WORLDCOM WORLDCOM Presented by: Eric Barr Stephanie Jenkins Robert Provost Adam Wear

WORLDCOM Presented by: Eric Barr Stephanie Jenkins Robert Provost Adam Wear.

Dec 18, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

WORLDCOMWORLDCOM

Presented by:

Eric Barr

Stephanie Jenkins

Robert Provost

Adam Wear

WorldCom

What are the facts?– Ebbers (CEO) had used his company stock as

collateral for both professional and personal loans– Ebbers and Sullivan (CFO/CPA) “frequently made

the decision to grant excessive compensation”– Line Costs were capitalized as “Prepaid Capacity”– A long time ensued before Cynthia Cooper came

forward with the inaccurate accounting practice

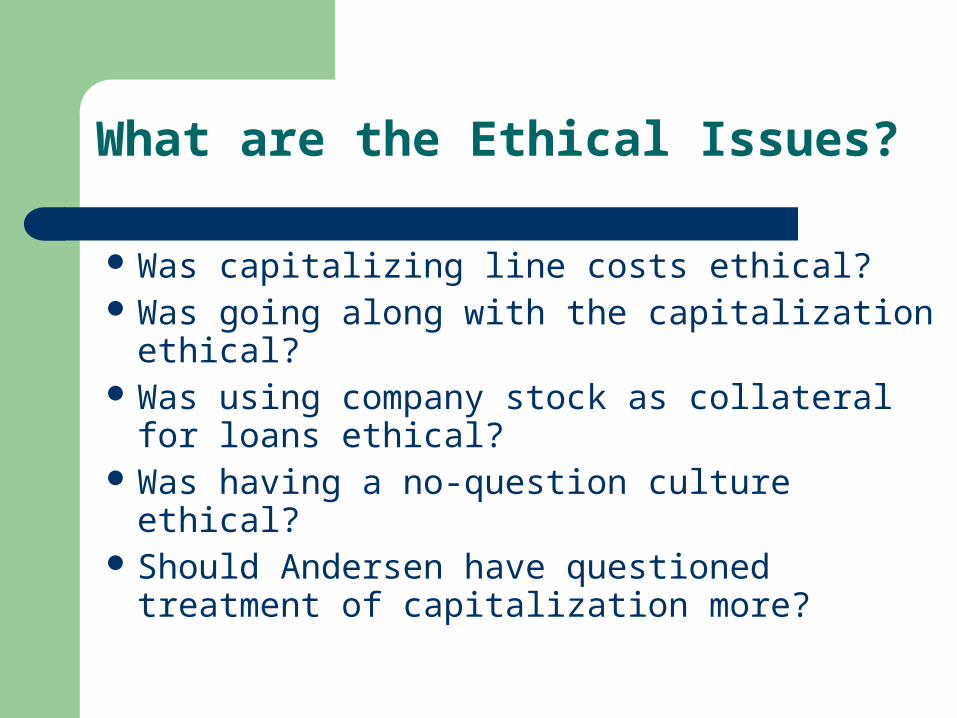

What are the Ethical Issues?

Was capitalizing line costs ethical? Was going along with the capitalization ethical? Was using company stock as collateral for

loans ethical? Was having a no-question culture ethical? Should Andersen have questioned treatment of

capitalization more?

Alternatives

Ebbers could have changed his business strategy

Sullivan could have refused to go along with accounting practices

External Auditors could have questioned more Internal employees could have come forward Internal Audit could have had stronger

presence

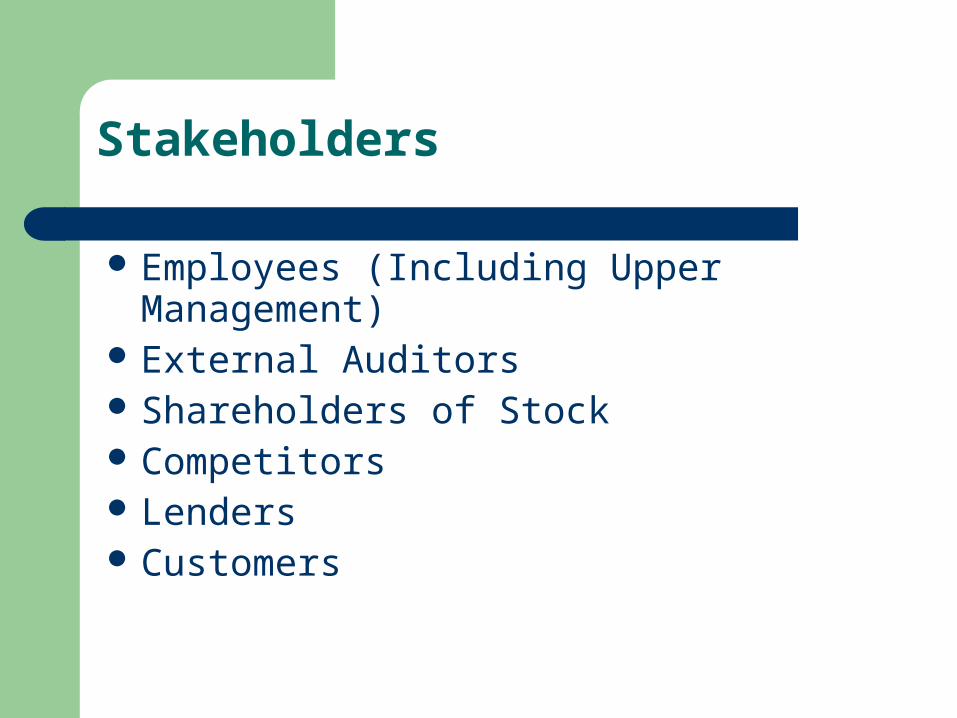

Stakeholders

Employees (Including Upper Management) External Auditors Shareholders of Stock Competitors Lenders Customers

Practical Constraints

Ebbers would have gone bankrupt Company would suffer large losses Employees could lose job External Audit Firm could lose client Internal Audit kept busy away from auditing

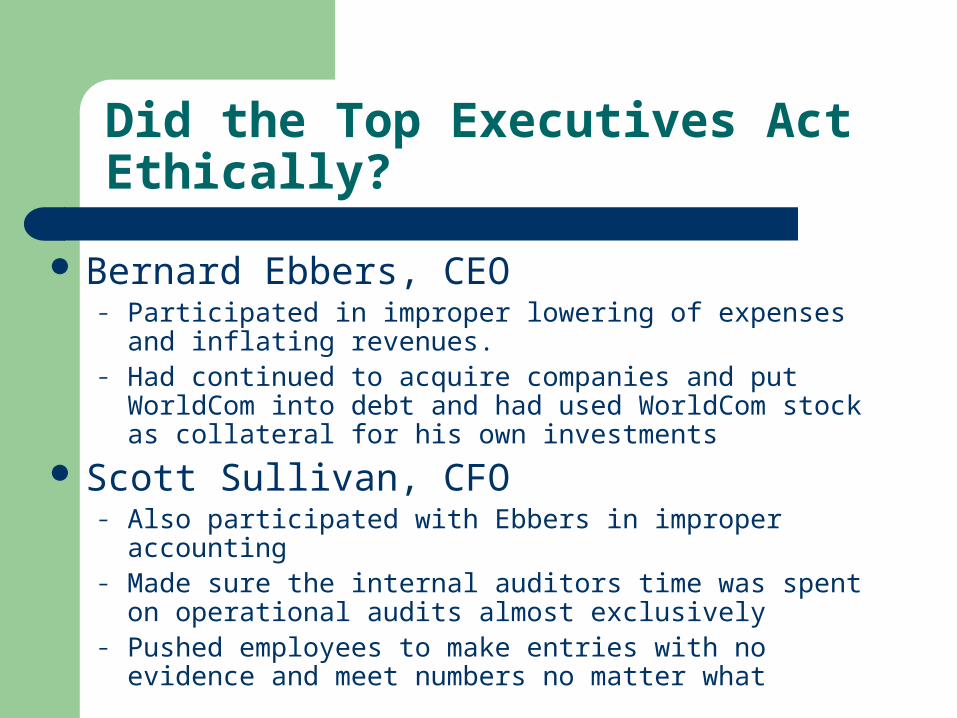

Did the Top Executives Act Ethically?

Bernard Ebbers, CEO– Participated in improper lowering of expenses and inflating

revenues. – Had continued to acquire companies and put WorldCom into

debt and had used WorldCom stock as collateral for his own investments

Scott Sullivan, CFO– Also participated with Ebbers in improper accounting – Made sure the internal auditors time was spent on operational

audits almost exclusively– Pushed employees to make entries with no evidence and meet

numbers no matter what

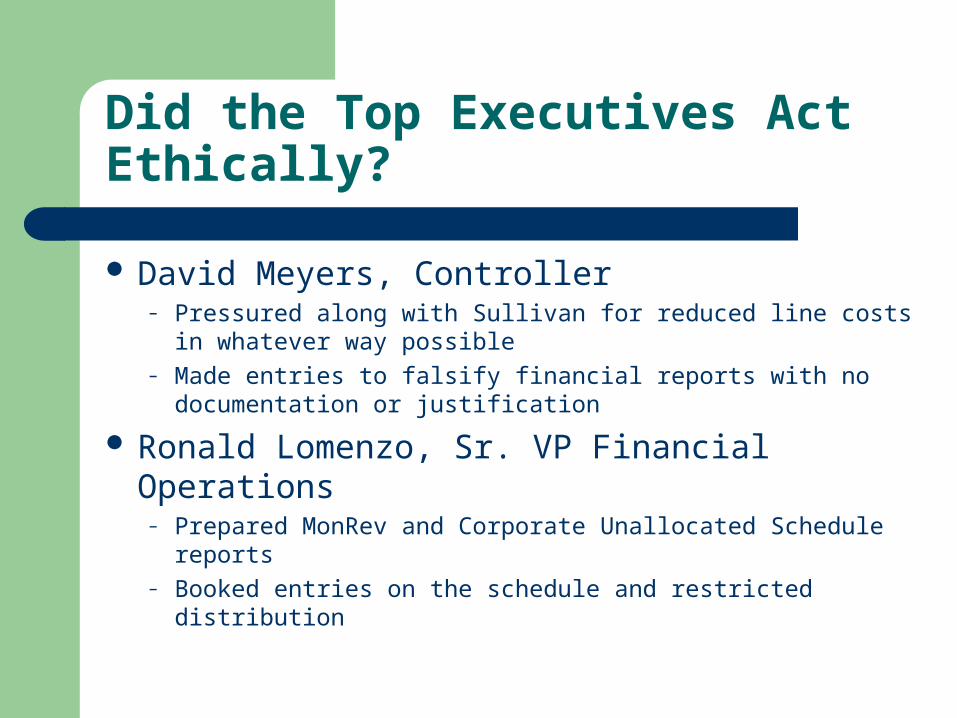

Did the Top Executives Act Ethically?

David Meyers, Controller– Pressured along with Sullivan for reduced line costs in

whatever way possible– Made entries to falsify financial reports with no documentation

or justification

Ronald Lomenzo, Sr. VP Financial Operations– Prepared MonRev and Corporate Unallocated Schedule

reports– Booked entries on the schedule and restricted distribution

Did the Top Executives Act Ethically?

Buford Yates, Director General Accounting– Participated in and encouraged the improper accounting even

though he saw no justification for it

Cynthia Cooper, VP Internal Audit– Uncovered the accounting fraud and blew the whistle

Steven Brabbs, Europe & Asia Executive– Questioned unjustified entries to top exectutives and Arthur

Anderson– Refused to make the entry, but eventually did record it through

a management company adjustment

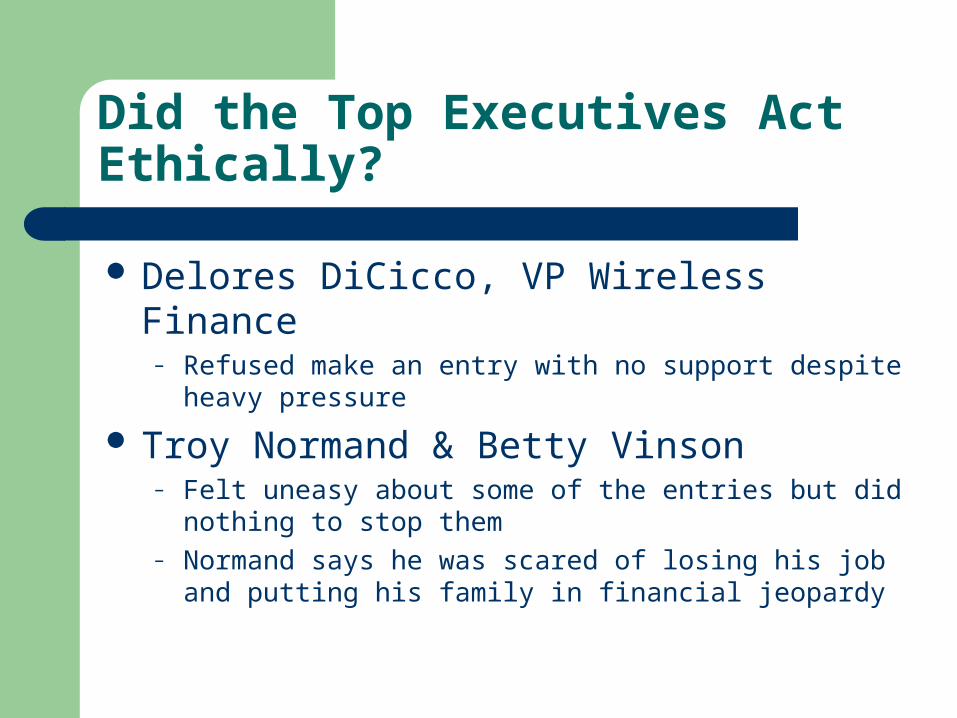

Did the Top Executives Act Ethically?

Delores DiCicco, VP Wireless Finance– Refused make an entry with no support despite heavy

pressure

Troy Normand & Betty Vinson– Felt uneasy about some of the entries but did nothing to stop

them– Normand says he was scared of losing his job and putting his

family in financial jeopardy

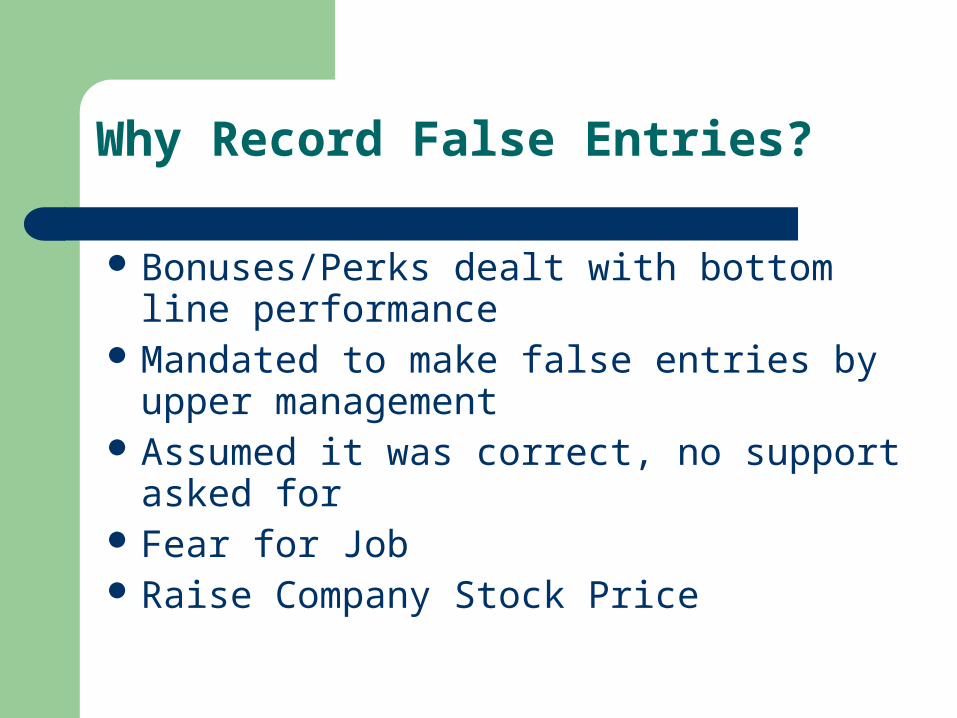

Why Record False Entries?

Bonuses/Perks dealt with bottom line performance

Mandated to make false entries by upper management

Assumed it was correct, no support asked for Fear for Job Raise Company Stock Price

What would you have done?

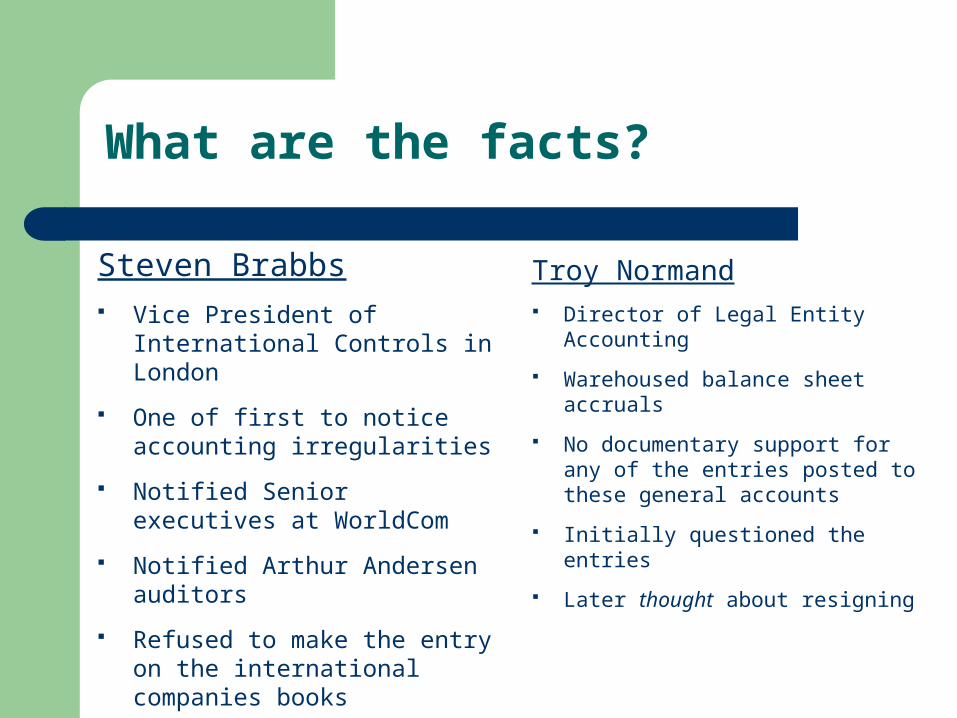

What are the facts?

Steven Brabbs Vice President of International

Controls in London

One of first to notice accounting irregularities

Notified Senior executives at WorldCom

Notified Arthur Andersen auditors

Refused to make the entry on the international companies books

Troy Normand Director of Legal Entity

Accounting

Warehoused balance sheet accruals

No documentary support for any of the entries posted to these general accounts

Initially questioned the entries

Later thought about resigning

What are the Ethical Issues?

Steven Brabbs

Should he make the entry without backup?

Does the entry fairly represent company events?

Who should he inform about the issue?

Troy Normand

Are the accruals appropriate?

Should he have taken a stronger stance?

Who should he inform about the issue?

What are the Alternatives?

Steven Brabbs

Follow corporate orders and make the entry

Make the entry on separate books

Refuse the entry

Report the incident

Resign

Troy Normand

Follow corporate orders and make the entry

Make the entry on separate books

Refuse the entry

Report the incident

Resign

Who are the Primary Stakeholders?

WorldCom Employees

Family Members

Stockholders

Creditors

Arthur Andersen Auditors

What are the Practical Constraints?

Disobeying could prevent future promotions

Difficult to identify when your boss is wrong

Need to support a family

Difficult to blow the whistle on something that you are involved in

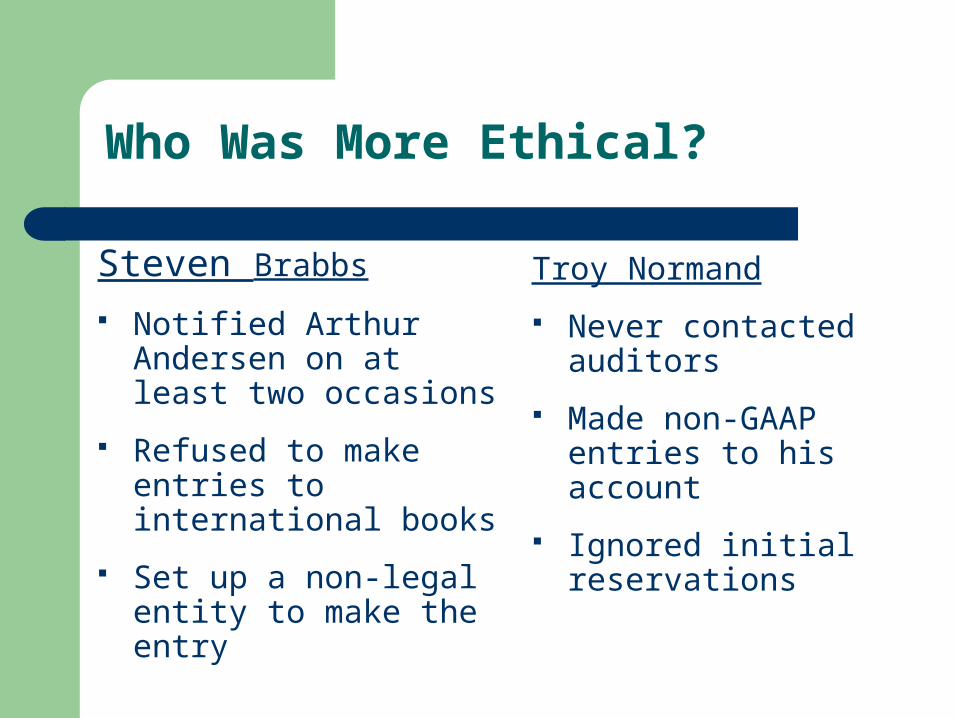

Who Was More Ethical?

Steven Brabbs

Notified Arthur Andersen on at least two occasions

Refused to make entries to international books

Set up a non-legal entity to make the entry

Troy Normand

Never contacted auditors

Made non-GAAP entries to his account

Ignored initial reservations

Internal Auditing

Portray the firm’s financial situation as accurately and truthfully as possible.

Maintain the highest standards of ethical conduct. Disclose fully all relevant information that could reasonably be

expected to influence an intended user’s understanding of the records, comments, and recommendations presented.

Maintain an appropriate level of knowledge and skill (competency).

Refrain from disclosing confidential information except when authorized or required by law (confidentiality).

Avoid conflicts of interest (integrity). Communicate information fairly and objectively (objectivity).

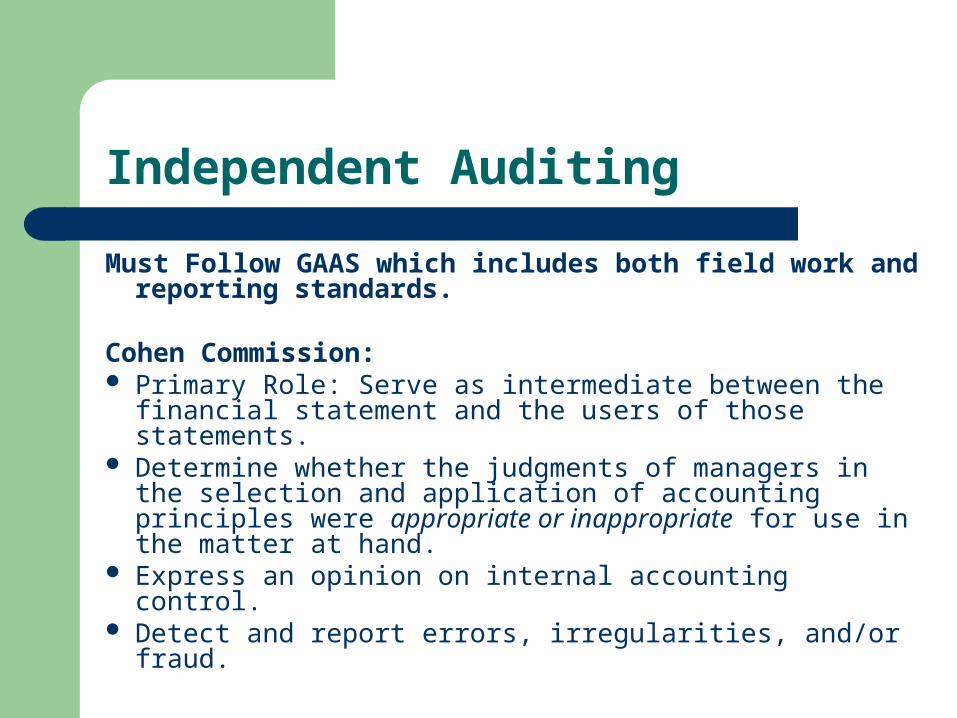

Independent Auditing

Must Follow GAAS which includes both field work and reporting standards.

Cohen Commission: Primary Role: Serve as intermediate between the

financial statement and the users of those statements. Determine whether the judgments of managers in the

selection and application of accounting principles were appropriate or inappropriate for use in the matter at hand.

Express an opinion on internal accounting control. Detect and report errors, irregularities, and/or fraud.

Independent Auditing

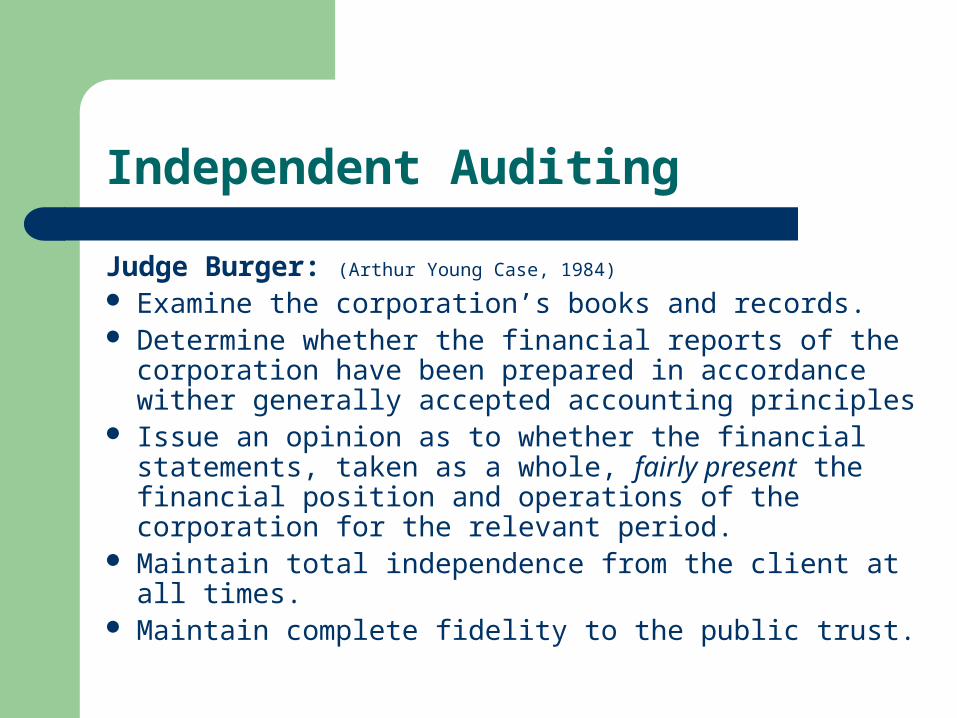

Judge Burger: (Arthur Young Case, 1984)

Examine the corporation’s books and records. Determine whether the financial reports of the

corporation have been prepared in accordance wither generally accepted accounting principles

Issue an opinion as to whether the financial statements, taken as a whole, fairly present the financial position and operations of the corporation for the relevant period.

Maintain total independence from the client at all times. Maintain complete fidelity to the public trust.

Operating Audit vs. Financial Audit

1. Purpose of Audit– Emphasizes effectiveness and

efficiency; concerns operating performance for the future;

2. Distribution of Reports– Reports are intended primarily

for management.

3. Inclusion of nonfinancial areas– Cover any aspect of efficiency

and effectiveness in an organization and involve a wide variety of activities.

– Emphasizes whether historical information was correctly reported; oriented to the past;

– Report typically goes to many users of financial statements.

– Limited to matters that directly affect the fairness of financial statement presentations.

WorldCom’s Internal Auditors and Audit Committee

Internal auditors performed mainly operational audits. Avoided financial audits that might overlap with the work of

external auditors on the grounds of cost savings. Internal Auditors only reported to audit committee at year-end. Reported to Scott Sullivan the rest of the year, who controlled

their promotions, salary increases, bonuses, stock options, and more.

Assignment of “special projects” with no audit purpose, which consumed most of the time of the Internal Audit’s staff.

Audit committee accepted proposed Internal Audit Plan that focused on operational effectiveness and efficiency, systems, and internal controls.

What are the Facts?

Salomon Smith Barney offered 1 million shares of IPOs to WorldCom CEO

Salomon Smith Barney gave WorldCom positive reports despite suspect financials

WorldCom CEO eventually made more than $11 million from trading

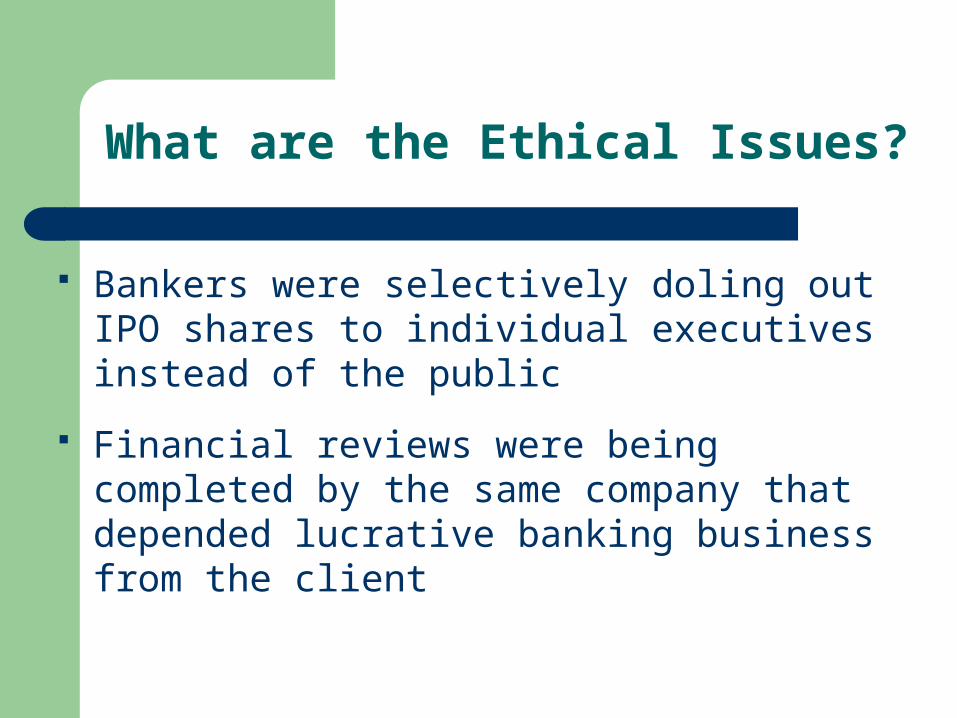

What are the Ethical Issues?

Bankers were selectively doling out IPO shares to individual executives instead of the public

Financial reviews were being completed by the same company that depended lucrative banking business from the client

What are the Alternatives?

Require that clients purchase their stock shares through public forum

Set guidelines for selling IPO shares to clients Disclose financial relationships of clients during

reviews Require holding period for IPO purchases for

clients

Who are the Primary Stakeholders?

Salomon Smith Barney

WorldCom CEO and IPO holder

The general public

The company offering the IPO

Analysts in charge of reviewing WorldCom

What are the Practical Constraints?

Trying to maintain practical professional relationships

Competitive environment pressures institutions to provide incentives

What Actions should be Taken?

IPOs should not be given out selectively by the bank to clients

Analyst reviews of clients should declare that relationship

WorldCom

2002 saw an unprecedented number of corporate scandals: Enron, Tyco, Global Crossing.

WorldCom went from being the nation’s second largest long distance carrier to the brink of bankruptcy as a result of massive fraudulent accounting practices.

WorldCom is another case of failed corporate governance, accounting abuses, and outright greed.

Related Documents