ab Investors’ presentation Zurich 4 November 2005 ab Page 2 Agenda Investors’ presentation 4 November 2005 Topic Presenter Time Welcome and introduction Ann Godbehere 14:00 – 14:02 Introductory video on Asia 14:02 – 14:04 Asia: Achieving scale Pierre Ozendo 14:04 – 14:45 Jean-Michel Chatagny Closing video on Asia 14:45 – 14:47 Q&A Asia Ann Godbehere 14:47 – 15:15 Pierre Ozendo Jean-Michel Chatagny Coffee break 15:15 – 15:30 Catastrophe perils: Under the weather? Brian Gray 15:30 – 15:50 Renewals: Swiss Re demonstrates leadership Stefan Lippe 15:50 – 16:10 Michel Liès Q&A all topics Ann Godbehere 16:10 – 16:45 All

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ab

Investors’ presentation

Zurich

4 November 2005

ab

Page 2

Agenda

Investors’ presentation4 November 2005

Topic Presenter Time

Welcome and introduction Ann Godbehere 14:00 – 14:02

Introductory video on Asia 14:02 – 14:04

Asia: Achieving scale Pierre Ozendo 14:04 – 14:45Jean-Michel Chatagny

Closing video on Asia 14:45 – 14:47

Q&A Asia Ann Godbehere 14:47 – 15:15Pierre OzendoJean-Michel Chatagny

Coffee break 15:15 – 15:30

Catastrophe perils: Under the weather? Brian Gray 15:30 – 15:50

Renewals: Swiss Re demonstrates leadership Stefan Lippe 15:50 – 16:10Michel Liès

Q&A all topics Ann Godbehere 16:10 – 16:45All

ab

Page 3

Cautionary note on forward-looking statements

Certain statements contained herein are forward-looking. These statements provide current expectations of future events based on certain assumptions and include any statement that does not directly relate to a historical fact or current fact. Forward-looking statements typically are identified by words or phrases such as “anticipate”, “assume”, “believe”, “continue”, “estimate”, “expect”, “foresee”, “intend”, “may increase” and “may fluctuate” and similar expressions or by future or conditional verbs such as “will”, “should”, “would” and “could”. These forward-looking statements involve known and unknown risks, uncertainties and other factors, which may cause Swiss Re’s actual results, performance, achievements or prospects to be materially different from any future results, performance, achievements or prospects expressed or implied by such statements. Such factors include, among others:

� cyclicality of the reinsurance industry;� changes in general economic conditions, particularly in our core markets;� uncertainties in estimating reserves;� the performance of financial markets;� expected changes in our investment results as a result of the changed composition of our investment assets or changes in our

investment policy; � the frequency, severity and development of insured claim events;� acts of terrorism and acts of war;� mortality and morbidity experience;� policy renewal and lapse rates;� changes in rating agency policies or practices;� the lowering or withdrawal of one or more of the financial strength or credit ratings of one or more of our subsidiaries;� changes in levels of interest rates;� political risks in the countries in which we operate or in which we insure risks; � extraordinary events affecting our clients, such as bankruptcies and liquidations;� risks associated with implementing our business strategies;� changes in currency exchange rates;� changes in laws and regulations, including changes in accounting standards and taxation requirements; and� changes in competitive pressures.

These factors are not exhaustive. We operate in a continually changing environment and new risks emerge continually. Readers are cautioned not to place undue reliance on our forward-looking statements. We undertake no obligation to publicly revise or update any forward-looking statements, whether as a result of new information, future events or otherwise.

Investors’ presentation4 November 2005

ab

Asia: Achieving scale

Pierre OzendoMember of the Executive BoardHead of Asia Division

Jean-Michel ChatagnyHead Life & Health, Asia Division

ab

Page 5

Agenda

Investors’ presentation4 November 2005

Asia: Swiss Re’s strategic priority

Why Asia?

Swiss Re is best positioned to further expand its Asian leadership

How Swiss Re will leverage its strengths in China & India

What this means for the future

ab

Page 6

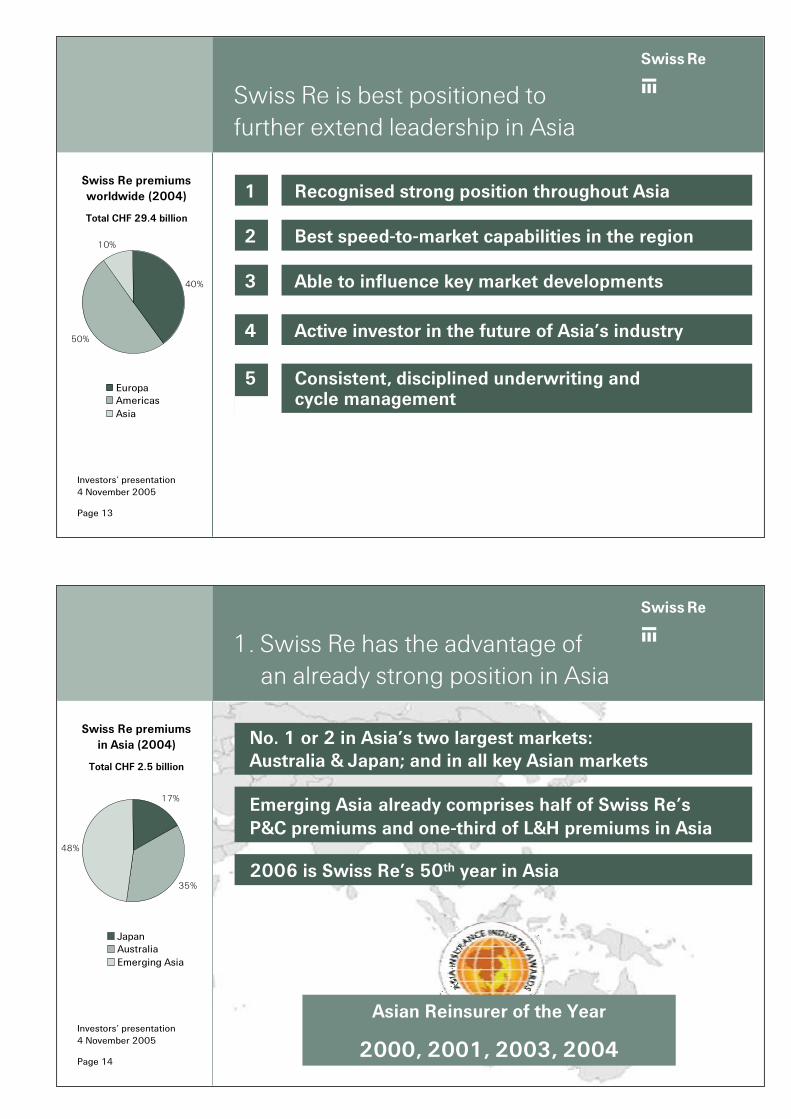

Client Markets

Actively manage the cycle for

profits

Swiss Re’s strategic priorities and organisational structure

Optimise organic and transactional

growth

Extend leadership in Asia

Accelerate the balance sheet

Financial ServicesProducts

ab

Page 7

Agenda

Investors’ presentation4 November 2005

Asia: Swiss Re’s strategic priority

Why Asia?

Swiss Re is best positioned to further expand its Asian leadership

How Swiss Re will leverage its strengths in China & India

What this means for the future

ab

Page 8

69%58%

50%

76%

10%21%

19%

8%6% 14%23%

14%7% 9% 12%

4%

0%

20%

40%

60%

80%

100%

Population GDP Non-lifepremiums

Life premiums

Asia Latin America Eastern Europe Africa

The Asian market opportunity

Asia accounts for 69% of emerging world’s population, 76% of life premiums and 50% of non-life premiums of emerging markets

Sources: Oxford Economic Forecasting; Swiss Re Economic Research & Consulting Emerging Asia includes Middle East. Figures refer to 2004

165.7

17.78.4

25.6USD bn

60.4

23.5

27.6

10.5

Investors’ presentation4 November 2005

Non-life premiums

USD bn

ab

Page 9

100

150

200

250

300

350

400

450

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

Industrialised countries Emerging markets Emerging Asia

Asian economies will see strong sustained growth

Real GDP, index 1990=100 CAGR 2006-15

2.5%

4.9%

5.7%

Note: Emerging Asia excludes Japan and Australia, which are included in Industrialised countriesSources: Oxford Economic Forecasting; Swiss Re Economic Research & Consulting

Investors’ presentation4 November 2005

ab

Page 10

Asia will experience increasing insurance demand…

Economic growth(4% above industrialised economies 1990-2005)

Demographics(60% of world population)

Increased stability(attracting 23% of world

Foreign Direct Investment)

Globalisation(21% of world trade)

0

50

100

150

200

250

300

350

400

450

500

1990 1995 2000 2005World (P&C) Emerging Asia P&CWorld (L&H) Emerging Asia L&H

Real premium index (1990=100)

Sources: Oxford Economic Forecasting; Swiss Re Economic Research & Consulting

ab

Page 11

… thus creating new opportunities for Swiss Re in Asia

� Rising household wealth

� Greater need for protection

� Alternative distribution channels

� Health & pensions reform

� Capital pressure from newbusiness growth

� Increasing trade and investment

� Casualty/liability demand

� Underinsured small and medium sized enterprises

� Heightened nat cat awareness

� e-business opportunities

Property &Casualty

Life & Health

� Skills shortage

� Trainingrequirements

� Market fragmentation

� Regulatoryconvergence

Opp

ortu

niti

es

Cha

lleng

es

ab

Page 12

Agenda

Investors’ presentation4 November 2005

Asia: Swiss Re’s strategic priority

Why Asia?

Swiss Re is best positioned to further expand its Asian leadership

How Swiss Re will leverage its strengths in China & India

What this means for the future

ab

Page 13

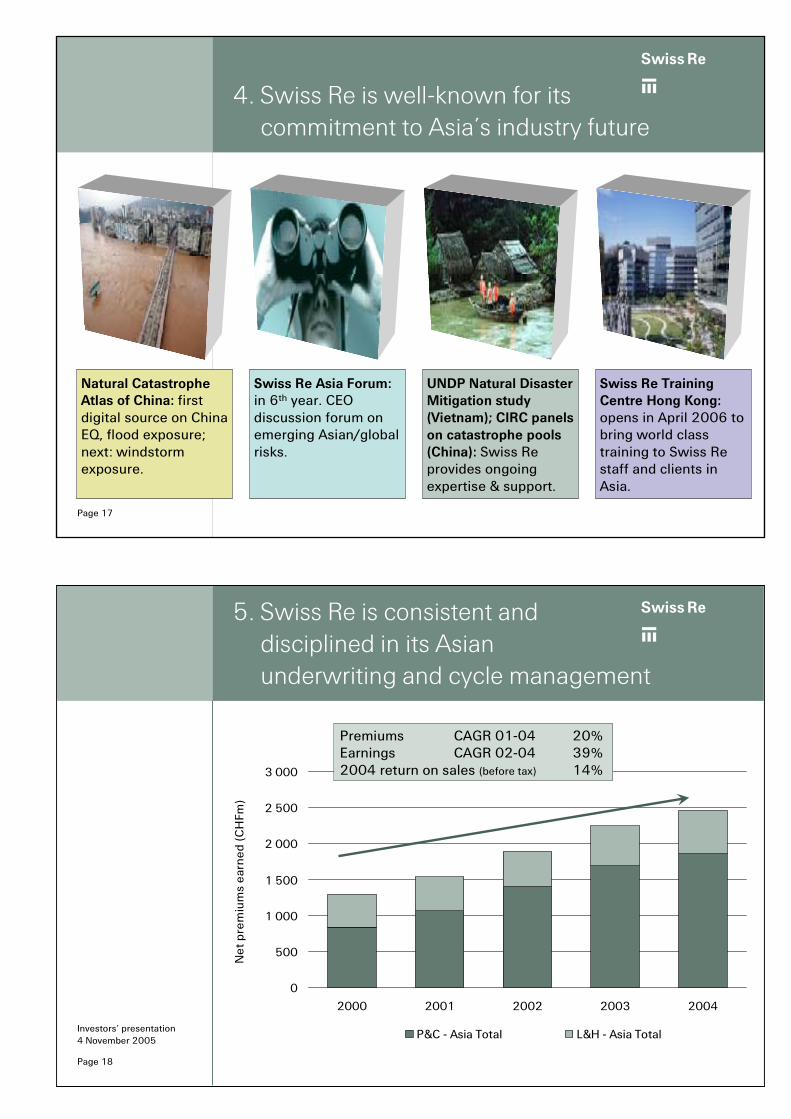

Swiss Re is best positioned to further extend leadership in Asia

Swiss Re premiumsworldwide (2004)

Total CHF 29.4 billion

40%

50%

10%

EuropaAmericasAsia

Investors’ presentation4 November 2005

1 Recognised strong position throughout Asia

5 Consistent, disciplined underwriting andcycle management

4 Active investor in the future of Asia’s industry

2 Best speed-to-market capabilities in the region

3 Able to influence key market developments

ab

Page 14

1. Swiss Re has the advantage of an already strong position in Asia

Investors’ presentation4 November 2005

No. 1 or 2 in Asia’s two largest markets:Australia & Japan; and in all key Asian markets

2006 is Swiss Re’s 50th year in Asia

Emerging Asia already comprises half of Swiss Re’sP&C premiums and one-third of L&H premiums in Asia

Asian Reinsurer of the Year

2000, 2001, 2003, 2004

Swiss Re premiumsin Asia (2004)

Total CHF 2.5 billion

17%

35%

48%

JapanAustraliaEmerging Asia

ab

Page 15 (1) Bangalore includes staff for other SR units (2) Excludes FPK

Full time employees: Asia Division (2) : 623

2. Swiss Re has the best speed-to-market capabilities in Asia

Full time employees: SSC Bangalore(1): 211

(Services P&C, L&H Asia, Europe and US)

Branches 8Offices 13

Singapore 79

Hong Kong (HQ) 155

Sydney 150

Tokyo 58

Zurich 54

Seoul 21

Mumbai 23Taipei 23

Beijing 30

Shanghai 5

Bangalore 211Manila 3

Kuala Lumpur 15

Shared Service Centre

Branch, Hub

Representative office or service company

As at end Sept 2005

Investors’ presentation4 November 2005

Product HubCasualty/ Property & Special Lines/Life & Health

ab

Page 16

3. Swiss Re is uniquely able to influence Asian market developments

Product development

� Leading influence among reinsurers in Asia on:– Critical illness– Catastrophe pools– Liability products

� First foreign shareholder in a Chinese insurance asset management company:

– China Re Asset Management Ltd

� Only global reinsurer with dedicated professionals in Asia focused on regulatory affairs and economic research:– Strong regulatory relations in key markets

Capital management

Regulatorydevelopments

ab

Page 17

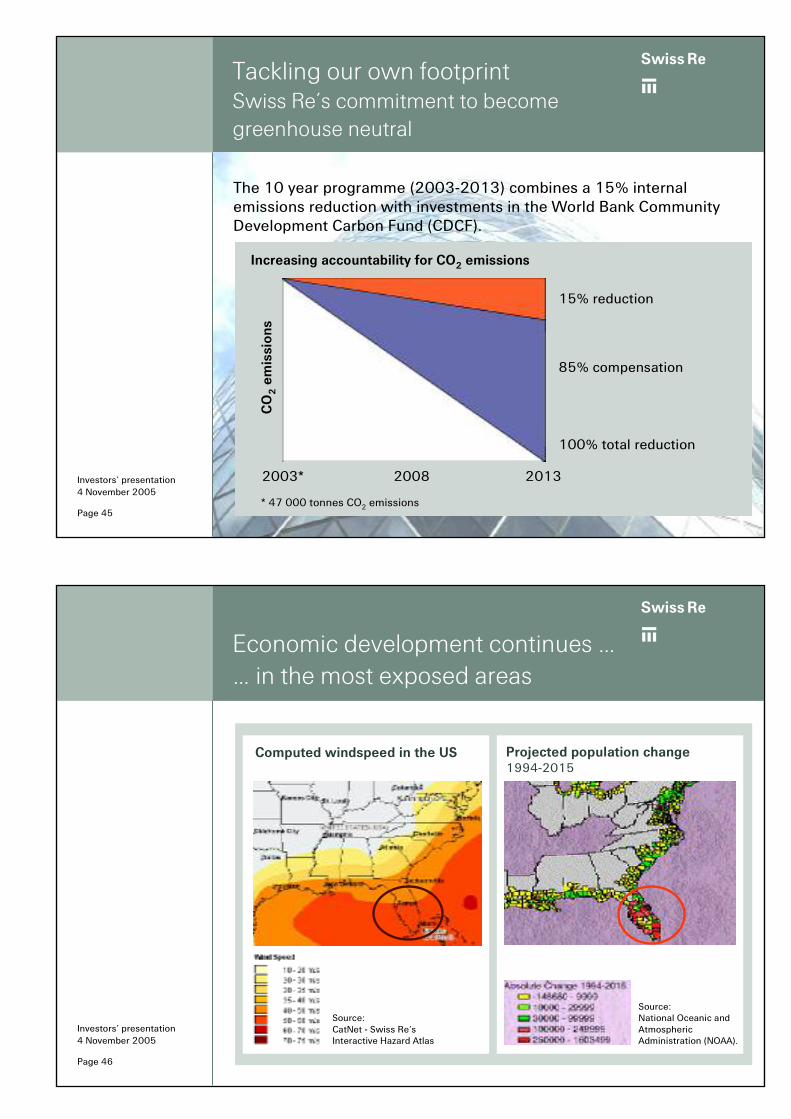

4. Swiss Re is well-known for its commitment to Asia’s industry future

Swiss Re Asia Forum: in 6th year. CEO discussion forum on emerging Asian/global risks.

Swiss Re Training Centre Hong Kong: opens in April 2006 to bring world class training to Swiss Re staff and clients in Asia.

Natural Catastrophe Atlas of China: first digital source on China EQ, flood exposure; next: windstorm exposure.

UNDP Natural Disaster Mitigation study (Vietnam); CIRC panels on catastrophe pools (China): Swiss Re provides ongoing expertise & support.

ab

Page 18

5. Swiss Re is consistent and disciplined in its Asian underwriting and cycle management

0

500

1 000

1 500

2 000

2 500

3 000

2000 2001 2002 2003 2004

Net

prem

ium

sea

rned

(CH

Fm)

P&C - Asia Total L&H - Asia Total

Premiums CAGR 01-04 20% Earnings CAGR 02-04 39%2004 return on sales (before tax) 14%

Premiums CAGR 01-04 20% Earnings CAGR 02-04 39%2004 return on sales (before tax) 14%

Investors’ presentation4 November 2005

ab

Page 19

Agenda

Investors’ presentation4 November 2005

Asia: Swiss Re’s strategic priority

Why Asia?

Swiss Re is best positioned to further expand its Asian leadership

How Swiss Re will leverage its strengths in China & India

What this means for the future

ab

Page 20

Emerging markets growing rapidly

Investors’ presentation4 November 2005

The white circles shows the size of GDP and per capita income of China and India in 2004Sources: Oxford Economic Forecasting; Swiss Re Economic Research & Consulting

U.A.E.

Saudi Arabia

Philippines

Turkey

Vietnam

India

ChinaMalaysia

Thailand

EgyptIndonesia

USD 1 000 billion in GDP

by 2015

US

UKJapan

Switzerland

Australia

Hong Kong

Singapore

South Korea

Taiwan

-10 000

10 000

30 000

50 000

70 000

90 000

0% 1% 2% 3% 4% 5% 6% 7% 8%

Average real GDP growth, 2006-2015

Per

capi

taG

DP

,20

15

(US

D)

Germany

UK

ab

Page 21

� Step change in demand function. When GDP per capita gets closeto USD 10 000, insurance penetration rises to a level above 4% with a steep slope

� Compulsory insurance andexposure to natural catastrophes support non-life insurancedemand

Attractive growth opportunities in emerging markets

Growth of free ceded premiums in China & India in real terms to 2015:

� P&C: 11% p.a.

� L&H: 29% p.a.

Source: Swiss Re Economic Research & Consulting

Premiums per GDP, life and non-life, 2004

UnitedStates

Germany

ChinaIndia

SpainMalaysia

GDP per capita, 1 000 USD, 2004

Czech RepublicThailand

Indonesia

SouthKorea

Vietnam

0%

2%

4%

6%

8%

10%

12%

0.1 1 10 100

ab

Page 22

Swiss Re’s China strategy

Investors’ presentation4 November 2005

ab

Page 23

China market drivers offer opportunities for Swiss Re

Market drivers

Industry momentum

� Natural catastrophe coverage including pools� Growth of environmental concerns� Policy-driven growth in liability and motor business� Further market reforms and corporate governance� Capital market development and expansion� The consequences of de-socialisation, such as pension reform,

health insurance, agriculture insurance and the role of private suppliers

� Life insurance products heavily oriented towards savings

P&C L&H

Direct premiums 2004 in CHF billions 22.1 46.7

Average annual real growth 1990-2004 in % 13.6 25.1

ab

Page 24

Recent Swiss Re initiatives in China put us in the lead

China ReAsset Management

Natural catastrophepools

China SustainabilitySummit (Sept 05)

Liability conferences:“Risks and opportunities”

ab

Page 25

Market liberalisation

De-socialisation

Risk awareness

Wealth accumulation

Swiss Re’s initiatives will capture new opportunities in China

Start-upsPartnership with

quota shares/ motor

e-BusinessAgriculture/

large projects

MortalityAlternative distribution

Personal accident, health & living benefits

Liability

ab

Page 26

Swiss Re’s India strategy

Investors’ presentation4 November 2005

© Magnum

ab

Page 27

India: key market drivers that impact Swiss Re’s strategy

Market drivers

Industry momentum

P&C L&H

Direct premiums 2004 in CHF billions 5.6 22.7Average annual real growth 1990-2004 in % 7.1 12.7

� Regulatory requirements moving towards liberalisation

� National insurers dominate with 80% market share

� New entrants/JV companies expanding rapidly

� Discontinuation of P&C tariff by end of 2006

� Natural catastrophe covers and pools

� Cap on foreign ownership in insurance of 26%

ab

Page 28

Recent Swiss Re initiatives in India create a strong foundation

Natural catastrophe pool and agricultural weather

covers

Corporate Social Responsibility: AIDS education, water& tsunami projects, biogas generators, micro-insurance

India CEO Summit

Investment and commitment via Shared Service Centre in Bangalore

ab

Page 29

Market liberalisation

De-socialisation

Risk awareness

Wealth accumulation

Swiss Re has a portfolio of initiatives to capture new opportunities in India

Alternative distribution

Living benefits Microfinance

Share of Wallet (existing clients)

Engineering/construction

Agriculture/rural coverages

ab

Page 30

Agenda

Investors’ presentation4 November 2005

Asia: Swiss Re’s strategic priority

Why Asia?

Swiss Re is best positioned to further expand its Asian leadership

How Swiss Re will leverage its strengths in China & India

What this means for the future

ab

Page 31

Asia will become a major contributor to Swiss Re‘s revenues

Investors’ presentation4 November 2005

34%

9%

57%

15%

44%41%P&C premiums

Japan, Australia & New Zealand

47%

Rest of Asia35%

China18%

60%

8%

32%

L&H premiums

Source: Swiss Re Economic Research & Consulting

2015

Primary market premium projections to 2015

USD 321bnUSD 161bn

USD 1 017bnUSD 477bn

2005E

ab

Page 32

6.0 6.7 6.911.0

10.3 11.6 13.1

33.2

0

10

20

30

40

50

2002 2003 2004 2015

Japan & Australia/New Zealand Emerging Asia

Swiss Re is in the best position to capitalise on Asia’s strong growth potential for reinsurance business

Source: Swiss Re Economic Research & Consulting. Compound growth rates are in nominal terms.

Reinsurance market premiums (USD billions)

CAGR 8.8%

CAGR 4.3%

Investors’ presentation4 November 2005

Swiss Re premiums in Asia : Property & Casualty 11%(CAGR 05-10E) Life & Health 19%

Combined 13%

Swiss Re premiums in Asia : Property & Casualty 11%(CAGR 05-10E) Life & Health 19%

Combined 13%

ab

Page 33

Asia: Achieving scale – Q&A

Investors’ presentation4 November 2005

ab

Catastrophe perils: Under the weather?

Brian GrayHead of Property & Specialty

ab

Page 35

Agenda

Investors’ presentation4 November 2005

Historic profitability

Climate variability

A growth business

Swiss Re’s strong position

ab

Page 36

2005 weather claimsEstimated Swiss Re claims above CHF 20 million

� Katrina, Rita, Wilma USD 1 950 million

� Other weather events CHF 450 million(California winter-storms & flood,winter-storm Erwin, Hurricane Dennis,European floods, Mumbai floods)

Investors’ presentation4 November 2005

ab

Page 37

0

2

4

6

8

10

12

14

16

18

20

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Realised premiums Expected claims Incurred claims

CHF bn

CAMARES markets (15 markets) Premium is shown after deducting external costs

uncertain

� Worldwide, the cat XL market has generated a positive return over the past 12 years, including Katrina - the largest insured loss in history

Source: Cat Perils, Camares

CHF bn

0

10

20

30

40

50

60

70

1994-2005Total 1994 – 2005

Historic worldwide cat XL profitabilityEstimated premium and claim history 1994 - 2005

Investors’ presentation4 November 2005

ab

Page 38

Market prices increase sharply after events: Typhoon Japan

-21% -22%

-10%

7%11%

-9%

17%

24%

37%

1996 1997 1998 1999 2000 2001 2002 2003 2004 20050

20

40

60

80

100

120

140

relative change of price level price index (1996=100)

� Natural catastrophe claims have driven up prices the following year, irrespective of underlying market trends

Typhoon Bart Sept ‘99

Typhoon Songda Sept ‘04

Investors’ presentation4 November 2005

ab

Page 39

Market prices increase sharply after events: Windstorm France

-17% -20%

5%

17%

-3% -2%

-15%

99%

-6%

1996 1997 1998 1999 2000 2001 2002 2003 2004 20050

20

40

60

80

100

120

140

160

relative change of price level price index (1996=100)

Storms Lothar & Martin

� Lothar and Martin occurred in the final week of December 1999, too late to affect 2000 renewal prices, but driving up 2001 prices substantially

Investors’ presentation4 November 2005

ab

Page 40

Climate variabilityCyclical change of ocean temperatures

Source: S. Goldenberg, W. GrayArea: 10° to 14°N, 20° to 70°WTemporal reconstruction of the sea surface temperature deviation from its mean, averaged over the rectangular area

Sea surface temperatures in the North Atlantic

Investors’ presentation4 November 2005

ab

Page 41

Climate variabilityAbove-normal hurricane activity in last decade

Investors’ presentation4 November 2005

ab

Page 42

Climate variabilityMore hurricanes striking U.S. mainland

0

1

2

3

4

5

6

7

1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000

Hurricanes making multiple landfalls during their lifecycle only counted once

1943 – 69 average: 2.01970 – 94 average: 1.21995 – 05 average: 2.2

Number of hurricanes making U.S. landfall (per year, 1900-2005)

Investors’ presentation4 November 2005

ab

Page 43

North Atlantic hurricaneModel changes

� Swiss Re’s model (and others) have modelled storm frequency and intensity based on long-term averages

� There is growing scientific evidence that activity in the North Atlantic varies between ‘more active’ and ‘less active’ periods, and that since the late 1990s we have been in a ‘more active’ period

� Swiss Re adjusted the storm frequency in its models in September 2005, and is already using this in the market

� Swiss Re has additionally implemented a newly-developed rating tool for US flood and storm surge

Investors’ presentation4 November 2005

ab

Page 44

Risk dialogue and awarenessSwiss Re plays a leading role

� Global warming: element of risk(1994)

� Coping with the risks of climatechange (1998)

� Opportunities and risks of climate change (2002)

� Wind/flood Japan – in search of sustainability (2003)

� Tackling climate change (2004)

� Long-established and proven expertise

� Extensive research and focused innovation

� Risk dialogue with internationally recognized partnersInvestors’ presentation4 November 2005

ab

Page 45

Tackling our own footprintSwiss Re’s commitment to become greenhouse neutral

The 10 year programme (2003-2013) combines a 15% internal emissions reduction with investments in the World Bank CommunityDevelopment Carbon Fund (CDCF).

Increasing accountability for CO2 emissionsC

O2

emis

sion

s

2003* 2008 2013

* 47 000 tonnes CO2 emissions

15% reduction

85% compensation

100% total reduction

Investors’ presentation4 November 2005

ab

Page 46

Economic development continues …… in the most exposed areas

Source: CatNet - Swiss Re’s Interactive Hazard Atlas

Projected population change1994-2015

Source:National Oceanic andAtmospheric Administration (NOAA).

Investors’ presentation4 November 2005

Computed windspeed in the US

ab

Page 47

The traditional catastrophe market is a strongly growing business segment

0

20

40

60

80

100

120

140

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Total reinsurance cover purchased in 15 prime markets (in CHFbn, at today’s exchange rates)

CAGR over the past 11 years

is 9.4%

Source: CAMARES (Swiss Re’s cat market research study)

Investors’ presentation4 November 2005

ab

Page 48

Summary

� The nat cat market has been historically profitable

� Prices will rise sharply in the near-term

� Climate variability and change create challenges but also opportunities

� The underlying risk characteristics of natural catastrophe are attractive

– diversifiable

– fortuitous

– tremendous transparency of result

� Natural and human factors make the catastrophe market a growth business

� Swiss Re is well positioned to benefit from market changesInvestors’ presentation4 November 2005

abRenewals: Swiss Re demonstrates leadership

Stefan Lippe, Head of Products

Michel Liès, Head of Client Markets

ab

Page 50

Agenda

Investors’ presentation4 November 2005

Changing risk landscape offers opportunities to Swiss Re

Where do we stand in the cycle?

Cycle management

Swiss Re is excellently positioned for 2006 renewals

ab

Page 51

The risk landscape is changing -opportunities for strong players

4 major hurricanes in 2004

5 major hurricanes in 2005,including highest ever insured loss

Major typhoons in 2004

Tsunami in 2004

2 major storms and floodsin Europe in 2005

Pharma claims

Financial Institutions

D&O

Liability regime

Investors’ presentation4 November 2005

ab

Page 52

Where do we stand in the cycle?Qualitative assessment by line of business mid 2005

Outlook 2006

Pricing levels peaked in 2003/4, the impact of Katrina will drive prices higher across all lines of business, not just nat cat

CM

PProperty

Casualty

Marine / Offshore

M

PC

Mid 2005

Investors’ presentation4 November 2005

ab

Page 53

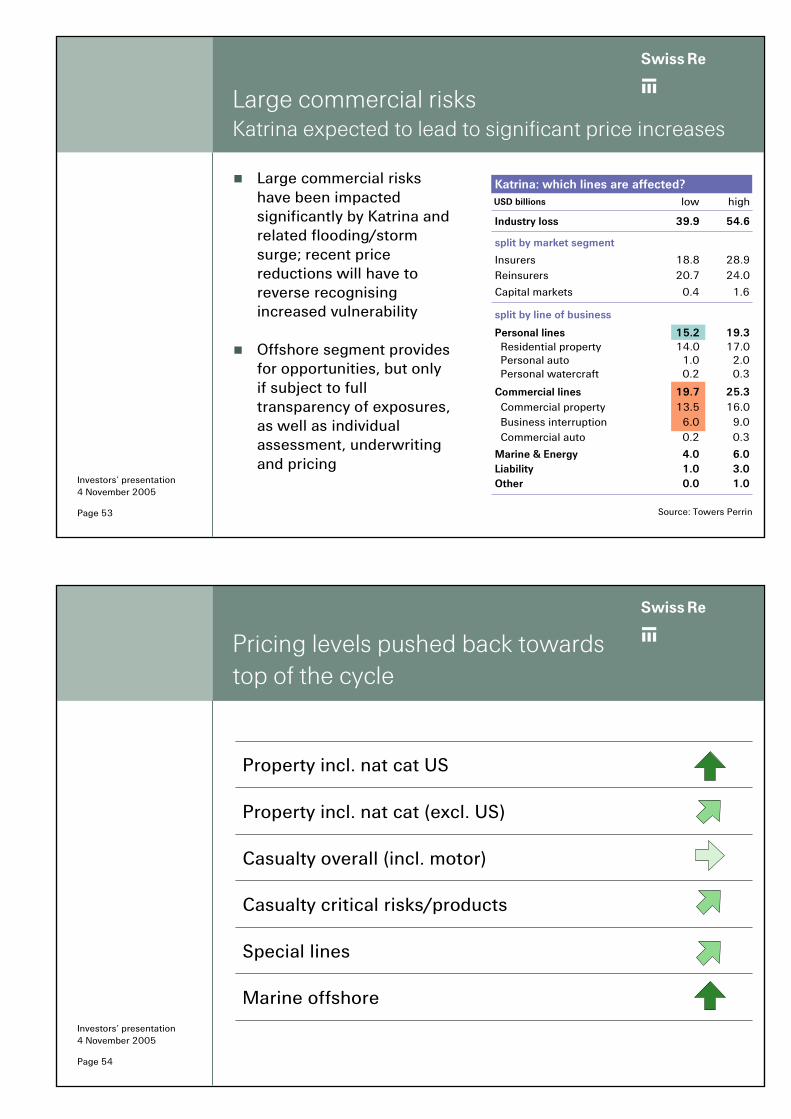

Large commercial risksKatrina expected to lead to significant price increases

� Large commercial risks have been impacted significantly by Katrina and related flooding/storm surge; recent price reductions will have to reverse recognising increased vulnerability

� Offshore segment provides for opportunities, but only if subject to full transparency of exposures, as well as individual assessment, underwriting and pricing

Source: Towers Perrin

Investors’ presentation4 November 2005

Katrina: which lines are affected?low high

Industry loss 39.9 54.6

split by market segment

Insurers 18.8 28.9Reinsurers 20.7 24.0

Capital markets 0.4 1.6

split by line of business

Personal lines 15.2 19.3Residential property 14.0 17.0Personal auto 1.0 2.0Personal watercraft 0.2 0.3

Commercial lines 19.7 25.3Commercial property 13.5 16.0Business interruption 6.0 9.0Commercial auto 0.2 0.3

Marine & Energy 4.0 6.0Liability 1.0 3.0Other 0.0 1.0

USD billions

ab

Page 54

Pricing levels pushed back towards top of the cycle

Property incl. nat cat US

Investors’ presentation4 November 2005

Property incl. nat cat (excl. US)

Casualty overall (incl. motor)

Special lines

Marine offshore

Casualty critical risks/products

ab

Page 55

Conclusions for 2006 renewals

� Changes to Swiss Re’s hurricane model to reflect flood and storm surge are implemented and in the market

� Swiss Re will write pharma business selectively and on facultative basis with specific endorsements securing aligned interests between insured and (re)insurer

� Swiss Re will introduce a specific tightening of contract language to significantly reduce the entrepreneurial risk in large D&O accounts

Investors’ presentation4 November 2005

� Swiss Re is demonstrating leadership in the market

ab

Page 56

Cycle managementComprehensive toolbox for real time steering

Weekly renewal monitoring provides management with real timeinformation on trends and allows for active steering

Rate levels

Business volume

Qualitative trends

Market developments

offered and realised rates compared to target

written premiums, number of accounts

wordings, exclusions, special clauses

cedant retention levels, competitor behaviour Investors’ presentation4 November 2005

ab

Page 57

Cycle managementMonitoring rate adequacy

Renewal Tracking Tool provides real time information on quotesand pricing levelsworldwide and thus enables management to actively steer the business

Investors’ presentation4 November 2005

ab

Page 58

Cycle managementMonitoring qualitative trends

Traffic light approach to monitor current situation and trend for both rate adequacy and coverage terms (wordings)

� Significantly better terms

� Significantly worse terms� Stable terms

� Weakening terms� Improving terms

Above Renewal TargetBetween Cycle Reference and Renewal TargetBetween Production Cost and Cycle ReferenceBelow Production Cost

Mar

ket

Un

it1

Mar

ket

Un

it2

Mar

ket

Un

it3

Mar

ket

Un

it4

Mar

ket

Un

it5

Mar

ket

Un

it6

Mar

ket

Un

it7

Mar

ket

Un

it8

Property Proportional � � � � � � � �Proprty non-proportional � � � � � � � �General Liability proportional � � � � � � � �General Liability non-proportional � � � � � � � �Professional Liability proportional � � � � �Professional Liability non-proportional � � � � � �Motor proportional � � � � � � �Motor non-proportional � � � � � � � �Marine proportional � � � � � �Marine non-proportional � � � � � � �Engineering proportional � � � � � � � �Engineering non-proportional � � � � � � � �Aviation proportional

Aviation non-proportional

Special Lines proportional

Special Lines non proportional

Illustration of a traffic light overview

Investors’ presentation4 November 2005

ab

Page 59

Swiss Re is excellently positioned for the 2006 renewals

� Business conditions have been favourable for the last 4 years, outlook is positive for all lines of business

� Retrocession prices are soaring (up to 3 times higher)� net writers are in the driving seat

� Swiss Re as a net writer can maximise the advantages of the current market conditions

� Swiss Re is financially very strong and does not need to raise new capital

� Changes to Swiss Re’s hurricane model to reflect flood and storm surge are implemented and in the market

Investors’ presentation4 November 2005 � Swiss Re is able and ready to deploy its full capacity at excellent

terms and conditions

ab

Appendix

ab

Page 61

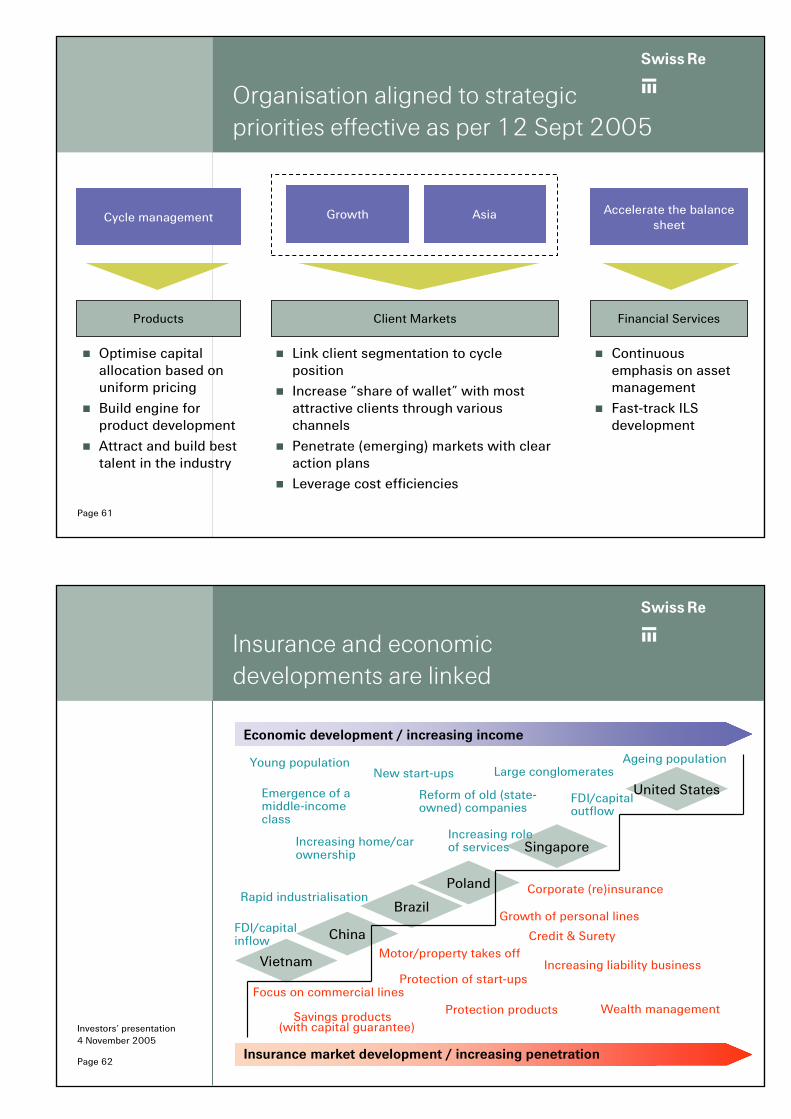

Organisation aligned to strategic priorities effective as per 12 Sept 2005

� Optimise capital allocation based on uniform pricing

� Build engine for product development

� Attract and build best talent in the industry

Cycle management

Products

� Continuous emphasis on asset management

� Fast-track ILS development

Accelerate the balance sheet

Financial Services

� Link client segmentation to cycle position

� Increase “share of wallet” with most attractive clients through various channels

� Penetrate (emerging) markets with clear action plans

� Leverage cost efficiencies

AsiaGrowth

Client Markets

ab

Page 62

Insurance and economic developments are linked

United States

Singapore

Reform of old (state-owned) companies

Increasing role of services

FDI/capital outflow

Large conglomerates

Motor/property takes off

Protection of start-ups

Growth of personal lines

Increasing liability business

Corporate (re)insurance

Ageing population

Credit & Surety

Protection products Wealth management

Brazil

Poland

Investors’ presentation4 November 2005

Savings products

China

Vietnam

Increasing home/car ownership

Emergence of a middle-income class

New start-ups

Rapid industrialisation

FDI/capital inflow

Focus on commercial lines

Young population

(with capital guarantee)

Economic development / increasing income

Insurance market development / increasing penetration

ab

Page 63

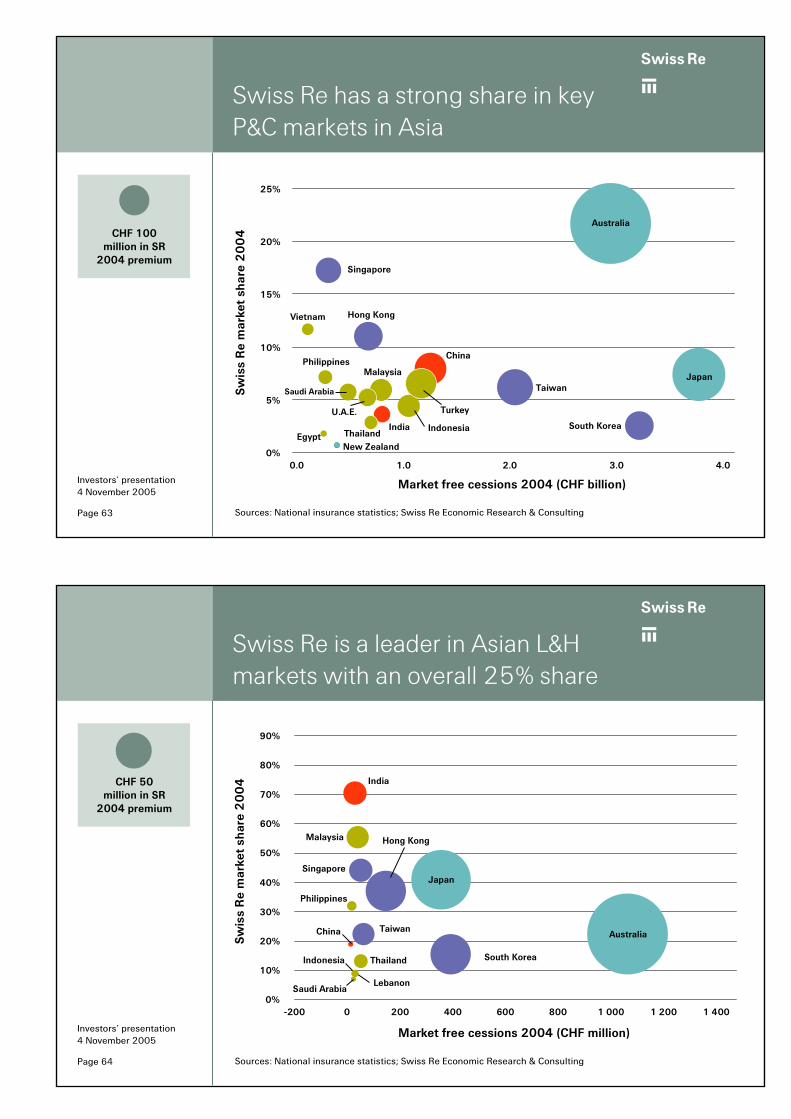

Swiss Re has a strong share in key P&C markets in Asia

Investors’ presentation4 November 2005

Sources: National insurance statistics; Swiss Re Economic Research & Consulting

China

Thailand

Malaysia

IndonesiaIndia

Vietnam

Philippines

TurkeyU.A.E.

Saudi Arabia

Egypt

Hong Kong

Singapore

South Korea

Taiwan

New Zealand0%

5%

10%

15%

20%

25%

0.0 1.0 2.0 3.0 4.0

Market free cessions 2004 (CHF billion)

Sw

iss

Re

mar

ket

shar

e2

00

4Australia

Japan

CHF 100 million in SR

2004 premium

ab

Page 64

Swiss Re is a leader in Asian L&H markets with an overall 25% share

Investors’ presentation4 November 2005

China

Thailand

Malaysia

Indonesia

India

Philippines

Saudi ArabiaLebanon

South Korea

Singapore

Hong Kong

Taiwan

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

-200 0 200 400 600 800 1 000 1 200 1 400

Sources: National insurance statistics; Swiss Re Economic Research & Consulting

Sw

iss

Re

mar

ket

shar

e2

00

4

Market free cessions 2004 (CHF million)

Australia

Japan

CHF 50million in SR

2004 premium

ab

Page 65

CAMARESPre-Katrina nat cat prices were declining, but still above cycle reference

� While prices remained under pressure in a competitive cat XL market environment,the 2004 hurricanes in the US and typhoons in Japan had a clear impact on prices in affected regions

� Swiss Re further strengthened its market position while maintaining price adequacy above market average as well as above cycle reference

Source: CAMARES (Swiss Re’s cat market research study analysing profitability of cat programmes in 13 largest markets)

-12%

0%

25%

-8%-7%

26%

-15%

11%

-6%

1996 1997 1998 1999 2000 2001 2002 2003 2004 20050

20

40

60

80

100

120

140

relative change (market) market index

Investors’ presentation4 November 2005

Annual premium level change in %

ab

Page 66

US flood & storm surge modelRolled out in September 2005

Investors’ presentation4 November 2005

ab

Page 67

Historic nat cat events

Earlier famous events

Ins. loss est. Date Event CountryUSD billions*

1. 70-80 1923 Tokyo Earthquake Japan2. 45-60 1906 San Francisco Earthquake US3. 40-50 1926 Florida Hurricane US

* Market loss estimate for the same event today

Ins. loss Date Event CountryUSD billions*

1. 21.5 08/92 Hurricane Andrew US2. 17.8 01/94 Earthquake Northridge US3. 11.0 09/04 Hurricane Ivan Caribbean/US4. 8.0 08/04 Hurricane Charley Caribbean/US5. 7.8 09/91 Typhoon Mireille Japan

* Loss data indexed to 2004 Source: Swiss Re sigma

Top 5 nat cat insurance losses 1990 - 2004

Investors’ presentation4 November 2005

Related Documents