1 HIGH TECH STRATEGIES Introduction to High Technology Industries

1 HIGH TECH STRATEGIES Introduction to High Technology Industries.

Dec 14, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

HIGH TECH STRATEGIES

Introduction to High Technology Industries

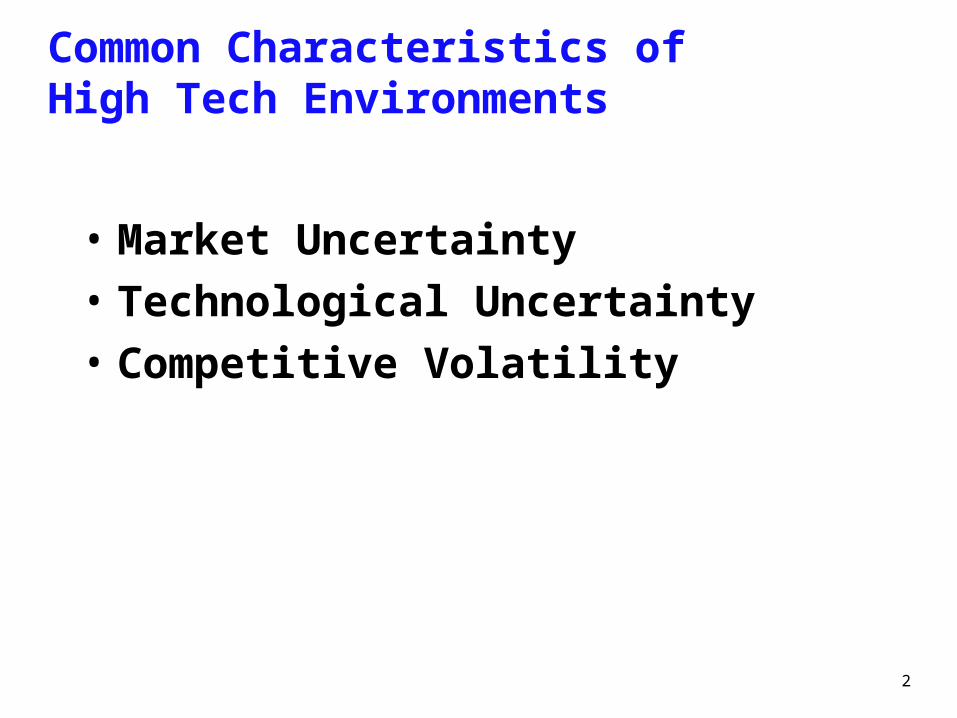

2

Common Characteristics of High Tech Environments

• Market Uncertainty

• Technological Uncertainty

• Competitive Volatility

3

Market Uncertainty

• Consumer fear, uncertainty and doubt • Customer needs change rapidly and unpredictably • Customer anxiety over the lack of standards and

dominant design • Uncertainty over the pace of adoption • Uncertainty over/inability to forecast market size

Market Uncertainty is the ambiguity about the type and extent of customer needs that can be satisfied by a particular technology

4

Technology Uncertainty

• Uncertainty over whether the new innovation will function as promised

• Uncertainty over timetable for new product development

• Ambiguity over whether the supplier will be able to fix customer problems with the technology

• Concerns over unanticipated/unintended consequences

• Concerns over obsolescence

Technology Uncertainty is not knowing whether the technology or the company can deliver on its promise

5

Competitive Volatility

• Uncertainty over who will be future competitors

• Uncertainty over “the rules of the game” (i.e., competitive strategies and tactics)

• Uncertainty over “product form” competition– competition between product classes vs. between

different brands of the same product

• Implication: Creative destruction

6

High Tech Strategy Field

Market Uncertainty

Technological Uncertainty

Competitive Volatility

High- Technology

Strategies

7

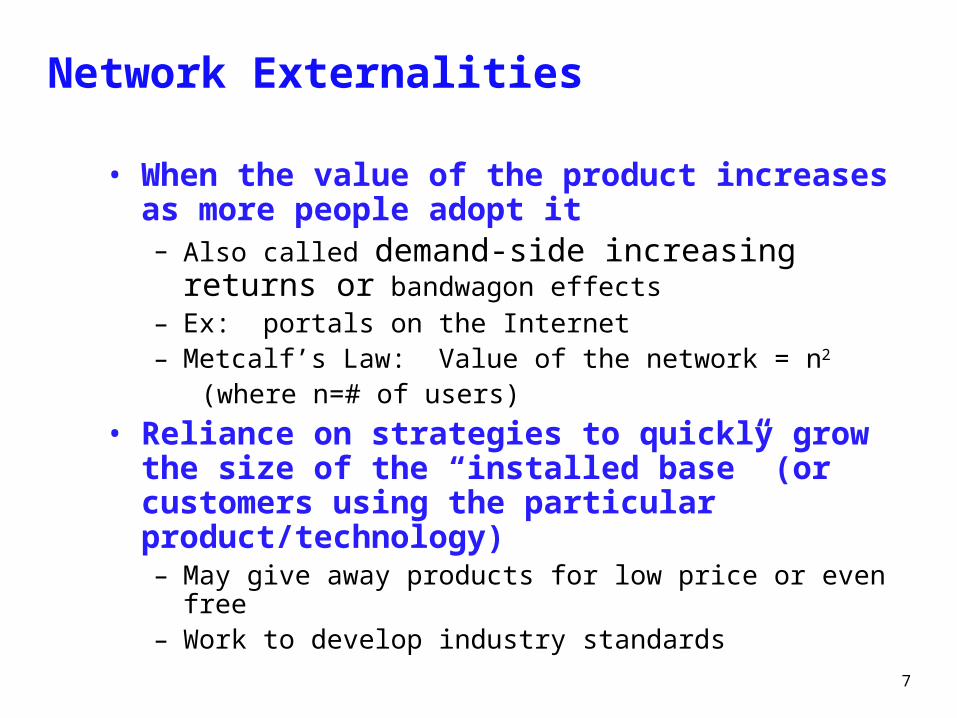

Network Externalities

• When the value of the product increases as more people adopt it– Also called demand-side increasing returns or

bandwagon effects– Ex: portals on the Internet – Metcalf’s Law: Value of the network = n2

(where n=# of users)

• Reliance on strategies to quickly grow the size of the “installed base” (or customers using the particular product/technology) – May give away products for low price or even free – Work to develop industry standards

8

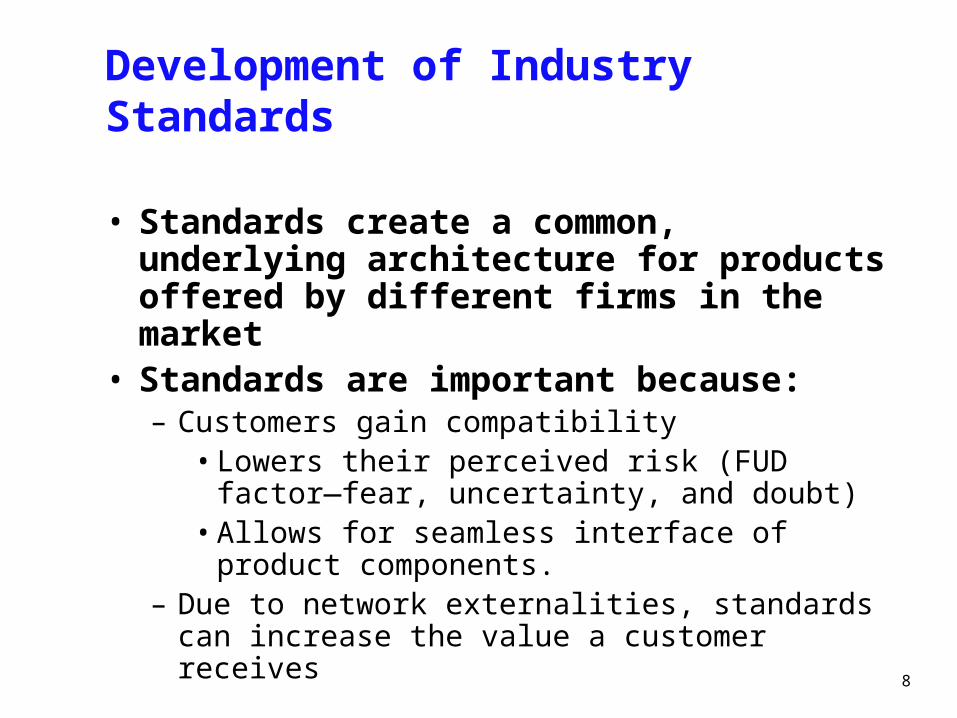

Development of Industry Standards

• Standards create a common, underlying architecture for products offered by different firms in the market

• Standards are important because:– Customers gain compatibility

• Lowers their perceived risk (FUD factor—fear, uncertainty, and doubt)

• Allows for seamless interface of product components.

– Due to network externalities, standards can increase the value a customer receives

9

Why are industry standards important? (Cont.)

• Availability of complementary products determined by the size of the “installed base” of a given product. – Therefore, standards help ensure greater availability of

complementary products by helping to ensure a larger size of the installed base.

– Customers get more value from the base product as more complementary products are available.

10

Self-reinforcing Nature of Standards

STANDARDS

Reduce customer

fear, uncertainty,

& doubt

Larger installed

base

More complementary

products developed

Increased customer

value

Increased demand for

product

11

• Lecture based on the concepts developed by the best all-time high-tech strategies guru, Geoffrey Moore•Books from Geoffrey Moore:

- Crossing the Chasm: Very good, sometimes difficult to read- Inside the Tornado: Moore’s best book- The Gorilla Game: high tech investor’s perspective- Living in the Fault Line: Some parts are excellent, other parts

have changed much after the internet

bubble.

INTRODUCTION

12

BASIC CONCEPTS

13

CONTINUOUS INNOVATIONS:

- Build upon existing standards and infrastructure- To enjoy the product benefits, users only need to buy the product and start using it

DISCONTINUOUS INNOVATIONS:

- Require new technologies and infrastructure that is incompatible with the existing one- Users will have to go through a a learning process- Vendors, partners, suppliers of complementary products will have to adapt to the new technology in order for the new product to be marketed

-Ex: when you buy a VCR you need movies to rent-Ex: when you buy a fax, you expects others to have it too

14

Discontinuous Innovations

High Tech Marketing Specializes in Discontinuous InnovationsHigh Tech Marketing Specializes in Discontinuous Innovations

Discontinuous

Electric car

Multimedia Set-Tops

Video Conferencing

Continuous

Better mileage cars

Remote-control tuning

Voice Mail

Diesel cars

Programmable VCRs

Conference Calling

15

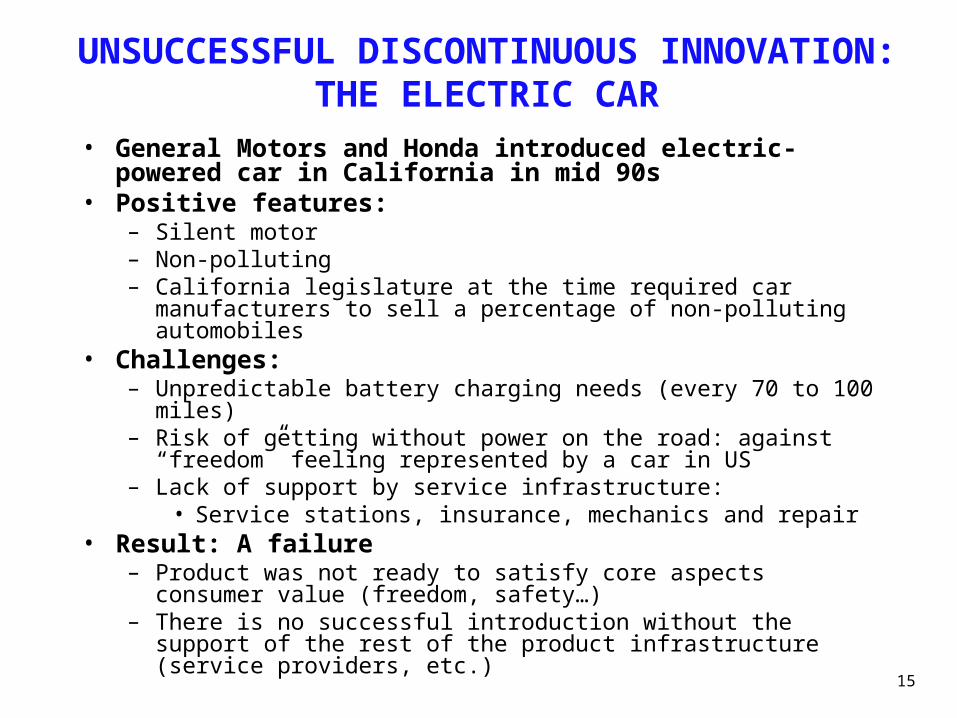

UNSUCCESSFUL DISCONTINUOUS INNOVATION: THE ELECTRIC CAR

• General Motors and Honda introduced electric-powered car in California in mid 90s

• Positive features:– Silent motor– Non-polluting– California legislature at the time required car manufacturers to sell a

percentage of non-polluting automobiles• Challenges:

– Unpredictable battery charging needs (every 70 to 100 miles)– Risk of getting without power on the road: against “freedom” feeling

represented by a car in US– Lack of support by service infrastructure:

• Service stations, insurance, mechanics and repair• Result: A failure

– Product was not ready to satisfy core aspects consumer value (freedom, safety…)

– There is no successful introduction without the support of the rest of the product infrastructure (service providers, etc.)

16

Industries where discontinuous innnovations are a driving force:

• High-tech industries:– Telecommunications (mobile phones, infrastructure,

telecommunications services)– Computers and ”hardware” – Chemicals– Software – Biotechnology – Electronics– Fiber optics– Microelectronics– Multimedia systems– Pharmaceutical industry– Robotics– Semiconductors– Defense– Other emerging high-tech

17

Industries where discontinuous innovations are a driving force:

• Main Industries outside high-tech but highly influenced by high-tech:– Financial services– Insurance– Health care– Aerospace– Utilities– Retailing– Publishing– Broadcasting

19

CustomersService ProvidersProduct Providers

Value Chain

$$

All these linkages are requiredfor a new technology wave to succeed

Applications

Products &Consumables

Technology

CustomerService

Sales &Support

Consulting

EconomicBuyers

End Users

TechnicalBuyers

20

Technology Adoption Life Cycle

Pragmatists create the dynamics of high-tech market development.Pragmatists create the dynamics of high-tech market development.

Innovators EarlyAdopters

Early Majority Late Majority Laggards

Techies:Try it!

Pragmatists:Stick with the herd!

Conservatives:Hold on!

Skeptics:No way!

Visionaries:Get ahead of the herd!

21

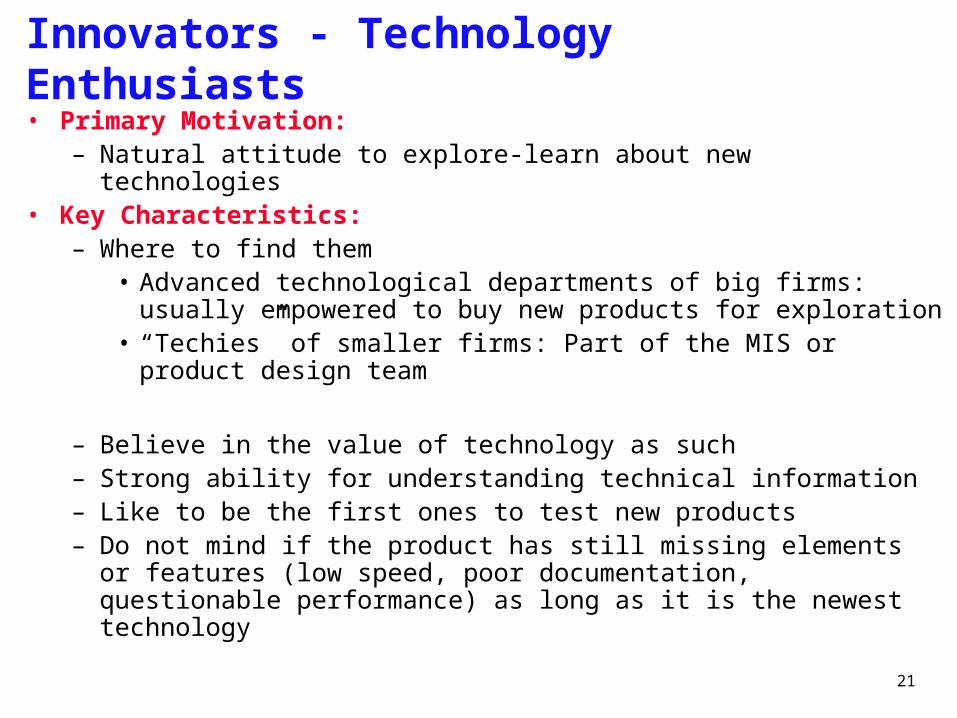

Innovators - Technology Enthusiasts• Primary Motivation:

– Natural attitude to explore-learn about new technologies• Key Characteristics:

– Where to find them• Advanced technological departments of big firms: usually

empowered to buy new products for exploration• “Techies” of smaller firms: Part of the MIS or product design team

– Believe in the value of technology as such– Strong ability for understanding technical information– Like to be the first ones to test new products– Do not mind if the product has still missing elements or features (low

speed, poor documentation, questionable performance) as long as it is the newest technology

22

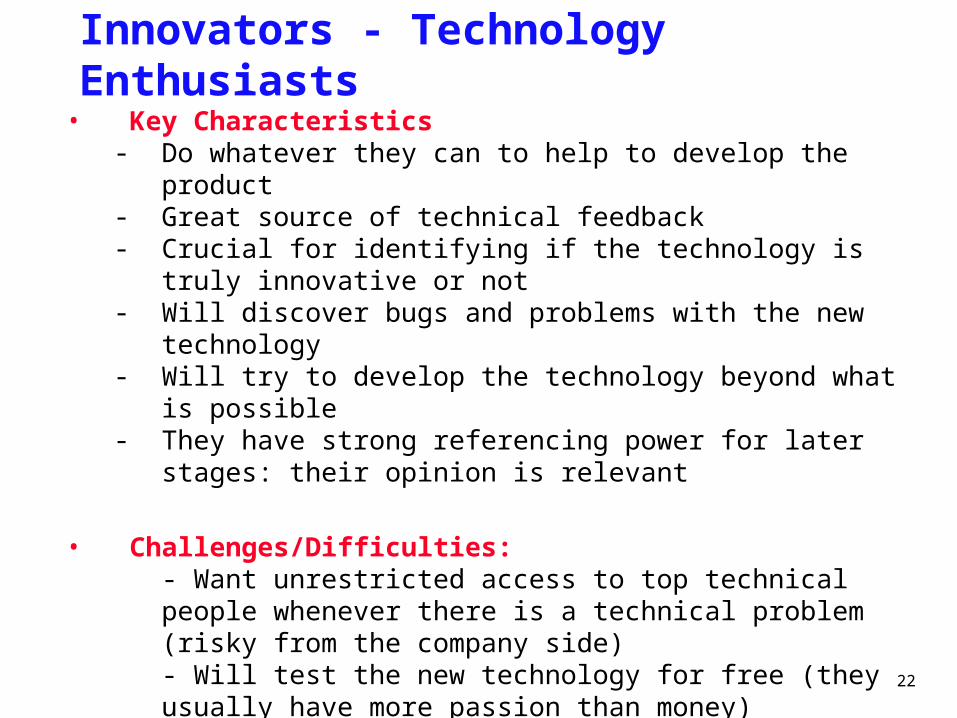

• Key Characteristics- Do whatever they can to help to develop the product- Great source of technical feedback- Crucial for identifying if the technology is truly innovative or not- Will discover bugs and problems with the new technology- Will try to develop the technology beyond what is possible- They have strong referencing power for later stages: their

opinion is relevant

• Challenges/Difficulties:- Want unrestricted access to top technical people whenever there is a technical problem (risky from the company side)- Will test the new technology for free (they usually have more passion than money) - They do not represent strong buying power- Not a market by themselves, but a test “if the product works”: crucial to find technology enthusiasts with access to big bosses

Innovators - Technology Enthusiasts

23

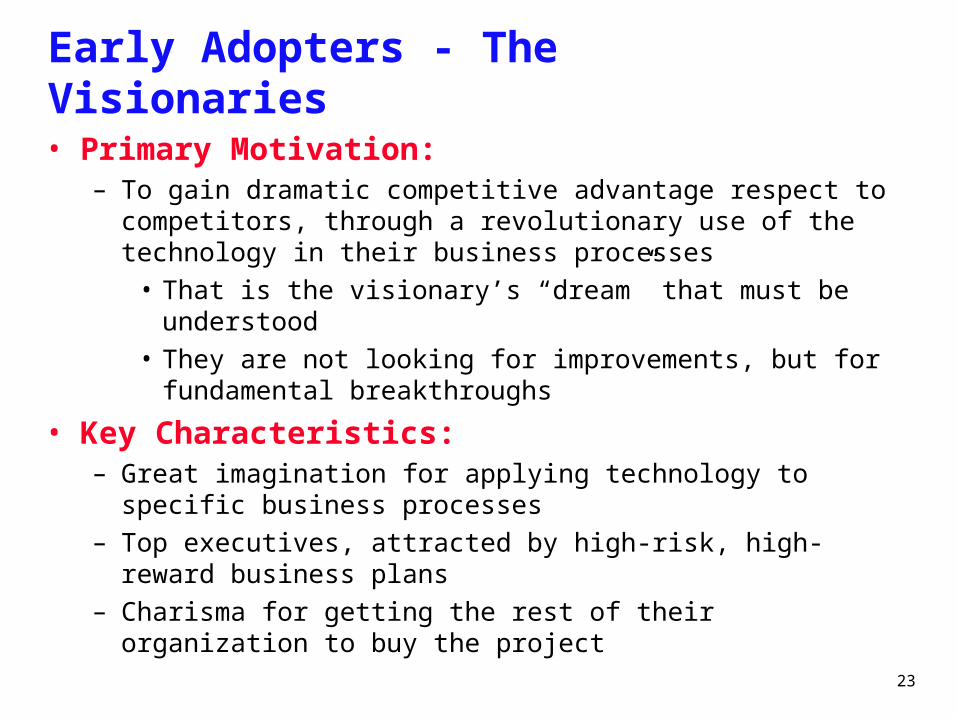

Early Adopters - The Visionaries

• Primary Motivation:– To gain dramatic competitive advantage respect to competitors,

through a revolutionary use of the technology in their business processes

• That is the visionary’s “dream” that must be understood• They are not looking for improvements, but for fundamental

breakthroughs

• Key Characteristics:– Great imagination for applying technology to specific business

processes– Top executives, attracted by high-risk, high-reward business plans– Charisma for getting the rest of their organization to buy the

project

24

Early Adopters - The Visionaries• Key Characteristics:

– Will commit to create the missing elements of the new technology, for making it ready to be used

– They are not price-sensitive: emphasize more the potential future gains (they bring real big money to develop the product): best source of high-tech development capital

– Motivated by the potential return on investment of their dream– Effective in informing the business community about technology

advances: draw media attention to themselves and indirectly to our product

– Easy to sell, hard to please (dreams are difficult to fulfill as initially imagined)

• Challenges/Difficulties:– Want to market the new technology fast (not always easy in high-

tech)– Demand high degree of customization of the technology to their very

particular needs, and demand a lot of technical support/resources:• Too much money can be spent in customization for just one

customer

25

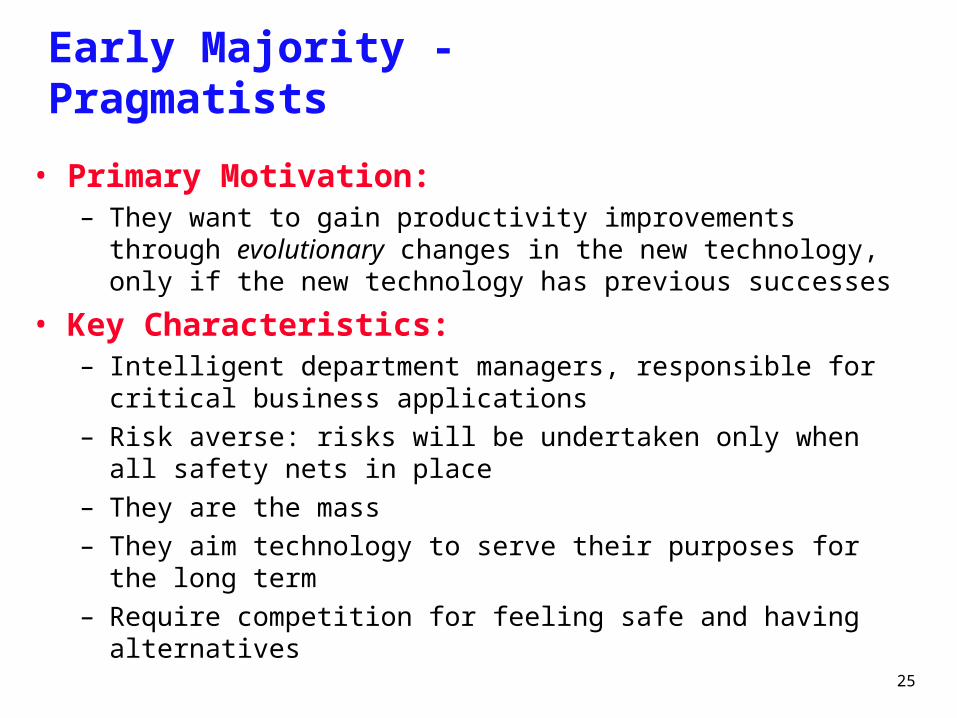

Early Majority - Pragmatists

• Primary Motivation:– They want to gain productivity improvements through evolutionary

changes in the new technology, only if the new technology has previous successes

• Key Characteristics:– Intelligent department managers, responsible for critical business

applications– Risk averse: risks will be undertaken only when all safety nets in

place– They are the mass– They aim technology to serve their purposes for the long term– Require competition for feeling safe and having alternatives

26

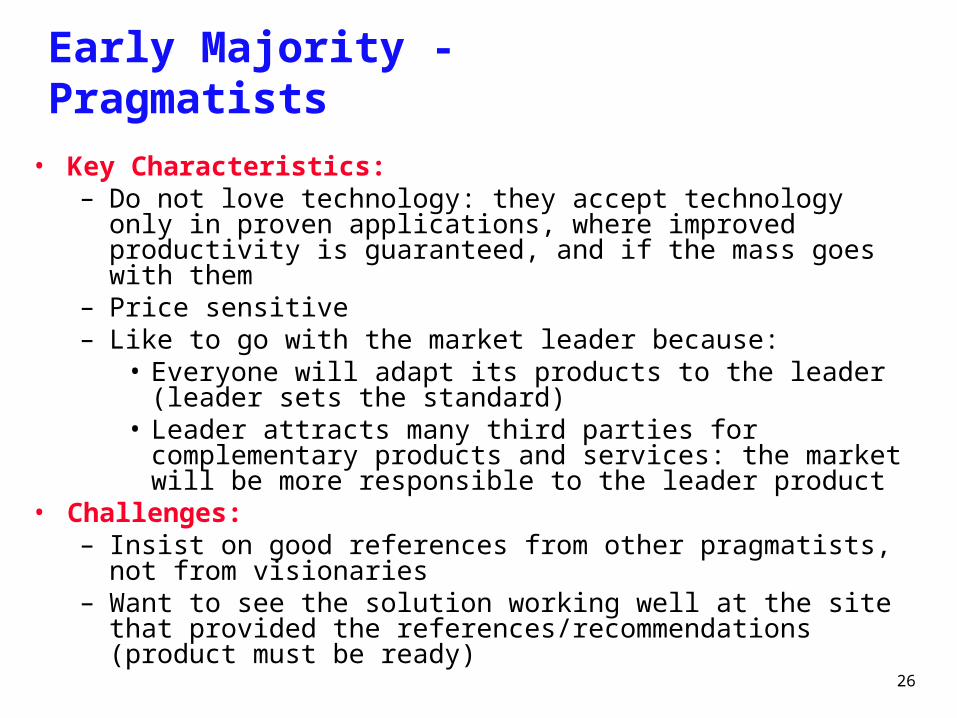

Early Majority - Pragmatists

• Key Characteristics:– Do not love technology: they accept technology only in proven

applications, where improved productivity is guaranteed, and if the mass goes with them

– Price sensitive– Like to go with the market leader because:

• Everyone will adapt its products to the leader (leader sets the standard)

• Leader attracts many third parties for complementary products and services: the market will be more responsible to the leader product

• Challenges:– Insist on good references from other pragmatists, not from

visionaries– Want to see the solution working well at the site that provided the

references/recommendations (product must be ready)

27

Late Majority - Conservatives

• Primary Motivation:– They acquire technology just to stay at the same level with the competition

(skeptical about value gains from technology).• Key Characteristics:

– Fear technology a little bit– Do not have high aspirations about high-tech investments: will not support high

margins– Not risk takers– Very much price-sensitive: buying late provides them with the opportunity to

negotiate better prices and conditions– Highly reliant on a single, trusted advisor

• Challenges:– Package required:

• Pre-assembled and bundled solution• Single-use and simple • User friendly solutions

– Would benefit from value-added services but do not want to pay for them

28

Laggards - Skeptics

• Primary Motivation:– To maintain things as they have traditionally been: prefer low-

cost and non-technical solutions

• Key Characteristics:– Good at criticizing technology marketing ”booms”– Do not believe productivity-improvement gain from technology – Seek to block purchases of new technology

• Challenges:– Not a customer, but should be considered– Can form a strong opposition to early technology adoption

29

Four Marketing Frameworks

DealDriven

NicheMarketing

MassMarketing

1 on 1Marketing

30

Four Product Management PrioritiesC

us

tom

er

Sat

isfa

ctio

n

Time

SolutionEnablers

Bowling Alley

CompetitivePrice/Performance

Tornado

End UserDelighters

Main StreetEarly Market

CoreProduct

32

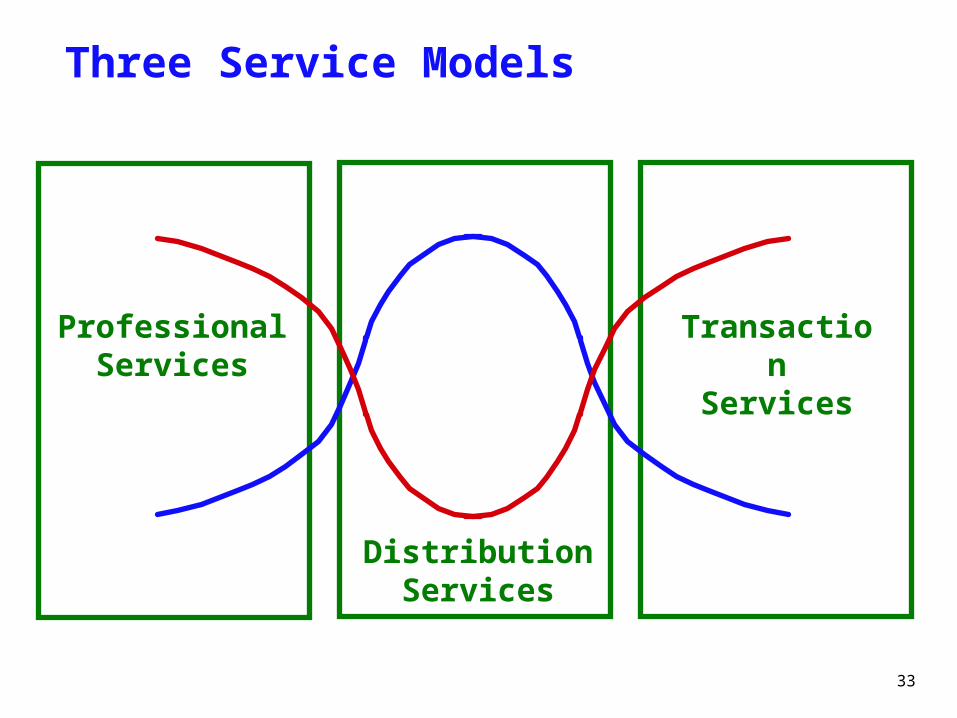

Product/Service Mix

Products + Services = The Whole Product

Services

Products

33

Three Service Models

ProfessionalServices

DistributionServices

TransactionServices

34

Sample Service Offerings

ProfessionalServices

• Consultative selling

• Business process reengineering

• Systems integration

• Project management

• Custom training

• System conversion

• Contract management

TransactionServices

• Order processing

• Maintenance

• Facilities management

• Outsourcing

• Upgrade management

• Broadcast data feeds

• Proprietary database access privileges

DistributionServices

• Competitive selling

• System configuration

• Implementation support

• Train-the-trainers

• Customer service

• Technical support

• Warranty

35

Service Management Priorities

Deep Water

Shallow Water

High marginCustom

Medium margin Customized

Low margin Standard

36

Part Two: Go-to-Market Strategy Models

39

Assessing Innovation Discontinuity

A B C D

4

3

2

1

ShadowArea

Gain

Pa

in

Ideal Positioning of the Innovation according to its stage in the TALC

41

Assessing Innovation Discontinuity

- Analysis- Shadow zone:

- Future is uncertain- There is gain at an equivalent level of pain- Not very compelling: markets will not move these innovations forward- Areas in the periphery are easier to dealt with than areas in the shadow zone (where benefit/pain tradeoffs are less visible- Action: Decide a specific TALC stage into which to move, and assess the needed strategy (explained further)

42

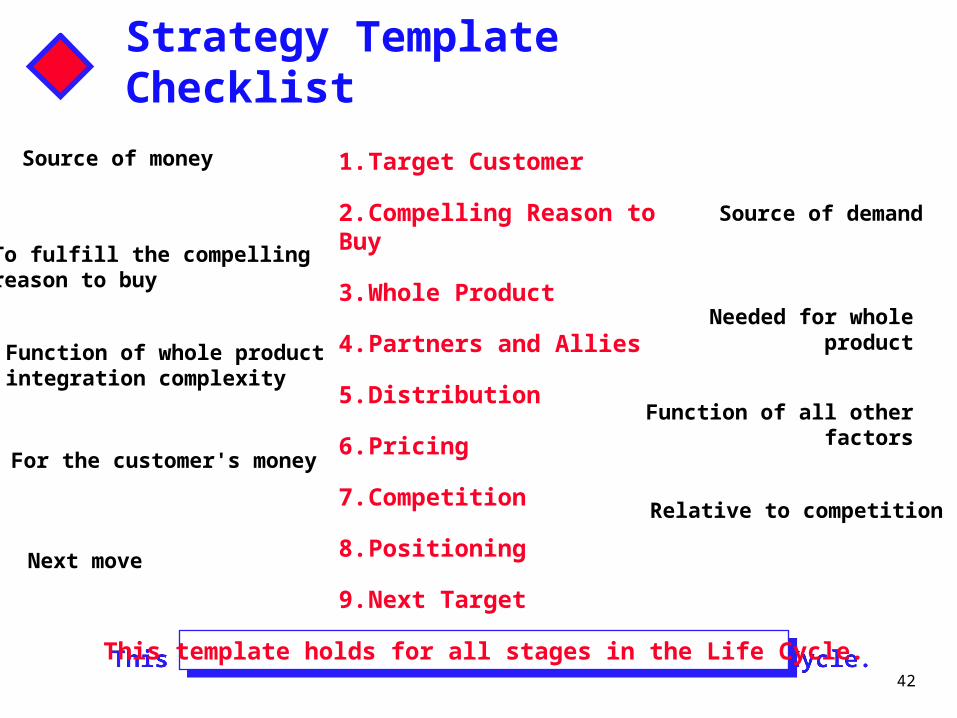

Strategy Template Checklist

1. Target Customer

2. Compelling Reason to Buy

3. Whole Product

4. Partners and Allies

5. Distribution

6. Pricing

7. Competition

8. Positioning

9. Next Target

Source of money

To fulfill the compellingreason to buy

Function of whole productintegration complexity

For the customer's money

Next move

Source of demand

Needed for whole product

Function of all other factors

This template holds for all stages in the Life Cycle.This template holds for all stages in the Life Cycle.

Relative to competition

43

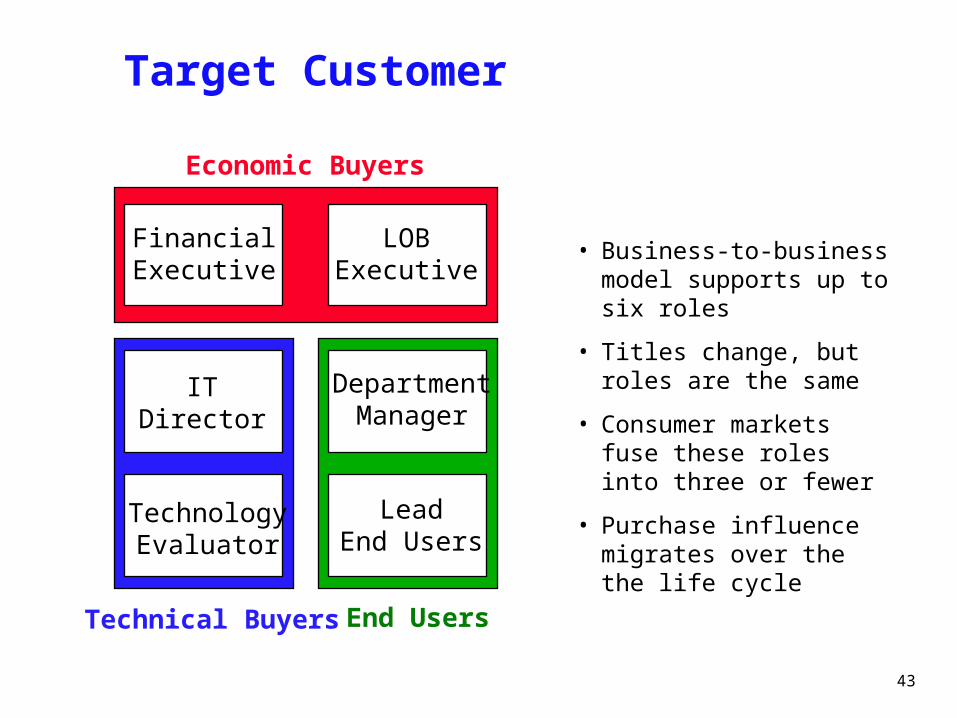

Target Customer

Economic Buyers

Technical Buyers End Users

LOBExecutive

DepartmentManager

LeadEnd Users

FinancialExecutive

ITDirector

TechnologyEvaluator

• Business-to-business model supports up to six roles

• Titles change, but roles are the same

• Consumer markets fuse these roles into three or fewer

• Purchase influence migrates over the the life cycle

44

Target Customer

• Success with a set of prospects will depend on:• Are customers identifiable?• Can customers be accessed through sales and marketing efforts?• Do customers have funds for purchasing in a reasonable time under appropriate circumstances?• Are customers able to make the purchase (power and financial ability)?

45

Compelling Reasons to Buy

Go ahead of the herd for competitive advantage.

Go ahead of the herd to fix a broken business process.

Go with the herd to get on the new infrastructure.

Go after the herd to get better values.

- Main motive: economic consequences of doing nothing vs. making an investment to address a current problem/exploit an opportunity

- Motivation is more apparent in bowling alley and tornado markets- Motivation is more latent in Early Markets and Main Street (more emotional as well)- Purchase must be justified to oneself, colleagues and superiors

Compelling Reasons to Buy and the TALC

46

Whole Product Elements

The whole product is the minimum set of products and servicesneeded to fulfill the target customer's compelling reason to buy.

The whole product is the minimum set of products and servicesneeded to fulfill the target customer's compelling reason to buy.

TheProduct

Hardware

Software

Legacyinterfaces Connectivity

Pre-salesservices

Post-salesservice

& support

Peripherals

Consulting

ComplementaryProducts

ComplementaryServices

47

Whole Product

Potential Product

AugmentedProduct

ExpectedProduct

GenericProduct

48

Whole Product

• Generic Product-What is shipped when the purchase is made

• Expected Product-What the customer things to be buying when the generic order is placed

- Example: If the generic order is a computer, the expected product is the CPU, keyboard, mouse, monitor and cabling

• Augmented Product-The idealized form of the product in which the buyer will achieve the buying objective

- Example: In a PC, the software, printer, Internet connections and other services

• Potential Product-An extension of the product benefits through a set of products and services

- Example: TV view hardware and software, infrared mouse…

49

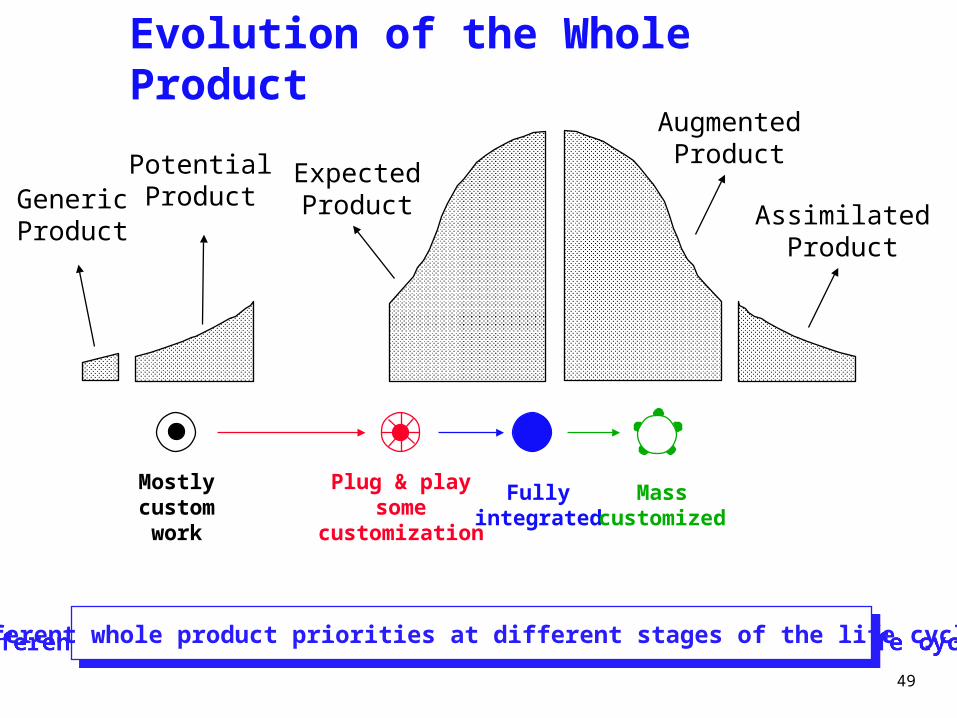

Evolution of the Whole Product

Different whole product priorities at different stages of the life cycle.Different whole product priorities at different stages of the life cycle.

Mostlycustom

work

Plug & playsome

customization

Fullyintegrated

Masscustomized

GenericProduct

PotentialProduct

ExpectedProduct

AugmentedProduct

AssimilatedProduct

51

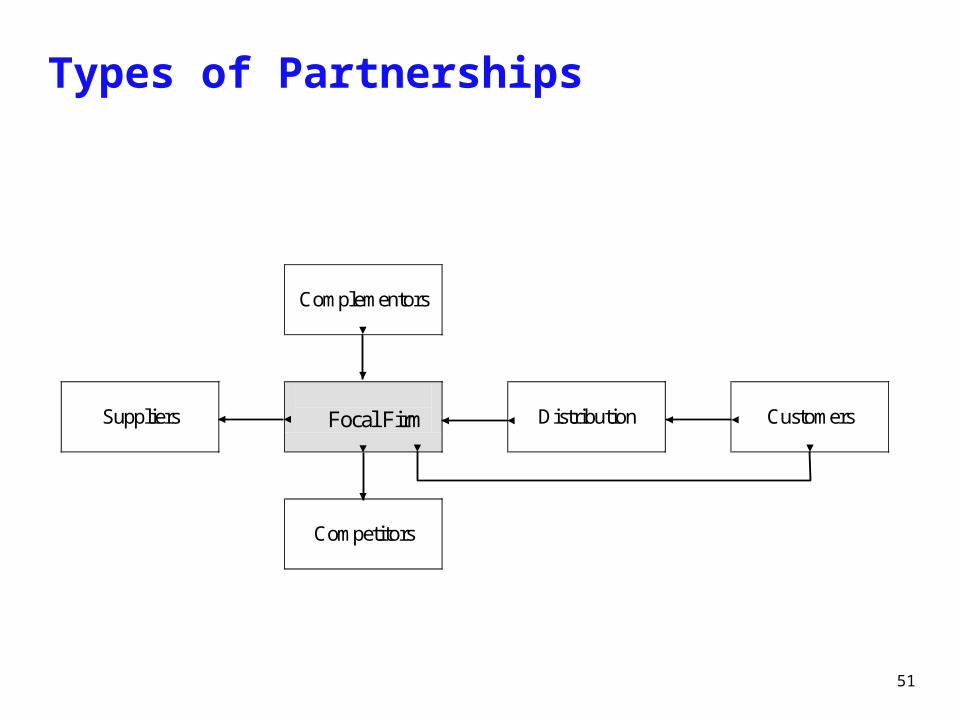

Types of Partnerships

Complementors

Suppliers

Focal Firm

Distribution

Customers

Competitors

52

Types of Partnerships (cont.)

• Vertical partnerships: with members at other levels of the supply chain– Suppliers– Distribution channel members– Customers

• Horizontal partnerships: with members at the same level of the supply chain – “Complementors:” makers of jointly-used

products– Competitors—”competition”

53

Reasons to Partner

• Accelerate Product Development• Access resources and skills• Gain cost efficiencies• Speed time-to-market• Access new markets• Define industry standards• Differentiate the Product• Develop complementary products• Gain market clout

54

Product Life Cycle, Innovation, and the Role of Alliances

Emergence Growth Maturity Decline

ProcessInnovation

ProductInnovation

StandardsLicensingTechnology

LicensingR&DMarketing

ManufacturingMarketingProcess R&D

AttackerIncumbent

High

Low

Rate ofMajor

Innovation

Stage of Product Life Cycle

Alliance Types

55

Risks in Partnering

• Failure of the relationship– Adversarial rather than cooperative thinking– Mistrust, insecurity, impatience, hidden agendas– Partners don’t invest energy in the alliance because it

requires a level of intimacy they are not used to

• Failure to understand the other Party’s Goal• Machiavellian attitudes

– Example: Strategic Alliance for Technology where the only real goal is to access each other customers

– Example: Lets join forces so me (A) and you (B) can both sell our products, degenerates into “lets partner so you (B) can sell our products for us (A)”, or A tries to sell in B, rather than sell through B.

56

• Loss of autonomy and control• Loss of proprietary information to partner• Potential legal issues and antitrust problems • Failure to achieve alliance objectives

• Unchecked Executive Egos• Excessive promises when negotiations are done without checking the organization and colleagues capabilities to deliver them

• Absence of a real strategy• Joint development fails, and ends up in both parties bundling or packaging difficult-to-sell-products instead of creating a better solution for the customer

• Resource commitments do not materialize

Risks in Partnering

57

Factors Contributing to Partnership Success

• Joint (bilateral) interdependence – Caution warranted with partners of unequal

size• Governance Structure• Joint Commitment • Trust in the partner’s motives and intents • Effective Communication• Compatible Corporate Cultures • Integrative conflict resolution and negotiation

(vs. “hard,” win/lose bargaining)

58

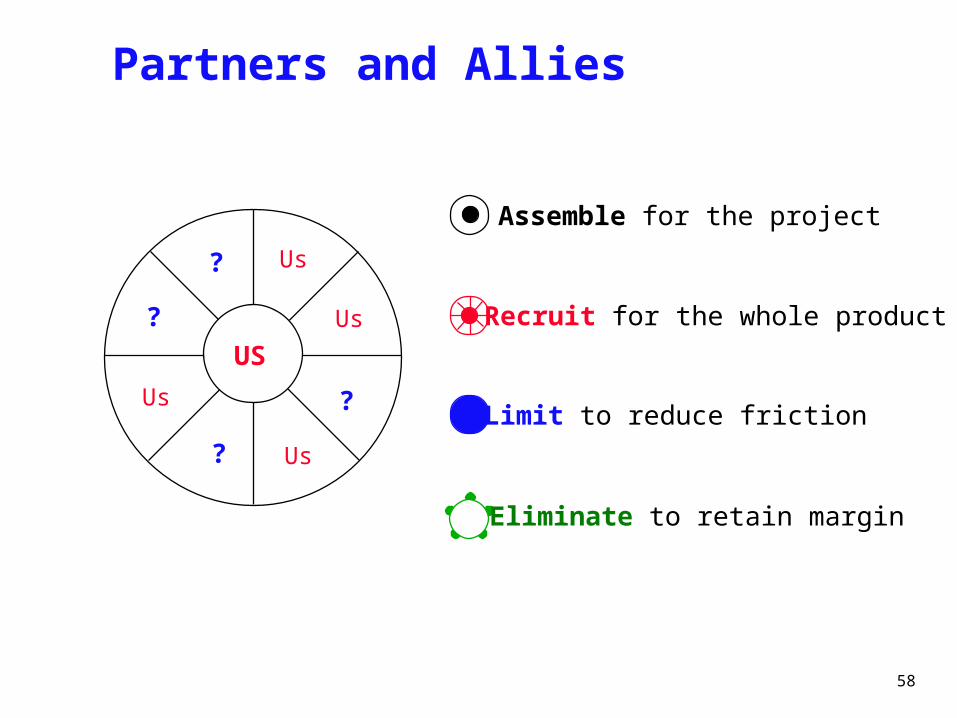

Partners and Allies

Us

Us

Us

Us

?

?

?

?

US

Assemble for the project

Recruit for the whole product

Limit to reduce friction

Eliminate to retain margin

60

Distribution Channels

Direct Sales

VARs

Retail

Web, Telesales

Systems Integrators

Mainframes

Minis

LANs

PC Servers

Desktop PCs

Printers

Keyboards

Toner

WANs

Global Systems

Ma

rke

tin

g C

om

ple

xity

Solution Complexity

Higher Value A

ddedHigher V

olume

Evangelists

ServiceTechnicians

61

Distribution Channels• Distribution Channel concepts:

- Define System Integrators• Dealers that manage very large and complex computer projects• Create customized solutions for customers (high level of consulting and tailoring required)• Bundle and Re-Sell different brands of equipment, providing the missing elements, and tailoring them for specific customer needs

• Define Direct Sales• Sales from Manufacturer to the customer through manufacturer’s own sales force or through the internet

• Define Value Added Retailers (VARs or VADs)• Purchase products from several hi-tech companies and add value to them for meeting the customer’s specific needs

• Ex.: VAR purchases hardware, operating system and bundles it with specific medical software for dentists. Some degree of tailoring, at much smaller scale than system integrators

• Retail• Web, Telesales

62

Distribution Channels• Primary Objective of Distribution Channel Selection

• To ensure that a relationship can be created and sustained with the most influential customer (economic, technical or final user) as the product moves through the TALC

• Criteria to design the Distribution Channel Choice:• Solution Complexity: How complex is the product to install, deploy and use?• Marketing Complexity: How difficult is the product to source, buy and support?

• Potential difficulties (outside the dotted-line)• High marketing complexity / Low solution complexity (Upper-left quadrant)

• The product is too easy for the channel use that wont be able to provide enough services/do enough businesses• Bad deal for the customer (channel will charge too much), customer feels paying for something which is not needed• Example: Sell PC through direct sales• Solution: Change the channel (killing flies with cannonballs!)

63

Distribution Channels• High solution complexity / Low marketing complexity (Lower-right quadrant)

• Too complicated product for the used channel • Distribution channel will suffer• Ex: Trying to sell a complex supply chain mgmt software application through avge. computer reseller• Solution: distribution channel will change the pricing (higher)

65

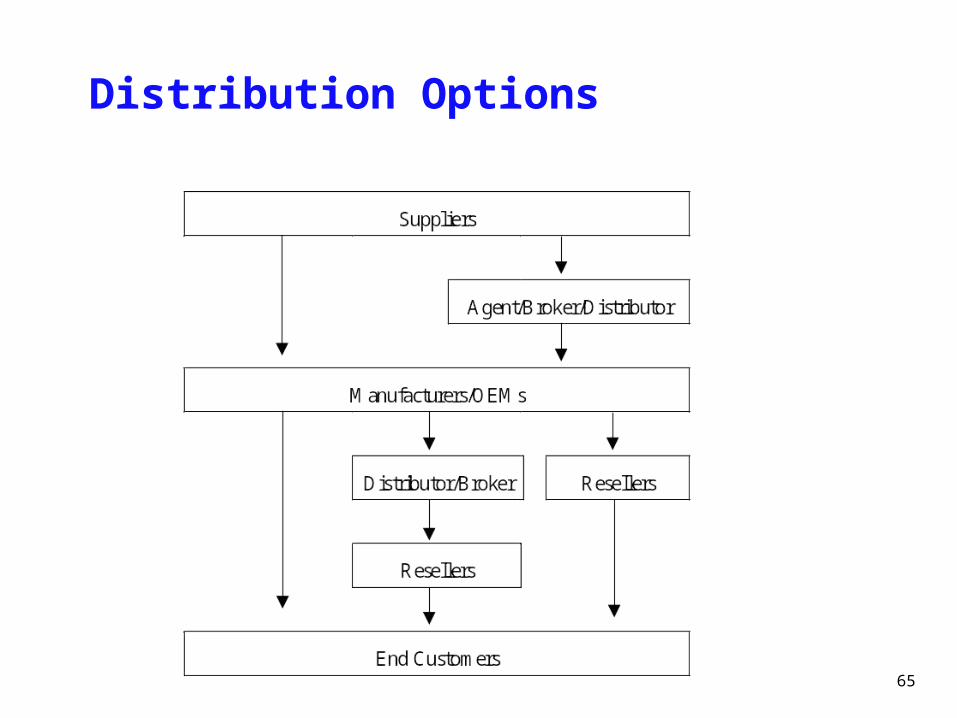

Distribution Options

66

Evaluation of Distribution Performance

Reseller’s contribution to supplier profits

Reseller’s contribution to supplier sales

Reseller’s contribution to growth

Reseller’s competence

Reseller’s compliance

Reseller’s adaptability

Reseller’s loyalty

Customer satisfaction with reseller

67

Blurring of Distinctions

• Distributors/resellers backward integrating into assembling products

• Suppliers forward integrating into computer manufacturing

• Channel assembly– Customization, speedy turnaround– Based on build-to-order model

• Co-location– Distributor’s employees work from vendor’s site – Customization

• Shift into services

68

Gray Markets

• Diversion of goods to unauthorized distributors, sold at discounted prices– Manufacturer loses control over distribution– Legitimate channels lose business– Loss of incentive for legitimate channel

members to push sales or provide service– Intra-brand competition, channel conflict

69

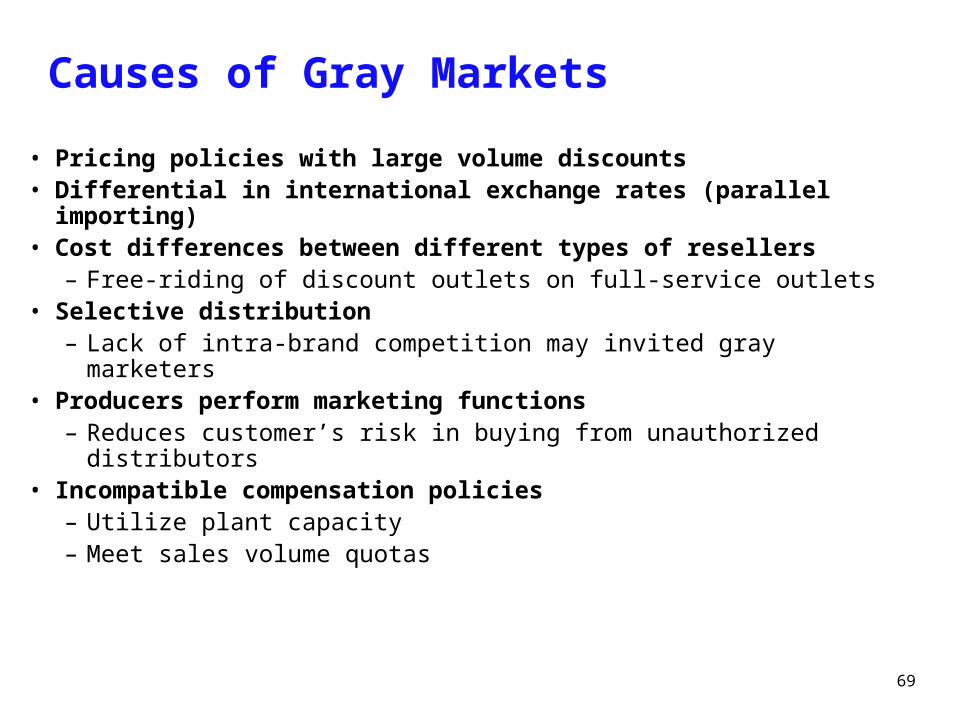

Causes of Gray Markets

• Pricing policies with large volume discounts• Differential in international exchange rates (parallel importing) • Cost differences between different types of resellers

– Free-riding of discount outlets on full-service outlets• Selective distribution

– Lack of intra-brand competition may invited gray marketers • Producers perform marketing functions

– Reduces customer’s risk in buying from unauthorized distributors• Incompatible compensation policies

– Utilize plant capacity– Meet sales volume quotas

70

Solutions to Gray Markets

• Track source of units and cut off supply to gray market– Signals commitment to legitimate channels – Mitigates price erosion– May be burdensome administratively

• One-price policy (no volume discounts)• Increase penetration in the market • Collect information on extent of the problem,

consistently measure channel member performance

71

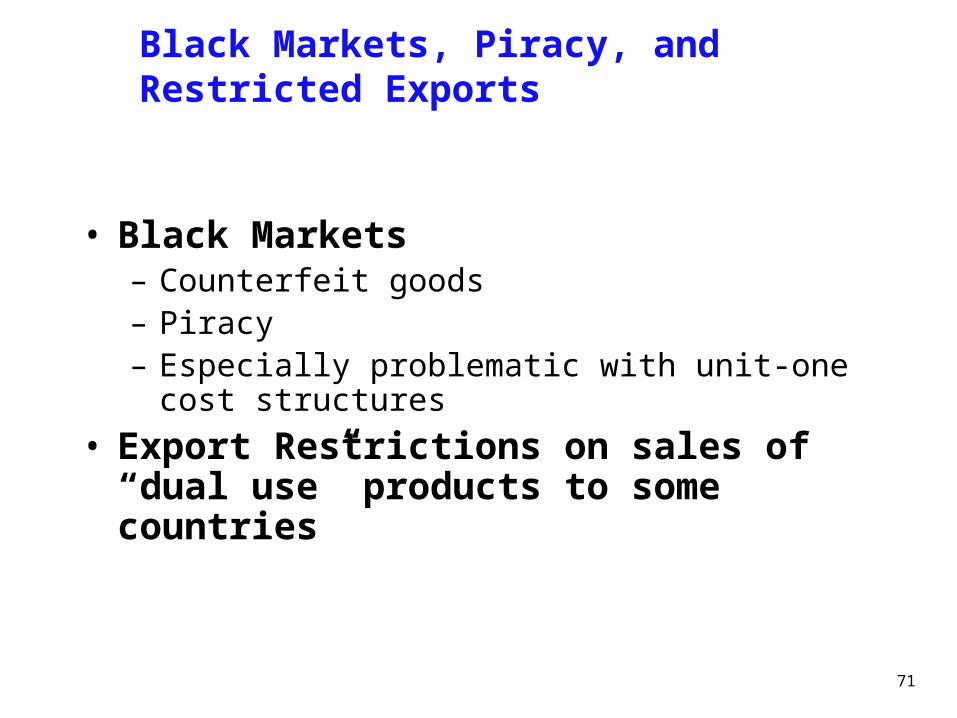

Black Markets, Piracy, and Restricted Exports

• Black Markets – Counterfeit goods– Piracy– Especially problematic with unit-one cost structures

• Export Restrictions on sales of “dual use” products to some countries

72

Adding New Channels: The Internet

• Hybrid channels – Conflicts between manufacturer and its dealers

pursuing same customers – “Co-opetition”

• Options – Avoid the Web (and conflict) – Go to the Web (invite conflict and even mutiny)– Disintermediate– Bricks-and-clicks model

73

Avoiding Conflict with Existing Channel

• Use website to disseminate only product information

• Use website only to generate leads; direct buyers to dealers

• Sell limited merchandise offerings through website

• Take online orders from small customers; direct larger customers to dealers

• Launch website without publicity

74

Trends in Supply Chain Management

• Vertical electronic markets on the Internet– Hubs used to connect suppliers to their manufacturing

customers– Often owned by cybermediaries

• Supply chain management software– Bring data from manufacturing, inventory, and suppliers

to integrate decision making

• Outsourcing– Reduces cost but increases supply chain vulnerability– Political backlash from unions and legislatures

75

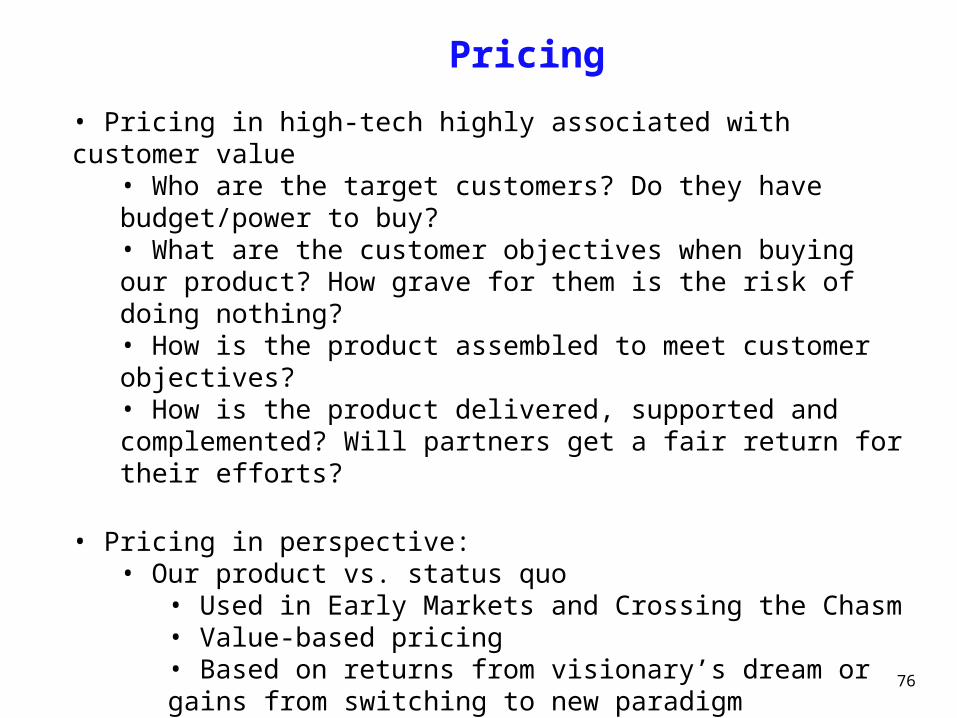

Pricing

Value-based

Competition-based

Gain Pain

Pricing Frame of Reference

Buyer Motivation

Early market Bowling alley

TornadoMain Street

vs. status quo vs. price leader

vs. market leadervs. status quo

76

Pricing

• Pricing in high-tech highly associated with customer value• Who are the target customers? Do they have budget/power to buy?• What are the customer objectives when buying our product? How grave for them is the risk of doing nothing?• How is the product assembled to meet customer objectives?• How is the product delivered, supported and complemented? Will partners get a fair return for their efforts?

• Pricing in perspective:• Our product vs. status quo

• Used in Early Markets and Crossing the Chasm• Value-based pricing• Based on returns from visionary’s dream or gains from switching to new paradigm• Inelastic• Pricing should reflect the need for margins in order to fund the creation of product infrastructure

77

Pricing

• Pricing in perspective:• Our product vs. market leader (used in tornado strategies)

• Product infrastructure is in place, product is commoditized• New Entrants in the industry

• Our product vs. Price Leader (Main Street)• Price can be higher or lower depending on strategy adopted (low price, differentiation, segmentation…)

78

Computing Customer Equity

-50

-40

-30

-20

-10

0

10

20

30

40

50

60

Year 1 Year 2 Year 3 Year 4 Year 5

Profit from Referrals

Profit from IncreasedPurchases

Base Profit

Acquisition Cost

79

Customer Acquisition Strategies

Retention ProfitPotential

Acquisition Investment Recovery Time

High

Low

Short Long

Take them all! Selective

Pay as You Go Restructure/Divest

80

Aspects of Cost to Serve

• Acquisition Costs

• Production Costs

• Distribution Costs

• Service Costs

81

Competition

Marketvs.

Market

Companyvs.

Company

Productvs.

Product

Categoryvs.

Category

Productvs.

Service

Reference competition (with a set of alternatives in the same category)Economic competition (set of alternatives competing for the same budget)

82

Basis for Positioning Strength

Thought leader in a new category

“Owns” one or more market niches

Has market share in a hypergrowth market

Continually makes great new offers

83

Next Target Customer

Mass market growth:Grow horizontally

into new channels,platforms, and geographies

The Tornado

Niche penetration:Dominate first niche

then go afteradjacent niches

The Bowling Alley

Niche expansion:Grow profitable

revenue from installed base through 1-on-1

marketing and mass customization

Main Street

The Early Market

Go get anotherbig deal

First customers

85

Strategy Thumbnail: Early Market

Target Customer

Compelling Reason to Buy

Whole Product

Partners and Allies

Distribution

Pricing

Competition

Positioning

Next Target Customer

Visionary LOB executive

Dramatic competitive advantage

Technology-based project

Consultants and integrators

Direct sales

Value-based, gain motivated

Category vs. category

Technology-based leadership

Another LOB exec in a different industry

89

Early Market Whole Product

• Technology Enthusiasts:• Value GENERIC PRODUCT• Will develop the elements pieces for making it work• GENERIC PRODUCT can be incomplete• Areas investigated in the core product by enthusiasts:

• Will technology work?• Will technology be supportable• Are other techies interested?• What are the camps forming around the product?

• Visionaries:• Value POTENTIAL PRODUCT: Ability of the product in creating competitive advantage• They will need strong system integrator partnership for transforming the CORE into the POTENTIAL PRODUCT of a specific application• Selling argument: The possibilities associated with specific applications of the emerging technology

96

Strategy Thumbnail: Bowling Alley

Target Customer

Compelling Reason to Buy

Whole Product

Partners and Allies

Distribution

Pricing

Competition

Positioning

Next Target Customer

Pragmatist departmental manager

Fix a problem business process

Niche-focused application

Emerging value chain

Direct sales transitioning to VARs

Value-based, pain motivated

Market vs. market

Niche market leadership

Adjacent niche market

108

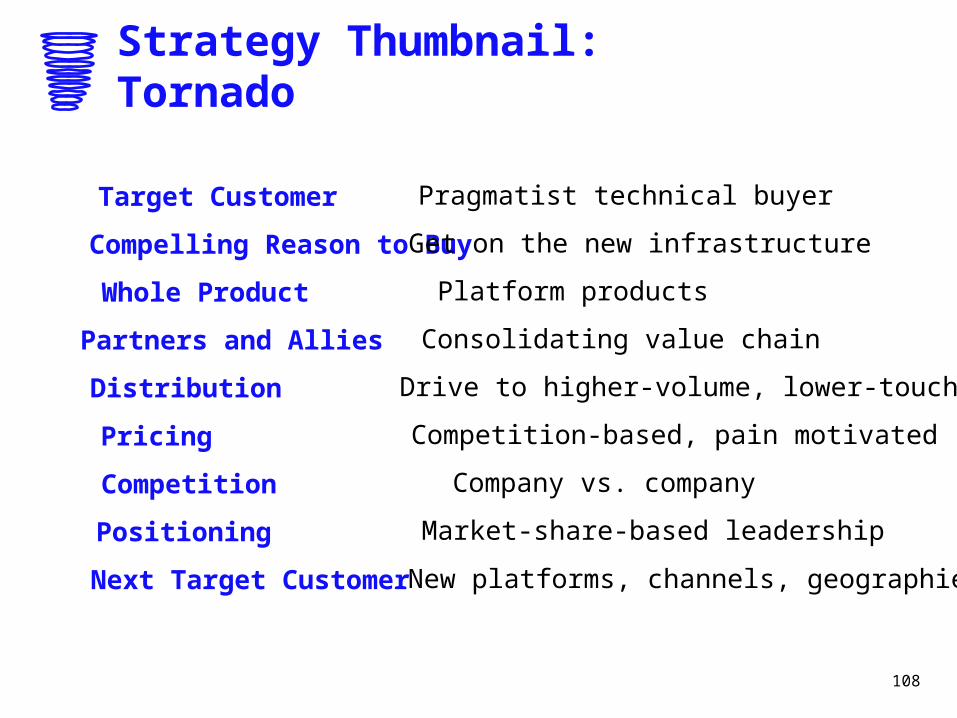

Strategy Thumbnail: Tornado

Target Customer

Compelling Reason to Buy

Whole Product

Partners and Allies

Distribution

Pricing

Competition

Positioning

Next Target Customer

Pragmatist technical buyer

Get on the new infrastructure

Platform products

Consolidating value chain

Drive to higher-volume, lower-touch

Competition-based, pain motivated

Company vs. company

Market-share-based leadership

New platforms, channels, geographies

119

Strategy Thumbnail: Main Street

Target Customer

Compelling Reason to Buy

Whole Product

Partners and Allies

Distribution

Pricing

Competition

Positioning

Next Target Customer

End-users

Better values with no risk

Add-ons, consumables, transactions

Disintermediated value chain

Low-cost, high-touch

Competition-based, gain motivated

Offer vs. offer

Better experience for end users

Next micro-niche

Related Documents

![Big Data and Analytics for Manufacturing and High-Tech Industries [ CON8257]](https://static.cupdf.com/doc/110x72/568139c5550346895da16ef7/big-data-and-analytics-for-manufacturing-and-high-tech-industries-con8257-568b58b5969e6.jpg)