2013 Retirement Webinar Series

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

2013 Retirement Webinar Series

2013 Trends in Retirement, Focusing on

Your Plan’s Financial Wellness

Byron Beebe, Virginia Maguire, Rob Reiskytl, Aon Hewitt

Alisa Hunt, Kimberly-Clark

1

Agenda

Section 1 Why Financial Wellness?

Section 2 Tools and Resources

Section 3 Motivating Employees to Take Action

Section 4 Case Study — Kimberly-Clark

2 Retirement Webinar Series | May 29, 2013

Why Financial Wellness?

3

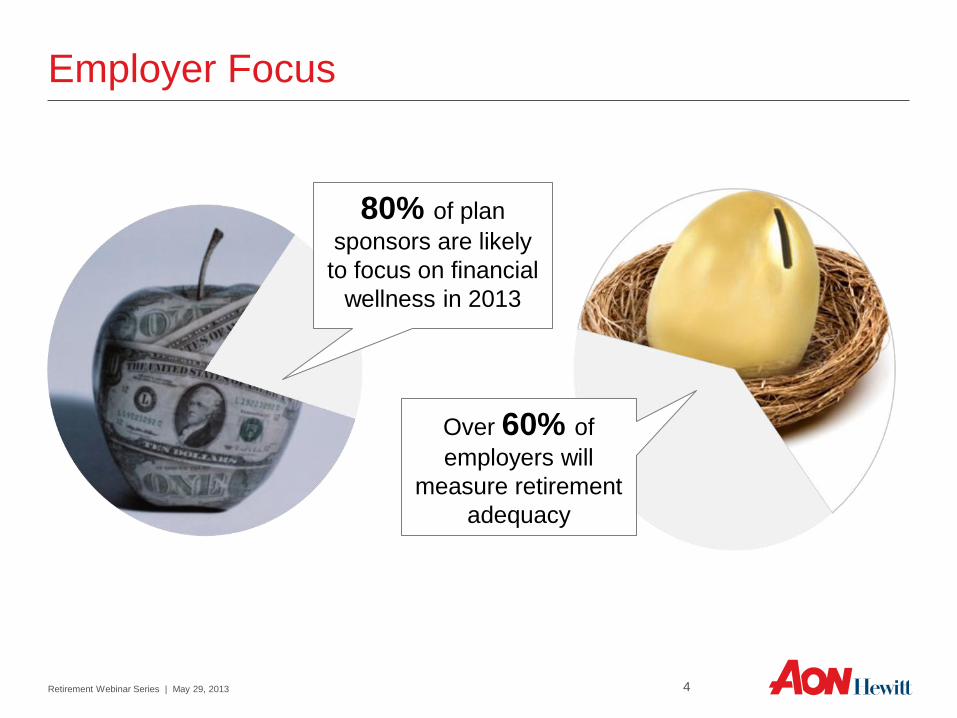

Employer Focus

80% of plan

sponsors are likely

to focus on financial

wellness in 2013

Over 60% of

employers will

measure retirement

adequacy

4 Retirement Webinar Series | May 29, 2013

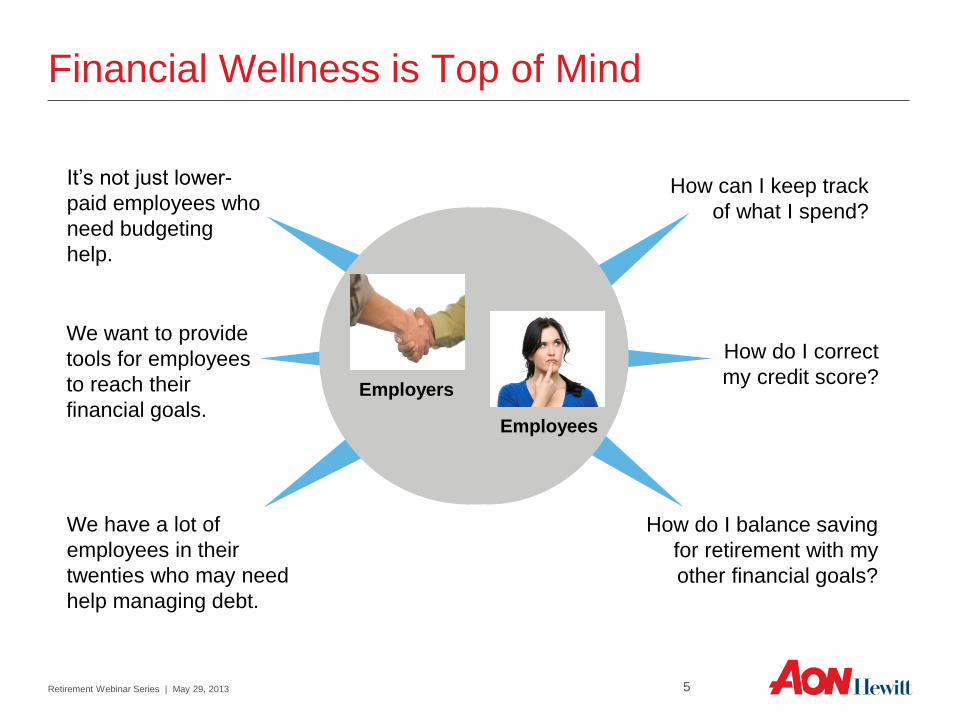

Financial Wellness is Top of Mind

Participants

How can I keep track

of what I spend?

How do I correct

my credit score?

How do I balance saving

for retirement with my

other financial goals?

It’s not just lower-

paid employees who

need budgeting

help.

We want to provide

tools for employees

to reach their

financial goals.

We have a lot of

employees in their

twenties who may need

help managing debt.

Employers

Employees

5 Retirement Webinar Series | May 29, 2013

Millennials Young Families Families With

Older Children

Pre-Retirees Retirees

Saving for…

A home

Paying down

debt

Financial

decisions

Saving for…

A home

College

Retirement

Paying down debt

Credit issues

Saving for…

College

Retirement

Financial help

A plan for the future

Insurance needs

Saving for…

Retirement

Starting a

business

Retirement

planning

Timing

Lifetime income

Tax and Estate

planning

Saving for…

Starting a

business

Tax-efficient

retirement income

Estate planning

Medical options

and cost

Retirement Webinar Series | May 29, 2013 6

Financial Needs

Path to Transformation

Go Deeper

Retirement

Savings

Lifetime

Income

Family

Expand Reach

Debt and

Credit

Financial

Literacy

Go Broader Other Long-term

Savings

Health

Impact on

Retirement

Income

Participant Spouse

ENABLERS: Research | Technology | Help | Access to Data

7 Retirement Webinar Series | May 29, 2013

Tools and Resources

8

Polling Question

9

As an organization, which financial wellness topic is most important

to your employees?

Financial Wellness—More Than Retirement

Retirement

Planning Lifetime Income

Taxation

Retiree Medical

Debt

Management Budgeting

Debt reduction

Credit

Financial

Planning Major purchases

Medical expenses

Risk management

Estate planning

Investment

Management Advice

Guidance

Targeted Messaging

Financial solutions today are holistic and can be targeted

Benefits and Resources:

DB and DC Plans

Social Security

Retiree Medical Funding

Education and Modeling Tools

Benefits and Resources:

Financial Planning

Financial Health Appraisal

Credit counseling, Budgeting tools

Online, phone, in-person help

10 Retirement Webinar Series | May 29, 2013

Help People…Improve Their Financial Future

Create the Foundation

Create a

brand/theme

Analyze the

workforce

Define tools

and resources

Retirement Webinar Series | May 29, 2013 11

Aon Hewitt The Real Deal—2012 Retirement Income Adequacy at Large Companies

12

On Track Not On Track

Average financial need for “comfortable” retirement:

85% pay replacement (including Social Security)

11 times final pay at retirement (beyond Social Security)

Can Employees Retire at Age 65

Retirement Webinar Series | May 29, 2013

0.00x

1.75x

4.00x

7.00x

11.00x

25 35 45 55 65

Aon Hewitt The Real Deal—2012 Retirement Income Adequacy at Large Companies

Increasing Awareness

Multiples of Pay

Milestones

Age

How can individuals quickly see if they are on track to retire comfortably?

13 Retirement Webinar Series | May 29, 2013

It depends on when they start, and when they want to retire

All contributions (employee and employer)

Percent of each year’s pay

Average percentage shown; approximately 3% range around average allows for changing assumptions. Calculations

assume consistent savings rate every year during working career until retirement at age 65 (or 67) with targeted retirement

resources of 11 times pay at 65 or 9.4 times pay at 67, 7% annual return on DC assets during accumulation, 4% annual pay

increases, and unsubsidized future retiree medical coverage

How much should employees save for retirement each year?

15% (age 65)

12% (age 67)

Start at 25 19%

(age 65)

15% (age 67)

Start at 30 24%

(age 65)

18% (age 67)

Start at 35

14 Retirement Webinar Series | May 29, 2013

Increasing Awareness

Financial Wellness

Message Measure Manage

15 Retirement Webinar Series | May 29, 2013

General Messaging—Help

employees establish goals. Promote

awareness, resources and tools.

Seminars, Webinars, Benefits

Fairs—Review and promote various

aspects of financial wellness.

Retirement Specialists—Call Center

representatives with specially trained

in counseling participants on financial

issues–also through in-person

meetings

Benefit Statements—Electronic or

paper statement of current and

projected amounts.

Projection Tools—Modeling and

what-if scenarios, including

aggregation across accounts.

Plan Efficiency—Plan sponsor

assessment of overall plan, fund, and

participant performance over time

Retirement Checklists—A guide for

those approaching retirement, including

references and links to helpful resources

Guidance and Advice—Tools and

advisors designed specifically to provide

decision support for investments, deferral

amounts, timing, and more

Income Solutions—Leverage institutional

plan structure/funds to provide lifetime

income alternatives to plan participants

Motivating Employees to Take

Action

16

Help People…Improve Their Financial Future

Create the Foundation

Create a

brand/theme

Analyze the

workforce

Define tools

and resources

Use multiple

channels

Target specific

actions

Promote what

you have

Motivate Action

17 Retirement Webinar Series | May 29, 2013

Push to Encourage Action

Inertia

Bias for status quo

Temporal Discounting

Present vs. Future

Choices

Liberation or Paralysis?

Loss Aversion

Losing hurts worse than winning feels good

Social Norms

What is everyone else doing?

1

3

4

5

2

People may need a “nudge” to help them take action.

18 Retirement Webinar Series | May 29, 2013

Customer Preferences Define Approach

19 Retirement Webinar Series | May 29, 2013

Gamification Modeling Tools

Are you on track to retire?

• How old are you?

• How much do you earn?

Personalized

Communication

Benefits Hubs Flash/Video

Attitudinal Segmentation

20 Retirement Webinar Series | May 29, 2013

Driving Behaviors and Outcomes

Case Study—Kimberly-Clark

Alisa Hunt

21

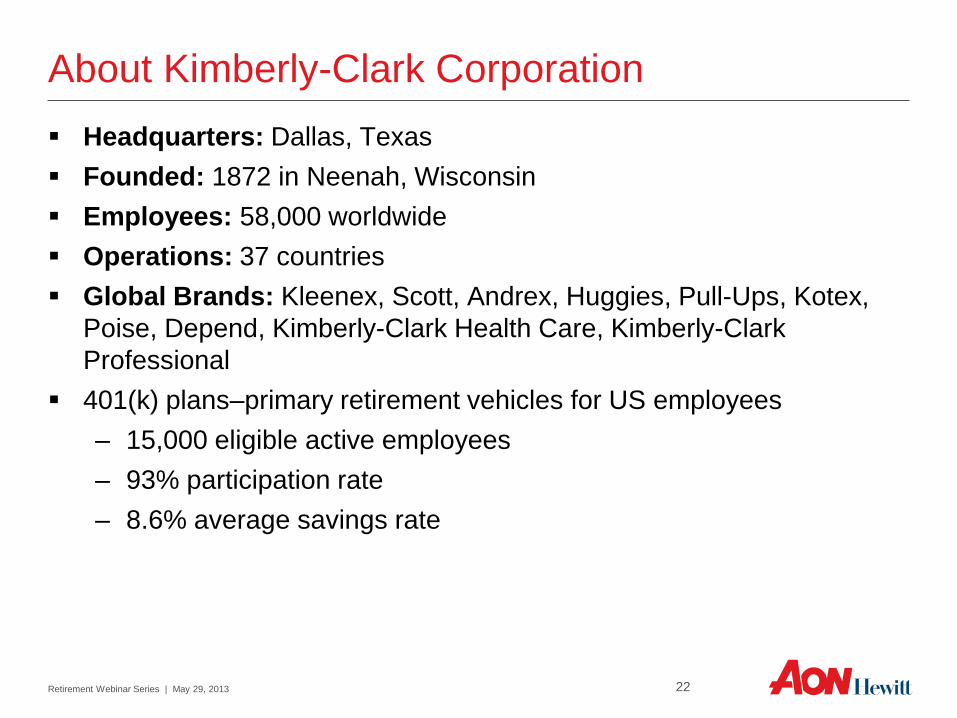

About Kimberly-Clark Corporation

Headquarters: Dallas, Texas

Founded: 1872 in Neenah, Wisconsin

Employees: 58,000 worldwide

Operations: 37 countries

Global Brands: Kleenex, Scott, Andrex, Huggies, Pull-Ups, Kotex,

Poise, Depend, Kimberly-Clark Health Care, Kimberly-Clark

Professional

401(k) plans–primary retirement vehicles for US employees

– 15,000 eligible active employees

– 93% participation rate

– 8.6% average savings rate

22 Retirement Webinar Series | May 29, 2013

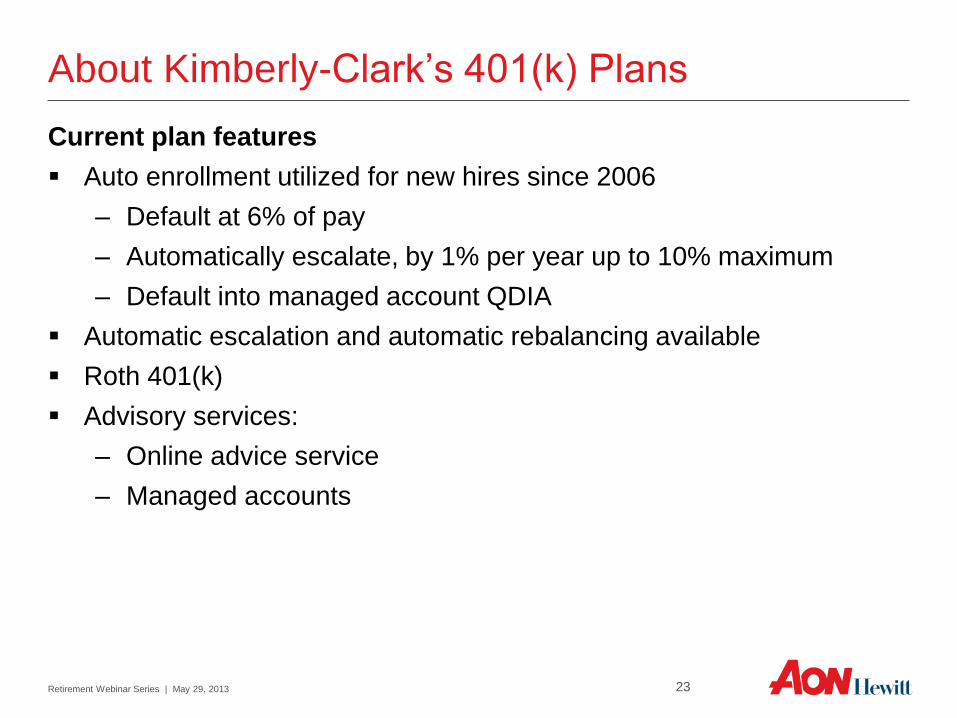

About Kimberly-Clark’s 401(k) Plans

Current plan features

Auto enrollment utilized for new hires since 2006

– Default at 6% of pay

– Automatically escalate, by 1% per year up to 10% maximum

– Default into managed account QDIA

Automatic escalation and automatic rebalancing available

Roth 401(k)

Advisory services:

– Online advice service

– Managed accounts

23 Retirement Webinar Series | May 29, 2013

Poster

Engaging Employees—401(k) Month

24

Postcard

Sticky Note

Table Tent

Retirement Webinar Series | May 29, 2013

Engaging Employees—401(k) Month

25

Microsite Videos

Weekly Emails

Benefits Site

Retirement Webinar Series | May 29, 2013

Results

Email Open Rate 65%-77%

Video Views 7,724

Saving Activity TBD

Survey Results TBD

Retirement Webinar Series | May 29, 2013 26

Microsite Usage

Questions & Answers

27

Retirement Webinar Series

June 26

The Empowered Fiduciary of Defined Contribution Plans

Register at www.aon.com/ah_retirementwebinars

28

29

Contact Us

Byron Beebe

U.S. Retirement Market Leader

Aon Hewitt

(216) 525.5362

Virginia Maguire

Director, Product Strategy

Aon Hewitt

(404) 291.1383

Rob Reiskytl

Leader of Retirement Strategy and Design

Aon Hewitt

(952) 807.0843

Retirement Webinar Series | May 29, 2013

30

About Aon Hewitt

Aon Hewitt empowers organizations and individuals to secure a better future through

innovative talent, retirement and health solutions. We advise, design and execute a wide

range of solutions that enable clients to cultivate talent to drive organizational and personal

performance and growth, navigate retirement risk while providing new levels of financial

security, and redefine health solutions for greater choice, affordability and wellness. Aon

Hewitt is the global leader in human resource solutions, with over 30,000 professionals in

90 countries serving more than 20,000 clients worldwide. For more information on Aon

Hewitt, please visit www.aonhewitt.com.

© 2013 Aon plc

This document is intended for general information purposes only and should not be construed as advice or opinions on

any specific facts or circumstances. The comments in this summary are based upon Aon Hewitt's preliminary analysis of

publicly available information. The content of this document is made available on an “as is” basis, without warranty of any

kind. Aon Hewitt disclaims any legal liability to any person or organization for loss or damage caused by or resulting from

any reliance placed on that content. Aon Hewitt reserves all rights to the content of this document.

Retirement Webinar Series | May 29, 2013

Related Documents