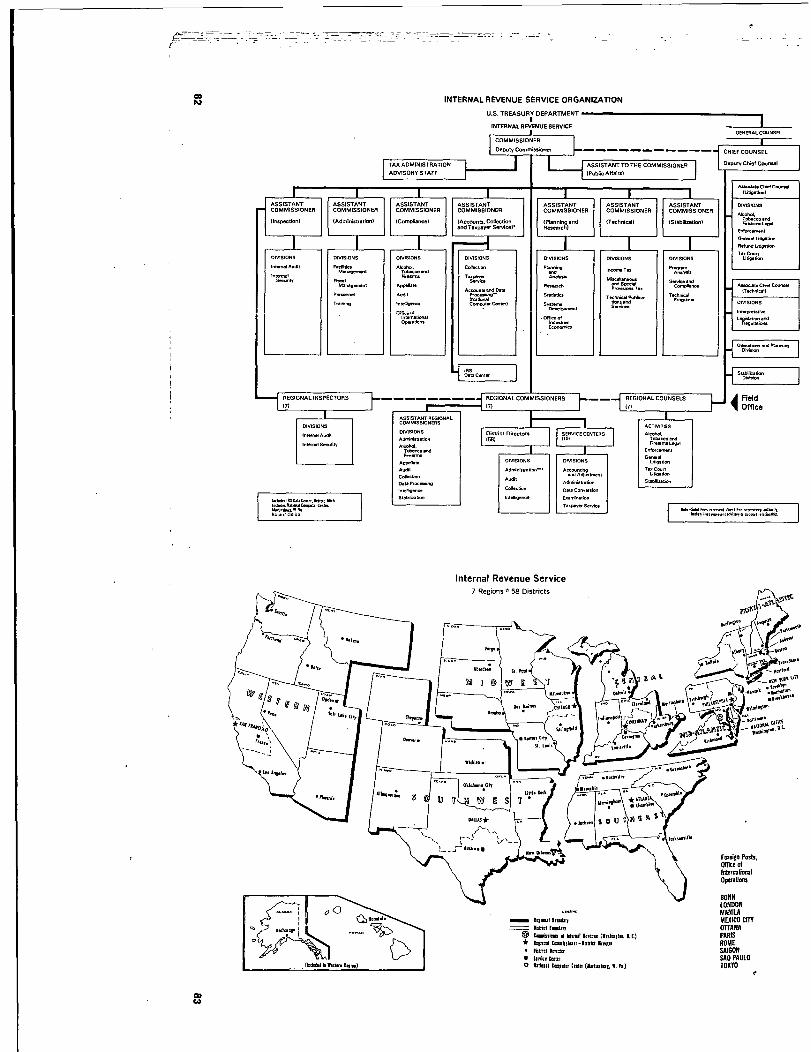

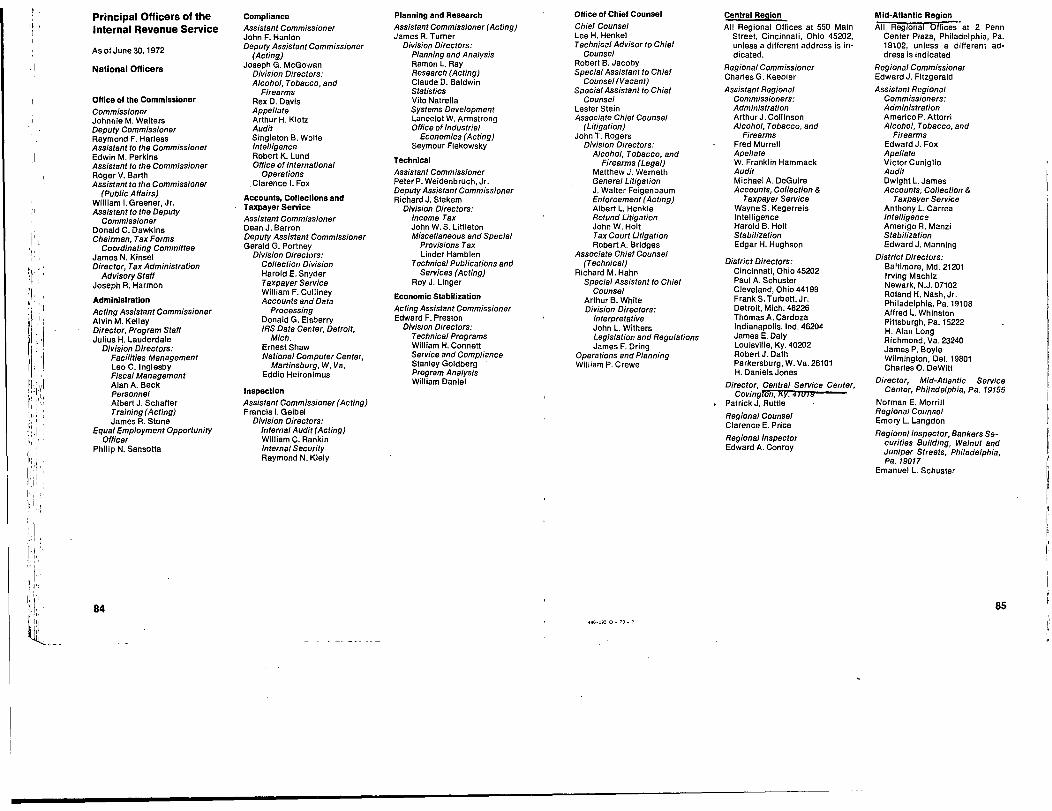

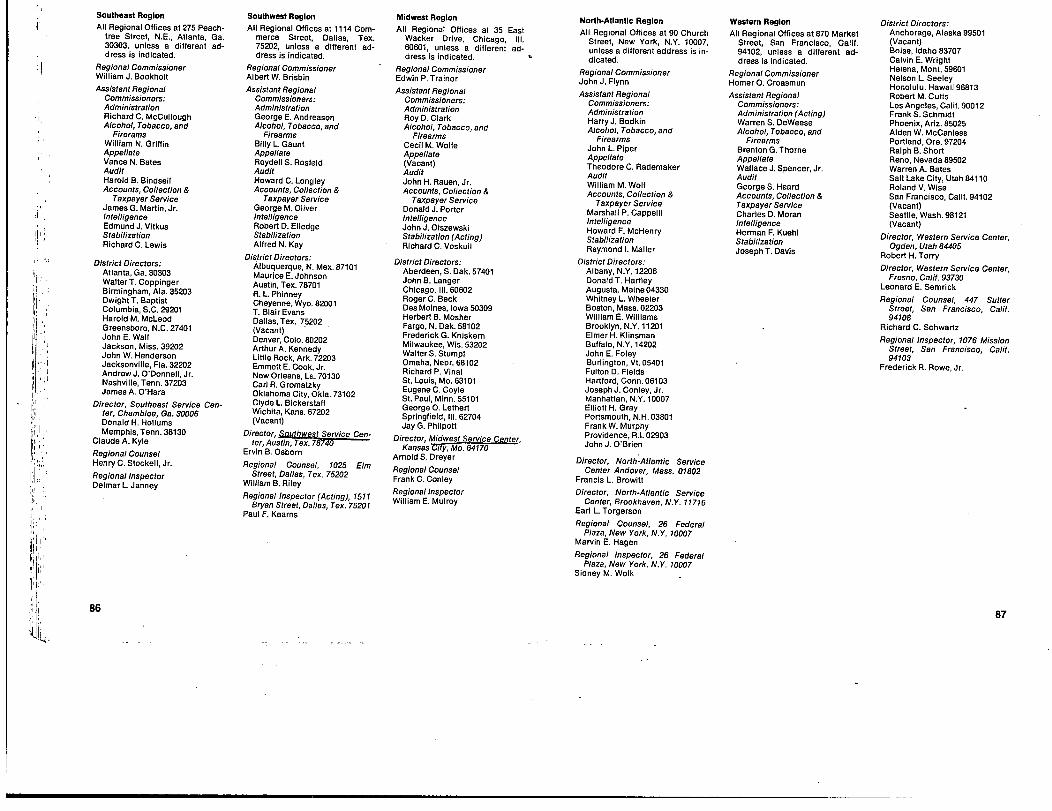

ORGANIZATION-PRINCIPAL OFFICERS

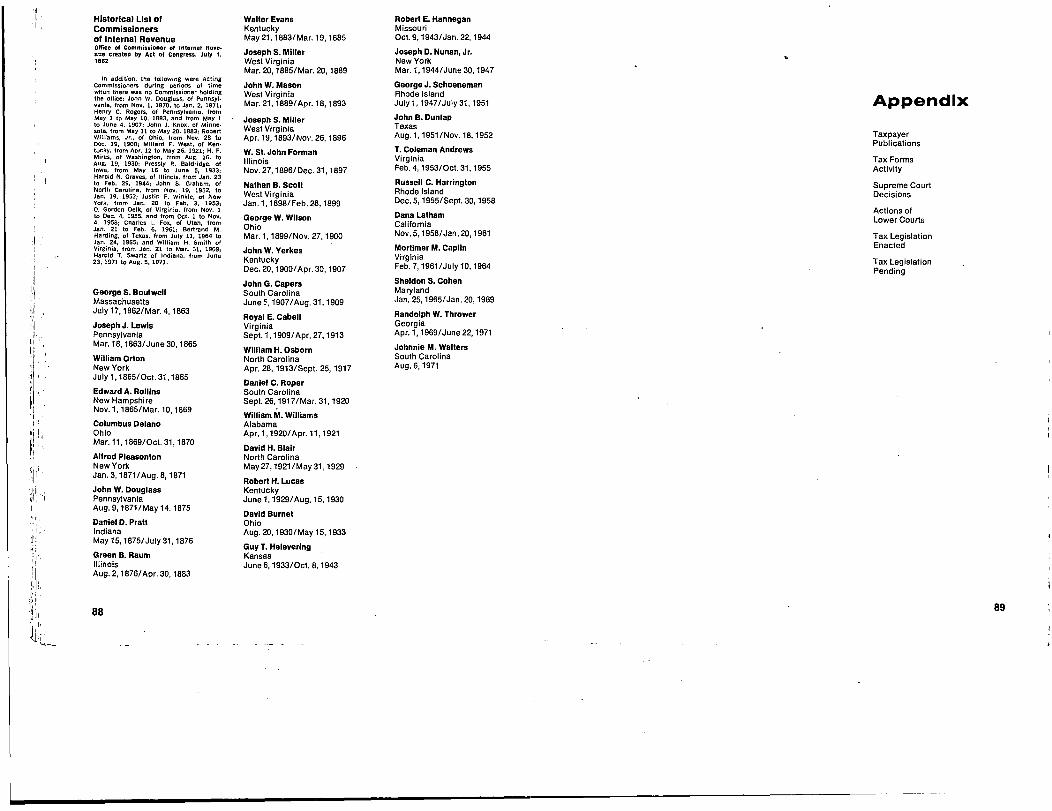

Organization ofthe Internal Revenue Service / 82Internal Revenue Regions and Districts / 83Principal Officers / 84Historical List of Commissioners / 88

APPENDIXTaxpayer Publications / 96TaxFormActivity / 92CourtDecisions 94Statistical Tables 10 3

NotesAll yearly data are on a fiscal yearbasis, unless otherwise specified . Forexample, data headed "1972" per-tain to the fiscal year ended June 30,1972 and "July 1" inventory itemsunder this heading reflect inventoriesas of July 1, 1971 .

In many tables and charts, figures

have been rounded and may not addto the totals which are based on un-rounded figures .

For sale by the Superintendent ofDocuments, U .S . Government PrintingOffice, Washington. D .C. 20402. Price$1 .75 (paper cover)-domestic post-paid, or$1 .50 GPO BookstoreStock Number 48D4-00591

New Dimensionsin Taxpayer ServiceAs part of the Service's continu-ing commitment to increase as-sistance to taxpayers and im-prove forms and instructions,Commissioner Walters ordered astudy to determine the feasibilityof reintroducing the short-formincome tax return (Form 1040A) .The study produced a simplifiedhalf-sheet size form for reporting1972 taxes which can be used bymore than 30 million taxpayers,or 40 percent of individual in-come tax filers. The RevenueAct of 1971 made an abbreviatedform especially practical becauseof an increase in the standarddeduction and extension of theoptional tax tables to more tax-payers . A simplified form alsowas desirable because of an in-creasing public reliance on com-merical returns preparers, espe-cially among lower income tax-payers. -

In 1972, the Service responded tomore than 41 million taxpayersseeking information and assist-ance with tax matters . Over 19million persons telephoned,about 9 million visited Serviceoffices, and almost 300,000 morewrote. The Service reached 13million through various educa-tional programs .

The Service provided prompt tax-payer assistance through a vari-ety of methods . Centiphone, asystem of toll-free telephonelines to Service offices, wasavailable to taxpayers in 27states . Nationwide, the Servicegave assistance at shopping cen-ters, public libraries, at taxmo-biles stationed at strategic loca-tions to assist low-income tax-payers and senior citizens, andat military installations, nursinghomes, hospitals and other insti-tutions . The Service increasedthe tempo of its assistance to-ward the close of the filing periodby adding more employees to theprogram and extending officehours . It helped more than 500,-000 taxpayers who visited Serviceoffices during the last six days ofthe 1972 filing season .

Taxpayer EducationAids MillionsThis year Service-sponsored tax-payer education programs helpedmore than 13,000,000 taxpayers .

Teaching Taxes, the largest Serv-ice taxpayer education program,provided materials and instruc-tion to 4 .1 million students in23,000 secondary schools. TheTeaching Taxes Program explainsthe tax system and teaches stu-dents to prepare accurate taxreturns .

Tax practitioner Institute pro-grams dealing with tax situationsof farmers, military personneland the general public providedtraining to 54,000 participantswho in turn assisted nearly8,000,000 taxpayers . The Vol-unteer Income Tax Assistance(VITA) Program trained volun-teers who then assisted 300,000low-income and other disadvan-taged taxpayers such as thosewith language problems, theblind, and the deaf . VITA is aprogram in which IRS employeestrain volunteers from the commu-nity to assist disadvantaged tax-payers in preparing their returns.Through VITA, members of di-verse organizations such as com-munity action groups, churches,colleges, and retirement organi-izations assisted taxpayers incommunity centers, Indian reser-vations, churches, store-fronts,hospitals, and elsewhere. Also aspart of the VITA program, the In-stitutes of Lifetime Learning co-ordinated with the Service inproviding assistance to 53,000elderly and retired taxpayers in317 cities . Other national organ-izations will be contacted nextyear to develop similar programsfor their groups .

Many junior colleges, colleges,and universities offered theTeaching Business Taxes Pro-gram with material provided bythe Service. In 1972, some 14,000students in economics, business,and accounting received instruc-tions through this program inpreparing tax forms filed forsmall businesses and corpora-tions.

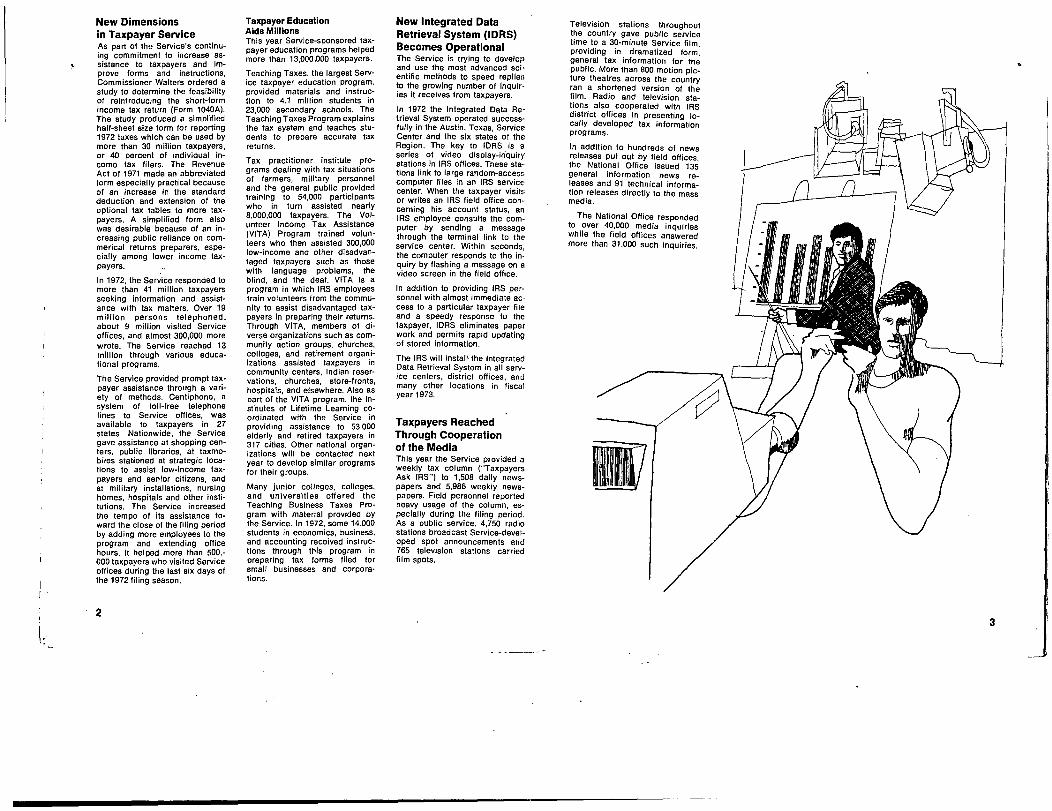

New Integrated DataRetrieval System (IDRS)Becomes Operationa lThe Service is trying to developand use the most advanced sci-entific methods to speed repliesto the growing number of inquir-ies it receives from taxpayers .

In 1972 the Integrated Data Re-trieval System operated success-fully in the Austin, Texas, ServiceCenter and the six states of the)Region . The key to IDRS is aseries of video display-inquirystations in IRS offices . These sta..tions link to large random-accesscomputer files in an IRS service,center. When the taxpayer visits ;or writes an IRS field office con .cerning his account status, anIRS employee consults the com. .puter by sending a messagethrough the terminal link to theservice center . Within seconds,the computer responds to the in-quiry by flashing a message on avideo screen in the field office.

In addition to providing IRS per-sonnel with almost immediate ac-cess to a particular taxpayer fileand a speedy response to thetaxpayer, IDRS eliminates paperwork and permits rapid updatingof stored information .

The IRS will install the IntegratedData Retrieval System in all serv-ice centers, district offices, andmany other locations in fiscalyear 1973.

Taxpayers ReachedThrough Cooperationof the MediaThis year the Service provided aweekly tax column ("TaxpayersAsk IRS") to 1,508 daily news-papers and 5,986 weekly news-papers . Field personnel reportedheavy usage of the column, es-pecially during the filing period .As a public service, 4,750 radiostations broadcast Service-devel-oped spot announcements and765 television stations carriedfilm spots .

Television stations throughoutthe country gave public servicetime to a 30-minute Service film,providing in dramatized form,general tax information for thepublic . More than 800 motion pic-ture theatres across the countryran a shortened version of thefilm . Radio and television sta-tions also cooperated with IRSdistrict offices in presenting lo-cally developed tax informationprograms .

In addition to hundreds of newsreleases put out by field offices,the National Office issued 135general information news re-leases and 91 technical informa-tion releases directly to the massmedia .

The National Office respondedto over 40,000 media inquirieswhile the field offices answeredMore than 31,000 such inquiries .

23

Taxpayer PublicationsExplain the Tax LawThe Service produces severalforms of interpretative publica-tions which explain the tax law innon-technical language. Servicepersonnel revise most of thesepublications annually to reflectchanges in the law, adding newpublications from time to timeand discontinuing others .

The Superintendent of Docu-ments of the Government Print-ing Office and IRS offices handlethe distribution and sales of tax-payer publications. This year,many local offices of the PostalService also sold "Your FederalIncome Tax" and "Tax Guide forSmall Business ." These are twoof the more popular publicationsand the only ones not distributedfree of charge .

"Your Federal Income Tax" con-tinues as one of the Govern-ment's best selling publicationswith 1,873,654 copies sold thisyear .

Service technicians rearrangedthe "Tax Guide for Small Busi-ness" to discuss in sequence thestarting, operating, and dispos-ing of a small business . The pub-lication also covers differences intax treatment of sole proprietor-ships, partnerships, corporations,and electing small business cor-porations .

This year the Service developedfour new publications : "Tax In-formation on United States Sav-ings Bonds," Publication 576 ;"Amortization of Pollution Con-trol Facilities," Publication 577 ;"Guides for Qualification of Pen-sion, Profit-Sharing, and - StockBonus Plans" Publication 778 ;and a Spanish language versionof "Information for Preparationand Filing of the Individual Fed-eral Income Tax Return," Publica-lion 579. For a list of titles of tax-payer publications see page 93 .

Public Informed onEconomic StabilizationProgra min suppgrt of the office of Em-ergency Preparedness, duringPhase I of the President's Eco-nomic Stabilization Program, theService responded to almost8,000 media inquiries ; participat-ed in 68 news conferences, 614radio and 330 television pro-grams ; furnished public speakerson 557 occasions ; and issued 746news releases. A weekly eco-nomic stabilization question andanswer column provided informa-tion to the public through 8,000daily and weekly newspapers .With the move into Phase 11 theService stepped up its informa-tion efforts and issued 1,367 newsreleases publicizing regulationsand informing the public of mat-ters of general interest . The Serv-ice responded to 11,004 mediainquiries ; participated in 58 newsconferences, 784 radio programs

Each year the Samice publishes a number of

Pamphlets and Instructional Packages to as-31st taxpayers in filing return, . Th. P.Mph-lots pictured abom Make UP Only a smallportion of the total tax Information Publica-fl.na issued.

and 446 television programs ; andprovided speakers for 2,938 meet-ings of business associations andother groups . The National Officeprepared 11 radio spot announce-ments for the Cost of LivingCouncil Radio Spotmaster Systemfor use by stations across thecountry .

Spanish LanguageProgra mFor the first time the Serviceundertook a program of provid-ing some tax information in Span-ish for the largest non-Englishspeaking group in the UnitedStates . Through simultaneouspress conferences in New YorkCity, Miami and Los Angeles andnews releases, the Service an-nounced the publication of a newSpanish language guidebook forindividual taxpayers . The Service31SO issued some Spanish lan-guaie news releases and spotannouncements to news mediathat print or broadcast in Span-ish . Spanish speaking Servicepersonnel appeared on radio andtelevision programs to broadcast'ax information .

Publicizing Changes inthe Tax Law-IncreaseIn Withholding Rate sThe Revenue Act of 1971 provid-3d for increased withholding ratesto eliminate the substantial un-derwithholding potential inherentin prior law. In some situations itwas apparent that the new rateswould cause too much tax to bewithheld from the paychecks ofmany taxpayers . To meet thisProblem, the Service conducted

program to inform taxpayers~!bout the latest change in the.,, thholding tables, and of reme-Jes available to prevent exces-,ve withholding .ie Service prepared news re-

:eases and articles and arranged.nterviews with wire services, na-ilonal magazines, and newsletterpublishers . Nearly 900 televisionstations and the networks carriedtwo television spot announce-ments on withholding, and Serv-'ce offices distributed four radiospots to nearly 5,000 stations .

The Commissioner sent letters tomore than 160,000 employers of100 or more persons, explainingchanges in the withholding rates.Service offices distributed copiesof the Employer's Tax Guide(Circular E), which explainedchanges in withholding to 4 .3 mil-lion employers who withhold

taxes from employees . The Serv-ice also sent explanatory lettersto Cabinet members and otherheads of Federal agencies withsizeable groups of employees .

Other Changes in

the Tax La wThe Revenue Act of 1971 broughtabout several other importantchanges for individual and corpo-rate taxpayers . The Service an-swered press inquiries and issuedreleases to inform individualsabout the increased staficlard de-duction, changes in filing require-ments, deductibility of householdand dependent care, limited de-duction or credit for politicalcontributions, and changes in es-timated tax filing requirements .Similar activities for corporatetaxpayers covered Domestic In-ternational Sales Corporations,the Work Incentive Program, theAsset Depreciation Range Sys-tem, and the Investment Credit .

Casualty LossDeductionsMany taxpayers in the East andNorthwest suffered severe lossesdue to flood and wind damage .To assist these taxpayers, Con-gress extended the time to fileamended 1971 tax returns so thattaxpayers can deduct disasterarea casualty losses sustainedafter the tax return filing dead-line . The Service also applied spe-cial techniques to claims for re-fund inihe disaster areas in orderto process them and authorize re-funds within three weeks.

Field offices in affected areasconducted information campaignsstressing local situations . TheNational Office answered pressand taxpayer inquiries on changesin the law and issued news re-leases advising taxpayers in dis-aster areas that they could fileamended 1971 tax returns.

Special ProceduresSpeed Up Processingof DISC RulingsThe Revenue Act of 1971 au-thorized creation of DomesticInternational Sales Corporations(DISC) . The purpose of this legis-lation was to make Americangoods and services more com-petitive * in foreign markets. TheService, in conjunction with theTreasury and Commerce Depart-ments, publicized advantages ofoperating a DISC to Chambers ofCommerce and World Trade Com-mittees in 40 cities.

Technical Interpretationsfor Taxpayers andService Employee sMany individuals and organize-tions write to the Service for in-terpretive assistance in the formof letter rulings where the taxtreatment and implications of theirfinancial transactions are notclear from the tax law regulationsor published rulings .

Taxpayer and field office re-quests for technical interpreta-tions and advice in various taxcategories appear below :

REQUESTS FOR TAX RULINGS & TECHNICAL ADVICE (CLOSINGS )

Taxpayers FieldSubject

Tota l

Actuarial MattersAdministratim ProvisionsAlcohol, Tobacco & Firearms TaxesEmployment & Self-Employment TaxesEngineering QuestionsEstate and Gift TaxesExempt OrganizationsOther Excise TaxesOther Income Tax MattersPension Trusts

Total Requests Requests

18,356 15,702 2,654

453 417 36as 64 21

3,647 2 .754 893264 219 45164 92 72503 "1 62

3.964 3.400 564322 231 91

6,569 6 .248 3212,385 1,836 549

4 - .1 .. - 11 - ~ 5

The Service received 13,671 ap-plications from taxpayers for per-mission to change their account-ing period or method, made 953earnings or profit determinations,and issued 1,336 supplementalgroup rulings to parent exemptorganizations .

Published Rulings andProcedures Guide Taxpayersand Service Personne lRevenue Rulings are publishedpositions of the Service basedprimarily on letter rulings on is-sues of general interest .

Revenue Procedures announceinternal practices and proceduresthat affect taxpayers' rights andobligations .

The table below shows the num-ber of Revenue Rulings and Rev-enue Procedures published dur-ing 1972 in the various tax cate-gories :

Revenue Rulings and RevenueProcedures Publishe d

Type Numbe r

Total 704

Administrative 27Alcohol, Tobacco an d

Firearms 26Employment taxes 41Estate and gift taxes 23Excise taxes 102Exempt organizations 40Income tax 372Pension trusts 65Tax conventions 8

6

Following Examples IllustrateSignificant AdministrativeInterpretations andProcedures Published :Revenue Ruling 71-425 providesthat, subject to ce 'tain guidelinesstated therein, amounts receivedby a participant in a work-train-Ing program, such as a programunder Title V of the EconomicOpportunity Act, are neither in-cludable in gross income nor con-sidered wages for purposes ofwithholding income tax or taxesunder the Federal Insurance Con-tributions Act.

Revenue Ruling 71-447 holds thata private school that otherwisemeets the requirements of sec-tion 501 (c)-(3) of the Code willnot qualify for exemption fromFederal income tax if it does nothave a racially nondiscriminatorypolicy as to students .

Revenue Ruling 71-556 presentsdetailed guidelines for integrationof benefits or contributions inqualified pension or profit-shar-ing plans with benefits providedunder the Social Security Act asamended through June 30, 1971 .(Basic integration rules appearin section 1 .401-3(e) of the regu-lations .)

Revenue Procedures 72-1 through72-9 update and restate the gen-eral procedures

ofthe Service

for issuing rulings and determin-alion letters to taxpayers andtechnical advice to district of-fices .

Bulletin ProvidesOfficial GuidanceThe Service publishes rulings,procedures, and other significanttechnical developments in theweekly Internal Revenue Bulletinfor the guidance of taxpayers,tax practitioners, and Servicepersonnel .

Bulletins in 1972 contained : &t7Revenue Rulings, 57 RevenueProcedures, 14 Public Laws relat-Ing to Internal Revenue matters,5 Committee Reports, 8 ExecutiveOrders, 2 Tax Conventions, 170Treasury Decisions containingnew or amended regulations, 'ItDelegation Orders, 6 Notices ofSuspension and Disbarment frompractice before the Service, and229 announcements

ofgeneral

interest . Bulletins also announced72 notices of acquiescence ornonacquiescence in adverse do-

cisions of the United States Tax

Court. The Service cumulatessemiannually, contents of theWeekly Bulletins and publishesthese as Cumulative Bulletins .

Regulations Aid in theUniform Administrationof Revenue Law sThe Service issues regulations tofurnish its personnel and'th6 pub-lic guidelines to minimize ad-ministrative discretion and en-courage uniformity in applicationof the taxing statutes .

Normally, the Service issues pro-posed regulations through publi-cation of the complete text in ap ublic notice of proposed rulemaking . All notices invite writtencomments on the proposed regu-lations and inform the public ofits right to request a hearing andto comment at the hearing . Afterconsidering the comments andsuggestions, the Service revisesproposed regulations as neces-sary. Preparation and publicationof a Treasury decision in the Fed-eral Register follows . These reg-ulations have the force and effectof law.

At times a new law may requiretaxpayers to make important de-cisions soon after the law's en-actment. To aid such taxpayers,the Service publishes temporaryregulations pending is~uance ofpermanent regulations in the nor-mal manner . Where a notice isunnecessa,ry or impractical, theService publishes regulationswithout a notice of proposed rulemaking .

During the year, the Service held24 public hearings on proposedregulations, with total attendanceover 960 .

The Tax Reform Act of 1969 re-quired 179 regulations projects .The Service also undertook 36projects to clarify changes madeby the Revenue Act of 1971 . Thefollowing appeared in the FederalRegister on projects associatedwith the Tax Reform Act of 1969 :22 Treasury decisions containingfinal regulations ; 3 Treasury deci-sions containing temporary reg-ulations ; and 39 notices of pro-posed rule making. These actionscovered income averaging, capi-tal losses, multiple corporations,charitable remainder trusts, andreserves for losses on mutualsavings banks . The following ap-peared in the Federal Register onprojects associated with the Rev-enue Act of 1971 : 4 Treasury de-cisions containing temporary reg-ulations; and 3 notices of pro-posed rule making . These actionsdealt with investment credit andtreatment of corporations quali-fied as a Domestic InternationalSales Corporation . On projectsnot under the Tax Reform Act of1969 or the Revenue Act of 1971,the following appeared : 24 Treas-ury decisions containing final reg-ulations ; 4 Treasury decisionscontaining temporary regula-tions ; and 22 notices of proposedrule making .

Deductible ContributionsGuide For Donors andService Personne lThe latest biennial revision ofPublication 78, Cumulative List ofExempt Organizati ons

'contains

the names of approx imately 130,-000 organizations . Cumulative bi-monthly supplements, issued in1972 added 11,430 names to anddeleted 943 names from this listof organizations to which contri-butions are deductible for Fed-eral income tax purposes . Thesupplements issued in 1971 add-ed 9,871 names to and deleted1,180 names from the list .

Pension Trust ActivityThe number of new pension andprofit-sharing plans continues toclimb . Based on letters of deter-mination issued in the first threequarters of the fiscal year, cor-porate pension and profit-sharingplans were up approximately31% and 15% respectively. Ap-proximately 35 million peopleparticipated in nongovernmentalpension and profit-sharing plansof various types . Assets of theseplans were

'about $151 billion at

the end of 1972 . The large num-ber of people and huge assetsinvolved in these plans generatedconsiderable interest on the partof the Press and the congress.

Determination Letters Issued on Employee Benefit Plans, FY 1972

Profit sharing Pensionand stock drannulty

It"m bmuss plans -plans

Detemni nation letterre I"uej~.1th-

nelpeln1=91 uslification IQ a plans:Pill. . n .apprered 19,061 : ~Number of Participating

b . Plans disapproved 241,7522. 'Termination of plans3 Armmdm`e'n0t1,s"" 7245,7094: in-trnents 317

cases closed without issuance o fdetermination letter and thertlLsposals' 1,618

Tota l

24,855 43,916

538,945230 780,597ass

.2,657 3,38114,075 19,784260 577

2,818 4,436

Alcohol and TobaccoIndustries, and Firearmsand Explosive MaterialsLicensees Notified ofTechnical Change sThe Service issues industry cir-culars to keep the alcohol and to-bacco industries, firearms licens-ees, and explosive materials li-censees informed about require-ments of laws, regulations, rul-ings, and procedures.

The majority of circulars informedindustry members of Treasury De-cislons and/or Revenue Rulings .Topics in the remaining circularsincluded : Environmental impactstatements concerning use ofpolyvinyl choloricle plastic in themanufacture of liquor bottles;changes in design of green stripstamps used on bottled-in-bond-whiskey ; revocation of approvalof various food activities usedin alcoholic beverages ; sale ofexplosive materials to nonper-mittees or nonlicensees ; and ap-plication of Federal explosiveregulations on finished commonfireworks .

The Internal Revenue Service'sresponsibility for regulation of thealcohol and tobacco industriesended at the close of the fiscalyear . The responsibility has beentransferred to the Treasury De-partment . The next chapter pro-vides information on 1972 accom-plishments in the alcohol andtobacco regulated operations .

7

I

New Challenges in

EnforcementEnforcement activities help as-sure that taxpayers compute theirtax liabilities properly and pay ac-cording to law. Most important,these activities serve to maintaingeneral confidence in the volun-tary self-assessment system .

In major enforcement develop-ments Commissioner Walters

'launched an investigation of theactivities of incompetent and un-scrupulous tax return preparers .At the same time, the Serviceshouldered new responsibilitiesin the tax investigations of keyfigures engaged in the narcoticstraffic, as part of the president'sWar on Narcotics Trafficers .

The Commissioner, in publicappearances, also expressedconcern about the disparity andinadequacy of judicial sentenceshanded down in tax fraud cases,as well as the questionable prac-tice of some societies and com-,mercial associations promotingconventions and seminars asbusiness endeavors when theyappear to be shallowly disguisedpersonal trips or vacations.

Tax Return Preparer sFor some time the Service hasbeen concerned about unscrupu-lous tax return preparers, their ef-fect on taxes paid, and their effecton voluntary compliance . Investi-gations have disclosed that somepreparers typically increased orcreated deductions, or falsifiedthe number of dependents. Duringthe 1972 filing period, the Servicelaunched a nationwide program toidentify and prosecute such taxreturn preparers. .

Of the 3200 tax prac titioners con-tacted throughout the nation, theService found that more than1,800 prepared inaccurate or falsereturns . The Service has filedcriminal action against practition-ers in 26 states . The program hasled to 430 potential or actualprosecutions so far, and 55 con-victions or guilty pleas .

Throughout the filing period theService worked through the news

10

media in cautioning taxpayers tochoose tax return preparers care-fully.

The Intelligence Division will con-tinue to monitor activities of sus-pected practitioners, and theService will audit, as necessary,individual returns prepared bythem .

Abuses by return preparers inrecent years have led to a numberof bills before Congress to pro-vide for regulation or licensing ofreturn preparers . This appears tohave encouraged an increasingnumber of tax practitioners totake the Service's annual SpecialEnrollment Examination to qualifyfor practice before the Service .

Deceptive Trade Practices byCommercial Tax ReturnPreparers

A side from evidence of improper

returns preparation, it appearsthat the search for increased busi-ness by preparers has led to anumber of deceptive trade prac-tices, including misleading ad-vertising, misleading guarantees,and using customer's tax informa-tion for preparation of mailinglists and other unauthorized pur-poses.

Number of tax returns examine d

(Figures in thousands)

Type of return

Tota l

1971

Grand total 1,646

Income tax, total 1,487corporation 130Individual and fiduciary 1,346

Exempt organization 11Estate and gift tax 41Excise and employment tax 117

I less than 1,000 .

The Service and the FederalTrade Commission have con-ferred to combat these abuses,(For a description of pending leg-islativip proposals see page 57 .)Some of the nations' largest re-turns preparation firms have en-tered into agreements with theFederal Trade Commission con-senting to a cease and desist or-der on deceptive trade practices .A number of other agreementsare pending approval . Further,the Revenue Act of 1971 prohibitsuse of a customers' confidentialtax information for purposesother than the preparation of taxreturns .

Examination Result sIn 1972, the Service examined1,695,849 returns, 49,920 morethan the preceding year, revers-ing a nine year downward trend .Recommendations for additionalassessments reached $3.413 bil-lion . The total included $1 .2 bil-lion in additional tax and penal-ties recommended underthe teamaudit approach used to examinelarge corporations . Examinationscover verification of income, de-ductions, and computation itemsreported on returns.

Individual and fiduciary returnscomprised 79.2 percent of all ex-aminations, and accounted for29 .3 percent of the additional taxrecommended, while corporationreturns accounted for over 50 percent of the additional tax recom-mended.

The table below shows the num-ber of returns examined in 1971and 1972 by type of tax .

Field Mile.

1972 1971 1972 1971 1972

1,696 566 593 2,080 1,103

1,497 429 424 1,058 1,073138 129 135 1 1

1,3" 289 271 1,057 1,072is 11 is (1) V)40 36 35 4 5158 100 133 is 25

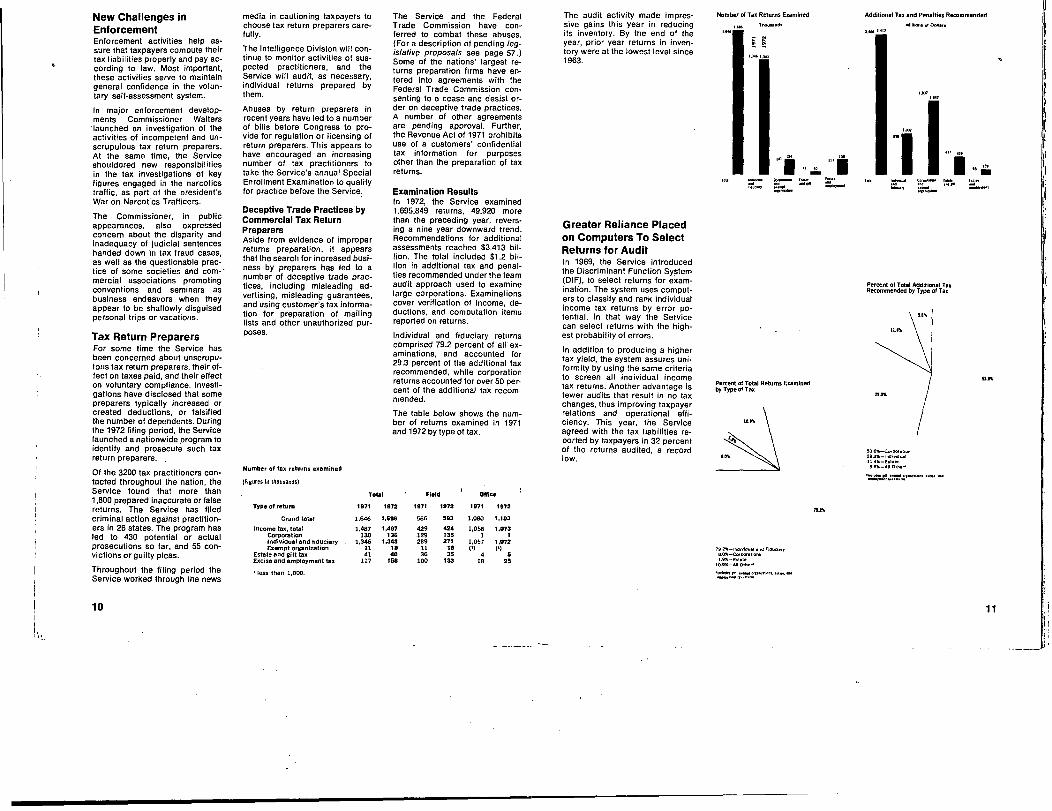

The audit activity made impres-sive gains this year in reducingits inventory . By the end of theyear, prior year returns in inven-tory were at the lowest level since1963 .

Greater Reliance Placedon Computers To SelectReturns for AuditIn 1969, the Service Introducedthe Discriminant Function System(DIF), to select returns for exam-ination . The system uses comput-e rs; to classify and rank individualincome tax returns by error po-tential . In that way the Servicecan select returns with the high-est probability of errors.

In addition to producing a highertax yield, the system assures uni-formity by using the same criteriato screen all individual incometax returns . Another advantage, isfewer audits that result in no taxchanges, thus improving taxpayerrelations and operational effi-ciency. This year, the Serviceagreed with the tax liabilities re-ported by taxpayers in 32 percentof the returns audited, a recordlow.

Number of Tax Returns Examined

Percent of Total Returns Examinedby Type of Tax

Additional Tax and Penalties Recommende d

!;d"

".r%

.1,

U .6E-1

Percent of Total Additional TaxRecommended by Type of Tax

9-

Studying output data for a joint audit-inteill .pence Investigation 1, the Ogden ServiceCenter ..movie, .am a,.: (L to .) HenryPhilcox, Computer Audit Specialist, Renoviwftl~ Ralph IngbWear, Assistant DivisionChief, Data Convention, Ogden Service Can.ht';

and ClIff Rich, Weals. Regional Inf.1li-g.rc. Analyst.

Increased ComputerAssisted Audit sComputer assisted techniquesplay an important role in tax au-dits of automatic data processingaccounting systems . Largemasses of data which meet pre-determined audit criteria arescanned, analyzed, and recom-puted at tremendous speed . Thistechnique produces printouts ofmanageable size, thus savingconsiderable resources for theService and taxpayers .

Revenue Ruling 71-20, requiresthat taxpayers retain pertinentcomputerized tax records . TheService has completed recordevaluation requests for a substan-tial number of taxpayers. Afterevaluation, Service personnel ad-vise the taxpayers as to whichrecords to retain in machine-.sensible form .

Joint Committee

Reviews Large

Overassessments

A report on all refunds and credits ;on income, estate and gift taxes,over $100,000 must be sent to theJoint Committee on Internal Rev-enue Taxation, as required bylaw . During 1972, the Service re-ported 1,171 cases involving over-assessments of $756.1 million tothe Joint Committee, as com-pared with 790 cases and $518 .3million in overassessments in1971 .

Exempt OrganizationProgramExempt organizations classifiedas private foundations reportedmore than $4 .3 million as initialtaxes under the excise tax provi-sions of the Tax Reform Act of1969 .

The Service makes every effort tokeep pace with its two-year auditcycle for large exempt organiza-tions and its five-year cycle forprivate foundations . In 1972, theService issued determination let-ters to 23 thousand organizationsthat applied for confirmation oftax exempt status under the law.In addition, the Service withdrewadvance assurance of the deduct-ibility of contributions from 45 pri-vate schools that failed to estab-lish a racially nondiscriminatoryadmissions policy.

The Exempt Organization MasterFile (EOMF) continued to grow.The number of exempt organize-lions in the file has increasedfrom 309 , 000 in 1967 to 535,00D in1972 . The rate of growth in 1972was almost 5 percent .

Team Audit TechniqueUsed for LargeTaxpayersThe Audit Division uses the teamaudit technique in examing com-plex corporate structures . Manycorporations have diverse activi-ties, intricate practices and trans-actions, and widely dispersedoperations across the nation andin foreign countries For thesereasons, the teams ~ay requireengineer agents, internationalexaminers, actuaries, data proc-essing specialists, attorneys, stat-isticians, and economists .

Expansion of AuditConcepts to ServiceCentersService centers conducted sev-eral correspondence aydit pro-grams in 1972, including the newUnallowable Items Program . Thisis a low cost audit program whichuses computers to contact tax-payers about deductions whichappear to be unallowable by law.Typical unallowable items Includedividends exclusions in excess ofthe amount allowable, failure toreduce medical expenses by thepercent of adjusted gross income,and the taking of fractional ex-emptions . In the period of Janu-ary 1 to June 30, the Service cor-rected 452,521 unallowable itemsreturns producing revenue of$24 .2 million.The Information DocumentMatching Program matches infor-mation documents and other rec-ords filed with the Service with in-formation reported on individualtax returns, thereby identifyingpersons who failed to report all oftheir income . Forms W-2 (Wageand Tax Statement) and Forms1099 (U .S . Information Return)are principally used in this pro-gram .The Multiple Filer Audit Programbegan in the final months of 1972 .Computers analyzed individualreturns to determine If more thanone return had been filed underthe same social security number .In, many instances, married tax-payers filed two joint returns orseparate returns and claimed du-plicate exemptions or deduc-tions, usually because of a mis-understanding in filing require-ments . The Service sent lettersto taxpayers explaining the errorand proper return filing require-ments and statements of addi-tional tax due,

Art Panel Assistsin Evaluation sSince 1968, a panel of art expertshas been assisting the Service indetermining whether realistic val-uations have been placed on con-tributed works of art and on artobjects valued for estate tax pur-poses .The panel met three times in 1972and reviewed 711 works of artvalued in tax returns at more than$18 million . The panel recom-mended a 30 percent reduction Inthe claimed value of works of artfor charitable contributions anda 25 percent increase in the valueof art objects included in estates .In its four years of operation, thepanel has reviewed approximate-ly $70 million worth of art and hasrecommended adjustments of ap-proximately $20 million .

12 13

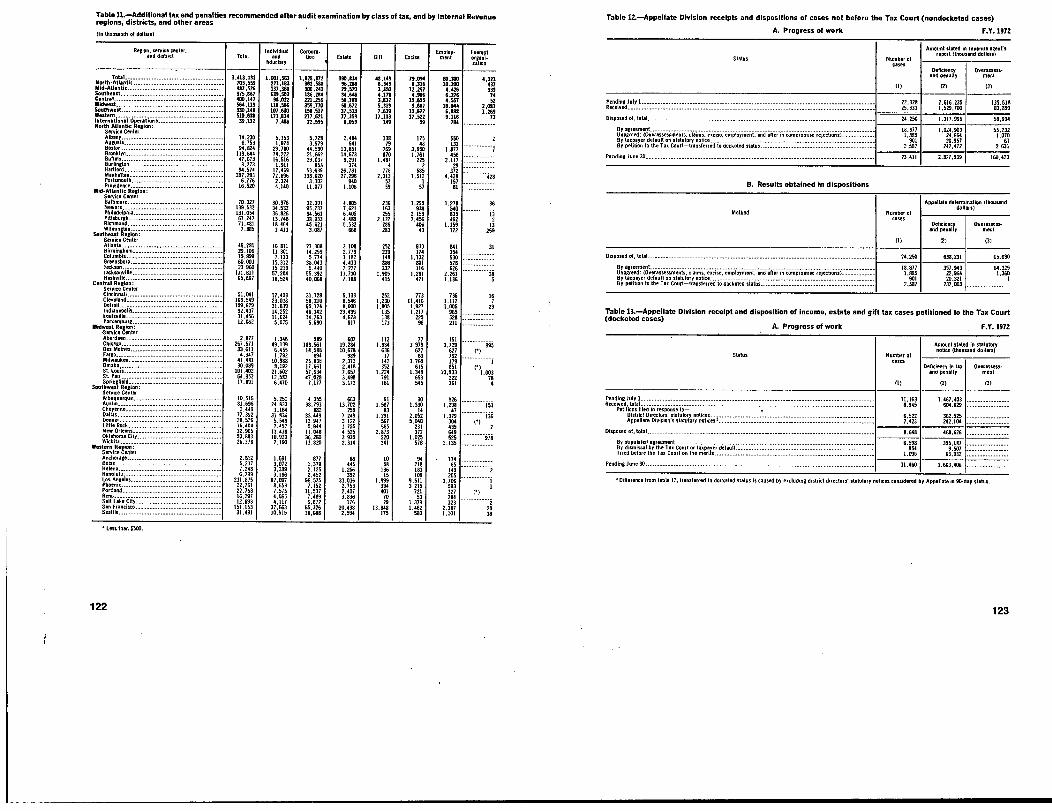

Administrative AppealsSystemGeneralThe appeals function of the Serv-ice provides the taxpayer who dis-agrees with a proposed adjust-ment to his tax liability an oppor-tunity for an early, independentreview of his case. The purposeis to enable the taxpayer to settlehis case promptly, without litiga-tion, on a fair and impartial basis .The appeals function is decen-tralized and operates in 58 dis-trict offices and 40 regional ap-pellate offices. As need arises,the Service provides conferencesat other locations . The taxpayercan go to either the district or re-gional office for an Initial confer-ence .Although differences in authorityand jurisdiction exist, both dis-trict and regional offices have thesame objective-to resolve casesas soon as possible on a basiswhich reflects a fair administra-tion of the law . The principal dif-ference in authority is that onlyregional appellate offices maydispose of cases by consideringhazards of litigation, that is, un-certainty as to outcome in theevent of trial . The appellate divi-sion has this authority in keepingwith longstanding Service policywhich favors administrative set-tlements over protracted litiga-tion .

Cases considered involve alltypes of taxes except those onalcohol, tobacco, firearms, nar-cotics and wagering . Issues runfrom the most elementary to themost complex, and deficienciesin tax from a few dollars to manymillions . Claims for refund of taxand offers in compromise alsorate consideration.

In most cases Service confereesand taxpayers reach a mutuallyacceptable basis for resolving thedispute, as a result, a relativelyfew cases actually go to trial . TheService closed over 98 percent ofall cases without trial in the lastseven years, and this year the ap-peals function achieved the great-est number of case disposals perconferee in history .

District Conference C. .. W .,X-I ..d

Case pending JulyCos" receivedConference complat

Number agreedAgreed as a percent Of total

Cases pending June 30

Early InformalHearing ProvidedAt both district and appellate lev-els, the Service offers a confer-ence soon after the case is re-calved . To the extent possitFle,the Service arranges a date, time,and place most convenient to thetaxpayer. Where the disputed taxis less than $2,500, the taxpayerneed not file a written protest forconference in the district office.The same rule applies In the re-glonal appellate office if the tax-payer has first availed himself ofa district conference .

Informal proceedings prevail atboth levels and the taxpayer mayrepresent himself or have coun-sel . If a conference fails to pro-duce agreement, the Service in-forms the taxpayer of his addi-tional rights and options .In 1972, the appeals function dis-posed of 52,189 cases by agree-ment ; the Tax Court decided1,096 cases ; U .S . District Courts,and the Court of Claims decided460 cases.About half of the cases closed byagreement are at the district leveland half at the appellate level .District conference staffs ob-tained agreement on about two-thirds of the cases . Activity in thedistrict conference staffs appearin the table below :

Field OfficeAudit Audit Total

8,769 3,1125 12,59424.882 17 .250 42,13224,141 166 8 40,7691 1 11 :8 24.86 53 26,714

61.5 71.2 65.591510 4,447 23,957

Appeal Options Availableto TaxpayerIf there is no agreement at eitherdistrict or regional level, the tax-payer can, in most instances,file an appeal with the Tax Court .Even though this is done, and thecase is docketed for trial, the tax-payer may still reach a settlementwith the appellate office . Exceptin unusual circumstances, thetimely filing of an appeal with theTax Court stays the assessmentand collection of the tax until theCourt has entered its decision .

As an alternative to trial in the TaxCourt, the taxpayer can pay thedeficiency in tax, file a claim forrefund (at any time within twoyears from date of payment) andafter either denial of the claim bythe Service, or after 6 monthsfrom date of filing, enter suit forrecovery against the Governmentin either . a United States districtcourt or the Court of Claims .

Appellate Receiptsand DisposalsReceipts in regional appellate of-fices had remained even at about33,000 cases in each of the pastfour years . This year receipts in-creased to 34,278. Both non-docketed and docketed case re-ceipts increased over the prioryear .

There also was a substantial in-crease in docketed cases involv-ing $1,000 or less of disputed tax(for which special simplified pro-visions were made in the Tax Re-form Act of 1969) . In 1968, theService received 972 cases ; in1969, 1970, 1971 and 1972 re-ceipts were 1,267, 2,100, 2,781and 3,321, respectively. Most ofthese cases were ultimately set-tled .

About 75 percent of the appellateworkload consists of nondoc-keted income, estate, gift, exiseand employment tax cases. In1972, appellate offices closed 78percent of these cases by agree-ment with the taxpayer . Agree-ments in this category have aver-aged more than 80 percent overthe past 5 years.

Taxpayers filed petitions for hear-ings before the Tax Court in 8,945cases in 1972, as compared to6,968 cases in 1970 and 8,299cases in 1971 . The increase waslargely in the small case categorywhere the Service offers informalprocedures . Settlement negotia-tions on docketed cases continueand most cases are ultimatelysettled without trial .

The following table and chartshows the processing of bothnondocketed and docketed casesI n 1971 and 1972 . (For additionalinformation see tables 12 and 13,page 123 ) .

Appellate Division processing of all cases for 1971-1972 (Income, estate, gift, exci ..,employment, and offers-in-compromise)

Statu s

Pending July IReceivedDisposed of, Tota l

By agreementUnagreed (overassessments, claims, excise. employment,

and ffer-in-c-promise rejections )Bytaxpayer default on statutory notice of dismisse( by

Tax CourtBy petition to the Tax CourtTried in the Tax Court

Pending June 30

Failure To Pay by thePrescribed DateThe Service makes every reason-able effort to collect taxes due,starting with notices to taxpayersrequesting payment and then es-tablishing delinquent accountsfor assignment to enforcementpersonnel .

New DelinquentAccounts Dro pEstablishment of delinquent ac-counts declined in 1972 despitecontinued growth in populationand taxable income . Principal fac-tors were : (1) increased use of th e

Number of cases1971 1972

33,468 33,49132 .682 34,27832.659 22,89825 .804 25,475

1,474 1 .885

1,602 1 .8552,814 2,58 7965 1,096

33,491 34,87 1

APPEALS- DISPOSALS IN REGIONAL APPELLATE DIVISION OFFICE S

Is-

NONDOCXUED CASES CASES DOCKETED IN TAX COURT

I.-Asa

IN DEPARTMENT OFJUSTICE ON

REFUND SUITS

- I-

14 is

I

essing system to mail out tax bills ;(2) the impact of recent tax legis-lation which removed many lowincome taxpayers from the taxrolls ; and (3) some easing in eco-nomic conditions . The Service es-tablished 2.6 million delinquentaccounts, 202,000 or 7 .2 percentfewer than last year . The amountof delinquent tax also dropped by$298 million or 8 .5 percent to$3 .2 billion.

Disposals Down Slightly ButInventory Down SharplyThe Service disposed of 2 .7 mil-lion delinquent accounts in 1972 .This was a decline of 138,000accounts or 4 .8 percent below1971 . Delinquent taxes collectedamounted to $2 .2 billion, which is$265 million below 1971 .

The relatively small reduction indisposals is evidence of notableaccomplishment considering : (1)increased budgetary limitations ;(2) heavy manpower demands im-posed by the Economic Stabiliza-tion Program which drained 1 .3million man hours from this en-forcement area ; and (3) expandedTaxpayer Service activity insti-tuted in April, which further lim-ited available manpower.'

For the second successive year,the inventory of delinquent ac-counts declined . The 1972 levelof 659,000 accounts is the lowestpoint reached since 1965, andrepresents a reduction of 100,000accounts, or 13 .2 percent, below1971 . The $1 .9 billion value ofthese accounts is $2.4 million lessthan the prior year's .

Taxpayer Delinquent Accounts

Status

- Us sa .- ut rrompixidentification of FederalTax Deposit OffendersThe Service is concerned espe-cially with the failure of employ-ers to deposit taxes withheld fromemployees' wages because in ef-fect, it represents a misappropria-tion of funds that belong to theGovernment. To combat the prob-lem, the Service initiated a Fed-eral Tax Deposit (FTD) Alert Pro-gram . The program involves earlyidentification of potential offend-ers through use of data process-ing . The system determines whichemployers,have failed to make de-posits . A notice then alerts an en-forcement officer who calls on theemployer to determine why he hasnot complied .

Automatic DataProcessing SystemAids Program AgainstDelinquent Filer sThe Service's automatic dataprocessing system played a majorrole in detecting non-filers, firstby monitoring and following uppreselected types; of delinquentaccounts, and secondly by in-creasing the use of four masterfiles to issue automatic delin-quency notices or investigations.These factors permitted a greaterdevelopment of enforcement per-sonnel in seeking out non-filers,thereby reversing the fall-off thathad occurred in recent years be-cause of budgetary limitations .

Number Amount(thoussend .) (thousand dollars)

197 1

Issued 2.4121Disposed, mal 2,847

By type of action:Collected 2,265Additional Collections -011her Disposals' 51

2Pendina June 30, total 759

1972 1971 1972

2.619 $3,509,677 $3.211,963

2.709 3,579,694 3,337,947

2,164 2,498,077 2=2.953- 108,761 S4 .632

546 972,856 1,010,364659 $1,899,804 $11,897 .38 4

I includes disposals due to nc .liectibility, erroneous and duplicate assessments, Pay-

Mont tracer and adjustment cases .

16

I axpayer Uelinquent Accounts

Millicepus of Dollars35 "310 3212

1EsUblished Closed

38

Increase in Number ofDelinquent Returns SecuredThe Service secured 815,000 de-linquent returns valued at $452million . This compares with 735,-000 delinquent returns assessedat $489 million in fiscal year 1971 . *

Master Files-The OperationalFoundation of Tax DelinquentReturns Progra mThe business master file (BMF),the individual master file (IMF),the exempt organization masterfile (EOMF), and the residual mas-ter file (RMF) provide the opera-tional foundation for a major por-tion of delinquent returns activity.Each has a routine tailored tomeet variations in tax regulationsand filing requirements and issuesa delinquency notice or investiga-tion in every apparent non-filersituation .

The business master file dealswith several classes of tax. TheService can program BMF to de-liver a single investigation for oneor more tax periods during theyear . This elminates massive pa-perwork as well as multiple an-.forcement contacts, since the

computer will not issue anotherinvestigation or accept as satis-factory any completed investiga-tion which does not satisfy allperiods of delinquency .

The in'dividual master file pro-

vides an annual delinquencycheck for instances of non-filingof individual income tax returns .

The exempt organization masterfile (EOMF) is relatively new. Pro-grams implemented under EOMFprovide for issuing delinquencyletters and taxpayer delinquencyinvestigations .

The residual master file (RMF)provides processing and handlingoperations for a variety of returnsof limited volume or unusual char-acteristics which did not adaptwell to earlier mechanization . TheRMF also provides timely issu-ance of delinquency notices andsubsequent delinquency investi-gations whenever required re-turns are not forthcoming .

Over half of all apparent non-filercases are resolved through com-puter generated issuances . Fortax year 1970, the I ndividual mas-ter file selected over 500,000 non-filer cases for delinquency check-ing, over twice as many as everbefore .

New Programs in

Returns ComplianceAmong several specialized pro-grams in progress is a survey of12,000 airport facilities across thecountry to insure compliance withtax provisions of the Airport andAirway Revenue Act of 1970. An-other program involves a nation-wide effort to achieve a higherlevel of compliance with FederalHighway Use Tax laws. Throughuse of available information, theService will identify virtually allmotor vehicles, or vehicle own-ers potentially liable for this tax .Expected benefits include a sub-stantial revenue return and great-er awareness of the tax require-ments among all segments of thetruck-owning public .

Returns compliance programs un-derway and planned involve co-ordination with nearly every mal. orFederal department or agencyand a number of private firms . TheServic& compares data fromthese sources against the variousmaster tax files for possible de-linquency .

While actual tax liabilities of sometaxpayers may be slight in com-parison with their neighbor's, alltaxpayers have an obligation tofile what is required and pay whatis due. Thus, the Service includesa significant number of individ-uals and smaller business enti-ties .

Enforcement ApproachGeared to ReduceNon-ComplianceThe Service trains enforcementpersonnel to review all possiblereturns delinquencies whenevertaxpayers are interviewed in ap-parent non-filer situations . For ex-ample, a self-employed individual,delinquent in filing an income taxreturn, may not have filed returnsfor recent income tax periods .The Service will also check forbusiness tax returns if the tax-payer employs other people, orfor excise tax returns if required .

Results fromDirect Enforcement

Maps. of wisrs

I'll

1.

Tax Fraud Investigationsand the IntelligenceDivisio nThe Intelligence Division Identi-fies areas of noncompliance andenforces the criminal sanctions ofthe Internal Revenue Code. TheIntelligence function employedover 3000 technical and clericalemployees in 1972 .

Tax Fraud Investigations,Indictments, and ConvictionsThe Service completed 8,882fraud investigations during theyear, with prosecution recom-mended in 1,777 cases . Agentsscreened more than 132,000 alle-gations of fraud in selecting theinvestigative caseload .

Grand juries indicted 1,074 de-fendants in tax fraud cases in fis-cal 1972 . A total of 772 defendantspleaded guilty ; courts convicted113 defendants after trial and ac-quitted 39, and dismissed 137 .

Intelligence ComplianceProgra mThe Service conducted a programI identify patterns of noncompli-o fance by homogeneous groups of

taxpayers, and areas of noncom-pliance not covered in other pro-grams .

Service investigators made com-pliance checks of more than 250professions, occupations, busi-nesses, industries, and income in-formation sources . Among pock-ets of noncompliance locatedwere sub-contractors in the con-struction Industry, area managersin the direct selling industry, in-surance salesmen, recipients ofland condemnation awards, at-tomeys, and persons liable forhighway use taxes . The Serviceimposes criminal sanctions whereevidence of tax evasion is discov-ered, and takes remedial action toassure future compliance .For example, offices in severalareas inquired into compliancewith reporting income require-ments by private duty nurses .All offices found noncompliancewhere payments were made incash without issuing information

17

documents (Forms 1099 or W-2) .In one district, the State NursesAssociation published an articleon the results of the compliancetest, advising nurses to reporttheir income from private assign-ments .

Another project involved scrapmetal and textile waste operators .Here, agents examined 258 re-turns and recommended defi-ciencies of $488,307 . They alsorecommended prosecution of fiveindustry officials .

The impact on voluntary compli-ance is apparent. Agents ex-amined returns of hospital med-ical employees who had notreported wages paid from schol-arship funds . The major hospitalswhich had been paying employ-ees from scholarship funds trans-ferred $500,000 annually to ac-counts to be included in futurewithholding tax statements .

Another investigation disclosed$3.4 million in unreported incomeearned by policemen in a largemetropolitan area . More than1900 policemen had not reportedon their tax returns earnings fromprivate employers for police re-lated security jobs, such asguarding property, crowd control,and watching for shoplifters . Thepolice department assigned po-licemen on a rotation basis. Fiveemployers paid the departmentwhich in turn paid the policemen.The department did not withholdtax or file information reports.City officials cooperated in cor-recting the situation .

A midwestern district found thathouse-to-house cosmetics salescan be big business . A revenueagent audited a parent corpora-tion and recorded serial numbersof United Savings Bonds awardedas prizes to sales persons whosold at least $3,000 in cosmeticsduring an eighteen-week period .The firm had awarded as prizesapproximately $4,000,000 inUnited States Savings Bonds . Aninspection of the tax returns ofknown sales representatives dis-closed that 80 percent eitherfailed to file or made no mentionof theirselling activity.

The Service had found that zonemanagers receive millions of dol-lars in promotional expenses withno accounting required nor with-holding statements issued . Onecompany disburses about $650,-000 in promotional expenses eachyear . This same company payscommissions of about $11,000,000a year of which only $3,000,000appears on information returns .

Sentencing i nTax Evasion CasesNationwide, only 43 percent ofthose convicted in income taxcases received jail terms . Com-parisons of the sentencing prac-tices by judicial districts reflectwide disparities .

In the first quarter of 1972 for ex-ample, courts in the Eastern Dis-trict of Michigan handed down 10sentences and imposed no prisonterms . Four of the cases involvedadditional taxes and penallties of$95,250, $203,552, $191,399, and$164,664 . During the same period,the court in the Central Distri ct

ofCalifornia ordered no confine-ments for six tax evasion convicts .On the other hand, tax violatorsgo to jail in the Southern Districtof Texas . Three recent sentencesincluded a six-month term andtwo four-year terms.

In Philadelphia, courts orderedconfinement for ten income taxevaders . They are : EDWARD P.SWARTZ, a physician and formerPublic Health Director, six-monthjail sentence ; MORRIS WEINER,• prominent dress manufacturer,• one-year prison sentence ;JOHN C . PARENTI, a major rack-eteer, a one-year prison sentence ;IRVING H . MYERS, a business ex-ecutive, a one-year sentence ;PAUL G . HOFFMAN, a restaurantoperator, 100 days imprisonment ;ANTHONY KLIJJIAN, a roofingcontractor, six months imprison-ment ; ANTHONY LEMISCH, avoting machines salesman, sixmonths imprisonment ; WILLIAMJ. KILROY, a "political expe-ditor", 90 days imprisonment ;LOUIS SALERNO, 60 days impris-onment; and FRED L . MATHERNfour months imprisonment . Someof these defendants also paidlarge fines .

Interesting CasesThe court fined Dan B . Ball, a for-mer county judge, $30,000 andplaced him on five years proba-tion forevading part of his incometaxes over a four-year period .During these four years, he pre-pared more than 800 income taxreturns for other people.John S . Allessio, a race track offi-clal, received three years inprison and a $20,000 fine for in-come tax evasion ; and his broth-er, Angelo Allessio, also asso-ciated with the race track, re-calved a sentence of one year inprison and a fine of $20,000 . Ad-d it ional taxes and penalties in thecase exceeded $6,000,000.

Gregory Taylor, a narcotics dis-tributor, received a sentence offive years in prison and a fine of$30,000 for income tax evasion .A lengthy arrest record and sev-eral previous prison confine-ments, plus the cooperation ofthe U .S . Bureau of Engraving andPrinting helped to refute his claimof a cash hoard used to pay forsubstantial real estate, automo-biles, jewelry, and other expendi-tures.

Lee W. Merrich, a dog food proc..essor, received a sentence ofeighteen months in prison for in-come tax evasion on unreportedsales of $170,000 . Cooperationfrom Canadian tax authoritiesmade it possible to locate cur-rency deposits of $142,000 in aCanadian bank account. He hadmade the bulk of unniported salesto a wholesaler of meat for humanconsumption . This meat camefrom the same supply processedfor dog food sales.

Morris Greenberg, an attorney,received a sentence of ninetydays in prison and a fine of $to,-000 for failure to file interestequalization tax returns . One in-criminating factor was a letter hehad written to a Canadian stocktransfer agent explaining the in-terest equalization tax provisions .

Emmett J . Ayo, a night club oper-ator, received a sentence of threeyears in prison for income taxevasion after understating incomeby $228,000 over a four year pe-riod .

Phillip Armento, Sr ., a county as-sessor, received a sentence ofthree years in prison for incometax evasion . This scheme in-volved special handling of per-sonal property tax bills and realestate valuations for fees not re-ported on his tax returns .

Lionel E . Clark, a former countyjudge received a sentence of oneyear in prison for failure to fileincome tax returns for four years.During this period his gross in-come was $62,352.

Nelson E . Weber,, an aircraft in-surance executive, received aprison term through revocation ofprobation of a previous tax eva-sion sentence . Part of the condi-tions of probation involved fullsettlement of his $170,000 taxliability . Instead, he filed an offerin compromise proposing to set-tie his liability for $10,000 basedon stated assets of only $13,000 .Agents discovered an undis-closed safe deposit box contain-ing over $219,000 . They seizedthe money to apply to his taxliability.

James G . Waller, a funeral homedirector, received a sentence ofthree years in prison for under-stating business receipts by$210,000 .

Referrals to the

Department of JusticeThis year, the Service forwardedprosecution recommiendations tothe Department of Justice in 1,355income and miscellaneous crim-inal cases (involving 1,364 pros-pective defendants) . Comparedwith the prior year, this was anincrease of 33 percent in the num-ber of referrals. In 1972, indict-ments in such cases were up 13percent .

In income, excise, and wageringtax criminal cases, the court re-sults included : 733 guilty or nolocontenclere (no contest) pleas,113 convictions after trial, 40acquittals, and 151 dismissals .

A comparison of indictments andcourt actions for the last twoyears follows :

Results of criminal action in tax fraud cases

Action

TotalIrldicinnentsand InformationsDisposals, total

Pleal, guilty or noJo contenclereConvicted after trialAcquitted .

Nol-prossed or dismissedIncome and rni.-Urmeou..-I

Indictments and Information sDisposals, tota l

Plea, guilty or nolo countendereConvicted after tria lAcquittedNol-plasslid or dismissed

Wagering Tax Calue sI rolictments and informationsDisposals, total

Ples, guilty or mlo contemi-Convicted afterth-lial lAcquitted 2 1Nol-prossed or dismissed 21 14

Include cases dismissed for the following reasons : 10 because of d path of principalde~endant, S6 because of serious illness, and 102 because principal defendant had pleadedguilty or had been convicted in . related case .

2 Includes income, estate, gift, and excise taxes other than wagering, alcohol, tobacco,and firearms taxes .

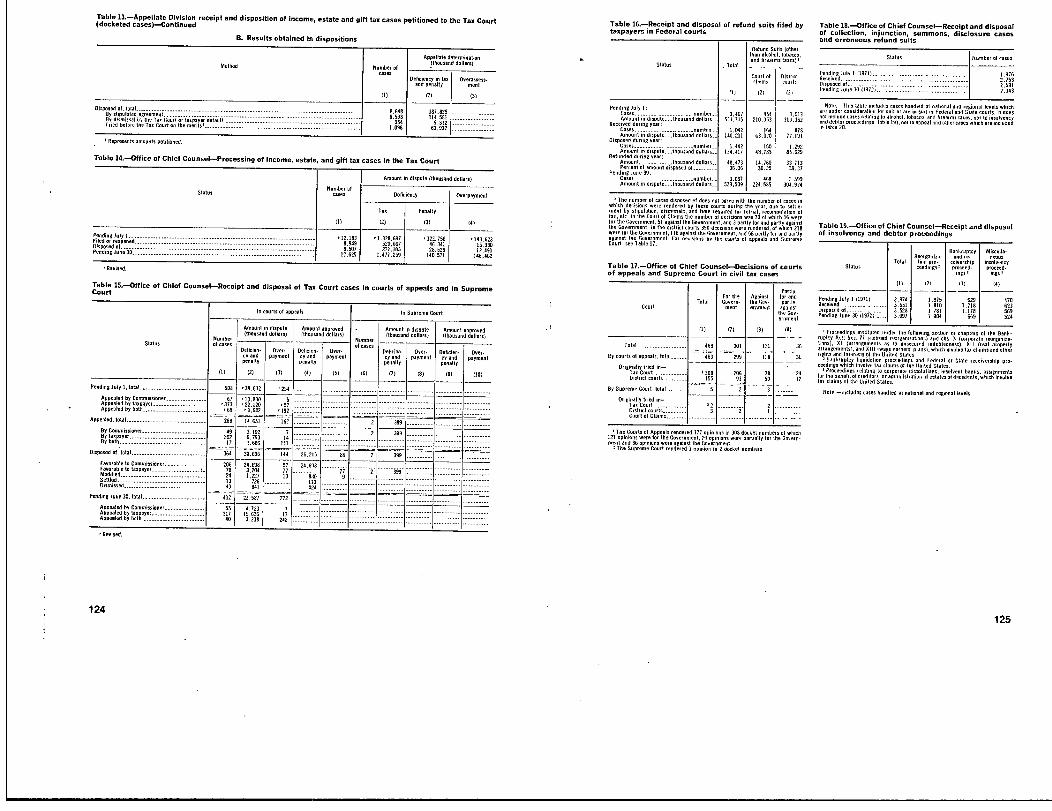

Cases Involving

Criminal ProsecutionCases received in the Chief Q*oun-sets' Office with recommenda-tions of criminal prosecution in-volved additional taxes and pen-alties of $193 million. This was$14 million more than the prioryear. An analysis of the receiptand disposal of criminal cases inthe Chief Counsel's Office fol-lows :

Receipt and disposal of criminal cases in Chief Counsel's Offic e

PemdIn87j6fy IReceived, total

1071

2,266----

With recommendations for pnrsecutfonWith requests for opinion, etc .

Oisposed of, totalProsecution mot %varrantedDepartment of Justice deeClinedProsecutionsOpinions deliveredAll other closings

Pending June 30

IsNumbefoldefenciants_71 1972

956 IM5997 1=7645 723142 113

-S340

.,0574,i'm 1

638 722136 11355 3996,

t 32 137I I r 1

4 1136 267 11

6

2,3131.204

1091r052

7948

75946

1202,467

1972

1,523'157

1,285

9457I,Wssa

1972,7

18 19

(Million, of dollars)

I __. . . . .. . ieve, or me U. system beat! years 1971 and 197 2

hmernal ravennue collections .tout T19-1-16117-11 -209 .856

Individual income taxes. totalDo

['1118A79Wildholding INZ. aa~trfoOtt,

Zt= 15,STGCorporation income taxes

0=034=9

133 .784Estate amd4ift taxes 5,490Employment taxes 43,7143

;18Eachgo tax 16 72 16.847

I a

Civil Causes

Additional to . and joeirlaftleff inci-5 INS~ of I .ounift divisions by Agreement. payment for cletauft

Additional tax and penalties in aeas disposed ofin appellate divisions by agreammult, paymentof defaul t

Additional taxand penalties determined by

itardthemeort Wr= Goo dAdditiortual tax&W penalties determined by Tax

Court decisions:DismissedDecisions an merits

Additional tax gold penalties in cieses, decided trysuperame

court"n" c"M of appeals,b'V.M

MfUnded to taxpayous as . result of refund. -it,

I fraud cases t

Deficiencies and penalties In cases disposed of in

ProosCatio-VoomemandedPwaseatior, net warranted and caseeideclined byDeptuanent

of Justice

1,499 1,41 9

349

101

21229

57

172

25

106

S17

2643

223

I Includes excise taxes

rross tax, penalties and interest resulting from direct nfa,.. . .nt

(in Thousands of dollars )

His.

Additional tax. penalties. and interest aS%esW, total

Free" "'"'Instionof tax returns, total

;ncema tax, totalCgirpongtion

4IE2

~4=705 1 4~iilild?2,708,153 1 3,203,7242.250,813 2,101113,21121,5m=3 1,127 .241

747,25D 156,021345,210 =114362,508 VSA3449.S52 =405

M3 052 11 :2512:141 174oM489 .359 t .432.324

Este IndlVidual and fiduciaryteand gift tax

Emplumolse, tax (including withhold income Me)Excise tax

lend" engtheromUcal va"ificaften of income tax returnsFinam Inevillhattion of estimated to. payments claimed f jFrom delinquent returns secured. tout

fly district collection divisions13Y district alldit divisions

I 427 647 ZN 67061 :712 711 :i~i

Tax and penalty and number of tax years involved in criminal fraud case disposal .

(Exclusive of wagering and coln-apemted gaming device ages)

mistrastitich971 1972

Total 2= 3.344

$107 77g,4Z3 $"'112t,7742,509 JIM i~~7,951 ss.Tn=7Proseecutions 2

Aflothercldofhhfdf~ 454 37,330,"r, 22 3315 477

includes cases declined by Department of Justice,

20

Summary of Additional

Taxes from Direct

Enforcement

Additional revenue resulting fromdirect enforcement historicallyhas represented a relatively smallpart of total tax collections, Themain imp6rtance of direct en,forcement cannot be expressed indollars . Its importance lies in re-assuring the public that the Serv-ice has an effective enforcementsystem, and a balanced programaimed at equitable enforcementof the law for all taxpayers, re-gardiess of position or wealth.

The table below sets forth for thelast two years the source of addi-tional tax, penalities, and interestassesed and certain other resultsof direct enforcement .

Additional detail on legal work-load involved in the prosecutionof criminal cases by Service at-torneys during the past two yearsappears in the table at the left .

Workflow in the Serviceand the CourtsThe unit of measurement at theaudit level is a return . In the Ap-pellate and Intelligence Divisions,as well as in the courts, the workunit is the case . A case may in-volve more than one return andmore than one taxpayer. The ta-ble at the right reflects compara-tive data on actions completedby the Service during 1971 and1972 .

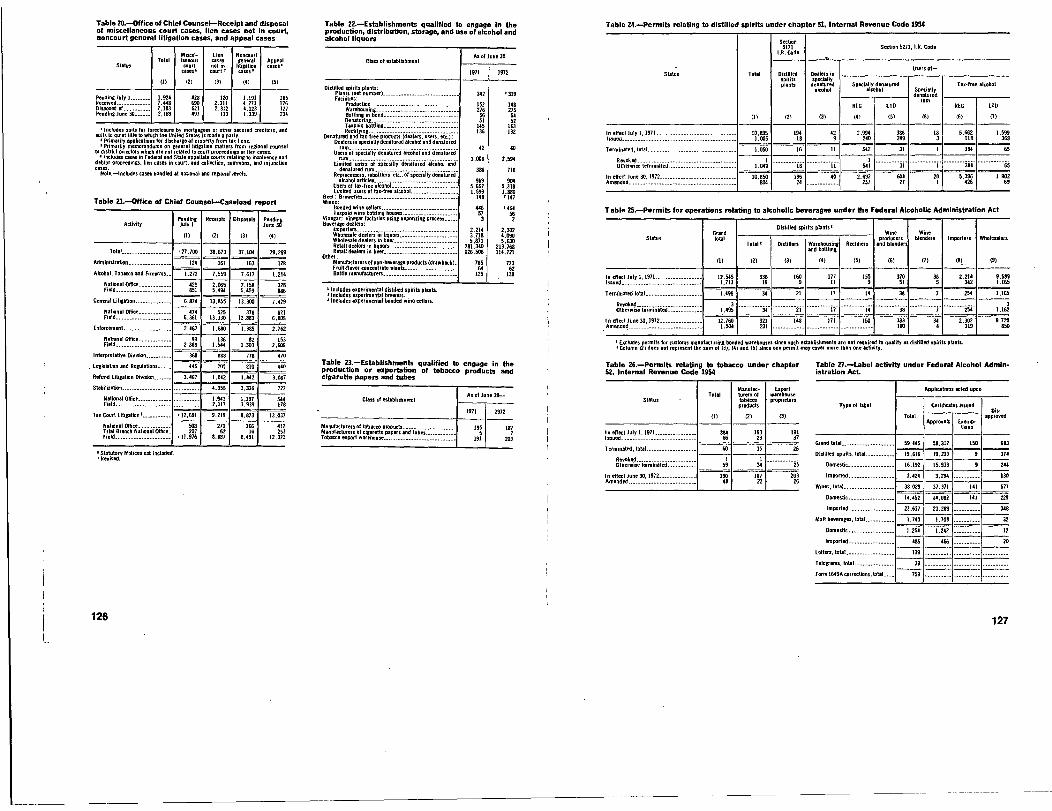

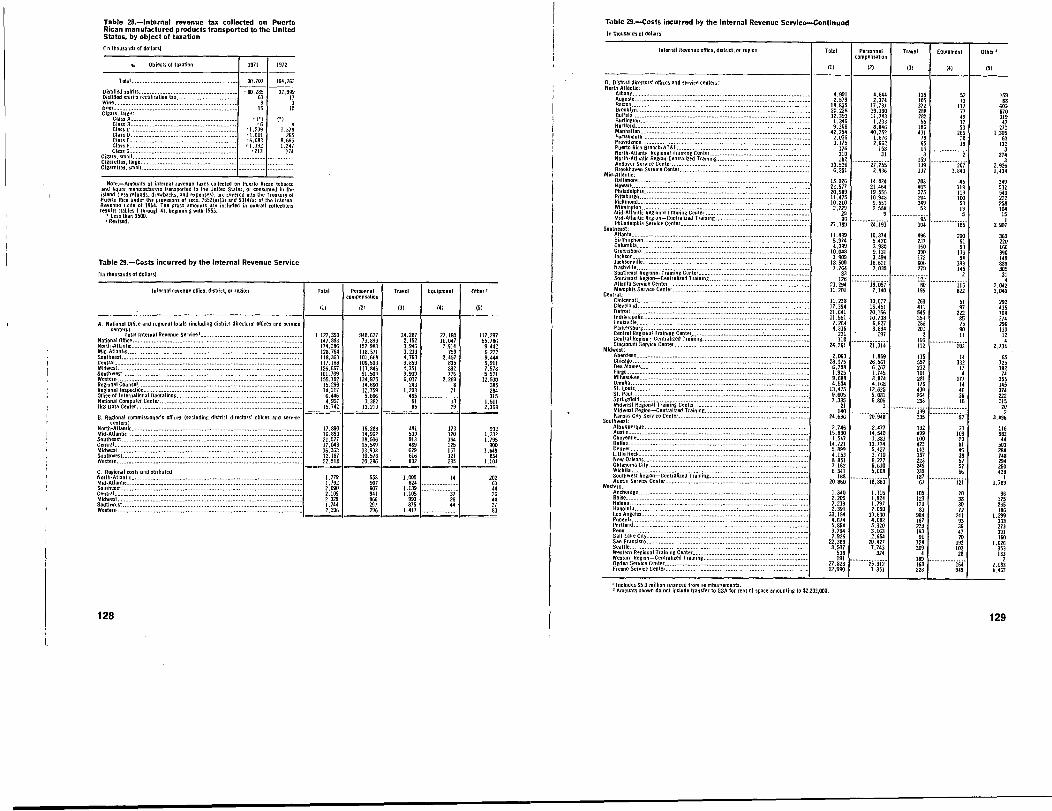

End of Era inRegulated OperationsThe Internal Revenue Service'sresponsibility for regulation of thealcohol and tobacco industries toassure compliance with variousFederal requirements ended atthe close of fiscal year 1972 after110 years . This responsibility andfirearms control activities, havebeen transferred to the TreasuryDepartment's Bureau of AlcoholTobacco and Firearms . In 197~the number of plants regulatedremained fairly stable, as did thenumber of activities requiringcompliance inspections . The ta-ble at the right and the firsttable on the next page reflectproduction volume and revenuecontrol manpower use for fiscalyear 1972 .

0 - 13 - 3

Workflow in the Internal Revenue Service and the courts, fiscal years 1971 and 107 2

'TWiri6mis India, teiaF-

Individual incomeCorporation incomeEstate and giftEmploy. tExciseOther income

Income, Estate, *no G

iF

L li,71 -72~W,446,§30 '111240111.449

76,619,563 77,105AS31,820,556 1 sibl'al 9

314 .913 =157621 .889 .343 22AO7435

2,400,704 11,3110,812L_2.401,85

- 19 .312.21 4

Number of refurims examined (Including terms 9901 1,5N,454 1,U7,30it fir djustments proposed by audit divisions 1.006,W 1,024.005Disposed of by audit divisions:

Agreed. paid, or obstaild led 956,311 111113.21160 me with 8It'a 46,119 36,723Transferred to appella

other 3,895 t 4,036

ciol cew sTotal received in appellate, division =LiVADisposed of by appellate divisions: Agreed,pald, or

defaulted 20--77 18,883L~o.ft. of .49inall jurisdiction !

Total petitioned to Tax Court Sam 8,949DismissedSettled by stipulation r

567 654'287 11,673

Settled by Tax C*urL decision 06 SaoTA t adby . but p 1 338 288

I

District courts and Court of Claims:Tout filed in district courts anti Court of Claim 1.177 1 A42Settled In district courts and Court of Cie I ms 647 B36Decided bydistriCtcmrtsand Courtof Claims

___!SO L ----!go

Settled by courts of appeals decision 355_'~ 463Favorable 1.Government 237 2"Favorable to taxpayers 95 128Modified 23 is

Decided by court of appeals but mi~ byWorteme Court 5

Supreme Court Settled by SuPmm& Ceurt decision 4 1 5

Fraud cesesi

IT-1pition in intelfilldivisions 2,482 2.S40

Disposed of be intelligence difrisivers;Pvtfuscution recommend 1:379 11795po,,.cut,ce, net

recommended 1 1421

486Disposed of by Office of Chief Ccureet h

Pnosecutim not warranted, including cases declinedby the Department of Justice

ProsectiI, i.-

Includes excise tax cases .

Production by alcohol and tba ... industries, fittest Yet, 197 2

Distilledst,'iri'sReCUlled distilled spirit.still wine

759 1

764.4 million tax gallons

120.7 million proof gallons

389a

i

efter~uscfxnt wines 22.9 million gallonsvermouth and other special 64 .5 fill- gallons

natural I.-Beer 140.3 Million gallons

Large cigarsSmall OffousCigarette.

165 .6 million596 .6 billion

1511,op q

~281.7 million gallons removed from bonded storage after determination of taxes due(in .l.de. 30 .3 million gallons of imported spirits transferred from Customs custody tobonded storage) ; 525 .3 million gallons tax freeF 1,107.6 million gallons in bonded storageat end of year.

Liquor Law EnforcementExtensive use of manpower tomeet expanded enforcement andregulatory responsibilities asso-ciated with intensified firearmsand explosive programs has hadan impact on Illicit liquor Investi-gations . In 1972, the Service usedonly 29 .4 percent of the investi-gator force for liquor law enforce-ment .

Illicit distillery seizures for 1972totaled 2,090, compared to 2,272in 1971 . Similar declines occurredin seizures of mash and non-taxpaid spirits . A more detailed sum-mary of accomplishments in liq-uor law enforcement is shown be-low .

Seizures of most of the nation'sillicit distilleries occur in theSoutheast Region and portions ofthe Central and Southwest Re-gions . The overwhelming majorityof these operations exist in therural areas of Alabama, Georgia,South Carolina, North Carolina,Mississippi, Tennessee, and Flor-ida.

"Operation Dry-Up," a programemploying heavy concentration ofFederal officers in three states ofthe Southeast Region, continuesto curb non-taxpaid whiskey traf-fic. This, along with stringent sen-tences in some court districts, hasreduced the number of personsderiving income from unregis-tered distilleries .

Revenue Growth-Alcohol and Tobacco TaxesDistilled spirits revenue rose to$3 .761 billion in fiscal year 1972,and tobacco taxpayments in-creased to $2 .207 billion In thesame period . The following tablepresents data on alcohol and to-bacco tax collections reflectingthe growth from 1863 to 1972 .

ATF revenue central manpower use

1971 107-1

Plants and permiteas subject to IRS regulatory control(excludes retail liquor defilers):Inspector man-years realized a3i

850On-site inspections completed 22,673 21,615Days of industry operation rec~uiring n.farmises,supervision 134,040 135,071

Permits issued, amended and terminated 24,471 21 A92Claim, offers-in-compromi- and assessment s

reviewed and processed 39,146 36,46 6

Results of criminal action in alcohol and tobacco case s

Action

Indictments and informationDisposals, tota l

Plan, guilty or nolo contehdereConvicted alter trialAcquittedNol-prossed or dismisse d

Seizures and arrests far alcohol and tobacco violations

It. .

Seizures ;DistilleriesStilts at distilleriesNon-taxpaid distilled spiritsMashVehiclesProperty (appraised value)

Arrests

Alcoholic BeverageAdvertising, Labeling ,Trade Practices

d bottlersDistillers, blenders anof spirits, producers and blendersof wine, and wholesalers and im-porters of all alcoholic beverages,operate under permits subject tosuspension or revocation for anyviolation of Federal liquor laws .in 1972, the Service revoked twopermits and suspended one per-mit while closing 83 cases involv-ing violations of the Federal Al-cohol Administration Act and theInternal Revenue Code throughacceptance of offers-in-compro-mise totaling $106,900 .

Revenue growth of alcohol and tobacco industries

(Amount-Thousand Dollam)

Distilled SpiritsWi aBeerTobacco Products

1863 197 2

3,3000 3,760,915.b8.8 101,223 .0

11558 .1 1,167,663.0

3,055.6 2,207,273.0

HUMber of defendants1971 1972

3,054 3,0293,169 3~lll2,166 2,11 5

612 478107 M284 2711

1971 1972 '

number 2,2722'090do 3327 21081

gallons 78,878 67'satzdo 1,387,986 .236,917

number 815 790dollars 1,071,138 :,490,686

number 3.222 3.19 1

Advertising Of alcoholic bever .ages must conform to statutoryand regulatory requirements andprohibitions. To insure compli .-ance, the Service examines ad-.vertising in a selected groupingof newspapers and magazines olgeneral circulation, and tradepublications . Service personnelexamined more than 18,000 pub-lications containing alcoholic

beverage advertisements duringthe year. In addition, comment Isoffered on proposed advertisingthemes or campaigns submittedfor examination .

Bottlers of distilled spirits, winesand malt beverages, and import-ers of such products, must obtaincertificates of label approval (orcertificates of exemption from la-bel approval for intrastate bot.tling) prior to removal of bottledgoods from establishments orCustoms custody. This year, theService approved 55,955 certifi-Cates of label approval and dis-approved 766 labels covering allclasses and types of alcoholicbeverages .

Alcohol, Tobacco andFirearms LaboratoriesSophisticated equipment and ad-ditional space enabled the Na-tional Office Laboratory and thethree field laboratories to broadenthe services offered in law en-forcement and revenue control .The number of criminal enforce-ment samples continued to in-crease. In 1972, the Service ana-lyzed 46,542 samples comparedto 33,374 in fiscal 1971 .

Chemical Staff ActivitiesThe laboratory received a largenumber of requests for non-alco-holic beverage flavors for specialnatural wines . Since artificial col-ors are not permitted In specialnatural wines, the laboratory isdeveloping less time-consumingartificial color tests using thinlayer chromatography .

In addition, the laboratory moni-tors various commercial wines forsodium content and pesticide res-idues and checks manufacturingProcesses of denatured alcoholusers for discharges of waste ma-terials . The staff authorized tol-uene as an alternate denaturantfor two denatured alcohol formu-las after reports that Benzene isa suspected carcinogenic agent

'The laboratory also devel0ped a

method of Differential Solvent Ex-tract to differentiate betweensmall cigars and cigarettes.

CERTIFICATES OF LABEL APPROVAL ISSUE D

no 1. - -

Forensic Staff WorkIn fiscal 1972, the Forensic Lab-oratory workload almost doubled .The staff examined approximately23,000 physical evidence samplesconnected with 3,230 cases in-volving illicit firearms and de-structive devices, illicit liquorconspiracies, income tax frauds,and other crimes. The photo lab-oratory processed about 80 re-quests per month for photographsof questioned documents. Thestaff also performed numerousspecial photo assignments foruse in court cases .

.1.

nz 1.

- - - 11. 111. 11.

The laboratory staff processedmore than 735 bomb cases andapproximately 344 documentcases. The Service used success .fully in court cases much of theevidence examined in connectionwith firearms and bomb offenses.Substantial increases occurred infirearms examinations involvingtool marks, ballistics, gunshotresidue, gunshot patterns andbullet identification . The numberof physical evidence samplessubmitted in connection with il-licit distillery operations re-mained nearly the same as lastfiscal year.

Formulas and Labels examimed

type 1971 1972

Formulas for nonbeverage food, flavors and medicinal products 2.010 2,100Formulas for specially denatured articles 3,897 4,151Label requests for alcoholic t0iietri~, medicines, etc . 8,286 6.873Rectified products 1,197 11089Wine 215 293

I Increase in wine formulas reflects apparent consumer acceptance of the cu, .rently Popular sweet-flavored wines.

22 23

Audit Contribution to

Strike Force ActivitiesThe Audit Division contributesleads and expertise in recon-structing complicated financialtransactions which help otherFederal agencies obtain indict-ments for violations outside ofthe Service's jurisdiction. It hasasserted substantial tax liabilitieswithin the Service's jurisdiction .The table at the right reflects theeffort expended and results ob-tained .

The War AgainstNarcotics Trafficker sIn June 1971, the President calledfor an increased effort to combatthe growing problem of drugabuse. The Service set up a spe-cial program to conduct tax in-vestigations on key figures en-gaged in narcotics traffic. Theobjectives are to prosecute thosewho have committed' criminaltax violations and to reducedrasticaly the profits from the il-licit drug traffic by assessingtaxes and penalties on unre-ported profits . The Service hasassigned 189 revenue agents, 268special agents, and 110 clericalsupport personnel to the project .A Target Selection Committeecomposed of Treasury's Directorof Law Enforcement, with mem-bers from the Bureau of Customs,the Bureau of Narcotics and Dan-gerous Drugs, and the Audit andIntelligence Divisions of the In-ternal Revenue Service estab-lishes criteria and Identifies sub-jects for investigation. The com-mittee identified 697 targets in 49districts for joint investigationand 94 for independent audit.Agents completed 155 cases andrecommended prosecutions of 56persons . Of those, 7 have beenindicted and convicted . Addi-tional tax and penalties of 43million have been assessed orrecommended for assessment.In addition, the Service issuedspontaneous assessments (ter-minations of taxable years andjeopardy assessments) amount-ing to $49 .9 million . Agentsseized $7.2 million in cash and

26

Audit Strike Force Accomplishments

PeriodRanumsho

AgentsAssigned

1967-1970 1761971 3511972 549

$1 .3 million in other propertyafter the spontaneous assess-ments . The largest seizure oc-curred in New York on April 29,1972, when investigators discov-ered $1,078,100, a part of whichwas concealed in a basementwall and the remainder foundburied in the backyard of a con-victed heroin distributor .

R-infinamde'dClosed Additiona l

Exami nations Tax &penalties

PendingExarni-nations

itnifficm.)

1 .302 $ 22.2 2.3682,731 $105.6 3,7085,894 $254.8 2.866

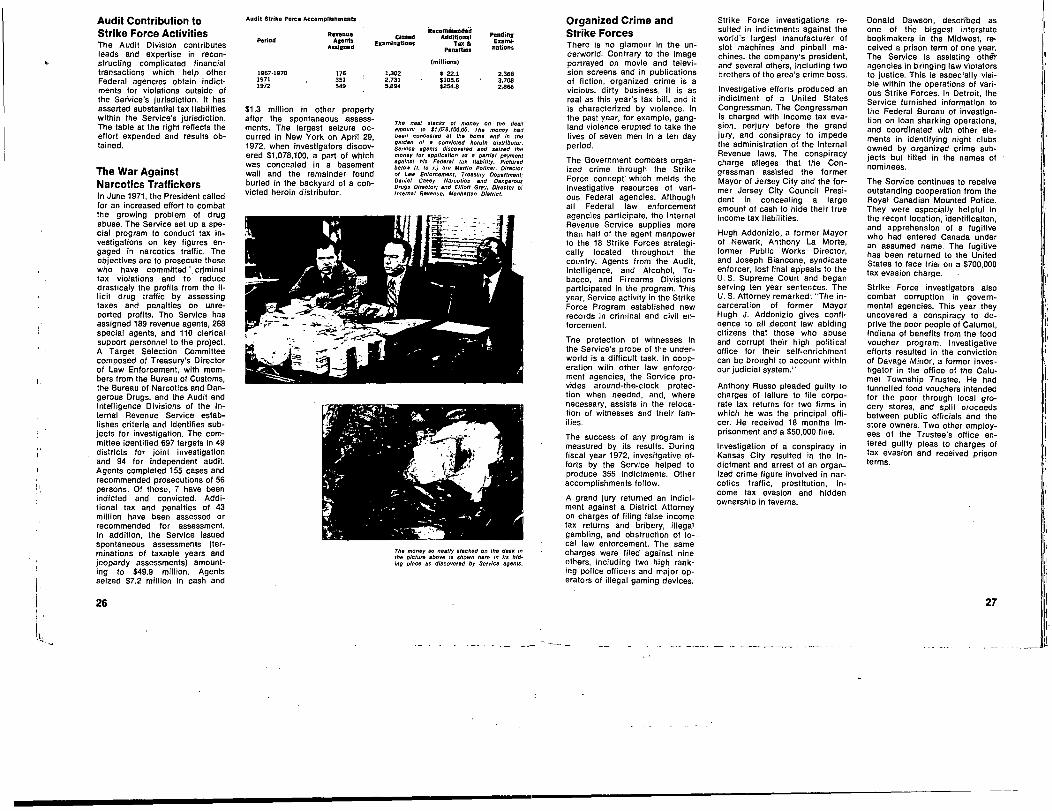

The neat stacks of money on the defutamount 10 $1,078,100.00. The money hadbeen concealed at the home and In theg:m6n of a convicted heroin distributor.S

rvice agents discovered and W~.d themoney to, application as a partial paymentag inst his Federal tax Ilebtlify . Picturedb