© The McGraw-Hill Companies, Inc., 2002 McGraw-Hill/Irwin

© The McGraw-Hill Companies, Inc., 2002 McGraw-Hill/Irwin.

Dec 17, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

© The McGraw-Hill Companies, Inc., 2002McGraw-Hill/Irwin

© The McGraw-Hill Companies, Inc., 2002McGraw-Hill/Irwin

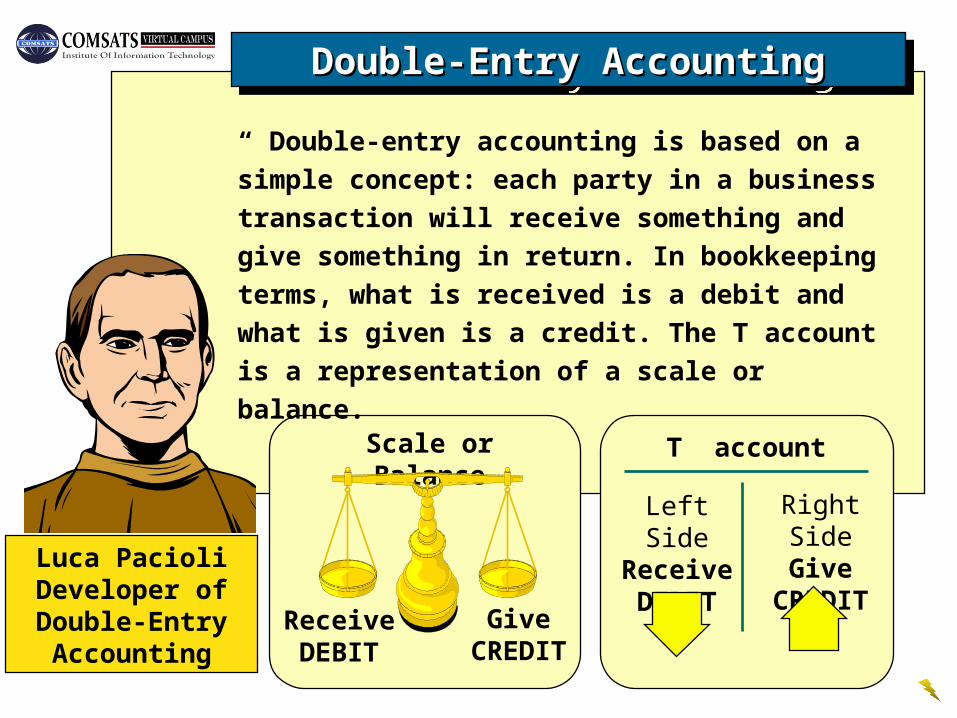

Double-Entry AccountingDouble-Entry AccountingDouble-Entry AccountingDouble-Entry Accounting

“ Double-entry accounting is based on a simple concept: each party in a business transaction will receive something and give something in return. In bookkeeping terms, what is received is a debit and what is given is a credit. The T account is a representation of a scale or balance.”

Luca PacioliDeveloper ofDouble-EntryAccounting

Scale or Balance

ReceiveDEBIT

GiveCREDIT

T account

Left SideReceiveDEBIT

Right SideGive

CREDIT

© The McGraw-Hill Companies, Inc., 2002McGraw-Hill/Irwin

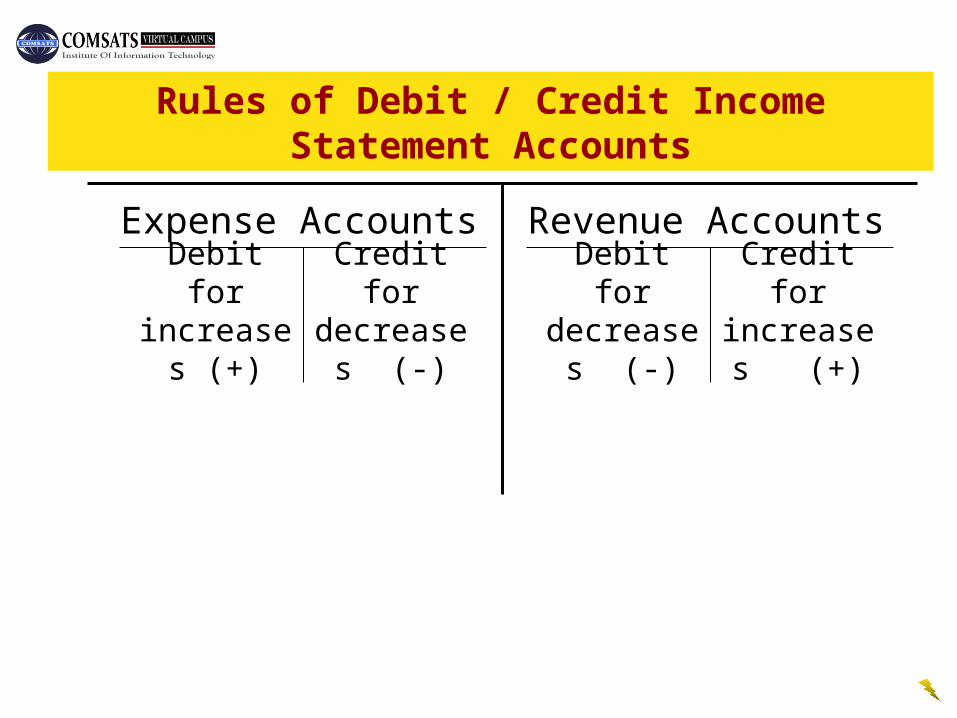

Credit for increases

(+)

Credit for decreases

(-)

Debit for increases

(+)

Debit for decreases

(-)

Expense Accounts Revenue Accounts

Rules of Debit / Credit Income Statement Accounts

© The McGraw-Hill Companies, Inc., 2002McGraw-Hill/Irwin

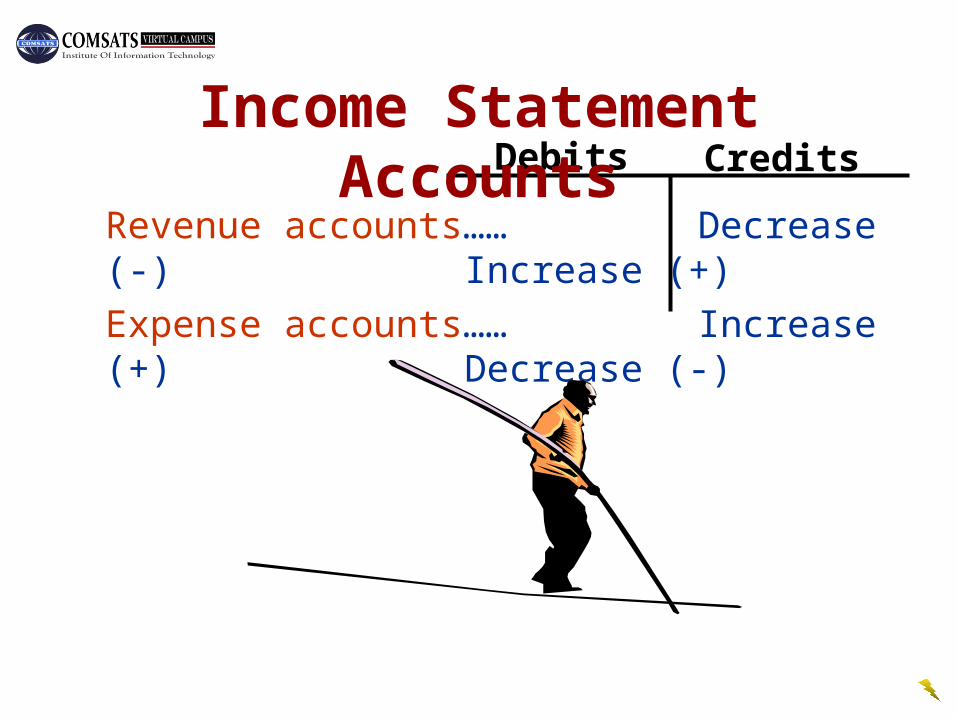

Debits Credits

Revenue accounts…… Decrease (-) Increase (+)

Expense accounts…… Increase (+) Decrease (-)

Income Statement Accounts

© The McGraw-Hill Companies, Inc., 2002McGraw-Hill/Irwin

Payment of dividends

Payment of dividends

© The McGraw-Hill Companies, Inc., 2002McGraw-Hill/Irwin

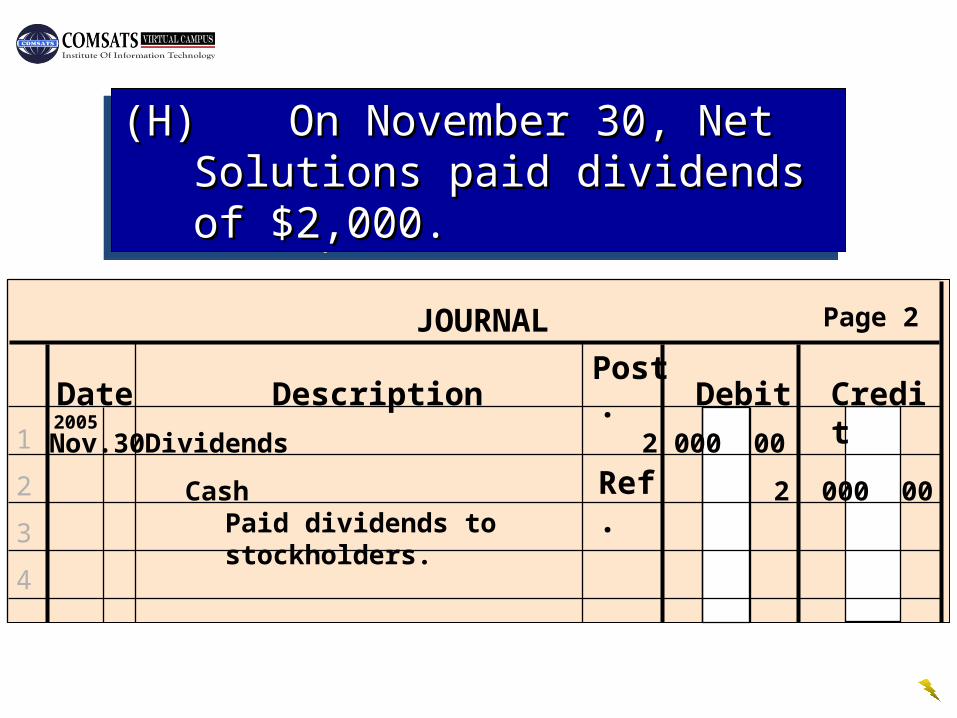

Post. Ref.

JOURNAL

Date Description Debit Credit

Page 2

1

2

3

4

Nov. 302005

Dividends 2 000 00

Cash 2 000 00

Paid dividends to stockholders.

(H)(H) On November 30, Net Solutions paid On November 30, Net Solutions paid dividends of $2,000.dividends of $2,000.

(H)(H) On November 30, Net Solutions paid On November 30, Net Solutions paid dividends of $2,000.dividends of $2,000.

© The McGraw-Hill Companies, Inc., 2002McGraw-Hill/Irwin

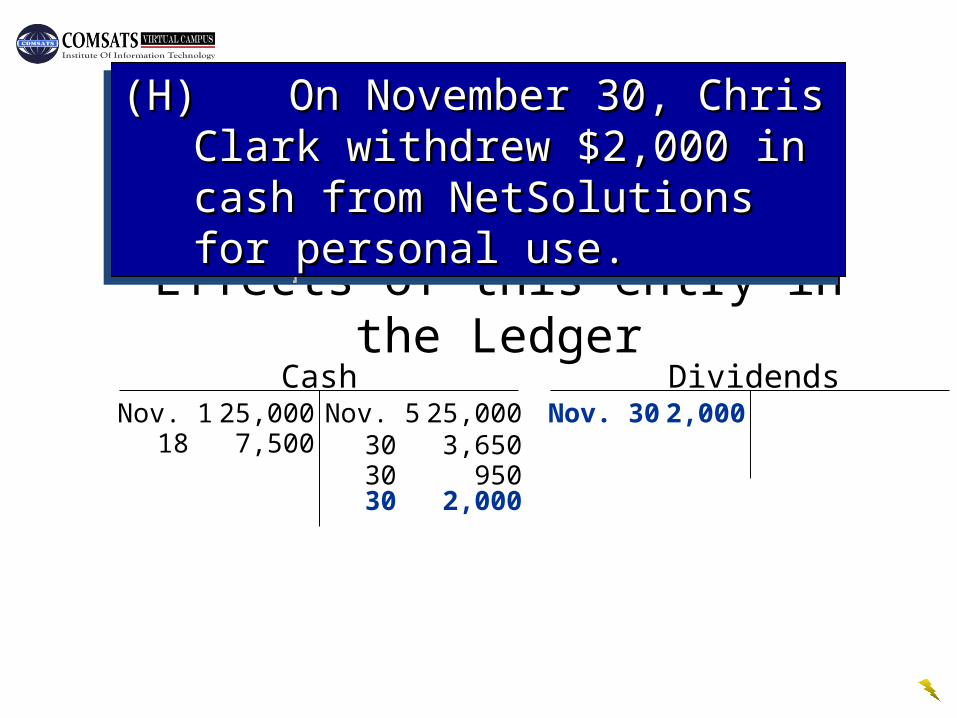

30 95030 2,000

CashNov. 1 25,000 Nov. 5 25,000

18 7,500 30 3,650

Effects of this entry in the LedgerDividends

Nov. 30 2,000

(H)(H) On November 30, Chris Clark On November 30, Chris Clark withdrew $2,000 in cash from withdrew $2,000 in cash from NetSolutions for personal use.NetSolutions for personal use.

(H)(H) On November 30, Chris Clark On November 30, Chris Clark withdrew $2,000 in cash from withdrew $2,000 in cash from NetSolutions for personal use.NetSolutions for personal use.

© The McGraw-Hill Companies, Inc., 2002McGraw-Hill/Irwin

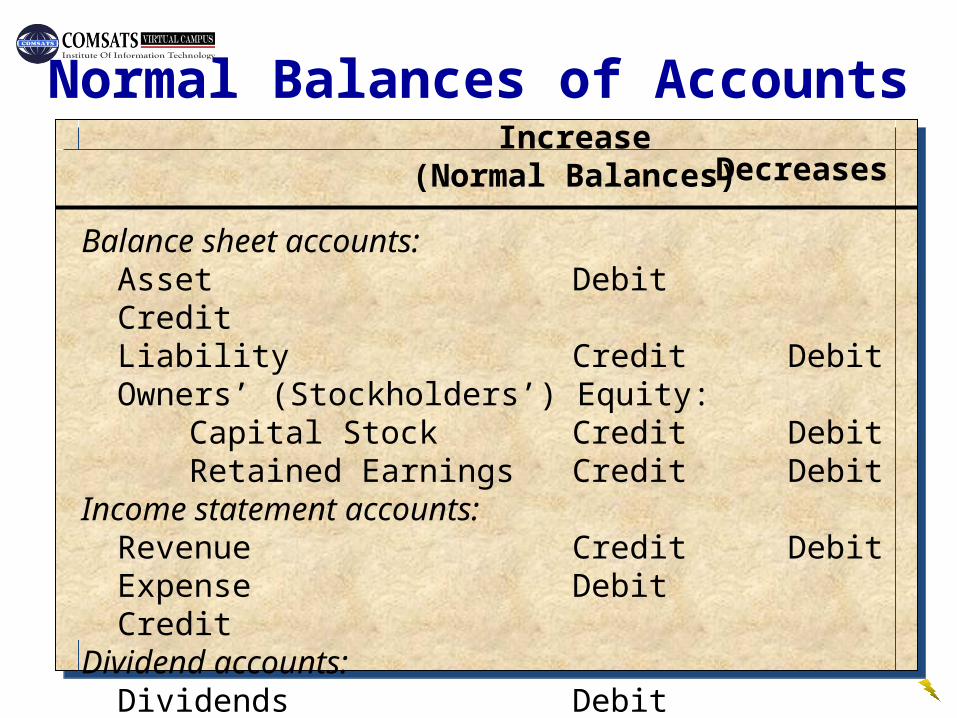

Increase(Normal Balances) Decreases

Balance sheet accounts:AssetDebit CreditLiability Credit DebitOwners’ (Stockholders’) Equity:

Capital Stock Credit DebitRetained Earnings Credit Debit

Income statement accounts:Revenue Credit DebitExpense Debit Credit

Dividend accounts:Dividends Debit Credit

Normal Balances of Accounts

© The McGraw-Hill Companies, Inc., 2002McGraw-Hill/Irwin

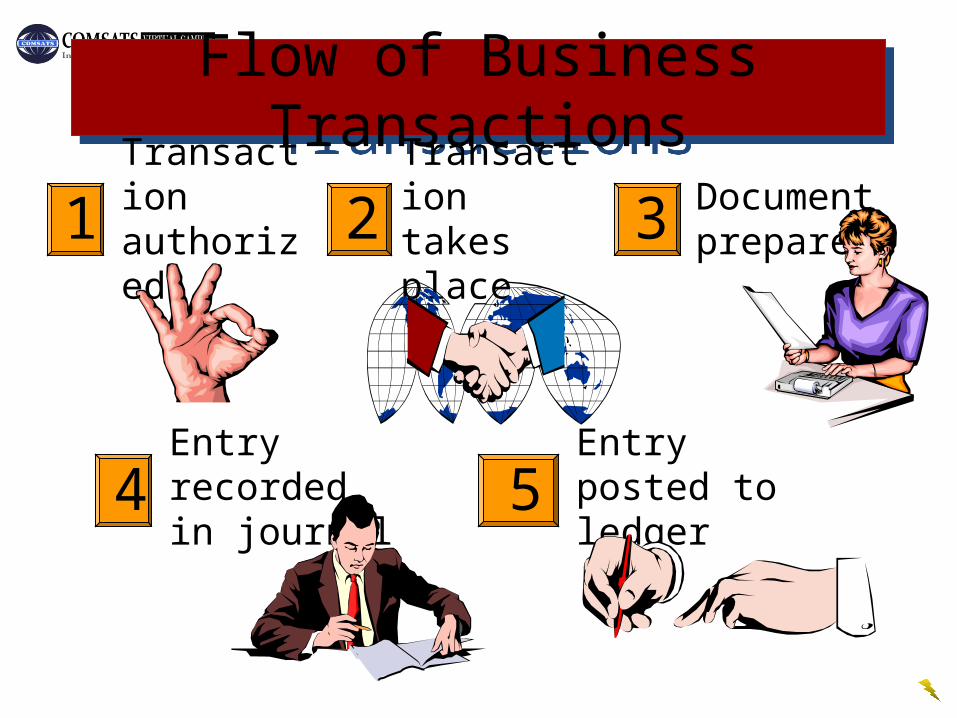

Flow of Business TransactionsFlow of Business Transactions

1 Transaction authorized 2 Transaction

takes place 3 Document prepared

4Entry recorded in journal 5

Entry posted to ledger

© The McGraw-Hill Companies, Inc., 2002McGraw-Hill/Irwin

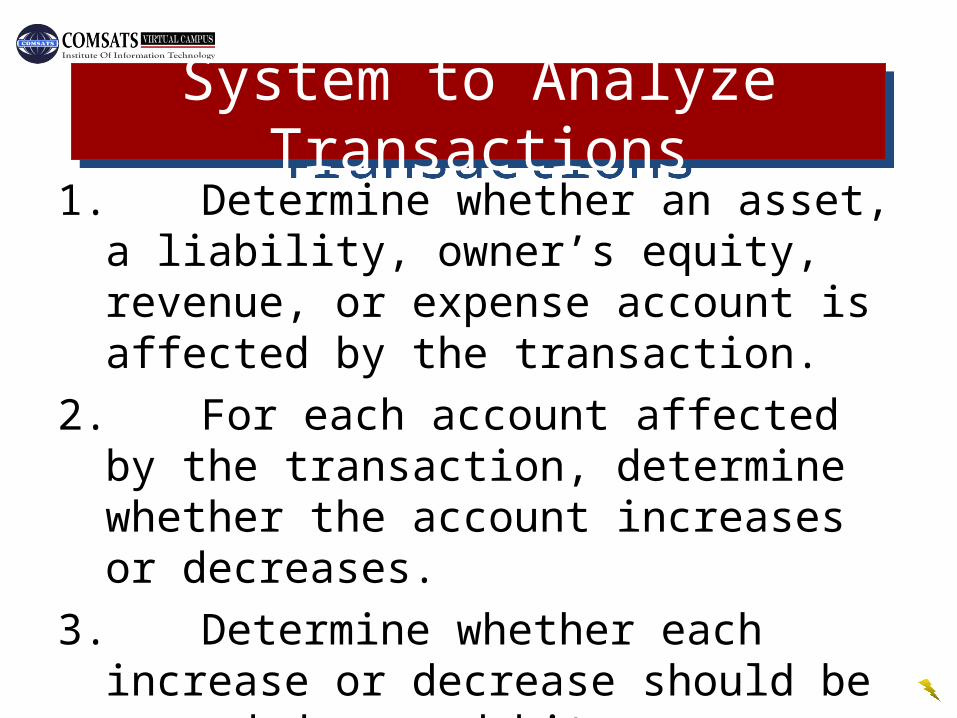

System to Analyze TransactionsSystem to Analyze Transactions1. Determine whether an asset, a liability,

owner’s equity, revenue, or expense account is affected by the transaction.

2. For each account affected by the transaction, determine whether the account increases or decreases.

3. Determine whether each increase or decrease should be recorded as a debit or a credit.

© The McGraw-Hill Companies, Inc., 2002McGraw-Hill/Irwin

Let’s see the example of JJ’s

Lawn Care Service.

Let’s see the example of JJ’s

Lawn Care Service.

© The McGraw-Hill Companies, Inc., 2002McGraw-Hill/Irwin

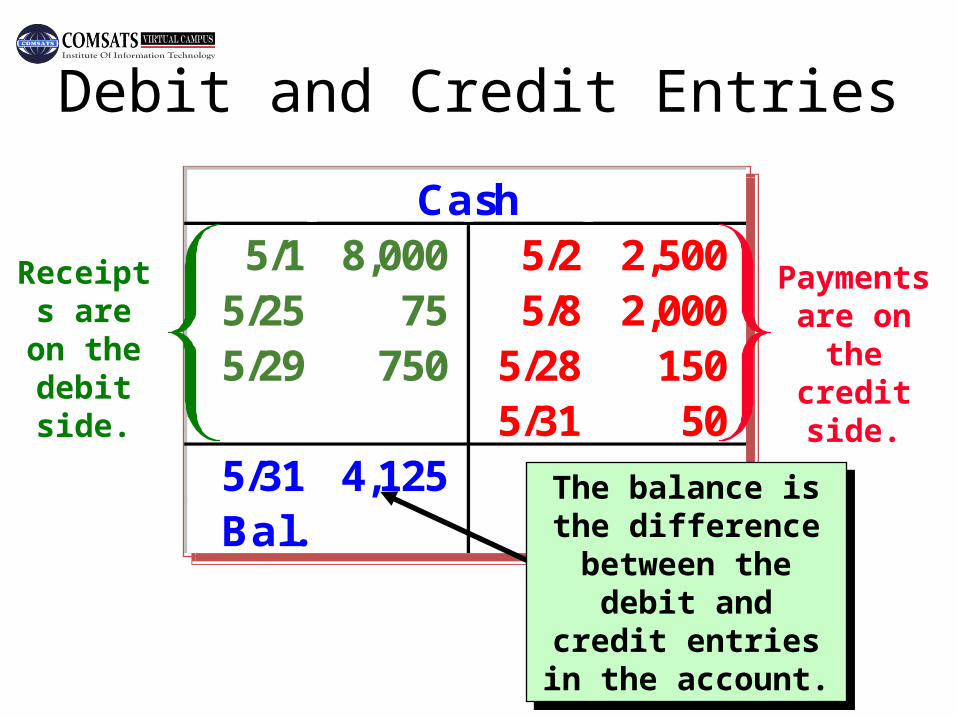

Cash5/1 8,000 5/2 2,500

5/25 75 5/8 2,0005/29 750 5/28 150

5/31 50 5/31 4,125Bal.

Cash5/1 8,000 5/2 2,500

5/25 75 5/8 2,0005/29 750 5/28 150

5/31 50 5/31 4,125Bal.

Receipts are on

the debit side.

Payments are on the

credit side.

The balance is the difference between the debit and credit

entries in the account.

The balance is the difference between the debit and credit

entries in the account.

Debit and Credit Entries

© The McGraw-Hill Companies, Inc., 2002McGraw-Hill/Irwin

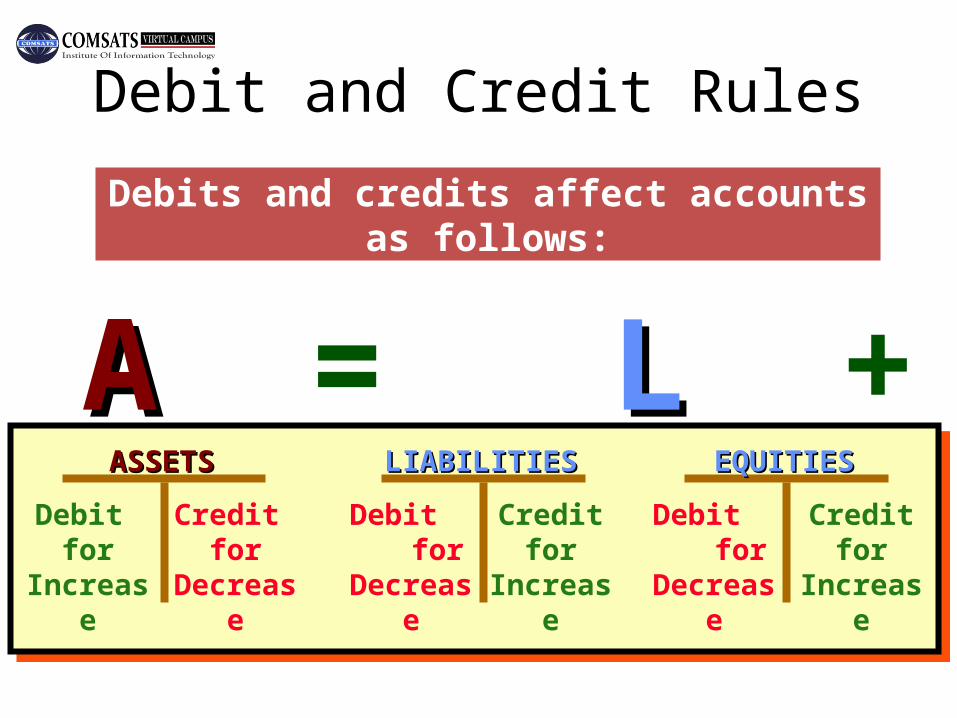

AA = LL + OEOEASSETSASSETS

Debit for

Increase

Credit for

Decrease

EQUITIESEQUITIES

Debit for

Decrease

Credit for

Increase

LIABILITIESLIABILITIES

Debit for

Decrease

Credit for

Increase

Debits and credits affect accounts as follows:

Debits and credits affect accounts as follows:

Debit and Credit Rules

© The McGraw-Hill Companies, Inc., 2002McGraw-Hill/Irwin

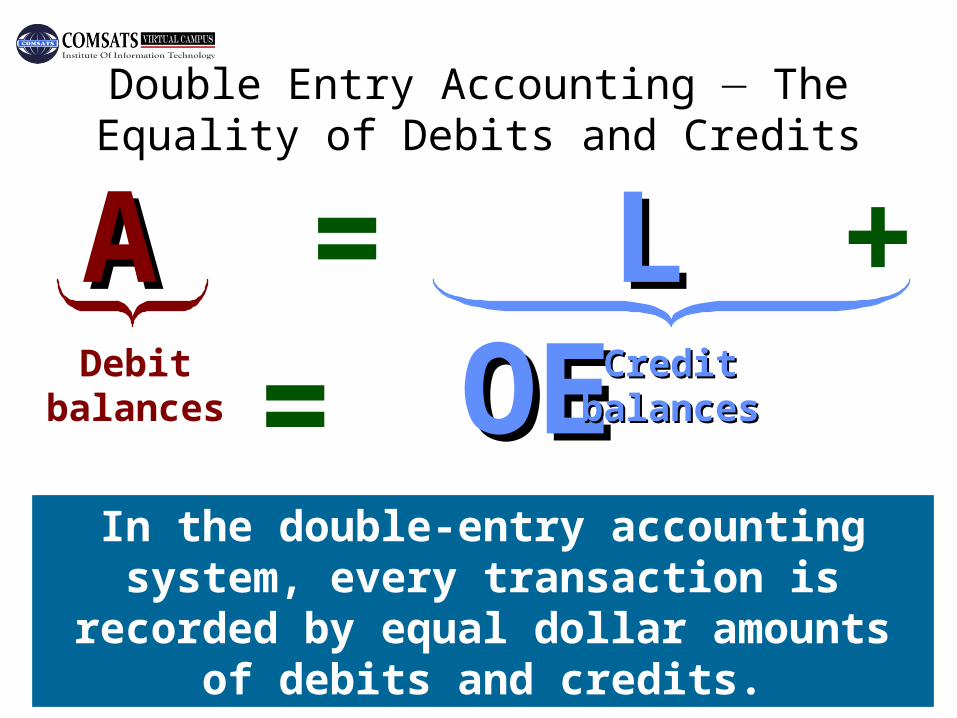

AA = LL + OEOEDebit

balancesCredit Credit

balancesbalances=In the double-entry accounting system, every transaction is recorded by equal dollar amounts of debits and credits.

In the double-entry accounting system, every transaction is recorded by equal dollar amounts of debits and credits.

Double Entry AccountingThe Equality of Debits and Credits

© The McGraw-Hill Companies, Inc., 2002McGraw-Hill/Irwin

Let’s record selected

transactions for JJ’s Lawn Care Service in the

accounts.

© The McGraw-Hill Companies, Inc., 2002McGraw-Hill/Irwin

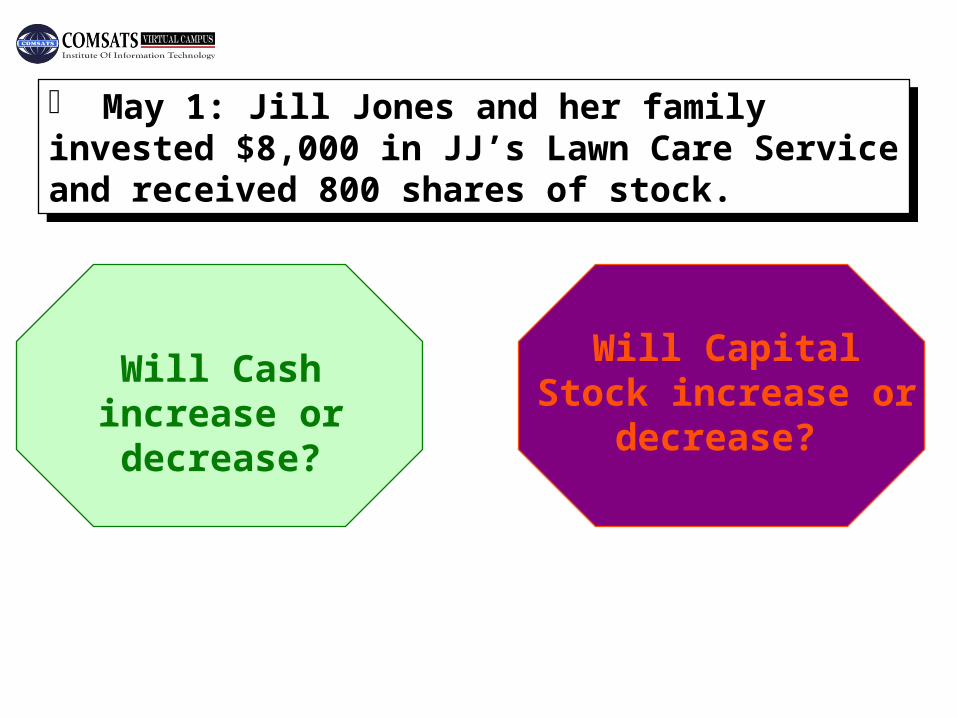

May 1: Jill Jones and her family invested $8,000 in JJ’s Lawn Care Service and received 800 shares of stock.

May 1: Jill Jones and her family invested $8,000 in JJ’s Lawn Care Service and received 800 shares of stock.

Will Cash increase or decrease?

Will Capital Stock increase or decrease?

© The McGraw-Hill Companies, Inc., 2002McGraw-Hill/Irwin

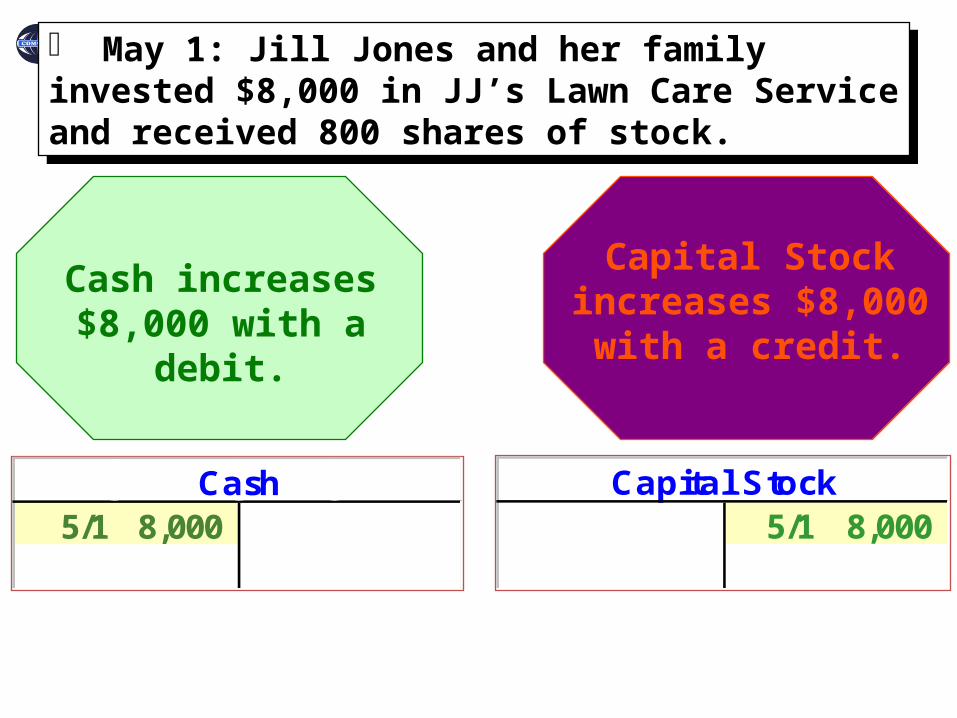

Capital Stock5/1 8,000

Cash5/1 8,000

May 1: Jill Jones and her family invested $8,000 in JJ’s Lawn Care Service and received 800 shares of stock.

May 1: Jill Jones and her family invested $8,000 in JJ’s Lawn Care Service and received 800 shares of stock.

Cash increases $8,000 with a debit.

Capital Stock increases $8,000

with a credit.

© The McGraw-Hill Companies, Inc., 2002McGraw-Hill/Irwin

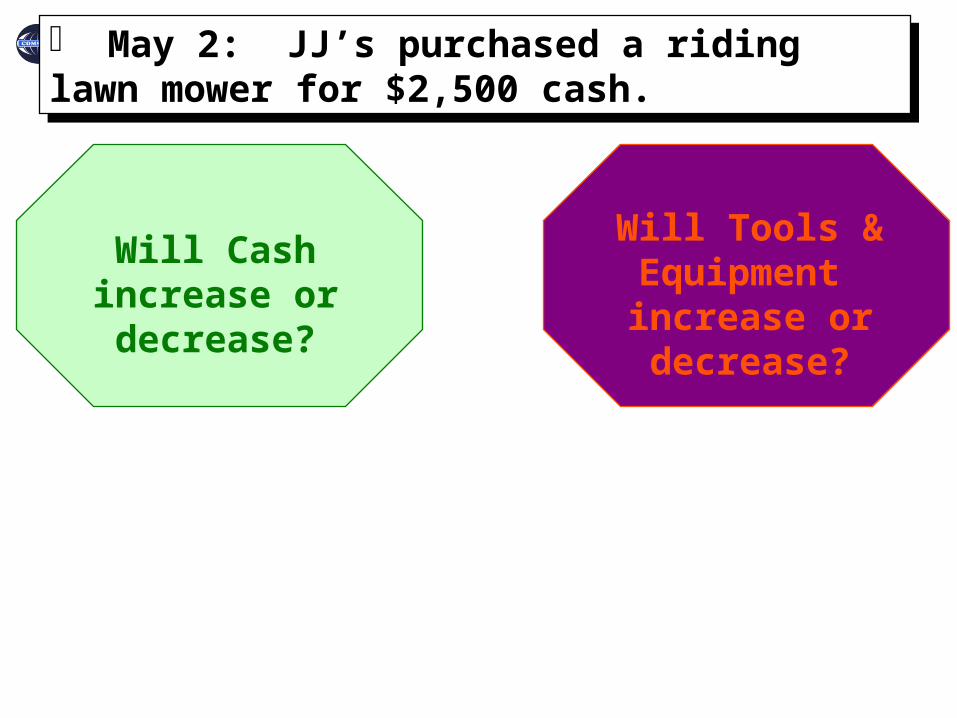

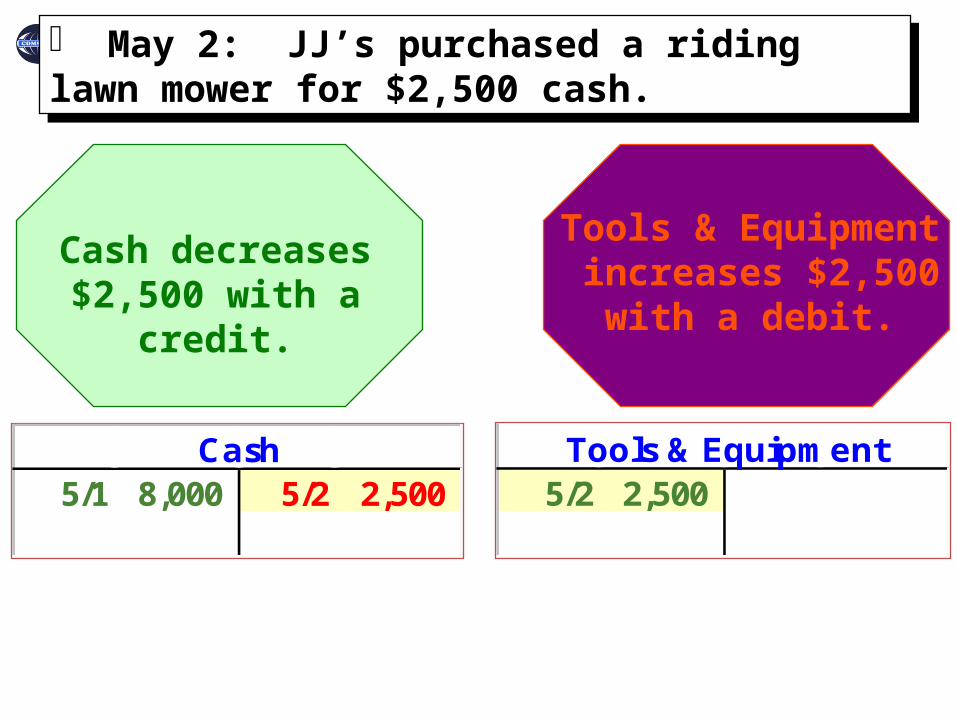

May 2: JJ’s purchased a riding lawn mower for $2,500 cash.

May 2: JJ’s purchased a riding lawn mower for $2,500 cash.

Will Cash increase or decrease?

Will Tools & Equipment increase

or decrease?

© The McGraw-Hill Companies, Inc., 2002McGraw-Hill/Irwin

May 2: JJ’s purchased a riding lawn mower for $2,500 cash.

May 2: JJ’s purchased a riding lawn mower for $2,500 cash.

Tools & Equipment5/2 2,500

Cash5/1 8,000 5/2 2,500

Cash decreases $2,500 with a credit.

Tools & Equipment increases $2,500

with a debit.

© The McGraw-Hill Companies, Inc., 2002McGraw-Hill/Irwin

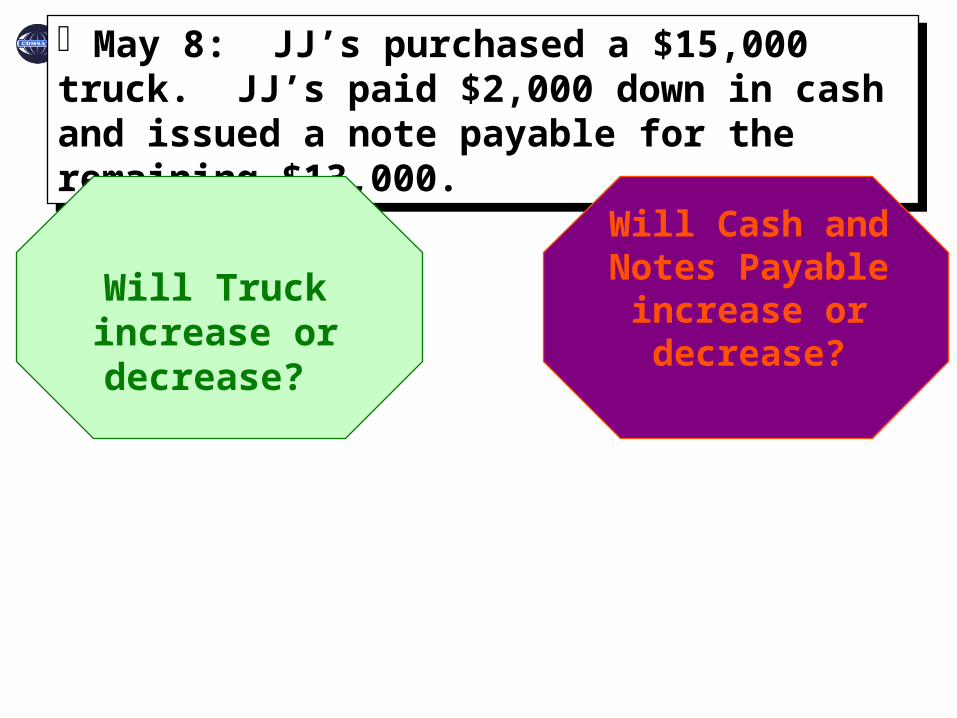

May 8: JJ’s purchased a $15,000 truck. JJ’s paid $2,000 down in cash and issued a note payable for the remaining $13,000.

May 8: JJ’s purchased a $15,000 truck. JJ’s paid $2,000 down in cash and issued a note payable for the remaining $13,000.

Will Truck increase or decrease?

Will Cash and Notes Payable

increase or decrease?

© The McGraw-Hill Companies, Inc., 2002McGraw-Hill/Irwin

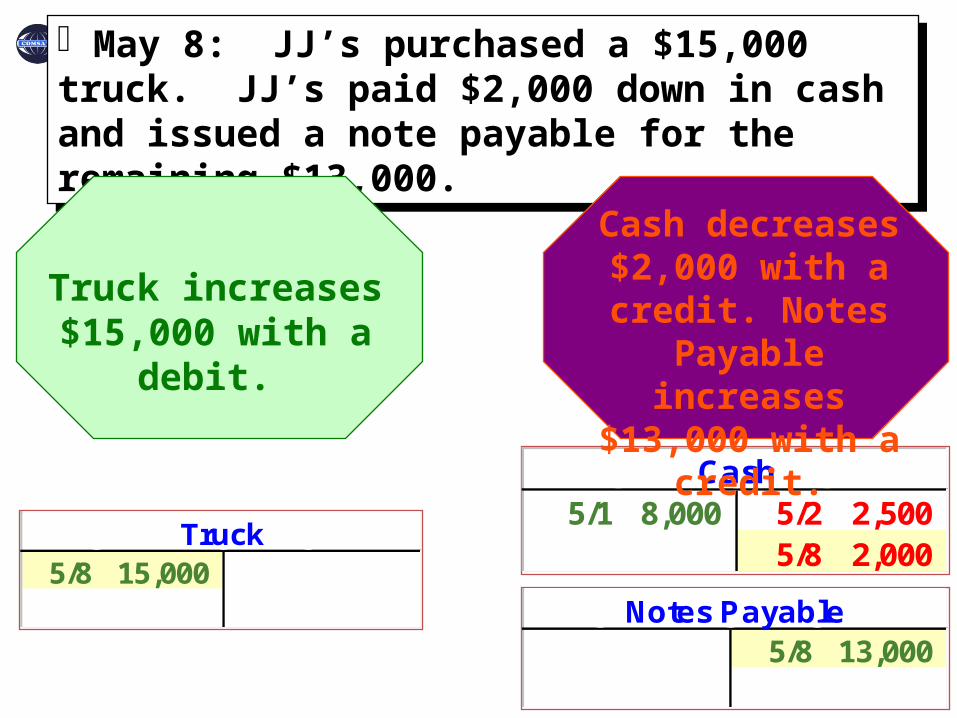

May 8: JJ’s purchased a $15,000 truck. JJ’s paid $2,000 down in cash and issued a note payable for the remaining $13,000.

May 8: JJ’s purchased a $15,000 truck. JJ’s paid $2,000 down in cash and issued a note payable for the remaining $13,000.

Truck5/8 15,000

Cash5/1 8,000 5/2 2,500

5/8 2,000

Notes Payable5/8 13,000

Truck increases $15,000 with a debit.

Cash decreases $2,000 with a credit.

Notes Payable increases $13,000

with a credit.

© The McGraw-Hill Companies, Inc., 2002McGraw-Hill/Irwin

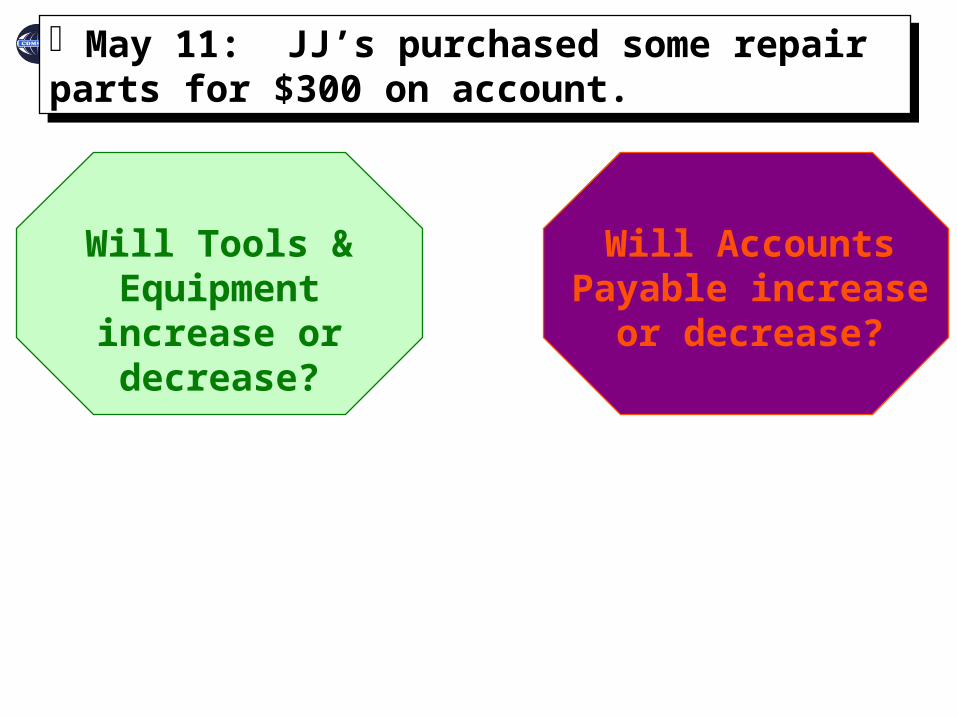

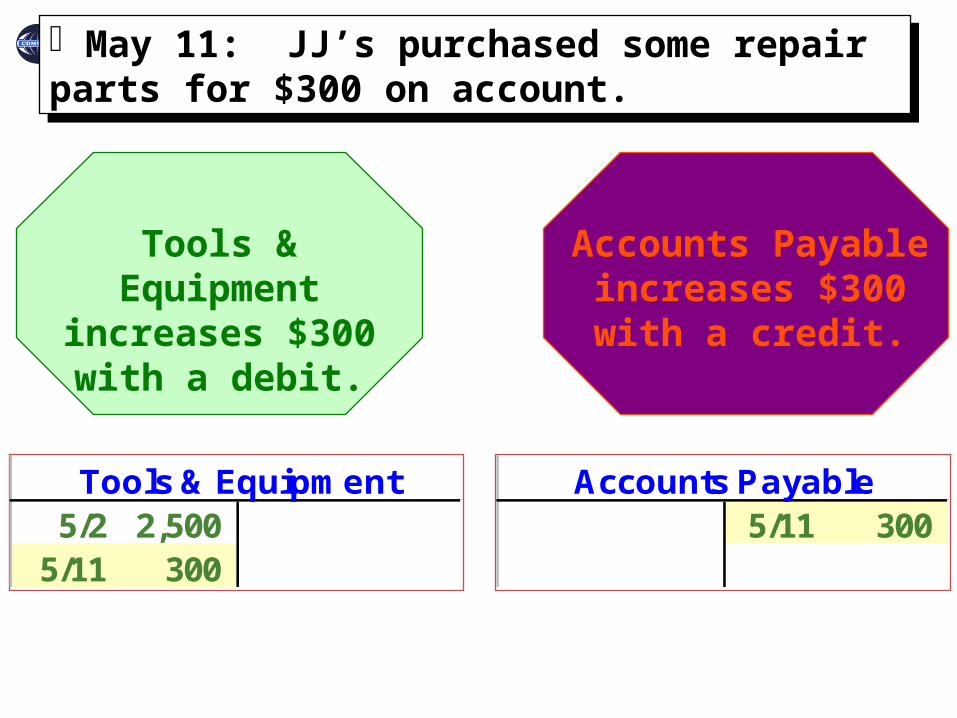

May 11: JJ’s purchased some repair parts for $300 on account.

May 11: JJ’s purchased some repair parts for $300 on account.

Will Tools & Equipment increase

or decrease?

Will Accounts Payable increase or

decrease?

© The McGraw-Hill Companies, Inc., 2002McGraw-Hill/Irwin

May 11: JJ’s purchased some repair parts for $300 on account.

May 11: JJ’s purchased some repair parts for $300 on account.

Tools & Equipment increases $300 with

a debit.

Accounts Payable increases $300 with

a credit.

Tools & Equipment5/2 2,500

5/11 300

Accounts Payable5/11 300

© The McGraw-Hill Companies, Inc., 2002McGraw-Hill/Irwin

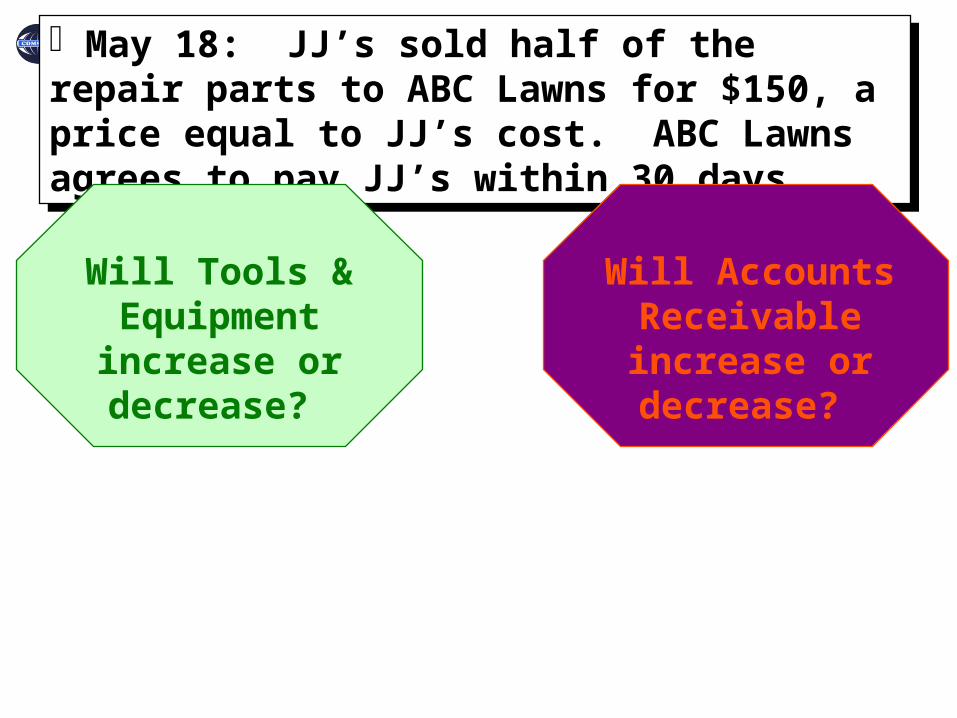

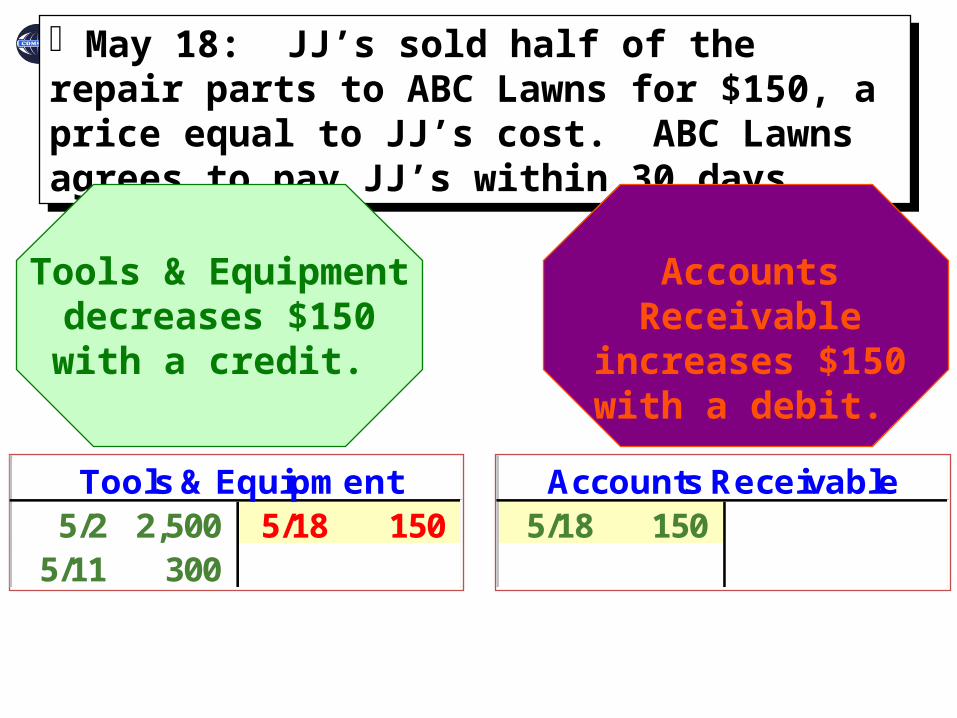

May 18: JJ’s sold half of the repair parts to ABC Lawns for $150, a price equal to JJ’s cost. ABC Lawns agrees to pay JJ’s within 30 days.

May 18: JJ’s sold half of the repair parts to ABC Lawns for $150, a price equal to JJ’s cost. ABC Lawns agrees to pay JJ’s within 30 days.

Will Tools & Equipment increase

or decrease?

Will Accounts Receivable increase

or decrease?

© The McGraw-Hill Companies, Inc., 2002McGraw-Hill/Irwin

May 18: JJ’s sold half of the repair parts to ABC Lawns for $150, a price equal to JJ’s cost. ABC Lawns agrees to pay JJ’s within 30 days.

May 18: JJ’s sold half of the repair parts to ABC Lawns for $150, a price equal to JJ’s cost. ABC Lawns agrees to pay JJ’s within 30 days.

Tools & Equipment decreases $150 with

a credit.

Accounts Receivable increases $150 with

a debit.

Tools & Equipment5/2 2,500 5/18 150

5/11 300

Accounts Receivable5/18 150

© The McGraw-Hill Companies, Inc., 2002McGraw-Hill/Irwin

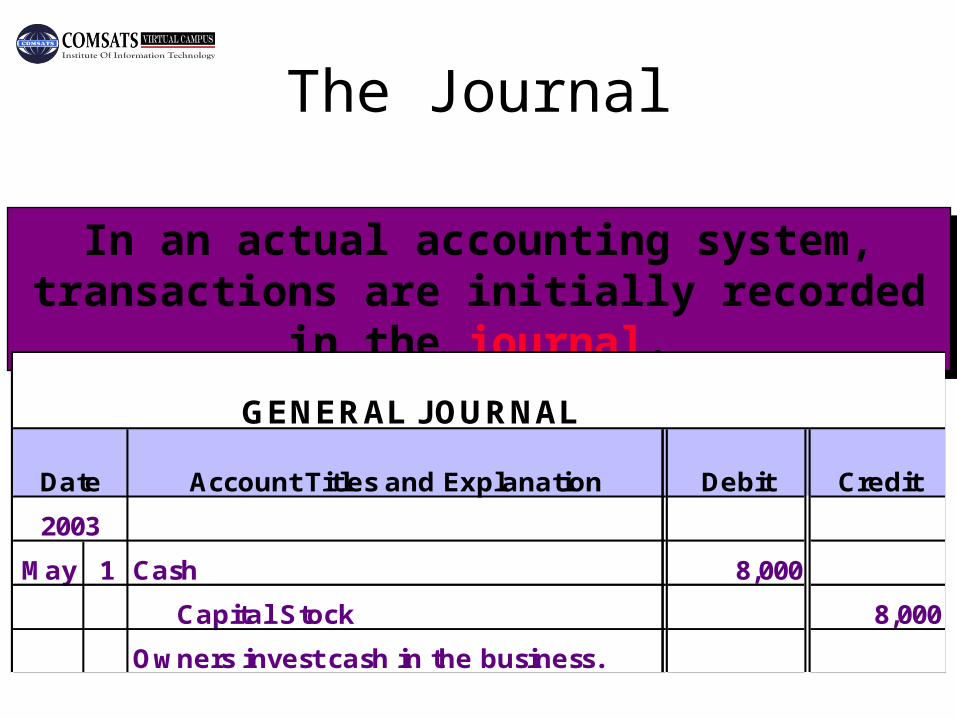

In an actual accounting system, transactions are initially recorded in the journal.

In an actual accounting system, transactions are initially recorded in the journal.

GENERAL JOURNAL

Date Account Titles and ExplanationPR Debit Credit

2003

May 1 Cash 8,000

Capital Stock 8,000

Owners invest cash in the business.

The Journal

© The McGraw-Hill Companies, Inc., 2002McGraw-Hill/Irwin

End of Todays Session

Related Documents