April 13, 2017 ICICI Securities Ltd | Retail Equity Research Result Update Tweaks margin band, Payout Policy… Infosys’ Q4FY17 performance was below our expectation on the operational front. US$ revenues grew 0.7% QoQ to $2,569 million, below 1.7% growth and $2,594.6 million estimate. Constant currency revenues were flat QoQ vs. our estimate of 2% QoQ Rupee revenues declined 0.9% QoQ to | 17,120 crore, below our 0.5% QoQ growth and | 17,358 crore estimate EBIT margins at 24.6% declined 50 bps QoQ and were below our estimate of 25.1% largely on account of slower revenue growth Reported PAT of | 3,603 crore was above our | 3,569.5 crore estimate led by lower tax expense The company announced a dividend of | 14.75 per share Guides for CC revenue guidance of 6.5-8.5% for FY18E… Infosys’ dollar revenues grew 0.7% sequentially to $2,569 million, below our 1.7% growth and $2,594.6 million estimate. Constant currency revenues were flat QoQ owing to weaker execution and drag in India geography revenues (declined 6.9% in CC terms) and retail, CPG & Lifesciences (declined 3.1% in CC terms). Going ahead, the management is optimistic about BFSI while retail and hi-tech could see some softness in the coming quarters. The company has guided for 6.5-8.5% CC revenue growth vs. our estimate of 7-9% citing a challenging demand environment and uncertain client spending among a few verticals. The revenue guidance implies growth of 2.1-2.9% QoQ over the next four quarters. Furthermore, the management remained optimistic about adoption of new offerings Skava, Mana, Panaya and Edge across verticals and cited that revenues from these offerings grew at ~20% YoY in FY17. Lowers EBIT margin band to 23-25% in FY18E… Infosys’ EBIT margins declined 50 bps QoQ to 24.6% in Q4FY17 below our expectation of 25.1%. Margins declined owing to rupee appreciation (35 bps impact), decline in realisation (65 bps impact) offset by cross currency tailwind and revenue hedges (50 bps) and operational efficiency. The management revised its targeted EBIT margin band downward to 23- 25% vs. 24-26% earlier due to rupee appreciation (70 bps impact), ramp up of onsite development centres in US to mitigate any visa concerns. Recast of capital allocation policy… The Board revised the capital allocation policy of the company after taking into consideration the strategic and operational cash requirements of Infosys in the medium term. The company plans to pay ~| 13,000 crore via dividend/share buyback to shareholders in FY18E. Additionally, effective from FY18E, Infosys revised its payout policy to 70% of free cash flow from ~50% of PAT earlier. The revised capital allocation policy seems to be a positive step in shareholder value creation. Maintain BUY with revised target price of | 1060… Though Infosys surprised negatively on the EBIT margin guidance front, we believe the current market price is already priced in. Currently, it is trading at attractive valuation of ~13.2x FY19 EPS & offers FY19 FCF yield of ~5%. Secondly, Infosys intends to return part of the cash and recast capital allocation policy that are steps in the right direction towards shareholder value creation. Hence, we maintain our BUY recommendation on the stock. We also roll over to FY19E and revise our target price to | 1060 (15x FY19E). Rating matrix Rating : Buy Target : | 1060 Target Period : 12 months Potential Upside : 14% What’s Changed? Target Changed from |1110 to |1060 EPS FY18E Changed from | 69.2 to | 64.6 EPS FY19E Introduced at | 70.7 Rating Unchanged Quarterly Performance Q4FY17 Q4FY16 YoY (%) Q3FY17 QoQ (%) Revenue 17,120 16,550 3.4 17,273 (0.9) EBIT 4,212 4,220 (0.2) 4,334 (2.8) EBIT (%) 24.6 25.5 -90 bps 25.1 -49 bps PAT 3,603 3,598 0.1 3,707 (2.8) Key Financials | Crore FY16 FY17E FY18E FY19E Net Sales 62,441 68,485 71,406 79,411 EBITDA 17,079 18,605 18,851 21,123 Net Profit 13,491 14,353 13,983 15,315 EPS (|) 59.0 62.8 64.6 70.7 Valuation summary FY16 FY17E FY18E FY19E P/E 15.8 14.8 14.4 13.1 Target P/E 18.0 16.9 16.4 15.0 EV / EBITDA 10.4 9.3 9.6 8.3 P/BV 3.4 3.1 3.2 2.9 RoNW (%) 21.8 20.8 22.3 21.7 RoCE (%) 30.2 28.8 31.0 30.5 Stock data Particular Amount Market Capitalization (| Crore) 212,553.7 Total Debt - Cash and Investments 32,697.0 EV (| Crore) 178,045.7 52 week H/L 1278 / 900 Equity capital 1,144.0 Face value | 5 Price performance (%) 1M 3M 6M 12M TCS (6.8) 3.9 1.1 (1.6) Infosys (6.4) (0.2) (4.3) (16.9) Wipro (0.1) 6.1 5.0 (8.9) HCL Tech (2.6) (0.8) 3.1 (0.2) Research Analysts Deepak Purswani, CFA [email protected] Deepti Tayal [email protected] Infosys (INFTEC) | 930

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

April 13, 2017

ICICI Securities Ltd | Retail Equity Research

Result Update

Tweaks margin band, Payout Policy…

Infosys’ Q4FY17 performance was below our expectation on the

operational front. US$ revenues grew 0.7% QoQ to $2,569 million,

below 1.7% growth and $2,594.6 million estimate. Constant currency

revenues were flat QoQ vs. our estimate of 2% QoQ

Rupee revenues declined 0.9% QoQ to | 17,120 crore, below our

0.5% QoQ growth and | 17,358 crore estimate

EBIT margins at 24.6% declined 50 bps QoQ and were below our

estimate of 25.1% largely on account of slower revenue growth

Reported PAT of | 3,603 crore was above our | 3,569.5 crore

estimate led by lower tax expense

The company announced a dividend of | 14.75 per share

Guides for CC revenue guidance of 6.5-8.5% for FY18E…

Infosys’ dollar revenues grew 0.7% sequentially to $2,569 million, below

our 1.7% growth and $2,594.6 million estimate. Constant currency

revenues were flat QoQ owing to weaker execution and drag in India

geography revenues (declined 6.9% in CC terms) and retail, CPG &

Lifesciences (declined 3.1% in CC terms). Going ahead, the management

is optimistic about BFSI while retail and hi-tech could see some softness

in the coming quarters. The company has guided for 6.5-8.5% CC

revenue growth vs. our estimate of 7-9% citing a challenging demand

environment and uncertain client spending among a few verticals. The

revenue guidance implies growth of 2.1-2.9% QoQ over the next four

quarters. Furthermore, the management remained optimistic about

adoption of new offerings Skava, Mana, Panaya and Edge across verticals

and cited that revenues from these offerings grew at ~20% YoY in FY17.

Lowers EBIT margin band to 23-25% in FY18E…

Infosys’ EBIT margins declined 50 bps QoQ to 24.6% in Q4FY17 below

our expectation of 25.1%. Margins declined owing to rupee appreciation

(35 bps impact), decline in realisation (65 bps impact) offset by cross

currency tailwind and revenue hedges (50 bps) and operational efficiency.

The management revised its targeted EBIT margin band downward to 23-

25% vs. 24-26% earlier due to rupee appreciation (70 bps impact), ramp

up of onsite development centres in US to mitigate any visa concerns.

Recast of capital allocation policy…

The Board revised the capital allocation policy of the company after taking

into consideration the strategic and operational cash requirements of

Infosys in the medium term. The company plans to pay ~| 13,000 crore

via dividend/share buyback to shareholders in FY18E. Additionally,

effective from FY18E, Infosys revised its payout policy to 70% of free cash

flow from ~50% of PAT earlier. The revised capital allocation policy

seems to be a positive step in shareholder value creation.

Maintain BUY with revised target price of | 1060…

Though Infosys surprised negatively on the EBIT margin guidance front,

we believe the current market price is already priced in. Currently, it is

trading at attractive valuation of ~13.2x FY19 EPS & offers FY19 FCF yield

of ~5%. Secondly, Infosys intends to return part of the cash and recast

capital allocation policy that are steps in the right direction towards

shareholder value creation. Hence, we maintain our BUY

recommendation on the stock. We also roll over to FY19E and revise our

target price to | 1060 (15x FY19E).

Rating matrix

Rating : Buy

Target : | 1060

Target Period : 12 months

Potential Upside : 14%

What’s Changed?

Target Changed from |1110 to |1060

EPS FY18E Changed from | 69.2 to | 64.6

EPS FY19E Introduced at | 70.7

Rating Unchanged

Quarterly Performance

Q4FY17 Q4FY16 YoY (%) Q3FY17 QoQ (%)

Revenue 17,120 16,550 3.4 17,273 (0.9)

EBIT 4,212 4,220 (0.2) 4,334 (2.8)

EBIT (%) 24.6 25.5 -90 bps 25.1 -49 bps

PAT 3,603 3,598 0.1 3,707 (2.8)

Key Financials

| Crore FY16 FY17E FY18E FY19E

Net Sales 62,441 68,485 71,406 79,411

EBITDA 17,079 18,605 18,851 21,123

Net Profit 13,491 14,353 13,983 15,315

EPS (|) 59.0 62.8 64.6 70.7

Valuation summary

FY16 FY17E FY18E FY19E

P/E 15.8 14.8 14.4 13.1

Target P/E 18.0 16.9 16.4 15.0

EV / EBITDA 10.4 9.3 9.6 8.3

P/BV 3.4 3.1 3.2 2.9

RoNW (%) 21.8 20.8 22.3 21.7

RoCE (%) 30.2 28.8 31.0 30.5

Stock data

Particular Amount

Market Capitalization (| Crore) 212,553.7

Total Debt -

Cash and Investments 32,697.0

EV (| Crore) 178,045.7

52 week H/L 1278 / 900

Equity capital 1,144.0

Face value | 5

Price performance (%)

1M 3M 6M 12M

TCS (6.8) 3.9 1.1 (1.6)

Infosys (6.4) (0.2) (4.3) (16.9)

Wipro (0.1) 6.1 5.0 (8.9)

HCL Tech (2.6) (0.8) 3.1 (0.2)

Research Analysts

Deepak Purswani, CFA

Deepti Tayal

Infosys (INFTEC) | 930

ICICI Securities Ltd | Retail Equity Research Page 2

Variance analysis

Q4FY17 Q4FY17E Q4FY16 YoY (%) Q3FY17 QoQ (%) Comments

Revenue 17,120 17,358 16,550 3.4 17,273 -0.9

Infosys' $ revenue grew 0.7% sequentially well below our expectation of 1.7%

growth

Employee expenses 10,324 10,466 9,843 4.9 10,407 -0.8

Gross Profit 6,796 6,892 6,707 1.3 6,866 -1.0

Gross margin (%) 39.7 39.7 40.5 -83 bps 39.7 -5 bps

Selling & marketing costs 889 889 909 -2.2 885 0.5

G&A expenses 1,249 1,220 1,159 7.8 1,214 2.9

EBITDA 4,658 4,784 4,639 0.4 4,767 -2.3

EBITDA Margin (%) 27.2 27.6 28.0 -82 bps 27.6 -39 bps

Depreciation 446 435 419 6.4 433 3.0

EBIT 4,212 4,348 4,220 -0.2 4,334 -2.8

EBIT Margin (%) 24.6 25.1 25.5 -90 bps 25.1 -49 bps

EBIT margin performance came below our expectation due to slower revenue

growth

Other income 721 788 772 -6.6 820 -12.1

PBT 4,933 5,136 4,992 -1.2 5,154 -4.3

Tax paid 1,330 1,566 1,394 -4.6 1,446 -8.0

PAT 3,603 3,570 3,598 0.1 3,707 -2.8 The bottomline was above our expectation led by lower tax expense

Key Metrics

Closing employees 200,364 200,000 194,044 3.3 199,763 0.3

LTM attrition-standalone (%) 13.5 14.0 13.6 -8 bps 14.9 -140 bps

Utilisation - IT Services (%) 82.0 81.0 80.1 190 bps 81.9 10 bps Higher utilisation YoY

Average $/| 66.6 66.9 67.7 -1.7 67.7 -1.6

Source: Company, ICICIdirect.com Research

Change in estimates

FY18E FY19E

(| Crore) Old New % Change Introduced Comments

Revenue 76,165 71,406 -6.2 79,411

EBIT 19,041 17,138 -10.0 19,217

EBIT Margin (%) 25.0 24.0 -105 bps 24.2 Revised margin estimates due to rupee estimates and US visa policy concerns

PAT 15,975 13,983 -12.5 15,315

EPS (|) 69.9 64.6 -7.6 70.7 Change in EPS estimates owing to change in EBIT margin revision

Source: Company, ICICIdirect.com Research

Assumptions

Current Earlier Introduced Comments

FY15 FY16 FY17E FY18E FY18E FY19E

Closing employees 176,187 194,044 200,364 200,309 213,851 207,265

Utilisation - IT Services (%) 69.4 71.2 75.4 76.3 84.3 81.2

Average $/| 54.5 65.7 67.1 65.0 68.0 66.0 Tweaked exchange rate estimates owing to recent rupee appreciation

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 3

Company Analysis

Revisits its CC revenue guidance to 6.5-8.5% in FY18E …

The company has guided for 6.5-8.5% CC revenue growth vs. our

estimate of 7-9% citing challenging environment and uncertain client

spending among few verticals. We now anticipate Infosys US$ revenue

will grow 7.6%, 9.5% in FY18E, FY19E, respectively. The management

said revenues from new software and software related services including

Mana, Panaya, Skava and Edge grew ~42% YoY in FY17. Infosys has

appointed Independent Director Ravikumar Venkatesan as Co-Chairman

of the Board.

Infosys won six large deals worth US$806 million during the quarter

implying a growth rate of ~6.5% YoY. Total order book for FY17 was up

~25% YoY. The aspirational target is to get total contract value (TCV) to

$1 billion. We believe strong deal wins may witness healthy growth in

FY18E.

Exhibit 1: Dollar revenues may grow at 8.2% CAGR in FY16-19E vs. 9.5% CAGR in FY11-16 7398

8249

8711

2256

2392

2407

2446

9501

2501

2587

2551

2569

10208

10986

12032

5.8

11.5

5.65.8

8.7

8.5

13.3

9.1

10.9

8.2

6.05.0

7.47.6

9.5

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

0

2000

4000

6000

8000

10000

12000

14000

FY13

FY14

FY15

Q1FY16

Q2FY16

Q3FY16

Q4FY16

FY16

Q1FY17

Q2FY17

Q3FY17

Q4FY17

FY17E

FY18E

FY19E

$ m

illion

Dollar revenue Growth, YoY

Source: Company, ICICIdirect.com Research

Exhibit 2: Infosys growth vs. Nasscom guidance

5.8

11.5

5.6

9.17.7

9.1 8.6

13.0 13.0 13

9.0

9.0

8.0 7.0

10.2

-5

3

11

19

27

35

FY13 FY14 FY15 FY16 FY17E

%

Growth, YoY Company guidance (mid-point) NASSCOM guidance (mid-point)

Source: Company, ICICIdirect.com Research

Optimistic about BFSI…

Among geographies, North America (62.3% of revenue) grew 1.2% in CC

while Europe (22.1% of revenue), India (3.2%) and RoW (12.4%)

witnessed a decline of 1.6%, 6.9% and 1.3% QoQ in CC terms,

respectively. Among industries, BFSI (33.5% of revenue) grew 0.5% in CC

basis while manufacturing (22.4%) was flat QoQ. RCL (22.7%) and ECS

ICICI Securities Ltd | Retail Equity Research Page 4

(21.4%) witnessed 3.1% and 2.8% CC decline, respectively. Going ahead,

the management is optimistic about BFSI while retail and hi-tech could

see some softness in coming quarters.

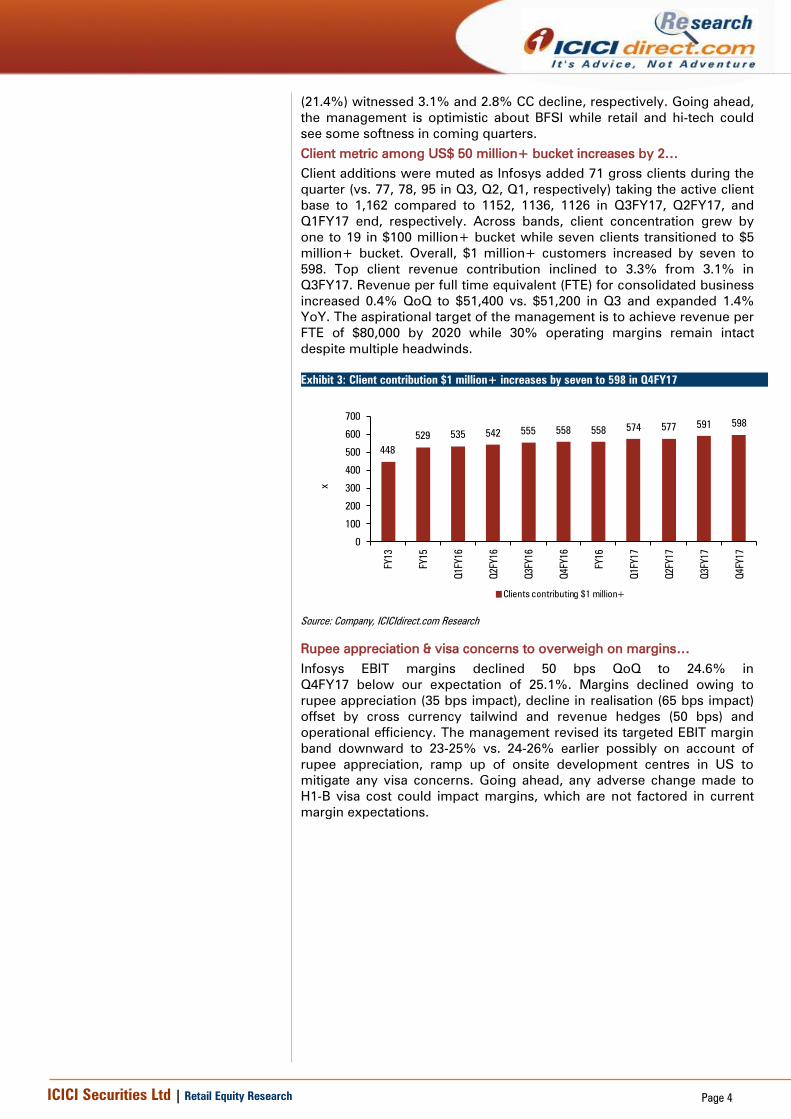

Client metric among US$ 50 million+ bucket increases by 2…

Client additions were muted as Infosys added 71 gross clients during the

quarter (vs. 77, 78, 95 in Q3, Q2, Q1, respectively) taking the active client

base to 1,162 compared to 1152, 1136, 1126 in Q3FY17, Q2FY17, and

Q1FY17 end, respectively. Across bands, client concentration grew by

one to 19 in $100 million+ bucket while seven clients transitioned to $5

million+ bucket. Overall, $1 million+ customers increased by seven to

598. Top client revenue contribution inclined to 3.3% from 3.1% in

Q3FY17. Revenue per full time equivalent (FTE) for consolidated business

increased 0.4% QoQ to $51,400 vs. $51,200 in Q3 and expanded 1.4%

YoY. The aspirational target of the management is to achieve revenue per

FTE of $80,000 by 2020 while 30% operating margins remain intact

despite multiple headwinds.

Exhibit 3: Client contribution $1 million+ increases by seven to 598 in Q4FY17

448

529 535 542 555 558 558574 577 591 598

0

100

200

300

400

500

600

700

FY13

FY15

Q1FY16

Q2FY16

Q3FY16

Q4FY16

FY16

Q1FY17

Q2FY17

Q3FY17

Q4FY17

x

Clients contributing $1 million+

Source: Company, ICICIdirect.com Research

Rupee appreciation & visa concerns to overweigh on margins…

Infosys EBIT margins declined 50 bps QoQ to 24.6% in

Q4FY17 below our expectation of 25.1%. Margins declined owing to

rupee appreciation (35 bps impact), decline in realisation (65 bps impact)

offset by cross currency tailwind and revenue hedges (50 bps) and

operational efficiency. The management revised its targeted EBIT margin

band downward to 23-25% vs. 24-26% earlier possibly on account of

rupee appreciation, ramp up of onsite development centres in US to

mitigate any visa concerns. Going ahead, any adverse change made to

H1-B visa cost could impact margins, which are not factored in current

margin expectations.

ICICI Securities Ltd | Retail Equity Research Page 5

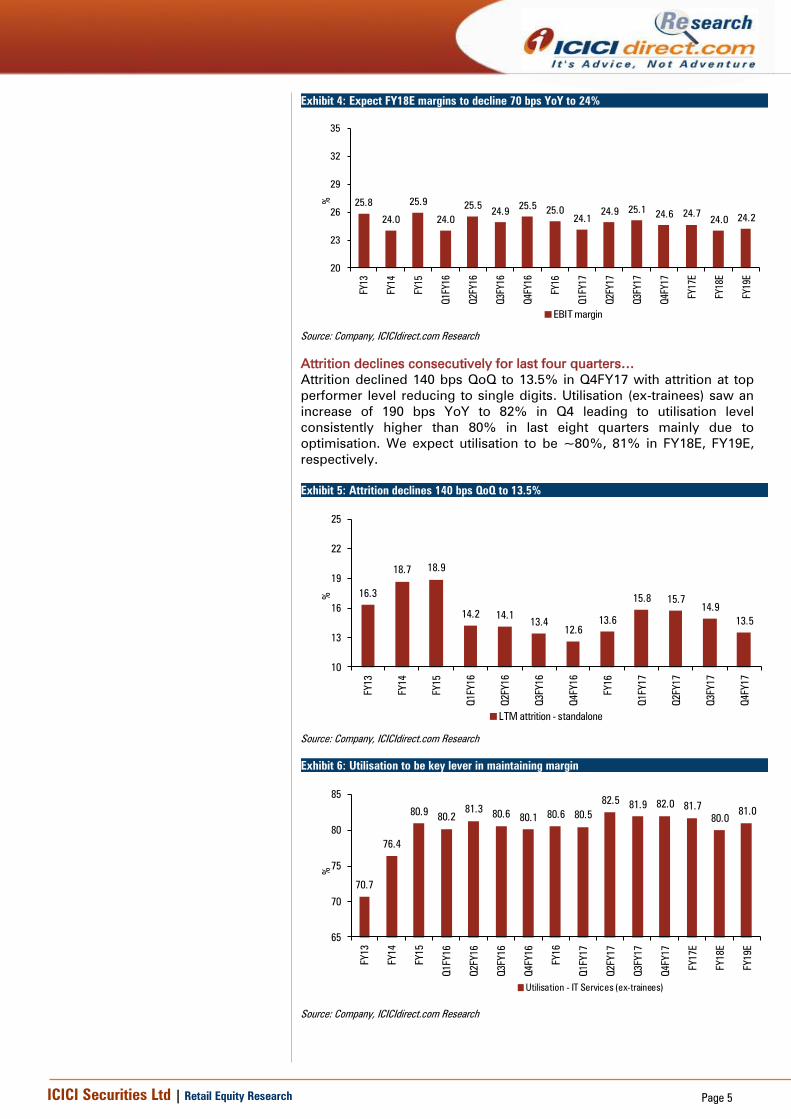

Exhibit 4: Expect FY18E margins to decline 70 bps YoY to 24%

25.8

24.0

25.9

24.0

25.524.9

25.525.0

24.1

24.9 25.124.6 24.7

24.0 24.2

20

23

26

29

32

35

FY13

FY14

FY15

Q1FY16

Q2FY16

Q3FY16

Q4FY16

FY16

Q1FY17

Q2FY17

Q3FY17

Q4FY17

FY17E

FY18E

FY19E

%

EBIT margin

Source: Company, ICICIdirect.com Research

Attrition declines consecutively for last four quarters…

Attrition declined 140 bps QoQ to 13.5% in Q4FY17 with attrition at top

performer level reducing to single digits. Utilisation (ex-trainees) saw an

increase of 190 bps YoY to 82% in Q4 leading to utilisation level

consistently higher than 80% in last eight quarters mainly due to

optimisation. We expect utilisation to be ~80%, 81% in FY18E, FY19E,

respectively.

Exhibit 5: Attrition declines 140 bps QoQ to 13.5%

16.3

18.7 18.9

14.2 14.113.4

12.6

13.6

15.8 15.7

14.9

13.5

10

13

16

19

22

25

FY13

FY14

FY15

Q1FY16

Q2FY16

Q3FY16

Q4FY16

FY16

Q1FY17

Q2FY17

Q3FY17

Q4FY17

%

LTM attrition - standalone

Source: Company, ICICIdirect.com Research

Exhibit 6: Utilisation to be key lever in maintaining margin

70.7

76.4

80.980.2

81.380.6

80.180.6 80.5

82.581.9 82.0 81.7

80.0

81.0

65

70

75

80

85

FY13

FY14

FY15

Q1FY16

Q2FY16

Q3FY16

Q4FY16

FY16

Q1FY17

Q2FY17

Q3FY17

Q4FY17

FY17E

FY18E

FY19E

%

Utilisation - IT Services (ex-trainees)

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 6

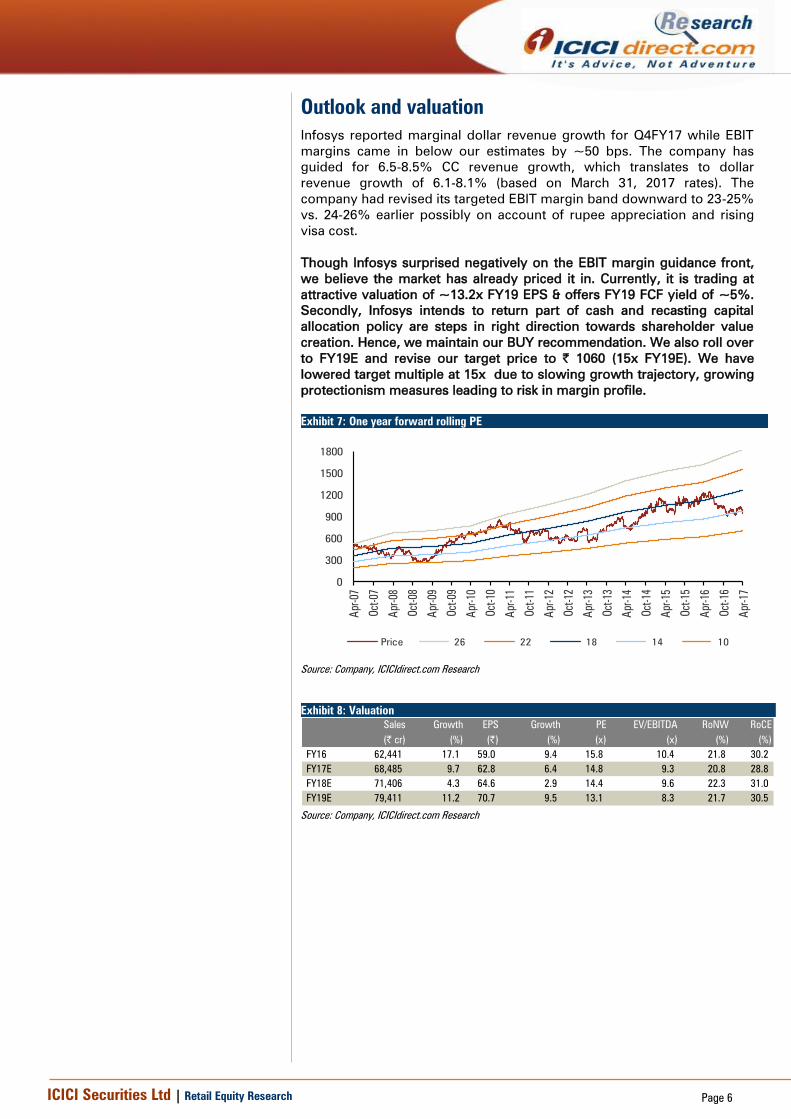

Outlook and valuation

Infosys reported marginal dollar revenue growth for Q4FY17 while EBIT

margins came in below our estimates by ~50 bps. The company has

guided for 6.5-8.5% CC revenue growth, which translates to dollar

revenue growth of 6.1-8.1% (based on March 31, 2017 rates). The

company had revised its targeted EBIT margin band downward to 23-25%

vs. 24-26% earlier possibly on account of rupee appreciation and rising

visa cost.

Though Infosys surprised negatively on the EBIT margin guidance front,

we believe the market has already priced it in. Currently, it is trading at

attractive valuation of ~13.2x FY19 EPS & offers FY19 FCF yield of ~5%.

Secondly, Infosys intends to return part of cash and recasting capital

allocation policy are steps in right direction towards shareholder value

creation. Hence, we maintain our BUY recommendation. We also roll over

to FY19E and revise our target price to | 1060 (15x FY19E). We have

lowered target multiple at 15x due to slowing growth trajectory, growing

protectionism measures leading to risk in margin profile.

Exhibit 7: One year forward rolling PE

0

300

600

900

1200

1500

1800

Apr-

07

Oct-

07

Apr-

08

Oct-

08

Apr-

09

Oct-

09

Apr-

10

Oct-

10

Apr-

11

Oct-

11

Apr-

12

Oct-

12

Apr-

13

Oct-

13

Apr-

14

Oct-

14

Apr-

15

Oct-

15

Apr-

16

Oct-

16

Apr-

17

Price 26 22 18 14 10

Source: Company, ICICIdirect.com Research

Exhibit 8: Valuation

Sales Growth EPS Growth PE EV/EBITDA RoNW RoCE

(| cr) (%) (|) (%) (x) (x) (%) (%)

FY16 62,441 17.1 59.0 9.4 15.8 10.4 21.8 30.2

FY17E 68,485 9.7 62.8 6.4 14.8 9.3 20.8 28.8

FY18E 71,406 4.3 64.6 2.9 14.4 9.6 22.3 31.0

FY19E 79,411 11.2 70.7 9.5 13.1 8.3 21.7 30.5

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 7

Recommendation History vs. Consensus

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

0

200

400

600

800

1,000

1,200

1,400

1,600

Apr-17Jan-17Nov-16Sep-16Jun-16Apr-16Jan-16Nov-15Aug-15Jun-15Apr-15

(%

)(|)

Price Idirect target Consensus Target Mean % Consensus with BUY

Source: Bloomberg, Company, ICICIdirect.com Research

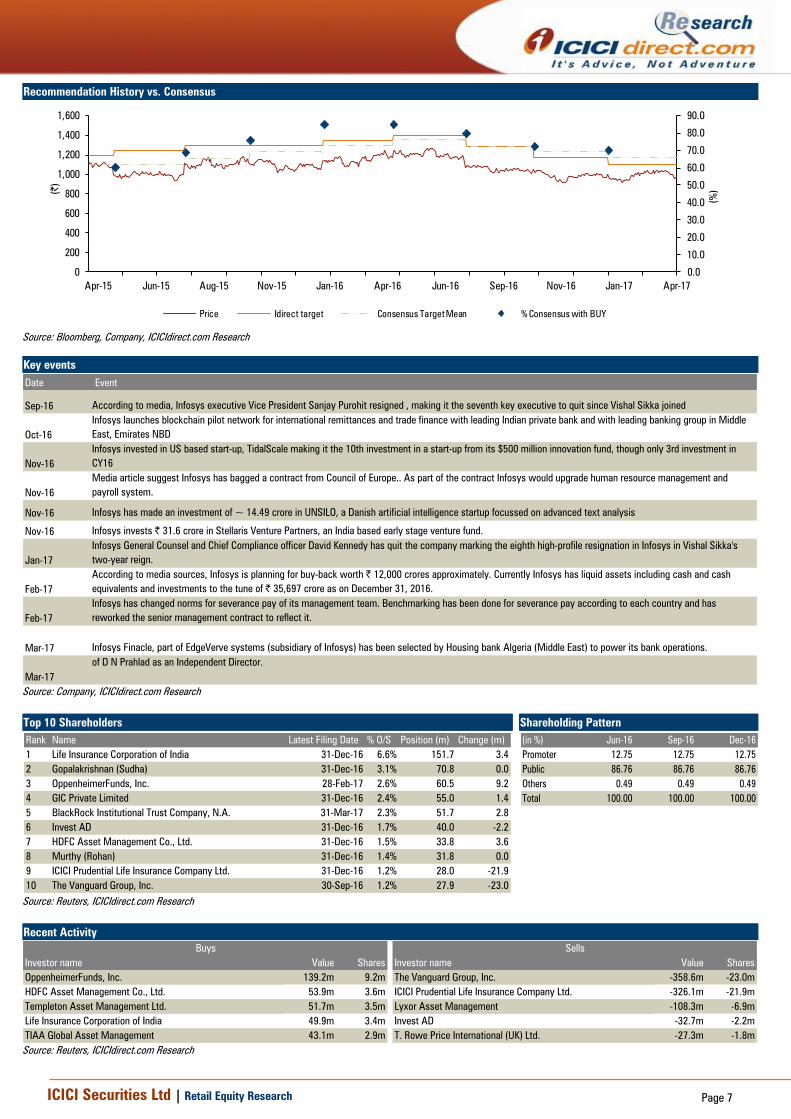

Key events

Date Event

Sep-16 According to media, Infosys executive Vice President Sanjay Purohit resigned , making it the seventh key executive to quit since Vishal Sikka joined

Oct-16

Infosys launches blockchain pilot network for international remittances and trade finance with leading Indian private bank and with leading banking group in Middle

East, Emirates NBD

Nov-16

Infosys invested in US based start-up, TidalScale making it the 10th investment in a start-up from its $500 million innovation fund, though only 3rd investment in

CY16

Nov-16

Media article suggest Infosys has bagged a contract from Council of Europe.. As part of the contract Infosys would upgrade human resource management and

payroll system.

Nov-16 Infosys has made an investment of ~ 14.49 crore in UNSILO, a Danish artificial intelligence startup focussed on advanced text analysis

Nov-16 Infosys invests | 31.6 crore in Stellaris Venture Partners, an India based early stage venture fund.

Jan-17

Infosys General Counsel and Chief Compliance officer David Kennedy has quit the company marking the eighth high-profile resignation in Infosys in Vishal Sikka's

two-year reign.

Feb-17

According to media sources, Infosys is planning for buy-back worth | 12,000 crores approximately. Currently Infosys has liquid assets including cash and cash

equivalents and investments to the tune of | 35,697 crore as on December 31, 2016.

Feb-17

Infosys has changed norms for severance pay of its management team. Benchmarking has been done for severance pay according to each country and has

reworked the senior management contract to reflect it.

Mar-17 Infosys Finacle, part of EdgeVerve systems (subsidiary of Infosys) has been selected by Housing bank Algeria (Middle East) to power its bank operations.

Mar-17

Infosys shareholders have approved the proposal to adopt a new AoA, revision in compensation of COO & Whole-time Director U B Pravin Rao, and also appointment

of D N Prahlad as an Independent Director.

Source: Company, ICICIdirect.com Research

Top 10 Shareholders Shareholding Pattern

Rank Name Latest Filing Date % O/S Position (m) Change (m)

1 Life Insurance Corporation of India 31-Dec-16 6.6% 151.7 3.4

2 Gopalakrishnan (Sudha) 31-Dec-16 3.1% 70.8 0.0

3 OppenheimerFunds, Inc. 28-Feb-17 2.6% 60.5 9.2

4 GIC Private Limited 31-Dec-16 2.4% 55.0 1.4

5 BlackRock Institutional Trust Company, N.A. 31-Mar-17 2.3% 51.7 2.8

6 Invest AD 31-Dec-16 1.7% 40.0 -2.2

7 HDFC Asset Management Co., Ltd. 31-Dec-16 1.5% 33.8 3.6

8 Murthy (Rohan) 31-Dec-16 1.4% 31.8 0.0

9 ICICI Prudential Life Insurance Company Ltd. 31-Dec-16 1.2% 28.0 -21.9

10 The Vanguard Group, Inc. 30-Sep-16 1.2% 27.9 -23.0

(in %) Jun-16 Sep-16 Dec-16

Promoter 12.75 12.75 12.75

Public 86.76 86.76 86.76

Others 0.49 0.49 0.49

Total 100.00 100.00 100.00

Source: Reuters, ICICIdirect.com Research

Recent Activity

Investor name Value Shares Investor name Value Shares

OppenheimerFunds, Inc. 139.2m 9.2m The Vanguard Group, Inc. -358.6m -23.0m

HDFC Asset Management Co., Ltd. 53.9m 3.6m ICICI Prudential Life Insurance Company Ltd. -326.1m -21.9m

Templeton Asset Management Ltd. 51.7m 3.5m Lyxor Asset Management -108.3m -6.9m

Life Insurance Corporation of India 49.9m 3.4m Invest AD -32.7m -2.2m

TIAA Global Asset Management 43.1m 2.9m T. Rowe Price International (UK) Ltd. -27.3m -1.8m

Buys Sells

Source: Reuters, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 8

.

Financial summary

Profit and loss statement | Crore

(Year-end March) FY16 FY17E FY18E FY19E

Total operating Income 62,441 68,485 71,406 79,411

Growth (%) 17.1 9.7 4.3 11.2

COGS (employee expenses) 37,639 41,550 43,629 48,520

Admin expenses 4,292 4,739 4,998 5,559

S&M expenses 3,431 3,591 3,927 4,209

Total Operating Expenditure 45,362 49,880 52,555 58,287

EBITDA 17,079 18,605 18,851 21,123

Growth (%) 14.6 8.9 1.3 12.1

Depreciation 1,459 1,703 1,714 1,906

Other Income 3,125 3,079 2,452 2,389

PBT 18,742 19,951 19,557 21,570

Total Tax 5,251 5,598 5,574 6,255

PAT 13,491 14,353 13,983 15,315

Growth (%) 9.4 6.4 (2.6) 9.5

EPS (|) 59 63 65 71

Growth (%) 9.4 6.4 2.9 9.5

Source: Company, ICICIdirect.com Research

Cash flow statement | Crore

(Year-end March) FY16 FY17E FY18E FY19E

Profit after Tax 13,491 14,353 13,983 15,315

Add: Depreciation 1,459 1,703 1,714 1,906

(Inc)/dec in Current Assets (3,096) (1,820) (880) (2,411)

Inc/(dec) in CL and Provisions 842 769 372 1,018

Taxes paid (5,865) (5,598) (5,574) (6,255)

CF from operating activities 12,243 11,925 12,736 13,439

(Inc)/dec in Investments* 88 3,079 2,452 2,389

(Inc)/dec in Fixed Assets (2,723) (2,500) (2,500) (2,500)

CF from investing activities (3,116) 579 (48) (111)

Dividend paid & dividend tax (6,813) (7,119) (7,165) (7,657)

Others - - - -

CF from financing activities (6,813) (7,119) (20,165) (7,657)

Net Cash flow 2,314 5,385 (7,477) 5,671

Exchange difference 16 - - -

Opening Cash 30,367 32,697 38,083 30,606

Closing Cash 32,697 38,083 30,606 36,277

Source: Company, ICICIdirect.com Research

Balance sheet | Crore

(Year-end March) FY16 FY17E FY18E FY19E

Equity Capital 1,144 1,144 1,084 1,084

Reserve and Surplus 60,635 67,869 61,747 69,405

Total Shareholders funds 61,779 69,013 62,831 70,489

Employee benefit obligations - - - -

Debt - - - -

Deferred Tax Liability 256 256 256 256

Other non current liabilties 115 115 115 115

Total Liabilities 62,150 69,384 63,202 70,860

Assets

Property,plant and equipment 10,530 11,327 12,113 12,707

Goodwill 3,764 3,764 3,764 3,764

Intangibles 985 985 985 985

Available for sale assets 1,811 1,811 1,811 1,811

Other assets 6,604 6,604 6,604 6,604

Cash 32,697 38,083 30,606 36,277

Investment in CD - - - -

Trade receivables 11,330 12,427 12,957 14,409

Unbilled revenue 3,029 3,322 3,464 3,852

Prepayment & O.fin.assets 4,448 4,879 5,087 5,657

Other current assets 191 191 191 191

Total Current Assets 51,695 58,901 52,304 60,386

Trade payables 386 423 441 491

Unearned revenue 1,332 1,461 1,523 1,694

OCL & provisions 11,521 12,124 12,415 13,213

Total Current Liabilities 13,239 14,008 14,379 15,398

Net Current Assets 38,456 44,893 37,925 44,989

Application of Funds 62,150 69,384 63,202 70,860

Source: Company, ICICIdirect.com Research

Key ratios

(Year-end March) FY16 FY17E FY18E FY19E

Per share data (|)

EPS 59.0 62.8 64.6 70.7

Cash EPS 65.4 70.2 72.5 79.6

BV 270.3 301.9 290.3 325.6

DPS 24.5 25.8 27.5 29.4

Cash Per Share 143.0 166.6 141.4 167.6

Operating Ratios (%)

EBIT Margin 25.0 24.7 24.0 24.2

PBT Margin 30.0 29.1 27.4 27.2

PAT Margin 21.6 21.0 19.6 19.3

Debtor days 66 66 66 66

Unbilled revenue 17 17 17 17

Creditor days 2 2 2 2

Return Ratios (%)

RoE 21.8 20.8 22.3 21.7

RoCE 30.2 28.8 31.0 30.5

RoIC 65.4 65.7 63.4 66.2

Valuation Ratios (x)

P/E 15.8 14.8 14.4 13.1

EV / EBITDA 10.4 9.3 9.6 8.3

EV / Net Sales 2.9 2.5 2.5 2.2

Market Cap / Sales 3.4 3.1 3.0 2.7

Price to Book Value 3.4 3.1 3.2 2.9

Solvency Ratios

Debt/EBITDA - - - -

Debt / Equity - - - -

Current Ratio 1.9 2.0 2.0 2.0

Quick Ratio 1.9 2.0 2.0 2.0

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 9

ICICIdirect.com coverage universe (IT)

CMP M Cap EPS (|) P/E (x) RoCE (%) RoE(%)

(|) TP(|) Rating (| Cr) FY16 FY17E FY18E FY16 FY17E FY18E FY16 FY17E FY18E FY16 FY17E FY18E FY16 FY17E FY18E

Cyient (INFENT) 483 540 Hold 5,438 29.0 32.2 38.6 16.7 15.0 12.5 11.2 9.2 7.7 20.3 19.9 21.4 17.1 17.0 18.0

Eclerx (ECLSER) 1,379 1,300 Sell 5,685 87.9 86.1 92.6 15.7 16.0 14.9 10.6 10.7 9.6 42.6 34.8 34.2 33.5 28.5 26.7

Firstsource (FIRSOU) 41 46 Buy 2,722 3.8 4.3 4.6 10.5 9.3 8.6 7.9 6.6 5.4 11.7 12.5 12.9 12.9 12.0 11.6

HCL Tech (HCLTEC) 831 950 Buy 117,312 40.0 58.1 64.6 16.6 10.2 8.8 3.5 2.3 2.0 35.9 51.5 54.3 23.5 30.3 32.5

Infosys (INFTEC) 930 1,060 Buy 212,554 59.0 62.8 64.6 15.8 14.8 14.4 10.4 9.3 9.6 30.2 28.8 31.0 21.8 20.8 22.3

KPIT Tech (KPISYS) 130 150 Hold 2,587 14.1 11.5 14.8 9.2 11.3 8.8 5.5 7.2 5.3 23.7 18.0 20.7 20.4 14.6 16.3

Mindtree (MINCON) 449 490 Hold 7,540 35.9 25.4 32.6 12.5 17.6 13.8 8.5 9.8 8.3 31.1 23.0 27.5 25.2 17.3 20.9

NIIT Technologies (NIITEC) 427 450 Hold 1,530 45.8 39.9 45.6 9.3 9.8 9.4 2.4 2.3 1.9 28.6 24.9 25.0 17.6 13.8 14.2

Persistent (PSYS) 567 725 Buy 4,535 37.2 40.0 47.0 18.3 17.0 14.5 11.2 9.3 7.4 27.9 27.3 28.1 21.2 20.4 20.7

TCS (TCS) 2,407 2,465 Hold 471,459 123.2 132.2 144.7 19.1 17.8 16.2 14.4 13.2 12.1 41.2 36.8 34.1 33.1 29.5 27.2

Tech Mahindra (TECMAH) 438 525 Buy 43,042 31.7 33.6 40.4 13.8 13.0 10.8 9.0 9.1 7.5 25.5 23.6 25.3 21.7 18.6 19.8

Wipro (WIPRO) 505 510 Hold 124,386 36.1 33.7 36.5 14.0 15.0 13.8 10.1 9.5 8.1 19.6 17.5 16.6 19.1 16.3 14.8

Sector / Company

EV/EBITDA (x)

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 10

RATING RATIONALE

ICICIdirect.com endeavours to provide objective opinions and recommendations. ICICIdirect.com assigns

ratings to its stocks according to their notional target price vs. current market price and then categorises them

as Strong Buy, Buy, Hold and Sell. The performance horizon is two years unless specified and the notional

target price is defined as the analysts' valuation for a stock.

Strong Buy: >15%/20% for large caps/midcaps, respectively, with high conviction;

Buy: >10%/15% for large caps/midcaps, respectively;

Hold: Up to +/-10%;

Sell: -10% or more;

Pankaj Pandey Head – Research [email protected]

ICICIdirect.com Research Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC,

Andheri (East)

Mumbai – 400 093

ICICI Securities Ltd | Retail Equity Research Page 11

ANALYST CERTIFICATION

We /I, Deepak Purswani, CFA MBA (Finance), Deepti Tayal, MBA, Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report

accurately reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or

view(s) in this report.

Terms & conditions and other disclosures:

ICICI Securities Limited (ICICI Securities) is a full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products. ICICI Securities

Limited is a Sebi registered Research Analyst with Sebi Registration Number – INH000000990. ICICI Securities is a wholly-owned subsidiary of ICICI Bank which is India’s largest private sector bank and has

its various subsidiaries engaged in businesses of housing finance, asset management, life insurance, general insurance, venture capital fund management, etc. (“associates”), the details in respect of which

are available on www.icicibank.com.

ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment banking

and other business relationship with a significant percentage of companies covered by our Investment Research Department. ICICI Securities generally prohibits its analysts, persons reporting to analysts

and their relatives from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover.

The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and

meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without

prior written consent of ICICI Securities. While we would endeavour to update the information herein on a reasonable basis, ICICI Securities is under no obligation to update or keep the information current.

Also, there may be regulatory, compliance or other reasons that may prevent ICICI Securities from doing so. Non-rated securities indicate that rating on a particular security has been suspended

temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in circumstances where ICICI Securities might be acting in an advisory capacity to this

company, or in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This

report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial

instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their

receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific

circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment

objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate

the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no liabilities whatsoever for any

loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the

risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to

change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment

in the past twelve months.

ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in

respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction.

ICICI Securities or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the companies mentioned

in the report in the past twelve months.

ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its associates or its analysts did not receive any

compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts

and their relatives have any material conflict of interest at the time of publication of this report.

It is confirmed that Deepak Purswani, CFA MBA (Finance), Deepti Tayal, MBA, Research Analysts of this report have not received any compensation from the companies mentioned in the report in the

preceding twelve months.

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.

ICICI Securities or its subsidiaries collectively or Research Analysts or their relatives do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month

preceding the publication of the research report.

Since associates of ICICI Securities are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject

company/companies mentioned in this report.

It is confirmed that Deepak Purswani, CFA MBA (Finance), Deepti Tayal, MBA, Research Analysts do not serve as an officer, director or employee of the companies mentioned in the report.

ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report.

Neither the Research Analysts nor ICICI Securities have been engaged in market making activity for the companies mentioned in the report.

We submit that no material disciplinary action has been taken on ICICI Securities by any Regulatory Authority impacting Equity Research Analysis activities.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution,

publication, availability or use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities

described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and

to observe such restriction.

Related Documents