Non discriminati on between countries: THE MFN TREATMENT. FREE TRADE Through Negotiation. Non discriminati on within a country: NATIONAL TREATMENT PREDICTABILI TY : Through binding COMPETITIO N w w w . S t u d s P l a n e t . c o m

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ww

w.S

tudsP

lanet.co

m

Non discrimination

between countries:THE MFN

TREATMENT.

FREE TRADE Through

Negotiation.

Non discrimination

within a country:

NATIONAL TREATMENT

PREDICTABILITY :

Through binding

COMPETITION

ww

w.S

tudsP

lanet.co

m

MFN TREATMENT : Every member has to be treated equally with out any discrimination. If a member grants favour ie., lowers Customs Duty rate for a product favoring one country, then same lower duty should be applicable to all other W.T.O members .favour one favour all.

For example BANANA WAR.

*The EC (European Community) charged lower duty on bananas imported from AFRICIAN CARIBBEAN PACIFIC (ACP) , when compared to duties levied on bananas from Americas.

*The complaining countries were the United States , Ecuador , Guatemala & Honduras besides Mexico.

ww

w.S

tudsP

lanet.co

m

INTRODUCTION:

The dispute evolved in EU’s 1993 Regulatory Regime for banana imported into EU. E.U wise Banana Trade Regime had a system of a Tariff Rate Quota (TRQ) based on the Country of Origin. Bananas from the ACP countries had duty free entry into the EU up to 85,77,000 metric tons . This quota was allocated to each of producing countries on the basis of their historic exports to EU. While ACP Bananas , in excess of quota, were levied 750 ECU per metric tons . Non –ACP bananas wear subjected to a duty of ECU 100 per metric tons on imports of up to 2 million metric tone and ECU 850 on imports of above the amount .

ww

w.S

tudsP

lanet.co

mThe dispute was between two powerful members of QUAD (US,EU,JAPAN and CANADA) who were confronting each other from the area of currency trade (Euro vs US$ ) to Military Understandings .

Some members of the EC appear to be inclined towards the belief that countries can flourish more in Bipolar World than Uni- polar one .

The dispute involved article 1 of GATT 1994, the Most Favored Nations

The DSB’s Appellate Body , hearing the dispute in 1997, indicated that the MFN philosophy transcended any Preferential Trade Agreement or understanding that contracting parties might have out side the WTO agreement . The Appellate Body did not agree with EC’s stand that Preferential Trade with African countries .

Aligned with the main complaint , the United States , wear as in the days of small countries like Ecuador , Guatemala & Honduras. The only big member in this group was NAFTA member, Mexico.

ww

w.S

tudsP

lanet.co

m

ABOVE 85,77,000

750 ECU/PMT

AFRICAN CARIBBEAN

PACIFIC (ACP)

UPTO 85,77,000

ZERO DUTY

CEILING

DUTYENTITLEMENT

ww

w.S

tudsP

lanet.co

m

CEILING

DUTYENTITLEMENT

NON- ACP COUNTRIES

UPTO 20,00,00

0100

ECU/PMT

ABOVE 20,00,00

0850

ECU/PMT

ww

w.S

tudsP

lanet.co

m

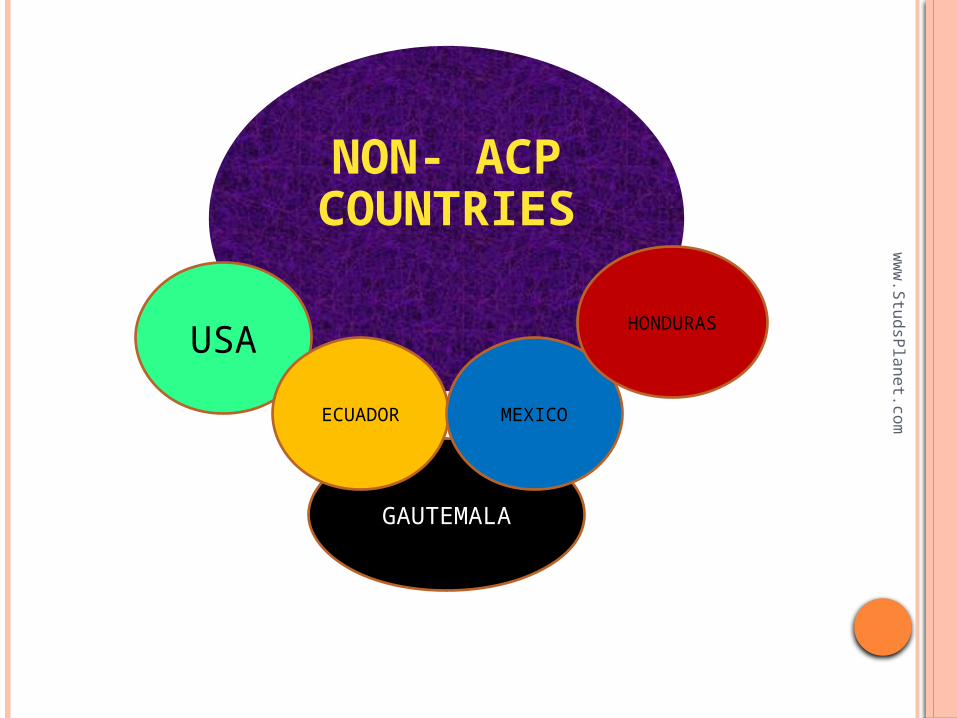

NON- ACP COUNTRIES

GAUTEMALA

USA

ECUADOR MEXICO

HONDURAS

ww

w.S

tudsP

lanet.co

m

1993 May 19 GATT panel finds against EC member state restrictions (banana-1)EC blocks the panel report from being adopted by GATT council

1994 Jan 18 GATT panel finding go against EC’s new regulations 404 (banana-2)

1994 Feb 07 EC blocks the (banana-2) panel report from being adopted by GATT council

1995-1996 New WTO dispute settelment provision prevents one member from blocking panel findings in 1995 . In 1996 equdor , guatemala & honduras and US (g-5) bring formal WTO cases

1997 May 22 WTO panel finds many goods and services violation of EC regime (banana 3 )

1997 Sept 9 WTO panel body up holds the findings of EC

1997 Spt 25 WTO dispute body adopts panel and appellate body reports

1998 Jan 08 WTO arbitrator gives until jan 1, 1999 . to complys WTO ruling

1998 June 26

European agriculture adopts modification to banana measures and unilaterally declares them WTO conistent.

1998 Dec 18 Ecudor request re-establishment of original panel to acess weather EC measures are WTO – conistent

1999 Jan 12 Original panel reconvened

1999 May 6 Panel report adopted .

1999 April 9 The united states requested that the DBS authorise suspension of concession to the level of nulification and impaiment , ie.,US$191.4million

2000 Mar 24

The arbitrator report on Ecudor request for suspenssion of concession circulated to members

2000 May 18

DBS authorises Ecudor to suspension of concession to EC

2001 Nov 14

Doha Ministrial waiver of article 1 & 13 , new TRQ Regime

ww

w.S

tudsP

lanet.co

m

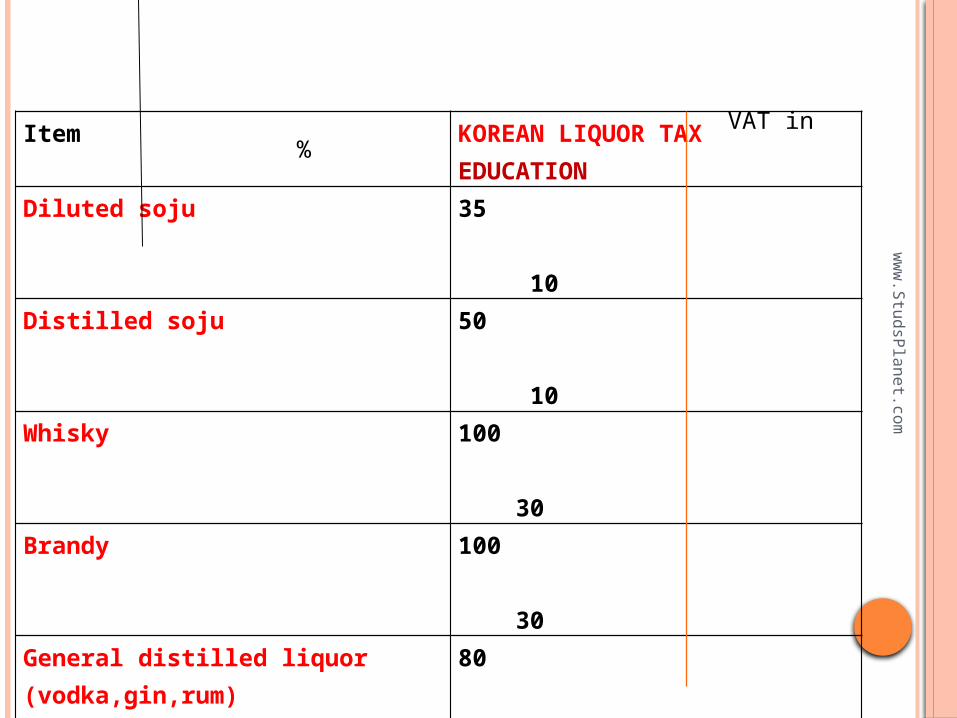

NATIONAL TREATMENT : Treating imported and domestically produced goods equally . An example is The Korean Soju case. The issue was consistency of two Korean tax laws : The Korean Liquor Tax Law 1949 & The Korean Education Tax Law of 1982 with National Treatment Principle of WTO .

ww

w.S

tudsP

lanet.co

m

Item KOREAN LIQUOR TAX EDUCATION

Diluted soju 35 10

Distilled soju 50 10

Whisky 100 30

Brandy 100 30

General distilled liquor (vodka,gin,rum) 80 30

General distilled liquor containing whisky or brandy

100 30

Liquor 50 10

Other liquors -with 25% or more alc.-with less than 25% alc.-which contain 20% or more whisky or brandy

80 30 70 10 100. 30

VAT in %

ww

w.S

tudsP

lanet.co

mThe EC, the complaining country argued that these two laws favored the Korean local sprits called ‘SOJU’ and discriminated the imported sprits and liqueurs , thus protecting the soju from the competition from imported Whisky, Rum, Brandy and Vodka.Under the Education Tax 1990 a Tax Surcharge was levied on the sale of variety of items , including most Alcoholic Beverages . for alc. Beverage The applicable rate was determined by the reference to another tax –tax applied liquor rate ,fro those assed liquor tax rate 80% or greater ,the law imposed an education sur tax calculated aas30% of the liquor tax imposed. For alcoholic beverages assessed a liquor tax rate of less than 80% , the law imposed an education tax of 10 % of the liquor tax imposed.The net result, according to the EC ,was that SOJU overwhelmingly dominated the Korean Spirits Market.the 1996 sales of SOJU amounted to 810 million liters , which represented as much as 94% of the Distilled Spirit Market .

ww

w.S

tudsP

lanet.co

m

The original panel recommended that 1.The SOJU, a traditional Korean Alc.Beverage and imported products such as Whisky, Brandy, Rum, Vodka, Gin, Tequila and liqueurs were directly substitutive products.2. These products competing for a share of the same market were being taxed dissimilary and 3. The dissimilar Taxation resulted in a protection to the locally produced SOJU over the imported products.

ww

w.S

tudsP

lanet.co

mThe Korean made the following observations with respect to physical character end use, place of consumption and pricing .1. SOJU and the imported products not physically identical merely because they shared the essential feature of being distilled alc. Korea argued that if similarity in raw materials used or the method of manufacture were the criteria for putting products under the same category, then paint thinners and ridding alcohol could also be deemed to directly competing products.2. SOJU had a different flavor when compared to the imported products.3. Diluted SOJU was consumed along with meals , which was not so the case with the other products in question.4. The huge price difference between diluted SOJU and most of the imported beverages also indicated they were competing for different segments of the market and thus it would not be proper to use the reasoning of directly competing or substitutable products.

ww

w.S

tudsP

lanet.co

m

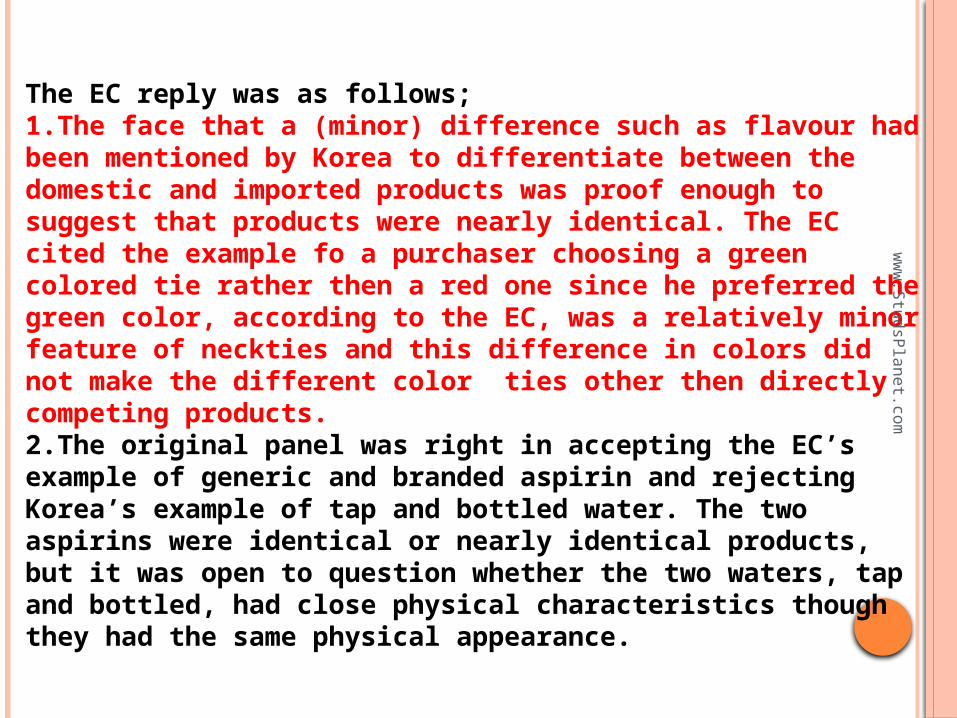

The EC reply was as follows; 1.The face that a (minor) difference such as flavour had been mentioned by Korea to differentiate between the domestic and imported products was proof enough to suggest that products were nearly identical. The EC cited the example fo a purchaser choosing a green colored tie rather then a red one since he preferred the green color, according to the EC, was a relatively minor feature of neckties and this difference in colors did not make the different color ties other then directly competing products.2.The original panel was right in accepting the EC’s example of generic and branded aspirin and rejecting Korea’s example of tap and bottled water. The two aspirins were identical or nearly identical products, but it was open to question whether the two waters, tap and bottled, had close physical characteristics though they had the same physical appearance.

ww

w.S

tudsP

lanet.co

m

3. As regards to the contention of Korea that SOJU and the imported beverages had to be on a different footing as the former was drunk with meals and at homes or friends’ places while the western spirits were standalone drinks consumption at restaurants and bars, the EC argued that a NIELSEN STUDY had indicated that 5.8%of Korean respondents drank whisky with meals.The APPELLATE body was of the view that common characteristics, end-uses and channels of distribution and prices confirmed the correctness of the original panel grouping SOJU and the imported beverages as directly competitive or substitutable products. With the appellate body confirming this aspect of the argument, the next conclusion on the protection being given to the native Korean brew was only matter of course due to the substantial tax differentials between SOJU and the imported western-style spirits. The Appellate Body recommended that the Dispute Settlement Body request Korea to bring the Korean Liquor Tax Law of 1949 and the Korean Education Tax Law of 1982 into conformity with its WTO obligations.”

ww

w.S

tudsP

lanet.co

m

•There was another dispute involving Korea under the same “National Treatment” issue. This was ‘Korea-measures affecting imports of fresh, chilled and frozen beef’•. Beef imported into Korea was distributed under conditions not applicable to domestic beef. Ed This dual retail system ensured that:Imported beef was displayed separately in those department stores and supermarkets that were authorized to sell such beef:Foreign beef shops had to bear a sign with the words “specialized imported beef store”.•Foreign beef imported had to undergo additional requirements, such as having to bear details regarding the end-consumer, the contract number and the importer bringing in the foreign beef:

ww

w.S

tudsP

lanet.co

m

• Generally, a more stringent record keeping practice was needed in the case of foreign beef.

The Appellate body hearing the dispute also upheld the original panel’s original conclusion that Korea’s dual retail system was inconsistent with Article: III:4 of the GATT1994.

While the dimensions of the briefly stated dispute regarding the Korean policy on imported beef could have been clear enough, the Soju dispute had marketing dimensions as well since the panels had to make a finding on directly competing or substitutable products.

ww

w.S

tudsP

lanet.co

m

Free Trade through negotiation. The barriers like tariffs and measures such as

import bans or quotas that selectively restrict import quantities

The Canadian Dairy caseThis issue is regarding Govt. Policy that

enabled Canadian exporters of cheese and its products to procure milk at advantage price “The price which the exporters paid for milk was

lower when compared to the milk prices prevailing in Canada’s domestic market”

The US and NEW ZEALAND argued such that such a govt. policy was not in conformity with Canada’s export subsidy commitments under the agreement on agriculture .

Introduction: milk production in Canada was governed by a quota system

ww

w.S

tudsP

lanet.co

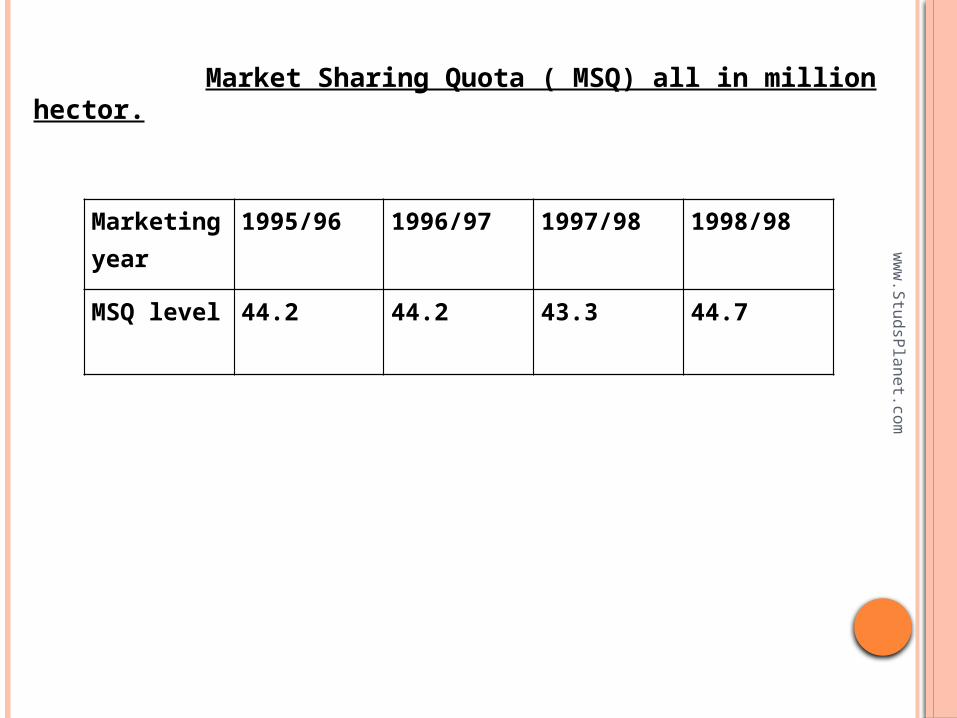

m Market Sharing Quota ( MSQ) all in million hector.

Marketing year

1995/96 1996/97 1997/98 1998/98

MSQ level 44.2 44.2 43.3 44.7

ww

w.S

tudsP

lanet.co

m

The Canadian milk producers were assigned a domestic sale quotaMilk produce with in the quota was sold in Canadian market the domestic market milk recording to New Zealand was sold C$ 49.48 and c$56.06 per hectoliter the average figure cited by united state was Canadian c$52.92 per hectoliter Milk production beyond this quota could not be sold within Canada.This over production milk has to be sold as commercial Export Milk (CEM)to processors exporting dairy products.

ww

w.S

tudsP

lanet.co

m

These export processors were able to get the commercial export milk at lower price as compare to milk sold in the domestic market according to Canada it self the price ranged from C$19.06 toC$36.86 per hectoliter of commercial export milkThe only way a producer could dispose of the over quota milk in the domestic market was by selling it as animal feedThis situation of govt. influenced policies enabling processor to get the milk at lower price for export of dairy products according to the US and NZ was not in conformity with article 9.1 (a)& (c)On export subsidy commitments of the agreement on agriculture .

ww

w.S

tudsP

lanet.co

m

Findings of the Appellate Body, the compliance panel made the fallowing conclusion:1. Payments provision of milk at discounted prices to dairy processors for export constituted payments within the meaning of 9.1(c)2. By virtue of Govt. action : The procedures of over quota milk had no other alternative but to sell to export processors at lower price . A dairy producer was, in principle, prevented from marketing his milk in the domestic market out side the quota allotted to him but governmental action, these producers would have preferred to sell the milk in the domestic market and realize a higher price

ww

w.S

tudsP

lanet.co

m

3. Simultaeously, processors who diverted CEM into domestic market were penalized presence of these conditions substantiated the reasoning and other dairy products this action of the royal dairy Commission, according to the compliance panel, fell within the meaning of export subsidy , commitment of article of 9.1(c)

4. Payment on the export of agriculture product: Only a contract for exports allowed dairy processors to have access to the lower priced commercial export milk an export processor functioned out side the regulatory frame work of price floors and quota ceiling applicable to domestic market milk transaction in Canada.

ww

w.S

tudsP

lanet.co

m

Given below is the simulation of the findings of the Appellate BodyCanada has modified the at Dairy Regulatory Regime so that market forces are at work in respect of the sale of dairy products. The original panel had taken international price and domestic price as the bench marks for determine subsidy. These bench mark prices may not be true indicators for calculating subsides that may be given by a government to a product. A better bench mark will be the total cost of production, which will ensure determination of the cost that may be subsidized by a government particularly in relation to exports .A direct subsidizing connectivity has to be established to prove non conformity to WTO commitments.

ww

w.S

tudsP

lanet.co

m

Panel report of July-11-2001 and Dec-20-2002.Given the Canadian Govt’s Quota on domestic sale of milk ,the producers had to choose at the second best option available and that was selling the excess at a lower price C$ 30 per hectolitre to export processors compared to C$53 per hectoliter that local market sales would fetch . How ever, selling selling at was better alternative to destroying the milkThe panels also pointed to the Canadian dairy commissions (CDC), prohibition on diversion of CEM , to the domestic market .the CDC had the “seizure power “over such diverted milk .more ever, in such instance the buyers of milk could end up paying the higher domestic price in addition to the CEM price already paid

ww

w.S

tudsP

lanet.co

m

There was also the issue of cross-subsidization of CEM . the fact that domestic sales of milk ensured 40% higer returnment that milk producer could afford to sell at a lower price to export processors . the Canadian system ensured that producers who sold milk at a lower price to export processors where compensated by a higer domestic price this higher enabled milk producers to derive the advantage of marginal costing in sales of commercial export milk

The panel found inconsistency with article 9.1(C) of the agreement on agriculture and recommended that the DSB request Canada to bring its measures in conformity which the WTO agreement.

Related Documents