©2008 Pearson Prentice Hall. All rights reserved. 4-1 Internal Control & Cash Chapter 4

©2008 Pearson Prentice Hall. All rights reserved. 4-1 Internal Control & Cash Chapter 4.

Dec 23, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

©2008 Pearson Prentice Hall. All rights reserved.

4-1

Internal Control & Cash

Chapter 4

©2008 Pearson Prentice Hall. All rights reserved.

4-2

Internal Control - Objectives

• Safeguard assets

• Encourage employees to follow company policy

• Promote operational efficiency

• Ensure accurate, reliable accounting records

• Comply with legal requirements

©2008 Pearson Prentice Hall. All rights reserved.

4-3

Sarbanes-Oxley Act (SOX)

• Accounting scandals shook the public’s confidence in the accounting profession Enron and WorldCom overstated profits Auditors Arthur Anderson went out of

business

• In response, Congress passed SOX Established new provisions for how large

corporations are audited

©2008 Pearson Prentice Hall. All rights reserved.

4-4

Learning Objective 1

Set up an internal control system

©2008 Pearson Prentice Hall. All rights reserved.

4-5

Control Environment Tone set “at the top”

Top management should set good example for employees

Information SystemProvides accurate information to keep track of

assets and measure income

Risk assessment Identify risks in the business environment

Control Procedures Ensure goals are achieved

Monitoring of ControlsAuditors make sure controls are working

©2008 Pearson Prentice Hall. All rights reserved.

4-6

Internal Control Procedures

• Competent, reliable and ethical employees Staff should be trained and fairly rewarded for

its work

• Assignment of Responsibilities Job descriptions should be clear

• Separation of Duties Operations from accounting Custody of assets from accounting

©2008 Pearson Prentice Hall. All rights reserved.

4-7

Internal Control Procedures

• Audits Internal or External

• Documents

• Electronic Devices

• Other controls Fireproof vaults for important documents Bonds on employees who handle cash Mandatory vacations and job rotation

©2008 Pearson Prentice Hall. All rights reserved.

4-8

Internal Controls for E-Commerce

• Risks of online business Stolen credit cards Computer viruses Phishing

• Security measures Encryption Firewalls

©2008 Pearson Prentice Hall. All rights reserved.

4-9

Limitations of Internal Control

• Collusion Two people working together can circumvent

system

• Cost Company must weigh the benefits of controls

with the cost

©2008 Pearson Prentice Hall. All rights reserved.

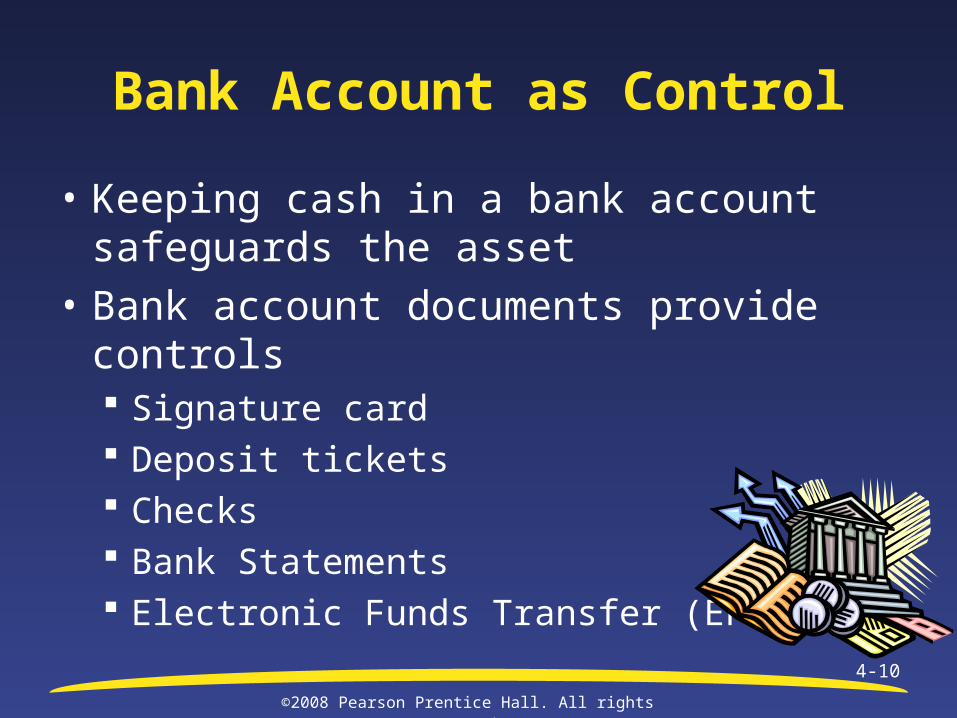

4-10

Bank Account as Control

• Keeping cash in a bank account safeguards the asset

• Bank account documents provide controls Signature card Deposit tickets Checks Bank Statements Electronic Funds Transfer (EFT)

©2008 Pearson Prentice Hall. All rights reserved.

4-11

Learning Objective 2

Prepare and use a bank reconciliation as a control device

©2008 Pearson Prentice Hall. All rights reserved.

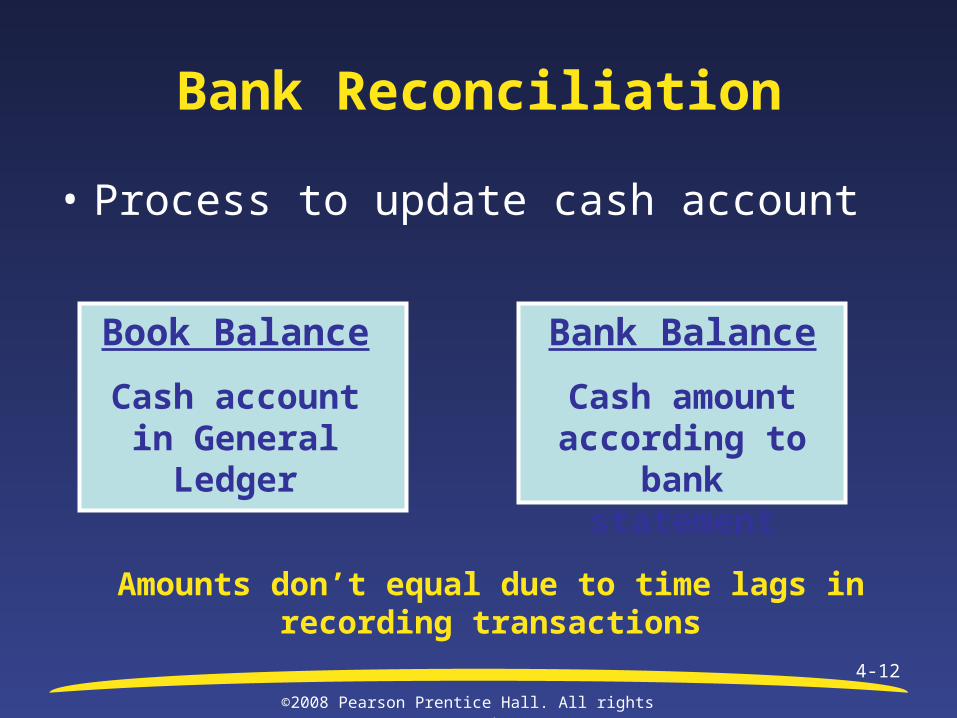

4-12

Bank Reconciliation

• Process to update cash account

Book Balance

Cash account in General Ledger

Bank Balance

Cash amount according to

bank statement

Amounts don’t equal due to time lags in recording transactions

©2008 Pearson Prentice Hall. All rights reserved.

4-13

Bank balance

Add: Deposits in transit

Subtract: Outstanding checks

Add or Subtract: Bank errors

Equals: Adjusted Cash Balance

Book balance

Subtract: EFT payments, service charges, NSF checks

Add: Bank collections & Interest revenue

Add or Subtract: Book errors

Equals: Adjusted Cash Balance

Preparing a Bank Reconciliation

©2008 Pearson Prentice Hall. All rights reserved.

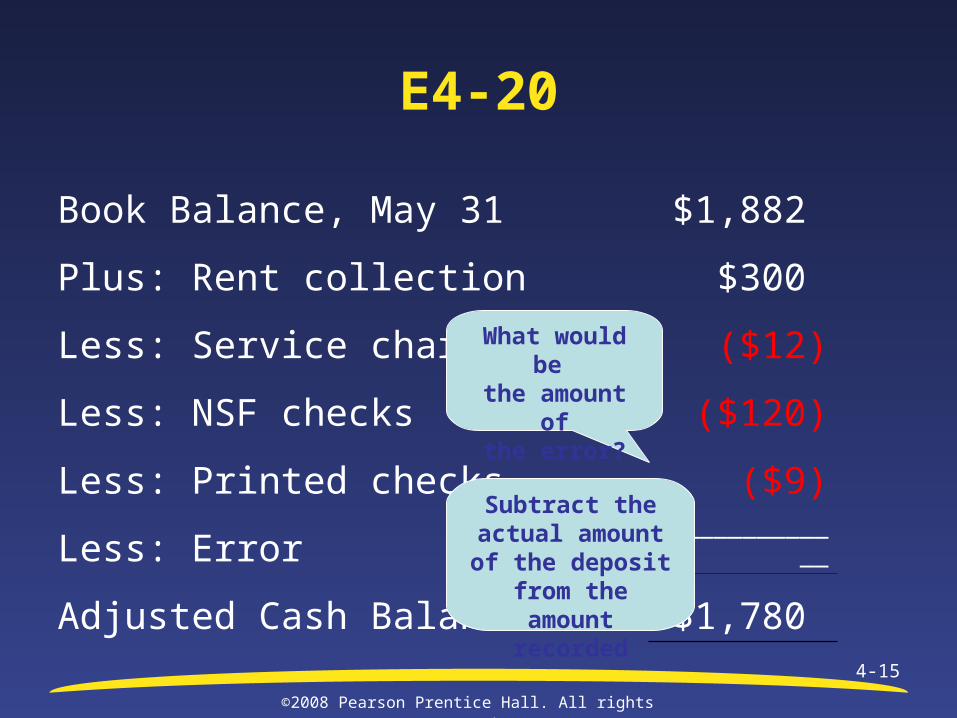

4-14

E4-20

Bank Balance, May 31 $595

Plus: deposit in transit $1,788

Less: outstanding checks ($603)

Adjusted Cash Balance $1,780

©2008 Pearson Prentice Hall. All rights reserved.

4-15

E4-20

Book Balance, May 31 $1,882

Plus: Rent collection $300

Less: Service charge ($12)

Less: NSF checks ($120)

Less: Printed checks ($9)

Less: Error____________

_

Adjusted Cash Balance $1,780

What would be the amount of

the error?

Subtract the actual amount of the deposit from

the amount recorded

©2008 Pearson Prentice Hall. All rights reserved.

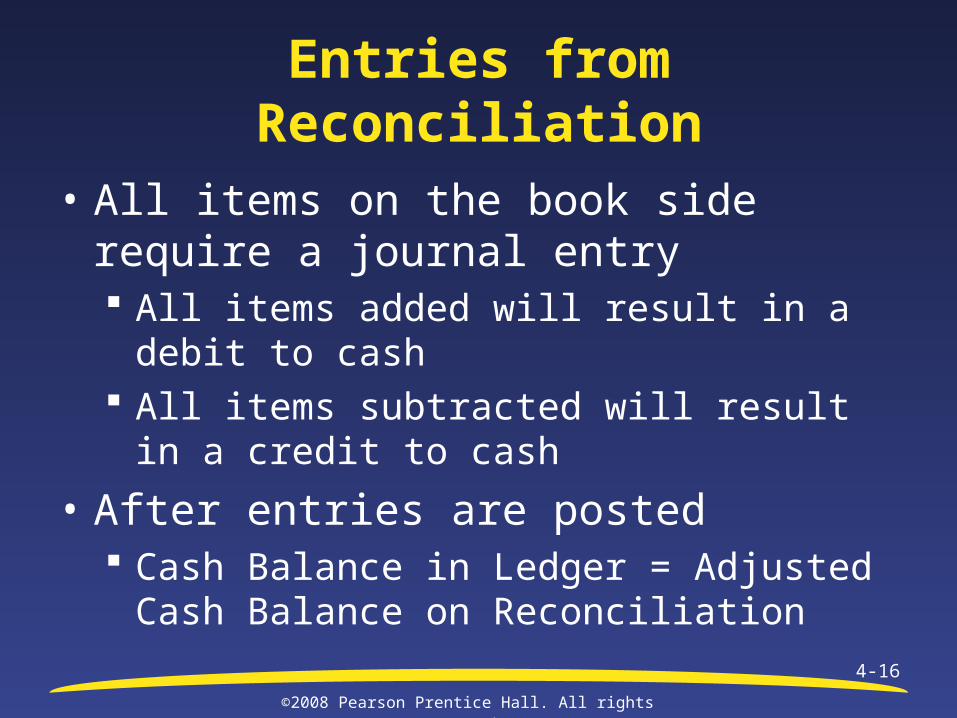

4-16

Entries from Reconciliation

• All items on the book side require a journal entry All items added will result in a debit to cash All items subtracted will result in a credit to

cash

• After entries are posted Cash Balance in Ledger = Adjusted Cash

Balance on Reconciliation

©2008 Pearson Prentice Hall. All rights reserved.

4-17

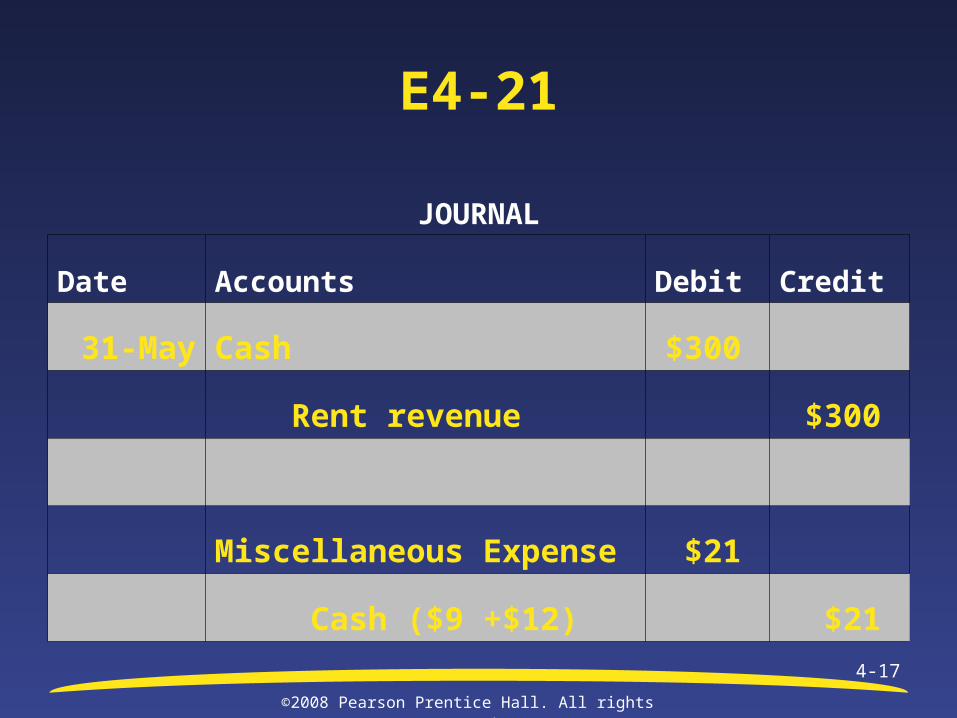

E4-21

JOURNAL

Date Accounts Debit Credit

31-May Cash $300

Rent revenue $300

Miscellaneous Expense $21

Cash ($9 +$12) $21

©2008 Pearson Prentice Hall. All rights reserved.

4-18

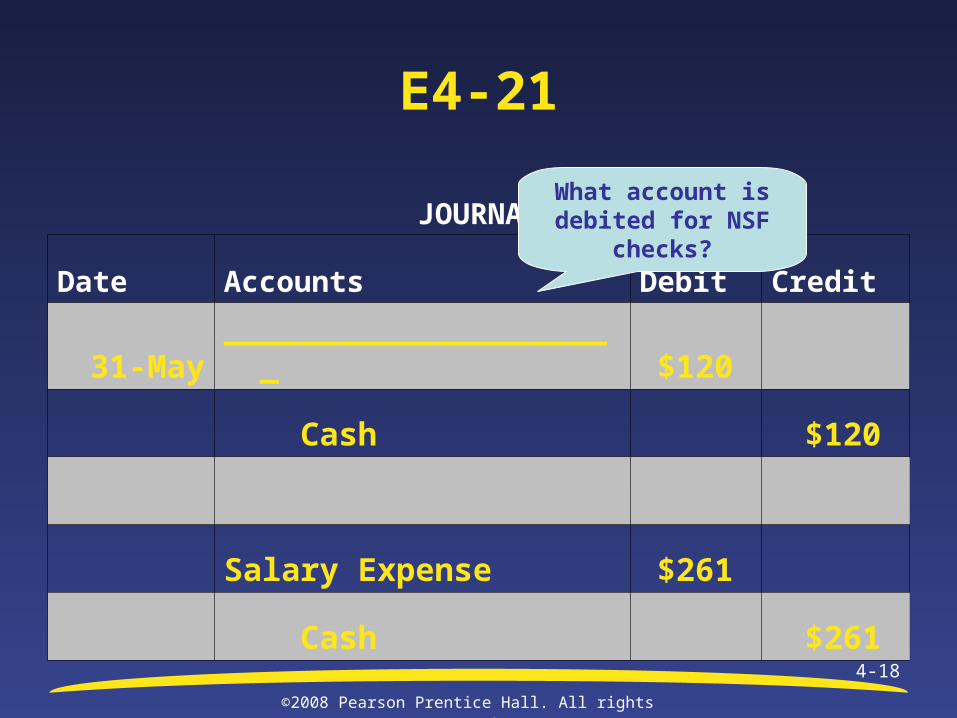

E4-21

JOURNAL

Date Accounts Debit Credit

31-May _____________________ $120

Cash $120

Salary Expense $261

Cash $261

What account is debited for NSF

checks?

©2008 Pearson Prentice Hall. All rights reserved.

4-19

Learning Objective 3

Apply internal controls to cash receipts and cash payments

©2008 Pearson Prentice Hall. All rights reserved.

4-20

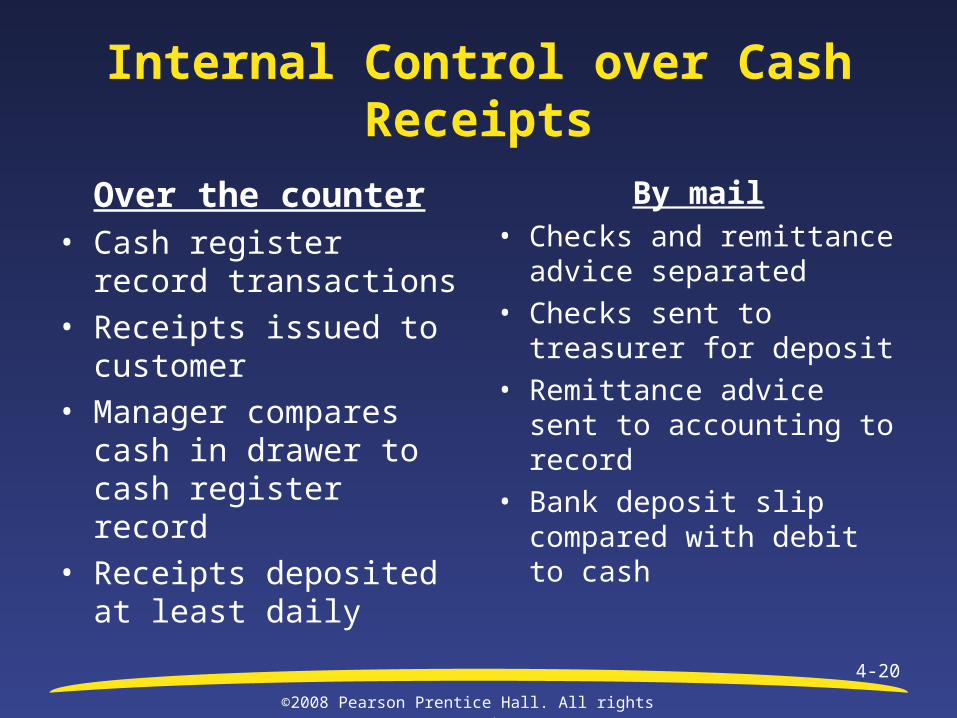

Internal Control over Cash Receipts

Over the counter• Cash register record

transactions• Receipts issued to

customer• Manager compares cash

in drawer to cash register record

• Receipts deposited at least daily

By mail• Checks and remittance

advice separated • Checks sent to treasurer

for deposit• Remittance advice sent to

accounting to record• Bank deposit slip

compared with debit to cash

©2008 Pearson Prentice Hall. All rights reserved.

4-21

Internal Control Over Cash Payments

• Payment by check Provides record of payment Must be signed by authorized official Official should study evidence supporting

payment

©2008 Pearson Prentice Hall. All rights reserved.

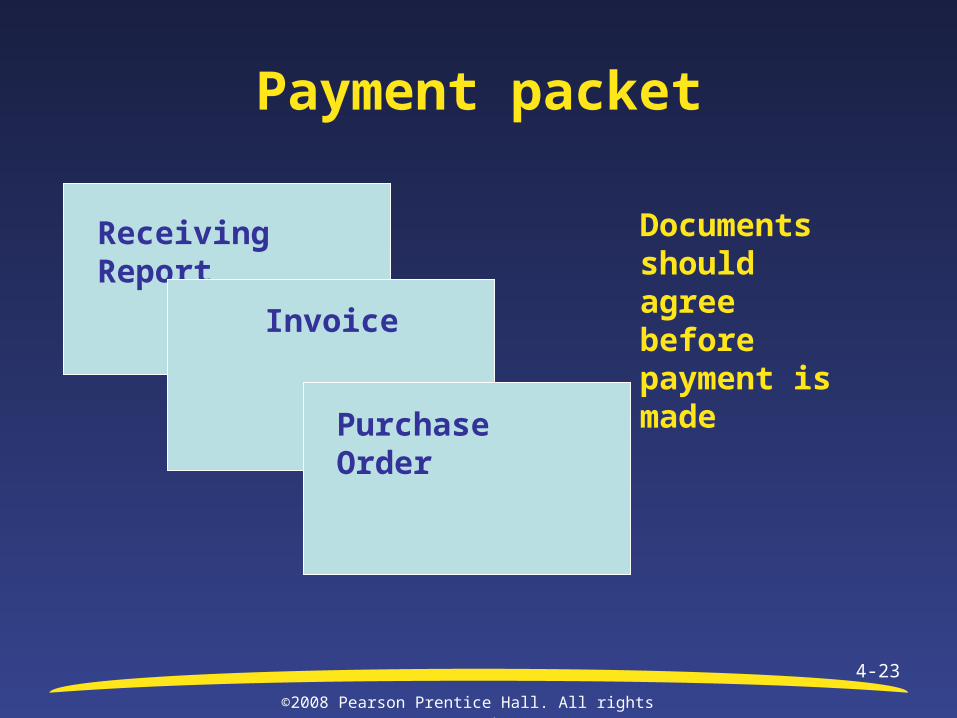

4-22

Documents Used to Control Purchases

• Purchase order Prepared by purchasing company to place

order

• Invoice Prepared by selling company to list items sent

and to request payment

• Receiving report Prepared by purchasing company to show

that goods were received

©2008 Pearson Prentice Hall. All rights reserved.

4-23

Payment packet

Receiving Report

Invoice

Purchase Order

Documents should agree before payment is made

©2008 Pearson Prentice Hall. All rights reserved.

4-24

Separation of Duties

• Responsibilities should be split: Purchasing goods Receiving goods Approving and paying for goods

©2008 Pearson Prentice Hall. All rights reserved.

4-25

Petty Cash

• Small amount of cash kept on hand for incidental purchases

• Fund is established at a set amount

• Custodian of fund prepares ticket that lists each item purchased

• Tickets plus remaining cash should equal fund balance

©2008 Pearson Prentice Hall. All rights reserved.

4-26

Learning Objective 4

Use a budget to manage your cash

©2008 Pearson Prentice Hall. All rights reserved.

4-27

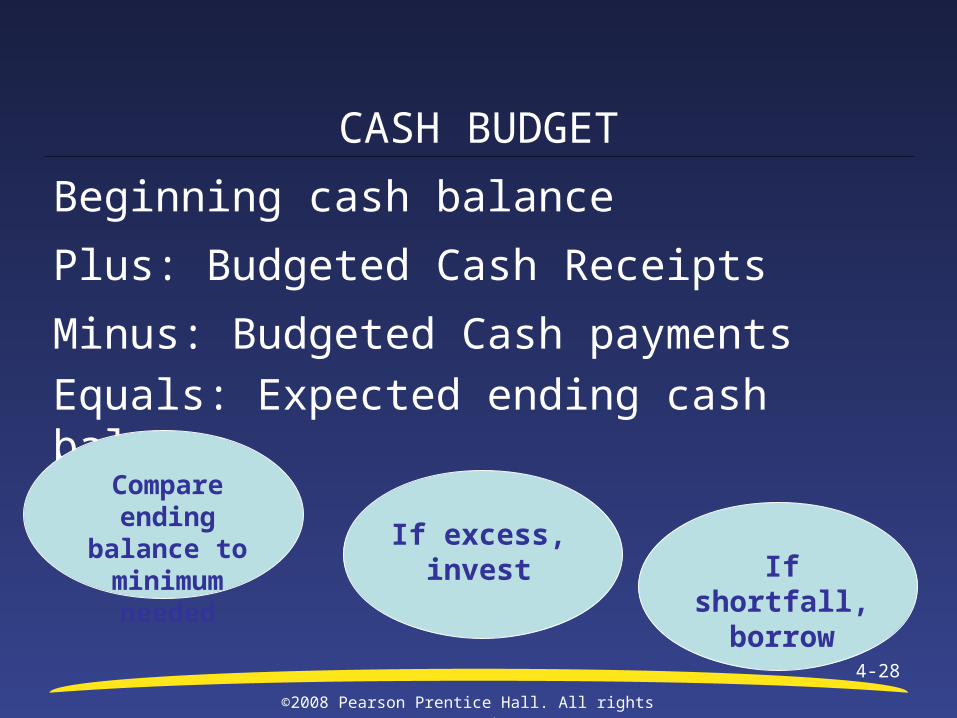

Budget

• Financial plan that helps coordinate business activities

• A cash budget helps a company manage cash by planning receipts and payments

©2008 Pearson Prentice Hall. All rights reserved.

4-28

CASH BUDGET

Beginning cash balance

Plus: Budgeted Cash Receipts

Minus: Budgeted Cash payments

Equals: Expected ending cash balance

Compare ending balance to

minimum needed If excess, invest If shortfall,

borrow

©2008 Pearson Prentice Hall. All rights reserved.

4-29

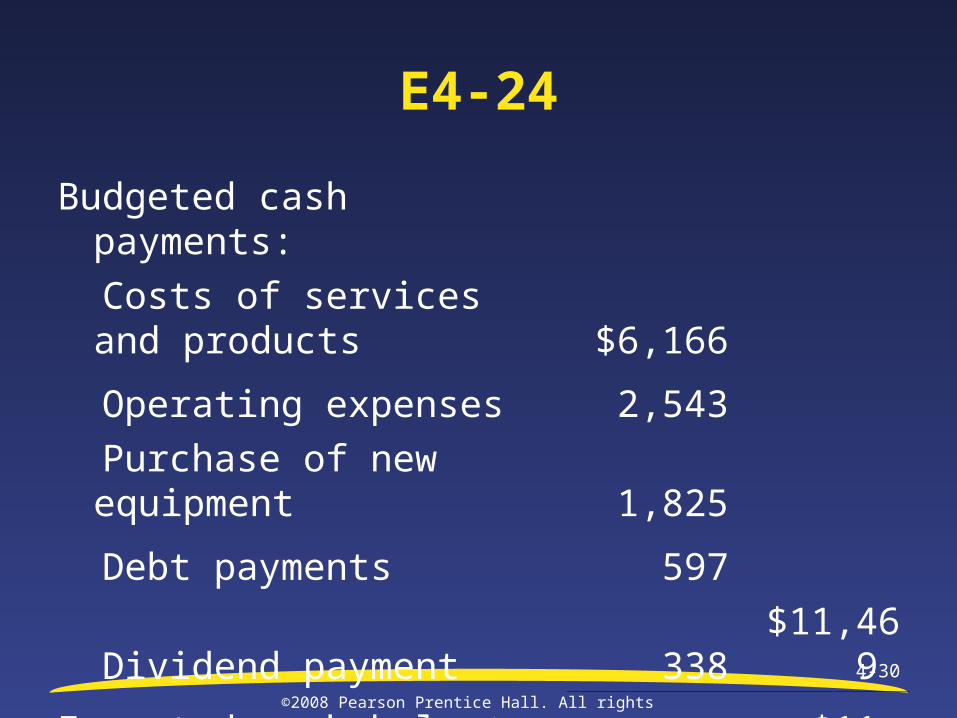

E4-24

Cash Budget 20X8

Beginning cash balance $81

Budgeted cash receipts:

Cash collections from customers $11,284

Sale of equipment 115 $11,399

©2008 Pearson Prentice Hall. All rights reserved.

4-30

E4-24

Budgeted cash payments:

Costs of services and products $6,166

Operating expenses 2,543

Purchase of new equipment 1,825

Debt payments 597

Dividend payment 338 $11,469

Expected cash balance $11

©2008 Pearson Prentice Hall. All rights reserved.

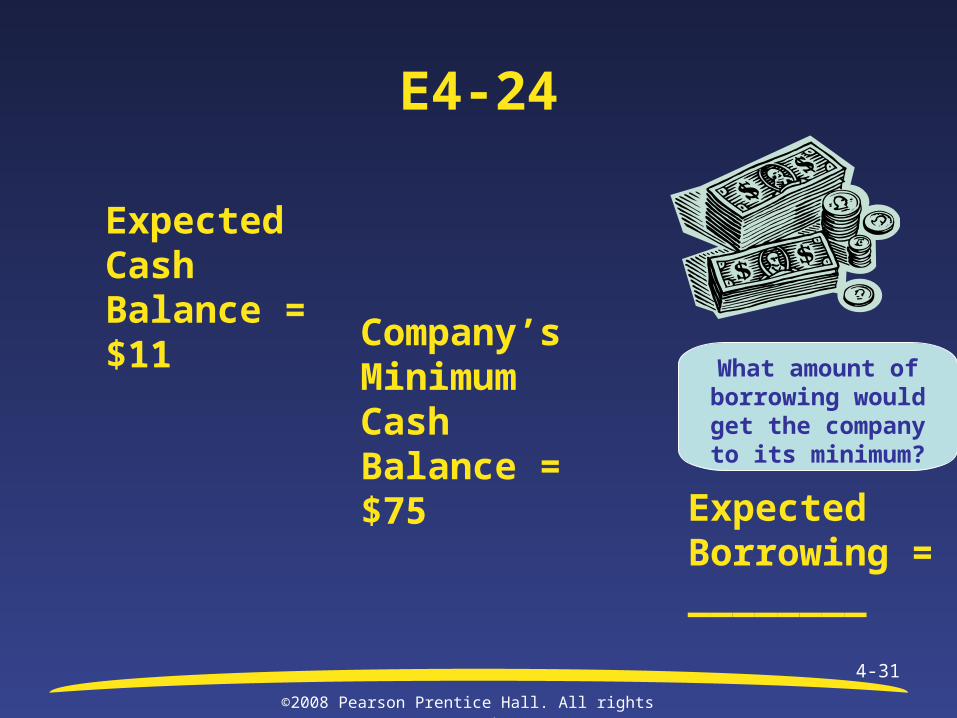

4-31

E4-24

Expected Cash Balance = $11

Company’s Minimum Cash Balance = $75

Expected Borrowing = ________

What amount of borrowing would get the company to its

minimum?

©2008 Pearson Prentice Hall. All rights reserved.

4-32

Learning Objective 5

Make ethical business judgments

©2008 Pearson Prentice Hall. All rights reserved.

4-33

Codes of Ethics

• Most companies have a code of ethics

• Owners and managers must set an ethical tone as well

• The accounting profession is expected to maintain higher standards AICPA Code of Professional Conduct Standards of Ethical Conduct for Management

Accountants

©2008 Pearson Prentice Hall. All rights reserved.

4-34

Ethical Issues in Accounting

• Pressure often exists for managers to reach earnings or stock price goals

• Earnings can be manipulated by Understating expenses Overstating revenues

• Use Framework for Making Ethical Judgments

©2008 Pearson Prentice Hall. All rights reserved.

4-35

Framework for Ethical Judgments

• Identify the ethical issue

• Specify the alternatives

• Assess the possible outcomes

• Make the decision

©2008 Pearson Prentice Hall. All rights reserved.

4-36

End of Chapter Four

Related Documents