Auditor General of Newfoundland and Labrador 379 2.25 Discovery Regional Development Board Inc. In 1992, the Province’s Strategic Economic Plan recommended the creation of economic zones which would: h facilitate the development of economic plans by the people in each zone; h facilitate joint initiatives by communities within the zone; h promote the economic opportunities and strengths of each zone and region; and h facilitate more regionalization of Government administration. In January 1995, on the basis of recommendations from the Task Force on Community Economic Development, Cabinet approved the establishment of 19 (now 20) regional economic zones and regional economic development boards. Initially, Government established provisional boards to determine the structure and process of establishing permanent boards. The permanent boards were established as incorporated entities with democratically elected members who are community based. The 20 regional economic development boards are outlined in Figure 1. Introduction

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Auditor General of Newfoundland and Labrador 379

2.25 Discovery Regional Development Board Inc.

In 1992, the Province’s Strategic Economic Plan recommended the creation of economic zones which would:

h facilitate the development of economic plans by the people in each zone;

h facilitate joint initiatives by communities within the zone;

h promote the economic opportunities and strengths of each zone and region; and

h facilitate more regionalization of Government administration.

In January 1995, on the basis of recommendations from the Task Force on Community Economic Development, Cabinet approved the establishment of 19 (now 20) regional economic zones and regional economic development boards.

Initially, Government established provisional boards to determine the structure and process of establishing permanent boards. The permanent boards were established as incorporated entities with democratically elected members who are community based. The 20 regional economic development boards are outlined in Figure 1.

Introduction

The Discovery Regional Development Board Inc. (Zone 15) covers an area on the island’s east coast, including 109 communities, with a combined population of approximately 33,470 (1996), bounded by Bonavista, Port Blandford, Swift Current and Chapel Arm. Figure 2 shows the area covered by the Corporation.

Figure 1

Regional Economic Development Boards31 March 2003

EconomicZone #

Regional Economic Development Board Head Office Location

1 Inukshuk Economic Development Corporation Makkovik

2 Hyron Regional Economic Development Corporation Labrador City

3 Central Labrador Economic Development Board Inc. Happy Valley - Goose Bay

4 Southeastern Aurora Development Corporation Cartwright

5 Labrador Straits Development Corporation Forteau

6 Nordic Economic Development Corporation Flower’s Cove

7 Red Ochre Regional Board Inc. Parson’s Pond

8 Humber Economic Development Board Inc. Corner Brook

9 Long Range Regional Economic Development Board Stephenville

10 Marine and Mountain Zone Corporation Port aux Basques

11 Emerald Zone Corporation Springdale

12 Exploits Valley Economic Development Corporation Grand Falls - Windsor

13 Coast of Bays Corporation St. Alban’s

14 Kittiwake Economic Development Corporation Gander

15 Discovery Regional Development Board Inc. Clarenville

16 Schooner Regional Development Corporation Marystown

17 Mariner Resource Opportunities Network Inc. Carbonear

18 Avalon Gateway Regional Economic Development Inc. Dunville

19 Capital Coast Development Alliance St. John’s

20 Irish Loop Regional Economic Development Board Trepassey

Source: Department of Industry, Trade and Rural Development

380 Auditor General of Newfoundland and Labrador

2.25 Discovery Regional Development Board Inc.

The Corporation is governed by an elected board of directors representing major stakeholder groups in the region. The Board is comprised of 17 representatives as follows:

h 6 members representing municipalities;

h 3 members representing development associations;

h 3 members representing business;

Figure 2

Economic Zone 15Discovery Regional Development Board Inc.Location and Boundaries

Auditor General of Newfoundland and Labrador 381

2.25 Discovery Regional Development Board Inc.

h 3 members elected at large;

h 1 member representing education; and

h 1 member representing labour.

We completed our review of the Discovery Regional Development Board Inc. in May 2003. Our review covered the period from 1 September 2001 to 31 March 2003. The objectives of our review were to:

h review the financial position and operating results of the Corporation;

h assess whether the management practices and control systems at the Corporation are adequate to provide information to management and the Board of Directors for decision making and control of the Corporation’s revenues and expenditures;

h assess the Corporation’s compliance with the terms of its performance contract, related agreements, and relevant authorities;

h determine whether controls over the purchasing of goods and services are adequate and that such expenditures are made in accordance with the Corporation’s policies and procedures; and

h assess whether the Corporation’s capital assets are adequately controlled and accounted for.

We had planned to commence our review in early April 2003; however, we found that the Discovery Regional Development Board Inc. had not been in operation since December 2002. We were informed that the Corporation’s inability to obtain Directors’ and Officers’ liability insurance had resulted in the termination of staff employment, closing of operations, and suspension of funding.

Corporation staff were rehired on 21 April 2003 when the Corporation secured liability insurance and had operational funding reinstated. Our review commenced on 22 April 2003. On 15 May 2003, the power to the building which housed the Corporation was discontinued, resulting in the suspension of our field work. We were advised that the power was discontinued due to the owner of the building, the Discovery Opportunity Centre Inc., not paying its electric bills. Further constraints were imposed on our review as one of the two existing Corporation staff was not employed during the full period of our review.

Scope andObjectives

382 Auditor General of Newfoundland and Labrador

2.25 Discovery Regional Development Board Inc.

In March 2003, the Public Accounts Committee made a resolution that “... the Auditor General be asked to consider performing an audit of the Regional Economic Development Boards in the Province ...”. Further to this resolution, I performed an audit of three zonal boards during the year. As requested by the Public Accounts Committee, the results of my work are included in my Annual Report to the House of Assembly on Reviews of Departments and Crown Agencies. This report item outlines my findings on one of the three zonal boards reviewed - the Discovery Regional Development Board Inc..

The Discovery Regional Development Board Inc. was incorporated in May 1996. The Corporation, along with 19 other regional economic development boards, was established on the basis of recommendations made to Cabinet in 1995 by the Task Force on Community Economic Development. The Corporation covers an area on the island’s east coast, including 109 communities, with a combined population of approximately 33,470 (1996).

The Corporation receives its funding from the Federal and Provincial governments. Due to the lack of externally prepared financial statements for all years since the Corporation’s inception in May 1996, we were unable to determine the total funding received relating to administration expenses since the Corporation’s inception or the amount received to fund initiatives in accordance with the Corporation’s Strategic Economic Plan.

Our review indicated that the Corporation did not always publicly tender for goods and services, did not fully comply with its performance contract with the Federal and Provincial governments, and that improvements in controls are required in several areas. Specifically:

h Property Purchase. One item of particular concern resulting from our review relates to the purchase of a property by the Discovery Opportunity Centre Inc. (DOC). The DOC was a company established by the Corporation for this purpose. The property was intended to provide rental accommodations for the local IT sector as well as for Corporation administrative and program staff. The property was purchased in July 2000 for $82,645 with an estimate of $519,500 for extensive renovations. Based on the most recent information available, the DOC owes $740,824 relating to the property purchase and renovations, consisting of $51,519 for the bank mortgage and $689,305 for various creditors.

Conclusions

Auditor General of Newfoundland and Labrador 383

2.25 Discovery Regional Development Board Inc.

Our review of the Corporation’s involvement with the DOC property indicated the following:

h The Corporation violated the terms of the performance contract by indirectly purchasing the DOC property. The performance contract indicates that funding is provided to cover eligible direct operating costs and, in cases where deviations from eligible expenses are going to be made, requires that written approval of the Federal/Provincial Management Committee be obtained. The purchase and renovation of the DOC property does not qualify as an eligible operating cost and would, therefore, require written approval. While the proposal relating to the DOC property was discussed with the Management Committee, no such written approval was provided. The establishment of the DOC, to enable the purchase and renovation of the DOC property, was designed by the Corporation in an attempt to circumvent the performance contract which did not permit such activities.

h No public tender was called for the purchase of the initial property which cost $82,645, and no information was provided that would suggest the Corporation considered other methods of securing the required accommodations. Therefore, the Corporation could not demonstrate whether the most appropriate space was obtained at the best price.

h No public tenders were called for any of the goods and services acquired during the renovation.

h Expenditures totalling $46,050 were incurred by the Corporation on behalf of the DOC.

h At the time of our review, renovations on the building had not been completed, the lone remaining IT sector tenant which had occupied some of the space had left, all former DOC Board Directors except the former President of the Corporation had resigned, several suppliers had yet to be paid for goods and services provided, and both the bank mortgage and a second mortgage with a local building materials supply company were in payment default. The total amount owed to all creditors at the time of our review was $740,824, which included balances and related interest/service charges of: $51,519 relating to the bank mortgage; $449,416 relating to the second mortgage with the building materials supplier; and $239,889 relating to other creditors.

384 Auditor General of Newfoundland and Labrador

2.25 Discovery Regional Development Board Inc.

h Planning, Monitoring and Reporting. No new long-term Strategic Economic Plan was developed to replace the original plan prepared in 1997 and which expired in 2002. Without a long-term strategic plan to provide a focus, it was difficult for the Corporation to demonstrate how annual initiatives contributed to any long-term objectives.

Also, while the Board did receive some information on the status of how projects were proceeding when it met, we found that there was insufficient information provided by Corporation officials at those meetings to enable the Board to monitor how resources were utilized in meeting stated objectives contained in work plans and the Strategic Economic Plan which expired in 2002.

As well, there was no annual evaluation undertaken by Corporation officials of the various initiatives and projects which could have been used by the Board to determine whether the initiatives or projects achieved the intended results and contributed to planned objectives.

h Compliance with Performance Contract. The Corporation receives its funding based on a performance contract with the Federal and Provincial governments. We found that the Corporation had not fully complied with the requirements of this contract. Most notable is the indirect purchase of the DOC property referred to above, which was not an eligible cost under the performance contract.

The Corporation is required to repay any unexpended operational funds promptly and in any event within 30 days of written notice by the Management Committee. However, the Corporation had not remitted any unexpended operational funds and furthermore, the Corporation had not received written notification requesting that the amounts be repaid.

h Controls and Expenditures. Although not documented as being Board policy, Corporation staff indicated that the Corporation follows the Public Tender Act in acquiring goods and services. Given that the DOC was established by the Corporation, we also used the Public Tender Act as a reference in reviewing the purchasing practices used by the DOC to ensure reasonable prices were obtained in acquiring goods and services relating to the purchase and renovation of the DOC property in Clarenville. The Act requires tenders to be invited where the cost of goods and

Auditor General of Newfoundland and Labrador 385

2.25 Discovery Regional Development Board Inc.

services is more than $10,000. The Act also requires three quotes to be obtained for purchases of goods and services costing $10,000 or less.

We found that in relation to the DOC property purchase no public tenders were called for purchases in excess of $10,000. We also found instances related to the property purchase and other Corporation purchases, where three written quotes were not obtained for purchases of less than $10,000.

Our review also identified issues with respect to documentation and payment of travel claims. Of particular concern was a notification the Board received in July 2002, from the Atlantic Canada Opportunities Agency (ACOA), of irregularities in travel claims by two of the Corporation’s Board members. Corporation staff informed us that the two Board members in question were found to be submitting travel claims to two ACOA funded boards for the same travel. In September 2002, the Board decided to suspend the two Board members indefinitely from the Board until ACOA or the two Board members could satisfactorily inform the Board that the matter had been resolved. We were informed by Corporation officials that no further action was taken in relation to this matter and that no monies were recovered from the two Board members.

h Human Resources. Corporation staff could not locate job competition files and personnel files. Given the absence of these files, we were unable to review the hiring practices of the Corporation or determine how people were selected for positions or whether salaries and benefits were in compliance with any employment contracts which may have been in place.

Corporation staff indicated they are responsible for monitoring their own attendance and that there are no attendance or leave records maintained. Also, there is no documented approval for overtime worked.

Our review also indicated that two complaints against the Corporation had been filed with the Human Rights Commission.

h Capital Assets. The Corporation does not have a complete and accurate record of its capital assets.

386 Auditor General of Newfoundland and Labrador

2.25 Discovery Regional Development Board Inc.

Financial Position and Operating Results

Government identified two phases to the implementation of the regional economic development boards and provided funding on that basis. Phase 1 included the development of a strategic plan for each zone while Phase 2 included the implementation of the strategic plans. The operational funding for the regional economic development boards was provided through the Comprehensive Economic Development Agreement (CEDA), (formerly Strategic Regional Diversification Agreement), and administered by the Department of Industry, Trade and Rural Development. Subsequent to the conclusion of the CEDA agreement in June 2002, the operational funding was provided by the Province and ACOA through separate agreements with the Corporation.

Our review of the Corporation’s financial position included an assessment of the annual operating results and the year end assets and liabilities. The financial position of the Corporation, represented by its assets and liabilities, as at 31 August each year is presented in Figure 3.

Findings andRecommendations

Figure 3

Discovery Regional Development Board Inc.Summary of Financial Position - Administrative Fund 31 August

Category 1996 1997 1998 1999 2000 2001

Cash

Not Available

$21,327 $ 23,067 $ 1,011 $ 500

Term deposit 33,413 22,295 - -

Accounts receivable 5,568 17,812 6,540 5,317

Prepaid expense - 2,100 - -

Capital assets 6,619 26,252 26,252 28,745

Total assets 66,927 91,526 33,803 34,562

Bank indebtedness

Not Available

- - - 4,880

Accounts payable and accrued liabilities 3,575 900 23,760 9,420

Surplus (Deficit) 56,733 64,374 (16,209) (8,483)

Investment in capital assets 6,619 26,252 26,252 28,745

Total liabilities and equity $66,927 $ 91,526 $ 33,803 $ 34,562

Source: Corporation Financial StatementsNote: No financial statements were available for the period from the date of incorporation in May 1996 through 31 August 1997 and no externally prepared financial statements were available for the year ended 31 August 2002.

Auditor General of Newfoundland and Labrador 387

2.25 Discovery Regional Development Board Inc.

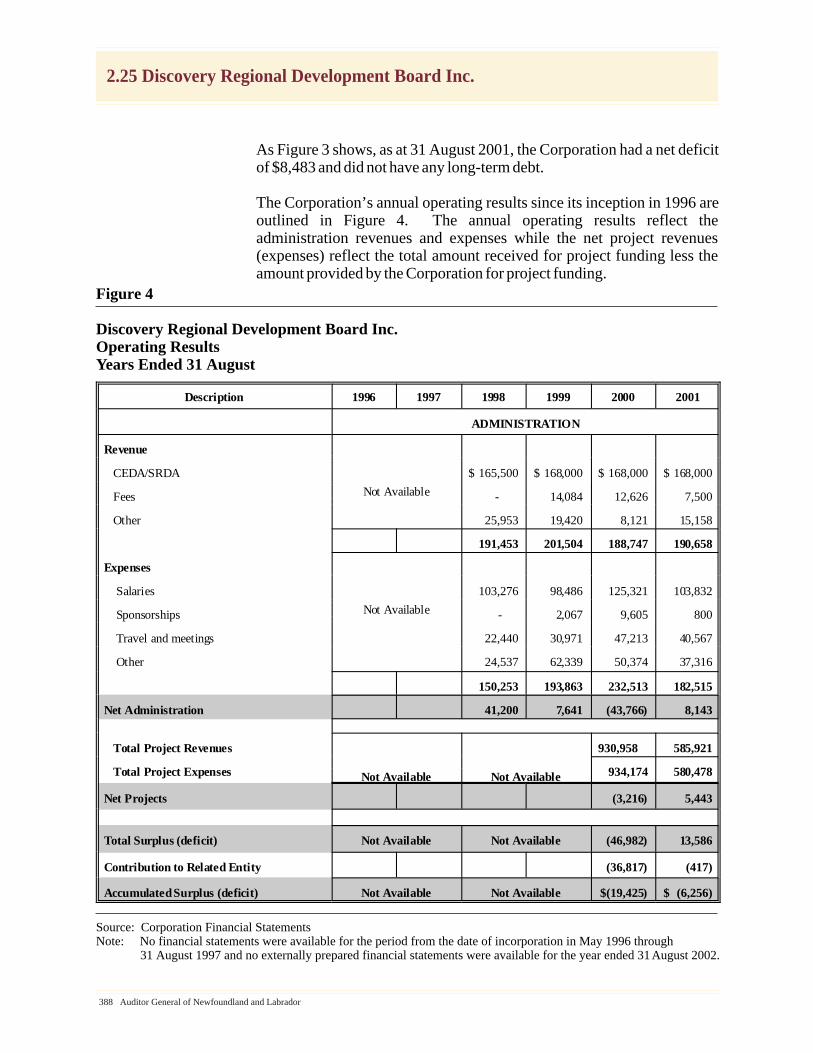

As Figure 3 shows, as at 31 August 2001, the Corporation had a net deficit of $8,483 and did not have any long-term debt.

The Corporation’s annual operating results since its inception in 1996 are outlined in Figure 4. The annual operating results reflect the administration revenues and expenses while the net project revenues (expenses) reflect the total amount received for project funding less the amount provided by the Corporation for project funding.

Figure 4

Discovery Regional Development Board Inc.Operating ResultsYears Ended 31 August

Description 1996 1997 1998 1999 2000 2001

ADMINISTRATION

Revenue

Not Available

CEDA/SRDA $ 165,500 $ 168,000 $ 168,000 $ 168,000

Fees - 14,084 12,626 7,500

Other 25,953 19,420 8,121 15,158

191,453 201,504 188,747 190,658

Expenses

Not Available

Salaries 103,276 98,486 125,321 103,832

Sponsorships - 2,067 9,605 800

Travel and meetings 22,440 30,971 47,213 40,567

Other 24,537 62,339 50,374 37,316

150,253 193,863 232,513 182,515

Net Administration 41,200 7,641 (43,766) 8,143

Total Project Revenues

Not Available Not Available

930,958 585,921

Total Project Expenses 934,174 580,478

Net Projects (3,216) 5,443

Total Surplus (deficit) Not Available Not Available (46,982) 13,586

Contribution to Related Entity (36,817) (417)

AccumulatedSurplus (deficit) Not Available Not Available $(19,425) $ (6,256)

Source: Corporation Financial StatementsNote: No financial statements were available for the period from the date of incorporation in May 1996 through 31 August 1997 and no externally prepared financial statements were available for the year ended 31 August 2002.

388 Auditor General of Newfoundland and Labrador

2.25 Discovery Regional Development Board Inc.

The Corporation receives its funding from the Federal and Provincial governments. Due to the lack of externally prepared financial statements for all years since the Corporation’s inception in May 1996, we were unable to determine the total funding received relating to administration expenses since the Corporation’s inception or the amount received to fund initiatives in accordance with the Corporation’s Strategic Economic Plan.

Our review of the Corporation’s financial position and operating results identified the following issues:

h The Board received information on cash balances; however, the information did not reflect expenditures incurred but unpaid and did not include explanations of variances from budget.

h There were no externally prepared financial statements from the date of incorporation in May 1996 through 31 August 1997. As well, consolidated financial statements which reflect the Corporation’s combined administration transactions and project transactions were only available for the year ended 31 August 2001. While financial statements were provided for the year ended 31 August 2002, they were based on internally prepared financial information which did not include all transactions and balances and which did not accurately reflect the external auditor’s adjustments from the previous year.

h The Corporation only prepares its Harmonized Sales Tax (HST) claim after year end. More frequent claim submission would allow HST amounts due to be received earlier. A final claim for the year ended 31 August 2001 totalling $10,398 was not filed until 29 March 2002, 4 months after the due date of 30 November 2001. The return was initially filed on 28 January 2002, but was completed incorrectly.

Planning, Monitoring and Reporting

The Corporation’s mandate is to facilitate the development of economic plans for the zone, facilitate joint initiatives by communities within the zone, promote the economic opportunities and strengths of the zone and region, and facilitate more regionalization of Government administration. To facilitate the achievement of this mandate, the Corporation operates through a Board of Directors elected annually to represent various stakeholders.

Auditor General of Newfoundland and Labrador 389

2.25 Discovery Regional Development Board Inc.

The Corporation developed a five-year Strategic Economic Plan covering the period 1997 to 2002, prepares an annual work plan and an annual budget. To effectively monitor activities of the Corporation and to evaluate progress towards meeting the objectives contained in its Strategic Economic Plan and its annual work plan, the Board requires complete and timely information on how Corporation resources are utilized.

Our review of Board activities and the Corporation’s planning, monitoring and reporting indicate that improvements are required. We identified the following issues:

h No new long-term Strategic Economic Plan was developed to replace the original plan prepared in 1997 and which expired in 2002. Without a long-term strategic plan to provide a focus, it was difficult for the Corporation to demonstrate how annual initiatives contributed to any long-term objectives. Although Government notified the Corporation in September 2000 that the revision of the Strategic Economic Plan was a condition of obtaining funding in following years, funding continued to be provided to the Corporation to the end of the funding period, 31 August 2002. Corporation officials informed us that they are currently developing a new Strategic Economic Plan.

h While the Board did receive some information on the status of how projects were proceeding, discussion with Corporation officials and our review of minutes of Board meetings indicated that there was insufficient information provided by Corporation officials at those meetings to enable the Board to monitor how resources were utilized in meeting stated objectives contained in work plans and the Strategic Economic Plan. The information that was provided consisted of reports as to the current status of the projects and was often verbal in nature.

h There was no annual evaluation of the various initiatives and projects undertaken by Corporation officials which could be used by the Board or Management Committee to determine whether the initiatives or projects achieved the intended results and contributed to planned objectives.

h Minutes of Board meetings are kept and approved at the next Board meeting; however, Board minutes were rarely signed to identify them as the official board minutes. As well, there was very little detail in the minutes and there were numerous in-camera discussions.

390 Auditor General of Newfoundland and Labrador

2.25 Discovery Regional Development Board Inc.

Our review also indicated that decisions being made and acted upon at the Executive Committee level were not always communicated to the full Board. For example, in August 2000 the Executive Committee discussed a transfer of the Corporation’s cash surplus of $13,755 from its operating account to the Discovery Opportunity Centre Inc., a related company. There was no evidence that the disbursement to the Discovery Opportunity Centre Inc., approved by members of the Executive Committee, was ever discussed with the full Board.

h Minutes of Board and committee meetings often did not contain approval for specific actions. For example, although we were informed that while, as a matter of practice, prior approval is obtained from the Board for significant purchases, in many cases there was no documented evidence of prior Board approval.

h The Corporation has not complied with the Corporations Act in that notices of changes in directors have not been filed since May 2000, annual information returns have not been filed since March 2000, and Directors’ and Officers’ liability insurance had not been in place since April 2002. The Corporation had obtained a proposal for Directors’ and Officers’ liability insurance from a broker and had accepted the proposal; however, the Corporation was later notified by the broker that the offer had been rescinded as the insurance company involved had discovered that another of its brokers had earlier declined coverage for the Corporation.

Compliance with Performance Contract

The Corporation’s administrative funding is based on a performance contract between the Federal and Provincial governments and the Corporation. Therefore, the Federal/Provincial Management Committee requires information on the Corporation’s compliance with this performance contract.

When the Corporation first commenced operations in 1996, it was in Phase 1 and was funded by the Provincial and Federal governments to develop a strategic plan. After the finalization of its strategic plan, the Corporation entered into a joint Phase 2 performance contract with the Provincial and Federal governments covering the period September 1997 to August 2002. The Corporation entered into separate performance contracts with the Provincial and Federal governments in April 2003.

Auditor General of Newfoundland and Labrador 391

2.25 Discovery Regional Development Board Inc.

These contracts include a number of requirements for the Corporation such as a detailed financial framework, monitoring, evaluation, and reporting. We identified several instances where the requirements of the performance contract were not being complied with as follows:

1. Discovery Opportunity Centre Inc.

In June 2000, the Corporation established the Discovery Opportunity Centre Inc. (DOC). The DOC’s mandate is “...to acquire and house infrastructure required by the information technology sector and obtain support staff, as a means of stimulating local IT business development.” The DOC was intended to provide rental accommodations for the local IT sector as well as for Corporation administrative and program staff. The Corporation’s Board of Directors also acted as the Board of Directors for the DOC.

In July 2000, the DOC purchased an existing property in Clarenville to provide the accommodations. The purchase price of the property was $82,645 which was funded through a bank mortgage of $60,000, with the remaining $22,645 funded through a payment received from the Discovery Regional Development Board Inc.

The building purchased by the DOC was essentially replaced through an extensive renovation. Renovation costs estimated by the DOC as of March 2001 totalled $519,500. Arrangements for financing the renovation costs included an increase of $35,000 in the existing bank mortgage, a second mortgage with a local building materials supply company for $325,000 to secure the supply of building materials, approved funding from Human Resources Development Canada of $149,590, and credit arrangements with local suppliers.

Based on the most recent information available, the DOC owes $740,824 relating to the property purchase and renovations, consisting of $51,519 for the bank mortgage and $689,305 for various creditors.

In September 2001, during the ongoing renovations, the Corporation moved its offices into the DOC building.

392 Auditor General of Newfoundland and Labrador

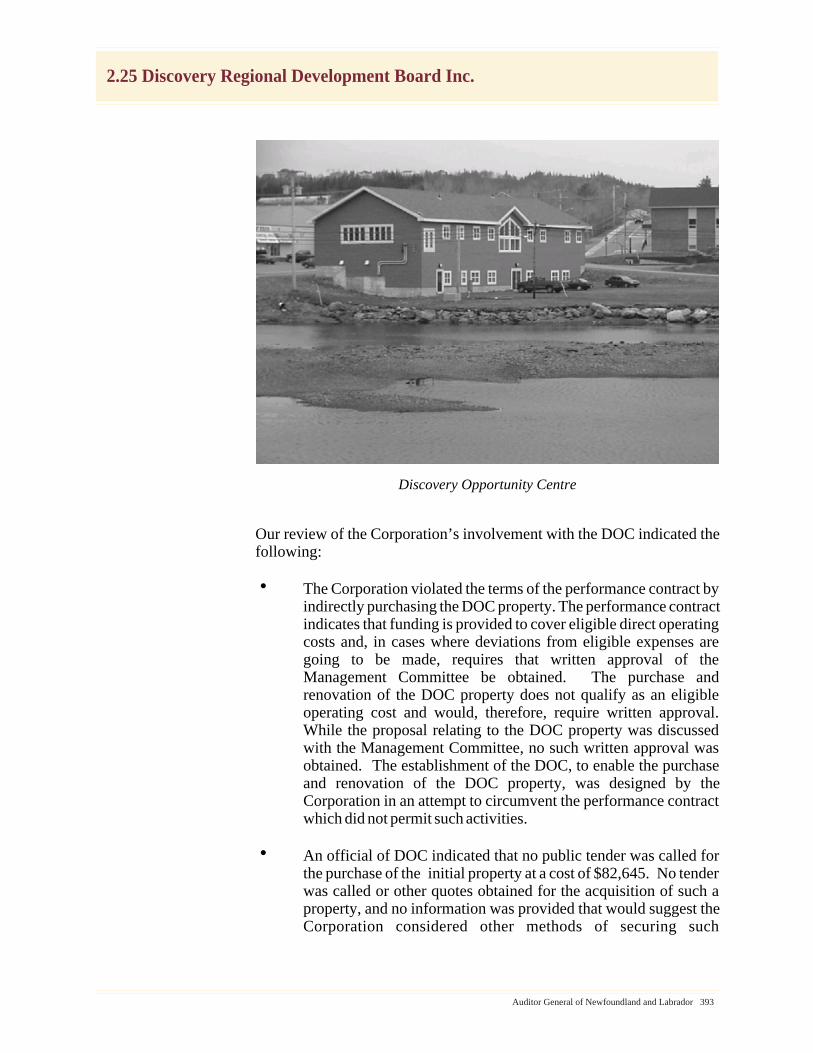

2.25 Discovery Regional Development Board Inc.

Discovery Opportunity Centre

Our review of the Corporation’s involvement with the DOC indicated the following:

h The Corporation violated the terms of the performance contract by indirectly purchasing the DOC property. The performance contract indicates that funding is provided to cover eligible direct operating costs and, in cases where deviations from eligible expenses are going to be made, requires that written approval of the Management Committee be obtained. The purchase and renovation of the DOC property does not qualify as an eligible operating cost and would, therefore, require written approval. While the proposal relating to the DOC property was discussed with the Management Committee, no such written approval was obtained. The establishment of the DOC, to enable the purchase and renovation of the DOC property, was designed by the Corporation in an attempt to circumvent the performance contract which did not permit such activities.

h An official of DOC indicated that no public tender was called for the purchase of the initial property at a cost of $82,645. No tender was called or other quotes obtained for the acquisition of such a property, and no information was provided that would suggest the Corporation considered other methods of securing such

Auditor General of Newfoundland and Labrador 393

2.25 Discovery Regional Development Board Inc.

accommodations, for example through leasing or complete construction. Therefore, the Corporation could not demonstrate whether the most appropriate space was obtained at the best price.

h An official of DOC indicated that no public tenders were called for any of the renovation work estimated in March 2001 to cost $519,500. Of particular note was that no public tender was called for the supply of building materials for the renovation and officials could not demonstrate on what basis the building materials supplier was chosen or whether similar financing arrangements could have been obtained from other suppliers. This was the most significant contract related to the renovation, with an anticipated $325,000 in building materials to be supplied.

h While there was evidence in Corporation records that the DOC did obtain quotes for some other aspects of the renovation work, Corporation staff could not demonstrate whether quotes were obtained for all goods and services acquired and on what basis received quotes were requested, reviewed and awarded.

h During the initial stages of the renovation, the DOC Board of Directors managed the project. At a DOC Executive Committee meeting held in May 2001, the Board’s Chair brought to the attention of the Committee the need for a Project Manager. Corporation staff could not demonstrate on what basis the Project Manager was chosen. Fees for the Project Manager of $4,500 were paid by the Corporation rather than the DOC.

h Expenditures totalling $46,050 were incurred by the Corporation on behalf of the DOC. These expenditures included telephone costs of $5,150, the project manager’s fees of $4,500, the $22,645 portion of the property purchase after bank mortgage financing, and an amount of $13,755 referenced as a transfer of earnings from the Corporation to the DOC. Aside from these direct payments, other costs were incurred by the Corporation including time spent by the office manager on record keeping for the DOC.

h The Corporation paid $22,645 “In Trust” to a law firm for the portion of the property purchase price after bank mortgage financing. These funds, with the exception of $955 for legal fees, were subsequently released on closing of the property purchase. A member of the DOC’s Board of Directors was a partner in this law firm. Legal fees of $955 incurred by the Corporation was for legal work conducted by the Board member relating to the purchase of the DOC property and related mortgage. This Board member was

394 Auditor General of Newfoundland and Labrador

2.25 Discovery Regional Development Board Inc.

also the vice-president of the Corporation. Corporation staff could not demonstrate on what basis the law firm was chosen.

h In October 2001, the Corporation paid the DOC $14,000 for

prepaid office rent for a full year to 31 August 2002. No rental agreement or other documentation could be provided to support the basis for the amount of rent or any other rental conditions.

h In August 2002, a report was provided to the Corporation by a consultant who had been engaged to complete an organizational review of the Corporation. The report stated that “Most respondents (based on workshops with stakeholders) felt that there is a lack of clear focus and direction from the Board itself.... the Board has focused too much attention and energy on one issue - the DO Centre in Clarenville.” It was further indicated that “There is a general perception that this project and its problems have dominated the energies of the Board at the expense of other responsibilities.” Corporation officials indicated that proposals were not called for the selection of this consultant as they were recommended by ACOA.

h An official of DOC indicated that the estimated rental income of $80,000 from the building did not materialize. Aside from occasional rental of the Board Room and of space for Elections Canada, only two tenants occupied space at the DOC building. Payments for one of the tenants totalled $14,000 for rent for a one year period, with payments for the other tenant totalling $9,000 for a similar one year period. Officials indicated that a major problem with respect to renting the space was that the DOC had not been able to obtain occupancy permits as the elevator had not been installed and therefore the building was not wheelchair accessible. It was further indicated that the rentals did take place even though the required occupancy permits were not obtained.

At the time of our review, renovations on the building had not been completed, the lone remaining IT sector tenant which had occupied some of the space had left, all former DOC Board Directors except the former President of the Corporation had resigned, numerous suppliers had yet to be paid for goods and services provided, and both the bank mortgage and the second mortgage with the building materials supplier were in payment default. The total amount owed to all creditors at the time of our review was $740,824, which included balances and related interest/service charges of: $51,519 relating to the bank mortgage; $449,416 relating to the second mortgage with the building materials supplier; and $239,889 relating to other creditors.

Auditor General of Newfoundland and Labrador 395

2.25 Discovery Regional Development Board Inc.

An official of DOC indicated that they were in the process of trying to sell the building and that one option being actively pursued is selling the building to the Department of Justice for development as a court facility. The DOC anticipates the selling price to be approximately $600,000, which will then be used in an attempt to settle its outstanding liabilities.

2. Other Compliance Issues

Other instances where the requirements of the performance contract were not being complied with included:

h The performance contract states that gifts and donations are ineligible costs unless authorized in writing by the CEDA/SRDA Management Committee. In December 2001, the Corporation spent $823 on a Christmas dinner and social, held for Corporation Board members, staff, and invited guests, following a Board meeting. Expenses included liquor costing $162.

These were not direct operating expenditures as defined in the performance contract and therefore would have required specific approval from the Management Committee. No such approval was requested or obtained.

h The funding agreement between the Province and the Corporation which expired in August 2002 required the Corporation to repay any unexpended operational funds promptly and in any event within 30 days of written notice by the Management Committee. The Corporation had not remitted any of its unexpended operational funds and furthermore, the Corporation had not received written notification requesting that the amounts be repaid.

h The performance contract requires that regular progress reports be provided to the Management Committee. These progress reports are to include a financial review and are the basis for advancing approved funding. Although the financial review submitted to the Management Committee as a basis for the renewal of funding for the year ended 31 August 2002 did not cover July and August 2001, funding was approved and disbursed in September 2001.

396 Auditor General of Newfoundland and Labrador

2.25 Discovery Regional Development Board Inc.

Controls and Expenditures

We reviewed the Corporation’s purchasing practices to determine if they were adequate. The Corporation has only two staff in the administration area which provides a challenge in the establishment of segregation of duties and controls over expenditures. However, given the limited number of staff, it is even more important that the Corporation be vigilant and have a system in place to maximize controls which are available.

Our review identified numerous instances where controls over expenditures were not in place, were inadequate or were disregarded. For example:

h The Corporation does not have documented policies and procedures in relation to purchasing activities or hiring of consultants. The presence of such policies and procedures would provide guidance related to purchase order preparation, expenditure approvals, accounting controls, payment verification, and monthly supplier reconciliations.

h Although not documented as being Board policy, Corporation staff indicated that the Corporation follows the Public Tender Act in acquiring goods and services. The Act requires tenders to be invited where the cost of goods and services is more than $10,000. The Act also requires three quotes to be obtained for purchases of goods and services costing $10,000 or less.

Aside from expenditures related to the purchase and renovation of a property through the Discovery Opportunity Centre Inc., the Corporation had very few expenditures in excess of $10,000. Our review of purchases of goods and services costing less than $10,000 indicated the following:

h The Corporation purchased a desk for the Executive Director’s office costing $3,481. Corporation officials advised that no quotes were obtained for this purchase and could not provide any information to support whether the best price had been obtained. It was also indicated that this significant purchase was made without the knowledge and approval of the Board. This was supported by our review of Board minutes.

Auditor General of Newfoundland and Labrador 397

2.25 Discovery Regional Development Board Inc.

Executive Director’s Desk

h The Corporation also purchased 2 used desks and 9 used filing cabinets from a surplus and salvage company costing $730. Corporation officials advised that no quotes were obtained for this purchase and could not provide any information to support whether the best price had been obtained. Corporation staff indicated that the desks and cabinets were of very poor quality.

Furniture from surplus and salvage company

398 Auditor General of Newfoundland and Labrador

2.25 Discovery Regional Development Board Inc.

h Corporation staff indicated that the Corporation’s financial statements for the year ended 31 August 1998 were prepared by a company which employed a member of the Corporation’s Board of Directors, and that a significant portion of the work was conducted by this individual. Corporation staff could not demonstrate on what basis the company was hired or whether any potential conflict of interest was addressed.

Our review of the financial statements prepared by this company indicated that no balance sheet was provided and also identified several errors and deviations from the normal information provided in general purpose financial statements.

h There is no documented approval for the acquisition of goods and services through the use of purchase orders or other means. As well, invoice approval was inadequate in that the Board did not make use of a procedure stamp which would evidence such procedures as ensuring receipt of goods, invoice additions checked, appropriate account to be charged, and payment approval.

h Although the office manager performed all accounting functions, there was no indication that the office manager’s work was reviewed or that reports such as payroll journals, bank reconciliations, general journals and general ledgers were independently reviewed. This individual has signing authority on the Corporation’s bank account and at times has also performed some of the duties of the Board’s Secretary and Treasurer. As well, while the office manager handles money on behalf of the Corporation, the individual was not bonded as was directed by the Board.

h We were informed that while, as a matter of practice, prior approval is obtained from the Board for significant purchases, there was no threshold amount or specifics provided on which purchases would be considered as significant. In many cases there was no documented evidence of prior Board approval. Controls would be strengthened if a threshold amount or specifics were provided, and if all required approvals were in writing. While some Board minutes indicated “invoices approved for payment”, there were no listings of the approved invoices in the minutes and no support to evidence approval was obtained from the Board prior to the purchase being made. Corporation staff indicated that these approvals are most often given verbally.

Auditor General of Newfoundland and Labrador 399

2.25 Discovery Regional Development Board Inc.

h There were a number of issues relating to travel claims as follows:

h The Corporation’s travel policies do not provide guidance for staff in several areas. For example, no guidance is provided on the time or distance away from head office required for meal reimbursement, the frequency or length of personal telephone calls, the use of rented vehicles, and travel advances.

h We identified two duplicate claims made by Board members. In one instance, the Corporation’s former President submitted two separate claims for personal vehicle mileage for $75. In the other instance, the Corporation’s former Treasurer submitted two separate claims relating to meals for $36. These overpayments were not detected by the Corporation and no recovery has been made.

h There was one instance where the former Executive Director submitted two separate travel claims which indicated travel on the same dates and times to two different locations. The total of both claims was $126.

h Travel claims did not always include the date of travel or the time of departure and return. Without this information it was difficult to determine if the travel expenditures claimed were legitimate. In some cases where the time of departure or return were provided, the times provided did not support the amounts claimed for meals.

h In addition to the above, our review of travel expenditures indicated that in July 2002, the Board was notified by the Atlantic Canada Opportunities Agency (ACOA) of irregularities in travel claims that had been identified during an ACOA review of the Corporation’s operating costs. In a letter to the Corporation’s former President from an ACOA official, dated 12 July 2002, it was indicated that there were concerns relating to directors’ travel claims and reference to the fact that the ACOA review also took into consideration the provision of federal funding to another named ACOA community development partner where there were overlapping memberships on the boards of directors. While the letter did not detail the particular irregularities, Corporation staff informed us that the two Board members in question were found to be

400 Auditor General of Newfoundland and Labrador

2.25 Discovery Regional Development Board Inc.

submitting travel claims under both boards for the same travel.

In an August 2002 report to Corporation Board members, the former President outlined the results of a meeting with the ACOA official and the Chair of the other named community development partner. The report referred to concerns ACOA had regarding travel claims by two board members who had seats on both boards. It was reported that the review covered the past two years and that 27 irregularities had been identified. It was also reported that ACOA was requesting that the irregularities cease immediately and that the Board take action to correct the matter. In September 2002, the Board decided to suspend the two Board members indefinitely from the Board until ACOA or the two Board members could satisfactorily inform the Board that the matter had been resolved.

We were informed by Corporation officials that no further action was taken in relation to this matter and that no monies were recovered from the two Board members.

In addition, we were advised by an official of the Department of Industry, Trade and Rural Development that, on one occasion, one of the two Board members submitted a travel claim for personal vehicle mileage to attend a Board meeting where the Board member travelled with another Board member. It was further disclosed that the Board member in question did not own a vehicle. Travel claims submitted by this Board member over a 46-month period, during appointment to the Board, totalled $8,258, of which $4,433 was for personal vehicle mileage.

h The Corporation spent a total of approximately $5,800 on expenses relating to cellular telephones from 1 September 2001 to 31 March 2003. During our review, we performed an analysis of these expenses. Our review in this area disclosed the following:

h Although the former Executive Director’s employment was terminated on 8 February 2002, the Corporation did not discontinue access to the cellular phone until June 2002. During this period, the Corporation paid a total of $694 in cellular phone charges for this individual.

Auditor General of Newfoundland and Labrador 401

2.25 Discovery Regional Development Board Inc.

h Monthly fees totalling $308 were paid for a cellular phone which was not used for a period of four months. Corporation staff could not demonstrate whether any analysis was completed of the continuing need for the cellular phone service versus the cost of maintaining the service.

Project Administration

The Corporation hires staff as required to head initiatives it has identified to forward its strategic plan. Such initiatives include: a Career Information Resource Centre, a Community Access Program, fisheries and agriculture development programs, and various information technology development initiatives.

Our review indicated that most project expenses consisted of salaries and related travel and administration expenses, and that with the exception of the Career Information Resource Centre project which was administered by Human Resources Development Canada, none of the projects involved significant capital expenditures.

As indicated elsewhere in this report, our review indicated that there was insufficient information provided on initiatives and projects to enable the Board to monitor how resources were utilized in meeting stated objectives contained in work plans and the Strategic Economic Plan. As well, there was no annual evaluation of the various initiatives and projects which could be used by the Board or Management Committee to determine whether the initiatives or projects achieved the intended results and contributed to planned objectives.

Human Resources

The Corporation currently has two employees who work in the administration area, an Executive Director and an Office Manager. The salaries of these two employees are paid through the administration account. The remaining employees are hired and assigned to various projects as needed. The salaries for these employees are charged to the various projects.

Employee salaries and benefits are the largest expenditure items of the Corporation. For example, for the year ended 31 August 2001, salaries for administrative employees was $103,832 or 57% of total administrative expenditures while salaries for employees assigned to various projects was $347,695 or 59% of total project funds.

402 Auditor General of Newfoundland and Labrador

2.25 Discovery Regional Development Board Inc.

Our review of the Corporation’s human resource practices indicated the following:

h Staff of the Corporation informed us that new positions are publicly advertised and that candidates are selected and interviewed by a committee of three individuals. However, no evidence could be provided, such as competition files or personnel files, to enable us to review for compliance with this process. Corporation staff indicated they have not been able to locate these files. Given the absence of personnel files, we were also unable to determine on what basis people were hired and whether salaries and benefits they received were in compliance with any employment contracts which may have been in place.

h There are no attendance records kept for staff to keep track of leave usage and accumulated balances. Corporation staff indicated they are responsible for monitoring their own attendance.

h Records of overtime and time taken in lieu of overtime are also maintained individually by each staff member, and there is no documented approval to work overtime.

h The Corporation’s Policy and Procedures Manual requires that staff performance appraisals be completed. While personnel files could not be located to determine compliance with this requirement, Corporation staff indicated that some appraisals have been conducted in the past.

h In lieu of a Corporation administered health and life insurance benefit program, the Corporation’s stated policy is that employees are to be paid a maximum of 50% of the costs of private health and life insurance. Our review indicated that instead, the Corporation paid a flat rate of $110 each month to employees and that no proof of insurance was requested. Corporation staff could not demonstrate why these flat rate payments were being made or provide the rationale for the $110 rate. Also, no taxable benefit was included on the employee’s Canada Customs and Revenue Agency (CCRA) Statement of Remuneration Paid relating to such payments.

h The Corporation’s payroll remittance for January 2002 was filed late with the CCRA, which resulted in the Corporation receiving a warning. No interest or penalties were incurred in this instance; however, at the time of our review, the remittance for December 2002 had not been forwarded.

Auditor General of Newfoundland and Labrador 403

2.25 Discovery Regional Development Board Inc.

h In October 1999, a former employee of the Corporation filed two separate complaints against the Board with the Human Rights Commission. The first complaint, alleging discrimination, sexual harassment and sexual solicitation, was settled in May 2000 through mutual agreement between the Board and the former employee.

In November 2000, the individual’s employment with the Corporation was terminated. The reason given for the termination was budgetary. The Corporation provided the employee with 12 weeks salary totalling $6,577, which was well in excess of the required 2 weeks. In December 2000, the complaint was re-opened and an additional complaint was filed alleging retaliation for filing the initial complaint. In December 2001, the Human Rights Commission referred this matter to a board of inquiry. Corporation officials indicated that both parties agreed to a settlement of $7,500 which was paid in April 2003.

The Corporation hired a law firm to represent the Board’s interests in these matters. Corporation staff indicated there was no call for proposals for this legal work and could not demonstrate whether the decision was approved by the Board. It was also indicated that the legal fees were not covered under the Corporation’s Directors’ and Officers’ liability insurance but that the Corporation was advised that legal fees would only amount to a few thousand dollars. Legal fees billed to the Corporation at the time of our review amounted to $28,106. Subsequent to our review, the Corporation negotiated a reduction in these legal fees to $20,000 and the amount was paid in May 2003.

In addition to legal costs incurred by the Corporation in relation to these complaints, the Corporation also incurred legal fees on behalf of another employee who was personally named in the complaints. We could not determine the extent to which legal fees incurred related to this other employee, as invoices supporting the legal costs paid by the Corporation did not distinguish time spent on the Corporation’s defence from time spent on the employee’s defence. In addition, three travel claims totalling $695 were submitted by this employee for travel to St. John’s to attend meetings at the law firm. Again, it is not determinable whether these claims were incurred in relation to the Corporation’s defence, the employee’s defence, or both.

404 Auditor General of Newfoundland and Labrador

2.25 Discovery Regional Development Board Inc.

h Corporation officials indicated that in October 2002, another former employee consulted a lawyer relating to an allegation of wrongful dismissal. This issue had not been resolved at the time of our review.

Capital Assets

As at 31 August 2002, the Corporation’s accounting records reflected a total of $165,181 in capital assets. These capital assets included those used for administration as well as for projects.

Our review indicated that the Corporation is not adequately controlling its capital assets. The following issues were identified:

h There is no capital asset ledger in place and no mechanism to identify the assets held by the Corporation. Corporation officials provided a listing of the Corporation’s assets which had been prepared in 2002; however, the listing was inadequate in that it did not include asset identifiers such as serial numbers, did not provide cost information related to the assets, and did not indicate whether the assets were traced to purchase invoices.

Given the lack of a Corporation capital asset ledger or asset listing, it was not possible to complete a physical count to compare against such records. A physical count was performed and compared to the external auditor’s working paper files; however, the count could not be performed on a specific identification basis as the working papers did not always provide details such as serial numbers or model numbers. As a result, for computer equipment in particular, we could only compare the number physically counted to the number listed for reasonableness. No detail was provided on assets held prior to September 1998.

h The Corporation’s general ledger reports as at 31 August 2002 were inaccurate as they included capital assets which had been returned to the funding partner during the year.

h The Corporation has not established operational policies and procedures governing the acquisition, movement, disposal, identification and recording of capital assets. Of particular concern is the lack of adequate safeguards in place to ensure the physical security of the assets held by the Corporation. Several assets were in rooms which were used by another tenant of the building, with other assets in publicly accessible rooms with doors which cannot be locked.

Auditor General of Newfoundland and Labrador 405

2.25 Discovery Regional Development Board Inc.

h The Corporation is not properly controlling its moveable assets that are on loan to staff and to the public. The Corporation does not record the loan of such assets to ensure they are returned and to determine responsibility for any damage to loaned assets. For example, while Corporation staff indicated that one computer and one computer projector were on loan to the public and that one computer was at a staff person’s home, there was no record maintained of who had the equipment.

h At the time of our review, there was no contents insurance in place to protect the assets of the Corporation.

Recommendations

The Corporation should:

h develop a new Strategic Economic Plan to replace the original Plan which expired in 2002;

h provide the Board with information on projects at its regular meetings to monitor how resources were utilized in meeting stated objectives, and prepare an annual evaluation of initiatives and projects to determine what results were achieved;

h comply with the requirements of its performance contract and the Corporations Act;

h comply with its indicated policy of issuing public tenders for expenditures in excess of $10,000 and obtaining quotes for purchases $10,000 or less;

h ensure that adequate documentation exists to support payment decisions and that only appropriate payments are made;

h ensure that documentation exists to support its human resource activities; and

h have a complete and accurate record of its capital assets.

406 Auditor General of Newfoundland and Labrador

2.25 Discovery Regional Development Board Inc.

Corporation’s Response

Discovery Regional Development Board recognized some of the concerns expressed in this report before this document was written. During the 2002 operating year the board decided to hire an outside consultant to perform a review of the internal management practices that were in place, to determine how effective they were and if they were being adhered to. The board was aware that it was time to do a review and implement any changes that were necessary. Many concerns that were identified are included in the recommendations of this report, these points have already been addressed.

There are seven recommendations:

1. Develop a new Strategic Economic Plan: This plan expired at the end of 2002. It was to be a significant piece of work during the last year, as identified in the work plan. However because of resources issues this was not completed. It will be completed this winter, 2004. The board is aware of the importance of the SEP.

2. Reporting on Initiatives and monitoring progress: Sector facilitators and the Executive Director are required to prepare monthly reports on the activity that they are involved with and their progress during the month. Semi-annual and annual reports have always been a part of the board’s policy. Funding partners also receive regular progress reports.

3. Comply with requirements of contract: Through a management committee consisting of the board and government partners the requirements of the contract are regularly monitored. The board understands its role and the responsibilities that it has.

4. Public Tenders, Obtaining quotes: These practices have been in place for several months.

5. Adequate documentation to support payment decisions: All payment decisions are now made by the finance committee and passed by the board at the monthly board meeting. Payments are made monthly, unless something has to be taken care of in a more timely manner.

6. Documentation to support Human Resources activity: All human resource activity is now systematically dealt with. The Human Resources committee is responsible for hiring and sector experts are often asked for advice on human resource requirements.

Auditor General of Newfoundland and Labrador 407

2.25 Discovery Regional Development Board Inc.

7. Accurate record of capital assets: Has been completed and regularly updated.

While these recommendations have been justly dealt with, there are other points arising from this report that the board feels requires some further clarification and explanation.

The board never felt it violated its contract in the purchase of the building that became known as the Discovery Opportunity Center. Money that was used to purchase this property was surplus money that was accumulated from various contracts, HST rebates, etc. It was not direct operating core money. The board did not actually purchase the building, but rather a separate incorporated company, the Discovery Opportunity Center was the buyer. At no time did that board feel that a breach of contract was carried out. The Corporation was established to move forward the Information Technology sector, not to circumvent the performance contract.

The board feels that the amount of focus on the DOC in this report is irrelevant. This is a separate entity that the board helped generate, just as it has assisted in many other initiatives in the zone. However other initiatives are not mentioned, nor should they be.

Practices such as applying for HST rebates annually is a policy that many boards and associations follow. Applying for rebates on a more frequent basis adds to the amount of paperwork and administrative functions that the board feels is not necessary.

The day to day management practices and procedures that are referred to in this report have been corrected. Efforts are made to ensure that items like overtime and travel are completed correctly and handled in the appropriate manner. The irregularities in travel that are identified in this report were also identified before this review commenced, management procedures that were in place by the board did identify these problems and the issues were dealt with.

Other points worth noting since this report has been completed:- Documented approval for goods and services is standard- Travel claims are completed, submitted and paid correctly- A finance committee is in place- Threshold amounts on purchases are in place- Overtime is documented and controlled by core staff, leave

requests are filed- Regular monitoring of projects and initiatives- Personnel files are kept up to date, Human Resources

committee in place

408 Auditor General of Newfoundland and Labrador

2.25 Discovery Regional Development Board Inc.

All these areas have been identified and improvements made.

The current volunteer board works closely with its partners to carry out the mandate. The board has attracted new members that are committed to provide the residents of the zone with the services that a zonal board can provide. The board is more transparent in its approach and will continue to move forward and make improvements in any area that requires change. This report reflects the way it was and not the way it is. The board also has a new group of employees that are committed to carrying out their contracts to the benefit of the residents of Zone 15.

Auditor General of Newfoundland and Labrador 409

2.25 Discovery Regional Development Board Inc.

410 Auditor General of Newfoundland and Labrador

2.25 Discovery Regional Development Board Inc.

Related Documents