©2015, College for Financial Planning, all rights reserved. Session 7 NUA Fundamentals and Keogh Contributions CERTIFIED FINANCIAL PLANNER CERTIFICATION PROFESSIONAL EDUCATION PROGRAM Retirement Planning & Employee Benefits

©2015, College for Financial Planning, all rights reserved. Session 7 NUA Fundamentals and Keogh Contributions CERTIFIED FINANCIAL PLANNER CERTIFICATION.

Dec 16, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

©2015, College for Financial Planning, all rights reserved.

Session 7NUA Fundamentals and Keogh Contributions

CERTIFIED FINANCIAL PLANNER CERTIFICATION PROFESSIONAL EDUCATION PROGRAMRetirement Planning & Employee Benefits

Session Details

Module(s) 3

Chapter(s)

5, 9

LOs 3-5 Describe the basic characteristics of stock bonus plans. *This session will cover the essentials of Net Unrealized Appreciation.

3-9 Describe the basic characteristics of a Keogh plan, and calculate the owner’s contribution amount.

7-2

Net Unrealized Appreciation (NUA)

• NUA treatment is available for any employer stock distributed from a qualified plan

• Stock bonus, ESOPs, 401(k) profit sharing, are all qualified plans, so the NUA rules would apply

• An advantage of NUA is that it is taxed as a long-term capital gain, not as ordinary income

7-3

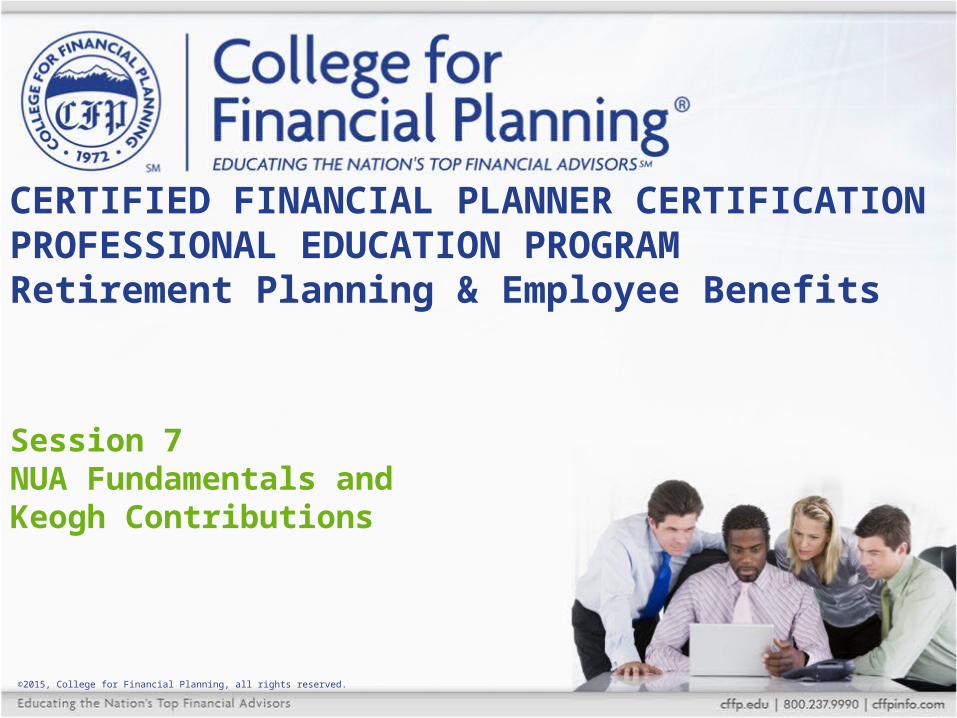

NUA Example

Josephine, age 53, takes a distribution on March 1, 2015, of 3,000 shares of company stock. Her cost basis is $65,000 (the amount of employer contributions) and the stock is worth $255,000 when distributed. She sells all 3,000 shares on July 15, 2015, for $270,000.

Ramifications are:o $65,000 taxed as ordinary income,

and subject to 10% penalty taxo $190,000 NUA taxed as a long-term

capital gaino $15,000 additional gain taxed as

a short-term capital gain (if held for more than one year from distribution date, then any additional gain would be long-term)

7-4

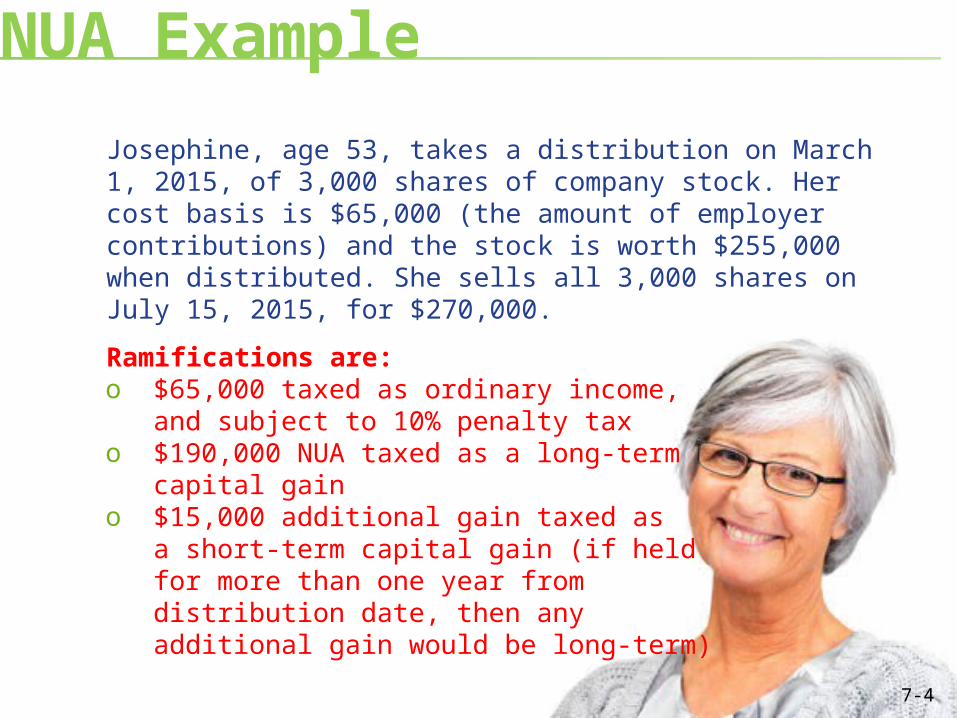

NUA Example

401(k) account balance $300,000

Company stock ($10,000 basis) taken as a taxable distribution in kind1

$100,000

Other assets rolled over to Traditional IRA $200,000

Taxed as ordinary income when received $10,000

Taxed as long-term capital gains when stock is sold

$90,000

Taxed as ordinary income when withdrawn from IRA2

$200,000

1 Does not consider the possibility of early distribution penalties.2 Assumes no increase in value.

7-5

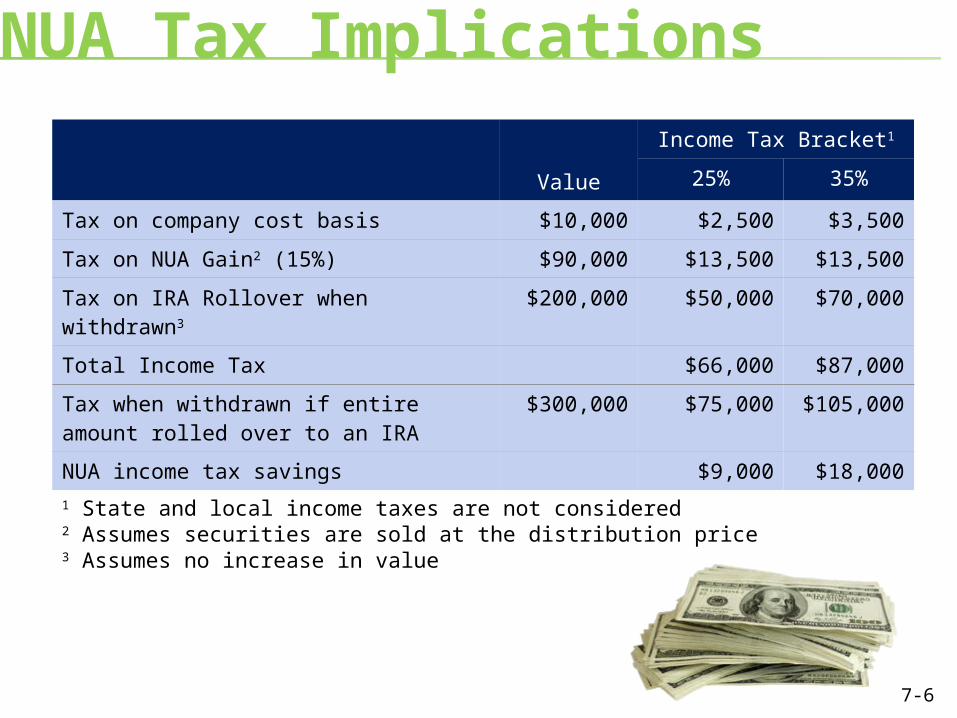

NUA Tax Implications

Value

Income Tax Bracket1

25% 35%

Tax on company cost basis $10,000 $2,500 $3,500

Tax on NUA Gain2 (15%) $90,000 $13,500 $13,500

Tax on IRA Rollover when withdrawn3 $200,000 $50,000 $70,000

Total Income Tax $66,000 $87,000

Tax when withdrawn if entire amount rolled over to an IRA

$300,000 $75,000 $105,000

NUA income tax savings $9,000 $18,0001 State and local income taxes are not considered2 Assumes securities are sold at the distribution price3 Assumes no increase in value

7-6

Keogh Plans—Basic Provisions• Available only to unincorporated

businesses—sole proprietor or partnership• Takes the form of a qualified plan (defined

contribution or defined benefit)• Certain provisions for owner/employee

are unique to Keoghs:o Owner/employee’s contribution is

calculated on net earningso Lump-sum distribution treatment is not

available to owner/employee for separation from service before age 59½—available only for death, disability, or attainment of age 59½

7-7

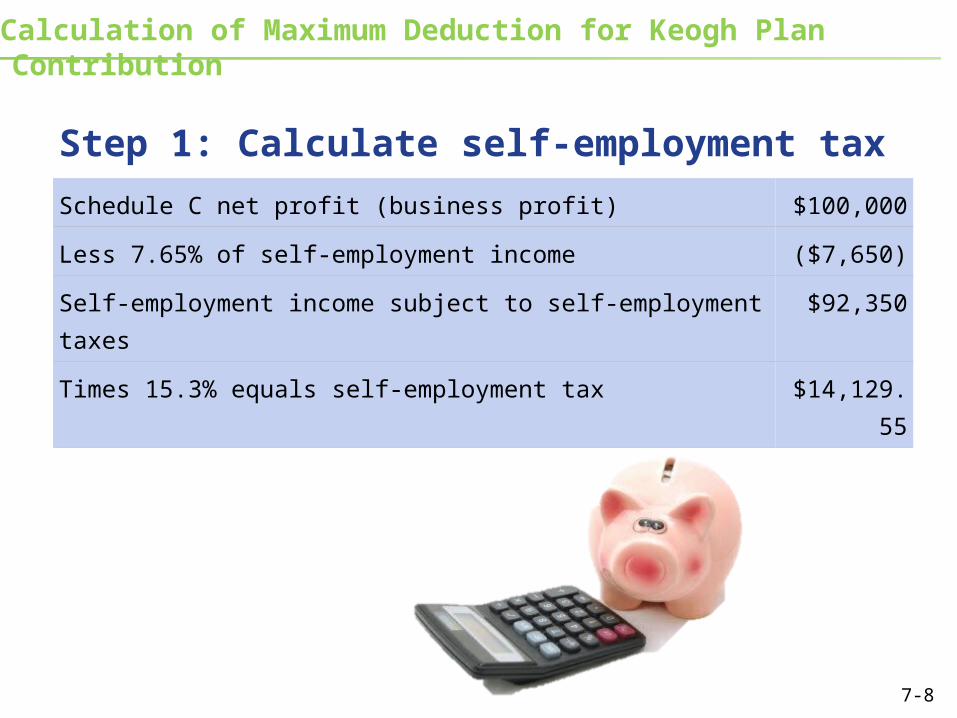

Calculation of Maximum Deduction for Keogh Plan Contribution

Step 1: Calculate self-employment tax

Schedule C net profit (business profit) $100,000

Less 7.65% of self-employment income ($7,650)

Self-employment income subject to self-employment taxes $92,350

Times 15.3% equals self-employment tax $14,129.55

7-8

Calculation of Maximum Deduction for Keogh Plan Contribution

Step 2: Determine adjusted contribution percentage for ownerPercentage contribution for employee participants (employee percentage)

.25

Divide by 1 plus employee percentage 1.25

Equals adjusted contribution percentage for owner

.20

7-9

Calculation of Maximum Deduction for Keogh Plan Contribution

Step 3: Multiply net earnings by adjusted contribution percentageSchedule C net profit $100,000

Less income tax deduction (1/2 self-employment tax)

$7,064.78

Net earnings $92,935.23

Times contribution percentage for owner .20

Owner’s contribution for his own benefit $18,587.05

7-10

Practice Problem

Jane Momeyer is a financial planner who grossed $200,000 this year. Her expenses including the plan contribution for her staff were $130,000. Her profit sharing contribution for her staff was 10% of compensation. How much can she contribute to the profit sharing plan for her own account?

7-11

©2015, College for Financial Planning, all rights reserved.

Session 7End of Slides

CERTIFIED FINANCIAL PLANNER CERTIFICATION PROFESSIONAL EDUCATION PROGRAMRetirement Planning & Employee Benefits

Related Documents