Worldwide ICT market beyond 2013 Steffi Han IDC Korea 8 October 2013

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Worldwide ICT market beyond 2013 Steffi Han

IDC Korea

8 October 2013

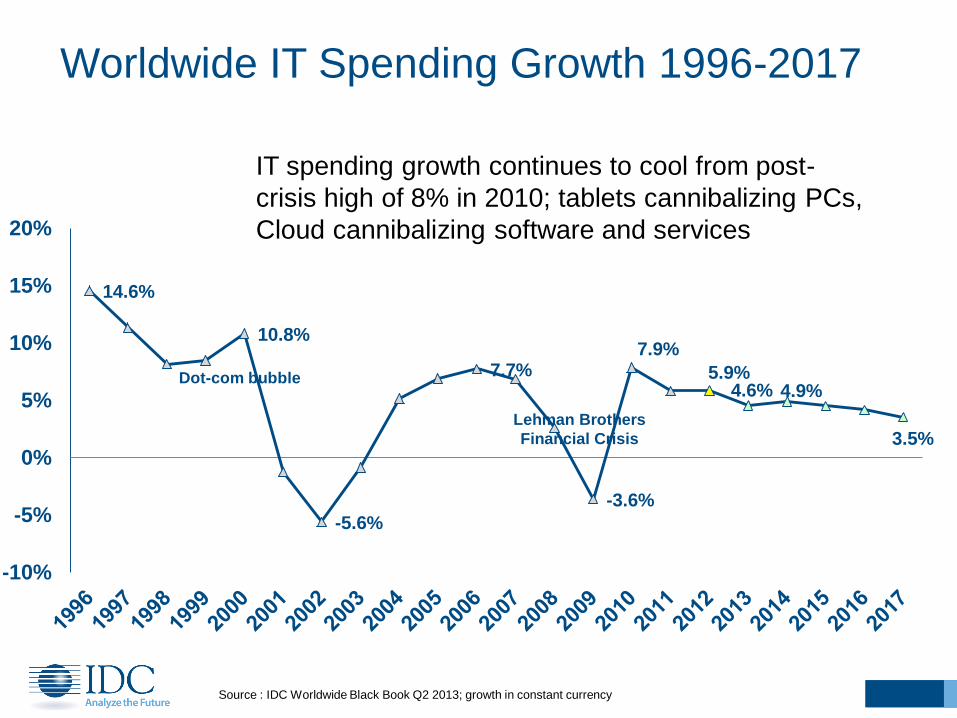

14.6%

10.8%

-5.6%

7.7%

-3.6%

7.9%

5.9% 4.6% 4.9%

3.5%

-10%

-5%

0%

5%

10%

15%

20%

Worldwide IT Spending Growth 1996-2017

Dot-com bubble

Lehman Brothers

Financial Crisis

Source : IDC Worldwide Black Book Q2 2013; growth in constant currency

IT spending growth continues to cool from post-

crisis high of 8% in 2010; tablets cannibalizing PCs,

Cloud cannibalizing software and services

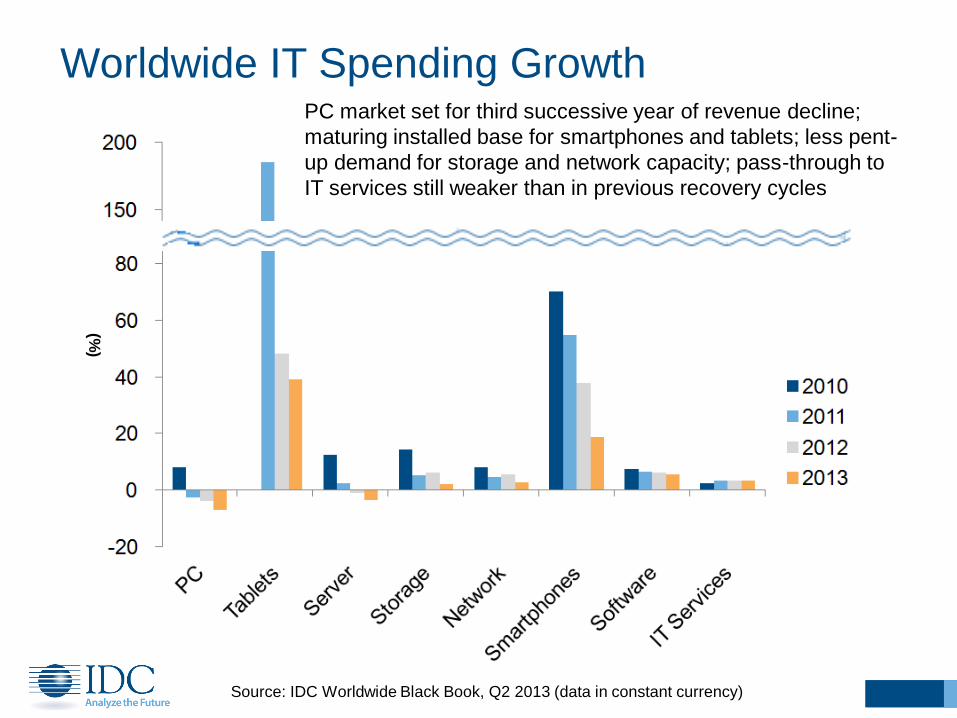

Worldwide IT Spending Growth

Source: IDC Worldwide Black Book, Q2 2013 (data in constant currency)

PC market set for third successive year of revenue decline;

maturing installed base for smartphones and tablets; less pent-

up demand for storage and network capacity; pass-through to

IT services still weaker than in previous recovery cycles

(%)

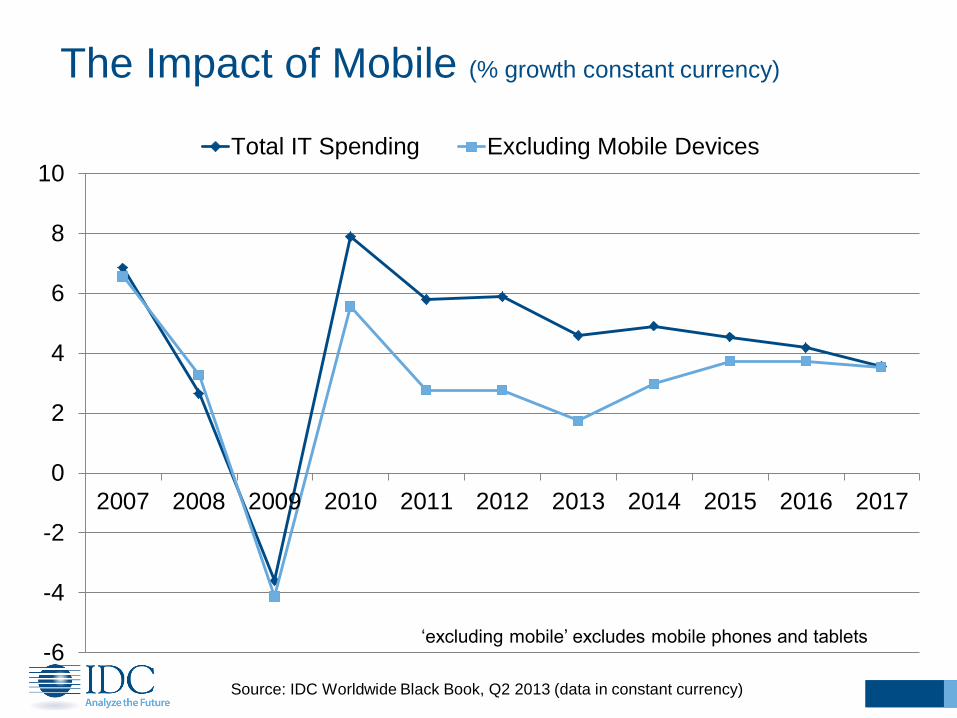

The Impact of Mobile (% growth constant currency)

-6

-4

-2

0

2

4

6

8

10

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Total IT Spending Excluding Mobile Devices

‗excluding mobile‘ excludes mobile phones and tablets

Source: IDC Worldwide Black Book, Q2 2013 (data in constant currency)

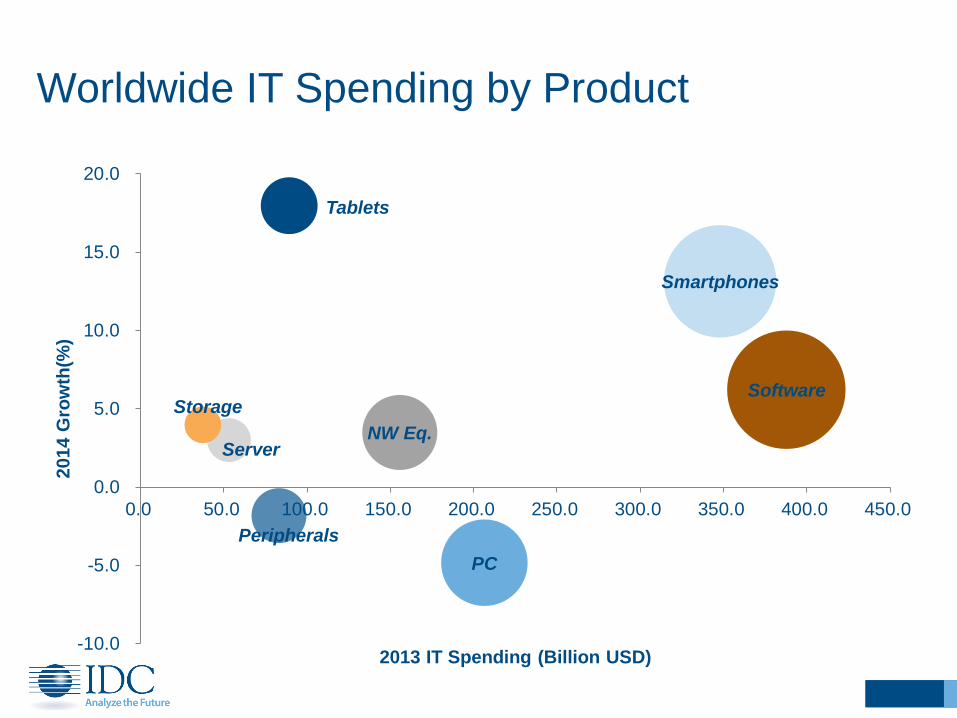

Worldwide IT Spending by Product

PC

Peripherals

Tablets

Server

Storage

NW Eq.

Smartphones

Software

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

0.0 50.0 100.0 150.0 200.0 250.0 300.0 350.0 400.0 450.0

2014 G

row

th(%

)

2013 IT Spending (Billion USD)

-10%

-5%

0%

5%

10%

15%

20%

Korea IT Korea Traditional IT WW IT

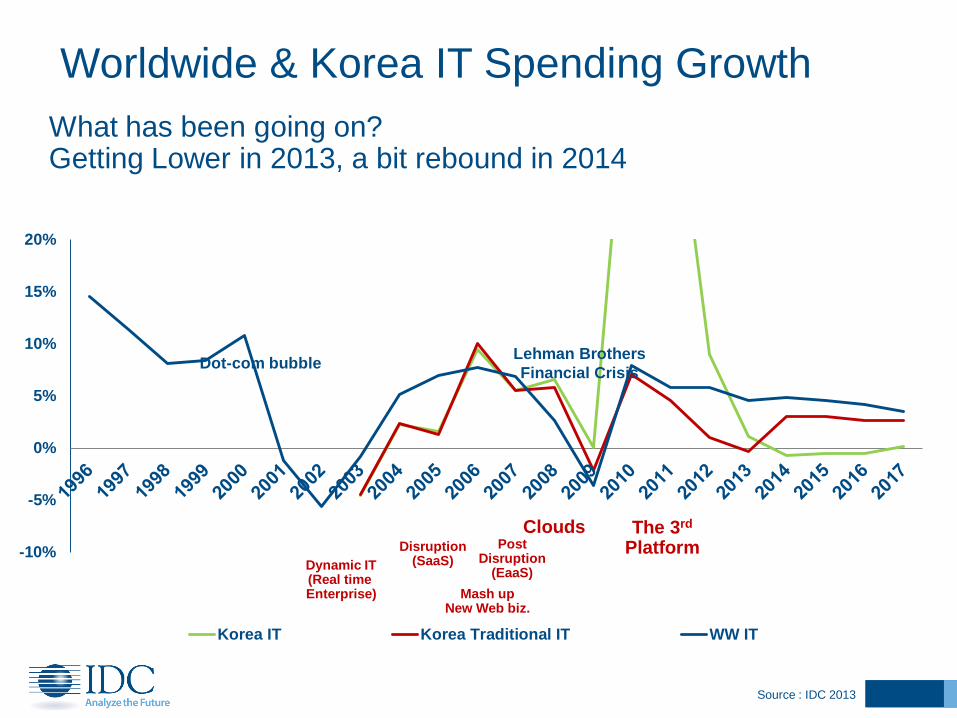

Worldwide & Korea IT Spending Growth

What has been going on? Getting Lower in 2013, a bit rebound in 2014

Dot-com bubble Lehman Brothers

Financial Crisis

Disruption (SaaS)

Post Disruption

(EaaS) Dynamic IT (Real time Enterprise)

Clouds The 3rd Platform

Mash up New Web biz.

Source : IDC 2013

7

2011, Welcome to the New Mainstream A select group of disruptive technologies will move beyond "early adopter" status, maturing and coalescing into a "new mainstream" platform

2012, Competing for 2020 Too early? But there is no doubt that having a clear eye on 2020 will be vitally important – for ICT vendors and for CIOs alike – when making decisions in 2012

Source: IDC 2013

For 2013, Competing on the 3rd Platform Theme will be similar to 2012‟s, there will be much greater urgency as the market moves way past the “exploration” stage to full-blown large-stakes competition

Key Themes Driving Strategy

For 2014, Accelerating the “Chapter Two” In the Chapter Two phase, the scale of the 3rd Platform technologies are going to be much larger, but — very importantly — the market will also be much less vendor- and technology driven and more user- and solution driven

Bring your own ―X‖(BYO‖X‖)

Availability of superior technology

Employees driving IT decisions

Security, Security,,

Social, collaborative enterprise

Rich media, multimedia

Work@home ↔ Personal@work

Simplicity, ease of use, UI/UX

Consumerization isn‘t about technology management

New apps and its distribution model

more Challenges, more Stress but more Opportunities

Consumerization of IT

is penetrating all aspects

Source: IDC 2013

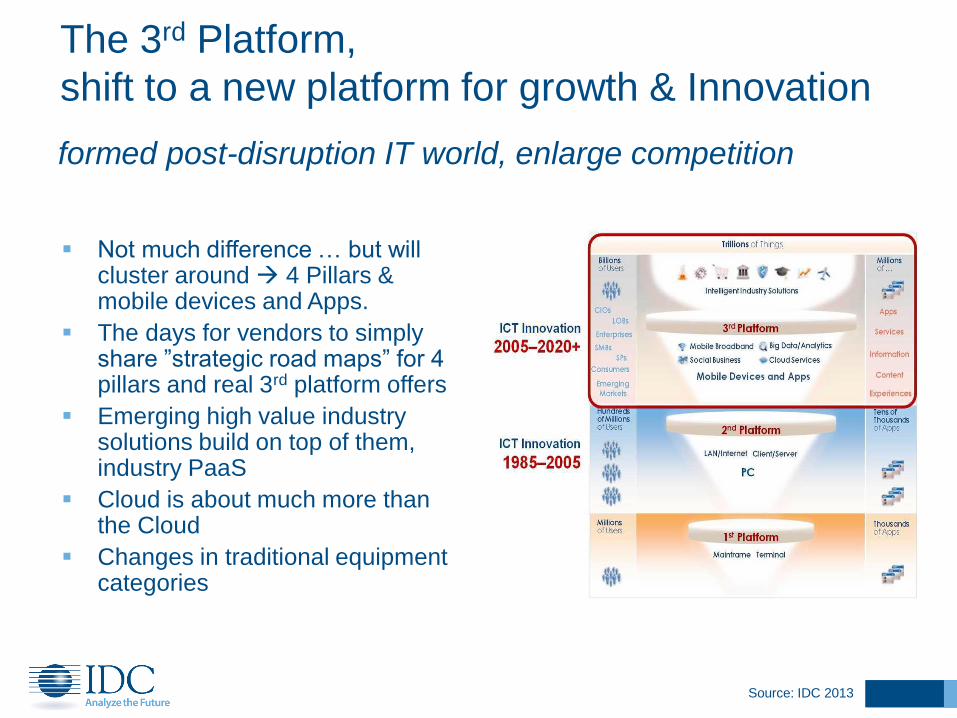

Not much difference … but will cluster around 4 Pillars & mobile devices and Apps.

The days for vendors to simply share ‖strategic road maps‖ for 4 pillars and real 3rd platform offers

Emerging high value industry solutions build on top of them, industry PaaS

Cloud is about much more than the Cloud

Changes in traditional equipment categories

formed post-disruption IT world, enlarge competition

The 3rd Platform,

shift to a new platform for growth & Innovation

Source: IDC 2013

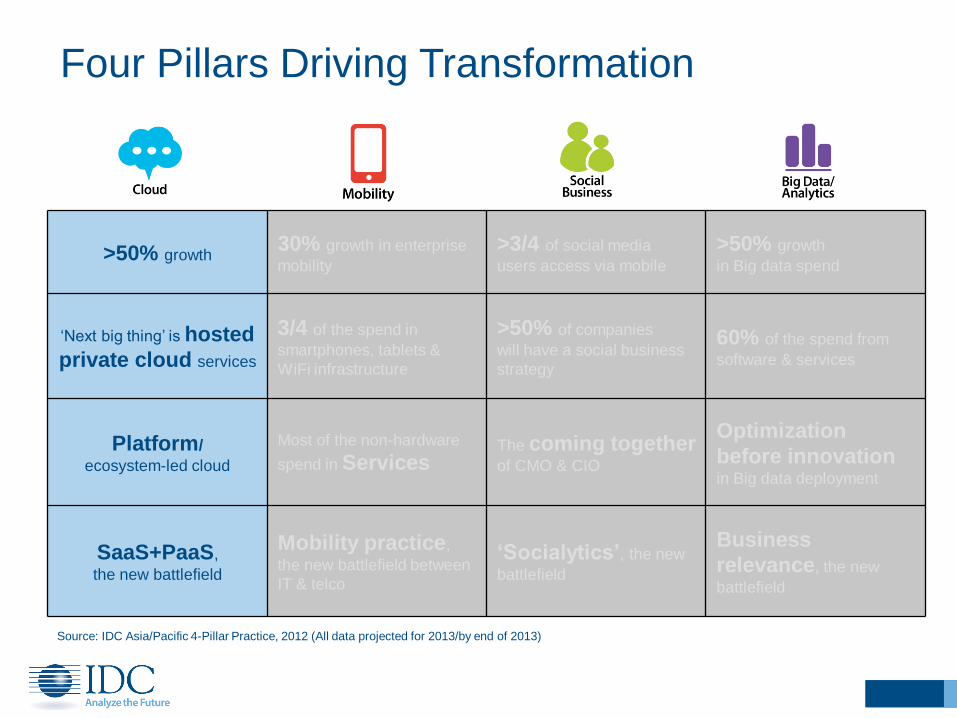

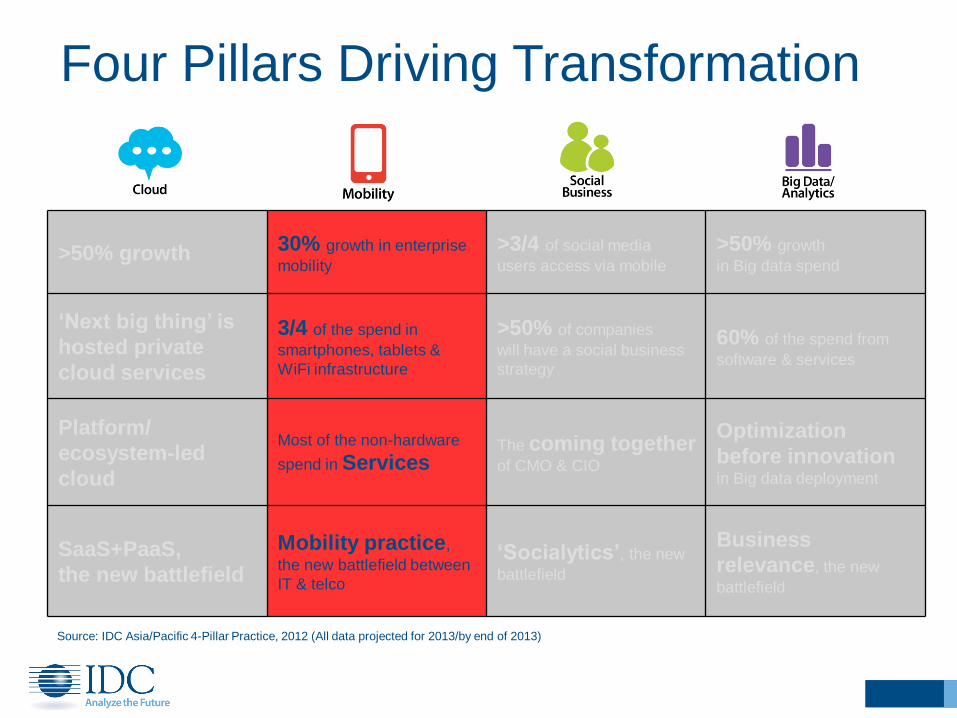

>50% growth 30% growth in enterprise

mobility

>3/4 of social media

users access via mobile

>50% growth

in Big data spend

‗Next big thing‘ is hosted

private cloud services

3/4 of the spend in

smartphones, tablets &

WiFi infrastructure

>50% of companies

will have a social business

strategy

60% of the spend from

software & services

Platform/

ecosystem-led cloud

Most of the non-hardware

spend in Services The coming together of CMO & CIO

Optimization

before innovation

in Big data deployment

SaaS+PaaS,

the new battlefield

Mobility practice,

the new battlefield between

IT & telco

„Socialytics‟, the new

battlefield

Business

relevance, the new

battlefield

Source: IDC Asia/Pacific 4-Pillar Practice, 2012 (All data projected for 2013/by end of 2013)

Four Pillars Driving Transformation

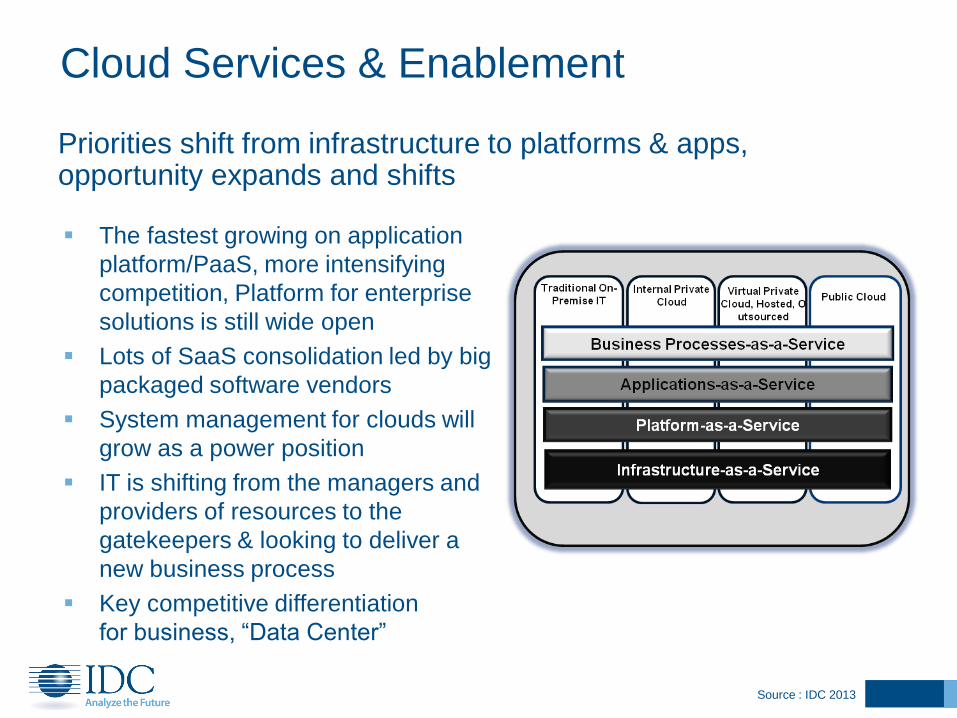

Cloud Services & Enablement

The fastest growing on application

platform/PaaS, more intensifying

competition, Platform for enterprise

solutions is still wide open

Lots of SaaS consolidation led by big

packaged software vendors

System management for clouds will

grow as a power position

IT is shifting from the managers and

providers of resources to the

gatekeepers & looking to deliver a

new business process

Key competitive differentiation

for business, ―Data Center‖

Priorities shift from infrastructure to platforms & apps, opportunity expands and shifts

Source : IDC 2013

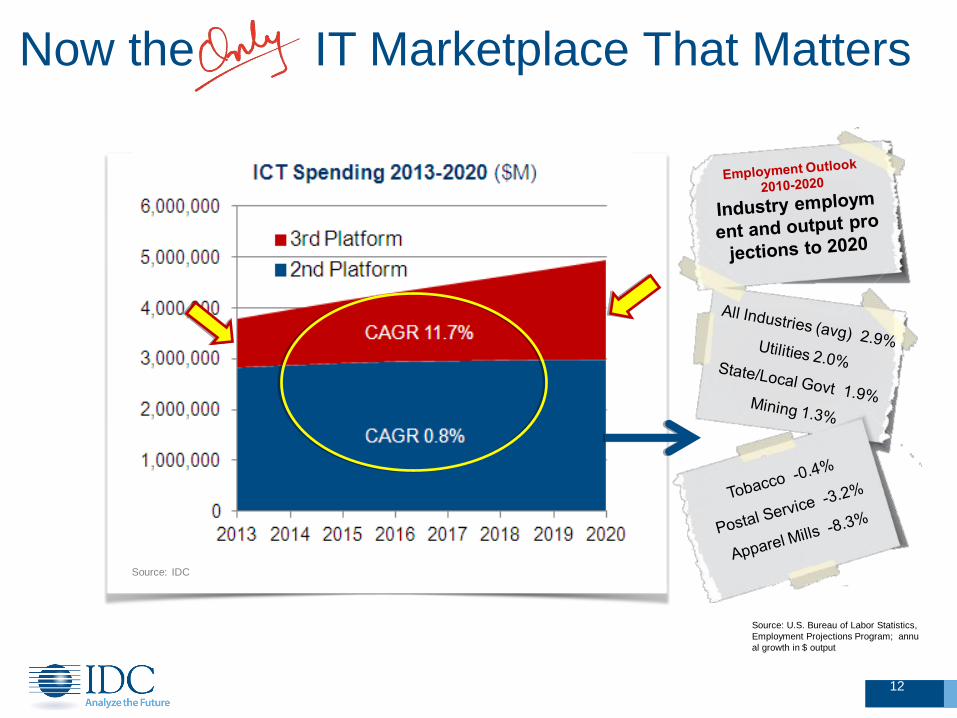

Source: IDC

12

Source: U.S. Bureau of Labor Statistics,

Employment Projections Program; annu

al growth in $ output

Now the IT Marketplace That Matters

13

13

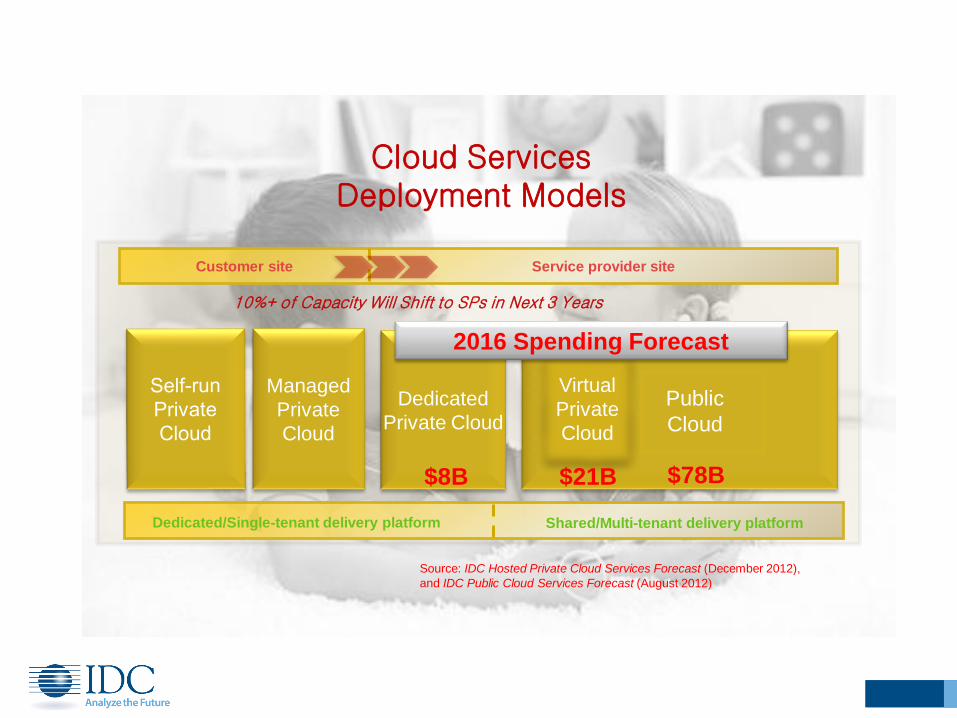

Cloud Services Deployment Models

Dedicated/Single-tenant delivery platform Shared/Multi-tenant delivery platform

Managed

Private

Cloud

Dedicated Private Cloud

Virtual

Private

Cloud

Public

Cloud

Customer site Service provider site

$78B $21B $8B

2016 Spending Forecast

Source: IDC Hosted Private Cloud Services Forecast (December 2012),

and IDC Public Cloud Services Forecast (August 2012)

10%+ of Capacity Will Shift to SPs in Next 3 Years

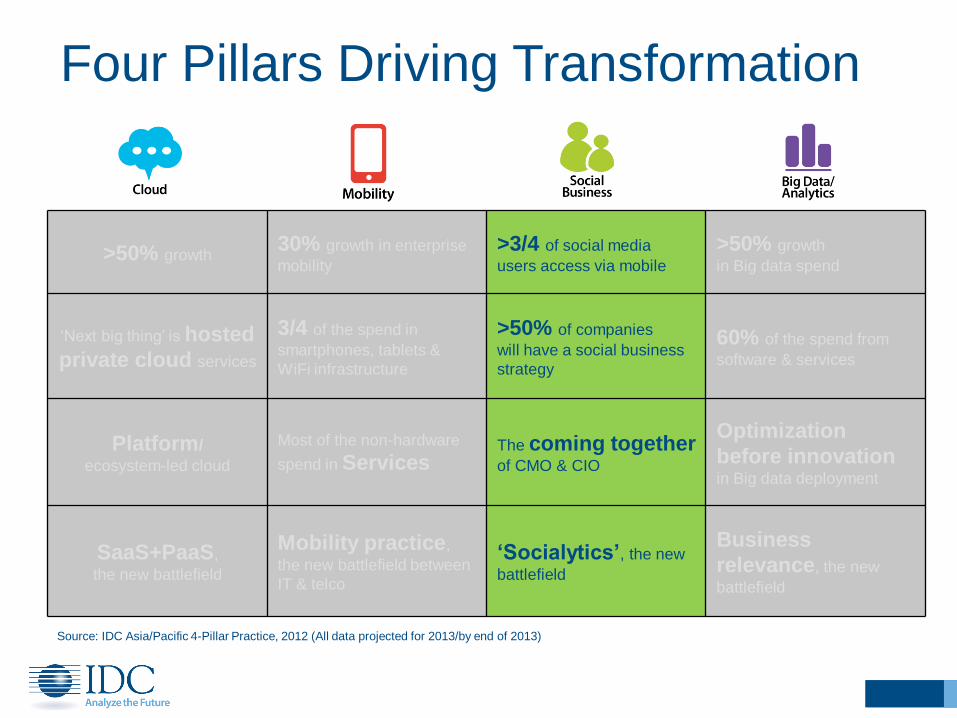

>50% growth 30% growth in enterprise

mobility

>3/4 of social media

users access via mobile

>50% growth

in Big data spend

„Next big thing‟ is

hosted private

cloud services

3/4 of the spend in

smartphones, tablets &

WiFi infrastructure

>50% of companies

will have a social business

strategy

60% of the spend from

software & services

Platform/

ecosystem-led

cloud

Most of the non-hardware

spend in Services The coming together of CMO & CIO

Optimization

before innovation

in Big data deployment

SaaS+PaaS,

the new battlefield

Mobility practice,

the new battlefield between

IT & telco

„Socialytics‟, the new

battlefield

Business

relevance, the new

battlefield

Source: IDC Asia/Pacific 4-Pillar Practice, 2012 (All data projected for 2013/by end of 2013)

Four Pillars Driving Transformation

Rapid Smart Phone growth will not happen, but keep growing

Tablets decrease usage of a PC, but not the need for a PC, sub 8 in. will be main growth engine

PC demand is decreasing, but not lose the key role of smart connected devices

New form factors - converged PC/Mobile Devices

New data plane

OS diversity, Windows 8 ??

How about TV, industry specific devices & others

Think mobile virtualization..

Multiple Devices per person is REAL Smart connected devices is the new metric for the future

Not replace, Supplementary !…

Smart Connected Devices

Source: IDC 2013

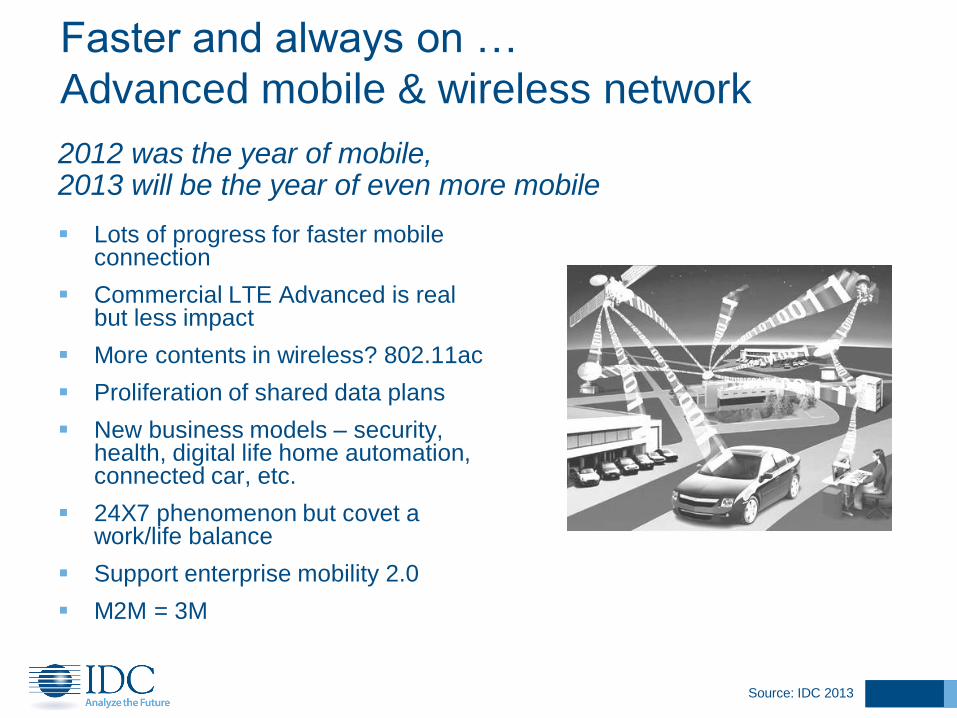

2012 was the year of mobile, 2013 will be the year of even more mobile

Lots of progress for faster mobile connection

Commercial LTE Advanced is real but less impact

More contents in wireless? 802.11ac

Proliferation of shared data plans

New business models – security, health, digital life home automation, connected car, etc.

24X7 phenomenon but covet a work/life balance

Support enterprise mobility 2.0

M2M = 3M

Faster and always on …

Advanced mobile & wireless network

Source: IDC 2013

>50% growth 30% growth in enterprise

mobility

>3/4 of social media

users access via mobile

>50% growth

in Big data spend

‗Next big thing‘ is hosted

private cloud services

3/4 of the spend in

smartphones, tablets &

WiFi infrastructure

>50% of companies

will have a social business

strategy

60% of the spend from

software & services

Platform/

ecosystem-led cloud

Most of the non-hardware

spend in Services The coming together of CMO & CIO

Optimization

before innovation

in Big data deployment

SaaS+PaaS,

the new battlefield

Mobility practice,

the new battlefield between

IT & telco

„Socialytics‟, the new

battlefield

Business

relevance, the new

battlefield

Source: IDC Asia/Pacific 4-Pillar Practice, 2012 (All data projected for 2013/by end of 2013)

Four Pillars Driving Transformation

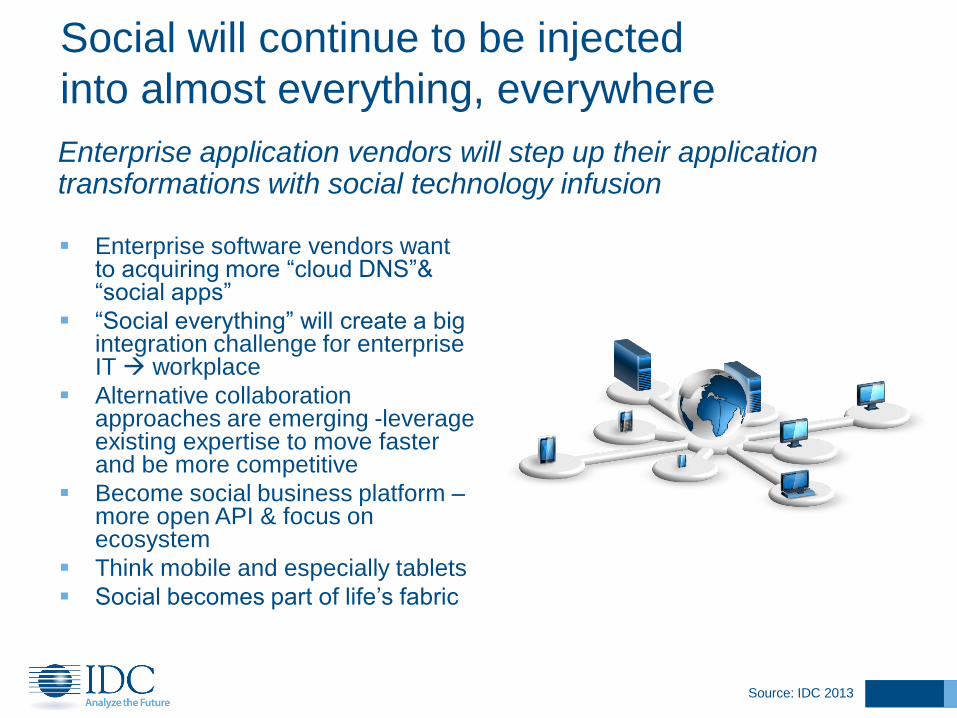

Enterprise software vendors want to acquiring more ―cloud DNS‖& ―social apps‖

―Social everything‖ will create a big integration challenge for enterprise IT workplace

Alternative collaboration approaches are emerging -leverage existing expertise to move faster and be more competitive

Become social business platform – more open API & focus on ecosystem

Think mobile and especially tablets

Social becomes part of life‘s fabric

Enterprise application vendors will step up their application transformations with social technology infusion

Social will continue to be injected

into almost everything, everywhere

Source: IDC 2013

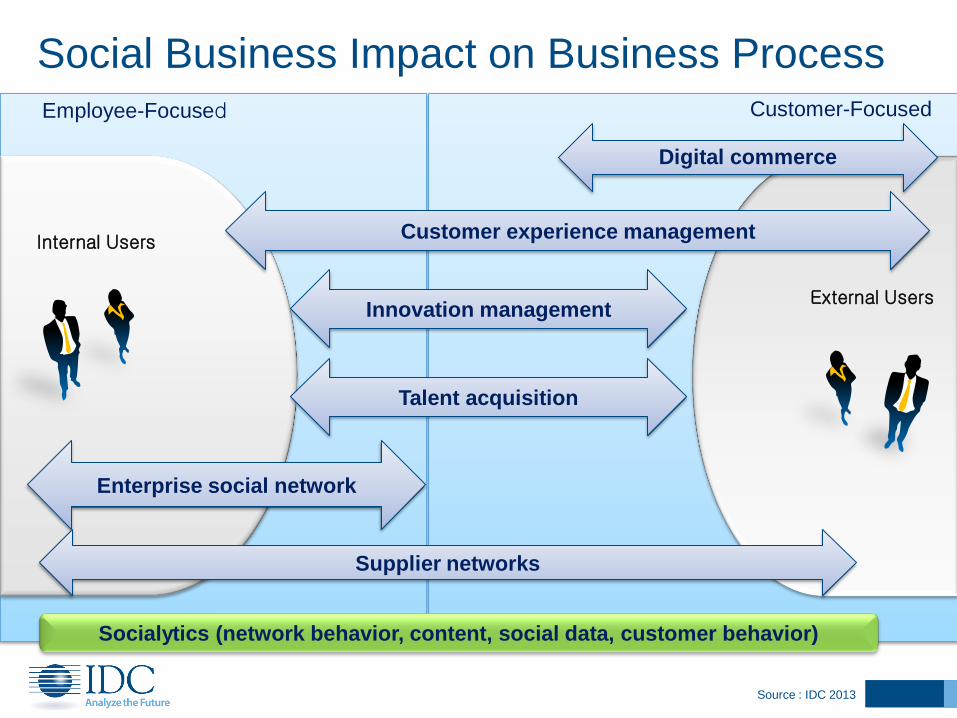

Social Business Impact on Business Process

Internal Users

External Users

Employee-Focused Customer-Focused

Enterprise social network

Innovation management

Talent acquisition

Digital commerce

Customer experience management

Socialytics (network behavior, content, social data, customer behavior)

Supplier networks

Source : IDC 2013

>50% growth 30% growth in enterprise

mobility

>3/4 of social media

users access via mobile

>50% growth

in Big data spend

‗Next big thing‘ is hosted

private cloud services

3/4 of the spend in

smartphones, tablets &

WiFi infrastructure

>50% of companies

will have a social business

strategy

60% of the spend from

software & services

Platform/

ecosystem-led cloud

Most of the non-hardware

spend in Services The coming together of CMO & CIO

Optimization

before innovation

in Big data deployment

SaaS+PaaS,

the new battlefield

Mobility practice,

the new battlefield between

IT & telco

„Socialytics‟, the new

battlefield

Business

relevance, the new

battlefield

Source: IDC Asia/Pacific 4-Pillar Practice, 2012 (All data projected for 2013/by end of 2013)

Four Pillars Driving Transformation

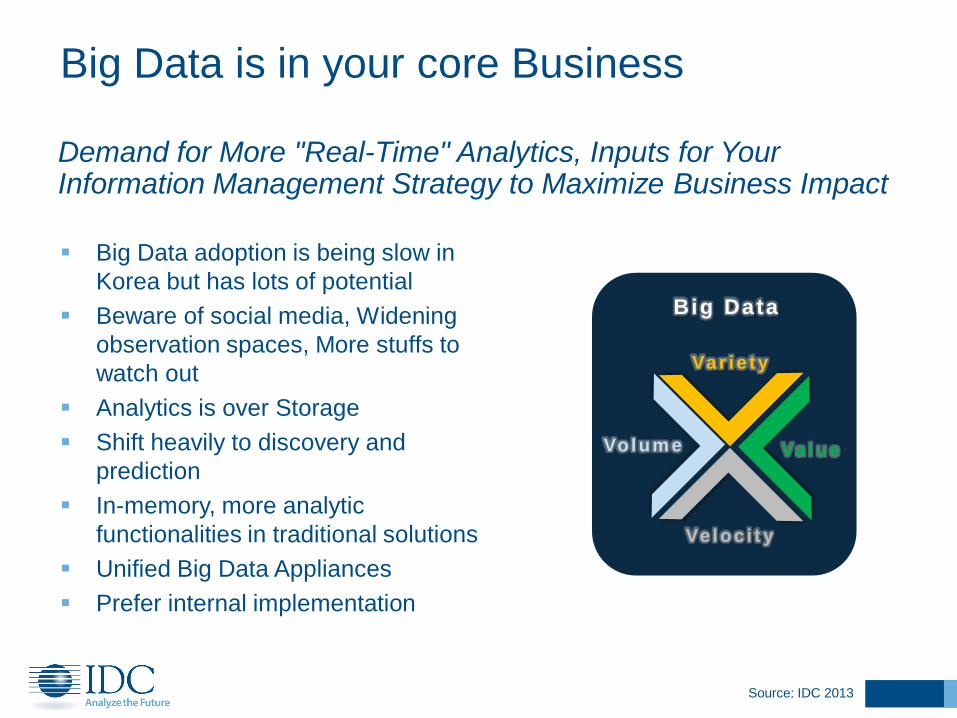

Big Data adoption is being slow in

Korea but has lots of potential

Beware of social media, Widening

observation spaces, More stuffs to

watch out

Analytics is over Storage

Shift heavily to discovery and

prediction

In-memory, more analytic

functionalities in traditional solutions

Unified Big Data Appliances

Prefer internal implementation

Demand for More "Real-Time" Analytics, Inputs for Your Information Management Strategy to Maximize Business Impact

Big Data is in your core Business

Volum e

Var ie ty

Veloc i t y

Value

Big Data

Source: IDC 2013

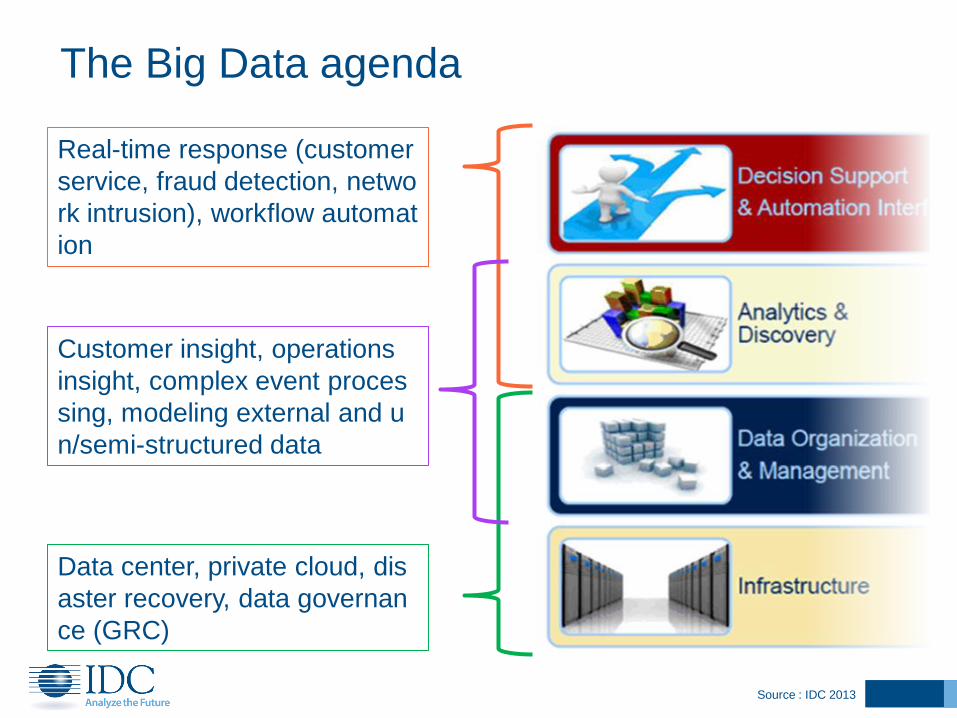

Data center, private cloud, dis

aster recovery, data governan

ce (GRC)

Real-time response (customer

service, fraud detection, netwo

rk intrusion), workflow automat

ion

Customer insight, operations

insight, complex event proces

sing, modeling external and u

n/semi-structured data

The Big Data agenda

Source : IDC 2013

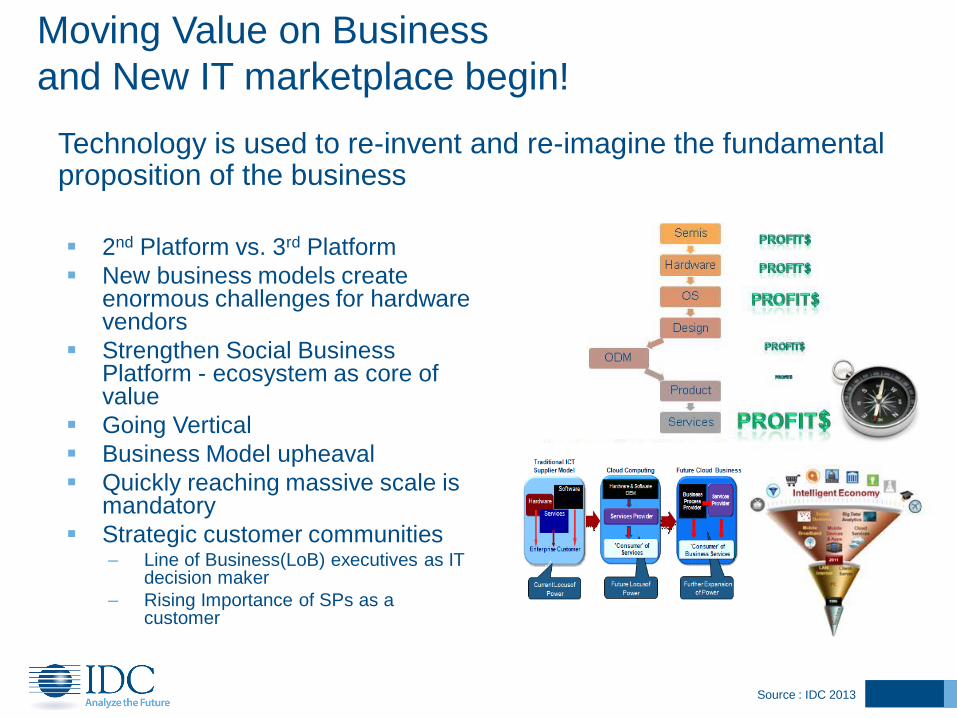

Moving Value on Business

and New IT marketplace begin!

Technology is used to re-invent and re-imagine the fundamental proposition of the business

2nd Platform vs. 3rd Platform

New business models create enormous challenges for hardware vendors

Strengthen Social Business Platform - ecosystem as core of value

Going Vertical

Business Model upheaval

Quickly reaching massive scale is mandatory

Strategic customer communities – Line of Business(LoB) executives as IT

decision maker

– Rising Importance of SPs as a customer

Source : IDC 2013

Consumerization/Mobility/Cloud data/information leaking & risks related to data privacy

Crimeware, Treat of APT(Advanced Persistent Threat),

Mobile device security lock phone and SIM card remotely, wipe important information from memory card and activate phone's built-in GPS chip to locate your lost or stolen device

More Malware will come from App stores

Cross-platform security solutions

Managed security services

The range and complexity of security threats are enlarged

New way of Security

Source: IDC 2013

Related Documents