5-1 pyright © 2004 by Nelson, a division of Thomson Canada Limited. Job-Order Job-Order Costing Costing 5 5 PowerPresentation® prepared by PowerPresentation® prepared by David J. McConomy, Queen’s David J. McConomy, Queen’s University University

5-1 Copyright © 2004 by Nelson, a division of Thomson Canada Limited. Job-Order Costing 5 PowerPresentation® prepared by David J. McConomy, Queen’s University.

Dec 26, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

5-1Copyright © 2004 by Nelson, a division of Thomson Canada Limited.

Job-OrderJob-OrderCostingCosting

55

PowerPresentation® prepared by PowerPresentation® prepared by

David J. McConomy, Queen’s UniversityDavid J. McConomy, Queen’s University

5-2Copyright © 2004 by Nelson, a division of Thomson Canada Limited.

Learning ObjectivesLearning Objectives

Describe the differences between job-order

costing and process costing, and identify

the types of organizations that would use

each method.

Identify and set up the source documents

used in job-order costing.

5-3Copyright © 2004 by Nelson, a division of Thomson Canada Limited.

Learning ObjectivesLearning Objectives

Discuss the cost flows associated with job-order costing.

Prepare the journal entries associated with job-order costing (Appendix).

5-4Copyright © 2004 by Nelson, a division of Thomson Canada Limited.

Comparison of Job-Order andComparison of Job-Order andProcess CostingProcess Costing

Job-Order Costing Process Costing

1. Wide variety of distinct 1. Homogeneous products

products

2. Cost accumulated by job 2. Costs accumulated by

process or department

3. Unit cost computed by 3. Unit cost computed by

dividing total job costs dividing process costs of

by units produced on that the period by the units

job produced in the period

5-5Copyright © 2004 by Nelson, a division of Thomson Canada Limited.

Johnson Leathergoods - ExampleJohnson Leathergoods - Example

Suppose that Stan Johnson forms a new company,

Johnson Leathergoods, which specializes in the

production of custom leather products. Stan believes

that there is a market for one-of-a-kind leather purses,

briefcases, and backpacks. In its first month of

operation, he obtains two orders: the first is for 20

leather backpacks for a local sporting goods store; the

second is for 10 distinctively tooled briefcases for the

coaches of a local college. Stan agrees to provide these

orders at a price of cost plus 50 percent.

5-6Copyright © 2004 by Nelson, a division of Thomson Canada Limited.

Johnson Leathergoods - Unit CostJohnson Leathergoods - Unit Cost

Direct materials $1,000

Direct labour 1,080

Overhead 240

Total cost $2,320

number of units 20

Unit cost $ 116

======

5-7Copyright © 2004 by Nelson, a division of Thomson Canada Limited.

Job Order Cost SheetJob Order Cost Sheet

(1) 1,000 (2) 1,080 (3) 240 (1) 500 (2) 450 (3) 100

2,320 1,050

Backpacks Briefcases

5-8Copyright © 2004 by Nelson, a division of Thomson Canada Limited.

A Job Order Cost SheetA Job Order Cost Sheet

Item Description: _________ Job Order Number: _______Quantity Competed: ______ Date Started: _____________ Date Completed:_________

Direct Materials Direct labour Overhead

Req. No. Amount Ticket # Hours Rate Amt. Hours Rate Amt. 24-A $ 30 49 40 $9 $360 40 $2.00 $8046-B 970 71 80 9 720 80 3.00 160

Cost Summary Direct Materials_______ Total Costs_________ Direct labour _______ Unit Cost _________ Overhead _______

$1,000$1,080$ 240

$2,320$116.00

Backpacks20

16-C1/25/01

1/31/01

5-9Copyright © 2004 by Nelson, a division of Thomson Canada Limited.

A Materials Requisition A Materials Requisition FormForm

Requisition No._______Date:______ Department___________ Job No._____

Description Quantity Cost/Unit Total Cost

Delivered By___________ Received by______________

24-A1/25/01 Fabrication 16-C

Buckles 10 $3.00 $30

J. Jones D. Reller

5-10Copyright © 2004 by Nelson, a division of Thomson Canada Limited.

A Job Time TicketA Job Time Ticket

Employee No.______ Name____________ Date_________

Start Time Stop Time Total Time Rate Amt. Job No.

8:00 a.m. 4:00 p.m. 8.0 hours $9 $ 72 16-C

Ticket No._________49

101 F. Flintstone 1/24/01

Approved by __________________________ Department Supervisor

8:00 a.m. 4:00 p.m. 8.0 hours $9 $ 72 16-C

8:00 a.m. 4:00 p.m. 8.0 hours $9 $ 72 16-C

8:00 a.m. 4:00 p.m. 8.0 hours $9 $ 72 16-C

8:00 a.m. 4:00 p.m. 8.0 hours $9 $ 72 16-C

5-11Copyright © 2004 by Nelson, a division of Thomson Canada Limited.

Job-Order Costing –Job-Order Costing –Material PurchasesMaterial Purchases

A. Raw materials account is debited for the cost of

materials purchased

Raw Materials Work in Process

2,5000

5-12Copyright © 2004 by Nelson, a division of Thomson Canada Limited.

Johnson LeathergoodsJohnson Leathergoods

A. Materials costing $2,500 were purchased on account.

Raw Materials 2,500

Accounts Payable2,500

5-13Copyright © 2004 by Nelson, a division of Thomson Canada Limited.

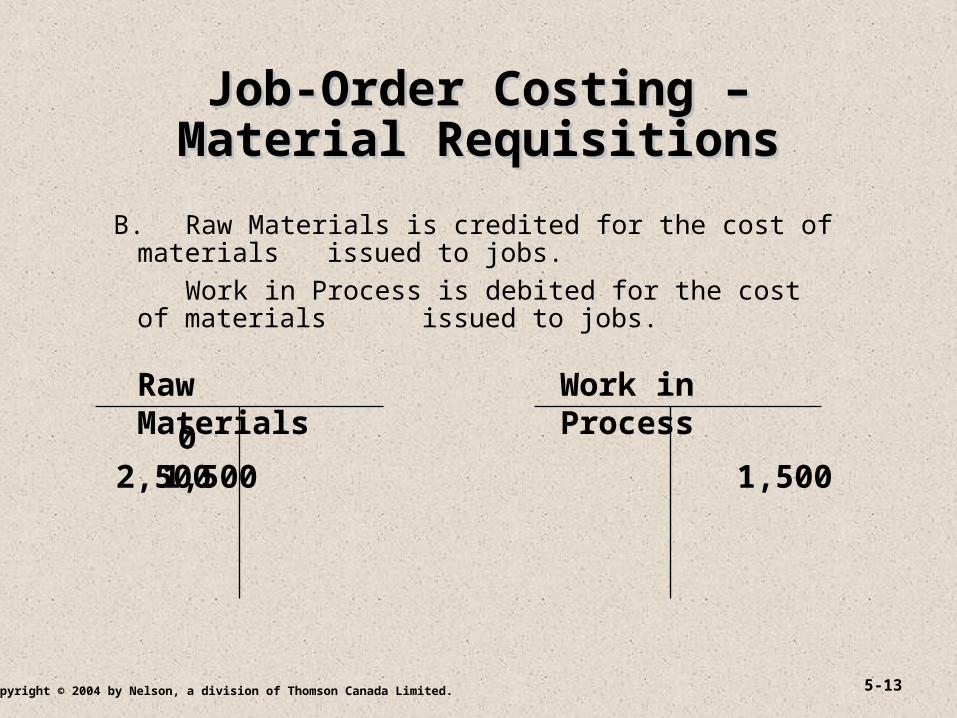

Job-Order Costing –Job-Order Costing –Material RequisitionsMaterial Requisitions

B. Raw Materials is credited for the cost of materials issued to jobs.

Work in Process is debited for the cost of materials issued to jobs.

Raw Materials Work in Process

2,500 1,500 1,5000

5-14Copyright © 2004 by Nelson, a division of Thomson Canada Limited.

Johnson Leathergoods (continued)Johnson Leathergoods (continued)

B. Materials totaling $1,500 were requisitioned for use in production, $1,000 for 20 Backpacks and the remainder for the 10 Briefcases.

Work in Process 1,500

Raw Materials1,500

5-15Copyright © 2004 by Nelson, a division of Thomson Canada Limited.

Job-Order Costing –Job-Order Costing –Direct Labour IncurredDirect Labour Incurred

C. Wages Payable is credited for the cost of direct labour.

Work in Process is debited for the cost of direct labour.

Wages Payable Work in Process

1,530 1,530

1,500

5-16Copyright © 2004 by Nelson, a division of Thomson Canada Limited.

Johnson Leathergoods (continued)Johnson Leathergoods (continued)

C. During the month, direct labourers worked 120 hours on the Backpacks and 50 hours on the Briefcases. Direct labourers are paid at the rate of $9 per hour.

Work in Process 1,530

Wages Payable1,530

5-17Copyright © 2004 by Nelson, a division of Thomson Canada Limited.

Job-Order Costing Job-Order Costing Actual OverheadActual Overhead

D. Overhead Control is debited for actual overhead.

Overhead Control Work in Process

415

5-18Copyright © 2004 by Nelson, a division of Thomson Canada Limited.

Johnson Leathergoods(cont’d)Johnson Leathergoods(cont’d)

D. Actual overhead for the month was $415 and was paid in cash.

Overhead Control 415

Cash415

5-19Copyright © 2004 by Nelson, a division of Thomson Canada Limited.

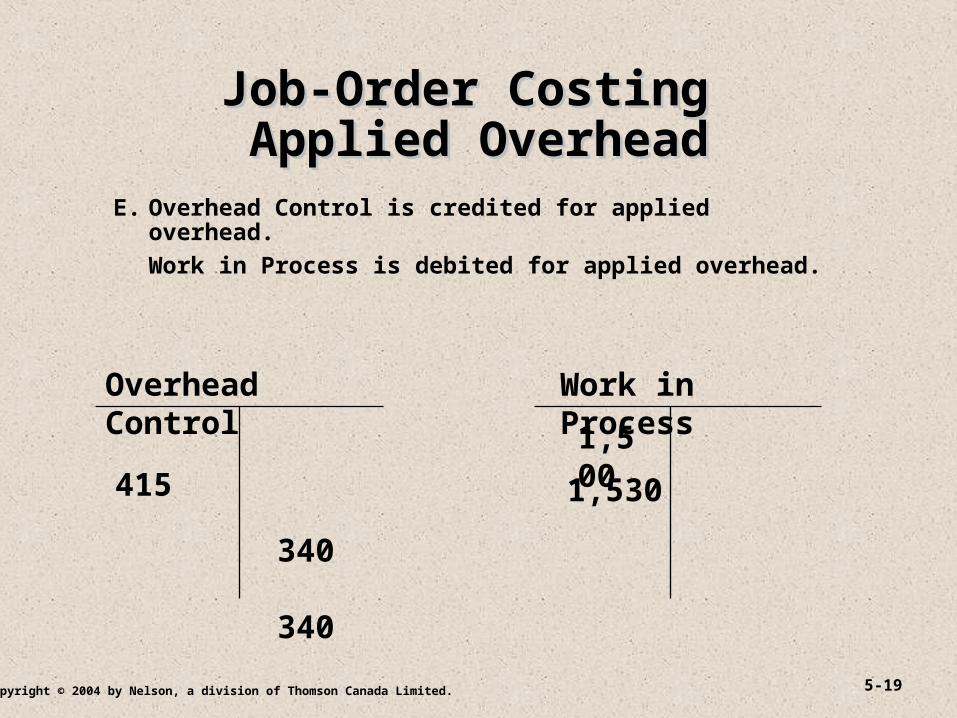

Job-Order Costing Job-Order Costing Applied OverheadApplied Overhead

E. Overhead Control is credited for applied overhead.

Work in Process is debited for applied overhead.

Overhead Control Work in Process

415

340 340

1,500

1,530

5-20Copyright © 2004 by Nelson, a division of Thomson Canada Limited.

Johnson Leathergoods (continued)Johnson Leathergoods (continued)

E. Overhead is applied using a plantwide rate of $2.00 per direct labour hour.

Work in Process 340

Overhead Control340

5-21Copyright © 2004 by Nelson, a division of Thomson Canada Limited.

Job-Order Costing –Job-Order Costing –Transfer of Completed GoodsTransfer of Completed Goods

F. Credit Work in Process for the COGM.

Debit Finished Goods for the COGM.

Work in Process Finished Goods

1,5001,530 340

2,320 2,320

5-22Copyright © 2004 by Nelson, a division of Thomson Canada Limited.

Johnson Leathergoods (continued)Johnson Leathergoods (continued)

F. The Backpacks were completed and transferred to Finished Goods.

Finished Goods 2,320

Work in Process2,320

5-23Copyright © 2004 by Nelson, a division of Thomson Canada Limited.

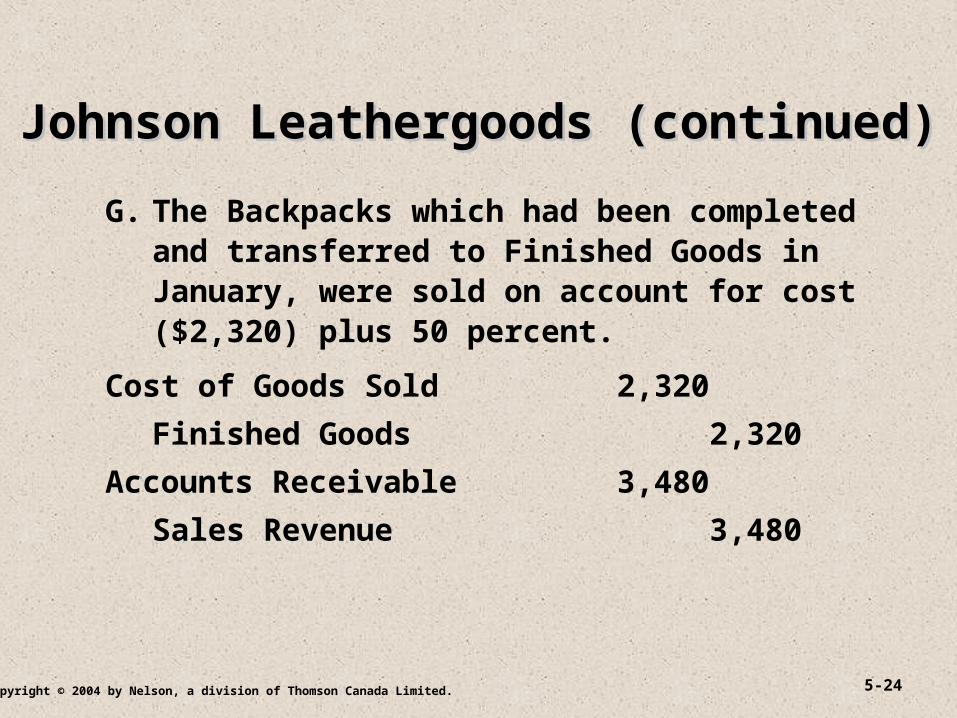

Job-Order Costing –Job-Order Costing –Recognition of ExpenseRecognition of Expense

G. Credit Finished Goods for value of units sold.

Debit Cost of Goods Sold for value of units sold.

Finished Goods Cost of Goods Sold

2,320 2,320

5-24Copyright © 2004 by Nelson, a division of Thomson Canada Limited.

Johnson Leathergoods (continued)Johnson Leathergoods (continued)

G. The Backpacks which had been completed and transferred to Finished Goods in January, were sold on account for cost ($2,320) plus 50 percent.

Cost of Goods Sold 2,320

Finished Goods2,320

Accounts Receivable 3,480

Sales Revenue3,480

5-25Copyright © 2004 by Nelson, a division of Thomson Canada Limited.

The Basic Concept of The Basic Concept of Overhead ApplicationOverhead Application

Applied overhead = Overhead rate x Actual production

activity

Applied overhead is the basis for computing per-unit overhead cost.

Applied overhead is rarely equal to a period's actual overhead costs.

Two Basic Points to Emphasized:

Related Documents