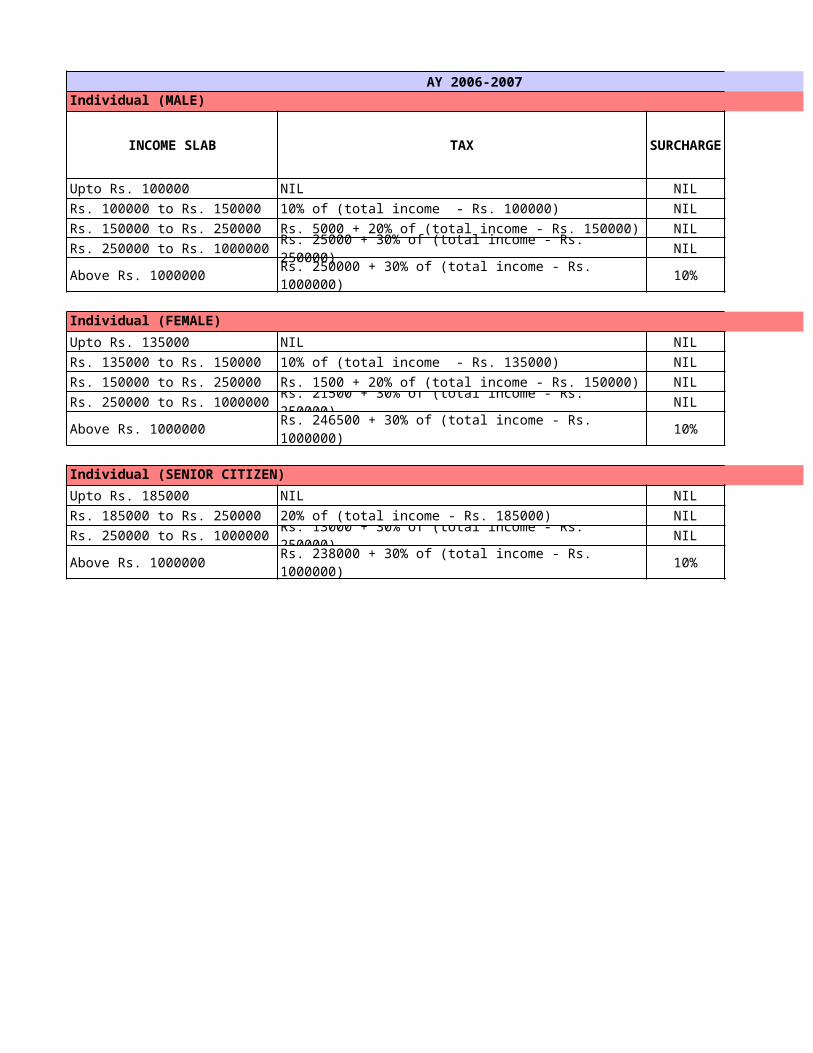

AY 2006-2007 Individual (MALE) INCOME SLAB TAX SURCHARGE Upto Rs. 100000 NIL NIL Rs. 100000 to Rs. 150000 10% of (total income - Rs. 100000) NIL Rs. 150000 to Rs. 250000 Rs. 5000 + 20% of (total income - Rs. 150000) NIL Rs. 250000 to Rs. 1000000 NIL Above Rs. 1000000 10% Individual (FEMALE) Upto Rs. 135000 NIL NIL Rs. 135000 to Rs. 150000 10% of (total income - Rs. 135000) NIL Rs. 150000 to Rs. 250000 Rs. 1500 + 20% of (total income - Rs. 150000) NIL Rs. 250000 to Rs. 1000000 NIL Above Rs. 1000000 10% Individual (SENIOR CITIZEN) Upto Rs. 185000 NIL NIL Rs. 185000 to Rs. 250000 20% of (total income - Rs. 185000) NIL Rs. 250000 to Rs. 1000000 NIL Above Rs. 1000000 10% Rs. 25000 + 30% of (total income - Rs. 250000) Rs. 250000 + 30% of (total income - Rs. 1000000) Rs. 21500 + 30% of (total income - Rs. 250000) Rs. 246500 + 30% of (total income - Rs. 1000000) Rs. 13000 + 30% of (total income - Rs. 250000) Rs. 238000 + 30% of (total income - Rs. 1000000)

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

AY 2006-2007

Individual (MALE)

INCOME SLAB TAX

Upto Rs. 100000 NIL NIL NIL

Rs. 100000 to Rs. 150000 10% of (total income - Rs. 100000) NIL 2%

Rs. 150000 to Rs. 250000 Rs. 5000 + 20% of (total income - Rs. 150000) NIL 2%

Rs. 250000 to Rs. 1000000 Rs. 25000 + 30% of (total income - Rs. 250000) NIL 2%

Above Rs. 1000000 Rs. 250000 + 30% of (total income - Rs. 1000000) 10% 2%

Individual (FEMALE)

Upto Rs. 135000 NIL NIL NIL

Rs. 135000 to Rs. 150000 10% of (total income - Rs. 135000) NIL 2%

Rs. 150000 to Rs. 250000 Rs. 1500 + 20% of (total income - Rs. 150000) NIL 2%

Rs. 250000 to Rs. 1000000 Rs. 21500 + 30% of (total income - Rs. 250000) NIL 2%

Above Rs. 1000000 Rs. 246500 + 30% of (total income - Rs. 1000000) 10% 2%

Individual (SENIOR CITIZEN)

Upto Rs. 185000 NIL NIL NIL

Rs. 185000 to Rs. 250000 20% of (total income - Rs. 185000) NIL 2%

Rs. 250000 to Rs. 1000000 Rs. 13000 + 30% of (total income - Rs. 250000) NIL 2%

Above Rs. 1000000 Rs. 238000 + 30% of (total income - Rs. 1000000) 10% 2%

SURCHARGE

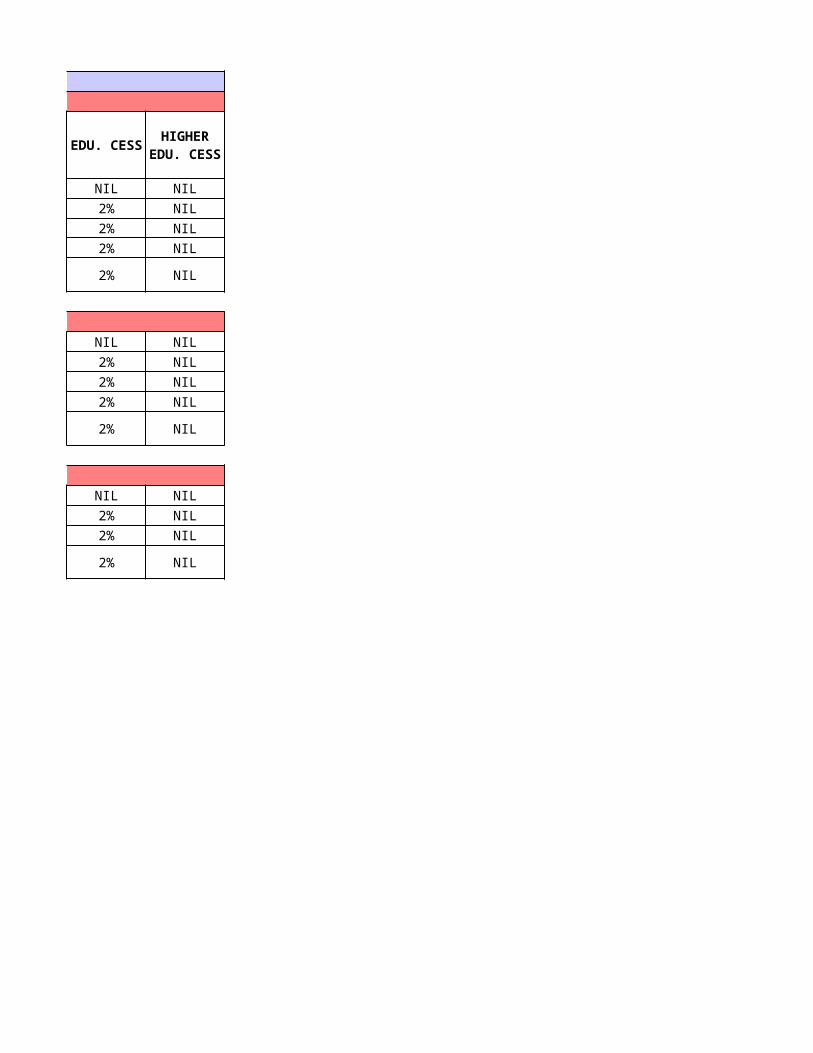

EDU. CESS

AY 2006-2007

Individual (MALE)

NIL

NIL

NIL

NIL

NIL

Individual (FEMALE)

NIL

NIL

NIL

NIL

NIL

Individual (SENIOR CITIZEN)

NIL

NIL

NIL

NIL

HIGHER EDU. CESS

AY 2007-2008

Individual (MALE)

INCOME SLAB TAX

Upto Rs. 100000 NIL NIL NIL

Rs. 100000 to Rs. 150000 10% of (total income - Rs. 100000) NIL 2%

Rs. 150000 to Rs. 250000 Rs. 5000 + 20% of (total income - Rs. 150000) NIL 2%

Rs. 250000 to Rs. 1000000 Rs. 25000 + 30% of (total income - Rs. 250000) NIL 2%

Above Rs. 1000000 Rs. 250000 + 30% of (total income - Rs. 1000000) 10% 2%

Individual (FEMALE)

Upto Rs. 135000 NIL NIL NIL

Rs. 135000 to Rs. 150000 10% of (total income - Rs. 135000) NIL 2%

Rs. 150000 to Rs. 250000 Rs. 1500 + 20% of (total income - Rs. 150000) NIL 2%

Rs. 250000 to Rs. 1000000 Rs. 21500 + 30% of (total income - Rs. 250000) NIL 2%

Above Rs. 1000000 Rs. 246500 + 30% of (total income - Rs. 1000000) 10% 2%

Individual (SENIOR CITIZEN)

Upto Rs. 185000 NIL NIL NIL

Rs. 185000 to Rs. 250000 20% of (total income - Rs. 185000) NIL 2%

Rs. 250000 to Rs. 1000000 Rs. 13000 + 30% of (total income - Rs. 250000) NIL 2%

Above Rs. 1000000 Rs. 238000 + 30% of (total income - Rs. 1000000) 10% 2%

SURCHARGE

EDU. CESS

AY 2007-2008

Individual (MALE)

NIL

NIL

NIL

NIL

NIL

Individual (FEMALE)

NIL

NIL

NIL

NIL

NIL

Individual (SENIOR CITIZEN)

NIL

NIL

NIL

NIL

HIGHER EDU. CESS

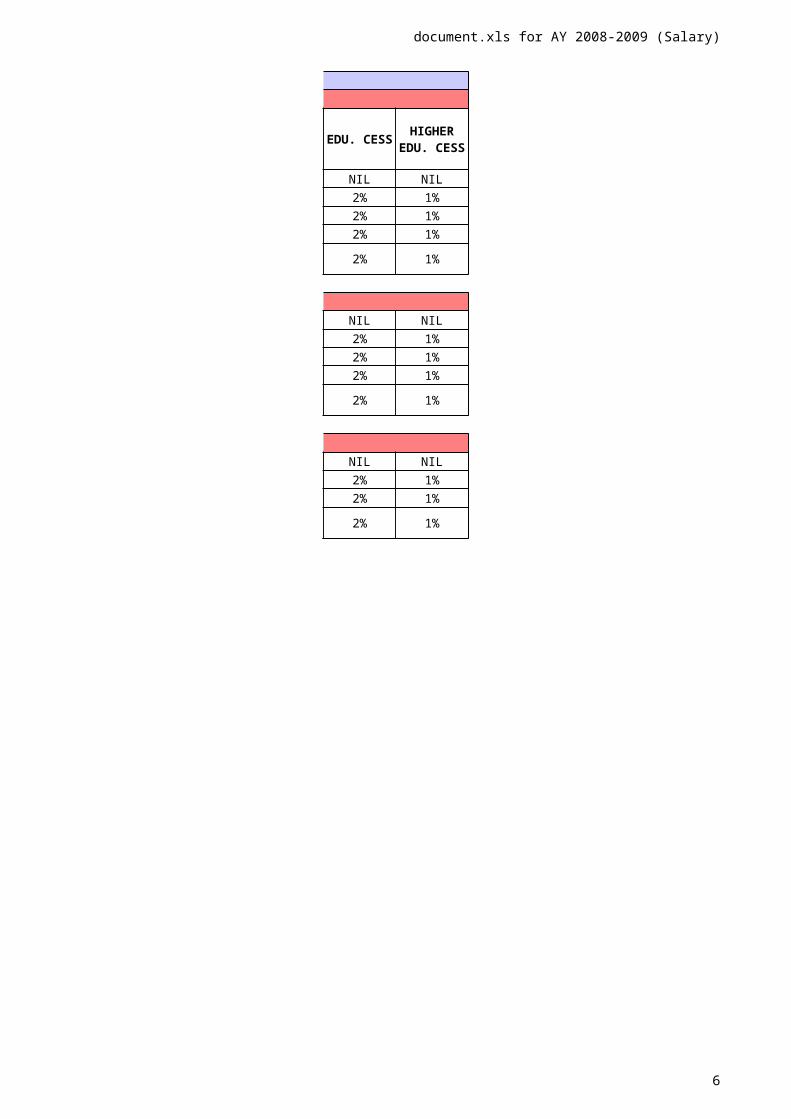

document.xls for AY 2008-2009 (Salary)

5

AY 2008 -2009

Individual (MALE)

INCOME SLAB TAX

Upto Rs. 110000 NIL NIL NIL NIL

Rs. 110000 to Rs. 150000 10% of (total income - Rs. 110000) NIL 2% 1%

Rs. 150000 to Rs. 250000 Rs. 4000 + 20% of (total income - Rs. 150000) NIL 2% 1%

Rs. 250000 to Rs. 1000000 Rs. 24000 + 30% of (total income - Rs. 250000) NIL 2% 1%

Above Rs. 1000000 Rs. 249000 + 30% of (total income - Rs. 1000000) 10% 2% 1%

Individual (FEMALE)

Upto Rs. 145000 NIL NIL NIL NIL

Rs. 145000 to Rs. 150000 10% of (total income - Rs. 145000) NIL 2% 1%

Rs. 150000 to Rs. 250000 Rs. 500 + 20% of (total income - Rs. 150000) NIL 2% 1%

Rs. 250000 to Rs. 1000000 Rs. 20500 + 30% of (total income - Rs. 250000) NIL 2% 1%

Above Rs. 1000000 Rs. 245500 + 30% of (total income - Rs. 1000000) 10% 2% 1%

Individual (SENIOR CITIZEN)

Upto Rs. 195000 NIL NIL NIL NIL

Rs. 195000 to Rs. 250000 20% of (total income - Rs. 195000) NIL 2% 1%

Rs. 250000 to Rs. 1000000 Rs. 11000 + 30% of (total income - Rs. 250000) NIL 2% 1%

Above Rs. 1000000 Rs. 236000 + 30% of (total income - Rs. 1000000) 10% 2% 1%

SURCHARGE

EDU. CESS

HIGHER EDU. CESS

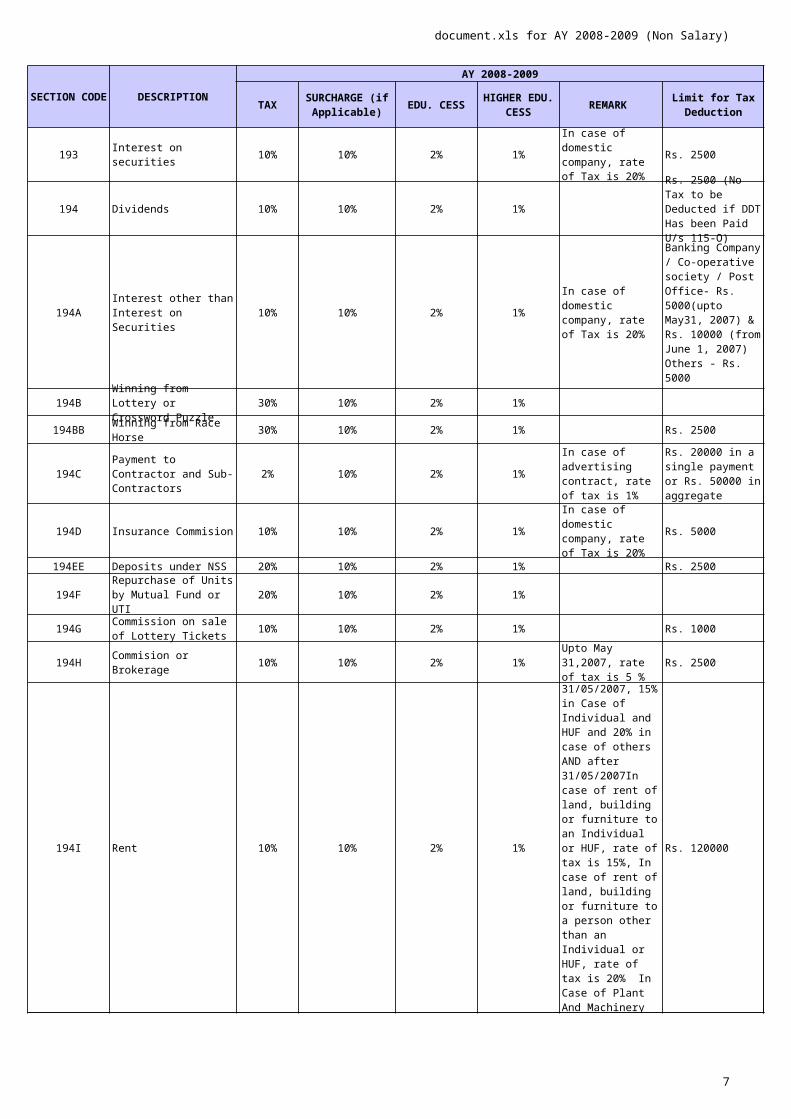

document.xls for AY 2008-2009 (Non Salary)

6

DESCRIPTION

AY 2008-2009

TAX EDU. CESS REMARK

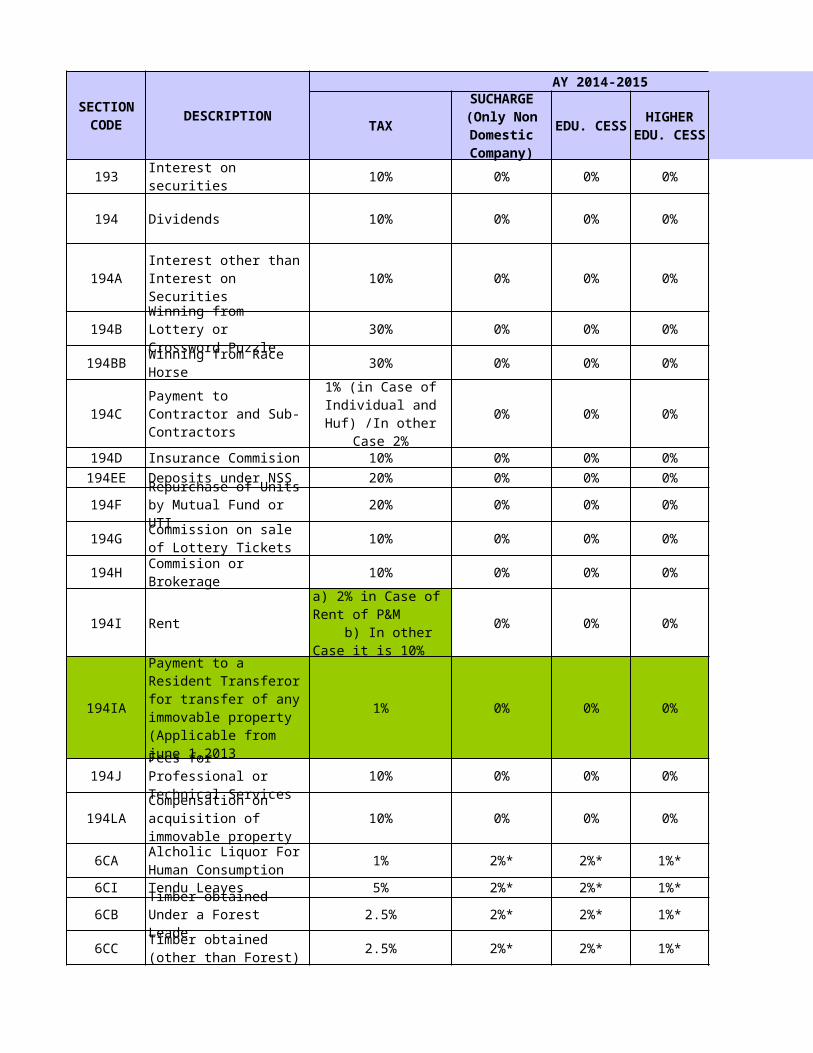

193 Interest on securities 10% 10% 2% 1% Rs. 2500

194 Dividends 10% 10% 2% 1%

194A 10% 10% 2% 1%

194B 30% 10% 2% 1%

194BB 30% 10% 2% 1% Rs. 2500

194C 2% 10% 2% 1%

194D Insurance Commision 10% 10% 2% 1% Rs. 5000

194EE Deposits under NSS 20% 10% 2% 1% Rs. 2500

194F 20% 10% 2% 1%

194G 10% 10% 2% 1% Rs. 1000

194H 10% 10% 2% 1% Rs. 2500

194I Rent 10% 10% 2% 1% Rs. 120000

194J 10% 10% 2% 1% Rs. 20000

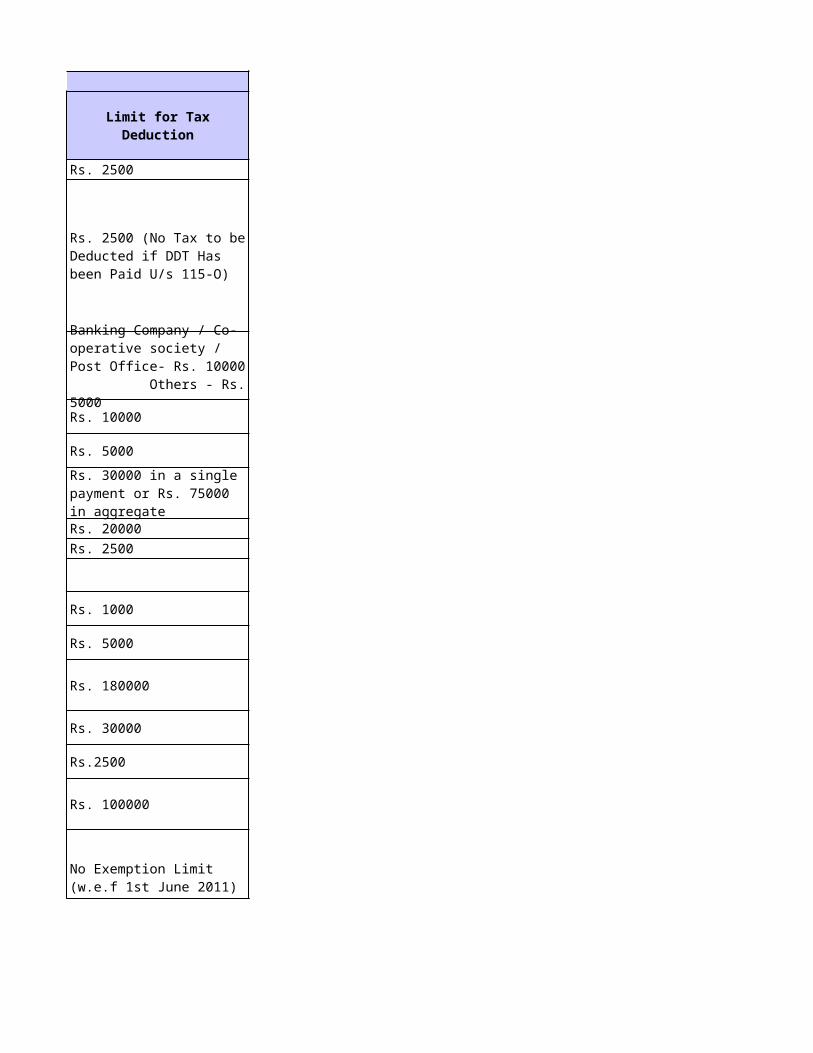

SECTION CODE SURCHARGE

(if Applicable)HIGHER

EDU. CESSLimit for Tax

Deduction

In case of domestic company, rate of Tax is 20%

Rs. 2500 (No Tax to be Deducted if DDT Has been Paid U/s 115-O)

Interest other than Interest on Securities

In case of domestic company, rate of Tax is 20%

Banking Company / Co-operative society / Post Office- Rs. 5000(upto May31, 2007) & Rs. 10000 (from June 1, 2007) Others - Rs. 5000

Winning from Lottery or Crossword Puzzle

Winning from Race Horse

Payment to Contractor and Sub- Contractors

In case of advertising contract, rate of tax is 1%

Rs. 20000 in a single payment or Rs. 50000 in aggregate

In case of domestic company, rate of Tax is 20%

Repurchase of Units by Mutual Fund or UTI

Commission on sale of Lottery Tickets

Commision or Brokerage

Upto May 31,2007, rate of tax is 5 %

Up to 31/05/2007, 15% in Case of Individual and HUF and 20% in case of others AND after 31/05/2007In case of rent of land, building or furniture to an Individual or HUF, rate of tax is 15%, In case of rent of land, building or furniture to a person other than an Individual or HUF, rate of tax is 20% In Case of Plant And Machinery Rate is 10%

Fees for Professional or Technical Services

Upto May 31,2007, rate of tax is 5 %

document.xls for AY 2008-2009 (Non Salary)

7

DESCRIPTION

AY 2008-2009

TAX EDU. CESS REMARK SECTION

CODE SURCHARGE (if Applicable)

HIGHER EDU. CESS

Limit for Tax Deduction

194K 10% 10% 2% 1% Rs.2500

194LA 10% 10% 2% 1% Rs. 100000

Note:

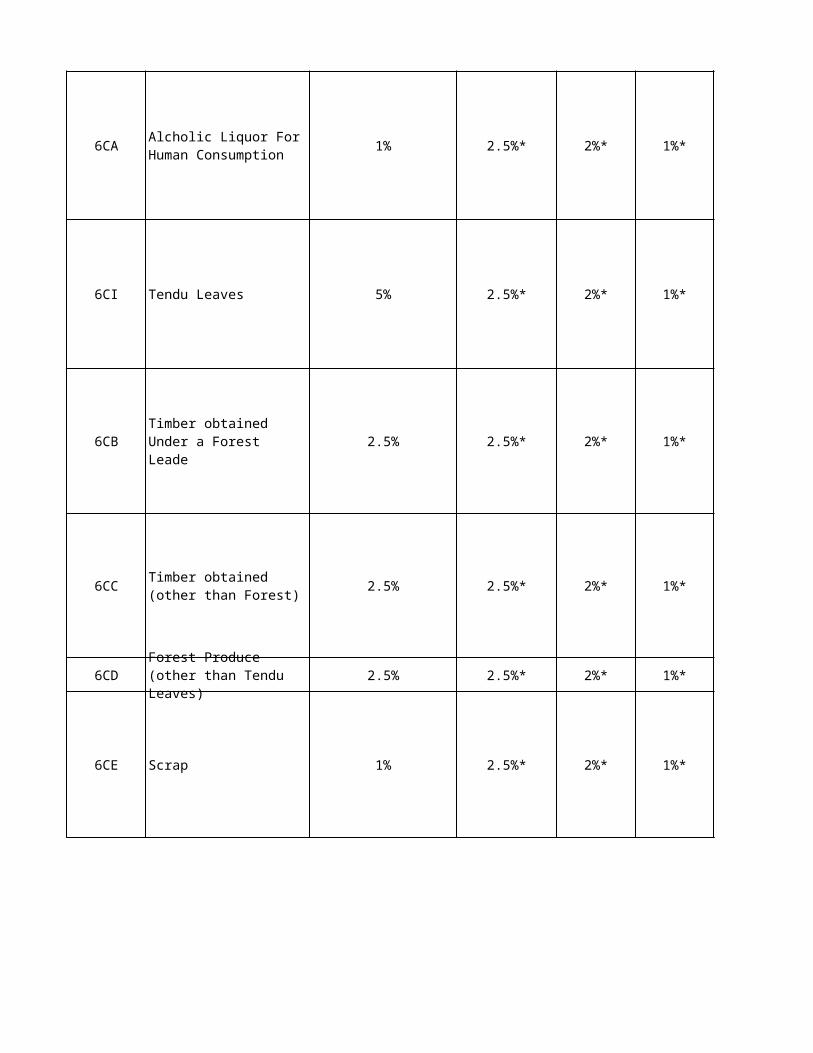

6CA 1% 10% 2% 1%

6CI Tendu Leaves 5% 10% 2% 1%

6CB 3% 10% 2% 1%

6CC 3% 10% 2% 1%

6CD 3% 10% 2% 1%

6CE Scrap 1% 10% 2% 1%

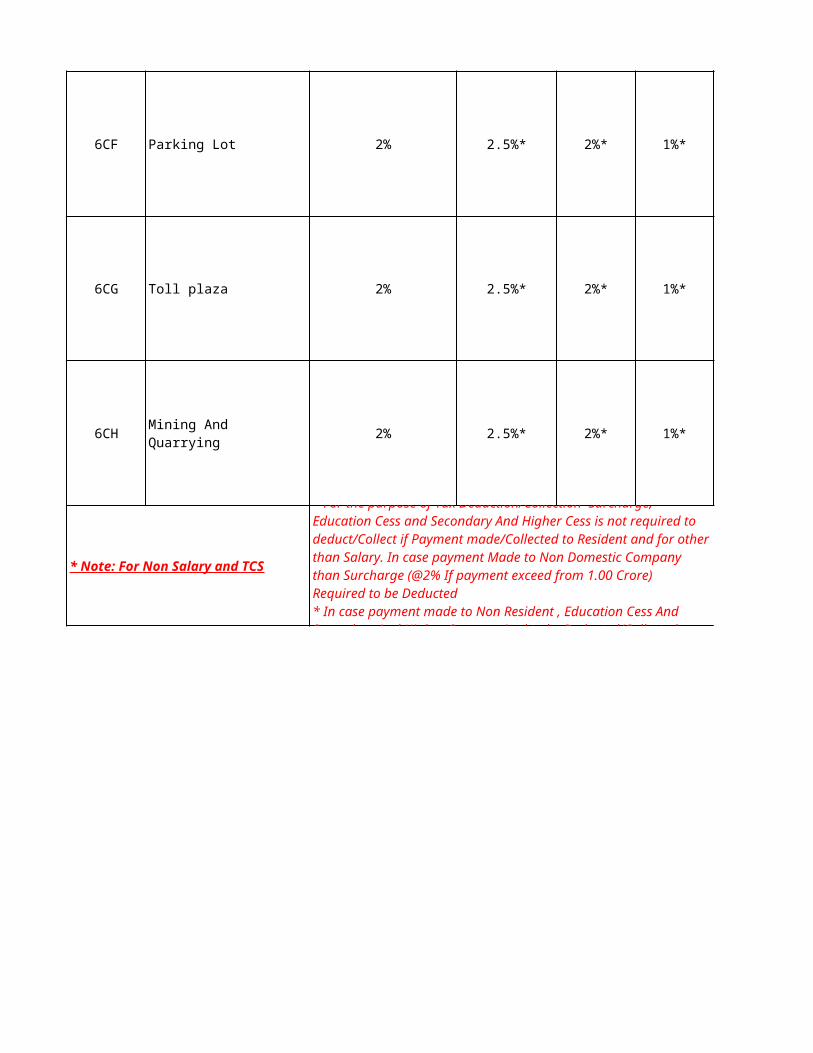

6CF Parking Lot 2% 10% 2% 1%

6CG Toll plaza 2% 10% 2% 1%

Income in respect of units

Compensation on acquisition of immovable property

Surcharge is applicable to every section in case where the amount subject to tax deduction exceeds Rs. 1000000 in case of an individual HUF, BOI, AOP & Rs. 1 crore in case of a firm/domestic company

Alcholic Liquor For Human Consumption

In case of non-domestic company & amount liable to tax exceeds Rs. 1 crore, rate of surcharge is 2.5%

In case of non-domestic company & amount liable to tax exceeds Rs. 1 crore, rate of surcharge is 2.5%

Timber obtained Under a Forest Leade

In case of non-domestic company & amount liable to tax exceeds Rs. 1 crore, rate of surcharge is 2.5%

Timber obtained (other than Forest)

In case of non-domestic company & amount liable to tax exceeds Rs. 1 crore, rate of surcharge is 2.5%

Forest Produce (other than Tendu Leaves)

In case of non-domestic company & amount liable to tax exceeds Rs. 1 crore, rate of surcharge is 2.5%

In case of non-domestic company & amount liable to tax exceeds Rs. 1 crore, rate of surcharge is 2.5%

In case of non-domestic company & amount liable to tax exceeds Rs. 1 crore, rate of surcharge is 2.5%

In case of non-domestic company & amount liable to tax exceeds Rs. 1 crore, rate of surcharge is 2.5%

document.xls for AY 2008-2009 (Non Salary)

8

DESCRIPTION

AY 2008-2009

TAX EDU. CESS REMARK SECTION

CODE SURCHARGE (if Applicable)

HIGHER EDU. CESS

Limit for Tax Deduction

6CH Mining And Quarrying 2% 10% 2% 1%

Note:

In case of non-domestic company & amount liable to tax exceeds Rs. 1 crore, rate of surcharge is 2.5%

Surcharge is applicable to every section in case where the amount subject to tax deduction exceeds Rs. 1000000 in case of an individual HUF, BOI, AOP & Rs. 1 crore in case of a firm/domestic company

document.xls for AY 2009-2010 (Salary)

9

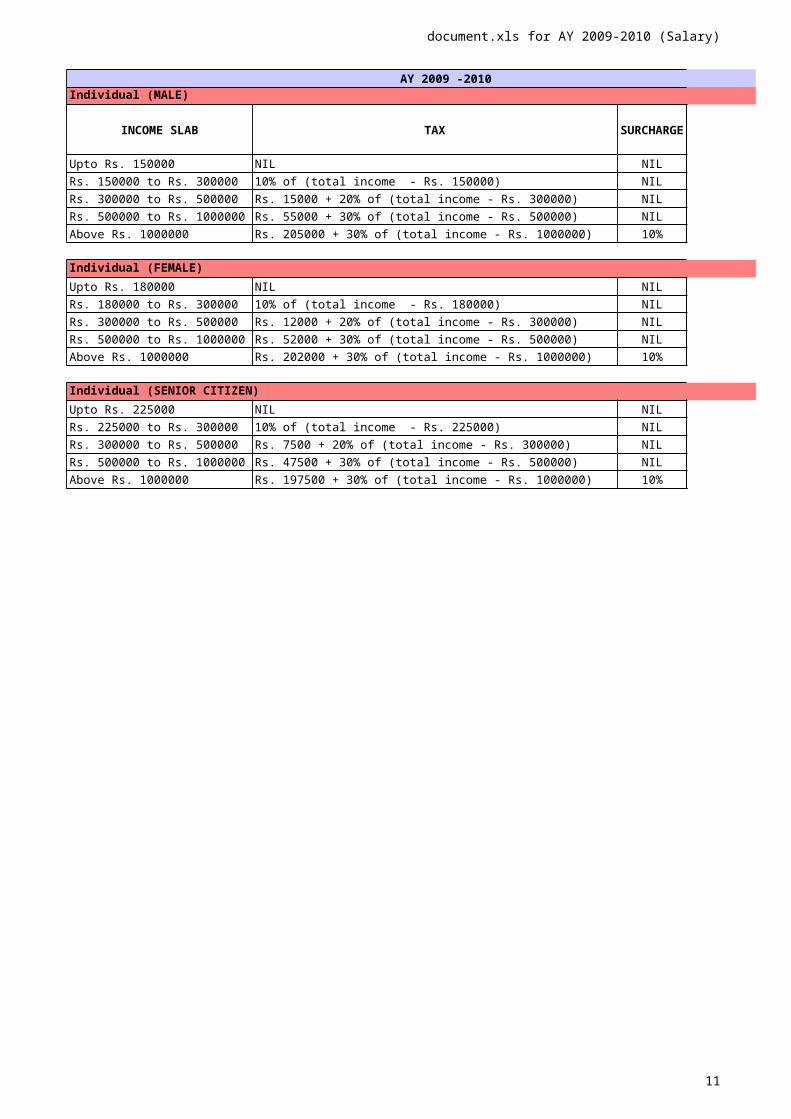

AY 2009 -2010

Individual (MALE)

INCOME SLAB TAX

Upto Rs. 150000 NIL NIL NIL NIL

Rs. 150000 to Rs. 300000 10% of (total income - Rs. 150000) NIL 2% 1%

Rs. 300000 to Rs. 500000 Rs. 15000 + 20% of (total income - Rs. 300000) NIL 2% 1%

Rs. 500000 to Rs. 1000000 Rs. 55000 + 30% of (total income - Rs. 500000) NIL 2% 1%

Above Rs. 1000000 Rs. 205000 + 30% of (total income - Rs. 1000000) 10% 2% 1%

Individual (FEMALE)

Upto Rs. 180000 NIL NIL NIL NIL

Rs. 180000 to Rs. 300000 10% of (total income - Rs. 180000) NIL 2% 1%

Rs. 300000 to Rs. 500000 Rs. 12000 + 20% of (total income - Rs. 300000) NIL 2% 1%

Rs. 500000 to Rs. 1000000 Rs. 52000 + 30% of (total income - Rs. 500000) NIL 2% 1%

Above Rs. 1000000 Rs. 202000 + 30% of (total income - Rs. 1000000) 10% 2% 1%

Individual (SENIOR CITIZEN)

Upto Rs. 225000 NIL NIL NIL NIL

Rs. 225000 to Rs. 300000 10% of (total income - Rs. 225000) NIL 2% 1%

Rs. 300000 to Rs. 500000 Rs. 7500 + 20% of (total income - Rs. 300000) NIL 2% 1%

Rs. 500000 to Rs. 1000000 Rs. 47500 + 30% of (total income - Rs. 500000) NIL 2% 1%

Above Rs. 1000000 Rs. 197500 + 30% of (total income - Rs. 1000000) 10% 2% 1%

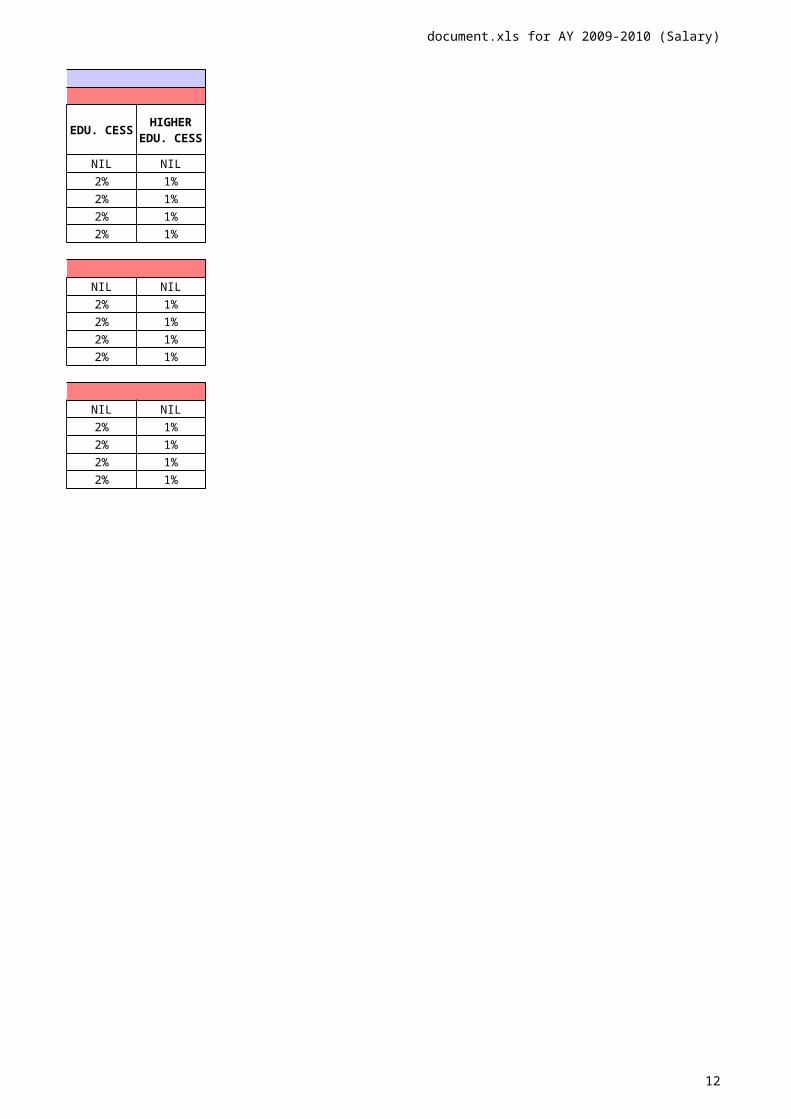

SURCHARGE

EDU. CESS

HIGHER EDU. CESS

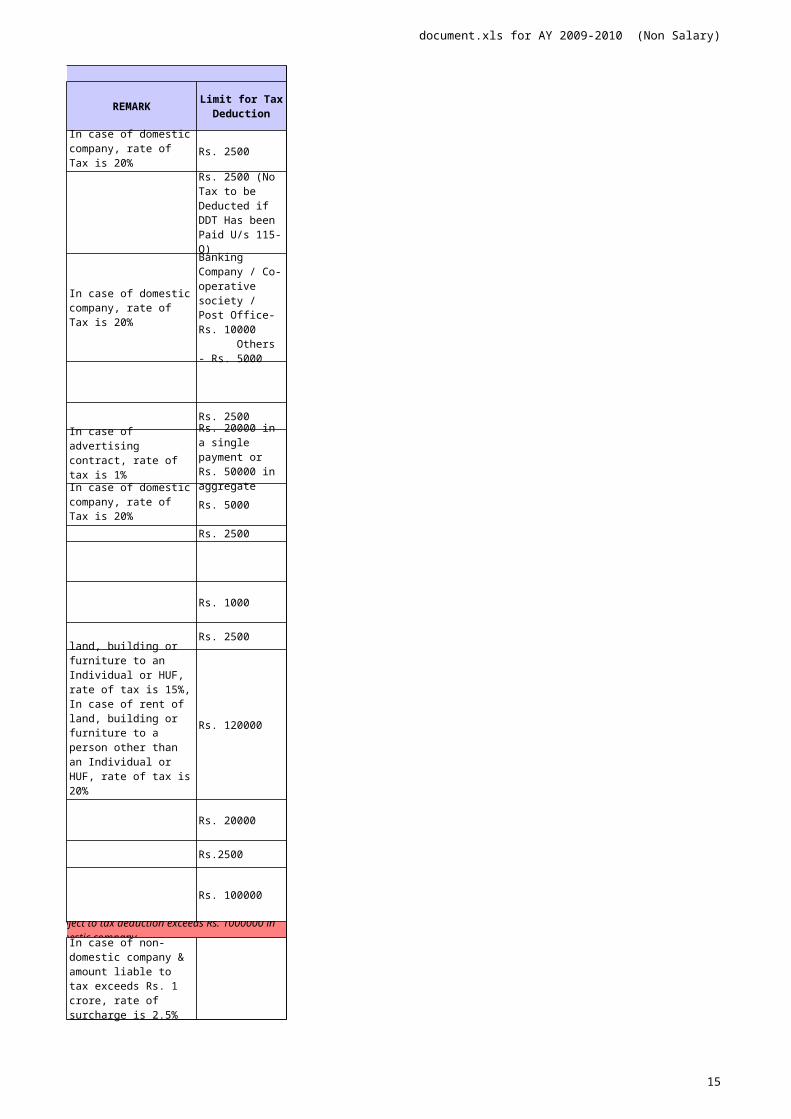

document.xls for AY 2009-2010 (Non Salary)

10

DESCRIPTION

AY 2009-2010

TAX EDU. CESS REMARK

193 Interest on securities 10% 10% 2% 1% Rs. 2500

194 Dividends 10% 10% 2% 1%

194A 10% 10% 2% 1%

194B 30% 10% 2% 1%

194BB 30% 10% 2% 1% Rs. 2500

194C 2% 10% 2% 1%

194D Insurance Commision 10% 10% 2% 1% Rs. 5000

194EE Deposits under NSS 20% 10% 2% 1% Rs. 2500

194F 20% 10% 2% 1%

194G 10% 10% 2% 1% Rs. 1000

194H 10% 10% 2% 1% Rs. 2500

194I Rent 10% 10% 2% 1% Rs. 120000

194J 10% 10% 2% 1% Rs. 20000

194K 10% 10% 2% 1% Rs.2500

194LA 10% 10% 2% 1% Rs. 100000

Note:

6CA 1% 10% 2% 1%

SECTION CODE SUCHARGE (if

Applicable)HIGHER

EDU. CESSLimit for Tax

Deduction

In case of domestic company, rate of Tax is 20%

Rs. 2500 (No Tax to be Deducted if DDT Has been Paid U/s 115-O)

Interest other than Interest on Securities

In case of domestic company, rate of Tax is 20%

Banking Company / Co-operative society / Post Office- Rs. 10000 Others - Rs. 5000

Winning from Lottery or Crossword Puzzle

Winning from Race Horse

Payment to Contractor and Sub- Contractors

In case of advertising contract, rate of tax is 1%

Rs. 20000 in a single payment or Rs. 50000 in aggregate

In case of domestic company, rate of Tax is 20%

Repurchase of Units by Mutual Fund or UTI

Commission on sale of Lottery Tickets

Commision or Brokerage

In case of rent of land, building or furniture to an Individual or HUF, rate of tax is 15%, In case of rent of land, building or furniture to a person other than an Individual or HUF, rate of tax is 20%

Fees for Professional or Technical Services

Income in respect of units

Compensation on acquisition of immovable property

Surcharge is applicable to every section in case where the amount subject to tax deduction exceeds Rs. 1000000 in case of an individual HUF, BOI, AOP & Rs. 1 crore in case of a firm/domestic company

Alcholic Liquor For Human Consumption

In case of non-domestic company & amount liable to tax exceeds Rs. 1 crore, rate of surcharge is 2.5%

document.xls for AY 2009-2010 (Non Salary)

11

DESCRIPTION

AY 2009-2010

TAX EDU. CESS REMARKSECTION

CODE SUCHARGE (if Applicable)

HIGHER EDU. CESS

Limit for Tax Deduction

6CI Tendu Leaves 5% 10% 2% 1%

6CB 3% 10% 2% 1%

6CC 3% 10% 2% 1%

6CD 3% 10% 2% 1%

6CE Scrap 1% 10% 2% 1%

6CF Parking Lot 2% 10% 2% 1%

6CG Toll plaza 2% 10% 2% 1%

6CH Mining And Quarrying 2% 10% 2% 1%

Note:

In case of non-domestic company & amount liable to tax exceeds Rs. 1 crore, rate of surcharge is 2.5%

Timber obtained Under a Forest Leade

In case of non-domestic company & amount liable to tax exceeds Rs. 1 crore, rate of surcharge is 2.5%

Timber obtained (other than Forest)

In case of non-domestic company & amount liable to tax exceeds Rs. 1 crore, rate of surcharge is 2.5%

Forest Produce (other than Tendu Leaves)

In case of non-domestic company & amount liable to tax exceeds Rs. 1 crore, rate of surcharge is 2.5%

In case of non-domestic company & amount liable to tax exceeds Rs. 1 crore, rate of surcharge is 2.5%

In case of non-domestic company & amount liable to tax exceeds Rs. 1 crore, rate of surcharge is 2.5%

In case of non-domestic company & amount liable to tax exceeds Rs. 1 crore, rate of surcharge is 2.5%

In case of non-domestic company & amount liable to tax exceeds Rs. 1 crore, rate of surcharge is 2.5%

Surcharge is applicable to every section in case where the amount subject to tax deduction exceeds Rs. 1000000 in case of an individual HUF, BOI, AOP & Rs. 1 crore in case of a firm/domestic company

document.xls for AY 2010-2011 (Salary)

12

AY 2010 -2011

Individual (MALE)

INCOME SLAB TAX

Upto Rs. 160000 NIL NIL NIL NIL

Rs. 160000 to Rs. 300000 10% of (total income - Rs. 160000) NIL 2% 1%

Rs. 300000 to Rs. 500000 Rs. 14000 + 20% of (total income - Rs. 300000) NIL 2% 1%

Above 500000 Rs. 54000 + 30% of (total income - Rs. 500000) NIL 2% 1%

Individual (FEMALE)

Upto Rs. 190000 NIL NIL NIL NIL

Rs. 190000 to Rs. 300000 10% of (total income - Rs. 190000) NIL 2% 1%

Rs. 300000 to Rs. 500000 Rs. 11000 + 20% of (total income - Rs. 300000) NIL 2% 1%

Above Rs. 500000 Rs. 51000 + 30% of (total income - Rs. 500000) NIL 2% 1%

Individual (SENIOR CITIZEN)

Upto Rs. 240000 NIL NIL NIL NIL

Rs. 240000 to Rs. 300000 10% of (total income - Rs. 240000) NIL 2% 1%

Rs. 300000 to Rs. 500000 Rs. 6000 + 20% of (total income - Rs. 300000) NIL 2% 1%

Above Rs 500000 Rs. 46000 + 30% of (total income - Rs. 500000) NIL 2% 1%

SURCHARGE

EDU. CESS

HIGHER EDU. CESS

document.xls for AY 2010-2011 (Non Salary)

13

DESCRIPTION

AY 2010-2011 (Payment Up to 18/08/2009) AY 2010-2011 (Payment after 18/08/2009)

TAX SUCHARGE EDU. CESS REMARK TAX EDU. CESS REMARK

193 Interest on securities 10% 10% 2% 1% Rs. 2500 10% 0% 2%* 1%* Rs. 2500

194 Dividends 10% 10% 2% 1% 10% 0% 2%* 1%*

194A 10% 10% 2% 1% 10% 0% 2%* 1%*

194B 30% 10% 2% 1% 30% 2.5%* 2%* 1%*

194BB 30% 10% 2% 1% Rs. 2500 30% 2.5%* 2%* 1%* Rs. 2500

194C 2%* 10% 2% 1% N.A. N.A. N.A. N.A.

194C N.A. N.A. N.A. N.A. N.A. N.A. 2% 0% 2%* 1%* N.A.

194D Insurance Commision 10% 10% 2% 1% Rs. 5000 10% 0% 2%* 1%* Rs. 5000

194EE Deposits under NSS 20% 10% 2% 1% Rs. 2500 20% 2.5%* 2%* 1%* Rs. 2500

SECTION CODE HIGHER

EDU. CESSLimit for

Tax Deduction

SUCHARGE (Only Non Domestic Company)

HIGHER EDU. CESS

Limit for Tax

Deduction

In case of domestic company, rate of Tax is 20%

Rs. 2500 (No Tax to be Deducted if DDT Has been Paid U/s 115-O)

Rs. 2500 (No Tax to be Deducted if DDT Has been Paid U/s 115-O)

Interest other than Interest on Securities

In case of domestic company, rate of Tax is 20%

Banking Company / Co-operative society / Post Office- Rs. 10000 Others - Rs. 5000

Banking Company / Co-operative society / Post Office- Rs. 10000 Others - Rs. 5000

Winning from Lottery or Crossword Puzzle

Winning from Race Horse

Payment to Contractor and Sub- Contractors In case of

advertising contract, rate of tax is 1%

Rs. 20000 in a single payment or Rs. 50000 in aggregate

Rs. 20000 in a single payment or Rs. 50000 in aggregate

Payment to Contractor and Sub- Contractors (on or After 01/10/2009)

In case of Individual and Huf Rate of TDS 1%

In case of domestic company, rate of Tax is 20%

document.xls for AY 2010-2011 (Non Salary)

14

DESCRIPTION

AY 2010-2011 (Payment Up to 18/08/2009) AY 2010-2011 (Payment after 18/08/2009)

TAX SUCHARGE EDU. CESS REMARK TAX EDU. CESS REMARKSECTION

CODE HIGHER EDU. CESS

Limit for Tax

Deduction

SUCHARGE (Only Non Domestic Company)

HIGHER EDU. CESS

Limit for Tax

Deduction

194F 20% 10% 2% 1% 20% 2.5%* 2%* 1%*

194G 10% 10% 2% 1% Rs. 1000 10% 2.5%* 2%* 1%* Rs. 1000

194H 10% 10% 2% 1% Rs. 2500 10% 0% 2%* 1%* Rs. 2500

194I Rent 10% 10% 2% 1% N.A. N.A. N.A. N.A. Rs. 120000

194I N.A. N.A. N.A. N.A. N.A. 10%* 0% 2%* 1%* Rs. 120000

194J 10% 10% 2% 1% Rs. 20000 10% 0% 2%* 1%* Rs. 20000

194K 10% 10% 2% 1% Rs.2500 10% 0% 2%* 1%* Rs.2500

194LA 10% 10% 2% 1% 10% 0% 2%* 1%* Rs. 100000

Repurchase of Units by Mutual Fund or UTI

Commission on sale of Lottery Tickets

Commision or Brokerage

In case of rent of land, building or furniture to an Individual or HUF, rate of tax is 15%, In case of rent of land, building or furniture to a person other than an Individual or HUF, rate of tax is 20%

Rs. 120000

Rent (on or After 01/10/2009)

Rs. 120000

In the Case of Rent of Plant And Machinery Rate of TDS is 2%.

Fees for Professional or Technical Services

Income in respect of units

No Tax to be deducted if Amount less than 2500/-

No Tax to be deducted if Amount less than 2500/-

Compensation on acquisition of immovable property

Rs. 100000

document.xls for AY 2010-2011 (Non Salary)

15

DESCRIPTION

AY 2010-2011 (Payment Up to 18/08/2009) AY 2010-2011 (Payment after 18/08/2009)

TAX SUCHARGE EDU. CESS REMARK TAX EDU. CESS REMARKSECTION

CODE HIGHER EDU. CESS

Limit for Tax

Deduction

SUCHARGE (Only Non Domestic Company)

HIGHER EDU. CESS

Limit for Tax

Deduction

6CA 1% 10% 2% 1% 1% 2.5%* 2%* 1%*

6CI Tendu Leaves 5% 10% 2% 1% 5% 2.5%* 2%* 1%*

6CB 2.5% 10% 2% 1% 2.5% 2.5%* 2%* 1%*

6CC 2.5% 10% 2% 1% 2.5% 2.5%* 2%* 1%*

6CD 2.5% 10% 2% 1% 2.5% 2.5%* 2%* 1%*

Alcholic Liquor For Human Consumption

In case of non-domestic company & amount liable to tax exceeds Rs. 1 crore, rate of surcharge is 2.5%

In case of non-domestic company & amount liable to tax exceeds Rs. 1 crore, rate of surcharge is 2.5%

Timber obtained Under a Forest Leade

In case of non-domestic company & amount liable to tax exceeds Rs. 1 crore, rate of surcharge is 2.5%

Timber obtained (other than Forest)

In case of non-domestic company & amount liable to tax exceeds Rs. 1 crore, rate of surcharge is 2.5%

Forest Produce (other than Tendu Leaves)

In case of non-domestic company & amount liable to tax exceeds Rs. 1 crore, rate of surcharge is 2.5%

document.xls for AY 2010-2011 (Non Salary)

16

DESCRIPTION

AY 2010-2011 (Payment Up to 18/08/2009) AY 2010-2011 (Payment after 18/08/2009)

TAX SUCHARGE EDU. CESS REMARK TAX EDU. CESS REMARKSECTION

CODE HIGHER EDU. CESS

Limit for Tax

Deduction

SUCHARGE (Only Non Domestic Company)

HIGHER EDU. CESS

Limit for Tax

Deduction

6CE Scrap 1% 10% 2% 1% 1% 2.5%* 2%* 1%*

6CF Parking Lot 2% 10% 2% 1% 2% 2.5%* 2%* 1%*

6CG Toll plaza 2% 10% 2% 1% 2% 2.5%* 2%* 1%*

6CH Mining And Quarrying 2% 10% 2% 1% 2% 2.5%* 2%* 1%*

* Note: For Non Salary and TCS

In case of non-domestic company & amount liable to tax exceeds Rs. 1 crore, rate of surcharge is 2.5%

In case of non-domestic company & amount liable to tax exceeds Rs. 1 crore, rate of surcharge is 2.5%

In case of non-domestic company & amount liable to tax exceeds Rs. 1 crore, rate of surcharge is 2.5%

In case of non-domestic company & amount liable to tax exceeds Rs. 1 crore, rate of surcharge is 2.5%

Surcharge is applicable to every section in case where the amount subject to tax deduction exceeds Rs. 1000000 in case of an individual HUF, BOI, AOP & Rs. 1 crore in case of a firm/ company. In case of Foreign Company Rate of Surcharge is 2.50%

* For the purpose of Tax Deduction/Collection Surcharge, Education Cess and Secondary And Higher Cess is not required to deduct/Collect if Payment made/Collected to Resident and for other than Salary. In case payment Made to Non Domestic Company than Surcharge (@2.5%) Required to be Deducted* In case payment made to Non Resident , Education Cess And Secondary And Higher Cess required to be Deducted/Collected.

AY 2011 -2012

Individual (MALE)

INCOME SLAB TAX

Upto Rs. 160000 NIL NIL NIL

Rs. 160000 to Rs. 500000 10% of (total income - Rs. 160000) NIL 2%

Rs. 500000 to Rs. 800000 Rs. 34000 + 20% of (total income - Rs. 500000) NIL 2%

Above 800000 Rs. 94000 + 30% of (total income - Rs. 800000) NIL 2%

Individual (FEMALE)

Upto Rs. 190000 NIL NIL NIL

Rs. 190000 to Rs. 500000 10% of (total income - Rs. 190000) NIL 2%

Rs. 500000 to Rs. 800000 Rs. 31000 + 20% of (total income - Rs. 500000) NIL 2%

Above Rs. 800000 Rs. 91000 + 30% of (total income - Rs. 800000) NIL 2%

Individual (SENIOR CITIZEN)

Upto Rs. 240000 NIL NIL NIL

Rs. 240000 to Rs. 500000 10% of (total income - Rs. 240000) NIL 2%

Rs. 500000 to Rs. 800000 Rs. 26000 + 20% of (total income - Rs. 500000) NIL 2%

Above Rs 800000 Rs. 86000 + 30% of (total income - Rs. 800000) NIL 2%

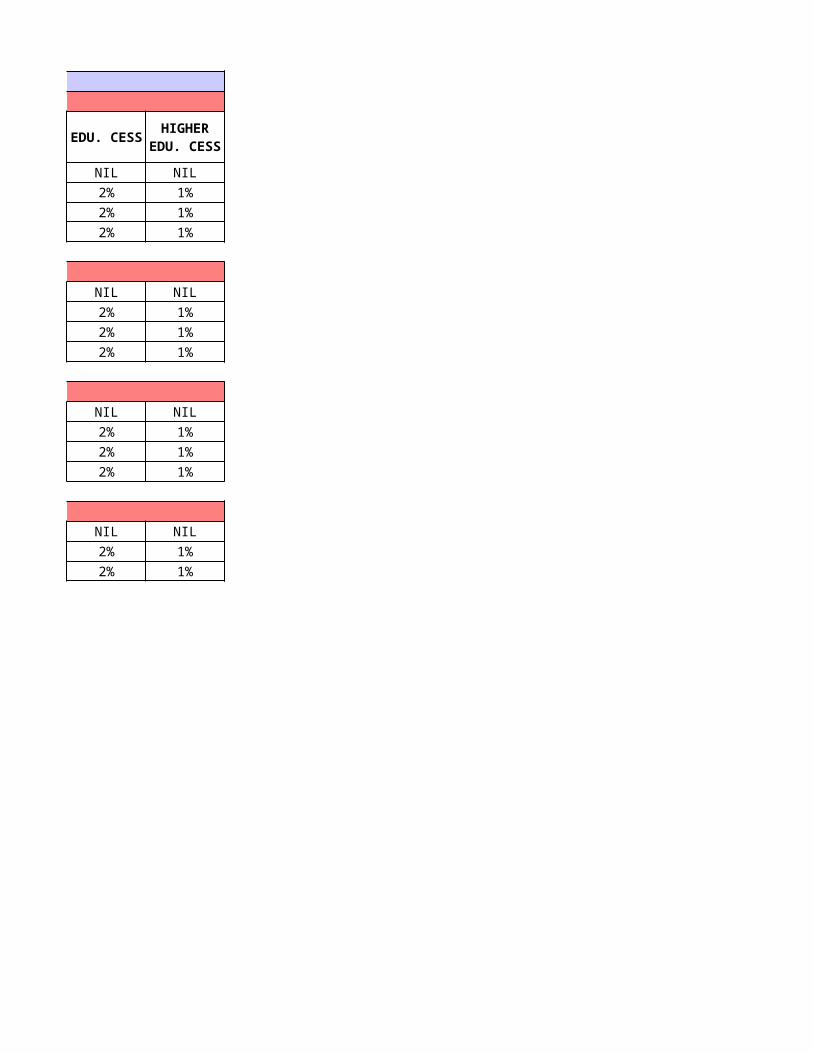

SURCHARGE

EDU. CESS

AY 2011 -2012

Individual (MALE)

NIL

1%

1%

1%

Individual (FEMALE)

NIL

1%

1%

1%

Individual (SENIOR CITIZEN)

NIL

1%

1%

1%

HIGHER EDU. CESS

DESCRIPTION

AY 2011-2012

TAX EDU. CESS

193 Interest on securities 10% 0% 0% 0%

194 Dividends 10% 0% 0% 0%

194A 10% 0% 0% 0%

194B 30% 0% 0% 0%

194BB 30% 0% 0% 0%

194C 0% 0% 0%

194D Insurance Commision 10% 0% 0% 0%194EE Deposits under NSS 20% 0% 0% 0%

194F 20% 0% 0% 0%

194G 10% 0% 0% 0%

194H 10% 0% 0% 0%

194I Rent 0% 0% 0%

194J 10% 0% 0% 0%

194K 10% 0% 0% 0%

194LA 10% 0% 0% 0%

6CA 1% 2.5%* 2%* 1%*

SECTION CODE

SUCHARGE (Only Non Domestic Company)

HIGHER EDU. CESS

Interest other than Interest on Securities

Winning from Lottery or Crossword Puzzle

Winning from Race Horse

Payment to Contractor and Sub- Contractors

1% (in Case of Individual and Huf) /In other Case 2%

Repurchase of Units by Mutual Fund or UTI

Commission on sale of Lottery Tickets

Commision or Brokerage

2% in Case of Rent of P&M / In other Case it is 10%

Fees for Professional or Technical Services

Income in respect of units

Compensation on acquisition of immovable property

Alcholic Liquor For Human Consumption

6CI Tendu Leaves 5% 2.5%* 2%* 1%*

6CB 2.5% 2.5%* 2%* 1%*

6CC 2.5% 2.5%* 2%* 1%*

6CD 2.5% 2.5%* 2%* 1%*

6CE Scrap 1% 2.5%* 2%* 1%*

6CF Parking Lot 2% 2.5%* 2%* 1%*

6CG Toll plaza 2% 2.5%* 2%* 1%*

Timber obtained Under a Forest Leade

Timber obtained (other than Forest)

Forest Produce (other than Tendu Leaves)

6CH Mining And Quarrying 2% 2.5%* 2%* 1%*

* Note: For Non Salary and TCS

* For the purpose of Tax Deduction/Collection Surcharge, Education Cess and Secondary And Higher Cess is not required to deduct/Collect if Payment made/Collected to Resident and for other than Salary. In case payment Made to Non Domestic Company than Surcharge (@2.5%) Required to be Deducted* In case payment made to Non Resident , Education Cess And Secondary And Higher Cess required to be Deducted/Collected.

AY 2011-2012

Rs. 2500 Rs. 2500

Rs. 5000 Rs. 10000

Rs. 2500 Rs. 5000

Rs. 5000 Rs. 20000Rs. 2500 Rs. 2500

Rs. 1000 Rs. 1000

Rs. 2500 Rs. 5000

Rs. 120000 Rs. 180000

Rs. 20000 Rs. 30000

Rs.2500 Rs.2500

Rs. 100000 Rs. 100000

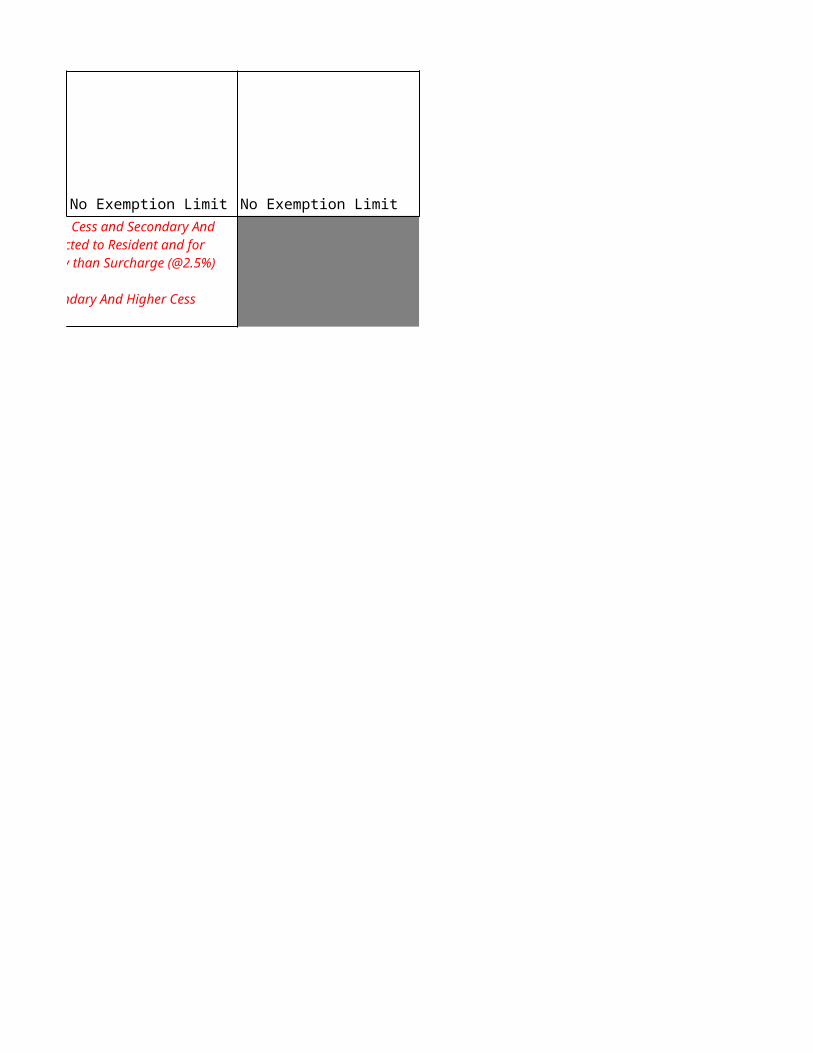

No Exemption Limit No Exemption Limit

Limit for Tax Deduction Upto June 30,2010

New Limit for Tax Deduction from July 1 ,

2010

Rs. 2500 (No Tax to be Deducted if DDT Has been Paid U/s 115-O)

Rs. 2500 (No Tax to be Deducted if DDT Has been Paid U/s 115-O)

Banking Company / Co-operative society / Post Office- Rs. 10000 Others - Rs. 5000

Banking Company / Co-operative society / Post Office- Rs. 10000 Others - Rs. 5000

Rs. 20000 in a single payment or Rs. 50000 in aggregate

Rs. 30000 in a single payment or Rs. 75000 in aggregate

No Exemption Limit No Exemption Limit

No Exemption Limit No Exemption Limit

No Exemption Limit No Exemption Limit

No Exemption Limit No Exemption Limit

No Exemption Limit No Exemption Limit

No Exemption Limit No Exemption Limit

No Exemption Limit No Exemption Limit

No Exemption Limit No Exemption Limit

* For the purpose of Tax Deduction/Collection Surcharge, Education Cess and Secondary And Higher Cess is not required to deduct/Collect if Payment made/Collected to Resident and for other than Salary. In case payment Made to Non Domestic Company than

* In case payment made to Non Resident , Education Cess And Secondary And Higher

AY 2012 -2013

Individual (MALE)

INCOME SLAB TAX

Upto Rs. 180000 NIL NIL NIL

Rs. 180000 to Rs. 500000 10% of (total income - Rs. 180000) NIL 2%

Rs. 500000 to Rs. 800000 Rs. 32000 + 20% of (total income - Rs. 500000) NIL 2%

Above 800000 Rs. 92000 + 30% of (total income - Rs. 800000) NIL 2%

Individual (FEMALE)

Upto Rs. 190000 NIL NIL NIL

Rs. 190000 to Rs. 500000 10% of (total income - Rs. 190000) NIL 2%

Rs. 500000 to Rs. 800000 Rs. 31000 + 20% of (total income - Rs. 500000) NIL 2%

Above Rs. 800000 Rs. 91000 + 30% of (total income - Rs. 800000) NIL 2%

Individual (SENIOR CITIZEN)

Upto Rs. 250000 NIL NIL NIL

Rs. 250000 to Rs. 500000 10% of (total income - Rs. 250000) NIL 2%

Rs. 500000 to Rs. 800000 Rs. 25000 + 20% of (total income - Rs. 500000) NIL 2%

Above Rs 800000 Rs. 85000 + 30% of (total income - Rs. 800000) NIL 2%

Individual (VERY SENIOR CITIZEN)

Upto Rs. 500000 NIL NIL NIL

Rs. 500000 to Rs. 800000 20% of (total income - Rs. 500000) NIL 2%

Above Rs 800000 Rs. 60000 + 30% of (total income - Rs. 800000) NIL 2%

SURCHARGE

EDU. CESS

AY 2012 -2013

Individual (MALE)

NIL

1%

1%

1%

Individual (FEMALE)

NIL

1%

1%

1%

Individual (SENIOR CITIZEN)

NIL

1%

1%

1%

Individual (VERY SENIOR CITIZEN)

NIL

1%

1%

HIGHER EDU. CESS

DESCRIPTION

AY 2012-2013

TAX EDU. CESS

193 Interest on securities 10% 0% 0% 0%

194 Dividends 10% 0% 0% 0%

194A 10% 0% 0% 0%

194B 30% 0% 0% 0%

194BB 30% 0% 0% 0%

194C 0% 0% 0%

194D Insurance Commision 10% 0% 0% 0%194EE Deposits under NSS 20% 0% 0% 0%

194F 20% 0% 0% 0%

194G 10% 0% 0% 0%

194H 10% 0% 0% 0%

194I Rent 0% 0% 0%

194J 10% 0% 0% 0%

194K 10% 0% 0% 0%

194LA 10% 0% 0% 0%

194LB

5% 0% 0% 0%

6CA 1% 2.5%* 2%* 1%*

SECTION CODE

SUCHARGE (Only Non Domestic Company)

HIGHER EDU. CESS

Interest other than Interest on Securities

Winning from Lottery or Crossword Puzzle

Winning from Race Horse

Payment to Contractor and Sub- Contractors

1% (in Case of Individual and Huf) /In other Case 2%

Repurchase of Units by Mutual Fund or UTI

Commission on sale of Lottery Tickets

Commision or Brokerage

2% in Case of Rent of P&M / In other Case it is 10%

Fees for Professional or Technical Services

Income in respect of units

Compensation on acquisition of immovable property

Income by way of interest from infrastructure debt fund payable

Alcholic Liquor For Human Consumption

6CI Tendu Leaves 5% 2.5%* 2%* 1%*

6CB 2.5% 2.5%* 2%* 1%*

6CC 2.5% 2.5%* 2%* 1%*

6CD 2.5% 2.5%* 2%* 1%*

6CE Scrap 1% 2.5%* 2%* 1%*

6CF Parking Lot 2% 2.5%* 2%* 1%*

6CG Toll plaza 2% 2.5%* 2%* 1%*

Timber obtained Under a Forest Leade

Timber obtained (other than Forest)

Forest Produce (other than Tendu Leaves)

6CH Mining And Quarrying 2% 2.5%* 2%* 1%*

* Note: For Non Salary and TCS

* For the purpose of Tax Deduction/Collection Surcharge, Education Cess and Secondary And Higher Cess is not required to deduct/Collect if Payment made/Collected to Resident and for other than Salary. In case payment Made to Non Domestic Company than Surcharge (@2% If payment exceed from 1.00 Crore) Required to be Deducted* In case payment made to Non Resident , Education Cess And Secondary And Higher Cess required to be Deducted/Collected.

AY 2012-2013

Limit for Tax Deduction

Rs. 2500

Rs. 10000

Rs. 5000

Rs. 20000Rs. 2500

Rs. 1000

Rs. 5000

Rs. 180000

Rs. 30000

Rs.2500

Rs. 100000

No Exemption Limit

Rs. 2500 (No Tax to be Deducted if DDT Has been Paid U/s 115-O)

Banking Company / Co-operative society / Post Office- Rs. 10000 Others - Rs. 5000

Rs. 30000 in a single payment or Rs. 75000 in aggregate

No Exemption Limit(w.e.f 1st June 2011)

No Exemption Limit

No Exemption Limit

No Exemption Limit

No Exemption Limit

No Exemption Limit

No Exemption Limit

No Exemption Limit

No Exemption Limit

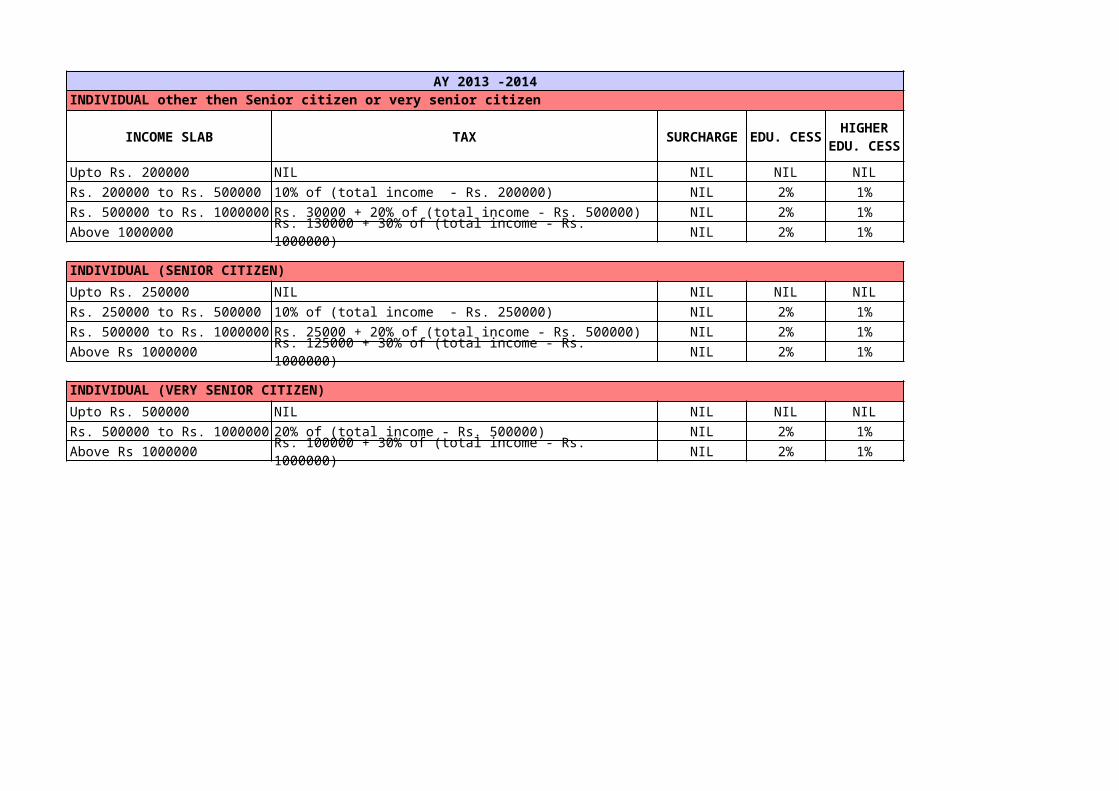

AY 2013 -2014

INDIVIDUAL other then Senior citizen or very senior citizen

INCOME SLAB TAX

Upto Rs. 200000 NIL NIL NIL NIL

Rs. 200000 to Rs. 500000 10% of (total income - Rs. 200000) NIL 2% 1%

Rs. 500000 to Rs. 1000000 Rs. 30000 + 20% of (total income - Rs. 500000) NIL 2% 1%

Above 1000000 Rs. 130000 + 30% of (total income - Rs. 1000000) NIL 2% 1%

INDIVIDUAL (SENIOR CITIZEN)

Upto Rs. 250000 NIL NIL NIL NIL

Rs. 250000 to Rs. 500000 10% of (total income - Rs. 250000) NIL 2% 1%

Rs. 500000 to Rs. 1000000 Rs. 25000 + 20% of (total income - Rs. 500000) NIL 2% 1%

Above Rs 1000000 Rs. 125000 + 30% of (total income - Rs. 1000000) NIL 2% 1%

INDIVIDUAL (VERY SENIOR CITIZEN)

Upto Rs. 500000 NIL NIL NIL NIL

Rs. 500000 to Rs. 1000000 20% of (total income - Rs. 500000) NIL 2% 1%

Above Rs 1000000 Rs. 100000 + 30% of (total income - Rs. 1000000) NIL 2% 1%

SURCHARGE

EDU. CESS

HIGHER EDU. CESS

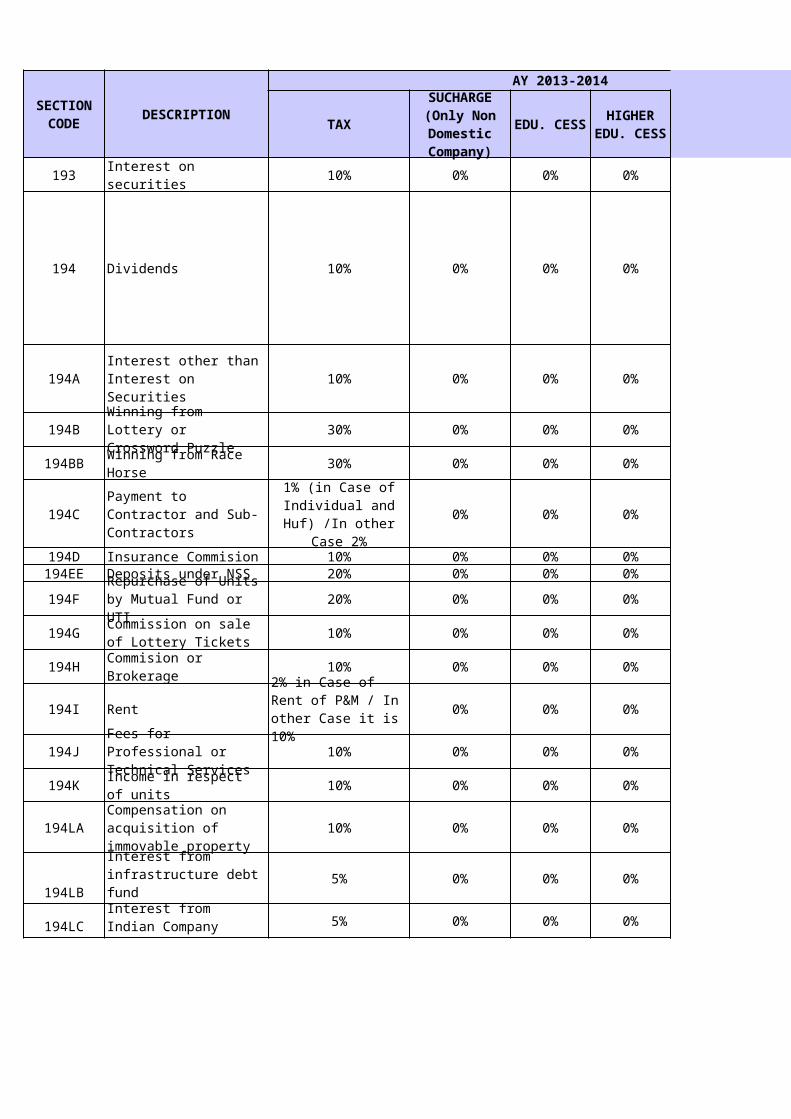

DESCRIPTION

AY 2013-2014

TAX EDU. CESS Limit for Tax Deduction

193 Interest on securities 10% 0% 0% 0%

194 Dividends 10% 0% 0% 0%

194A 10% 0% 0% 0%

194B 30% 0% 0% 0% Rs. 10000

194BB 30% 0% 0% 0% Rs. 5000

194C 0% 0% 0%

194D Insurance Commision 10% 0% 0% 0% Rs. 20000194EE Deposits under NSS 20% 0% 0% 0% Rs. 2500

194F 20% 0% 0% 0%

194G 10% 0% 0% 0% Rs. 1000

194H 10% 0% 0% 0% Rs. 5000

194I Rent 0% 0% 0% Rs. 180000

194J 10% 0% 0% 0% Rs. 30000

194K 10% 0% 0% 0% Rs.2500

194LA 10% 0% 0% 0%

194LB5% 0% 0% 0%

194LC 5% 0% 0% 0%

SECTION CODE

SUCHARGE (Only Non Domestic Company)

HIGHER EDU. CESS

Rs. 2500 (Rs. 5000/- From 1st July , 2012)

Rs. 2500 (No Tax to be Deducted if DDT Has been Paid U/s 115-O)

Interest other than Interest on Securities

Banking Company / Co-operative society / Post Office- Rs. 10000 Others - Rs. 5000

Winning from Lottery or Crossword Puzzle

Winning from Race Horse

Payment to Contractor and Sub- Contractors

1% (in Case of Individual and

Huf) /In other Case 2%

Rs. 30000 in a single payment or Rs. 75000 in aggregate

Repurchase of Units by Mutual Fund or UTI

Commission on sale of Lottery Tickets

Commision or Brokerage

2% in Case of Rent of P&M / In other Case it is 10%

Fees for Professional or Technical Services

Income in respect of units

Compensation on acquisition of immovable property

Rs. 100000 (Increased to Rs. 200000/- W.e.f 01/07/2012)

Interest from infrastructure debt fund

No Exemption Limit(w.e.f 1st June 2011)

Interest from Indian Company

No Exemption Limit(w.e.f 1st July 2012)

6CA 1% 2.5%* 2%* 1%*

No Exemption Limit

6CI Tendu Leaves 5% 2.5%* 2%* 1%*

No Exemption Limit

6CB 2.5% 2.5%* 2%* 1%*

No Exemption Limit

6CC 2.5% 2.5%* 2%* 1%*

No Exemption Limit

6CD 2.5% 2.5%* 2%* 1%* No Exemption Limit

6CE Scrap 1% 2.5%* 2%* 1%*

No Exemption Limit

6CF Parking Lot 2% 2.5%* 2%* 1%*

No Exemption Limit

Alcholic Liquor For Human Consumption

Timber obtained Under a Forest Leade

Timber obtained (other than Forest)

Forest Produce (other than Tendu Leaves)

6CG Toll plaza 2% 2.5%* 2%* 1%*

No Exemption Limit

6CH Mining And Quarrying 2% 2.5%* 2%* 1%*

No Exemption Limit

6CJ 1% 2.5%* 2%* 1%*

6CK

Bullion or jewellery

1% 2.5%* 2%* 1%*

* Note: For Non Salary and TCS

Minerals, being coal or lignite or iron ore

No Exemption Limit (w.e.f 1st July 2012)

Rs. 200000/- in case of BullionRs. 100000/- in case of Jewellery(w.e.f 1st July 2012)

* For the purpose of Tax Deduction/Collection Surcharge, Education Cess and Secondary And Higher Cess is not required to deduct/Collect if Payment made/Collected to Resident and for other than Salary. In case payment Made to Non Domestic Company than Surcharge (@2% If payment exceed from 1.00 Crore) Required to be Deducted* In case payment made to Non Resident , Education Cess And Secondary And Higher Cess required to be Deducted/Collected.

AY 2014 -2015

INDIVIDUAL other then Senior citizen or very senior citizen

INCOME SLAB TAX

Upto Rs. 200000 NIL NIL NIL

Rs. 200000 to Rs. 500000 10% of (total income - Rs. 200000) NIL 2%

Rs. 500000 to Rs. 1000000 Rs. 30000 + 20% of (total income - Rs. 500000) NIL 2%

Above 1000000 Rs. 130000 + 30% of (total income - Rs. 1000000) 10% 2%

INDIVIDUAL (SENIOR CITIZEN)

Upto Rs. 250000 NIL NIL NIL

Rs. 250000 to Rs. 500000 10% of (total income - Rs. 250000) NIL 2%

Rs. 500000 to Rs. 1000000 Rs. 25000 + 20% of (total income - Rs. 500000) NIL 2%

Above Rs 1000000 Rs. 125000 + 30% of (total income - Rs. 1000000) 10% 2%

INDIVIDUAL (VERY SENIOR CITIZEN)

Upto Rs. 500000 NIL NIL NIL

Rs. 500000 to Rs. 1000000 20% of (total income - Rs. 500000) NIL 2%

Above Rs 1000000 Rs. 100000 + 30% of (total income - Rs. 1000000) 10% 2%

Rebate U/S 87A, Where Total Income does not Exceed Rs. 500000/- Lower of the Following

1 Tax Payable2 2000/-

SURCHARGE ( Total Income

Exceed Rs. 1 Crore)

EDU. CESS

AY 2014 -2015

INDIVIDUAL other then Senior citizen or very senior citizen

NIL

1%

1%

1%

INDIVIDUAL (SENIOR CITIZEN)

NIL

1%

1%

1%

INDIVIDUAL (VERY SENIOR CITIZEN)

NIL

1%

1%

HIGHER EDU. CESS

DESCRIPTION

AY 2014-2015

TAX EDU. CESS

193 Interest on securities 10% 0% 0% 0%

194 Dividends 10% 0% 0% 0%

194A 10% 0% 0% 0%

194B 30% 0% 0% 0%

194BB 30% 0% 0% 0%

194C 0% 0% 0%

194D Insurance Commision 10% 0% 0% 0%194EE Deposits under NSS 20% 0% 0% 0%

194F 20% 0% 0% 0%

194G 10% 0% 0% 0%

194H 10% 0% 0% 0%

194I Rent 0% 0% 0%

194IA 1% 0% 0% 0%

194J 10% 0% 0% 0%

194LA 10% 0% 0% 0%

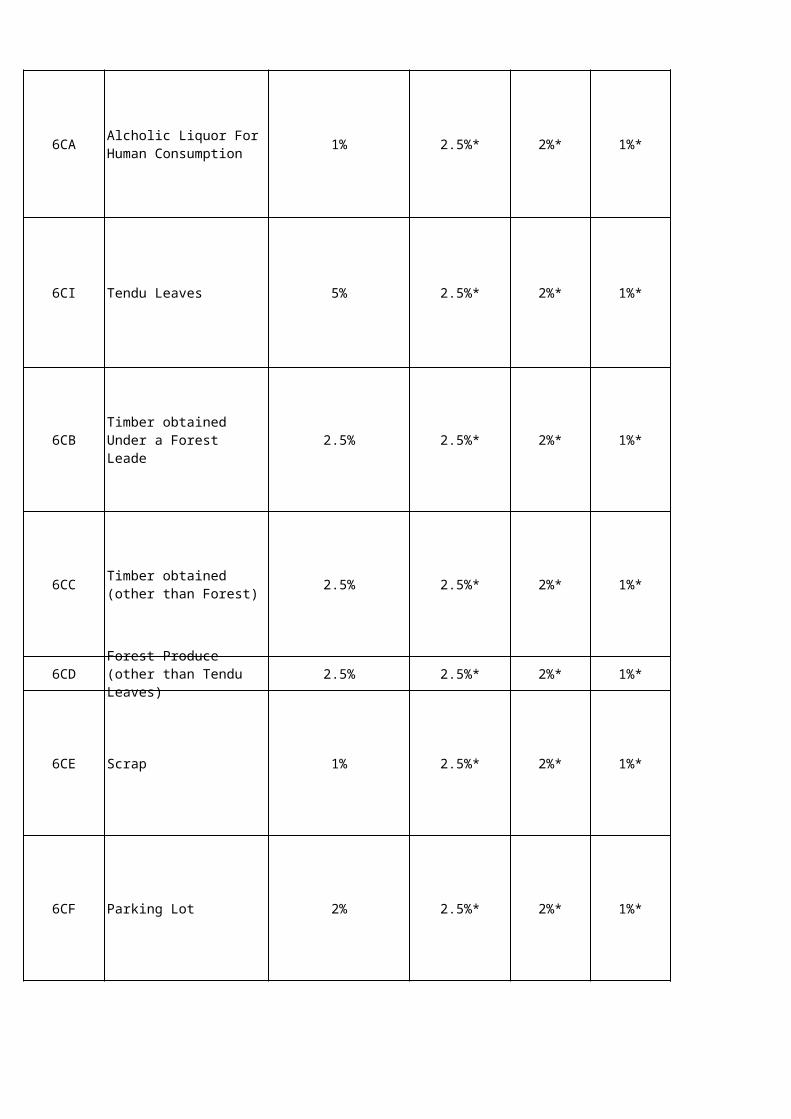

6CA 1% 2%* 2%* 1%*

6CI Tendu Leaves 5% 2%* 2%* 1%*

6CB 2.5% 2%* 2%* 1%*

6CC 2.5% 2%* 2%* 1%*

6CD 2.5% 2%* 2%* 1%*

6CE Scrap 1% 2%* 2%* 1%*6CF Parking Lot 2% 2%* 2%* 1%*

SECTION CODE

SUCHARGE (Only Non Domestic Company)

HIGHER EDU. CESS

Interest other than Interest on Securities

Winning from Lottery or Crossword Puzzle

Winning from Race Horse

Payment to Contractor and Sub- Contractors

1% (in Case of Individual and

Huf) /In other Case 2%

Repurchase of Units by Mutual Fund or UTI

Commission on sale of Lottery Tickets

Commision or Brokerage

a) 2% in Case of Rent of P&M b) In other Case it is 10%

Payment to a Resident Transferor for transfer of any immovable property (Applicable from june 1,2013

Fees for Professional or Technical Services

Compensation on acquisition of immovable property

Alcholic Liquor For Human Consumption

Timber obtained Under a Forest Leade

Timber obtained (other than Forest)

Forest Produce (other than Tendu Leaves)

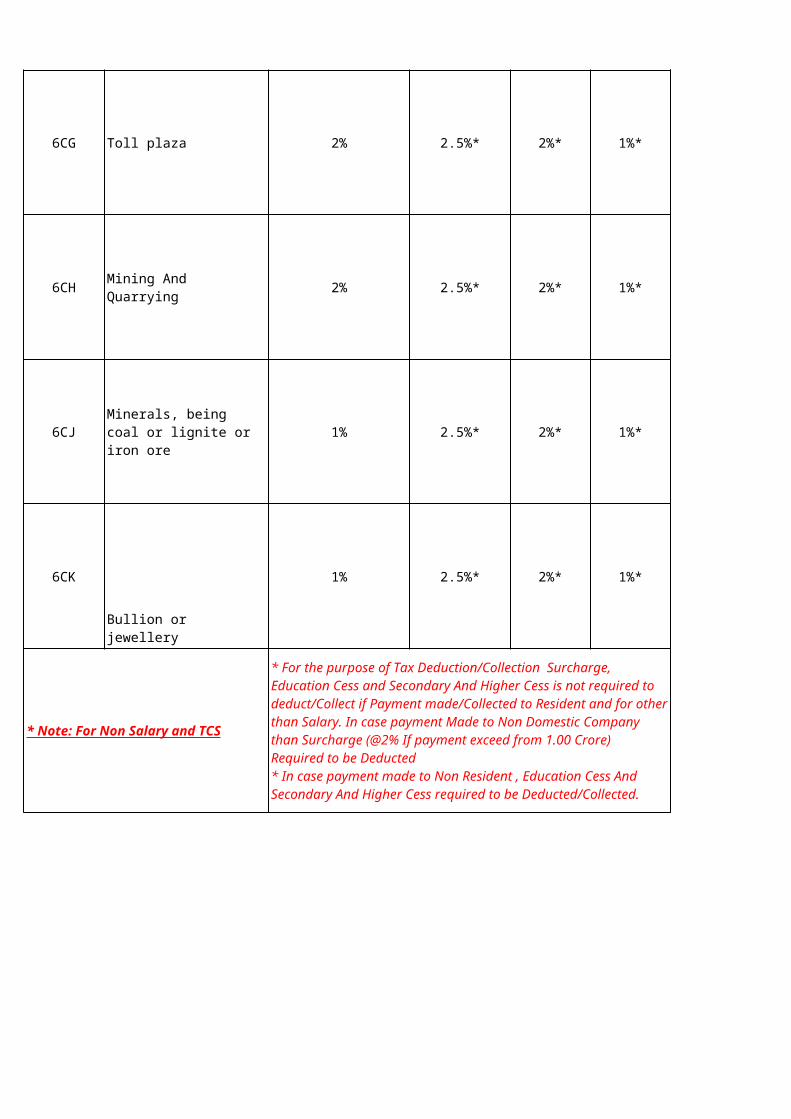

6CG Toll plaza 2% 2%* 2%* 1%*6CH Mining And Quarrying 2% 2%* 2%* 1%*

6CJ 1% 2%* 2%* 1%*

6CK Bullion or jewellery 1% 2%* 2%* 1%*

* Note: For Non Salary and TCS

Minerals, being coal or lignite or iron ore

* For the purpose of Tax Deduction/Collection Surcharge, Education Cess and Secondary And Higher Cess is not required to deduct/Collect if Payment made/Collected to Resident and for other than Salary. In case payment Made to Non Domestic Company than Surcharge (@2% If payment exceed from 1.00 Crore but not Exceed 10 Crore, In case Payment Exceed From 10 Crore than rate of Surcharge will be @5%) Required to be Deducted* In case payment made to Non Resident, Surcharge (@10% when Payment exceed Rs. 1 Crore) , Education Cess And Secondary And Higher Cess required to be Deducted/Collected.

AY 2014-2015

Limit for Tax Deduction

Rs. 10000

Rs. 5000

Rs. 20000Rs. 2500

Rs. 1000

Rs. 5000

Rs. 180000

Rs. 5000000

Rs. 30000

No Exemption LimitNo Exemption Limit

No Exemption Limit

No Exemption Limit

No Exemption LimitNo Exemption LimitNo Exemption Limit

Rs. 2500 (Rs. 5000/- From 1st July , 2012)

Rs. 2500 (No Tax to be Deducted if DDT Has been Paid U/s 115-O)

Banking Company / Co-operative society / Post Office- Rs. 10000 Others - Rs. 5000

Rs. 30000 in a single payment or Rs. 75000 in aggregate

Rs. 100000 (Increased to Rs. 200000/- W.e.f

01/07/2012)

No Exemption LimitNo Exemption Limit

No Exemption Limit (Effective on or after 1st

July, 2012)

Exemption limit 100000/- (effective on or after 1st

July, 2012)

AY 2015-2016

INDIVIDUAL other then Senior citizen or very senior citizen

INCOME SLAB TAX

Upto Rs. 250000 NIL NIL NIL

Rs. 250000 to Rs. 500000 10% of (total income - Rs. 250000) NIL 2%

Rs. 500000 to Rs. 1000000 Rs. 25000 + 20% of (total income - Rs. 500000) NIL 2%

Above 1000000 Rs. 125000 + 30% of (total income - Rs. 1000000) 10% 2%

INDIVIDUAL (SENIOR CITIZEN)

Upto Rs. 300000 NIL NIL NIL

Rs. 300000 to Rs. 500000 10% of (total income - Rs. 300000) NIL 2%

Rs. 500000 to Rs. 1000000 Rs. 20000 + 20% of (total income - Rs. 500000) NIL 2%

Above Rs 1000000 Rs. 120000 + 30% of (total income - Rs. 1000000) 10% 2%

INDIVIDUAL (VERY SENIOR CITIZEN)

Upto Rs. 500000 NIL NIL NIL

Rs. 500000 to Rs. 1000000 20% of (total income - Rs. 500000) NIL 2%

Above Rs 1000000 Rs. 100000 + 30% of (total income - Rs. 1000000) 10% 2%

Rebate U/S 87A, Where Total Income does not Exceed Rs. 500000/- Lower of the Following

1 Tax Payable2 2000/-

SURCHARGE ( Total Income

Exceed Rs. 1 Crore)

EDU. CESS

AY 2015-2016

INDIVIDUAL other then Senior citizen or very senior citizen

NIL

1%

1%

1%

INDIVIDUAL (SENIOR CITIZEN)

NIL

1%

1%

1%

INDIVIDUAL (VERY SENIOR CITIZEN)

NIL

1%

1%

HIGHER EDU. CESS

DESCRIPTION

AY 2015-2016

TAX EDU. CESS

193 Interest on securities 10% 0% 0% 0%

194 Dividends 10% 0% 0% 0%

194A 10% 0% 0% 0%

194B 30% 0% 0% 0%

194BB 30% 0% 0% 0%

194C 0% 0% 0%

194D Insurance Commision 10% 0% 0% 0%

194DA 2% 0% 0% 0%

194EE Deposits under NSS 20% 0% 0% 0%

194F 20% 0% 0% 0%

194G 10% 0% 0% 0%

194H 10% 0% 0% 0%

194I Rent 0% 0% 0%

194IA 1% 0% 0% 0%

194J 10% 0% 0% 0%

194LA 10% 0% 0% 0%

194LBA (1) 10% 0% 0% 0%

6CA 1% 2%* 2%* 1%*

SECTION CODE

SUCHARGE (Only Non Domestic Company)

HIGHER EDU. CESS

Interest other than Interest on Securities

Winning from Lottery or Crossword Puzzle

Winning from Race Horse

Payment to Contractor and Sub- Contractors

1% (in Case of Individual and

Huf) /In other Case 2%

Sum paid under a life insurance policy including Bonus

Repurchase of Units by Mutual Fund or UTI

Commission on sale of Lottery Tickets

Commision or Brokerage

a) 2% in Case of Rent of P&M b) In other Case it is 10%

Payment to a Resident Transferor for transfer of any immovable property (Applicable from june 1,2013

Fees for Professional or Technical Services

Compensation on acquisition of immovable property

Distributed Income referred to in section 115UA

Alcholic Liquor For Human Consumption

6CI Tendu Leaves 5% 2%* 2%* 1%*

6CB 2.5% 2%* 2%* 1%*

6CC 2.5% 2%* 2%* 1%*

6CD 2.5% 2%* 2%* 1%*

6CE Scrap 1% 2%* 2%* 1%*6CF Parking Lot 2% 2%* 2%* 1%*6CG Toll plaza 2% 2%* 2%* 1%*6CH Mining And Quarrying 2% 2%* 2%* 1%*

6CJ 1% 2%* 2%* 1%*

6CK Bullion or jewellery 1% 2%* 2%* 1%*

* Note: For Non Salary and TCS

Timber obtained Under a Forest Leade

Timber obtained (other than Forest)

Forest Produce (other than Tendu Leaves)

Minerals, being coal or lignite or iron ore

* For the purpose of Tax Deduction/Collection Surcharge, Education Cess and Secondary And Higher Cess is not required to deduct/Collect if Payment made/Collected to Resident and for other than Salary. In case payment Made to Non Domestic Company than Surcharge (@2% If payment exceed from 1.00 Crore but not Exceed 10 Crore, In case Payment Exceed From 10 Crore than rate of Surcharge will be @5%) Required to be Deducted* In case payment made to Non Resident, Surcharge (@10% when Payment exceed Rs. 1 Crore) , Education Cess And Secondary And Higher Cess required to be Deducted/Collected.

AY 2015-2016

Limit for Tax Deduction

Rs. 10000

Rs. 5000

Rs. 20000

Rs. 100000

Rs. 2500

Rs. 1000

Rs. 5000

Rs. 180000

Rs. 5000000

Rs. 30000

No Exemption Limit

No Exemption Limit

Rs. 2500 (Rs. 5000/- From 1st July , 2012)

Rs. 2500 (No Tax to be Deducted if DDT Has been Paid U/s 115-O)

Banking Company / Co-operative society / Post Office- Rs. 10000 Others - Rs. 5000

Rs. 30000 in a single payment or Rs. 75000 in aggregate

Rs. 100000 (Increased to Rs. 200000/- W.e.f

01/07/2012)

No Exemption Limit

No Exemption Limit

No Exemption Limit

No Exemption LimitNo Exemption LimitNo Exemption LimitNo Exemption LimitNo Exemption Limit

No Exemption Limit (Effective on or after 1st

July, 2012)

Exemption limit 100000/- (effective on or after 1st

July, 2012)

AY 2016-2017

INDIVIDUAL other then Senior citizen or very senior citizen

INCOME SLAB TAX

Upto Rs. 250000 NIL NIL NIL

Rs. 250000 to Rs. 500000 10% of (total income - Rs. 250000) NIL 2%

Rs. 500000 to Rs. 1000000 Rs. 25000 + 20% of (total income - Rs. 500000) NIL 2%

Above 1000000 Rs. 125000 + 30% of (total income - Rs. 1000000) 12% 2%

INDIVIDUAL (SENIOR CITIZEN)

Upto Rs. 300000 NIL NIL NIL

Rs. 300000 to Rs. 500000 10% of (total income - Rs. 300000) NIL 2%

Rs. 500000 to Rs. 1000000 Rs. 20000 + 20% of (total income - Rs. 500000) NIL 2%

Above Rs 1000000 Rs. 120000 + 30% of (total income - Rs. 1000000) 12% 2%

INDIVIDUAL (VERY SENIOR CITIZEN)

Upto Rs. 500000 NIL NIL NIL

Rs. 500000 to Rs. 1000000 20% of (total income - Rs. 500000) NIL 2%

Above Rs 1000000 Rs. 100000 + 30% of (total income - Rs. 1000000) 12% 2%

Rebate U/S 87A, Where Total Income does not Exceed Rs. 500000/- Lower of the Following

1 Tax Payable2 2000/-

Rate of Surcharge is 12% where Total Income is more than 10000000/-

SURCHARGE ( Total Income

Exceed Rs. 1 Crore)

EDU. CESS

AY 2016-2017

INDIVIDUAL other then Senior citizen or very senior citizen

NIL

1%

1%

1%

INDIVIDUAL (SENIOR CITIZEN)

NIL

1%

1%

1%

INDIVIDUAL (VERY SENIOR CITIZEN)

NIL

1%

1%

HIGHER EDU. CESS

DESCRIPTION

AY 2016-2017

TAX EDU. CESS

192A 10% 0% 0% 0%

193 Interest on securities 10% 0% 0% 0%

194 Dividends 10% 0% 0% 0%

194A 10% 0% 0% 0%

194B 30% 0% 0% 0%

194BB 30% 0% 0% 0%

194C 0% 0% 0%

194D Insurance Commision 10% 0% 0% 0%194DASum paid under a life insurance policy including Bonus0.02 0 0 0194EE Deposits under NSS 20% 0% 0% 0%

194F 20% 0% 0% 0%

194G 10% 0% 0% 0%

194H 10% 0% 0% 0%

194I Rent 0% 0% 0%

194IA 1% 0% 0% 0%

194J 10% 0% 0% 0%

194LA 10% 0% 0% 0%

194LBA (1) 10% 0% 0% 0%

SECTION CODE

SUCHARGE (Only Non Domestic Company)

HIGHER EDU. CESS

Accumulated PF balance due to employees (Applicable from 01/06/2015)

Interest other than Interest on Securities

Winning from Lottery or Crossword Puzzle

Winning from Race Horse

Payment to Contractor and Sub- Contractors

1% (in Case of Individual and

Huf) /In other Case 2%

Repurchase of Units by Mutual Fund or UTI

Commission on sale of Lottery Tickets

Commision or Brokerage

a) 2% in Case of Rent of P&M b) In other Case it is 10%

Payment to a Resident Transferor for transfer of any immovable property (Applicable from june 1,2013

Fees for Professional or Technical Services

Compensation on acquisition of immovable property

Distributed Income referred to in section 115UA

194LBB 10% 0% 0% 0%

6CAAlcholic Liquor For Human Consumption 0.01 2%* 2%* 1%*6CI Tendu Leaves 5% 2%* 2%* 1%*

6CB 2.5% 2%* 2%* 1%*

6CC 2.5% 2%* 2%* 1%*

6CD 2.5% 2%* 2%* 1%*

6CE Scrap 1% 2%* 2%* 1%*6CF Parking Lot 2% 2%* 2%* 1%*6CG Toll plaza 2% 2%* 2%* 1%*6CH Mining And Quarrying 2% 2%* 2%* 1%*

6CJ 1% 2%* 2%* 1%*

6CK Bullion or jewellery 1% 2%* 2%* 1%*

* Note: For Non Salary and TCS

Income in respect of Units of an investment fund U/S 115UB

Timber obtained Under a Forest Leade

Timber obtained (other than Forest)

Forest Produce (other than Tendu Leaves)

Minerals, being coal or lignite or iron ore

* For the purpose of Tax Deduction/Collection Surcharge, Education Cess and Secondary And Higher Cess is not required to deduct/Collect if Payment made/Collected to Resident and for other than Salary. In case payment Made to Non Domestic Company than Surcharge (@2% If payment exceed from 1.00 Crore but not Exceed 10 Crore, In case Payment Exceed From 10 Crore than rate of Surcharge will be @5%) Required to be Deducted* In case payment made to Non Resident, Surcharge (@10% when Payment exceed Rs. 1 Crore) , Education Cess And Secondary And Higher Cess required to be Deducted/Collected.

AY 2016-2017

Limit for Tax Deduction

30000/-

Rs. 10000

Rs. 5000

Rs. 20000Rs. 100000

Rs. 2500

Rs. 1000

Rs. 5000

Rs. 180000

Rs. 5000000

Rs. 30000

No Exemption Limit

Rs. 2500 (Rs. 5000/- From 1st July , 2012)

Rs. 2500 (No Tax to be Deducted if DDT Has been Paid U/s 115-O)

Banking Company / Co-operative society / Post Office- Rs. 10000 Others - Rs. 5000

Rs. 30000 in a single payment or Rs. 75000 in aggregate

Rs. 100000 (Increased to Rs. 200000/- W.e.f

01/07/2012)

No Exemption Limit

No Exemption LimitNo Exemption Limit

No Exemption Limit

No Exemption Limit

No Exemption LimitNo Exemption LimitNo Exemption LimitNo Exemption LimitNo Exemption Limit

No Exemption Limit (Effective on or after 1st

July, 2012)

Exemption limit 100000/- (effective on or after 1st

July, 2012)

Related Documents