World Bank’s Energy Week Washington DC, 6 March 2006 Natural gas:”bridging fuel “ for the next decades A global perspective Marcel Kramer, Chairman and CEO Gasunie, The Netherlands

World Banks Energy Week Washington DC, 6 March 2006 Natural gas:bridging fuel for the next decades A global perspective Marcel Kramer, Chairman and CEO.

Dec 10, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

World Bank’s Energy WeekWashington DC, 6 March 2006

Natural gas:”bridging fuel “ for the next decadesA global perspective

Marcel Kramer, Chairman and CEO Gasunie, The Netherlands

Global trends

• Fuel demand increases steadily

Total Energy Demand by Region 2002 and 2030

0

500

1000

1500

2000

2500

3000

3500

USAEU

-25

Japa

n/Ko

rea

Indi

a

China

Russia

Latin

Am

erica

Africa

Mid

dle

East

Mto

e 2002

2030

Regional shares in world primary energy demand

Two-thirds of increase in world demand in 2003 - 2030 comes from developing countries, especially in Asia

62%51%

42%

16%

10%

9%

22%39%

49%

0%

20%

40%

60%

80%

100%

1971 2003 2030

OECD Transition economies Developing countries

Global energy demand: forecast IEA

Gas demand is expected to grow faster than total energy demand……

100

118

139

159

54

100

123

157

187

41

1971 2002 2010 2020 2030

Total primary energy

Gas

Reference yearIndex=100

Global energy demand: forecast IEA

Global trends

• Fuel demand increases steadily

• Gas is a relatively low CO2 emittor

Power generation is a major driver of the growth in gas demand

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

1971 2002 2010 2020 2030

Mto

e

54

100

118

139

159

187157

123

41

TOTAL PRIMARY ENERGY

Gas for

Power

Gas for other market segments

Global energy demand: forecast IEA

Life-cycle CO2 emissions from Power Plants

Sources: life-cycle assessment of electricity generation systems and applications for climate change policy analysis, Meier, 2002, published on website Nuclear Energy Institute; own data; IEA

0100200300400500600700800900

10001100

gra

m/k

Wh

coalgas

gas, CCGT

wind

nuclear

hydro

biomass

geothermal

solar pv

CCGT as Back UP

spread due to type of coal (lignite/hard coal) and technology (old/new-high-efficiency)

Global trends

• Fuel demand increases steadily

• Gas is a relatively low CO2 emittor

• Large world gas reserves

Data: BP Statistical Review 2005

North America

2.5

South and Central America

2.5

1.8

Europe

Africa

4.9

Middle East

25.7

Russia

Asia Pacific Region

16.9

4.9

Proven reserves: 6,354 trillion cubic feet .Shown in 1000 TCF:

Current proven gas reserves equivalent of 67 years gas consumption (level 2004)

Global trends

• Fuel demand increases steadily

• Gas is a relatively low CO2 emittor

• Large world gas reserves

• Increased oil and gas prices

Gas price linkage to oil price

• Gas and Oil remain substitutes in major parts of the energy market

• Important parts of industry dual-fired• Large hedging users prefer oil-related gas prices• Upstream shackles of the gas and oil chains are very

similar

Gas Prices will remain linked to oil prices, but with their own volatility

Global trends

• Fuel demand increases steadily

• Gas is a relatively low CO2 emittor

• Large world gas reserves

• Increased oil and gas prices

• LNG projects allow for global competition in gas

LNG

• Gas importing regions will have to compete for supply

• LNG market still small (6,5% of gas is traded as LNG)

• Bottlenecks in LNG-chains till 2008 – 2010

• many large projects in execution phase

• Global price level of natural gas is so high that LNG is competitive wherever it originates from

• Traditional gas supply patterns (Russian gas to Europe, Mid Eastern gas to Pacific Rim, North America autarctic) will give way

Global trends

• Fuel demand increases steadily

• Gas is a relatively low CO2 emittor

• Large world gas reserves

• Increased oil and gas prices

• LNG projects allow for global competition in gas

• Markets develop to more competition and short-term contracts

Will world gas prices become more aligned?

Benchmark World Gas Prices

$1

$2

$3

$4

$5

$6

$7

$8

$9

$10

$ /

MM

BT

U

US Henry HubJapan LNG, RegasifiedUK National Balancing PointContinental Europe Indicator

Source: M. Speltz, Chevron, sept 2005

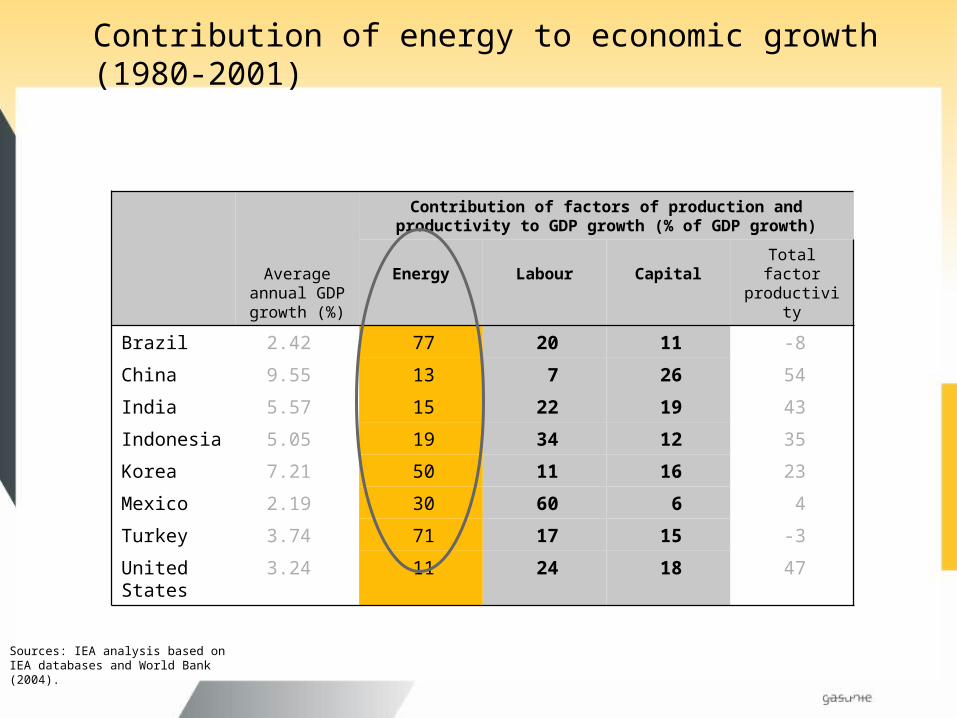

Contribution of energy to economic growth (1980-2001)

Average annual GDP growth (%)

Contribution of factors of production and productivity to GDP growth (% of GDP growth)

Energy Labour CapitalTotal factor productivity

Brazil 2.42 77 20 11 -8

China 9.55 13 7 26 54

India 5.57 15 22 19 43

Indonesia 5.05 19 34 12 35

Korea 7.21 50 11 16 23

Mexico 2.19 30 60 6 4

Turkey 3.74 71 17 15 -3

United States 3.24 11 24 18 47

Sources: IEA analysis based on IEA databases and World Bank (2004).

Conclusions

• Energy supply important driver behind economic growth• Gas is attractive fuel option

– Low Co2 emissions – Global market– LNG opens non-traditional gas markets – Large global gas reserves– Rapid growing gas market fosters liquidity and transparency

• Expanding gas infrastructure is pre-requisite for well functioning global gas market

• This requires a stimulating policy and regulatory framework: – predictable – consistent – transparent

Related Documents