©2008 Pearson Prentice Hall. All rights reserved. 12-1 The Statement of Cash Flows Chapter 12

©2008 Pearson Prentice Hall. All rights reserved. 12-1 The Statement of Cash Flows Chapter 12.

Dec 29, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

©2008 Pearson Prentice Hall. All rights reserved.12-1

The Statement of Cash Flows

Chapter 12

©2008 Pearson Prentice Hall. All rights reserved.12-2

Learning Objective 1

Identify the purpose the statement of

cash flows

©2008 Pearson Prentice Hall. All rights reserved.12-3

Cash Flow Statement

• Shows cash receipts and payments during a period

• Purposes: Predicts future cash flows Evaluates management decisions Determines ability to pay dividends and

interest Shows relationship of net income to cash

flows

©2008 Pearson Prentice Hall. All rights reserved.12-4

Importance of Cash Flow

A company needs both net income and strong cash flow to succeed

©2008 Pearson Prentice Hall. All rights reserved.12-5

Learning Objective 2

Distinguish among operating, investing and financing cash flows

©2008 Pearson Prentice Hall. All rights reserved.12-6

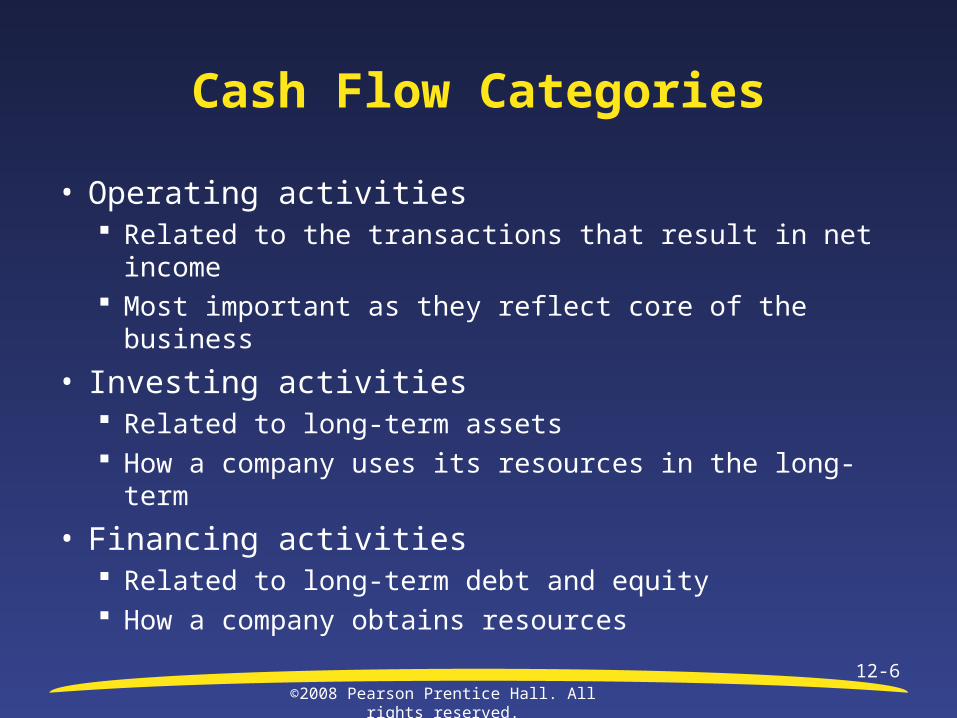

Cash Flow Categories

• Operating activities Related to the transactions that result in net income Most important as they reflect core of the business

• Investing activities Related to long-term assets How a company uses its resources in the long-term

• Financing activities Related to long-term debt and equity How a company obtains resources

©2008 Pearson Prentice Hall. All rights reserved.12-7

Formats for Operating Cash Flows

• Indirect Reconciles net income to cash provided by

operating activities Easier to prepare

• Direct Shows cash inflows and outflows by type Easier to interpret

©2008 Pearson Prentice Hall. All rights reserved.12-8

Learning Objective 3

Prepare a statement of cash flows by the indirect method

©2008 Pearson Prentice Hall. All rights reserved.12-9

The Indirect Method

Net Income

Reconciling adjustments:

+ Depreciation/depletion/amortization

+ Losses on sales of long-term assets

- Gains on sales of long-term assets

+ or - changes in current assets & current liabilities

Net cash provided by operating activities

©2008 Pearson Prentice Hall. All rights reserved.12-10

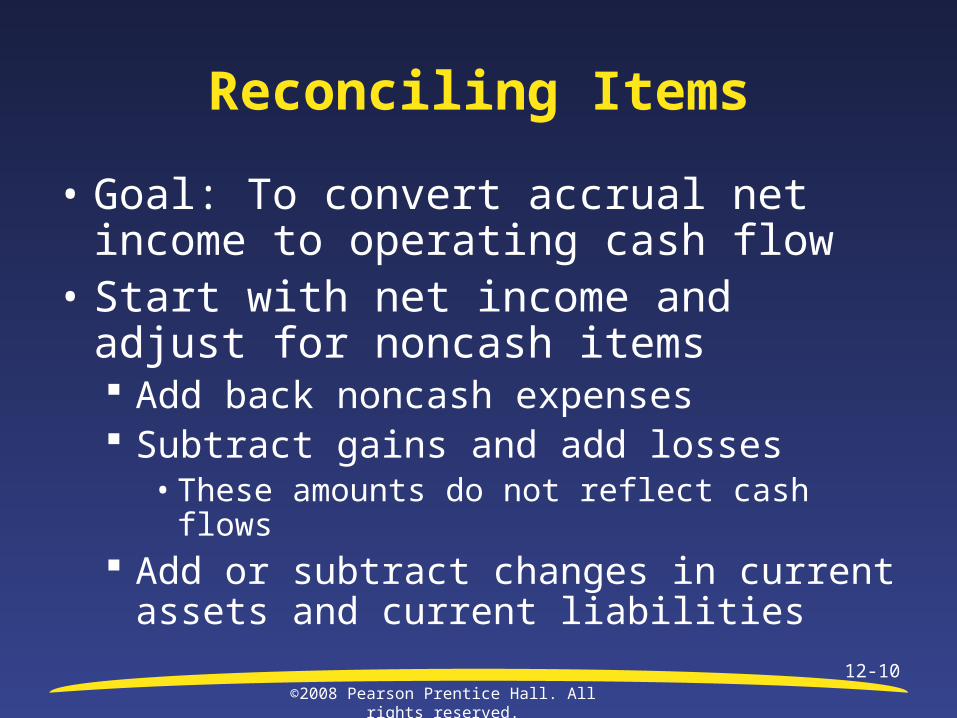

Reconciling Items

• Goal: To convert accrual net income to operating cash flow

• Start with net income and adjust for noncash items Add back noncash expenses Subtract gains and add losses

• These amounts do not reflect cash flows Add or subtract changes in current assets and

current liabilities

©2008 Pearson Prentice Hall. All rights reserved.12-11

Current Assets and Current Liabilities

• Each account relates to an income statement item Accounts receivable Sales Salaries payable Salaries expense

• The change in each account is computed Change = Current year balance – prior year balance

• Current assets inverse relationship Subtract increases from net income; add decreases

• Current liabilities direct relationship Add increases to net income; subtract decreases

©2008 Pearson Prentice Hall. All rights reserved.

12-12

E12-15

Item O I or F + or -

a. Net Income O +

b. Cash dividend F -

c. Sale of LT investment I +

d. Loss on sale of equip. O +

e. Amortization O +

f. Issuance of LTNP F +

g. Depreciation expense O +

h. Issuance of stock ___ +

What type of account is

stock?

©2008 Pearson Prentice Hall. All rights reserved.

12-13

E12-15Item O I or F + or -

j. Increase in accts pay O +

k. Purchase of equipment with note payable

NIF

l. Payment of long-term debt

F -

m. Purchase building I -

n. Accrual of salary expense N

o. Purchase of long-term investment

I -

©2008 Pearson Prentice Hall. All rights reserved.

12-14

E12-15

Item O I or F + or -

p. Decrease in inventory O +

q. Increase in prepaid expenses

O -

r. Sale of land I +

s. Decrease in accrued liabilities

O -

©2008 Pearson Prentice Hall. All rights reserved.12-15

Preparing the Operating Section – Indirect Method

• Use current year income statement for the following amounts Net Income Depreciation, depletion and amortization

expense Gains or losses on sales of assets

• Use comparative balance sheets to compute the changes in current assets and current liabilities

©2008 Pearson Prentice Hall. All rights reserved.12-16

The Indirect Method

Revenues 100,000$ Cost of Goods Sold 40,000 Gross Profit 60,000 Operating expenses:

Salaries expense 20,000 Depreciation expense 10,000 Other expenses 5,000

Total operating expenses 35,000 Other income: Gain on sale of plant assets 3,000 Net Income 38,000$

Income Statement

Use as first line in operating section

Add back to net income

Subtract from net income

©2008 Pearson Prentice Hall. All rights reserved.12-17

12-31-09 12-31-08 ChangeCash 20,000$ 18,000$ Accounts Receivable 25,000 30,000 (5,000) Inventory 42,000 30,000 12,000 Long-term assets 150,000 162,000 Total assets 237,000$ 240,000$ Accounts payable 15,000 18,000 (3,000) Salaries payable 10,000 6,000 4,000 Long-term liabilities 98,000 105,000 Stockholders' equity 114,000 111,000 Total liabilities & equity 237,000$ 240,000$

Comparative Balance Sheets December 31, 2009 and 2008

Added to net income

Subtracted from net income

Added to net income

Subtracted from net income

©2008 Pearson Prentice Hall. All rights reserved.12-18

E12-17

Net Income $ 35,000

Reconciling items:

Depreciation 18,000

Loss on sale of land 5,000

Changes in current assets & current liabilities

Increase in current assets _______

Decrease in current liabilities (20,000)

Net cash provided by operating activities $ 11,000

Remember: inverse

relationship

©2008 Pearson Prentice Hall. All rights reserved.12-19

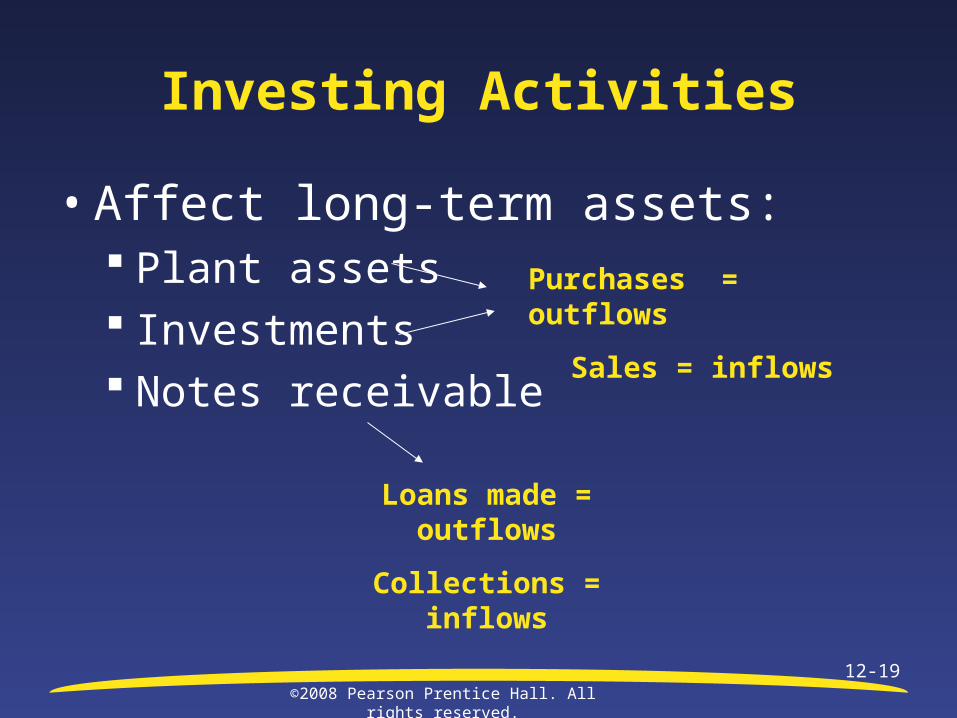

Investing Activities

• Affect long-term assets: Plant assets Investments Notes receivable

Purchases = outflows

Sales = inflows

Loans made = outflows

Collections = inflows

©2008 Pearson Prentice Hall. All rights reserved.12-20

Computing Purchases and Sales of Plant Assets

Plant assets, net, beginning balance

+ Acquisitions

- Depreciation

- Book value of assets sold

= Plant assets, net, ending balance

From Balance Sheet

From Balance Sheet

From Income Statement

©2008 Pearson Prentice Hall. All rights reserved.12-21

Proceeds from Sales of Plant Assets

• Compare book value of assets sold to gain or loss Gain or loss located on income statement

Book value + Gain on sale

Book value – Loss on sale

Cash Proceeds

©2008 Pearson Prentice Hall. All rights reserved.12-22

Computing Purchases and Sales of Investments

Investments, beginning balance

+ Purchases

- Cost of investments sold

= Investments, ending balance

Cost + Gain on sale

Cost – Loss on sale

Cash Proceeds

To compute cash proceeds of investments sold:

©2008 Pearson Prentice Hall. All rights reserved.12-23

Computing Loans Made and Collections on Notes

Notes receivable, beginning balance

+ Loans made

- Collections

= Notes receivable, ending balance

©2008 Pearson Prentice Hall. All rights reserved.12-24

Financing Activities

• Affect long-term liabilities & equity: Long-term Debt

• Notes payable• Bonds payable

Common stock and Paid-in Capital Retained earnings

Payments = outflows Borrowings = inflows

Cash dividends = outflows Issuance of new shares = inflows

©2008 Pearson Prentice Hall. All rights reserved.12-25

Computing Issuance and Payments of Long-Term Debt

Long-term debt, beginning balance

+ Issuance of new debt

- Payments of debt

= Long-term debt, ending balance

©2008 Pearson Prentice Hall. All rights reserved.12-26

Computing Issuance of Stock and Purchases of Treasury Stock

Common stock, beginning balance

+ Issuance of new stock

= Common stock, ending balance

Treasury stock, beginning balance

+ Purchase of treasury stock

= Treasury stock, ending balance

Inflow of cash

Outflow of cash

©2008 Pearson Prentice Hall. All rights reserved.12-27

Computing Dividend Payments

Retained earnings, beginning balance

+ Net Income

- Dividends declared

= Retained earnings, ending balance

From income statement

©2008 Pearson Prentice Hall. All rights reserved.12-28

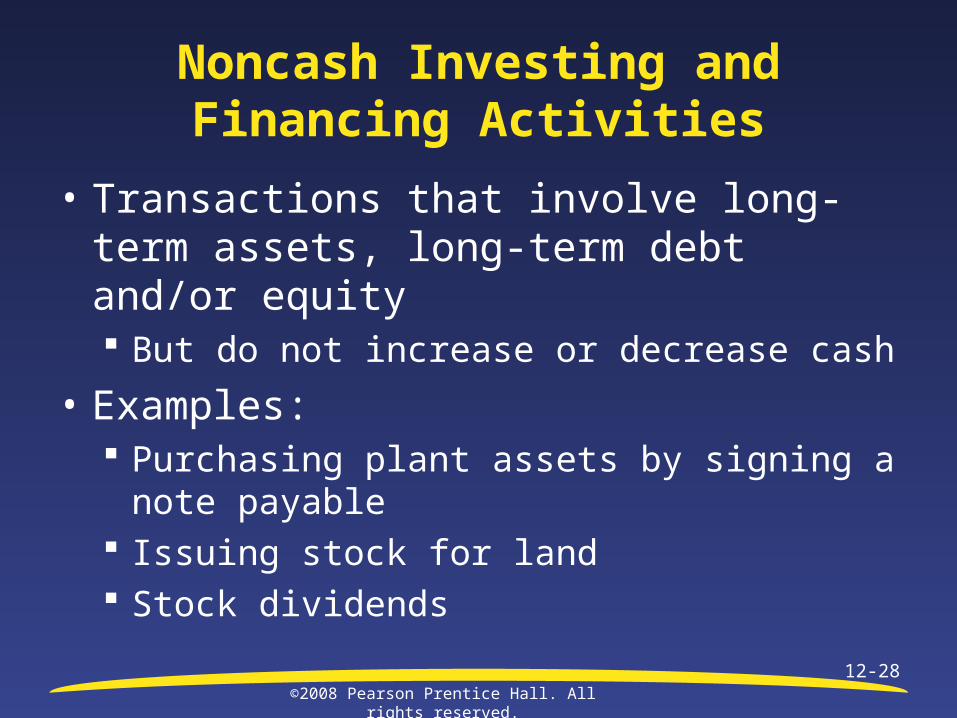

Noncash Investing and Financing Activities

• Transactions that involve long-term assets, long-term debt and/or equity But do not increase or decrease cash

• Examples: Purchasing plant assets by signing a note

payable Issuing stock for land Stock dividends

©2008 Pearson Prentice Hall. All rights reserved.12-29

Cash flows from operating activities:Net IncomeReconciling adjustments: + Depreciation/depletion/amortization + Losses on sales of long-term assets - Gains on sales of long-term assets + or - changes in current assets & current liabilities

Net cash provided by operating activitiesCash flows from investing activities:

Purchase of plant assets & investmentsSale of plant assets & investments

Net cash provided by investing activitiesCash flows from financing activities:

Issuance of stockPayment of dividendsIssuance of long-term note payable Purchase of treasury stock

Net cash provided by financing activitiesNet increase (decrease) in cash

Cash balance, beginning of yearCash balance, end of year

Statement of Cash Flows

Proves that cash flow statement “works”

©2008 Pearson Prentice Hall. All rights reserved.12-30

Learning Objective 4

Prepare a cash flow statement by the direct method

©2008 Pearson Prentice Hall. All rights reserved.12-31

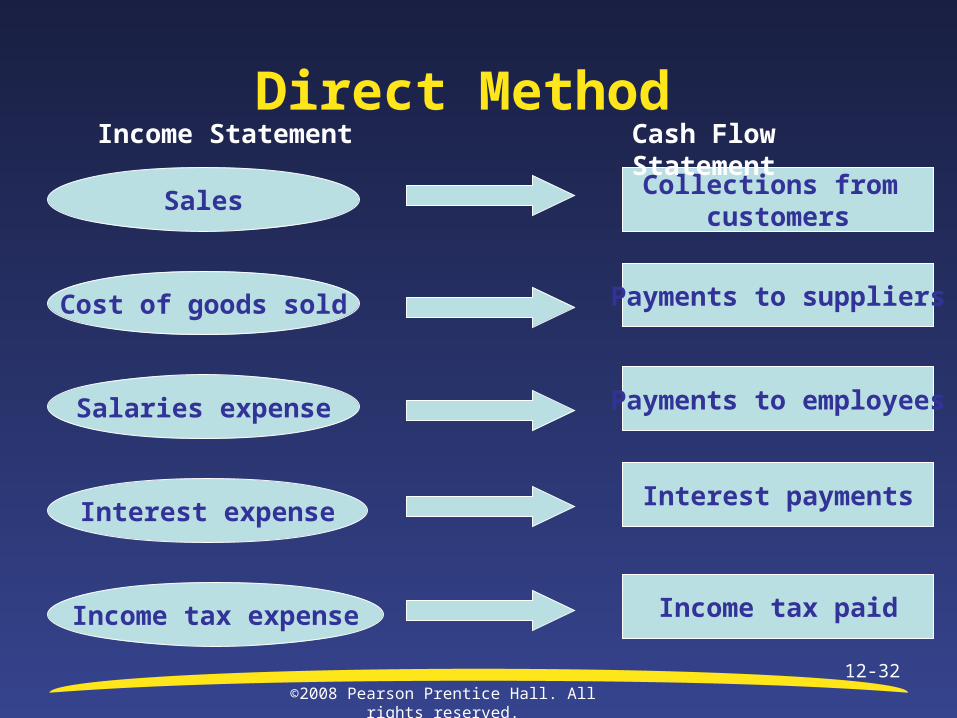

Direct Method

• FASB prefers as it provides clearer information Rarely used as it requires more calculations

• Refers to how operating section is prepared Investing and Financing activities always prepared

using the direct method

• Goal: Convert each income statement item into a cash amount Or exclude if a noncash item

©2008 Pearson Prentice Hall. All rights reserved.12-32

Direct Method

Collections from customers

Sales

Cost of goods sold Payments to suppliers

Salaries expense Payments to employees

Interest expenseInterest payments

Income Statement Cash Flow Statement

Income tax expense Income tax paid

©2008 Pearson Prentice Hall. All rights reserved.12-33

Direct Method Formulas

RECEIPTS

Income Statement

Balance Sheet Change

From customers

Sales

+ Decrease in accounts receivable

- Increase in accounts receivable

Of interest Interest revenue

+ Decrease in interest receivable

- Increase in interest receivable

©2008 Pearson Prentice Hall. All rights reserved.12-34

Direct Method Formulas

PAYMENTS

Income Statement

Balance Sheet Change

To suppliers Cost of goods sold

+ Increase in inventory

- Decrease in inventory

AND

+ Decrease in accounts Payable

- Increase in accounts payable

©2008 Pearson Prentice Hall. All rights reserved.12-35

Direct Method Formulas

PAYMENTS

Income Statement

Balance Sheet Change

For expenses

Operating expenses

+ Increase in prepaid

- Decrease in prepaids

OR

+ Decrease in accrued liabilities

- Increase in accrued liabilities

©2008 Pearson Prentice Hall. All rights reserved.12-36

Direct Method Formulas

PAYMENTS

Income Statement

Balance Sheet Change

To employees

Salaries expense

+ Decrease in salaries payable

- Increase in salaries payable

For interest Interest expense

+ Decrease in interest payable

- Increase in interest payable

©2008 Pearson Prentice Hall. All rights reserved.12-37

Direct Method Formulas

PAYMENTS

Income Statement

Balance Sheet Change

For income taxes

Income tax expense

+ Decrease in income tax payable

- Increase in income tax payable

©2008 Pearson Prentice Hall. All rights reserved.12-38

E12-27

Credit sales $60,000

Ending accounts receivable 32,000

Beginning accounts receivable 22,000

Increase in accounts receivable 10,000

Collections from customers

If more customers buy on account, how would that

affect cash flow?

Add or subtract?

©2008 Pearson Prentice Hall. All rights reserved.12-39

E12-27

Cost of goods sold $111,000

Ending inventory 21,000

Beginning inventory 24,000

Decrease in inventory (3,000)

Ending accounts payable 8,000

Beginning accounts payable 14,000

Decrease in accounts payable 6,000

Payments to suppliers $114,000

©2008 Pearson Prentice Hall. All rights reserved.12-40

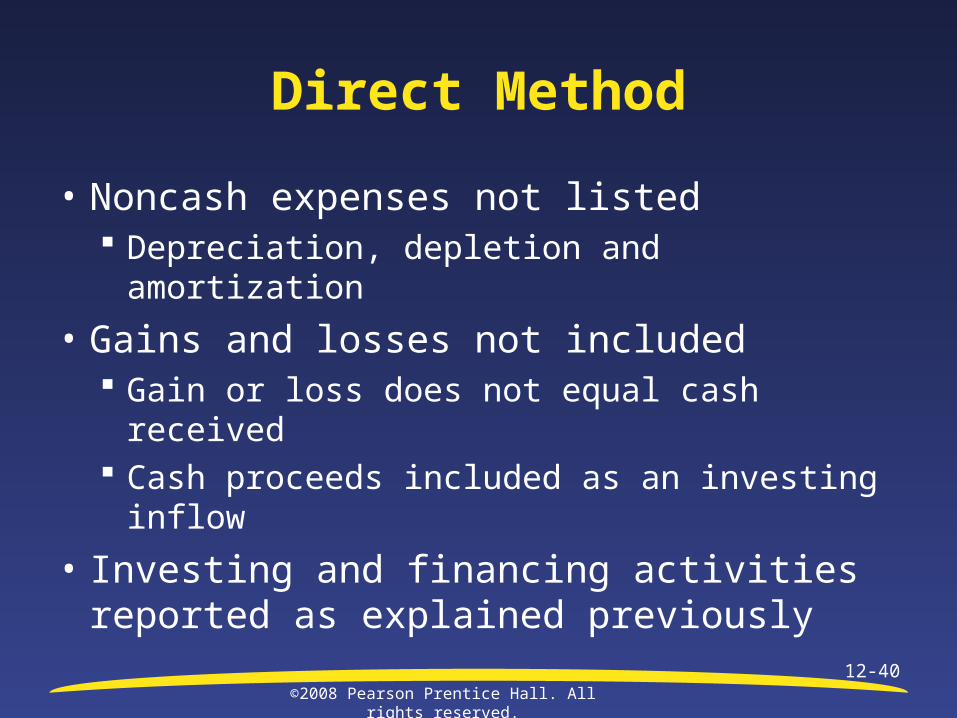

Direct Method

• Noncash expenses not listed Depreciation, depletion and amortization

• Gains and losses not included Gain or loss does not equal cash received Cash proceeds included as an investing

inflow

• Investing and financing activities reported as explained previously

©2008 Pearson Prentice Hall. All rights reserved.12-41

End of Chapter 12

Related Documents