BBM 605 A comparative study on Indian banks on the basis of Capital adequacy norms by BASEL II (A global standard Framework) UNDER THE GUIDANCE OF SUBMITTED BY-

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

BBM 605

A comparative study on Indian bankson the basis of Capital adequacy norms by BASEL II

(A global standard Framework)

UNDER THE GUIDANCE OF SUBMITTED BY-

Dr. SANJAY BHUSHAN Mahima Sharan

BBM 6 SEM

097523

EXECUTIVE SUMMARY

Banks offer various loans and advances to its

customers to achieve their financial plans. A customer

is satisfied only when the banker knows, understands

and meets the needs the needs and expectations of the

customer.

‘Weighted assets’ is a measure of the amount of a

bank’s assets, adjusted for risk. By adjusting the

amount of each loan for an estimate of how risky it is,

we can transform this percentage into a rough measure

of the financial stability of a bank. The main use of

risk weighted assets is to calculate tier 1 and tier 2

capital adequacy ratios. Basel I used a comparatively

simple system of risk weighing.

Capital adequacy ratios are a measure of the amount of

a bank's capital expressed as a percentage of its risk

weighted credit exposures. The minimum capital adequacy

ratios have been developed to ensure banks can absorb a

reasonable level of losses before becoming insolvent. A

minimum capital adequacy ratio serves to protect

depositors and promote the stability and efficiency of

the financial system. Two types of capital are measured

- tier one capital which can absorb losses without a

bank being required to cease trading, e.g. ordinary

share capital, and tier two capital which can absorb

losses in the event of a winding-up and so provides a

lesser degree of protection to depositors, e.g.

subordinated debt.

CHAPTER – I

INTRODUCTION

1.1 INTRODUCTION TO CAPITAL ADEQUACY

Risk weighted assets is a measure of the amount of a

bank’s assets, adjusted for risk. The nature of a

bank’s business means it is usual for almost all of a

bank’s assets will consist of loans to customers.

Comparing the amount of capital a bank has with the

amount of its assets gives a measure of how able the

bank is to absorb losses. It its capital is 10% of its

assets, then it can lose 10% of its assets without

becoming insolvent.

Capital Adequacy

Central Bank Governors of the ten countries formed a

committee of banking supervisory in 1975. This

committee usually meets at the BIS in Basel,

Switzerland. Hence it has come to know as the Basel

Committee. The Basel Committee provided the framework

for capital adequacy in 1988.

The Basel – II accord is expected to establish a

minimum level of capital for international active bank.

National regulatory are free to set higher standards

for international active bank. National regulatory are

free to set higher standards for minimum capital.

Capital Adequacy Ratios

Capital adequacy ratios are a measure of the amount of

a bank’s capital expressed as a percentage of its risk

weighted credit exposures.

The Basel Capital Accord sets minimum capital adequacy

ratios that supervisory authorities are encouraged to

apply. These are:

Tier one capital to total risk weighted credit

exposures to be not less than 4 per cent.

Total capital (i.e. tier one plus tier two less

certain deductions) to total risk weighted credit

exposures to be not less than 8 per cent.

There are some further standards applicable to tier two

capital:

Tier two capital may not exceed 100 percent of tier

one capital

Lower tier two capital may not exceed 50 percent of

tier one capital

Lower tier two capital is amortized on a straight

line basis over the last five years of its life.

1.2 STATEMENT OF THE PROBLEM

With the implementation of Basel I and Basel II norms,

the Indian Banks are forced to maintain adequate

capital in both tier I and tier II.

CAR is calculated taking into account the RWA. Capital

Adequacy Ratio is a measure of the amount of a bank’s

capital expressed as a percentage of its risk weighed

credit exposures. Thus the present study entitled “A

Study on Capital Adequacy of State Bank of India” has

been taken off.

1.3 Objectives of the Study

To compare the working of different Indian Banks onthe basis of capital adequacy norms by Basel II.

To give suitable operational strategies helpingselected banks conforming to BASEL II norms..

1.4 Research Methodology

Case studies related to Banks selected.

The data required for the study were collected from

secondary sources.

The data required were collected from the records

of SBI, UBI, ICICI, HDFC and RBI web sites. The

collected data were compiled and analyzed using

ratios. The ratios used include Tangible Common

Equity ratio and Capital Adequacy ratio.

1.5 Period of the Study

The present study has taken into account five years

of data from 2007-12.

1.6 Limitations of the Study

Due to paucity of time, more years of data could

not be taken.

The data were kept confidential and hence, it was

difficult to access the adequate data.

1.7 Chapters

Chapter I deal with introduction to Risk Weighted

Assets, Capital Adequacy, Statement of Problem,

Objective of the Study, Research Methodology,

Limitations and Chapters.

Chapter II deals with the profile of Indian Banking

Industry and that of selected banks.

Chapter III deals with Basel I and Basel II norm

for capital adequacy.

Chapter IV deals with the analysis and

interpretation of data & information.

Chapter V deals with the findings, suggestion and

conclusion that derived from the study.

CHAPTER – II

PROFILES

2.1 PROFILE OF THE INDIAN BANKING INDUSTRY

The Indian Banking industry, which is governed by the

Banking Regulation Act of India, 1949 can be broadly

classified into two major categories, non-scheduled

banks and scheduled banks. Scheduled banks comprise

commercial banks and the co-operative banks. In terms

of ownership, commercial banks can be further grouped

into nationalized banks, the State Bank of India and

its group banks, regional rural banks and private

sector banks (the old/ new domestic and foreign). These

banks have over 67,000 branches spread across the

country.

The first phase of financial reforms resulted in the

nationalization of 14 major banks in 1969 and resulted

in a shift from Class banking to Mass banking. This in

turn resulted in a significant growth in the

geographical coverage of banks. Every bank had to

earmark a minimum percentage of their loan portfolio to

sectors identified as “priority sectors”. The

manufacturing sector also grew during the 1970s in

protected environs and the banking sector was a

critical source. The next wave of reforms saw the

nationalization of 6 more commercial banks in 1980.

Since then the number of scheduled commercial banks

increased four-fold and the number of bank branches

increased eight-fold.

After the second phase of financial sector reforms and

liberalization of the sector in the early nineties, the

Public Sector Banks (PSB) s found it extremely

difficult to compete with the new private sector banks

and the foreign banks. The new private sector banks

first made their appearance after the guidelines

permitting them were issued in January 1993. Eight new

private sector banks are presently in operation. These

banks due to their late start have access to state-of-

the-art technology, which in turn helps them to save on

manpower costs and provide better services.

Indian banking system is based on strong fundamentals

and more specially PSUs will become stronger in the

face of foreign bank competition. Although PSU's do

have qualified manpower , up-graded technology , vast

infrastructure , network and growing professionalism

and have the capability to effectively provide

diversified products and customized solutions in the

light of emerging competition but rather than hitting

the market overnight with aggressive strategies ,they

might choose a cautious ,slow and calculated

"watch ,pause and proceed" strategy for long term

sustainability and market positioning. Their national

character and identity with the masses and high

domestic presence and reach in rural and semi urban

areas are the greatest strength which are crucial in

Indian environment dominated by socio-cultural and

psychological factors. Their past history, growth and

development and more specially their firm standing in

the face of recent global recession are quite

reflective of their intrinsic strength and their

readiness for future .PSUs have learnt hardways all

these years and grown so well. They have a very good

feel of the Indian market and I personally feel that in

the longer run they will capitalise on their strengths

and opportunities and out play foreign bank competition

.We shall never underestimate them .Foreign banks may

talk high fi but PSUs understand the grassroots

realities. Performance shall not be judged by

profitability or business volume but by the economic

and social contribution which perhaps will be the point

PSUs will be scoring over.

2.2 PROFILE OF STATE BANK OF INDIA

The State Bank of India (SBI) is the largest commercial

bank in India in terms of profits, assets, deposits,

branches and employees. State Bank of India was

constituted through an act of Parliament in 1955.The

Bank is actively involved since 1973 in non-profit

activity called Community Services Banking. All

branches and administrative offices throughout the

country sponsor and participate in large number of

welfare activities and social causes. Business is more

than banking because it touches the lives of people

anywhere in many ways.

SBI is the only bank in India to be ranked among

the top 100 banks in the world and among the top 20

banks in Asia in the annual survey by The Banker. SBI

has eight business units, namely corporate banking;

international banking and domestic banking for

concentrating on core areas; associate banks division

for looking after the working of these banks; credit

division to monitor the overall credit; and three other

business units, namely finance, corporate development

in house works. The bank has a network of 66

offices/branches in 29 countries spanning all time

zones. The SBI`s international presence is supplemented

by a group of overseas and NRI branches in India and

correspondent links with over 522 leading banks of the

world. SBI`s offshore joint ventures and subsidiaries

enhance its global stature. Keeping in view the

exponential growth achieved in self help group (SHG)

financing in the recent past and good repayments (over

90%) under the scheme, the bank has decided to credit

link 1,000,000 SHGs by the end of march 2008. The bank

is entering into many new businesses with strategic tie

ups – Pension Funds, General Insurance, Custodial

Services, Private Equity, Mobile Banking, Point of Sale

Merchant Acquisition, Advisory Services, structured

products etc – each one of these initiatives having a

huge potential for growth.

The Bank is forging ahead with cutting edge

technology and innovative new banking models, to expand

its Rural Banking base, looking at the vast untapped

potential in the hinterland and proposes to cover

100,000 villages in the next two years. It is also

focusing at the top end of the market, on whole sale

banking capabilities to provide India’s growing mid /

large Corporate with a complete array of products and

services. It is consolidating its global treasury

operations and entering into structured products and

derivative instruments. Today, the Bank is the largest

provider of infrastructure debt and the largest

arranger of external commercial borrowings in the

country. It is the only Indian bank to feature in the

Fortune 500 list.

The Bank is changing outdated front and back end

processes to modern customer friendly processes to help

improve the total customer experience. With about 8500

of its own 10000 branches and another 5100 branches of

its Associate Banks already networked, today it offers

the largest banking network to the Indian customer. The

Bank is also in the process of providing complete

payment solution to its clientele with its over 8500

ATMs, and other electronic channels such as Internet

banking, debit cards, mobile banking, etc. With four

national level Apex Training Colleges and 54 learning

Centre’s spread all over the country the Bank is

continuously engaged in skill enhancement of its

employees. Some of the training programes are attended

by bankers from banks in other countries.

The bank is also looking at opportunities to grow

in size in India as well as internationally. It

presently has 82 foreign offices in 32 countries across

the globe. It has also 7 Subsidiaries in India – SBI

Capital Markets, SBICAP Securities, SBI DFHI, SBI

Factors, SBI Life and SBI Cards - forming a formidable

group in the Indian Banking scenario. It is in the

process of raising capital for its growth and also

consolidating its various holdings. Throughout all this

change, the Bank is also attempting to change old

mindsets, attitudes and take all employees together on

this exciting road to Transformation. In a recently

concluded mass internal communication programme termed

‘Parivartan’ the Bank rolled out over 3300 two day

workshops across the country and covered over 130,000

employees in a period of 100 days using about 400

Trainers, to drive home the message of Change and

inclusiveness. The workshops fired the imagination of

the employees with some other banks in India as well as

other Public Sector Organizations seeking to emulate

the programme.

SBI along with its associate banks offer a wide

range of banking products and services across its

different client markets. The bank has entered the

market of term lending to corporates and infrastructure

financing, traditionally the domain of the financial

institutions. It has increased its thrust in retail

assets in the last two years, and has built a strong

market position in housing loans.

SBI, through its non-banking subsidiaries, offers a

host of financial services, viz., merchant banking,

fund management, factoring, primary dealership,

broking, investment banking and credit cards. SBI has

commenced its life insurance business by setting up a

subsidiary, SBI Life Insurance Company Limited, which

is a joint venture with Cardiff S.A., one of the

largest insurance companies in France. SBI currently

holds 74% equity in the joint venture.

SBI will maintain a good earnings profile in the

medium term despite high pressure on yields due to the

increasing competition in the banking sector. SBI’s

earning profile is characterised by consistency in the

return on assets (PAT/Average Assets), at around 1% per

annum for the past three years, and diverse income

streams. State Bank of India is entering the private

equity sector by picking up close to 20% equity stake

in Sage Capital Funds Management, an asset management

company (AMC) floated by Sage Capital. The company has

started a USD 200-million fund, Sage Capital Value

Fund, that will invest in Indian companies, as a

volatile capital market pushes down valuations of firms

prompting this class of investors to value-pick stocks

in the world`s second-fastest growing economy.

2.3 PROFILE OF UBI

Originally established as United Bank of India Ltd., the bank was a result of merger of four Bengali banks -Comilla Banking Corporation Ltd., Bengal Central Bank Ltd., Comilla Union Bank Ltd. and Hooghly Bank Ltd. in 1950. Almost two decade later, in 1969, United Bank of India was one among the major banks that were nationalized. Thereafter, the bank expanded in a major way, covering all the states of India. It also was an active participant in the growth and developmental

activities, mainly in the rural and semi-urban regions.

Acknowledging the efforts made by United Bank of India,it was honored as a Lead Bank in several districts of India. Presently, it the Lead Bank in 30 districts in the States of West Bengal, Assam, Manipur and Tripura. The Bank also holds the position of being the Convener of the State Level Bankers' Committees (SLBC) for the States of West Bengal and Tripura. The bank is known tospread its banking services especially in the Eastern and North-Eastern parts of India. United Bank of India supported the 4 Regional Rural Banks (RRB) at West Bengal, Assam, Manipur and Tripura.

Thanks to United Bank of India, even places with littleor no reach such as the Sunderbans in West Bengal, today, have an access to banking services. UBI had established two floating mobile branches on motor launches. These moved from one island to another on different days of the week, providing people with all the facilities. However, the floating branches paved way to the full-fledged bank branches at these centers.The largest lender to the tea industry, UBI is also recognized as the 'Tea Bank', for its longstanding involvement with the financing of tea gardens.

Branches & ATM Services Presently the Bank has a three-tier organizational set-

up consisting of the Head Office, 28 Regional Offices. Out of its total 1450 branches, 500 of them have been automated either fully or partially. Its branches in all the metropolitan cities of India are equipped with Electronic Fund Transfer System. UBI has ATMs all over the country and having Cash Tree arrangement with 11 other Banks.

Products & Services Deposit Scheme Credit Scheme NRI Services United Mobile Services FOREIGN Exchange Insurance Policies RTGS Tax- Collection E-Payment Nomination Facility Lockers Credit Cards ATM Cum Debit Cards Remittance Service in tie up with Western Union

Money Transfer

Third Party Banking Products Mutual Funds Life Insurance in tie up with Tata AIG Life

Insurance Company

Non- Life Insurance policies in tie-up with Bajaj Allianz Insurance Company Ltd

Credit Card in tie-up with SBI cards Foreign Remittance Services in tie-up with Western

Union Demat Depository Services in association with

Central Depository Services (India) Ltd. (CSDL)

2.4 PROFILE OF ICICI

ICICI Bank is India's second-largest bank with totalassets of Rs. 4,062.34 billion (US$ 91 billion) atMarch 31, 2011 and profit after tax Rs. 51.51 billion(US$ 1,155 million) for the year ended March 31, 2011.The Bank has a network of 2,621 branches and 8,003 ATMsin India, and has a presence in 19 countries, includingIndia.

ICICI Bank offers a wide range of banking products andfinancial services to corporate and retail customersthrough a variety of delivery channels and through itsspecialised subsidiaries in the areas of investmentbanking, life and non-life insurance, venture capitaland asset management.

The Bank currently has subsidiaries in the UnitedKingdom, Russia and Canada, branches in United States,

Singapore, Bahrain, Hong Kong, Sri Lanka, Qatar andDubai International Finance Centre and representativeoffices in United Arab Emirates, China, South Africa,Bangladesh, Thailand, Malaysia and Indonesia. Our UKsubsidiary has established branches in Belgium andGermany.

ICICI Bank's equity shares are listed in India onBombay Stock Exchange and the National Stock Exchangeof India Limited and its American Depositary Receipts(ADRs) are listed on the New York Stock Exchange(NYSE).

2.5 PROFILE OF HDFC

Housing Development Finance Corporation Limited, more popularly known as HDFC Bank Ltd, was established in the year 1994, as a part of the liberalization of the Indian Banking Industry by Reserve Bank of India (RBI).It was one of the first banks to receive an 'in principle' approval from RBI, for setting up a bank in the private sector. The bank was incorporated with the name 'HDFC Bank Limited', with its registered office inMumbai. The following year, it started its operations as a Scheduled Commercial Bank. Today, the bank boasts of as many as 1412 branches and over 3275 ATMs across India.

Amalgamations

In 2002, HDFC Bank witnessed its merger with Times BankLimited (a private sector bank promoted by Bennett, Coleman & Co. / Times Group). With this, HDFC and Timesbecame the first two private banks in the New Generation Private Sector Banks to have gone through a merger. In 2008, RBI approved the amalgamation of Centurion Bank of Punjab with HDFC Bank. With this, theDeposits of the merged entity became Rs. 1,22,000 crore, while the Advances were Rs. 89,000 crore and Balance Sheet size was Rs. 1,63,000 crore.

Tech-SavvyHDFC Bank has always prided itself on a highly automated environment, be it in terms of information technology or communication systems. All the braches ofthe bank boast of online connectivity with the other, ensuring speedy funds transfer for the clients. At the same time, the bank's branch network and Automated Teller Machines (ATMs) allow multi-branch access to retail clients. The bank makes use of its up-to-date technology, along with market position and expertise, to create a competitive advantage and build market share.

Capital StructureAt present, HDFC Bank boasts of an authorized capital of Rs 550 crore (Rs5.5 billion), of this the paid-up amount is Rs 424.6 crore (Rs.4.2 billion). In terms of equity share, the HDFC Group holds 19.4%. Foreign

Institutional Investors (FIIs) have around 28% of the equity and about 17.6% is held by the ADS Depository (in respect of the bank's American Depository Shares (ADS) Issue). The bank has about 570,000 shareholders. Its shares find a listing on the Stock Exchange, Mumbaiand National Stock Exchange, while its American Depository Shares are listed on the New York Stock Exchange (NYSE), under the symbol 'HDB'.

Products & Services

Personal Banking Savings Accounts Salary Accounts Current Accounts Fixed Deposits Demat Account Safe Deposit Lockers Loans Credit Cards Debit Cards Prepaid Cards Investments & Insurance Forex Services Payment Services NetBanking InstaAlerts MobileBanking InstaQuery

ATM PhoneBanking

NRI Banking Rupee Savings Accounts Rupee Current Accounts Rupee Fixed Deposits Foreign Currency Deposits Accounts for Returning Indians Quickremit (North America, UK, Europe, Southeast

Asia) IndiaLink (Middle East, Africa) Cheque LockBox Telegraphic / Wire Transfer Funds Transfer through Cheques / DDs / TCs Mutual Funds Private Banking Portfolio Investment Schemes Loans Payment Services NetBanking InstaAlerts MobileBanking InstaQuery ATM PhoneBanking

CHAPTER – III

BASEL IINORMS FOR BANKS

Central Bank Governors of the Group of Ten Countries

formed a Committee of banking supervisory authorities

in 1975. This Committee usually meets at the Bank of

International Settlement (BIS) in Basel, Switzerland.

Hence it has come to be known as the Basel Committee.

The Basel Committee provided the framework for capital

adequacy in 1988, which is known as the Basel I accord.

The norms for adequacy of capital used to differ from

bank and country to country. Japanese banks used to

consider capital to the extent of 1 to 2 % of their

assets level as adequate. Banks in some European

countries used to require 8 – 10 % of their assets as

their capital. The Basel Committee addressed the issue

of standardization and provided the requisite

framework. It defined components of capital, allotted

risk weights to different types or categories of assets

and pronounced as to what should be the minimum ratio

of capital to sum total of risk-weighted assets.

The Basel-I norms for risk weights were more of a

straightjacket nature. For example, all exposures to

sovereigns were given 0% risk weight. All bank

exposures had a risk weight of 20%. Corporate advances

had a risk weight of 100%. Such rigid approach without

any consideration for the strengths or weaknesses of

individual entities was the main shortcoming of the

Basel-I accord. The position that an excellent

corporate such as L & T could have less risk weight

than some of the banks was not recognized under this

accord. This accord continued to be operative for about

fifteen years, of course with some modifications from

time to time. It came for a total overhaul and review

during the last few years.

The first round of proposal for changes in the Basel-I

accord came up for deliberations and consultative

process in June 1999. An extensive consultative process

was initiated and the supervisory authorities across

the world were roped in this exercise. After five years

of deliberations, the framework for capital adequacy

was finalized with the approval of all the ten members

of the Basel Committee in June 2004.

The report of the Committee is titled as “International

Convergence of Capital Measurement and Capital

Standards – A revised framework”. The Committee intends

that the revised framework would be implemented by the

end of year 2006. In India, the parallel runs commenced

in April 2006 and implementation was complete on 31st

March 2007.

The fundamental objective of the Committee was to

revise the 1988 accord and strengthen the soundness and

stability of the banking system. The revised framework

would promote the adoption of stronger risk management

practices by banks. The revised framework provides

greater use of assessment of risk provided by Banks’

internal systems as inputs to capital calculations. It

demands capital allocation for operational risk for the

first time. It provides a range of options for

determining capital requirements for credit risk and

operational risk. It also emphasizes the need for

consistency in approach.

The Basel-II accord is expected to establish a minimum

level of capital for internationally active banks.

National regulators are free to set higher standards

for minimum capital. The revised framework is perceived

as more forward-looking approach and has a capacity to

evolve with time.

The new capital accord will require banks to manage

risks by not only allocating regulatory capital but

also by disclosing greater risk information and setting

standards for risk management processes. Basel-II

provides incentives for banks to invest and increase

the sophistication of their internal risk management

capabilities in order to gain reductions in capital.

This will help them to increase a bank’s lending which

in turn will give higher returns and value to its

shareholders.

Generally, banks consider a regulatory requirement as

an administrative burden with little or no benefit to

their bottom line. However, the Basel capital

requirements are viewed as an opportunity to

demonstrate their credentials. The reputation of a bank

is very important. Banks would ensure compliance with

the Basel standards to show themselves as good

practitioners in risk management.

SCOPE OF APPLICATION

The Basel – II accord aligns regulatory capital

with the banks’ risk profiles. The Basel Committee

recognizes that home country supervisors have an

important role in leading the enhanced cooperation

between home and host country supervisors that will be

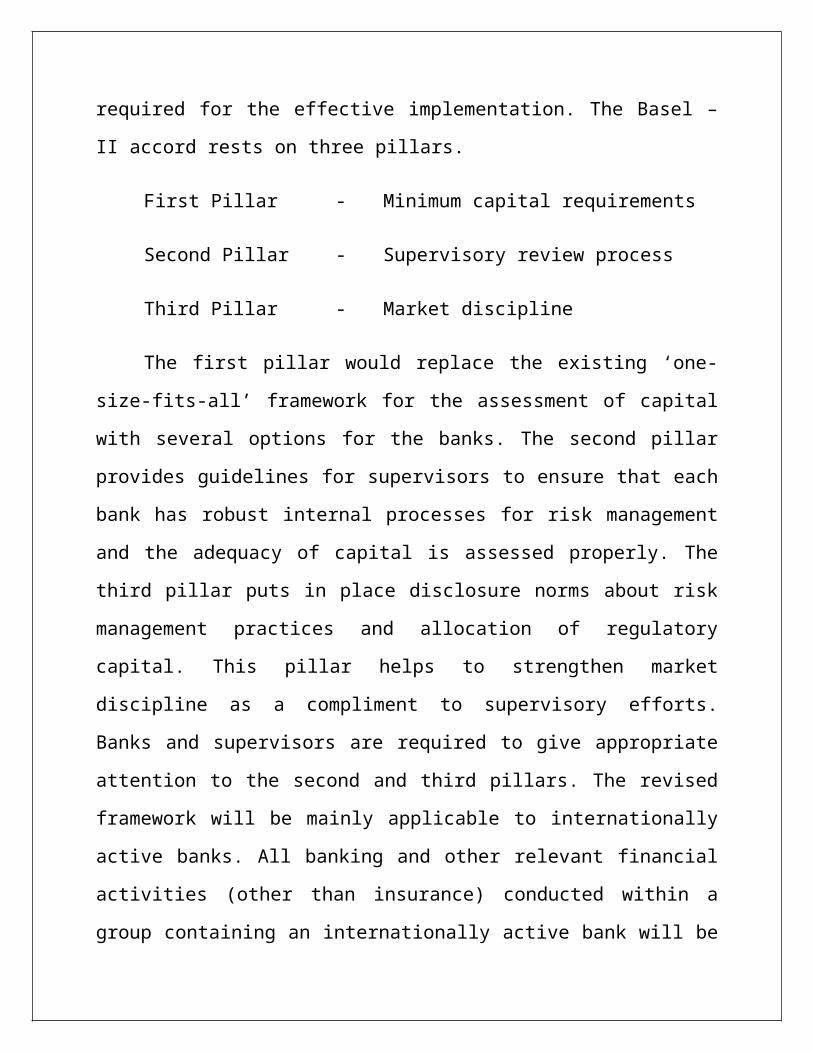

required for the effective implementation. The Basel –

II accord rests on three pillars.

First Pillar - Minimum capital requirements

Second Pillar - Supervisory review process

Third Pillar - Market discipline

The first pillar would replace the existing ‘one-

size-fits-all’ framework for the assessment of capital

with several options for the banks. The second pillar

provides guidelines for supervisors to ensure that each

bank has robust internal processes for risk management

and the adequacy of capital is assessed properly. The

third pillar puts in place disclosure norms about risk

management practices and allocation of regulatory

capital. This pillar helps to strengthen market

discipline as a compliment to supervisory efforts.

Banks and supervisors are required to give appropriate

attention to the second and third pillars. The revised

framework will be mainly applicable to internationally

active banks. All banking and other relevant financial

activities (other than insurance) conducted within a

group containing an internationally active bank will be

captured through a consolidation process. The revised

accord provides incentives to banks to improve their

risk management systems. The components of the three

pillars are presented below:

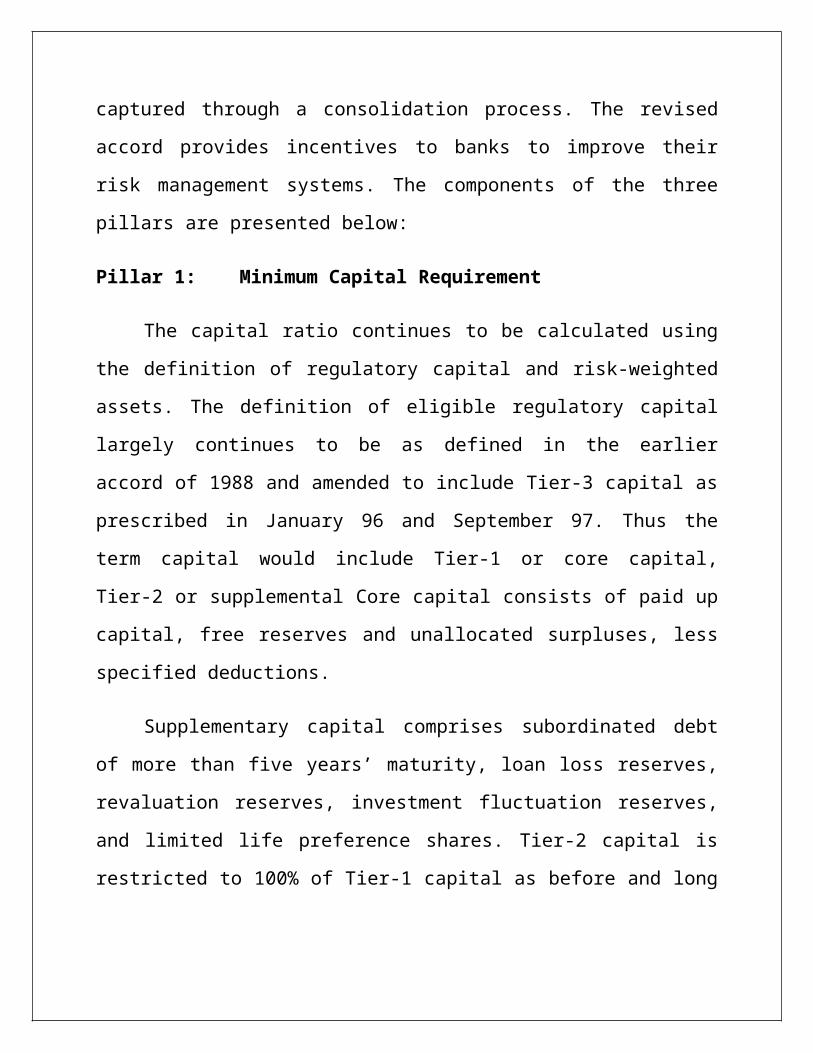

Pillar 1: Minimum Capital Requirement

The capital ratio continues to be calculated using

the definition of regulatory capital and risk-weighted

assets. The definition of eligible regulatory capital

largely continues to be as defined in the earlier

accord of 1988 and amended to include Tier-3 capital as

prescribed in January 96 and September 97. Thus the

term capital would include Tier-1 or core capital,

Tier-2 or supplemental Core capital consists of paid up

capital, free reserves and unallocated surpluses, less

specified deductions.

Supplementary capital comprises subordinated debt

of more than five years’ maturity, loan loss reserves,

revaluation reserves, investment fluctuation reserves,

and limited life preference shares. Tier-2 capital is

restricted to 100% of Tier-1 capital as before and long

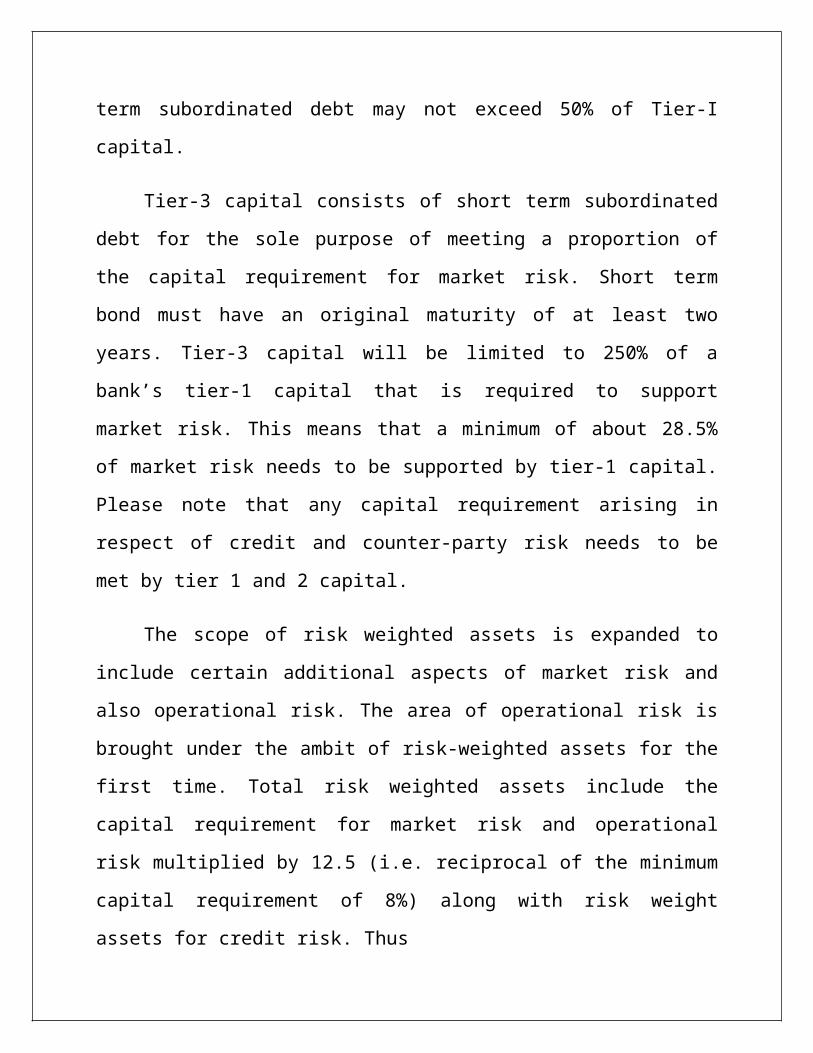

term subordinated debt may not exceed 50% of Tier-I

capital.

Tier-3 capital consists of short term subordinated

debt for the sole purpose of meeting a proportion of

the capital requirement for market risk. Short term

bond must have an original maturity of at least two

years. Tier-3 capital will be limited to 250% of a

bank’s tier-1 capital that is required to support

market risk. This means that a minimum of about 28.5%

of market risk needs to be supported by tier-1 capital.

Please note that any capital requirement arising in

respect of credit and counter-party risk needs to be

met by tier 1 and 2 capital.

The scope of risk weighted assets is expanded to

include certain additional aspects of market risk and

also operational risk. The area of operational risk is

brought under the ambit of risk-weighted assets for the

first time. Total risk weighted assets include the

capital requirement for market risk and operational

risk multiplied by 12.5 (i.e. reciprocal of the minimum

capital requirement of 8%) along with risk weight

assets for credit risk. Thus

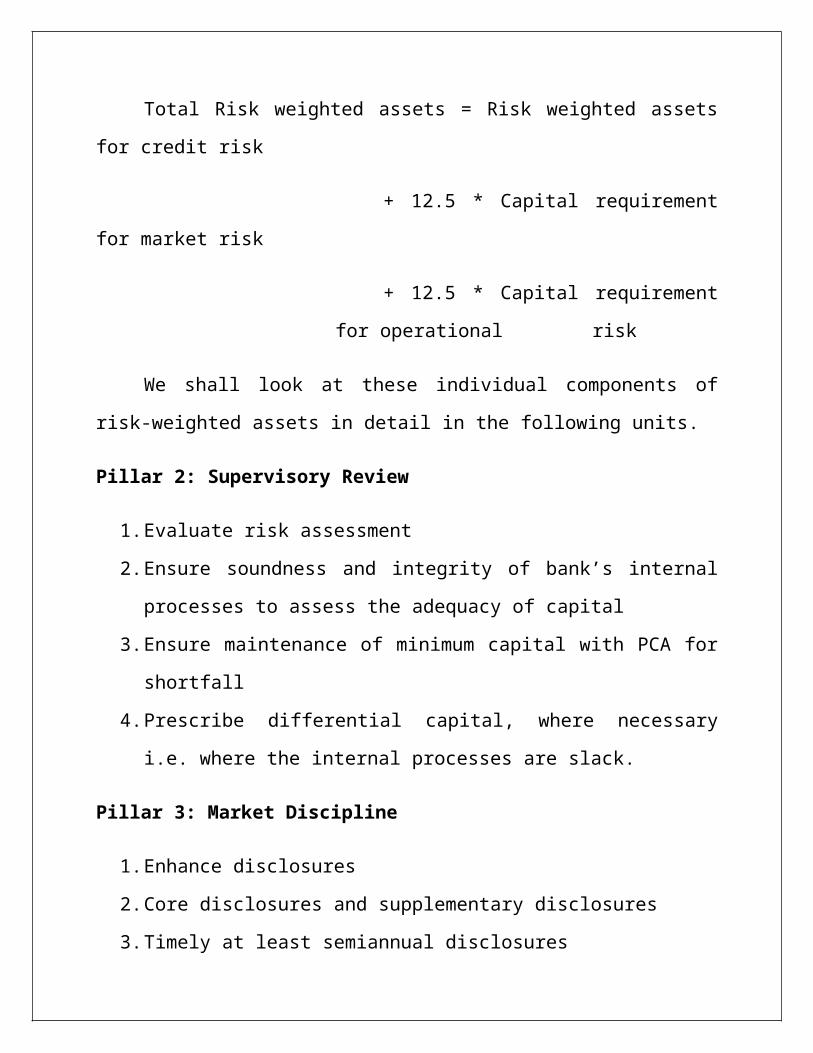

Total Risk weighted assets = Risk weighted assets

for credit risk

+ 12.5 * Capital requirement

for market risk

+ 12.5 * Capital requirement

for operational risk

We shall look at these individual components of

risk-weighted assets in detail in the following units.

Pillar 2: Supervisory Review

1.Evaluate risk assessment

2.Ensure soundness and integrity of bank’s internal

processes to assess the adequacy of capital

3.Ensure maintenance of minimum capital with PCA for

shortfall

4.Prescribe differential capital, where necessary

i.e. where the internal processes are slack.

Pillar 3: Market Discipline

1.Enhance disclosures

2.Core disclosures and supplementary disclosures

3.Timely at least semiannual disclosures

Thus the Basel-II accord does not merely prescribe

minimum capital requirement, but envisages processes

of supervisory review and market discipline. The

revised framework is more risk sensitive then the

1988 accord. There are incentives for those banks,

which have better risk management capabilities.

CHAPTER – IV

DATA AND

CALCULATION

RISK WEIGHTED ASSETS;

Risk weighted assets is a measure of the amount of a

bank’s assets, adjusted for risk. The nature of a

bank's business means it is usual for almost all of a

bank's assets will consist of loans to customers.

Comparing the amount of capital a bank has with the

amount of its assets gives a measure of how able the

bank is to absorb losses. If its capital is 10% of its

assets, then it can lose 10% of its assets without

becoming insolvent.

By adjusting the amount of each loan for an estimate of

how risky it is, we can transform this percentage into

a rough measure of the financial stability of a bank.

It is not a particularly accurate measure because of

the difficulties involved in estimating these risks.

These difficulties are exacerbated by the motivation

banks have to distort it.

The main use of risk weighted assets is to calculate

tier 1 and tier 2 capital adequacy ratios.

Risk weighting adjusts the value of a asset for risk,

simply by multiplying it be a factor that reflects its

risk. Low risk assets are multiplied by a low number,

high risk assets by 100% (i.e. 1).

Suppose a bank has the following assets: 1C in gilts,

2c secured by mortgages, and 3 of loans to businesses.

The risk weightings used as 0% for gilts (a risk free

asset), 50% for mortgages, and 100% for the corporate

loans. The bank’s risk weighted assets are (0 × 1C) +

(50% × 2C) + (100% × 3C) = 4c.

Basel I used a comparatively simple system of risk

weighting that is used in the calculation above. Each

class of asset was assigned a fixed risk weight. Basel

II uses a different classification of assets with some

types having weightings that depend on the borrower’s

credit rating or the bank’s own risk models.

Banks have a motive to take on more risk. If they win

their bets, the shareholders (and management) take the

profit, if they lose then the loss us likely to be

shared with debt holders or governments (as banks are

rarely allowed to fail). Part of the motivation for

Basel II was that banks were able to work around the

Basel I system by selecting riskier business within

each asset class. Given this it seems remiss to have

allowed the banks to use their own risk models,

especially given that model risk was quite high even

without the incentives the banks had to manipulate the

models to understate risk.

CALCULATION OF RISK WEIGHTED ASSETS

TANGIBLE COMMON EQUITY RATIO

The tangible common equity ratio (TCE ratio) is a

measure of the financial soundness of banks. It is more

conservative than the usual capital adequacy ratios

(including tier 1) because it excludes preference share

capital and all intangible assets. The TCE ratio is

also usually calculated using actual total assets with

no risk weighting. It is:

Tangible common equity ÷ total tangible assets

In other words it is the shareholders funds belonging

to ordinary shareholders as a proportion of a bank's

tangible assets (most of which are usually loans to

customers).

The TCE ratio became prominent because it became

evident, during the credit crunch, that some banks had

apparently healthy capital adequacy ratios only because

of large amounts of preference share capital and

intangible assets of uncertain value such as deferred

tax. With the banks' own risk models discredited, a

simple and conservative measure was useful to both

regulators and investors.

Table 4.1 TANGIBLE COMMON EQUITY RATIO

Sources: SBI Records. Results computed.

TCE= Tangible Common Equity

TTA= Total Tangible Assets

TCER=Tangible Common Equity Ratio

CAPITAL ADEQUACY

Central bank governors of the ten countries formed a

committee of banking supervisory in 1975.This committee

usually meets at the of international settlement (BIS)

in Basel, Switzerland. Hence it has come to know as the

Basel committee. The Basel committee provided the

framework for capital adequacy in 1988.

The Basel-2 accord is expected to establish a minimum

level of capital for international active bank.

National regulatory are free to set higher standards

for minimum capital.

The new capital accord will require banks to manage

risk by not only allocating regulatory capital but also

by disclosing greater risk information and setting

standards for risk management processes.basel-2

provides incentives for banks to invest and increase

the sophistication of their internal risk management

capabilities in order to gain reducing in capital. This

will help them to increase a bank’s lending which in

turn will give higher returns and value to its

shareholders.

Regulators try to ensure that banks and other financial

institutions have sufficient capital to keep them out

of difficulty. This not only protects depositors, but

also the wider economy, because the failure of a big

bank has extensive knock-on effects.

The risk of knock-on effects that have repercussions at

the level of the entire financial sector is called

systemic risk.

Capital adequacy requirements have existed for a long

time, but the two most important are those specified by

the Basel committee of the Bank for International

Settlements.

Basel 1 defined capital adequacy as a single number

that was the ratio of a bank’s capital to its assets.

There are two types of capital, tier one and tier two.

The first is primarily share capital, the second other

types such as preference shares and subordinated debt.

The key requirement was that tier one capital was at

least 8% of assets.

Each class of asset has a weight of between zero and 1

(or 100%). Very safe assets such as government debt

have a zero weighting, high risk assets (such as

unsecured loans) have a rating of one. Other assets

have weightings somewhere in between. The weighted

value of an asset is its value multiplied by the weight

for that type of asset.

In addition to specifying levels of capital adequacy,

most countries have regulator run guarantee funds that

will pay depositors at least part of what they are

owed. It is also usual for regulators to intervene to

prevent outright bank defaults

MINIMUM CAPITAL REQUIREMENTS

The term capital would include Tier-1 or core capital,

Tire- 2 or supplemental capital, and Tier-3 capital.

The total capital ratio must not be lower than 8%. Core

capital consists of paid up capital, free reserve and

unallocated surplus, less specified deductions.

The minimum of 8% of risk weighted assets must be met

by Tier-1 plus Tier-2 capital, 4% of risk weighted

assets must be core tire-1 capital.

CAPITAL ADEQUACY RATIO

Capital adequacy ratios are a measure of the amount of

a bank's capital expressed as a percentage of its risk

weighted credit exposures.

Minimum capital adequacy ratios have been developed to

ensure banks can absorb a reasonable level of losses

before becoming insolvent.

Applying minimum capital adequacy ratios serves to

protect depositors and promote the stability and

efficiency of the financial system.

The purpose of having minimum capital adequacy ratios

is to ensure that banks can absorb a reasonable level

of losses before becoming insolvent, and before

depositors funds are lost.

Applying minimum capital adequacy ratios serves to

promote the stability and efficiency of the financial

system by reducing the likelihood of banks becoming

insolvent. When a bank becomes insolvent this may lead

to a loss of confidence in the financial system,

causing financial problems for other banks and perhaps

threatening the smooth functioning of financial

markets.

It also gives some protection to depositors. In the

event of a winding-up, depositors' funds rank in

priority before capital, so depositors would only lose

money if the bank makes a loss which exceeds the amount

of capital it has. The higher the capital adequacy

ratio, the higher the level of protection available to

depositors.

Development of Minimum Capital Adequacy Ratios

The "Basle Committee" (centered in the Bank for

International Settlements), which was originally

established in 1974, is a committee that represents

central banks and financial supervisory authorities of

the major industrialized countries (the G10 countries).

The committee concerns itself with ensuring the

effective supervision of banks on a global basis by

setting and promoting international standards. Its

principal interest has been in the area of capital

adequacy ratios. In 1988 the committee issued a

statement of principles dealing with capital adequacy

ratios. This statement is known as the "Basle Capital

Accord". It contains a recommended approach for

calculating capital adequacy ratios and recommended

minimum capital adequacy ratios for international

banks. The Accord was developed in order to improve

capital adequacy ratios (which were considered to be

too low in some banks) and to help standardize

international regulatory practice.

It has been adopted by the OECD countries and many

developing countries. The Reserve Bank applies the

principles of the Basle Capital Accord in India.

Capital

The calculation of capital (for use in capital adequacy

ratios) requires some adjustments to be made to the

amount of capital shown on the balance sheet. Two types

of capital are measured in India - called tier one

capital and tier two capital.

Tier one capital is capital which is permanently and

freely available to absorb losses without the bank

being obliged to cease trading. An example of tier one

capital is the ordinary share capital of the bank. Tier

one capital is important because it safeguards both the

survival of the bank and the stability of the financial

system.

Tier two capital is capital which generally absorbs

losses only in the event of a winding-up of a bank, and

so provides a lower level of protection for depositors

and other creditors. It comes into play in absorbing

losses after tier one capital has been lost by the

bank. Tier two capital is sub-divided into upper and

lower tier two capital. Upper tier two capital has no

fixed maturity, while lower tier two capital has a

limited life span, which makes it less effective in

providing a buffer against losses by the bank. An

example of tier two capital is subordinated debt. This

is debt which ranks in priority behind all creditors

except shareholders. In the event of a winding-up,

subordinated debt holders will only be repaid if all

other creditors (including depositors) have already

been repaid.

The Basle Capital Accord also defines a third type of

capital, referred to as tier three capital. Tier three

capital consists of short term subordinated debt. It

can be used to provide a buffer against losses caused

by market risks if tier one and tier two capital are

insufficient for this. Market risks are risks of losses

on foreign exchange and interest rate contracts caused

by changes in foreign exchange rates and interest

rates. The Reserve Bank does not require capital to be

held against market risk, so does not have any

requirements for the holding of tier three capital.

The composition and calculation of capital are

illustrated by the first step of the capital adequacy

ratio calculation example shown later in this article.

Credit Exposures

Credit exposures arise when a bank lends money to a

customer, or buys a financial asset (e.g. a commercial

bill issued by a company or another bank), or has any

other arrangement with another party that requires that

party to pay money to the bank (e.g. under a foreign

exchange contract). A credit risk is a risk that the

bank will not be able to recover the money it is owed.

The risks inherent in a credit exposure are affected by

the financial strength of the party owing money to the

bank. The greater this is, the more likely it is that

the debt will be paid or that the bank can, if

necessary, enforce repayment.

Credit risk is also affected by market factors that

impact on the value or cash flow of assets that are

used as security for loans. For example, if a bank has

made a loan to a person to buy a house, and taken a

mortgage on the house as security, movements in the

property market have an influence on the likelihood of

the bank recovering all money owed to it. Even for

unsecured loans or contracts, market factors which

affect the debtor's ability to pay the bank can impact

on credit risk.

The calculation of credit exposures recognizes and

adjusts for two factors:

On-balance sheet credit exposures differ in their

degree of riskiness (e.g. Government Stock compared

to personal loans). Capital adequacy ratio

calculations recognise these differences by

requiring more capital to be held against more

risky exposures. This is done by weighting credit

exposures according to their degree of riskiness. A

broad brush approach is taken to defining degrees

of riskiness. The type of debtor and the type of

credit exposures serve as proxies for degree of

riskiness (e.g. Governments are assumed to be more

creditworthy than individuals, and residential

mortgages are assumed to be less risky than loans

to companies). The Reserve Bank defines seven

credit exposure categories into which credit

exposures must be assigned for capital adequacy

ratio calculation purposes.

Off-balance sheet contracts (e.g. guarantees,

foreign exchange and interest rate contracts) also

carry credit risks. As the amount at risk is not

always equal to the nominal principal amount of the

contract, off-balance sheet credit exposures are

first converted to a "credit equivalent amount".

This is done by multiplying the nominal principal

amount by a factor which recognises the amount of

risk inherent in particular types of off-balance

sheet credit exposures. After deriving credit

equivalent amounts for off-balance sheet credit

exposures, these are weighted according to the

riskiness of the counterparty, in the same way as

on-balance sheet credit exposures. Nine credit

exposure categories are defined to cover all types

of off-balance sheet credit exposures.

The credit exposure categories and the risk weighting

process are illustrated by the second step of the

calculation example.

Minimum Capital Adequacy Ratios

The Basle Capital Accord sets minimum capital adequacy

ratios that supervisory authorities are encouraged to

apply. These are:

tier one capital to total risk weighted credit

exposures to be not less than 4 percent;

total capital (i.e. tier one plus tier two less

certain deductions) to total risk weighted credit

exposures to be not less than 8 percent;

There are some further standards applicable to tier two

capital:

tier two capital may not exceed 100 percent of tier

one capital;

lower tier two capital may not exceed 50 percent of

tier one capital;

lower tier two capital is amortised on a straight

line basis over the last five years of its life.

The Reserve Bank will not register banks in India that

do not meet these standards - and maintaining the

minimum standards is always made a condition of

registration.

If the registered bank is incorporated in India,

then the minimum standards apply to the financial

reporting group of the bank.

If the registered bank is a branch of an overseas

bank, then it is the capital adequacy ratios of the

whole overseas bank (and not the branch) which are

relevant. Overseas banks which operate as branches

are registered in India on the condition that they

comply with the capital adequacy ratio requirements

imposed by the financial authorities in their home

country and that these requirements are no less

than those recommended by the Basle Capital Accord.

When a registered bank falls below the minimum

requirements it must present a plan to the Reserve Bank

(which is publicly disclosed) aimed at restoring

capital adequacy ratios to at least the minimum level

required.

Even though a bank may have capital adequacy ratios

above the minimum levels recommended by the Basle

Capital Accord, this is no guarantee that the bank is

"safe". Capital adequacy ratios are concerned primarily

with credit risks. There are also other types of risks

which are not recognized by capital adequacy ratios

e.g.. Inadequate internal control systems could lead to

large losses by fraud, or losses could be made on the

trading of foreign exchange and other types of

financial instruments. Also capital adequacy ratios are

only as good as the information on which they are

based, e.g. if inadequate provisions have been made

against problem loans, then the capital adequacy ratios

will overstate the amount of losses that the bank is

able to absorb. Capital adequacy ratios should not be

interpreted as the only indicators necessary to judge a

bank's financial soundness.

Requirement of Capital adequacy ratio (CAR):

Capital adequacy norm – 8.00%

Scheduled commercial banks CAR- 9.00%

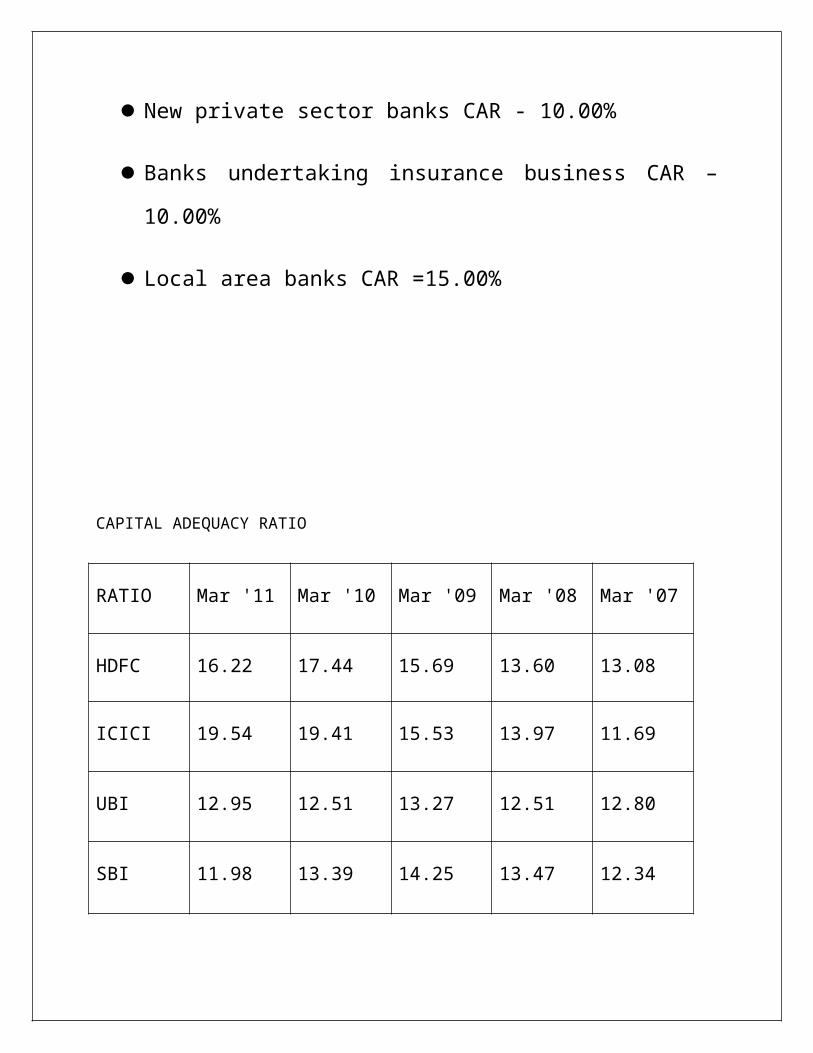

New private sector banks CAR - 10.00%

Banks undertaking insurance business CAR –

10.00%

Local area banks CAR =15.00%

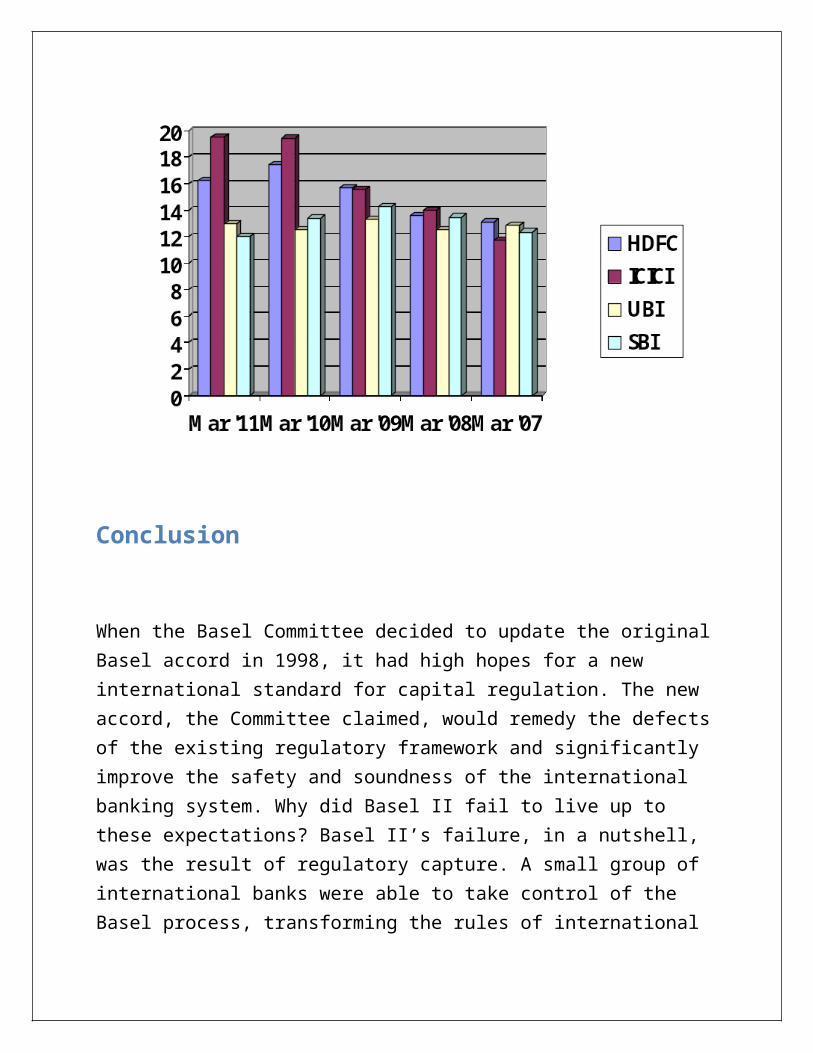

CAPITAL ADEQUACY RATIO

RATIO Mar '11 Mar '10 Mar '09 Mar '08 Mar '07

HDFC 16.22 17.44 15.69 13.60 13.08

ICICI 19.54 19.41 15.53 13.97 11.69

UBI 12.95 12.51 13.27 12.51 12.80

SBI 11.98 13.39 14.25 13.47 12.34

Conclusion

When the Basel Committee decided to update the originalBasel accord in 1998, it had high hopes for a new international standard for capital regulation. The new accord, the Committee claimed, would remedy the defectsof the existing regulatory framework and significantly improve the safety and soundness of the international banking system. Why did Basel II fail to live up to these expectations? Basel II’s failure, in a nutshell, was the result of regulatory capture. A small group of international banks were able to take control of the Basel process, transforming the rules of international

capital regulation to maximize their profits at the expense of those without a seat at the decision-making table. According to the neo-proceduralist analysis I have presented, capture had its origins in the interaction of demand- and supply-side factors in the negotiation stages ofthe regulatory process. Large asymmetries in information on the demand-side, exacerbated by a closedand club-like regulatory forum on the supply-side, gavelarge international banks crucial first-mover advantagein negotiations, allowing them to shape decisions in a way that was difficult to reverse at later stages. Latecomers had little choice but to accept what was in effect a fait accompli.Unfortunately, as we have seen, these very same factorsmay have also jeopardized more recent efforts to raise international capital requirements in the form of ‘Basel III’. Given the importance of reform in this area for the health of the global economy, it is crucial therefore that we heed the lessons of the neo-proceduralist analysis. Future efforts to revise capital adequacy standards must both observe basic standards of due process and ensure that information asymmetries are as small as possible – principally, butnot exclusively, by maintaining some kind of distance between supervisory bodies and the banking industry. Though difficult in practice to achieve, if implementedfaithfully, these changes would go a long way towards ensuring that the next time regulators set out to

revise international capital standards, they achieve every one of their aims.

Reference:Bailey, R (2005), “Basel II and Development Countries: Understanding theImplications”, London School of Economics Working Paper No. 05-71.Basel Committee on Banking Supervision (1988), “International Convergence of CapitalMeasurement and Capital Standards”, available at www.bis.orgBasel Committee on Banking Supervision (1996), “Amendment to the Capital Accord toincorporate market risks” available at www.bis.orgBasel Committee on Banking Supervision (2006), “International Convergence of CapitalMeasurement and Capital Standards: A Revised Framework”, available atwww.bis.orgFerri, G., L. Liu and J.E. Stiglitz (1999), “The Procyclical Role of Rating Agencies:Evidence from the East Asian Countries” Economic Notes, 28 (3), pp. 335-355.Ferri, G., L. Liu and G. Majnoni (2000), “How the Proposed Basel Guidelines on Rating-Agency Assessments Would Affect Developing Countries”, Policy ResearchWorking Paper 2369, The World Bank.

Financial Stability Institute (2006), “Implementation of the new capital adequacyframework in non-Basel Committee member countries: Summary of responses tothe 2006 follow-up Questionnaire on Basel II implementation”, Occasional Paper6, available at www.bis.orgGhosh, S. and D.M. Nachane (2003), “Are Basel Capital Standards Pro-cyclical? SomeEmpirical Evidence from India”, Economic and Political Weekly, 38(8), pp. 777-783Gill, S. (2005), “An Analysis of Defaults of Long-term Rated Debts”, Vikalpa 30 (1), pp.35-50Griffith-Jones, S., M. Sefoviano and S. Spratt (2002), “Basel II and DevelopingCountries: Diversification and Portfolio Effects”, Working Paper of Institute ofDevelopment Studies, University of Sussex available athttp://www.ids.ac.uk/ids/global/pdfs/FINALBasel-diversification2.pdfGupta, L.C., C P. Gupta and N. Jain (2001), Indian Households’ Investment Preferences:The Third All-India Survey, Society for Capital Market Research andDevelopment, New DelhiHill, C. (2004), “Regulating the Rating Agencies”, Washington University Law Quarterly,82(43), pp. 43-95Joshi, V. and I.M.D. Little (1996), India's Economic Reforms 1991-2001, Delhi, OxfordUniversity Press.18

Kaminsky, G.L. and C.M. Reinhart (1999), “The Twin Crises: The Causes of Bankingand Balance-Of-Payments Problems”, the American Economic Review, 89 (3), pp.473-500McKinnon, R.I. (1973), Money and Capital in Economic Development, Washington D.C,Brookings Institutions.Leeladhar, V. (2006), “Demystifying Basel II”, Reserve bank of India Bulletin October2006, pp. 1153-1157Monfort, B. and C. Mulder (2000), “The Impact of Using Sovereign Ratings by CreditRating Agencies on the Capital Requirements for Banks: A Study of EmergingMarket Economies”, IMF Working Paper WP/00/69, MarchNachane, D.M., S. Ghosh and P. Ray (2006), “Basel II and Bank Lending Behaviour:Some Likely Implications for Monetary Policy”, Economic and Political Weekly,41(11), pp. 1053-1058Nitsure, R.R. (2005), “Basel II Norms: Emerging Market Perspective with Indian Focus”,Economic and Political Weekly, 40(12), pp. 1162-1166Nikaido, Y. (2004), “Technical Efficiency of Small-Scale Industry-Application ofStochastic Production Frontier Model”, Economic and PoliticalWeekly, 39(6), pp.592-597Raghunathan, V. and J.R. Varma (1992), “CRISIL Rating: When Does AAA Mean B?”,Vikalpa 17 (2), pp. 35 -42Raghunathan, V. and J.R. Varma (1993), “When AAA Means B: The State of Credit

Rating in India”, IIM Ahmedabad Working Paper.Reddy, Y.V. (2006), “Challenges and Implications of Basel II for Asia”, BIS Review37/2006 available at www.bis.orgReserve Bank of India (2005a), “Draft Guidelines for Implementation of the New CapitalAdequacy Framework”, RBI Circular DBOD No. BP. 1163/21.04.118/2004-05Reserve Bank of India (2005b), “Reserve Bank of India Annual Report 2004-05”,available at www.rbi.org.inReserve Bank of India (2006), “Reserve Bank of India Annual Report 2005 -06”,available at www.rbi.org.inReserve Bank of India (2007a), “Revised Draft Guidelines for Implementation of theNew Capital Adequacy Framework”, RBI Circular DBOD No. BP.

Related Documents