Report No. 5221-TO 5221 Togo° lssues and Optons M the Energy Sector June 1985 Report of the joint UNDP/World Bank Energy Sector Assessment IPrograrm This document hasa restricted distribution. Itscontentsmay not be disclosed without authorization from the Government, the UNDP or the WorMd Bank. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Welcome message from author

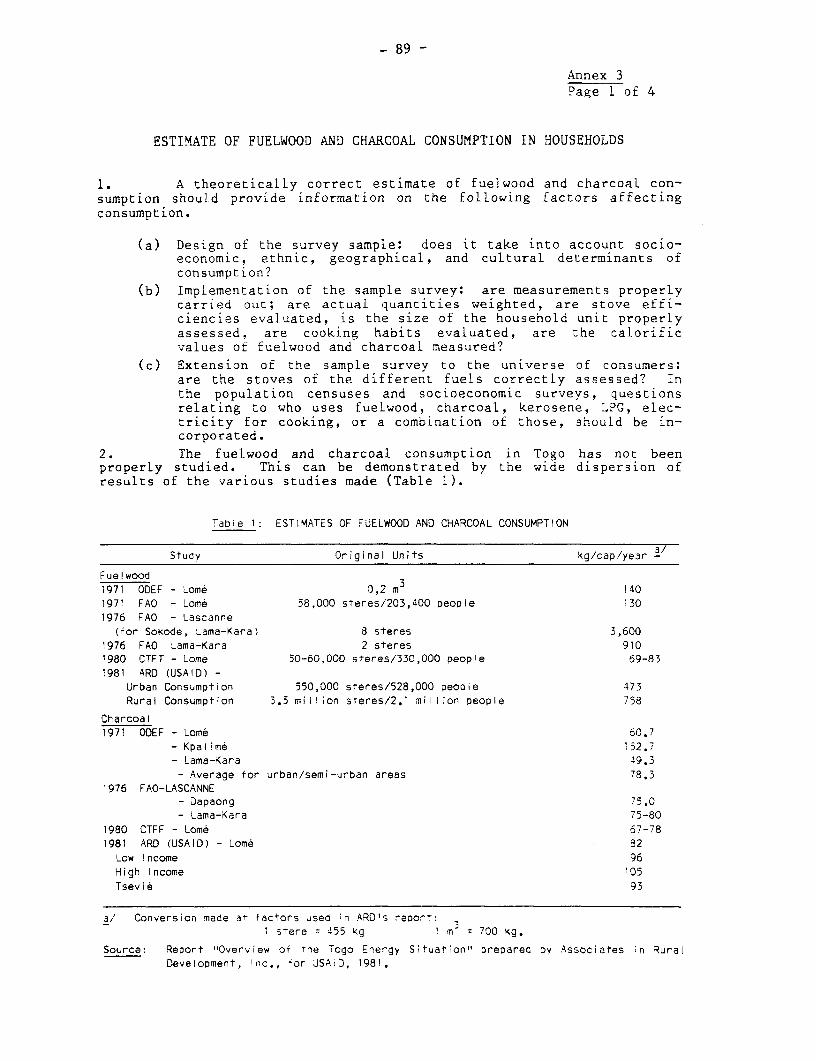

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

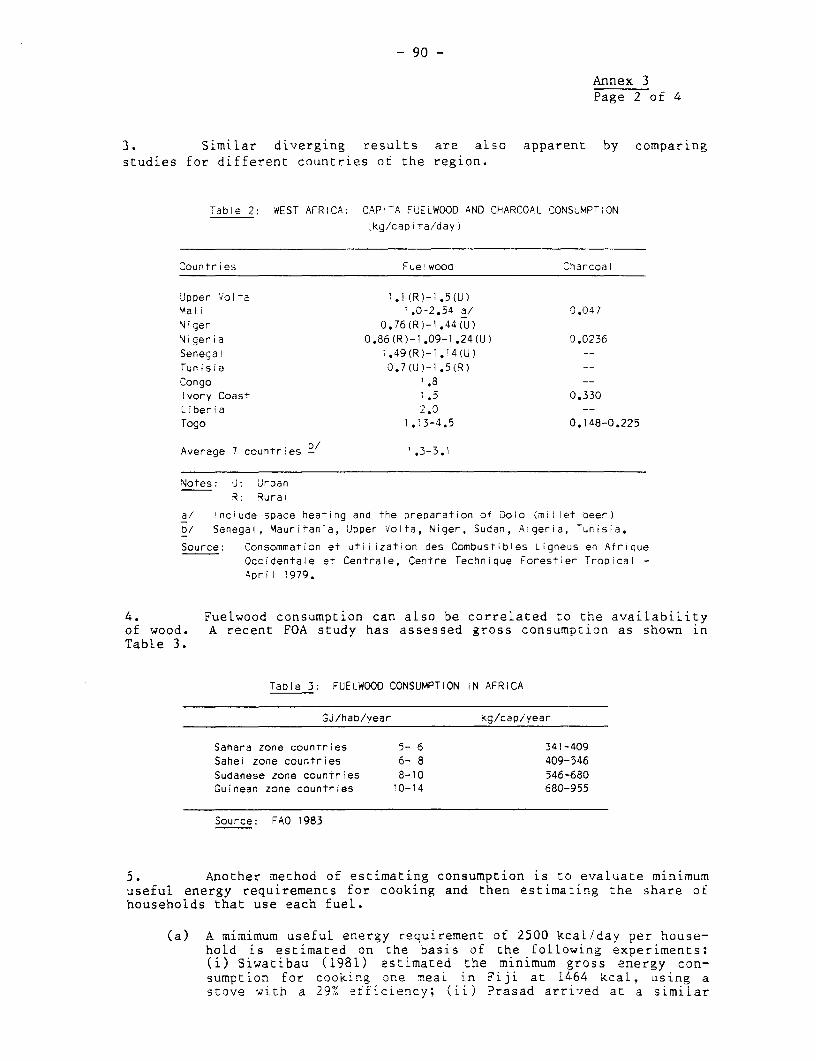

Transcript

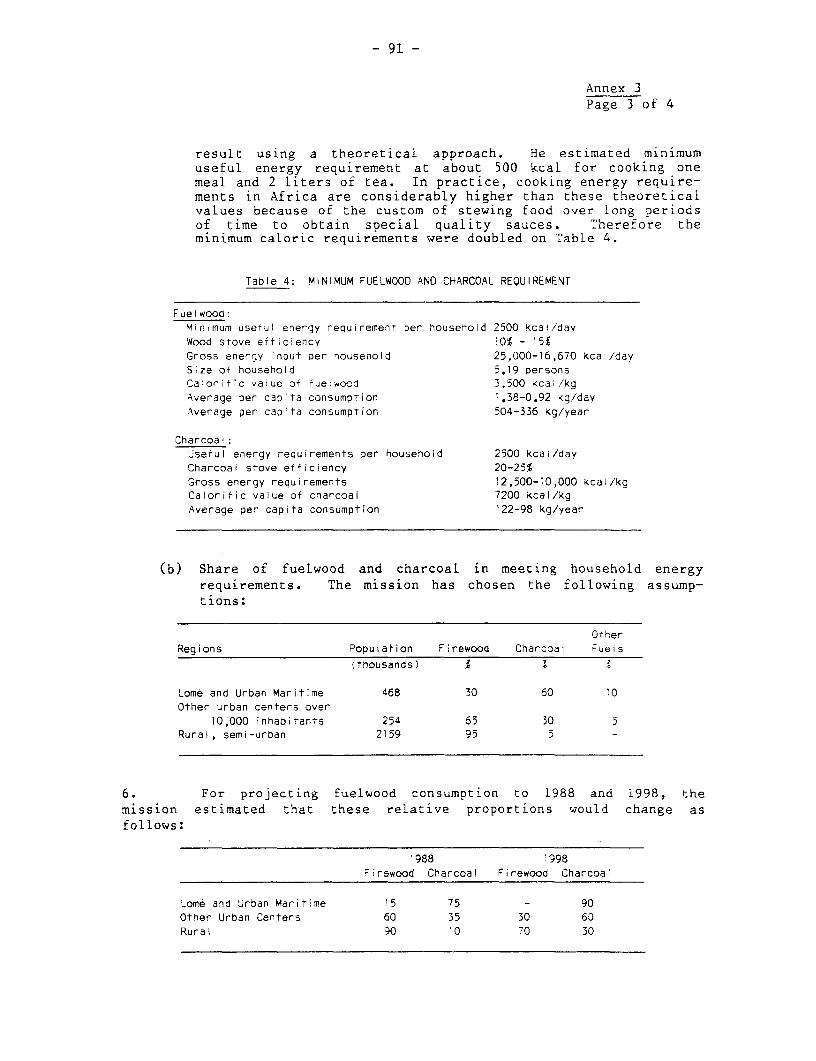

Report No. 5221-TO 5221Togo° lssues and OptonsM the Energy Sector

June 1985

Report of the joint UNDP/World Bank Energy Sector Assessment IPrograrmThis document has a restricted distribution. Its contents may not be disclosedwithout authorization from the Government, the UNDP or the WorMd Bank.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

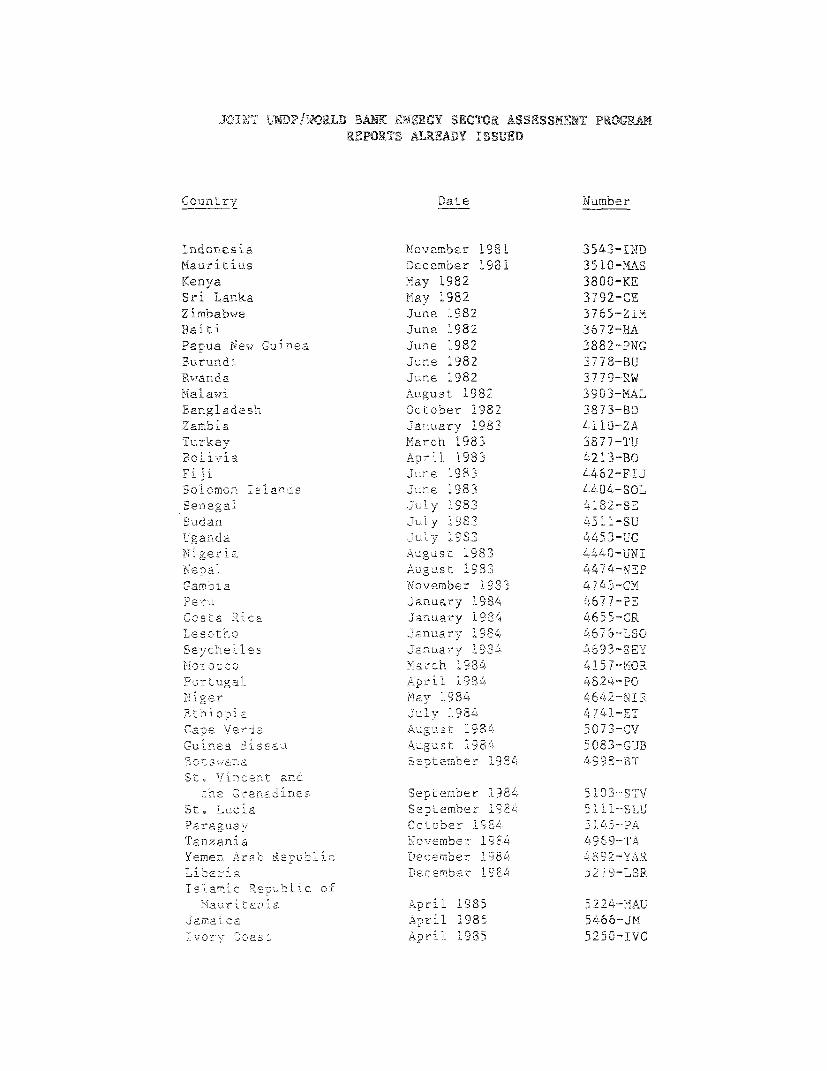

3'0IT U tDP/NAW D BANK RY SECTC-R ASS2SS sr PRORP

URPORTS ALREADY I S SED

Country Date Number

hndonesia November 1981 3543-I-NM

Mauritius December 1981 3510-MAS

Kenya May 1982 3800-KE

Sri Lanka May 1982 3792-CE

Zimbabwe June 1982 3765-ZIMT

Haiti June 1982 3672-HA

PaDua Ne., Guinea June 1982 3882-PNG

Burundi june 1982 3778-U

Rwanda June 1982 1779-RW

iata-wi Anuust 1938z 3903-MAT

Bangladesh October 1982 3873-BD

Zamib ia anuary 198 4;10-ZA

Turkey March 1983 3877-TU

3oI-via Apur 1933 4213-BO

Eiji iJune 1938 $462-FIJ

o0Lomon Islans June 1983 f494-SOLT

e a Ju ly 1.983 4i82 SE

udan July 1Q83 iSU

ganda July 983 44 5 'C

Ig L g eria August 19 83 4440-UN-

e 2 a August 1983 4T74 NEP

Ga 1ib I aG Novembeir 104ov7er

pe--u January 1984 677 -PE

osta nina January 19-34 465Y-CR

ct. r oanuary arh 1984 4657 MOR

Secvhen 12s fl-ay 1R 6g EHoroi Bi ~~~~Aprr 1, .,T. .. '

_Nitr g a L A P T 9 1 ; ,i 84A 4. 2 4- P-

2 .e-i .'i'j7 8 4 4.ii3's C, T i T

E C i pi-a cuL&- 198$ 4 499C741-ET

a V erde 'Alugust l3 03£

_U'. ea 35i_Algust !Q8iX 5_ 083 - '5U

Ste Vincsnt anl-le Cnref.-aines Serp eamber 198fT 5i93-ST-v

S L 2 S e p t e m"-LOer I S P SLfJ

Paragua- 'ac t obe-- . 154 PA

Tan z an i a 'o\vember 15.i, ' 4 569-TA

Yemen Ar-b RepJlin Decemnber '<a 8L 'o;I 2 -YARLibe. i- Decearber 1981 27 9 -LLR

Aiaurit :aO April 198,3 5224-A4A-U

Ja anl.a 2 April 1985 66J2-

T-jCoi._ o f g__ Apri 1985 5239-IVC

FOR OFFICIAL USE ONLY

Report No. 5221-TO

TOGO

ISSUES AND OPTIONS IN THE ENERGY SECTOR

JUNE 1985

This is one of the series of reports of the Joint UNDP/World Bank EnergySector Assessment Program. Finance for this work has been provided, inpart, by the UNDP Energy Account, and the work has been carried out bythe World Bank. This report has a restricted distribution. Its contentsmay not be disclosed without authorization from the Government, the UNDPor the World Bank.

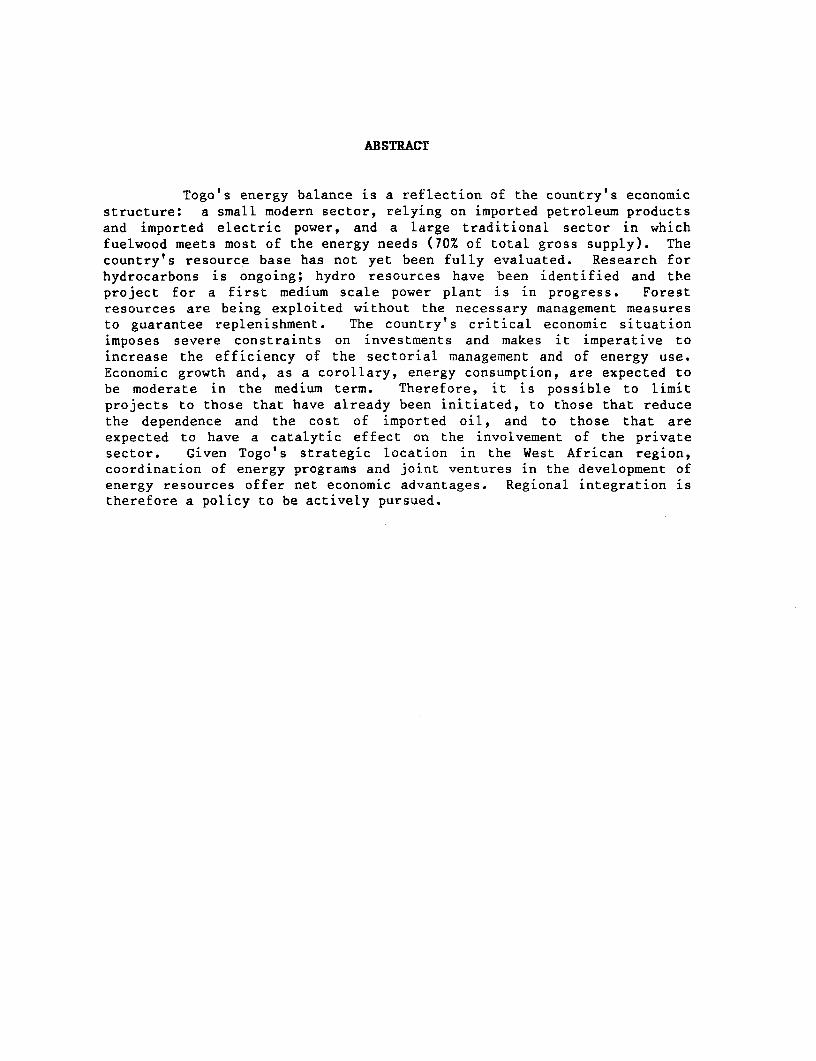

ABSTRACT

Togo's energy balance is a reflection of the country's economicstructure: a small modern sector, relying on imported petroleum productsand imported electric power, and a large traditional sector in whichfuelwood meets most of the energy needs (70% of total gross supply). Thecountry's resource base has not yet been fully evaluated. Research forhydrocarbons is ongoing; hydro resources have been identified and theproject for a first medium scale power plant is in progress. Forestresources are being exploited without the necessary management measuresto guarantee replenishment. The country's critical economic situationimposes severe constraints on investments and makes it imperative toincrease the efficiency of the sectorial management and of energy use.Economic growth and, as a corollary, energy consumption, are expected tobe moderate in the medium term. Therefore, it is possible to limitprojects to those that have already been initiated, to those that reducethe dependence and the cost of imported oil, and to those that areexpected to have a catalytic effect on the involvement of the privatesector. Given Togo's strategic location in the West African region,coordination of energy programs and joint ventures in the development ofenergy resources offer net economic advantages. Regional integration istherefore a policy to be actively pursued.

ABBREVIATIONS

b/d barrels per day

cal calorie

GDP Gross Domestic Product

GWh gigawatt hour (10 6/kWh)

ha hectare

k thousand

kcal thousand calories

kgoe kilogram of oil

equivalent

kWh kilowatt hour

LPG Liquid Petroleum Gas

(Butane)

M million

MCF thousand cubic feet

MWh megawatt hour (103 kWh)

,,3 cubic meter

toe tons of oil equivalent

This report reflects the conclusions of the energy assessment mission whichvisited Togo in June-July 1983. The mission was composed of Miss UrsulaWeimper (mission leader), and Messrs. E. Symonds (consultant, petroleumeconomist), L. Sayn-Wittgenstein (consultant, forest engineer), A Larreture(consultant, specialist in renewable energy applications), A. Streicher(consultant, energy conservation specialist), and J. Hatfield (consultant,electric energy economist). The mission also received the cooperation ofMr. M. Wilton of the Bank's regional power division. The text for the finalreport was processed by Ms. Norma Kraushaar.

ACRONYMS

ADB African Development BankAFME Agence Francaise de La Maitrise de l'EnergieARD Associates in Rural Development, Inc.BB Brasserie du BeninCEB Communaute Eiectrique de BeninCEET Compagnie d'Energie Electrique de TogoCTF Chemin de Fer TogolaiseCIMAO Societ6 des Ciments de l'Afrique de l'OuestCIMTOGO Ciment du TogoCTL Centrale Thermique de LomeDEF Direction des Productions ForestieresDGT Direction Generale des TransportsECOWAS Economic Community of West AfricaEEC European Economic CommunityESIE Ecole Superieure Interafricaine de l'ElectriciteFAO Organisation des Nations Unies Pour l'Alimentation

et l'AgricultureFED Fonds Europeens de D6veloppementGEMS Global Environmental Monitoring SystemsGPP Groupement Professionnel de PetroleNEPA Nigerian Electric Power AuthorityODEF Office pour le Developpement et l'Exploitation des

Ressources ForestieresOPAT Office des Produits Agricole du TogoOTP Office Togolais de PhosphatesRMTU R6gie Municipale des Transports UrbainesRNET Regie Nationale des Eaux de TogoSBEE Societe Beninoise d'Electricite et d'EauSFCE Services des Forets, Chasses et EnvironmentsSTE Societe Togolaise d'EntreposageSTH Societe Togolaise des HydrocarburesVRA Volta River AuthorityUSAID US Agency for International Development

CONVERSION FACTORS

Monetary: 50 FCFA = I FF

370 FCFA = I US$ (June 1983)

Energy:

Specific Net Calorific Oil

Gravity Value Equivalent

(kcal/kg) (toe/ton)

LPG 0.58 10,700 1.049

Gasoline - Super 0.721 10,500 1.029

- Regular 0.726 10,500 1.029

Kerosene 0.82 10,400 1.02

Gasoil/diesel 0.84 10,200 1.00

Fuel Oil - Light 0.93 9,900 0.97

- Heavy 0.96 9,600 0.94

Electricity - 28.5% efficiency 3,018 kWh 295.88/Gwh

- 100% efficiency 860 kWh 84.314/Gwh

Natural Gas 9,000 m3 0.880/1000 m3

Biogas 5,500 m3 0.539/1000 m3

Fuelwood

(cubic meter solid 25% MC) 0.7 3,500 0.343

Charcoal 7,000 0.686

Corncobs 3,500 0.343

Corn, rice, sorghum and

millet straw 2,500 0.245

Oil palm stems 1,300 0.127

Oil palm fibers 2,500 0.245

Oil palm hulls 4,000 0.392

Oil palm leaves 2,000 0.196

Cotton stalks 4,100 0.402

Cotton seed hulls 3,900 0.382

Groundnut hulls 4,000 0.392

Coffee hulls 3,700 0.363

Rice husks 3,000 0.294

Coconut hulls 4,300 0.422

TABLE OF CONTENTS

I. SUMMARY AND RECOMMENDATIONS0.. aa... aa..... .... 1Resource Development ............ a ... ..a ...... , e ... e a a , a 1

Forestry- .... ..... 2Agricultural Residues..a..ae.... oa.aaaaae .aaao,i .. cs. 3Commercial Energy Resources.e a9aa.aa e a .. a .so a,aaa..a 3Electricity .......................................... 3Petroleum . . . ................ 5.0.c.... 4Demand Management ...O... a.a.. . ...a .a.a.... 5Sector Policy Recommendations. a ... *a aaa..... a.a..aaaaa.. e 6

II. ENERGY AND THE ECONOMY .......... co*a,afa*a*ae@a*aaa*anese 7Economic Backgroundesa a a a ... a ...a a ...........a a a 7Energy Balance: Resources and Consumption ...... a 8

Demand Management by Economic Subsectors,aa-. ...... ,a 10

Household and Artisanal Energy Consumption .a.a a a....... a a 11

Price of Household Fuelsa......aaaaaaaaaaaaaaaaa ac.a. 13Recommendations for Energy Savings.000aaaaaaa a ... 0aa 15Industrial Energy Consumption .... a ... a a.a ....a a 16Conclusions and Recommendations. a e a9 aa a .. aaaa aa 19Energy Consumption in Hotels in Togogo... aa......a. 21Transport Energy Consumptiona . aaaaao aaaa oa 24Shift from Road to Railroadoa.aaaaa.aa*eaa oe.ea e aees 27Improved Efficiency within the Road Transport Mode..,. 28More Efficient Use of Existing Freight CarryingCapacityaaaaaaaaa ...aa e-aaaaa ...aas*a....... *.*a.. 29

Recommendations....aaaa,aaaaaaaaaaaaaaa.aaaaaaaaaa 31

rIII BIOMASS DEVELOPMENT OPTIONSa................aaa a aa*aaa *a0a 32General Situationaaa.aaaaa.asaaaaaaaaaaaea.a ... so.aa 32Inventory and Wood Growth Ratest... 949486464.....a 32Regional Supply-Demand Balance .......a..., 34Reforestation Projects. a a 35Reduction of Energy Losses in Charcoal Productionoo,.a 36Recommendations for a Forestry Strategy. .. ...a.a.O. 37

Agricultural Residues .... ....... a .......... a a a a 39Present Use of Residues. a a a a a a a 41Recommendationa.a.aaaaa...aa.aaa.ae .aaaa ....a.,.a... 41Solar Energya aa aa ... a ........ a aaaaaaa .a aa a aa aa 42

IV. PETROLEUM SECTOR ..............a a. aaaa aaaaaaaaa......... 43

Resource Evaluationa ae a ao aaaaaaa a ... a a. a 43Present and Projected Supplyas.a .............a........ 43Supply Cost and Prices ........a a a a a a a t a 45Oil Procurement Mechanism and Government Controls....a 46Petroleum Retail Prices a a a a 48

Import Cost Saving Opportunities .. ................. , 49Use of the Refinery's Storage Facilitiesa........a..a 49New Oil ProcurementArrangements .... a.aa........ 51Oil Substitution Opportunitiest .a. aae a...aa..a . .. aaa a 51

V. ELECTRIC POWER ............... .......... .................... . 54Role of Electricity ..................... *....... .O. .. 54Characteristics of Togo's Electric System...,......... 55

Interconnected Coastal System...... ..... .... ..... ... 57Togo Coastal System...,,*..,# ......... -............ 57Binational Coastal System (CEB) ............I.... ...... 61Binational Strategy-ooee.e..... ................,, 65

Inland Centers ......... . . .O - .... ... ..... ............ * 66Necessary Short-term Actions ............... ...0 ........ 67Specific Medium-term Issues .... 67Investments in the Inland Centers .......... I........... 69

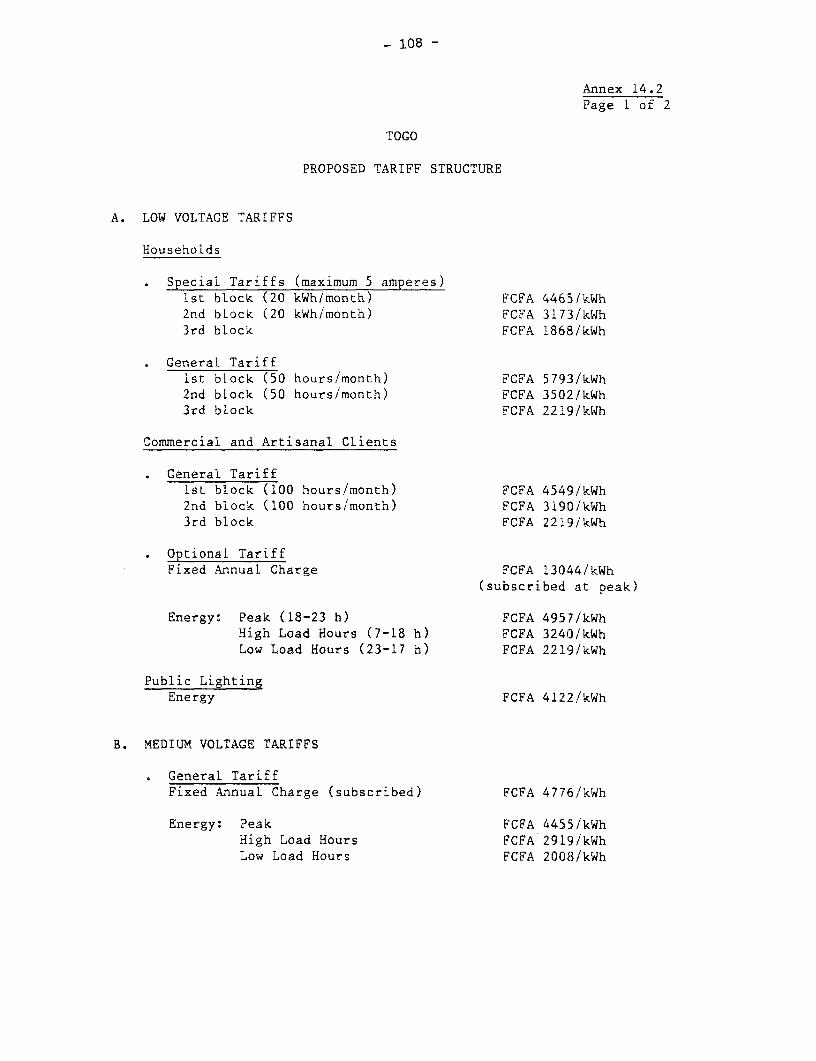

Tariffs* ..................................... 69CEB's Purchase and Sales Tariffs ............ Al .......... 69CEET's Tariffs ....... .................. S..0... 70

VI. INVESTMENTS, PLANNING AND TECHNICAL ASSISTANCE........... 72

Tr In vetmnts ............. ...... ... .. **........... ,.....,. 74

Energy Planning................ ...,......... S* 74Forestry Institutions......*.** ... ....... .......... 75Biomass and Nonconventional Renewable EnergyResources: Institutional Aspects ......... ........... 77

Petroleum Institutionsti.ou ti..n... ... ......... .. .. 77Electricity....e o t.0.0ct......y..-..........0-....... 78The Communaute Electrique du Benin (C E B ) 78Compagnie Energie Electrique de Togo...........o.. . 79Centrale Thermique de Lome (CTL) ......... 0..00.... 80Energy Conservationo..o..........................o. 80Industrial Energy Conservation............ o.. . 80Transport Sc.... 80Households, Cottage Industry, and Other Sectorsr...... 81

ANNEXES

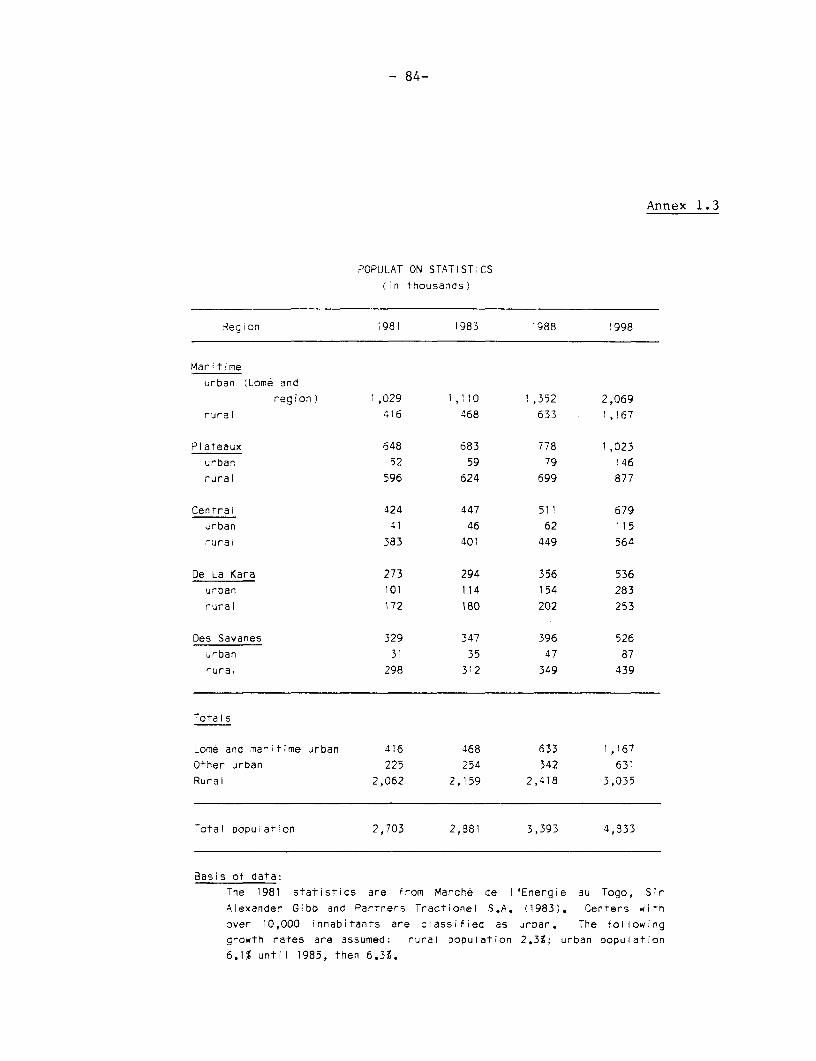

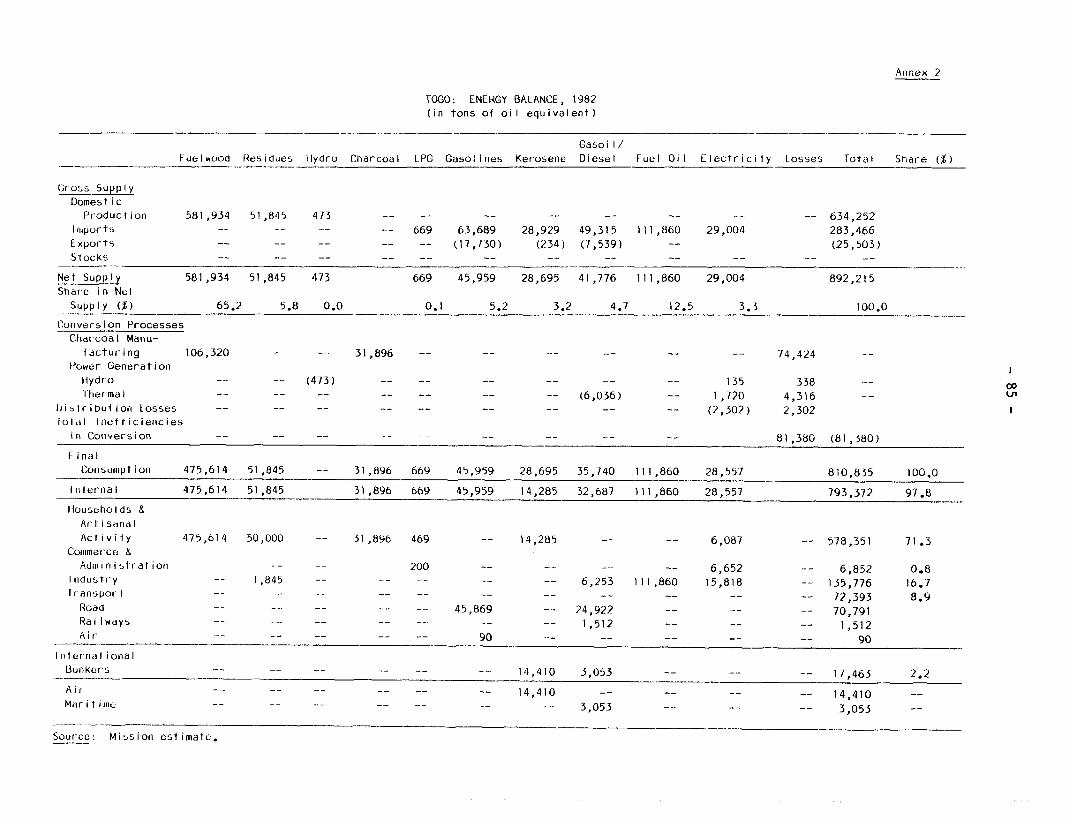

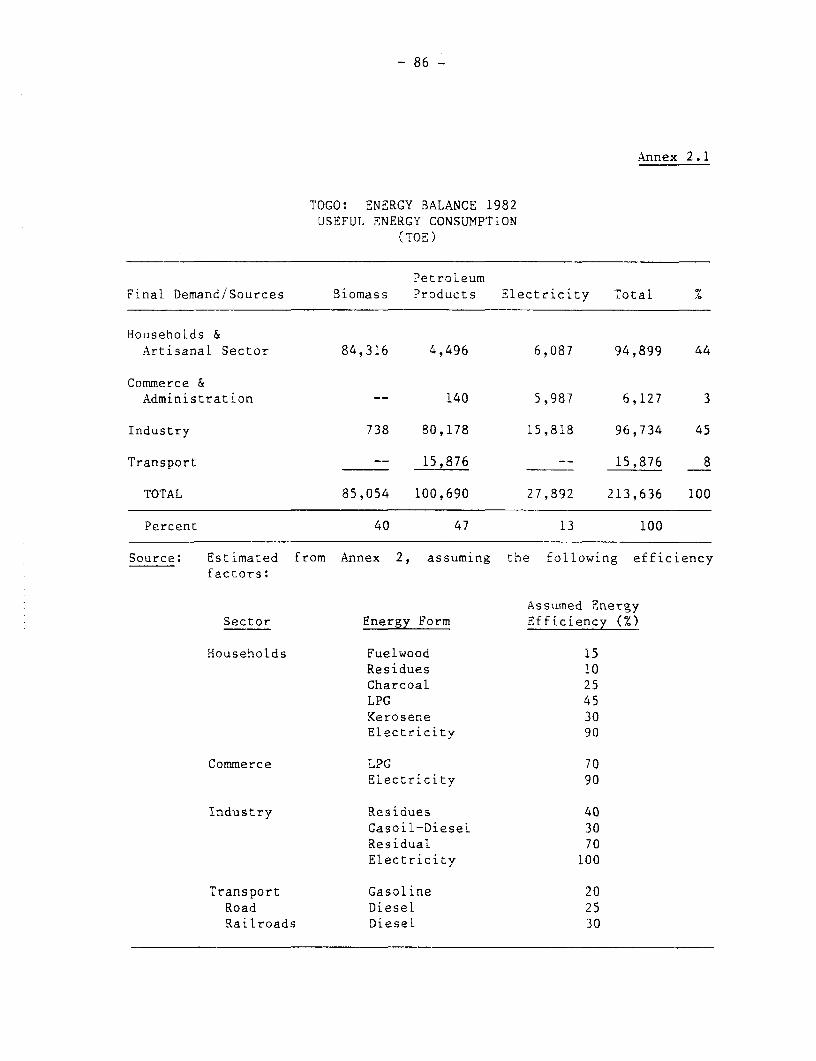

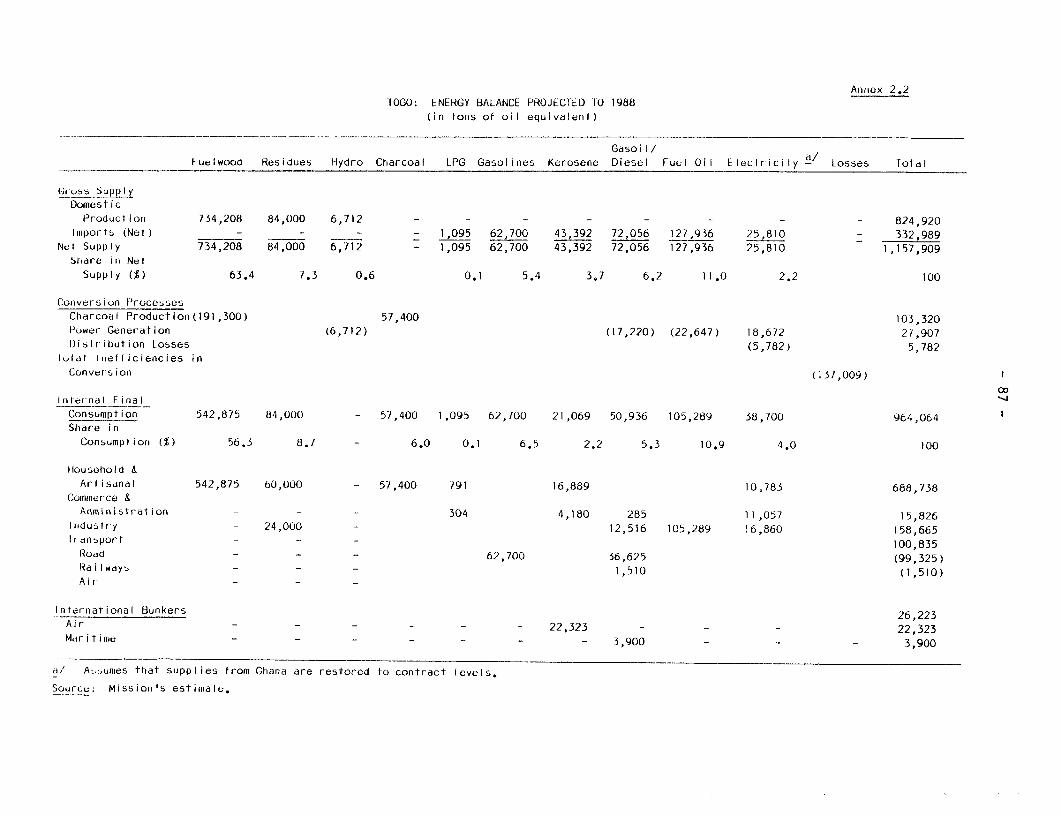

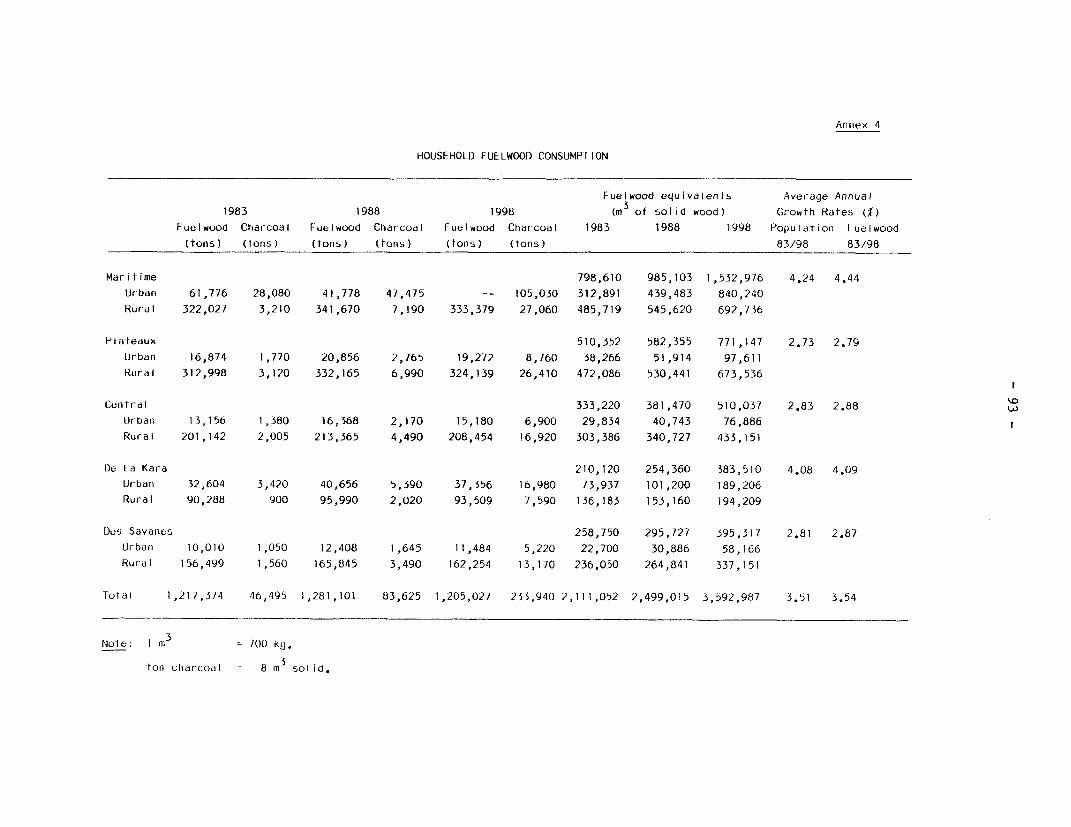

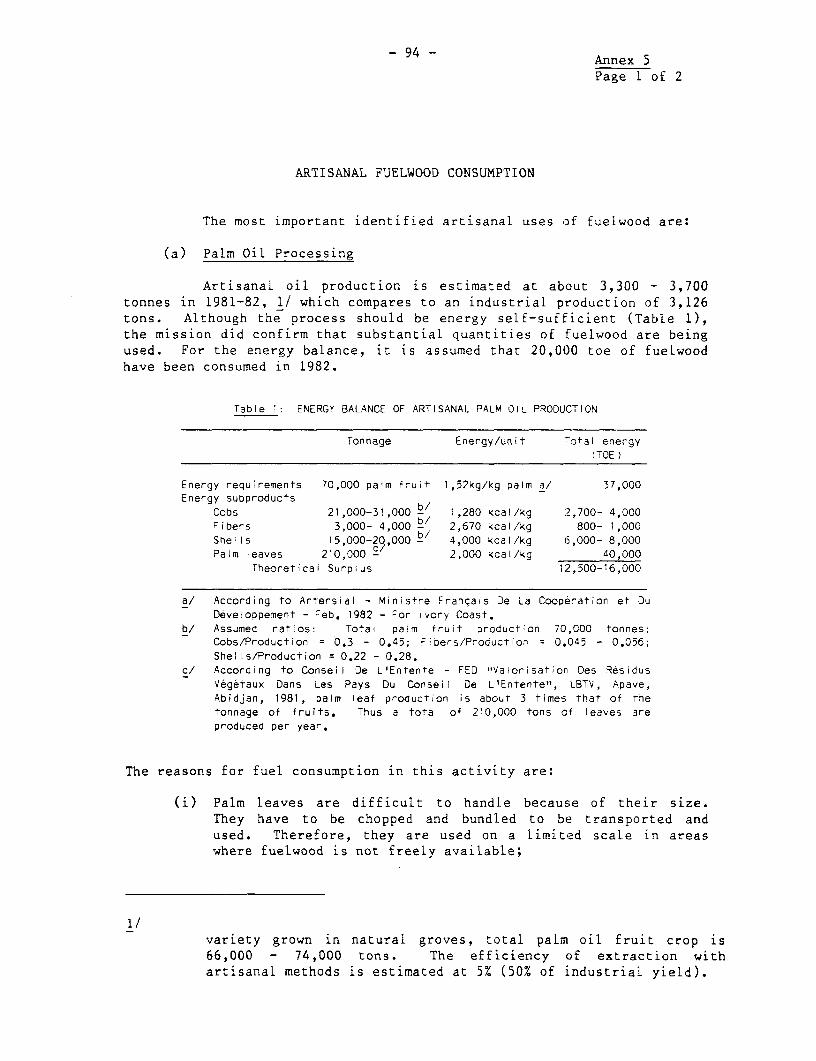

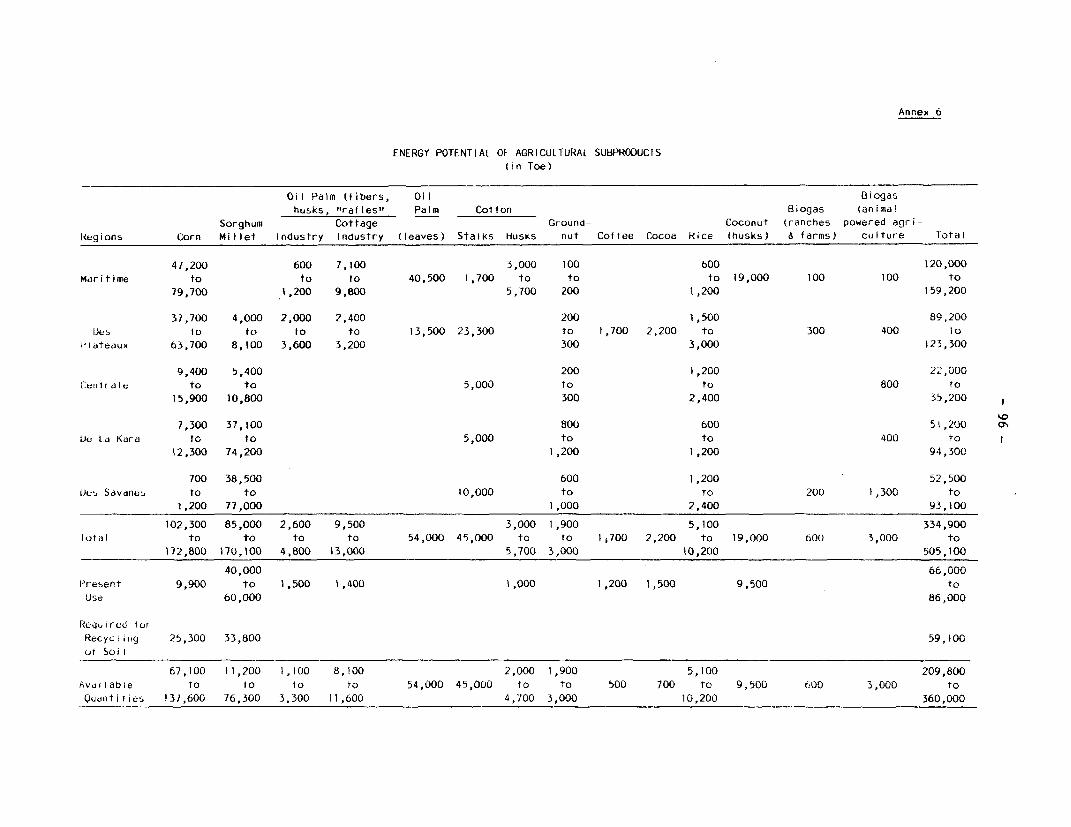

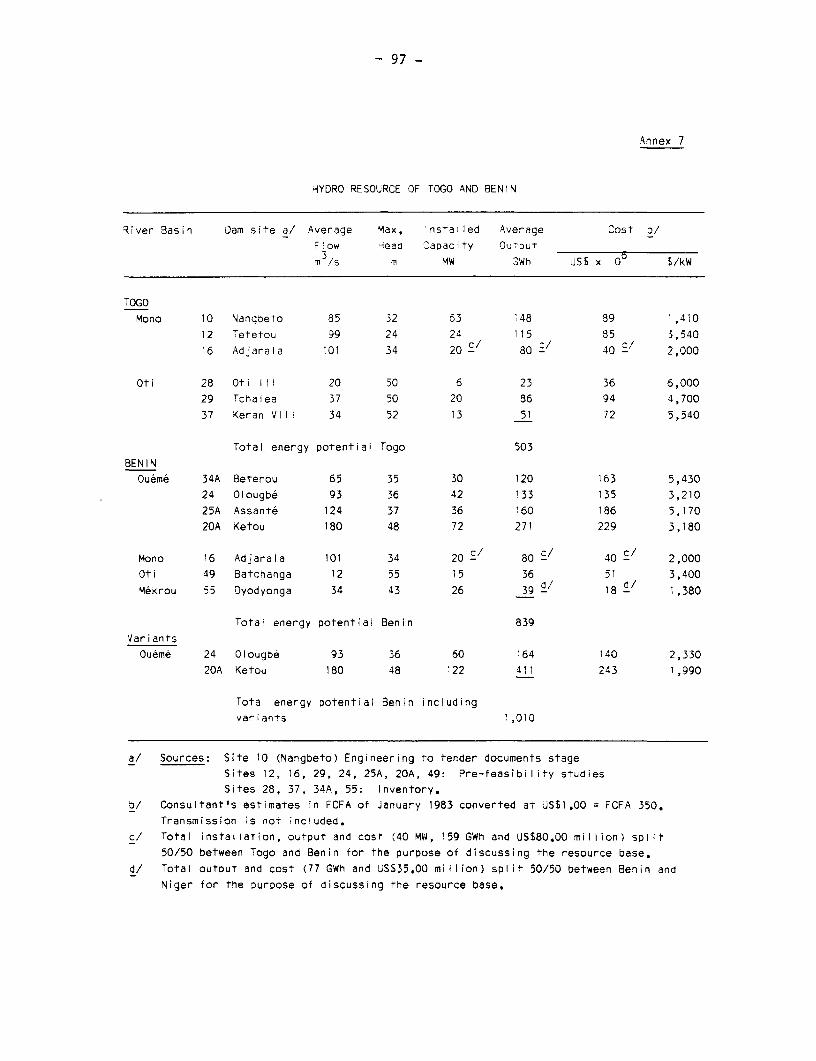

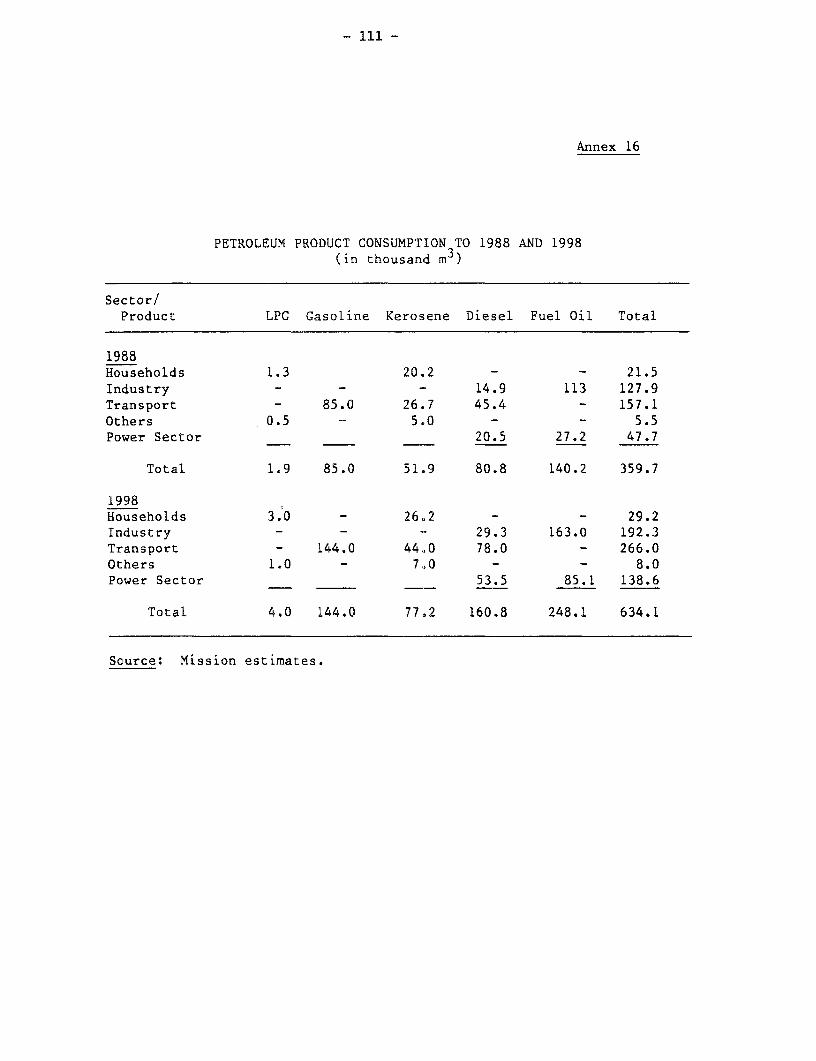

1,1 Population ........s . 821.2 Projected Population Growth Rateso.t.e s.... ............... 831.3 Population Statistics.,o.o.oo.oo...o................ ... ,. 842. Togo: Energy Balance, 1982, ................................ . 852.1 Togo: Energy Balance, 1982 - Useful Energy Consumption ... oo 862.2 Togo: Energy Balance Projected to 1988 ...............o...... 872.3 Togo: Energy Balance Projected to 1998 ..... o....... ,, .,6 883. Estimate of Fuelwood and Charcoal Consumption

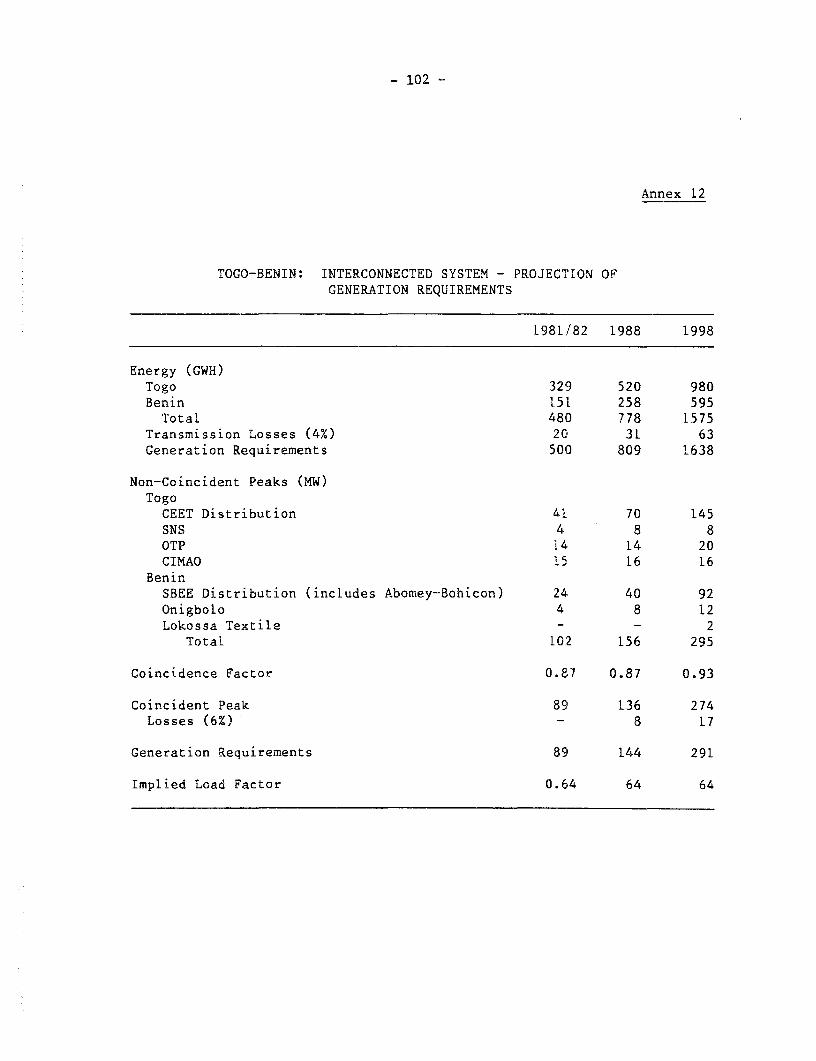

in Households ...................... 440....$ ....... 894. Household Fuelwood Consumption.............................. 935. Artisanal Fuelwood Consumption... ........................... 946. Energy Potential of Agricultural Subproducts................ 967. Hydro Resources of Togo and Benin ........ &6 ........ 978. Power Generation Capacity in Togo 989. Electric Power Supply, Historical Data ...................... 9910. Togo: Electric Demand Projections.....oo................ 10011. Benin: Electric Demand Projections , 10112. Interconnected System - Projection of Generation

Requirements...o ..............o.. o...............o.o.o 102

13.1 Togo: Inland Centers - Peak Demand and PresentInstalled Capacity ..................................................... 103

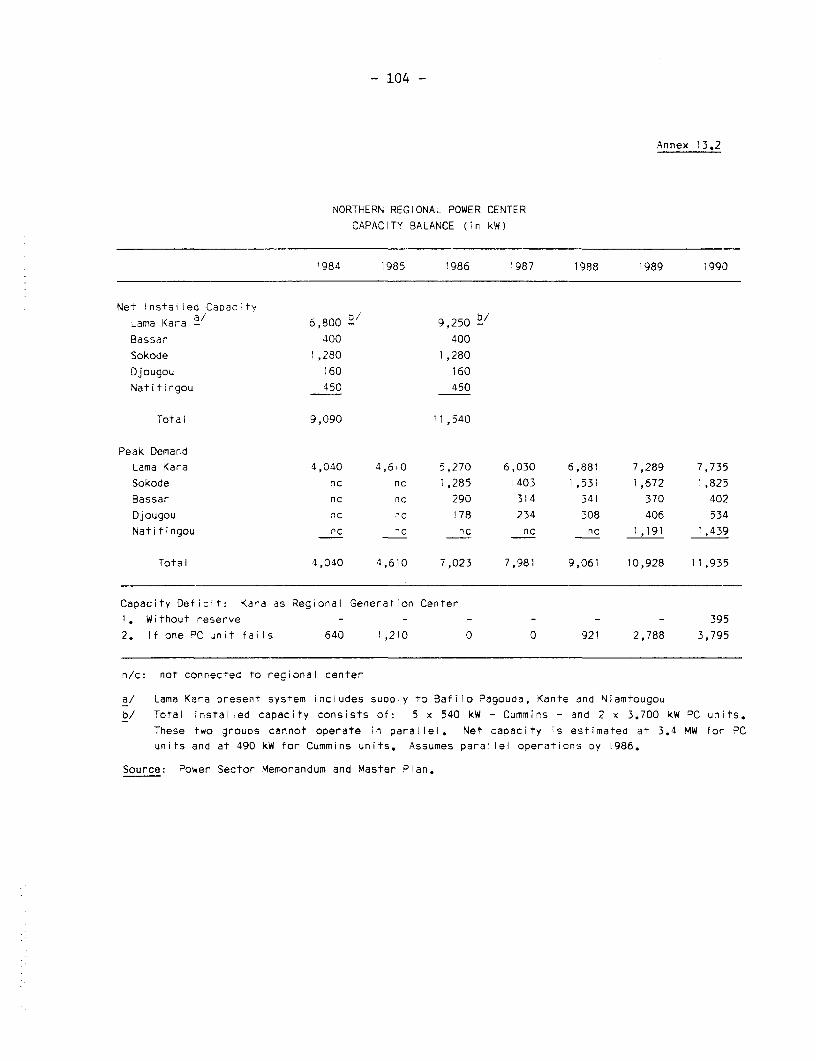

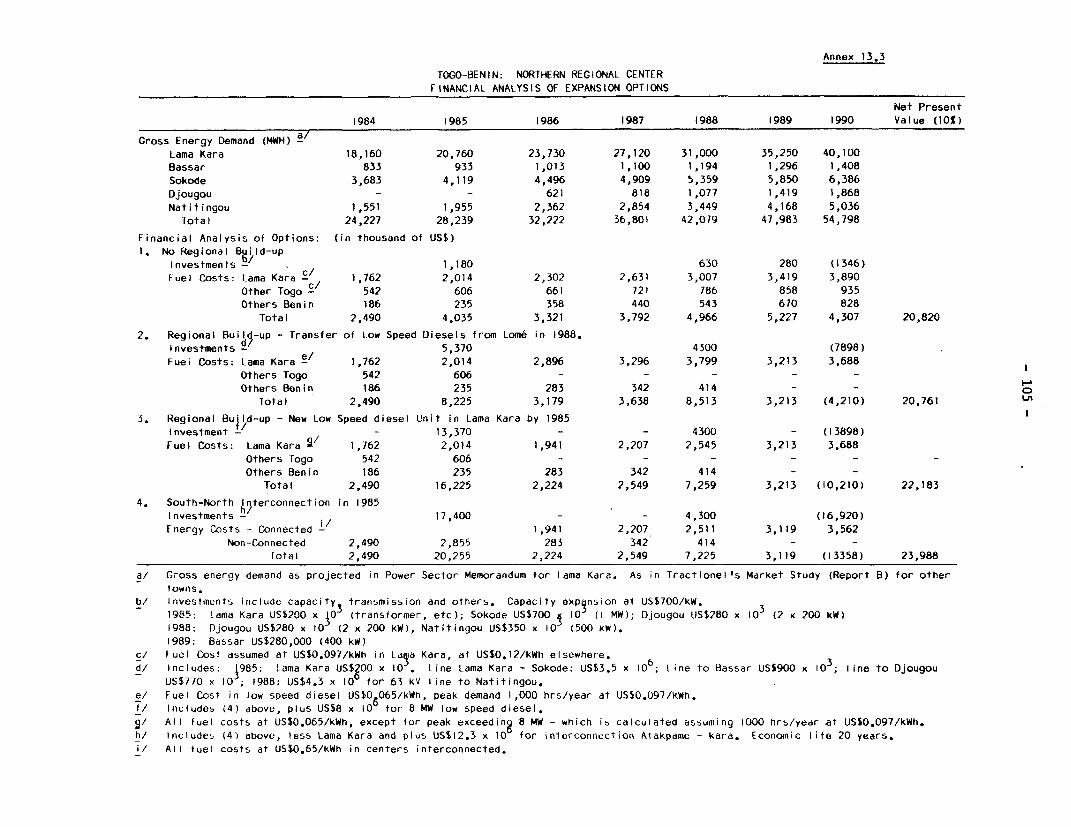

13.2 Northern Regional Power Center Capacity Balance ............ 10413.3 Togo-Benin: Northern Regional Center Financial

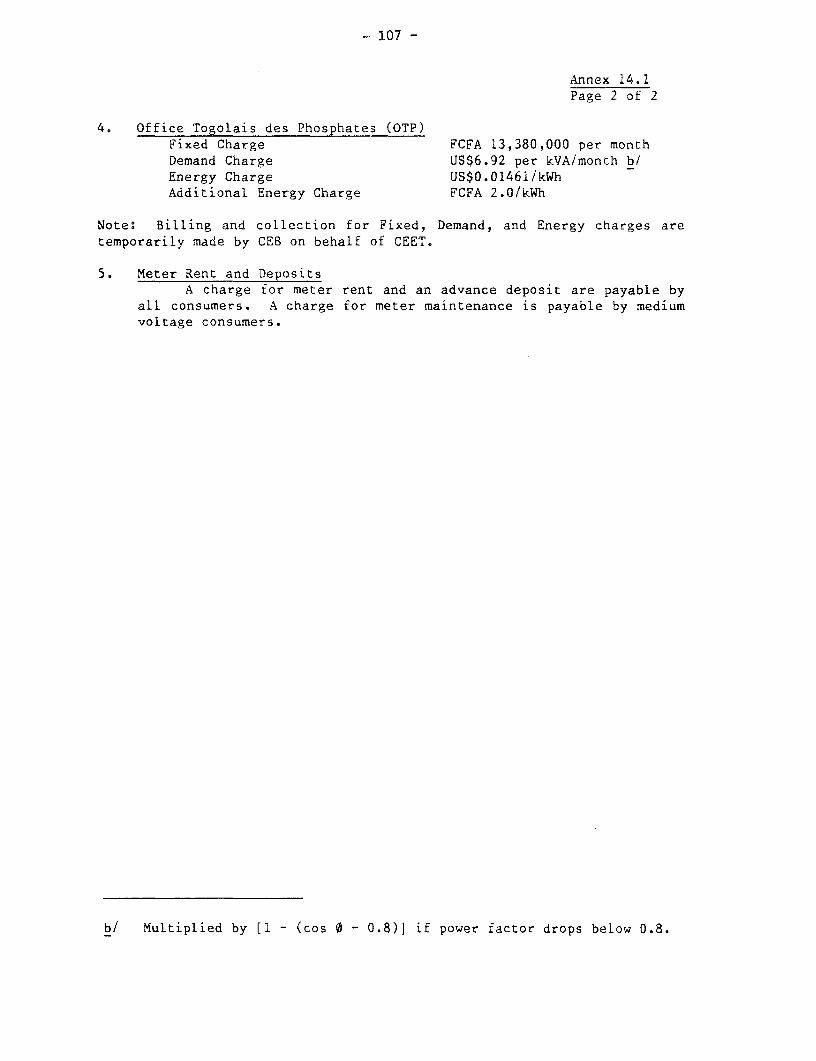

Analysis of Expansion Options ..................... 9.......9 10514.1 Togo: CEET-Existing Tariffs ........... .. ......... , 10614.2 Togo: Proposed Tariff Structure .. 10815. Petroleum Energy Product Sales .............................. 11016. Petroleum Product Consumption to 1988 and 1998 , 11117. Togo-Benin: Petroleum Requirements for

Power Generation .......................................... 11218. 1982: Petroleum Products - Demand of West African

Neighboring Countries. . ... ................. ....... ...... . 11319. West Africa - Petroleum Demand Projections to 1988:

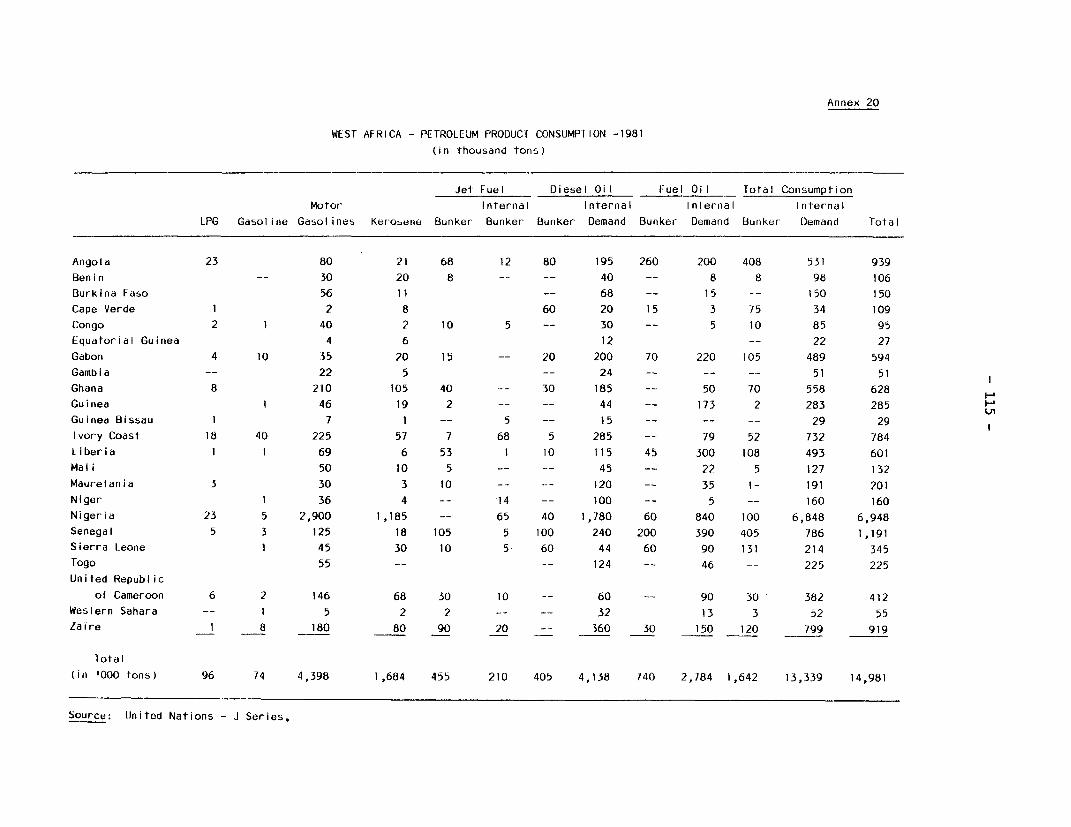

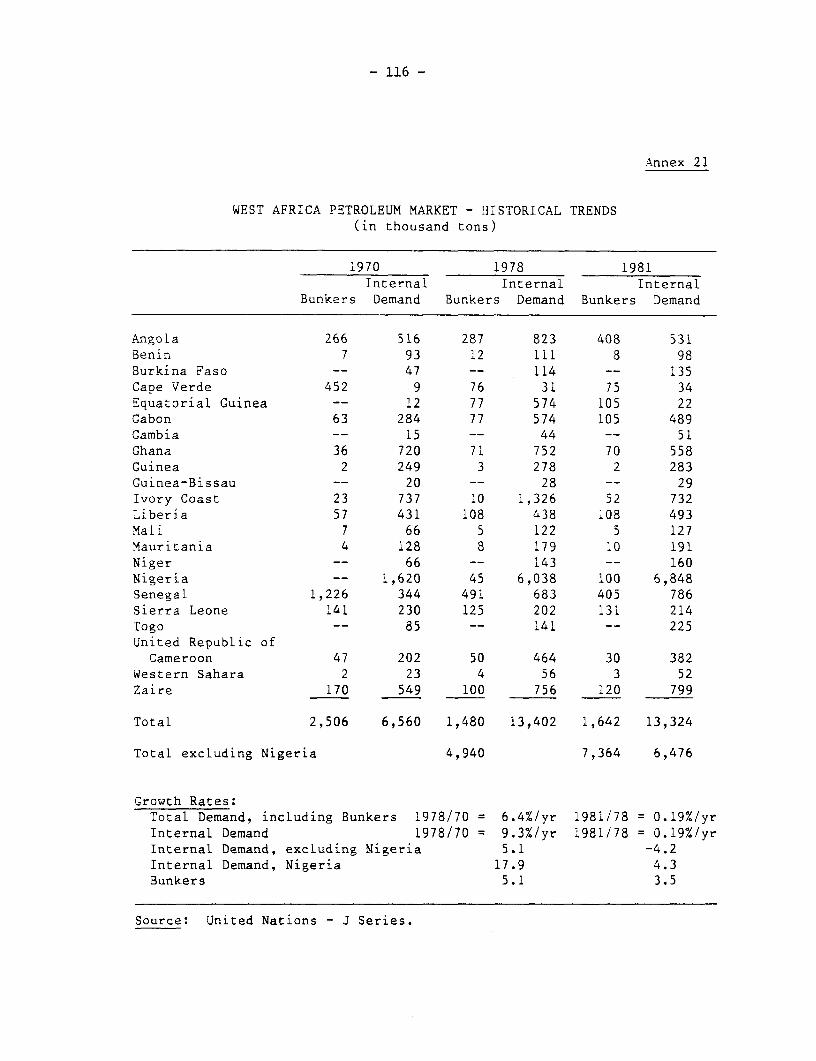

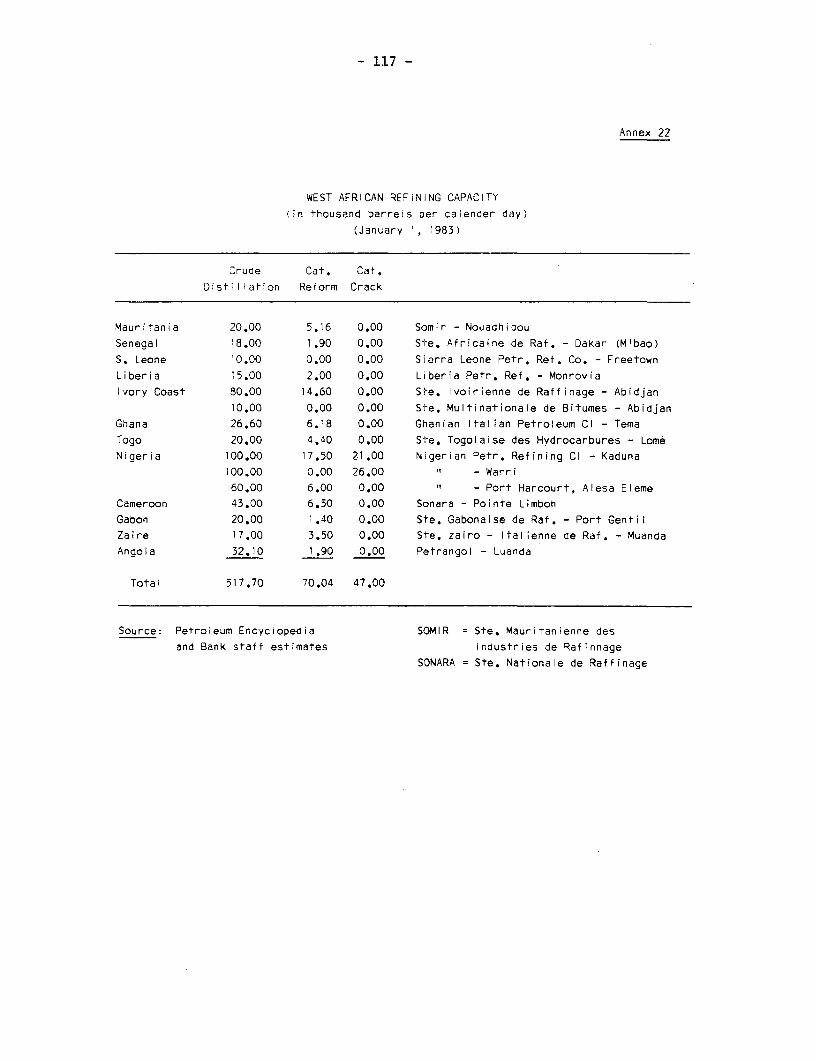

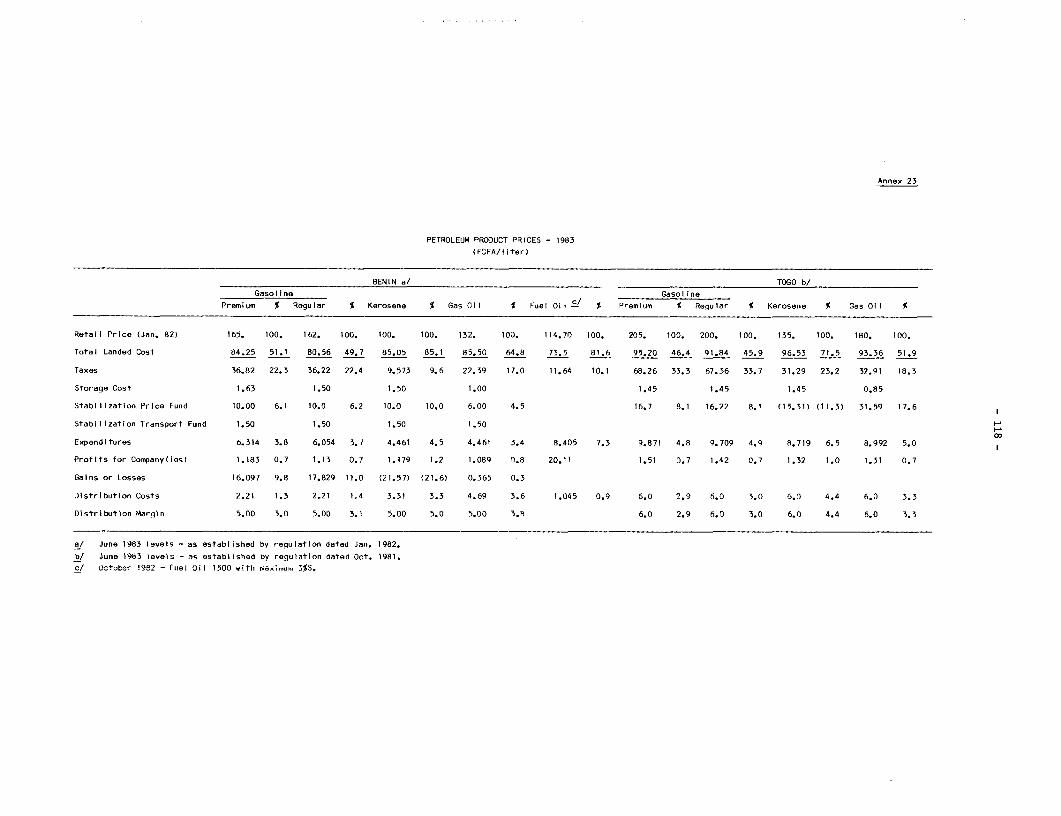

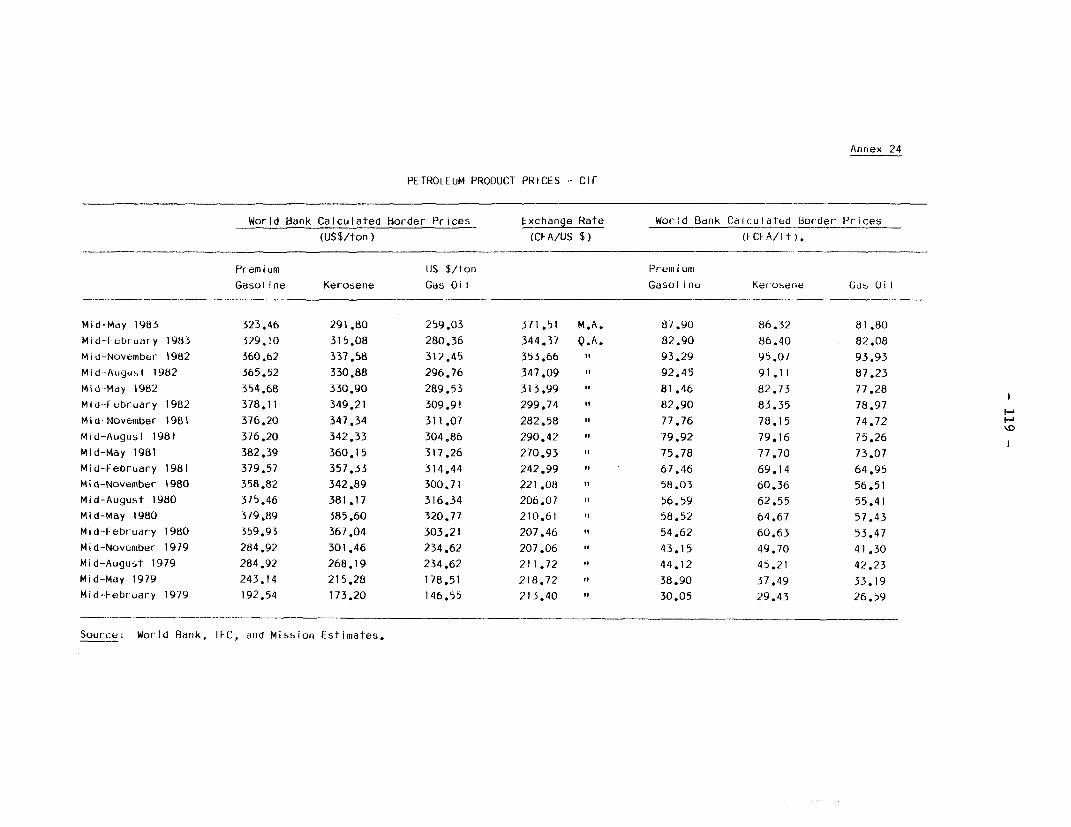

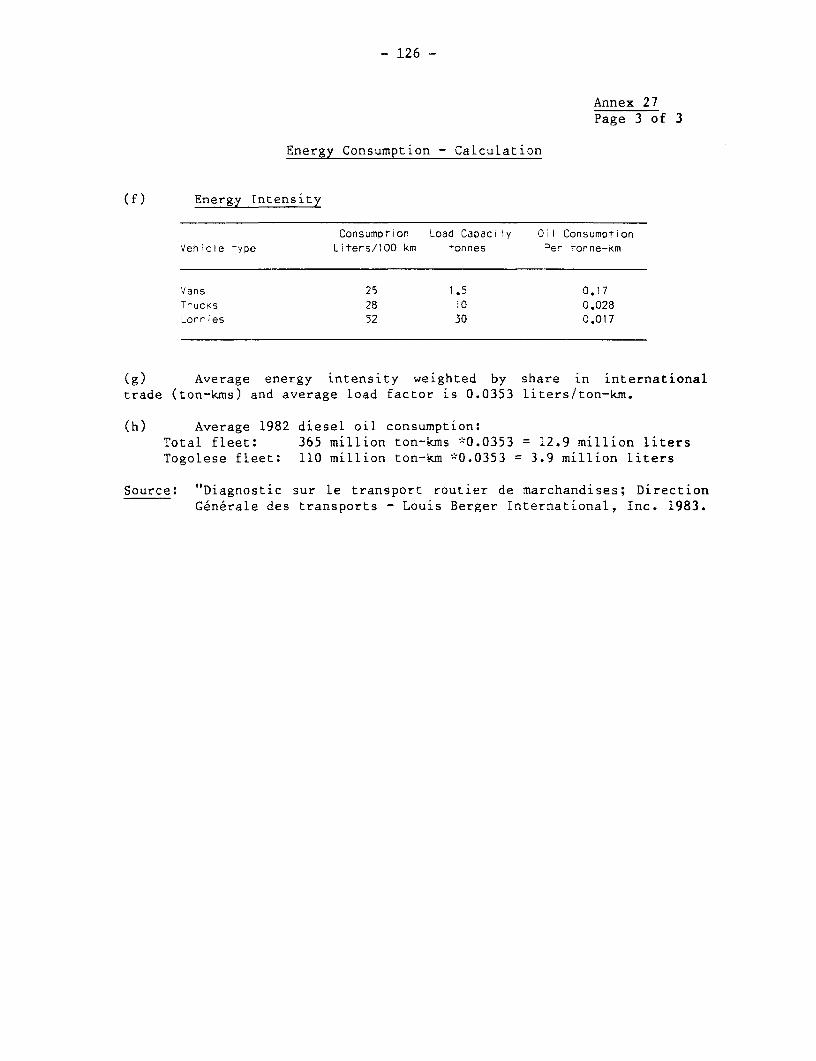

Neighboring Countries ....................................... 11420. West Africa - Petroleum Product Consumption - 1981 .......... 11521. West Africa Petroleum Market - Historial Trends .......... e 11622. West African Refining Capacity ..................... ......... 11723. Petroleum Product Prices - 1983 ... ................ 11824. Petroleum Product Prices - CIF ..... ....................... 11925. Togo: Vehicle Registrations, 1974-1982 .................... .. 12026. Characteristics of the Togolese Vehicle Fleet ............... 12127. Energy Consumption in International

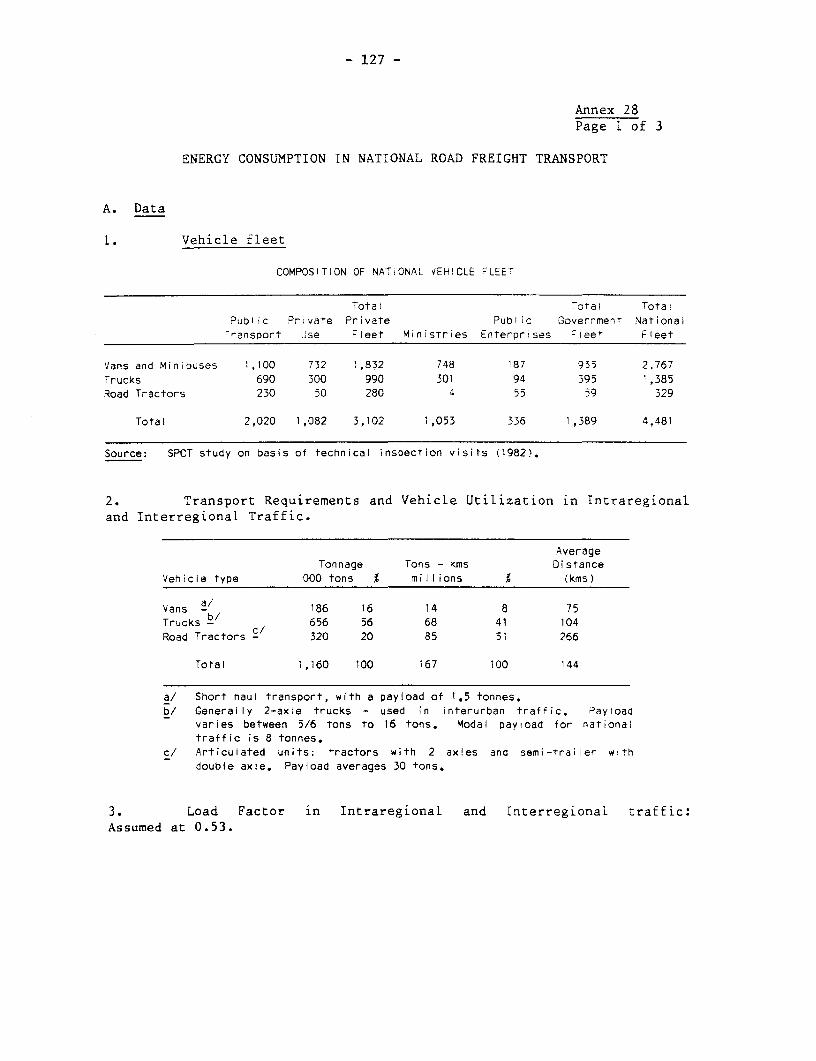

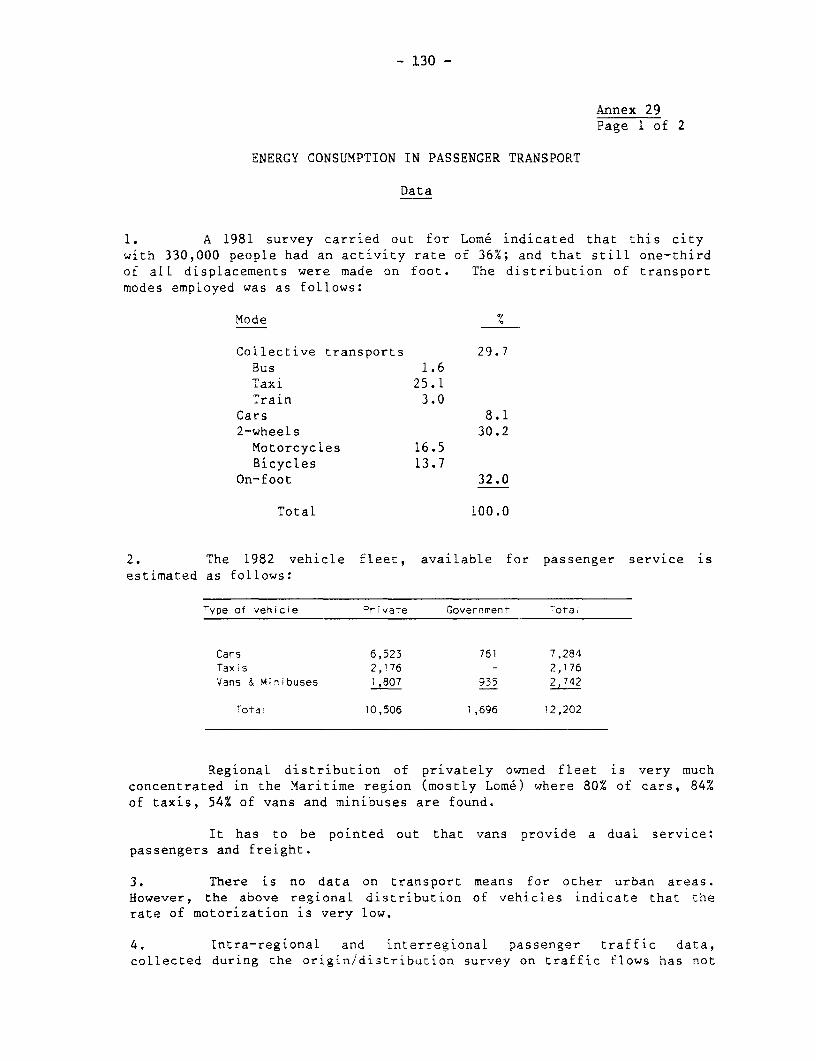

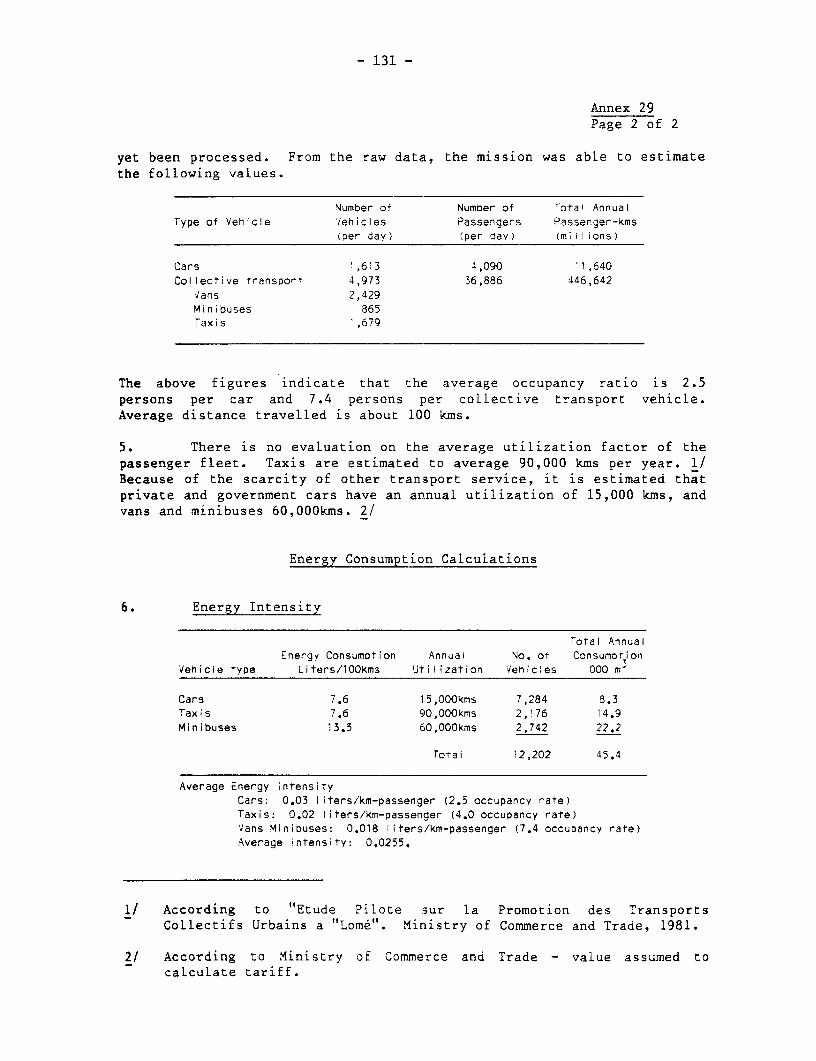

Road Freight Transport ..... .. .......... ....... ... 12428. Energy Consumption in National Road Freight Transport ....... 12729. Energy Consumption in Passenger Transport .................. 130

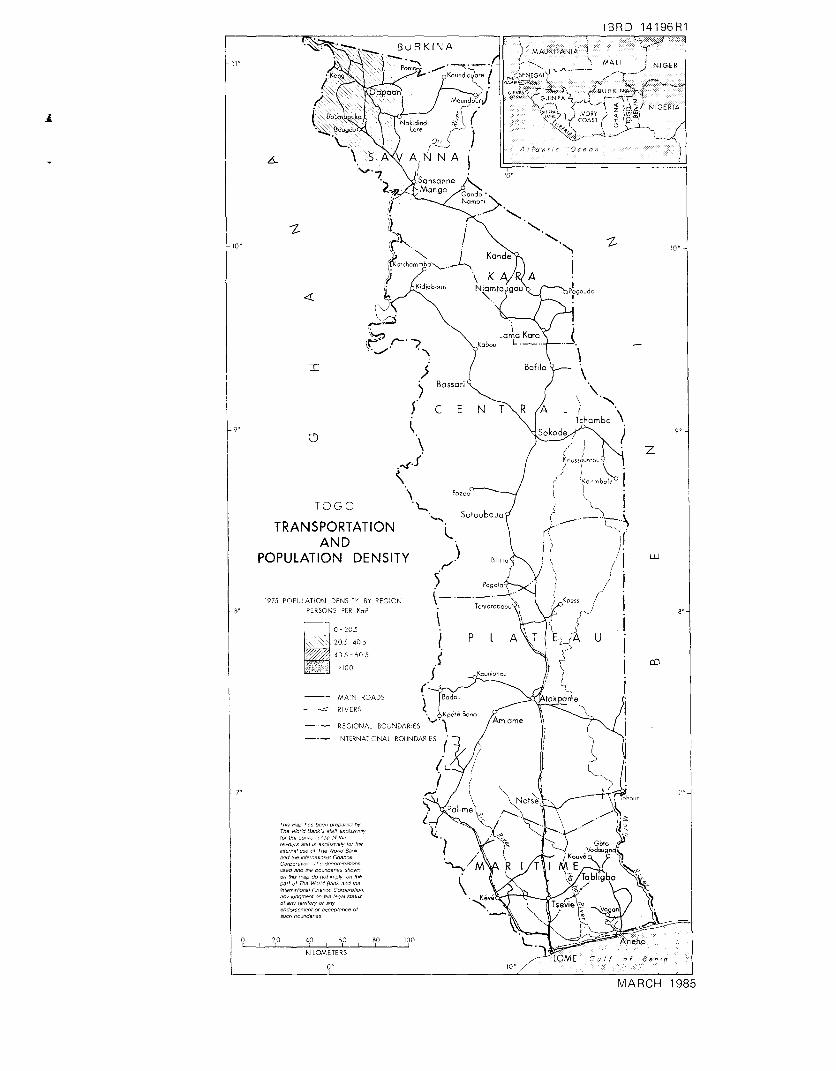

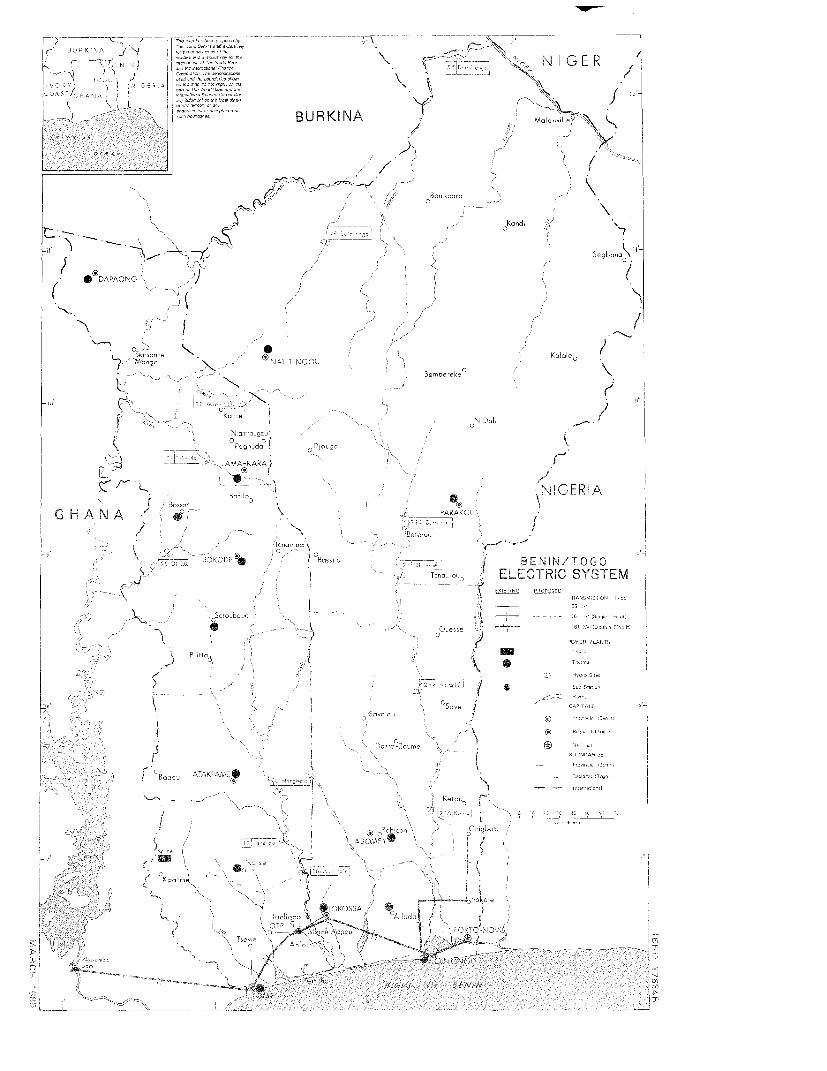

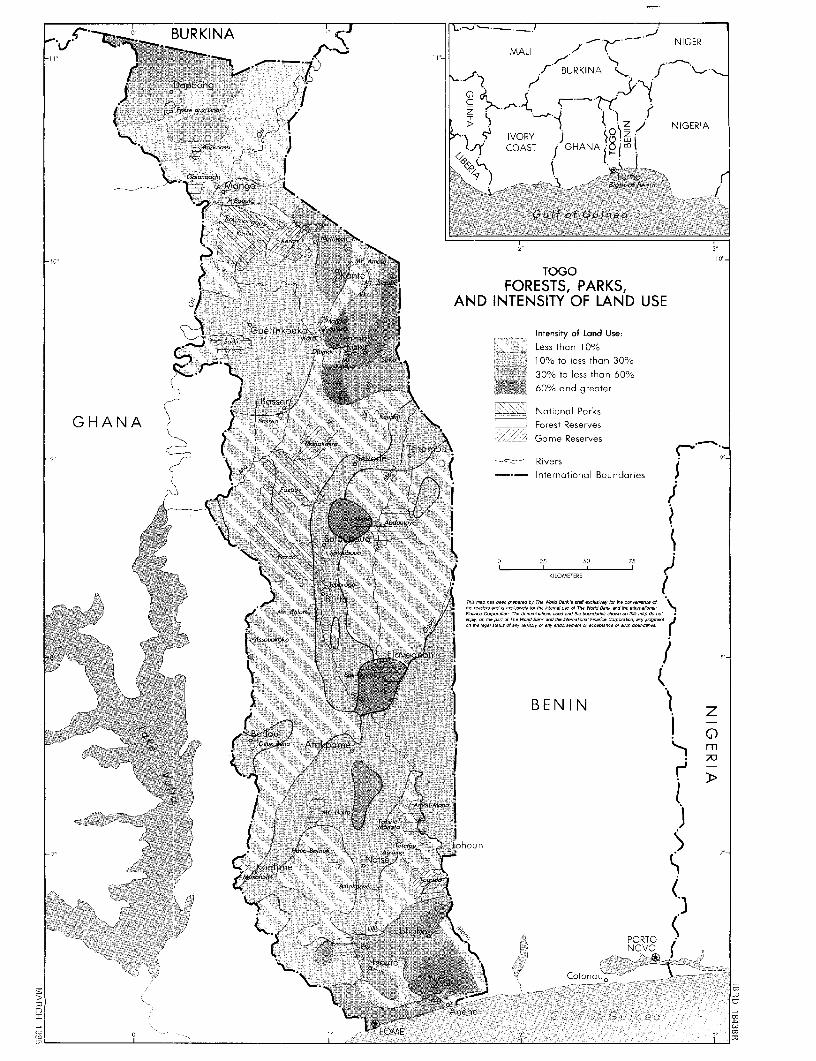

MAPSIBRD 14196: Togo Transportation and Population DensityIBRD 17684: Benin/Togo Electric SystemIBRD 18438: Togo Forests, Parks, and Intensity of Land Use

I. SUMMARY AND RECOMMENDATIONS

1.1 Togo's economic crisis makes it imperative to avoid unnecessaryenergy investments and inefficient energy consumption. At the same time,the country's long-term reliance on agriculture requires that strongremedial action be taken to maintain self-sufficiency in woodfuels with-out continuing deforestation, and that growing attention be given to thelinks between energy and agricultural development.

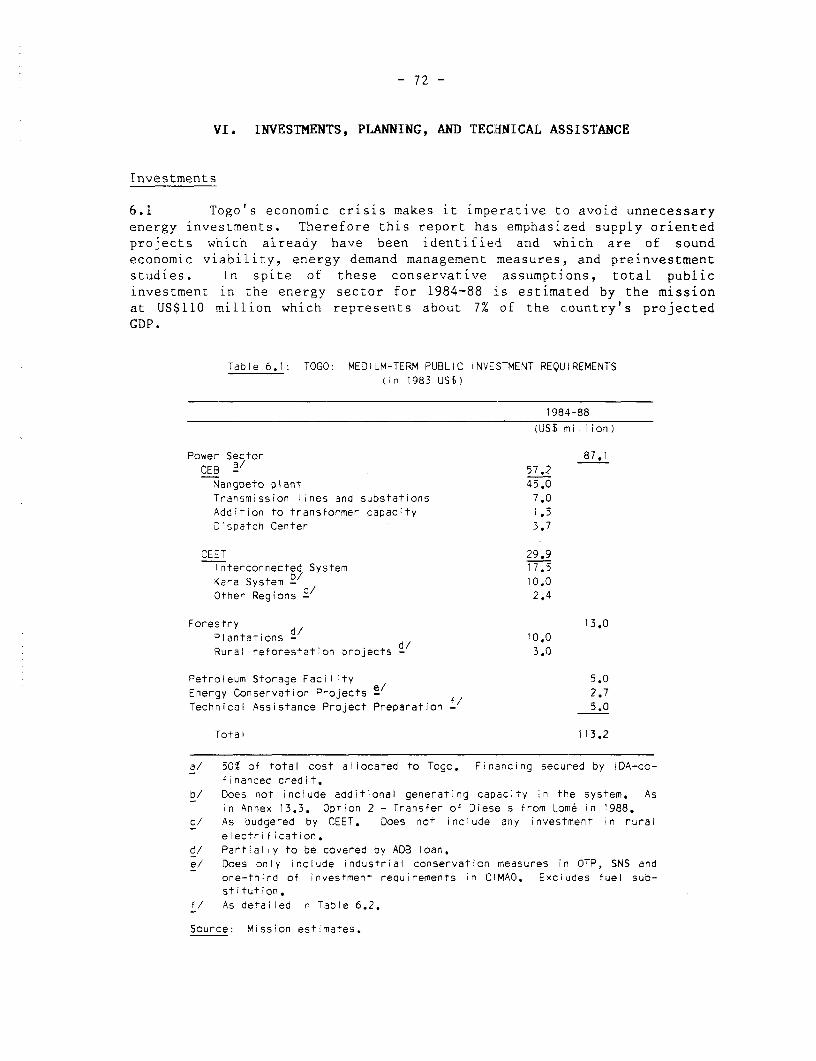

1.2 The mission estimates total public investment requirements inthe energy sector at US$110 million for the period 1984-88, which repre-sents about 7% of the country's projected CDP. Almost four-fifths of theinvestments are in the electric sector, for developing hydropower capa-city and improving the transmission and distribution network to reduceoperating costs. About 10% of the investments are allocated towards con-tinuing reforestation projects already initiated to meet the fuelwoodrequirements of major urban centers and to promote rural reforestationprojects. Less than 2% of the investments consist of projects related toenergy conservation at the final consumer level and 5% to the creation ofan oil storage facility. These projects have a short payback period andpotentially could save the economy the equivalent of US$6-10 million peryear (Table 6.1).

1.3 Energy sector management in the broad sense, including not onlythe administration of operating entities in the sector, but also the pro-cedures and policies followed in establishing investment programs andpricing policies, must be significantly strengthened if needed measuresare to be implemented efficiently and in good time. Some of these proj-ects are geared to set up an incentive system to achieve a more activeinvolvement of the private sector. In answer to this requirement, themission proposes technical assistance programs specific to each sub-sector, with an intensive training component. Given the fact that Togoand Benin have similar technical assistance requirements, the missionrecommends coordinating the programs for the two countries in otherenergy subsectors besides electricity, where bi-national programs havebeen established successfully.

Resource Development

'.4 Under present economic and technical conditions, the annualenergy potential of biomass in Togo is estimated at 1.4 Mtoe, whichcompares with a total energy consumption of 0.9 Mtoe. This balanceindicates that, in principle, there are opportunities to replace importedenergy sources with more intensive uses of biomass. Such a development,however, is limited by the concentration of energy demand in specificareas and the lack of technical expertise for project identification andimplementation. Forestry should be singled out as the priority sectorfor the medium-term energy strategy. The conversion of agriculturalresidues into usable energy forms must be preceded by a detailed

agricultural balance. This balance should determine the net volumesavailable on a regional basis, considering soil recycling needs andalternative uses (Chapter III).

Forestry

1.5 With proper management, logo's forests can meet the nation'srequirements for fuelwood and charcoal over the coming decades. Inphysical terms, the major problems to be dealt with are the progressivedegradation of the vegetal cover in northern Togo and shortages of fuel-wood in urban areas, particularly in the south. Several reforestationprojects have been initiated in these critical zones, but their progresshas been slower than expected. The experience, however, is invaluable interms of providing information on biological and climatic constraints,and on the attitude of the population towards reforestation. It has alsopermitted the building of a core of local expertise in the many phases ofplantation and forest management. The experience has shown that in ruralreforestation projects land ownership and exploitation rights have to beclarified and the preference for multipurpose tree species has to betaken into account, and that intensive wood plantations are costly toestablish, technically exacting to manage and difficult to keepfinancialLy viable.

1.6 In view of the financial constraints of the Togolese economyand the low absorbtive capacity of the institution in charge of managingforest resources, the mission recommends in Chapter 3 that between 1983and 1988 the already initiated peri-urban afforestation projects be con-solidated and that rural reforestation projects be initiated under alter-native management systems to test their long-term economic viability.Further, the mission recommends:

(a) further strengthening the existing forestry institutions,particularly those responsible for agro-forestry development.The mission recommends closer cooperation between ODEF and DPF,and use of the former's facilities for training and seedlingproduction.

(b) defining an effective policy to resolve land use conflicts andto set aside land for wood production within agriculturalzones.

(c) increasing efficiency in charcoal production and both charcoaland fuelwood utilization.

1.7 At the end of the decade, Togo will be in a better position todefine a long-term forestry plan. In the mission's view it will benecessary to continue peri-urban plantations. Consideration shouldtherefore be given to the establishment of 4,000 ha of additional energyplantations to supply Lome and 2,000 ha in the Lama Kara area after 1988,which would produce the equivalent of two years growth cf demand in thesetwo cities, and allow the time necessary to promote ruraL reforestationprojects. These projects ideally should be designed as extensions of theprojects already executed.

- 3 -

1.8 The current market price for fuelwood and charcoal does notreflect its economic cost, which includes the cost of reforestation. Themission recommends the establishment of stumpage fees for fuelwood fromnatural forest to enhance private reforestation and to create a soundincentive for conservation, both at the level of charcoal conversion andthat of the final consumer.

Agricultural Residues

1.9 The development of a sound policy for the use of agricuLturalresidues requires creating a center for research and testing. Themission suggests that consideration be given to structuring such a centerwithin the Direction de la Recherche Agronomique or the Direction desEtudes Pedologiques et de l'Ecologie Generale. It is also suggested thattechnology demonstration projects be implemented. In particular, themission recommends implementing a pilot project for briquetting residuesin rural areas near Lome, and studying the economic and technicalfeasibility for enhancing the use of residues in the industrial sector.

Commercial Energy Resources

1.10 Imported petroleum products and electricity make up less than30% of gross energy inputs into the economy. However, the importance ofthese sources is considerably greater when analyzed in terms of effectiveend-use energy (50% of total) and in terms of their cost in foreignexchange (more than 20% of export earnings). The energy intensity of theTogolese economy is expected to grow at a moderate rate. The imple-mentation of basic energy conservation measures and the development ofnational resources will permit energy imports to grow at tolerablelevels. At present, a hydrocarbon exploration campaign is under way inthe offshore area that may result in discoveries leading to long-termforeign exchange relief. The hydro potential is about equal to presentelectricity demand (30 ktoe). Its economic development must be envisagedin the international context and requires backup by interconnectionand/or thermal power.

Electricity

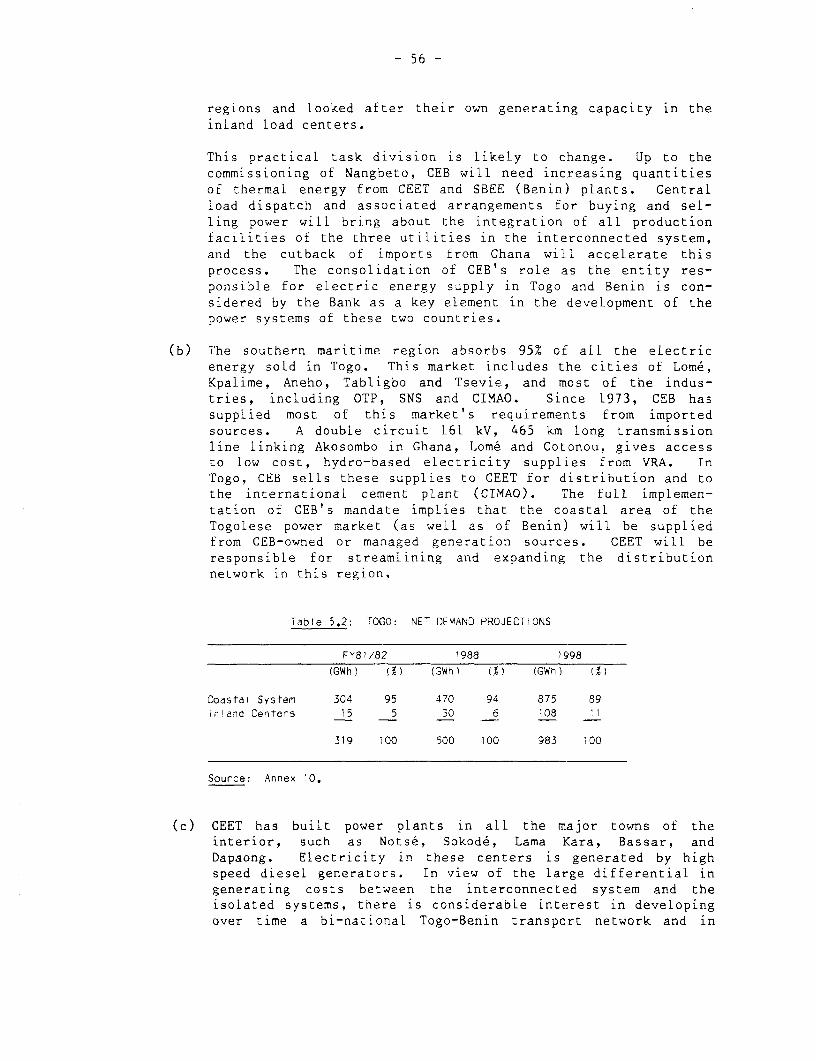

1.11 The main characteristics of the electric power subsector(Chapter 5) are: (a) Electricity supply is restricted to major towns,and less than 30% of the urban population has access to this service.(b) The southern electric system, representing 95% of total demand, isinterconnected with Benin and Ghana and has access to low cost hydropowerfrom Ghana. (c) Isolated centers generate electric power from high costdiesel units. Although the cost differential favors the construction ofa nation-wide interconnected network, large transmission distances andlow load densities in the interior limit the practical possibilitiesuntil the end of this decade. (d) The electricity tariff does notreflect regional differences in supply costs. Consideration should begiven to establishing tariff levels sufficient to recover at least thevariable costs in the regional centers. On the other hand, the tariffstructure is not conducive to capacity and energy savings. The recom-mendations made in the tariff study should be implemented without delay.

- 4 -

1.12 An unprecedented drought affected West Africa in 1983 whichalmost took out of service the Akosombo hydro plant in Ghana, on whichTogo depends for the bulk of its electric supply. Although normal rain-falls have resumed, imports from Ghana are likely to remain curtailed forseveral years. Although spare capacity is sufficient to meet demand, thehigher cost of thermal generation induced the Government to impose severedemand rationing measures: closing down energy intensive industries suchas cement, and increasing the average tariff by 25%. An additionalsurcharge is necessary to compensate for the increased cost of thermalgeneration. Further, it is also necessary to ensure (a) proper operatingand maintenance practices at CEET so that standby reserve capacity isavailable when needed; and (b) coordination of supplies with Benin, byformulating joint short-term operational generation Drograms to makeleast cost operation of the system feasible and consistent with theinterest of each partner, until the load dispatch center envisaged underthe Bank's Nangbeto credit is built.

1.13 Medium- to long-term options for expanding the capacity of thebinational electric system revolve around the proposed West Africaninterconnection (WAPSI) and the development of the primary energyresources available in Togo and Benin. The first hydro power plant(Nangbeto), scheduled to be commissioned in 1988, will Lead to signif-icant fuel economies to both Togo and Benin. A possible next economicproject might be for the binational power company to study the con-struction of a second hydro pLant downstream from Nangbeto.

1.14 The West African interconnection has been proposed to linkNigeria's mixed hydro-thermal system with the predominantly hydro systemsof Ivory Coast and Ghana, and to allow for a least cost development planfor the region as a whole. CEB, the joint Togo-Benin power utility, actsas coordinator for the study of this project. Once the transmission line(in 330 kV) is built, confidence in the system must be developed andoperational problems will have to be mastered. Therefore, it is prudentto formuLate a binational expansion program to meet incrementaL demandassuming that during its first operational phase, tne regional transmis-sion line will predominantly facilitate exchanges of contingency powerand of energy.

Petroleum

1-15 The Government has decided to maintain the STH refinery underminimum mothballing in the hope of finding some economic use for therefining equipment, which otherwise has a low salvage value. A study todetermine the feasibility of converting the refinery's tank farm into apetroleum terminaL has been completed in 1984, and a contract for themanagement of the facility has been signed with Shell-Togo. Grossbenefits accrued from the reduction in the landed cost of importedpetroleum products are expected to be on the order of US$3 million peryear if the terminal serves onLy the Togolese market. In the longer termthe terminal could become a regional transshipment facility. The newstorage facility will permit significant freight savings to be realizedby increasing the average cargo sizes from 4,500 m3 to 20,000 m3. Should

the countries of the region in the future decide to pool their petroleumprocurements, the terminal could receive shipments of up to 100,000 m3.The net benefits to the Government and consumers from the terminaloperations will depend on the efficiency with which the facility ismanaged.

1.16 The existing regulatory system does not offer private oilcompanies an incentive to reduce the landed cost of imports or torationalize distribution costs. The commissioning of the new terminalprovides the opportunity to modify this system. As a first step, themission suggests that the Government define with the importing companiesa methodology for calculating reference landed costs. This methodologywill then be used by the Ministry of Commerce and Transport forevaluating the competetiveness of actual import costs. In the longerterm, consideration could be given to establishing a system of inter-national tenders to supply the market's requirements. Under this system,bids from companies established in Togo as well as from recognized inter-national brokers would be sought periodically. The distribution com-panies would continue to serve the market and be guaranteed adequateremuneration for their services. In order to ensure the efficiency ofthe government's supervisory role, the mission suggests that selectedgovernment officials be trained in all aspects of oil procurementarrangements and in market planning techniques. In addition, it issuggested that the assistance of the established oil companies beobtained in this endeavor.

1.17 The distribution services in the interior of Togo should beimproved, and storage capacity should be built to avoid supply inter-ruptions. The mission suggests that alternative incentives be studied,such as a franchise system under which the companies' share of theprofitable Lom6 market is linked to their share in the provinces, and/orthe establishment of differential retail prices that reflect the fulleconomic cost of supplying regionaL markets.

Demand Management

1.18 As the industrial and transport sectors are the main users ofimported petroleum products and electricity (57% and 31%, respectively,of final consumption of these products), they are important targets inany demand management policy. The potential savings that could beachieved through improved energy efficiency are estimated at about 8% ofconsumption in these sectors (9,000 to 15,000 toe per year). Large scaleinterfuel substitution is not envisaged until the end of the decade,despite the important reductions in the cost of imported fuels that couldbe achieved by replacing fuel oil with coal in Togo's main industries(OTP and CIMAO). 1/ On the other hand, the development of a natural gastransport infrastructure in Nigeria and the discovery of natural gas in

1/ CIMAO was shut down in 1984, and it's financial viability in thelong term is doubtful.

- 6 -

other countries of the region might offer new, more advantageous sub-stitution opportunities. For the medium term, the mission suggestspromoting efficient energy use in all sectors of the economy, includinghouseholds, and enhancing the use of internal energy sources (agricul-tural residues, solar energy in water heating applications, etc.).Direct government involvement should take the form of increasing publicawareness about the energy problem, providing information on measuresconducive to savings, and setting in place adequate pricing policies.Chapter II discusses possible actions leading to higher efficiency, andChapter VI discusses technical assistance requirements to implement theserecommendations.

Sector Policv Recommendations

1.19 The development of an effective energy planning capacity isessential for achieving the two main sector objectives: (a) ensuringcontinuing self-sufficiency in fuelwood, and (b) securing reliablesupplies of petroleum products and electricity at competitive prices.However, the rationalization process in allocating scarce financial andtechnical resources to highest priority programs has to start at thesubsectorial level, before an effective planning mechanism can beestablished at the national energy level. The mission thereforerecommends strengthening planning and project implementation in theinstitutions responsible for forestry, petroleum and electricity, andsetting up groups to coordinate programs within each subsector.

1.20 Private initiative is well developed in Togo. Therefore,government actions should focus on policies leading to the activeinvolvement of the private sector, by creating the necessary economicincentives and providing technical and financial assistance. Decen-tralized energy production, the introduction of new renewable energytechnologies, and simple techniques to enhance more efficient energy useare some of the areas where private sector participation can be costeffective and help to develop new entrepreneurial acitivities.

1.21 Togo is located strategically in a region that has a diver-sified and abundant energy resource base, and a large and rapidly growingconsumer market. Coordination of energy programs among the countries ofthe region and joint development of the resources offer clear economicadvantages for the region as a whole. The progress achieved in inter-connecting the electric systems of Ghana, Togo and Benin, and of Ghanaand the Ivory Coast serves as an incentive to try to expand the coop-erative effort. In addition to the project of creating the West AfricanInterconnected Electric System. coordination should proceed in the areasof petroleum procurement, identification of energy substitution andconservation opportunities, technological research and development, andtraining.

II. ENERGY AND THE ECONOMY

Economic Background

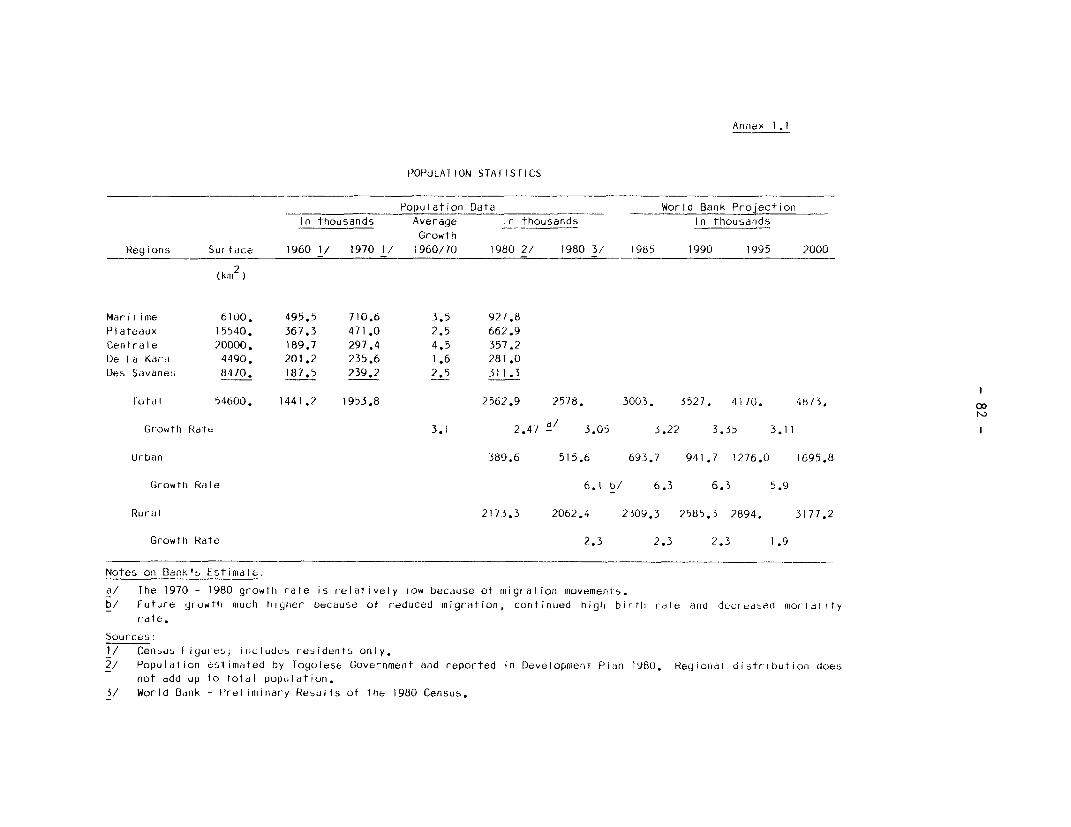

2.1 Togo is a small countrv (56,000 kmi2) with a population of about2.8 million and a per capita GNP of about US$340 (1982). About 90% ofthe population is engaged in traditional activities, mainly food cropagriculture and regional trade. The modern sector development is sus-tained by phosphate mining, which started in 1960. This industry is theprincipal source of foreign exchange earnings, accounting for nearly 40%of export revenues in recent years and for about 30% of governmentrevenues.

2.2 Slow growth and increasing financial disequilibrium have beenthe main features of the economy since the mid-1970s. An expansionarystrategy was adopted during the phosphate price boom of 1974-75 and wasnot adjusted when phosphate prices fell. Heavy public investments in themodern sector were not self-sustaining. The growing financial gap wasfilled by external borrowing, and by 1978 the outstanding debt reached65% of GDP. The deteriorating fiscal situation forced the Government toreconsider economic Dolicies in 1979. In 1983, the Government adopted afinanciaL stabilization program supported by IMF and a structural adjust-ment program backed by the World Bank.

2.3 The rehabilitation program calls for a radical reorientation ofthe economic policy. The objective is to achieve and sustain a higherlevel of economic activity consistent with the constraints imposed by thebalance of payments. A significant untapped development potential hasbeen identified in three sectors: mining, agriculture and industry. Inmining, the most concrete project is a phosphoric acid plant, which wouldprocess new, low-grade phosphate deposits and provide an effective meansto restore the trade balance. If the plant is completed by 1987-88,exports of phosphoric acid could make up 24% of all exports by 1990. Inthe agricultural sector, production could be increased through morecompetitive pricing and marketing policies, and through careful coor-dination of projects and support services in the rural area. The foodcrop strategy is aimed at eventually penetrating regional markets,especially Nigeria. In the industrial sector, more active private parti-cipation could be encouraged. Several measures could be undertaken topromote the establishment of small and medium-sized industries, such as(a) improving the structure of effective protection; (b) offeringincentives to the banking system to finance private investments; and(c) promoting technical assistance to the sector. In addition, therehabilitation of selected state enterprises is intended to increasevalue added, occasionally add to exports, and relieve the Government of amajor financial burden. An IDA-supported Technical Assistance Projecthas been started to help the Government improve its planning capacity andeconomic management, both of which are indispensabLe to successfullycarry out the new economic poLicy.

- 8 -

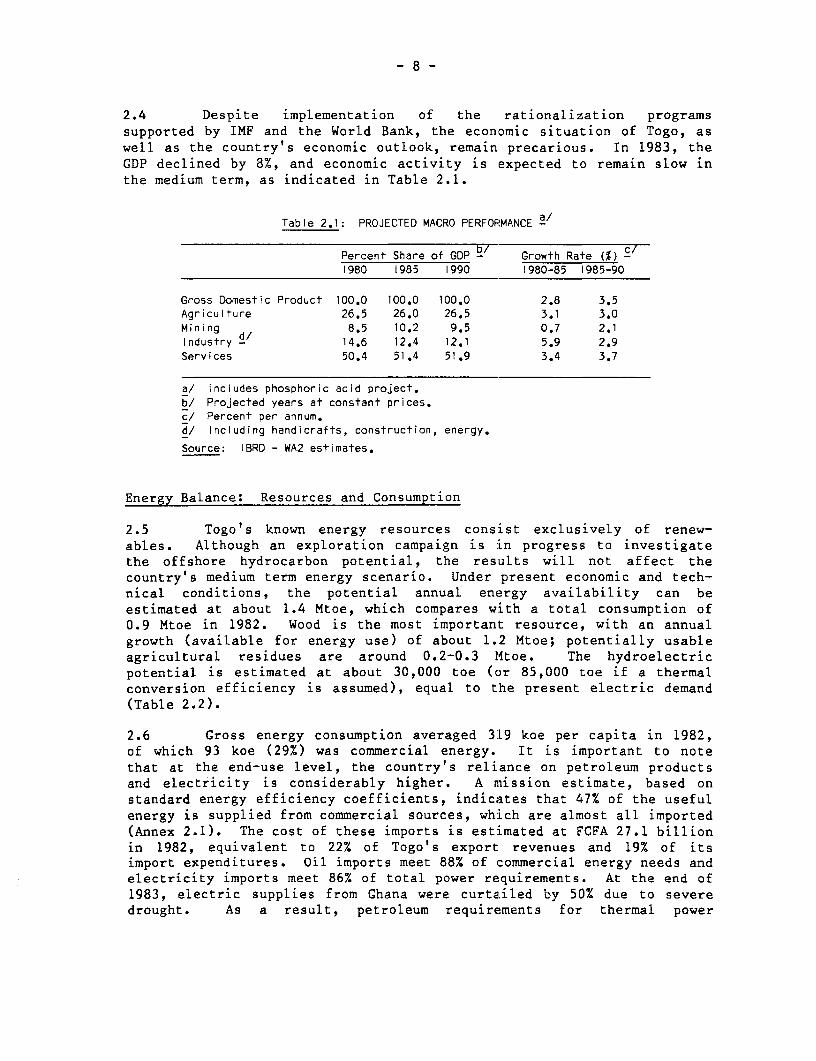

2.4 Despite implementation of the rationalization programssupported by IMF and the World Bank, the economic situation of Togo, aswell as the country's economic outlook, remain precarious. In 1983, theGDP declined by 8%, and economic activity is expected to remain slow inthe medium term, as indicated in Table 2.1.

Table 2.1: PROJECTED MACRO PERFORMANCE 2/

Percent Share of GDP Growth Rate )c1980 1985 1990 1980-85 1985-90

Gross Domestic Product 100.0 100.0 100.0 2.8 3.5Agriculture 26.5 26.0 26.5 3.1 3.0Mining 8.5 10.2 9.5 0.7 2.1Industry - 14.6 12.4 12.1 5.9 2.9Services 50.4 51.4 51.9 3.4 3.7

a/ Includes phosphoric acid project.b/ Projected years at constant prices.c/ Percent per annum.d/ Including handicrafts, construction, energy.

Source: IBRD - WA2 estimates.

Energy Balance: Resources and Consumption

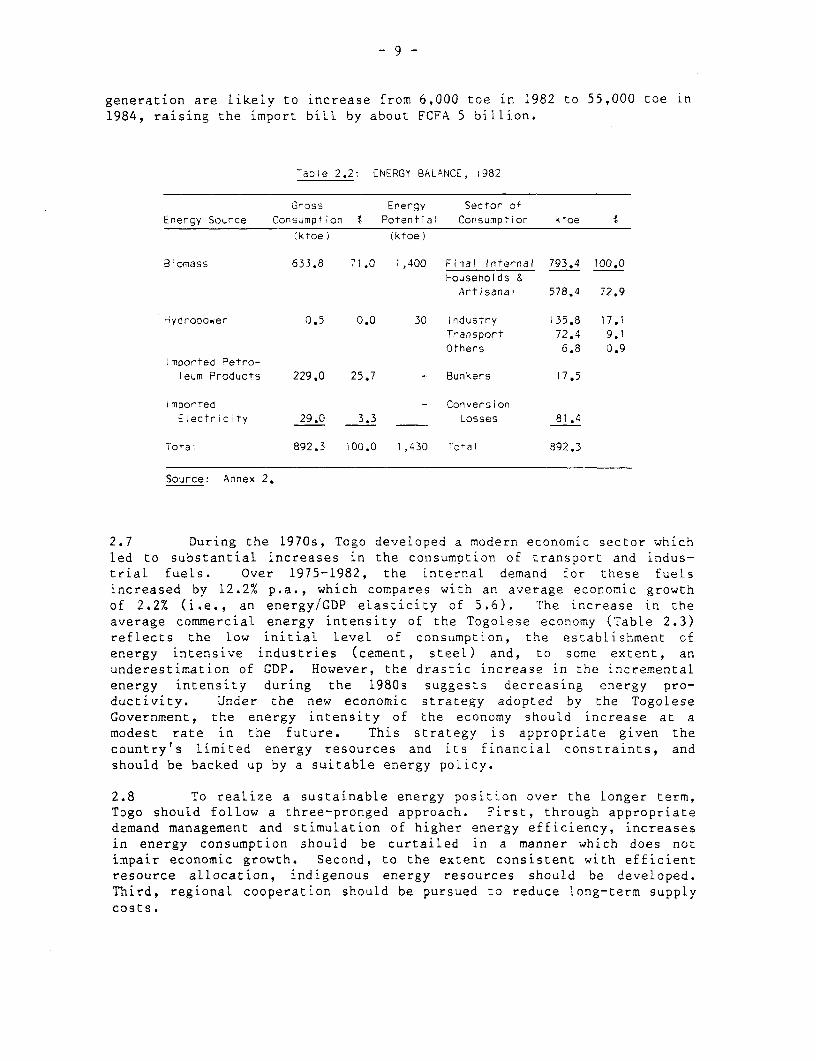

2.5 Togo's known energy resources consist exclusively of renew-ables. Although an exploration campaign is in progress to investigatethe offshore hydrocarbon potential, the results will not affect thecountry's medium term energy scenario. Under present economic and tech-nical conditions, the potential annual energy availability can beestimated at about 1.4 Mtoe, which compares with a total consumption of0.9 Mtoe in 1982. Wood is the most important resource, with an annualgrowth (available for energy use) of about 1.2 Mtoe; potentially usableagricultural residues are around 0.2-0.3 Mtoe. The hydroelectricpotential is estimated at about 30,000 toe (or 85,000 toe if a thermalconversion efficiency is assumed), equal to the present electric demand(Table 2.2).

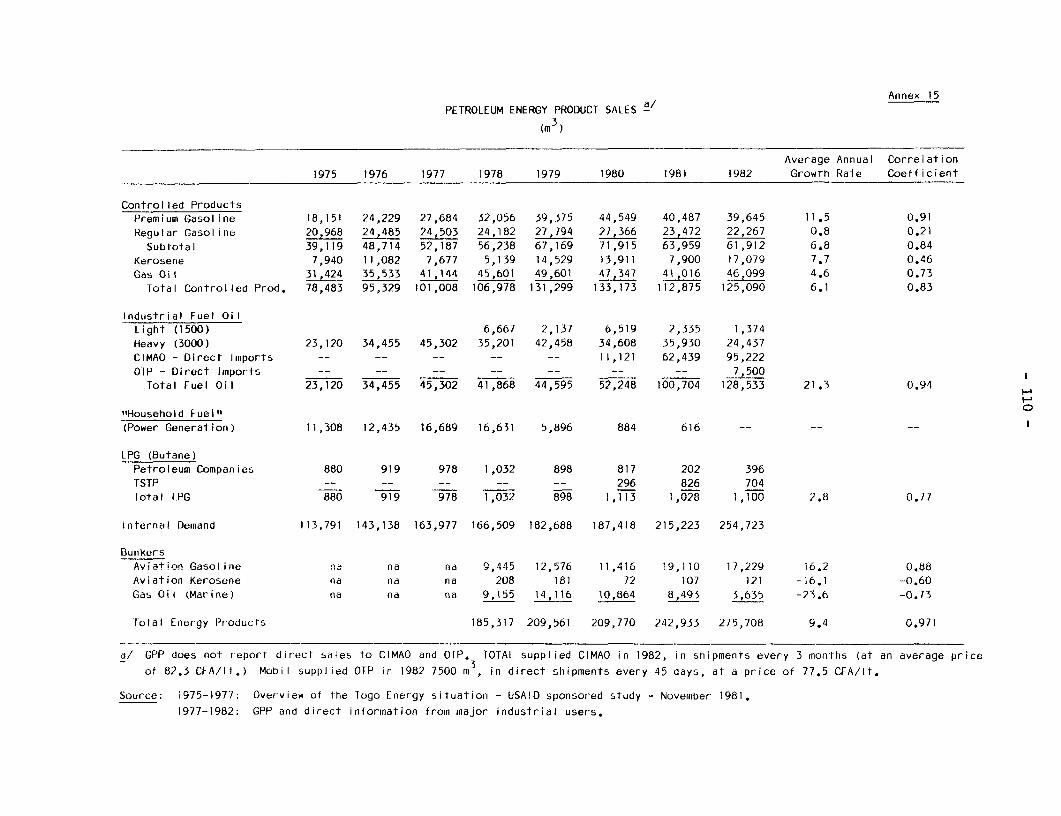

2.6 Gross energy consumption averaged 319 koe per capita in 1982,of which 93 koe (29%) was commercial energy. It is important to notethat at the end-use level, the country's reliance on petroleum productsand electricity is considerably higher. A mission estimate, based onstandard energy efficiency coefficients, indicates that 47% of the usefulenergy is supplied from commercial sources, which are almost all imported(Annex 2.1). The cost of these imports is estimated at FCFA 27.1 billionin 1982, equivalent to 22% of Togo's export revenues and 19% of itsimport expenditures. Oil imports meet 88% of commercial energy needs andelectricity imports meet 86% of total power requirements. At the end of1983, electric supplies from Ghana were curtailed by 50% due to severedrought. As a result, petroleum requirements for thermal power

-9-

generation are likely to increase from 6,000 toe in 1982 to 55,000 toe in1984, raising the import bill by about FCFA 5 billion.

,aDle 2.2: ENERGY BALANCE, i982

Gross Energy Sector ofEnergy Source Consimp+ion t Potential Consumption ktoe I

(ktoe) (ktoe)

Biomass 633.8 71.0 1,400 Final Internal 793.4 100.0Households &Artisanal 578.4 72.9

4-ydropower 0.5 0.0 30 Industry 135.8 17.1Transport 72.4 9.1Others 6.8 0.9

!mDorted Petro-leum Products 229.0 25.7 - Bunkers 17.5

Imported - ConversionElectricity 29.0 3.3 _ Losses 81.4

Total 892.3 100.0 1,430 Total 892.3

Source: Annex 2.

2.7 During the 1970s, Togo developed a modern economic sector whichled to substantial increases in the consumption of transport and indus-trial fuels. Over 1975-1982, the internal demand for these fuelsincreased by 12.2% p.a., which compares with an average economic growthof 2.2% (i.e., an energy/GDP elasticity of 5.6). The increase in theaverage commercial energy intensity of the Togolese economy (Table 2.3)reflects the low initial level of consumption, the establishment cfenergy intensive industries (cement, steel) and, to some extent, anunderestimation of CDP. However, the drastic increase in the incrementalenergy intensity during the 1980s suggests decreasing energy pro-ductivity. Under the new economic strategy adopted by the TogoleseGovernment, the energy intensity of the economy should increase at amodest rate in the future. This strategy is appropriate given thecountry's limited energy resources arid its financial constraints, andshould be backed up by a suitable energy policy.

2.8 To realize a sustainable energy position over the longer term,Togo should follow a three-pronged approach. First, through appropriatedemand management and stimulation of higher energy efficiency, increasesin energy consumption should be curtailed in a manner which does notimpair economic growth. Second, to the extent consistent with efficientresource allocation, indigenous energy resources should be developed.Third, regional cooperation should be pursued to reduce long-term supplycosts.

- 10 -

Table 2.3: ECONOMIC GROWTH AND COMMERCIAL ENERGY CONSUMPTION

Growti Rates

1975 1980 1982 1980/75 '982/80 1982/75

internal Petroleum Demand

(ktoe) 91.0 I50.0 203.8 '0.5 16.6 12.2

Electricity

(ktoe) 5.3 11.5 12.0 16.7 2.2 i2.4

Total Commercial Energy 96.3 161,5 215.8 i0.9 15.6 12.2

GDP (US$ milions) a/ 912.3 1130.6 1056.0 4.4 3.4 2.1

Average Energy

Intensity b/ 106 143 204

incremental Energy

Intensity b/ 473 13923

a/ in constant 1980 Drices.

b/ toe/Million US$.

Source: Mission estimate.

Demand Management by Economic Subsectors

2.9 The following section studies the current energy use in each

sector of consumption, projects energy demand to 1988 and 1998, and

evaluates energy conservation and substitution opportunities.

2.10 The mission has projected the energy balance to 1988 and 1998

(Table 2.4), with the objective of assessing the aggregate results that

could be achieved through the demand management recommendations made in

this section. These projections are based on the low demand growth

scenario, with gross per capita consumption rising at about 1.5% per

annum (from 319 koe in 1982 to 402 koe in 1998). On the supply side, the

projections assume continued financial restrictions on oil imports and

limits on electricity supplies from Ghana determined by contract Levels

in 1988 and the physical carrying capacity of the existing transmission

line by 1998 taking into account the Benin load. In the event that the

West Africa Interconnection becomes operational in the 1990s, a more

rapid growth of electricity consumption could be envisaged. The latter

also implies that other concomitant conditions to expand electric service

be met (such as the level and distribution of personal income and new

productive applications of eLectricity).

- il -

Table 2.4: PROJECTED 4INAL iNTERNAL DEMAND

'982 1988 1998

(ktoe) 1) (ktoe) () (ktoe) !

Fuelwood - Residues 527 66 627 65 827 58

Charcoal 32 4 57 6 160 II

Petroleum Products 205 26 241 25 375 26

Eiectricity 29 4 39 4 68 5

Toral 793 100 964 100 1,430 100

Averace Annuai Growth Rate 3.3% 4.0%

Source: Anrexes 2.2 and 2.3.

Household and Artisanal Energy Consumption

2.11 The use of energy by households and by cottage industries (71%of total energy consumption in 1982) cannot be differentiated for Lack ofdata. Fuelwood and charcoal are the basic energy sources used for cook-ing. Kerosene, LPG and electricity have only marginally entered thismarket; kerosene is mostly used for lighting (TabLe 2.5).

Table 2.5: TOGO: 1982 HOUSEHOLD AND ARTISANALENERGY CONSUMPT iON

(in tons of oii equivalent)

loiuume Percent

Biomass a/ 557,510 96.4

LPG 469 0.'

Kerosene 14,285 2.5

Electricity 6,087 1.0

Total 578,351 100.0

a/ Annexes 2-5.

Source: Mission esTimates.

2.12 The data base on actual fuelwood and charcoal consumption inTogo is poor. No theoretically sound study has been made to determinethe level of consumption and the relative share of each fuel. The

- 12 -

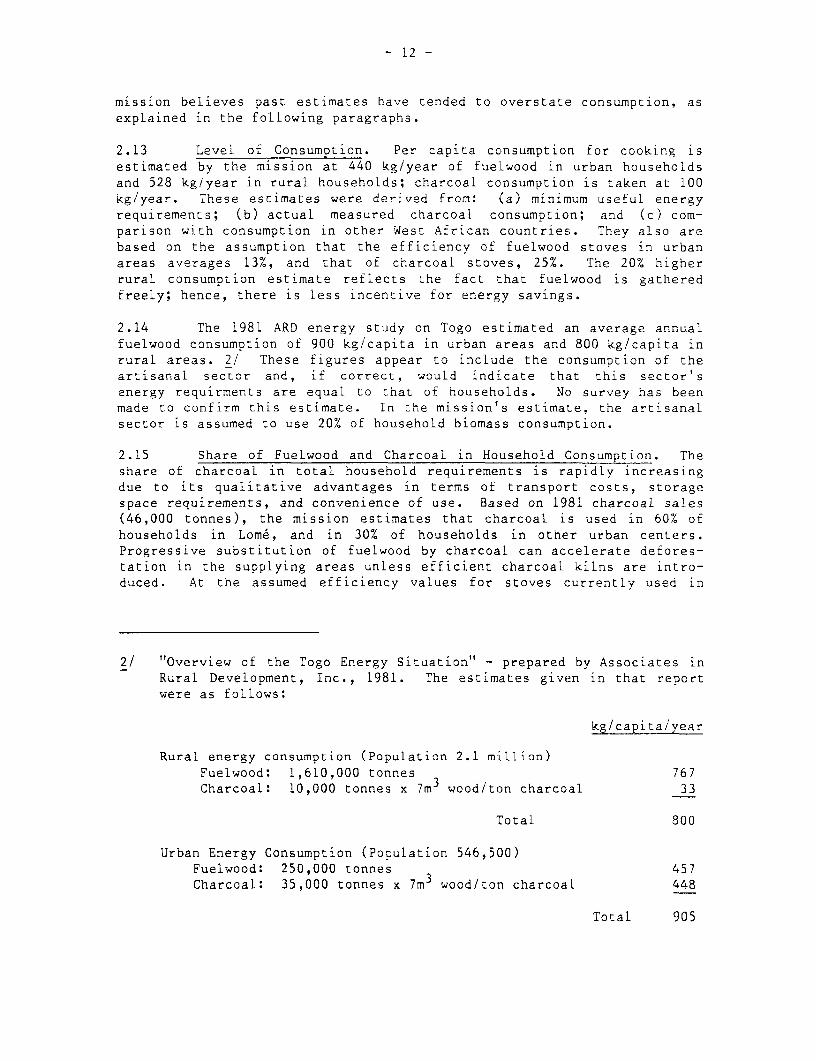

mission believes past estimates have tended to overstate consumpcion, asexplained in the following paragraphs.

2.13 Level of Consumption. Per capita consumption for cooking isestimated by the mission at 440 kg/year of fuelwood in urban householdsand 528 kg/year in rural households; charcoal consumption is taken at 100kg/year. These estimates were derived from: (a) minimum useful energyrequirements; (b) actual measured charcoal consumption; and (c) com-parison with consumption in other West African countries. They also arebased on the assumption that the efficiency of fuelwood stoves in urbanareas averages 13%, and that of charcoal stoves, 25%. The 20% higherrural consumption estimate reflects the fact that fuelwood is gatheredfreely; hence, there is less incentive for energy savings.

2.14 The 1981 ARD energy study on Togo estimated an average annualfuelwood consumption of 900 kg/capita in urban areas and 800 kg/capita inrural areas. 2/ These figures appear to include the consumption of theartisanal sector and, if correct, would indicate that this sector'senergy requirments are equal to that of households. No survey has beenmade to confirm this estimate. In the mission's estimate, the artisanalsector is assumed to use 20% of household biomass consumption.

2.15 Share of Fuelwood and Charcoal in Household (onsumption. Theshare of charcoal in total household requirements is rapidly increasingdue to its qualitative advantages in terms of transport costs, storagespace requirements, and convenience of use. Based on 1981 charcoal sales(46,000 tonnes), the mission estimates that charcoal is used in 60% ofhouseholds in Lome, and in 30% of households in other urban centers.Progressive substitution of fuelwood by charcoal can accelerate defores-tation in the supplying areas unless efficient charcoal kilns are intro-duced. At the assumed efficiency values for stoves currently used in

2/ "Overview of the Togo Energy Situation" - prepared by Associates inRural Development, Inc., 1981. The estimates given in that reportwere as follows:

kg/capita/year

Rural energy consumption (Population 2.1 million)Fuelwood: 1,610,000 tonnes 767Charcoal: 10,000 tonnes x 7m3 wood/ton charcoal 33

Total 800

Urban Energy Consumption (Population 546,500)Fuelwood: 250,000 tonnes 457Charcoal: 35,000 tonnes x 7m3 wood/ton charcoal 448

Total 905

- 13 -

Togo, the charcoal alternative equals direct fuelwood use only if thethermal efficiency of charcoal conversion is 52%. 3/

Price of Household Fuels

2.16 Typical firewood and charcoal prices are given in Table 2.6.Firewood prices at the village level are'extremely variable, so averagestatistics should be used with great caution. ODEF sells both charcoaland firewood at subsidized prices, but in small quantities that fallshort of demand and do not influence the free market price. Charcoalprices have risen more sharply than firewood prices. For example, theprice of charcoal was FCFA 440 per sac in 1974, FCFA 800 in early 1981,FCFA 1,100 by late 1981, and FCFA 1,200 in 1983. On the other hand, the1975 firewood price of FCFA 800/stere can be compared with the 1983 priceof FCFA 1500. Charcoal prices are expected to continue to rise at afaster rate than firewood prices.

Table 2.6: FIREWOOD AND CHARCOAL PRICES

Firewood FCFA/stere FCFA/kg FCFA/Mcal

ODEF price, Lome 1500 3.57 1.02Free market, Lome 2000-2500 4.76-5.95 1.36-1.70Interior town (La Kara) 2500 5.95 1.70Village market Highly variable 1.5-4 0.43-1.14

Charcoal (CFA/sac) CFA/kg CFA/Mcal

ODEF price, Lome 1200 30.8 4.4Free market, Lome 1500-2000 38.5-51.3 (5.5-7.3)Interior town (Sokod6) 1000-2000 25.6-51.3 (3.7-7.3)

2.17 The analysis of end use costs at the consumer level indicatesthat at present market prices, fuelwood and charcoal are the mosteconomic energy sources for cooking. In addition, access to kerosene andLPG is limited to the higher income groups that can afford to purchase astove. In the longer term, fuelwood prices will have to reflect the

3/ Direct fuelwood utilization:

1 m3 of solid wood 700 kg/m3 x 3,500 kcal/kgx 0.13 (stove efficiency) = 318,500 kcal

Charcoal Conversion1 m3 of solid wood * 700 kg/m3 x 3,500 kcal * 0.52

(charcoal conversion efficiency) * (0.25/stove efficiency)= 318,500 kcal

- 14 -

replacement value of wood. The fuel comparisons, basedc on full economiccosts, indicate that unless replantation activities are accompanied byserious efforts to introduce efficient wood and charcoal stoves, con-sumers will tend to shift their cooking energy demand towards petroleumproducts.

2.18 Forecast of household and artisanal energy consumption. Theprojection was made by assuming that petroleum products and electricitywould not replace fuelwood for cooking and artisanal activities, and thatthe share of charcoal would gradually increase. Thus, gross demand forfuelwood, as well as kerosene for lighting, was projected to grow in linewith the population, while electricity was forecast as a function ofeconomic growth.

Table 2.7: COST COMPARISON OF COOKING FUELS AT THE END USE a!(in FCFA)

Concepts Fuelwood Charcoal Kerosene LPG

Market Price Level

Price (per M cal) 1.5 4.4 16.8 17.3 'Stove Efficiency q/ 9/ 13 (25) 25 (30) 30 (45) 55.0

End-Use Cost (per M cal) 11.5(6.0) 17.6(14.7) 67.2(37.3) 31.4

Stove Cost ',000 1,500 5,000 20,000

Macroeconomic Level c/ d/ e/ f/Economic Cost (per M cal ) 3.8 - 6.8 - 13.9 - 14.2 -

End-Use Cost (per M cal) 29.7(15.2) 27.1(22.6) 46.5(31.0) 25.8

a/ Prices refer to Lome.b/ No official price is determined for LPG. The mission estimates US$500/ton.

c/ Economic cost of wood includes plantation cost (based or US$2,000/ha, 10m /ha/year growth, 10% capital cost), plus transport and distribution margin

(FCFA 2,600/ton)d/ Calculated on the basis of the economic cost of wood, assuming a thermai

conversion efficiency of 45%.e/ Economic cost is estimated in Table 4.6.fi Estimated assuming a f.o.o. price of US$230/ton, transporl- cost US$50/ton,

and bottling and distribution cost of US$130/ton.

g/ Efficiencies in parentheses refer to improved stoves.

Source: Mission estimate.

Table 2.8: HOUSEHOLD AND ARTISANAL ENERGY CONSUMPTION(tons of oil equivalent)

Growth Growth

1982 Rate 1 1988 Rate % 1998

Biomass 557,510 2.9 660,275 3.7 948,950

Kerosene & LPG 14,754 3.0 17,620 3.0 23,680

Electricity 6,087 4.4 7,880 5.9 13,980

Total 578,351 685,775 986,610

Source: Mission estimate.

- 15 -

Recommendations for Energy Savings

2.19 The efficiency of the fuelwood chain can, and should, beimproved. At the end-use level, the mission suggests that:

(a) technical assistance be provided to establish a viable stoveprogram in Togo. The present research and development effortsof the Solar Energy Laboratory of the University of Benin inLome on improved clay stoves are insufficient to achieve sig-nificant market penetration. Experiences in other countrieshave shown that the introduction of improved metal stoves inurban areas through commercial channels permits the accel-eration of dissemination and that in rural areas an initialstrong promotional campaign has to be deployed to insure self-sustaining propagation of clay stoves. Tests with the "Ouaga"fuelwood stove have revealed that stoves with a thermal effi-ciency of 40% (about 25% in field tests) can be bulk producedat low cost and with good quality control. In Togo, theeffects of introducing a similar stove can be very important:(a) fuelwood consumption could be cut significantly (25% effi-ciency in the Ouaga stove compared to about 13% in the currentstove); (b) household welfare can be improved, with savings ofFCFA 5,500 in wood purchases, 4/ which compares to an invest-ment of FCFA 1200 per stove; and (c) creation of new artisanalemployment.

2.20 Given the social and economic similarities of Benin and Togo,the mission suggests the establishment of a joint improved stove programfor both countries, with the following components:

(a) Identification of a recipient institution for technicaL assis-tance that would test the adaptability of improved stovedesigns (such as the Ouaga stove) to local conditions andsolve, with the assistance of outside experts, the tech-nological problems of locally manufacturing stoves.

(b) Training of personnel of the recipient institution on thetechnological, social and economic aspects of developing anddisseminating improved stoves.

(c) Training of local artisans in the production of improved stovesand introduction of quality control systems.

(d) Field testing of locally produced stoves and an informationcampaign to alert the consumers to the advantages of the tech-nology.

4/ Fuelwood consumption: urban: 440 kg/capita/year x 5 persons/house-hold x 5 FCFA/kg = 11,000 FCFA/year.

- 16 -

2.21 The program should have as initial targets the markets of thetwo capital cities. This implies that at least three stoves have to beintroduced: a metallic wood stove -- mainly for Cotonou, a metalliccharcoal stove -- mainly for Lome, and a clay wood stove for rural areasof both countries. The mission estimates that the first phase of thisprogram would cost US$400,000 (US$200,000 for each country) over aboutthree years.

2.22 The mission also recommends that a survey of the main artisanalactivities be made to evaluate wood and charcoal consumption in thissector and to identify opportunities for savings. This study shouldinclude edible oil extraction (palm oil), fish and meat smoking, corn andmillet beer fabrication, tuber drying and grinding (corn and maniocflour, gari), baking, salt, metalwork and pottery. This would require asix-month study costing about US$75,000 for each country.

Industrial Energy Consumption

2.23 Current Energy Use Patterns. In 1982, the Togolese industryconsumed roughly 117,000 tons of petroleum products, of which about 87%was fuel oil and the remainder diesel oil, and 162 GWh ot- electric energy(Table 2.9). The CIMAO and OTP plants jointly consamed 93% of thepetroleum products and 77% of the electricity used in the whole sector.Preliminary estimates for 1983 indicate a likely decrease in both fueland electricity consumption for the sector because of lower productionlevels in all activities. 5/

2.24 Plant visits indicated that both OTP's and CIMAO's energy effi-ciencies compare favorably with international standards as their equip-ment is recent and well maintained and operated. For example, CIMAO'sclinker kilns consume an estimated 875 kcal/kg of clinker and thegrinder-predryer another 58 kcal/kg. If fuel preheating and othersecondary fuel uses are included, total fuel-specific consumption isabout 940-950 kcal/kg of clinker, well within the best internationalstandard for similar operation. Electricity specific consumption runs at74-75 kWh/metric ton, which is also a good performance given the highcrude humidity. 6/

2.25 OTP phosphate dryers, which are the major fuel users of thefacility, consume 125-135 kcal/kg of product, which corresponds to 720-790 kcal/kg of water evaporated, or an average thermal efficiency of 80%.

5/ Total petroleum product consumption should not reach 100,000 TOE andelectricity consumption is likely to decrease below 150 GWh.

6/ Average moisture content of crude is between 12 and 16%.

- 17 -

Table 2.9: 1982 iNDUSTRIAL ENERGY USE

Commerc al EnergyPetroleum Eiectricity Agricuiture Residues

6(toe) (10 KWh) (toe)

Plant

CIMAO (clinker) 84,100 63.9 -

OTP (phosphates) 25,100 61.1 _

Brasserie du Benin (brewery) 1,900 4.2 _

CIMTOGO (cement grinding) - 10.5 _

S.N.S. (steei) 1,100 12.0 -

S.T.H. (refinery) - 2.2 3/

SOTOMA (construction

marerials) - .9 350

Subtotal 112,200 154.8 350

Other 5,000 (est) 14.5 b/ N/A

Total c/ 117,200 169.3 N/A

a/ For ma;ntenance only.b/ Other industriai MV customers - source: CEETc In 1984 the CIMAO Dlant was closed and the SNS plant was streamlined

to produce rods from imported steel ingots. Energy requirements

dropped accordingly.

Source: Plant vis,ts, CEET, CE8, World Bank.

2.26 Other industrial plants, which include Brasserie du Benin

(breweries in Lom6 and Lama Kara), CIMTOGO (cement grinding plant),

Societe Nationale de Siderurgie (SNS steel mill), Societe Togolaise

d'Hydrocarbures (STH-petroleum refinery) and SOTOMA (construction

materials plant), show various degrees of energy efficiency, which

indicate a savings potential.

2.27 While CIMTOGO and Brasserie du Benin compare very favorably to

international standards (see Table 2.10), both SNS and SOTOMA 7/ offer

energy saving opportunities, although recently SOTOMA successfully con-

verted its brick kilns from imported diesel oil to domestic agricultural

by-products (cotton seed hulls) and subsequently eliminated all fuel oil

purchases.

2.28 Industrial Energy Prices. As of July 1983, the price of fuel

oil (Bunker C) delivered to CIMAO and OTP was 81,000 FCFA/ton ($230/ton),

which seems high despite the relatively high fuel quality (low density

and low sulphur content). Average electricity prices were between CFA 14

7/ STH refinery is not considered here because it is shutdown. CIMAO

also was closed in 1984, and SNS is not using its smelter and

produces rods from imported ingots.

- 18 -

and 20/kWh for the larger users (CIMAO, OTP, SNS), and between CFA 25 and35/kWh for smaller users. Owing to CEB's source of supply (hydro fromGhana), industrial electricity prices in Togo compares favorably withthose of most developing countries (US¢4-10/kWh).

Table 2.10: ENERGY PERFORMANCE OF MAJOR INDUSTRIAL PLANTS

Fuer 0i Electricity

Current Standard Current Standard

(toe) (KWh)

CIMAO (clinker) .095 0.085-0.097 74-75 65- 80

OTP (phosphates) .013 0.011-0.015 22-28 N/ABrasserie Du Benin (beer) .053 0.050-0.070 120 100-130

CIMTOGO (cement) N/A N/A 35 30- 40

SNS (steel rods) .110 0.080-0.090 1,440 900SOTOMA (Bricks) 0 0.065-0.075 58 - 40- 50

a/ Partially shut down.

Source: WORLD BANK; (Hagler, Bailly & Company).

2.29 Energy Efficiency Improvement Opportunities. Except CIMTOGOand STH, aLl other plants have an energy saving potential. As shown inTable 2.11, energy conservation opportunities in the remaining largeplants (i.e., OTP, CIMAO, Brasserie du Benin, SNS and SOTOMA) may repre-sent up to 9,000 toe or 8% of the petroleum consumption of the sector.This potential is relatively low compared to that of many LDCs where itusually ranges between 10 and 25 percent. This is due to the fact thatmost plants in Togo are recent and well designed. Still, this potentialrepresents a foreign exchange savings of up to CFA 700 million a year.

2.30 More importantly, fuel switching in both CIMAO and OTP fromheavy oil to coal could reduce the sector's petroleum consumption by astaggering 90% and translate into potential foreign exchange savings ofCFA 4 biLlion a year. While coal conversion would definitely improve theplants' competitiveness, the large investment requirements (roughly CFA8-9 billion) and the lack of skills to handle the new fuel make theseswitches unlikeLy before the end of the decade. Postponing the decisionto convert to coal also would allow time to obtain confirmation ofnatural gas resources in neighboring countries and/or in Togo (para.4.31).

2.31 Conservation benefits, on the other hand, may be captured veryquickly, i.e., in less than three years for most opportunities.

2.32 Industrial Energy Demand Forecast. The mission's estimates,based on the assumption that CIMAO will resume operation, indicate thattotal fuel consumption in the industrial area will not increase signif-icantly by 1988 from its 1982 leveL of 117,000 toe, but will increase to165,000-180,000 toe by 1998, an average 2.2-2.7%/year.

- 19 -

Table 2.11: ENERGY SAVING OPPORTUNITIES IN MAJOR INDUSTRIAL

PLANTS - SUMMARY

From conservation From fuel switching

Potential Investment Potential Investment

Savings Required Savings Required

(TOE/Year) (CFA-Million) (TOE/Year) (CFA-Million)

CIMAO 1,700-3,500 170-220 84,000 a/ 5,600 bOTP 2,500-5,100 500-700 25,000 a/ 2,000-3,000 -

Brasserie du Benin 50- 100 5- 8 N/A N/ASNS 150- 250 5- 10 - (1,000) d

SOTOMA 10- 20 e 4- D _ -

Total 5 plants 4,410-8,970 684-943 '110,000) a! 7,600-8,600

a! If Bunker C is repiaced by coal, dol ar savings of $70 (FCFA 25,000) perton of oil dispiaced would result, assuming a de! ivered price of coal of590/ton - (CIF-LOME).

b/ Large uncertainty on investment, as detailed study is required to Droveoroject feasibility.

0/ Includes audit cost.d/ Switch from diesel oil to heavy oil.

e/ Electricity.

2.33 Electricity consumption is projected to increase from 169.3 GWhin 1982 to 195.7-210.3 GWh in 1988 and 285.7-331.5 GWh in 1998, anaverage annual growth rate of 3.3 - 4.3%. This differential rate ofgrowth between fuel and electricity consumption reflects the fact thatmedium size enterprises, operating in the mechanical and metal fields,are expected to grow faster than fuel intensive activities, such asproduction of construction materials.

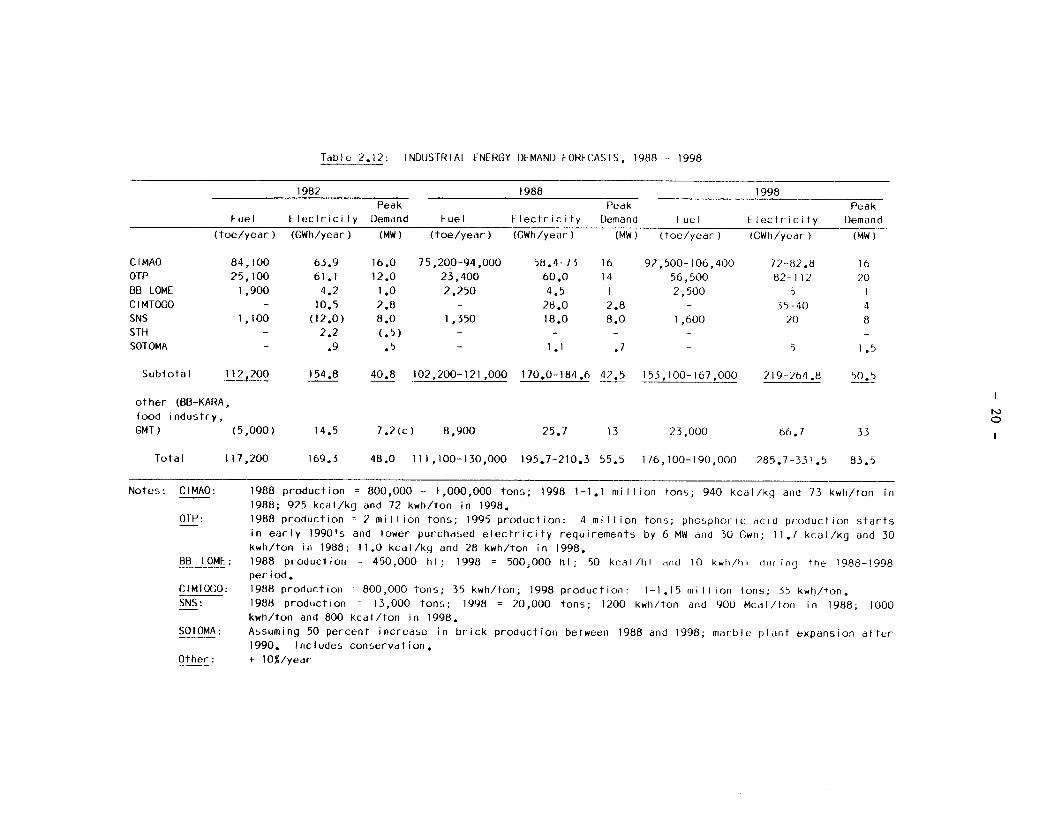

2.34 The peak electric load is also projected to grow moderatelyfrom 48 MW in 1982 to 55.5 MW in 1988 and 85.5 MW in 1998 (see Table2.12).

Conclusions and Recommendations

(a) The current institutional framework in Togo is not adequate toensure efficient industrial energy planning and assist indus-tries in improving their energy performance. The missiontherefore suggests that the Ministry of Planning and Industryshould attract at least one energy conservation officer (engin-eer) to organize the conservation activities. The Direction del'Hydraulique et de l'Energie has a few capable, young engin-eers. Consideration should be given to transfering one of themto the Ministry of Planning and Industry. A short trainingcourse offshore would be sufficient to qualify this officer forthe following tasks:

- collecting industrial production statistics and forecastsfor major energy users, including OTP, CIMAO and SNS, aspart of their annual survey;

Table 2.12: INDUSTRIAL ENERGY DEMAND FORECASIS, 1988 - 1998

1982 1988 1998Peak Pedk Peak

Fuel Flectricily Demand Fuel Electricity Demand iuel Electricity Demand

(toe/year) (GWh/year) (MW) (toe/year) (GWh/year) (MW) (toe/year) (GWh/year) (MW)

CIMAO 84,100 63.9 16.0 75,200-94,000 58.4-73 16 92,500-106,400 72--82.8 16OTP 25,100 61.1 12.0 23,400 60.0 14 56,500 82-112 20BB LOME 1,900 4.2 1.0 2,250 4.5 1 2,500 5 1CIMTOGO - 10.5 2.8 - 28.0 2.8 - 35-40 4SNS 1,100 (12.0) 8.0 1,350 18.0 8.0 1,600 2( 8STH - 2.2 (.5) - - - - - -SOTOMA - .9 .5 - 1.1 .7 - 5 1.5

Subiotal 112,200 154.8 40.8 102,200-121,000 170.0-184.6 42.5 153,100-167,000 219-264.8 50.5

other (BB-KARA,

food industry, OGMT) (5,000) 14.5 7.2(c) 8,900 25.7 13 23,000 66.7 33

lotal 117,200 169.3 48.0 111,100-130,000 195.7-210.3 55.5 176,100-190,000 285.7-331.5 83.5

Notes: CIMAO: 1988 production = 800,000 - 1,000,000 tons; 1998 1-1.1 million tons; 940 kcal/ky and 73 kwh/Ion in1988; 925 kcal/kg and 72 kwh/ton in 1998.

OTP: 1988 production = 2 million tons; 1995 production: 4 million tons; phosphoric dcid production startsin early 1990's and lower purchased electricity requirements by 6 MW and 30 Gwh; 11.1 kcal/kg and 30kwh/ton in 1988; 11.0 kcal/kg and 28 kwh/ton in 1998.

BB LOME: 1988 productionf 450,000 hl; 1998 = 500,000 hl; 50 kcal/hl dnd 10 kwh/hI during the 1988-1998period.

CIMIOGO: 1988 production= 800,000 tons; 35 kwh/ton; 1998 production: 1-1.15 mnillion tons; 35 kwh/ton.SNS: 1988 production = 13,000 tons; 1998 = 20,000 tons; 1200 kwh/ton and 900 Mcdl/ton in 1988; 1000

kwh/ton and 800 kcal/ton in 1998.SOTOMA: Assuming 50 percent increase in brick production between 1988 arnd 1998; marble plant expansion after

1990. Includes conservation.Other: + 10%/year

- 21 -

- assisting industries with energy conservation programs. Thesame Ministry should organize with a short-term consultantan audit program for major energy users, according to theschedule outlined in Table 2.13. Simultaneously, it shouldprovide them with brochures, pamphlets and similar materialsdescribing energy saving activities and associated costs(available in French from the French Energy ConservationAgency - AFME); disseminate case studies on successfulexperiences (e.g. SOTOMA's switch from oil to cotton seedhulls) and suggest detailed feasibility studies for majorretrofit or fuel switching projects (e.g. OTP);

- finally, conduct a two-day seminar, sponsored by theMinistry of Planning and the Direction de l'Hydraulique etde l'Energie, to inform and train plant engineers andmanagement. Local speakers should be invited and couldinclude representatives from CIMAO, CEET, Hotel du 2 F6vrierand Brasserie du Benin who demonstrated good knowledge andawareness of energy efficiency matters during the in-countrymission.

Table 2.13: TENTATIVE INDUSTRIAL ENERGY CONSERVATION PROGRAM1984-1986

Detailed FeasibilityTraining Audit Study

OTP Dryers operation Presses and Coalcoal use dryers Conversion

CIMAO - Use of waste fuels b/

SNS Electricity and All plant -/ Continuousfuel use casting

Brasserie duBenin - Steam system -

SOTOMA Electricity Electrical -

use system

a/ During rehabilitation project.b/ Before coal conversion, cement plant could use agricultural wastes

(cotton seed, cornstalks or bagasse for which a '5,000 ron excess isanticipated at the fut ure ANIE sugar plant).

Energy Consumption in Hotels in Togo

2.35 Conservation opportunities in the hotel industry exist in thefollowing three areas: (a) building structure; (b) heating, ventilating,and air-conditioning (HVAC) systems; and (c) appliances. Some of theenergy conservation measures that can be introduced are exemplified in

- 22 -

the two largest hotels in Togo visited by the mission, the 2 Fevrier andthe Sarakawa. Both are major energy consumers.

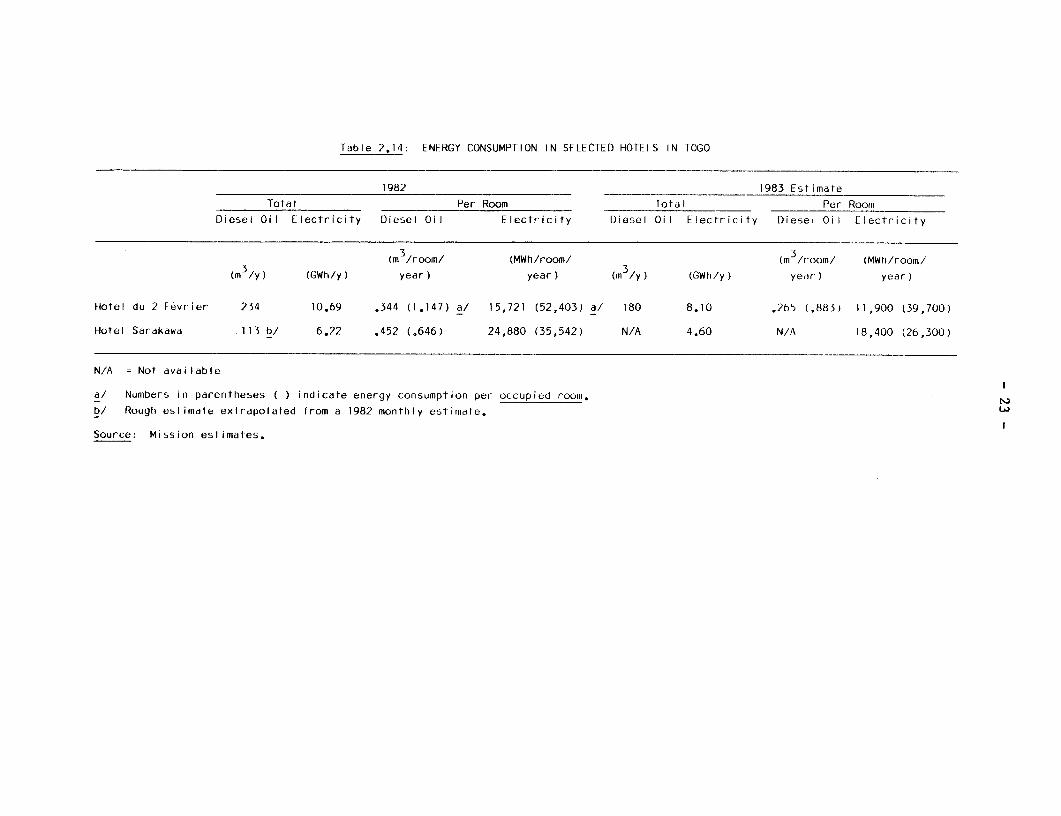

2.36 In 1982, the 2 Fevrier Hotel consumed 10.7 GWh of electricityand 234 m3 of diesel oil. The Sarakawa consumed 6.2 CWh of electricityand an unknown quantity of oil 8/ (probably less than 120 m3). In termsof electricity consumed per room, 2 Fevrier (680 rooms) averaged 15,721kWh and Sarakawa (250 rooms) 24,880 kWh. These numbers compare with USstandards (17,500-19,200 kWh/room in Miami and Hawaii). If the numbersare adjusted for occupancy rates, however, performances fall con-siderably, at 52,403 kWh/room at 2 Fevrier (20% average occupancy rate)and at 35,542 kWh/room at Sarakawa (70% occupancy rate).

2.37 In 1983, however, much better results are expected as aggres-sive energy saving activities are under way, including shutting offequipment where possible, installing timers, repairing/increasing insula-tion, and installing capacitors. Expected 1983 performances are 39,700kWh/occupied room for the 2 Fevrier and 26,300 kWh/room at Sarakawa(Table 2.14).

2.38 These figures indicate that there is still much room for addi-tional savings. The mission estimates that the 2 Fevrier probably couldlower its electricity consumption to 6 GWh/year or 8,800 kWh/room or29,000 kWh/occupied room, and that Sarakawa could achieve an annual elec-tricity consumption of 3.5 GWh/year or 14,000 kWh/room or 20,000 kWh/oc-cupied room.

2.39 Recommendations to achieve such performance are indicatedbelow:

2 Fevrier Sarakawa

Install condensate return sys- . Calibrate instrumentationtem

Increase laundry operating . Investigate economics of solarfactor water heating and preheating

Conduct detailed analysis of . Install additional capaci-electrical system tators

Install energy management . Install energy managementsystem for peak load shaving system for peak load shaving

8/ The chief hotel engineer (Technical Director) had been on the jobfor only a few months at the time of the mission and did not haveall the information available.

Table 2,14: ENERGY CONSUMPTION IN SELECTED HOTELS IN TOGO

1982 1983 Estimate

Total Per Room Total Per Room

Diesel Oil Electricity Diesel Oil Electricity l)iesel Oil Electricity Diesel Oil Electricity

3 3(m /room/ (MWh/room/ (m /room/ (MWh/room/

(m /y) (GWh/y) year) year) (m /y) (GWh/y) ye,r) year)

Hotel du 2 Fevrier 234 10.69 .344 (1.147) a/ 15,721 (52,403) a/ 180 8.10 .265 (.883) 11,900 (39,700)

Hotel Sardkawa 113 b/ 6.22 .452 (.646) 24,880 (35,542) N/A 4.60 N/A 18,400 (26,300)

N/A = Not dvailable

d/ Numbers in parentheses ( ) indicate energy consumption per occupied room. r

b/ Rough estimate extrapolated from a 1982 monthly estirnate.

Source: Mission estimates.

- 24 -

2.40 Total investments required to implement recommended projects inthe Hotel Fevrier are likely to be CFA 25-45 million and shouLd lead,together with improved maintenance and operation practices, to savings of1-1.5 CWh/year or CFA 30-45 million/year. That is roughly a one yearpayback.

2.41 Total investments required for Sarakawa are estimated atCFA 15-20 million and lead to savings of .75-1 GWh/year or CFA 23-30million, which correspond to less than one year payback.

2.42 As a result of its discussions, the mission concluded thathotel technical staff could carry out these projects by themselves asthey demonstrated good knowledge of energy efficiency matters.

Transport Energy Consumption

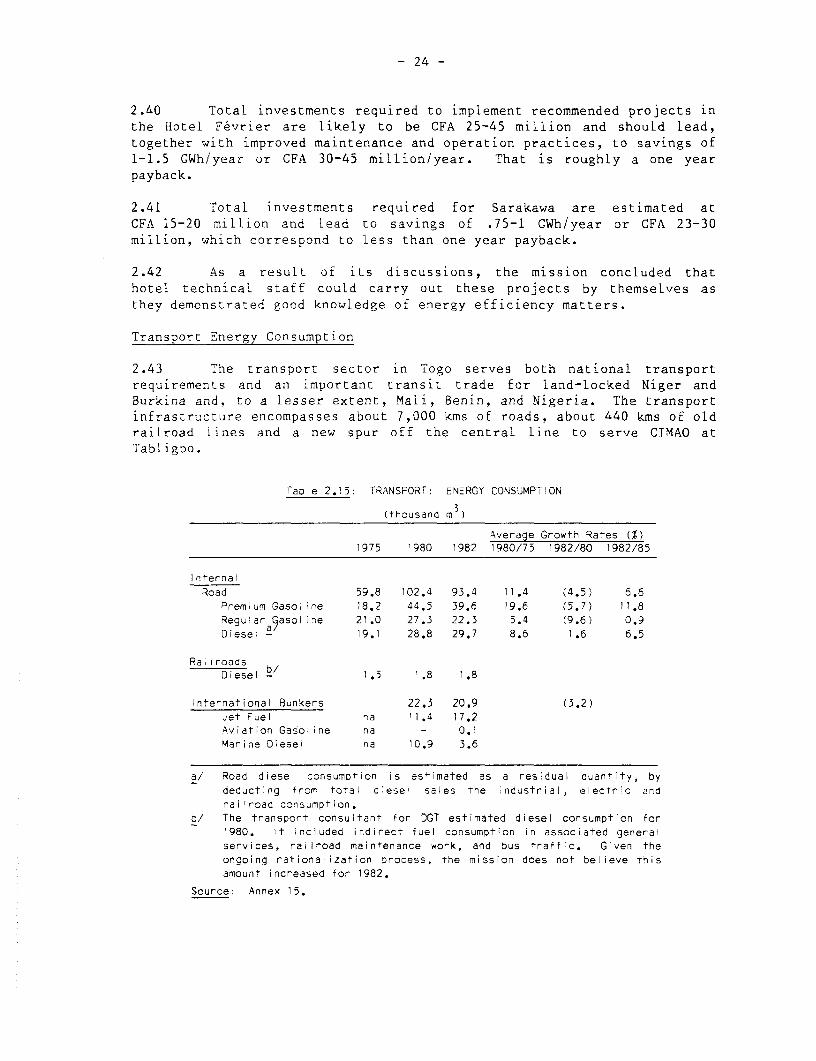

2.43 The transport sector in Togo serves both national transportrequirements and an important transit trade for land-locked Niger andBurkina and, to a lesser extent, Mali, Benin, and Nigeria. The transportinfrastructure encompasses about 7,000 kms of roads, about 440 kms of oldrailroad lines and a new spur off the central line to serve CIMAO atTabligbo.

.abie 2.15: TRANSPORT: ENERGY CONSUMPT ON

(thousand m3)

Average Growth Rates (%)1975 1980 1982 1980/75 1982/80 1982/85

Internal

Road 59.8 102.4 93.4 11.4 (4.5) 6.6Premium Gasoline 18.2 44.5 39.6 19.6 (5.7) 11.8Regular a5asoline 21.0 27.3 22.3 5.4 (9.6) 0.9Diesel - 19.1 28.8 29.7 8.6 1.6 6.5

Ra iroadsDiesel 1.5 1.8 1.8

International Bunkers 22.3 20.9 (3.2)Jet Fuel na 11.4 17.2Aviation Gasoline na - 0.1Marine Diesel na 10.9 3.6

a/ Road diesel consumption is es,imated as a residual quantity, bydeducting from total diesei sales the industrial, electric and

railroad consumption.b/ The transport consuitant for DGT estimated diesel consumption for

1980. It included indirect fuel consumption in associated generalservices, railroad maintenance work, and bus traffic. Given theongoing rationalization Drocess, the mission does not believe thisamount increased for 1982.

Source: Annex 15.

- 25 -

2.44 In 1982, the transport sector consumed roughly 120,000 m3 ofpetroleum products (Table 2.15), equal to about 40% of the country'stotal oil consumption. The energy demand of the sector increased on theaverage by 6.6% p.a. during the 1975-1982 period, which, when compared tothe average economic growth rate, indicates an elasticity of 3. Totalbunker sales in 1982 amounted to about 21,000 m3. Marine diesel saleshave been declining, reflecting price competition from Nigeria andAngola. Domestic air traffic is negligible.

2.45 Transport Fuel Prices. Retail prices well exceed economiccosts in Togo. Diesel oil is less taxed than gasoline (Table 2.16) andis considerably cheaper to the final consumer considering the higherefficiency of diesel engines if properly used in long haul traffic. Thegovernment of Togo is reviewing a proposal to increase taxes on alltransport fuels to encourage higher efficiency in energy use and to meetthe maintenance costs of its expanding highway network. A complementarymeasure to collect road user charges might be to establish a limited tollsystem at Togo's main border check points to cover foreign transitvehicles using the country's international corridors. A special check-point with parking spaces for such vehicles has in fact already beenestablished north of Lome with the purpose of controlling tax collec-tion. 9/

Table 2.16: TRANSPORT FUEL PRICES, 1983

Economic Theoretical Price perCost a! Retail Prices Efficiency Useful Energy

-------(FCFA/lt)-------- (%) (FCFA/toe)

Premium Gasoline 120.0 205 20 1,381Regular Gasoline 116.4 200 20 1,338Diesel Oil 115.5 180 25 857

a! Actual landed cost for shipment received in June 1983, plus internalcost elements in price structure as of October 14, 1981.

2.46 Road Transport. The consumption of petroleum products in roadtransport increased an average of 11.4% p.a. during 1975-1980. Thedecline since 1980 (4.5%) can be attributed to: (a) slowdown of economicactivity; (b) price elasticity; and (c) possibly increased purchases inBenin and Nigeria where prices are lower.

9/ Road maintenance has deteriorated in recent years, in part due toinsufficient funding. Allocations to the road maintenance programhave averaged about CFAF 750 million in recent years, whereas anadequate level of funding is estimated at CFAF 2.5 billion per year.

- 26 -

Table 2.17: COMPARISON OF RETAIL PRICES INNEIGHBORING COUNTRIES, 1983

(FCFA/li ter)

GasolinePremium Regular Gas Oii

Togo 205 200 180

Benin 165 162 132Burkina 285 272 240Niger 240 225 170

Nigeria 104 88 68

Ghana a- 140 116 88

a/ Prices being increased in line with IMF agree-

ment.

2.47 Another feature of the past trend is the very high rate ofgrowth in premium gasoline consumption. This partly reflects theunusually small retail price differential (2.5% compared to a moretypical 5-10%) between the two fuel grades, 10/ and that a significantportion of the market is represented by customers that are less pricesensitive. It is estimated that transport diesel consumption increasedat about 8.6% during 1975-80, and continued to grow through 1982.

2.48 A recent transport study provides basic data for estimatingfuel consumption in each of the road market segments and assessing energysaving opportunities. The mission estimates that about 60% of roaddiesel is used in the international freight transit, and about 20% eachin national interurban and intraurban freight traffic. About 80% of thegasoLine is consumed in passenger transport, 20% for freight (Annexes 27,28 & 29).

2.49 The mission estimates the maximum theoretical energy savingsfrom possible shifts of traffic from less to more efficient transportmodes, and by improvements within modes, at about 20,000 m , or about 20%of the total 1982 gasoline and diesel road consumption (Table 2.18).Realistically perhaps only one-third of these savings can be achieved,which represents a foreign exchange savings of almost one million U.S.dollars per year.

10/ These differentials are not justified in terms of the quality: asin other import markets in the region, premium gasoline averagessome 90 octane against approximately 85 for regular.

- 27 -

Table 2.18: MAXIMUM THEORETICAL ENERGY SAVINGS IN THE

TRANSPORT SECTOR

% of Transport FueisType of Measure Volume Diesel Gasoline

(m3)

Shift of traffic to theLome-Blitta railroad line 6,100

Coliective transport 5,000 8

Engine Efficiency 6,500 10

Yore intensive use ofexisting fleet 2,000 6

Source: Mission estimate.

Shift from Road to Railroad

2.50 The share of the Chemin de Fer Togolais (CTF) in total trans-port supply has fallen to less than 12% of the national and internationalfreight demand (1.76 million tons in 1982) and to 13% of passengertraffic (19.1 million). The railroad action plan, currently underreview, considers that the Lome-Blitta railroad line (276 km) couldbecome an important carrier for heavy bulk transport such as cement,hydrocarbons and containers directed towards northern Togo and theSahel. 11/ The estimate of maximum theoretical savings is based on theassumption that the energy intensity of railways is about one-fourth thatof trucks 12/, and that 100% of the 1982 northbound traffic (580,000tonnes) would be shifted to the railroad. Given this important savingspotential, the mission fully supports the establishment of a marketpromotion office within CFT, as proposed in the Action Plan. It furthersuggests that a detailed tariff analysis be made, in order to establisheconomically viable but competitive railroad rates for the Lome-Blittaline.

11/ The use of containers is rapidly growing at the Lome port, from7,000 units in 1976 to 37,000 units in 1982.

12/ For 1980, the energy intensity of the Lome-Tabligbo line was 9.9grams of oil equivalent per ton-km (goe/t-km), well in line withinternational standards, although the clinker plant had barelystarted operations. However, the other three lines had an energyintensity of 44 goe/t-km, due to low load factors and probably tomismanagement. It is to be expected that with increased traffic andtighter controls on the use of diesel oil, the Lome-BLitta linecould achieve an energy efficiency similar to that of the Lom6-Tabligbo line.

- 28 -

Improved Efficiency within the Road Transport Mode

2.51 Collective Passenger Traffic. The rate of motorization inTogo 13/ is still only 4.5 vehicles per 1,000 persons in 1982, althoughthe number of new vehicles registered each year increased at a rate ofnine percent per annum between 1975 and 1981. About 80% of all passengervehicles are registered in Lome. The city, with 370,000 inhabitants,already confronts traffic congestion in the main feeder roads towards thecenter. Collective transport services currently are restricted to taxisand mini buses. Larger bus service is practically non-existent, sinceservice with units of more than eight seats is reserved for municipalinstitutions which do not have the financial resources to provide them.It should be noted that in early 1985 the Government imported about 100Japanese mini-buses, which are to be transferred to the private sectorfor service in Lome. It is advisable to also consider introducing busesin inter-city traffic, replacing the traditional taxi-brousse, on routesof high enough passenger demand, such as Lom6 Aneho, where bus servicecould replace inefficient railroad service.

2.52 Expansion of the coLlective transport systems should bepromoted to reduce energy consumption and investment requirements forenlarging the road infrastructure in Lome. However, the policy must takeinto account: (a) the Government's financial constraints; (b) the entre-preneurship of the Togolese people; (c) the characteristics of the pre-sent service, i.e., service from door-to-door and short waiting times;and (d) the relatively low load factor to be expected in the outskirts.