1 RICE UNIVERSITY World Gas Trade Model: Some Implications for South Korea Amy Myers Jaffe Peter Hartley Kenneth B. Medlock III Presented at an International Energy Seminar on Energy Security of Korea for the Next Decades: Economics and Geopolitics Hosted by The Policy Committee, The Uri Party Organized by Korea Energy Economics Institute (KEEI) Convention Hall, Hyundai Capital Building Seoul, South Korea July 22, 2005 James A. Baker III Institute for Public Policy RICE UNIVERSITY

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

RICEUNIVERSITY

World Gas Trade Model:Some Implications for South Korea

Amy Myers JaffePeter Hartley

Kenneth B. Medlock III

Presented at an International Energy Seminar on

Energy Security of Korea for the Next Decades: Economics and Geopolitics

Hosted by

The Policy Committee, The Uri Party

Organized by Korea Energy Economics Institute (KEEI)

Convention Hall, Hyundai Capital Building

Seoul, South Korea

July 22, 2005

James A. Baker IIIInstitute for Public Policy

RICE UNIVERSITY

2

RICEUNIVERSITY

Overview and motivationWorldwide, the demand for natural gas is rising:

Key reasons for the demand increase:Environmental pressure for cleaner fuelsWholesale electricity market competition raised the demand for smaller scale electricity plant, which CCGT satisfied

The share of gas may continue to rise:Gas may supply transport fuel needs (GTL, oil shale, fuel cell)A possible contrary influence is that coal gasification, solar, hydro and/or nuclear power, perhaps assisted by falling costs of HVDC,could displace gas in electricity generation

Source: EIA

Petroleum (45%)

Natural Gas (19%)

Coal (26%)

Hydroelectric (6%)

Nuclear (3%)Renewables, waste (1%)

Petroleum (38%)

Natural Gas (22%)

Coal (27%)

Hydroelectric (7%)

Nuclear (6%)

Renewables, waste (1%)

Petroleum (36%)

Natural Gas (24%)

Coal (25%)

Hydroelectric (7%)

Nuclear (7%)

Renewables, waste (1%)1980 1990 2002

289.05×1015

BTU 351.08×1015

BTU 405.12×1015

BTU

3

RICEUNIVERSITY

Overview and motivationSouth Korea began importing gas in 1986, but gas was < 5% of Korean primary energy demand until 1994 and is now > 10%

South Korea will face more competition for LNG suppliesThere is high growth in energy demand in China and IndiaDeclining North American and North Sea reserves with increasing demand has stimulated actual and planned LNG importFalling LNG shipping costs have expanded the options for suppliers

World gas supply potential is large, but:It is concentrated in areas remote from marketsProduction and transport infrastructure is requiredPrices need to rise in real terms to finance the investmentsUnstable political regimes may make investments unattractive

Russia could be a big supplier of natural gas to both Europe andAsia, making developments there critical

The Rice World Gas Trade Model, based on economic and geological fundamentals, can be used to examine political and economic influences on the world market for natural gas

4

RICEUNIVERSITY

Rice World Gas Trade ModelModel framework: Market Builder from Altos Partners

The model calculates equilibrium prices and quantities across a fixed number of locations and time periods

In each period, gas is produced or transported until there are no opportunities for profitable arbitrage across locationsProducers schedule production to eliminate profitable arbitrage across time periodsSupplies isolated from markets, or in areas lacking infrastructure, earn lower rents and are extracted lastConsumers shift the timing of demand in response to anticipated changes in prices

The supply data is based on the USGS World Resource Assessmentupdated with latest reserve revisions

The econometric model for forecasting demand was developed usingEIA International Energy Outlook 2004, IEA World Energy Outlook 2002 andWorld Bank data on population and economic growth

The demand for natural gas is related to:The level of economic development (GDP/capita)

Following Medlock and Soligo (2001), energy demand increases with GDP/capita but at a decreasing rateBut the natural gas share in primary energy demand also increases with development

PopulationCountry-specific effects reflecting, for example, resource endowment or climatePrices (wholesale industrial $/BTU) of natural gas, oil and coal

5

RICEUNIVERSITY

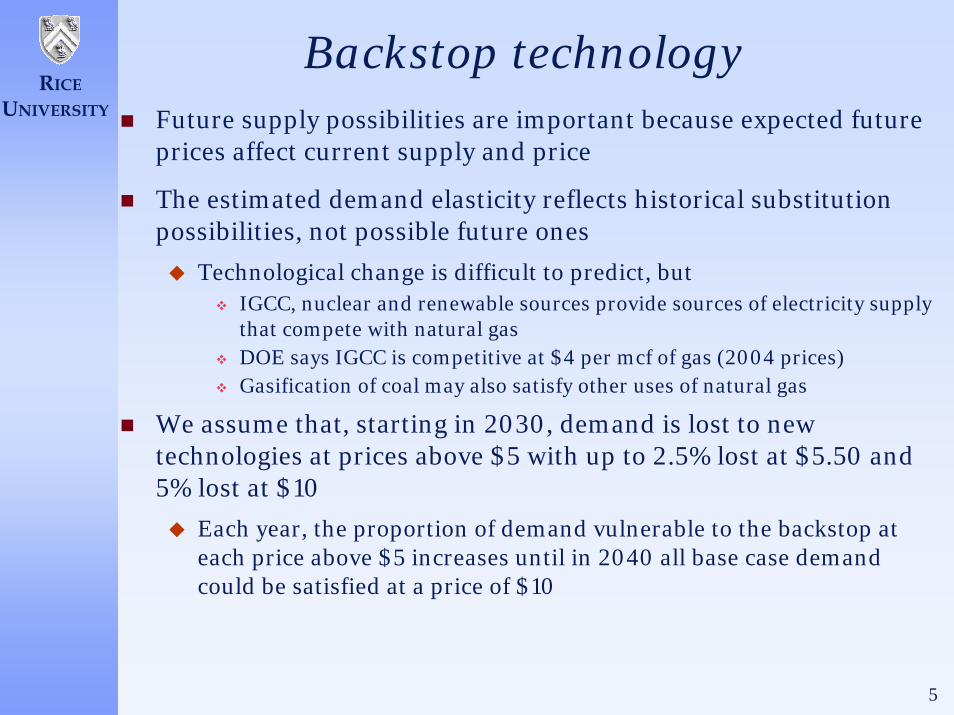

Backstop technologyFuture supply possibilities are important because expected future prices affect current supply and price

The estimated demand elasticity reflects historical substitutionpossibilities, not possible future ones

Technological change is difficult to predict, butIGCC, nuclear and renewable sources provide sources of electricity supply that compete with natural gas DOE says IGCC is competitive at $4 per mcf of gas (2004 prices)Gasification of coal may also satisfy other uses of natural gas

We assume that, starting in 2030, demand is lost to new technologies at prices above $5 with up to 2.5% lost at $5.50 and 5% lost at $10

Each year, the proportion of demand vulnerable to the backstop at each price above $5 increases until in 2040 all base case demandcould be satisfied at a price of $10

6

RICEUNIVERSITY

More detail on supplyRegional resource potential of

associated and unassociated natural gas resources,

both conventional and unconventional gas deposits in North America and Australia (CBM), and

conventional gas deposits in the rest of the world

was assessed in three categories:

proved reserves (2003 Oil & Gas Journal estimates)

growth in known reserves (P-50 USGS estimates)

undiscovered resource (P-50 USGS estimates)

Cost estimates for North America (including Canada and Mexic0) were applied elsewhere based on geological characteristics

The North American estimates (developed by Altos & USGS) include:capital cost of development,operating and maintenance costs, andcost changes by region and deposit type as resources deplete

7

RICEUNIVERSITY

Example cost of supply curves

0

5

10

15

20

25

0 500 1000 1500 2000 2500

Cumulative Reserve Additions (Quadrillion BTU)

Alaska Qatar Saudi Arabia Iran West Siberia

Comparative Cost of Supply Curves for Selected Regions

Sources: USGS, EIA, author calculations

8

RICEUNIVERSITY

Technological change in mining

Technology Curves in the Resource Extraction IndustriesPercentage of Initial Cost

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

CAPEX OPEX

Source: Adapted from "Balancing Natural Gas Policy" National Petroleum Council, 2003

9

RICEUNIVERSITY

Linking supply with demand

10

RICEUNIVERSITY

Representing transport networksThe model examines a world market of expanding depth and geographical extent

North American, European pipeline networks are now the main transport systems

LNG is only about 5% of world demand, but is important in Japan & Korea, and increasing elsewhere

To allow calculations, supplies and demands are aggregated into discrete “nodes”, parallel pipes are aggregated into a single link, and minor distribution and gathering pipes are ignored

Transport links are inherently discrete

We allow many potential pipeline links including ones that have been discussed and others that might appear profitable at prices calculated in initial iterations of the model

A hub and spoke representation is used for LNG to allow many potential trading partnersWhile bilateral contracts now dominate LNG trade, the market is becoming more flexibleDecreasing distances between suppliers and customers increases arbitrage opportunitiesContracts are financial arrangements that do not necessarily constrain physical trades

Contracts can be fulfilled by swap agreements as increased market depth increases trading options

The model chooses new or expanded transport capacity from supply sources to demand sinks based on:

capital costs of expansion, and

operating and maintenance costs of new and existing capacity

11

RICEUNIVERSITY

Pipeline costs

EIA published cost data for 52 pipeline projects

Using this data, we estimated a regression relating specific capital cost (annual cost per unit of capacity) to project characteristics

Project cost is raised by:Length of the pipelineCrossing mountainsMoving offshore or crossing a lake or seaDeveloping in more populous areas

Higher capacity reduces per unit costs as a result of scale economies

12

RICEUNIVERSITY

LNG transportation network

13

RICEUNIVERSITY

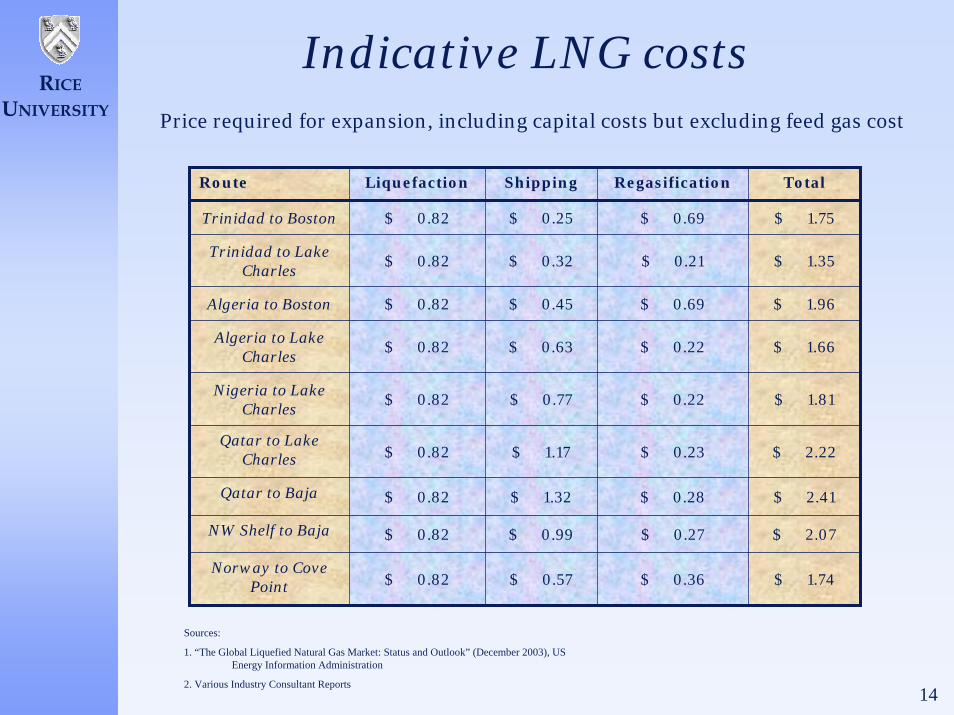

LNG costs

Consulted a variety of sources (including a 2003 EIA report and industry contacts)

Shipping costs split into a fixed capital cost for ship development plus operating costs of:

2.25% of fixed cost of developmentfuel use during transit (0.15% per day)

Liquefaction costs are a fixed cost ($4.11/mcf/yr) plus a variable feed gas cost (model calculated)

Regasification costs vary by location (primarily because land costs vary)

14

RICEUNIVERSITY

Indicative LNG costsPrice required for expansion, including capital costs but excluding feed gas cost

Route Liquefaction Shipping Regasification Total

Trinidad to Boston $ 0.82 $ 0.25 $ 0.69 $ 1.75

Trinidad to Lake Charles

$ 0.82 $ 0.32 $ 0.21 $ 1.35

Algeria to Boston $ 0.82 $ 0.45 $ 0.69 $ 1.96

Algeria to Lake Charles

$ 0.82 $ 0.63 $ 0.22 $ 1.66

Nigeria to Lake Charles

$ 0.82 $ 0.77 $ 0.22 $ 1.81

Qatar to Lake Charles $ 0.82 $ 1.17 $ 0.23 $ 2.22

Qatar to Baja $ 0.82 $ 1.32 $ 0.28 $ 2.41

NW Shelf to Baja $ 0.82 $ 0.99 $ 0.27 $ 2.07

Norway to Cove Point $ 0.82 $ 0.57 $ 0.36 $ 1.74

Sources:

1. “The Global Liquefied Natural Gas Market: Status and Outlook” (December 2003), US Energy Information Administration

2. Various Industry Consultant Reports

15

RICEUNIVERSITY

Technological change in LNGLNG transport, liquefaction, and regasification capital and O&M costs are expected to decline

Rates of change in the model are based on a statistical fit to WEIO rates

$-

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

$16.00

1995 2000 2005 2010 2015 2020 2025 2030 2035 2040

$/mcf

Total

Regasification

Liquefaction

Shipping

LNG Capital Costs$/MMBtu/yr

Source: World Energy Investment Outlook, 2003 , International Energy Agency

16

RICEUNIVERSITY

Selected price projections

2002 2006 2010 2014 2018 2022 2026 2030 2034 2038$0

$1

$2

$3

$4

$5

$6

$7

$8

Henry Hub

Beijing

Tokyo

Zeebrugge

Buenos Aires

Delhi

Seoul

Source: RWGTM, Hartley and Medlock (2005)

17

RICEUNIVERSITY

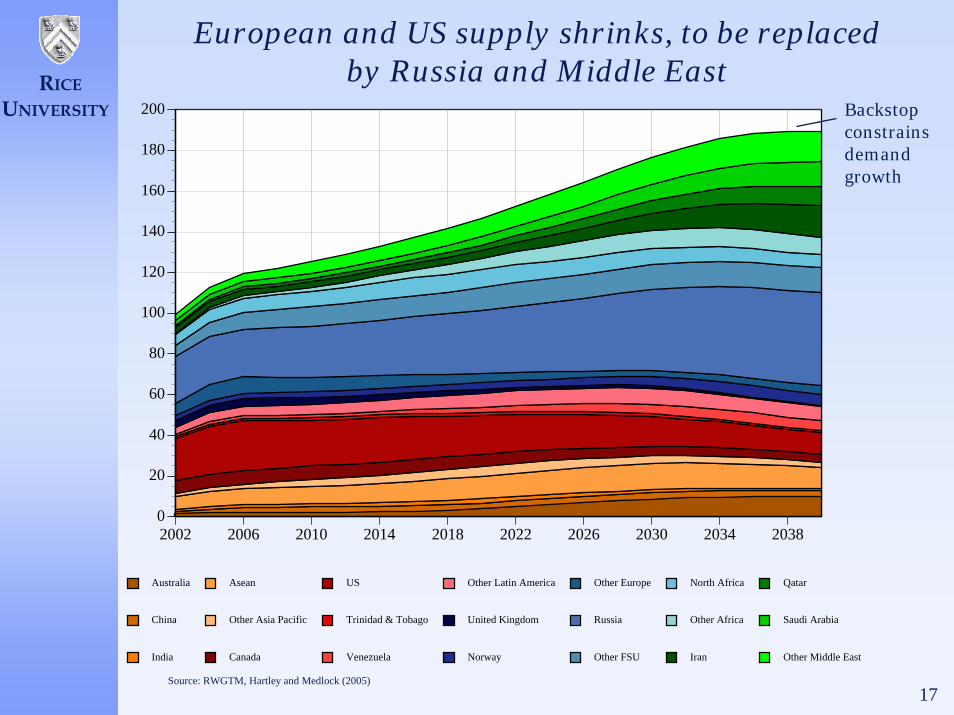

European and US supply shrinks, to be replaced by Russia and Middle East

2002 2006 2010 2014 2018 2022 2026 2030 2034 20380

20

40

60

80

100

120

140

160

180

200

Australia

China

India

Asean

Other Asia Pacific

Canada

US

Trinidad & Tobago

Venezuela

Other Latin America

United Kingdom

Norway

Other Europe

Russia

Other FSU

North Africa

Other Africa

Iran

Qatar

Saudi Arabia

Other Middle East

Source: RWGTM, Hartley and Medlock (2005)

Backstop constrains demand growth

18

RICEUNIVERSITY

Demand projections

2002 2006 2010 2014 2018 2022 2026 2030 2034 20380

20

40

60

80

100

120

140

160

180

200

Australia

China

India

Japan

Asean exporters

Asean importers

Other Asia Pacific

Canada

US

Brazil

Mexico

Venezuela

Other Latin America

France

Germany

Italy

Spain

United Kingdom

Other Europe

Russia

Other FSU

Africa

Iran

Saudi Arabia

Other Middle East

Source: RWGTM, Hartley and Medlock (2005)

19

RICEUNIVERSITY

Natural gas trades

2002 2006 2010 2014 2018 2022 2026 2030 2034 2038-80

-60

-40

-20

0

20

40

60

80

China

India

Japan

Asean importers

Other Asia Pacific

US

Mexico

France

Germany

Italy

Spain

United Kingdom

Other Europe/FSU

Australia

Asean exporters

Canada

Venezuela

Norway

Russia

North Africa

Other Africa

Iran

Qatar

Saudi Arabia

Other Middle East

Other Latin America

Exports

Imports

Source: RWGTM, Hartley and Medlock (2005)

20

RICEUNIVERSITY

LNG exports to come from higher risk sources

2002 2006 2010 2014 2018 2022 2026 2030 2034 20380

10

20

30

40

50

60

Australia

Indonesia

Malaysia

Papua New Guinea

Other Pacific Basin

Qatar

Iran

UAE

Saudia Arabia

Other Middle East

North Africa

Nigeria

Equitorial Guinea

Angola

Greenland

Russia Atlantic

Venezuela

Other Atlantic Basin

Pacific

Mid-East

Atlantic

Source: RWGTM, Hartley and Medlock (2005)

21

RICEUNIVERSITY

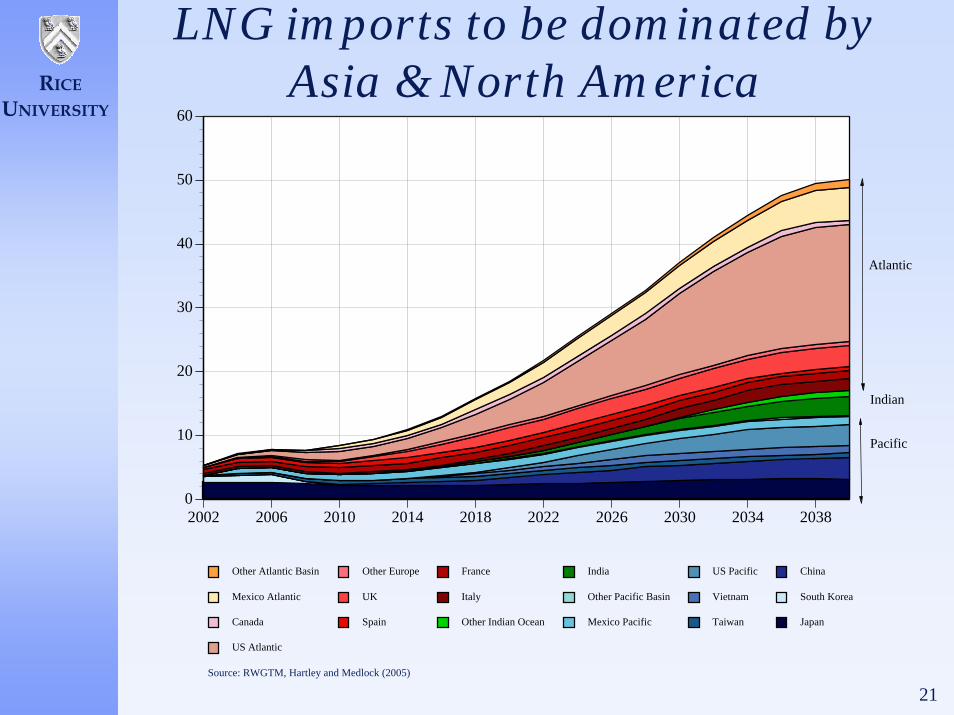

LNG imports to be dominated by Asia & North America

2002 2006 2010 2014 2018 2022 2026 2030 2034 20380

10

20

30

40

50

60

Japan

South Korea

China

Taiwan

Vietnam

US Pacific

Mexico Pacific

Other Pacific Basin

India

Other Indian Ocean

Italy

France

Spain

UK

Other Europe

US Atlantic

Canada

Mexico Atlantic

Other Atlantic Basin

Pacific

Indian

Atlantic

Source: RWGTM, Hartley and Medlock (2005)

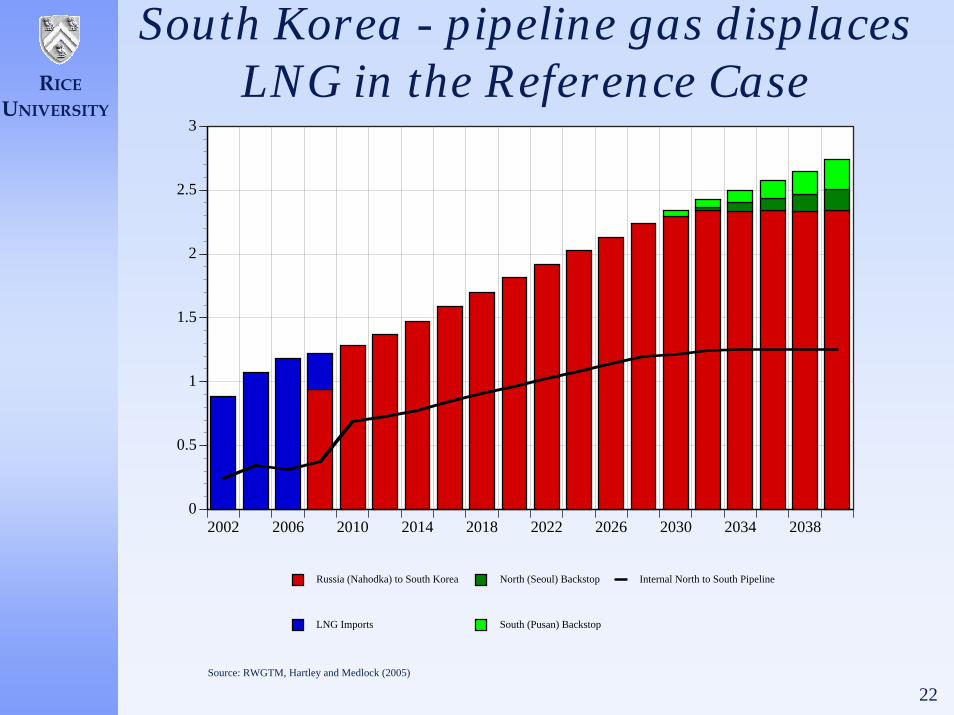

22

RICEUNIVERSITY

South Korea - pipeline gas displaces LNG in the Reference Case

2002 2006 2010 2014 2018 2022 2026 2030 2034 20380

0.5

1

1.5

2

2.5

3

Russia (Nahodka) to South Korea

LNG Imports

North (Seoul) Backstop

South (Pusan) Backstop

Internal North to South Pipeline

Source: RWGTM, Hartley and Medlock (2005)

23

RICEUNIVERSITY

Some implications of the Reference CaseRussia becomes a major force in the global gas market

Russian pipeline gas continues to be important for EuropeRussia also becomes a major supplier of natural gas to China, Korea and Japan

Japan continues to import LNG as the high cost of a national gas grid is prohibitiveUltimately, gas is also piped east from West SiberiaKorea shifts to pipeline gas from Russia and stops importing LNGIn consequence, Seoul prices fall from approximating Tokyo prices to approximating Beijing prices

Russia also enters the LNG market possibly supplying the US“Net-back” prices in Russia have to be equilibrated

Over the period from 2002-2040 Australia, Qatar and Indonesia are the largest suppliers ofLNG (>40% of total), but in 2040 Iran, Russia and Saudi Arabia join Australia and Qatar to supply more than 60% of LNG exports

Russian pipeline gas exports to Europe and Asia make Russia the dominate exporter overall

Other long-haul international pipelines are constructedThe trans-Saharan pipeline (Nigeria to Algeria) is constructed in 2012India imports Iranian gas via pipeline from 2020Europe also imports gas from the Middle East via Turkey in substantial amounts from 2020A pipeline from West Siberia to East Siberia is constructed in the mid 2030’s to supply NE Asia

North America becomes a major importer of LNGAlaska gas serves only to replace declines in other North American production having no dramatic impact on pricesGas prices in the US eventually exceed prices in JapanRussia, Middle East, Australia retain low gas prices

South American gas is consumed primarily in South AmericaTrinidad LNG export growth is limited to the near term, but Venezuela is significant laterBrazil imports Bolivian and Venezuelan suppliesArgentina imports Bolivian supplies and becomes an LNG importer

A backstop technology is implemented almost everywhere by 2040, but is used most heavily in the US, western Europe and Japan

24

RICEUNIVERSITY

Will Russia Continue to Increase its Oil and Gas Exports?

Sustainable Russian export growth depends on removing major bottlenecks in

Eastern Siberia

Northern route to Barent’s Sea for ocean bound movements by ultra large tankers

Bypass to Bosporus Strait

State control in pipeline sector unlikely to change

Problem of financing –state funds and higher tariffs unlikely to be enough

Outside investors?

State Stabilization Fund?

25

RICEUNIVERSITY

Putin reasserting government control over Russia’s natural resources

Philosophy dates back to late 1990s

Believes in a mixed system of state and private ownership in assets but state protecting the interests of the nation

Since early 2004, new appointments of like minded officials to cabinet, presidential administration and state oil and gas firms

Many have background that includes service in state security organs

Sea change likely to affect business model for Russian industry

New round of redistribution of petroleum assetsCorporate responsibility a la Russe; need to follow “unwritten rules” to succeed in RussiaThese rules involve limits to Western involvement and Western style managementKremlin decides export routes

26

RICEUNIVERSITY

Geopolitical Trends1. Russia actively being courted by U.S., China, Japan,

Europe Kremlin as a moderator of global prices?

2. Kremlin’s plans for industry reorganization is dampening level of increase by disrupting speedy implementation of plans to remove infrastructure constraints or if it causes a slow down in capital expenditures and project development

3. Russia worried about fate of eastern regionsEmigration a demographic threat to Russia’s sovereigntyFears of splintering of oil-rich distant regionsWants to use East Siberian resources to spur local economic develop; many in the Kremlin take a Russia first attitude towards energy resources

4. Energy as key plank to Russia’s diplomacy in AsiaRussia wants to speed up integration process with Asia Pacific but pipeline routing remains an economic and diplomatic problem, but political/diplomatic problems surrounding the routing question remain to be tackled

27

RICEUNIVERSITY

Two scenario analyses

1. Pipelines from Nahodka & NE China through North Korea are blocked

Political relations with North Korea prevent them

An undersea pipeline to South Korea from China can still be built

Connections between South Korea and Japan are also permitted, but these are too expensive to use

2. Russia to China pipelines also don’t get built

Political difficulties may also prevent this developmentWe also rule out the pipeline from Uzbekistan to China

It otherwise provides an indirect route for gas sales from the Volga-Urals region in Russia to China

Sakhalin pipeline to Japan still is possible

28

RICEUNIVERSITY

No North Korea pipes: LNG and China pipeline share South Korean market more equally

2002 2006 2010 2014 2018 2022 2026 2030 2034 20380

0.5

1

1.5

2

2.5

3

LNG Imports

China to South Korea (undersea)

North (Seoul) Backstop

South (Pusan) Backstop

Internal North to South Pipeline

29

RICEUNIVERSITY

No North Korea pipes:Changes in Selected Prices

2002 2006 2010 2014 2018 2022 2026 2030 2034 2038$-1.5

$-1.0

$-0.5

$0.0

$0.5

$1.0

$1.5

Henry Hub

Beijing

Tokyo

Zeebrugge

Buenos Aires

Delhi

Seoul

Price zig-zag results from earlier construction of a pipeline (2006 instead of 2008). The price is lowered below the reference case price in 2006, and no longer falls in 2008 as the reference price does.

30

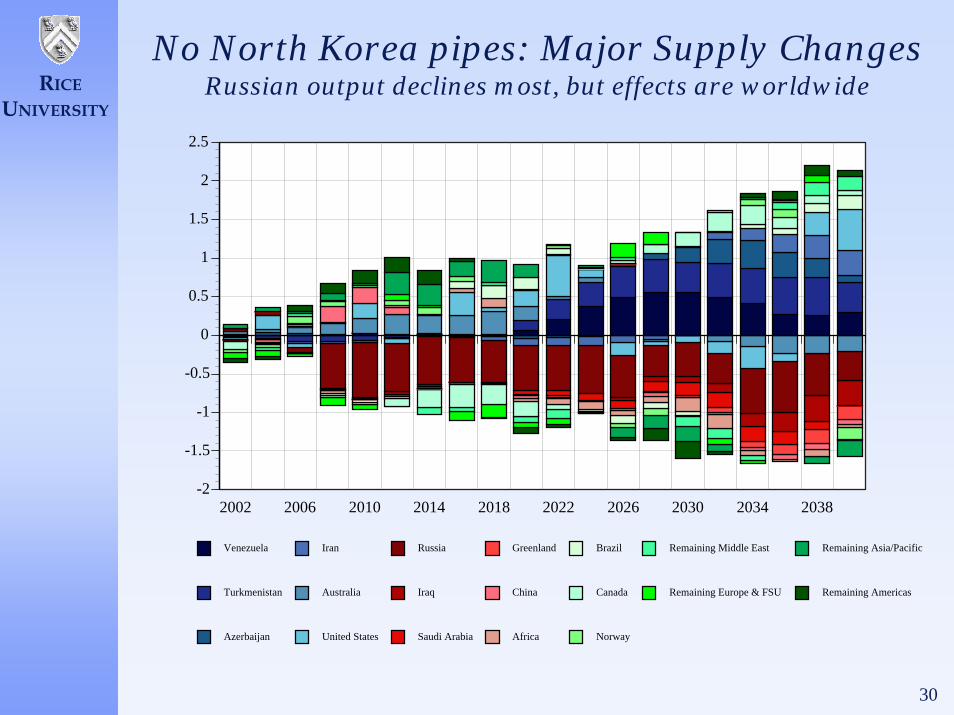

RICEUNIVERSITY

No North Korea pipes: Major Supply ChangesRussian output declines most, but effects are worldwide

2002 2006 2010 2014 2018 2022 2026 2030 2034 2038-2

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

Venezuela

Turkmenistan

Azerbaijan

Iran

Australia

United States

Russia

Iraq

Saudi Arabia

Greenland

China

Africa

Brazil

Canada

Norway

Remaining Middle East

Remaining Europe & FSU

Remaining Asia/Pacific

Remaining Americas

31

RICEUNIVERSITY

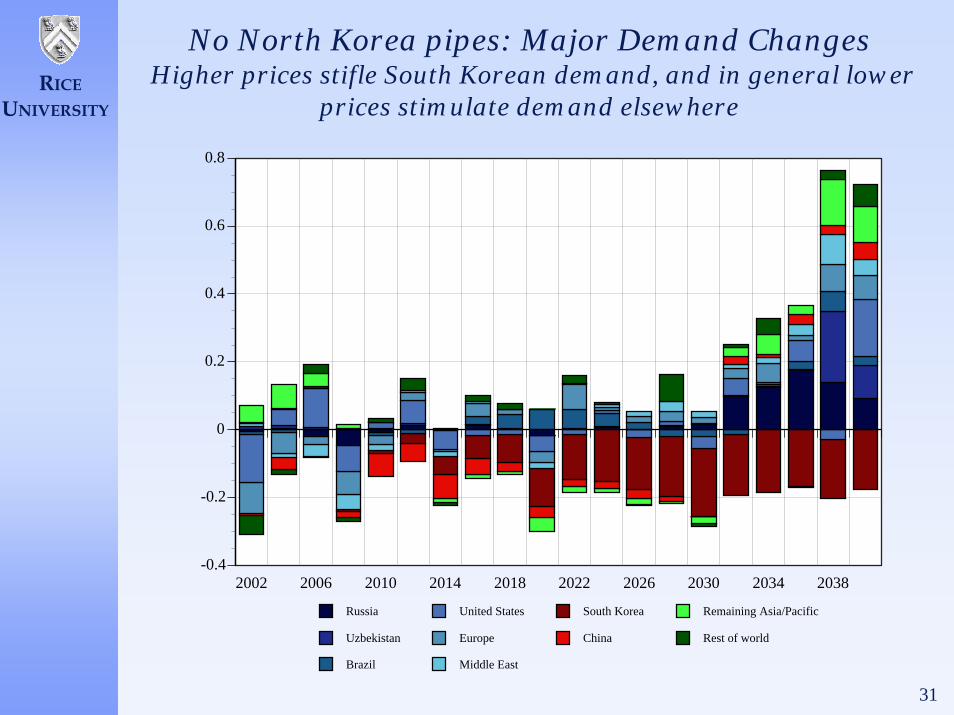

No North Korea pipes: Major Demand ChangesHigher prices stifle South Korean demand, and in general lower

prices stimulate demand elsewhere

2002 2006 2010 2014 2018 2022 2026 2030 2034 2038-0.4

-0.2

0

0.2

0.4

0.6

0.8

Russia

Uzbekistan

Brazil

United States

Europe

Middle East

South Korea

China

Remaining Asia/Pacific

Rest of world

32

RICEUNIVERSITY

No North Korea pipes: Major Changes in LNG SupplyMore Sakhalin gas is now exported as LNG, beating out other LNG

from Australia and Saudi after 2030

2002 2006 2010 2014 2018 2022 2026 2030 2034 2038-1.5

-1

-0.5

0

0.5

1

1.5

2

Russia Pacific

Venezuela

Iran

Papua New Guinea

Brunei

Indonesia

Egypt

Qatar

Philippines

Russia Atlantic

Australia

Greenland

Nigeria

Malaysia

Saudia Arabia

Remaining

33

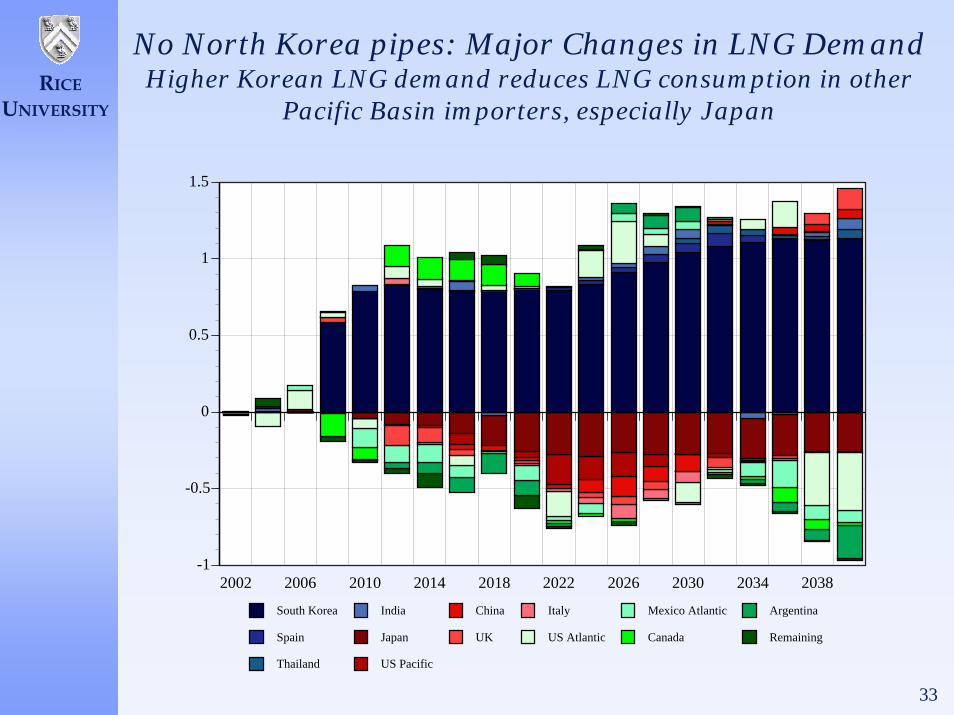

RICEUNIVERSITY

No North Korea pipes: Major Changes in LNG Demand Higher Korean LNG demand reduces LNG consumption in other

Pacific Basin importers, especially Japan

2002 2006 2010 2014 2018 2022 2026 2030 2034 2038-1

-0.5

0

0.5

1

1.5

South Korea

Spain

Thailand

India

Japan

US Pacific

China

UK

Italy

US Atlantic

Mexico Atlantic

Canada

Argentina

Remaining

34

RICEUNIVERSITY

China & Korea pipes off: Effects on Korean Supplies LNG beats a potential Sakhalin-Japan-Korea pipe

2002 2006 2010 2014 2018 2022 2026 2030 2034 20380

0.5

1

1.5

2

2.5

3

LNG Imports

North (Seoul) Backstop

South (Pusan) Backstop

Internal North to South Pipeline

35

RICEUNIVERSITY

China & Korea pipes off:Changes in Selected Prices

2002 2006 2010 2014 2018 2022 2026 2030 2034 2038$-1.0

$-0.5

$0.0

$0.5

$1.0

$1.5

Henry Hub

Beijing

Tokyo

Zeebrugge

Buenos Aires

Delhi

Seoul

36

RICEUNIVERSITY

China & Korea pipes off:Major Supply ChangesNow higher overall LNG demand allows main LNG

exporters (Australia, Iran, Qatar, Indonesia) to expand

2002 2006 2010 2014 2018 2022 2026 2030 2034 2038-3

-2.5

-2

-1.5

-1

-0.5

0

0.5

1

1.5

2

Australia

Iran

Azerbaijan

Qatar

United States

Indonesia

China

Russia

Saudi Arabia

Greenland

Nigeria

Iraq

Canada

Norway

Turkmenistan

Venezuela

Remaining

37

RICEUNIVERSITY

China & Korea pipes off: Major Demand ChangesNow Chinese demand decline exceeds the Korean one; remaining

Pacific Basin importers are again adversely affected

2002 2006 2010 2014 2018 2022 2026 2030 2034 2038-1.4

-1.2

-1

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

Russia

Remaining FSU

Middle East

China

South Korea

Remaining Asia Pacific

United States

Canada & Mexico

Africa

Europe

South America

38

RICEUNIVERSITY

China & Korea pipes off: Major Changes in LNG SupplyAgain Sakhalin LNG exports rise, but now the overall LNG market

expands enough that few LNG exports decline

2002 2006 2010 2014 2018 2022 2026 2030 2034 2038-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

3

3.5

Russia Pacific

Australia

Remaining Pacific Basin

Iran

Saudia Arabia

Qatar

Remaining Middle East

Greenland

Nigeria

Russia Atlantic

Venezuela

Remaining Atlantic Basin

39

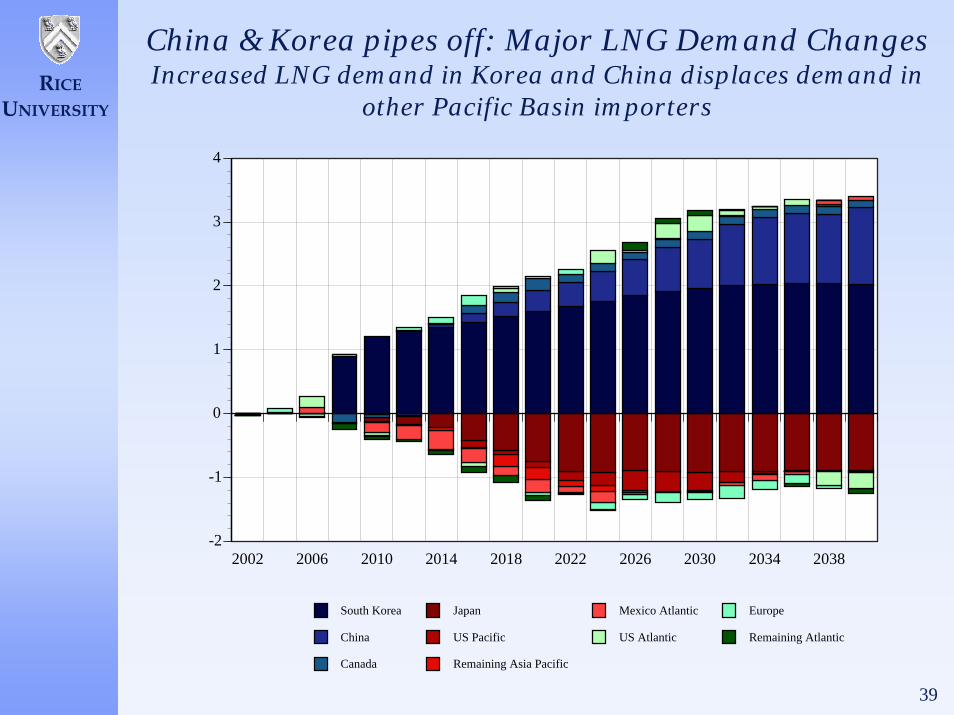

RICEUNIVERSITY

China & Korea pipes off: Major LNG Demand ChangesIncreased LNG demand in Korea and China displaces demand in

other Pacific Basin importers

2002 2006 2010 2014 2018 2022 2026 2030 2034 2038-2

-1

0

1

2

3

4

South Korea

China

Canada

Japan

US Pacific

Remaining Asia Pacific

Mexico Atlantic

US Atlantic

Europe

Remaining Atlantic

40

RICEUNIVERSITY

Some implications of the ResultsIn the coming worldwide market for natural gas, political disturbances in one area have global effects

The results illustrate the key role Russia will play in the future world gas market

Russia not only has a lot of gasIt also is strategically placed to ship gas either east or west and hence in a position to arbitrage between European and Asian marketsToward the end of the horizon, Russia also becomes a significantexporter of LNG, thus helping to solidify the link between LNG prices and pipeline gas prices around the world

North America and the Middle East also link Pacific and Atlanticgas markets

Middle East producers can export LNG east or west, and also can ship gas via pipeline to Europe or the Indian sub-continentIn North America, if Pacific Basin gas prices rise, more Atlantic Basin LNG is imported and the arbitrage point moves toward the west coast

A final point more specific to the Korean experiments is that Japan is a close competitor to South Korea for Pacific Basin LNGand increased Korean demand raises Japanese prices

41

RICEUNIVERSITY

References for further informationDetails on the construction of the model can be found in the paper:

Hartley and Medlock (2005a), “The Baker Institute World Gas Trade Model”, available at

http://www.rice.edu/energy/publications/docs/GAS_BIWGTM_March2005.pdf

Other scenarios are discussed in the companion paper:

Hartley and Medlock (2005b), “Political and Economic Influences on the Future World Market for Natural Gas”, available at

http://www.rice.edu/energy/publications/docs/GAS_PoliticalEconomicInfluences.pdf

The model of economic development and energy demand is explained further in:

Medlock and Soligo (2001), “The Composition and Growth in Energy Demand in China”, available at

http://www.rice.edu/energy/publications/docs/AsianEnergySecurity_CompositionGrowthEnergyDemandChina.pdf

Related Documents