© 2004 The McGraw-Hill Companies, Inc. McGraw-Hill/Irwin Chapter 14 Chapter 14 Bonds and Bonds and Long-Term Notes Long-Term Notes

© 2004 The McGraw-Hill Companies, Inc. McGraw-Hill/Irwin Chapter 14 Bonds and Long-Term Notes.

Dec 19, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Chapter 14Chapter 14

Bonds andBonds andLong-Term NotesLong-Term Notes

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-2

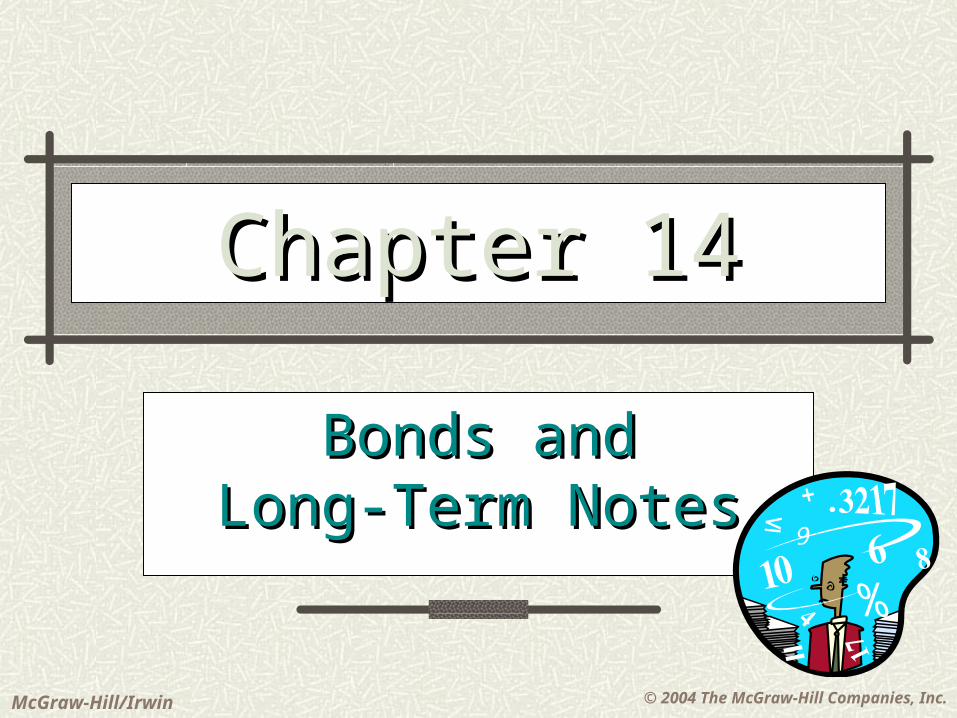

Nature of Long-Term Debt

Obligations that extend Obligations that extend beyond one year or the beyond one year or the

operating cycle, operating cycle, whichever is longerwhichever is longer

Obligations that extend Obligations that extend beyond one year or the beyond one year or the

operating cycle, operating cycle, whichever is longerwhichever is longer

Mirror image of an Mirror image of an assetasset

Mirror image of an Mirror image of an assetasset

Accrue interest Accrue interest expenseexpense

Accrue interest Accrue interest expenseexpense

Reported at present Reported at present valuevalue

Reported at present Reported at present valuevalue

Loan agreement Loan agreement restrictionsrestrictions

Loan agreement Loan agreement restrictionsrestrictions

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-3

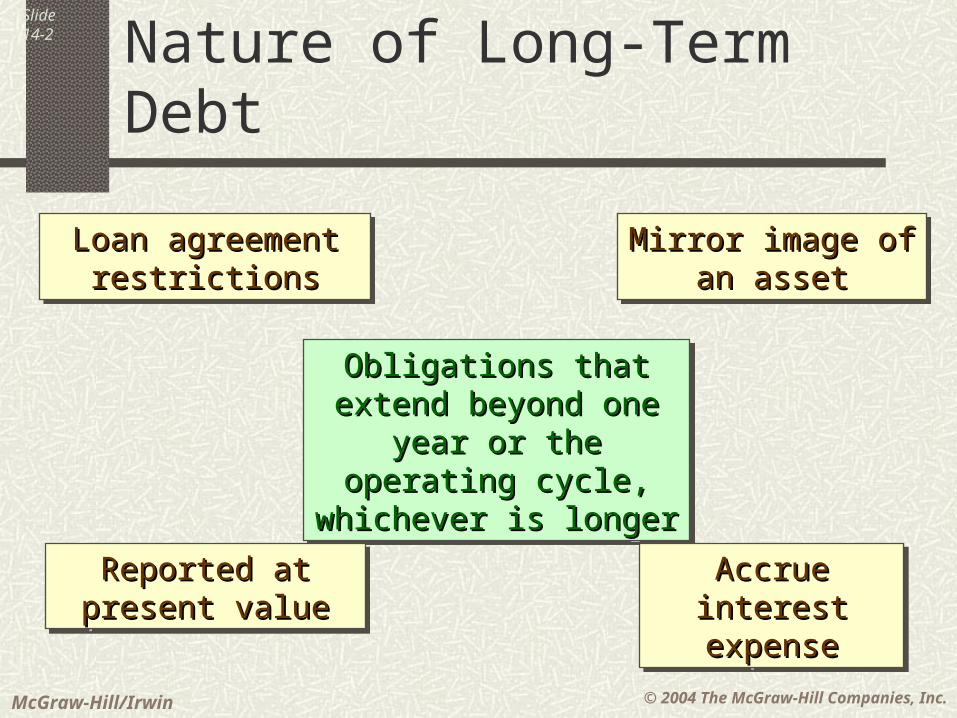

Bonds

Bond Selling PriceBond Selling Price

Bond CertificateBond Certificate

Interest PaymentsInterest Payments

Face Value Payment at Face Value Payment at End of Bond TermEnd of Bond Term

At Bond Issuance DateAt Bond Issuance Date

Company Company Issuing Issuing BondsBonds

Company Company Issuing Issuing BondsBonds

Subsequent PeriodsSubsequent Periods

Investor Investor Buying Buying BondsBonds

Investor Investor Buying Buying BondsBonds

Company Company Issuing Issuing BondsBonds

Company Company Issuing Issuing BondsBonds

Investor Investor Buying Buying BondsBonds

Investor Investor Buying Buying BondsBonds

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-4

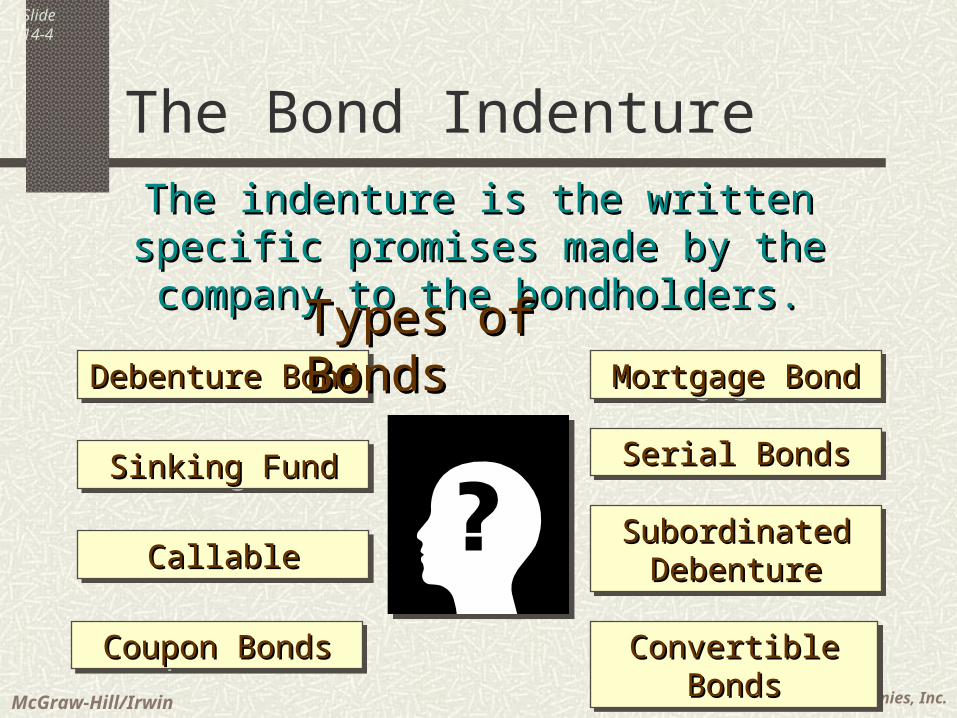

The Bond Indenture

Debenture BondDebenture BondDebenture BondDebenture Bond Mortgage BondMortgage BondMortgage BondMortgage Bond

Subordinated Subordinated DebentureDebenture

Subordinated Subordinated DebentureDebenture

Coupon BondsCoupon BondsCoupon BondsCoupon Bonds

CallableCallableCallableCallable

Sinking FundSinking FundSinking FundSinking Fund Serial BondsSerial BondsSerial BondsSerial Bonds

Convertible BondsConvertible BondsConvertible BondsConvertible Bonds

The indenture is the written specific promises The indenture is the written specific promises made by the company to the bondholders.made by the company to the bondholders.

Types of BondsTypes of Bonds

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-5

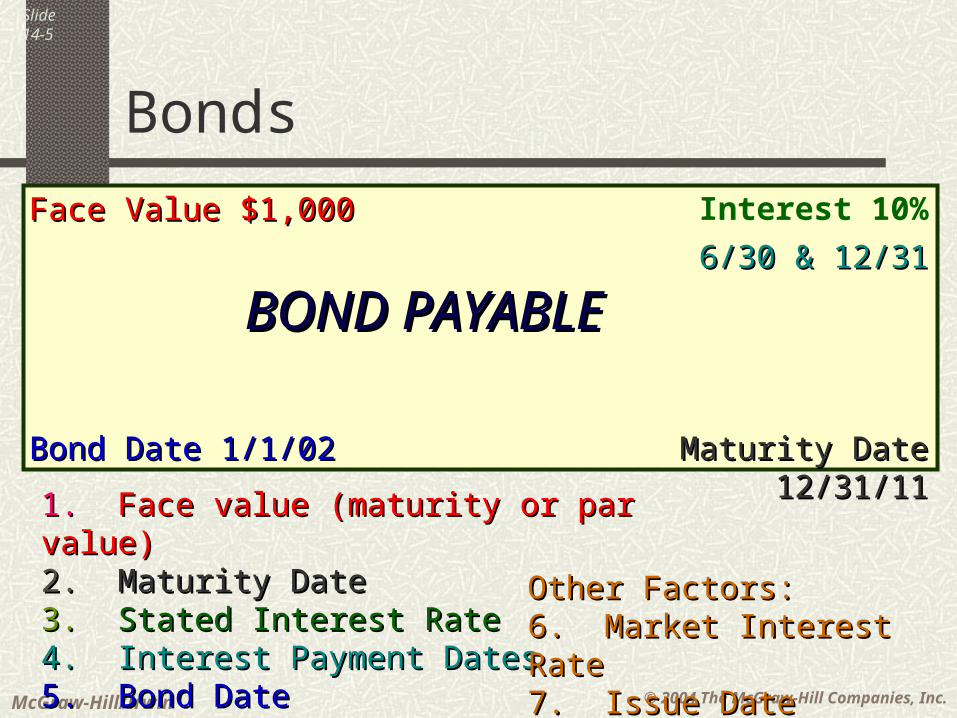

Bonds

BOND PAYABLEBOND PAYABLE

Face Value $1,000Face Value $1,000 Interest 10%

6/30 & 12/316/30 & 12/31

Maturity Date 12/31/11Maturity Date 12/31/11Bond Date 1/1/02Bond Date 1/1/02

1. 1. Face value (maturity or par value)Face value (maturity or par value)2. 2. Maturity DateMaturity Date3. 3. Stated Interest RateStated Interest Rate 4.4. Interest Payment DatesInterest Payment Dates5. Bond Date5. Bond Date

Other Factors:Other Factors:6. Market Interest Rate6. Market Interest Rate7. Issue Date7. Issue Date

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-6

Recording Bonds at Issuance

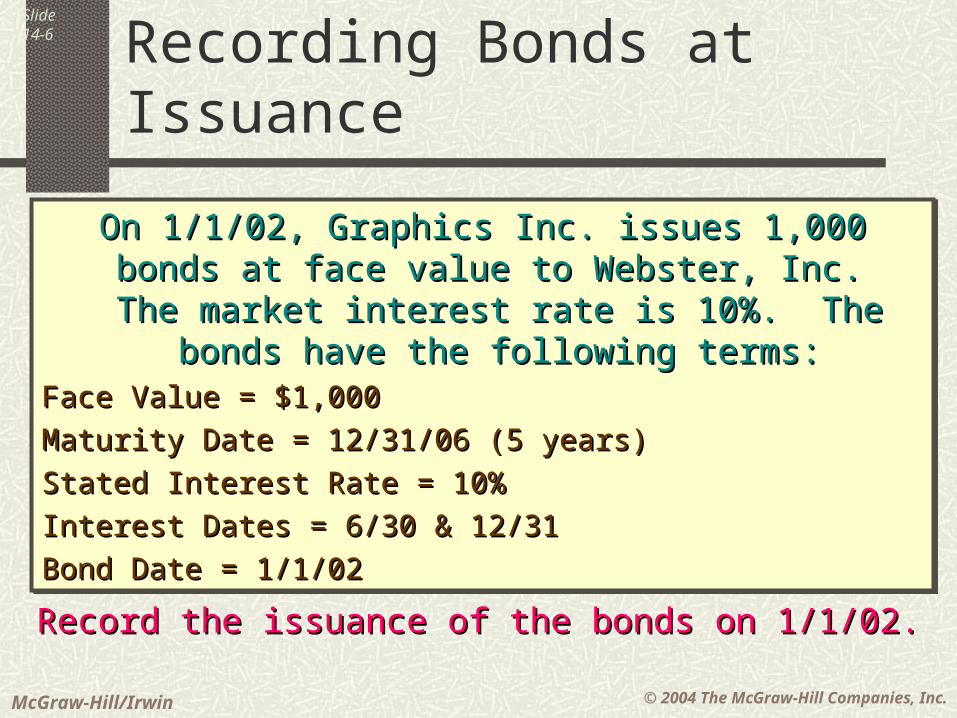

On 1/1/02, Graphics Inc. issues 1,000 bonds at face On 1/1/02, Graphics Inc. issues 1,000 bonds at face value to Webster, Inc. The market interest rate is value to Webster, Inc. The market interest rate is

10%. The bonds have the following terms:10%. The bonds have the following terms:Face Value = $1,000Face Value = $1,000

Maturity Date = 12/31/06 (5 years) Maturity Date = 12/31/06 (5 years)

Stated Interest Rate = 10%Stated Interest Rate = 10%

Interest Dates = 6/30 & 12/31Interest Dates = 6/30 & 12/31

Bond Date = 1/1/02Bond Date = 1/1/02

On 1/1/02, Graphics Inc. issues 1,000 bonds at face On 1/1/02, Graphics Inc. issues 1,000 bonds at face value to Webster, Inc. The market interest rate is value to Webster, Inc. The market interest rate is

10%. The bonds have the following terms:10%. The bonds have the following terms:Face Value = $1,000Face Value = $1,000

Maturity Date = 12/31/06 (5 years) Maturity Date = 12/31/06 (5 years)

Stated Interest Rate = 10%Stated Interest Rate = 10%

Interest Dates = 6/30 & 12/31Interest Dates = 6/30 & 12/31

Bond Date = 1/1/02Bond Date = 1/1/02

Record the issuance of the bonds on 1/1/02.Record the issuance of the bonds on 1/1/02.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-7

Recording Bonds at Issuance

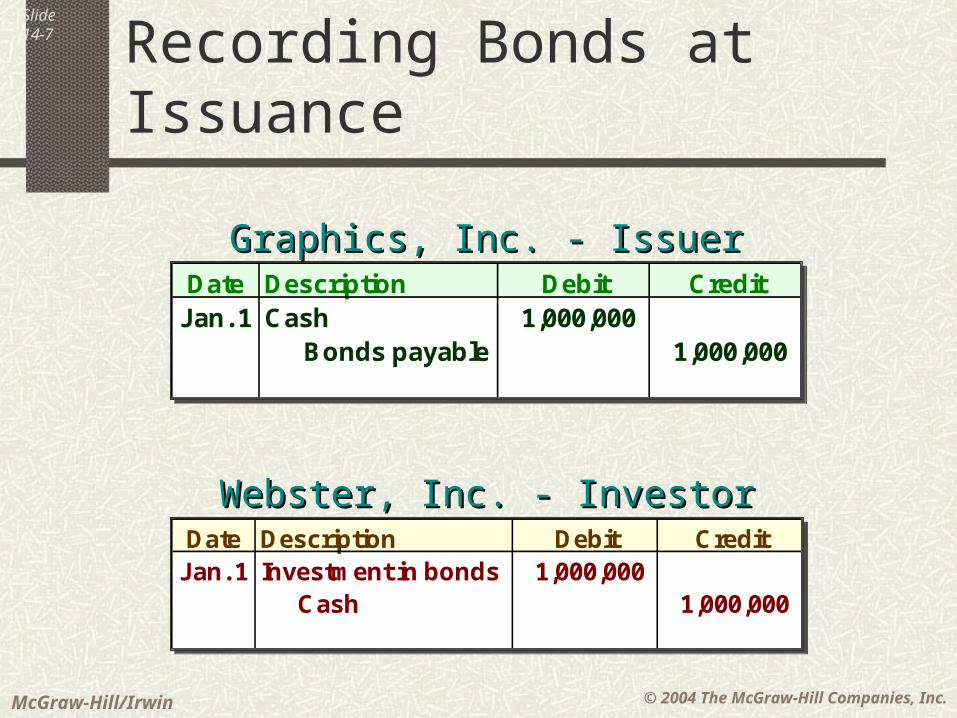

Date Description Debit CreditJan. 1 Cash 1,000,000

Bonds payable 1,000,000

Date Description Debit CreditJan. 1 Cash 1,000,000

Bonds payable 1,000,000

Graphics, Inc. - IssuerGraphics, Inc. - Issuer

Date Description Debit CreditJan. 1 Investment in bonds 1,000,000

Cash 1,000,000

Date Description Debit CreditJan. 1 Investment in bonds 1,000,000

Cash 1,000,000

Webster, Inc. - InvestorWebster, Inc. - Investor

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-8

Bonds Issued Between Interest Date

Interest begins to accrue on the date the Interest begins to accrue on the date the bonds are dated. If the bonds are issued bonds are dated. If the bonds are issued after the day they are dated, the investor after the day they are dated, the investor

would be asked to pay the company would be asked to pay the company accrued interest. On the interest payment accrued interest. On the interest payment date, the investor will receive a check for date, the investor will receive a check for

the full period’s interest.the full period’s interest.

Interest begins to accrue on the date the Interest begins to accrue on the date the bonds are dated. If the bonds are issued bonds are dated. If the bonds are issued after the day they are dated, the investor after the day they are dated, the investor

would be asked to pay the company would be asked to pay the company accrued interest. On the interest payment accrued interest. On the interest payment date, the investor will receive a check for date, the investor will receive a check for

the full period’s interest.the full period’s interest.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-9

Bonds Issued Between Interest Date

On On 2/1/022/1/02, Graphics Inc. issues 1,000 bonds at face , Graphics Inc. issues 1,000 bonds at face value plus accrued interest to Webster, Inc. The value plus accrued interest to Webster, Inc. The market interest rate is 10%. The bonds have the market interest rate is 10%. The bonds have the

following terms:following terms:Face Value = $1,000Face Value = $1,000

Maturity Date = 12/31/06 (5 years) Maturity Date = 12/31/06 (5 years)

Stated Interest Rate = 10%Stated Interest Rate = 10%

Interest Dates = 6/30 & 12/31Interest Dates = 6/30 & 12/31

Bond Date = Bond Date = 1/1/021/1/02

On On 2/1/022/1/02, Graphics Inc. issues 1,000 bonds at face , Graphics Inc. issues 1,000 bonds at face value plus accrued interest to Webster, Inc. The value plus accrued interest to Webster, Inc. The market interest rate is 10%. The bonds have the market interest rate is 10%. The bonds have the

following terms:following terms:Face Value = $1,000Face Value = $1,000

Maturity Date = 12/31/06 (5 years) Maturity Date = 12/31/06 (5 years)

Stated Interest Rate = 10%Stated Interest Rate = 10%

Interest Dates = 6/30 & 12/31Interest Dates = 6/30 & 12/31

Bond Date = Bond Date = 1/1/021/1/02

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-10

Bonds Issued Between Interest Date

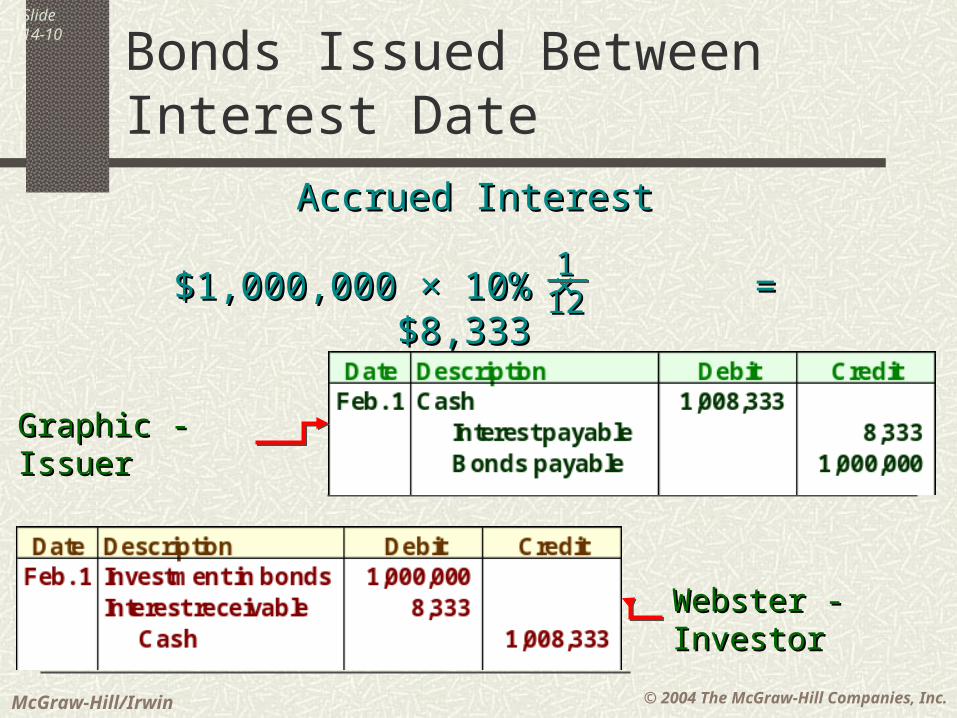

Accrued InterestAccrued Interest

$1,000,000 $1,000,000 × 10% × 10% × = $8,333× = $8,333 11

1212

Graphic - IssuerGraphic - Issuer

Webster - InvestorWebster - Investor

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-11

Bonds Issued Between Interest Date

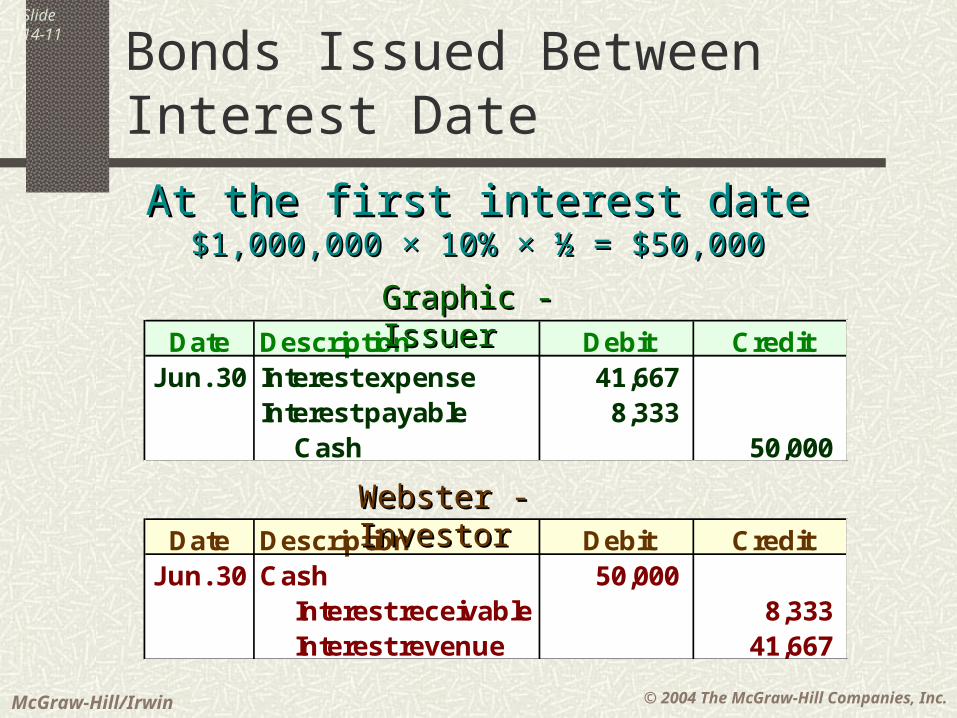

At the first interest dateAt the first interest date$1,000,000 $1,000,000 × 10% × ½ = $50,000× 10% × ½ = $50,000

Date Description Debit CreditJun. 30 Interest expense 41,667

Interest payable 8,333 Cash 50,000

Graphic - IssuerGraphic - Issuer

Date Description Debit CreditJun. 30 Cash 50,000

Interest receivable 8,333 Interest revenue 41,667

Webster - InvestorWebster - Investor

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-12

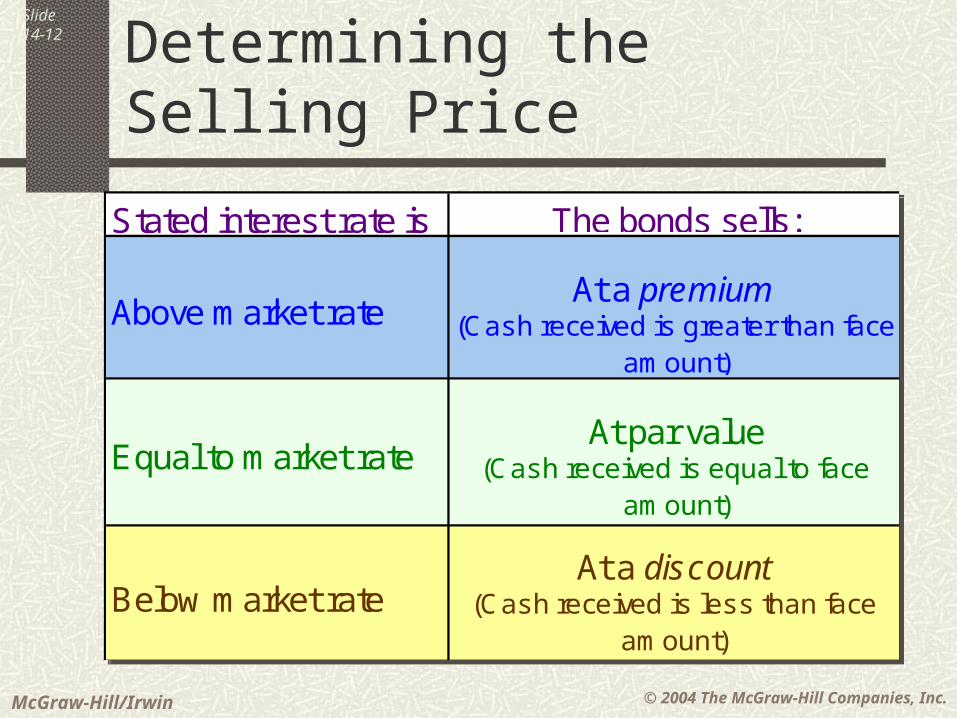

Determining the Selling Price

Stated interest rate is The bonds sells:

Above market rateAt a premium

(Cash received is greater than face amount)

Equal to market rateAt par value

(Cash received is equal to face amount)

Below market rateAt a discount

(Cash received is less than face amount)

Stated interest rate is The bonds sells:

Above market rateAt a premium

(Cash received is greater than face amount)

Equal to market rateAt par value

(Cash received is equal to face amount)

Below market rateAt a discount

(Cash received is less than face amount)

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-13

Determining the Selling Price

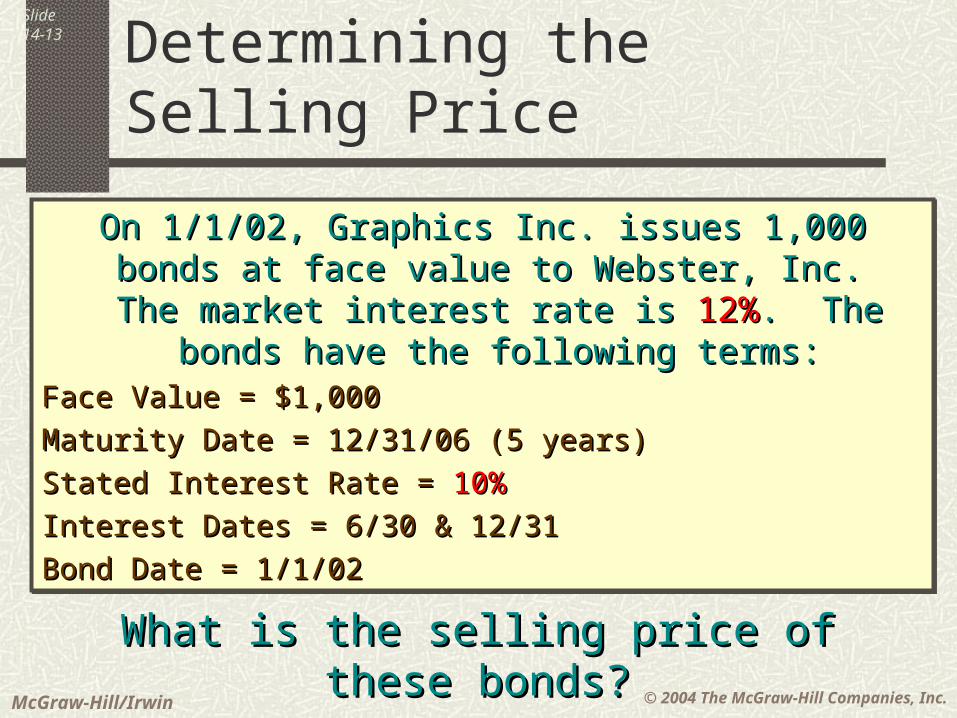

On 1/1/02, Graphics Inc. issues 1,000 bonds at face On 1/1/02, Graphics Inc. issues 1,000 bonds at face value to Webster, Inc. The market interest rate is value to Webster, Inc. The market interest rate is

12%12%. The bonds have the following terms:. The bonds have the following terms:Face Value = $1,000Face Value = $1,000

Maturity Date = 12/31/06 (5 years) Maturity Date = 12/31/06 (5 years)

Stated Interest Rate = Stated Interest Rate = 10%10%

Interest Dates = 6/30 & 12/31Interest Dates = 6/30 & 12/31

Bond Date = 1/1/02Bond Date = 1/1/02

On 1/1/02, Graphics Inc. issues 1,000 bonds at face On 1/1/02, Graphics Inc. issues 1,000 bonds at face value to Webster, Inc. The market interest rate is value to Webster, Inc. The market interest rate is

12%12%. The bonds have the following terms:. The bonds have the following terms:Face Value = $1,000Face Value = $1,000

Maturity Date = 12/31/06 (5 years) Maturity Date = 12/31/06 (5 years)

Stated Interest Rate = Stated Interest Rate = 10%10%

Interest Dates = 6/30 & 12/31Interest Dates = 6/30 & 12/31

Bond Date = 1/1/02Bond Date = 1/1/02

What is the selling price of these bonds?What is the selling price of these bonds?

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-14

Determining the Selling Price

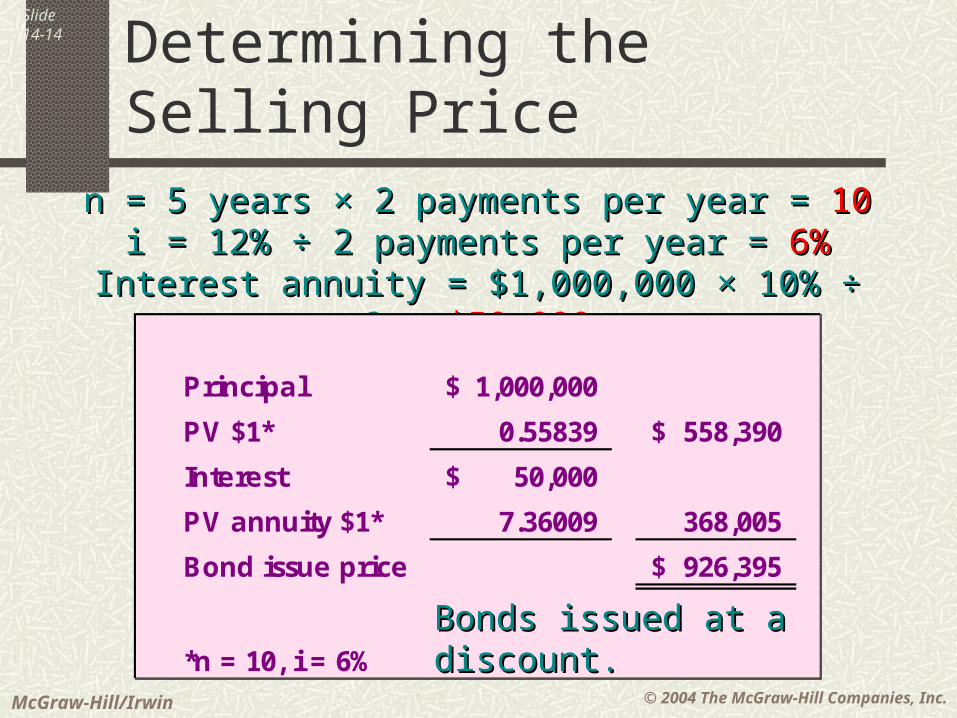

n = 5 years n = 5 years × 2 payments per year = × 2 payments per year = 1010i = 12% ÷ 2 payments per year = i = 12% ÷ 2 payments per year = 6%6%

Interest annuity = $1,000,000 × 10% ÷ 2 = Interest annuity = $1,000,000 × 10% ÷ 2 = $50,000$50,000

Principal 1,000,000$

PV $1* 0.55839 558,390$

Interest 50,000$

PV annuity $1* 7.36009 368,005

Bond issue price 926,395$

*n = 10, i = 6%

Principal 1,000,000$

PV $1* 0.55839 558,390$

Interest 50,000$

PV annuity $1* 7.36009 368,005

Bond issue price 926,395$

*n = 10, i = 6%Bonds issued at a discount.Bonds issued at a discount.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-15

Determining the Selling Price

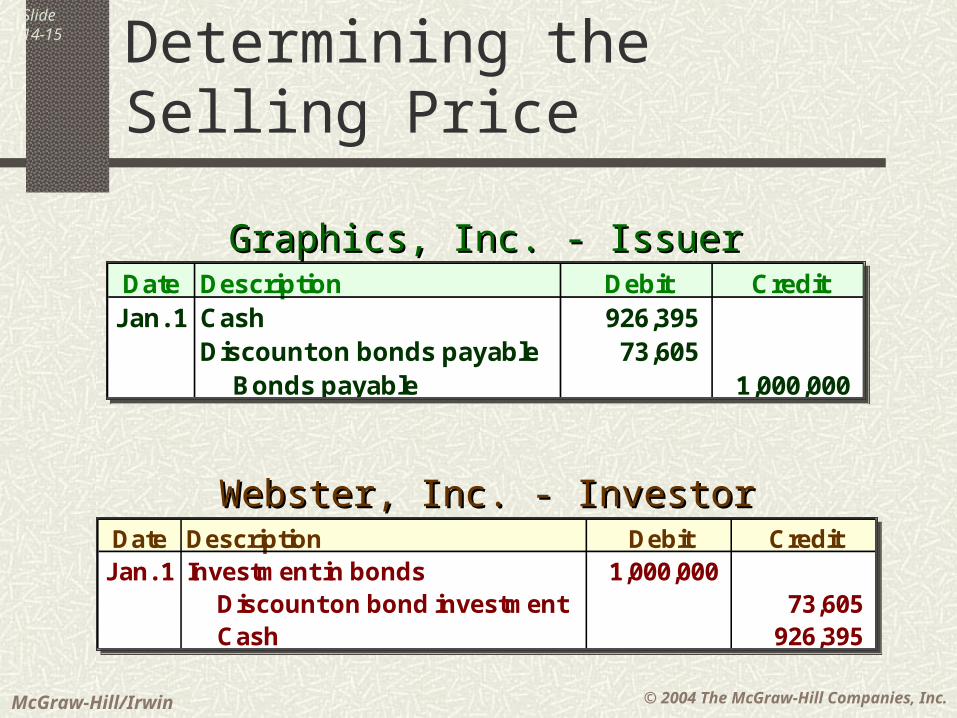

Date Description Debit CreditJan. 1 Cash 926,395

Discount on bonds payable 73,605 Bonds payable 1,000,000

Date Description Debit CreditJan. 1 Cash 926,395

Discount on bonds payable 73,605 Bonds payable 1,000,000

Graphics, Inc. - IssuerGraphics, Inc. - Issuer

Date Description Debit CreditJan. 1 Investment in bonds 1,000,000

Discount on bond investment 73,605 Cash 926,395

Date Description Debit CreditJan. 1 Investment in bonds 1,000,000

Discount on bond investment 73,605 Cash 926,395

Webster, Inc. - InvestorWebster, Inc. - Investor

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-16

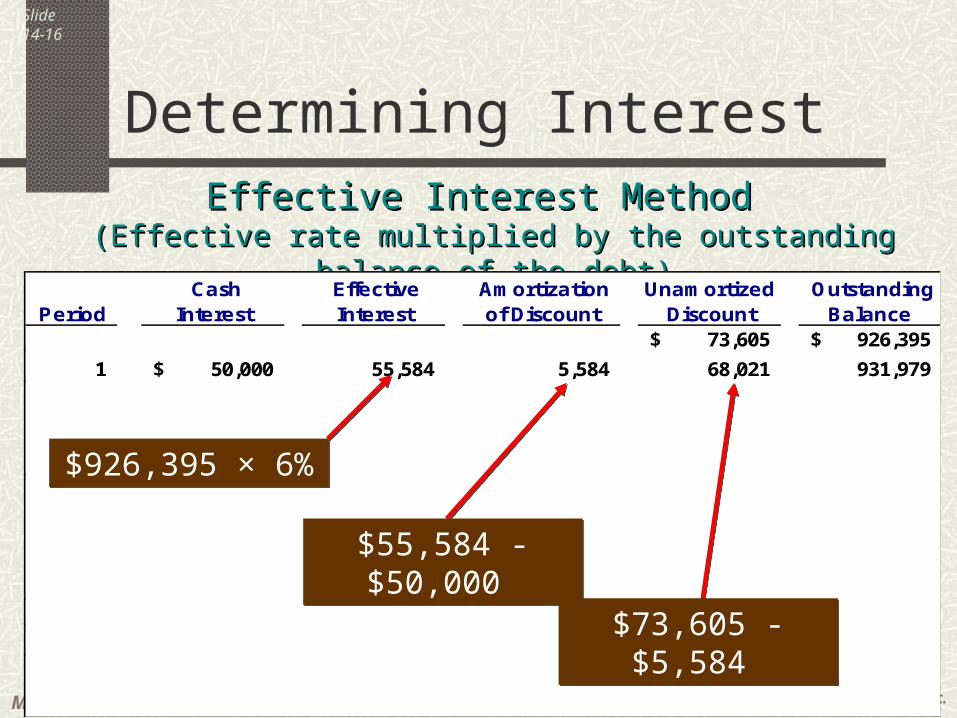

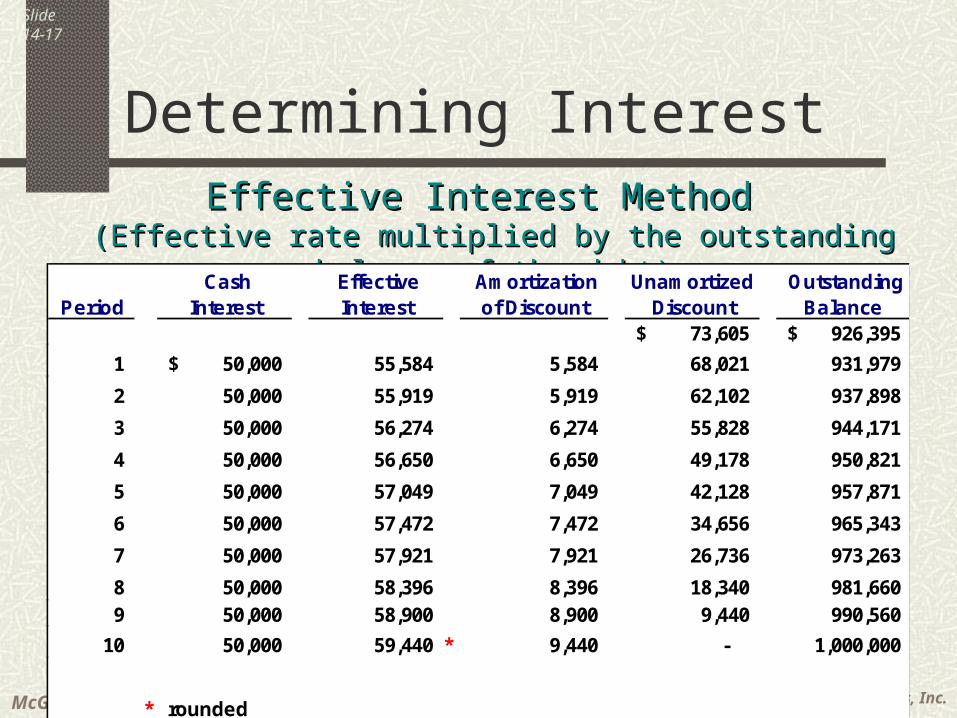

Determining Interest

Effective Interest MethodEffective Interest Method(Effective rate multiplied by the outstanding balance of the debt)(Effective rate multiplied by the outstanding balance of the debt)

Period Cash

Interest Effective Interest

Amortization of Discount

Unamortized

Discount Outstanding

Balance 73,605$ 926,395$

1 50,000$ 55,584 5,584 68,021 931,979

$926,395 × 6%$926,395 × 6%

$55,584 - $50,000 $55,584 - $50,000

$73,605 - $5,584 $73,605 - $5,584

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-17

Determining Interest

Effective Interest MethodEffective Interest Method(Effective rate multiplied by the outstanding balance of the debt)(Effective rate multiplied by the outstanding balance of the debt)

Period Cash

Interest Effective Interest

Amortization of Discount

Unamortized

Discount Outstanding

Balance 73,605$ 926,395$

1 50,000$ 55,584 5,584 68,021 931,979

2 50,000 55,919 5,919 62,102 937,898

3 50,000 56,274 6,274 55,828 944,171

4 50,000 56,650 6,650 49,178 950,821

5 50,000 57,049 7,049 42,128 957,871

6 50,000 57,472 7,472 34,656 965,343

7 50,000 57,921 7,921 26,736 973,263

8 50,000 58,396 8,396 18,340 981,660 9 50,000 58,900 8,900 9,440 990,560

10 50,000 59,440 * 9,440 - 1,000,000

* rounded

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-18

Determining Interest

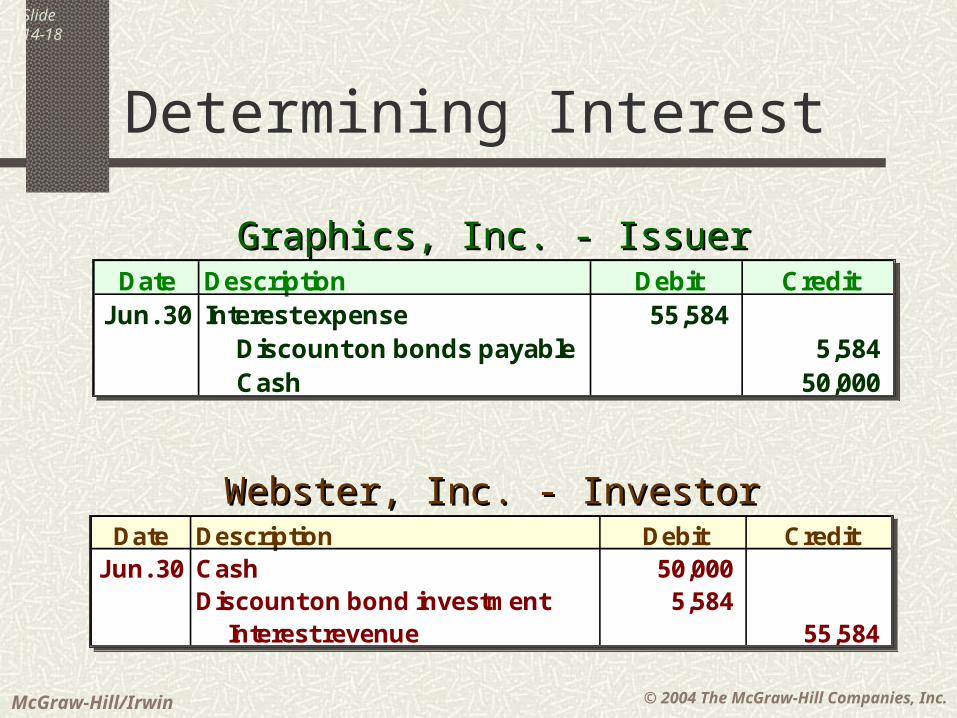

Date Description Debit CreditJun. 30 Interest expense 55,584

Discount on bonds payable 5,584 Cash 50,000

Date Description Debit CreditJun. 30 Interest expense 55,584

Discount on bonds payable 5,584 Cash 50,000

Graphics, Inc. - IssuerGraphics, Inc. - Issuer

Date Description Debit CreditJun. 30 Cash 50,000

Discount on bond investment 5,584 Interest revenue 55,584

Date Description Debit CreditJun. 30 Cash 50,000

Discount on bond investment 5,584 Interest revenue 55,584

Webster, Inc. - InvestorWebster, Inc. - Investor

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-19

Zero-Coupon Bonds

These bonds do not pay interest. These bonds do not pay interest. Instead, they offer a return in the Instead, they offer a return in the form of a “deep discount” from form of a “deep discount” from the face amount. Those who the face amount. Those who invest in zero-coupon bonds invest in zero-coupon bonds

usually have tax-deferred or tax-usually have tax-deferred or tax-exempt status.exempt status.

These bonds do not pay interest. These bonds do not pay interest. Instead, they offer a return in the Instead, they offer a return in the form of a “deep discount” from form of a “deep discount” from the face amount. Those who the face amount. Those who invest in zero-coupon bonds invest in zero-coupon bonds

usually have tax-deferred or tax-usually have tax-deferred or tax-exempt status.exempt status.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-20

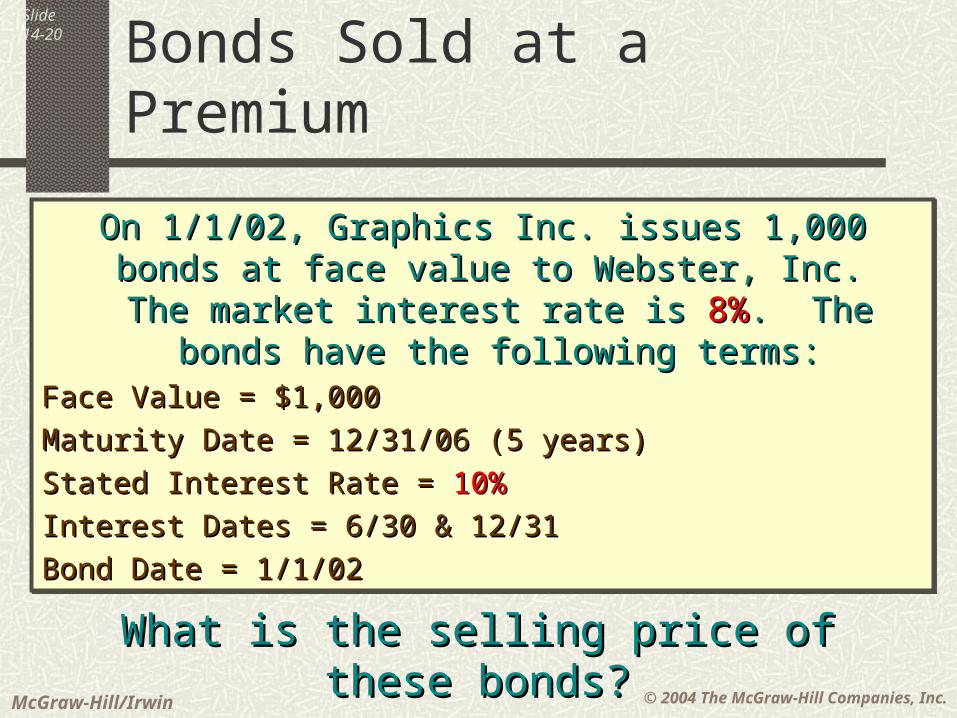

Bonds Sold at a Premium

On 1/1/02, Graphics Inc. issues 1,000 bonds at face On 1/1/02, Graphics Inc. issues 1,000 bonds at face value to Webster, Inc. The market interest rate is value to Webster, Inc. The market interest rate is

8%8%. The bonds have the following terms:. The bonds have the following terms:Face Value = $1,000Face Value = $1,000

Maturity Date = 12/31/06 (5 years) Maturity Date = 12/31/06 (5 years)

Stated Interest Rate = Stated Interest Rate = 10%10%

Interest Dates = 6/30 & 12/31Interest Dates = 6/30 & 12/31

Bond Date = 1/1/02Bond Date = 1/1/02

On 1/1/02, Graphics Inc. issues 1,000 bonds at face On 1/1/02, Graphics Inc. issues 1,000 bonds at face value to Webster, Inc. The market interest rate is value to Webster, Inc. The market interest rate is

8%8%. The bonds have the following terms:. The bonds have the following terms:Face Value = $1,000Face Value = $1,000

Maturity Date = 12/31/06 (5 years) Maturity Date = 12/31/06 (5 years)

Stated Interest Rate = Stated Interest Rate = 10%10%

Interest Dates = 6/30 & 12/31Interest Dates = 6/30 & 12/31

Bond Date = 1/1/02Bond Date = 1/1/02

What is the selling price of these bonds?What is the selling price of these bonds?

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-21

Bonds Sold at a Premium

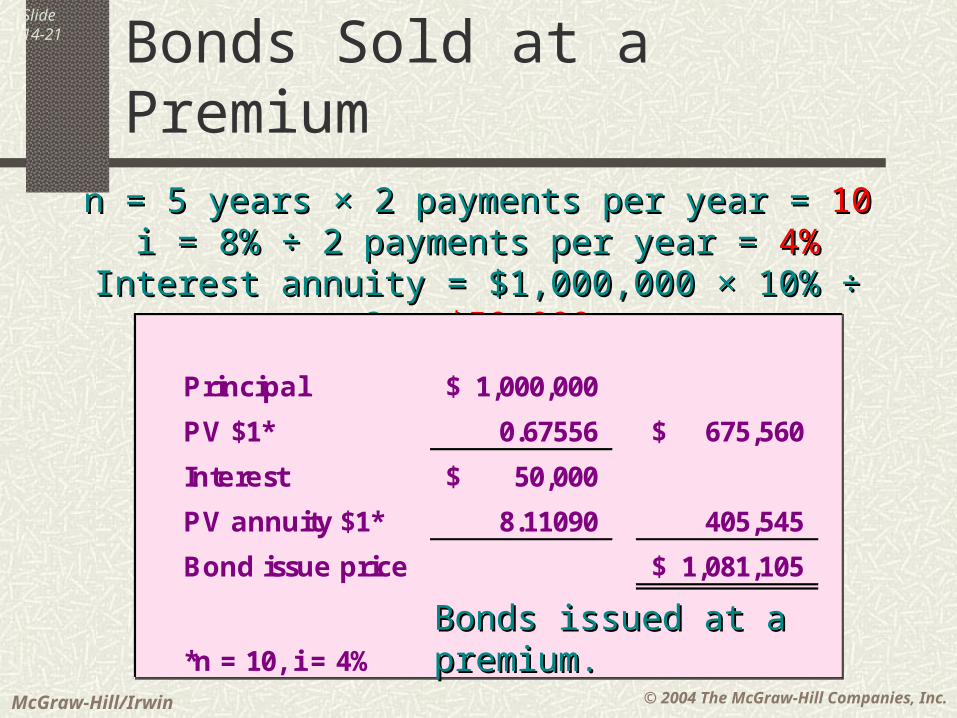

n = 5 years n = 5 years × 2 payments per year = × 2 payments per year = 1010i = 8% ÷ 2 payments per year = i = 8% ÷ 2 payments per year = 4%4%

Interest annuity = $1,000,000 × 10% ÷ 2 = Interest annuity = $1,000,000 × 10% ÷ 2 = $50,000$50,000

Principal 1,000,000$

PV $1* 0.67556 675,560$

Interest 50,000$

PV annuity $1* 8.11090 405,545

Bond issue price 1,081,105$

*n = 10, i = 4%

Principal 1,000,000$

PV $1* 0.67556 675,560$

Interest 50,000$

PV annuity $1* 8.11090 405,545

Bond issue price 1,081,105$

*n = 10, i = 4%Bonds issued at a premium.Bonds issued at a premium.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-22

Bonds Sold at a Premium

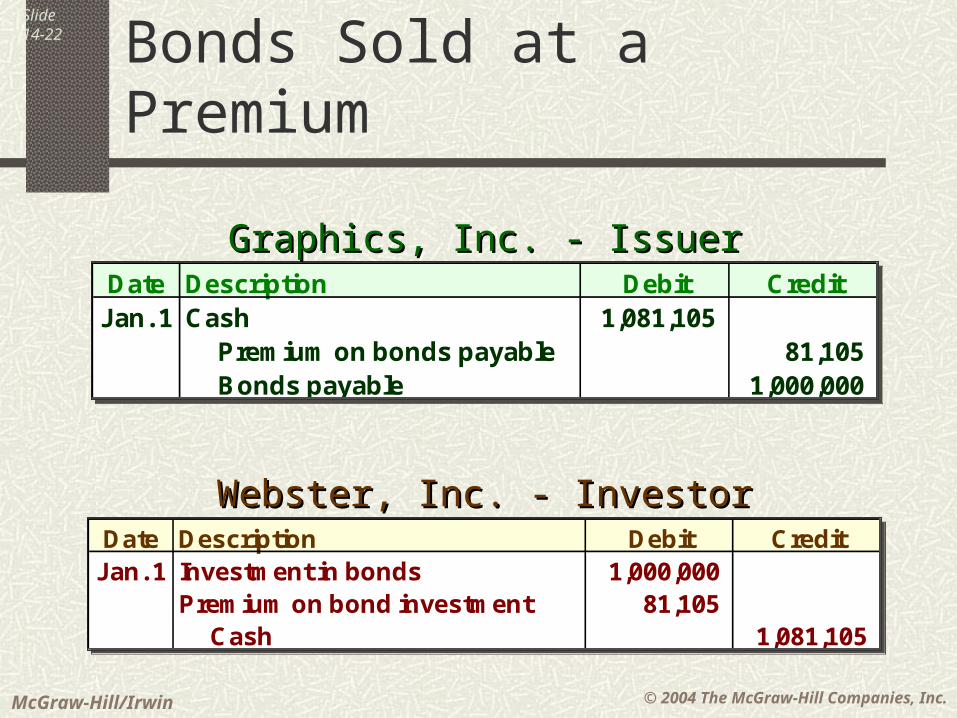

Date Description Debit CreditJan. 1 Cash 1,081,105

Premium on bonds payable 81,105 Bonds payable 1,000,000

Date Description Debit CreditJan. 1 Cash 1,081,105

Premium on bonds payable 81,105 Bonds payable 1,000,000

Graphics, Inc. - IssuerGraphics, Inc. - Issuer

Date Description Debit CreditJan. 1 Investment in bonds 1,000,000

Premium on bond investment 81,105 Cash 1,081,105

Date Description Debit CreditJan. 1 Investment in bonds 1,000,000

Premium on bond investment 81,105 Cash 1,081,105

Webster, Inc. - InvestorWebster, Inc. - Investor

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-23

Bonds Sold at a Premium

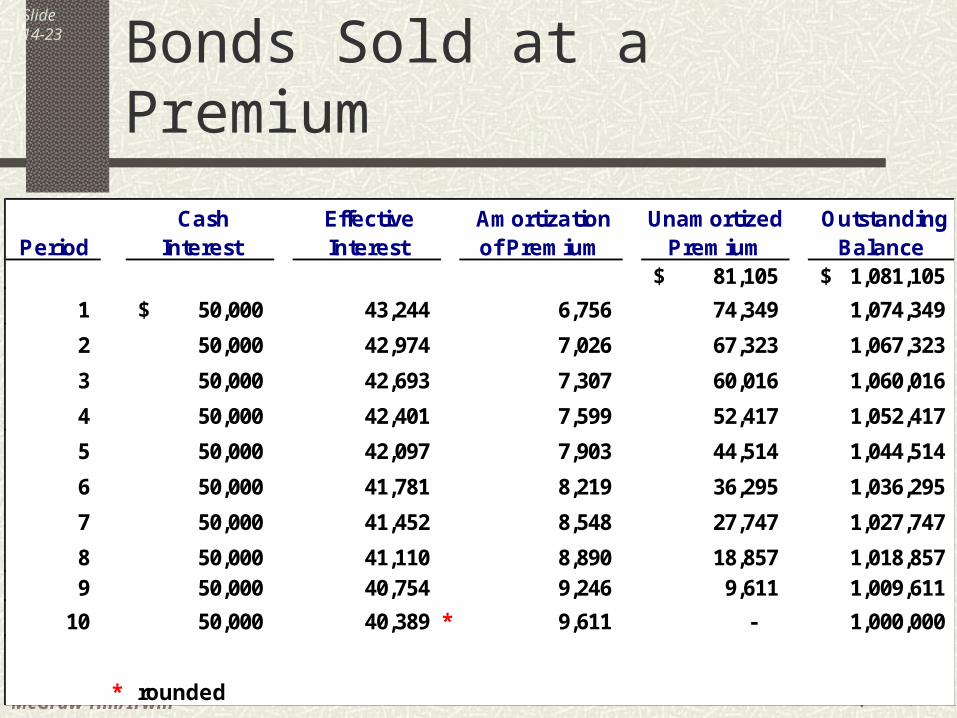

Period Cash

Interest Effective Interest

Amortization of Premium

Unamortized

Premium Outstanding

Balance 81,105$ 1,081,105$

1 50,000$ 43,244 6,756 74,349 1,074,349

2 50,000 42,974 7,026 67,323 1,067,323

3 50,000 42,693 7,307 60,016 1,060,016

4 50,000 42,401 7,599 52,417 1,052,417

5 50,000 42,097 7,903 44,514 1,044,514

6 50,000 41,781 8,219 36,295 1,036,295

7 50,000 41,452 8,548 27,747 1,027,747

8 50,000 41,110 8,890 18,857 1,018,857 9 50,000 40,754 9,246 9,611 1,009,611

10 50,000 40,389 * 9,611 - 1,000,000

* rounded

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

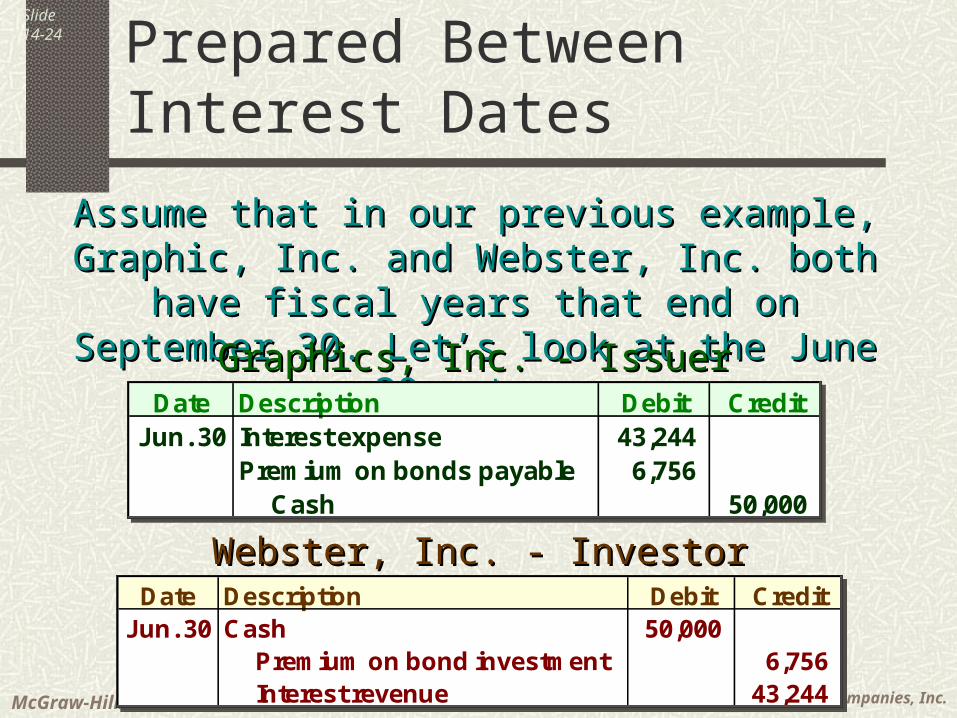

Slide14-24 Financial Statements Prepared

Between Interest Dates

Assume that in our previous example, Graphic, Inc. Assume that in our previous example, Graphic, Inc. and Webster, Inc. both have fiscal years that end and Webster, Inc. both have fiscal years that end on September 30. Let’s look at the June 30 entry:on September 30. Let’s look at the June 30 entry:

Date Description Debit CreditJun. 30 Interest expense 43,244

Premium on bonds payable 6,756 Cash 50,000

Date Description Debit CreditJun. 30 Interest expense 43,244

Premium on bonds payable 6,756 Cash 50,000

Graphics, Inc. - IssuerGraphics, Inc. - Issuer

Date Description Debit CreditJun. 30 Cash 50,000

Premium on bond investment 6,756 Interest revenue 43,244

Date Description Debit CreditJun. 30 Cash 50,000

Premium on bond investment 6,756 Interest revenue 43,244

Webster, Inc. - InvestorWebster, Inc. - Investor

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

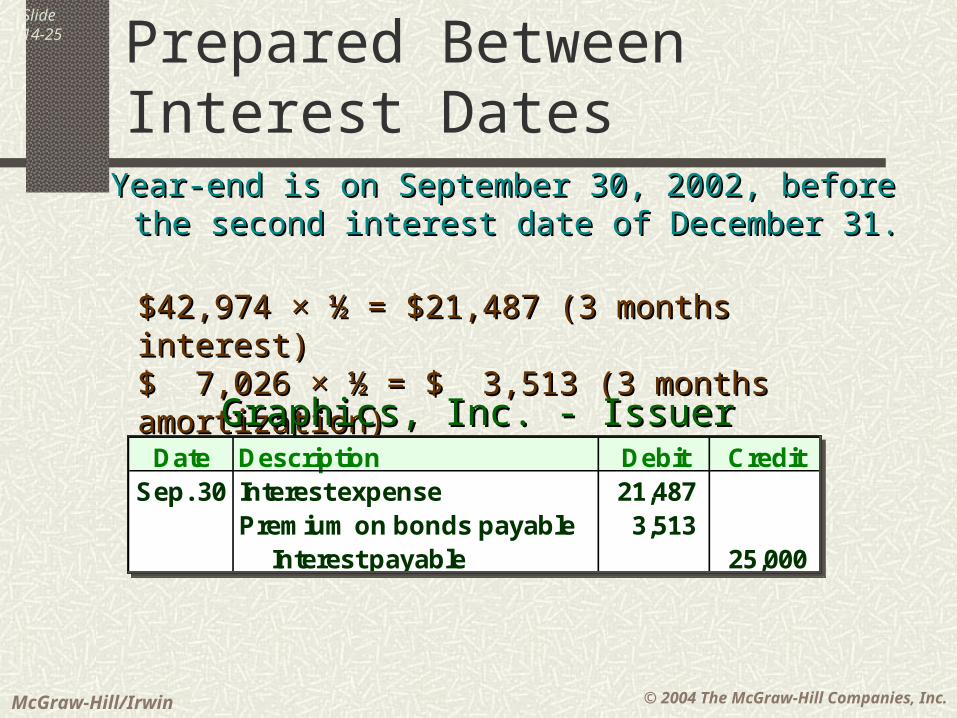

Slide14-25 Financial Statements Prepared

Between Interest DatesYear-end is on September 30, 2002, before Year-end is on September 30, 2002, before

the second interest date of December 31.the second interest date of December 31.

$42,974 $42,974 × ½ = $21,487 (3 months interest)× ½ = $21,487 (3 months interest)$ 7,026 × ½ = $ 3,513 (3 months amortization)$ 7,026 × ½ = $ 3,513 (3 months amortization)

Date Description Debit CreditSep. 30 Interest expense 21,487

Premium on bonds payable 3,513 Interest payable 25,000

Date Description Debit CreditSep. 30 Interest expense 21,487

Premium on bonds payable 3,513 Interest payable 25,000

Graphics, Inc. - IssuerGraphics, Inc. - Issuer

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

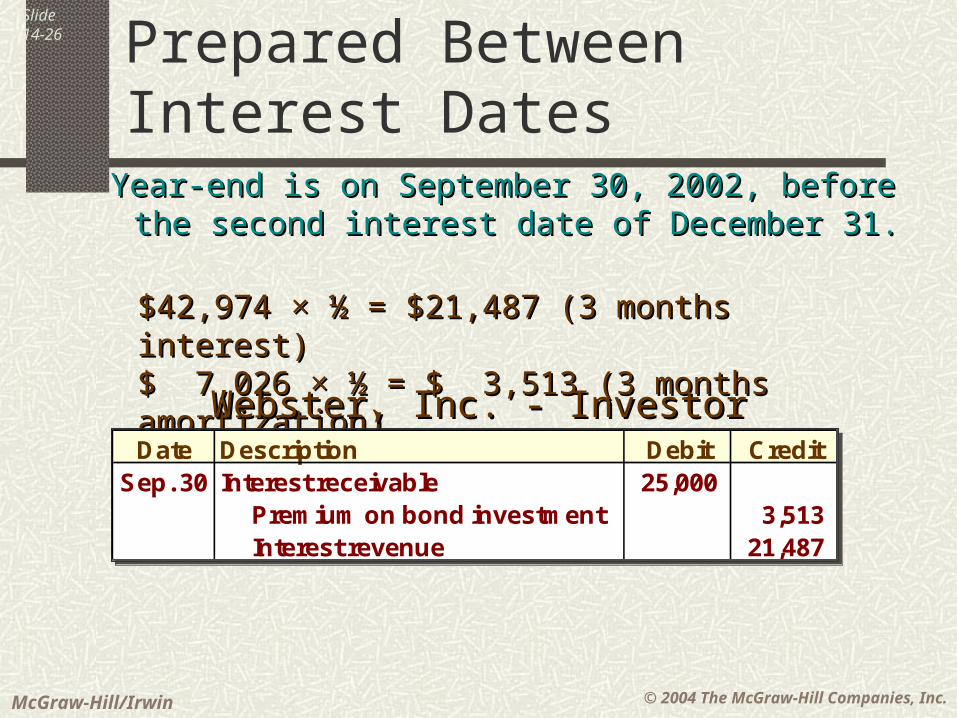

Slide14-26 Financial Statements Prepared

Between Interest DatesYear-end is on September 30, 2002, before Year-end is on September 30, 2002, before

the second interest date of December 31.the second interest date of December 31.

$42,974 $42,974 × ½ = $21,487 (3 months interest)× ½ = $21,487 (3 months interest)$ 7,026 × ½ = $ 3,513 (3 months amortization)$ 7,026 × ½ = $ 3,513 (3 months amortization)

Date Description Debit CreditSep. 30 Interest receivable 25,000

Premium on bond investment 3,513 Interest revenue 21,487

Date Description Debit CreditSep. 30 Interest receivable 25,000

Premium on bond investment 3,513 Interest revenue 21,487

Webster, Inc. - InvestorWebster, Inc. - Investor

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

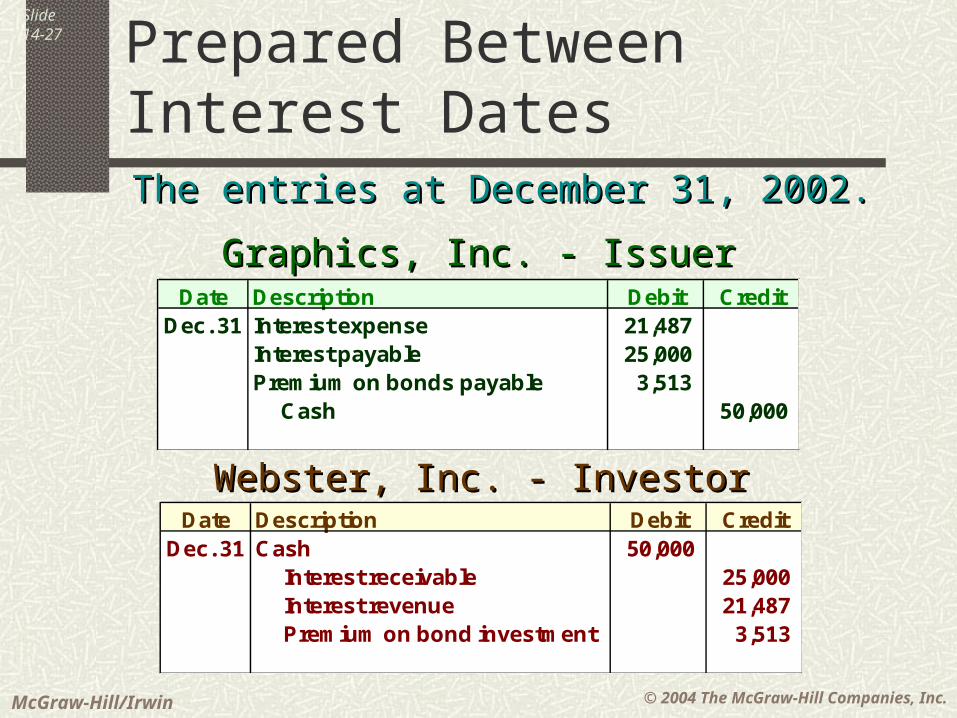

Slide14-27 Financial Statements Prepared

Between Interest DatesThe entries at December 31, 2002.The entries at December 31, 2002.

Date Description Debit CreditDec. 31 Interest expense 21,487

Interest payable 25,000 Premium on bonds payable 3,513 Cash 50,000

Graphics, Inc. - IssuerGraphics, Inc. - Issuer

Date Description Debit CreditDec. 31 Cash 50,000

Interest receivable 25,000 Interest revenue 21,487 Premium on bond investment 3,513

Webster, Inc. - InvestorWebster, Inc. - Investor

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-28

Straight-Line Method

The discount or The discount or premium is premium is allocated allocated

equallyequally to each to each period over the period over the outstanding life outstanding life

of the bond.of the bond.

ConsideredConsideredpracticalpractical

andandexpedient.expedient.

ConsideredConsideredpracticalpractical

andandexpedient.expedient.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-29

Straight-Line Method

In our last example, straight-lineIn our last example, straight-linepremium amortization would be:premium amortization would be:

$81,105 $81,105 ÷ 10 = ÷ 10 = $8,111 every six months$8,111 every six months..

In our last example, straight-lineIn our last example, straight-linepremium amortization would be:premium amortization would be:

$81,105 $81,105 ÷ 10 = ÷ 10 = $8,111 every six months$8,111 every six months..

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-30

Debt Issue Costs

LegalLegal

AccountingAccounting

UnderwritingUnderwriting

CommissionCommission

EngravingEngraving

PrintingPrinting

RegistrationRegistration

Promotion Promotion

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-31

Debt Issue Costs

These costs should be recorded These costs should be recorded separately and amortized over separately and amortized over the term of the related debt.the term of the related debt.

Straight-line amortization is often Straight-line amortization is often used. used.

These costs should be recorded These costs should be recorded separately and amortized over separately and amortized over the term of the related debt.the term of the related debt.

Straight-line amortization is often Straight-line amortization is often used. used.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-32

Long-Term Notes

Present value techniques are used Present value techniques are used for valuation and interest for valuation and interest

recognition.recognition.

The procedures are similar to those The procedures are similar to those we encountered with bonds. we encountered with bonds.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-33

Notes Exchanged for Assets or Services

On 1/1/03, Matters, Inc. issued a $100,000, 3-year, On 1/1/03, Matters, Inc. issued a $100,000, 3-year, 6% note in exchange for equipment owned by 6% note in exchange for equipment owned by West, Inc. Interest is paid every 12/31. The West, Inc. Interest is paid every 12/31. The

equipment does not have a ready market value. equipment does not have a ready market value. The appropriate rate of interest for notes of this The appropriate rate of interest for notes of this

type is 9%.type is 9%.

Let’s determine the present value of the note.Let’s determine the present value of the note.

On 1/1/03, Matters, Inc. issued a $100,000, 3-year, On 1/1/03, Matters, Inc. issued a $100,000, 3-year, 6% note in exchange for equipment owned by 6% note in exchange for equipment owned by West, Inc. Interest is paid every 12/31. The West, Inc. Interest is paid every 12/31. The

equipment does not have a ready market value. equipment does not have a ready market value. The appropriate rate of interest for notes of this The appropriate rate of interest for notes of this

type is 9%.type is 9%.

Let’s determine the present value of the note.Let’s determine the present value of the note.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-34

Notes Exchanged for Assets or Services

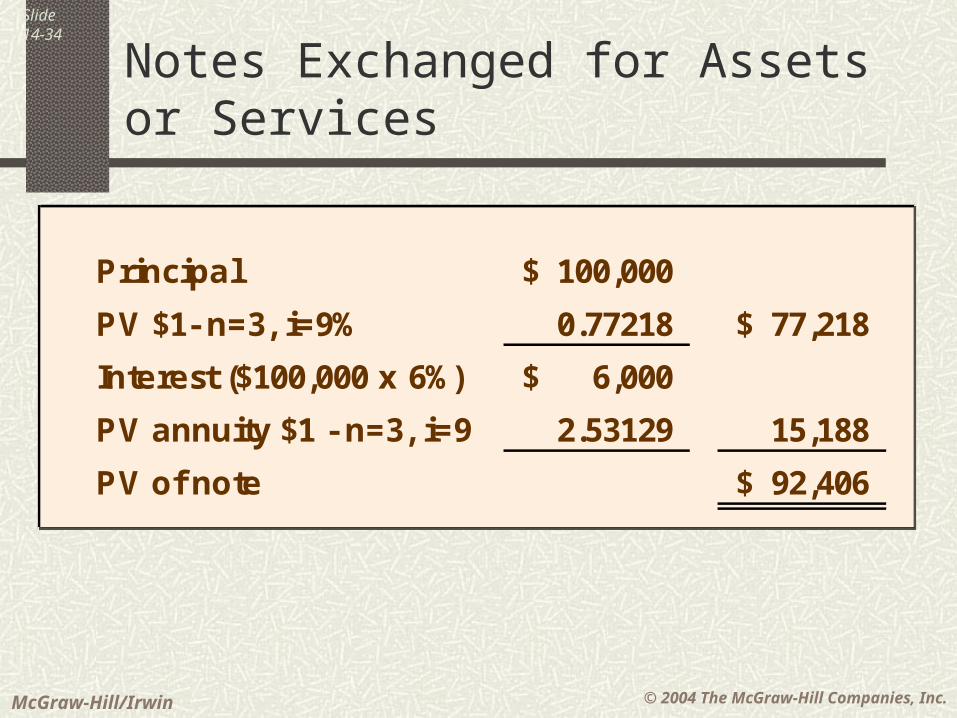

Principal 100,000$

PV $1- n=3, i=9% 0.77218 77,218$

Interest ($100,000 x 6%) 6,000$

PV annuity $1 - n=3, i=9 2.53129 15,188

PV of note 92,406$

Principal 100,000$

PV $1- n=3, i=9% 0.77218 77,218$

Interest ($100,000 x 6%) 6,000$

PV annuity $1 - n=3, i=9 2.53129 15,188

PV of note 92,406$

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-35

Notes Exchanged for Assets or Services

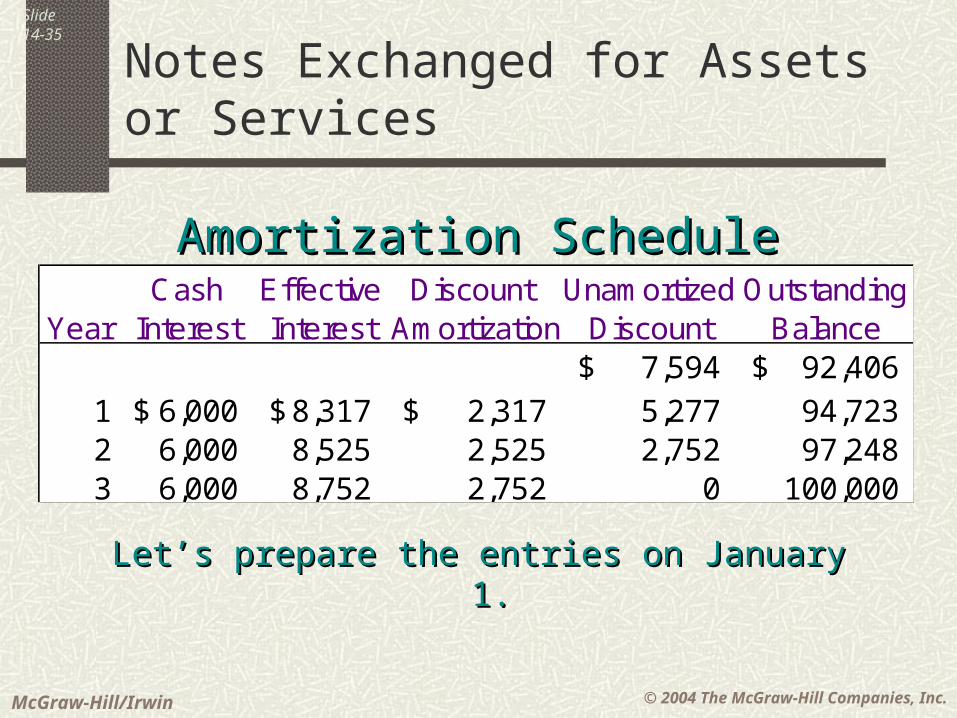

Cash Effective Discount Unamortized OutstandingYear Interest Interest Amortization Discount Balance

7,594$ 92,406$

1 6,000$ 8,317$ 2,317$ 5,277 94,723 2 6,000 8,525 2,525 2,752 97,248 3 6,000 8,752 2,752 0 100,000

Let’s prepare the entries on January 1.Let’s prepare the entries on January 1.

Amortization ScheduleAmortization Schedule

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-36

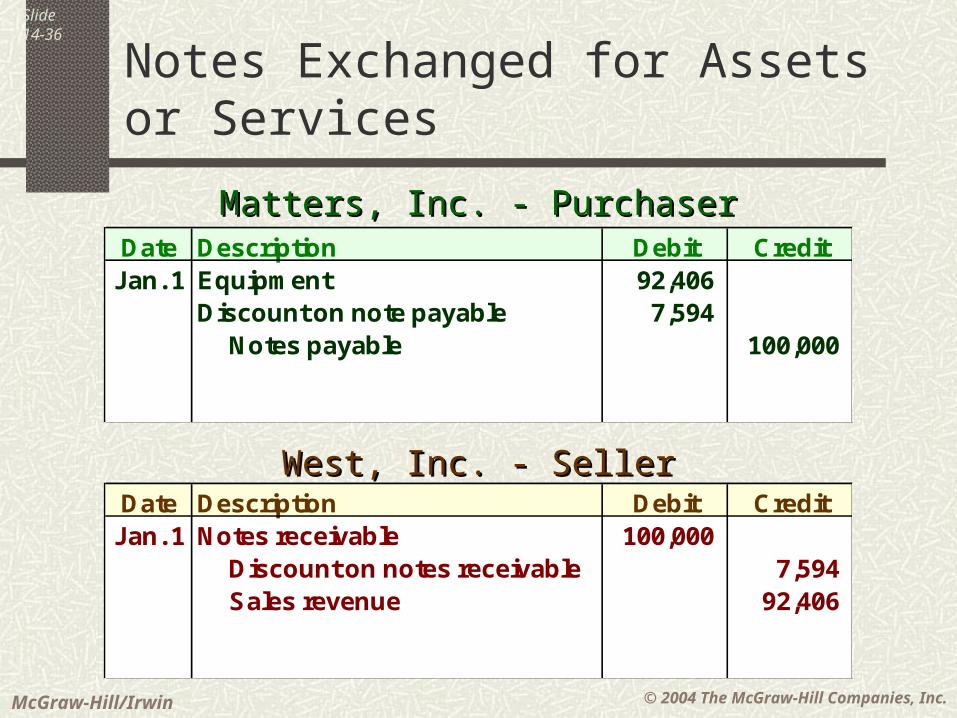

Notes Exchanged for Assets or Services

Date Description Debit CreditJan. 1 Equipment 92,406

Discount on note payable 7,594 Notes payable 100,000

Matters, Inc. - PurchaserMatters, Inc. - Purchaser

Date Description Debit CreditJan. 1 Notes receivable 100,000

Discount on notes receivable 7,594 Sales revenue 92,406

West, Inc. - SellerWest, Inc. - Seller

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-37

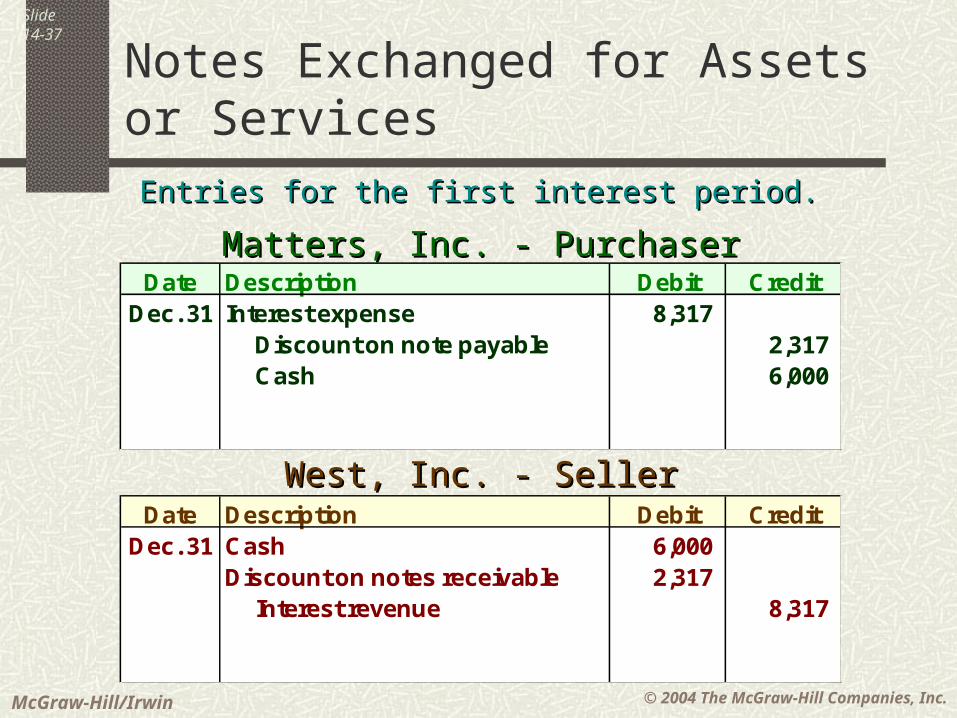

Notes Exchanged for Assets or Services

Entries for the first interest period.Entries for the first interest period.

Date Description Debit CreditDec. 31 Interest expense 8,317

Discount on note payable 2,317 Cash 6,000

Matters, Inc. - PurchaserMatters, Inc. - Purchaser

Date Description Debit CreditDec. 31 Cash 6,000

Discount on notes receivable 2,317 Interest revenue 8,317

West, Inc. - SellerWest, Inc. - Seller

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-38

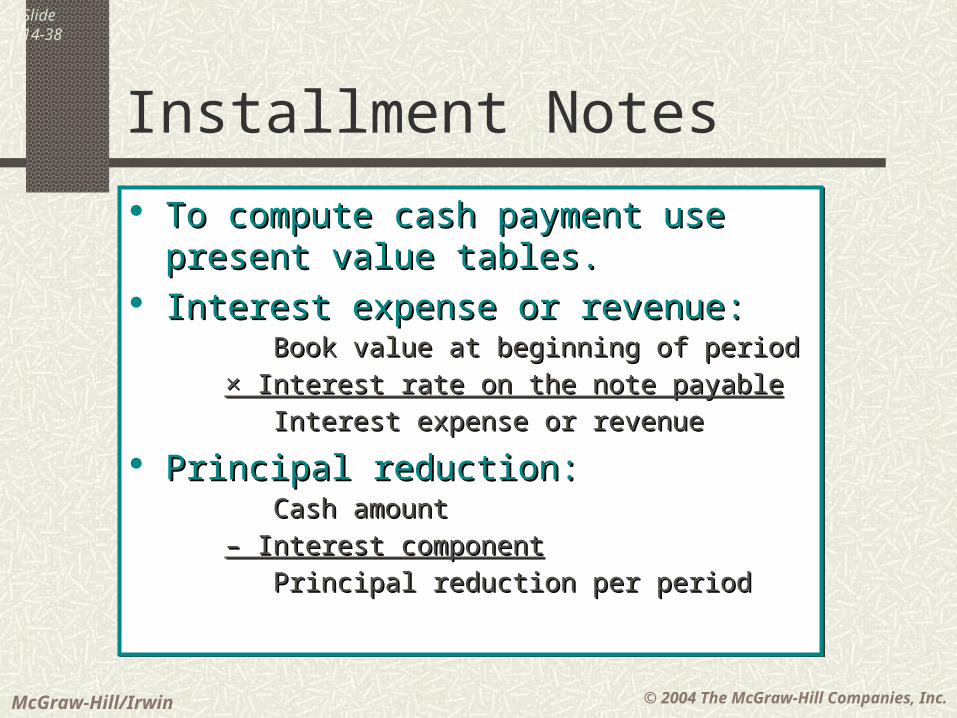

Installment Notes

To compute cash payment use present value To compute cash payment use present value tables.tables.

Interest expense or revenue:Interest expense or revenue: Book value at beginning of periodBook value at beginning of period

× Interest rate on the note payable× Interest rate on the note payable

Interest expense or revenueInterest expense or revenue

Principal reduction:Principal reduction: Cash amountCash amount

– – Interest componentInterest component

Principal reduction per periodPrincipal reduction per period

To compute cash payment use present value To compute cash payment use present value tables.tables.

Interest expense or revenue:Interest expense or revenue: Book value at beginning of periodBook value at beginning of period

× Interest rate on the note payable× Interest rate on the note payable

Interest expense or revenueInterest expense or revenue

Principal reduction:Principal reduction: Cash amountCash amount

– – Interest componentInterest component

Principal reduction per periodPrincipal reduction per period

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-39

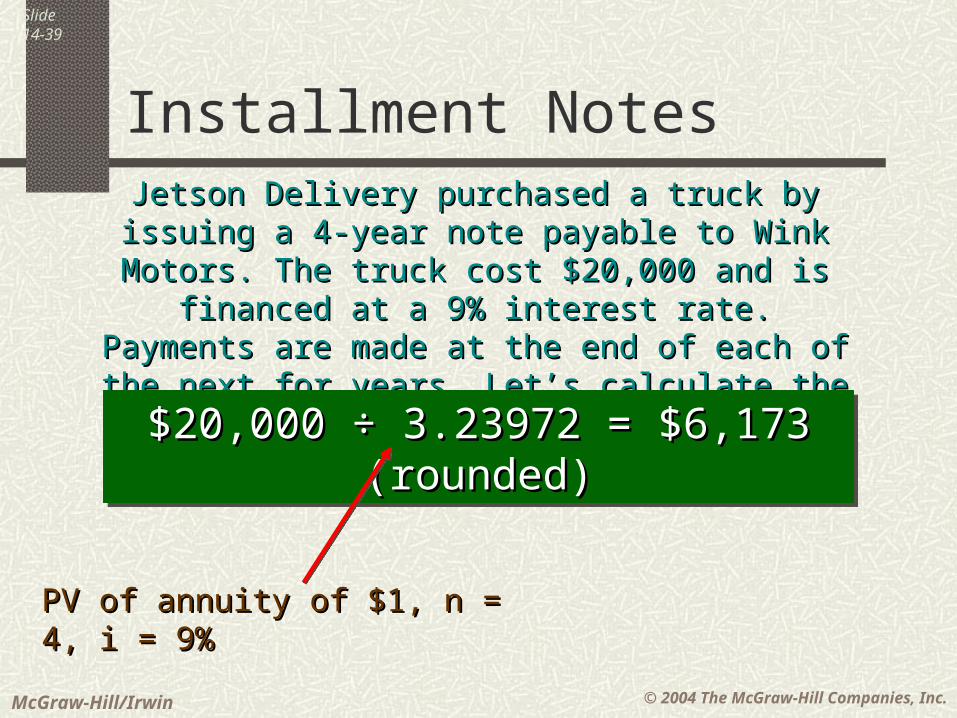

Installment NotesJetson Delivery purchased a truck by issuing a 4-Jetson Delivery purchased a truck by issuing a 4-year note payable to Wink Motors. The truck cost year note payable to Wink Motors. The truck cost

$20,000 and is financed at a 9% interest rate. $20,000 and is financed at a 9% interest rate. Payments are made at the end of each of the next for Payments are made at the end of each of the next for

years. Let’s calculate the annual payment.years. Let’s calculate the annual payment.

$20,000 $20,000 ÷ 3.23972 = $6,173 (rounded)÷ 3.23972 = $6,173 (rounded)$20,000 $20,000 ÷ 3.23972 = $6,173 (rounded)÷ 3.23972 = $6,173 (rounded)

PV of annuity of $1, n = 4, i = 9%PV of annuity of $1, n = 4, i = 9%

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-40

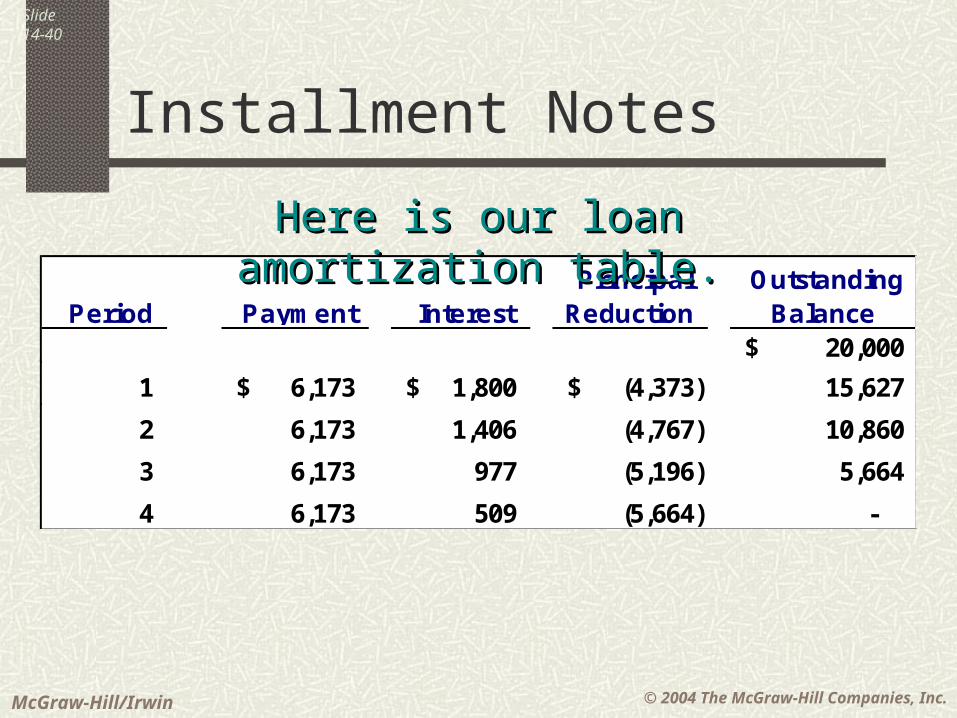

Installment Notes

Period Payment Interest Principal Reduction

Outstanding Balance

20,000$

1 6,173$ 1,800$ (4,373)$ 15,627

2 6,173 1,406 (4,767) 10,860

3 6,173 977 (5,196) 5,664

4 6,173 509 (5,664) -

Here is our loan amortization table.Here is our loan amortization table.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-41

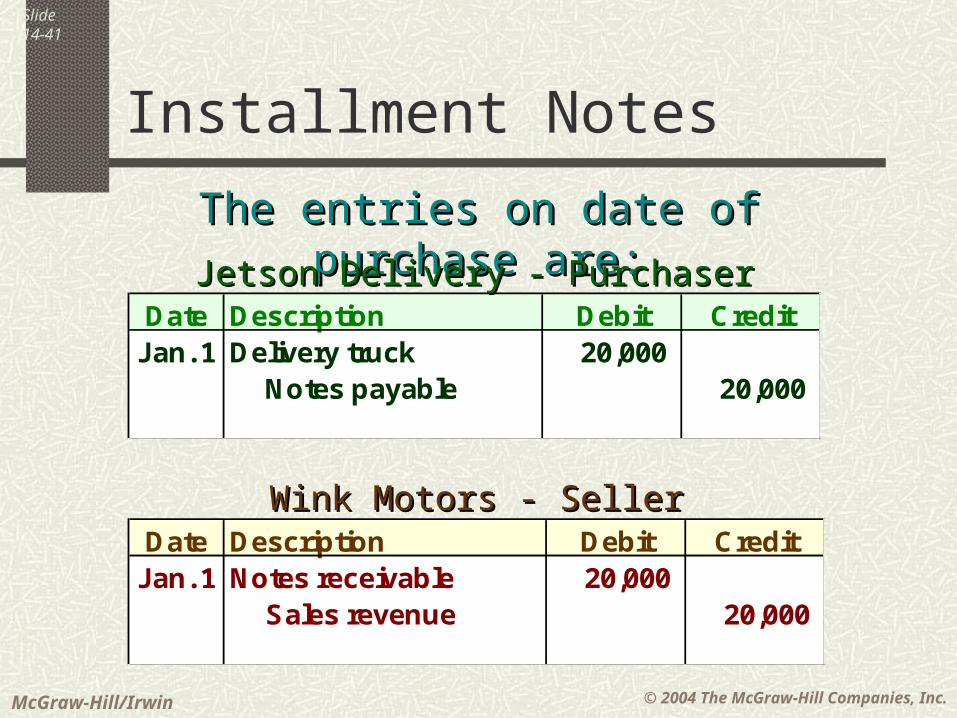

Installment Notes

The entries on date of purchase are:The entries on date of purchase are:

Date Description Debit CreditJan. 1 Delivery truck 20,000

Notes payable 20,000

Jetson Delivery - PurchaserJetson Delivery - Purchaser

Date Description Debit CreditJan. 1 Notes receivable 20,000

Sales revenue 20,000

Wink Motors - SellerWink Motors - Seller

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-42

Installment Notes

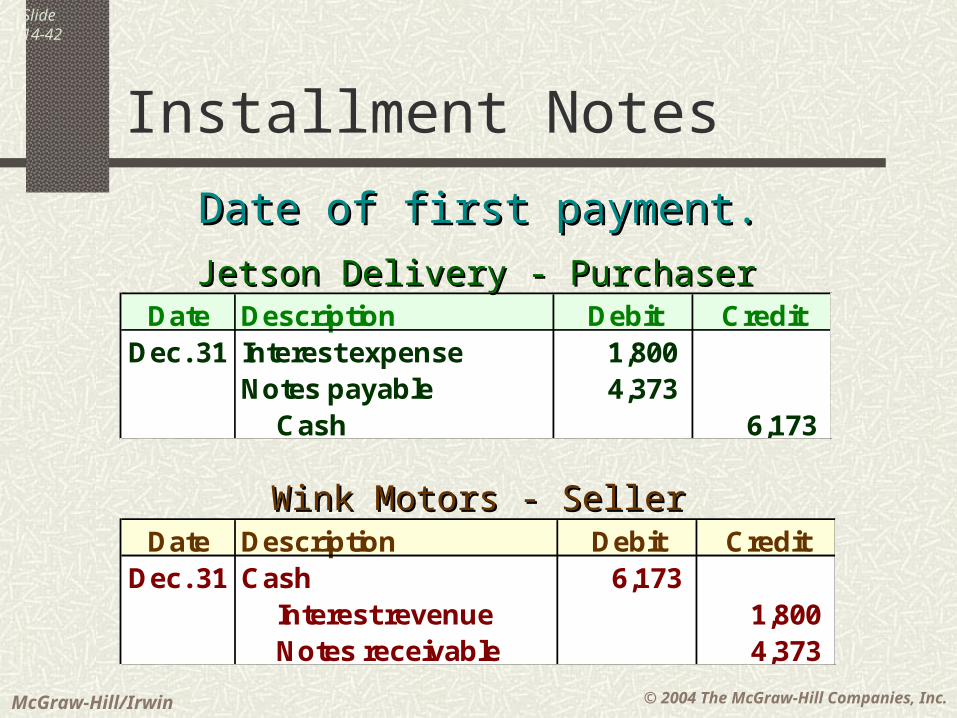

Date of first payment.Date of first payment.

Date Description Debit CreditDec. 31 Interest expense 1,800

Notes payable 4,373 Cash 6,173

Jetson Delivery - PurchaserJetson Delivery - Purchaser

Date Description Debit CreditDec. 31 Cash 6,173

Interest revenue 1,800 Notes receivable 4,373

Wink Motors - SellerWink Motors - Seller

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-43

Financial Statement Disclosures

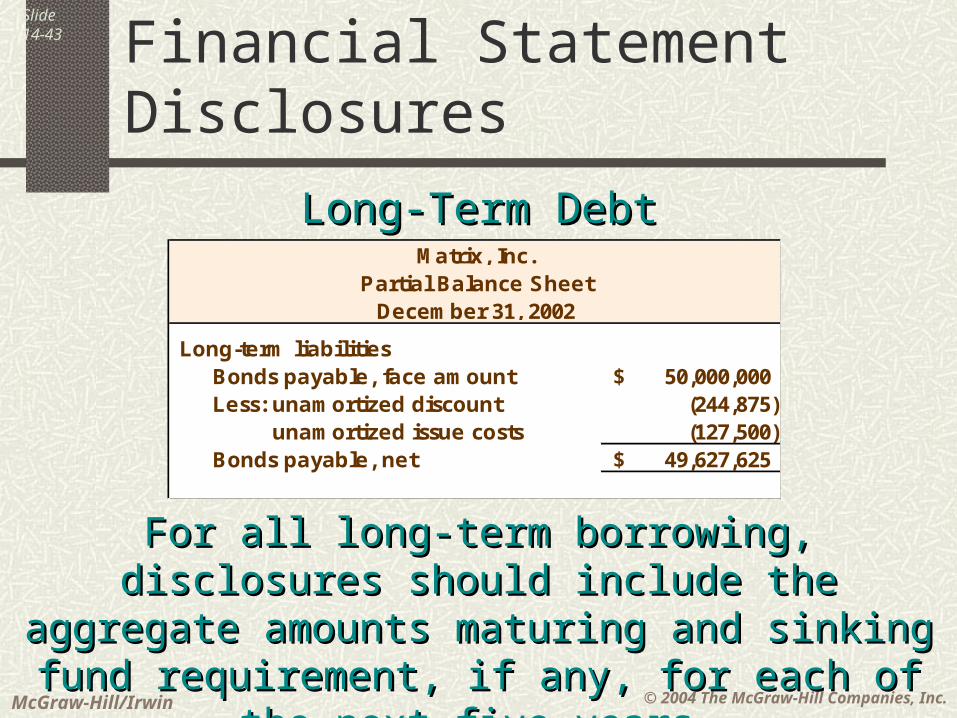

Long-Term DebtLong-Term Debt

Long-term liabilities Bonds payable, face amount 50,000,000$ Less: unamortized discount (244,875) unamortized issue costs (127,500) Bonds payable, net 49,627,625$

Matrix, Inc.Partial Balance Sheet

December 31, 2002

For all long-term borrowing, disclosures should include For all long-term borrowing, disclosures should include the aggregate amounts maturing and sinking fund the aggregate amounts maturing and sinking fund

requirement, if any, for each of the next five years.requirement, if any, for each of the next five years.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-44

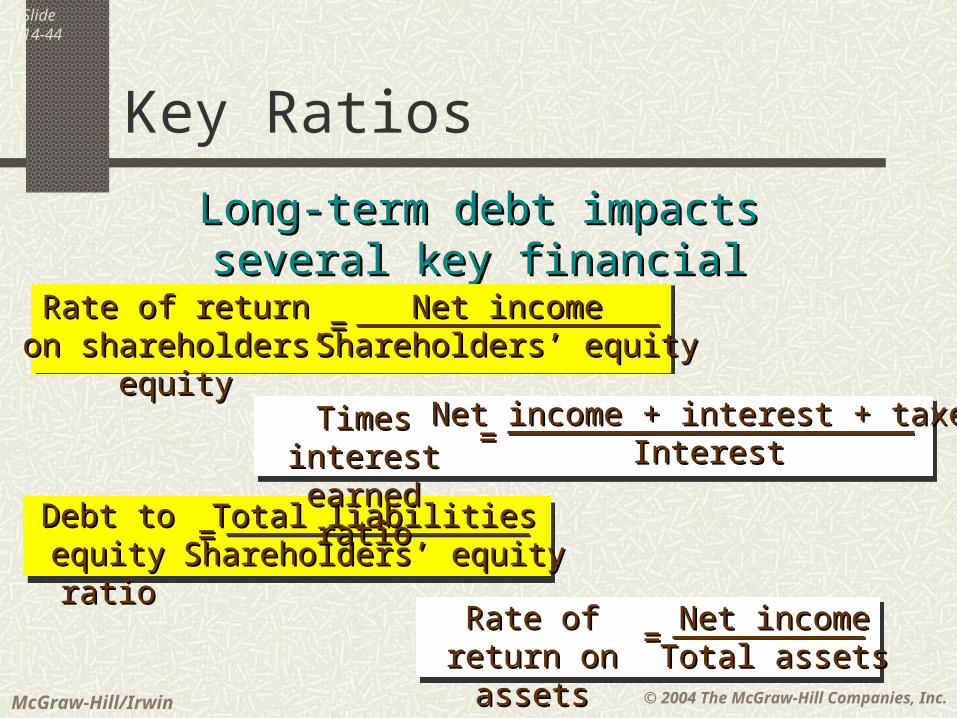

Key Ratios

Long-term debt impacts several key Long-term debt impacts several key financial ratios.financial ratios.

Debt toDebt toequity ratioequity ratio

Total liabilitiesTotal liabilitiesShareholders’ equityShareholders’ equity==

Rate of return Rate of return on assetson assets

Net incomeNet incomeTotal assetsTotal assets==

Rate of return on Rate of return on shareholders’ equityshareholders’ equity

Net incomeNet incomeShareholders’ equityShareholders’ equity==

Times interest Times interest earned ratioearned ratio ==

Net income + interest + taxesNet income + interest + taxesInterestInterest

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-45

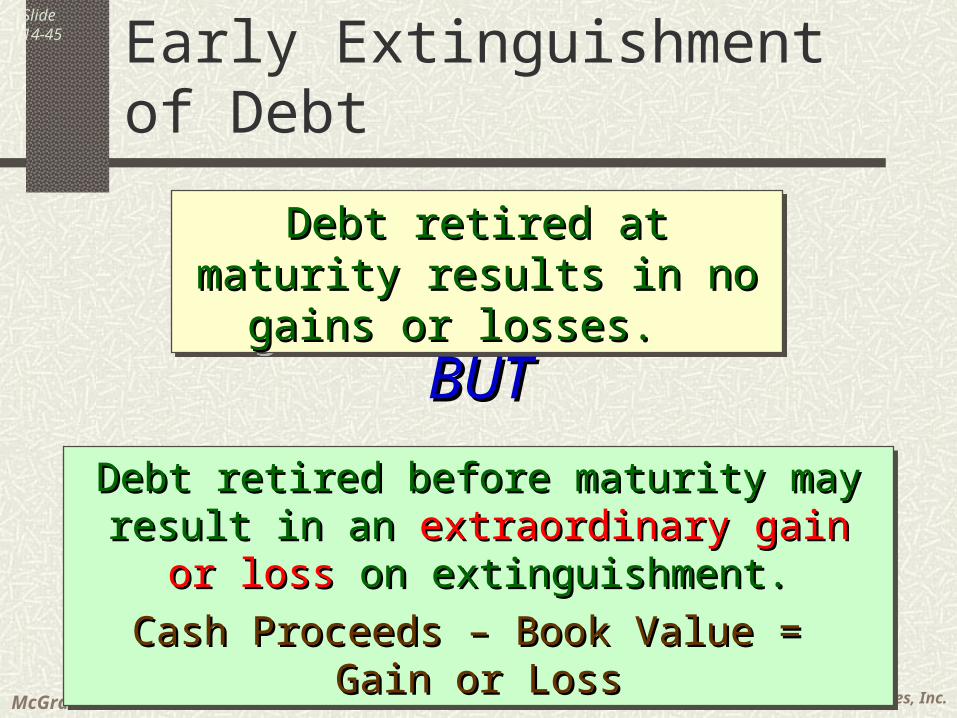

Early Extinguishment of Debt

Debt retired at maturity results Debt retired at maturity results in no gains or losses. in no gains or losses.

Debt retired at maturity results Debt retired at maturity results in no gains or losses. in no gains or losses.

Debt retired before maturity may result in an Debt retired before maturity may result in an extraordinary gainextraordinary gain or lossor loss on extinguishment. on extinguishment.

Cash Proceeds – Book Value = Gain or LossCash Proceeds – Book Value = Gain or Loss

Debt retired before maturity may result in an Debt retired before maturity may result in an extraordinary gainextraordinary gain or lossor loss on extinguishment. on extinguishment.

Cash Proceeds – Book Value = Gain or LossCash Proceeds – Book Value = Gain or Loss

BUTBUT

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-46

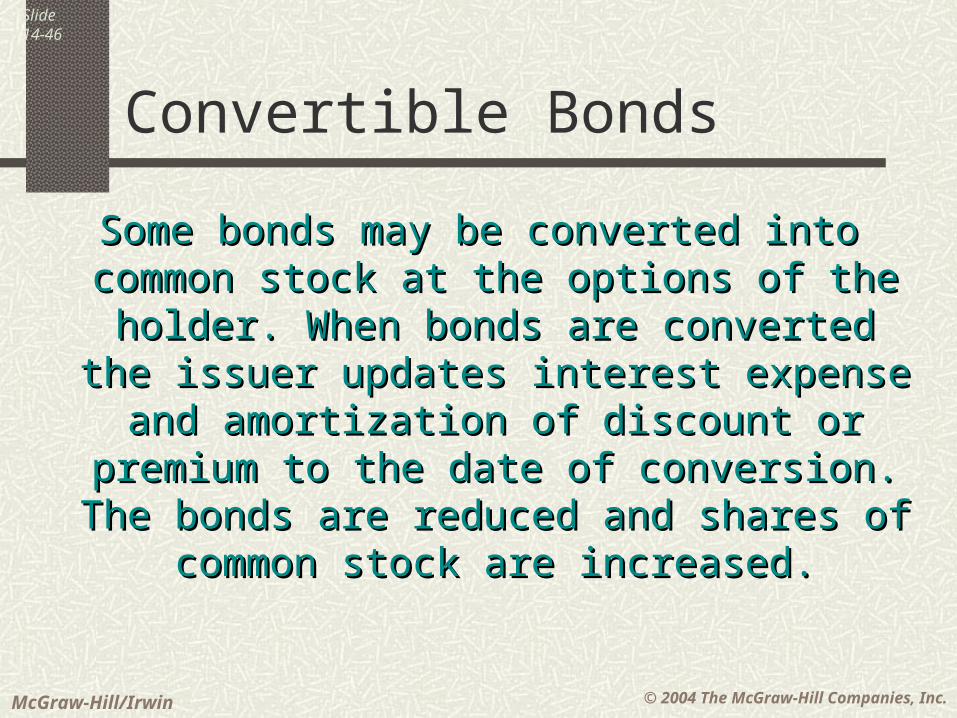

Convertible Bonds

Some bonds may be converted into common Some bonds may be converted into common stock at the options of the holder. When stock at the options of the holder. When bonds are converted the issuer updates bonds are converted the issuer updates

interest expense and amortization of interest expense and amortization of discount or premium to the date of discount or premium to the date of

conversion. The bonds are reduced and conversion. The bonds are reduced and shares of common stock are increased.shares of common stock are increased.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-47

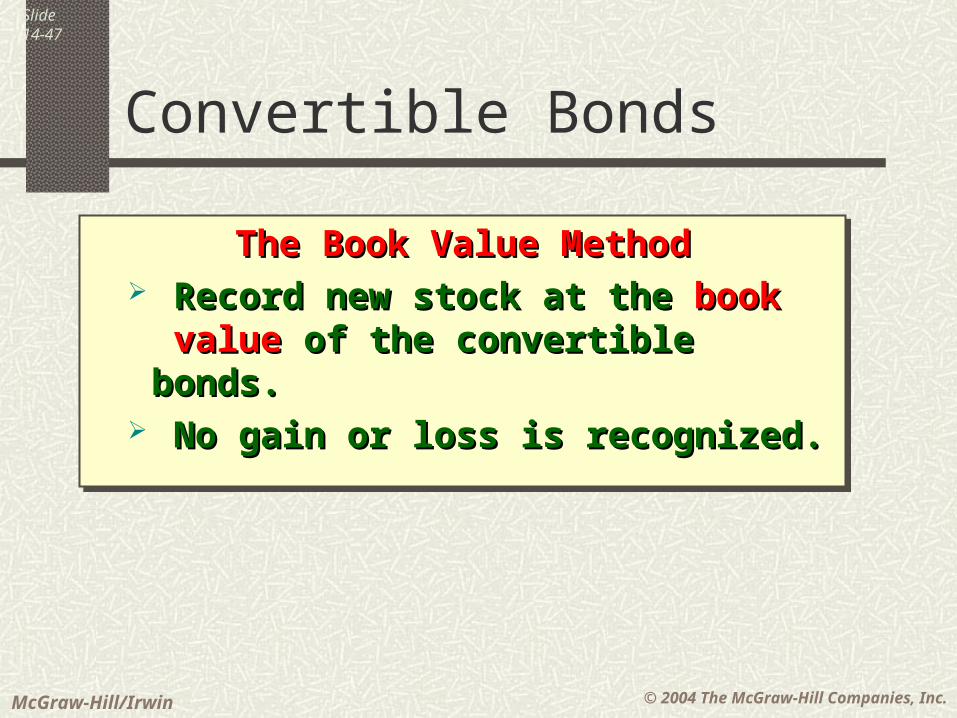

Convertible Bonds

The Book Value MethodThe Book Value Method Record new stock at the Record new stock at the bookbook

value value of the convertible bonds. of the convertible bonds. No gain or loss is recognized.No gain or loss is recognized.

The Book Value MethodThe Book Value Method Record new stock at the Record new stock at the bookbook

value value of the convertible bonds. of the convertible bonds. No gain or loss is recognized.No gain or loss is recognized.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-48

Convertible Bonds

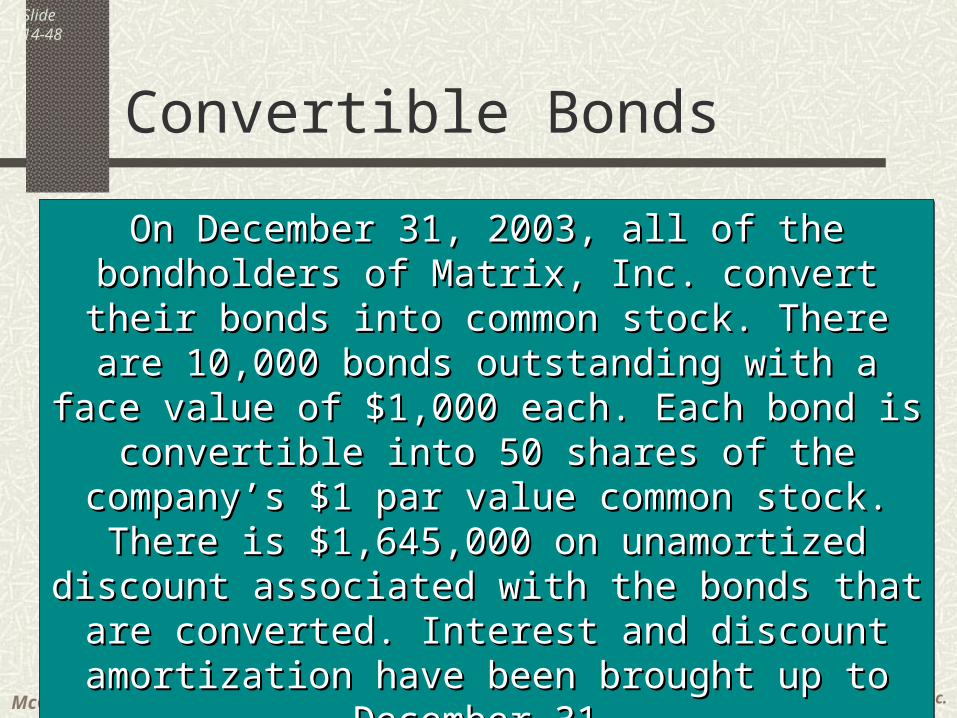

On December 31, 2003, all of the bondholders of On December 31, 2003, all of the bondholders of Matrix, Inc. convert their bonds into common stock. Matrix, Inc. convert their bonds into common stock.

There are 10,000 bonds outstanding with a face There are 10,000 bonds outstanding with a face value of $1,000 each. Each bond is convertible into value of $1,000 each. Each bond is convertible into 50 shares of the company’s $1 par value common 50 shares of the company’s $1 par value common

stock. There is $1,645,000 on unamortized discount stock. There is $1,645,000 on unamortized discount associated with the bonds that are converted. associated with the bonds that are converted. Interest and discount amortization have been Interest and discount amortization have been

brought up to December 31.brought up to December 31.

Let’s look at the entry to record the conversion.Let’s look at the entry to record the conversion.

On December 31, 2003, all of the bondholders of On December 31, 2003, all of the bondholders of Matrix, Inc. convert their bonds into common stock. Matrix, Inc. convert their bonds into common stock.

There are 10,000 bonds outstanding with a face There are 10,000 bonds outstanding with a face value of $1,000 each. Each bond is convertible into value of $1,000 each. Each bond is convertible into 50 shares of the company’s $1 par value common 50 shares of the company’s $1 par value common

stock. There is $1,645,000 on unamortized discount stock. There is $1,645,000 on unamortized discount associated with the bonds that are converted. associated with the bonds that are converted. Interest and discount amortization have been Interest and discount amortization have been

brought up to December 31.brought up to December 31.

Let’s look at the entry to record the conversion.Let’s look at the entry to record the conversion.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-49

Convertible Bonds

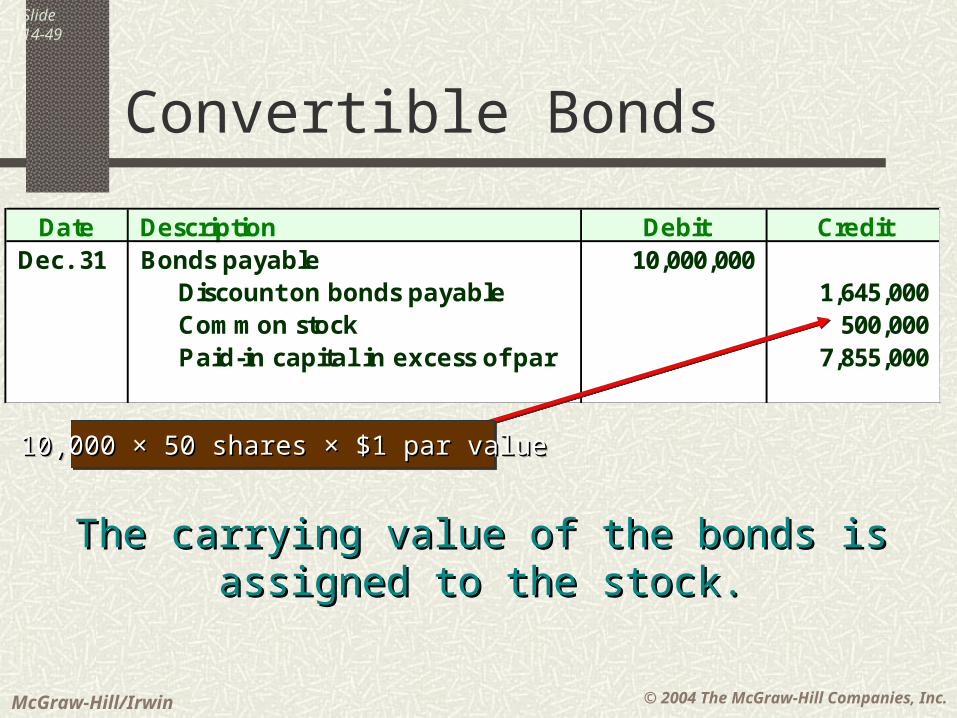

Date Description Debit CreditDec. 31 Bonds payable 10,000,000

Discount on bonds payable 1,645,000 Common stock 500,000 Paid-in capital in excess of par 7,855,000

10,000 10,000 × 50 shares × $1 par value× 50 shares × $1 par value10,000 10,000 × 50 shares × $1 par value× 50 shares × $1 par value

The carrying value of the bonds is assigned to the stock.The carrying value of the bonds is assigned to the stock.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-50

Bonds With Detachable Warrants

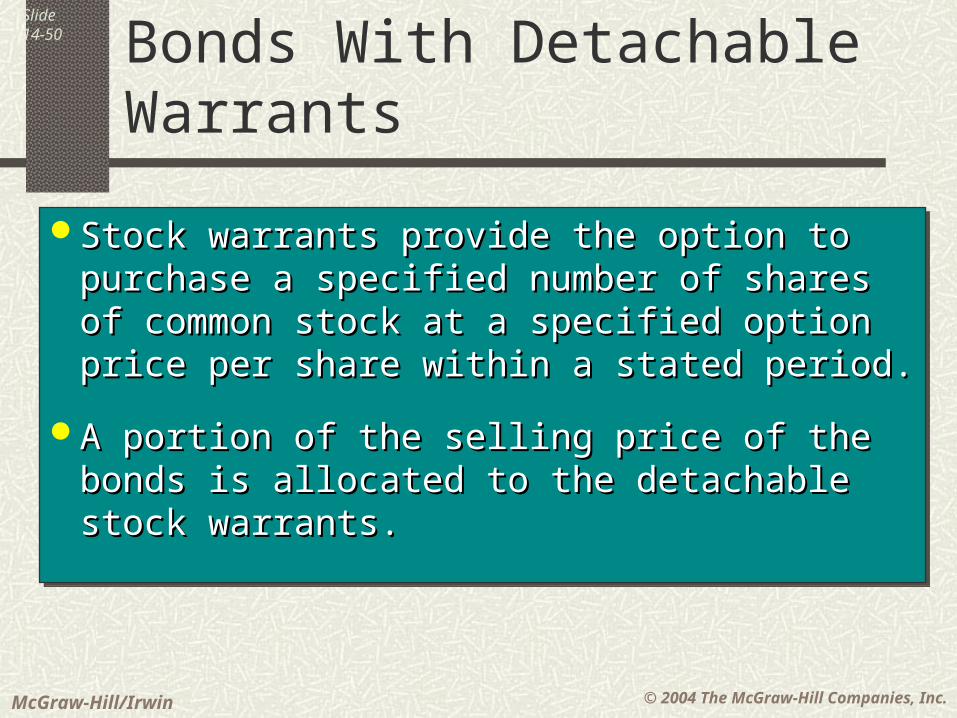

Stock warrants provide the option to Stock warrants provide the option to purchase a specified number of shares of purchase a specified number of shares of common stock at a specified option price common stock at a specified option price per share within a stated period.per share within a stated period.

A portion of the selling price of the bonds is A portion of the selling price of the bonds is allocated to the detachable stock warrants.allocated to the detachable stock warrants.

Stock warrants provide the option to Stock warrants provide the option to purchase a specified number of shares of purchase a specified number of shares of common stock at a specified option price common stock at a specified option price per share within a stated period.per share within a stated period.

A portion of the selling price of the bonds is A portion of the selling price of the bonds is allocated to the detachable stock warrants.allocated to the detachable stock warrants.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-51

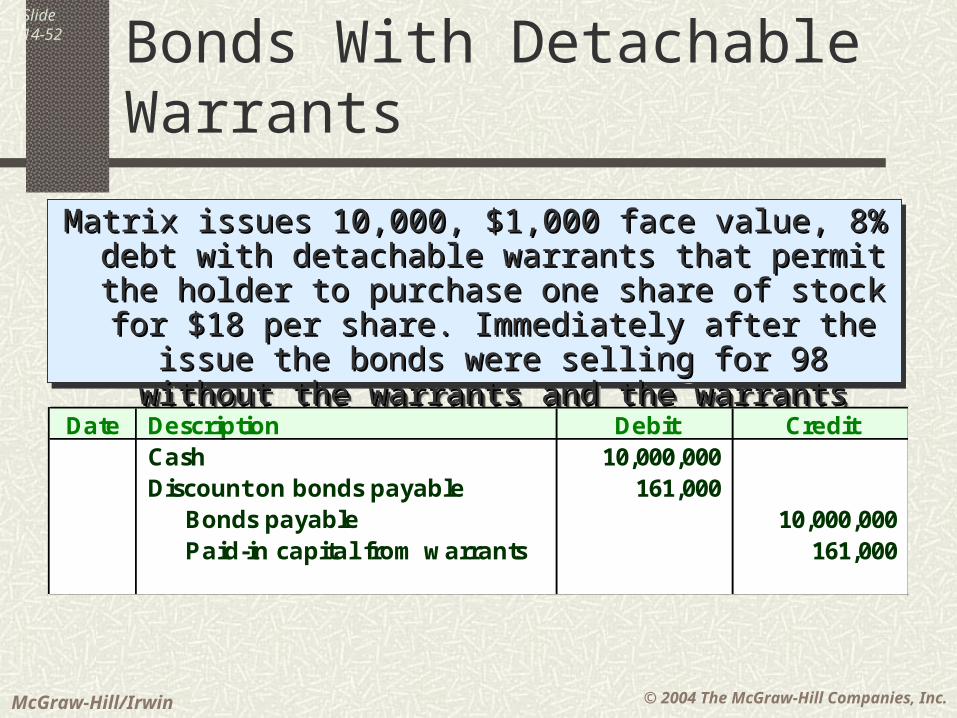

Bonds With Detachable Warrants

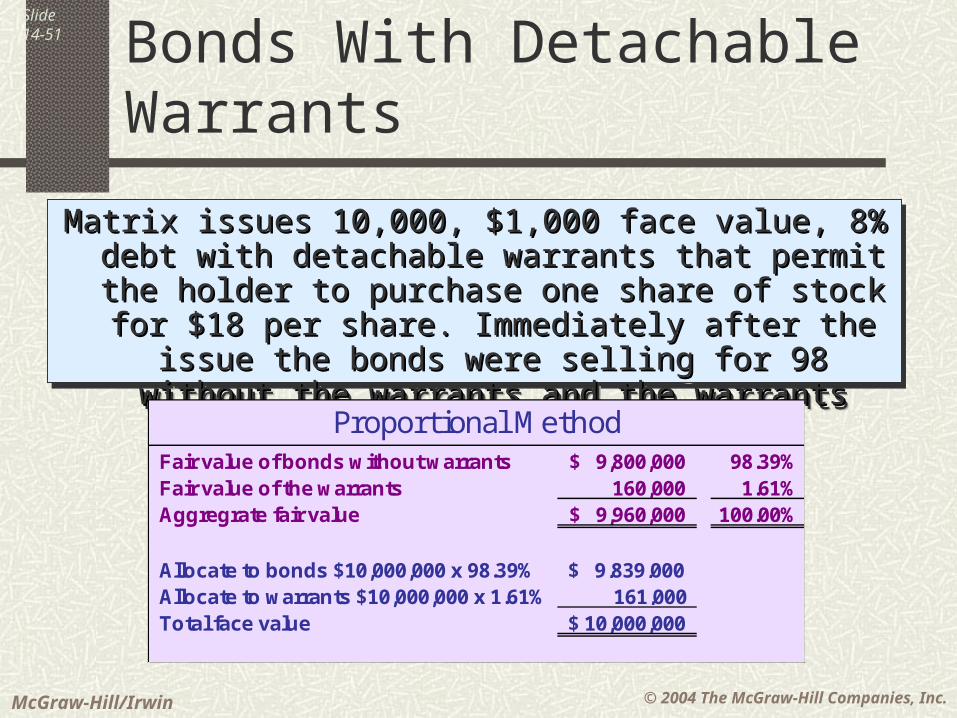

Matrix issues 10,000, $1,000 face value, 8% debt with Matrix issues 10,000, $1,000 face value, 8% debt with detachable warrants that permit the holder to purchase detachable warrants that permit the holder to purchase one share of stock for $18 per share. Immediately after one share of stock for $18 per share. Immediately after

the issue the bonds were selling for 98 without the the issue the bonds were selling for 98 without the warrants and the warrants have a market value of $16. warrants and the warrants have a market value of $16.

Matrix issues 10,000, $1,000 face value, 8% debt with Matrix issues 10,000, $1,000 face value, 8% debt with detachable warrants that permit the holder to purchase detachable warrants that permit the holder to purchase one share of stock for $18 per share. Immediately after one share of stock for $18 per share. Immediately after

the issue the bonds were selling for 98 without the the issue the bonds were selling for 98 without the warrants and the warrants have a market value of $16. warrants and the warrants have a market value of $16.

Fair value of bonds without warrants 9,800,000$ 98.39%Fair value of the warrants 160,000 1.61%Aggregrate fair value 9,960,000$ 100.00%

Allocate to bonds $10,000,000 x 98.39% $ 9,839,000 Allocate to warrants $10,000,000 x 1.61% 161,000 Total face value $ 10,000,000

Proportional Method

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-52

Bonds With Detachable Warrants

Matrix issues 10,000, $1,000 face value, 8% debt with Matrix issues 10,000, $1,000 face value, 8% debt with detachable warrants that permit the holder to purchase detachable warrants that permit the holder to purchase one share of stock for $18 per share. Immediately after one share of stock for $18 per share. Immediately after

the issue the bonds were selling for 98 without the the issue the bonds were selling for 98 without the warrants and the warrants have a market value of $16. warrants and the warrants have a market value of $16.

Matrix issues 10,000, $1,000 face value, 8% debt with Matrix issues 10,000, $1,000 face value, 8% debt with detachable warrants that permit the holder to purchase detachable warrants that permit the holder to purchase one share of stock for $18 per share. Immediately after one share of stock for $18 per share. Immediately after

the issue the bonds were selling for 98 without the the issue the bonds were selling for 98 without the warrants and the warrants have a market value of $16. warrants and the warrants have a market value of $16.

Date Description Debit CreditCash 10,000,000 Discount on bonds payable 161,000 Bonds payable 10,000,000 Paid-in capital from warrants 161,000

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-53

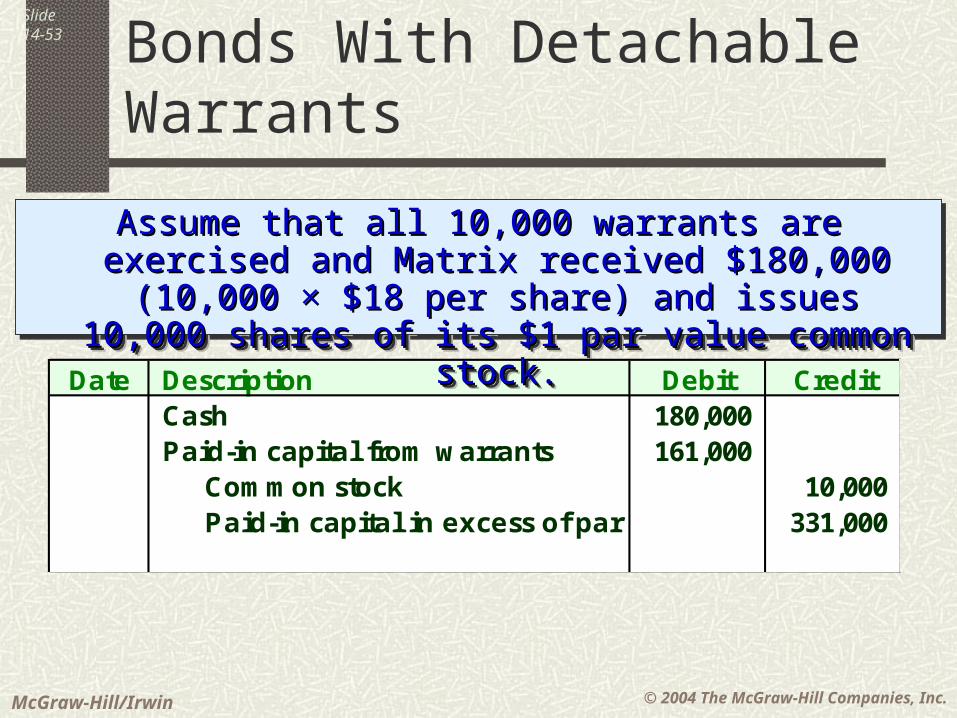

Bonds With Detachable Warrants

Date Description Debit CreditCash 180,000 Paid-in capital from warrants 161,000 Common stock 10,000 Paid-in capital in excess of par 331,000

Assume that all 10,000 warrants are exercised and Matrix Assume that all 10,000 warrants are exercised and Matrix received $180,000 (10,000 received $180,000 (10,000 × $18 per share) and issues × $18 per share) and issues

10,000 shares of its $1 par value common stock.10,000 shares of its $1 par value common stock.

Assume that all 10,000 warrants are exercised and Matrix Assume that all 10,000 warrants are exercised and Matrix received $180,000 (10,000 received $180,000 (10,000 × $18 per share) and issues × $18 per share) and issues

10,000 shares of its $1 par value common stock.10,000 shares of its $1 par value common stock.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-54

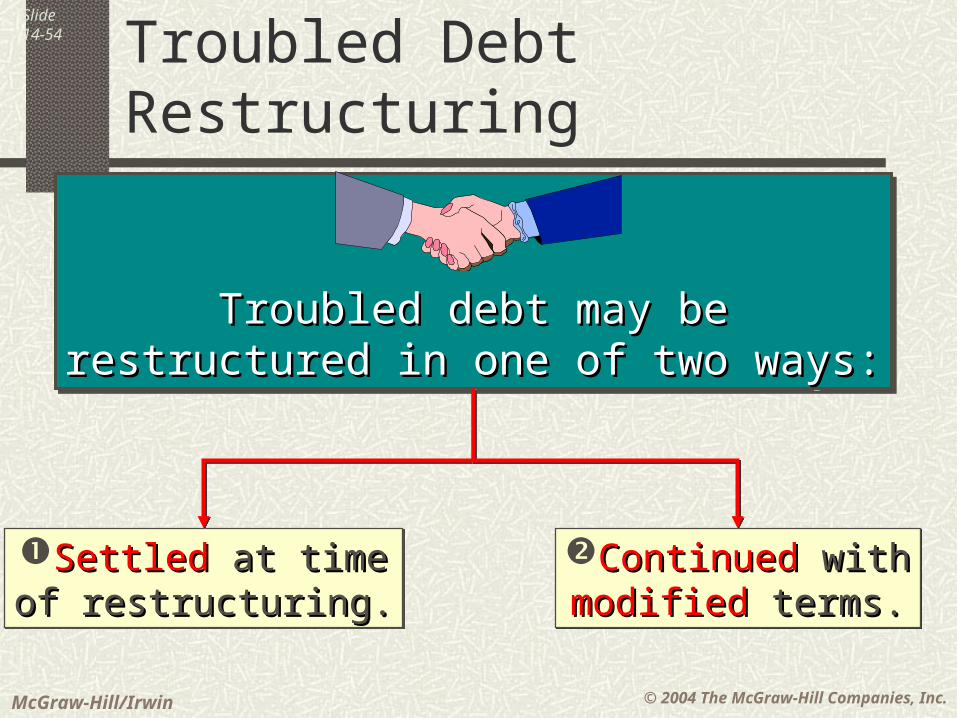

Troubled Debt Restructuring

Troubled debt may beTroubled debt may berestructured in one of two ways:restructured in one of two ways:

Troubled debt may beTroubled debt may berestructured in one of two ways:restructured in one of two ways:

SettledSettled at time at timeof restructuring.of restructuring.

SettledSettled at time at timeof restructuring.of restructuring.

Continued Continued withwithmodifiedmodified terms.terms.

Continued Continued withwithmodifiedmodified terms.terms.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-55

Troubled Debt Restructuring

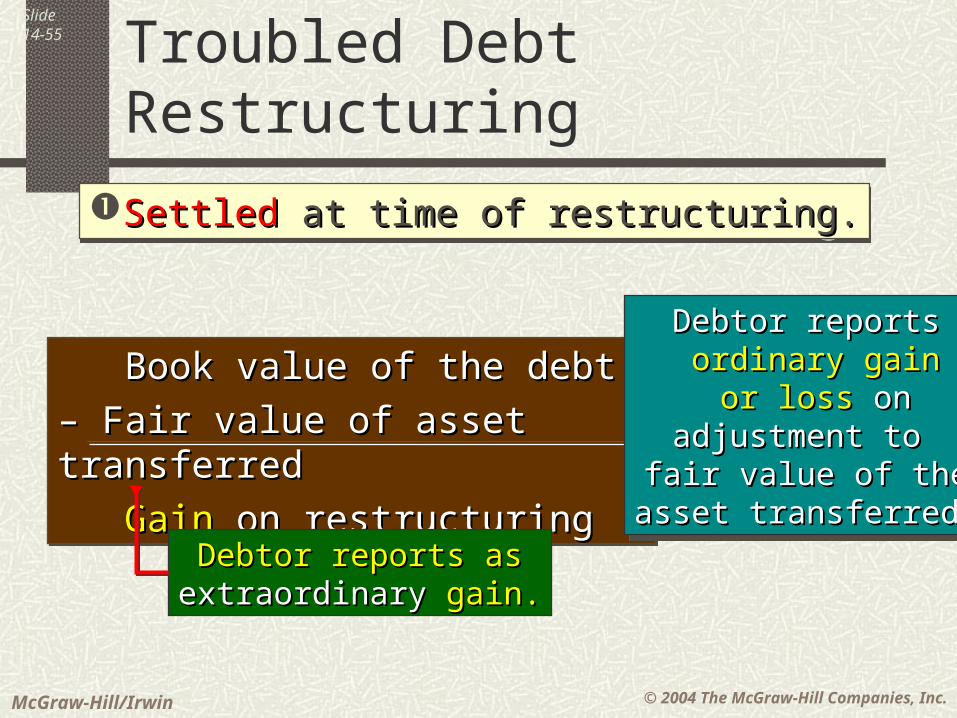

SettledSettled at time of restructuring. at time of restructuring.SettledSettled at time of restructuring. at time of restructuring.

Book value of the debtBook value of the debt

– – Fair value of asset transferredFair value of asset transferred

GainGain on restructuring on restructuring

Book value of the debtBook value of the debt

– – Fair value of asset transferredFair value of asset transferred

GainGain on restructuring on restructuring

Debtor reports asDebtor reports asextraordinaryextraordinary gain. gain.

Debtor reportsDebtor reports ordinary gainordinary gain

or loss or loss on onadjustment to adjustment to

fair value of thefair value of theasset transferred.asset transferred.

Debtor reportsDebtor reports ordinary gainordinary gain

or loss or loss on onadjustment to adjustment to

fair value of thefair value of theasset transferred.asset transferred.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-56

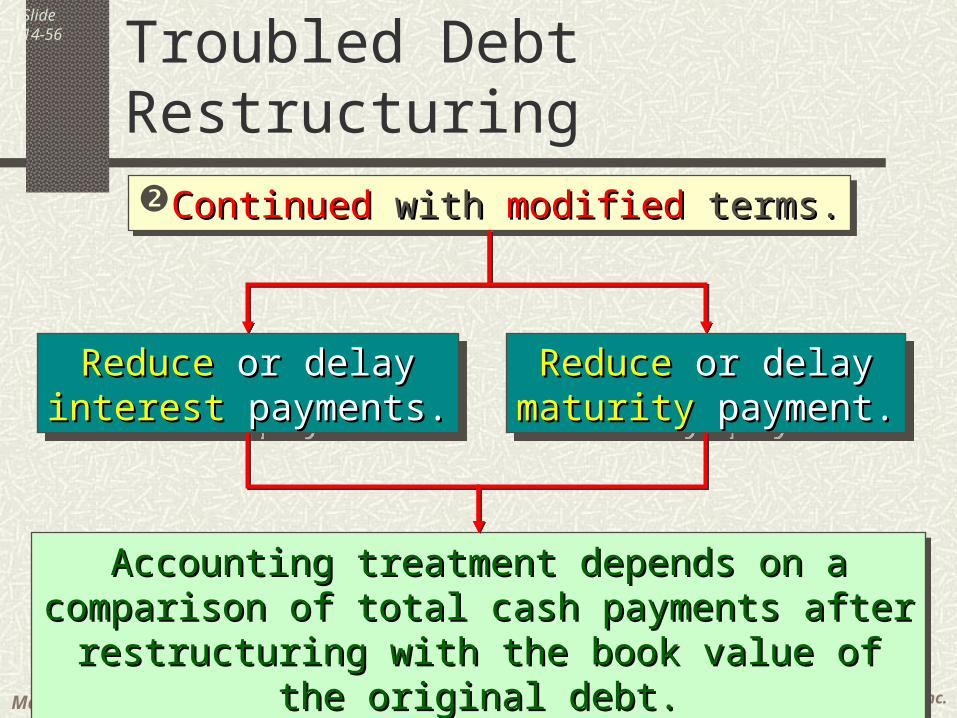

Troubled Debt Restructuring

ContinuedContinued with with modified modified terms.terms.ContinuedContinued with with modified modified terms.terms.

ReduceReduce or delay or delayinterest interest payments.payments.ReduceReduce or delay or delay

interest interest payments.payments.ReduceReduce or delay or delay

maturitymaturity payment. payment.ReduceReduce or delay or delay

maturitymaturity payment. payment.

Accounting treatment depends on a comparison of Accounting treatment depends on a comparison of total cash payments after restructuring with the book total cash payments after restructuring with the book

value of the original debt.value of the original debt.

Accounting treatment depends on a comparison of Accounting treatment depends on a comparison of total cash payments after restructuring with the book total cash payments after restructuring with the book

value of the original debt.value of the original debt.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-57

Troubled Debt Restructuring

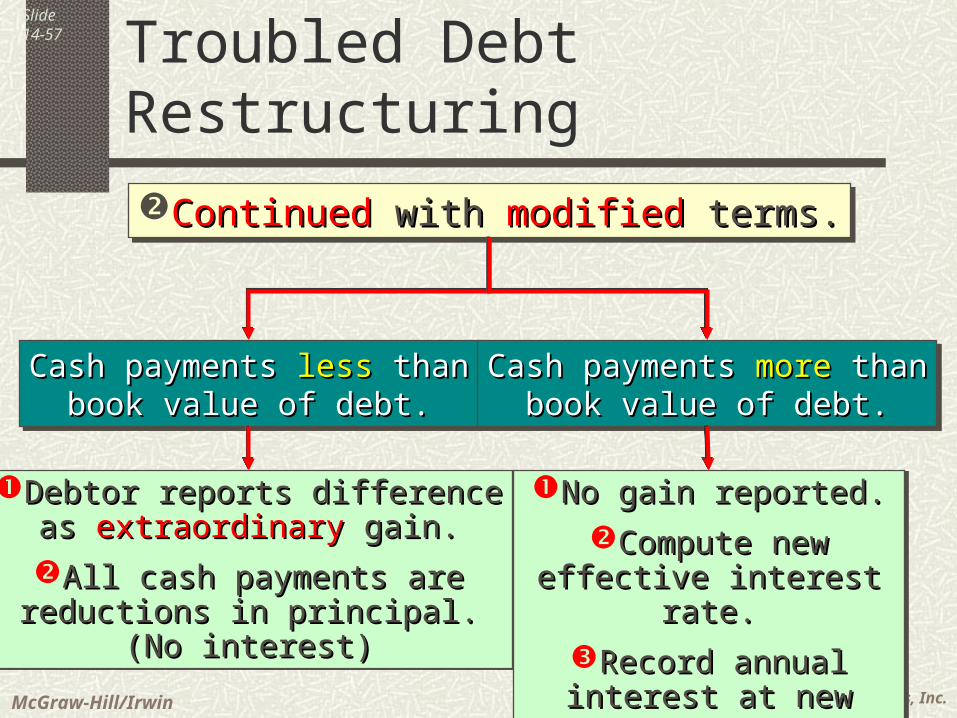

ContinuedContinued with with modifiedmodified terms.terms.ContinuedContinued with with modifiedmodified terms.terms.

Cash payments Cash payments less less thanthanbook value of debt.book value of debt.

Cash payments Cash payments less less thanthanbook value of debt.book value of debt.

Cash payments Cash payments moremore than thanbook value of debt.book value of debt.

Cash payments Cash payments moremore than thanbook value of debt.book value of debt.

Debtor reports differenceDebtor reports differenceas as extraordinaryextraordinary gain. gain.

All cash payments areAll cash payments arereductions in principal.reductions in principal.

(No interest)(No interest)

Debtor reports differenceDebtor reports differenceas as extraordinaryextraordinary gain. gain.

All cash payments areAll cash payments arereductions in principal.reductions in principal.

(No interest)(No interest)

No gain reported.No gain reported.

Compute newCompute neweffective interest rate.effective interest rate.

Record annualRecord annualinterest at new rate.interest at new rate.

No gain reported.No gain reported.

Compute newCompute neweffective interest rate.effective interest rate.

Record annualRecord annualinterest at new rate.interest at new rate.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide14-58

End of Chapter 14

Related Documents