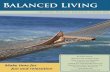

weabenefits.com 2013 SUMMER your insurance When a tree falls, who’s responsible? your retirement Does converting to a ROTH IRA make sense? your kiosk Vacation car rental: Are you covered? Last call for financial mentor nominations. } your $ ™ A magazine from WEA Trust Member Benefits GAUGING RETIREMENT READINESS

Yours magazine - Summer 2013

Mar 11, 2016

Gauging your retirement readiness; When a tree falls, who's responsible?; Roth conversion Q&A; Vacation car rental: Are you covered?

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

weabenefits.com

2013 SUMMER

your insuranceWhen a tree falls, who’s responsible?

your retirementDoes converting to a ROTH IRA make sense?

your kioskVacation car rental: Are you covered? Last call for financial mentor nominations.

}

your$™A magazine from WEA Trust Member Benefits

GauGinG retirement reaDineSS

president’s letterDave Kijek, President/CEO, WEA Trust Member Benefits{

2 weabenefits.com

© 2013 WEA Member Benefit Trust.All rights reserved.

Give us a piece of your mind…anytime.

Follow us.

3 YOUR ACCOUNT- Make IRA contributions the easy

way.

- Get “back on track” with financial seminars this summer.

4 YOUR MONEY- What’s the real retirement reality?

Member Chris Silver wants to know.

6 YOUR INSURANCE- Trees: Who’s responsible when a

tree falls and will insurance pay?

8 YOUR RETIREMENT- The Roth IRA conversion: What,

when, why, and how.

4

your$CONTENTS SUMMER 2013

{

10 YOUR KIOSK- Does my existing policy cover a

vacation rental car?

- Public adjusters: Buyer beware.

- Scholarships awarded.

- Last call for financial mentor nominees.

™

6

Our organization is passionate about helping Wisconsin public school employees become financially secure. The purpose of this magazine is to provide information that will help you make sound financial decisions.

We often do this by sharing member stories that we think will encourage others. We recently received a call from Chris Silver, a participant in our 403(b) program who

felt we were missing the mark. In general, Chris said the member

stories didn’t reflect his situation and that he was having a hard time relating. In particular, he felt we may have given readers a false sense of when they could or should expect to retire. He suggested we may actually be putting people off instead of encouraging them.

This wasn’t an easy thing to hear, but he had a point. The landscape is different now. Wisconsin public school employees have been hit hard by district budget cuts and other economic conditions, and there’s a lot of uncertainty. We took the

opportunity to address the issues and concerns that are top of mind for Chris in the article on page 4. Chris’s feedback and willingness to help us out is much appreciated.

This is an open invitation to all readers to tell us what you think and what you need. We are all ears.

8

3

{weabenefits.com

{ your accountIRA and 403(b) NewsEasy, budget-friendly IRA contribution

Are you contributing to your IRA the hard way by sending checks sporadically throughout the year, or worse, trying to come up with a large amount just before tax day?

There is an easier way…SmartPlan. SmartPlan breaks down your annual IRA contribution into smaller, more manageable amounts that are automatically made to your IRA account from your checking or savings account.

For more information, please call us at 1-800-279-4030 or go to our Web site at weabenefits.com and search “smartplan.”

Even better, if your district participates in our Trust Advantage™ program, you can payroll deduct your IRA contributions. It doesn’t get any easier than that! Contact your business office for details.

Retired or changed jobs? If you have a 403(b) or an IRA with us, you can keep it here regardless

of your employment status or district decisions about health insurance or other group plans. Call us if you have questions.

New address? Let us knowIf you have recently moved or have plans to move this summer, please let

us know your new address.

• Contact us directly at 1-800-279-4030 or log into your WEAccess account to change your address on your retirement savings accounts.

• If you also have your auto or homeowners insurance with us, you can use our online Update Your Policy application or call 1-800-279-4010 to make the change.

Increase your 403(b) contributionsNow is a good time to update your Salary Reduction Agreement (SRA)

to take advantage of new 2013 403(b) contribution limits. Do it now and you’ll be ready to go for the school year. To obtain an SRA for your district, you may print one from our Web site at www.weabenefits.com or call us at 1-800-279-4030 and we’ll send it to you.

The Trustee for the WEAC IRA program is First Business Trust & Investments. The 403(b) retirement program is offered by the WEA TSA Trust. TSA program registered representatives are licensed through WEA Investment Services, Inc., member FINRA.

Content in this magazine is for informational purposes only and not intended to be legal or tax advice. Consult your tax advisor or attorney before taking any action.

SUMMER SEMINARS

Your Road Map to $ucce$$

Free Financial Seminars

Your Road Map to

There’s still time to register. Seminars run through

August 8.

Award-Winning

Don’t Be Jack™ Game

Understanding Long-Term

Care Insurance

Back on Track for a

Secure Retirement

Registration and information at:

weabenefits.com/roadmapor 1-800-279-4030, Ext. 8563

weabenefits.com4

Act 10 has started to take its toll and while all Wisconsin public school employees will be financially impacted by Act 10, those in Chris’s age group—between 45 and 55—are hardest hit.

A c t 10 reduced salary and benefits at a time when this group s h o u l d be at their peak earning and saving. “Their younger colleagues have time to adjust their strategy to fit the new reality, and those over 55 are more likely to be taken care of by benefits that are still in place,” Michelle says. In addition to the added financial burden resulting from Act 10, this group also experienced two significant market crashes during their savings years.

The combination of these economic events puts a lot of pressure on current and future finances. If you find yourself in this

C hris Silver is a teacher in River Falls and a participant in our 403(b) program. He called us concerned that we were sending the wrong message to our

readers. Chris observed that our member stories of late tended to be about educators who retired early…in their 50s. “I find it discouraging because it makes me feel that if I can’t retire early, I’ve failed somehow. Don’t get me wrong, I think it’s great that they found a way to do it, but I just can’t relate.”

He had a point. While we have written articles about a variety of topics—taking care of elderly parents, finding a financial planner, keys to retirement satisfaction—many of our stories have featured members who retired before age 65. As a result, we may have unintentionally conveyed a false sense that this is the retirement norm.

Chris, 51, went on to say that with all the economic pressures, he wonders if he’ll ever be able to retire. “I know I’m not alone. I have friends and colleagues who are concerned as well. I think it would be helpful to know what we can reasonably expect.”

It was an eye opening conversation. We thought we were inspiring people by sharing success stories, so it was a little hard to hear that we might actually be putting people off.

The story unfoldsChris agreed to share his list of concerns

and questions that contribute to his low expectations for retiring with Michelle Slawny, a Certified Financial Planner® and Worksite Benefit Consultant for Member Benefits. Michelle has worked in the financial services industry since 1994, and she has completed more than 500 retirement plans for Wisconsin public school employees over the last five years. She confirms that those who are able to comfortably retire in their 50s are more the exception than the rule.

“The reality is that most Wisconsin public school employees are not financially prepared to retire in their 50s,” she says.

This jibes with national trends as well. A May 2013 Gallup research study found that the average retirement age in the U.S. has risen from 57 in 1991 to 61, and the average nonretired American now expects to retire at age 66.

{ your money

GauGinG retirement reaDineSSNot everyone can retire early. In fact, most people can’t. ACT 10 and other economic pressures muddied the waters for Wisconsin public school employees—especially for those between age 45-55. Many wonder where they stand and what they can do to salvage their retirement dreams. But, it may not be as bad as you think.

Every little Bit helps

I started saving late. My balance is unimpressive. Why bother?

DEBT HAPPENS

I’m uncomfortable with debt. It’s weighing on me.

ACT 10 and other economic pressures are taking a toll.Ages 45-55 are most impacted. But, there’s still time to adjust.

TIME TO GET A PLAN!

5

situation, however, there are still plenty of choices you can make to maximize your retirement security. Let’s take a look at some of Chris’s concerns.

Debt happensDebt is a reality for most of us. It’s hard

to avoid borrowing money for large ticket items such as homes or cars. But, debt and retirement don’t go together. As you move closer to retirement, you need to be thinking about retiring your debt as well. Ideally, you want to go into retirement debt free.

“Most Wisconsin public school employees in their late 40s to early 50s have debt—a mortgage, varying degrees of credit card debt, and some have home equity loans,” Michelle acknowledges.

“These are the years to pay down debt, not accumulate,” she says. But, unexpected home or car repairs or other costly items like appliances or medical costs can make it easy to build up credit card debt, if you don’t have an emergency fund to tap into.

The reduction planAttack any credit card debt first because

credit cards tend to carry the highest interest. Use a calculator, such as the Credit Card Paydown calculator at weabenefits.com, to come up with a payment plan that’s realistic and doesn’t compromise your other financial obligations.

Finding the extra money to pay down your balance may require a closer look at your spending habits in order to balance the household budget.

“Once the credit card is paid off, immediately redirect that money to any other debt such as a home equity loan. Do not let it work back into your household budget,” Michelle urges.

Reward your achievementsPaying off debt is like dieting. It’s not

fun and it might take a long time before you reach your goal. However, depriving yourself of all the joys of life isn’t realistic

or healthy either, and it may jeopardize your long-term goals. “Everything can’t be for the future,” Michelle says. “Find a good recipe that allows you to live for today while preparing for the future.”

Michelle suggests breaking the big goal of eliminating debt into smaller milestones and setting up a reward system. “Maybe you take a vacation after paying off your credit cards. It doesn’t have to be an expensive trip, but it will give you something to look forward to. It’s important to take time to enjoy your family, relax, have fun, and make memories.”

Retirement savings: Why bother?

For Wisconsin public school employees who retire after 30 years of service, at least 25% of your retirement income will likely be funded by personal savings from an IRA or 403(b).

Those in their late-40s or 50s who haven’t done much saving on their own (or haven’t started) often question whether it’s worth it this late in the game. Michelle says, “Yes. It absolutely is worth it.”

While starting early is best, the old adage of better late than never rings true. Even if you can only contribute a small amount, some is better than none.

Retirement savings vs. debt“People are often conflicted between

saving for retirement and paying off debt. ‘Wouldn’t it be better to put all my money toward my debt?’ Generally, the answer is no,” Michelle says. “This financial game is about balance. It is important to eliminate debt but equally important to build up the nest egg. If you focus 100% on eliminating debt, you are sacrificing the nest egg. So continue directing money to your 403(b) or IRA.”

Michelle says another reason to continue regular contributions is that when you are saving you are learning to live on less

than you make. “If you are putting $100 a month into a 403(b), you learn to live without the $100. It’s $100 you are not spending. So when it comes time to retire, that’s $100 you don’t need to replace.”

Take opportunities to save moreAs you pay off a loan, an expense goes

away or is reduced, you get a little bump in pay…redirect it to your retirement savings. “Even small amounts add up. Twenty dollars here, $20 there. Don’t bend to the notion that ‘it’s too small to matter.’ It does,” Michelle encourages.

Remember, when you retire you don’t save any more. Saving now builds that extra source of retirement income and teaches you to live on less.

Health insurance: Retirement deal breaker

The biggest unknown with retirement before age 65 (the age at which Medicare currently kicks in) is the cost of health insurance. If we don’t have a better system in place by the time you retire, health insurance may be the biggest expense you have to prepare for. Michelle tells participants to expect to pay anywhere from $12,000 to $20,000 per year for insurance depending on the level of coverage you choose and whether you have an individual or family plan. Having the extra savings in a 403(b) or IRA could mean the difference between retiring early or needing to work to 65.

Kids are great

They are also expensive. According to the U.S. Department of Agriculture, which has been tracking the cost of raising a child since 1960, middle-income families (incomes between $59,000 and $103,000) with a child born in 2011 can expect to spend roughly $235,000 over 17 years. That cost factors in food, shelter and other necessities to raise a child, and does not account for inflation. It also doesn’t include the cost of college.

I have three kids at home. How should I fund their college?

FUND RETIREMENT FIRST

KIDS

How do I fund my retirement and college for my children?Don’t sacrifice your retirement to give your kids a free ride.

FUND RETIREMENT FIRST

FUND RETIREMENT FIRST

I have three kids at home. How should I fund their college?

Every little Bit helps

I started saving late. My balance is unimpressive. Why bother?

I’m uncomfortable with debt. It’s weighing on me.Debt and retirement don’t go together. Reduce debt now.DE

BT

PLAN TO BE DEBT FREE

weabenefits.com

My WRS statement is depress-ing. Will I ever be able to retire?

PROJECTING BENEFITS

I started saving late. Is it worth it to keep funding my 403(b)?Saving builds your nest egg and teaches you to live on less.SA

VING

BETTER LATE THAN NEVER

What we coverTree removal is covered

on a Member Benefits home insurance policy for trees, including those downed due to wind or hail, up to $1,500. Most companies will pay only a minimum amount (usually $250) to remove downed trees that do not cause other property damage, and will pay a higher amount (usually $500) if the downed tree causes damage to your house or other structure. “Our coverage is unique in that we pay to remove the tree, period,” says Bob Manor, Claims Manager at WEA Trust Member Benefits. “We don’t make distinctions about where it hit, what it damaged, etc. If a tree from our insured’s property fell, we will pay to have it removed.”

If you have extensive landscaping including ornamental trees, shrubs, and plants, your Member Benefits homeowners insurance policy may include some coverage for certain losses due to fire, lightning,

Trees are a beautiful addition to your yard-they bring shade, privacy, wildlife, and add value to your property. They are an

investment and can be expensive: from the purchasing, to the maintaining, to removal and replacement, there are costs all along the way.

In addition, trees are sometimes the cause of disputes and lawsuits between neighbors, especially after one falls and damages property. Knowing whose responsibility it is to clean up after tree damage, how to maintain healthy trees to minimize your risk, and what protection your insurance offers is helpful before an incident occurs.

Who’s responsible when it’s ... >your tree, your property

Generally speaking, if a tree falls in your yard and causes damage to your home or other insured outbuildings, your homeowners insurance will pay for damages up to your policy limit, as long as it fell because of a covered loss.

If a tree falls on your car, the damage would typically be covered by your auto insurance policy’s comprehensive coverage.

If your tree falls in your yard but doesn’t damage your home, car or another

building, most insurers provide only $250 to $500 in coverage for this. However, if your homeowners insurance is with Member Benefits, we will cover the cost of removing the tree—up to $1,500—subject to your deductible.

Tree removal can be pricey depending on the size of the tree, its location in your yard, and whether or not any parts of the tree interfere with structures, utility lines, etc. Often stump removal, grinding, clean-up, and re-landscaping of the area is extra and not included in the cost to remove the tree, which can be upwards of several thousand dollars.

>your tree, your neighbor’s propertyIf your tree falls on your neighbor’s home

or neighbor’s property, your neighbor’s insurance policy would cover the damages.

Likewise, if your neighbor’s tree falls on your property and damages your home, your homeowners insurance coverage pays for it.

However, the major exception to this rule is in the case of negligence by the tree owner. If the tree wasn’t properly maintained—it was diseased, dead, and posed an imminent hazard-and the tree owner knew about it, they may be at fault.

6

{ your insurance

If a tree falls…

7

explosion, riot or civil

commot ion , and aircraft.

Coverage also includes damage done by

vehicles, vandalism, or theft.

What’s not coveredGenerally, insurance companies

do not cover damage caused to trees by heavy snow or ice build-up. Also, if a tree falls down because of rot or disease in absence of a storm, it’s not covered.

To mitigate a potential hazard, inspect your trees annually to safeguard against common problems and hire a certified arborist if you think you have a troubled tree. Proper maintenance of your trees will help extend their life and ensure a beautiful addition to your landscape for years to come.

Certain policy exclusions and limitations may apply. The terms and conditions of your coverage are exclusively controlled by your written policy. Please refer to your policy for details. Underwritten by WEA

Property & Casualty Insurance Company.

When a tree falls

Tree care tips

Homeowners insurance policies generally hold you (the insured) responsible for mitigating loss. So, if a tree falls and puts a hole in your roof, you must take action. Cover the hole or make a temporary fix to prevent further loss until it can be professionally repaired. Contact your insurance company to report a claim as soon as possible and confirm their expectations for mitigating loss and reimbursement. Be sure to keep your receipts for any expenses related to the repair, because your insurance company may reimburse you.

weabenefits.com

“The true meaning of life is to plant trees, under whose shade you do not expect to sit.”—Nelson Henderson

Trim trees in late fall or early winter while they’re dormant. This minimizes the risk of fungus and insect infestation.

To protect trees from storms and wind, remove outer branches from the end of long limbs while retaining the interior branches.

Remove branches and limbs that touch your roof or gutters.

Call an expert—a certified arborist—to prune large trees or to remove trees you think may have succumbed to disease or insect infestation.

The average cost for trimming a mature tree is $250–$500.

Carefully survey the area for downed power lines or other hazards.

Assess the damage and call your insurer right away. Your insurer should explain what action if any you need to take.

Take photos.

Call the power company if the tree is hanging over or touching wires.

When hiring a tree service company, make sure they are insured and bonded and provide you with a written guarantee for the work that will be performed.

7

8

{ your retirement

roth ira conversions

If you have saved for retirement in a pretax retirement account (Traditional IRA, SEP, Simple IRA, 403(b), 401(k), or 457 plan), you may have the option to convert some or all of your pretax dollars into a Roth IRA.

Is converting to a Roth IRA a good idea? It depends. Here’s what you should know before you decide.

Pretax IRA vs. Roth IRA Traditional IRAs and other pretax

accounts allow you to defer the taxes on your contributions and at the same time reduce your taxable income. The earnings grow tax-deferred but both the earnings and initial investment will be taxed when withdrawn.

Roth IRAs allow for after-tax contributions. You pay taxes now in exchange for tax-free treatment of earnings on qualified withdrawals.

What is a Roth conversion? Converting to a Roth means changing

the tax treatment your retirement savings will be subject to upon withdrawal. You will be undoing the original tax-deferral by paying tax on the contributions that were made pretax as well as the accumulated earnings. This process converts the funds into after-tax money.

What’s involved in a conversion? Converting to a Roth IRA is fairly

simple. Ask your pretax retirement account provider to convert some or all of your pretax funds to a Roth.

You will likely be able to keep your funds at the same financial institution and in the same investments if you choose. However, you may be able to reduce your account fees by switching to another provider.

For instance, a WEAC Roth IRA through Member Benefits has one low fee with an annual fee cap. Call us to find out if you’re eligible to convert your pretax retirement account from a different provider to the WEAC Roth IRA.

Is it all or nothing? No. You can convert none, some, or

all of your pretax savings. You should consider:1. What the tax cost of converting to a

Roth will be. 2. Whether converting to a Roth will save

or cost you money over the long-run. 3. How much you should convert.

Is converting it worth it for me? Most sources of retirement income for

Wisconsin public school employees will be taxed in retirement. Roth savings can help diversify your tax liability in retirement. It may be worth converting to a Roth IRA if:• You have funds (outside of a retirement

account) to pay the tax for converting to a Roth.

• The value of your pretax retirement accounts has fallen, making converting more affordable.

• You expect to be in the same or a higher tax bracket in the future than you are in today.

• You can utilize losses, deductions, or credits to help offset the tax impact of a Roth conversion.It may not be a good idea to pay tax now

at a higher tax rate if you reasonably expect

to be in a lower tax bracket in retirement or if you might need to tap into those funds in the next five years. Converted money withdrawn before five years or age 591/2 may be subject to the IRS 10% early withdrawal penalty. Earnings withdrawn before five years and age 591/2 may be subject to taxes and a penalty.

You may also want to keep estate planning in mind when considering a Roth conversion. When a beneficiary inherits a Roth IRA account, he or she does not pay income tax on withdrawals. If a person inherits a pretax IRA, that person is subject to income taxes (at his or her tax rate) on withdrawals, because inherited pretax IRAs cannot be converted to Roths. If you don’t anticipate needing the funds and want to provide for your heirs, you may want to take this into account when making your decision.

What should I do next if I am considering a conversion?

Take advantage of our Roth conversion calculator at weabenefits.com, to help you decide if a Roth conversion is right for you. If you have questions about Roth IRA conversions, contact us at 1-800-279-4030, and we’ll help you sort out the details. Be sure to consult your tax professional to ensure you fully understand any tax consequences that may apply.

The Trustee for the WEAC IRA program is First Business Trust & Investments. This article is for informational purposes only and not intended to be legal or tax advice.

imPOrtant: Know the deadlinesConversions need to take place before December 31 to apply to

that tax year. However, you must give your institution lead time to process your request. We recommend starting early. If your account is with Member Benefits, you must have the completed form to us by December 13 of this year.!

Questions and answers

weabenefits.com 9

continued from page 5future monthly benefit would be if you continued to work in public service until you retire.

The footnote in Section 10 states: *These unofficial amounts do not reflect future benefits. They are based on your account balance as of January 1.

For the purposes of projecting your future WRS state pension benefit, your three highest years of earnings, total years of service, and your age are used.

To project your future retirement benefits, visit the WRS Retirement Benefits Calculator at etf.wi.gov/calculator.htm.

So...is retirement doable?Michelle took a look at Chris’s specific

situation, his debt, savings, WRS and Social Security projections, as well as his family situation. “Chris is pretty typical,” she said after her analysis. “Will he be able to retire at 57? No. Sixty-two would be a stretch, but possible. I think 64 is very likely.”

Chris was happy to have some answers and now has a more realistic picture of what he can expect in terms of retirement.

“Michelle shed light on my situation and it’s not as hopeless as I thought. I feel better knowing that those who retire early and are truly financially prepared for it are the exception, not the norm.”

How about you?You still have options for securing your

retirement even if it’s not that far away. If you have questions about what you could be doing at various stages of your career to ensure a comfortable retirement, plan to attend our Back on Track to a Secure Retirement seminar this summer. We’ll address questions and concerns about retirement benefits and address some of the challenges Wisconsin public school employees are facing. Go to weabenefits.com/roadmap to register.

Looking for more help? Take advantage of our financial planning services which offer services designed for every stage of life. Go to weabenefits.com/fps to check them out.

{

{

When it comes to funding college…don’t sacrifice your own financial situation in an attempt to give your kids a free ride.

Your kids can fund college with loans, scholarships, grants, and their own hard-earned cash, but there are no loans to pay for retirement. Michelle suggests you set up 529 savings accounts for your kids. “You can do that with just $20. Then encourage relatives to make contributions in lieu of holiday gifts.”

Not surprisingly, the size of your family factors into the when and how of your retirement plans. Additionally, the age at which you have your children also matters. “If you have kids later in life, and many people do, you can’t expect to retire at 55. It’s not likely to happen. Children are great—I have three of my own—but they are expensive and you need to be realistic about the impact that will have on your personal finances and your retirement timeline,” says Michelle.

Hopefully your children will be on their own when you retire, so you will no longer have the related expenses.

WRS: Confusion in Section 10When the Wisconsin Retirement

System was created, its purpose was to replace half of the employee’s ending salary, assuming 30 years of service and at least 57 years of age. It’s a nice benefit.

However, Michelle notes that people are often disappointed when they get their WRS statement from the Employee Trust Fund because they misinterpret the information in Section 10: Retirement Benefit Projection. “They think it reflects what their monthly benefit will be when they retire because it’s titled “Retirement Benefit Projection.” In reality, the numbers in Section 10 are real time— assuming that you stopped working on January 1 of the statement year, it reflects an estimate of what you would get at your current age or 65. It does NOT represent what your

TIME TO REASSESS

ACT 10 and other economic pressures are taking a toll. I don’t see how I will ever retire.

My pension benefit statement is discouraging. Statement information is often misinterpreted. W

RS

LEARN ABOUT WRS

PROF

ILE

This article is for informational purposes only and not intended to be legal or tax advice. Consult your tax advisor or attorney before taking any action.

All investment advisory services are offered through WEA Financial Advisors, Inc.

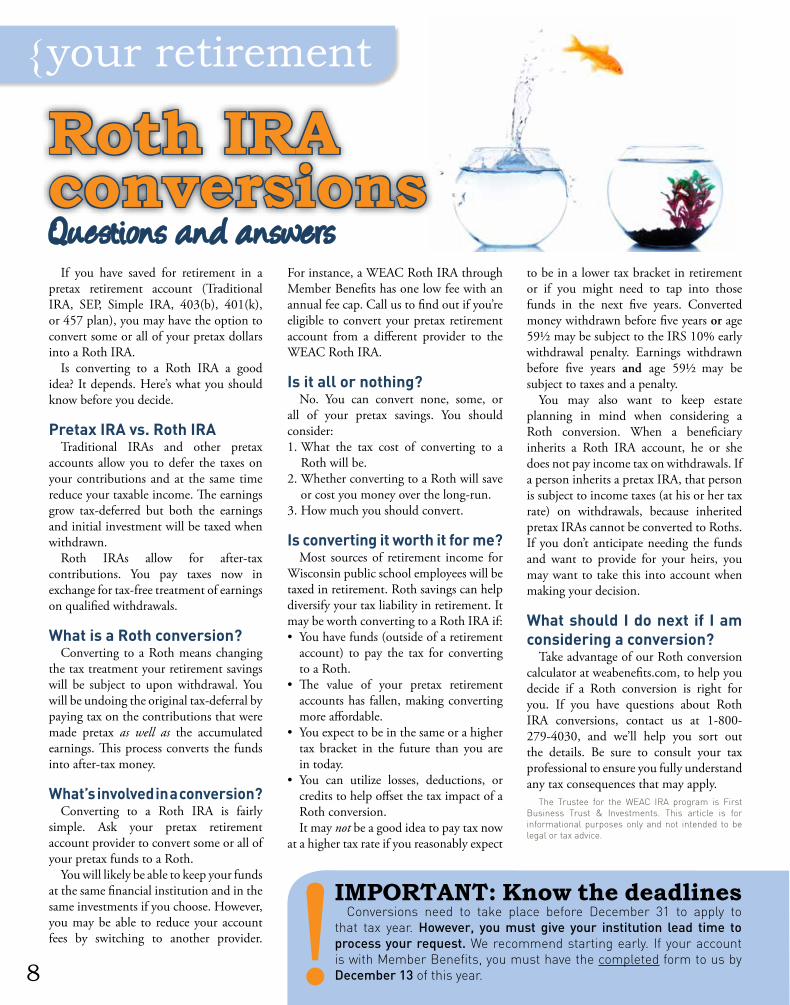

Chris Silver has been teaching business education at River Falls High School for the past 13 years. He spent the nine years prior teaching in Minnesota and working as a professional musician.

Chris and his wife Naomi live in River Falls. He has four children ages 24, 15, 13, and 9.

Chris enjoys playing guitar, mandolin, and fiddle, and he is particularly fond of bluegrass and folk music.

Hiking, fly fishing, and snowboarding with his boys are also on his list of favorite things to do.

WHAT’S YOUR STORY?Do you have a question, concern, or topic you’d like us to write about? Send your ideas to [email protected]. Type “your$” in the subject line.

Or, call us at 1-800-279-4030 and ask for communications.

Sometimes public insurance adjusters troll for claims—they call you out of the blue or come wandering through the neighborhood after a damaging storm. The sales pitch often includes a promise to get you a bigger settlement, they’ll settle your claim faster, take care of all the paperwork, and negotiate with the insurance company and contractors on your behalf.

“Be aware, if you decide to hire a public insurance adjuster to help you through the

process, you are obligated to give a portion of your insurance settlement to the adjuster, leaving less for your repairs,” says Bob Manor, Claims Manager for WEA Trust Member Benefits. It’s not unheard of for a public insurance adjuster to take a hefty fee—between 10%–20%—of your claim settlement.

If you consider hiring a public insurance adjuster:• Carefully read and understand the

terms and obligations in the contract—

Filing a claim for a large insurance loss can cost you a lot of time and energy, so some people decide to hire a public insurance adjuster to help negotiate with their insurance company on their behalf. On its face, working with a public insurance adjuster sounds like it might be a good idea, but buyer beware. If you find yourself in a situation that you feel may be better handled by a third party, there are a few things you should know before hiring a public insurance adjuster.

What is an insurance adjuster?An insurance adjuster is the person who

evaluates losses and settles policyholder claims. Typically, they are either employed solely by the insurance company or they are independent professionals under contract with one or more insurance companies. Public insurance adjusters are hired by and work only for the consumer or homeowner.

An unregulated riskWisconsin is one of only a handful

of states that does not require public insurance adjusters to be licensed. This creates a host of problems for uninformed consumers.

People tend to hire a public insurance adjuster after they’ve experienced a large or catastrophic homeowners loss.

Here’s the skinny on public insurance adjusters

Wisconsin is one of only a handful of states that does not require public insurance adjusters to be licensed.

sometimes these contracts can be difficult to cancel without penalty or obligation after you’ve signed.

• Look out for public insurance adjusters who also work as contractors, or insist on using a specific contractor, this can be a conflict of interest.

• Pay attention to who will receive the payment from the insurance company. Some public insurance adjusters will include a provision in the contract that requires the insurance check to be made out to them.

• Know your homeowners insurance policy—what’s covered and what’s not—to avoid any surprises down the road.

• Do your due diligence to make sure you are working with someone who has your best interest in mind.

Call usIf your insurance is through WEA Trust

Member Benefits and you experience a major claim, be sure to call us first before hiring a public insurance adjuster. We will help you sort out the details and handle your claim fairly, accurately, and promptly, or we’ll refund up to $250 of your deductible—it’s our claim service guarantee.

10 weabenefits.com

{ your kioskDoes my existing policy cover a vacation rental car?

In some cases, the coverage and deductibles you have on your personal auto policy would apply to a rented vehicle. To be adequately covered, your existing policy should include liability, comprehensive, and collision coverage. Check with your credit card company to see if they provide coverage. Also, consider taking the extra Collision Damage Waiver offered by the rental car company, as it relieves you of financial responsibility if your rental car is damaged or stolen. The waiver covers “loss of use”—the money a rental agency loses when the vehicle can’t be rented due to damages. It may also include “diminished value” protection to cover claims for the reduced value of the vehicle after a loss. In most states, your personal auto insurance policy won’t cover these costs, so you should consider taking the added protection.

Have more questions about coverage? Call us at 1-800-279-4010.Certain policy exclusions and limitations may apply. The terms and conditions of your coverage are exclusively controlled by your written policy. Please refer to your policy for details. Underwritten by WEA Property & Casualty Insurance Company.

Q:

Sylvia Johnson • MilwaukeeMath Teacher

Sylvia works at Transformation Learning Community High School and has taught math in the Milwaukee Public School District for 24 years. She plans to attend all three NIFEL courses this summer. Sylvia believes that when students have the right tools early enough, they will become good stewards over their finances, and that will impact those around them. “I feel so blessed and honored to be a recipient of this scholarship,” says Sylvia.

Stephen Zittlow • BrodheadMath Teacher Stephen has worked in the Brodhead School District for 11 years. He is interested in learning new ways to teach his students the financial implications of starting a business, financial contracts and paychecks, and how mathematics is applied in these situations. Stephen says, “This scholarship shows me that Member Benefits’ programs are truly designed to benefit the members. I appreciate their

{

{WEA Trust Member Benefits is pleased

to award scholarships once again this summer to four attendees of the National Institute for Financial and Economic Literacy (NIFEL) program hosted by Edgewood College in Madison.

The NIFEL program provides educators with the tools and expertise they need to teach personal finance in the classroom, with seminars on basic to advanced financial topics. The goal is for future generations to become better prepared to make sound financial decisions.

Sherri Hendrickson • MonroeBusiness and Information Technology Teacher

Sherri has been at Monroe High School for 13 years and a teacher for over 28 years. She has attended the NIFEL program in previous years and found the courses to be some of the most valuable she has ever taken. “I’m really looking forward to attending the Credit and Money class. I’m hoping to network with industry and education professionals and gather resources to help my students better understand financial topics.”

assistance to help me become a better teacher.”

James Sachs • MarshfieldMath Teacher

James is finishing his 23rd year of teaching and is currently at Marshfield High School. He is accumulating credits for relicensure and is looking for new ways to enhance his financial literacy projects. James says he is “going to enjoy being the student for a change.”

Educators receive scholarships from Member BenefitsSupport offered to further financial literacy in schools

Who’s your financial mentor?Last year, 11 public school employees were nominated and received

our Financial Mentor Award (see the Spring 2012 your$™ magazine). These individuals were recognized because they take the time to give financial encouragement, advice, and guidance to their colleagues.

Chances are you know someone in your district who goes the extra mile to help others build financial security. Or maybe it’s you!

Take a minute to submit your nomination(s) for the 2013 Financial Mentor Award. They will be mentioned in the next your$ and will receive a certificate of recognition. Go to weabenefits.com/mentor.

WANT MORE:For more information about NIFEL educational opportunities, visit wdfi.org.

{

Nominations due September 3, 2013.

11

PRESORTED STANDARD

US POSTAGE PAID

MADISON WI PERMIT NO 2750

PO Box 7893, Madison, WI 53707-7893

NO GIMMICK!

At MEMBER BENEFITS, there’s…

Simply better insurance.We’re the real deal.

Real people helping Wisconsin public school employees become financially secure.

Underwritten by WEA Property & Casualty Insurance Company.

Let us help you find the right balance between protection and price.

1-800-279-4010 • weabenefits.com/getaquote

DOUBLE CHECK

Related Documents