Corporate Vision Dedicated to serve the needs of the farming community, by delivering financial products and technical services on a competitive and sustainable basis, in a convenient , efficient and professional manner, leading to success of the Bank and the farmers. Back to Top Corporate Mission To play effective role in the promotion of economic growth, by enhancing the availability of credit to the agriculture sector, through reliable access to sustainable financing, special lending programs, technical assistance, and other products & services, and to promote career development opportunities for increasing professionalism and technical proficiencies of employees. Back to Top Brief on ZTBL Zarai Taraqiati Bank Limited (ZTBL) erstwhile Agricultural Development Bank of Pakistan (ADBP) is the premier financial institution geared towards the development of agriculture sector through provision of financial services and technical know how. The restructuring of former ADBP is being carried out with the aim to uplift the agriculture and rural sector by raising farm productivity, streamlining the institutional credit and increasing income generating

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Corporate Vision

Dedicated to serve the needs of the farming community, by delivering financial products and technical services on a competitive and sustainable basis, in a convenient , efficient and professional manner, leading to success of the Bank and the farmers.

Back to Top

Corporate Mission

To play effective role in the promotion of economic growth, by enhancing the availability of credit to the agriculture sector, through reliable access to sustainable financing, special lending programs, technical assistance, and other products & services, and to promote career development opportunities for increasing professionalism and technical proficiencies of employees.

Back to Top

Brief on ZTBL

Zarai Taraqiati Bank Limited (ZTBL) erstwhile Agricultural Development Bank of Pakistan (ADBP) is the premier financial institution geared towards the development of agriculture sector through provision of financial services and technical know how. The restructuring of former ADBP is being carried out with the aim to uplift the agriculture and rural sector by raising farm productivity, streamlining the institutional credit and increasing income generating capacity of the farming community. ZTBL was incorporated as a Public Limited Company on 14th December, 2002 through repeal of ADB Ordinance of 1961.

The new corporate structure redefines the bank's status as a public limited company registered under companies Ordinance'1984 with an independent Board of Directors which aims at ensuring good governance, autonomy, delivering high quality

ZTBL is a key R.F.I of Pakistan providing affordable, rural and agriculture financial/non-financial services to the rural Pakistan , comprising 68 % of the total population. The Bank through a country-wide network of 341 branches is serving around half a million clients annually and over one million accumulated account holders with the average loan size of around Rs.89,000 serving 65%, 31% & 4 %

of subsistence, economic and large growers respectively.

The total assets of the Bank stand at Rs.84 billion with authorized capital of Rs.25 billion as of 31.12.2005, with a nation-wide working strength comprises 5500 employees. The share of ZTBL in total national institutional agricultural credit remains around 35%.

ZTBL was incorporated as a Public Limited Company on 14th December, 2002 through repeal of formal Agricultural Development Bank of Pakistan Ordinance of 1961. Thereby transforming the bank as a corporate entity to serve as a R. F.I

Back to Top

Corporate Objectives

Develop and operate as a financially and operationally sustainable R.F.I of the country. Assist rural community, particularly the small farmers, in raising their productivity and income levels through timely delivery of credit, advisory and ancillary services.

Build ZTBL's image as a proactive, client friendly, financially & operationally sustainable with indigenous product deployment. Establish and provide backward and forward linkages to strengthen agri. value added commodity chains. Engage in public - private and wholesale - retail partnership to deepen outreach and reduce operating cost. To function as a rural commercial bank to mobilize rural capital formation and to commercialize the agri. sector by delivering the true value of credit to the client. Provide a wide range of risk insurance products to its clients. Open up it venues of operation to Domestic & International Banking Industry to avail comparative advantages.

Back to Top

Transformation of ZTBL to R.F.I of the country and road to excellence.

Healthy and well-functioning rural finance markets are directly related to achieving the two key national policy objectives of accelerating rural/agriculture growth and reducing poverty. The realization of these objectives depends on the

simultaneity of developments in rural finance and non-financial markets to foster the creation of diverse sources of rural finance to build sustainable financial institutions, and stimulate products and capital flows in the rural sector. For this, rural finance must be seen as an integral part of equitable development within a framework of macro economic stability. The ongoing corporatize restructuring lays the basis for fundamental reforms for rural finance market development.

The recurring financial drain, pursuing the old rural finance paradigm and the narrowing fiscal space have also promoted a shift in Government strategy that now seeks viable intermediaries for enhancing outreach.

For the majority, access to affordable rural finance services is also important to enable them to compete in the post-World Trade Organization scenario. Inability to compete because of high financial costs could reduce income of the majority of farmers and rural clients, particularly the small and subsistence clients. Lack of access to affordable rural finance services will also prevent the clients from switching to non-farm activities.

The ZTBL restructuring plan covering the following; (i) governance: establish an environment that facilitates good governance and accountability; (ii) systems: modernize operations through use of technology, networking, and communication tools; (iii) business processes: streamline products and delivery systems so as to reduce transaction costs, simplify operations, and increase outreach; (iv) products and services: introduce products and services that are financially economically viable; (v) human resource development: improve standards and skills of management and staff and strengthen training capacity; and (vi) IT: establish new hardware and software platform to support MIS, accounting system including forensic accounting, and risk management functions.

The reforms shall establish ZTBL as a key R.F.I of the country, aiming to outreach annual rural clientele to 600,000 by the end of year 2008. By expanding its private sector role, the bank aims to establish network of high tech rural and agri. financial services through intermediations under public private participation and whole-sale -retail lending mechanism.

Loan Schemes

Crop Maximization Project-II

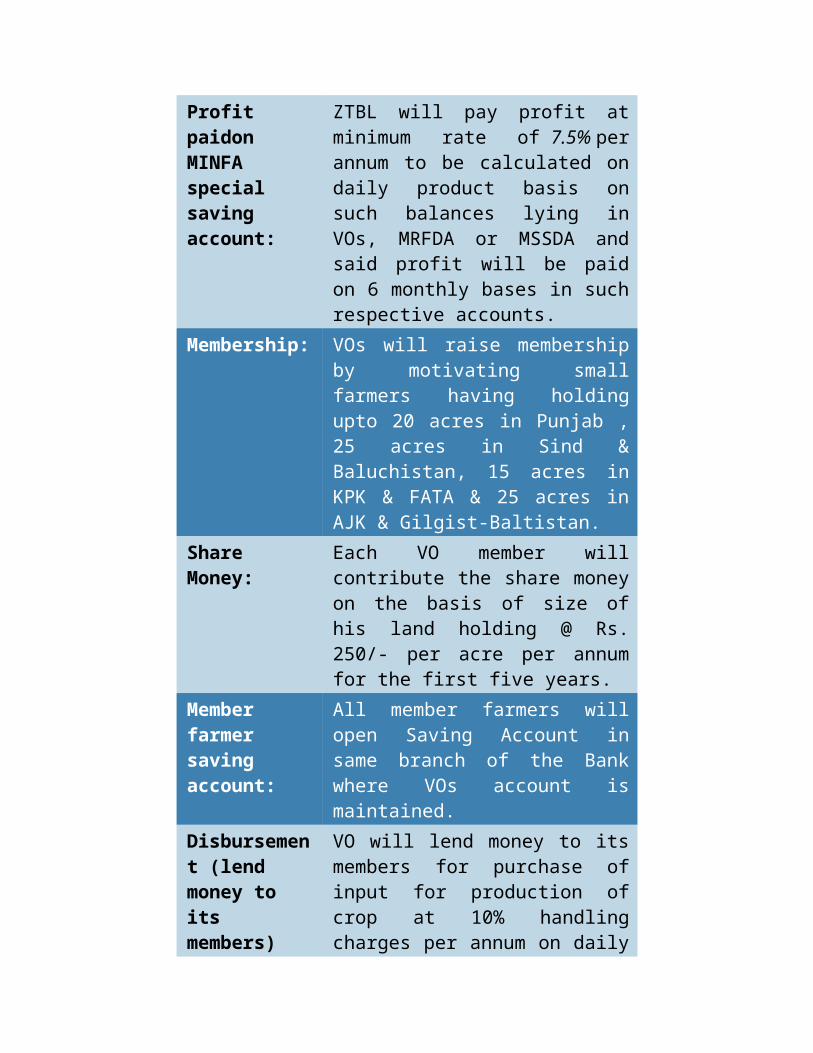

An agreement was executed between Ministry of Food & Agriculture (CMP-II M1NFA) and ZTBL on 06.6.2009 for implementation of Crop Maximization Project-II in which both have agreed to participate in establishment and Operationalization of Revolving Fund.

To implement the decision a new saving scheme under the name and style of “MINFA Revolving Fund Deposit Account” (MRFDA), “M1NFA Special Saving Deposit Account” (MSSDA.) and Member Farmers Saving Account (MFSA) have been exclusively designed for Government's Crop Maximization Project-TI (CMP-II M11'JFA).

Name of Project

Special Programme for Food Security and Productivity Enhancement of Small Farmers (Crop Maximization Project-Il)

Operational Jurisdication:

All over Pakistan in 28 Districts & 842 Villages as per annexure-I.

Sponsoring: Government of Pakistan .

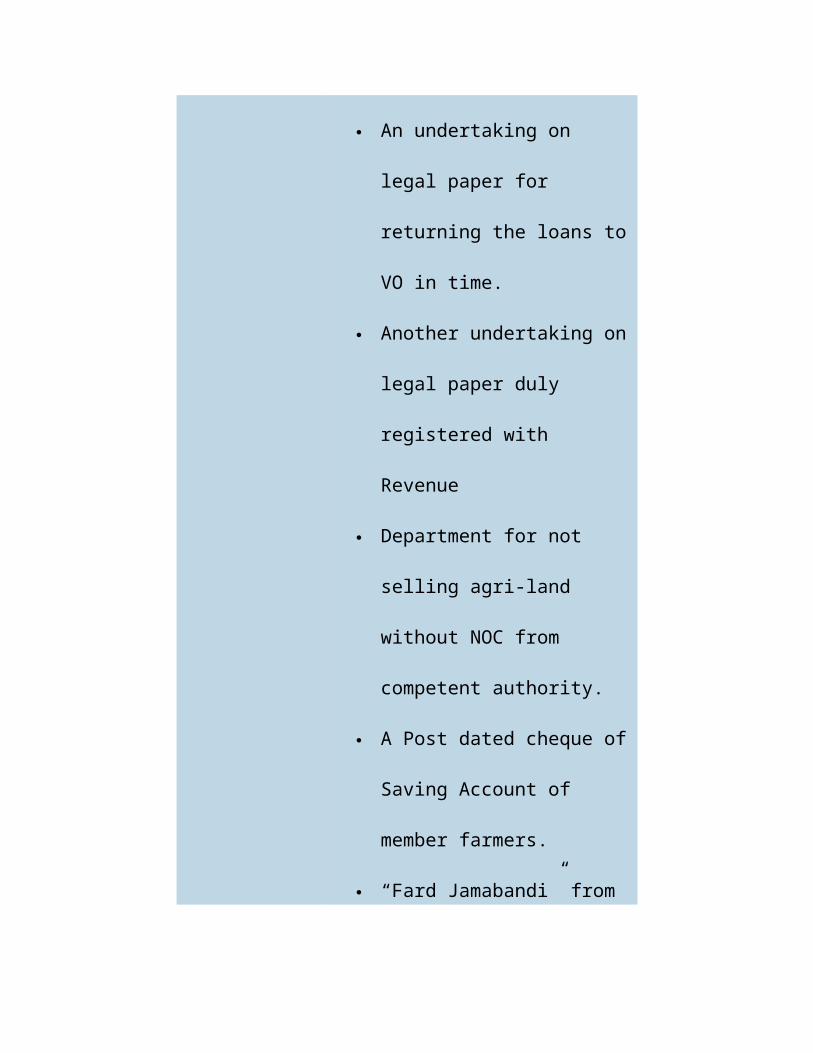

Profit paidon MINFA special saving account:

ZTBL will pay profit at minimum rate of 7.5% per annum to be calculated on daily product basis on such balances lying in VOs, MRFDA or MSSDA and said profit will be paid on 6 monthly bases in such respective accounts.

Membership: VOs will raise membership by motivating small farmers having holding upto 20 acres in Punjab , 25 acres in Sind & Baluchistan, 15 acres in KPK & FATA & 25 acres in AJK & Gilgist-Baltistan.

Share Money: Each VO member will contribute the share money on the basis of size of his land holding @ Rs. 250/- per acre per annum for the first five years.

Member farmer saving account:

All member farmers will open Saving Account in same branch of the Bank where VOs account is maintained.

Disbursement (lend money to its members)

VO will lend money to its members for purchase of input for production of crop at 10% handling charges per annum on daily product basis. In case of late repayment by the beneficiary, 12% per annum handling charges will be recovered.

Approval of loan proposal:

Loan proposal of VO level will be prepared by VOs Accountant with the assistance of the concerned Agriculture Officer/Field Assistant/Stock Assistant and presented the same before committee comprising of President, Secretary of VO and Credit Officer of the Project for approval. On

approval check/loan ceiling will be issued alongwith approval letter for Revolving Fund Special Saving Account maintained by VO at the nearest Bank Branch.

Documents Required:

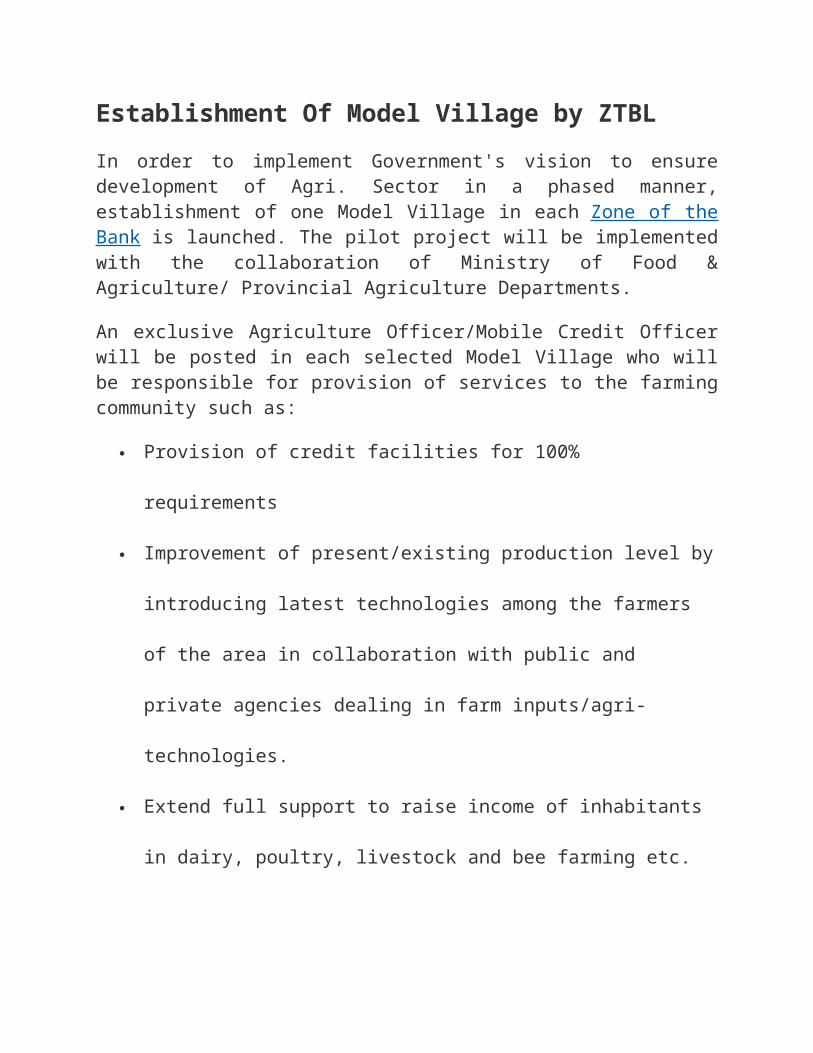

While issuing the Cheque/loan ceiling following prescribed documents will be obtained by VOs from the ir borrowing members in consultation with the Bank concerned.

An undertaking on legal paper

for returning the loans to VO

in time.

Another undertaking on legal

paper duly registered with

Revenue

Department for not selling

agri-land without NOC from

competent authority.

A Post dated cheque of

Saving Account of member

farmers.

“Fard Jamabandi” from

Revenue Department

An attested copy of CNIC.

Annexure-IProvince Districts No. of

Villages

Punjab Sialkot 30 Gujranwala 30 Sargodha 72 Sahiwal 72 Muzaffargarh 30 R.Y.Khan 72 Kasur 30 Mandi Bahauddin 30 Sub-total: 366

Sindh Sanghar 30 Mirpur Khas 32 Larkana 25 Shaheed Benazir

Abad(Nawabshah)

30

Naushehro Feroz 25 Khairpur 25 Sub-total: 167

Khayber Pkhtunkhwa

D.I.Khan 25

Bannu 25 Peshawar 25

Charsada 32 Sawabi 32 Sub-total: 139

Balochistan Jaffarabad 30 Khuzdar 20 Pishin 20 Qilla Saifullah 30 Lasbella 20 Sub-total: 120

AJK Kotli 20 Poonch 20 Sub-total: 40

FANA Gilgit/Biltistan 5FATA Khyber Agency 5 Sub-total: 10

Grand-total: 842

Crop Loan Insurance Scheme

ZTBL has launched Crop Loan Insurance scheme (CLIS) as per instructions of Government/ SBP. The main features of this scheme are listed hereunder:-

Operational Jurisdiction:

All branches of the Bank throughout the country.

Premium: Premium will be charged @ 1.3% (inclusive of all taxes and levies) of loan sanctioned for Rabi and Kharif crops separately. Bank will pay the premium for subsistence farmers and will get reimbursement from the Government on half yearly basis.

Maximum loan limit Insured :

Rs. 500,000 in an individual case.

Sum insured: Production loan for agreed crops of each season (Rabi & Kharif) for which premium is

paid.Crops covered:

Wheat, Cotton, Sugarcane, Rice & Maize

Perils covered: Excessive rain, Flood, Drought, Hailstorm, Frost, Locust attack and Insect attack.

Period of Insurance:

From the date of sowing/transplantation to completion of harvesting of the insured crop.

Compensation: Full compensation will be paid if the insured standing crop is damaged by the perils covered in calamity notified areas by the Government.

Establishment Of Model Village by ZTBLIn order to implement Government's vision to ensure development of Agri. Sector in a phased manner, establishment of one Model Village in each Zone of the Bank is launched. The pilot project will be implemented with the collaboration of Ministry of Food & Agriculture/ Provincial Agriculture Departments.

An exclusive Agriculture Officer/Mobile Credit Officer will be posted in each selected Model Village who will be responsible for provision of services to the farming community such as:

Provision of credit facilities for 100% requirements

Improvement of present/existing production level by introducing latest

technologies among the farmers of the area in collaboration with

public and private agencies dealing in farm inputs/agri-technologies.

Extend full support to raise income of inhabitants in dairy, poultry,

livestock and bee farming etc.

Facilitate farmers in marketing of the ir crops/produces on the best

prevailing market rates.

Rate of Mark up: 9% p.a. with 1% rebate on timely repayment.

Documents Required: CNIC Photocopy, Loan Case File, IB-7 Agreement, Agri-Pass Book & 2 Latest Photographs.

Maximum Loan Limit: Rs.1.000 million per borrower/party.Other information can be had from nearest Zonal Office & Branch Offices. Name & addresses of Zonal Offices/Branches are available at website (www.ztbl.com.pk)

Zone-wise list of Model VillagesS.No.

Zone Name

District Branch Model Villages

1Islamabad Rawal

PindiRawal Pindi

Ghazi Kholi

2 Lahore Lahore Chung Kamas

3Sargodha Sargodha

BhalwalChak No.16-SB

4M.B.Din Chaillianw

alaChaillianwala

5M.B.Din Chaillianw

alaChak Jani

6Faisalabad Faisalabad

FaisalabadChak # 32-JB

7Gujranwala

Gujranwala Wazirabad

Kot Inayat Khan

8 Sahiwal Sahiwal Sahiwal 92/6-R

9Vehari Vehari Tibba

SultanpurDurpur

10Multan Multan Multan Jahangirab

ad

11D.G. Khan D.G. Khan D.G. Khan Khakhi

Gharbi

12Muzaffargarh

Muzaffargarh

Muzaffargarh Doaba

13Bahawalpur

Bahawalpur

Bahawalpur

Goth Gehna

14 R.Y. Khan R.Y. Khan R.Y. Khan Kandewali15 Peshawar Peshawar Peshawar Ternab16 D.I. Khan D.I.Khan D.I.Khan Dial17 Mianwali Piplan 3-4/M-L18 Abottabad Haripur Haripur Dingi

19Karachi Thatta Mirpur

SakroDeh Naihki

20Hyderabad Hyderabad

Tando JamSarang Faqeer

21

Shaheed Benazirbad

Shaheed Benazirbad Sakrand

19-Jalalani

22

Shaheed Benazirbad

Dour Baloo -Ja-Quba

23 Sukkur Sukkur Sukkur Akbarpur24 Larkana Larkana Larkana Dhamrah

25Mirpur Khas

Mirpur Khas

Mirpur Khas

Doulatpur

26 Quetta Quetta Quetta Kuchlak

27

D. M. Jamali

Naseerabad

D.M. Jamali

Goth Shafi Muhammad

AGRI. TECHNOLOGIES TO BE DISSEMINATED IN MODEL VILLAGESAgriculture officer/MCO of Model Village will provide technical guidance and will be responsible for utilization of modern agri. Technology on the followings:

Proper time of sowing .

Selection of high yielding varieties.

Seed treatment before sowing.

Proper seed bed preparation.

Use of hybrid/certified seed.

Appropriate method of sowing – use of seed cum fertilizer drill.

Appropriate method of sowing – use of seed cum fertilizer drill.

Education of farmers regarding pest scouting.

Proper application of pesticide.

Awareness regarding rodent control.

Effective weed control – use of herbicides / weedicides.

Effective irrigation techniques – sprinkler – drip irrigation systems.

Mechanized harvesting.

Farm storage to save post harvest losses.

Effective role in the marketing of produce.

One Window Operation/ Zarkhaiz Scheme (ZS)Salient features of the Scheme:-

An easy way to get Agri.Pass Books.

Credit needs of the farmers at the ir doorsteps.

All formalities from the issuance of Agro.Pass Book to processing of

loan are completed on the spot.

Efficient and cheaper lending procedure.

Simplified documentation.

Timely disbursement.

Transparent services.

Focus on small farmers.

Low recovery rate as compared with o the r Banks/DFIs.

Operational Jurisdiction:

Throughout Pakistan (except Mingora Zone in NWFP, Turbat Zone in Balochistan Province and FANA being un-settled/hilly areas).

Selection of Farmers/ Borrowers:

ZTBL MCOs, Revenue and postal staff meet at selected focal points once a week on each Monday. Blank Agri.Pass Books are supplied by the postal authorities. Patwari/Revenue officials enter land record in Agri.Pass Books. Farmers after obtaining pass books from revenue officials meet ZTBL MCOs for loans. Loan Case File (costing Rs.100/-) o the rwise is supplied to the intending borrowers free of cost.

Delivery Channel: ZTBL, Revenue, Postal authorities and Supplier through selected focal points.

Collateral: Agri.Land mentioned in Agri. Pass BookEligibility Ctiteria : Farmers having irrigated land up to 25 acres and

barani land up to 50 acres.Documents Required:

CNIC Photocopy, Loan Case File, IB-7 Agreement, Agri. Pass Book & 2 Photographs of

borrower.Maximum Sanction Limit:

Rs.0.2 million per borrower/party.

Rate of Mark up: 9% p.a with 1% rebate on timely repayment.Incentive: The farmers are facilitated at the focal point

where the bank, revenue and postal officials

are available.

The loan is disbursed within 3 days.

Repayment: Rabi loans are recoverable on 7 th July & Kharif loans on 7 th January.

Loanable Items: Inputs-Seed-fertilizer,pesticides/insecticides/POL/labour charges etc)

Canola Re-Financing SchemeConcessional Financing and Guarantee Scheme for Canola Cultivation in Flood Affected Area

In line with the policy of Federal Government SBP ZTBL has launched a “Concessional Financing and Guarantee Scheme” for the current financial year 2010-11 in following flood affected areas:-

S. No.

District S. No.

District

Punjab Khyber Pakhtunkhwa1. Layyah 1. Nowshera2. Muzaffargarh 2. Charsadah

3. Rajanpur 3. D.I. Khan4. Rahim Yar Khan 4. Peshawar5. Multan 6. D.G Khan Sindh Balochistan1. Sukkur 1. Nasirabad2. Nausheroferoz 2. Jaffarabad3. Benazirabad 3. Jhal Magsi4. Larkana

Salient feature of the scheme:-

Scope/ Eligibility criteria:

All categories of farmers (owner, owner-cum-

tenant and tenant) of the specified areas are

eligible for agricultural loans under the Scheme.

Branches shall provide agri. loans to farmers as

per Bank's credit policy and SBP regulations.

Production loans would be provided under One

Window Scheme as well as through General

Credit Scheme in branches as it is one time

arrangement without involving revolving limit on

the pattern of Sada Bahar/Awami Zarai Schemes.

Branches would arrange for the insurance of loan

cases provided under the scheme to avoid risk of

losses due to natural calamities.

The loan would be processed under scheme

during current Rabi season up to expiry of the

sowing period of the canola crop as per local

conditions

Security: The loan would be secured against the acceptable forms of security as per policy of the Bank. The surety loans would be advanced up to Rs.25,000/- per borrower against two sureties as per standing instructions of the Bank.

Sanction of Loans:

Production loans upto Rs. 0.500 million would be sanctioned by the Managers. In case the amount of loan to be sanctioned including amount of loan(s) outstanding exceeds Rs.0.500 million the loan would be sanctioned by the respective Zonal Chief .

Legal Documentation

Legal documentation would be executed as per type of security and system to be followed according to standing instructions of the Bank.

Disbursement: The sanctioned loan would be disbursed in cash through current deposit account of the borrower.

Rate of Mark-up

Mark up rate to be charged from the borrower at 8% per annum and in case of default 9% per annum would be charged from 08.06.2011 till its repayment/closure of loan case.

Repayment of Loans to SBP:

Principal amount of loans under the scheme shall have to be repaid on the agreed date between bank and the borrower.

Utilization: MCO would check the utilization in each and every case within 30 days of disbursement. In case the loan case is declared as misutilized this would be recalled in lump sum as per Bank's instructions. Random rechecking of utilization would be done as per standing instructions.

Monitoring: All concerned Branch Managers, Zonal Chiefs and SVP, Credit Operations Department ZTBL HO Islamabad will be responsible for overall monitoring of the scheme so as to ensure the achievement of given targets and compliance of all the terms & conditions of the SBP scheme.

Financing Package for KarachiA financing package for the branches falling under Karachi Zone has been notified through which financing for Fisheries, Dairy, Poultry Farming, Feed Mill, Horticulture, Vegetable raising & Nursery for Orchards, Covered Horticulture, Cut Flower, Ornamental Plants, Agri. Machinery, Irrigation Schemes & Milk Collection Centres, is advanced to accelerate the ir development.

Security: The loans are advanced against tangible security i.e. agri. land, plot/residential building or commercial property. Valuation of land/property offered in security is worked out on the basis of average sale mutation value or residential/commercial auction price fixed by the concerned land allotting agencies like DHA, MDA, KDA & Cantonment Board etc.

Conditional Ties :

Preference is given to new borrowers.

The old borrower having good track

record can also avail loan facility.

Experience and technical know how

would be added qualification to get

loan.

MCO/Managers are responsible for the

recovery and proper utilization of loan.

Capped deposit/ Equity Contribution:

10% current deposit in lieu of equity contribution is obtained from the borrower which should be maintained during the currency period of the loan.

Sanction Authority :

The Branch Manager sanctions all types of loans under the financing package upto Rs.0.500 million, whereas more than Rs.0.500 to Rs.1.000 million, loan would be sanctioned by the concerned Zonal Credit Committee.

Rate of Mark up :

Mark up rate of 9% per annum will remain operative with 1% rebate on timely repayment would be charged.

Utilization/ Monitoring :

The utilization of loan would be checked by the Assistant Manager (Desk) after one month of the disbursement. The monitoring of the se loans would also be made by deputing a Senior Officer by Credit Division

Awami Zarai Scheme (AZS)- Farm CreditMandatory for all new borrowers and optional for existing borrowers of crop production loan under Sada Bahar Scheme to avail revolving limit under Awami Zarai Scheme to get inputs through M/s Kissan Support Services Limited (KSSL) - a subsidiary of ZTBL under kind system. The prime features of this scheme are hereunder:-

Operational Jurisdiction:

All over Pakistan

Selection of Borrowers :

Bank MCO Selects the Borrowers keeping in view the criteria fixed for Sada Bahar Scheme

Delivery Channel:

Branch/KSSL/Supplier

Collateral: Tangible Securities.Rate of Mark up:

9% p.a with 1% rebate for timely repayment.

Documents Required:

CNIC Photocopy, Loan Case File, IB-7 Agreement, Agri. Pass Book & 2 Photographs

Working of Revolving limit:

It will be worked out as per crop wise ceilings fixed and revised from time to time.

Maximum Limit:

Rs.0.500 million per borrower/party.

Loan Disbursement:

Disbursement is made after supply of inputs on the basis of supply order issued in the name of KSSL, receipt of bill & acknowledgement receipt duly signed by the borrower in the branch

Repayment: This scheme is meant for 3 years with yearly renewal/clean up. Rabi crop loans are repayable on 7 th July and Kharif on 7 th January each year with grace period of one month. In case of sugarcane two installments would be fixed, 1 st on 7 th January and 2 nd on 7 th April each year with grace period of one month.

Loanable Items:

Inputs i.e. seed, fertilizer and pesticides etc.

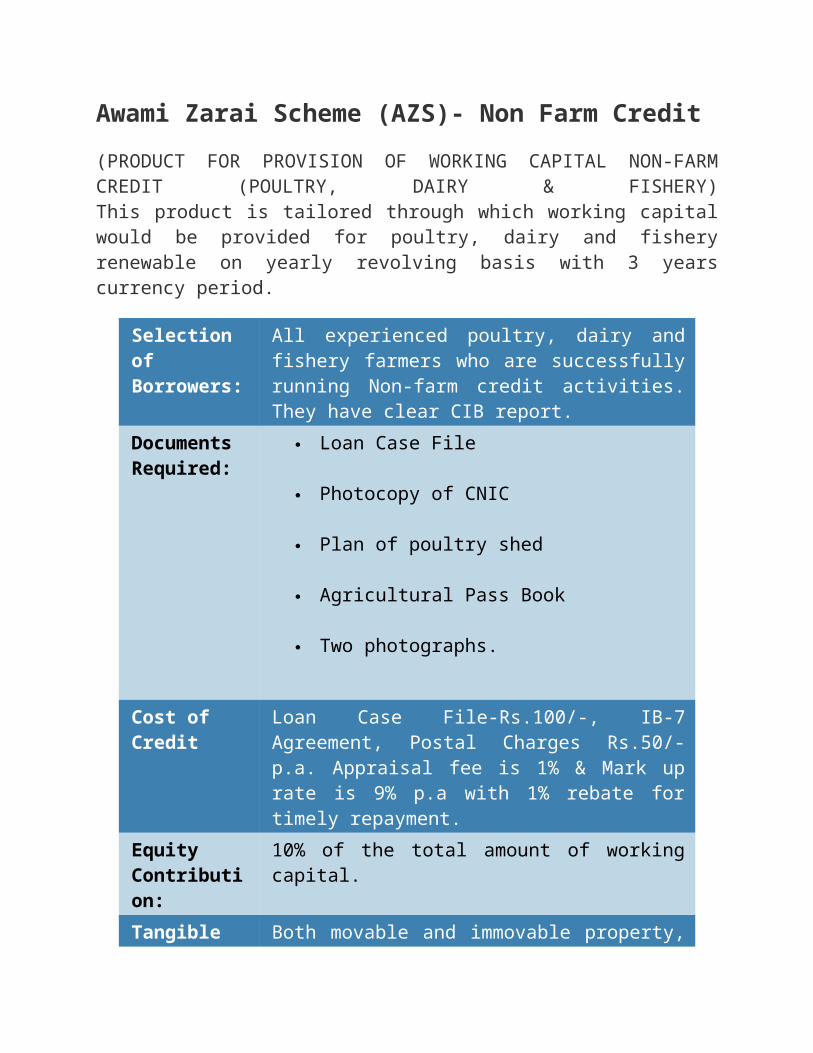

Awami Zarai Scheme (AZS)- Non Farm Credit(PRODUCT FOR PROVISION OF WORKING CAPITAL NON-FARM CREDIT (POULTRY, DAIRY & FISHERY)This product is tailored through which working capital would be provided for poultry, dairy and fishery renewable on yearly revolving basis with 3 years currency period.

Selection of Borrowers:

All experienced poultry, dairy and fishery farmers who are successfully running Non-farm credit activities.They have clear CIB report.

Documents Required:

Loan Case File

Photocopy of CNIC

Plan of poultry shed

Agricultural Pass Book

Two photographs.

Cost of Credit

Loan Case File-Rs.100/-, IB-7 Agreement, Postal Charges Rs.50/- p.a. Appraisal fee is 1% & Mark up rate is 9% p.a with 1% rebate for timely repayment.

Equity Contribution:

10% of the total amount of working capital.

Tangible Security:

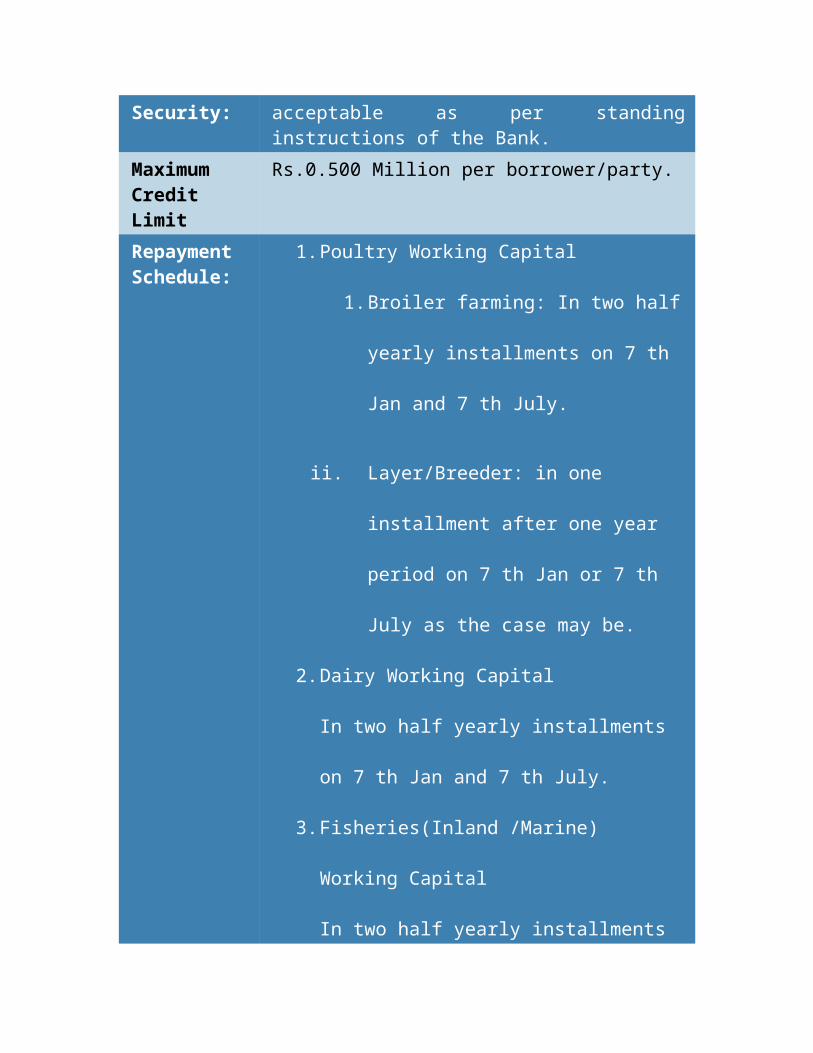

Both movable and immovable property, acceptable as per standing instructions of the Bank.

Maximum Credit Limit

Rs.0.500 Million per borrower/party.

Repayment Schedule:

1. Poultry Working Capital

1. Broiler farming: In two half yearly

installments on 7 th Jan and 7 th July.

ii. Layer/Breeder: in one installment after

one year period on 7 th Jan or 7 th

July as the case may be.

Dairy Working Capital

In two half yearly installments on 7 th Jan

and 7 th July.

Fisheries(Inland /Marine) Working Capital

In two half yearly installments on 7 th Jan

and 7 th July.

Red Meat Financing Package for Sheep/ Goat RearersPakistan 's economy is predominantly agrarian. The agriculture sector contributes 21% to the GDP. Livestock being largest sub sector of the agriculture accounts for 50% of value addition. 35 million rural population depends directly on this sector. Thus this scheme has been launched to promote this sector.

AREA of Operation: Initially the financing package is implemented in Multan , Faisalabad , D.G.Khan, D.I.Khan, Bhakkar, Nawabshah, Dadu, Sukkur, Peshawar , Lasbella, Loralai, Khuzdar Districts branches having good potential and repayment culture. The scheme will be scaled-up in a phased manner

Size of Farm: New/Fresh enterprise 10-20 heads

Existing/Medium Farmer with 3 years experience

20-50 heads

Escalators/expanding with above 5 years experience

80-100 heads

Maximum Loan Limit :

Per sheep/ Goat Rs. 5,000/-Per Teddy/ Goat Rs. 3,500/-Per Kid Rs. 1,200/-

Borrower Equity:

10% of the project cost

Recovery Period:

Fattening 6-15 monthsBreeding 5 years

White Revolution- ZTBL & NestléZarai Taraqiati Bank Ltd has been financing Milk Processing Units for UHT as well as pasteurized besides conventional dairy farming in the country since long. Bank has now embarked upon to bring white revolution in the country through integration of dairy farmers and milk processors.

In order to increase milk supply, mitigate poverty in the country and improve the living standard of the rural populace, as a first step, modalities of Strategic Partnership of Bank with M/s. Nestlé Pakistan Ltd. have been worked out and an agreement to this effect has been executed.

Operational Jurisdiction:

Throughout Punjab Province

Selection of Borrowers:

M/s Nestlé identifies the borrowers (existing as well as new dairy farmers) to recommend concerned ZTBL Branch through Model Branch Lahore.

Delivery Channel: Nestlé/ ZTBL BranchCollateral: Tangible PropertiesDocuments Required:

CNIC Photocopy, Loan Case File, IB-7 Agreement , Agri. Pass Book & 2 Photograph & Building Plan (if dairy structure involves).

Loanable Items/maximum limit:

Dairy

sheds/struct

ure

Local

Buffalo/Cow

As per prescribed ratesUpto Rs. 80,000/- per headUpto Rs.125,000/- per headUpto Rs. 6,000/ per head

Imported

Cow with calf

Working

Capital

Maximum Loan Limit:

Rs.1 million per borrower/party.

Cost of Credit: Loan Case File- Rs.100/-, Appraisal Fee @1% of loan amount, Postal Charges Rs.500/- per year, Mark-Up Rate is 9% p.a. with 1% rebate for timely repayment.

Insurance of Animals

Bank arranges insurance of animals through M/s Adamjee Insurance Company Ltd.

Equity Contribution:

10% of the cost of the Project

Disbursement of Loan:

Loans for sheds and working capital will be

disbursed in cash in suitable installments.

Imported cows through Nestlé.

Local Cow/Buffaloes through pay order/DD

in the name of seller.

Allocation of Funds:

For the five years 2007-2011 Rs.5 Billion have been allocated to finance 10,000 animals each year.

Monitoring of Loan:

M/s Nestlé will carry out monitoring of loan to update the branch periodically.

Recovery Period: 5 years in monthly/weekly installments with grace period of 1-3 months for local and imported animals respectively.

White Revolution- ZTBL & PDDCTo modernize the existing dairy farming and in order to increase milk supply in the country, a Strategic Partnership between ZTBL & PDDC has been made. Under the Scheme M/s PDDC recommends good dairy farmers to ZTBL for provision of finances for the purpose. Provision of assured quality dairy equipments i.e. milk chilling tanks, geezers, fodder machines/mixtures, water pumps/diesel engines etc. & installation the reof on competitive market rates to the farmers. Salient features of the scheme are as under:-

Coverage: Throughout the country.Eligible Farmers: Existing good dairy farmers duly selected/recommended

by PDDC.Delivery Channel:

PDDC/ZTBL Branch/ Supplier.

Documents Required:

CNIC copy, Loan Case File, Agri. Pass Book & 2 Photographs

Type of Security: Agri Land /other Tangible Security.Loan Limit: Rs.1.000 Million per borrower/party.Equity Contribution:

10% of the Project cost

Cost of Credit: Loan Case File Rs.100/-, IB-7 Agreement, Appraisal Fee @1% of loan amount, Postal Charges Rs.500/- per year

Mark Up Rate: 9% p.a with 1% rebate for timely repayment.Incentives: Borrowers are required to pay only 50% of principal

amount on due dates whereas mark-up as well as 50% of principal amount shall be paid by PDDC

Recovery Period: 5 years in monthly installments with grace period of 3 months

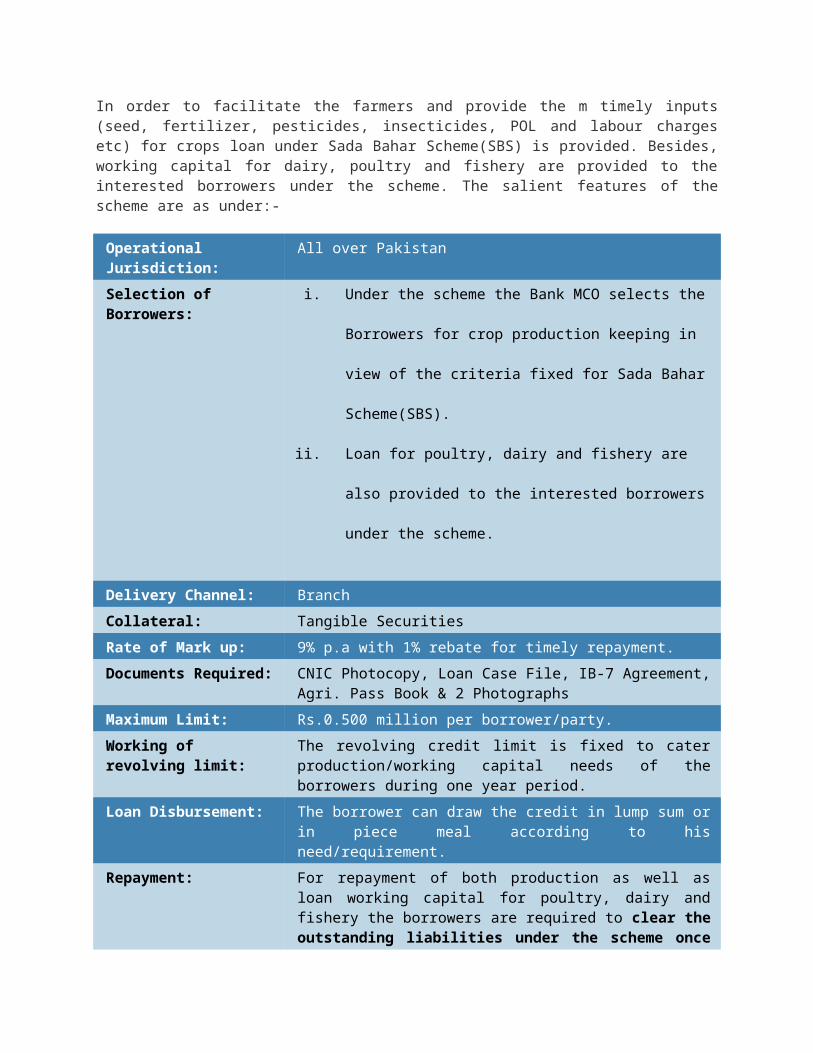

Sada Bahar Scheme (SBS)In order to facilitate the farmers and provide the m timely inputs (seed, fertilizer, pesticides, insecticides, POL and labour charges etc) for crops loan under Sada Bahar Scheme(SBS) is provided. Besides, working capital for dairy, poultry and fishery are provided to the interested borrowers under the scheme. The salient features of the scheme are as under:-

Operational Jurisdiction:

All over Pakistan

Selection of Borrowers: i. Under the scheme the Bank MCO selects the Borrowers

for crop production keeping in view of the criteria fixed

for Sada Bahar Scheme(SBS).

ii. Loan for poultry, dairy and fishery are also provided to

the interested borrowers under the scheme.

Delivery Channel: BranchCollateral: Tangible SecuritiesRate of Mark up: 9% p.a with 1% rebate for timely repayment.Documents Required: CNIC Photocopy, Loan Case File, IB-7 Agreement, Agri. Pass

Book & 2 PhotographsMaximum Limit: Rs.0.500 million per borrower/party.Working of revolving limit:

The revolving credit limit is fixed to cater production/working capital needs of the borrowers during one year period.

Loan Disbursement: The borrower can draw the credit in lump sum or in piece meal according to his need/requirement.

Repayment: For repayment of both production as well as loan working capital for poultry, dairy and fishery the borrowers are required to clear the outstanding liabilities under the scheme once in a year by the due date and get renewed credit limit for next year up to 3 years.

Loanable Items: Inputs i.e. seed, fertilizer and pesticides etc.Working capital for Poultry, Dairy and Fishery.

Green Revolution SchemeIn order to achieve the aim of providing farm machinery and implements to encourage the mechanized farming for the enhancement of agriculture productivity as compared with traditional tillage system a Memorandum of Understanding between Zarai Taraqiati Bank Ltd. and Department of Agriculture. AJ&K has been signed under title of Green Tractor Scheme. The main features of this scheme are listed hereunder:-

Operational Jurisdiction:

Throughout AJ&K Area

Selection of Borrowers:

Bank MCO Selects the Borrowers on the recommendation of Department of Agriculture, AJ&K

Delivery Channel :

Branch/Department of Agriculture, AJ&K

Mark up Rate: 9% p.a with 1% rebate on timely repayment.Document CNIC Photocopy, Loan Case File, IB-7 Agreement, Agri. Pass Book &

Required : 2 Photographs of borrowerCollateral: Tangible PropertiesMaximum Credit Limit:

Rs.1.000 million per borrower/party

Incentive: AJ&K Government would reimburse the amount of mark up charged by the Bank provided the borrowers repay the loans on due date.

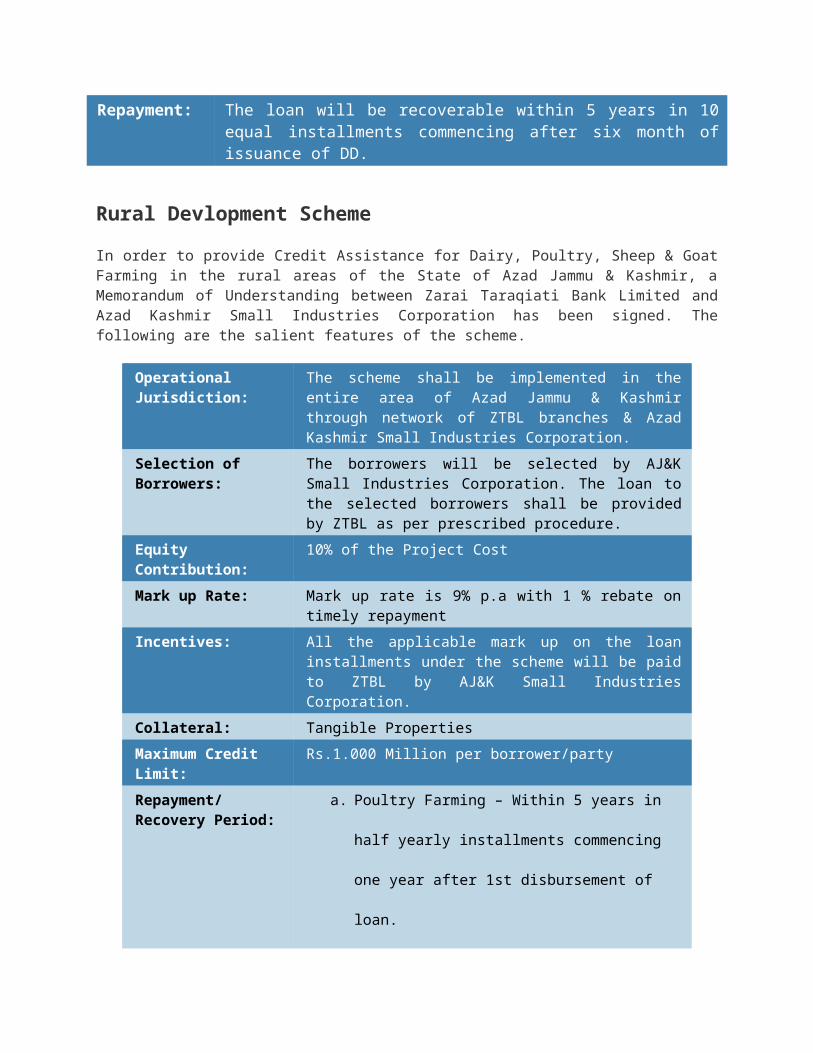

Repayment: The loan will be recoverable within 5 years in 10 equal installments commencing after six month of issuance of DD.

Rural Devlopment Scheme

In order to provide Credit Assistance for Dairy, Poultry, Sheep & Goat Farming in the rural areas of the State of Azad Jammu & Kashmir, a Memorandum of Understanding between Zarai Taraqiati Bank Limited and Azad Kashmir Small Industries Corporation has been signed. The following are the salient features of the scheme.

Operational Jurisdiction:

The scheme shall be implemented in the entire area of Azad Jammu & Kashmir through network of ZTBL branches & Azad Kashmir Small Industries Corporation.

Selection of Borrowers:

The borrowers will be selected by AJ&K Small Industries Corporation. The loan to the selected borrowers shall be provided by ZTBL as per prescribed procedure.

Equity Contribution: 10% of the Project CostMark up Rate: Mark up rate is 9% p.a with 1 % rebate on timely

repaymentIncentives: All the applicable mark up on the loan installments under

the scheme will be paid to ZTBL by AJ&K Small Industries Corporation.

Collateral: Tangible PropertiesMaximum Credit Limit:

Rs.1.000 Million per borrower/party

Repayment/Recovery Period:

a. Poultry Farming – Within 5 years in half yearly

installments commencing one year after 1st

disbursement of loan.

b. For Dairy/Livestock Farming – Within 5 years in

half yearly installments commencing six months

after 1st disbursement of loan.

Agriculture Technology

Dairy machinery Potato digger

Fruit grader Potato graderGarden waste

chipperPotato planter

M E S C E R O

Pruning equipment

Modern agri machinery implements

S A L U S T I A N A

FLAIL MOWER

Self Propelled rotary hoe

Agro based industries

Solar devices

Irrigation machinery

Stubble shaver

Crops orchard

Tunnels

Cut flower crops

Water reel sprinkler

High tech cheaper Technologies

Yanmar combine harvester

Offset rotavator

Fertilizer spreader

Groundnut thresher

Inter row rotary cultivator

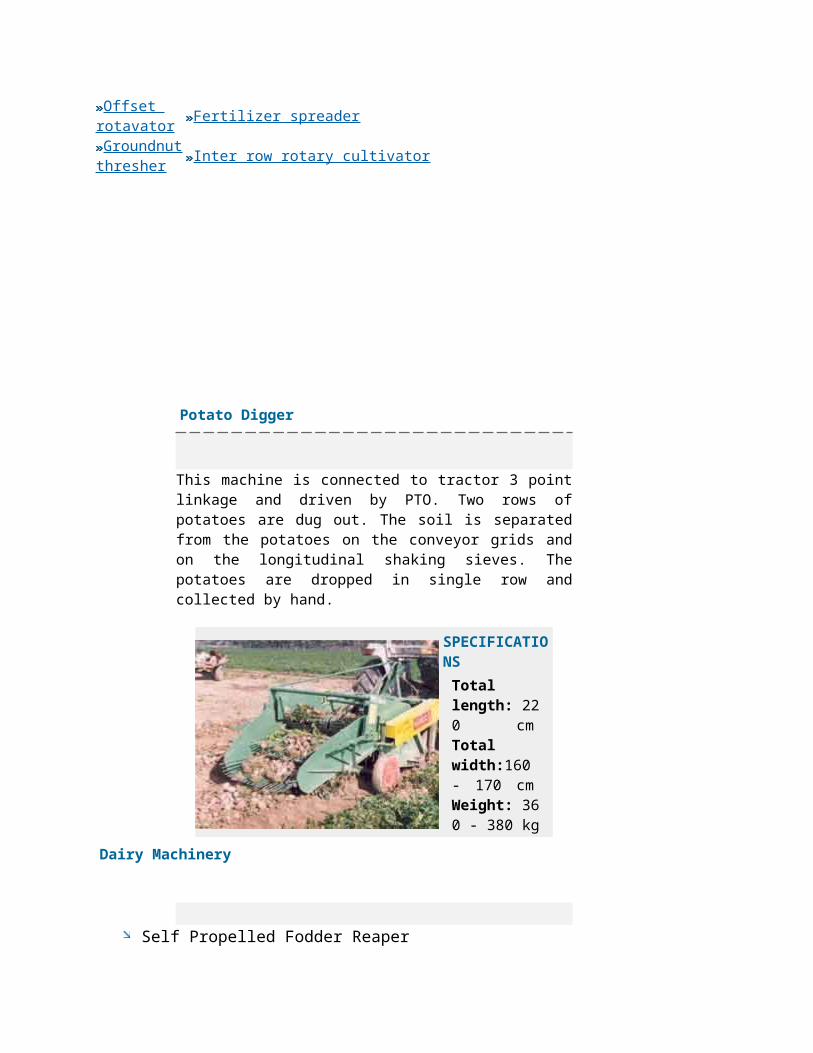

Potato Digger

This machine is connected to tractor 3 point linkage and driven by PTO. Two rows of potatoes are dug out. The soil is separated from the potatoes on the conveyor grids and on the longitudinal shaking sieves. The potatoes are dropped in single row and collected by

hand.

SPECIFICATIONS

Total length: 220 cm Total width:160 - 170 cm Weight: 360 - 380 kg

Dairy Machinery

Self Propelled Fodder Reaper

Milking Machine

Milk Chilling UnitsFarm Yard Mannure Spreader

Fruit Grader

For grading all kinds of fruits this machine is equipped with roller inspection belt, conveyer belt and grading disc for six sizes + Handling of fruit is without damage.

SPECIFICATIONSGrading Disc:Speed variablePower Required:1x

½ HP + 1 x 1/3 HPSizes of Fruits:Stepless adjustableWeight: 400 kg

Potato Grader

Potatoes are fed by elevator belt (variable speed to 3 riddles which move the potatoes with adjustable shocks to roller inspection belts. The machine has 4 outlets to provide different sized potatoes. Handling of potatoes is with out damage, especially suitable for seed potatoes.

SPECIFICATIONSOverall Length: 525 cm Overall width:125 cm Riddles: 3 with square holes, 1 with barMotor: 0.75 KW Capacity:4000 Kg/hr

Garden waste chipper

Chips wood up till 8 cm with a knife disc and shreds branches and other garden waste like grass, herbs etc. the machine is tractor mounted and PTO driven.

SPECIFICATIONSDiam. Knife disc:45cmNumber of knifes:2Revolution of knife disc:1800 RPMWeight:250 kgPower Requirement:25- 30 HP

Potato Planter

The seeding mechanism is land wheel driven. The elevator chain is mounted with cups lifting the seed potatoes from the hopper to the seed funnel. Furrow openers open the furrows where the seed is dropped. Seed is later covered by means of adjustable disc/ridger.

SPECIFICATIONSNo. of Rows: 2No. of Hopper: 2Row to Row Distance:AdjustableField Capacity: 2 hours/acre

M E S C E R O

seedless

Acidic / juicy

Highly productive

Round the year bearer

Export Oriented

An excellent crushing variety

Pruning Equipment

Tractor mounted compressor with big capacity tank provides air to two automatic hose reels with 50 meters house each. A variety of pruning shear, tree shear, hedge trimmer (65 cm) and chain saw (length 24 cm) is available.

SPECIFICATIONSSuction capacity: 850 L/MinTank capacity:250 LMax. pressure:18 Bars Normal pressure: 8- 12 Bars Cutting capacity shears: 30-35

Small HP Tractors (14-35 HP)

Combine Harvesters

Seed Processing UnitPotato Grader

Multi Crop Planter

Potato Planter

Potato Digger

Groundnut Thresher

Self Propelled Reaper for Wheat & Paddy

Reversible Disc plough

Three Rows Ridger

Rice Transplanter

Cotton Picker

Inter Row Rotary Cultivator

Sugarcane HarvesterOff Set Rotavator

Orchard Sprayer

Electrodyne Sprayer

Flail Mower

Stubble Shaver

Maize Sheller

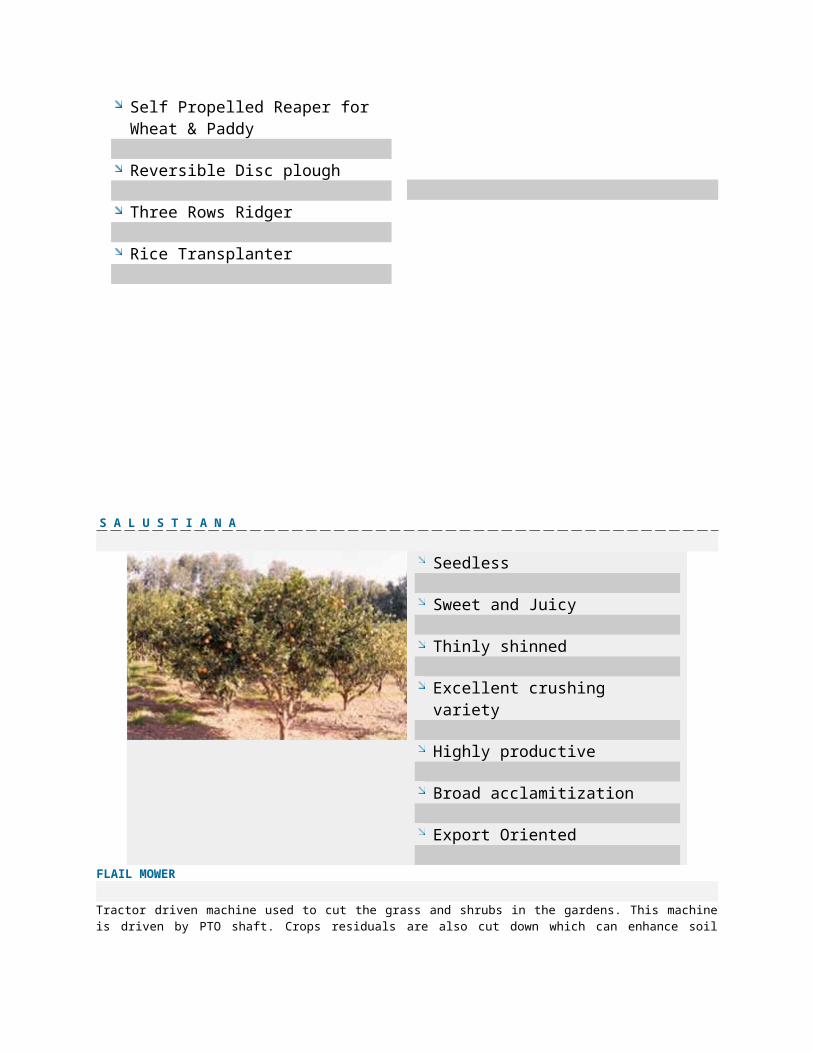

S A L U S T I A N A

Seedless

Sweet and Juicy

Thinly shinned

Excellent crushing variety

Highly productive

Broad acclamitization

Export Oriented

FLAIL MOWER

Tractor driven machine used to cut the grass and shrubs in the gardens. This machine is driven by PTO shaft. Crops residuals are also cut down which can enhance soil fertility.

SPECIFICATIONSWorking Width: 72 Inches (180 cm)Power Required: 1x ½ HP + 1 x 1/3 HP

Self Propelled Rotary Hoe

SPECIFICATIONSEngine: 5 HP

Fuel: Petrol Field Capacity:0.75-1 acre/hr.

Agro Based Industries

U.H.T. Treated Milk Plants

Yogurt Plants

Rice Mills

Juice Plants with paper packing facility

Packing Material for food items

Solar Devices

Solar Lift Irrigation System/Tubewell

Solar Fencing

Solar Gyser

Solar Loud Speaker System

Solar Berg Alarm System

Irrigation Machinery

High Speed Diesel Engines

Sprinkler Irrigation Systems

Drip Irrigation SystemStubble Shaver

For vigorous deep rooted ratoon of sugarcane crop stubble shaving is essential. The process

destroys unwanted cane stubble so that the ratoon growth can develop further.

SPECIFICATIONSBlades: 6Required HP:55 HP

Crops Orchard

Soybean Cultivation

Multicut Hybrid Sorghum

Hybrid Maize

Tea Cultivation

Mint Cultivation and Distilation Unit

Hot Bin Mist Propagation Unit

Polythene Tunnels

Shade Netting

E.M. Technology

Exatic Fruit Plants

Deciduous

Mother plants

Dwafing apple rootstoc

Recommended varieties

Star Krimson (apple)

Red Beauty (plum)

Salustiana (orange)

Mescero (lemon)

MM 106 (apple rootstock)

Export Oriented Citrus plants

Sweet oranges

Mandarines

LemonsTunnels

Production three folds as compared to open conditions

Early and late production

Considerable water savings

Weed control easy and effective

Helps raising ornamental plants

Cut Flower Crops

Roses

Tube Roses

Gladioloi

Water Reel Sprinkler

This machine is used to irrigate almost all the agricultural crops. Considerable water saving is made since there is noloss of water due to seepage. The pump is operative by tractor PTO.

SPECIFICATIONSFlow:2-4 Lit/ SecThrow:35 MeterPipe Length:180 Meter

Development of High Tech Cheaper Technologies

Potato Digger

Inter Row Rotary Cultivator

Self Propelled Rotary Hoe

Self Propelled Reaper for wheat & paddy

Groundnut Thresher

Potato Planter

Water Reel Travelling Sprinkler

Three Row Ridger

Border Disc

Off Set Rotavator

Stubble Shaver

Flail Mower

Fertilizer Spreader

Seed Processing Plant

Fruit Grader

Yanmar Combine Harvester

This combine harvester is basically designed for harvesting of paddy crop but it is also capable of harvesting wheat, sunflower, maize and canola crops etc. It is fitted with screw rotor type threshing drum due to which it does not cause grain breakage. 04 Units of this combine harvesters are available in stock for sale which will be supplied to intending buyers on " first come first served basis" against cash or credit.

SPECIFICATIONSModel:CA-760Engine:Yanmar 4TN100 , Water - cooled , 4 - Cycle , Vertical 4-Cylinder , Diesel EngineEngine output: 76 PS/2600 rpm (75 HP)Grain Handling System:Bagging typeAv. Field Capacity: 1.25 - 1.50 acre/hr Paddy 1.50 - 2.00 acre/hr Wheat

Offset Rotavator

Its blades cut and pulverize the soil and incorporate trash effectively. Offset type rotary cultivators are especially suitable for soil cultivation in orchards particularly under trees. As the implement is off-set to one side of the tractor, therefore, tree branches do not cause hindrance to tractor operator.

SPECIFICATIONSSpeed:540 RPMPower required: 45- 50 HP

Groundnut Thresher

This machine is used for separating pods from peanut vines. Pods attached to the vines are fed from the top of the thresher. Clean pods can be collected in sacks. This machine is powered by a small HP Engine.

SPECIFICATIONSEngine Power: 2HPWorking Capacity:300-370/ KG/HourDrum Revolutions:400- 500 RPM

Fertilizer Spreader

Chemical fertilizers utility increases if kit is evenly spread. Fertilizer spreader evenly spreads if it is evenly spread. Fertilizer spreader evenly spreads both granular and powdered fertilizers. The quantity of fertilizer application can be adjusted according to requirement without any wastage, thus ensuring optimum returns on fertilizer investments. Fertilizer is put in the hopper, two rod like structures continuously agitate the fertilizer.

SPECIFICATIONSHopper capacity: 300 kgFertilizer spreading width: 10mWeight:20 kgPower Required:30-35 HP Tractor

Inter Row Rotary Cultivator

This Rotary Cultivator can be used for hoeing of cotton, maize, sugarcane, groundnut, tobacco and other row crops. Weeds are controlled mechanically while aeration and infiltration of soil are also improved.

SPECIFICATIONSNo. of Rows:3Row to Row Distance:AdjustableWorking Width:20" / 50 cm

Credit LimitsOverall Credit Limit Per Borrower Rs.1.000 Million

Sada Bahar Scheme under one window operation or otherwise Rs.0.500 Million

PER ACRE CREDIT LIMITS

Major Crops:Wheat 16,000Paddy (Rice) 19,000Sugarcane 30,000Cotton 21,000Maize 20,000

Minor Crops:

Potato 36000 Bajra 11000Tobacco 29000 Jawar 11000Mustard Mung 11000 Gram 12000Tomato 19000 Guara 3000Mash 3000 Caster Oil 6000

Lentil 11000 Barlay 9000Groundnut 14000 Berceme 4900Sunflower 15000 Janter 4000Soyabean 12000 Garloc 26000Canola 13000 Turmeric 25000Rape Seed 11000 Ginger 30000Til(Sesame) 12500 Lacern & Shaftal 4500Suger beet 12000

Mature Orchard/Fruits Crops:

Pear 24000 Dates 31000Loquat 24000 Strawberry 25000Plum 33000 Tea 60000Apple 37000 Guava 24000Papaya 22600 Pomegrante 33000Almond 32000 Palm 22000Coconut 21000 Olive Oil 13000Lichi 32000 Walnut 23000Cherry 33000 Persimen 15000Mango 37000 Zizi Phus(Bher) 25000Apricot 31000 Melon 16000Banana 37000 Water Melon 16000Peach 32000 Musk Melon 16000Citrus 34000

Growing Orchards

SNo. Trees 1st Year 2nd Year 3rd Year 4th Year 5th Year

1 Mango 24,000 13,000 13,000 13,000 14,000

2 Citrus 21,000 12,000 11,000 13,000 13,000

3 Apple 23,000 12,000 12,000 12,,000 14,000

4 Banana 29,000 20,000 23,000 30,000 26,000

5 Jujuba 19,000 9,000 10,000 10,000 10,000

6 Guava 21,000 12,000 11,000 13,000 13,000

7 Coconut 29,000 6,000 6,000 7,000 8,000

8 Palm Oil 18,000 6,000 7,000 7,000 7,000

9 Dated 33,000 12,000 11,000 12,000 13,000

Growing Agro Forest TreesSNo. Trees 1st Year 2nd Year 3rd Year

1 Bamboo 34,000 8,000 3,000

Types of SecurityImmovable Property

Agricultural Land

Under Pass Book System 80% Outside Pass Book System 70% Under Alienability Certificate 66%

Commercial/Industrial Land under Pass Book 80%

Outside Passbook System

Urban Residential/Commercial Plots in all localities outside Pass Book

75%

Alienability Certificate 66% Residential/Commercial Buildings 70%

Lease hold rights of a leased land of CDA/KDA with 99 years lease 70%Back to Top

Movable Property

Unconditional Bank guarantee from scheduled Banks

Upto maximum amount of an un-conditional Bank guarantee after keeping sufficient margin for un-paid mark-up, cost, charges and expenses.

Guarantee issued by Central or Provincial Government

Full amount of loan plus return and other charges.

Government securities 85% of face value or market value whichever is less.

Defense Savings & FEB Certificates 75%Fix Term Deposits Receipts 85% of face value.

NIT Units 80% of the face value or market value whichever is less.

Life Insurance policies 85% of surrender value

Pledge of Potatoes/Seed Potatoes price or market value which ever is less

Upto 75% of Govt. support

Back to Top

Personal Surety

Against a bond with two sureties under General Credit and one surety in Special Schemes upto Rs.25,000/-

Upto 50% of appraised value of properties of sureties.

Back to TopDebt Equity Ratio

For Tubewell/Tractors/Implements/Attachments/Equipments1 All kinds of Tubewells/ Turbines 25% Within 5 years in annual/bi-annual

installments commencing one year after first disbursement

2 New Tractor No equity but 10% of the loan is to be needed in PLS Account

Within 8 years in monthly/quarterly or half yearly installments to be decided by Manager in consultation with borrower.

3 Used Tractor, Equipments/attachments/implements and used tractor

-do- Within 5 years in monthly/quarterly or half yearly installments to be decided by the Manager in consultation with borrower.

Except Tubewell/Tractors/Implements/ Attachments/Equipments

Production Loan upto Rs.0.100 Million NIL

Land holding upto 25 acres/loan amount upto Rs.0.2 Million 15%

Land holding beyond 25 acres to 50 acres/loan amount beyond Rs.0.2 Million upto Rs.0.5 Million

25%

Land holding beyond 50 acres/loan amount beyond Rs.0.5 Million upto Rs.1 Million.

30%

Repayment Periods

S.No. Types of Loans Recovery Period

1 Short Term LoansCrop production working capital loans recoverable in lump sum commencing after the harvest/marketing of respective crops and within maximum period of 12 months.

2 Medium Term Loans

Dairy farming and livestock etc. In yearly/half yearly/monthly installments and within maximum period of 5 years.

3 Long Term LoansTractor, agricultural machinery, poultry farming, godowns and orchard iIn yearly/half yearly installments within maximum period of 8 years and. above.

Recovery ProcedureRecovery Schedule

Recovery schedule in each loan case as per terms of sanction of loan is fixed and communicated to the borrowers after disbursement of loan.

In case of default or failure in repayment of any installment on due date the mark-up shall continue to be charged and last installment due to this may differ from the amount of installments fixed at the time of disbursement.

Back to Top

Issuance of Notices

Demand notice is issued before the due date of every installment.

A Legal Notice is issued one month after the due date informing the borrower that if the amount is not repaid within next one month, further legal action will be taken to recover the dues.

Back to Top

LEGAL ACTION

Legal action can be initiated against the defaulter if loan is not repaid even after expiry of legal Notice period.

Where the court in bank's favour has decreed a case, account is to be settled by recovery of amount from the auction of the mortgaged property.

The bank may purchase the mortgaged property if considered feasible to dispose it off later on through auction or in any manner deemed fit for getting the best price.

The bank may dispose off the mortgaged properties of defaulters for satisfaction of its dues with out intervention of courts under Financial Institutions (Recovery of Finances) Ordinance 2001.Rescheduling of Loan Repayment Facility

Rescheduling of Loan Repayment Facility

ZTBL allows rescheduling of repayment of installments to its borrowers in order to maintain credit discipline and to mitigate their genuine problems in real hardship cases and in areas declared as calamity hit by the respective Provincial Governments

The Rescheduling facility is to be considered by bank on case¬to-case basis and is to be allowed on borrower's request only.

The relaxation in recovery period shall not be allowed beyond one year in any case.

The borrowers shall have to execute a supplementary loan agreement on Non Judicial Stamp Paper of appropriate value to give legal cover to extended period.

The borrowers shall have to pay the return for the extended period.

Down Payment for Rescheduling of Loans

Rescheduling Number

Rate of down payment as against due installments to be rescheduled

1st 10%2nd 20%3rd 30%

Board of DirectorsSultan Ali ChaudhryChairman Board

Mr. Muhammad Zaka AshrafPresident/ CEO(Brief Resume)

Ms. Nazrat BashirDirector

Dr. Amir MuhammedDirector

Mr. Abdul Wajid ArainDirector

Mr. Zafar-IqbalDirector

Mr. Muhammad Iftikhar Khan MohmandDirector

Mr. M.Yaqoob VardagDirector

Dr. Khalid Ahmad KhokharDirector

Mr. Mahmood Nawaz ShahDirector

Muazam AliCompany Secretary

Official Software

Sr# Software Title Contact Person's Email

1 Employee Circles [email protected]

2 HAMS - Hajj Applications Management System [email protected]

3 ICRMS - Internal Credit Risk Management System [email protected]

4 IdMS - Identity Management System [email protected]

5 NIVS - National Identity Verfications System [email protected]

6 Di-MIS - Dynamic Integrated MIS [email protected]

6.1 Flood Affected Areas [email protected]

7 BTSMS - Benazir Tractor Scheme Management System [email protected]

8 RRIS – Regulatory Reporting Information System [email protected]

9 OPAM – Online Performance Appraisal Management [email protected]

10

VSL – Vendors Short Listing System [email protected]

11

CRM – Customer Relationship Management [email protected]

12

IAMS - Internal Audit Management System [email protected]

Press release

ZTBL organized Kissan Mela for farmer in Badeen and President ZTBL Muhammad Zaka Ashraf participated as a chief guest.Dated: 13-04-2011

ZTBL organized Kissan Mela for farmer in Larkana and President ZTBL Muhammad Zaka Ashraf participated as a chief guest. Dated: 07-04-2011

Inaugural Ceremony of demonstration of solar energy with high efficiency irrigation in model village chak no. 16-GB Sargodha.Dated: 31-03-2011

On the eve of Golden Jubilee Ceremony of University of Agriculture, Faisalabad, visit of different stalls of exhibition, meeting with VC & Address to International Seminar on value Addition Concerns, by President ZTBLDated: 18-03-2011

A Chinese delegation led by Mr. F. U Junhai Vice President of China Council for the Promotion of International Trade visited ZTBL H.O Islamabad and meet Muhammad Zaka Ashraf President ZTBL.Dated: 16-03-2011

ZTBL organized Kissan Mela for farmer in DG Khan and Governor Punjab Sardar Latif Khosa attended as a chief guest.Dated: 07-03-2011

A Sudanese delegation led by H.E Mr. Muhammad Omar Musa the ambassador of Sudan visited ZTBL to attend a meeting with Mr. Muhammad Zaka Ashraf, President, ZTBL and other Senior Executives of the Bank.Dated: 02-03-2011

A delegation of Chinese Company M/s Shaanxi Xintong Intelligent demonstrated the working of solar energy pump, Sprinkle and Drip Irrigation system at village Mann near Kasur.Dated: 22-01-2011

On the 3rd anniversary of Shaheed Mohtarma Benazir Bhutto ZTBL Officer Association and Peoples Worker Union held dua and Fateha Ceremony in ZTBL HO, Islamabad.Dated: 27-12-2010

President ZTBL visit the Hyderabad Zone (19-24 December 2010) and meet the press on 24-12-2010.

KSSL Board of Director meeting Chair by Muhammad Zaka Ashraf President ZTBL at Hyderabad.

Dated: 23-12-2010.

Pakistan Women's Cricket team at 16th Asian games includes nine playing members from ZTBL cricket XI.Dated: 20-11-2010

Chinese company Chaguang Electronic keen to introduce and provide LED lights and solar technology in Pakistan.Dated: 12-11-2010

A Malaysian delegation led by H.E Dato Ahmad Anwar Bin Adnan visitedZTBL to attend a meeting with Mr. Muhammad Zaka Ashraf, President.Dated: 07-10-2010

High level USAID delegation led by Ambassador Robin Raphel visited ZTBL HO, Islamabad.Dated: 30-09-2010

President ZTBL Zaka Ashraf in a simple ceremony formally handed over the relief goods containing food items & non-food items.Dated: 27-09-2010

Signing Ceremony between ZTBL and Chinese Company M/S YTO at ZTBL HO, IslamabadDated: 27-09-2010

ZTBL Objective

Restructuring plan under RFSDP

To operate on commercial lines to expand its

outreach, the Bank is under going a process of

organizational, financial and functional

restructuringZTBL HR Strategy

Bank to look at activities it performs and attach

economic value to undertake the activity

commercially.

Ensure the Bank’s financial and human capital

is rightly deployed

As strategy Bank should use “excessively

outsource” as medium to add flexibility to its

use of Human Resource

To ensure that non-business/support function

have just the right staff complementFormatting Of KSS

1st meeting of Human Resource Management

Committee of the Board held on November

10th, 2005 approved the proposal to outsource

non core services of the Bank and formation of

Bank’s Subsidiary to provide different kind of

support services

Formation of the Bank’s subsidiary KSSL

subsequently endorsed in 20th meeting of ZTBL

Board held on November 16, 2005.

The Security Exchange Commission of Pakistan

allowed incorporation of KSSL, a Subsidiary of

the BankAppointment of MD

1st Meeting of the BOD of KSSL held on

04.03.2006 approved appointment of CEO/MD

of the companyFinancially Viability

Established purely for strategic and

administrative reasons by exercising control on

related work force and maintaining prescribed

service quality standard

Transfer of approved share capital of Rs.100

Million to KSSL

Decided that all day to day expenditure of the

Company shall be paid by the ZTBL through an

inter Company Account

Radio Pakistan

Scheme's BrochuresCrops Cultivation Guide

S.No. Title Language Type Size

1Raising Goats and Sheep in Pakistan Urdu

569 KB

2Support and cultivation guide for Peanuts Urdu

586 KB

3 Fooder Preserving guide- Silage Urdu 510 KB

4Support and cultivation guide for Sesame Seeds Urdu

448 KB

5Support and cultivation guide for Lentil pulse Urdu

384 KB

6Support and cultivation guide of Sunflower Urdu

515 KB

7Support and cultivation guide of Canola and Brassica Urdu

2.20 MB

8Support and cultivation guide of Wheat Urdu

410 KB

9Support and plantation guide for Tea Urdu

171 KB

10Support and cultivation guide for chick peas Urdu

1.43 MB

Scheme's Brochures

S.No. Brochure Title Language Type Size

1 Sada Bahar Scheme Urdu 409 KB

2 KSB Zarai Turbine User Guide Urdu 2.22 MB

3 Sairab Pakistan Scheme Urdu 560 KB

4

White Revolution Scheme- ZTBL and Nestlé Pakistan Ltd. Collaboration Urdu

636 KB

5 White Revolution Scheme Urdu 683 KB

6 Loan Scheme for poultry Urdu 517 KB

7 Loan through one window operation Urdu 191 KB

8 ZTBL Loan FAQs Urdu 1.57 MB

ZTBL BANK BRANCHES - AS ON 15-01-2011Total Zones: 31 Total Branches: 355

SR# ZONE BRANCH ADDRESS TELEPHONE

#

PUNJAB

1 Islamabad ISLAMABAD

ZTBL, ISLAMABAD BRANCH, BLOCK 7/F, OFFICERS COLONY, G-7/2, ISLAMABAD

051-9252022

Total Br = 13 HO BRANCHZTBL, HEAD OFFICE, 1-FAISAL AVENUE, ISLAMABAD

051-9252782

ATTOCKD-109 NEAR MAIN BAZAR, ATTOCK CITY

057-9316145

PINDIGHEB NEAR GOVT. HIGH SCHOOL, PINDIGHEB 0572-352508

JHELUM

NEAR ISLAMIA HIGH SCHOOL, KATCHERY ROAD, JHELUM

0544-625703

MURREEKASHMIR POINT, OPP. GOVERNOR HOUSE, MURREE

051-3410463

KAHUTA OPP. TEHSIL HOSPITAL, KAHUTA 051-3312603

TALAGANGNEAR OLD LARI ADDA, MIANWALI ROAD, TALAGANG

0543-412021

CHAKWAL JHELUM ROAD, CHAKWAL 0543-544009

JAND MOHALLAH GHOUSIA, JAND 0572-621059

GUJAR KHANG.T. ROAD NEAR BUS STAND, GUJAR KHAN

051-3511317

RAWALPINDIHAIDERY CHOWK, SATELLITE TOWN, RAWALPINDI

051-4427794

FATEHJANG

NEAR ALMAS MEDICAL CENTRE, ATTOCK ROAD, FATEHJANG

0572-212582

2 Gujranwala Alipur Chatha Thana Road, Ali pur Chatha. 055-6332375

Total Br = 11 Gujranwala D.C.Road Gujranwala. 055-9200206

Gujrat Alipur Road Near,Usmania 053-9260417

Plaza,Gujrat

Hafizabad 330-B, ADS-I Housing Colony 0547-524919

Kamoke Near Madina Hotel, G.T.Road Kamoke. 055-6811891

Lala Musa G.T.Road Lala Musa 053-7515001

Noshera virkan Tatley Road , Noshera Virkan 055-6760421

Pindi SultanpurDinga Road ,Pindi Sultanpur,Tehsil Kharian.

053-7611117

Qila Deedar SinghCivil Hospital chowk ,Qila Deedar Singh.

055-4710018

Wahndo Ghala Mandi, Wahndo . 055-6798115

Wazirabad Dhaunkal Road, Wazirabad. 055-6601449

3 Sialkot Daska Circular Road, Daska. 052-9200040

Total Br = 7 Sialkot Pak pura Kutchery Road Sialkot 052-4292542

Kotli Loharan Kotli Loharan Mashrqi near PTCL Exchange 052-3530272

Pasrur Model Town, Civil Hospital Road , Pasrur. 055-6441876

Satrah Gujranwala Road Satrah. 055-6280344

Narowal Circular Road Narowal. 054-2412871Shakargarh Zia Road , Shakar garh. 054-2450922

4 Lahore ChungNear New Khan Petrol Pump, Main Multan Road Chung

0423-7511219

Total Br = 21 Kasur Bhatta Chowk, College Road, Kasur 049-9250174

Khuddian Depalpur Road, Khuddian 049-2791195

K. R. Kishen Sabzi Mandi, K.R. Kishen 049-2382304

ChunianMuhala Talab Wala, Opp Veternary Hospital, Chunian

049-4310019

Kanganpur Depalpur Road, Ellah Abad, Kanganpur 049-4751303

Pattoki Main Multan Road, Pattoki 049-4420055

FerozewalaNear Malik Taj Din Building, Shahdara, Lahore

0423-7933668

ManawalaMain Faisalabad/Sheikhupura Road, Manawala.

056-3771054

Narang Mandi Rafiqabad Narang Mandi 056-2410117

Nankana Sahib Near General Buss Stand, Nankana Sahib 056-2874744

Sangla HillMaher Balocha Road, Near Post Office, Sangla Hill

056-3703056

Sharaqpur New Hospital Road, Shraqpur Shariff 056-2591022

Muridke Near Tehsil Office, Bangla Road, Muridke. 0423-7981745

Khanqa DogranMain G. T. Road, Muhallah Islampur, Khanqa Dogran

056-3726331

More KhundaMadina Colony, Jaranwala Road, More Khunda

056-2442473

SheikhupuraMalik Anwar Road, Civil Lines, Sheikhupura

056-9200091

Model Br. 47-C, The Mall, Lahore. 0423-7312297

Lahore Cantt.27-C, Old Army Officer Colony, Zarar Shaheed Road, Lahore.

0423-6662393

PhoolnagarOpp. Town Committee Office, Lumbey Jaggir Road, Phoolnagar

049-4510501

Syed Wala Main Jaranwala Road, Syed Wala 056-2722112

5 Multan MULTAN. 61-A, Abdali Road, Multan 061-9200509

Total Br = 8 M. RASHEED Vehari Road, Makhdoom Rasheed 061-4592210

SHUJABAD Jalalpur Pirwalal Road, Shujabad 061-4396336

JALALPUR Khan Baila Road, Jalalpur Pirwala 061-4210202

BASTI MALOOK Shahab Centre, 061-4250125

Bahawalpur Road

LODHRAN Near Super Chowk, Lodhran 0608-9200039

DUNYAPUR Basti Malook Road, Dunyapur 0608-305279

K. PACCA Lodhran Road, Kehror Pacca 0608-342624

6 R. Y. Khan Rahim yar KhanAllama Iqbal Town,Church Road Rahim yar Khan

068-9230050

Total Br = 7 Khan Pur KatoraH.No181/182,Model Town-A Khan Pur Katora

068-5573079

Sadiq AbadMehar Abad Shemla Point,Nehar Kinara Sadiq Abad

068-5703546

Liaquat PurH.No. 4/B-1,Town Committee, Housing Scheme,Liaquat pur

068-5795309

Sanjar Pur Main KLP, Road Sanjar pur 068-5780016

Mian Wali Qureshian

Main KLP,Road Mian Wali Qureshian 068-5565160

Zahir PirMouza Muhammad Khan, Main KLP Road,Chock Zahirpir,

068-5563030

7 Sargodha SARGODHA KATCHERY ROAD, SARGODHA. 048-9230491

Total Br = 17 BHAGTANWALAMAIN LAHORE ROAD, BHAGTANWALA

048-3780041

SILLANWALIREHMANPURA, LARI ADDA ROAD, SILLANWALI.

048-6532087

SAHIWAL TOWNOPP. SHELL PETROL PUMP, JHANG ROAD, SAHIWAL

048-6786061

BHALWAL286, BLOCK NO.1 SATELLITE TOWN, BHALWAL

048-6642873

BHERANEAR ISLAMIA MODEL HIGH SCHOOL, BHERA

048-6691486

KOT MOMIN MOHALLAH 048-6682051

KHAWAJABAD, BHALWAL RD, KOT MOMIN

SHAHPUR

NEAR POLICE STATION, KHUSHAB ROAD SHAHPUR SADAR

048-6310530

JAUHARABAD KOTHI NO.3, BLOCK NO.1, JAUHARABAD. 0454-920255

NOORPUR THALNEAR REVENUE OFFICE, NOORPUR THAL

0454-850842

MALAKWAL

MOHALLAH KANIANWALA, POST OFFICE ROAD, MALAKWAL

0546-591339

PHALIANEAR HALLIAN CHONGI, GUJRAT ROAD, PHALIA

0546-596069

M.B.DINSUTSIRA CHOWK, MANDI BAHA-UD-DIN.

0546-500562

CHALLIANWALA

M.B.DIN - KHARIAN ROAD, CHALLIANWALA.

0546-590299

P.D.KHAN RAILWAY ROAD, PIND DADAN KHAN. 0544-210262

PINDI BHATTIANNEAR AQIL GATE, LAHORE ROAD, PINDI BHATTIAN.

054-7531484

GOJRAMAIN ROAD GOJRA, DISTRICT Mandi Bahauddin

0546-588339

8 Vehari Vehari 150-A-O Block Danewal 067-3362408

Total Br = 11 Mailsi Ward No.3, Multan Rd. 067-3410341

BurewalaHouse No.25,26,27 Gulshan-e-Rehman Town

067-9200068

T.S.Pur Ward No.4 Qutabpur Rd. 067-3692077

Karampur Mailsi Rd. 067-3696029

Ludden Hasilpur Rd.,Ludden Tehsil 067-3691136

KhanewalHouse No.25, St.No.1, Block-W, Peoples Colony

065-9200083

Kabirwala Jhang Rd.Kabirwala 065-2410619

Abdul HakimMultan Rd., Abdul Hakim, Tehsil Kabirwala

065-2441056

Mian Channu ZTBL Mian Channu GT Road Mian Channu. 065-2664870

JhanianOpp.Govt.Degree College for Boys, Jahanian .

065-2210878

9 Sahiwal Arifwala Fausal Town 457832739

Total Br = 9 Bunga Hayat Adda Bunga Hayat Pakpattan Road 457520107

Chichawatni 6-E Housing colony 405485549Kassowal Zameer colony GT road 405410496Noor Shah Faisal Abad Road 404469133

Noorpur Adda Noor pur Pakpattan Road 404018025

Pakpattan 10-8 Green Town 457372187Qaboola Qaboola By pass 457851915Sahiwal 915-D Farid Town 409200424

10 Okara Okara 27-C Lala zar Colony 449200126Total Br = 7 Depalpur Khalil abad colony 444540988

Haveli lakha Dehli Multan Road 444775772Basirpur Committee Road 444771189Gogera Faisal Abad Road 442662030

Renala Khurd 6-B Low incom Housing scheme 442621212

Nol Plot Post Office, 12/GD 0442010810

11 Faisalabad Chak Jhumra Chiniot Road, Chak Jhumra 041-8763407

Total Br = 13 FaisalabadJail Road, Opp. Punjab Medical College, Faisalabad.

041-9210008

Gojra Samundri Road, Gojra 046-9200096

Jaranwala Faisalabad Road, Jaranwala 041-4310584

Kamalia Mal Fatiana Road, Kamalia. 0463-411525

Mamunkanjan Lakar Mandi, Mamunkanjan. 041-3431791

Pir Mahal Gala Mandi, Pir Mahal. 0463-360301

Rajana Town Canal Road, Rajana Town. 0462-262744

Samundri Main Faisalabad Road, Samundri. 041-3422395

Sandhilianwali School Road, Sandhilianwali. 0463-522048

Satiana Tadlianwala Road, Satiana 041-4600131

T.T. SinghHouse No.17 St.No.102 Housing Colony No.1, T.T.Singh

0462-510712

Tandlianwala Main Road, Tandlianwala 041-3441907

12 Jhang Jhang Ayub Chowk Jhang. 047-9200039

Total Br = 10 Shah Jewana Mandi Shah Jewana Road, Shah Jewana. 0477-641270

Athara Hazari Bhakkar Road, 18-Hazari. 0477-645209

Shorkot Cantt Road, Shorkot city. 0475-310584

Chiniot Faisalabad Road, Chiniot. 0476-332811

Garh Marharaja Garh Mor G.M. Raja. 0475-320578

Bhawana Old Bus Stand Chiniot Road, Bhowana. 0476-201039

Bhakkar Mandi Town near Jhang Moore, Bhakkar. 0453-9200437

Kalurkot Near Housing Colony, Kalurkot. 0453-200904

Mankera Mohallah Khiaran Wali, Jhang Road, Mankera. 0453-410055

13 Muzaffargarh Layyah TDA Colony Layyah 0606-412570Total Br = 11 Choubara Jhang Road Choubara 0606-440144

Karor Lal Easan Layyah Road Karor Lal Easan 0606-810574

Muzaffargarh Jail Road Muzaffargarh 066-9200207Khan Garh Ali Pur Road Khangarh 066-2610486

Ali Pur Circular Road, Near Fateh Pur Gate Ali Pur 066-2700140

Shahersultan Jatoi Road Shahersultan 066-2620055Jatoi Permet Road Jatoi 066-2591170Kot Adu G.T.Road Kot Adu 066-2242934

Sanawan G.T.Road Sanawan 066-2250028

Chowk Munda M.M.Road Chowk Munda 066-2210175

14 D.G.KHAN D.G.KHANMultan Road,opposite khayyaban-e-sarwar,D.G.Khan

064-9260419

Total Br = 6 TAUNSA SHARIFCollege Road,near Hashim chowk,Taunsa Sharif

064-2602451

KOT CHUTTA Indus Highway,Araien Market,kot chutta 064-2843551

RAJAN PUR Indus Highway,Juggan khan Market,Rajan pur 0604-688698

JAM PURIndus Highway,near boys degree college,Jam Pur

0604-567464

ROJHAN Near Police Station,Rojhan 0604-610044

15 Bahawalpur Ahmedpur East Kachari Road, Ahmedpur East 062-277820

Total Br = 8 Bahawalpur Main Ahmedpur Road, Bahawalpur. 062-9255303

HasilpurChishtian Highway Road, Mehmood Colony, Hasilpur.

062-2442582

Head Rajkan Near Green Market, Head Rajkan 062-2781666

Khairpur Tamewali Mouza Ghnipur, Khairpur Tamewali 062-2261590

Noorpur NourangaGanwar Shah Road, Khanqah Sharif, Distt: Bahawalpur

062-2790077

Uch Sharif Main Ahmedpur Road, Sami Town, Uch Sharif. 062-2551307

Yazman Lower Income Housing Scheme, Yazman. 062-2702733

16 Bahawalnagar Bahawalnagar

Kamboh House Degree College Road, Bahawalnagar.

063-2274443

Total Br = 5 ChishtianHouse No.39/GI, Balidia Colony, Chishtian

062-2502940

Minchinabad Pakpattin Sharif Road, near A.C.Office,

063-2750331

Minchinabad.Fortabbas Marot Road Fortabbas. 063-2510967

Haroonabad Bahawalnagar Road, Haroonabad. 063-2250941

SINDH

17 Karachi. Model Branch, Gulistan-e-Johar

St.4/3, Block No.1, Scheme No.36, Gulistan-e-Johar, Karachi.

0213-34613618

Total Br = 15 Karachi Branch, Shafi Court

Shafi Court Building, Merewether Road, Near Metropol Hotel, Karachi.

0213-99206006

Fish Harbour Branch.

Naghani Chamber, West Wharf Road, Karachi. 0213-32315339

Ibrahim Hyderi Branch.

679-B, Bhittai Colony, Ibrahim Hyderi Road, Korangi Crossing, Karachi.

0213-35120584

Memon Goth Branch.

Murad Memon Goth, Memon Goth Town, Malir Karachi.

0213-34560239

Deh Tore (Gadap) Branch.

Deh Tore, Near Baqai Medical University, Gadap Town, Super Highway, Karachi.

0213-37613037

Thatta Branch.

Main National Highway, Near National Bank Of Pakistan, Thatta Branch, District Thatta.

0298-923024

Mirpur Sakro Branch.

Mirpur Sakro Town, District Thatta. 0298-775016

Vur Branch. Post Office Vur Town, District Thatta. 0298-774037

Jati Branch.Raj Malak Road, Near Drainage Office, Jati Town, District Thatta.

0298-777044

Chouhar Jamali.

Shah Aqiq Road, Post Office Chohar Jamali, Taluka Shah Bunder, District Thatta.

0298-778076

Sujawal Branch. Near Qasmi Petrol Pump, Wapda Office, Sujawal Town, District

0298-510074

Thatta.

Mirpur Bathoro Branch.

Near Union Council Office, Mirpur Bathoro Town, District Thatta, Postal Code 73030.

0298-779216

Hub Chowki Branch.

Near Sher Ali Patrol Pump, Mooza Tathra, Hub City, District Lasbela.

0853-363474

Uthal Branch. Lasbela University, Uthal. 0853-610761

18 Hyderabad Hyderabad Banglow No 6-A, Unit No.7 Latifabad 022-9260058

Total Br = 14 Tando Jam Mir Colony Tando Jam 0222-765968

Matiari Main Rd. Opp. Govt. Boys High School 0222-760285

Hala National High way Rd. 022-3332142

Tando Allah YarPlot No.14, Zardari Colony Main Tando Adam Road

0223-891383

Tando M.Khan Station Rd. Near Masjid-e-Aqsa 022-3341356

Sehwan Sharif Aeroplane Chowk Main Road Hyderabad. 025-4620363

Kotri Darya Road, Kotri 022-3874230

Badin Al Aman Hotel,Near Bus Stand 0297-861291

Talhar Tando Bago Rd. 0297-830233Matli Hyderabad- Badin Rd 0297-840265

Golarchi Ward No. 2,Girls High School Rd. 0297-853116

Tando Bhago Hyderabad Road near Girls High School. 0297-854020

Tando Ghulam Ali Shahi Bazar Rd. 0297-851091

19 Nawabshah Nawabshah.Bunglow No. 1-A/2 Housing Society Nawabshah

0244-9370115

Total Br = 14 Dour Bandhi Road Dour 0244-325224

Sakrand. Muhalla Azim Colony, Main Road Sakrand 0244-322714

Qazi Ahmed National Highway Qazi Ahmed 0244-321284

Doulatpur Main Road Doulatpur 0244-320678Moro Near Session Court 0242-410626

Main Road Moro

Naushehro Feroze Opposite Wapda Colony Naushehro Feroze 0242-448883

Bhiriacity Bhiria Chowk Main Road Bhiriacity 0242-432232

Kandiaro Taluka Hospital Road Kandiaro 0242-449576

Mehrabpur Mallah Muhallah Mehrabpur 0242-430505

Dadu Shahani Muhalla Dadu 025-9200311Johi Wahi Pandhi Road Johi 025-4740258

Bhan Saeedabad Near Hotel Usman Solangi Bhan Saeedabad 025-4660389

Seeta RoadNear Bunglow Asif Khan leghari Seeta Road

025-4760088

20 Larkana MEHAR Akhound Muhalla Ghari Road Mehar. 0254730293

Total Br = 18 K.N.SHAH Near Mukhtiarkar Office Road K.N.Shah 0254720295

RADHAN Shahi Bazar Radhan. 0254750236

JACOBABADNear Saheed Allah Bux park Quatta Raod Jacobabad

0722653464

THULL Kandhkot Road Thull. 0722610269

SHAHDADKOT Old Anaj Mandi Shahdadkot 0744012788

KAMBER Larkana Road Kamber 0744210545

WARAH Gaji Khuhawar Road Warah 0744060230

MIROKHAN Main Road Mirokhan. 0744049320

KANDHKOT Near Main Bazar Kandhkot 0722573252

KASHMORE Soomra Muhalla Kashmore. 0722576613

DOKRI Moenjodaro Road Dokri 07454080296

LARKANAShaheed Benazir Bhutto Building VIP Road Larkana

0749410826

NAUDERO Opposite Govt.High School Nuadero. 0744047491

KHANPUR Main Road Khanpur 0726571025

SHIKARPUR S.P OFFICE ROAD SHIKARPUR. 0726920166

GARHI YASIN MARKET ROAD GARHI YASIN 0726572041

LAKHI Opposite Govt.Grils High School Lakhi 0726573035

21 Mirpurkhas MirpurkhasNear Chandni Chowk, Mirwaha Road Mirpurkhas

0233-9290192

Total Br = 14 Hingorno Main Khipro sindhri Road Hingorno 02355-22026

Digri Ward No.5 Gharibabad, Digri 0233-869642

Kot Ghulam Muhammad

Near Hashmi Masjid, K.G.Muhammad 0233-866431

UmerkotGulistan Saleem Near Rohal Bus stand Umerkot

0238-571230

Samaro Kunri Road Samaro 0238-551040

Pithoro Opposite Akri Jama Masjid Pithoro 0238-541556

Mithi Shoukat Manzil, Diplo Road Mithi 0232-261320

SangharNear Police Head Quarter, Hyderabad Road Sanghar

0235-542032

Kandiari Rural health centre Kandiari 0235-521101

Shahdadpur Near Hala Chowk, Shahdadpur 0235-841239

Sinjhoro Sanghar Road Sinjhoro 0235-531116

Tando AdamKhandoo Road Opp. Civil Court Tando Adam

0235-574328

KhiproNear Police Station, Taluka office Road Khipro

0235-879237

22 Sukkur Dharaki G.T Road Ghotki 0723-642577Total Br = 15 Pacca Chang Garibabad Mohallah a 0243-557020

Gambat Station R oa d. 0243-640970Agra Town Shahi Bazar, Agra Town 0243-780076

Ghotki Shanti Nagar Rahomowali Rd. 0723-681302

Khairpur Katchery Road Khairpur 0243-9280096Kingri Near Dargah Pir jo Goth 243-610110Kot Digi Main R oa d.Kot 0243-556359

Bunglow

Mirpur MatheloNear Sardar Rahim Bux Bozdar Bunglow M.Mathelo

0723-651680

Thari Mirwah Near DDO, Revenue Office 0243-790268

Chandiko(Nara) Near Mujahid Petrol Pump , Main Chowk 0243-559045

Pano Aqil Near Mukhtarkar Office, Pano Akil 071-5690547

Sohbo Dero Main Stand, New Evershine School 0243-750216

Sukkur Minara Road, Sukkur 071-9310303Ubauro Near Shah Petrol Pump 0723-688429

KHYBER PAKHTUN KAWAH

23 Peshawar Peshawar G.T.Road, Chughal Pura, Peshawar 091-2262279

Total Br = 20 BadaberScheme Chowk, Inqilab Road, Badaber, Peshawar

091-2324815

Bara Bara Gate, Bara Road,Peshawar 091-5253433

Nowshera Club Road, Nowshera Cantt. 0923-9220037

Charsadda Mardan Road, Charsadda 091-9220112

Tangi College Road Near Police Station, Tangi 091-6555263

Shabqadar Matta Road, Near GPO, Shabqadar 091-6281497

MardanCantt. Colony, Opp. G.P.O, the Mall Road, Mardan

0937-866404

Rustam Main Bazar, Rustam 0937-800183

ShergarhMalakand Road, Shergarh, Near Police Station

0937-820353

Katlang Inzergai, Mardan Road, Katlang 0937-575367

Takhtbhai Floor Mill Road, Takhtbhai 0937-552002

Swabi Jehangira Road, Jamal Abad, Swabi 0938-221244

Lahore Chota Jehangira Road, Opp. 0938-300065

Tehsil Office, Lahore Chota

Kohat House No.13, Sector-IV, KDA Gate-2, Kohat 0922-513743

KarakMain High Way, Opp. Ghalnai CNG, Tangori Chowk, Karak

0927-210549

B.D.Shah Opposite Police Station, Bannu Road, B.D.Shah 0927-333540

Hangu

Opp. Hangu Public School & College, Main Hangu Tall Road, Hangu

0925-621093

SaddaManan Market, Near UBL, Parachinar Road, Sadda

0926-520509

Parachinar Opposite Zanana Hospital, Parachinar 0926-310658

24 D.I.Khan BannuNear Regal Cinema, Miranshah Road, Bannu.

0928-622188

Total Br = 11 D.I.Khan Prova Adda, D.I.Khan. 0966-718225

DomailMuhammad Din Market, Kohat Road, Main Bazar Domail.

0928-653515

EssakhelAl-Assad Market, Mianwali Road, Essakhel.

0459-285020

Kulachi Inside Sheikhi Gate Kulachi. 0966-760363

Lakki MarwatMohallah Haqdad Abad near Bus Stand, Lakki Marwat.

0969-510586

Mianwali PAF Road, Mianwali. 0459-920091

Paharpur Rangpur Road, Paharpur. 0966-775341

Piplan Opposite Grain Market, Liaqat Abad, Piplan. 0459-201128

Serai NaurangD.I.Khan Road Opposite Police Graond, Serai Naurang.

0969-352261

TankHassan Market near Degree College(Male), Tank.

0963-512558

25 Mingora Batkhela Nera PESCO, Batkhela 0932-411792

Total Br = 15 Mingora College Colony, Saidu Sharif, Swat. 0946-9240183

Daggar Main Bazar Daggar 0939-555466

TimergaraBalambat Road, uposit Tablighi Markaz, Timergara.

0945-9250117

Chakdara G.T. Road, Chakdara. 0945-761178

Khar Near Scout Cant, Khar Bajaur Agency. 0942-220903

Alpurai Main Besham Road, Alpurai. 0996-850034

Dargai G.T. Road Dargai 0932-332043Dir G.T. Road, Dir. 0944-880822Matta Near Bus Stand, Matta 0946-790095Behrain Main Bazar Behrain 0946-780127

Chitral Governor Cottage Road, Chitral 0943-412624

Warijune G.T. Road, Warijun 0943-474014Booni Main Bazar Booni 0943-470032Drosh Main Bazar Drosh 0943-480208

26 Abbottabad Abbottabad PMA Kakul Road, Abbottabad 0992-9310152

Total Br = 7 Haripur Shakar Shah Road, Haripur 0995-610835

MansehraBedra Chowk, Main Shahrah-Resham, Mansehra

0997-305069

Oghi Kutchehry Road, Oghi. 0997-320106Balakot Main Bazar, Balakot 0997-500329

Battagram Main Karakuram Highway, Battagram 0997-310073

Dassu Kumela Bazar, Dassu. 0998-407105GILGIT - BALTISTAN

27 Gilgit-Baltistan GILGIT SADAR BAZAR,

GILGIT 5811920766

Total Br = 7 SKARDU YADGAR, CHOKE SKARDU 5815920268

GAHKUCH MAIN ROAD GAHKUCH 5814921020

ALIABAD MAIN ROAD ALIABAD 5813920804

ASTORE NEAR P.W.D OFFICE 5817920289

ASTORE