1 CYS COST ALLOCATION WORKSHOP March 26 - 28, 2007 Chicago, Illinois Presented by R. Armstrong

1 CYS COST ALLOCATION WORKSHOP March 26 - 28, 2007 Chicago, Illinois Presented by R. Armstrong.

Dec 16, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

CYS COST ALLOCATION WORKSHOP

March 26 - 28, 2007

Chicago, Illinois

Presented by R. Armstrong

2

AGENDA – Cost Allocation

INTRODUCTIONS PURPOSE QUESTIONS ELEMENTS - COST ALLOCATION PLAN QUESTION COSTS UNALLOWABLE METHODS OF ALLOCATION THREE PROGRAM FIGURATIONS SUGGESTED BASES FOR COST ALLOCATION EXERCISES REFERENCES WRAP UP

3

PURPOSE

To provide overview of cost allocation and how to avoid question costs

To assist Delegates and Partners required to prepare a cost allocation plan

4

PRE and POST QUESTIONS

1. What is the purpose of a cost allocation plan?

2. Is an indirect cost rate the same as a cost allocation plan? Yes or No

3. My agency is a freestanding organization that provides only Head Start services and has no other source of funding.

Is a cost allocation plan required?

Yes or No

5

5. A Head Start grantee in collaboration with the State child care funding source (CCDF) provides a full day of Head Start services which meet all of the Performance Standards for the entire period at the Head Start facility. The grantee includes in its proposed budget reimbursement from CCDF through direct funding from the State or through certificates or vouchers from the parents. If all children are enrolled in Head Start and are receiving services which meet the Performance Standards, is a cost allocation plan required?

Yes or No

6

5.Can a grantee with multiple sources of funding have both an indirect cost rate and a cost allocation plan?

Yes or No

6. Is there any restriction on outside CPA firm performing the annual audit and preparing the cost allocation plan for your agency?

Yes or No

7

COST ALLOCATION

Means the process of assigning to two or more programs the costs of an item shared by the programs. The goal is to ensure that each program bears its fair share, and only its fair share, of the total cost of the item.H. S. Fiscal Assistant – Cost Allocation

8

Cost Allocation Plan

A written account of the methods used by the grantee to allocate costs to its various funding sources.

In order to document that costs have been properly allocated, the grantee must have a written plan.

9

FISCAL CHECKLIST - 2007

SECTION II – USE OF HEAD START GRANT FUNDS

Compliance Question #2B If the grantee and delegate have shared

costs with other programs, have they used an allocation base that best measures the relative degree of benefit for all benefiting functions?

2 CFR Part 230, Appendix A, Nonprofit Organizations

10

Designate Person to Answer Fiscal Questions

Does the delegate have a cost allocation plan that describes the methodology for allocating shared costs?

Is the allocation methodology based on current data?

Does the delegate have a process to establish that estimated data used in the allocation process is reasonable?

11

Are occupancy costs based on the proportion of usable space occupied by each program?

Are salaries allocated based on the employee’s actual activity in each program?

12

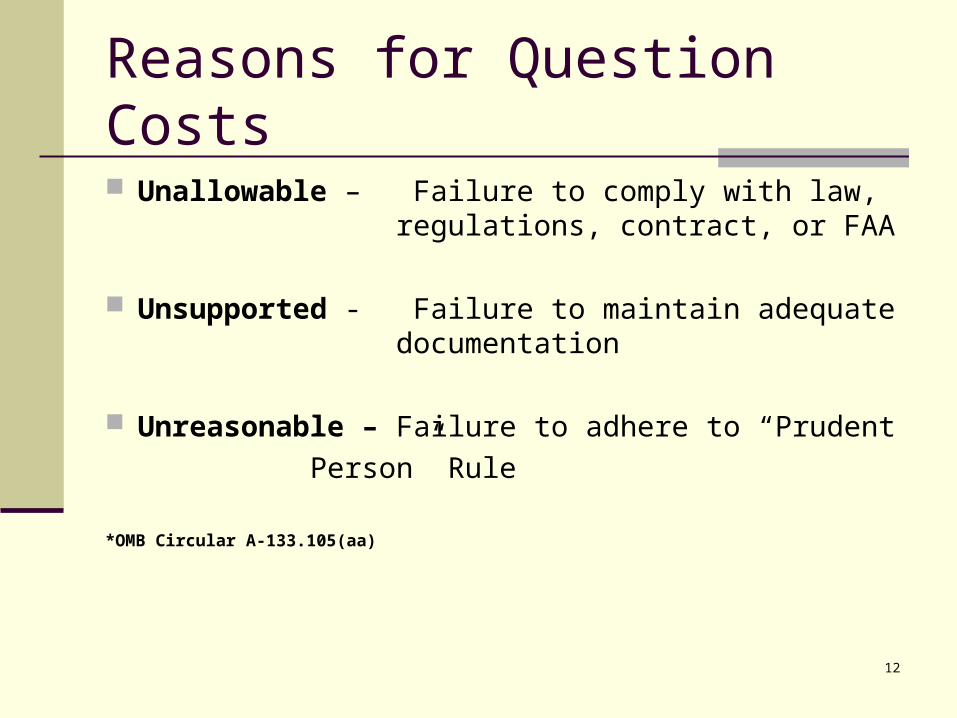

Reasons for Question Costs

Unallowable – Failure to comply with law, regulations, contract, or FAA

Unsupported - Failure to maintain adequate documentation

Unreasonable – Failure to adhere to “Prudent

Person” Rule

*OMB Circular A-133.105(aa)

13

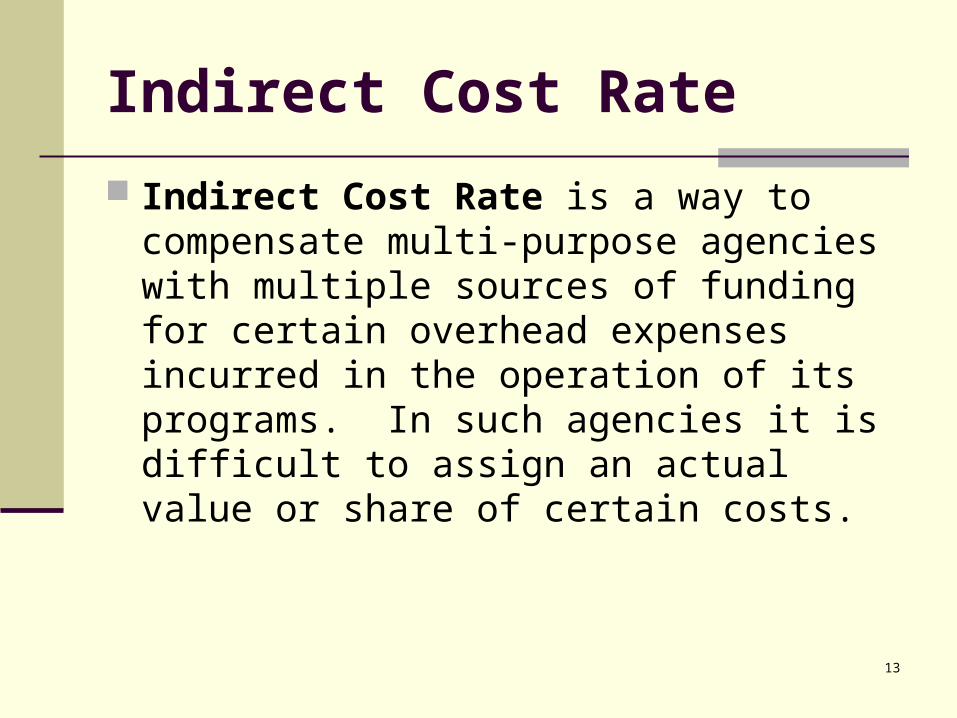

Indirect Cost Rate

Indirect Cost Rate is a way to compensate multi-purpose agencies with multiple sources of funding for certain overhead expenses incurred in the operation of its programs. In such agencies it is difficult to assign an actual value or share of certain costs.

14

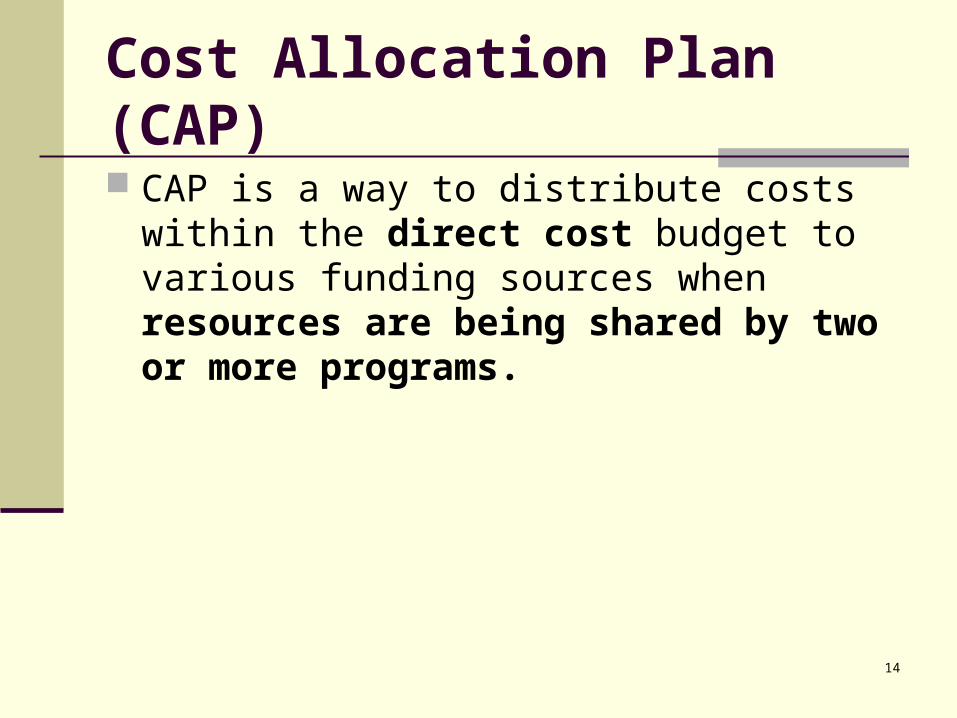

Cost Allocation Plan (CAP)

CAP is a way to distribute costs within the direct cost budget to various funding sources when resources are being shared by two or more programs.

15

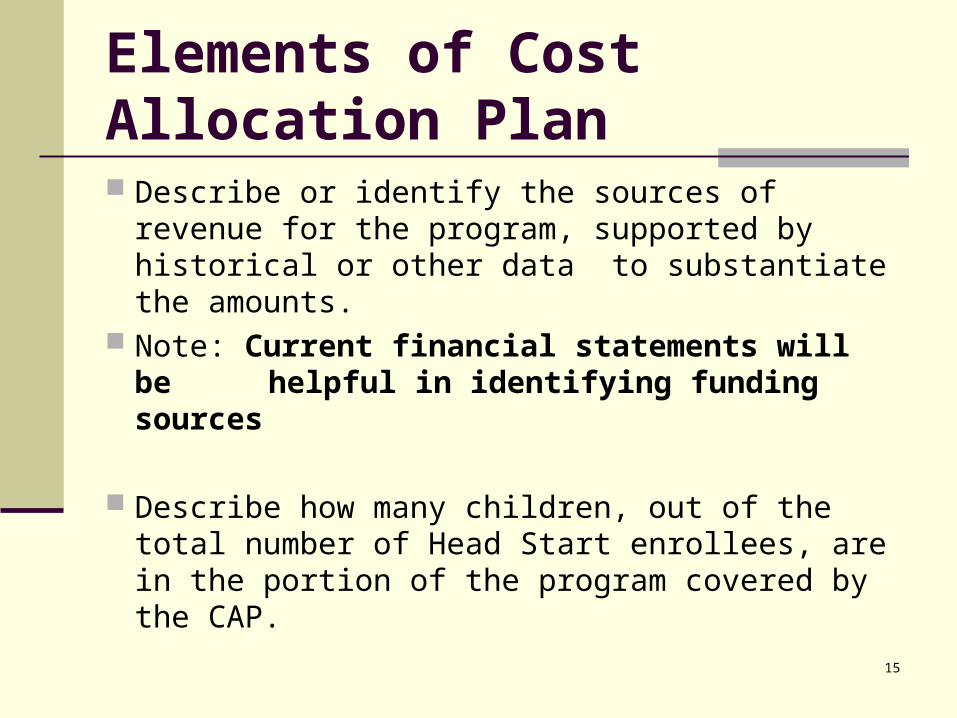

Elements of Cost Allocation Plan

Describe or identify the sources of revenue for the program, supported by historical or other data to substantiate the amounts.

Note: Current financial statements will be helpful in identifying funding

sources

Describe how many children, out of the total number of Head Start enrollees, are in the portion of the program covered by the CAP.

16

Describe the methodology used to determine the allocation of the costs of services to the various funding sources.

Describe the basis for allocating costs within specific cost categories (personnel, space, supplies, etc.) and a description of how expenditures within the major cost categories will be apportioned and recorded in the grantee’s accounting system.

NOTE: An organization chart will be helpful.

17

EXCEPTION TO COST ALLOCATION PLAN When there is a collaborative activity between

Head Start and another Federal child care or early education program, two cost categories, equipment and nonconsumable supplies, do not have to be allocated between the programs, so long as Head Start is the predominant source of funding for the activity.

*Section 640 (a)(5)(E) of the Head Start Act

18

UNALLOWABLE METHODS OF ALLOCATION

Head Start has the largest budget, so Head Start should pay the largest share of costs

Estimates of time spent on a program or activity

New funds are used only for the increased incremental cost--- not its fair share of costs

19

PRISM Cost Allocation Finding

NONPROFIT ORGANIZATIONS

45 CFR 74.21(b)(6)

Lack of written procedures for determining allowability, allocability, and reasonableness of costs in accordance with the provisions of the applicable Federal costs principles and conditions of the award

20

COMMON CONFIGURATIONS

Agency program is entirely Head Start

Agency manages a Head Start program and in collaboration with the state funding source provides a full day of Head Start services. Agency includes reimbursement in its grant application with HHS.

Agency manages two or more separate programs that do not share costs

Agency has two or more programs which it operates as a single program with shared resources. This is a multiple purpose agency and requires a cost allocation plan.

21

SUGGESTIONS-ALLOCATION

The allocation base selected must be Reasonable and consistently applied Supported by accurate and current data Appropriate to the particular cost being

distributed Must result in an accurate measure of the

benefits provided to each program

22

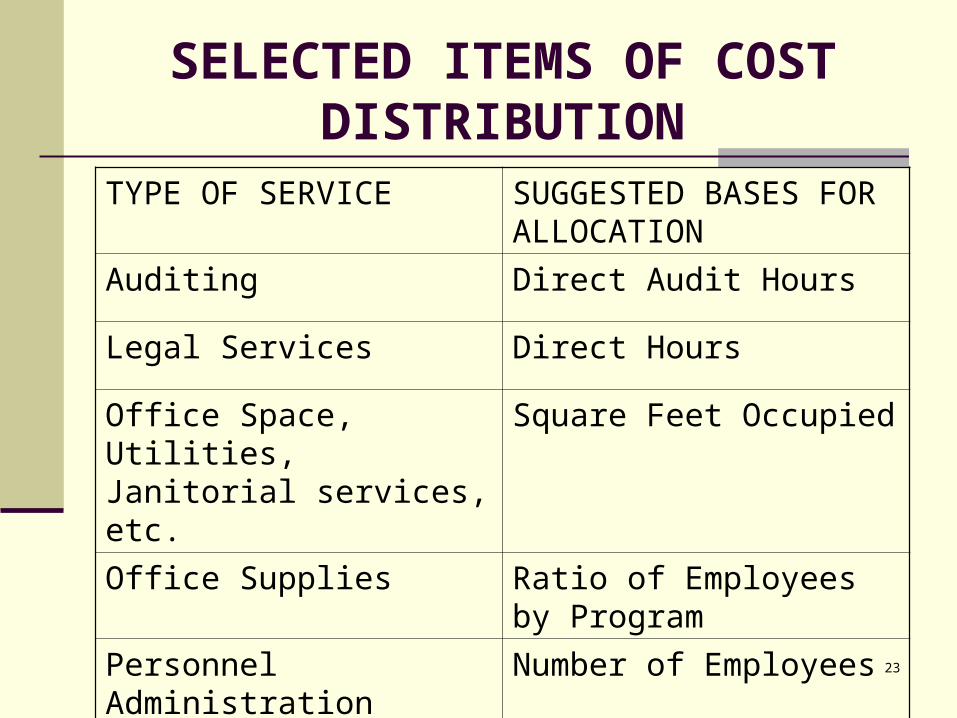

SUGGESTED BASES FOR COST DISTRIBUTION The handout contains suggested allocation

bases that might be used to direct charge joint costs to Federal awards and other activities of the grantee.

The bases are suggestions only, and should not be used if they are not suitable for the particular service involved.

ANY METHOD OF ALLOCATION CAN BE USED WHICH WILL PRODUCE AN EQUITABLE DISTRIBUTION OF COSTS

23

SELECTED ITEMS OF COST DISTRIBUTION

TYPE OF SERVICE SUGGESTED BASES FOR ALLOCATION

Auditing Direct Audit Hours

Legal Services Direct Hours

Office Space, Utilities, Janitorial services, etc.

Square Feet Occupied

Office Supplies Ratio of Employees by Program

Personnel Administration Number of Employees

Telephone – Local Number of Telephones

24

HANDOUTS

Cost Allocation Narrative

ACYF-IM-HS-01-06 dated 3/8/01

Exercises

25

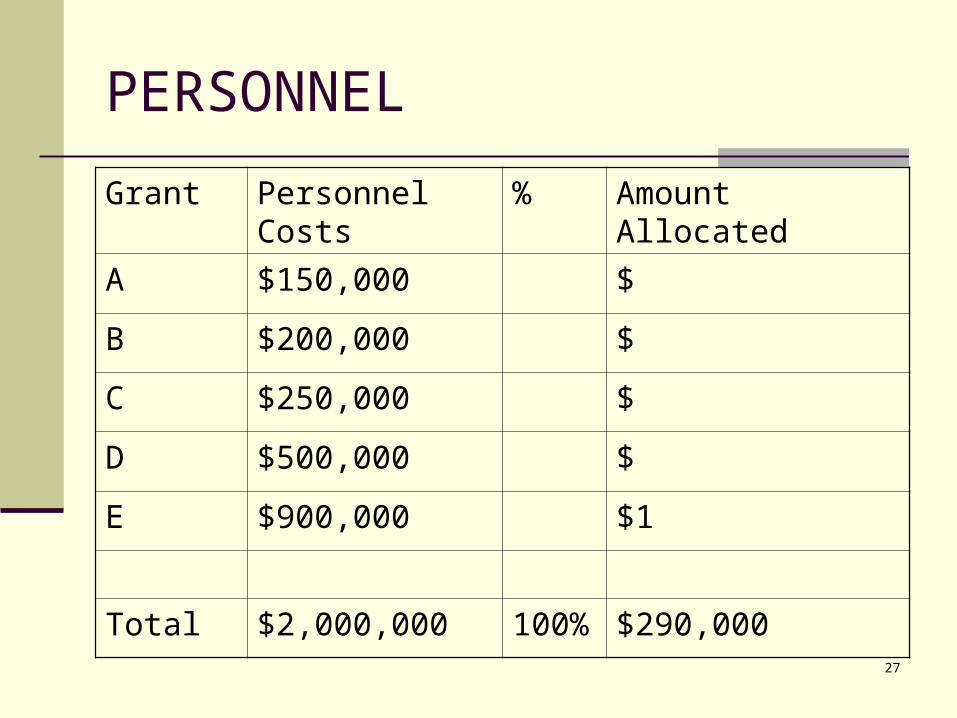

PERSONNEL

Costs that benefit all programs are allocated based on a ratio of each program’s personnel costs (salaries and fringe benefits) to total personnel costs.

26

PERSONNEL

The total salaries for five programs are $2,000,000 to be divided as follows: A $150,000; B $200,000; C $250,000; D $500,000; and E $900,000. The total costs to be distributed for this agency is $290,000 for accounting, human resources, MIS, and executive office. These costs benefit all five programs and are to be distributed based upon your analysis. Fringe benefits are to be distributed in the same manner as salaries.

Your assignment is to determine the method you would use to allocate the costs, reason for choice, and then allocate the costs among the five programs.

27

PERSONNEL

Grant Personnel Costs % Amount Allocated

A $150,000 $

B $200,000 $

C $250,000 $

D $500,000 $

E $900,000 $1

Total $2,000,000 100% $290,000

28

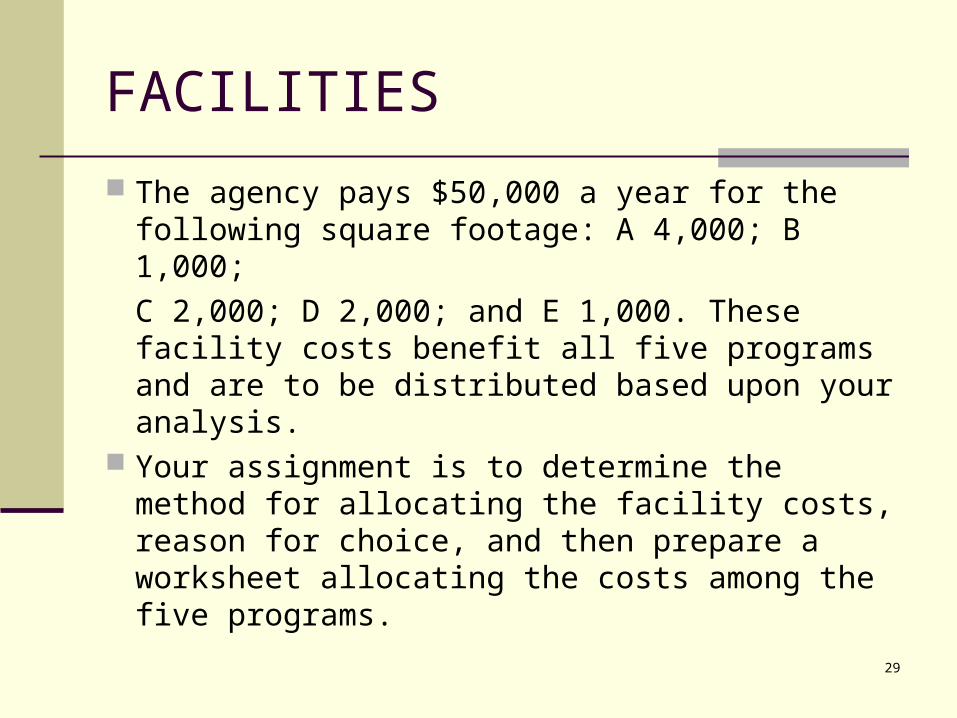

FACILITIES

Facilities cost that benefit all programs are allocated based upon a ratio of square footage used by each program compared to the total square footage of the facility.

NOTE: Do not forget to include square feet for the common areas. e.g.

hallways

29

FACILITIES

The agency pays $50,000 a year for the following square footage: A 4,000; B 1,000;

C 2,000; D 2,000; and E 1,000. These facility costs benefit all five programs and are to be distributed based upon your analysis.

Your assignment is to determine the method for allocating the facility costs, reason for choice, and then prepare a worksheet allocating the costs among the five programs.

30

FACILITIES

Grant Square Footage

% $ Square Foot

Amount Allocated

A 4,000 $ $

B 1,000 $ $

C 2,000 $ $

D 2,000 $ $

E 1,000 $ $

Total 10,000 100 $ $50,000

31

PRINTING

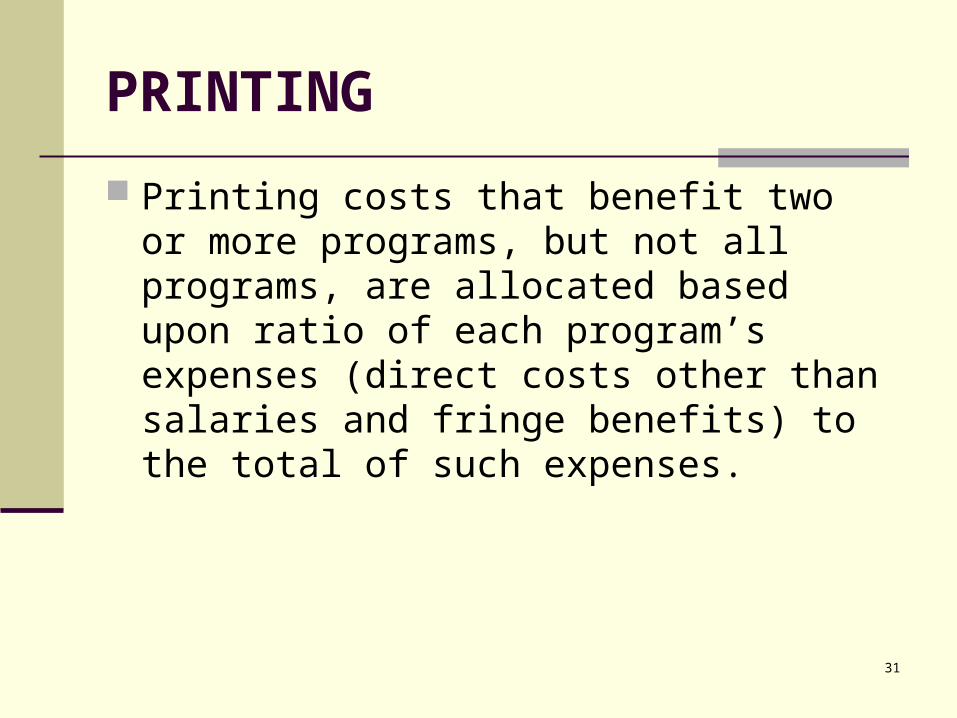

Printing costs that benefit two or more programs, but not all programs, are allocated based upon ratio of each program’s expenses (direct costs other than salaries and fringe benefits) to the total of such expenses.

32

PRINTING

The agency pays $12,000 for printing costs that are shared with A, B, and D programs. The costs for the programs, other than salaries and fringe benefits, are as follows: A $150,000; B $200,000; D $250,000; and E $500,000. C and E programs have their own printers and thus do not share any printing costs.

Your assignment is to determine the method for allocating printing costs, reasons for choice, and then prepare a worksheet allocating the costs among the three programs.

33

PRINTING – One Method

Grant Program Expenses (other than salaries)

% Amount Allocated

A $150,000 $

B $200,000 $

D $250,000 $

Total $600,000 100% $12,000

34

QUESTIONS

1. See Slide #7 2. No, See Slide #13 3. No, See Fiscal Assistant 4. No, See ACYF-IM-HS-01-13 5. Yes, See Fiscal Assistant 6. Yes, See Fiscal Assistant

35

REFERENCES

FINANCIAL MANAGEMENT ISSUES IN HEAD START PROGRAMS…

ACYF-IM-HS-01-06 BUDGETING for PARTNERSHIPS between

CHILD CARE and HEAD START

ACYF-IM-HS-01-13 FISCAL ASSISTANT, COST ALLOCATION

36

Summary of Cost Distribution Requirements

Head Start only budget Cost allocation not required

Head Start budget with reimbursement from other program sourcesCost Allocation not required

Joint use of Head Start resources with other non-Head Start sourcesCost allocation required and costs of resource must be fairly allocated among the program sources so that programs share costs in accordance with the benefits derived

*****

Related Documents

![Modèles structuraux et fonctionnels du site actif des … · 2014. 10. 4. · Ni Cys-S S S Cys-S Fe CN CN CO Cys Cys Site actif des H2ases [NiFe] Dérivés du [Ni(xbsms)]: 1. Synthèse](https://static.cupdf.com/doc/110x72/5fc526ed9695db7c55538df1/modles-structuraux-et-fonctionnels-du-site-actif-des-2014-10-4-ni-cys-s-s.jpg)