Tax Deducted at Source ax Deducted at Source (TDS) (TDS) Rates & Provisions Name:- Vinod Vyas Batch No.:- 126 Reg. No.:- CRO0239893

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/6/2019 59_project Tds Rate & Provision

http://slidepdf.com/reader/full/59project-tds-rate-provision 1/15

TTax Deducted at Sourceax Deducted at Source

(TDS)(TDS)

Rates & Provisions

Name:- Vinod Vyas

Batch No.:- 126

Reg. No.:- CRO0239893

8/6/2019 59_project Tds Rate & Provision

http://slidepdf.com/reader/full/59project-tds-rate-provision 2/15

What is TDS?What is TDS?

TDS means Tax Deducted at Source. As per provisions of

Income Tax Act, 1961 some part of a specified income is

deducted from the person who earn that income before

making payment of such income. In other words, tax on

income deducted where the income is earned.

8/6/2019 59_project Tds Rate & Provision

http://slidepdf.com/reader/full/59project-tds-rate-provision 3/15

Rules & Provisions Related to

TDS

Rules & Provisions Related to

TDS� The person who deduct TDS is called Deducter and the person from whom

TDS is deducted is called deductee.

� Deducting TDS from deductee and than deposit the same in Central Govt.

account is responsibility of deducter.

� TDS deducted is required to be deposited within one week from the last

day of the month of deduction. If TDS amount is not deposited by the due

date , then for each month a penalty of interest equal to 1% of the TDS

amount to be paid.

� Return of TDS filed quarterly. If the quarterly TDS return is not filed within15 days from the last day of the quarter, then a penalty of Rs. 100 per day

subject to maximum limit equal to theTDS amount is chargeable.

8/6/2019 59_project Tds Rate & Provision

http://slidepdf.com/reader/full/59project-tds-rate-provision 4/15

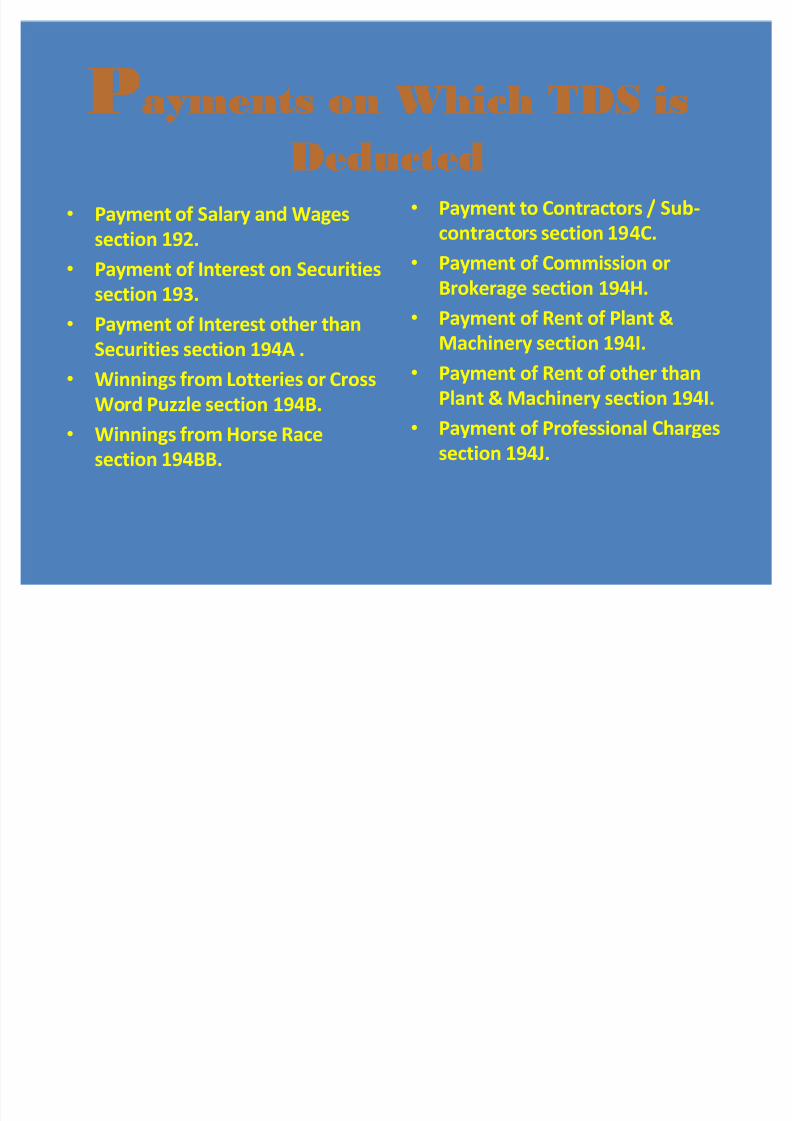

Payments on Which TDS is

Deducted

Payments on Which TDS is

Deducted

� Payment of Salary and Wages

section 192.

�

Payment of Interest onS

ecuritiessection 193.

� Payment of Interest other than

Securities section 194A .

� Winnings from Lotteries or Cross

Word Puzzle section 194B.� Winnings from Horse Race

section 194BB.

� Payment to Contractors / Sub-

contractors section 194C.

� Payment of Commission or

Brokerage section 194H.

� Payment of Rent of Plant &

Machinery section 194I.

� Payment of Rent of other than

Plant & Machinery section 194I.

� Payment of Professional Charges

section 194J.

8/6/2019 59_project Tds Rate & Provision

http://slidepdf.com/reader/full/59project-tds-rate-provision 5/15

Payment of Salary and Wages

Section 192

Payment of Salary and Wages

Section 192Criteria of Deduction TDS is deductible if the estimated

total income of the employee is

taxable.

TDS Rate Normal rate of income tax including

surcharge (if applicable) and

education cess.

8/6/2019 59_project Tds Rate & Provision

http://slidepdf.com/reader/full/59project-tds-rate-provision 6/15

Payment of Interest on Securities

Section 193

Payment of Interest on Securities

Section 193Criteria of Deduction TDS is deductible if payment is in

excess of Rs. 5,000/- per annum.

TDS Rate 1) If the recipient is a Company, Firm

or Cooperative Society. 22.66%

2) If the recipient is an Individual or

HUF and payment exceeds Rs. 10

lacks per annum. 11.33%

3) If the recipient is an Individual or

HUF and payment does not exceeds

Rs. 10 lacks per annum. 10.30%.

8/6/2019 59_project Tds Rate & Provision

http://slidepdf.com/reader/full/59project-tds-rate-provision 7/15

Payment of Interest Other

Than SecuritiesSection 194A

Payment of Interest Other

Than SecuritiesSection 194A

Criteria of Deduction TDS is deductible if payment is in excess

of Rs. 5,000/- per annum.TDS Rate 1) If the recipient is a Company, Firm or

Cooperative Society. 22.66%

2) If the recipient is an Individual or

HUF and payment exceeds Rs. 10

lacks per annum. 11.33%3) If the recipient is an Individual or

HUF and payment does not exceeds

Rs. 10 lacks per annum. 10.30%.

8/6/2019 59_project Tds Rate & Provision

http://slidepdf.com/reader/full/59project-tds-rate-provision 8/15

Winnings from Lotteries or

CrossWord PuzzleSection 194B

Winnings from Lotteries or

CrossWord PuzzleSection 194B

Criteria of Deduction TDS is deductible if payment is in excess

of Rs. 5,000/- per annum.TDS Rate 1) If the recipient is an Individual or

HUF and payment exceeds Rs. 10

lacks per annum. 33.99%.

2) If the recipient is an Individual or

HUF and payment does not exceeds

Rs. 10 lacks per annum. 30.90%.

8/6/2019 59_project Tds Rate & Provision

http://slidepdf.com/reader/full/59project-tds-rate-provision 9/15

Winnings from Horse Race

Section 194BB

Winnings from Horse Race

Section 194BBCriteria of Deduction TDS is deductible if payment is in excess

of Rs. 2,500/- per annum.

TDS Rate 1) If the recipient is an Individual or

HUF and payment exceeds Rs. 10

lacks per annum. 11.33%

2) If the recipient is an Individual or

HUF and payment does not exceeds

Rs. 10 lacks per annum. 10.30%.

8/6/2019 59_project Tds Rate & Provision

http://slidepdf.com/reader/full/59project-tds-rate-provision 10/15

Payment to Contractors /

Sub-ContractorsSection 194C

Payment to Contractors /

Sub-ContractorsSection 194C

Criteria of Deduction TDS is deductible if payment is in

excess of Rs. 20,000/- per contract or

Rs. 50,000/- per annum.

TDS Rate 1) If the recipient is a Company, Firm

or Cooperative Society. 2.266%

2) If the recipient is an Individual or

HUF and payment exceeds Rs. 10

lacks per annum. 2.266%3) If the recipient is an Individual or

HUF and payment does not exceeds

Rs. 10 lacks per annum. 2.06%.

8/6/2019 59_project Tds Rate & Provision

http://slidepdf.com/reader/full/59project-tds-rate-provision 11/15

Payment of Commission or

BrokerageSection 194H

Payment of Commission or

BrokerageSection 194H

Criteria of Deduction TDS is deductible if payment is in

excess of Rs. 2,500/- per annum.TDS Rate 1) If the recipient is a Company, Firm

or Cooperative Society. 11.33%

2) If the recipient is an Individual or

HUF and payment exceeds Rs. 10

lacks per annum. 11.33%

3) If the recipient is an Individual or

HUF and payment does not

exceeds Rs. 10 lacks per annum.

10.30%.

8/6/2019 59_project Tds Rate & Provision

http://slidepdf.com/reader/full/59project-tds-rate-provision 12/15

Payment of Rent of Plant &

MachinerySection 194I

Payment of Rent of Plant &

MachinerySection 194I

Criteria of Deduction TDS is deductible if payment is in excess

of Rs. 1,20,000/- per annum.

TDS Rate 1) If the recipient is a Company, Firm or

Cooperative Society. 11.33%

2) If the recipient is an Individual or

HUF and payment exceeds Rs. 10

lacks per annum. 11.33%3) If the recipient is an Individual or

HUF and payment does not exceeds

Rs. 10 lacks per annum. 10.30%.

8/6/2019 59_project Tds Rate & Provision

http://slidepdf.com/reader/full/59project-tds-rate-provision 13/15

Payment of Rent of Other Than

Plant & MachinerySection 194I

Payment of Rent of Other Than

Plant & MachinerySection 194I

Criteria of Deduction TDS is deductible if payment is in excess

of Rs. 1,20,000/- per annum.

TDS Rate 1) If the recipient is a Company, Firm or

Cooperative Society. 22.66%

2) If the recipient is an Individual or HUF

and payment exceeds Rs. 10 lacks per

annum. 16.995%3) If the recipient is an Individual or HUF

and payment does not exceeds Rs. 10

lacks per annum. 15.45%.

8/6/2019 59_project Tds Rate & Provision

http://slidepdf.com/reader/full/59project-tds-rate-provision 14/15

Payment of Professional

ChargesSection 194J

Payment of Professional

ChargesSection 194J

Criteria of Deduction TDS is deductible if payment is in

excess of Rs. 20,000/- per annum.TDS Rate 1) If the recipient is a Company, Firm

or Cooperative Society. 11.33%

2) If the recipient is an Individual or

HUF and payment exceeds Rs. 10

lacks per annum. 11.33%3) If the recipient is an Individual or

HUF and payment does not exceeds

Rs. 10 lacks per annum. 10.30%.

8/6/2019 59_project Tds Rate & Provision

http://slidepdf.com/reader/full/59project-tds-rate-provision 15/15

Related Documents