1 MT 483 Investments Unit 6: Ch 10 and 11

1 MT 483 Investments Unit 6: Ch 10 and 11. Copyright © 2011 Pearson Prentice Hall. All rights reserved. 10-2 Interest Rates and Bonds The behavior of.

Dec 27, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

MT 483 InvestmentsUnit 6: Ch 10 and 11

Copyright © 2011 Pearson Prentice Hall. All rights reserved.10-2

Interest Rates and Bonds

• The behavior of interest rates is the single most important force in the bond market

• Interest rates and bond prices move in opposite directions

• When interest rates rise, bond prices fall

• When interest rates drop, bond prices move up

• Bond markets are bullish when interest rates are low or falling

• Bond markets are bearish when interest rates are high or rising

Copyright © 2011 Pearson Prentice Hall. All rights reserved.10-3

Bonds Versus Stocks

• Compared to stocks, bonds offer lower returns

• Main benefits of bonds in portfolio:– Lower risk and level of stability– High levels of current income– Diversification

• Bonds add an element of stability to a portfolio

Copyright © 2011 Pearson Prentice Hall. All rights reserved.10-4

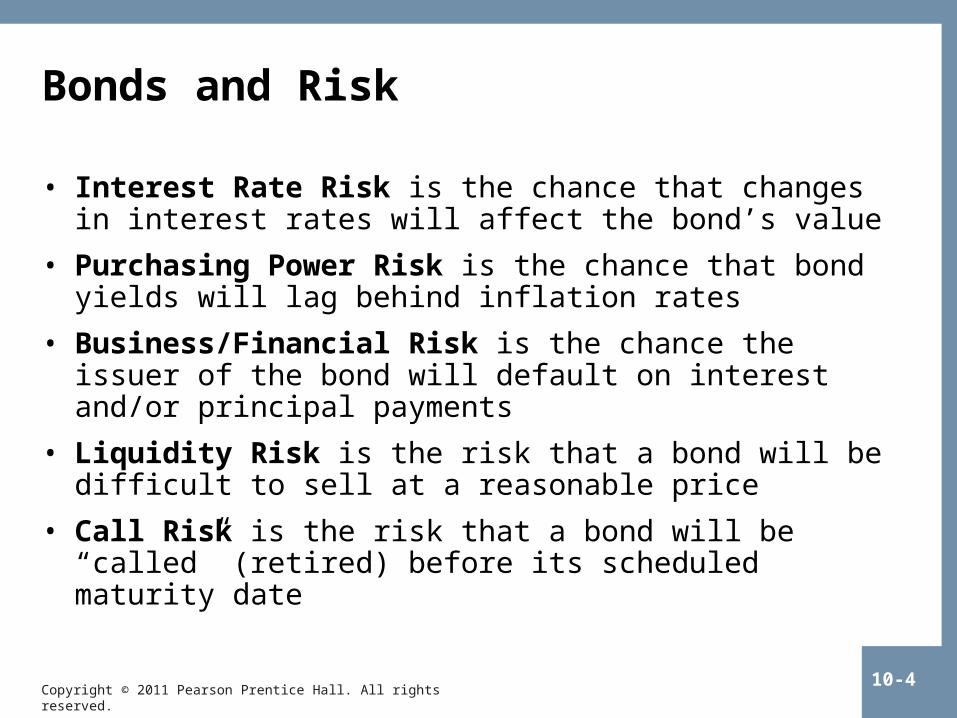

Bonds and Risk

• Interest Rate Risk is the chance that changes in interest rates will affect the bond’s value

• Purchasing Power Risk is the chance that bond yields will lag behind inflation rates

• Business/Financial Risk is the chance the issuer of the bond will default on interest and/or principal payments

• Liquidity Risk is the risk that a bond will be difficult to sell at a reasonable price

• Call Risk is the risk that a bond will be “called” (retired) before its scheduled maturity date

Copyright © 2011 Pearson Prentice Hall. All rights reserved.10-5

Principles of Bond Price Behavior

• Price of a bond is a function of its coupon rate, its maturity, and market movements in interest rates

• Longer maturities move more with changes in interest rates

• Premium bond has a market value that is above par value– Occur when market interest rates are below bond’s coupon rate

• Discount bond has a market value that is below par value– Occur when market interest rates are above bond’s coupon rate

Copyright © 2011 Pearson Prentice Hall. All rights reserved.10-6

Figure 10.3 The Price Behavior of a Bond

Copyright © 2011 Pearson Prentice Hall. All rights reserved.10-7

Essential Features of a Bond (cont’d)

• Call feature allows the issuer to repurchase the bonds before the maturity date– Freely callable– Noncallable– Deferred call

• Call premium is the amount added to bond’s par value and paid upon call to compensate bondholders

• Call price is the bond’s par value plus call premium

• Refunding provision prohibits the premature retirement of an issue from proceeds of a lower-coupon refunding bond

Copyright © 2011 Pearson Prentice Hall. All rights reserved.10-8

Treasury Bonds

• Considered risk free—no risk of default

• Interest is exempt from state and local taxes

• Sold in $1,000 denominations

• Types of Treasury Bonds– Treasury notes: maturities of 2, 3, 5, 7, and 10 years– Treasury bonds: mature in 30 years

• Treasury Inflation-Indexed Obligations (TIPS)– Protect against inflation by adjusting investor returns– Interest rates are very low– Maturities of 5, 10, and 20 years

Copyright © 2011 Pearson Prentice Hall. All rights reserved.10-9

Agency Bonds

• Issued by U.S. government agencies – Federal Home Loan Bank– Federal National Mortgage Association– Small Business Administration

• High quality securities with almost no risk of default

• Interest rates usually higher than Treasury issues

Copyright © 2011 Pearson Prentice Hall. All rights reserved.10-10

Municipal Bonds

• Issued by states, counties, cities and any other political subdivision

• Issued to fund public projects

• Two basic types – General obligation bonds are paid from general fund of

the issuer– Revenue bonds are paid from revenues from the project

being financed

• Often guaranteed by private insurers to lower risk and interest rates

Copyright © 2011 Pearson Prentice Hall. All rights reserved.10-11

Municipal Bonds

• Interest is tax-exempt for Federal taxes

• Interest can be tax-exempt from state taxes if you live in the state where the bond was issued

Copyright © 2011 Pearson Prentice Hall. All rights reserved.10-12

Zero-Coupon Bonds

• Do not pay interest

• Sold at deep discount from par value

• Value increases over time

• Subject to tremendous price volatility as interest rates fluctuate

• Interest must be reported as it is accrued for tax purposes, even though no interest is actually received.

• Treasury strips are zero-coupon bonds created from U.S. Treasury securities.

Copyright © 2011 Pearson Prentice Hall. All rights reserved.10-13

Mortgage-Backed Securities

• Bond backed by pool of residential mortgages

• Principal and interest are paid monthly

• Governmental agencies are major issuers: – Government National Mortgage Association (GNMA)– Federal Home Loan Mortgage Corporation (FHLMC)– Federal National Mortgage Association (FNMA)

• Self-liquidating investment since portion of principal is received each month

Copyright © 2011 Pearson Prentice Hall. All rights reserved.10-14

Collateralized Mortgage Securities

• Mortgage-back bond pool that is divided into “tranches,” or classes of investors

• All principal payments go first to the shortest tranche until it is fully retired, then the next in sequence is paid

• Allows investors to choose short-term, medium-term or long-term investment

• Potentially complex; interest rate fluctuations may have significant impact upon bond prices

Copyright © 2011 Pearson Prentice Hall. All rights reserved.10-15

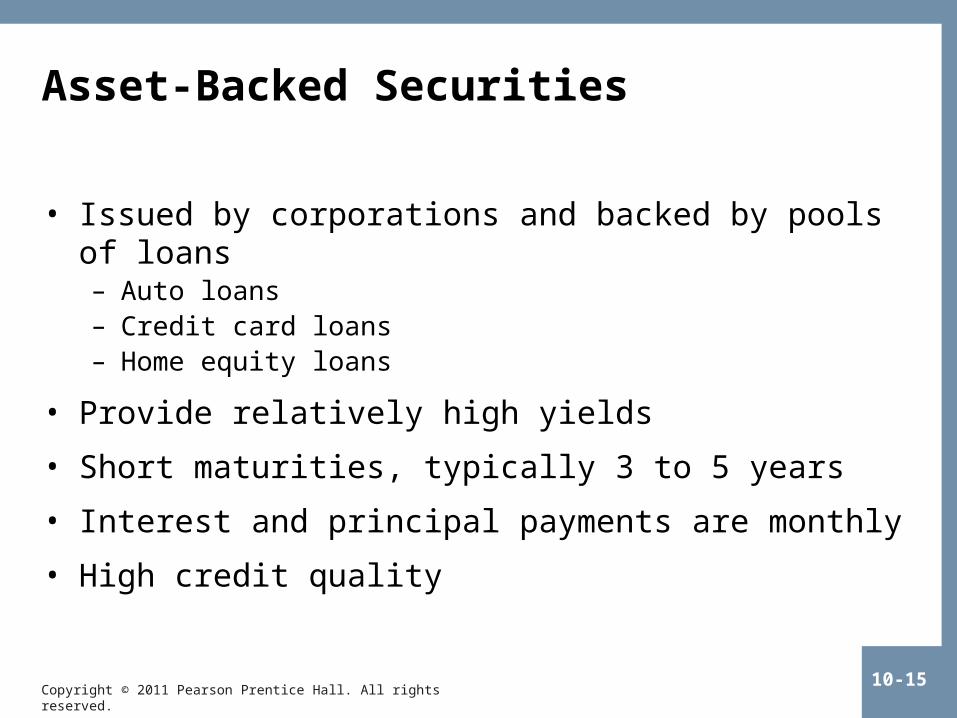

Asset-Backed Securities

• Issued by corporations and backed by pools of loans – Auto loans– Credit card loans– Home equity loans

• Provide relatively high yields

• Short maturities, typically 3 to 5 years

• Interest and principal payments are monthly

• High credit quality

Copyright © 2011 Pearson Prentice Hall. All rights reserved.10-16

For bonds, the risk premium depends upon:• the default, or credit, risk of the issuer• the term-to-maturity• any call risk, if applicable

Measuring Return

• Required Return: the rate of return an investor must earn on an investment to be fully compensated for its risk

Required ReturnOn Investment

Real Rateof Return

Expected Inflation

Premium

Risk Premiumfor Investment

Copyright © 2011 Pearson Prentice Hall. All rights reserved.10-17

Copyright © 2008 Pearson Addison-Wesley. All rights reserved.

Term Structure of Interest Ratesand Yield Curves

• Term Structure of Interest Rates: relationship between the interest rate or rate of return (yield) on a bond and its time to maturity

• Yield Curve: a graph that represents the relationship between a bond’s term to maturity and its yield at a given point in time

Copyright © 2011 Pearson Prentice Hall. All rights reserved.10-18

Theories on Shape of Yield Curve

• Slope of yield curve affect by:

– Inflation expectations

– Liquidity preferences of investors

– Supply and demand

Copyright © 2011 Pearson Prentice Hall. All rights reserved.10-19

Theories on Shape of Yield Curve (cont’d)

• Expectations Hypothesis

– Shape of yield curve is based upon investor expectations of future behavior of interest rates

– If expecting higher inflation, investors demand higher interest rates on longer maturities to compensate for risk

– Increasing inflation expectations will result in upward-sloping yield curve

– Decreasing inflation expectations will result in downward-sloping yield curve

Copyright © 2011 Pearson Prentice Hall. All rights reserved.10-20

Theories on Shape of Yield Curve (cont’d)

• Liquidity Preference Theory

– Shape of yield curve is based upon the length of term, or maturity, of bonds

– If investors’ money is tied up for longer periods of time, they have less liquidity and demand higher interest rates to compensate for real or perceived risks

– Investors won’t tie their money up for longer periods unless paid more to do so

Copyright © 2011 Pearson Prentice Hall. All rights reserved.10-21

Theories on Shape of Yield Curve (cont’d)

• Market Segmentation Theory

– Shape of yield curve is based upon the supply and demand for funds

– The supply and demand changes based upon the maturity levels: short-term vs. long-term

– If more borrowers (demand) want to borrow long-term than investors want to invest (supply) long-term, then the interest rates (price) for long-term funds will go up

– If fewer borrowers (demand) want to borrow long-term than investors want to invest (supply) long-term, then the interest rates (price) for long-term funds will go down

Copyright © 2011 Pearson Prentice Hall. All rights reserved.10-22

Interpreting Shape of Yield Curve

• Upward-sloping yield curves result from:– Higher inflation expectations– Lender preference for shorter-maturity loans– Greater supply of shorter-term loans

• Flat or downward-sloping yield curves result from:– Lower inflation expectations– Lender preference for longer-maturity loans– Greater supply of longer-term loans

Copyright © 2011 Pearson Prentice Hall. All rights reserved.10-23

The Pricing of Bonds

• Bonds are priced according to the present value of their future cash flow streams

Copyright © 2011 Pearson Prentice Hall. All rights reserved.10-24

The Pricing of Bonds (cont’d)

• Bond Pricing Example:

– What is the market price of a $1,000 par value 20 year bond that pays 9.5 % compounded annually when the market rate is 10%?

Copyright © 2011 Pearson Prentice Hall. All rights reserved.10-25

Ways to Measure Bond Yield

• Current yield

• Yield-to-Maturity

• Yield-to-Call

• Expected Return

Copyright © 2011 Pearson Prentice Hall. All rights reserved.10-26

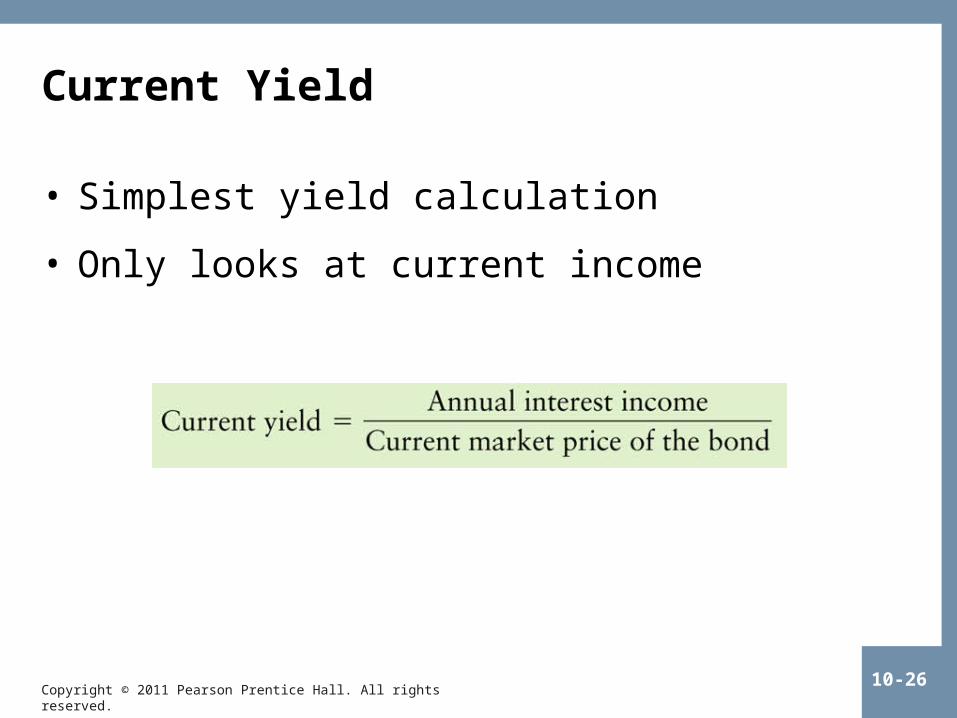

Current Yield

• Simplest yield calculation

• Only looks at current income

Copyright © 2011 Pearson Prentice Hall. All rights reserved.10-27

Yield-to-Maturity

• Most important and widely used yield calculation

• True yield received if the bond is held to maturity

• Assumes all interest income is reinvested at rate equal to market rate at time of YTM calculation—no reinvestment risk

• Calculates value based upon PV of interest received and the appreciation of the bond if held until maturity

• Difficult to calculate without a financial calculator

Copyright © 2011 Pearson Prentice Hall. All rights reserved.10-28

Yield-to-Maturity (cont’d)

• Yield-to-Maturity Example:

– Find the yield-to-maturity on a 7.5 % ($1,000 par value) bond that has 15 years remaining to maturity and is currently trading in the market at $809.50?

Copyright © 2011 Pearson Prentice Hall. All rights reserved.10-29

Yield-to-Call (cont’d)

• Yield-to-Call Example:

– Find the yield-to-call of a 20-year, 10.5 % bond that is currently trading at $1,204, but can be called in 5 years at a call price of $1,085?

Copyright © 2011 Pearson Prentice Hall. All rights reserved.10-30

Expected Return (cont’d)

• Expected Return Example:

– Find the expected return on a 7.5% bond that is currently priced in the market at $809.50 but is expected to rise to $960 within a 3-year holding period?

Related Documents