GST Guide for the Catholic Church GST Guide for the Catholic Church Australia

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

GST Guide for theCatholic ChurchGST Guide for theCatholic Church

Australia

iG S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

i

GST Guide for theCatholic ChurchGST Guide for theCatholic Church

Australia

The costs associated with the development of the materials set out in thisresource kit have been funded by the Commonwealth Government's GST Start-up

Assistance Program. The costs of mounting seminars based on the information contained in the resource kit have also

been funded by the same program.

Designed and Printed byColourprint Australia Pty Ltd

203 Arden Street, North Melbourne 3051

Acknowledgment

iiG S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

ii

Catholic Bishop Australian Conference

Australian Conference ofLeaders of Religious Institutes

iiiG S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

iii

Important information concerning this material - please read

These limitations and warnings also apply to information based on this material presented at anyseminars or workshops provided as part of the GST Start-up Assistance Program.

This material is provided under theCommonwealth's GST Start-up AssistanceProgram, and is designed to provide generalinformation on the GST and on business skills,practices and processes necessary to operatewith the GST, focussed on small and mediumenterprises and the community and educationsectors. Because business circumstances canvary greatly, the material is not designed toprovide specific GST or business advice forparticular circumstances. Also, because aspectsof the GST are complex and detailed, thematerial is not designed to comprehensivelycover all aspects of the GST as it applies tosmall and medium enterprises and thecommunity and education sectors. Further, thelaws implementing GST, and rulings anddecisions under those laws, may change.

Before you use this material for any importantmatter for your business, you should:

▲ make your own enquiries aboutwhether the material is relevant andstill current, and whether it dealsaccurately and completely with thatparticular matter; and

▲ as appropriate, seek your ownprofessional advice relevant to thatparticular matter.

This material is provided on the understandingthat neither the Commonwealth or itspersonnel, nor any other organisation orperson involved in developing or delivering theGST Start-up Assistance Program, is therebyengaged in providing professional advice for aparticular purpose.

DISCLAIMER

ivG S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

iv

General IssuesFor a considerable period, the Catholic Church and Religious Orders in Australia have been largelyexempted from taxes in lieu of the not-for-profit service they have provided to society. Whilst thisprinciple of exemption from taxation has been maintained in The New Tax System to operate from 1July 2000, the Catholic Church, Religious Orders and their various operating entities will be drawninto the taxation system for the first time through a process of registration and endorsement of theirindividual taxation status.

The centerpiece of The New Tax System is a goods and services tax (GST) that will apply to a widerange of goods and services. Not all goods and services will be subject to GST. However, there are noexemptions available to individuals or other entities (religious, charitable, not-for-profit orcommercial). Given these features of The New Tax System, all aspects of the operations of entitiesof the Catholic Church and Religious Orders may be subject to the provisions of the GST.

Depending on decisions made by individual entities of the Catholic Church and Religious Ordersregarding registration connected with The New Tax System, many entities will take on particularperiodic reporting responsibilities to the Australian Taxation Office (ATO) for the first time.

This consequence of The New Tax System means that entities within the Catholic Church andReligious Orders will face a number of challenges. These include the following:

(1) The assimilation of new concepts associated with the manner in which the detail of theiroperations are described.

(2) The cash flows of individual entities will be impacted by the GST and the removal ofWholesale Sales Tax.

(3) Individual entities will need to arrange their affairs to accurately record the collection andpayment of the GST to facilitate the completion of periodic reporting to the ATO.

(4) Individual entities will need to become aware of the specific requirement of the legislation asregards GST invoices and other matters such as withholding of tax which will have animportant bearing on periodic reporting to the ATO. In this context, entities will need to payparticular attention to the training of staff and the upgrading of record keeping systems.

(5) Individual entities may need to upgrade the responsiveness of their reporting systems so thatperiodic reporting to the ATO is timely, accurate and capable of passing audit by the ATO. Inthe past, financial reporting in a commercially orientated time-frame was often a matter ofrelatively low priority.

Against the background of these challenges, this reference resource has been prepared. The resourceconcentrates on those issues connected with The New Tax System that are of particular concern toentities connected with the Catholic Church and Religious Orders.

It is important to note that by virtue of the structure of the Church in Australia, and the fact that the existing structure has developed over a long period without contact with the taxation system, it will be impossible for every situation connected with The New Tax System and the Churchto be canvassed.

Individual entities are encouraged to develop appropriate working relationships with Diocesan orReligious Order co-ordinators in developing management techniques to adapt to the new operatingenvironment precipitated by the legislative requirement of The New Tax System.

I n t r o d u c t i o n

INTRODUCTION

vG S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

v

viG S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

vi

Contents

viiG S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

vii

1 1. Objective of the Material 1

2 2. The New Tax System 32.1 The Introduction of Goods & Services Tax 32.2 Personal Income Tax Cuts 32.3 Pay As You Go (PAYG) 32.4 Fringe Benefits Tax Changes (FBT) 3

3 3. Assistance Available for Change to GST 5-73.1 Government Assistance 5

3.1.1 GST Start-Up Assistance Office 53.1.2 Australian Taxation Office 53.1.3 New Taxation System Advisory Board 5

3.2 Australian Catholic Church Tax Working Group 5-63.3 Other Government Organisations 6

3.3.1 Australian Competition & Consumer Commission (ACCC) 6

3.4 Commonwealth Ombudsman 7

4 4. Introduction and Overview 9-10

5 5. GST Terms and Specific Meanings 11-155.1 Enterprise 115.2 Entity 115.3 Acquisition 115.4 Adjustments 11-125.5 Attribution Rules 12

5.5.1 Cash Basis 125.5.2 Accrual Basis 12

5.6 Australian Business Number (ABN) 12-135.7 Business Activity Statement (BAS) 135.8 Consideration 135.9 Creditable Acquisitions 135.10 Goods & Services 13-145.11 Input Tax Credit 145.12 Sub-Entity 145.13 Supply 145.14 Tax Fraction 155.15 Tax Invoice 155.16 Tax Period 15

C o n t e n t s

5.17 Value 15

6 6. How the GST Operates 17

7 7. Impact on the Church 19-217.1 Diocesan Parish Priests 197.2 Diocesan Assistant Priests, Specialist Priests, Deacons 207.3 Diocesan Priest - Chaplains 207.4 Religious Orders 207.5 Parishes/Religious Congregations - Income 207.6 Parishes/Religious Congregations - Expenditure 20-217.7 Associated Church Entities 21

8 8. Supply Transactions 23-258.1 Taxable Supplies 23-248.2 GST-free Supplies 24-258.3 Input Taxed Supplies 258.4 Other Supplies 25

9 9. Church Transactions 27-289.1 Religious Services 279.2 Charities 27-28

9.2.1 Non-Commercial Activities 279.2.2 Fundraising 27-289.2.3 Donations & Gifts 289.2.4 Grants 289.2.5 Sponsorships 28

10 10. Acquisitions (Purchases) 29

11 11. Specific Requirements for the Church 30-3611.1 Working out the GST 30-3111.2 Identification of the GST Implications of all Transactions 3111.3 Record Keeping 31-3211.4 System Checks 3211.5 Transaction Analysis 33-36

12 12. Registration and Endorsement 37-3812.1 Registration for an Australian Business Number (ABN) 3712.2 Registration for GST 37

C o n t e n t s

viiiG S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

viii

12.3 Endorsement as a Income Tax Exempt Charity (ITEC) 3812.4 Endorsement as a Deductible Gift Recipient (DGR) 38

13 13. Australian Business Number (ABN) Registration 39-40

14 14. GST Registration 41-4314.1 Turnover 4114.2 Why Register for GST 4114.3 Registration Implications 42

14.3.1 Charge GST 4214.3.2 Claim Input Tax Credits 4214.3.3 Reporting to the ATO 4214.3.4 Cash Flow Implications 42 14.3.5 Other Implications 42

14.4 Non-Registration Implications 42-4314.4.1 Cannot Claim Input Tax Credits 4214.4.2 Cannot Claim a WST Credit 4214.4.3 Reporting to the ATO 42-4314.4.4 Constant Monitoring of Turnover 43

14.5 Registering for GST 4314.6 Cancelling your GST Registration 43

15 15. Form of Registration 45-4615.1 Individual 4515.2 Grouping 4515.3 Branches 4515.4 Non-Profit Sub-Entities 45-46

16 16. Income Tax Exempt Charity (ITEC) Endorsement 47-48

17 17. Deductible Gift Recipient (DGR) Endorsement 49-50

18 18. Registration Sequence 5118.1 Registering Legal Entities 5118.2 Registering a Non-Profit Sub-Entity 5118.3 Applying for ITEC & DGR Endorsement 5118.4 Registering a Branch 5118.5 Registering a Group 51

19 19. Accounting for GST 53

C o n t e n t s

ixG S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

ix

19.1 Cash v Accrual Accounting 5319.2 Cash Basis 5419.3 Accrual Basis 54

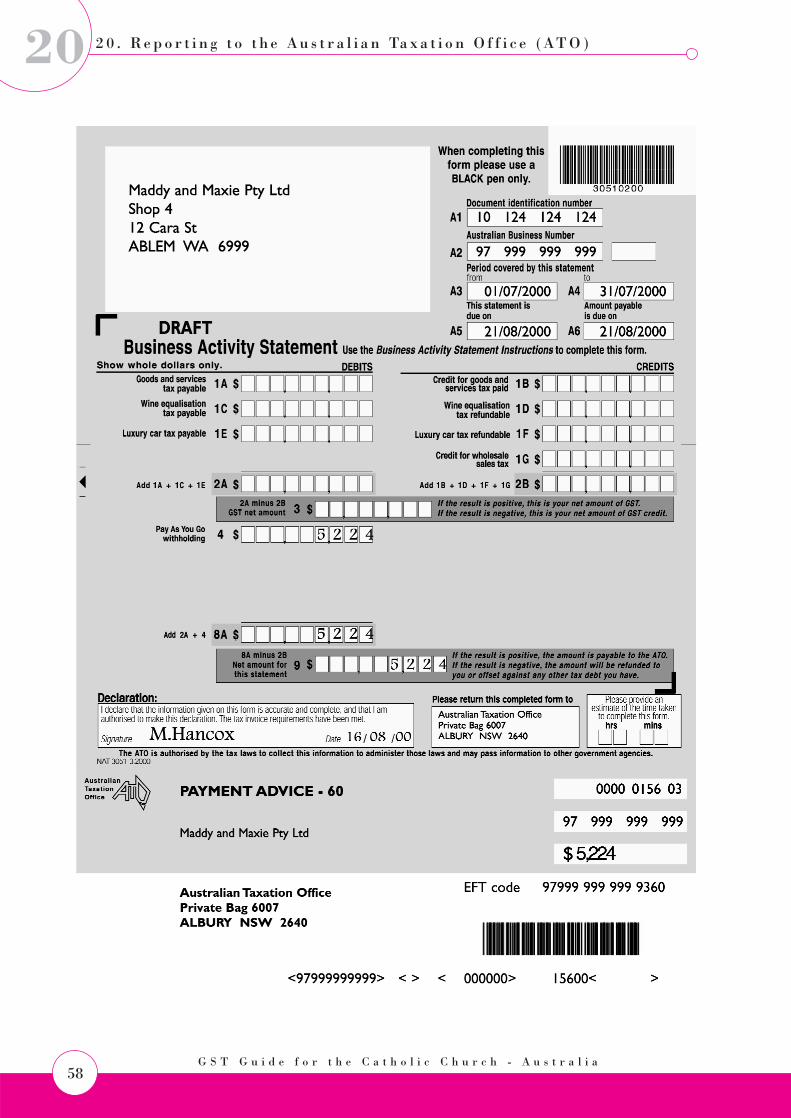

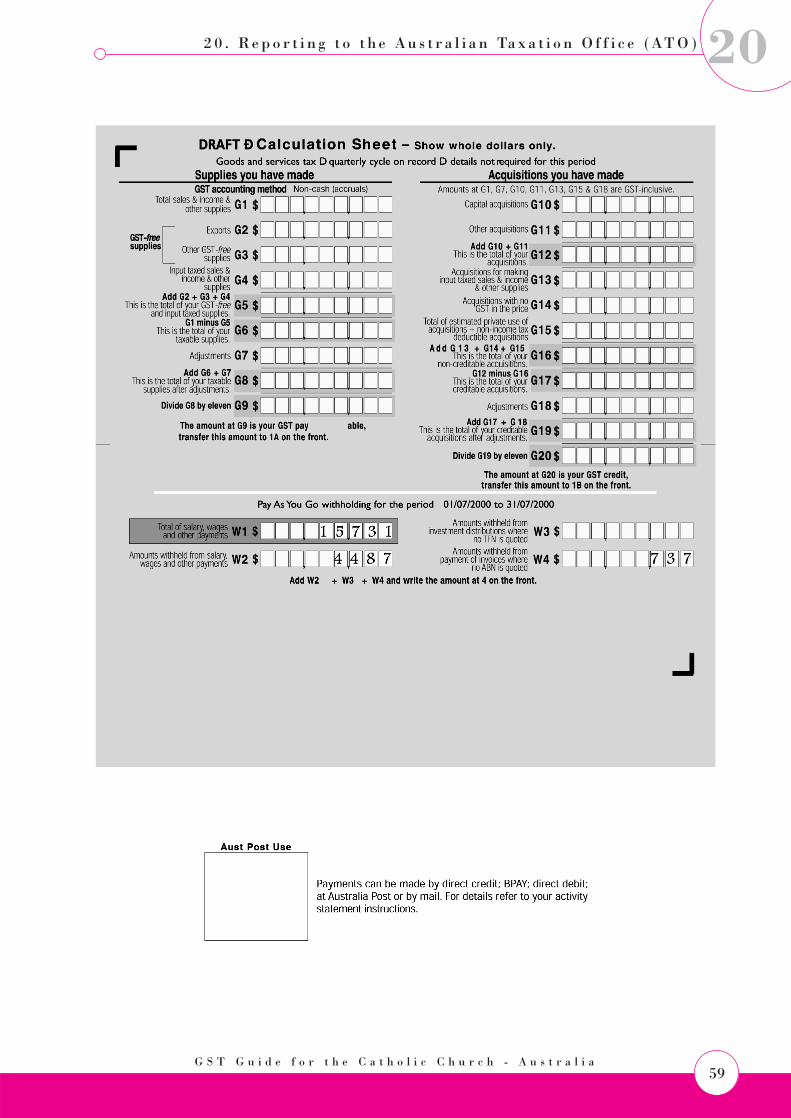

20 20. Reporting to the Australian Taxation Office (ATO) 55-5920.1 Tax Periods 5520.2 Quarterly Reporting 5520.3 Monthly Reporting 5620.4 Business Activity Statement (BAS) 57-59

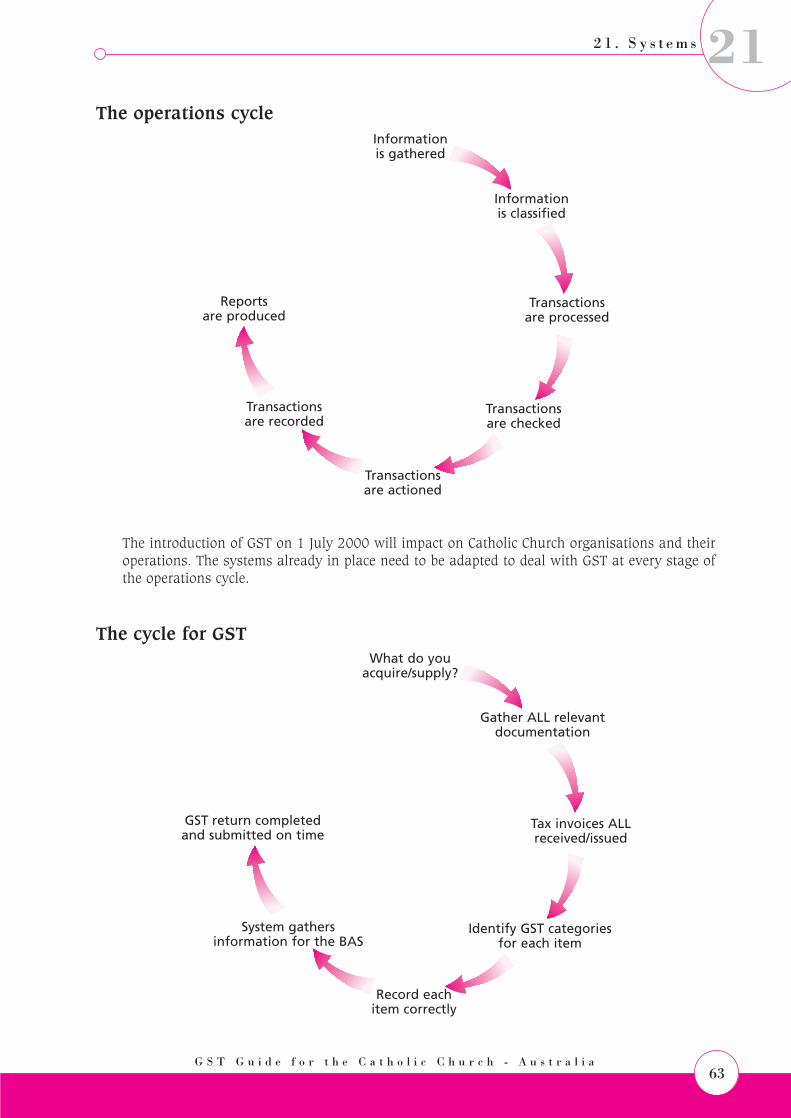

21 21. Systems 61-6321.1 What is a System? 6121.2 Why are Systems Important? 6221.3 Why Do Systems Change? 6221.4 The Operation Cycle 62-63

22 22. Systems & Staff 65-66

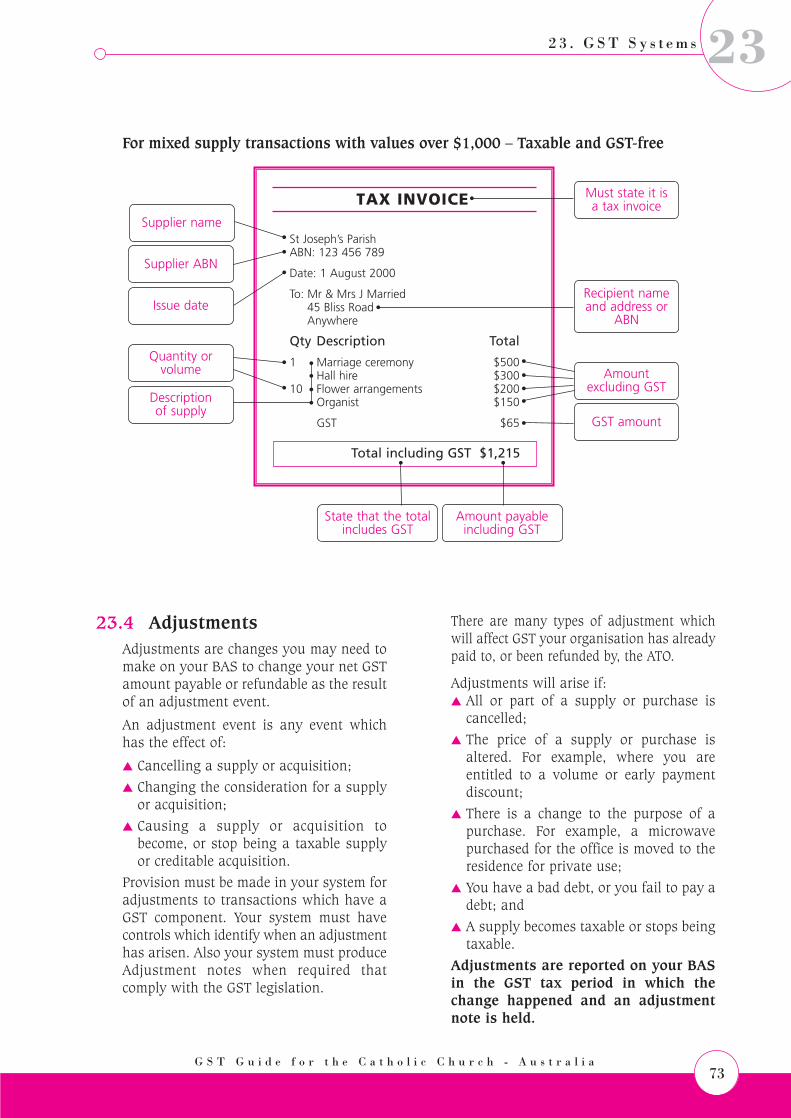

23 23. GST Systems 67-7523.1 Supplies & Acquisitions 6723.2 GST Status of Transactions 67-6823.3 Source Documents 68-73

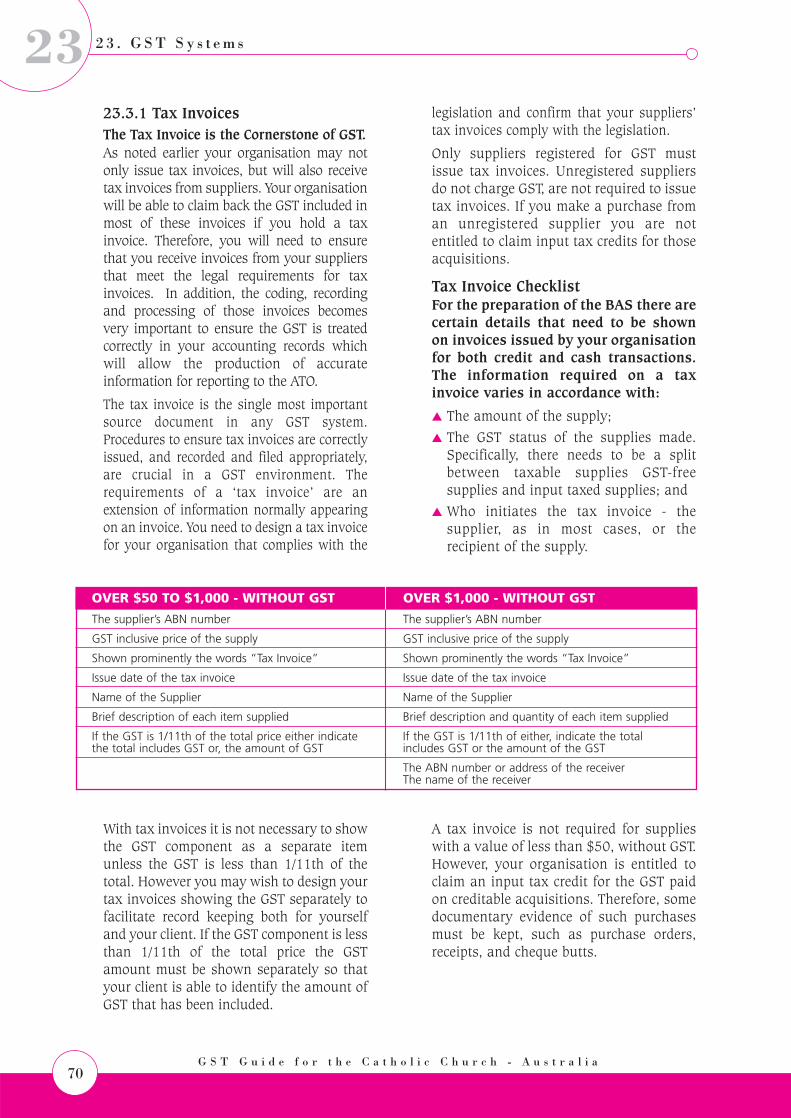

23.3.1 Tax Invoices 70-7123.3.2 Bank Statements 71-73

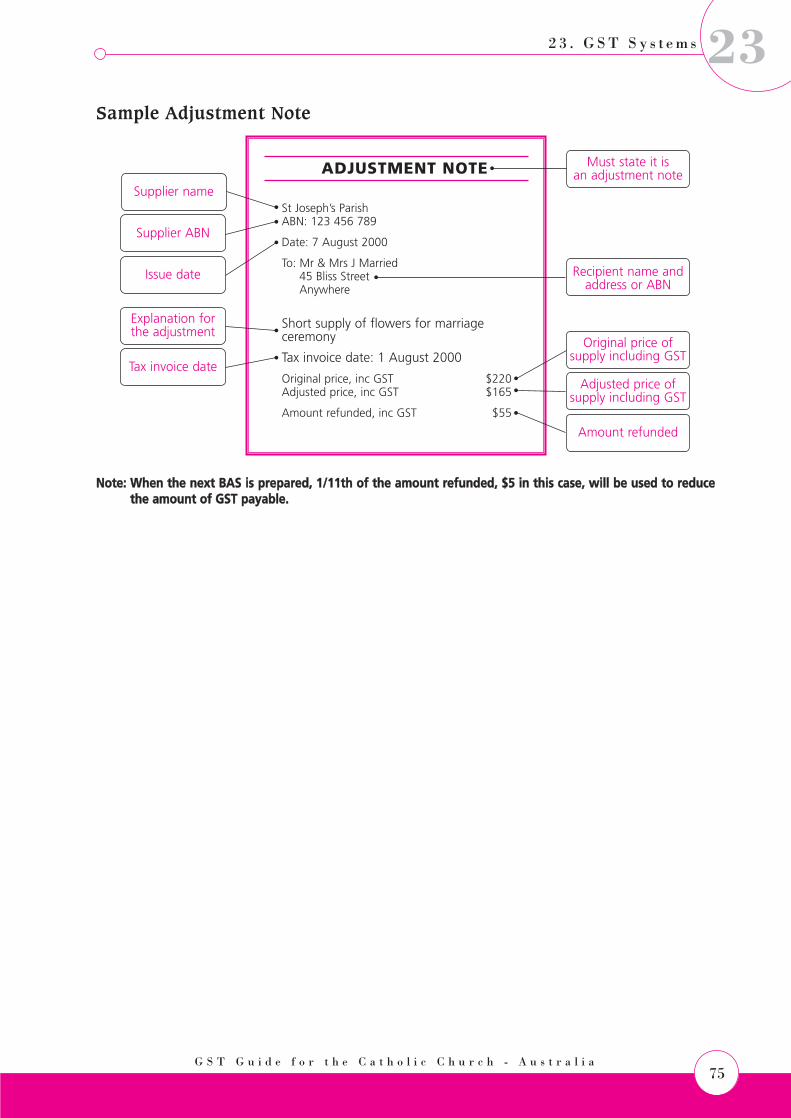

23.4 Adjustments 73-75

24 24. GST Systems - Recording 77-7924.1 Computer or Manual 78-7924.2 Income & Expenditure 7924.3 Irregular Transactions 79

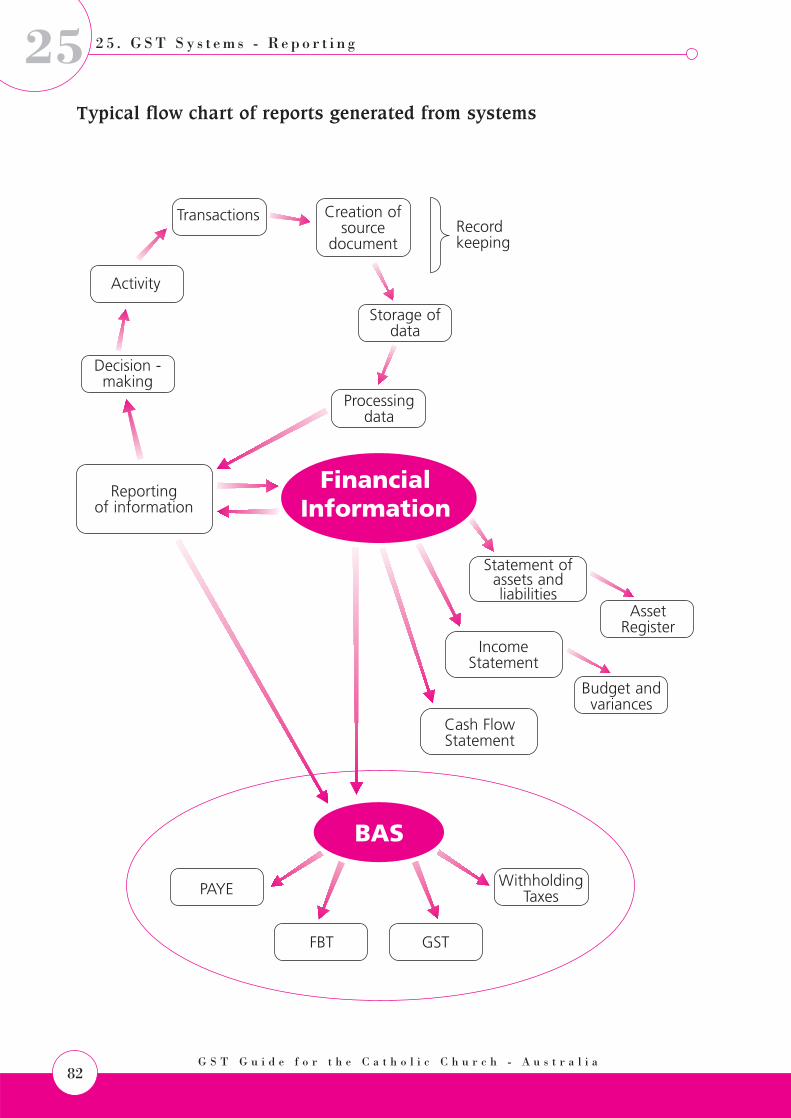

25 25. GST Systems - Reporting 81-82

26 26. Risk Management 8526.1 Misclassifying Supplies 8526.2 Incorrect Recording & Reporting of GST 8526.3 Tax Invoices 8526.4 Cashflow 8626.5 Contracts 86

C o n t e n t s

xG S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

x

26.6 Insurance 8626.7 Pricing 86

C o n t e n t s

xiG S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

xi

xiiG S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

xii

The introduction of The New Tax Systemincluding the GST has required the CatholicChurch in Australia to address the issue oftaxation. Previously, the Catholic Churchonly had to deal with some of these issueslisted below:

▲ Tax deductibility status;▲ Sales tax exempt status;▲ Fringe benefits tax for employees; and▲ Income tax for employees.From 1 July, all Catholic Church entitieswill be required to pay a business taxrelated to that entity's economic activityand to produce additional financialstatements on a regular basis.

This information therefore, aims to providea comprehensive and straightforwardapproach for parish/congregationalpersonnel to deal with the key issues of taxreform and its implementation withinparish/congregational financial structureswith minimal input from specialistadvisers.

1 . O b j e c t i v e o f t h e M a t e r i a l

1. Objective of the Material

1G S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

1

N o t e s

Notes

2G S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

2.1 The Introduction of Goodsand Services Tax

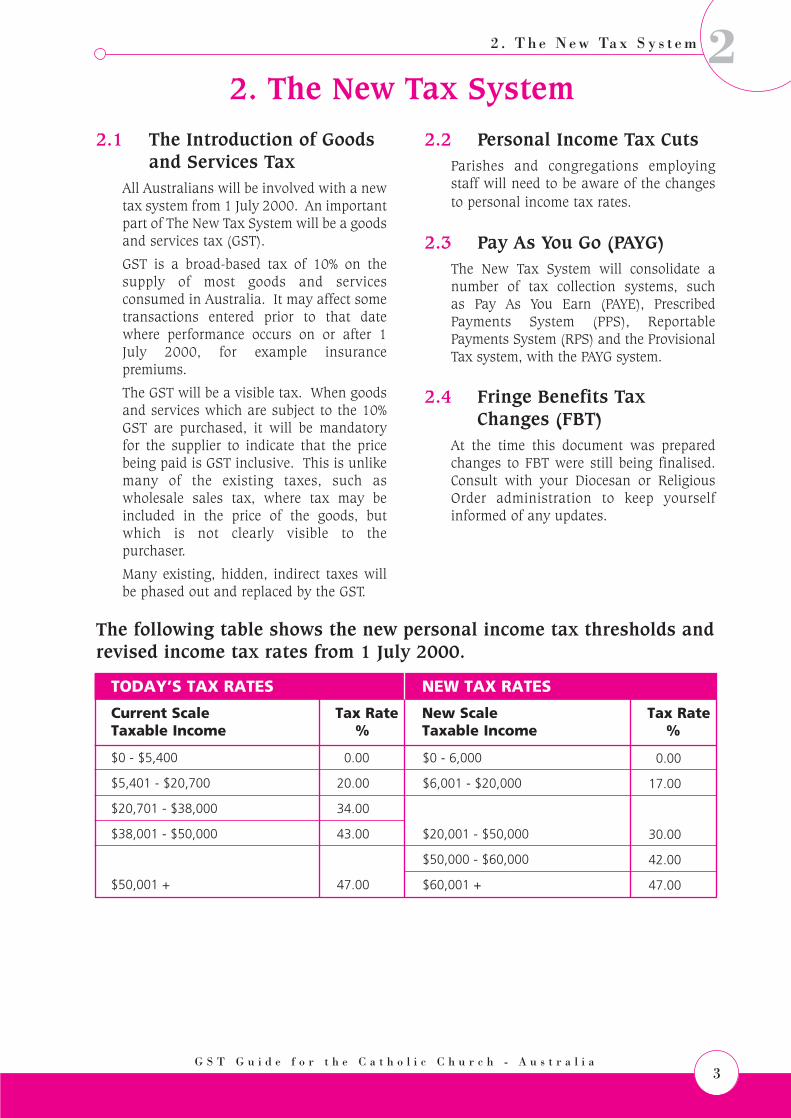

All Australians will be involved with a newtax system from 1 July 2000. An importantpart of The New Tax System will be a goodsand services tax (GST).

GST is a broad-based tax of 10% on thesupply of most goods and servicesconsumed in Australia. It may affect sometransactions entered prior to that datewhere performance occurs on or after 1July 2000, for example insurancepremiums.

The GST will be a visible tax. When goodsand services which are subject to the 10%GST are purchased, it will be mandatoryfor the supplier to indicate that the pricebeing paid is GST inclusive. This is unlikemany of the existing taxes, such aswholesale sales tax, where tax may beincluded in the price of the goods, butwhich is not clearly visible to thepurchaser.

Many existing, hidden, indirect taxes willbe phased out and replaced by the GST.

2.2 Personal Income Tax CutsParishes and congregations employingstaff will need to be aware of the changesto personal income tax rates.

2.3 Pay As You Go (PAYG)The New Tax System will consolidate anumber of tax collection systems, suchas Pay As You Earn (PAYE), PrescribedPayments System (PPS), ReportablePayments System (RPS) and the ProvisionalTax system, with the PAYG system.

2.4 Fringe Benefits TaxChanges (FBT)

At the time this document was preparedchanges to FBT were still being finalised.Consult with your Diocesan or ReligiousOrder administration to keep yourselfinformed of any updates.

2 . T h e N e w Ta x S y s t e m

2. The New Tax System

3G S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

2

TODAY’S TAX RATES NEW TAX RATES

Current Scale Tax Rate New Scale Tax RateTaxable Income % Taxable Income %

$0 - $5,400

$5,401 - $20,700

$20,701 - $38,000

$38,001 - $50,000

$50,001 +

$0 - 6,000

$6,001 - $20,000

$20,001 - $50,000

$50,000 - $60,000

$60,001 +

0.00

17.00

30.00

42.00

47.00

0.00

20.00

34.00

43.00

47.00

The following table shows the new personal income tax thresholds andrevised income tax rates from 1 July 2000.

N o t e s

Notes

4G S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

3.1 Government Assistance

3.1.1 GST Start-Up Assistance OfficeThe Government has set aside $500million to assist small and mediumenterprises, the community sector andeducational bodies (SMECEs) to adjust tothe GST environment.

The GST Start-Up Assistance Office wasestablished to administer these funds inconsultation with The New Tax SystemAdvisory Board and two advisory panels;one covering small and mediumbusinesses and the other the communitysector and educational bodies.

What kind of assistance is available?The GST Start-Up Assistance Office hasdeveloped four programmes to helpSMECEs adjust their business practices,namely:

Organisation-Delivered AssistanceSelected industry and professionalorganisations will provide a broad range ofeducation and information services to theirmembers and non-members.

Business Skills EducationThe GST and Business Skills - an ActionGuide is available now to help you becomeGST-ready. The GST Business AssistHelpline (13 30 88) is open from 9am -9pm nationally to provide help on thenecessary skills, practises and processes toprepare you for the GST.

Adviser EducationAn education programme for informaladvisers who assist small business,community groups and educational bodies.

Direct AssistanceDirect assistance will also be available tosmall and medium businesses andcommunity organisations that register forGST. Redeemable certificates that can beexchanged for products or servicesacquired to assist in the implementation ofthe GST will be available.

These four programmes have the commongoal of ensuring that SMECEs have the

opportunity to access information andassistance to adjust their enterprises to theGST environment.

3.1.2. Australian Taxation Office(ATO)

The ATO has the role of providing guidanceand assistance with technical changes thatwill arise from the introduction of The NewTax System.

The assistance provided by the ATOincludes a range of publications fromgeneral purpose guides, to industry sectorpublications directed at the specific issuesto be addressed by various industries andcommunity groups.

The ATO is also providing a wide range ofseminars to assist with the introductionand implementation of the changes.

3.1.3 New Tax SystemAdvisory Board

To ensure the successful introduction ofThe New Tax System the Government hasput in place a large number of programmesto assist businesses, community groups,the educational sector, and the Australianpublic prepare for the changes arising fromThe New Tax System.

To oversee the changes the Governmenthas established The New Tax SystemAdvisory Board. This “Board” has as oneof its most important roles, the oversight ofa major education programme about TheNew Tax System for all sectors of Australiansociety to assist them with preparations forthe changes that will be necessary.

3.2 Australian Catholic ChurchTax Working Group

The Australian Catholic Church TaxWorking Group (ACCTWG) was formed tofacilitate a national coordinated approachto deal with tax reform issues as a result ofThe New Tax System. There had been anumber of local meetings at diocesan levelbetween heads of department and taxexperts, followed later by nationalmeetings. The first national meeting was

3 . A s s i s t a n c e Av a i l a b l e f o r C h a n g e t o G S T

3. Assistance Available for Change to GST

5G S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

3

held on 11 January 1999. Soon after, asubmission was made to the AustralianCatholic Bishop Conference (ACBC) &Australian Conference of Leaders ofReligious Institutes (ACLRI) for theformation of a national tax working group.The ACCTWG was formed in March 1999.The main aim of the group is to:

▲ Provide a point of reference and liaisonwith Tax and Treasury officials;

▲ Assist Dioceses, Religious Orders andAgencies to define and describe commonissues in dealing with tax reform, inparticular with GST;

▲ To assist in the development of strategyand policy in response to tax reform;and

▲ Address issues concerning GST start upand implementation around Australia.

The ACCTWG has also been activelyinvolved in meeting with and lobbying,both government and ATO officials inmatters concerning interpretation andrefinement of tax legislation.

3.3 Other GovernmentOrganisations

3.1.3 Australian Competition &Consumer Commission (ACCC)

The ACCC has specific legal powers toensure that there is no price exploitation inrelation to price changes brought about byThe New Tax System changes.

Tax Changes Covered by the PriceExploitation GuidelinesThe ACCC will ensure that there is no priceexploitation in respect of the followingtaxation changes:

▲ A reduction in the Wholesale Sales Tax(WST) rate of 32 percent to 22 percent(29 July 1999);

▲ Introduction of the GST (1 July 2000);▲ Abolition of WST (1 July 2000);▲ Changes to excise on petrol and diesel

and to the Diesel Fuel Rebate Scheme(1 July 2000);

▲ Changes to excise on alcoholic beverages(1 July 2000);

▲ Changes to excise on cigarettes (from1 November 1999);

▲ Introduction of a ‘Luxury Car Tax’(1 July 2000);

▲ Abolition of bed taxes (1 July 2000); and▲ Abolition of State taxes on bank

transactions (Financial Institutions Duty1 July 2001 Debits Tax by 1 July 2002)and stamp duties on marketablesecurities (1 July 2001) and remainingbusiness stamp duties (date to bedetermined).

The ACCC’s Focus in Evaluating PricesIt is the Government’s intention thatconsumers should benefit fully fromreductions in indirect tax and should notbe exposed to greater than necessary taxrelated price rises. There should be no priceexploitation of consumers.

In line with the Government’s intention,the ACCC will examine how prices move inrelation to The New Tax System changes.The ACCC’s focus is on prices set byindividual entities and is primarily onchanges in prices resulting from the taxchanges, not on the level of prices.

Price Exploitation Hotline on1300 302 502.

ExamplePrior to 30 June 2000, Vinnie’s Boutiquepurchased a microwave oven for $100(including WST). They typically added a50% markup, and sold such items for $150.

With the introduction of GST and theabolition of WST, a like item would bepurchased for say $88. Eg. The item wouldcost $80 and there would be $8 GST.

In a GST environment, the pricingpattern would become:Full purchase price 88.00Less: GST 8.00Net cost 80.00Normal dollar margin 50.00New selling value 130.00Add: GST 13.00New selling price 143.00

3 . A s s i s t a n c e Av a i l a b l e f o r C h a n g e t o G S T

6G S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

3

3.4 CommonwealthOmbudsman

The Commonwealth Ombudsmaninvestigates complaints aboutCommonwealth Government Departmentsand Agencies. S/he may also recommendthat Departments and agencies provide asolution or remedy to complaints.

Individuals, businesses, clubs, groups,community organisations, Commonwealthgrant recipients, charities and others mayhave a complaint about the actions ordecisions of government agencies as TheNew Tax System is implemented. Wherecomplaints cannot be resolved directlywith the agency the matter can be raisedwith the Special Tax Adviser of theCommonwealth Ombudsman.

The Ombudsman’s Office has wide powersto conduct an independent investigationof complaints. Call the NationalComplaints Line on 1 300 362 072.

3 . A s s i s t a n c e Av a i l a b l e f o r C h a n g e t o G S T

7G S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

3

N o t e s

Notes

8G S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

Introduction DateGST starts on 1 July 2000; however, it mayaffect some transactions entered prior tothat date where performance occurs on orafter 1 July 2000.

Tax RateGST is a broad-based tax of 10% on thesupply of most goods and servicesconsumed in Australia.

Replacement TaxGST is a visible tax. When goods andservices which are subject to the 10% GSTare purchased, it will be mandatory for thesupplier to indicate that the price beingpaid is GST inclusive. Many existing,hidden, indirect taxes will be phased outand GST will replace them. (See Chapter3.3.1 on the role of the ACCC for a listing ofwhich taxes are being abolished.)

Although GST will replace some existingtaxes, the GST charged to an enterprise byits suppliers, in many situations, will berecoverable from the ATO.

A Tax on Transactions - A Consumption TaxWhat is a GST? The main principles arethat it is a tax:▲ Applied to the domestic Australian

consumption of goods and services, ieon transactions; and

▲ It is paid by the final consumer.The first key concept here is domesticAustralian consumption. That meansthe GST does apply to imports, but doesnot apply to exports

As well, it is about the consumption ofgoods and services. So GST is a tax ongoods and services and not on income.Therefore, an intention to make a profit isirrelevant in deciding whether anorganisation must pay GST.

No Entities are Exempt from GSTIt follows that many organisations that arenot currently considered to be carrying ona ‘business’ for income tax purposes willnevertheless be included in the GST net.Such organisations (which the legislationcalls entities) include church bodies,charities, trusts, co-operatives, sportingand other clubs, statutory bodies and localauthorities.

Not all Goods/Services are Subject to GSTGST is not charged, or payable to the ATO,on GST-free supplies. The major categoriesof GST-free supplies are:

▲ Basic food▲ Medical services▲ Other health services▲ Hospital treatment▲ Residential care▲ Community care▲ Private health insurance▲ Education services▲ Child care ▲ Exports▲ Religious services▲ Farm land▲ Supplies through inward duty free shops▲ Supplies of precious metals▲ Sales of going concerns

(sale of ‘businesses’)But not all supplies falling into thesecategories will be GST-free.

While these general categories of supplymay be GST-free, each has a very specificmeaning. Your supplies need to fall intothose very specific definitions to be GST-free. Remember - if you make a mistakeand don’t charge GST because you thoughtthe supply was GST-free, but it later turnsout to be taxable, the GST liability restswith you not the consumer.

4 . I n t r o d u c t i o n & O v e r v i e w

4. Introduction and Overview

9G S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

4

Be sure you carefully check the details ifyou make supplies that fall into thesecategories. You may want to seek adviceon the impact of the GST-free rules for yourparticular entity from your Diocesan orCongregational contact, a professionaladviser or the ATO.

If a an entity makes GST-free supplieshowever, it is still able to claim back GSTinput tax credits on the purchase of anygoods and services acquired to allow it tomake those GST-free supplies.

Example

A priest conducts a funeral service andreceives a stipend. In this situation, thepriest makes a GST-free supply. Thoughthe priest is making a GST-free supply,he is still able to claim back the GST paidon the expenses of running the churchsuch as telephone, electricity, insurance,candles, incense, and charcoal.

The GST is RecoverableIf an entity is registered for GST, the GSTpaid on acquisitions is recoverable fromthe ATO. For unregistered entities the GSTis a cost because it cannot be recovered.

Church entities will need to balance thelikely level of compliance costs against thecost of absorbing the GST paid onacquisitions when deciding whether or notto register for GST. This only applies forentities connected with the Church andReligious Orders with annual turnover lessthan $100,000.

4 . I n t r o d u c t i o n & O v e r v i e w

10G S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

4

5 . G S T Te r m s a n d S p e c i f i c M e a n i n g s

5. GST Terms and Specific Meanings

11G S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

5

To register for GST you must be an entityconducting an enterprise. So both of theseterms - enterprise and entity - are central tothe operation of the GST, and are critical indetermining if you are required to registerfor GST. We look at these terms in turn.

5.1 EnterpriseEnterprise is about making things happenand getting things done.

Enterprise manifests itself in many ways.It may be parishioners grouping togetherto raise funds for the parish or it may bethe parish providing a range of services forthose in the community who are in need ofspecial support and assistance. In abusiness context it may be a designer whohas the courage to start her own business.

Enterprise involves planning, organising,and managing. Enterprise involves bothformal and informal structures. Enterpriseinvolves people doing things, makingthings happen, and providing things.Enterprise involves everything from theactivities undertaken by Australia’s largestcompanies, to the facilities provided tomembers by the local parish. Enterprise,enterprising people, and enterprises deliverthe things that society needs and wants.

In the GST legislation, the term enterpriseis used to describe an activity, or a series ofactivities, undertaken by a person or anorganisation. Enterprise is a veryimportant term in the context of GSTbecause enterprises that meet certaincriteria are required to register for GST.

It is important to realise that enterprisesthat are required to register for GST maynot be ‘businesses’ or ‘organisations’ in theway those terms are normally perceived.

Enterprise includes:▲ A business, trade or profession;▲ A lease, licence or other grant of interest

in property;▲ Activities of charities or gift deductible

entities;▲ Activities of religious organisations; and

▲ Certain activities of government andgovernment corporations.

Some activities are excluded from being anenterprise. These are:

▲ Hobbies or recreational activities;▲ Activities by individuals or partnerships

where there is no reasonable expectationof profit or gain. Input tax credits cannotbe claimed for these activities; and

▲ Employees salaries and wages.

5.2 EntityIn the context of the GST an entity caninclude:

▲ An individual (eg a priest/deacon);▲ A company or Body Corporate (eg a

Religious Order/Congregation);▲ A Corporation Sole;▲ A Partnership;▲ Any other Unincorporated Association

or Body of Persons (e.g. kindergartenrun by a parish); and

▲ A Trust or a Superannuation Fund.

5.3 AcquisitionAcquisitions include everything you buyfor your enterprise including buying goodsor services, getting advice or information,taking out a lease of premises, hiringbusiness equipment, and anything else.

5.4 AdjustmentsAdjustments are changes you may need tomake on your BAS to change your net GSTamount payable or refundable as the resultof an adjustment event.

An adjustment event is any event that hasthe effect of:▲ Cancelling a supply or acquisition;▲ Changing the consideration for a supply

or acquisition, or▲ Causing a supply or acquisition to

become, or stop being a taxable supplyor creditable acquisition.

5 . G S T Te r m s a n d S p e c i f i c M e a n i n g s

12G S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

5This may occur if:▲ All or part of a supply or acquisition is

cancelled;▲ You receive or give a discount on a

supply;▲ You change the purpose of an

acquisition; or▲ One of your debtors fails to pay.

5.5 Attribution RulesWhen, for any tax period, an entitycompletes the GST section of the BAS it isrequired to include:

▲ The total amount of taxable suppliesmade by the entity during the period; and

▲ The total amount of the taxable suppliesit acquired during the period that relatesto its taxable activity.

It follows that the entity must determine inwhich tax period a particular transactionmust be accounted for. This need is coveredby the attribution rules. They determine towhich period a GST supply should beattributed.

The attribution rules differ dependingwhether the enterprise is GST registered ona ‘cash basis’ or an ‘accrual basis’.

5.5.1 Cash Basis Attribution Taxable supplies made by the entityGST is attributed to the GST period inwhich the entity receives a payment inrespect of the taxable supply.

Taxable supplies acquired by the entityGST is attributed to the GST period inwhich the entity makes a payment inrespect of the taxable supply.

5.5.2 Accrual Basis Attribution RulesTaxable supplies made by the entityGST is attributed to the first GST period inwhich the entity either, receives a paymentin respect of the taxable supply, or issuesan invoice in respect to that supply.

Taxable supplies acquired by the entityGST is attributed to the GST period inwhich the entity receives a tax invoice inrespect of the supply.

In effect, the attribution rules are the

equivalent of GST time of supply rules.They determine the period in which thesupply is to be regarded as occurring andin relation to which the applicable GST isto be accounted for.

Example:

A congregation is registered for GST on acash basis. On 24 June it purchased soilfrom Jax Garden Yard Ltd for $3,300(including $300 GST) for landscapingworks at the convent.

Jax Garden Yard Ltd issued thecongregation with a tax invoice for$3,300 on 25 June which it paid on 4July. The congregation’s GST tax periodends on 30 June.

It attributes the supply to the GST periodcommencing on 1 July, as it did notmake the payment in the GST periodended 30 June.

Jax Garden Yard Ltd is registered for GSTon an accrual basis. As it issued aninvoice in the GST period ended 30 June,it must attribute the supply and the GSTpayment to the 30 June GST period.

5.6 Australian BusinessNumber (ABN)

The ABN is critical to the operation of theGST system, as every entity that isregistered for GST will have an ABN andthis is the number that must be quoted onall your tax invoices.

As a general rule entities should registerfor an ABN even if they do not register forGST. If the entity does not have an ABN, ordoes not provide that number to people towhom it supplies goods and services, theirclients ordinarily will be required to deductwithholding tax from payments to thatbusiness. There are very limited exceptionsto the rule. This withholding tax will be atthe rate of 48.5 cents in the dollar.

The ABN registration form includes theoption to register for GST.

The New Tax System will change the waytax is collected in Australia from 1 July. Aspart of the changes The New Tax System

5 . G S T Te r m s a n d S p e c i f i c M e a n i n g s

13G S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

5also puts in place an ABN that will enableentities in Australia to deal with the ATOand a range of government departments oragencies using the one number.

If an entity does not obtain an ABN, anddoes not register for GST, it will be unableto claim back the GST that it pays to itssuppliers.

An entity will also need to show its ABN onthe tax invoices it issues. If it doesn’t, thedocument will not constitute a tax invoice(even if so described) and its clients wouldnot be able to claim input tax credits.

The ABN will not replace a tax file number,so tax file information will still be protectedby the existing privacy guidelines.

When an entity has been allocated an ABNits relevant details will be placed on theAustralian Business Register which theCommissioner of Taxation will administer.

5.7 Business ActivityStatement (BAS)

Every entity that registers for GST will berequired to submit a BAS that will shownot just GST paid or due, but a range ofother taxes as well. The BAS is your GSTreturn - but it includes a lot more than justGST.

With the BAS, most parishes/congregationswill make one payment and one statementto the ATO per quarter. That is, mostentities will only be required to lodge fourreturns and make four payments per year.For parishes and congregations this willinclude:

▲ GST;▲ Income tax withholding (PAYE/PAYG

withholding); and▲ FBT instalments.For each tax period the entity will receivefrom the ATO a single tax form: the BAS.

As from July 1 the BAS will be used toadvise the ATO of the GST liability of theentity as well as being used to advise itsother tax liabilities. For most entities thismeans that there will only be one form tothe ATO and only one payment each quarter.

The exception will be for entities thatchoose to remit GST on a monthly basis.

A BAS will have to be filed when it isdue, even if no tax liability exists forthat tax period.

The BAS can be sent to the entity, by the ATOeither through the mail as a paper form, orover the Internet as an electronic form. Theentity will be required to lodge its BAS withthe ATO twenty-one days after the end of theGST tax period. The GST tax period willeither be one month or three months. (Thiswill be discussed in Chapter 20)

The entity will be required to keepadequate records so it can accuratelycomplete the GST section of the BAS todetermine the amount of GST it will haveto pay to the ATO or the amount that maybe refunded, depending on itscircumstances.

Any refunds of GST may be used to reduceother amounts of tax that may need to bepaid (such as group tax) on the BAS forthat period. The ATO will pay interest onall refunds not remitted by them within 14days.

5.8 ConsiderationFor most entities, the consideration thatthey receive for their goods and serviceswill be the money paid. However, the GSTis intended to be very broad in its coverage,so consideration extends well beyondmoney to include non-cash transactions,such as barter transactions.

5.9 Creditable AcquisitionsCreditable acquisitions are acquisitionsacquired for a creditable purpose. Youacquire a thing for a creditable purpose ifyou acquire it for use in your business,unless it is for use in making input taxedsupplies. Things acquired for private useare not creditable acquisitions.

5.10 Goods and ServicesThe GST is intentionally very broad in itscoverage. It is intended to capture all

forms of domestic consumption, so mayinclude a range of things that you may nothave thought of. It is important that youcharge GST on all taxable supplies, so youneed to have a good understanding ofwhat we mean by goods and services.

If you don’t charge GST when you shouldhave, you as the supplier will still berequired to pay 1/11th of the price chargedto the ATO - so making a mistake can bevery expensive!

Enterprises produce a huge range of goodsand services that are available toconsumers. Goods can be grown, made, orimported, and can be bought and soldrepeatedly.

Services also come in many differentforms. Services can involve a plumberfixing a blocked drain, or the localswimming club teaching the kids to swim.The local Council, Federal Government,and the local Citizens Advice Bureau allprovide services. Some services we use arecostly, some cost nothing, and someorganisations provide them in return forsubscriptions and members donations.

Some service organisations are huge,highly structured, and are ‘big businesses’to run. Other service organisations are lessformal, less organised, and small. Onething is common to all enterprises thatprovide goods and services, they involvepeople in planning, organising, andmanaging the supply of a huge range ofgoods and services that people consumeevery day.

It is very important to appreciate thatfor GST to be payable, there must be ataxable supply of goods and services.

In some cases the goods or services beingsupplied may be GST-free, or input taxed.These are not taxable supplies of goodsand services and accordingly GST is notincluded in the price paid (we explain theseterms later).

This material also looks at the supplyof goods and services. It considers what isbeing supplied, when is it being supplied,

what is the value of the supply. Thismaterial considers the relationshipsbetween enterprises, their clients, and thegoods and services provided.

5.11 Input Tax CreditRegistered entities can claim back from theATO the GST that is included in the price ofgoods and services they acquire for thepurpose of making taxable supplies andGST-free supplies. These are called inputtax credits.

It is critical that every registered entity isable to keep track of these credits. Anunclaimed input tax credit is a cost to anorganisation.

To be able to claim GST input tax credits,an entity must hold a valid tax invoice atthe time the input tax credits are claimedin the BAS.

5.12 Sub-EntityCharities and gift deductible entities withsmall independent branches (sub-entities)have the option of treating these units as ifthey are separate entities for GST purposes.

A sub-entity is considered to beindependent if it keeps its own accountingrecords and can be separately identified bythe nature of its activities or by itslocation.

Where a sub-entity's turnover is less than$100,000, it can choose whether to registerfor GST. If the sub-entity's turnover is$100,000 or more, it will have to registerseparately for GST.

The election to branch units of anorganisation as sub-entities for GSTpurposes cannot be revoked for 12 months.

5.13 SupplySupply is a broad term and includes sellinggoods and services, providing advice orinformation, and other transactions.

5 . G S T Te r m s a n d S p e c i f i c M e a n i n g s

14G S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

5

5 . G S T Te r m s a n d S p e c i f i c M e a n i n g s

15G S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

55.14 Tax Fraction

Rule of Thumb: The GST is 1/11th ofthe price charged or paid.

The tax fraction can be important:▲ In isolating the GST content of a

transaction; and▲ Identifying the true ‘income’ and

‘expenditure’ of the entity.

Total price includes GSTWhen a parish/congregation enters into atransaction that is taxable, GST must beadded to the value of the transaction.

Example

The parish bookshop is registered forGST and sells 10 statues to the parishschool which is also registered for GST.The value of the supply is $250.00 andthe bookshop adds 10% GST ($25) andcharges the school a price of $275.00.

When the bookshop completes the GSTportion of the BAS it will disclose thetotal of its taxable supplies for the taxperiod. It will calculate 1/11th (the taxfraction) of the total price charged to theschool ($25). This will be included in thetotal GST reported to the ATO.

The remaining 10/11ths of the price($250.00) is the gross income thatbookshop receives from the transaction.

When the school completes the GSTportion of the BAS it will disclose thetotal amount of its acquisitions. It willcalculate 1/11th (the tax fraction) of thetotal price paid ($25). This will beincluded in the total GST claimed backfrom the ATO. The remaining 10/11ths($250.00) is the actual acquisition costof the item to the school.

5.15 Tax InvoiceA tax invoice is a document usually issuedby the supplier. A tax invoice includes theinformation normally shown on an invoiceplus additional information required byGST law, including:

▲ The ABN of the supplier;▲ The value of the supply;▲ The amount of GST; and▲ The total price, including GST.

5.16 Tax PeriodTax periods are the reporting period forGST on your BAS. Tax periods are monthlyor quarterly. A BAS must be lodged foreach tax period.

5.17 ValueIn a GST context, references to the value ofsomething means the price of an itembefore GST is added. Thus, GSTpublications often make reference toadding GST to the value of the item toarrive at the ‘GST inclusive price’. In thecontext of most GST taxable supplies, theuse of the term value, means 10/11ths ofthe price. The final 1/11th is the GSTcomponent of the price.

Example

In the above example, the value of thestatues sold by the parish bookshop tothe school is $250. Likewise the valueof the statues to the school is $250.

N o t e s

Notes

16G S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

Broadly speaking in the case of GSTregistered entities:

▲ GST is a tax of 10% on consumption, i.e.most transactions; and

▲ Most entities will charge and collect theGST.

▲ Entities pay the GST on the acquisitionsto their operations; and

▲ Claim a credit from the ATO for the GSTpaid on the items purchased or acquiredto use in that entity.

▲ GST is levied on each taxable supply byregistered entities; and

▲ The registered entity will report to theATO the GST movements on a BAS.

Unlike sales tax there is no provision forexempt bodies such as Public BenevolentInstitutions to provide exemptioncertificates to the vendor.

There are a number of detailed rules,which modify this basic position.

6 . H o w t h e G S T O p e r a t e s

6. How the GST Operates

G S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

6

17

N o t e s

Notes

18G S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

The key elements of the introduction ofGST, as a component of the New Tax System,for a parish/congregational entity are:

1)GST is a tax on goods and services andnot a tax on income. Therefore, itfollows that parishes/congregations thatare not currently considered to becarrying on a business for income taxpurposes will nevertheless be includedin the GST net.

2)No entity will be exempt from GST.3)A parish/congregation may be required

to register for GST.3)A registered entity must include 10%

GST in the price of ‘taxable supplies’.4)A parish/congregation will find that GST

is included in the prices charged to it byits suppliers for many of the goods andservices it purchases.

5)Parishes/congregations need to startpreparing now to become accustomed tothe system by:

▲ Providing education and trainingfor all personnel involved in theimplementation of GST;

▲ Recognising the importance of systemsand record keeping required to accountfor the GST (addressed in Chapter 21);

▲ Recognising the impact GST will haveon staff, particularly the additionalresponsibilities;

▲ Identifying the GST implications of alltransactions;

▲ Identifying transitional issues;▲ Review all contracts (obtain advice from

the Diocesan or Congregational contact);▲ Identifying risks that may arise as a

consequence of GST;▲ Recognising the importance of an

appropriate Chart of Account; and▲ Ensuring that the appropriate

documentation is printed and availablefor use by staff from 1 July 2000.

7.1 Diocesan Parish PriestsGST does not apply to:▲ First (or Second) Collection at Masses –

as these are donations. Further, thesupply of religious services are GST-freeprovided they are considered essential tothe practice of the religion;

▲ Christmas & Easter dues; and▲ Stole fees or stipends for masses,

weddings, baptisms, funerals.Diocesan Priests are able to and may haveto register for an ABN because theyconduct an enterprise:

▲ Being their vocation;▲ Having an expectation of profit or gain;

and▲ Are not employees for PAYE (PAYG).If registered for an ABN, diocesan priestsmay in some cases subsequently register forGST. This would allow them to claim inputcredits on creditable acquisitions such as:

▲ Theological library books;▲ Clerical robes; and▲ Car expenses (excluding private running).It will be important for priests to maintainrecords and lodge BAS returns with the ATO.

However, diocesan priests cannot claiminput credits on such things as:

▲ Holidays;▲ Private car expenses;▲ Newspapers and subscriptions for

periodicals that are “non-theological”;and

▲ Personal clothing.Subsequent registration for GST involvesmeeting all the legislative requirements eg.income level thresholds, etc. If, under thelegislation, there is no requirement toregister for GST, and if the claim on inputcredits are only minimal, it may be morebeneficial not to register for GST.

It is important that diocesan priests consultthe Diocesan Business Manager for adviceand information on clergy registration issues.

7 . I m p a c t o n t h e C h u r c h

7. Impact on the Church

19G S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

7

7.2 Diocesan Assistant Priests,Specialist Priests, Deacons

May have to register for an ABN.Subsequently may register for GST to claiminput credits but it may not be worthwhileto register for GST – see implications forParish Priests.

▲ Stipend is not subject to GST; and▲ GST free income – weddings, baptisms

and funerals.

7.3 Diocesan Priest-ChaplainsSame as for specialist priests but ifregistered for GST:

▲ Grants received from governments aretaxable for GST; and

▲ Can claim input credits for creditableacquisitions.

7.4 Religious Orders ▲ Offerings for religious services &

donations are GST-free to the Order.This does not include stipends, whichare payments made to the ReligiousOrder/Congregation for a service;

▲ The Religious Order may claim inputcredits except for entertainment andpurchases made from the personalallowance provided by the Order.

7.5 Parishes/Religious OrderEnterprises – Income

GST applies to:▲ Piety stall sales (refer to Chapter 15.4

Non-Profit Sub-Entities);▲ Cake stalls (refer to Chapter 15.4 Non-

Profit Sub-Entities);▲ Sponsorships where a local entity makes

a donation to the parish/congregation inreturn for a service such as advertising;and

▲ Rental of parish/congregationalpremises (eg parish hall, parish tenniscourts, etc).

7 . I m p a c t o n t h e C h u r c h

20G S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

7

7 . I m p a c t o n t h e C h u r c h

21G S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

7

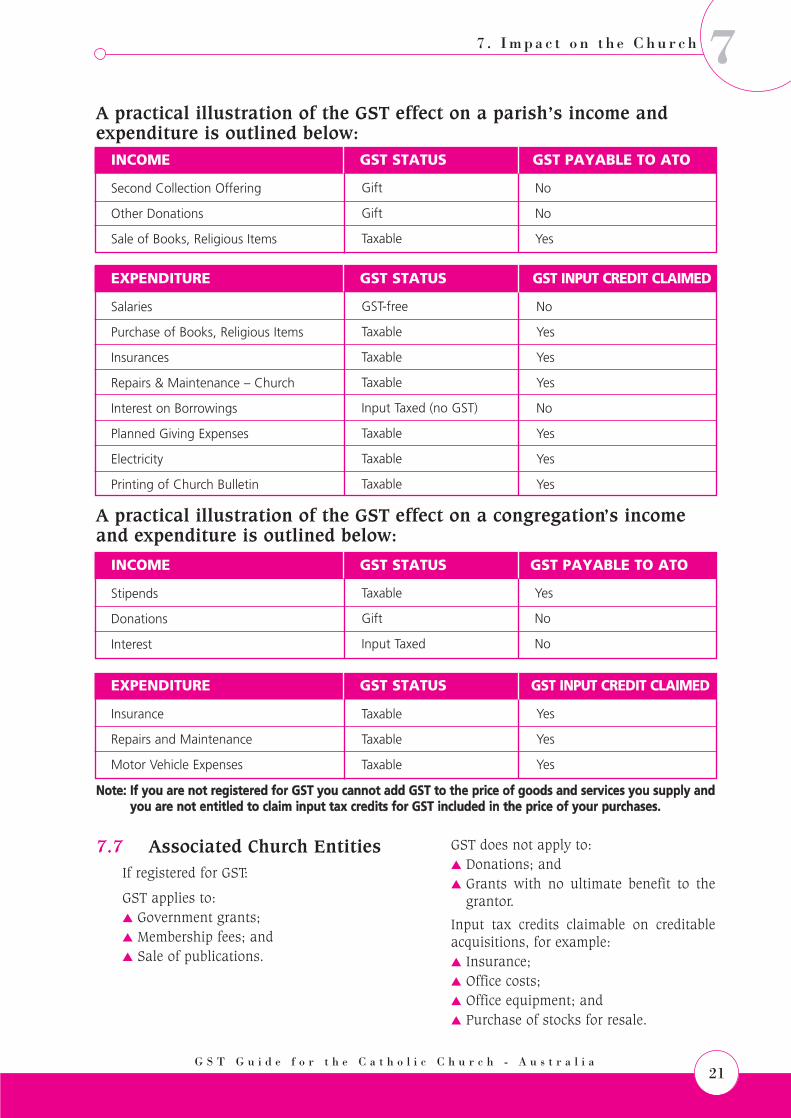

7.7 Associated Church EntitiesIf registered for GST:

GST applies to:▲ Government grants;▲ Membership fees; and▲ Sale of publications.

GST does not apply to:▲ Donations; and▲ Grants with no ultimate benefit to the

grantor.

Input tax credits claimable on creditableacquisitions, for example:▲ Insurance;▲ Office costs;▲ Office equipment; and▲ Purchase of stocks for resale.

A practical illustration of the GST effect on a congregation’s incomeand expenditure is outlined below:

A practical illustration of the GST effect on a parish’s income andexpenditure is outlined below:

NNoottee:: IIff yyoouu aarree nnoott rreeggiisstteerreedd ffoorr GGSSTT yyoouu ccaannnnoott aadddd GGSSTT ttoo tthhee pprriiccee ooff ggooooddss aanndd sseerrvviicceess yyoouu ssuuppppllyy aannddyyoouu aarree nnoott eennttiittlleedd ttoo ccllaaiimm iinnppuutt ttaaxx ccrreeddiittss ffoorr GGSSTT iinncclluuddeedd iinn tthhee pprriiccee ooff yyoouurr ppuurrcchhaasseess..

INCOME GST STATUS GST PAYABLE TO ATO

Second Collection Offering

Other Donations

Sale of Books, Religious Items

No

No

Yes

Gift

Gift

Taxable

INCOME GST STATUS GST PAYABLE TO ATO

Stipends

Donations

Interest

Yes

No

No

Taxable

Gift

Input Taxed

EXPENDITURE GST STATUS GST INPUT CREDIT CLAIMED

Insurance

Repairs and Maintenance

Motor Vehicle Expenses

Yes

Yes

Yes

Taxable

Taxable

Taxable

EXPENDITURE GST STATUS GST INPUT CREDIT CLAIMED

Salaries

Purchase of Books, Religious Items

Insurances

Repairs & Maintenance – Church

Interest on Borrowings

Planned Giving Expenses

Electricity

Printing of Church Bulletin

No

Yes

Yes

Yes

No

Yes

Yes

Yes

GST-free

Taxable

Taxable

Taxable

Input Taxed (no GST)

Taxable

Taxable

Taxable

N o t e s

Notes

22G S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

GST is a tax on transactions. For GSTpurposes sales transactions are calledsupplies.

As part of preparations for dealing with theGST a parish/congregation should identifythe supplies it makes and the GST status ofthose supplies.

There are four kinds of supply which aredescribed in the following pages. Insummary they are:

Taxable SuppliesThe supplier charges GST on sales theymake and can claim full input tax creditsfor GST paid on purchases.

Taxable supplies made by an entitycould include:▲ Resale of purchased furniture, clothes etc▲ Sale of a commercial building; and▲ Ministry of an individual religious for

which a stipend is paid.

Taxable supplies acquired by an entitycould include:▲ Purchase of computer equipment;▲ Repairs to a motor vehicle used in

ministry; and▲ Services such as telephones, electricity

and gas.

GST-free SuppliesThe supplier does not charge GST on salesthey make and can claim full input taxcredits for GST paid on purchases.

GST-free supplies made by an entity couldinclude:

▲ Sale of donated goods that retain theiroriginal character; and

▲ Providing a religious ceremony.

Input Taxed SuppliesThe supplier does not charge GST on salesthey make and cannot claim input taxcredits for GST paid on purchases made tomake those sales.

Input taxed supplies made by abusiness could include:▲ Renting a house as a residence at full

market rate.

To avoid any confusion later on, makea mental note now that input taxedsupplies are not the same as input taxcredits. Input taxed supplies have justbeen described. Input tax credits arethe credits allowed for GST paid onexpenses incurred to make taxable orGST-free supplies.

Other Supplies(Supplies by Non-Registered Persons)The supplier does not charge GST on salesthey make and cannot claim input taxcredits for GST paid on purchases.

8.1 Taxable SuppliesEntities that are registered for GST mustcharge GST on their taxable supplies, andwill be entitled to input tax credits on theGST they have paid on purchases to makethose supplies.

It is critical that every registered entityunderstands this. Failure to charge GSTwhen it should have will result in aliability for GST of 1/11th of the pricecharged. Failure to track creditableacquisitions will result in an underclaiming of input tax credits. That is realmoney down the drain!

Supplies of goods and services are made byentities to their clients. In broad termssupplies include all forms of supply ofgoods and services.

A taxable supply specifically excludessupplies that are GST-free, and suppliesthat are input taxed. Consequently GST isnot charged on either GST-free supplies orinput taxed supplies. (These terms will beconsidered shortly).

For the supply of goods or services to be ataxable supply, it must be connected withAustralia. This means that, generally,anything done or made in Australia will besubject to GST. If you have transactionsthat relate to exports then the rules aremore complex. You may need to seek advicefrom the ATO or a professional adviser.

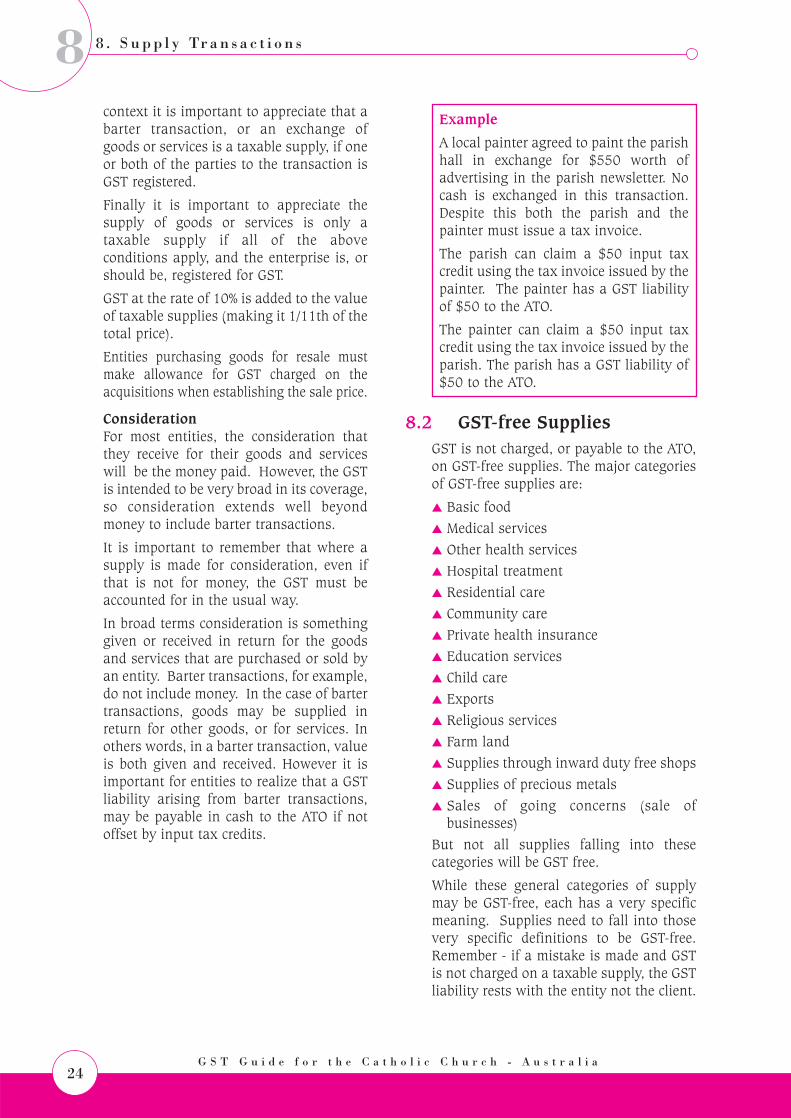

To be a taxable supply the supply must involve consideration. In this

8 . S u p p l y Tr a n s a c t i o n s

8. Supply Transactions

23G S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

8

context it is important to appreciate that abarter transaction, or an exchange ofgoods or services is a taxable supply, if oneor both of the parties to the transaction isGST registered.

Finally it is important to appreciate thesupply of goods or services is only ataxable supply if all of the aboveconditions apply, and the enterprise is, orshould be, registered for GST.

GST at the rate of 10% is added to the valueof taxable supplies (making it 1/11th of thetotal price).

Entities purchasing goods for resale mustmake allowance for GST charged on theacquisitions when establishing the sale price.

ConsiderationFor most entities, the consideration thatthey receive for their goods and serviceswill be the money paid. However, the GSTis intended to be very broad in its coverage,so consideration extends well beyondmoney to include barter transactions.

It is important to remember that where asupply is made for consideration, even ifthat is not for money, the GST must beaccounted for in the usual way.

In broad terms consideration is somethinggiven or received in return for the goodsand services that are purchased or sold byan entity. Barter transactions, for example,do not include money. In the case of bartertransactions, goods may be supplied inreturn for other goods, or for services. Inothers words, in a barter transaction, valueis both given and received. However it isimportant for entities to realize that a GSTliability arising from barter transactions,may be payable in cash to the ATO if notoffset by input tax credits.

Example

A local painter agreed to paint the parishhall in exchange for $550 worth ofadvertising in the parish newsletter. Nocash is exchanged in this transaction.Despite this both the parish and thepainter must issue a tax invoice.

The parish can claim a $50 input taxcredit using the tax invoice issued by thepainter. The painter has a GST liabilityof $50 to the ATO.

The painter can claim a $50 input taxcredit using the tax invoice issued by theparish. The parish has a GST liability of$50 to the ATO.

8.2 GST-free SuppliesGST is not charged, or payable to the ATO,on GST-free supplies. The major categoriesof GST-free supplies are:

▲ Basic food▲ Medical services▲ Other health services▲ Hospital treatment▲ Residential care▲ Community care▲ Private health insurance▲ Education services▲ Child care ▲ Exports▲ Religious services▲ Farm land▲ Supplies through inward duty free shops▲ Supplies of precious metals▲ Sales of going concerns (sale of

businesses)But not all supplies falling into thesecategories will be GST free.

While these general categories of supplymay be GST-free, each has a very specificmeaning. Supplies need to fall into thosevery specific definitions to be GST-free.Remember - if a mistake is made and GSTis not charged on a taxable supply, the GSTliability rests with the entity not the client.

8 . S u p p l y Tr a n s a c t i o n s

24G S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

8

8 . S u p p l y Tr a n s a c t i o n s

25G S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

8Be sure you carefully check if you makesupplies that fall into these categories. Youmay want to seek advice on the impact ofthe GST-free rules for your particular entityfrom your Diocesan or Congregationalcontact, professional adviser or the ATO.

If an entity makes GST-free supplieshowever, it is still able to claim back GSTinput tax credits on the purchase of anygoods and services acquired to allow it tomake those GST-free supplies.

8.3 Input Taxed SuppliesThe major categories of input taxedsupplies are:

▲ Residential rents where the rent chargedis at market rates. Where the rentcharged is less than the threshold (at thetime of printing, the threshold is 75% ofthe market rent or the cost of theaccommodation), the supply will be aGST-free supply.NOTE that if a supply is GST-free,this overrides the fact that it wouldhave been an input taxed supply;and

▲ Financial services.Most organizations won't make inputtaxed supplies, although some will beproviding residential accommodation.

An entity cannot charge GST on any inputtaxed supplies it makes, and cannot claimback any GST on acquisitions made inrelation to those supplies.

If an entity supplies input taxed supplies inaddition to taxable supplies and/or GST-free supplies, input tax credits must beapportioned. This apportionment isrequired as no input tax credit is availablefor the GST paid on acquisitions used inmaking input taxed supplies. If your entitymakes input taxed supplies and input taxcredits need to be apportioned, seek advisefrom your Diocesan or Congregationalcontact, a professional advisor or the ATO.

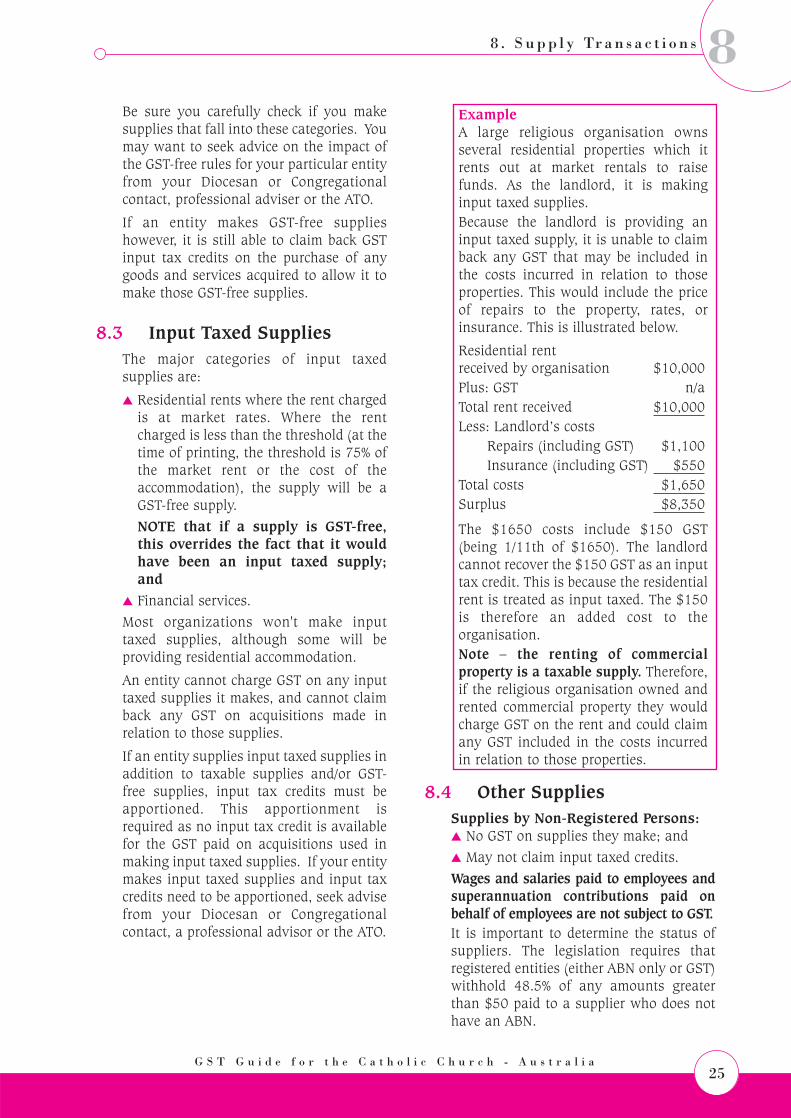

ExampleA large religious organisation ownsseveral residential properties which itrents out at market rentals to raisefunds. As the landlord, it is makinginput taxed supplies. Because the landlord is providing aninput taxed supply, it is unable to claimback any GST that may be included inthe costs incurred in relation to thoseproperties. This would include the priceof repairs to the property, rates, orinsurance. This is illustrated below.

Residential rentreceived by organisation $10,000Plus: GST n/aTotal rent received $10,000Less: Landlord’s costs

Repairs (including GST) $1,100Insurance (including GST) $550

Total costs $1,650Surplus $8,350

The $1650 costs include $150 GST(being 1/11th of $1650). The landlordcannot recover the $150 GST as an inputtax credit. This is because the residentialrent is treated as input taxed. The $150is therefore an added cost to theorganisation.Note – the renting of commercialproperty is a taxable supply. Therefore,if the religious organisation owned andrented commercial property they wouldcharge GST on the rent and could claimany GST included in the costs incurredin relation to those properties.

8.4 Other SuppliesSupplies by Non-Registered Persons:▲ No GST on supplies they make; and▲ May not claim input taxed credits.Wages and salaries paid to employees andsuperannuation contributions paid onbehalf of employees are not subject to GST.It is important to determine the status ofsuppliers. The legislation requires thatregistered entities (either ABN only or GST)withhold 48.5% of any amounts greaterthan $50 paid to a supplier who does nothave an ABN.

N o t e s

Notes

26G S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

9.1 Religious ServicesThe supply of religious services by areligious institution or entity will be GST-free if the services are:Integral to the Practice of the ReligionThis includes:▲ Religious celebrations such as mass,

funerals, marriages and baptisms;▲ Chaplaincy services, religious

conferences and seminars; and▲ Theological training, adult faith

education, after school catechism.

"Religious Service" is not confined to aservice inside a church.

The ATO has also ruled that the followingservices would, generally, be religiousservices and thus GST-free:▲ Home church group activities;▲ Bible study groups;▲ Sunday school;▲ Chaplaincy services;▲ Religious conferences & seminars;▲ Theological training; and▲ Leadership training activities (subject to

them being considered essential to thepractice of the Catholic religion).

Not Considered to be Integral to thePractice of Religion:▲ Car hire and purchase of flowers for a

church wedding;▲ Religious items

– a bible for private devotion;▲ Youth camp

– if mainly social/ recreational; and▲ Friendship clubs.

9.2 CharitiesA charity is an organisation thatundertakes charitable activities. Activitiesare charitable if they benefit the communityor section of the community through:▲ The relief of poverty or sickness or the

needs of the aged;▲ The advancement of education;▲ The advancement of religion; or▲ Other purposes beneficial to the

community.

Religious charities include:▲ Churches;▲ Seminaries;▲ Religious orders;▲ Organisations for maintaining clergy/

religious; and▲ Organisations for spreading religious

doctrine and practice.While most supplies made by charities willbe taxable, certain non-commercialsupplies will be GST-free.

9.2.1 Non-Commercial ActivitiesNon Commercial Activities are GST-free ifthe following conditions are met:▲ All activities provided at no cost;▲ Supplies sold for less than 50% of the

GST inclusive market value of the item orless than 75% of the cost of the supply;

▲ Supplies of accommodation provided forless than 75% of the GST inclusivemarket value of the supply or less than75% of the cost of providing theaccommodation; and

▲ Sales of donated second hand goodsthat retain their original character.

The Treasurer has recently requested the ATOissue a ruling to clarify that newsletters,magazines and journals sold by charities,which are not commercial sales are GST-free.Supplies that do not meet the aboveconditions are generally taxable supplies.

9.2.2 FundraisingGST is generally payable on fundraisingactivities. The GST treatment variesdepending on the nature of the activity andthe registration option chosen by yourorganisation. Registration options, includingsub-entities, will be discussed in Chapter 15.If fundraising activities are undertaken bya sub-entity that is not registered for GSTno GST will be accounted for on sales.However, GST paid on acquisitions willbecome an expense.If the fundraising activities are undertaken by aGST registered entity the general rules willapply. Activities such as fetes, cake stalls andfundraising dinners will entail taxable supplies.If an entity is registered any purchase, suchas items for a raffle, or chocolate for a

9 . C h u r c h Tr a n s a c t i o n s

9. Church Transactions

27G S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

9

chocolate drive, are creditable acquisitions.Raffles, bingo and other games of chanceconducted by Church entities will be GST-free.

9.2.3 Donations and GiftsGST will not be payable provided that the donation is both voluntary andunconditional. There must be no services,benefits or rights afforded to the donor asany of these might be construed as a‘consideration’ (see Chapter 8.2) and turnthe transaction into a taxable supply.A gift must be given by a donor out ofgenerosity or benefaction. A gift is madevoluntarily with no material benefitprovided to the donor as a result of the gift.Donations given for a specific purpose willnot give rise to a GST liability providedthey are in the nature of a gift.

9.2.4 GrantsIs GST payable on a grant?The answer to this question depends on thenature of the grant. If it is for a specificpurpose then it will be subject to GST. TheATO has issued a specific ruling on this area.The Commonwealth Government hasindicated that it may “gross up” the grants sothat organisations should receive the sameamount after GST effects are eliminated.The grants received from the governmentare treated as being a payment for servicesprovided by your organisation. You are, ineffect, invoicing the government for theseservices and the service is subject to GST.This is so even though you then supply theservices as GST-free supplies to your clients.Conditional grants made to a registeredgrantee will usually be subject to GST. Agrant will be subject to GST if the followingfour tests are satisfied:1) Is the grant consideration for a supply

by the recipient to the grantor?2) Is the supply to which the grant relates

made as part of the recipient’s enterprise?3) Is the supply for which the grant is paid

connected with Australia? and4) Is the recipient of the grant registered, or

required to be registered, for GST?1. Grant as consideration for supply?

The first test can be answered byconsidering whether the grant is

conditional or unconditional. If therecipient undertakes or is required to dosomething in exchange for the funds thegrant is a taxable supply.While a gift to a non-profit body is notconsideration and so not subject to GST,most grants are not gifts. However, insome instances grants can be non-conditional and will be GST-free.

2. EnterpriseThe second test asks whether the supplyby the recipient is made in the course ofthe recipient’s enterprise. All activities ofa religious institution or a charitableinstitution or fund, fall within this test.

3. Connected with AustraliaThe third test requires that the supply isconnected with Australia. Most suppliesfor which grants are consideration aresupplies other than of goods or realproperty, that is, services. The supply ofservices is connected with Australia ifthe service is done in Australia or ismade through an enterprise carried onin Australia. The ATO will issue a rulingon the meaning of “connected withAustralia” in the near future.

4. Is the grantee registered?The last test requires the supplier to beregistered, or required to be registered,for GST.

9.2.5 SponsorshipAmounts paid as sponsorship fees are usuallypayment for services (such as advertising)and will be subject to GST if the sponsoredentity is registered for GST. If the organisationsupplying the service (such as advertising) isregistered or required to be registered for GST,the organisation paying the sponsorship feewill be entitled to an input tax credit of 1/11thof the payment if it is registered. If the entitysupplying the services is registered it will beliable to pay GST on the supply.

Non-monetary SponsorshipIf a sponsor provides goods and services inreturn for other goods and services, suchas advertising or promotion, there is asupply by both parties to each other. This iscalled 'contra sponsorship'. If both partiesare registered for GST, each will be liable topay GST on the supply to each other.

9 . C h u r c h Tr a n s a c t i o n s

28G S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

9

29G S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

Parishes/congregations can claim backfrom the ATO the GST that is included inthe price of goods and services they acquirefor the purpose of making taxable suppliesand GST-free supplies. To be able to claimGST input tax credits the organisationmust hold a valid tax invoice in respect ofthe goods or services at the time the inputtax credits are claimed in the BAS.

An organisation, however, cannot claimback GST that is included in the price ofsupplies that it acquires for private ordomestic use.

Purchases Of Goods and ServicesInput Tax Credits claimedInput tax credits are available to entitiesregistered for GST purposes.

The input tax credit is the GST paid on thepurchases of goods and services used bythe entity. For example, a parish wouldclaim input tax credits for the following‘purchases’ it may have made:

▲▲ Parish and Presbytery Outgoings– Cleaning, Repairs and Maintenance,Electricity, Insurance, Gas and rentpaid for premises.

▲▲ Stipend Payments – Stipends paidto Religious Congregations andOrders.

▲▲ Operating Expenses – Telephone,Printing and Stationary, Parishgoods and supplies, Book purchases,Motor Vehicle Expenses, Subscriptionsand Accounting Fees.

▲▲ Capital Expenditure – Equipmentand furniture, Building renovations.

Input Tax credits are available whereGST is charged and a tax invoice issupplied.In order for an entity to claim back theinput tax credit it must ensure that thesupplier (who is registered for GSTpurposes) of the goods or services providesa Tax Invoice.

▲▲ The Tax Invoice must be in the form that complies with the GSTLegislation;

▲▲ The Tax Invoice is the proof as to the GST paid on the goods andservices supplied;

▲▲ The Tax Invoice must be supplied tothe entity within 28 days;

▲▲ The Tax Invoice is used to makepayment to the supplier for thegoods and services provided.

Tax Credits not claimedAn entity cannot claim input tax credits forgoods and services where:

▲▲ No tax invoice is provided.▲▲ Supplies are from a non-registered

GST organisation.▲▲ Goods are consumed for private or

domestic purposes.▲▲ Goods are used in making input

taxed supplies.▲▲ The input tax credits are precluded

by legislation.

1 0 . A c q u i s i t i o n s ( P u r c h a s e s )

10. Acquisitions (Purchases)10

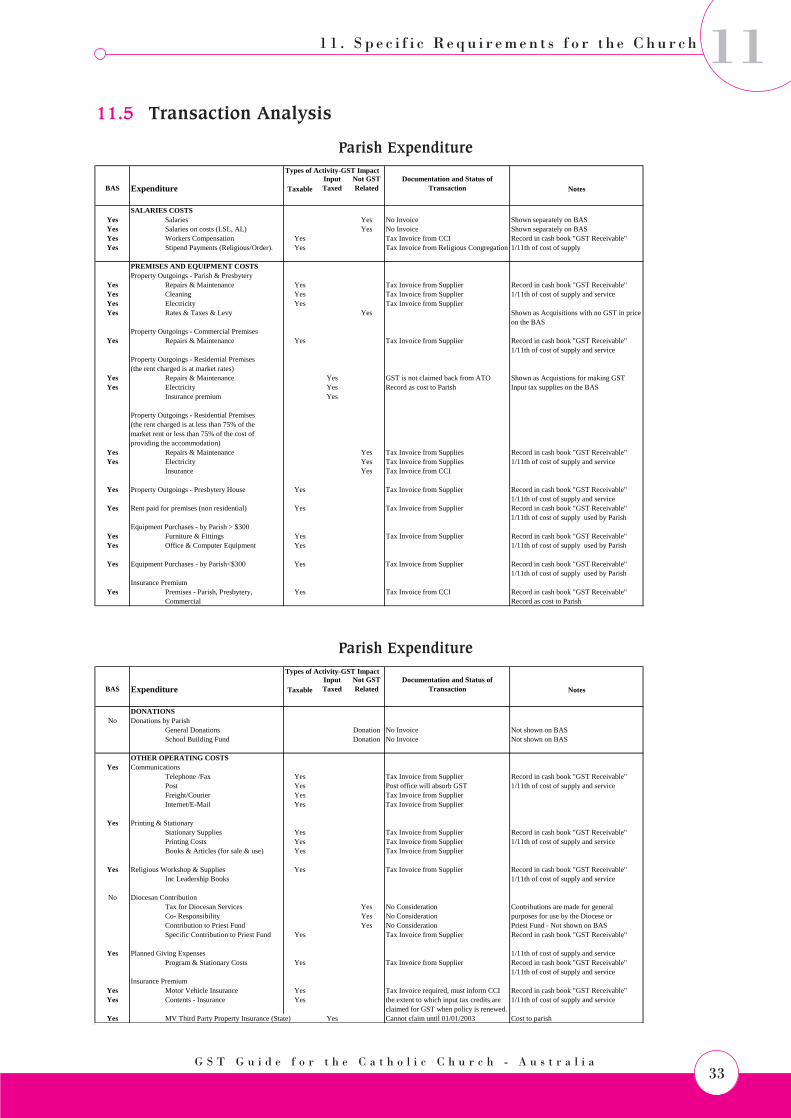

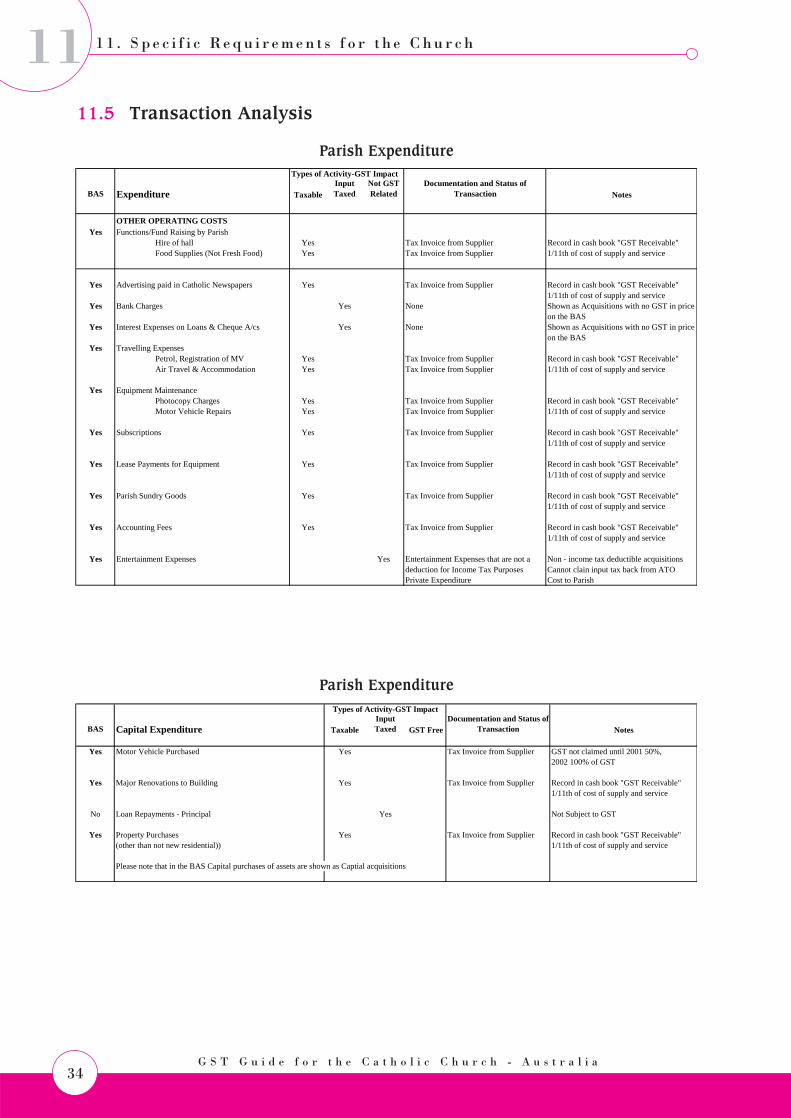

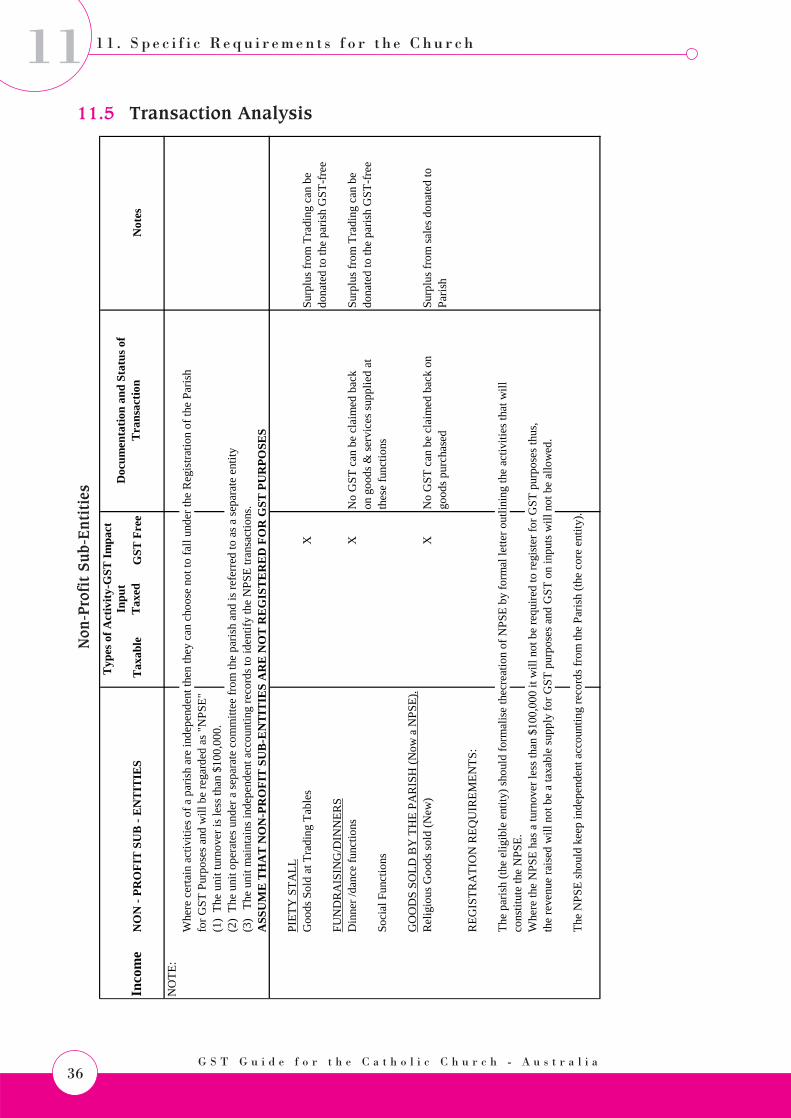

1 1 . S p e c i f i c R e q u i r e m e n t s f o r t h e C h u r c h

11. Specific Requirements for the Church

30G S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

11

The following example has been tailoredspecifically for a parish. However, theprinciples demonstrated in the examplecan be applied in an analysis for any typeof activity within the Catholic Church.

11.1 Working out the GSTParishes will be required to allocate extrastaff to properly account for the GST andmaintain proper accounting records.

In order to work out the GST the parishmust identify all transactions and howGST is applied.

IncomeParish income must be classified into fourtypes of supplies, namely:

▲ Income that is a taxable supply where1/11th of receipts is paid to the ATO.

▲ Income that is GST-free that relate to thesupply of religious services.

▲ Income that is an input tax supplywhere no GST is charged.

▲ Income that is not a supply forconsideration which is mainlydonations.

ExpenditureParish expenditure must be classified intothe following categories to complete theinformation required in the BAS.

▲ Capital expenditure needs to be recordedseparately in the parish accountingrecords (cash book or computeraccounting system) to be reported on theBAS;

▲ The purchase of goods and services whereGST is included in the purchase price;

▲ Expenditure (acquisitions) with no GSTin the purchase price paid;

▲ Expenditure relating to input taxsupplies;

▲ Expenditure that relates to salary &wages is shown separately;

▲ Expenditure that is used for private useor is a not allowable as a tax deduction.

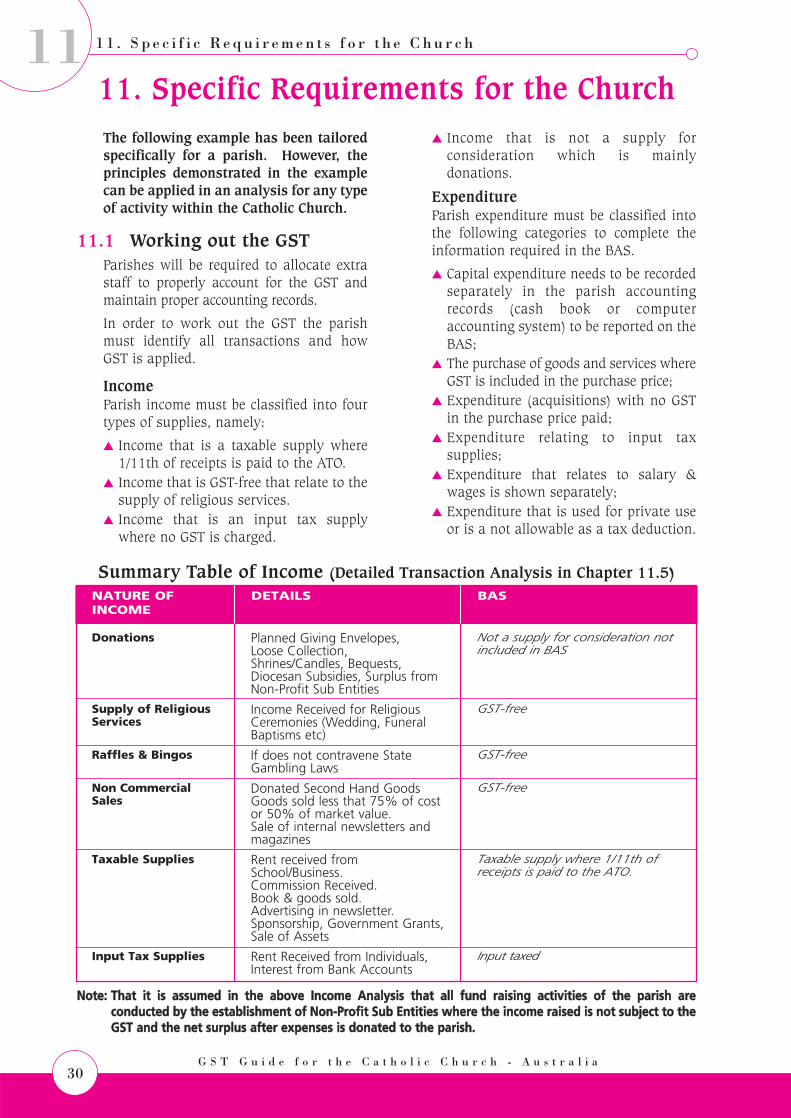

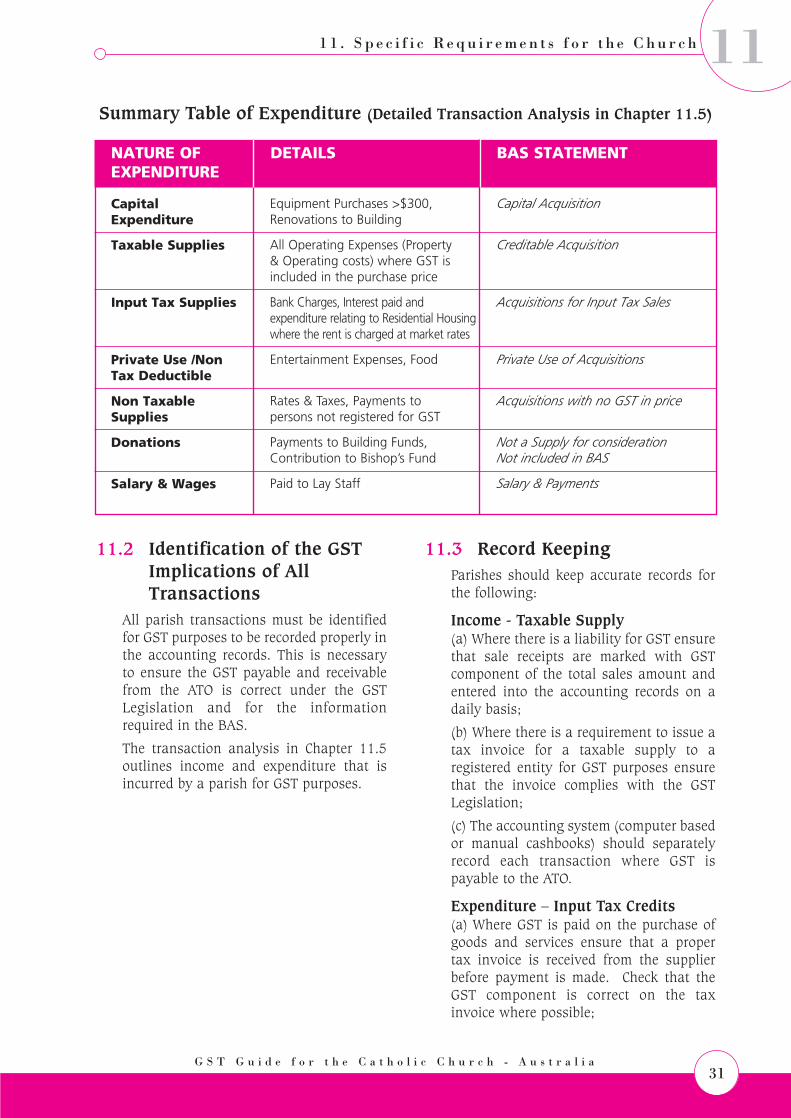

Summary Table of Income (Detailed Transaction Analysis in Chapter 11.5)NATURE OF DETAILS BASINCOME

Donations

Supply of ReligiousServices

Raffles & Bingos

Non CommercialSales

Taxable Supplies

Input Tax Supplies

Planned Giving Envelopes,Loose Collection,Shrines/Candles, Bequests,Diocesan Subsidies, Surplus fromNon-Profit Sub Entities

Income Received for ReligiousCeremonies (Wedding, FuneralBaptisms etc)

If does not contravene StateGambling Laws

Donated Second Hand GoodsGoods sold less that 75% of costor 50% of market value.Sale of internal newsletters andmagazines

Rent received fromSchool/Business.Commission Received.Book & goods sold.Advertising in newsletter.Sponsorship, Government Grants,Sale of Assets

Rent Received from Individuals,Interest from Bank Accounts

Not a supply for consideration notincluded in BAS

GST-free

GST-free

GST-free

Taxable supply where 1/11th ofreceipts is paid to the ATO.

Input taxed

NNoottee:: TThhaatt iitt iiss aassssuummeedd iinn tthhee aabboovvee IInnccoommee AAnnaallyyssiiss tthhaatt aallll ffuunndd rraaiissiinngg aaccttiivviittiieess ooff tthhee ppaarriisshh aarreeccoonndduucctteedd bbyy tthhee eessttaabblliisshhmmeenntt ooff NNoonn--PPrrooffiitt SSuubb EEnnttiittiieess wwhheerree tthhee iinnccoommee rraaiisseedd iiss nnoott ssuubbjjeecctt ttoo tthheeGGSSTT aanndd tthhee nneett ssuurrpplluuss aafftteerr eexxppeennsseess iiss ddoonnaatteedd ttoo tthhee ppaarriisshh..

1 1 . S p e c i f i c R e q u i r e m e n t s f o r t h e C h u r c h

31G S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

11

11.2 Identification of the GSTImplications of AllTransactions

All parish transactions must be identifiedfor GST purposes to be recorded properly inthe accounting records. This is necessaryto ensure the GST payable and receivablefrom the ATO is correct under the GSTLegislation and for the informationrequired in the BAS.

The transaction analysis in Chapter 11.5outlines income and expenditure that isincurred by a parish for GST purposes.

11.3 Record KeepingParishes should keep accurate records forthe following:

Income - Taxable Supply (a) Where there is a liability for GST ensurethat sale receipts are marked with GSTcomponent of the total sales amount andentered into the accounting records on adaily basis;

(b) Where there is a requirement to issue atax invoice for a taxable supply to aregistered entity for GST purposes ensurethat the invoice complies with the GSTLegislation;

(c) The accounting system (computer basedor manual cashbooks) should separatelyrecord each transaction where GST ispayable to the ATO.

Expenditure – Input Tax Credits(a) Where GST is paid on the purchase ofgoods and services ensure that a propertax invoice is received from the supplierbefore payment is made. Check that theGST component is correct on the taxinvoice where possible;

NATURE OF DETAILS BAS STATEMENTEXPENDITURE

CapitalExpenditure

Taxable Supplies

Input Tax Supplies

Private Use /NonTax Deductible

Non TaxableSupplies

Donations

Salary & Wages

Equipment Purchases >$300,Renovations to Building

All Operating Expenses (Property& Operating costs) where GST isincluded in the purchase price

Bank Charges, Interest paid andexpenditure relating to Residential Housingwhere the rent is charged at market rates

Entertainment Expenses, Food

Rates & Taxes, Payments topersons not registered for GST

Payments to Building Funds,Contribution to Bishop’s Fund

Paid to Lay Staff

Capital Acquisition

Creditable Acquisition

Acquisitions for Input Tax Sales

Private Use of Acquisitions

Acquisitions with no GST in price

Not a Supply for considerationNot included in BAS

Salary & Payments

Summary Table of Expenditure (Detailed Transaction Analysis in Chapter 11.5)

1 1 . S p e c i f i c R e q u i r e m e n t s f o r t h e C h u r c h

32G S T G u i d e f o r t h e C a t h o l i c C h u r c h - A u s t r a l i a

11(b) Before an order is made for goods andservices check with the supplier on hisstatus for GST purposes;

(c) The accounting system (computer basedor manual cashbooks) should separatelyrecord each transaction where GST isrefundable from the ATO.

Record all InflowsAs parishes operate on a cash basis for therecording of all receipts ensure thatbankings are made promptly andreconciled to the bank statement andsupporting records, (eg sale receipts).

File Tax Invoices receivedParishes should be aware that theiraccounting records and supportingdocumentation will be subject to ATOaudits for compliance with GSTLegislation. Tax invoices in particularrequire proper filing for inspection as theyare the proof for the GST paid andsubsequently claimed as input tax creditsin the BAS. Filing is normally done in acash payments system in cheque numberorder.

Keep all Bank StatementsParishes should keep all bank statementsand agree banking details (receipts andcheques presented) to supporting records.

Record Debtors and Creditors.Where parishes use an accrual basis ofaccounting, tax invoices for debtors shouldbe issued in the correct accounting taxperiod.

Similarly for creditors, the recording ofliability for payment should occur when atax invoice is received from the supplier.This is the tax period when the GST can beclaimed.

Keep Records Up-to DateIt is important that the accounting systemfor parishes is kept up-to date on a regularbasis:

(a) For receipts, the money is banked dailyand recorded in the accounting system ona daily basis;