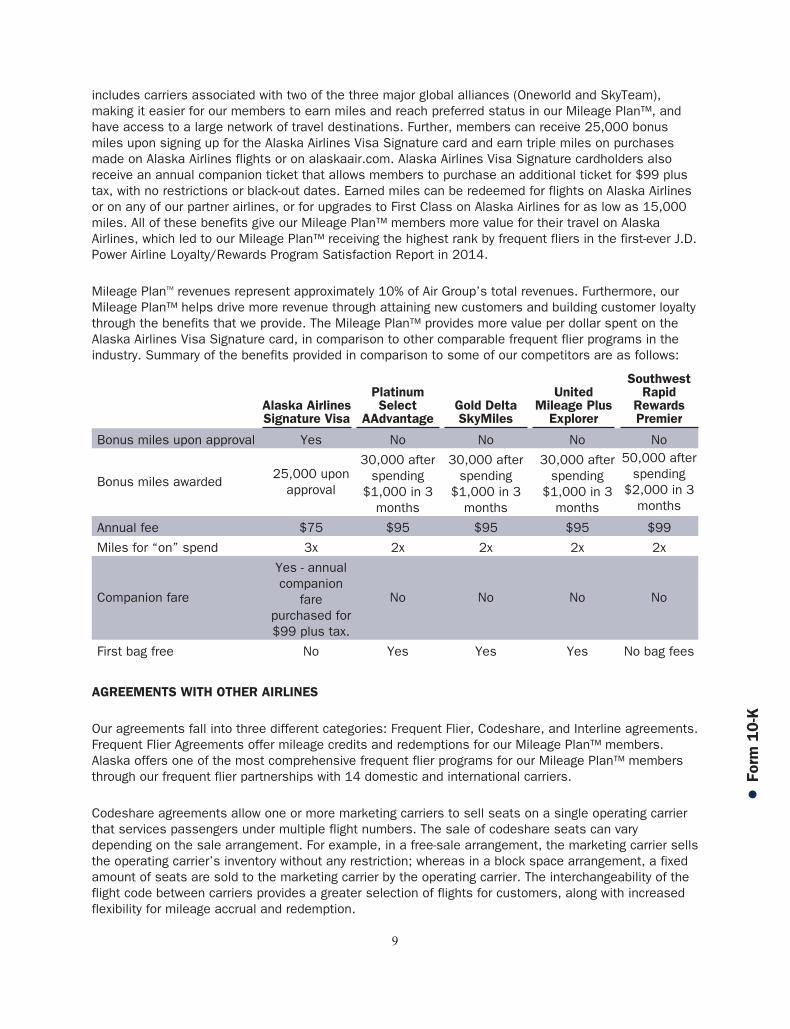

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

TO OUR SHAREHOLDERS

2014 was a record year for Alaska Air Group on many levels. We succeeded

financially, our operation was strong, and our people delivered the great customer

service for which we are known. But, before I provide you greater detail on our 2014

accomplishments, I want to share my thoughts on the backdrop for the year.

In last year’s letter, I noted unprecedented

competition in Seattle, our largest hub,

and I described the steps we were taking

to defend our position as the carrier of

choice in the Pacific Northwest. I’m happy

to report that in 2014, despite intense

competition in our hometown, we

produced the best results in our history.

For this, we have our 13,000 employees at Alaska and Horizon to thank. We’ve got a

fabulous group of people here — folks that look at the outside world realistically and

then get to work putting together plans that will succeed. And then they relentlessly

focus on executing those plans. Earlier this year I heard Satya Nadella, the new CEO

of Microsoft, speak at an event where he mentioned a Peter Drucker quote that

resonated with me — “Culture eats strategy for breakfast.” We have a fantastic

culture here at Alaska. Our people care about each other and this company, and they

work together to execute our plan — every flight, every day, with every customer, and

on every project. This fabulous team and this culture are the drivers of the results

we’re sharing in this report.

Here are some of the highlights from this year:

Safety is our top priority and the foundation for everything we do. This year, we

launched a program called “Ready, Safe, Go,” designed to increase safety

awareness across the Air Group system. We have a strong safety record at

both Alaska and Horizon, and this will help us be even better.

#1 on-time airline: Our frontline folks and the leaders throughout our operation

continue to run an excellent operation. 86.0% of our mainline flights arrived on

time — the highest percentage of on-time flights among the eight largest North

American carriers. Reliability is one of the biggest sources of customer

satisfaction, which in turn, drives customer preference. Our 13,000 employees

worked hard every day to get our customers to their destinations safely, on

time, and with their bags.

J.D. Power award for customer service and loyalty program: Simply put, great

customer service is the reason Alaska is here today and thriving as an

independent airline. Our employees were recognized in 2014, earning the J.D.

Power award for “Highest in Customer Satisfaction Among Traditional Network

Carriers” for the seventh year in a row. J.D. Power also published its first-ever

Airline Loyalty Program Satisfaction Report in 2014, in which Alaska was

ranked highest by frequent fliers. We know that taking care of our customers

every day is the best way to sustain our success. We could not be more proud

of our people for these extraordinary accomplishments.

Engaged employees and good labor relations: We are pleased to have a new

five-year agreement with Alaska’s flight attendants. Our inflight group is the best

in the business, and they proved it once again by providing outstanding service

throughout the contract negotiations. We now

have agreements in place with all of our labor

groups. The length of our labor contracts is

about four years on average, which compares

very favorably to the rest of the industry. Our

level of employee engagement was 82% in

our annual employee survey, up 3 points from

the prior year, and up 19 points from three

years ago. Engaged employees who are

aligned with our goals are the reason we are

succeeding.

Low costs, low fares, and network growth: Are low costs important? You bet

they are; they enable us to provide our customers with outstanding value and

enlarge the economic moat that we are building around our business. Last

year, we reduced our unit costs, excluding fuel, for the 12th year out of the last

13. Alaska’s costs — and our fares — are now much closer to low-cost

carriers’ than to legacy airlines’. And low fares mean that we can grow. In 2014

we added 16 new routes. We now serve the top 25 destinations from Seattle

for business travelers, and our network now encompasses 105 cities with 216

non-stop city pairs. Low costs are a result of our continued (some say

obsessive) focus on productivity and cost management.

Investment-grade credit rating: Alaska is one of only two U.S. airlines to have

an investment-grade credit rating. Our balance sheet is not only one of the

strongest in the business, but it also compares very favorably with high-quality

industrial firms. Our long-term debt on the balance sheet back in 2008 was

$1.6 billion and today it is $686 million. In fact, today we have more cash than

debt on our balance sheet, and this reflects our conscious effort to put capital

to work in a balanced manner and de-risk cash flows for you, our shareholders.

Shareholder returns: Strong fundamental performance in the areas I outlined

above allowed us to post a record $571 million in profit and increase our

earnings per share by 55%. And robust earnings enabled us to return cash to

you. Based on our strong 2014 results, we increased our dividend by 60% in

January. Together with our share repurchases, we distributed $417 million in

cash to shareholders during 2014.

These are compelling results on multiple fronts, and some people who observe our

performance ask us how we do it. The short answer is the same reason Seattle

Seahawks third-year quarterback Russell Wilson got to the Big Game — twice. At the

heart of this achievement is an incredible commitment to performance, to each other

and to the team. We have the best employees in the business — people who are

talented and dedicated and who enjoy working together to help Alaska and Horizon

compete and win. Their caring and dedication comes from their fundamental values of

integrity — doing the right thing — and from something we call Alaska Spirit and

Horizon Heart. As I’ve watched the Company over the last several years, I’ve seen that

our incredible frontline folks are matched by a highly talented group of leaders. I am

regularly amazed by their heart and their ability to make positive changes.

And whether it’s on a football field or

off, our other CFO (our chief football

officer) reminds us that champions

never rest. We are undertaking several

key initiatives to keep our airline strong.

These initiatives include rolling out

Alaska Beyond (our new inflight

experience), developing new technology

to make travel more hassle-free, improving customer service, and continuing to run a

safe, reliable and on-time operation.

We’re excited about the future, and our entire team is completely focused on

achieving our plan so that we can continue to deliver strong results in the years to

come.

Thank you for supporting and investing in Alaska Air Group.

Sincerely,

Brad Tilden

Chairman and Chief Executive Officer

2015PROXY STATEMENT

ŠP

roxy

NOTICE OF ANNUAL MEETING OF STOCKHOLDERSP.O. Box 68947

Seattle, Washington 98168

To our Stockholders:

The Annual Meeting of Stockholders of Alaska Air Group, Inc. (the Annual Meeting) will be held in theWilliam M. Allen Theater at the Museum of Flight, 9404 East Marginal Way South, Seattle, Washingtonat 3 p.m. on Thursday, May 7, 2015, for the following purposes:

1. to elect to the Board of Directors the 11 nominees named in this Proxy Statement, each for aone-year term;

2. to ratify the appointment of KPMG LLP as the Company’s independent registered publicaccountants (the independent accountants) for fiscal year 2015;

3. to seek an advisory vote to approve the compensation of the Company’s Named ExecutiveOfficers;

4. to consider a stockholder proposal regarding an independent board chairman policy; and

5. to transact such other business as may properly come before the meeting or anypostponement or adjournment thereof.

The Board of Directors set March 18, 2015 as the record date for the Annual Meeting. This means thatowners of Alaska Air Group common stock as of the close of business on that date are entitled toreceive this notice, attend the meeting in person with proper proof of ownership or by proxy (see Can Iattend the Annual Meeting, and what do I need for admission? in the following Questions and AnswersAbout the Annual Meeting section of this Proxy Statement); and vote at the meeting and anyadjournments or postponements.

Whether or not you attend the meeting in person, we encourage you to vote by Internet or phone or tocomplete, sign and return your proxy prior to the meeting.

Because the majority of our stockholders will not be able to attend in person, we invite you to submitany questions you may have that would be of general stockholder interest to the Corporate Secretary viaemail at [email protected]. We will include as many of your questions as possible duringthe Q&A session of the meeting and will send you a copy of the response. Every stockholder vote isimportant. To ensure your vote is counted at the Annual Meeting, please vote as promptly as possible.

By Order of the Board of Directors,

Shannon K. AlbertsCorporate Secretary

March 27, 2015

IMPORTANT NOTICE REGARDING THE INTERNET AVAILABILITY OF PROXYMATERIALS FOR THE STOCKHOLDERS MEETING TO BE HELD ON MAY 7, 2015.

Stockholders may access, view and download the 2015 Proxy Statement and 2014 Annual Report atwww.edocumentview.com/alk.

ŠP

roxy

ALASKA AIR GROUP, INC.NOTICE OF ANNUAL MEETING OF STOCKHOLDERS AND PROXY STATEMENT

TABLE OF CONTENTS

GENERAL INFORMATIONAnnual Meeting Information 1Questions and Answers about the Annual Meeting 1

PROPOSALS TO BE VOTED ONProposal 1: Election of Directors to One-Year Terms 9Proposal 2: Ratification of the Appointment of the Company’s Independent Accountants for

Fiscal Year 2015 13Proposal 3: Advisory Vote Regarding the Compensation of the Company’s Named Executive

Officers 13Proposal 4: Stockholder Proposal Regarding an Independent Chairman 15

CORPORATE GOVERNANCEStructure of the Board of Directors 20Director Independence 24Director Nomination Policy 25Board Leadership 28Executive Sessions and Lead Director 29Risk Oversight 29Code of Conduct and Ethics 30Certain Relationships and Related Transactions 30Stockholder Communication Policy 31

AUDIT COMMITTEE MATTERSIndependent Registered Public Accountants 32Audit Committee Report 33

DIRECTOR COMPENSATION2014 Director Compensation 35Director Stock Ownership Policy 36

EXECUTIVE COMPENSATIONCompensation Discussion and Analysis 37Compensation and Leadership Development Committee Report 52Compensation and Leadership Development Committee Interlocks and Insider Participation 522014 Summary Compensation Table 532014 Grants of Plan-Based Awards 562014 Outstanding Equity at Fiscal Year End 582014 Options Exercised and Stock Vested 61Pension and Other Retirement Plans 622014 Nonqualified Deferred Compensation 64Potential Payments Upon Change in Control and Termination 64

SECURITIES OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENTSecurity Ownership of Management 68Beneficial Owners of 5% or More 69Section 16(a) Beneficial Ownership Reporting Compliance 69

Annual Meeting Information

The Board of Directors of Alaska Air Group, Inc.(Air Group or the Company) is soliciting proxiesfor the 2015 Annual Meeting of Stockholders.This Proxy Statement contains importantinformation for you to consider when decidinghow to vote on the matters brought before themeeting. Please read it carefully.

The Board set March 18, 2015 as the recorddate for the meeting. Stockholders who ownedAir Group common stock on that date areentitled to vote at the meeting, with each shareentitled to one vote. There were 130,869,463shares of Air Group common stock outstandingon the record date.

Internet Availability of Annual MeetingMaterials

On or about March 27, 2015, stockholders ofrecord, beneficial owners and employeeparticipants in the Company’s 401(k) plans weremailed a Notice of Internet Availability of ProxyMaterials (the Notice) directing them to awebsite where they can access the Company’s2015 Proxy Statement and 2014 Annual Report(the Annual Meeting Materials). The Company’s

Form 10-K for the year ended December 31,2014 is included in the 2014 Annual Report. Itwas filed with the Securities and ExchangeCommission (SEC) on February 11, 2015.

If you would prefer to receive a paper copy of theproxy materials, please follow the instructionsprinted on the Notice and the material will bemailed to you.

All stockholders may access, view and downloadthe Annual Meeting Materials atwww.edocumentview.com/alk. Other informationon the website does not constitute part of thisProxy Statement.

Admission to the Annual Meeting

If you would like to attend the meeting in person,you must present proof of stock ownership as ofthe record date along with valid, government-issued photo identification. For further details,see Can I attend the Annual Meeting, and whatdo I need for admission? in the followingQuestions and Answers About the AnnualMeeting section of this Proxy Statement.

Questions and Answers about the Annual Meeting

Why am I receiving the Annual MeetingMaterial?

You are receiving the Annual Meeting Materialfrom us because you owned Air Group commonstock as of the record date for the AnnualMeeting. This Proxy Statement describes issueson which you may vote and provides you withother important information so that you canmake informed decisions.

You may own shares of Air Group common stockin several different ways. If your stock isrepresented by one or more stock certificatesregistered in your name or if you have a DirectRegistration Service (DRS) advice evidencingshares held in book entry form, then you have astockholder account with the Company’s transferagent, Computershare Trust Company, N.A.

(Computershare), and you are a stockholder ofrecord. If you hold your shares in a brokerage,trust, or similar account, then you are thebeneficial owner but not the stockholder ofrecord of those shares. Employees of theCompany’s subsidiaries who hold shares ofstock in one or more of the Company’s 401(k)retirement plans are beneficial owners.

What am I voting on?

You are being asked to vote on the election ofthe 11 director nominees named in this ProxyStatement, to ratify the appointment of KPMGLLP as the Company’s independent accountants,to provide an advisory vote in regard to thecompensation of the Company’s NamedExecutive Officers, and to vote on a stockholderproposal regarding an independent chairman

ŠP

roxy

GENERAL INFORMATION 1

policy. When you sign and mail the proxy card orsubmit your proxy by phone or the Internet, youappoint each of Bradley D. Tilden and ShannonK. Alberts, or their respective substitutes ornominees, as your representatives at themeeting. (When we refer to the “named proxies,”we are referring to Mr. Tilden and Ms. Alberts.)This way, your shares will be voted even if youcannot attend the meeting.

How does the Board of Directors recommend Ivote on each of the proposals?

• FOR the election of each of the Board’s 11director nominees named in this ProxyStatement;

• FOR the ratification of the appointment ofKPMG LLP as the Company’s independentaccountants for fiscal year 2015;

• FOR the ratification of the compensation ofthe Company’s Named Executive Officers;

• AGAINST the stockholder proposal regardingan independent chairman policy.

How do I vote my shares?

Stockholders of record can vote by using theproxy card or by phone or the Internet.

Beneficial owners whose stock is held:

• in a brokerage account can vote by using thevoting instruction form provided by the brokeror by phone or the Internet;

• by a bank, and who have the power to vote orto direct the voting of the shares, can voteusing the proxy or the voting information formprovided by the bank or, if made available bythe bank, by phone or the Internet;

• in trust under an arrangement that providesthe beneficial owner with the power to vote orto direct the voting of the shares can vote inaccordance with the provisions of sucharrangement; and/or

• in trust in one of the Company’s 401(k)retirement plans can vote by telephone or

internet, or by mailing the voting instructionform provided by the trustee.

Beneficial owners other than those whobeneficially own stock held in trust in one of theCompany’s 401(k) retirement plans can vote atthe meeting provided that he or she obtains a“legal proxy” from the person or entity holdingthe stock for him or her (typically a broker, bank,or trustee). A beneficial owner can obtain a legalproxy by making a request to the broker, bank, ortrustee. Under a legal proxy, the bank, broker, ortrustee confers all of its rights as a record holderto grant proxies or to vote at the meeting.

Listed below are the various means you can useto vote your shares without attending the AnnualMeeting.

You can vote on the Internet.

Stockholders of record and beneficial owners ofthe Company’s common stock can vote via theInternet regardless of whether they receive theirannual meeting materials through the mail or viathe Internet. Instructions for voting are providedalong with your notice, proxy card or votinginstruction form. If you vote on the Internet,please do not mail your proxy card if you receivedone (unless you intend for it to revoke your priorInternet vote). Your Internet vote will authorizethe named proxies to vote your shares in thesame manner as if you marked, signed andreturned your proxy card.

You can vote by phone.

Stockholders of record and beneficial owners ofthe Company’s common stock can vote byphone. Instructions are provided along with yourproxy card or voting instruction form. If you voteby phone, do not mail your proxy card if youreceived one (unless you intend for it to revokeyour prior vote submitted by phone). Your vote byphone will authorize the named proxies to voteyour shares in the same manner as if youmarked, signed and returned your proxy card.

2 GENERAL INFORMATION

You can vote by mail.

If you received this Proxy Statement by mail,simply sign and date the enclosed proxy card orvoting instruction form and mail it in theenclosed prepaid and addressed envelope. If youmark your choices on the card or votinginstruction form, your shares will be voted as youinstruct.

You can vote by telephone or by the Internet.

Internet and telephone voting facilities forstockholders of record and beneficial owners willbe available 24 hours a day and will close at11:59 p.m. Eastern Time on Wednesday, May 6,2015. To allow sufficient time for voting by thetrustee, voting instructions for the Company’s401(k) plan shares must be received no laterthan 11:59 p.m. Eastern Time on Monday,May 4, 2015.

Voting by the Internet or phone is fast andconvenient and your vote is immediatelyconfirmed and tabulated. By using the Internet orphone to vote, you help Alaska Air Groupconserve natural resources and reduce postageand proxy tabulation costs.

How will my shares be voted if I return a blankproxy or voting instruction form?

If you sign and return a proxy card without givingspecific voting instructions, your shares will bevoted in accordance with the recommendationsof the Board of Directors shown above and asthe named proxies may determine in theirdiscretion with respect to any other mattersproperly presented for a vote during the meetingor any postponement or adjournment of themeeting.

If my shares are held in a brokerage account,how will my shares be voted if I do not returnvoting instructions to my broker?

If you hold your shares in street name through abrokerage account and you do not submit votinginstructions to your broker, your broker maygenerally vote your shares in its discretion on

matters designated as routine under the rules ofthe New York Stock Exchange (NYSE). However, abroker cannot vote shares held in street name onmatters designated as non-routine by the NYSE,unless the broker receives voting instructionsfrom the street name (beneficial) owner.

The proposal to ratify the appointment of theCompany’s independent accountants for fiscalyear 2015 is considered routine under NYSErules. Each of the other items to be submittedfor a vote is considered non-routine underapplicable NYSE rules. Accordingly, if you holdyour shares in street name through a brokerageaccount and you do not submit votinginstructions to your broker, your broker mayexercise its discretion to vote your shares on theproposal to ratify the appointment of theCompany’s independent accountants but will notbe permitted to vote your shares on any of theother items. If your broker exercises thisdiscretion, your shares will be counted aspresent for the purpose of determining a quorumat the Annual Meeting and will be voted on theproposal to ratify the Company’s independentaccountants in the manner instructed by yourbroker, but your shares will constitute “brokernon-votes” on each of the other items at theAnnual Meeting.

For a description of the effect of broker non-votes on the proposals, see How many votesmust the nominees have to be elected? and Notincluding the election of directors, how manyvotes must the proposals receive in order topass?.

What other business may be properly broughtbefore the meeting, and what discretionaryauthority is granted?

Under the Company’s Bylaws, as amendedApril 30, 2010, a stockholder may bringbusiness before the meeting or for publication inthe Company’s 2015 Proxy Statement only if thestockholder gave written notice to the Companyon or before November 28, 2014 and compliedwith the other requirements included in Article IIof the Company’s Bylaws.

ŠP

roxy

GENERAL INFORMATION 3

The Company has not received valid notice thatany business other than that described orreferenced in this Proxy Statement will bebrought before the meeting.

As to any other matters that may properly comebefore the meeting and are not on the proxycard, the proxy grants to Mr. Tilden andMs. Alberts the authority to vote in theirdiscretion the shares for which they hold proxies.

What does it mean if I receive more than oneproxy card, voting instruction form or emailnotification from the Company?

It means that you hold Alaska Air Group stock inmore than one account. Please complete andsubmit all proxies to ensure that all your sharesare voted or vote by Internet or phone using eachof the identification numbers.

What if I change my mind after I submit myproxy?

Stockholders, except for persons whobeneficially own shares held in trust in one of theCompany’s 401(k) retirement plans, may revokea proxy and change a vote by delivering a later-dated proxy or by voting at the meeting. Thelater-dated proxy may be delivered by phone,Internet or mail and need not be delivered by thesame means used in delivering the prior proxysubmission.

Except for persons beneficially owning shares inone of the Company’s 401(k) retirement plans,stockholders may do this at a later date or timeby:

• voting by phone or the Internet before 11:59p.m. Eastern Time on Wednesday, May 6,2015 (your latest phone or Internet proxy willbe counted);

• signing and delivering a proxy card with alater date; or

• voting at the meeting. (If you hold your sharesbeneficially through a broker, you must bring

a legal proxy from the broker in order to voteat the meeting. Please also note thatattendance at the meeting, in and of itself,without voting in person at the meeting, willnot cause your previously granted proxy to berevoked.)

Persons beneficially owning shares in one of theCompany’s 401(k) retirement plans cannot votein person at the meeting and must vote inaccordance with instructions from the trustees.Subject to these qualifications, such holdershave the same rights as other record andbeneficial owners to change their votes by phoneor the Internet, however, in all cases your votemust be submitted by 11:59 p.m. Eastern Timeon Monday, May 4, 2015.

Stockholders of record can obtain a new proxycard by contacting the Company’s CorporateSecretary, Alaska Air Group, Inc., P.O. Box68947, Seattle, WA 98168, telephone(206) 392-5719.

Stockholders with shares held by a broker,trustee or bank can obtain a new votinginstruction form by contacting your broker,trustee or bank.

Stockholders whose shares are held in one ofthe Company’s 401(k) retirement plans canobtain a new voting instruction form bycontacting the trustee of such plan. You canobtain information about how to contact thetrustee from the Company’s Corporate Secretary.Please refer to the section below titled How areshares voted that are held in a Company 401(k)plan? for more information.

If you sign and date the proxy card or votinginstruction form and submit it in accordance withthe accompanying instructions and in a timelymanner, any earlier proxy card or votinginstruction form will be revoked and your newchoices will be voted.

4 GENERAL INFORMATION

How are shares voted that are held in theCompany’s 401(k) plan?

On the record date, 3,822,103 shares were heldin trust for Alaska Air Group 401(k) planparticipants. The trustees, Vanguard FiduciaryTrust Company (Vanguard) and FidelityManagement Trust Company (Fidelity), providedNotice of Proxy and Access instructions to eachparticipant who held shares through theCompany’s 401(k) plans on the record date. Thetrustees will vote only those shares for whichinstructions are received from participants. If aparticipant does not indicate a preference as toa matter, including the election of directors, thenthe trustees will not vote the participant’s shareson such matters.

To allow sufficient time for voting by the trustee,please provide voting instructions no later than11:59 p.m. Eastern Time on Monday, May 4,2015. Because the shares must be voted by thetrustee, those who hold shares through the401(k) plans may not vote these shares at themeeting.

Can I attend the Annual Meeting, and what do Ineed for admission?

Admission to the Annual Meeting is limited to AirGroup stockholders as of March 18, 2015 andpersons holding valid proxies from stockholdersof record. To be admitted to the Annual Meeting,you must present proof of your stock ownershipas of the record date and valid, government-issued photo identification. Acceptable proof ofstock ownership includes:

• the admission ticket attached to the top ofyour proxy card (or made available byComputershare if you submit your proxyonline);

• a copy of the Notice of Proxy and AccessInstructions you received by mail;

• a photocopy of your voting instruction form;

• a letter from your bank or broker confirmingyour ownership as of the record date;

• a brokerage statement evidencing ownershipof shares of Alaska Air Group stock as of therecord date; or

• a valid proxy form.

If you do not provide photo identification orcomply with the other procedures outlined aboveupon request, you will not be admitted to theAnnual Meeting. Guests of stockholders will notbe admitted unless they provide their own proofof ownership according to the criteria outlinedabove.

Each stockholder of record or beneficialstockholder, including institutional holders, maydesignate one person to represent their sharesat the meeting. If multiple representativesrequest admission on behalf of the samestockholder, the first person to register at thedoor with appropriate proof of ownership andproper delegation of voting authority will beallowed to attend the meeting.

Security measures may include bag search,metal detector and hand-wand search. The useof cameras (including cell phones withphotographic capabilities), recording devices,smart phones and other electronic devices isstrictly prohibited.

May I vote in person at the meeting?

We will provide a ballot to any record holder ofthe Company’s stock who requests one at themeeting. If you hold your shares through abroker, you must bring a legal proxy from yourbroker in order to vote by ballot at the meeting.You may request a legal proxy from your brokerto attend and vote your shares at the meeting bymarking your voting instruction form or theInternet voting site to which your voting materialsdirect you. Please allow sufficient time to receivea legal proxy through the mail after your brokerreceives your request. Because shares held byparticipants in the Company’s 401(k) plans mustbe voted by the trustee, these shares may notbe voted at the meeting.

ŠP

roxy

GENERAL INFORMATION 5

How can I reduce the number of annual meetingmaterials I receive?

If you are a stockholder of record receivingmultiple copies of the annual meeting materialseither because you have multiple registeredstockholder accounts or because you share anaddress with other registered stockholders, andyou would like to discontinue receiving multiplecopies, you can contact the Company’s transferagent, Computershare, by telephone at(877) 282-1168 or by writing to them c/oComputershare, P.O. Box 30170, CollegeStation, TX 77842-3170.

If you are a beneficial stockholder, but not aregistered stockholder, and you share anaddress with other beneficial stockholders, thenumber of annual meeting materials you receiveis already being reduced because your broker,bank or other institution is permitted to deliver asingle copy of this material for all stockholdersat your address unless a stockholder hasrequested separate copies. If you would like toreceive separate copies, please contact yourbroker, bank or institution and update yourpreference for future meetings.

Can I receive future materials via the Internet?

If you vote on the Internet, simply follow theprompts for enrolling in electronic proxy deliveryservice. This will reduce the Company’s printingand postage costs, as well as the number ofpaper documents you will receive.

Stockholders of record may enroll in that serviceat the time they vote their proxies via theInternet or at any time after the Annual Meetingand can read additional information about thisoption and request electronic delivery by going towww.computershare.com/investor. If you holdshares beneficially, please contact your broker toenroll for electronic proxy delivery.

At this time, employee participants in a Company401(k) plan may not elect to receive notice andproxy materials via electronic delivery.

If you already receive your proxy materials via theInternet, you will continue to receive them thatway until you instruct otherwise through themethods referenced above.

How many shares must be present to hold themeeting?

A majority of the Company’s outstanding sharesentitled to vote as of the record date, or65,434,732 shares, must be present orrepresented at the meeting and entitled to votein order to hold the meeting and conductbusiness (i.e., to constitute a quorum). Sharesare counted as present or represented at themeeting if the stockholder of record attends themeeting; if the beneficial owner attends with a“legal proxy” from the record holder; or if therecord holder or beneficial owner has submitteda proxy or voting instructions, whether byreturning a proxy card or a voting instruction formor by phone or Internet, without regard towhether the proxy or voting instructions actuallycasts a vote or withholds or abstains fromvoting.

How many votes must the nominees have to beelected?

The Company’s Bylaws (as amended April 30,2010) require that each director be electedannually by a majority of votes cast with respectto that director. This means that the number ofvotes “for” a director must exceed the number ofvotes “against” that director. In the event that anominee for director receives more “against”votes for his or her election than “for” votes, theBoard must consider such director’s resignationfollowing a recommendation by the Board’sGovernance and Nominating Committee. Themajority voting standard does not apply,however, in the event that the number ofnominees for director exceeds the number ofdirectors to be elected. In such circumstances,directors will instead be elected by a plurality ofthe votes cast, meaning that the personsreceiving the highest number of “for” votes, upto the total number of directors to be elected atthe Annual Meeting, will be elected.

6 GENERAL INFORMATION

With regard to the election of directors, theBoard intends to nominate the 11 personsidentified as its nominees in this ProxyStatement. Because the Company has notreceived notice from any stockholder of an intentto nominate directors at the Annual Meeting,each of the directors must be elected by amajority of votes cast.

“Abstain” votes and broker non-votes are nottreated as votes cast with respect to a directorand therefore will not be counted in determiningthe outcome of the election of directors.

What happens if a director candidate nominatedby the Board of Directors is unable to stand forelection?

The Board of Directors may reduce the number ofseats on the Board or it may designate asubstitute nominee. If the Board designates asubstitute, shares represented by proxies heldby the named proxies will be voted for thesubstitute nominee.

Not including the election of directors, howmany votes must the proposals receive in orderto pass?

Ratification of the appointment of KPMG LLP asthe Company’s independent accountants

A majority of the shares present in person or byproxy at the meeting and entitled to vote on theproposal must be voted “for” the proposal inorder for it to pass. “Abstain” votes are deemedpresent and entitled to vote and are included forpurposes of determining the number of sharesconstituting a majority of shares present andentitled to vote. Accordingly, an abstention,because it is not a vote “for” will have the effectof a negative vote.

Advisory vote regarding the compensation of theCompany’s Named Executive Officers

A majority of the shares present in person or byproxy at the meeting and entitled to vote on theproposal must be voted “for” the proposal inorder for it to pass. “Abstain” votes are deemed

present and entitled to vote and are included forpurposes of determining the number of sharesconstituting a majority of shares present andentitled to vote. Accordingly, an abstention,because it is not a vote “for” will have the effectof a negative vote. In addition, broker non-votesare not considered entitled to vote for purposesof determining whether the proposal has beenapproved by stockholders and therefore will notbe counted in determining the outcome of thevote on the proposal.

Stockholder proposal regarding an independentchairman policy

A majority of the shares present in person or byproxy at the meeting and entitled to vote on theproposals must be voted “for” the proposal inorder for it to pass. “Abstain” votes are deemedpresent and entitled to vote and are included forpurposes of determining the number of sharesconstituting a majority of shares present andentitled to vote. Accordingly, an abstention,because it is not a vote “for” will have the effectof a negative vote. In addition, broker non-votesare not considered entitled to vote for purposesof determining whether the proposal has beenapproved by stockholders and, therefore, will notbe counted in determining the outcome of thevote on the proposal.

How are votes counted?

Voting results will be tabulated byComputershare. Computershare will also serveas the independent inspector of election.

Is my vote confidential?

The Company has a confidential voting policy asa part of its governance guidelines, which arepublished on the Company’s website.

Who pays the costs of proxy solicitation?

The Company pays for distributing and solicitingproxies and reimburses brokers, nominees,fiduciaries and other custodians their reasonablefees and expenses in forwarding proxy materialsto beneficial owners. The Company has engaged

ŠP

roxy

GENERAL INFORMATION 7

Georgeson Inc. (Georgeson) to assist in thesolicitation of proxies for the meeting. It isintended that proxies will be solicited by thefollowing means: additional mailings, personalinterview, mail, phone and electronic means.Although no precise estimate can be made atthis time, we anticipate that the aggregateamount we will spend in connection with thesolicitation of proxies will be approximately$33,000. To date, $29,000 has been incurred.This amount includes fees payable toGeorgeson, but excludes salaries and expensesof the Company’s officers, directors andemployees.

Is a list of stockholders entitled to vote at theAnnual Meeting available?

A list of stockholders of record entitled to vote atthe 2015 Annual Meeting will be available at themeeting. It will also be available Monday throughFriday from March 30, 2015 through May 6,2015 between the hours of 9 a.m. and 4 p.m.,Pacific Time, at the offices of the CorporateSecretary, 19300 International Blvd., Seattle,WA 98188. A stockholder of record may examinethe list for any legally valid purpose related tothe Annual Meeting.

Where can I find the voting results of theAnnual Meeting?

We will publish the voting results on Form 8-K onor about May 13, 2015. You can read or print acopy of that report by going to InvestorInformation-SEC Filings at www.alaskaair.com orby going directly to the SEC EDGAR files atwww.sec.gov. You can also request a copy bycalling us at (206) 392-5719 or by calling the

SEC at (800) SEC-0330 for the location of apublic reference room.

How can I submit a proposal for next year’sannual meeting?

The Company expects to hold its next annualmeeting on or about May 5, 2016. If you wish tosubmit a proposal for inclusion in the proxymaterials for that meeting, you must send theproposal to the Corporate Secretary at theaddress below. The proposal must be received atthe Company’s corporate offices no later thanNovember 28, 2015 to be considered forinclusion. Among other requirements set forth inthe SEC’s proxy rules and the Company’sBylaws, you must have continuously held aminimum of either $2,000 in market value or 1%of the Company’s outstanding stock for at leastone year by the date of submitting the proposal,and you must continue to own such stockthrough the date of the meeting.

If you intend to nominate candidates for electionas directors or present a proposal at the meetingwithout including it in the Company’s proxymaterials, you must provide notice of suchproposal to the Company no later thanFebruary 5, 2016. The Company’s Bylaws outlineprocedures for giving the required notice. If youwould like a copy of the procedures contained inThe Company’s Bylaws, please contact:

Corporate SecretaryAlaska Air Group, Inc.P.O. Box 68947Seattle, WA 98168

8 GENERAL INFORMATION

Proposal 1: Election of Directors to One-Year Terms

The Company’s Bylaws provide that directorsshall serve a one-year term. Directors are electedto hold office until their successors are electedand qualified, or until resignation or removal inthe manner provided in the Company’s Bylaws.Eleven directors are nominees for election thisyear and each has consented to serve a one-yearterm ending in 2016.

Patricia M. BedientDirector since 2004Age – 61

Ms. Bedient chairs the Board’s Audit Committee.In January 2015, Ms. Bedient was also appointeda member of the Board’s Governance andNominating Committee. She is executive vicepresident and CFO for The WeyerhaeuserCompany, one of the world’s largest integratedforest products companies. A certified publicaccountant (CPA) since 1978, she served asmanaging partner of the Seattle office of ArthurAndersen LLP prior to joining Weyerhaeuser.Ms. Bedient also worked at Andersen’s Portlandand Boise offices as a partner and as a CPAduring her 27-year career with the firm. Sheserves on the boards of Alaska Airlines andHorizon Air (subsidiaries of Alaska Air Group), theOverlake Hospital Medical Center Board, theOregon State University Board of Trustees, andthe University of Washington Foster School ofBusiness Advisory Board. She has also served onthe boards of a variety of civic organizations,including the Oregon State University FoundationBoard of Trustees, the World Forestry Center, CityClub of Portland, St. Mary’s Academy of Portland,and the Chamber of Commerce in Boise, Idaho.She is a member of the American Institute ofCPAs and the Washington Society of CPAs.Ms. Bedient received her bachelor’s degree inbusiness administration, with concentrations infinance and accounting, from Oregon StateUniversity in 1975.

Ms. Bedient’s extensive experience in publicaccounting and financial expertise qualify her toserve on the Board and to act as an auditcommittee financial expert, as defined by the SEC.

Marion C. BlakeyDirector since 2010Age – 66

Ms. Blakey is chair of the Board’s SafetyCommittee. Ms. Blakey was recently namedpresident and CEO of Rolls-Royce North America.For the last seven years, she was president andCEO of Aerospace Industries Association (AIA),the nation’s largest aerospace and defensetrade association. Prior to her current position,she served as the Administrator of the FederalAviation Administration (the FAA) from 2002 to2007 and chair of the National TransportationSafety Board (the NTSB) from 2001 to 2002.Ms. Blakey also serves on the boards of AlaskaAirlines and Horizon Air (subsidiaries of AlaskaAir Group), Noblis, the NASA Advisory Council,the President’s Export Council Subcommittee onExport Administration (PECSEA), the IndependentTakata Quality Assurance Panel, the InternationalCoordinating Council of Aerospace IndustriesAssociations (ICCAIA), as well as a number ofphilanthropic and community organizations,including the Washington Area Airports TaskForce Advisory Board and the InternationalAviation Women’s Association.

Ms. Blakey’s experience with AIA, the FAA andthe NTSB qualify her for service on theCompany’s Board and, because of herexperience with the FAA and NTSB, she brings avery relevant and important perspective to thedeliberations of the Safety Committee.

Phyllis J. CampbellDirector since 2002Age – 63

Ms. Campbell is lead director and chair of theBoard’s Governance and Nominating Committee.She has been chairman of the Pacific NorthwestRegion for JPMorgan Chase & Co. since April2009. She is the firm’s senior executive inWashington, Oregon, and Idaho , representingJPMorgan Chase at the most senior level. From2003 to 2009, Ms. Campbell served aspresident and CEO of The Seattle Foundation,one of the nation’s largest community

ŠP

roxy

PROPOSALS TO BE VOTED ON 9

philanthropic foundations. She was president ofU.S. Bank of Washington from 1993 until 2001and served as chair of the bank’s CommunityBoard. Ms. Campbell has received severalawards for her corporate and communityinvolvement. These awards include Women WhoMake A Difference and Director of the Year fromthe Northwest Chapter of the NationalAssociation of Corporate Directors. Since August2007, Ms. Campbell has served on Toyota’sDiversity Advisory Board. She also serves on theboards of Alaska Airlines and Horizon Air(subsidiaries of Alaska Air Group) andNordstrom, where she chaired the auditcommittee until November 2013. Until February2009, she served on the boards of Puget Energyand its subsidiary, Puget Sound Energy.

Ms. Campbell’s business and communityleadership background and her extensivegovernance experience qualify her for her role aslead director of the Board.

Dhiren R. FonsecaDirector since 2014Age – 50

Mr. Fonseca was appointed to the Alaska AirGroup Board in October 2014. He is a memberof the Board’s Audit Committee. He joinedCertares LP as a partner in December 2014.Previously, Mr. Fonseca was chief commercialofficer at Expedia, Inc., where he served for morethan 18 years. He contributed greatly to theonline travel company’s growth and success,serving in a host of key roles including co-president of its global partner services group andsenior vice president of corporate developmentamong others. Mr. Fonseca helped foundExedia.com as part of the management team atMicrosoft Corporation that brought the onlinetravel company to life in 1995 and subsequentlytook it public in 1999. Before Expedia, he heldmultiple roles in product management andcorporate technical sales at MicrosoftCorporation. Mr. Fonseca currently serves on theboards of Alaska Airlines and Horizon Air(subsidiaries of Alaska Air Group), CaesarsAcquisition Corporation, eLong, Inc., andRentPath, Inc.

Mr. Fonseca’s expertise in the online travelservices industry, combined with hismanagement and technology experience at amajor software and computer services companycorrespond with key aspects of the Company’sbusiness strategy and qualify him for service onthe Alaska Air Group Board.

Jessie J. Knight, Jr.Director since 2002Age – 64

Mr. Knight serves on the Board’s SafetyCommittee and its Governance and NominatingCommittee. He also served on the Board’sCompensation and Leadership DevelopmentCommittee during 2014. Mr. Knight is executivevice president of external affairs for SempraEnergy, as well as chairman of San Diego Gasand Electric Company and chairman of SouthernCalifornia Gas Company, both subsidiaries ofSempra Energy. From 2010 to 2014, he waschairman and CEO of San Diego Gas & Electric.From 2006 to 2010, he was executive vicepresident of external affairs at Sempra Energy.From 1999 to 2006, Mr. Knight served aspresident and CEO of the San Diego RegionalChamber of Commerce, and from 1993 to 1998,he was a commissioner of the California PublicUtilities Commission. Prior to this, for eightyears, Mr. Knight was vice president ofmarketing and strategic planning for the SanFrancisco Chronicle and San Francisco Examinernewspapers. While there, he won five NationalClio Awards for television, radio and printedadvertising and a Cannes Film Festival GoldenLion Award for business marketing. Prior to hismedia career, Mr. Knight spent ten years infinance and marketing with the Dole FoodsCompany in its banana and pineapplebusinesses. Mr. Knight serves on the boards ofAlaska Airlines and Horizon Air (subsidiaries ofAlaska Air Group), the Timken Museum of Art inSan Diego, the Southern California LeadershipCouncil, and the University of California SanDiego Foundation. He is a life member of theCouncil on Foreign Relations and is a corporatemember of the Hoover Institution at StanfordUniversity. He is a board member of the U.S.Chamber of Commerce, The Energy Institute and

10 PROPOSALS TO BE VOTED ON

The Inter-American Dialogue. He previouslyserved ten years on the board of the San DiegoPadres Baseball Club. He served seven years onthe board of Avista Corp., a utility in Spokane,Washington, where he served on the audit andgovernance committees, and as lead director.

Mr. Knight’s expertise in brand marketing, energymarkets and economic development, as well ashis broad business experience qualify him forservice on the Alaska Air Group Board.

Dennis F. MadsenDirector since 2003Age – 66

Mr. Madsen serves on the Board’sCompensation and Leadership DevelopmentCommittee and its Audit Committee. From 2000to 2005, Mr. Madsen was president and CEO ofRecreational Equipment, Inc. (REI), a retailer andonline merchant for outdoor gear and clothing.He served as REI’s executive vice president andCOO from 1987 to 2000, and prior to that heldnumerous other positions at REI. In 2010,Mr. Madsen was appointed a director of WestMarine Inc., a publicly traded retail company inthe recreational boating sector. He also chairsWest Marine’s compensation and leadershipdevelopment committee and serves on itsnominations and governance committee. Otherboards on which Mr. Madsen serves includeAlaska Airlines and Horizon Air (subsidiaries ofAlaska Air Group), the Western WashingtonUniversity Foundation, Forterra, and the YouthOutdoors Legacy Fund.

Because of his varied business background andhis experience in leading a large people-orientedand customer-service-driven organization,Mr. Madsen is qualified to serve on the AlaskaAir Group Board.

Helvi K. SandvikDirector since 2013Age – 57

Ms. Sandvik serves on the Board’s SafetyCommittee. Since 1995, Ms. Sandvik has beenpresident of NANA Development Corporation, a

diversified business engaged in governmentcontracting, oilfield and mining support,professional management services, andengineering and construction. She also serveson the not-for-profit board of the Native AmericanContractors Association and as an advisor to theRobert Aqqaluk Newlin Trust. She was director ofthe Federal Reserve Bank of San Francisco,Seattle Branch from 2004 to 2009 and servedas its chair from 2008 to 2009. Ms. Sandvikalso serves as a director of Alaska Airlines andHorizon Air (subsidiaries of Alaska Air Group).

Ms. Sandvik’s business leadership experienceand her intimate knowledge of the Native cultureand transportation industry requirements in thestate of Alaska qualify her to serve on the AlaskaAir Group Board.

Katherine J. SavittDirector since 2014Age – 51

Ms. Savitt was appointed to the Alaska Air GroupBoard in October 2014. She is a member of theBoard’s Compensation and LeadershipDevelopment Committee. Ms. Savitt is chiefmarketing officer for Yahoo!, responsible forglobal marketing and media. Prior to Yahoo!,Ms. Savitt was founder and CEO of Lockerz, astart-up focused on social commerce forGeneration Z. Previously, she was executive vicepresident and chief marketing officer at AmericanEagle Outfitters, Inc., where she led both theglobal marketing efforts of the company’sportfolio of brands and the digital and e-commerce channels. Ms. Savitt has also servedas vice president of strategic communications,content and entertainment initiatives forAmazon.com. She founded MWW/Savitt, anintegrated marketing communications firmrepresenting a diverse array of world classbrands and consumer technology start-ups. Sheholds a bachelor’s degree from CornellUniversity. Ms. Savitt also serves on the boardsof Alaska Airlines and Horizon Air (subsidiaries ofAlaska Air Group), and the Vitamin Shoppe, Inc.

Ms. Savitt’s business and entrepreneurialexpertise as well as her experience with digital

ŠP

roxy

PROPOSALS TO BE VOTED ON 11

and e-commerce marketing channels andstrategic communications support areas ofstrategic importance and qualify her for serviceon the Alaska Air Group Board.

J. Kenneth ThompsonDirector since 1999Age – 63

Mr. Thompson is chair of the Board’sCompensation and Leadership DevelopmentCommittee and also serves on the SafetyCommittee. Since 2000, Mr. Thompson hasbeen president and CEO of Pacific Star EnergyLLC, a private energy investment company inAlaska with partial ownership in the oilexploration firm Alaska Venture Capital Group(AVCG LLC). From 1998 to 2000, Mr. Thompsonserved as executive vice president of ARCO’sAsia Pacific oil and gas operating companies inAlaska, California, Indonesia, China andSingapore. Prior to that, he was president ofARCO Alaska, Inc., the parent company’s oil andgas producing division based in Anchorage,Alaska. He currently serves on the boards ofAlaska Airlines and Horizon Air (subsidiaries ofAlaska Air Group), Pioneer Natural ResourcesCompany, Tetra Tech, Inc., and Coeur MiningCorporation, as well as on the non-profit board ofProvision Ministry Group. Mr. Thompson chairsthe environmental, health, safety and socialresponsibility committee and serves on thegovernance and nominating and the auditcommittees of Coeur Mining Corporation. AtTetra Tech, Mr. Thompson serves on the strategyplanning committee and chairs thecompensation committee. At Pioneer NaturalResources, he serves on the governance andnominating, compensation and hydrocarbonreserves committees and chairs the health,safety and environmental committee.

Mr. Thompson’s business leadership and hisbreadth of experience in planning, operations,engineering, and safety/regulatory issues qualifyhim for service on the Alaska Air Group Board.

Bradley D. TildenDirector since 2010Age – 54

Mr. Tilden has been chairman of Alaska AirGroup and of Alaska Airlines and Horizon Air(subsidiaries of Alaska Air Group) since January2014. He has served as president of AlaskaAirlines since December 2008. In May 2012,Mr. Tilden was named president and CEO ofAlaska Air Group and CEO of Alaska Airlines andHorizon Air. He served as executive vicepresident of finance and planning from 2002 to2008 and as CFO from 2000 to 2008 for AlaskaAirlines and Alaska Air Group, and prior to 2000,was vice president of finance at Alaska Airlinesand Alaska Air Group. Before joining AlaskaAirlines, Mr. Tilden worked for the accountingfirm PricewaterhouseCoopers. He serves on theboards of Alaska Airlines and Horizon Air, Airlines4 America, Pacific Lutheran University, and theBoy Scouts of America. Mr. Tilden also serves onand chairs the board of the WashingtonRoundtable.

Mr. Tilden’s role as CEO of Alaska Air Group andits operating subsidiaries, his deep airlineexperience, strategic planning skills and financialexpertise qualify him to serve on the Air GroupBoard.

Eric K. YeamanDirector since 2012Age – 47

Mr. Yeaman serves on the Board’s AuditCommittee. He is president and CEO of HawaiianTelcom (a telecommunications company servingthe state of Hawaii). Prior to joining HawaiianTelcom in June 2008, he was senior executivevice president and COO of Hawaiian ElectricCompany, Inc. (HECO). Mr. Yeaman joinedHawaiian Electric Industries, Inc. (HEI), HECO’sparent company, in 2003 as financial vicepresident, treasurer and CFO. Prior to joining HEI,Mr. Yeaman held the positions of chief operatingand financial officer for Kamehameha Schoolsfrom 2000 to 2003. He began his career atArthur Andersen LLP in 1989. Mr. Yeamanserves on the not-for-profit boards of Queen’s

12 PROPOSALS TO BE VOTED ON

Health Systems, Hawaii Community Foundation,Hawaii Business Roundtable, The NatureConservancy of Hawaii, Kamehameha SchoolsAudit Committee, Aloha United Way, and theHarold K.L. Castle Foundation. He is also adirector of Alaska Airlines and Horizon Air(subsidiaries of Alaska Air Group), Alexander &Baldwin, the United States Telcom Association,and is a member of the Hawaii Asia PacificAssociation.

Mr. Yeaman’s extensive business background,his experience as CEO of a public company, andhis intimate knowledge of the culture of Hawaii(a region that accounts for a significant portionof Alaska’s business) qualify him to serve as amember of the Air Group Board.

THE BOARD OF DIRECTORS RECOMMENDS THAT YOU VOTE FOR THEELECTION OF THE 11 DIRECTOR NOMINEES NAMED ABOVE.

UNLESS OTHERWISE INDICATED ON YOUR PROXY, THE SHARES WILL BEVOTED FOR THE ELECTION OF THESE 11 NOMINEES AS DIRECTORS.

Proposal 2: Ratification of the Appointment of the Company’s Independent Accountants

The Audit Committee has selected KPMG LLP(KPMG) as the Company’s independentaccountants for fiscal year 2015, and the Boardis asking stockholders to ratify that selection.Although current law, rules, and regulations, aswell as the charter of the Audit Committee,require the Audit Committee to engage, retain,and supervise the independent accountants, theBoard considers the selection of theindependent accountants to be an importantmatter of stockholder concern and is submitting

the selection of KPMG for ratification bystockholders as a matter of good corporatepractice.

The affirmative vote of holders of a majority ofthe shares of common stock represented at themeeting and entitled to vote on the proposal isrequired to ratify the selection of KPMG as theCompany’s independent accountant for thecurrent fiscal year.

THE BOARD OF DIRECTORS RECOMMENDS THAT YOU VOTE FOR THE RATIFICATION OF THECOMPANY’S INDEPENDENT ACCOUNTANTS.

Proposal 3: Advisory Vote Regarding the Compensation of theCompany’s Named Executive Officers

The Company is providing its stockholders with theopportunity to cast a non-binding, advisory vote onthe compensation of the Company’s NamedExecutive Officers as disclosed pursuant to theSEC’s executive compensation disclosure rulesand set forth in this Proxy Statement (including thecompensation tables and the narrative discussionaccompanying those tables as well as in theCompensation Discussion and Analysis).

As described more fully in the CompensationDiscussion and Analysis section of this ProxyStatement, the structure of the Company’s

executive compensation program is designed tocompensate executives appropriately andcompetitively and to drive superior performance.For the Named Executive Officers, a highpercentage of total direct compensation isvariable and tied to the success of the Companybecause they are the senior leaders primarilyresponsible for the overall execution of theCompany’s strategy. The Company’s strategicgoals are reflected in its incentive-basedexecutive compensation programs so that theinterests of executives are aligned withstockholder interests. Executive compensation is

ŠP

roxy

PROPOSALS TO BE VOTED ON 13

designed to be internally equitable, to rewardexecutives for responding successfully tobusiness challenges facing the Company, and totake into consideration the Company’s sizerelative to the rest of the industry.

The Compensation Discussion and Analysissection of this Proxy Statement describes inmore detail the Company’s executivecompensation programs and the decisions madeby the Compensation and LeadershipDevelopment Committee during 2014. Highlightsof these executive compensation programsinclude the following:

Base Salary

In general, for the Named Executive Officers, theCommittee targets base salary levels at the 25th

percentile relative to the Company’s airline peergroup with the opportunity to earn market-level orabove compensation through short- and long-term incentive plans that pay when performanceobjectives are met.

Annual Incentive Pay

The Company’s Named Executive Officers areeligible to earn annual incentive pay under thebroad-based Performance-Based Pay Plan, inwhich all employees participate and which isintended to motivate the executives to achievespecific Company goals. Annual targetperformance measures reflect near-term financialand operational goals that are consistent withthe strategic plan.

Long-term Incentive Pay

Equity-based incentive awards that link executivepay to stockholder value are an importantelement of the Company’s executivecompensation program. Long-term equityincentives that vest over three- or four-yearperiods are awarded annually, resulting in

overlapping vesting periods that are designed todiscourage short-term risk taking and to alignNamed Executive Officers’ long-term interestswith those of stockholders while helping theCompany attract and retain top-performingexecutives who fit a team-oriented andperformance-driven culture.

In accordance with the requirements ofSection 14A of the Exchange Act (which wasadded by the Dodd-Frank Wall Street Reform andConsumer Protection Act) and the related rulesof the SEC, the Board of Directors will requestyour advisory vote on the following resolution atthe 2015 Annual Meeting:

RESOLVED, that the compensation paidto the Named Executive Officers, asdisclosed in this Proxy Statement pursuantto the SEC’s executive compensationdisclosure rules (which disclosure includesthe Compensation Discussion and Analysis,the compensation tables and the narrativediscussion that accompanies thecompensation tables), is hereby approved.

This proposal regarding the compensation paidto the Company’s Named Executive Officers isadvisory only and will not be binding on theCompany or the Board and will not be construedas overruling a decision by the Company or theBoard or as creating or implying any additionalfiduciary duty for the Company or the Board.However, the Compensation and LeadershipDevelopment Committee, which is responsiblefor designing and administering the Company’sexecutive compensation program, values theopinions expressed by stockholders in their voteon this proposal and will consider the outcomeof the vote when making future compensationdecisions for the Named Executive Officers.Stockholders will be given an opportunity to castan advisory vote on this topic annually, with thenext opportunity occurring in connection with theCompany’s annual meeting in 2016.

THE BOARD OF DIRECTORS RECOMMENDS THAT YOU VOTE FOR THE APPROVAL OF THECOMPENSATION OF THE NAMED EXECUTIVE OFFICERS, AS DISCLOSED IN THIS PROXY STATEMENT

PURSUANT TO THE SEC’S EXECUTIVE COMPENSATION DISCLOSURE RULES.

14 PROPOSALS TO BE VOTED ON

Proposal 4: Stockholder Proposal Regarding Independent Board Chairman

Mr. John Chevedden has given notice of hisintention to present a proposal at the 2015Annual Meeting. Mr. Chevedden’s address is2215 Nelson Avenue, No. 205, Redondo Beach,California 90278, and Mr. Chevedden representsthat he has continuously owned no less than100 shares of the Company’s common stocksince July 1, 2013. Mr. Chevedden’s proposaland supporting statement, as submitted to theCompany, appear below.

The Board of Directors opposes adoption ofMr. Chevedden’s proposal and asksstockholders to review the Board’s response,which follows Mr. Chevedden’s proposal andsupporting statement below.

The affirmative vote of the holders of a majority ofthe shares of common stock present, in person orrepresented by proxy at the meeting and entitled tovote is required to approve this proposal.

ALK: Rule 14a-8 Proposal, November 2, 2014

Proposal 4 - Independent Board Chairman

Resolved: Shareholders request that theBoard of Directors adopt a policy that theChair of the Board of Directors shall be anindependent director who is not a current orformer employee of the company, andwhose only nontrivial professional, familialor financial connection to the company or itsCEO is the directorship. The policy should beimplemented so as not to violate existingagreements and should allow for departureunder extraordinary circumstances such asthe unexpected resignation of the chair.

When our CEO is our board chairman, thisarrangement can hinder our board’s abilityto monitor our CEO’s performance. Manycompanies already have an independentChairman. An independent Chairman is theprevailing practice in the United Kingdomand many international markets. Thisproposal topic won 50%-plus support at 5major U.S. companies in 2013 including73%-support at Netflix.

This topic is of additional importance forAlaska Air because our company seems tohave a default type of quasi-lead director.Plus there are questions on theindependence of 5 of our directors who eachhave 10 to 32-years of long-tenure: PatriciaBedient, Jessie Knight, Phyllis Campbell,Kenneth Thompson and Byron Mallott. GMIRatings, an independent investmentresearch firm, said long-tenured directors

can form relationships that may compromisedirector independence and therefore hinderdirector ability to provide effective oversightof our CEO/Chairman. These 5 directorsontrolled [sic] 87% of the votes on our 3most important board committees.

Other concerns with director oversightinclude the assignment of KennethThompson to our executive pay committeeas chairman when he is potentiallyoverextended with seats on 4 public boards.And Alaska Air did $2.7 million of businesswith Helvi Sandvik’s company.

Additional issues (as reported in 2014) arean added incentive to vote for this proposal:

GMI was concerned with excessive CEO perksand pension benefits. Unvested equity awardspartially or fully accelerate upon CEOtermination. Meanwhile shareholders had apotential 14% stock dilution. GMI rated AlaskaAir D in accounting. Alaska Air reported a$120 million charge related to how it reportsits revenue from its Bank of America creditcard agreement (October 2013).

Returning to the core topic of this proposalfrom the context of our clearly improvablecorporate governance, please vote to protectshareholder value:

Independent Board Chairman - Proposal 4

ŠP

roxy

PROPOSALS TO BE VOTED ON 15

THE BOARD OF DIRECTORS RECOMMENDS THAT YOU VOTE AGAINST PROPOSAL 4FOR THE FOLLOWING REASONS:

At the Company’s 2014 annual meeting ofstockholders, Mr. Chevedden proposed that theBoard of Directors adopt this policy. The Board ofDirectors opposed the proposal last year, andstockholders rejected the proposal with over 80percent of the votes cast opposed to it.

The Board maintains that the current leadershipstructure best serves the interests of theCompany and its stockholders. The Board’sleadership structure generally features acombined chairman and CEO role and a strong,independent lead director. However, the Boardhas discretion to depart from this structurewhere circumstances warrant and has done so inthe past. The proponent would eliminate theBoard’s flexibility to combine the chairman andCEO roles except in “extraordinarycircumstances.” The Board believes that it is notin the shareholders’ interests to restrict theBoard’s discretion in this respect.

The Board’s existing leadership structure iseffective and appropriately flexible

In the Board’s view, the leadership structure inwhich the chairman and CEO roles are combinedserves a number of important goals. A chair/CEOfacilitates the flow of information betweenmanagement and the Board, keeps the Boardinformed about the Company’s business and theairline industry, and consults with boardmembers in a timely manner about importantissues facing the Company. The Board alsobelieves that the current structure providesfocused leadership for the Company, helpsensure accountability for the Company’sperformance and promotes a clear, unified visionfor Alaska Air Group by assuring that thestrategies adopted by the Board will be wellpositioned for execution by management. The

Board regards this leadership structure as astrong contributor to the Company’s recentsuccess.

The Board considers many factors indetermining optimal leadership structure

In choosing to combine the roles of chairman andCEO, the Board takes into consideration the highlytechnical nature of the airline industry and thecomplexity and dynamic nature of the Company’sbusiness and operating environment. In addition,the Board considers, among other things, theexperience and capacity of the sitting CEO, therigor of independent director oversight of financial,operational and safety regulatory issues, thecurrent climate of openness between managementand the Board, and the existence of other checksand balances that help ensure independentthinking and decision-making by directors.

Restricting Board discretion would bedetrimental to stockholders’ interests

The proposal seeks to mandate one leadershipstructure that would apply except in “extraordinarycircumstances.” Because of the presence of theindependence safeguards noted above, the Boardbelieves it is not only unnecessary, but that itwould be detrimental to restrict the Board’sleadership structure to one form. The members ofthe Board have experience with and knowledge ofthe challenges and opportunities the Companyfaces at any given time, and therefore they are inthe best position to choose the leadershipstructure that is most appropriate for thesituation. The Board’s commitment to select aleadership structure that is most appropriate forthe Company and its stockholders is bestevidenced by the Board’s decision to separate thechairman and CEO positions during 2012-2013 inconnection with the transition to a new CEO.

16 PROPOSALS TO BE VOTED ON

Ten of the Board’s eleven directors areindependent

The Company’s Governance Guidelines requirethat at least 75% of directors satisfyindependence criteria established by the SECand the NYSE and those set forth in the DirectorIndependence section of this Proxy Statement. Atpresent, the Board has determined that 10 outof 11 directors, or 91%, are independentaccording to these standards.

The Board has a strong, independent leaddirector

The Board’s lead director is appointed by andfrom among the independent board membersand has specific authority that ensures objective,independent oversight of management’sstrategic decisions, risk management,succession planning, and executive performanceand compensation. The authority andresponsibilities of the lead director are outlinedin the Company’s Governance Guidelines, whichare available at www.alaskaair.com. The leaddirector:

• serves as liaison between the chairman andthe independent directors;

• is authorized to call a meeting of theindependent directors at any time;

• is authorized to call a meeting of the fullboard at any time;

• presides at meetings where the boardchairman is not present or where he/shecould be perceived as having a conflict ofinterest;

• presides over quarterly executive sessions ofthe independent directors;

• approves board meeting agendas andmeeting schedules to ensure that appropriatetime is allotted to topics of importance;

• approves information sent to board members;

• leads the independent directors’ annualevaluation of the CEO’s performance;

• conducts interviews of independent directorsannually prior to nomination for election;

• discusses proposed changes to committeeassignments with each director; and

• makes herself or himself available forconsultation and direct communication withmajor stockholders.

Responding to the proponent’s assertion thatthe Company has “a default type of quasi-leaddirector,” the Board wishes to state that the leaddirector role and responsibilities are meaningfuland carefully tailored to promote the Board’soversight and independence obligations.

The governance structure fosters boardindependence

The Board believes the Company’s corporategovernance practices, beyond those allowing fora strong lead director, make it unnecessary torequire an independent chairman. For example:

• Each of the Audit, the Compensation andLeadership Development, and theGovernance and Nominating Committees isrequired to be composed solely ofindependent directors. This means that theoversight of key matters, such as the integrityof financial statements, CEO performance,executive compensation, the nomination ofdirectors, and evaluation of the Board and itscommittees, is entrusted exclusively toindependent directors.

• The Board and its committees meet regularlyin executive session without management,and they have access to management andthe authority to retain independent advisors,as they deem appropriate.

• All independent directors play a role inoverseeing the CEO’s performance, with theBoard routinely discussing this subject inexecutive session without the CEO present.

• The Company has a 15-year maximum termlimit for new directors elected since 2012 inorder to ensure fresh perspectives on theBoard.

ŠP

roxy

PROPOSALS TO BE VOTED ON 17

Alaska Air Group governance practices rankedamong the best by ISS

As of the printing of this proxy statement, AlaskaAir Group maintains a governance rating of “1”from Institutional Shareholder Services (ISS),which is the highest ranking possible.

Additional information

In considering how to vote on the proposal, it isimportant to note that the proponent has madeseveral assertions that are false or misleading.The assertions are not directly related to theproposal to require an independent chairman,and they are addressed here in the interest ofproviding full information to investors.

• The proponent correctly cites the fact thatfive directors serving on the Board as ofNovember 2, 2014 have tenures of 10 yearsor more, and the Board wishes to provide thefollowing context:

The Board has added five independentdirectors over the past five years, and twolong-tenured directors stepped down in 2014,resulting in an average tenure of seven yearsamong the Company’s ten independentdirectors. The Board has a 15-year maximumterm limit for directors elected since 2012 inorder to ensure fresh perspectives on theBoard. The Board values the experience of itsdirectors and views a diversity of tenure as anasset that compromises neither directors’independence nor their ability to oversee theCEO.

• The proponent incorrectly states that fivelong-tenured directors (as of November 2,2014) “controlled 87% of the votes on ourthree most important board committees.”

As a result of the board refreshmentdescribed above, the average tenures ofdirectors on board committees has alsodeclined. The average tenure of directors onthe Audit Committee, the Compensation andLeadership Development Committee, and theGovernance and Nominating Committee is sixyears, nine years and 12 years, respectively.

• The proponent incorrectly states that AlaskaAir Group reported a $120 million “charge”related to its Bank of America credit cardagreement.

In connection with modifications to AlaskaAirlines’ affinity card agreement with Bank ofAmerica in July 2013, the Company recordeda one-time, favorable “special” revenue itemof $192 million pre-tax ($120 million post-tax) in the third quarter of 2013. The Boardrefers interested investors to pages 9-10 ofthe Company’s report on Form 10-Q for thequarter ended September 30, 2013, foradditional information on this accountingmatter.

• The proponent imprecisely states that“Alaska Air did $2.7 million of business withHelvi Sandvik’s company.”

As disclosed in this Proxy Statement, AlaskaAirlines purchased $3 million in services froman entity in which NANA DevelopmentCorporation holds a 51% interest. DirectorHelvi Sandvik is the president of NANADevelopment Corporation and has no directmaterial interest in the reported transactions.Accordingly, the Board affirmed herindependence in light of SEC, NYSE and theCompany’s independence standards.

• The proponent asserts that the CEO receivesexcessive perquisites and pension benefits.

In 2014, the Compensation and LeadershipDevelopment Committee decided to phaseout the CEO’s and other executives’perquisite allowances over a three-yearperiod. With respect to pension benefits, theRetirement Plan for Salaried Employees andthe Company’s 401(k) plans are tax-qualifiedretirement plans in which the CEOparticipates on substantially the same termsas other participating employees. Federal lawlimits the amount that may be paid toexecutives under a tax-qualified retirementplan, meaning that pension benefits thatwould otherwise be provided to the CEO arerequired to be limited. The CEO receivesmake-up retirement benefits through an

18 PROPOSALS TO BE VOTED ON

unfunded defined-benefit plan. The Boardrefers interested investors to theCompensation and Leadership DevelopmentCommittee’s detailed discussion of theseexecutive compensation arrangements underPerquisites and Personal Benefits andRetirement Benefits/Deferred Compensationin the Compensation Discussion and Analysissection of this Proxy Statement.

• The proponent states that the CEO’sunvested equity awards would partially or fullyaccelerate upon his termination.

The Compensation and LeadershipDevelopment Committee has put in placechange-in-control severance arrangementsthat trigger only if there has been a change incontrol and the CEO has been terminated not“for cause.” The arrangements are in linewith market practice and are designed to

help retain the Company’s key employeesand maintain a stable work environmentleading up to and during a change in control.For more information on the arrangements,see Agreements Regarding Change in Controland Termination in the CompensationDiscussion and Analysis section of this ProxyStatement.

• The proponent states that shareholders face“a potential 14% stock dilution,” presumablypremised on the full acceleration of theCEO’s unvested equity awards upon a changein control.

If a change in control occurs and the CEO isterminated not “for cause,” dilution of lessthan 0.5% would occur based on theacceleration of the CEO’s unvested equityunder existing change-in-controlarrangements.

ACCORDINGLY, THE BOARD OF DIRECTORS UNANIMOUSLY RECOMMENDS A VOTEAGAINST PROPOSAL 4.

ŠP

roxy

PROPOSALS TO BE VOTED ON 19

Structure of the Board of Directors

In accordance with the Delaware GeneralCorporation Law and the Company’s Certificateof Incorporation and Bylaws, the Company’sbusiness affairs are managed under the directionof the Board of Directors. Directors meet theirresponsibilities by, among other things,participating in meetings of the Board and Boardcommittees on which they serve, discussingmatters with the chairman and CEO and otherexecutives, reviewing materials provided to them,and visiting the Company’s facilities.

Pursuant to the Bylaws, the Board of Directorshas established four standing committees, whichare the Audit Committee, the Compensation and

Leadership Development Committee, theGovernance and Nominating Committee, and theSafety Committee. Only independent directorsserve on these committees. The Board hasadopted a written charter for each committee.These charters are posted on the Company’swebsite, can be accessed free of charge atwww.alaskaair.com and are available in print toany stockholder who submits a written request tothe Company’s Corporate Secretary at P.O. Box68947, Seattle, WA 98168.

The table below shows the current members andchairs of the standing Board committees.

Board Committee Memberships

Name Audit Committee

Compensation andLeadership

DevelopmentCommittee

Governance andNominating Committee Safety Committee

Patricia M. Bedient Chair Š

Marion C. Blakey ChairPhyllis J. Campbell ChairDhiren R. Fonseca Š

Jessie J. Knight, Jr. Š Š

Dennis F. Madsen Š Š

Helvi K. Sandvik Š

Katherine J. Savitt Š

J. Kenneth Thompson Chair Š

Eric K. Yeaman Š

The principal functions of the standing Boardcommittees are as follows:

Governance and Nominating Committee

Pursuant to its charter, the Governance andNominating Committee’s responsibilitiesinclude the following: