Page INDONESIA THE RISE OF METROPOLITAN REGIONS: TOWARDS INCLUSIVE AND SUSTAINABLE REGIONAL DEVELOPMENT Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Page

INDONESIA

THE RISE OF METROPOLITAN REGIONS:

TOWARDS INCLUSIVE AND SUSTAINABLE REGIONAL DEVELOPMENT

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

wb406484

Typewritten Text

71740

wb406484

Typewritten Text

i

PREFACE In recent years, Indonesia has made great strides in economic growth and development. This growth has

been accompanied by rapid urbanization that has transformed Indonesian cities. Urbanization has the

potential to boost national economic growth by facilitating the emergence of agglomeration and

localization economies. Increasing urbanization presents Indonesia with an opportunity to leverage the

transformation taking place to ensure that it is harnessed for economic growth and, more importantly,

sustained improvements in the quality of life of its community members.

To ensure that urbanization and demographic growth generate optimal levels of economic growth, the

Government of Indonesia (GOI) needs to foster the development of agglomeration and localization

economies. In turn, these economies can drive increases in the economic productivity of cities and

metropolitan regions. At the national level, Indonesia needs an overall national urban development

strategy for guiding local activities and for fostering effective sub-national government coordination of

development plans and activities.

Unfortunately, research shows that over the last four decades, Indonesia has not derived optimal returns on

urban development, as can be seen by comparisons with the level of benefit derived by other Asian

countries passing through similar processes of urbanization. Urbanization in Indonesia is driving the

emergence of metropolitan areas whose boundaries stretch beyond the jurisdiction of administratively

defined cities, creating an urgent need for mechanisms that optimize and coordinate development beyond

the formal city unit.

The spatial structure of urban growth and development will critically shape the rate and quality of

economic growth over the next 15 years. This structure wil determine the quality of life for urban dwellers

and define the level of competitiveness of Indonesia‘s cities. To foster productive economic clusters of

economic activity, the GOI needs to encourage efficient urban spatial structures; appropriate and timely

investments in critical large-scale infrastructure in cities; the provision of spatially comprehensive basic

services; effective urban management; strengthening of institutional capacity; and proactive horizontal and

vertical coordination of local government actions.

The purpose of this report on Indonesia‘s regional and urban development is to provide a comprehensive

assessment of the country‘s spatial patterns of urbanization and economic development and to evaluate

the extent to which Indonesia‘s urbanization has fostered increases in agglomeration economies and

economic productivity growth. The study provides the analytical work to evaluate such performance and to

identify key issues, constraints and opportunities for promoting faster and more inclusive growth. The

overarching goal of the study is to provide a timely and rigorous analysis of regional and urban

development in order to foster informed policy discussion at the central, provincial and local government

levels.

Page ii

ACKNOWLEDGEMENTS This study on Indonesia‘s regional and urban economic development was funded by AusAID, the Swiss

Economic Development Cooperation, and the World Bank. The team conducted a series of in-depth case

studies of Indonesia‘s national urban planning laws, case studies on transportation and inter-city

connectivity, access to local water and sanitation services, local roads, and metro-level case studies of

Jakarta, Makassar, Medan and Surabaya. This report was prepared by a team led by Peter Ellis and

included David Dowall, Jennifer Day, Thalyta E. Yuwono, Blane Lewis, Arish Dastur, Renata Simatupang,

Arlan Rahman, Rumayya Batubara, Harun al-Rasyid Lubis, Edy Priyono, Arief Ramadhian, Wilmar Salim,

Rulli Setiawan, the Urban and Regional Development Institute.

The report benefited from guidance from Franz Drees-Gross and Sonia Hammam. Valuable inputs were

received from Lili Liu, Yan F. Zhang, Enrique Blanco-Armas, and Taimur Samad. A larger group from within

the World Bank, including Somik Lall, Nancy Lozano Gracia and Hyoung Gun Wang from the Urban

Anchor, contributed to the report, for which contribution the team expresses its gratitude. Victor Vergara

provided the team with valuable inputs and coordinated the team‘s work with the World Bank‘s ECO2

initiative. Jemima Sy provided input and data related to basic service accessibility. Ahya Ihsan, Cut Dian

Agustina, and Sukmawah Yuningsih provided additional data and information for the report.

The team would especially like to express its gratitude to the team from the Government of Indonesia that

provided valuable insights, close involvement, and support for the report, included Max Pohan (Deputy of

Regional and Local Autonomy, Bappenas), Hayu Parasati (Bappenas), Velix Vernando Wanggai

(Presidential Special Staff on Local Autonomy and Regional Development), Bambang Susantono (Vice

Minister for Ministry of Transportation), Fauzi Bowo (Governor of DKI Jakarta), Sarwo Handayani (Head

of Bappeda DKI Jakarta), Tri Rismaharini (Mayor of Surabaya), Rahudman Harahap (Mayor of Medan)

and Ilham Arief Sirajuddin (Mayor of Makassar).

Disclaimer: The views expressed in this report are those of the authors and do not constitute official policy

positions of either the World Bank, the Government of Indonesia, or any government institution.

Page iii

TABLE OF CONTENTS Preface i

Acknowledgements ii

Executive Summary ix

Chapter 1 Overview and Methodology 1

Chapter 2 Urbanization and Metropolitan Growth 5

Regional Development Policy: People vs. Place Prosperity 5

Urbanization pattern and trajectory 9

Urbanization trends in Indonesia‘s seven island regions 11

Poverty in urban areas 12

Agglomeration Index and metropolitan regions 13

Infrastructure investment‘s role 15

Factor markets 15

Functionally defined metropolitan regions 16

Evolving spatial structure of metropolitan regions 18

The shifting hierarchy of Indonesia‘s urban system 23

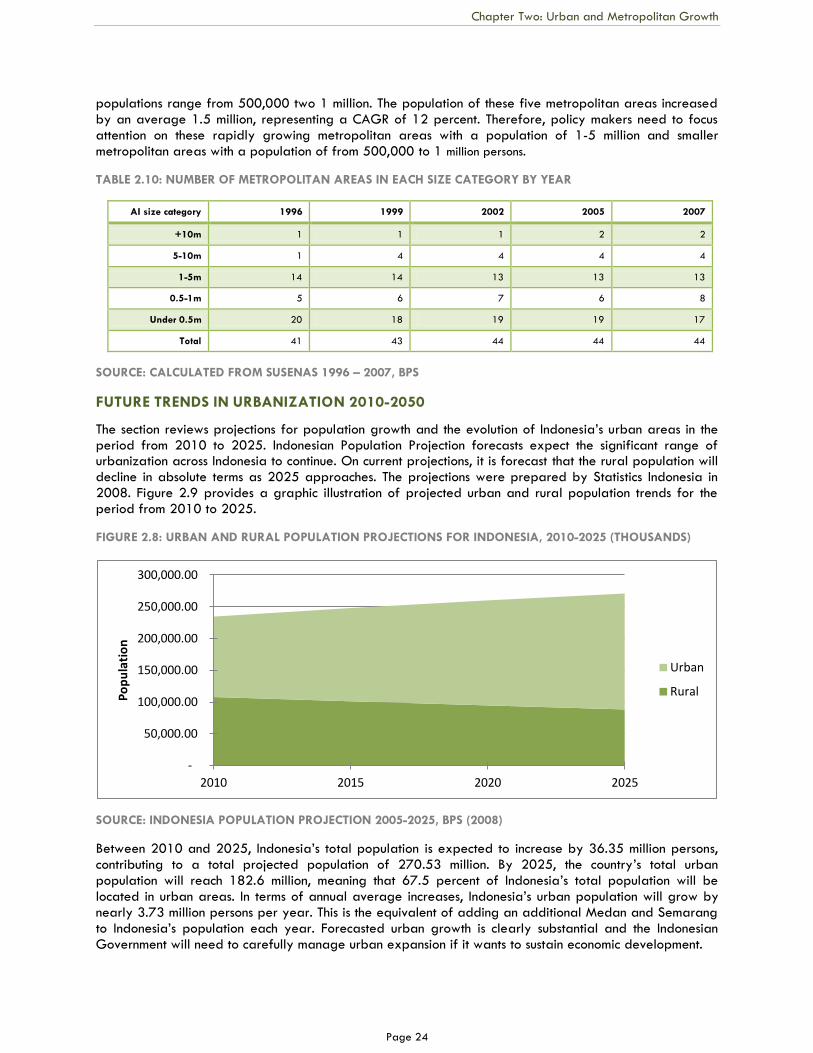

Future trends in urbanization 2010-2050 24

Conclusion 25

Policy recommendations 26

Chapter 3 Leveraging Urbanization and Agglomeration 27

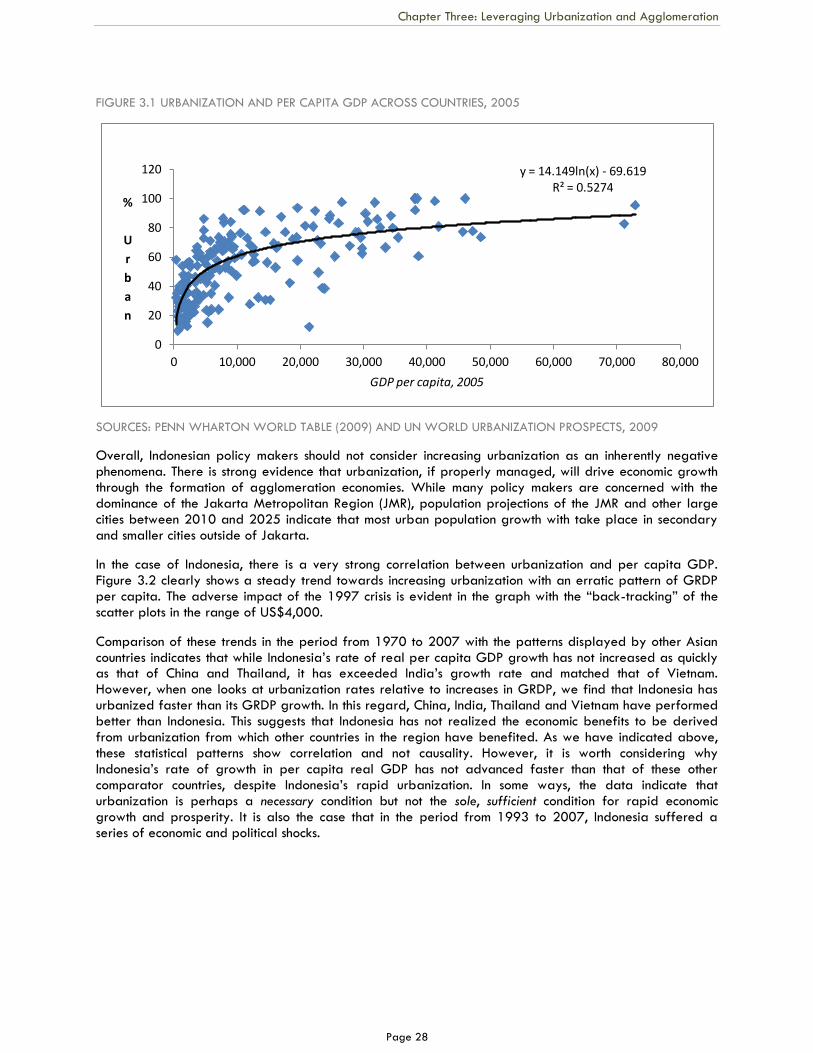

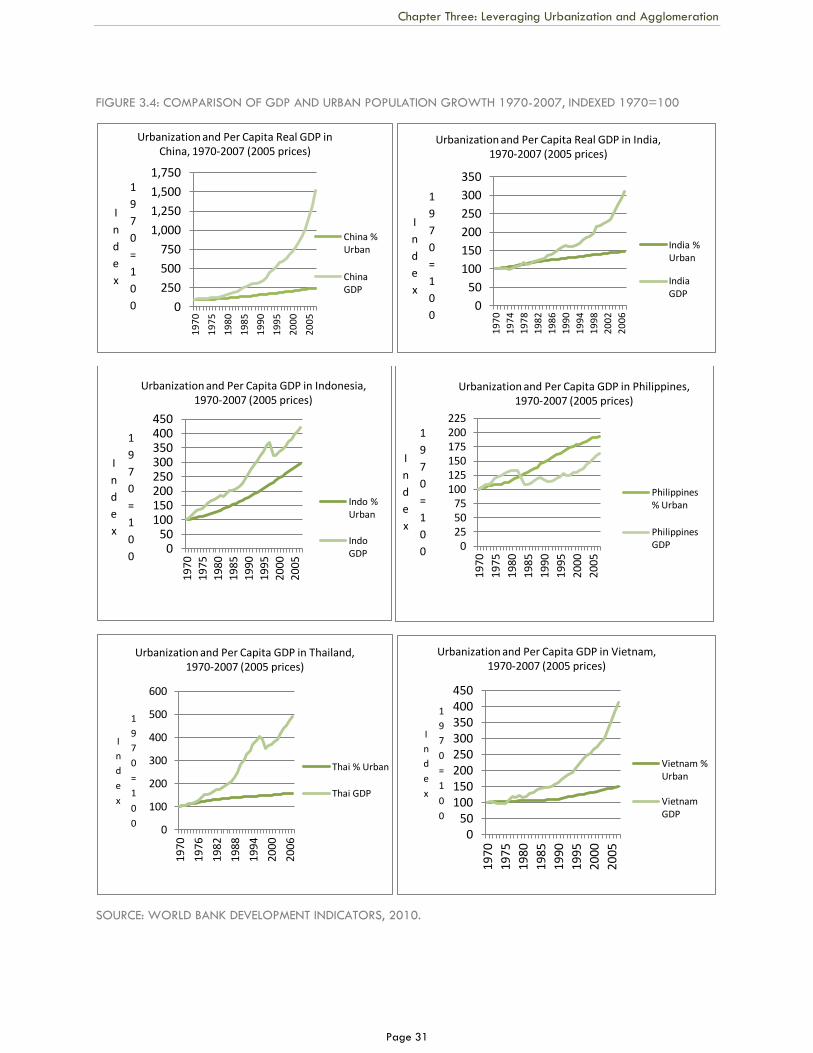

Urbanization and economic development go hand in hand 27

Indonesia has not fully leveraged the economic benefits of rapid urbanization 29

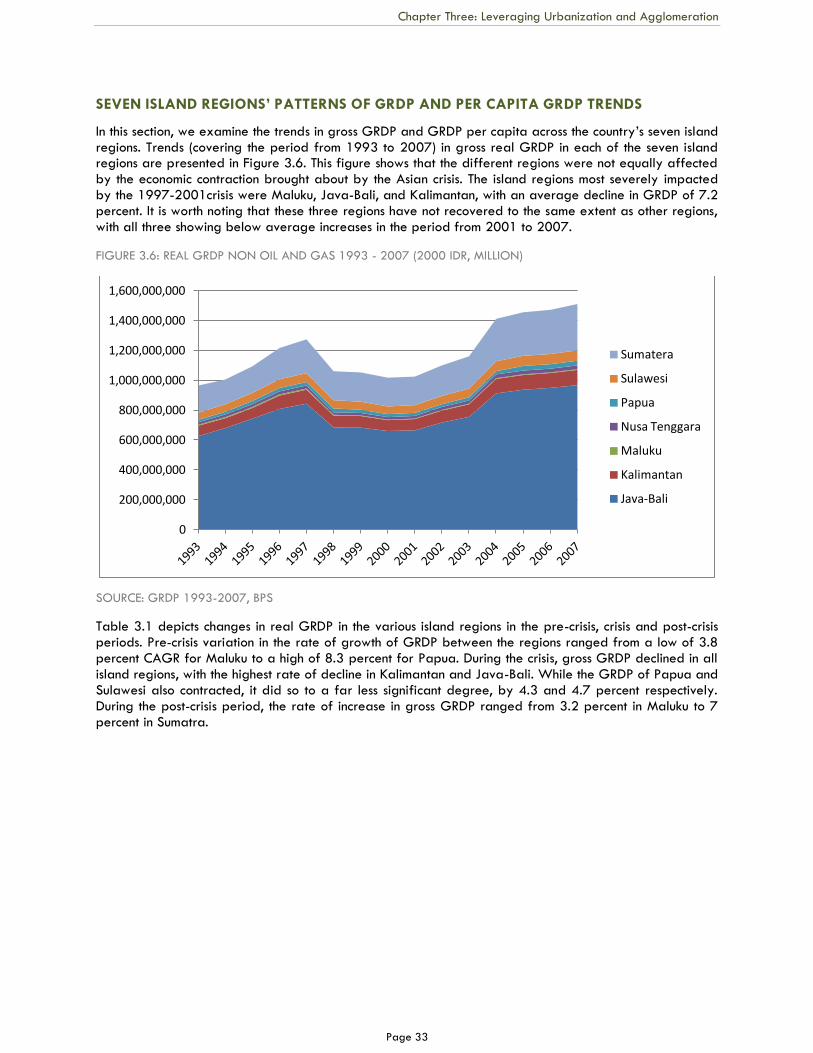

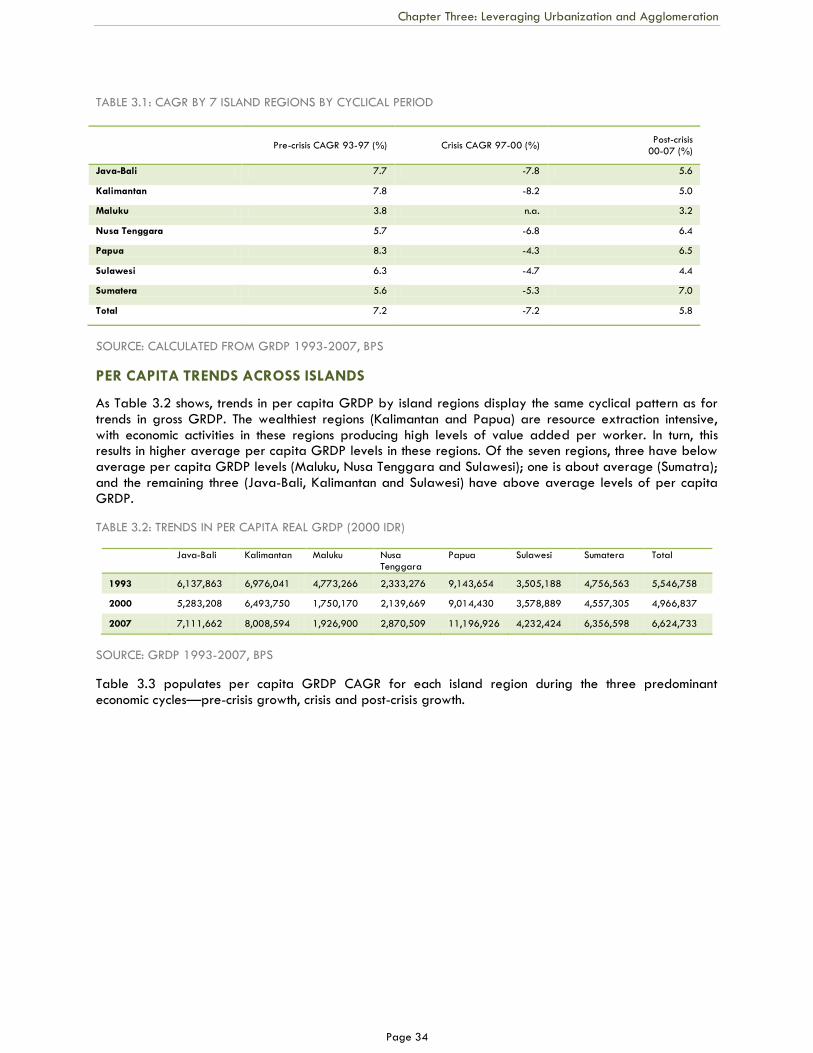

Seven island regions‘ patterns of GRDP and per capita GRDP trends 33

Per capita trends across islands 34

Trends in gross GRDP and per capita GRDP for urban and rural areas 35

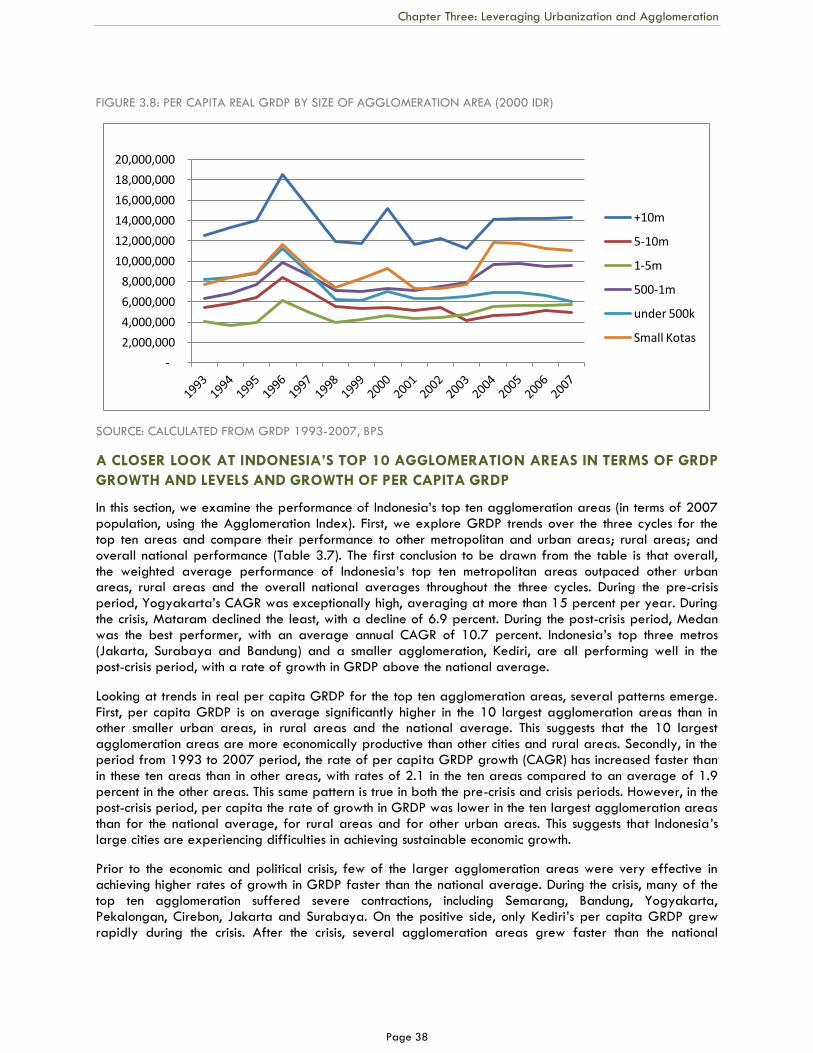

GRDP trends in metropolitan regions 37

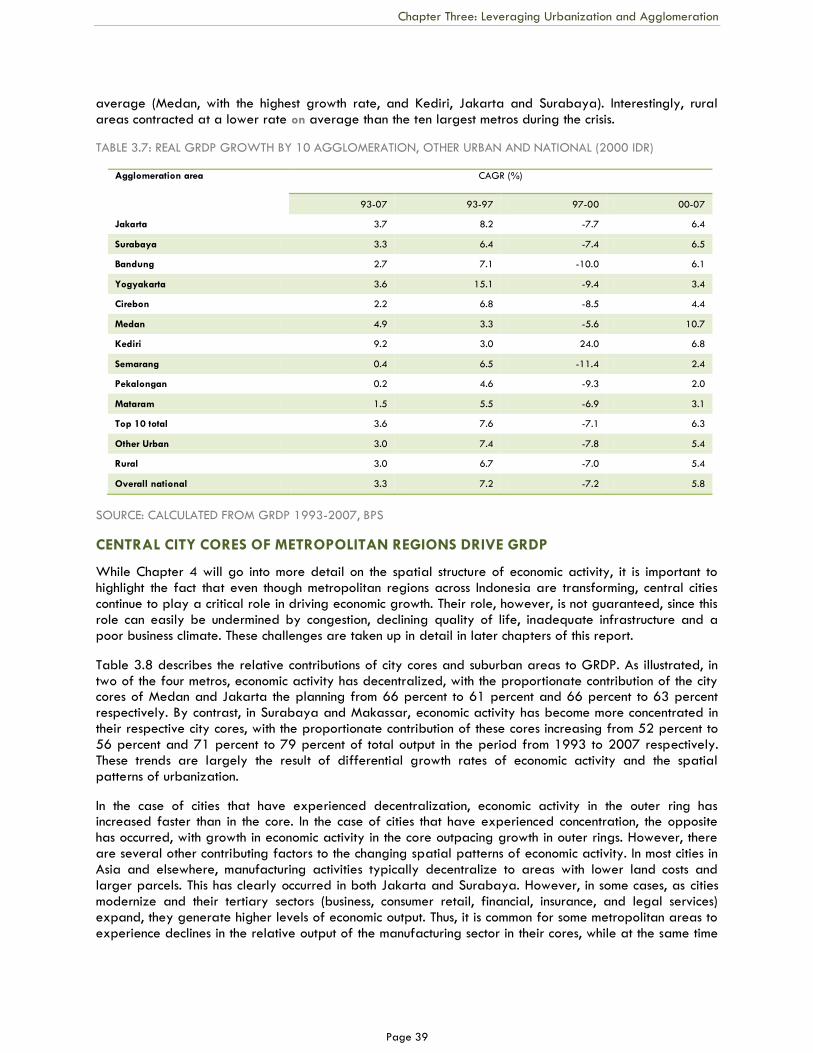

A closer look at Indonesia‘s top 10 agglomeration areas in terms of GRDP growth and levels and growth of per capita GRDP 38

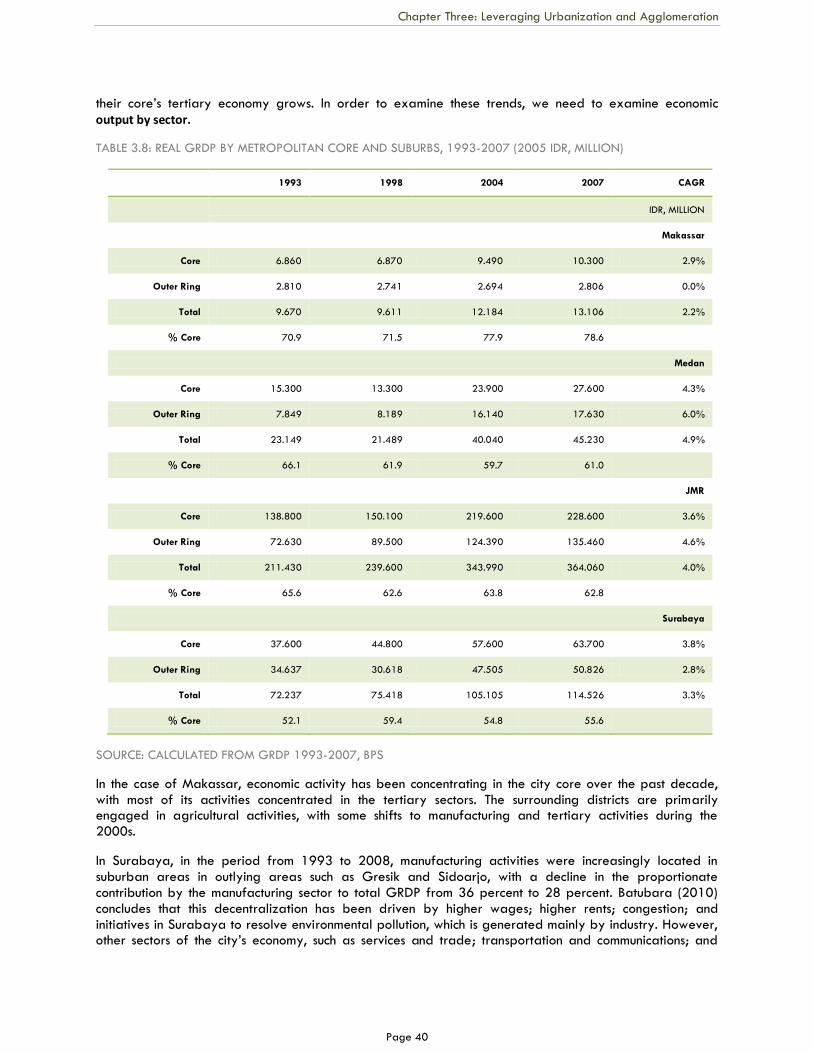

Central city cores of metropolitan regions drive GRDP 39

Linking urbanization and regional economic development 42

Conclusion 43

Policy recommendations 44

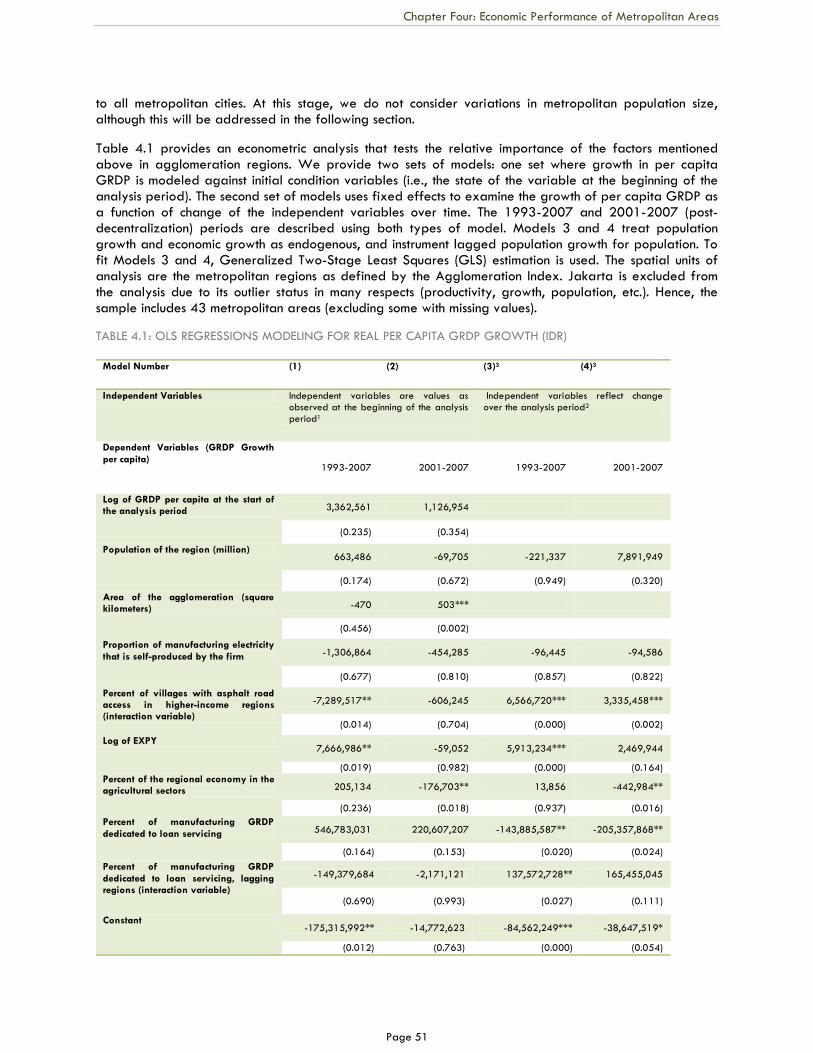

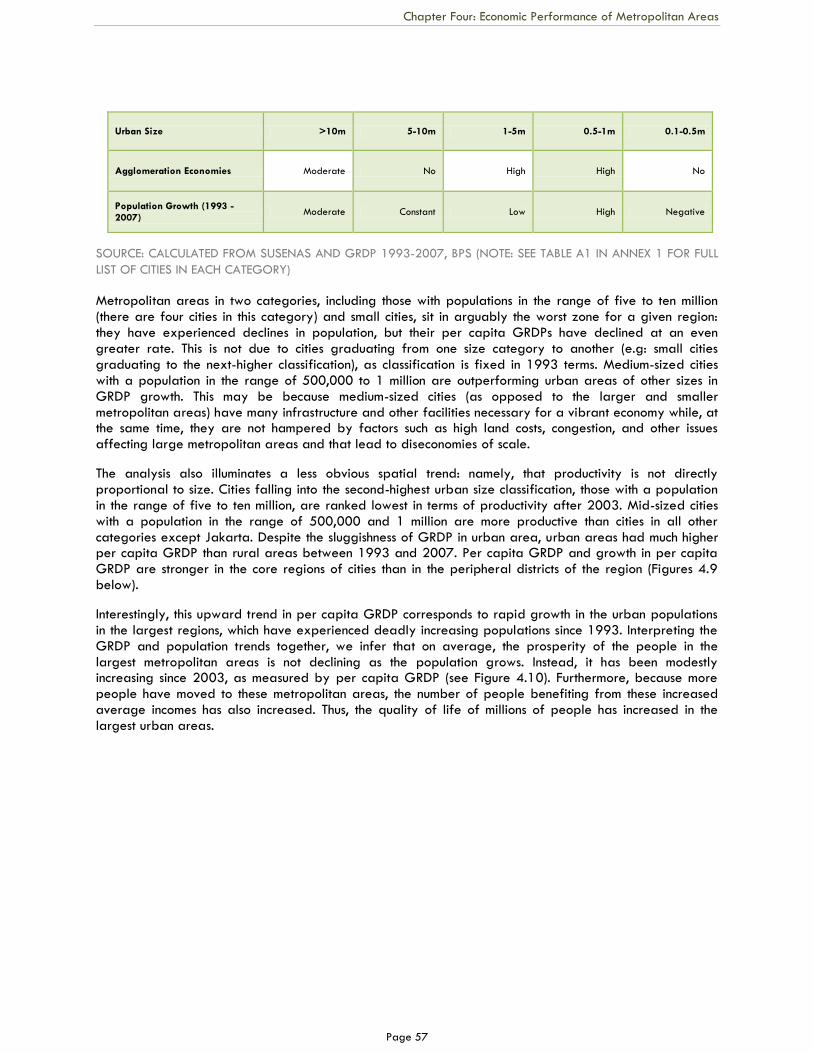

Chapter 4 Economic Performance of Metropolitan Regions 45

What constrains agglomeration economies in Indonesia metropolitan areas? 45

Spatial structure and the location of economic activities 45

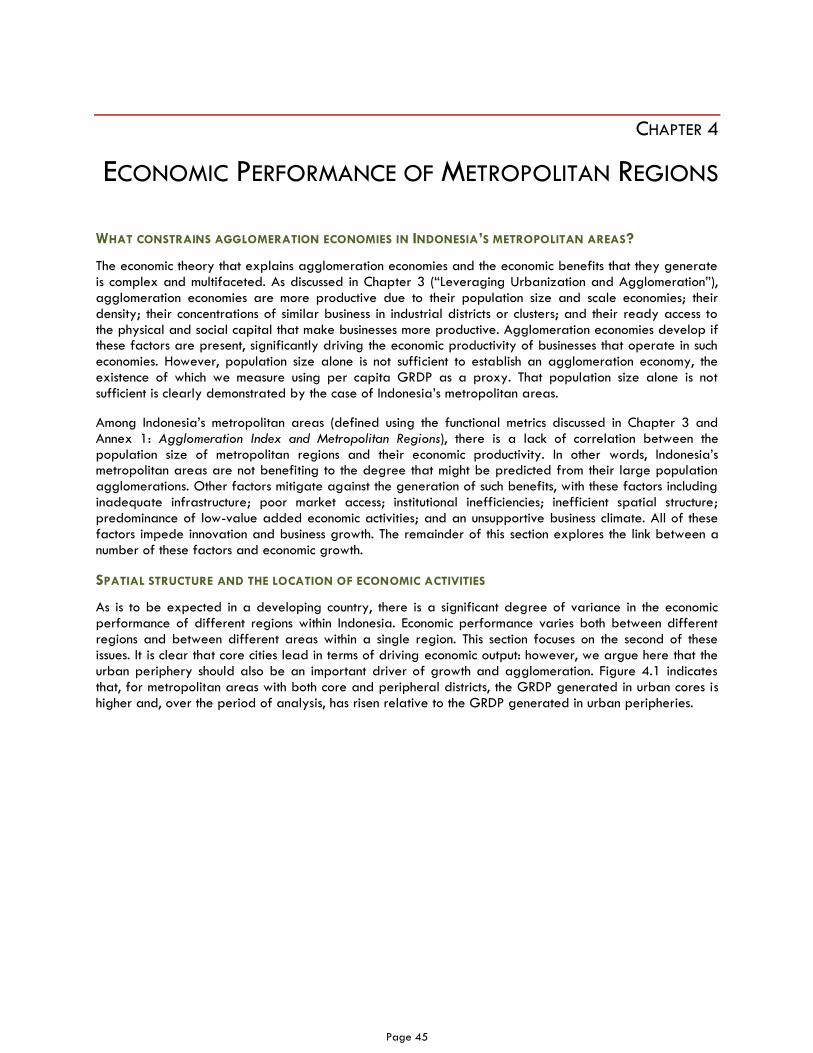

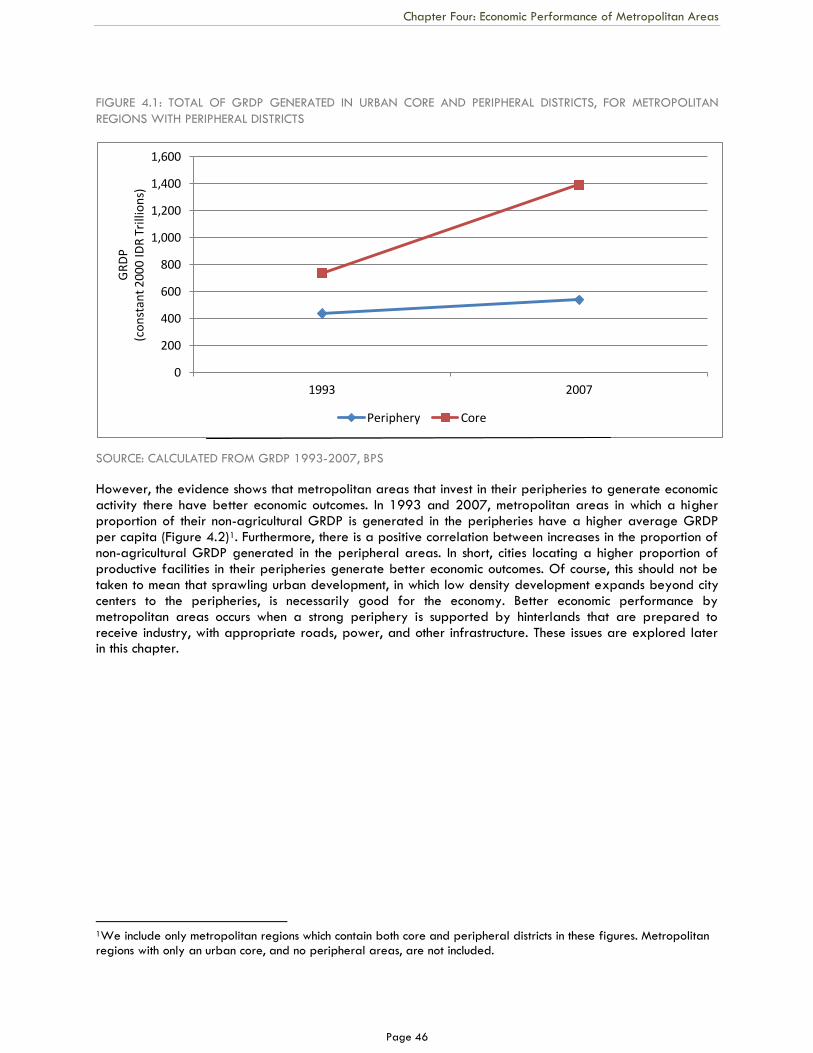

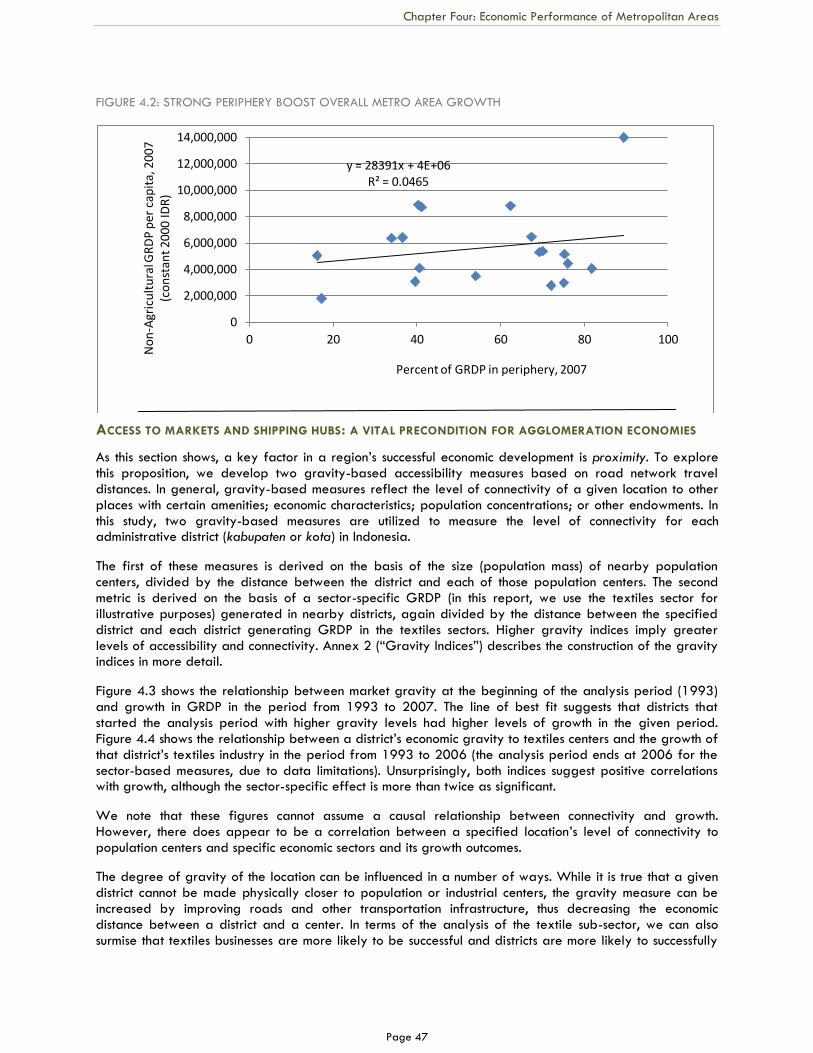

Access to markets and shipping hubs 47

Page iv

Higher value added production boosts economic productivity 48

A multivariate assessment of what is driving agglomeration economies 50

Economic performance and agglomeration economies 54

Infrastructure and connectivity matter 59

Integrating the story 61

Conclusion 61

Policy recommendations 62

Chapter 5 Infrastructure Investments and Urban Development 63

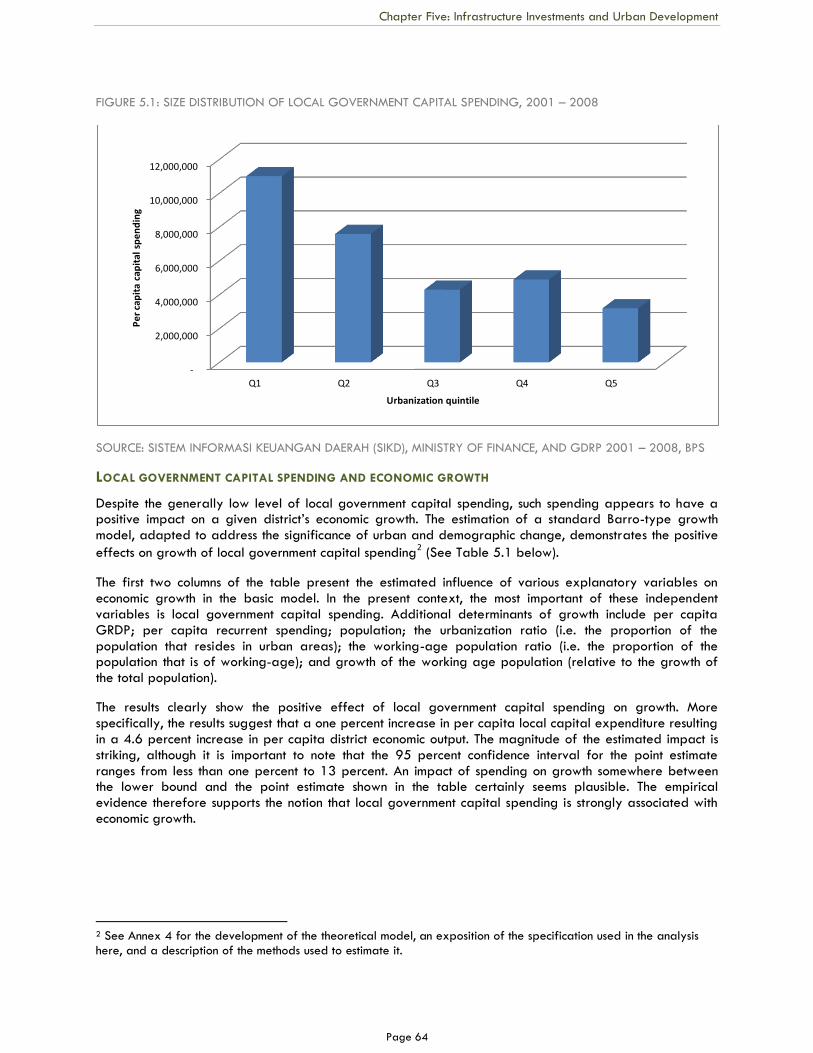

Local government capital spending 63

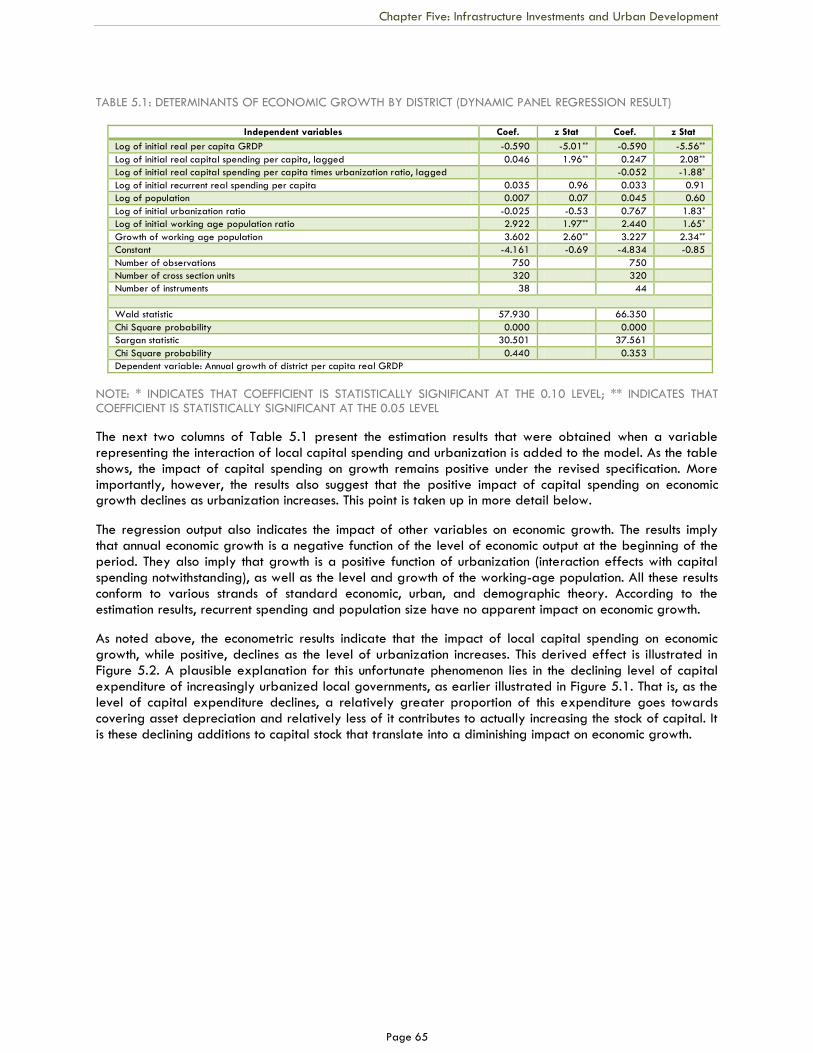

Local government capital spending and economic growth 64

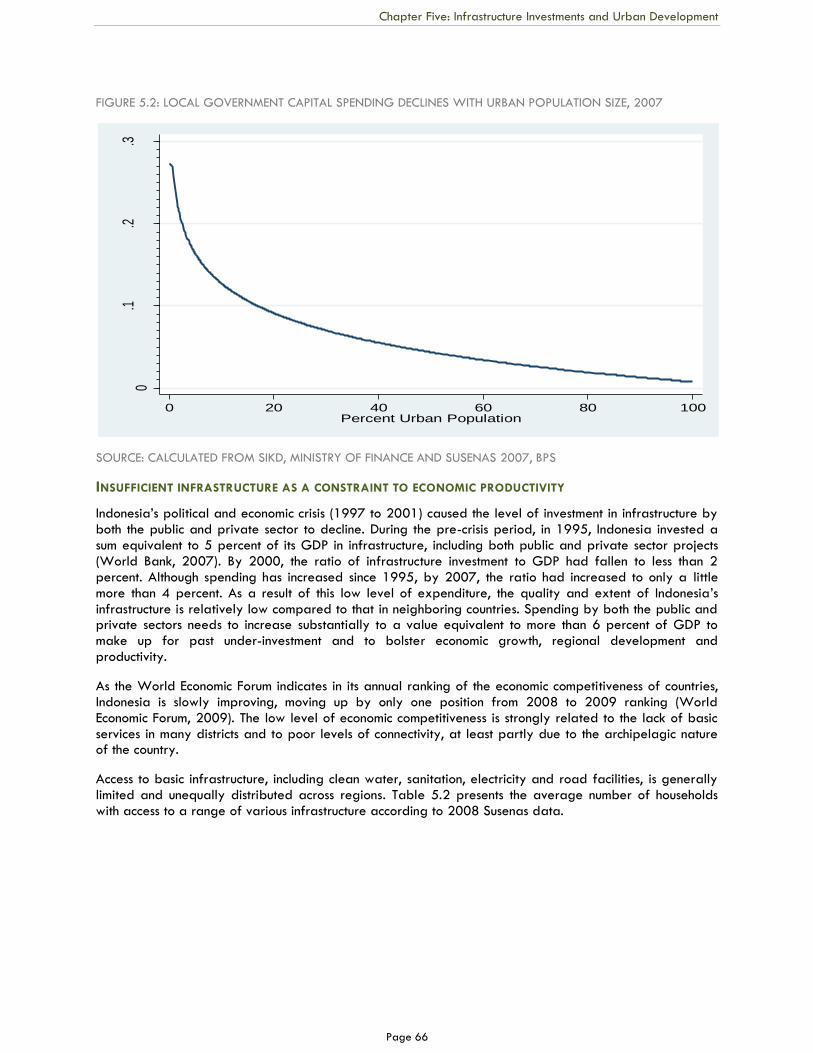

Insufficient infrastructure as a constraint to economic productivity 66

Conclusion 68

Policy recommendations 69

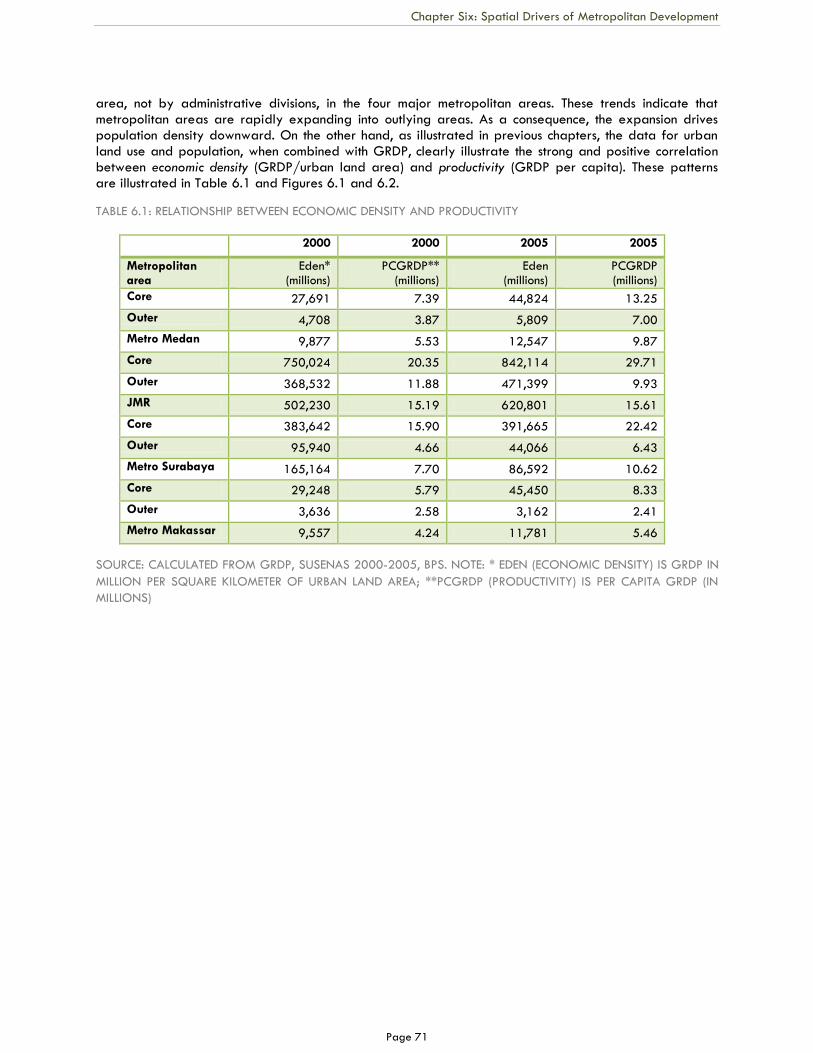

Chapter 6 Spatial Drivers of Metropolitan Development 70

Urbanization and sprawl 70

Does inappropriate spatial planning undermine economic productivity? 72

Metropolitan coordination 74

Indonesia‘s complex land and property rights system 75

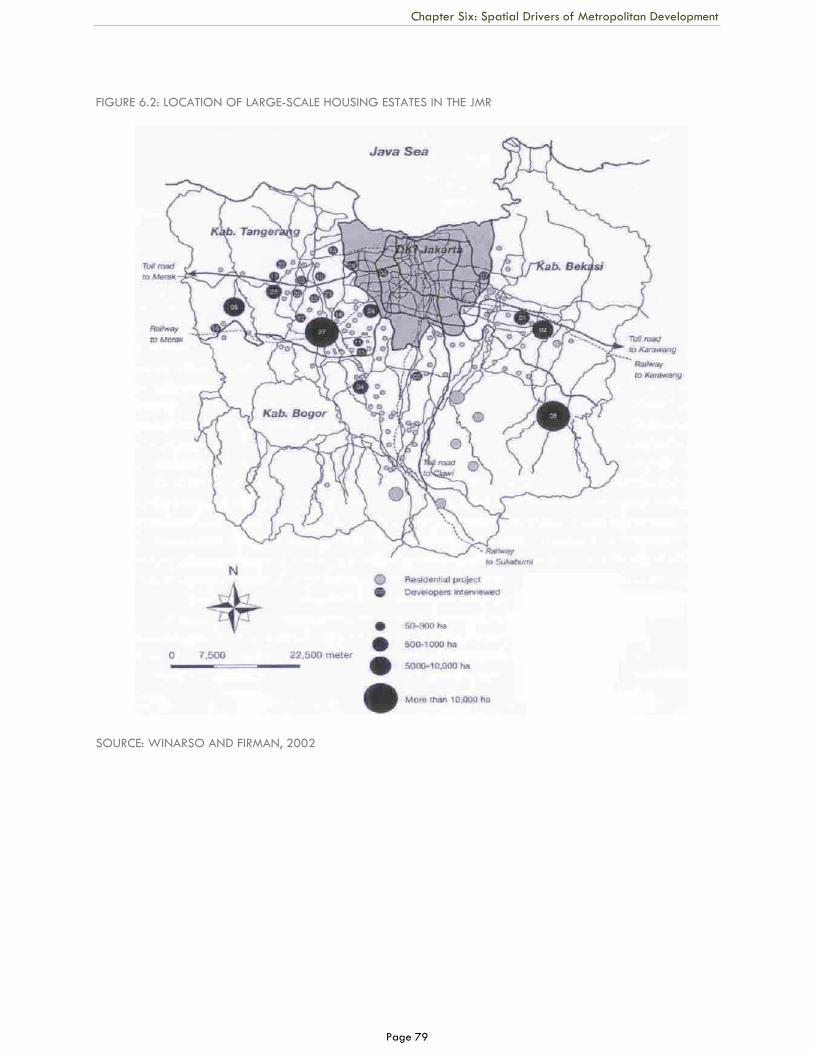

Large-scale industrial, residential and commercial districts 78

Conclusion 80

Policy recommendations 81

Chapter 7 Conclusion 82

Central government actions 82

Policy actions for large metropolitan regions 83

Policy initiatives for smaller metropolitan areas 84

References

Annex 1 Agglomeration Index and Metropolitan Regions 86

Annex 2 Gravity Indices 93

Annex 3 PRODY and EXPY 96

Annex 4 Capital Spending, Urbanization, and Demographic Change 102

Annex 5 Development trends in Jakarta, Makassar, Medan and Surabaya 105

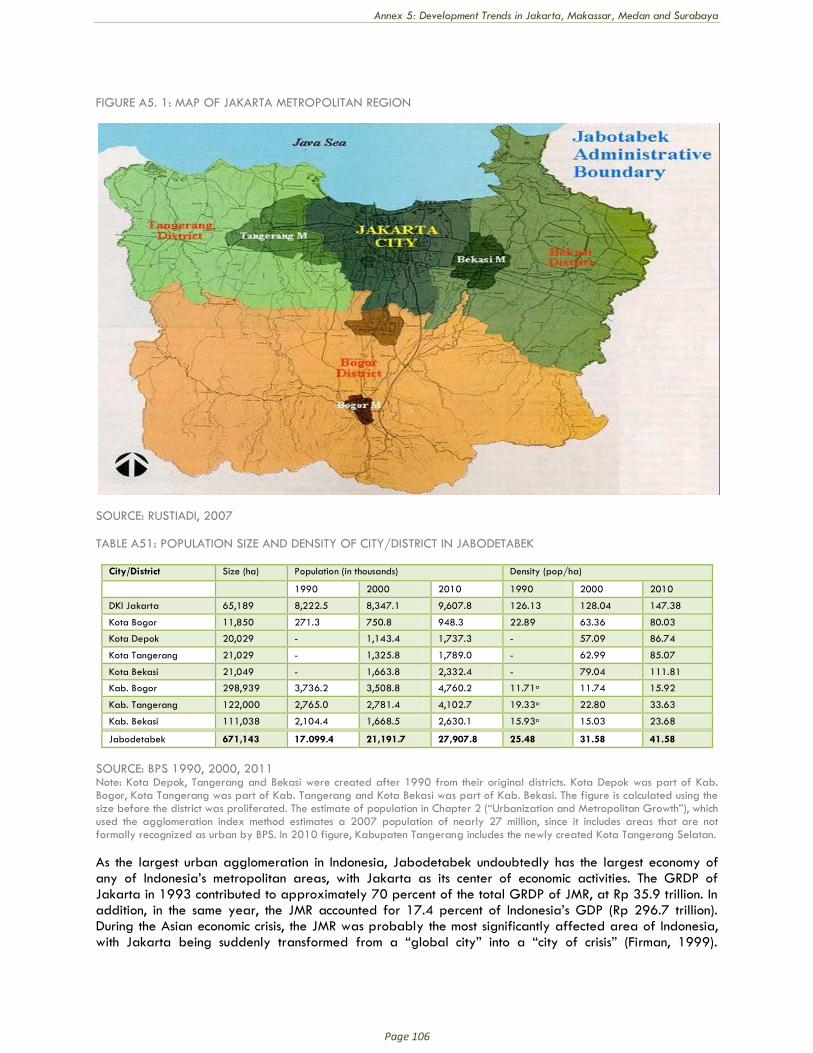

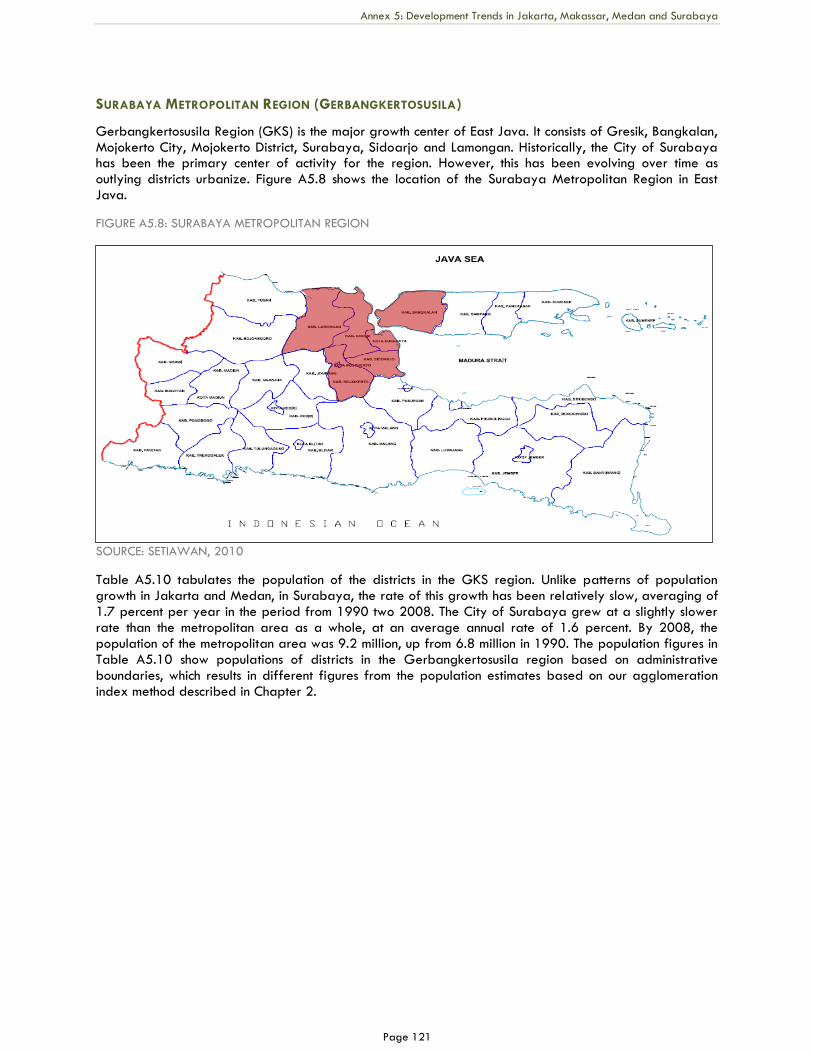

Jakarta Metropolitan Region (Jabodetabek) 105

Makassar Metropolitan Region (Mamminasata) 110

Medan Metropolitan Region (Mebidang) 116

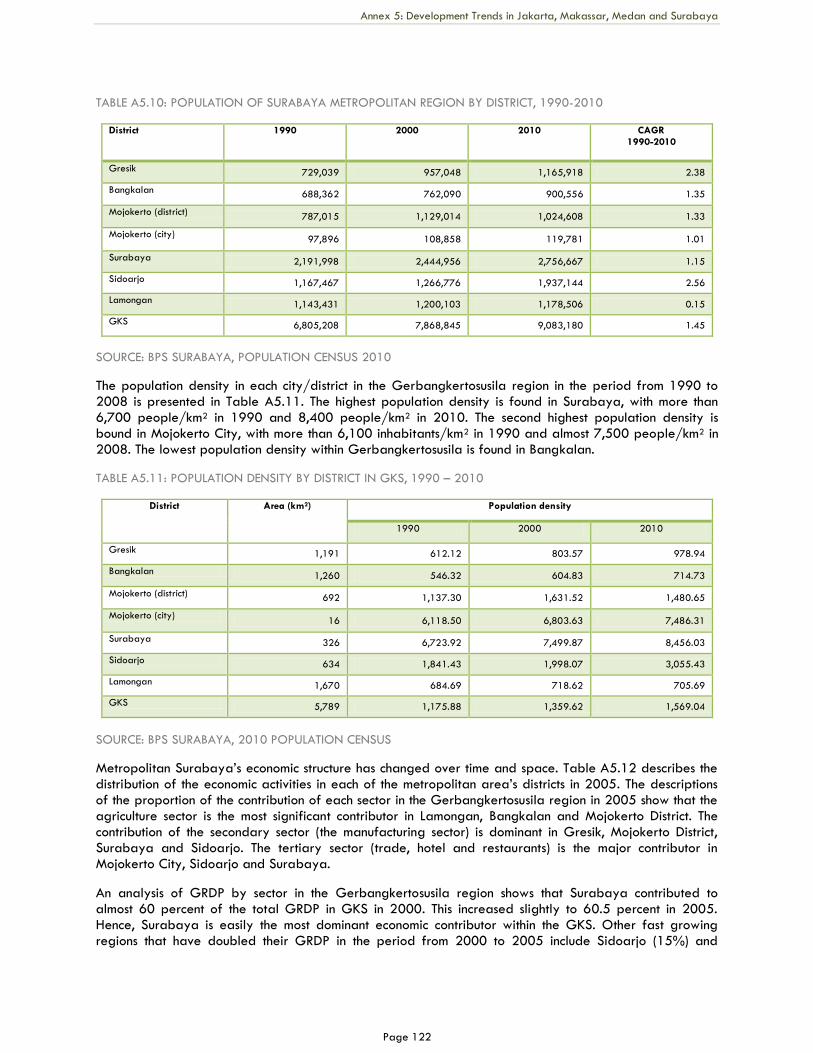

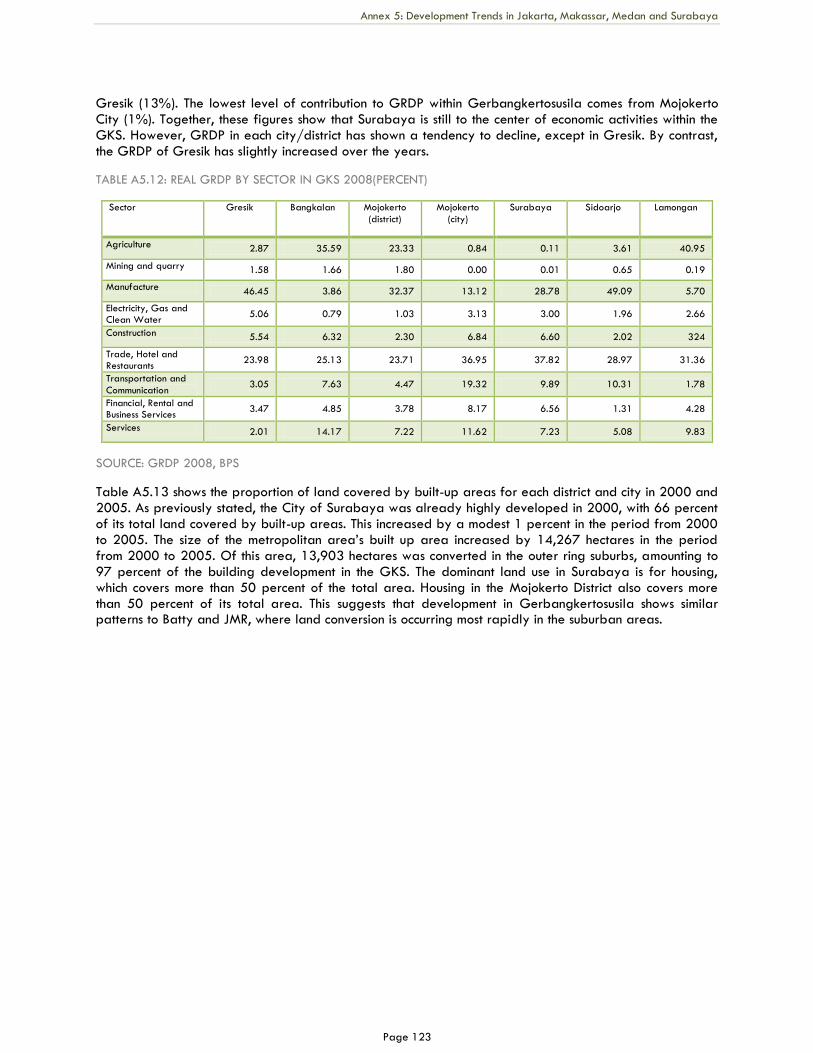

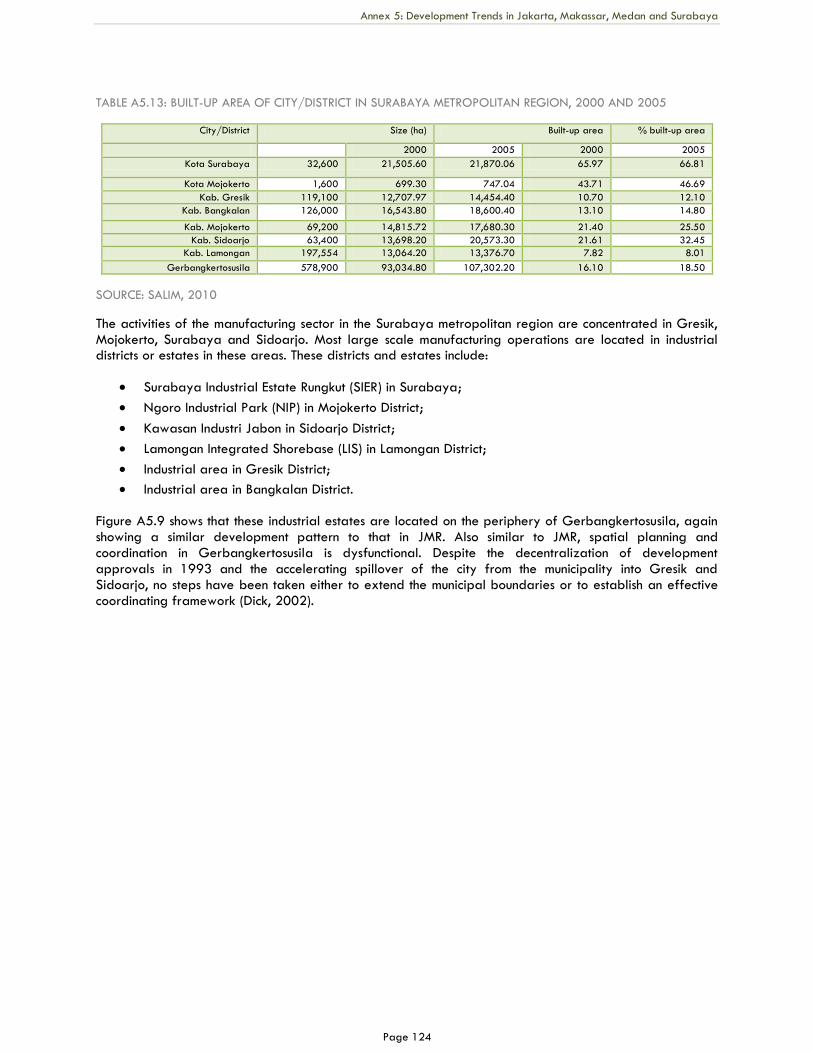

Surabaya Metropolitan Region (Gerbangkertosusila) 121

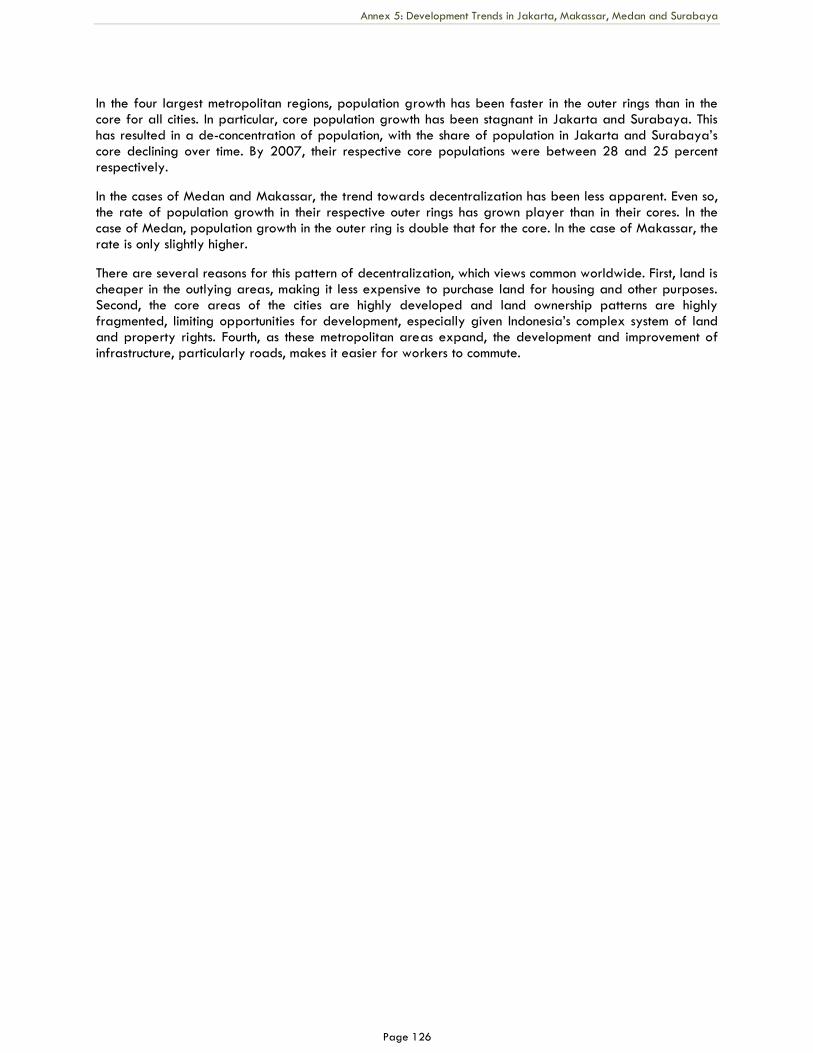

Comparison of the economic geography of the four metropolitan regions 125

Page v

LIST OF TABLES Table 2. 1 Economic corridors in the Master Plan for Acceleration and Expansion of Indonesia‘s Economic Development (MP3EI) 7

Table 2. 2 Urban and rural population, Indonesia 1971-2010 10

Table 2. 3 Total population of Indonesia‘s seven island regions, 1993-2007 12

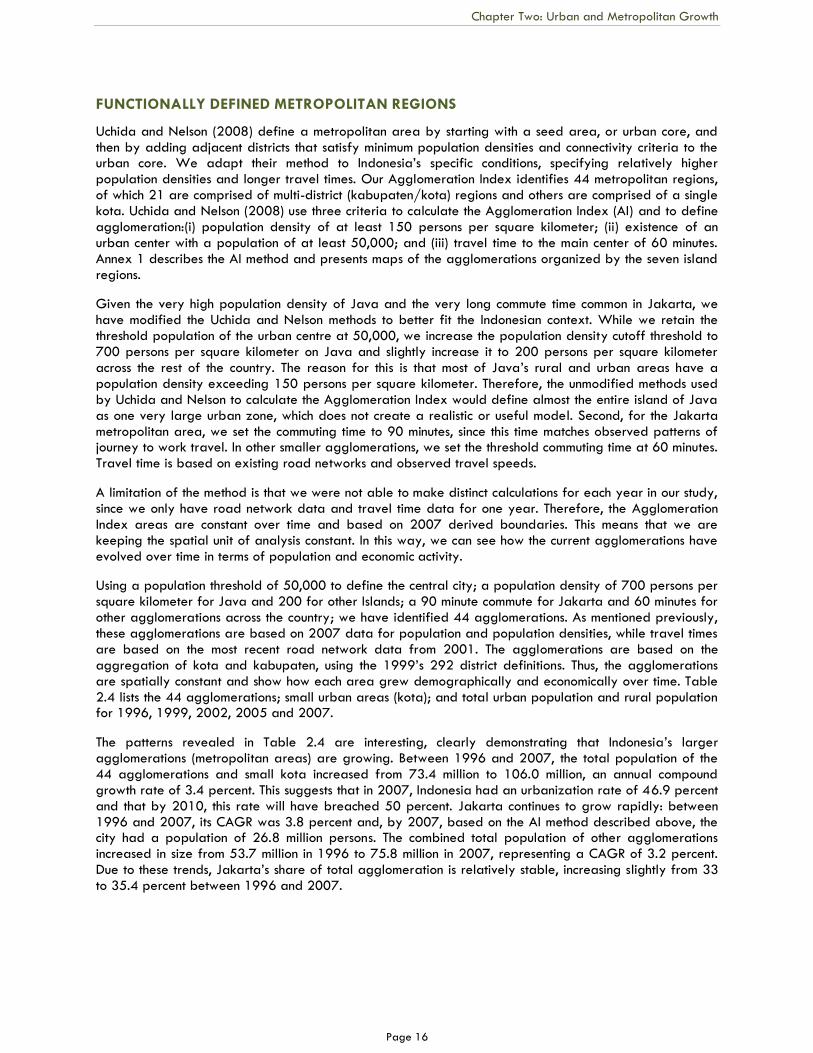

Table 2. 4 Indonesian agglomerations, population 1996-2007 17

Table 2. 5 Total population in metropolitan, urban and rural areas, 1996-2007 19

Table 2. 6 Population trends by urban core and suburban ring in 21 multi districts metros, 1996-2007 19

Table 2. 7 Land use patterns in the four metropolitan areas, 2000-2005 21

Table 2. 8 Population density per square kilometer in the four metropolitan areas, 2000-2005 22

Table 2. 9 Relationship between the size of urban metropolitan areas, small kota and population growth 23

Table 2. 10 Number of metropolitan areas in each size category by year 24

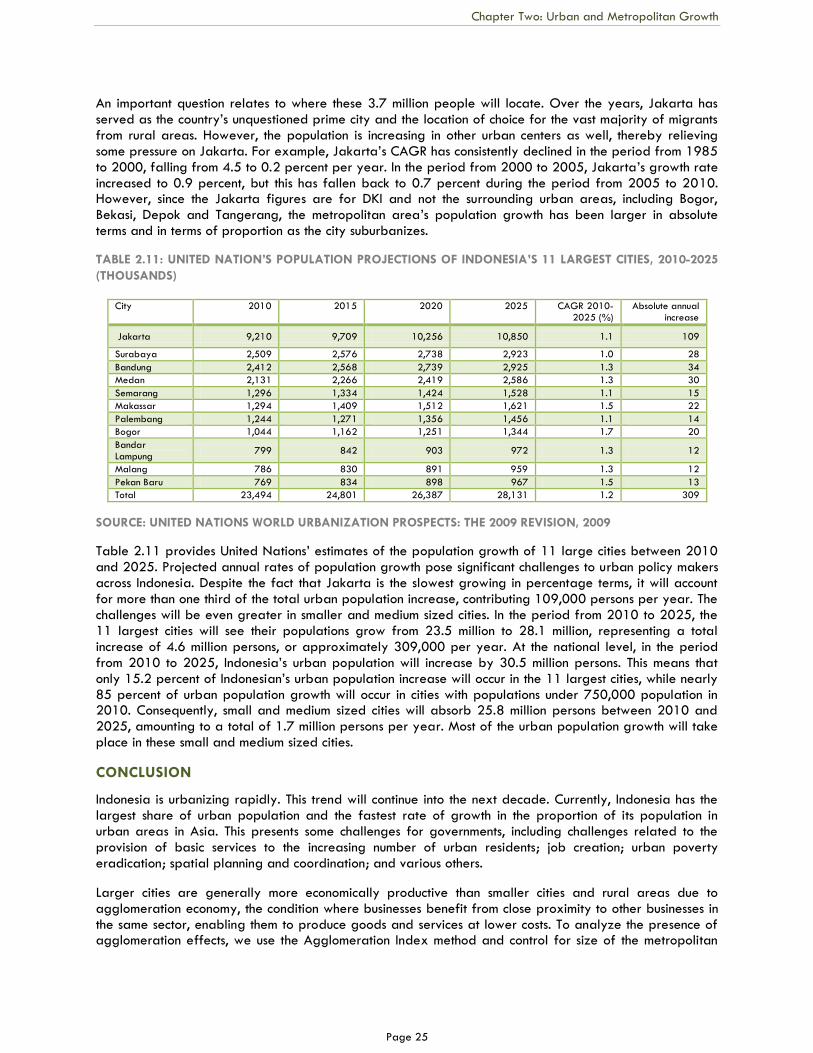

Table 2. 11 United Nation‘s population projections of Indonesia‘s 11 largest cities, 2010-2025 25

Table 3. 1 CAGR by 7 island regions by cyclical period 34

Table 3. 2 Trends in per capita Real GRDP 34

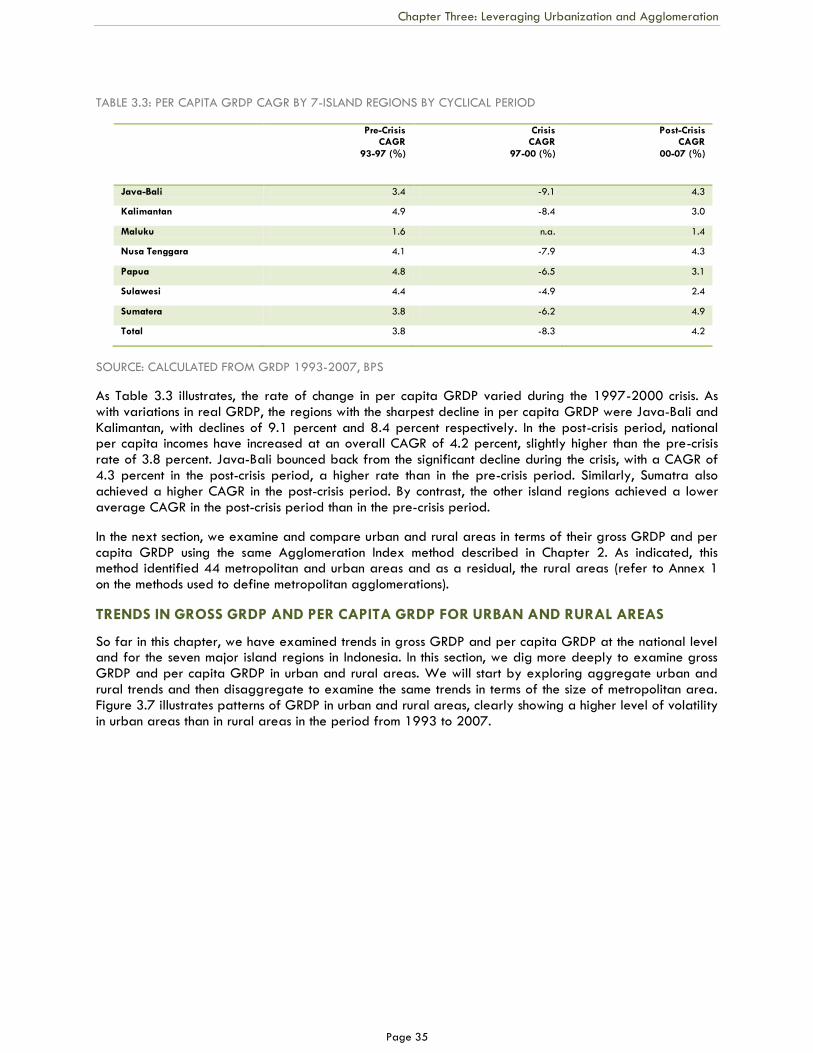

Table 3. 3 Per capita GRDP CAGR by 7-island regions by cyclical period 35

Table 3. 4 GRDP urban and rural CAGR by cyclical period 36

Table 3. 5 Real GRDP Makassar, Medan, JMR and Surabaya 37

Table 3. 6 Real GRDP per capita Makassar, Medan, JMR and Surabaya 37

Table 3. 7 Real GRDP growth by 10 agglomeration, other urban and national 39

Table 3. 8 Real GRDP by metropolitan core and suburbs, 1993-2007 40

Table 4. 1 OLS regressions modeling for real per capita GRDP growth (IDR) 51

Table 4. 2 Metropolitan agglomeration by population size (2007) 55

Table 5. 1 Determinants of economic growth by district 65

Table 5. 2 Access to water, sanitation, electricity and road, 2008 67

Table 6. 1 Relationship between economic density and productivity 71

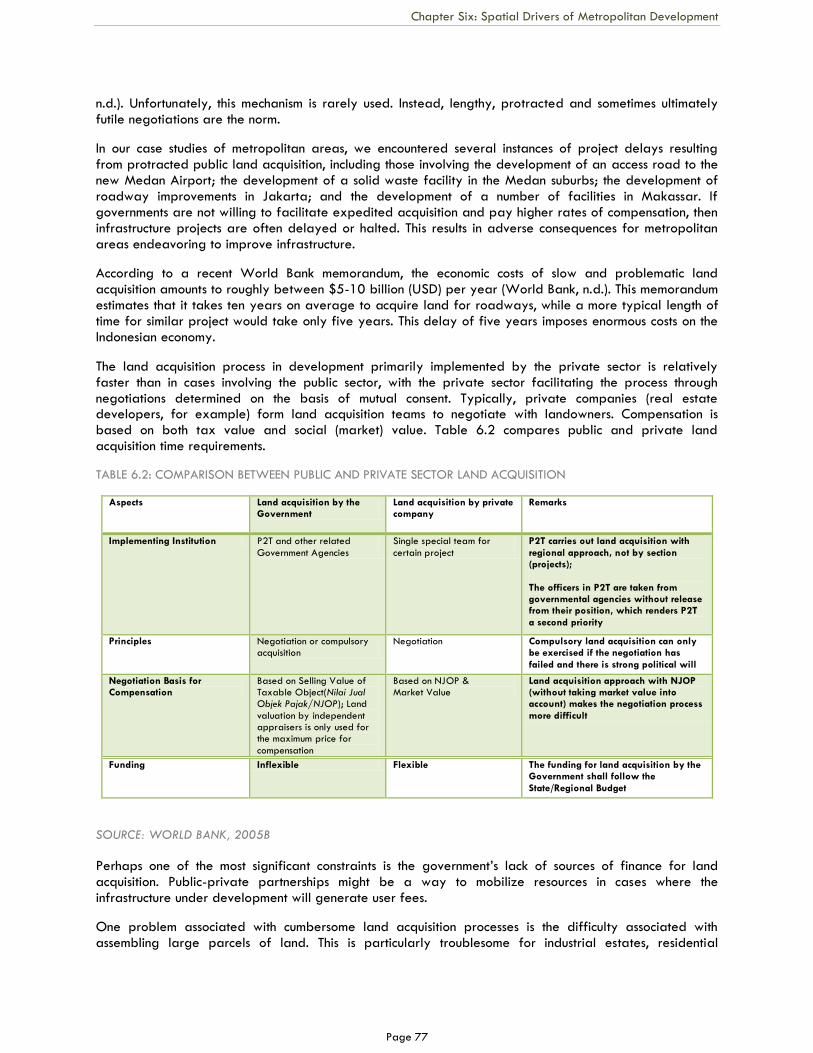

Table 6. 2 Comparison between public and private sector land acquisition 77

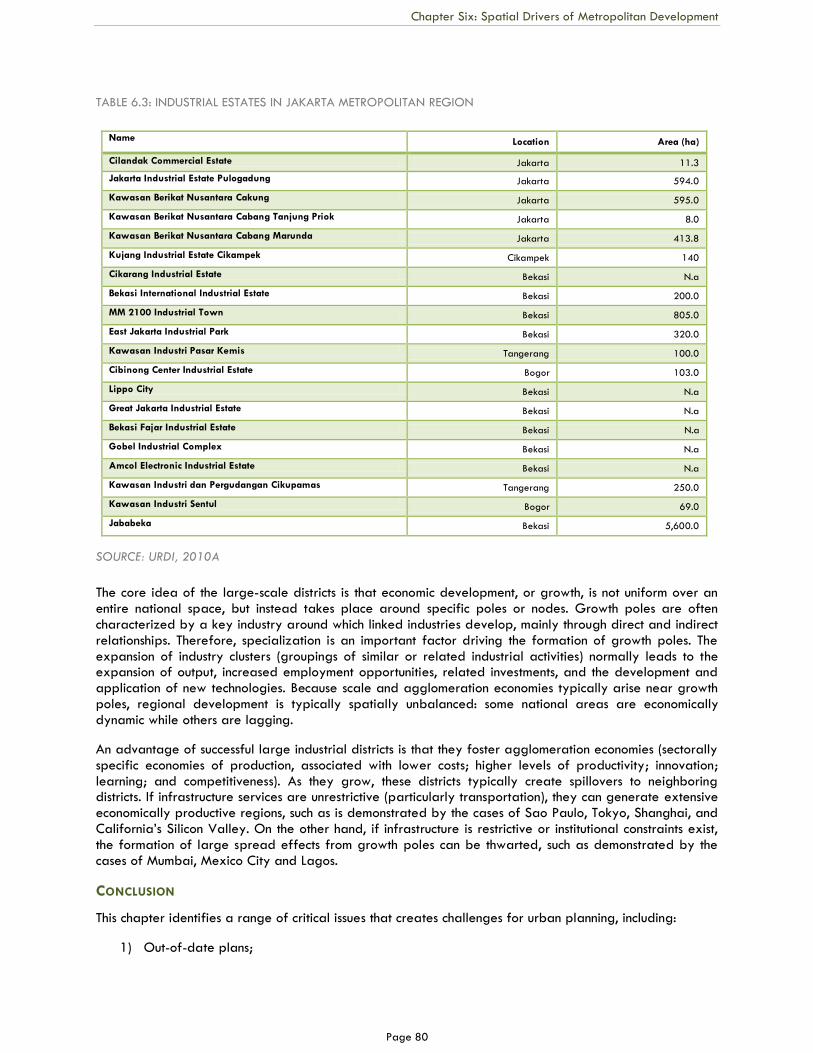

Table 6. 3 Industrial estates in Jakarta Metropolitan Region 80

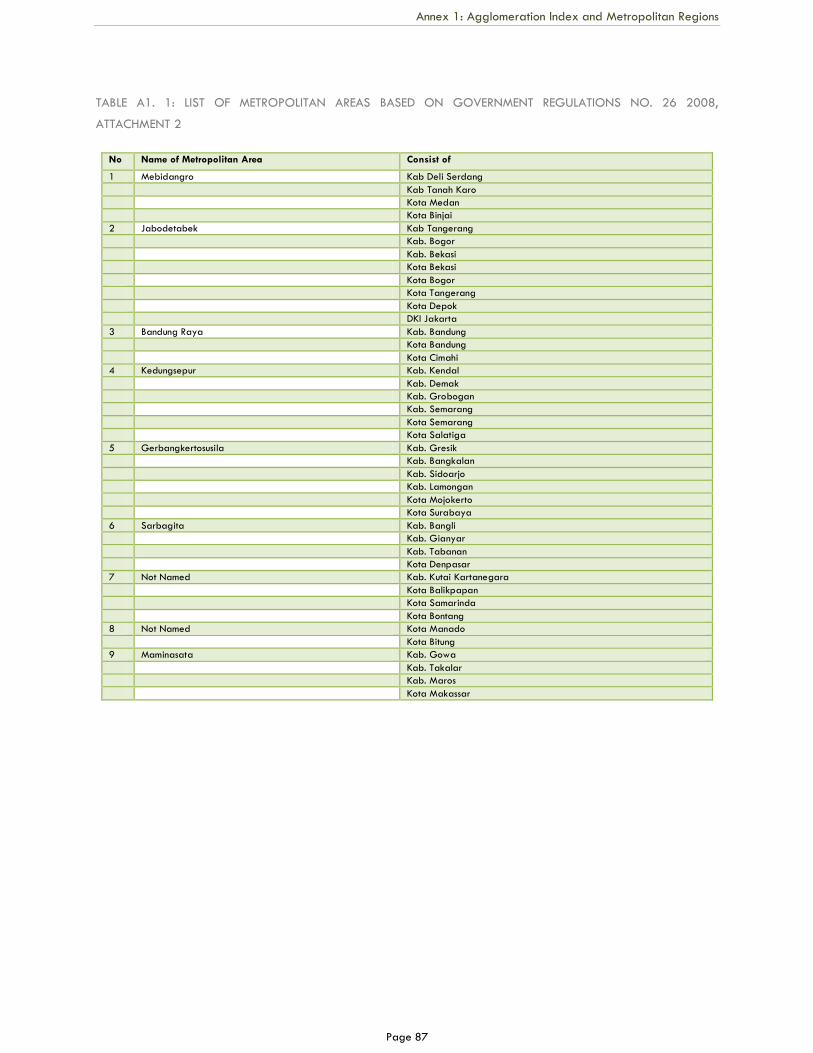

Table A1. 1 List of Metropolitan Areas based on Government Regulations No. 26 2008, Attachment 2 87

Table A1. 2 Metropolitan agglomerations by size 91

Table A1. 3 Metropolitan agglomeration by population size (2007) 92

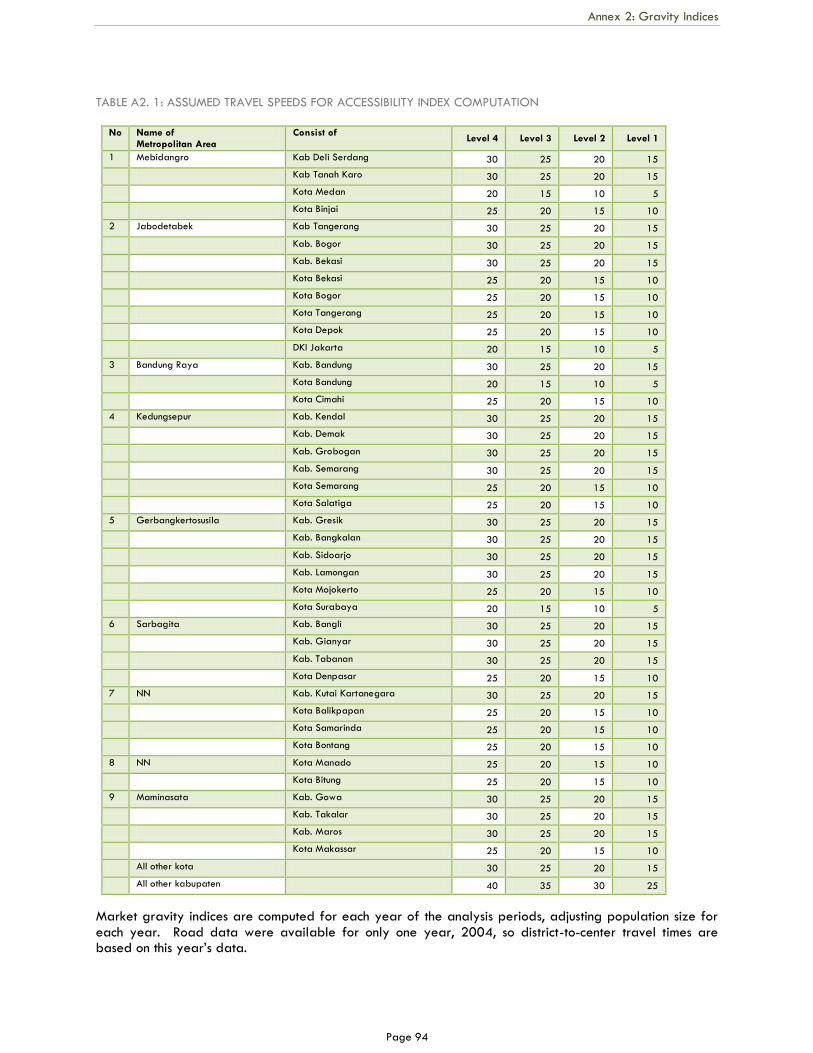

Table A2. 1 Assumed travel speeds for Accessibility Index computation 94

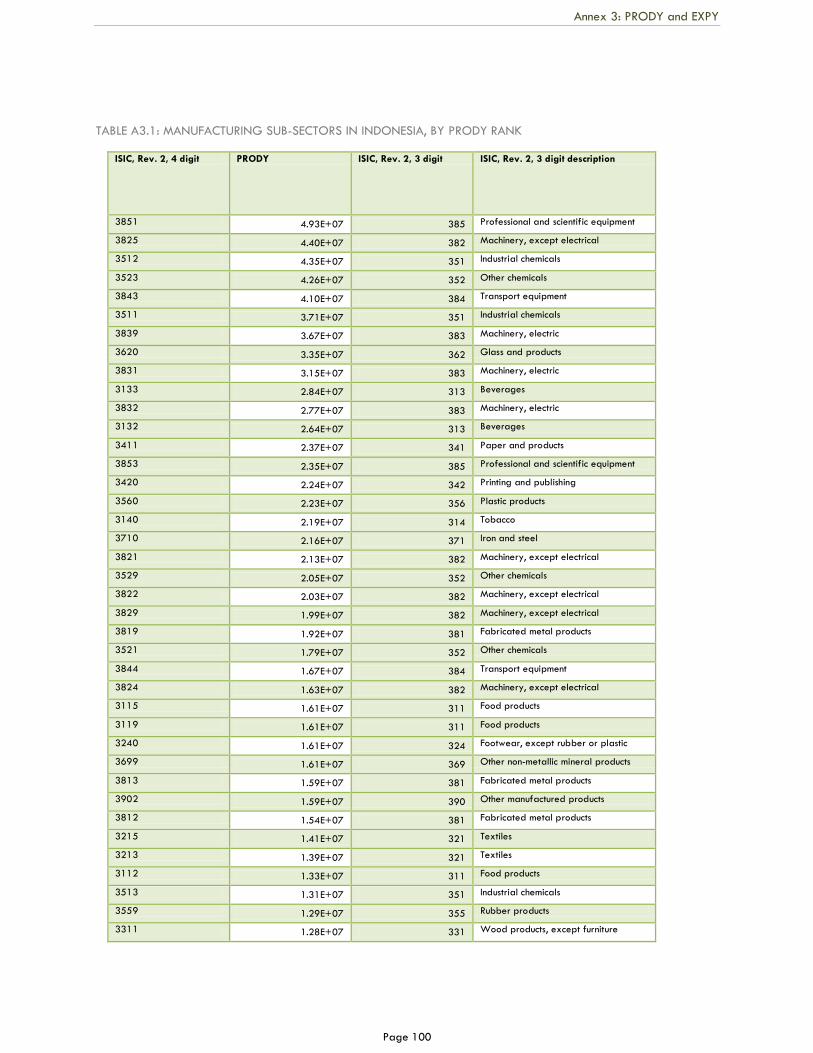

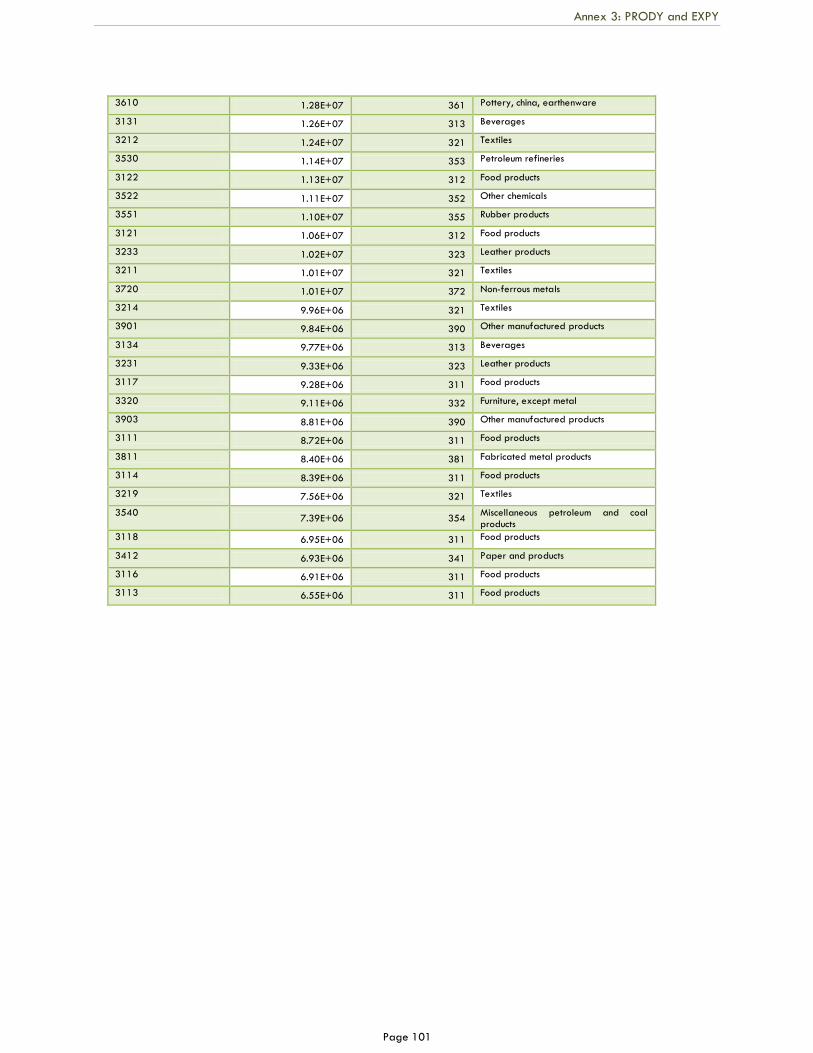

Table A3. 1 Manufacturing sub-sectors in Indonesia, by PRODY Rank 100

Table A5. 1 Population size and density of city/district in Jabodetabek 106

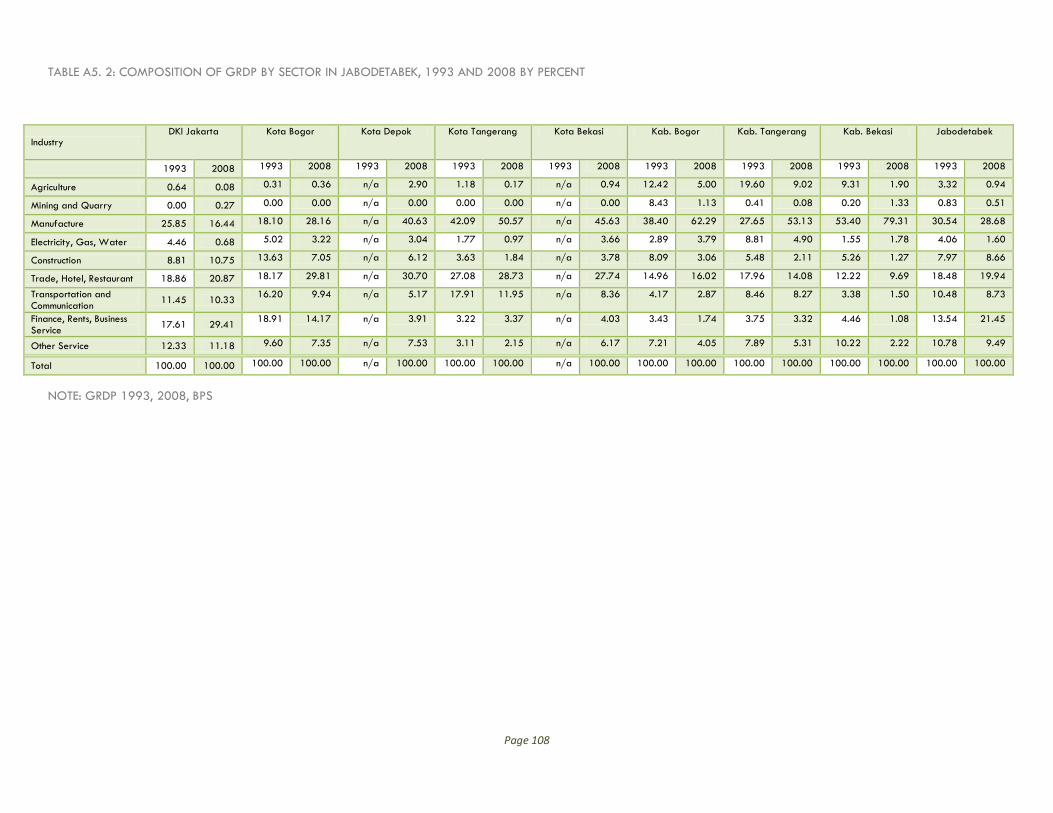

Table A5. 2 Composition of GRDP by sector in Jabodetabek, 1993 and 2008 by percent 108

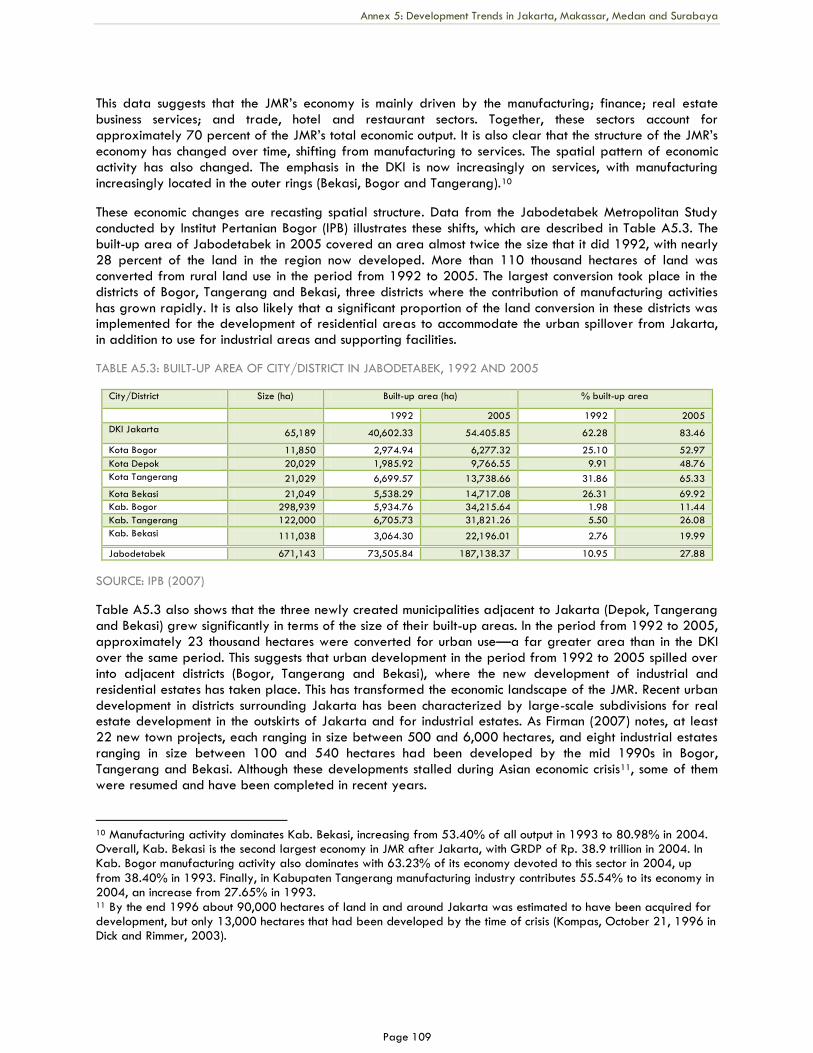

Table A5. 3 Built-up area of city/district in Jabodetabek, 1992 and 2005 109

Page vi

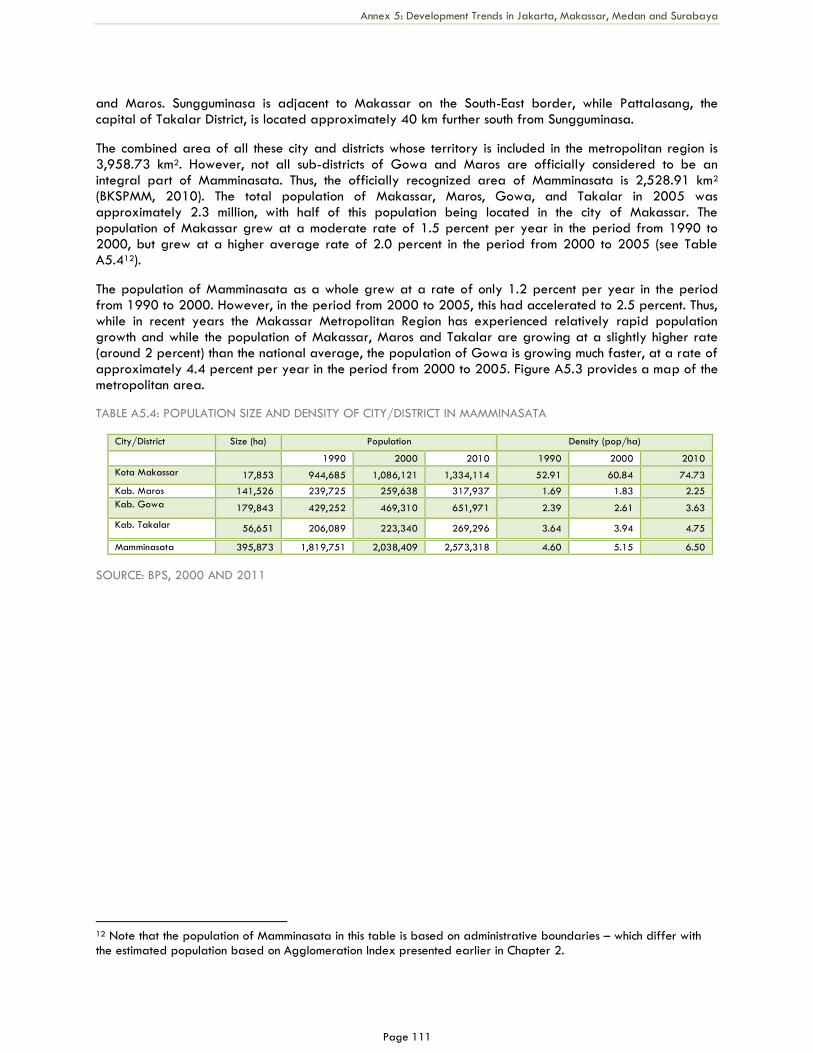

Table A5. 4 Population size and density of city/district in Mamminasata 111

Table A5. 5 Composition of real GRDP by sector in Mamminasata, 1993 and 2008 113

Table A5. 6 Land use of Mamminasata in 2003 (Km2) 115

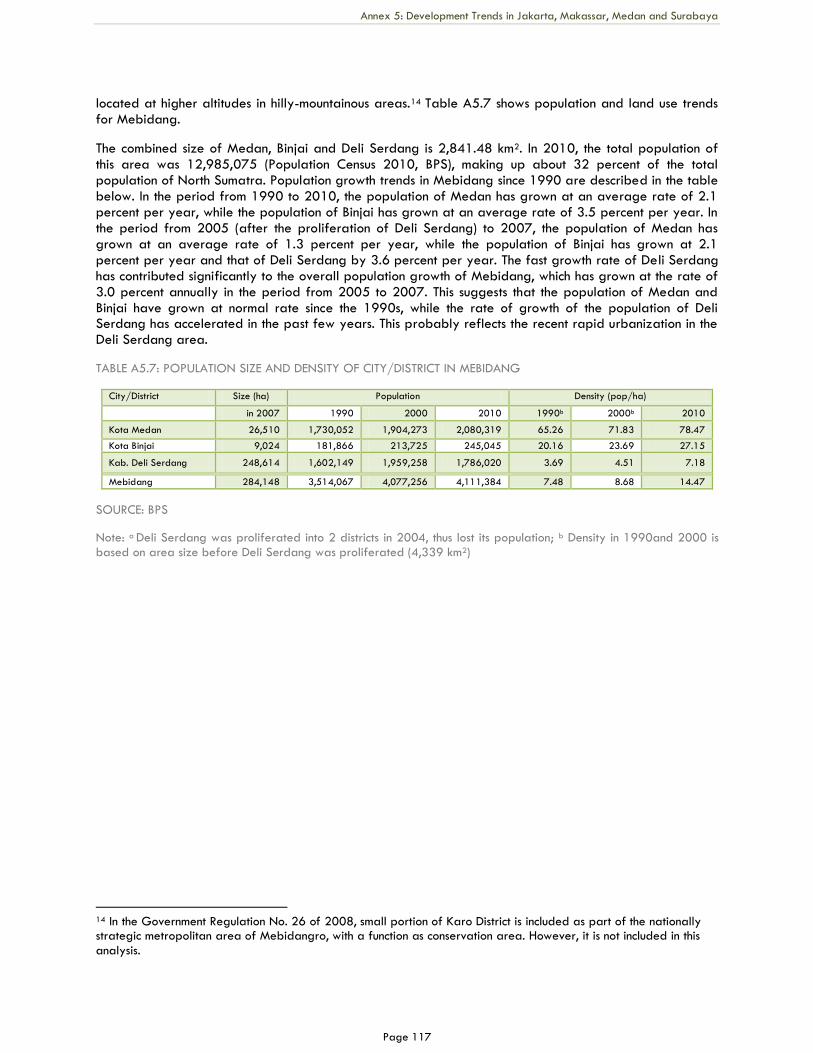

Table A5. 7 Population size and density of city/district in Mebidang 117

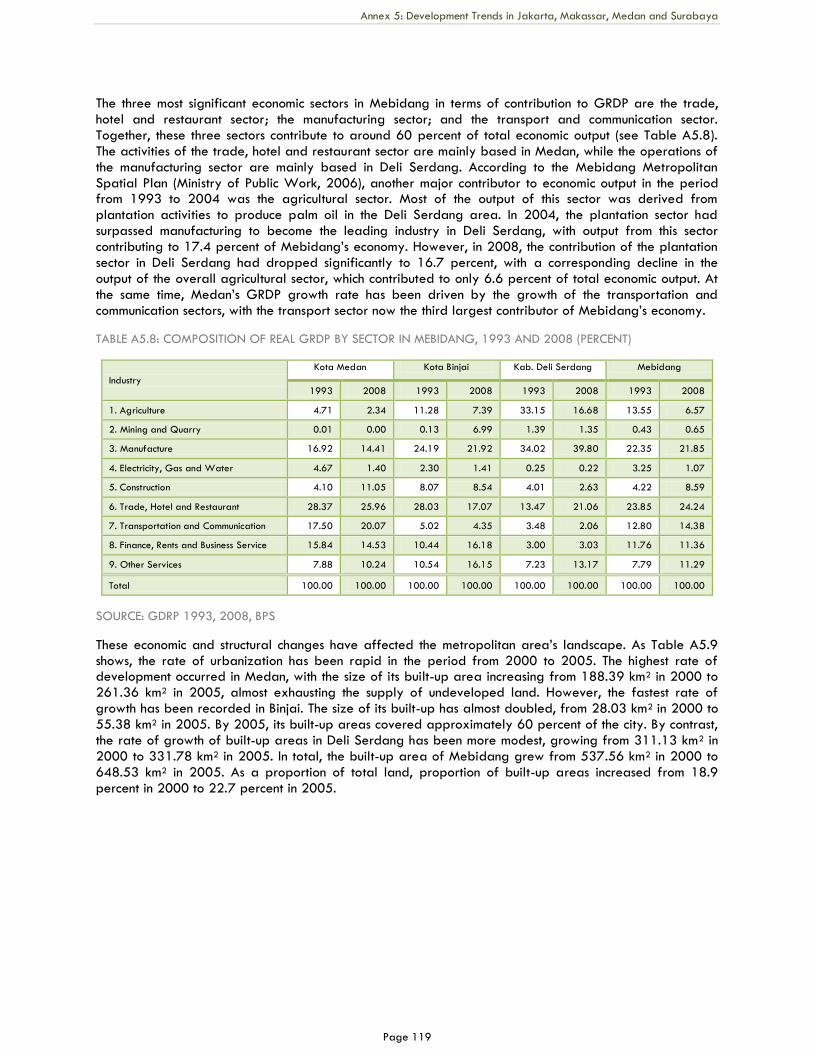

Table A5. 8 Composition of real GRDP by sector in Mebidang, 1993 and 2008 (percent) 119

Table A5. 9 Built-up area of city/district in Mebidang, 2000 and 2005 120

Table A5. 10 Population of Surabaya metropolitan region by district, 1990-2010 122

Table A5. 11 Population density by district in GKS, 1990 – 2010 122

Table A5. 12 Real GRDP by sector in GKS 2008 123

Table A5. 13 Built-up area of city/district in Surabaya metropolitan region, 2000 and 2005 124

Table A5. 14 Population in four metropolitan regions, 1993-2007 125

Page vii

LIST OF FIGURES AND BOX

Figure 1 Economic density is dominant in Java xi

Figure 2. 1 Compound annual growth urbanization rate 1970-2010 9

Figure 2. 2 Urban and rural population, 1970-2010 10

Figure 2. 4 Poverty ratio versus GRDP per capita for districts in metropolitan agglomerations, 2007 13

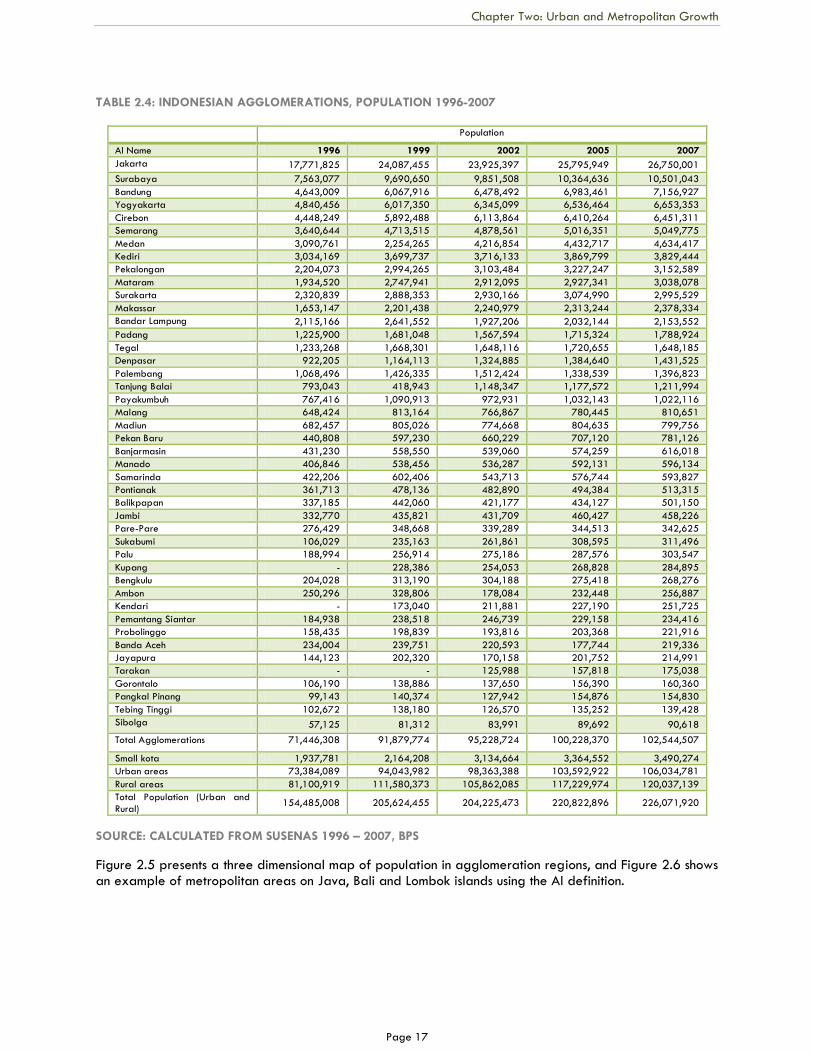

Figure 2. 5 Population in agglomeration region, 2007 18

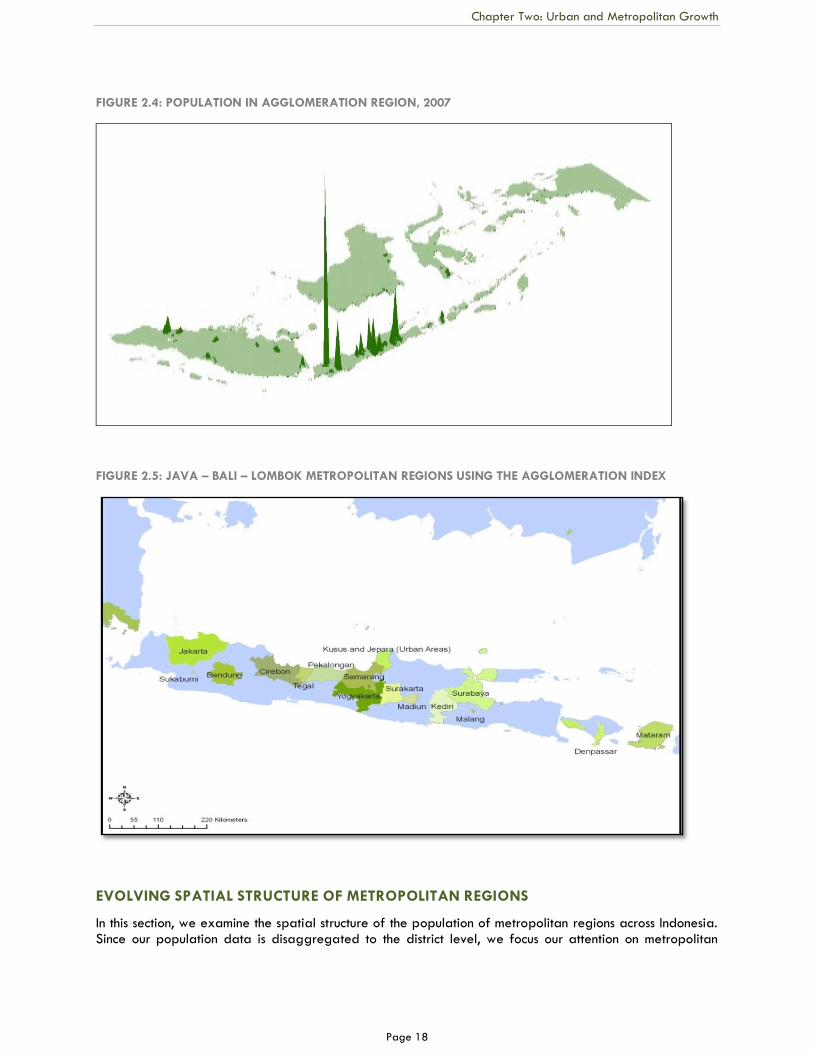

Figure 2. 6 Java – Bali – Lombok Metropolitan Regions using the Agglomeration Index 18

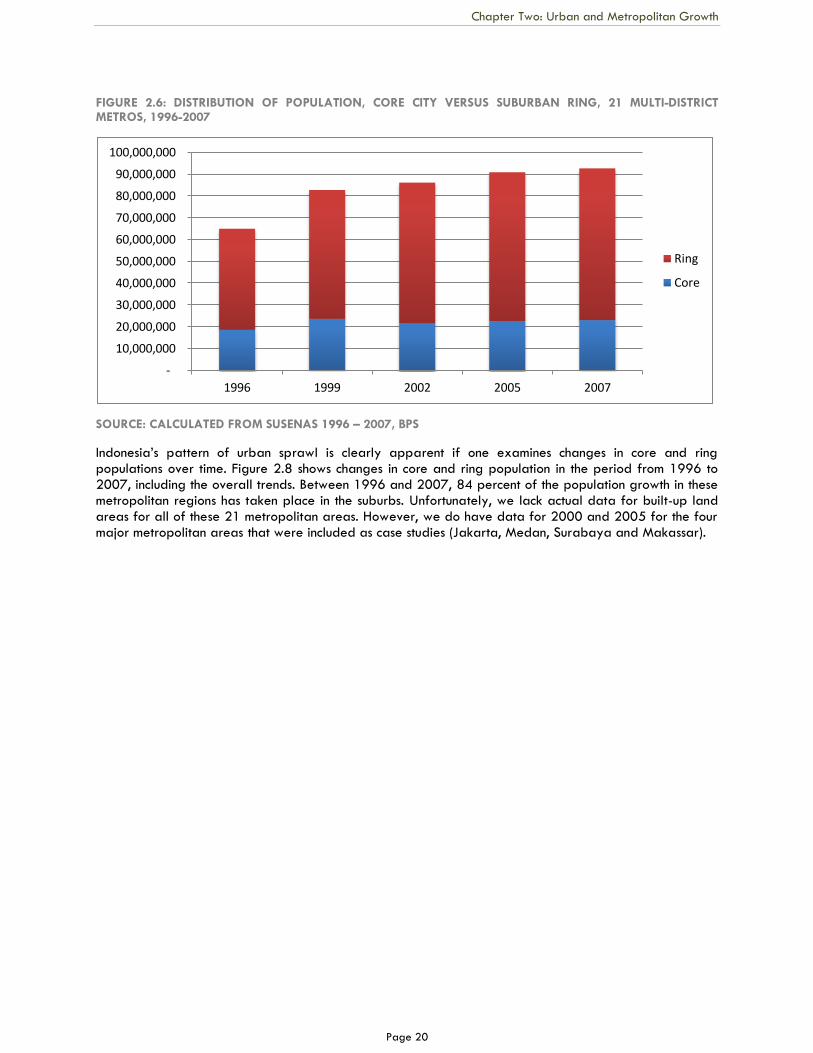

Figure 2. 7 Distribution of population, core city versus suburban ring, 21 multi-district metros, 1996-2007 20

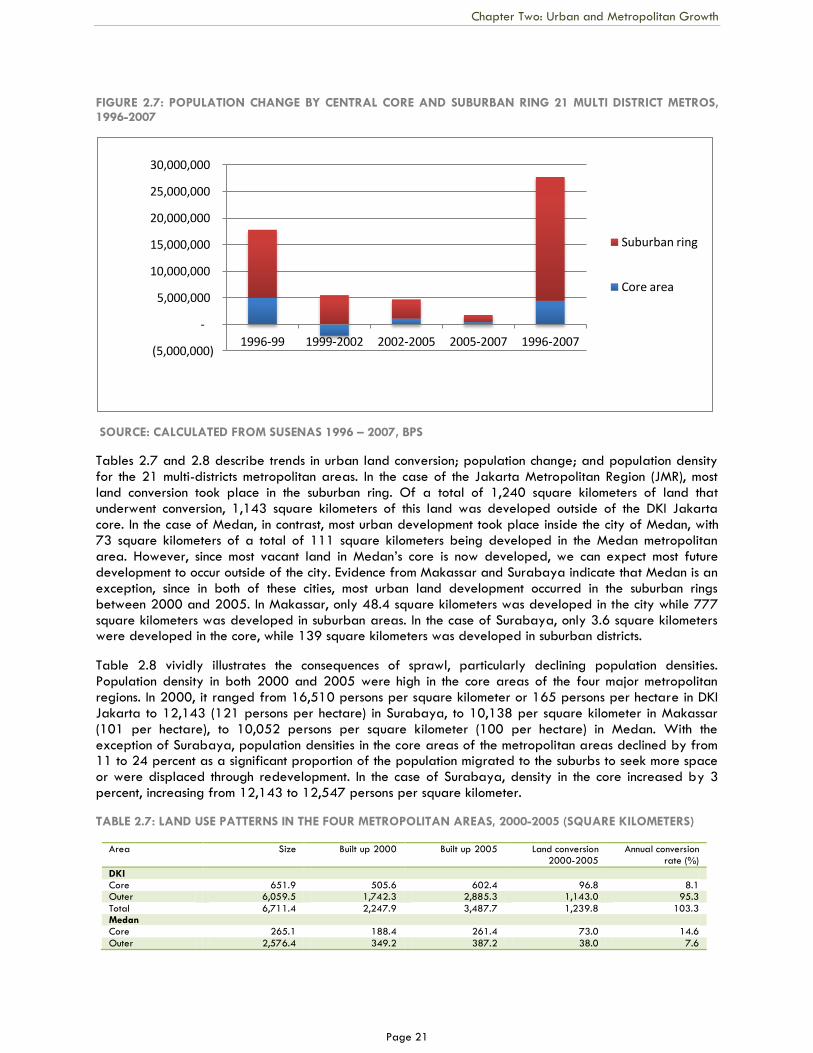

Figure 2. 8 Population change by central core and suburban ring, 21 multi district metros, 1996-2007 21

Figure 2. 9 Urban and rural population projections for Indonesia, 2010-2050 24

Figure 3. 1 Urbanization and per capita GDP across countries, 2005 28

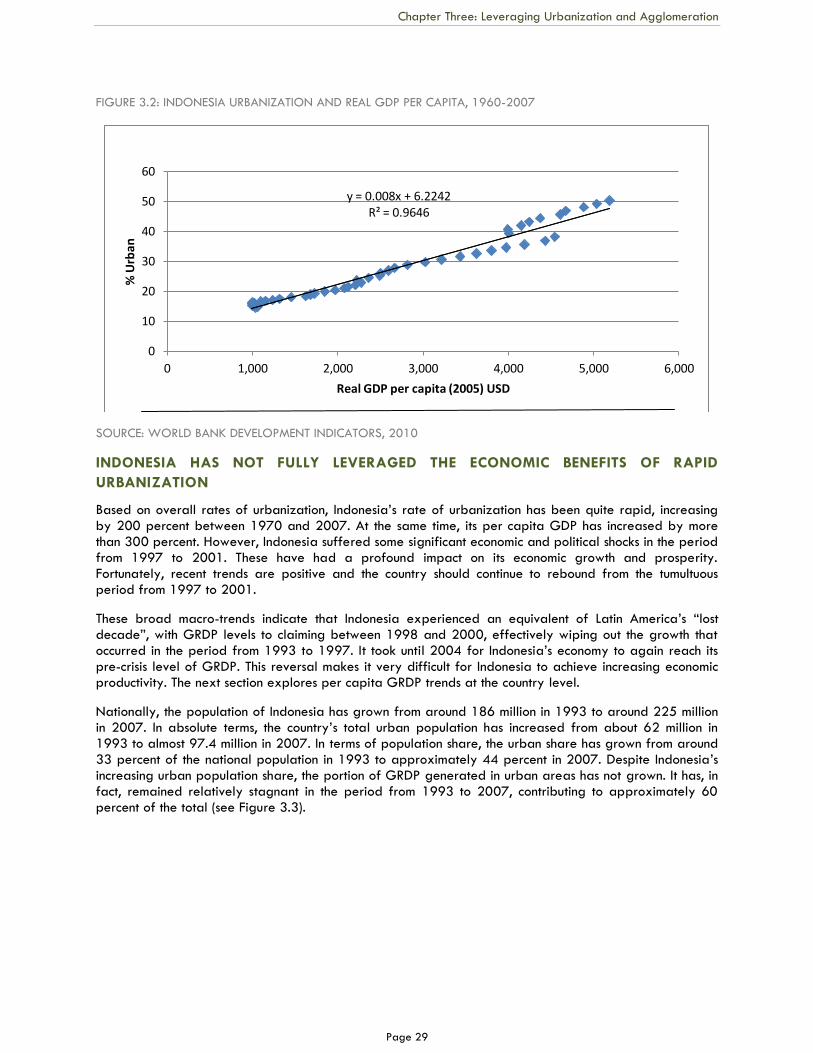

Figure 3. 2 Indonesia urbanization and real GDP per capita, 1960-2007 29

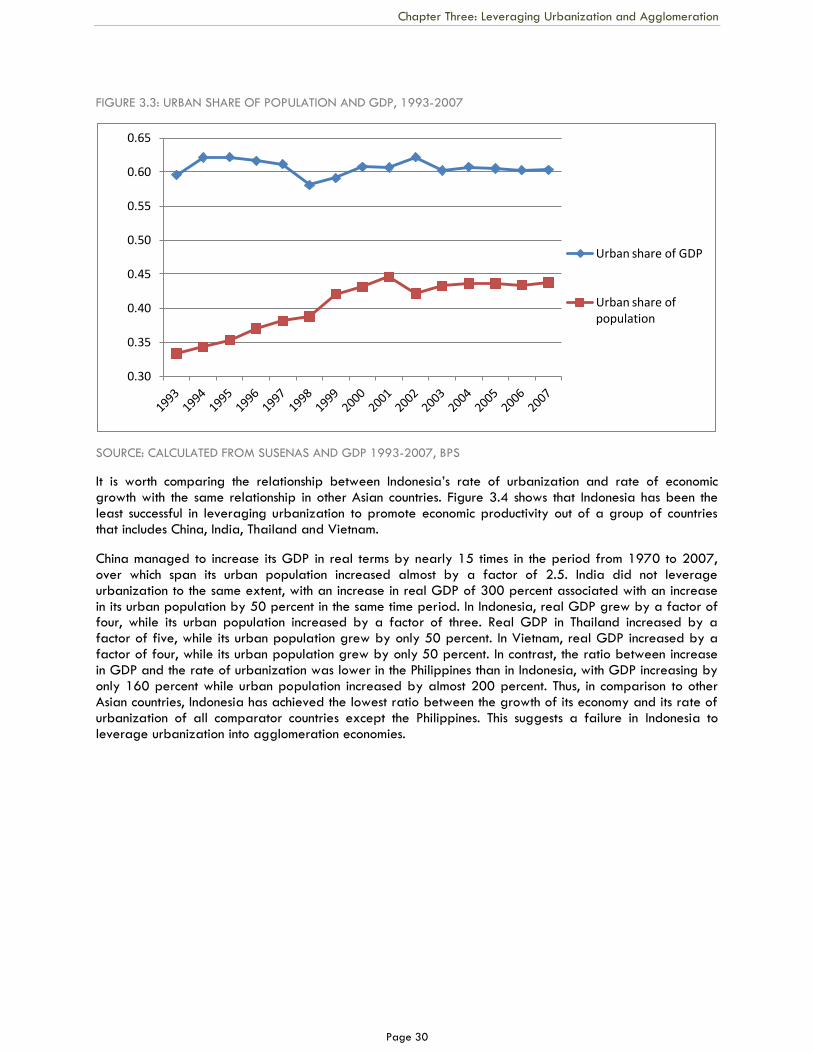

Figure 3. 3 Urban share of population and GDP, 1993-2007 30

Figure 3. 4 Comparison of GDP and urban population growth 1970-2007, indexed 1970 = 100 31

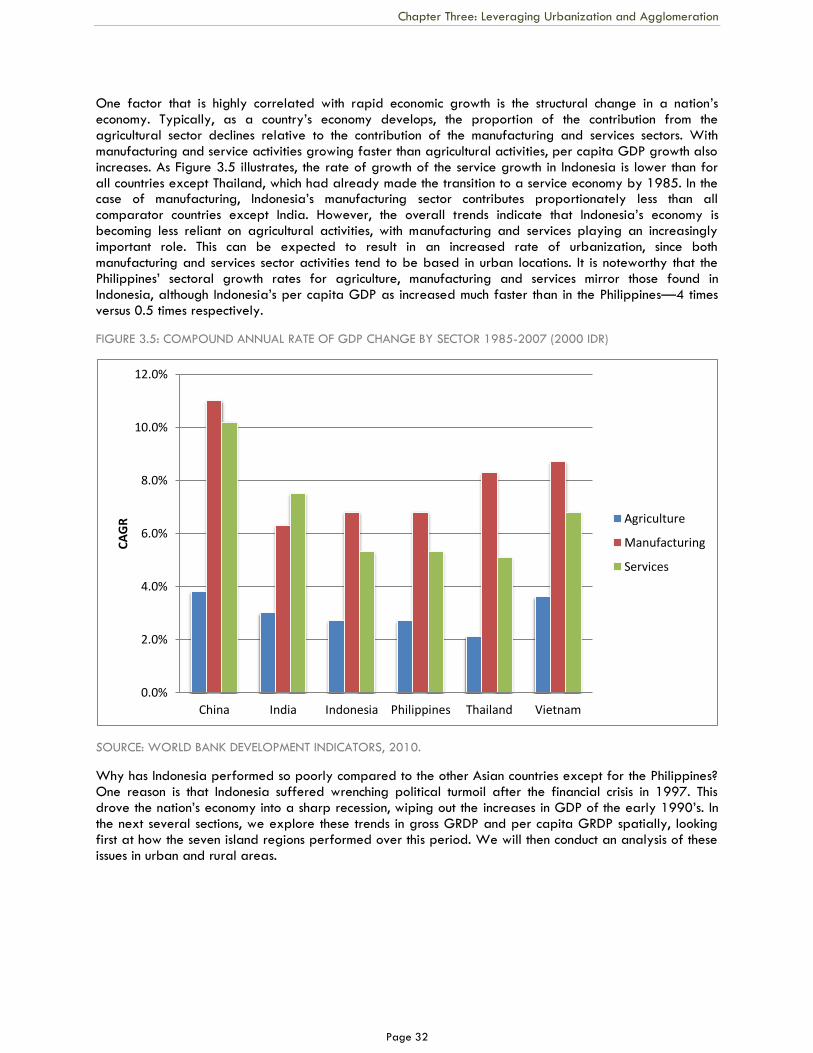

Figure 3. 5 Compound annual rate of GDP change by sector 1985-2007 32

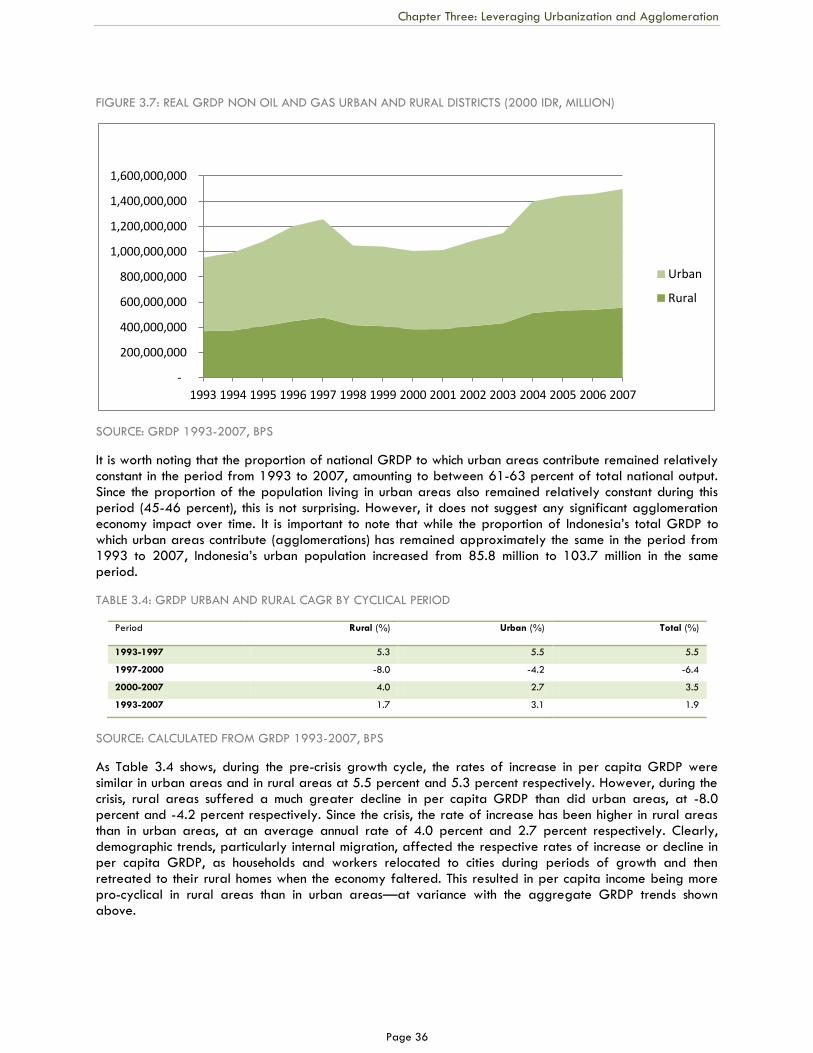

Figure 3. 6 Real GRDP non oil and gas 1993 - 2007 33

Figure 3. 7 Real GRDP non oil and gas urban and rural districts 36

Figure 3. 8 Per capita real GRDP by size of agglomeration area 38

Figure 4. 1 Total of GRDP generated in urban core and peripheral districts, for metropolitan regions with peripheral districts 46

Figure 4. 2 Strong periphery boost overall Metro area growth 47

Figure 4. 3 Per capita GRDP growth with better accessibility to population centers 48

Figure 4. 4 Textile firm growth improves when textile firms are clustered 48

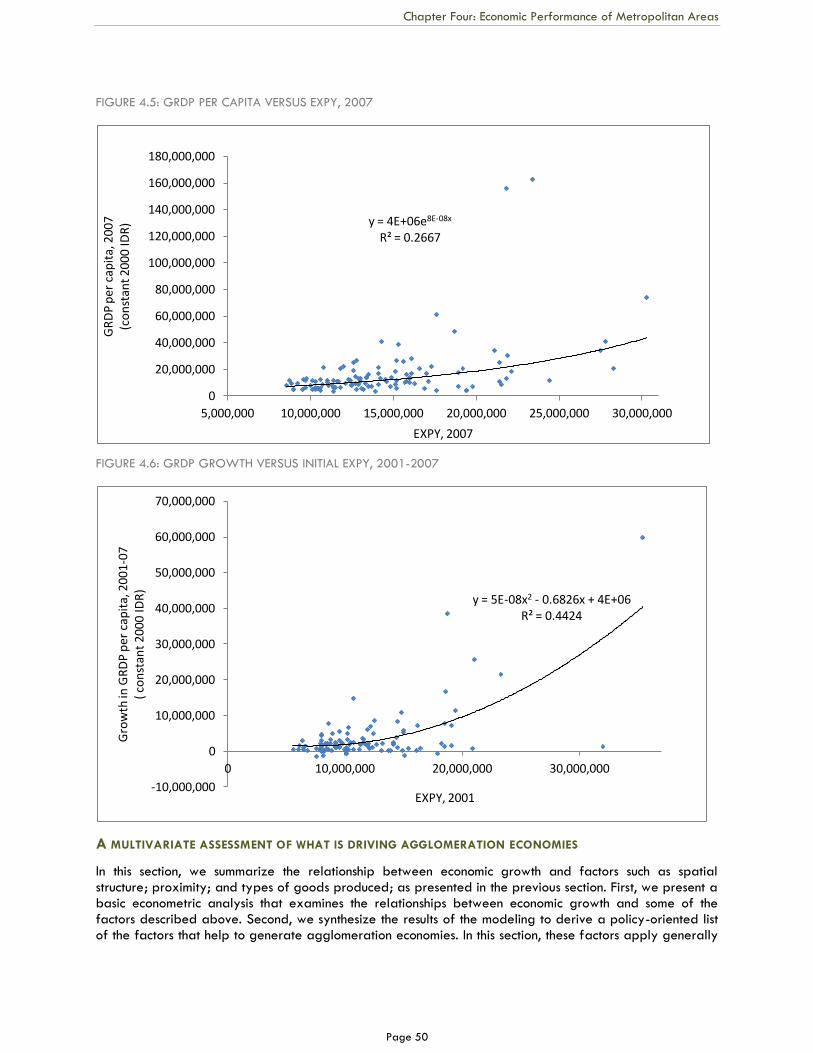

Figure 4. 5 GRDP per capita versus EXPY, 2007 50

Figure 4. 6 GRDP growth versus initial EXPY, 2001-2007 50

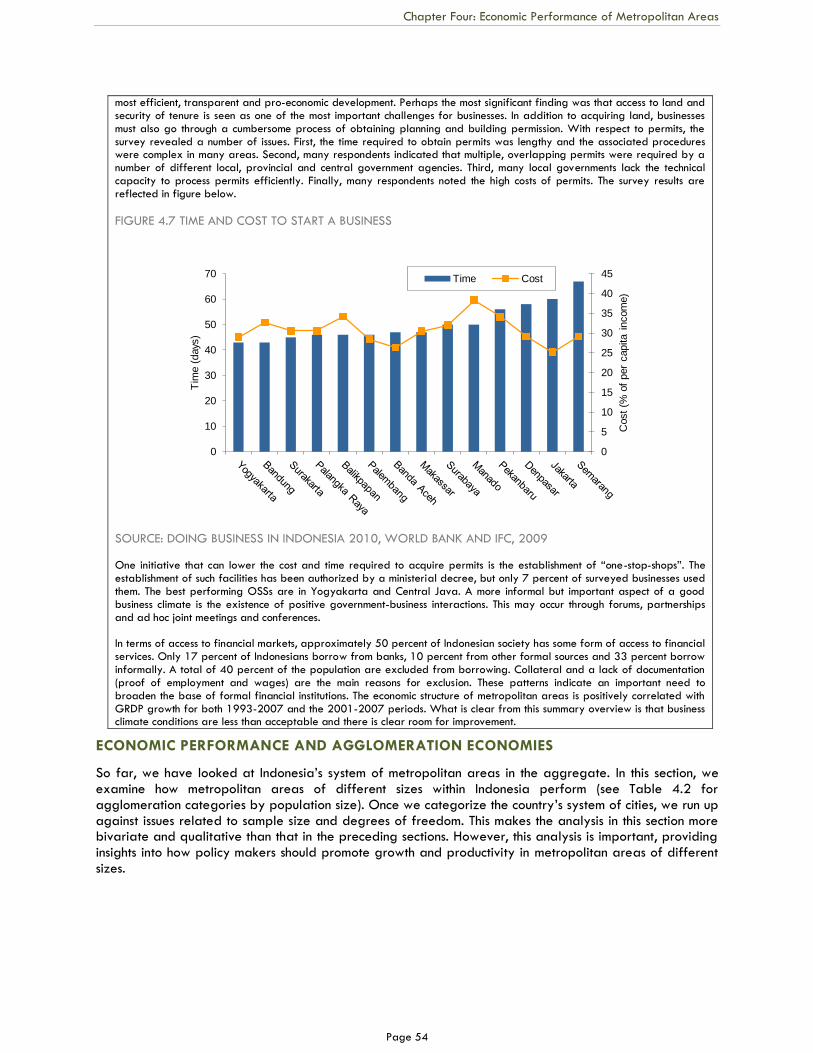

Figure 4. 7 Time and cost to start a business 54

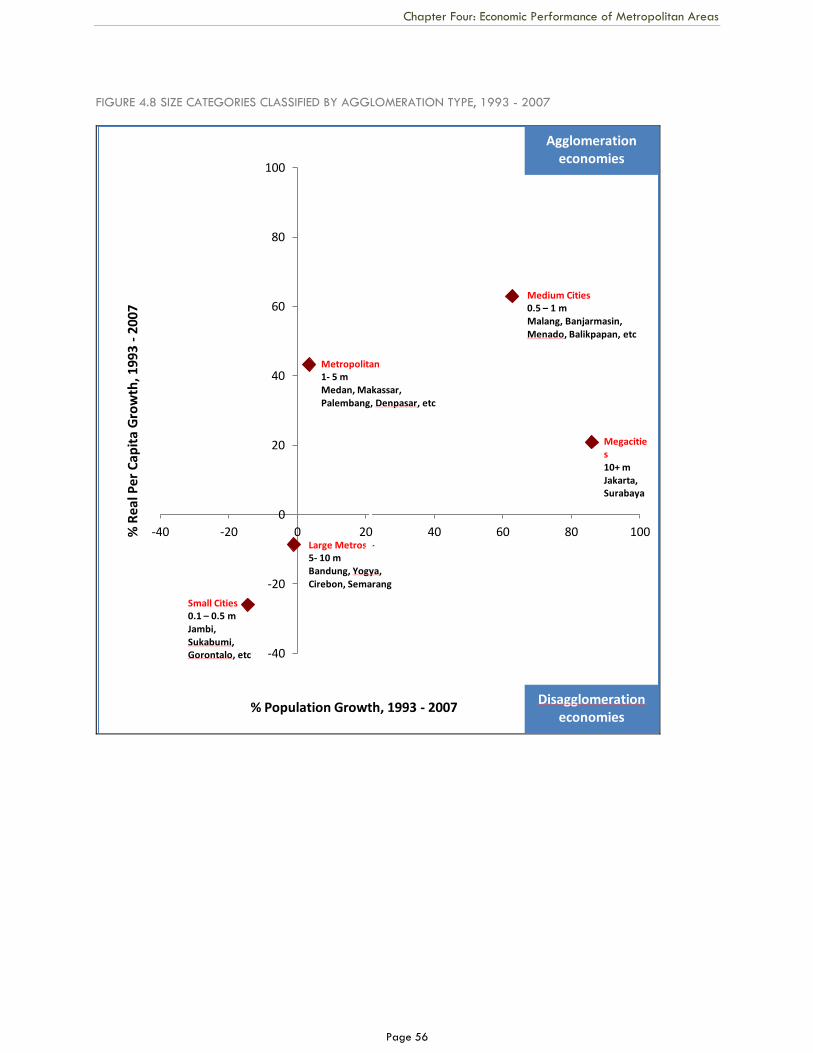

Figure 4. 8 Size categories classified by agglomeration type, 1993 - 2007 56

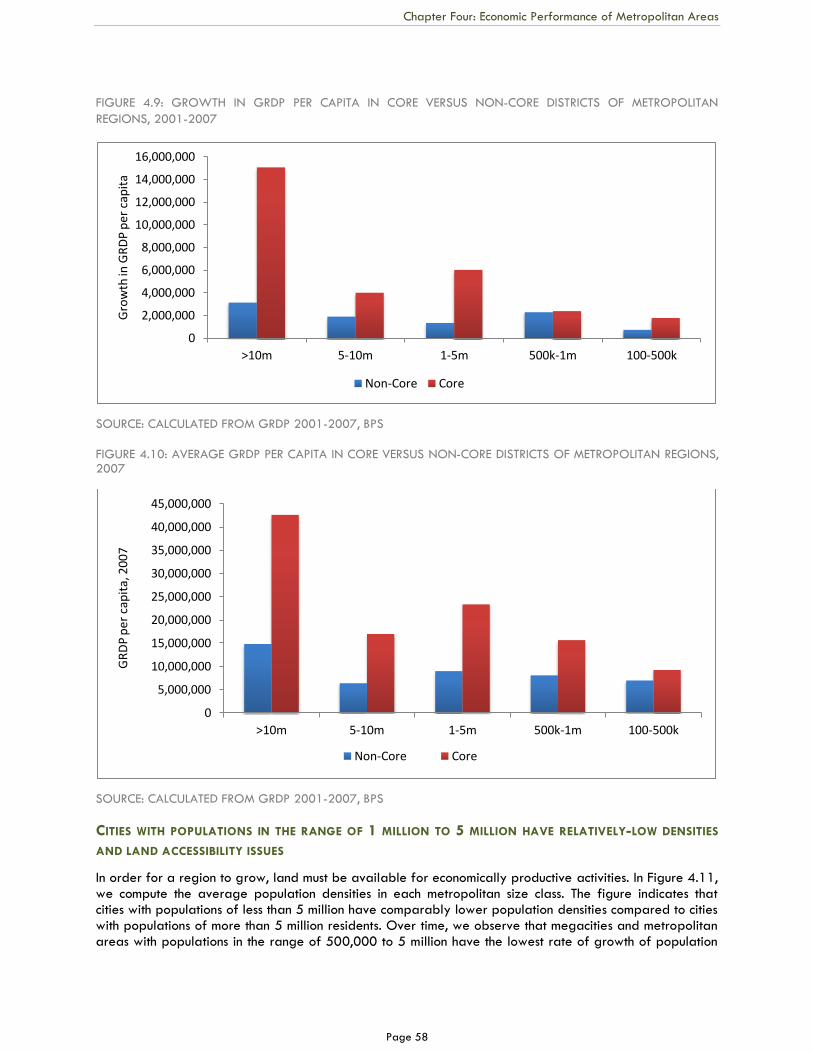

Figure 4. 9 Growth in GRDP per capita in core versus non-core districts of metropolitan regions, 2001-2007 58

Figure 4. 10 Average GRDP per capita in core versus non-core districts of metropolitan regions, 2007 58

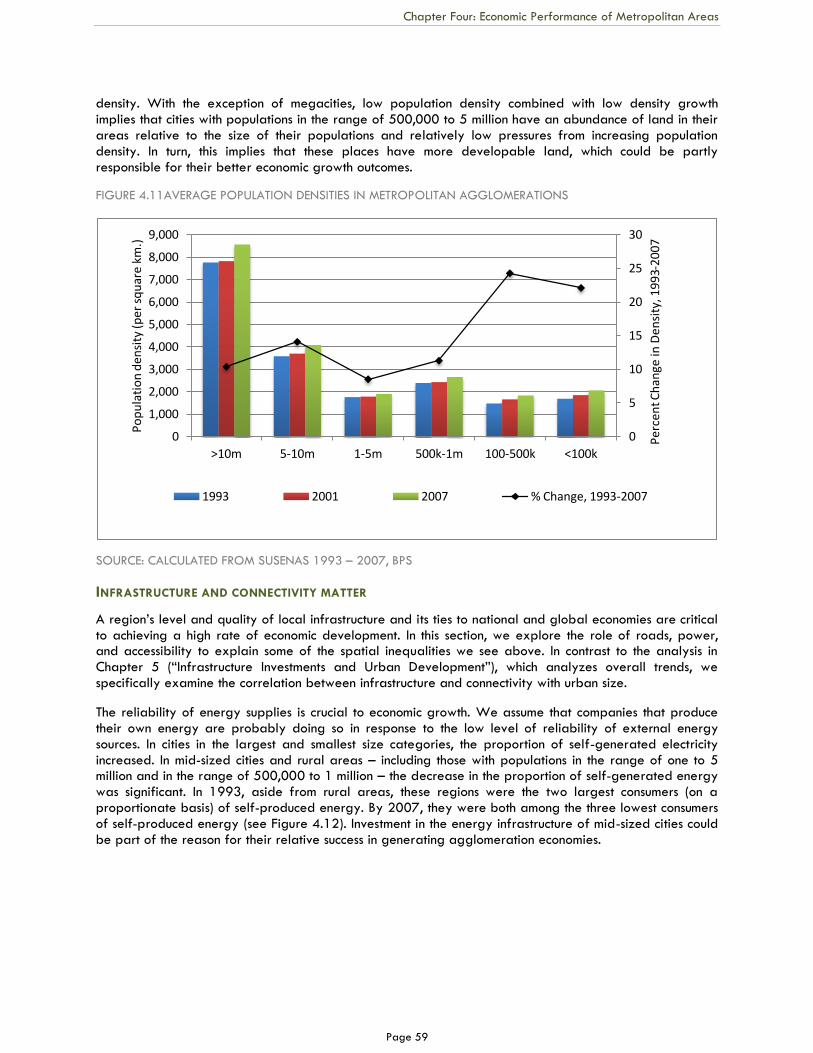

Figure 4. 11 Average population densities in metropolitan agglomerations 59

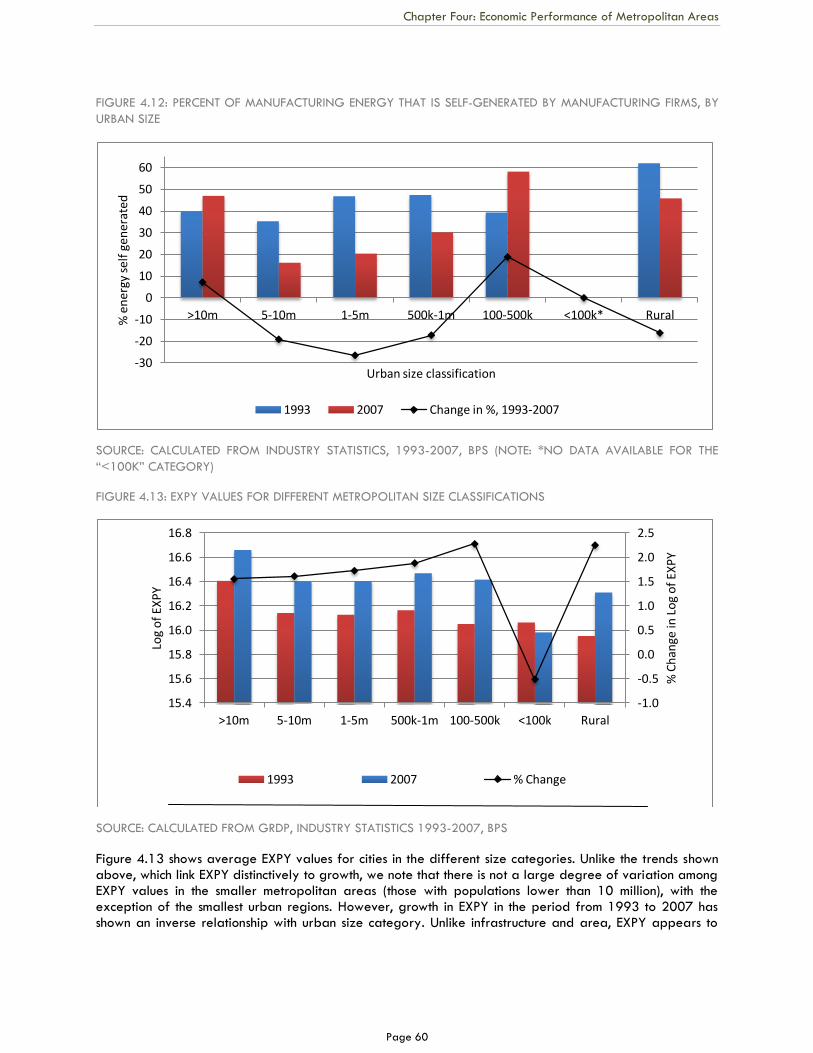

Figure 4. 12 Percent of manufacturing energy that is self-generated by manufacturing firms, by urban size 60

Figure 4. 13 EXPY values for different metropolitan size classifications 60

Figure 5. 1 Size distribution of local government capital spending, 2001 – 2008 64

Page viii

Figure 5. 2 Local government capital spending declines with urban population size, 2007 66

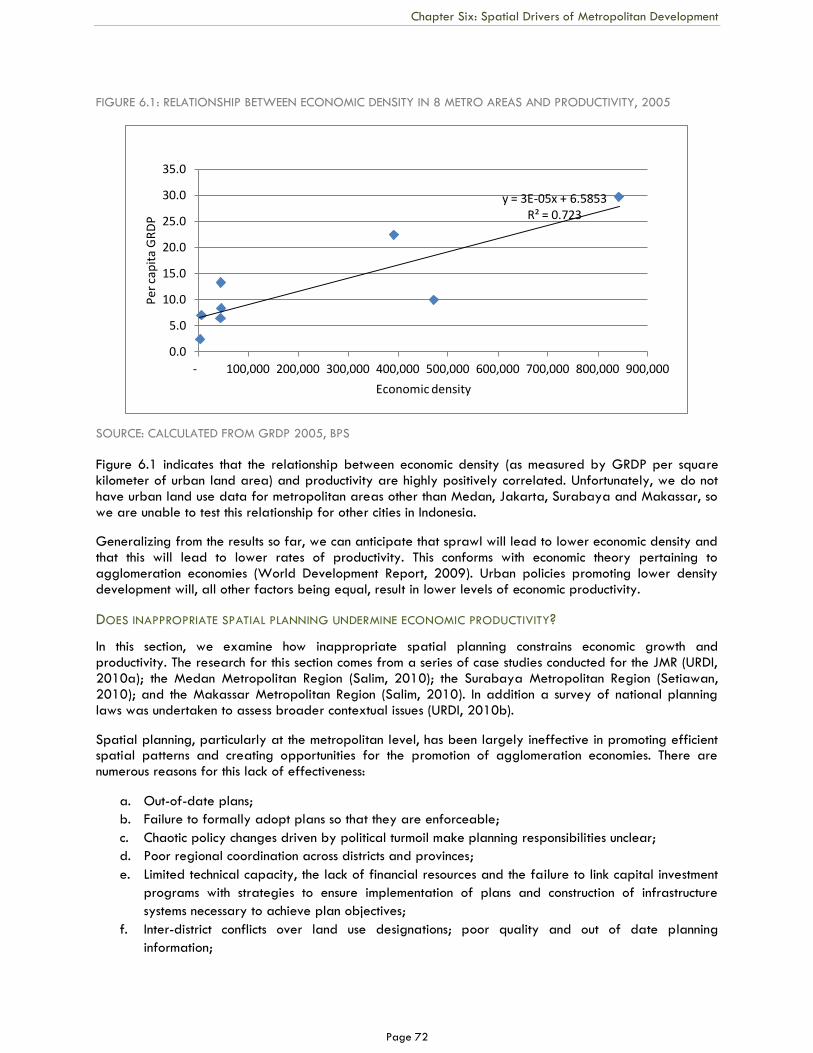

Figure 6. 1 Relationship between economic density in 8 metro areas and productivity, 2005 72

Figure 6. 2 Location of large-scale housing estates in the JMR 79

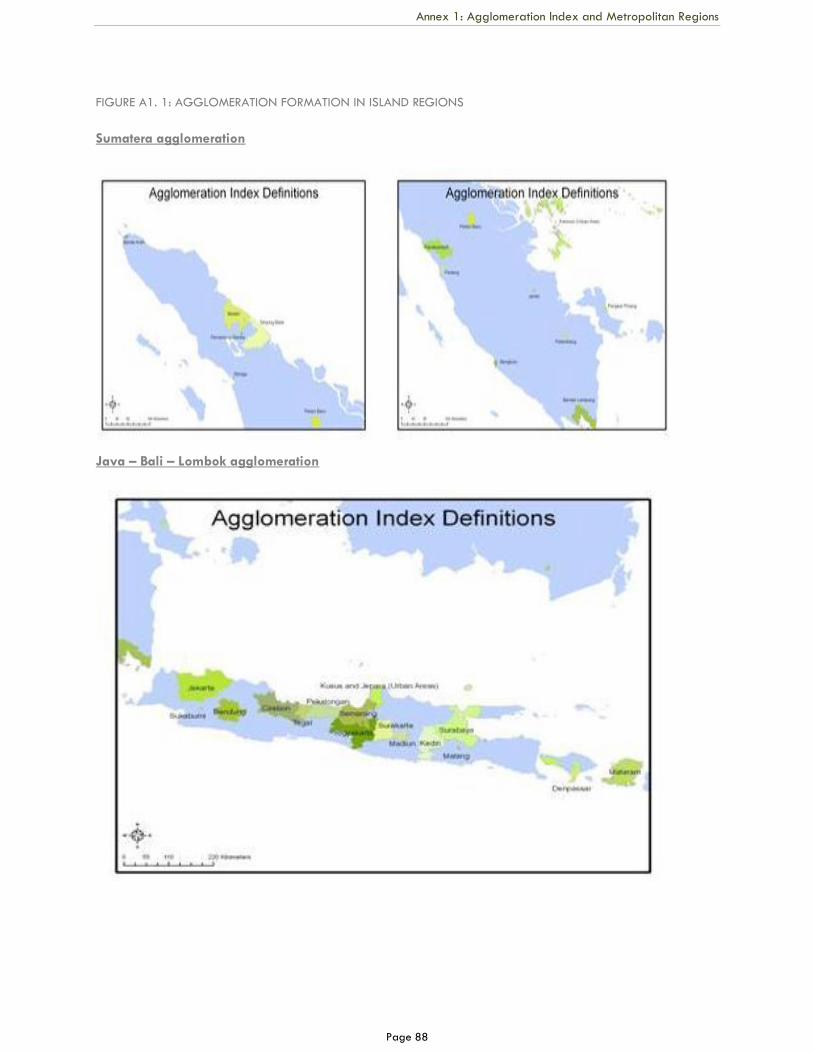

Figure A1. 1 Agglomeration formation in island regions 88

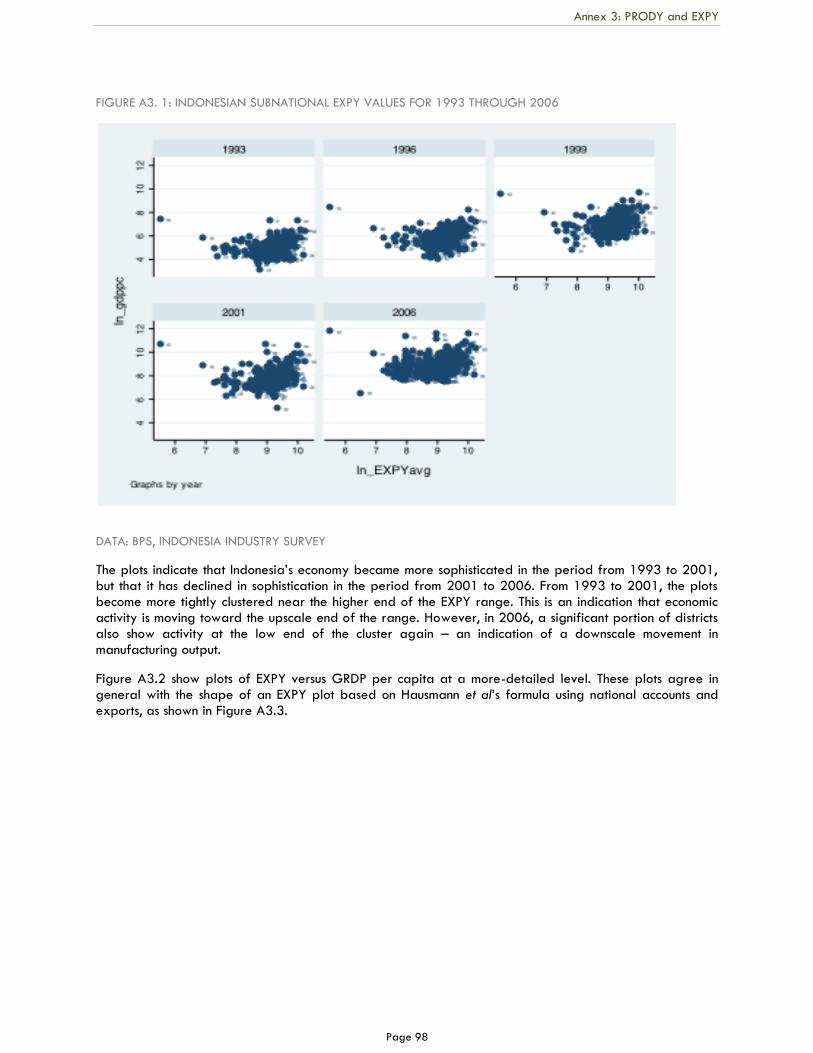

Figure A3. 1 Indonesian subnational EXPY values for 1993 through 2006 98

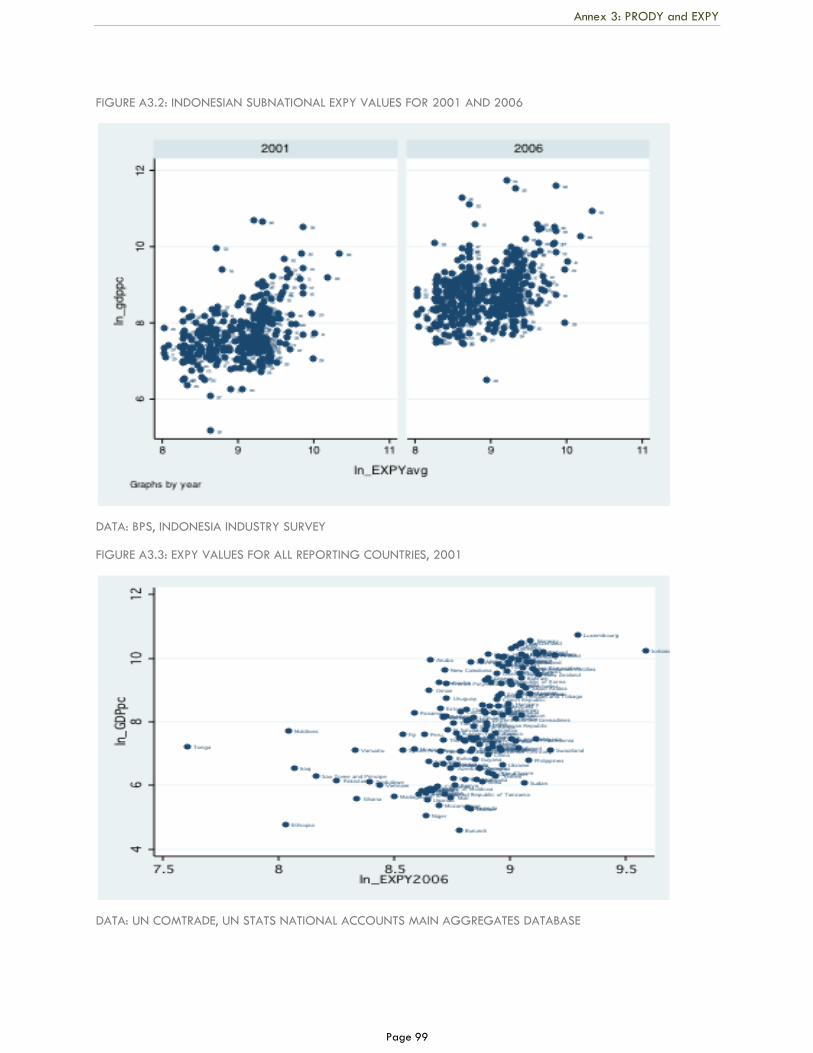

Figure A3. 2 Indonesian subnational EXPY values for 2001 and 2006 99

Figure A3. 3 EXPY values for all reporting countries, 2001 99

Figure A5. 1 Map of Jakarta Metropolitan Region 106

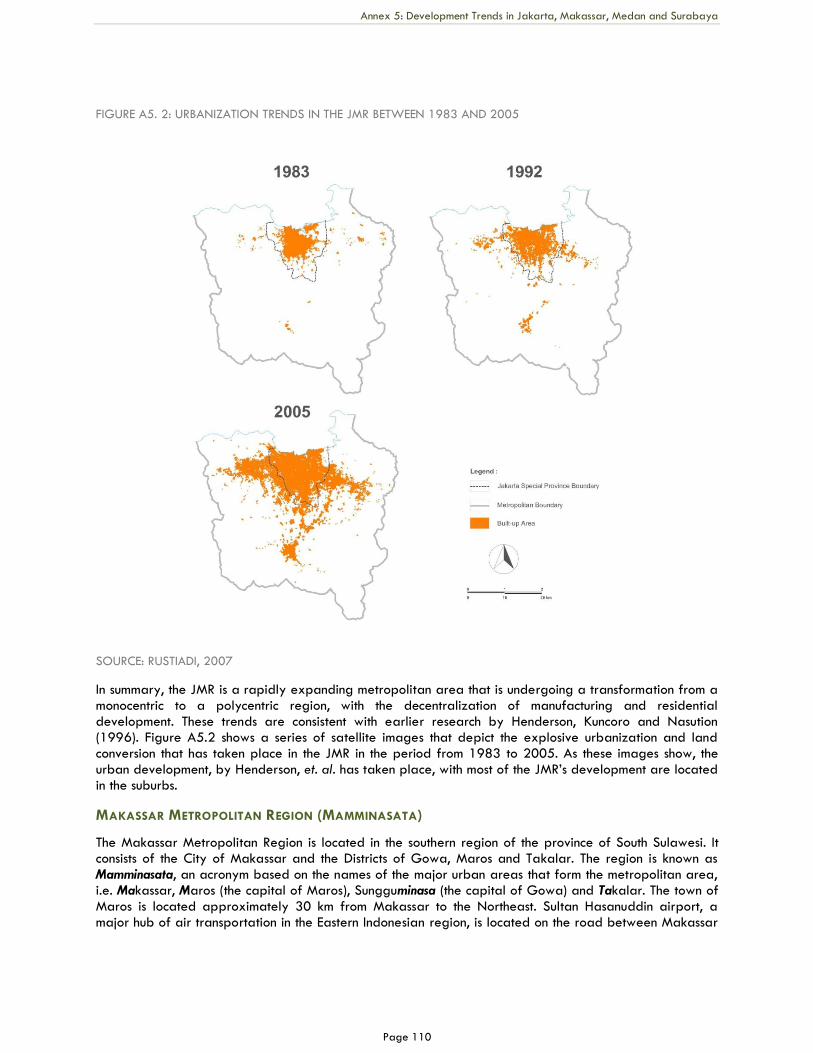

Figure A5. 2 Urbanization trends in the JMR between 1983 and 2005 110

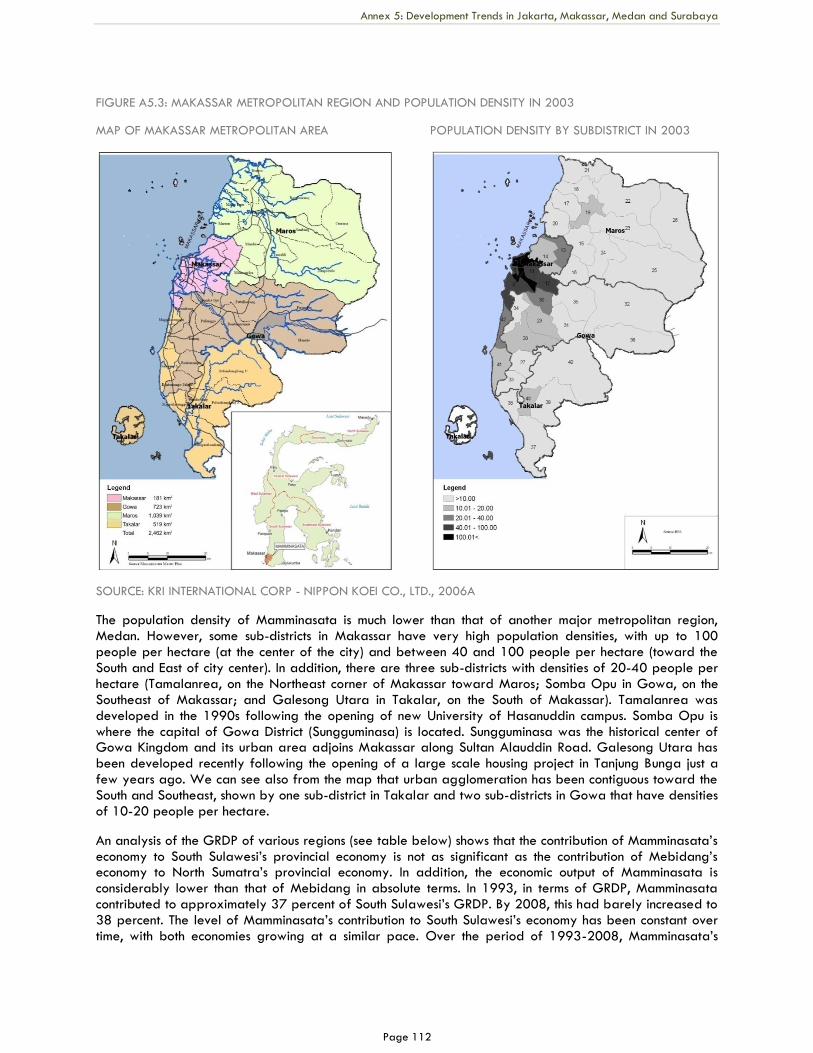

Figure A5. 3 Makassar Metropolitan Region and population density in 2003 112

Figure A5. 4 Land coverage map of Makassar Metropolitan Region in 2003 114

Figure A5. 5 Photos of peripheral development in Makassar 116

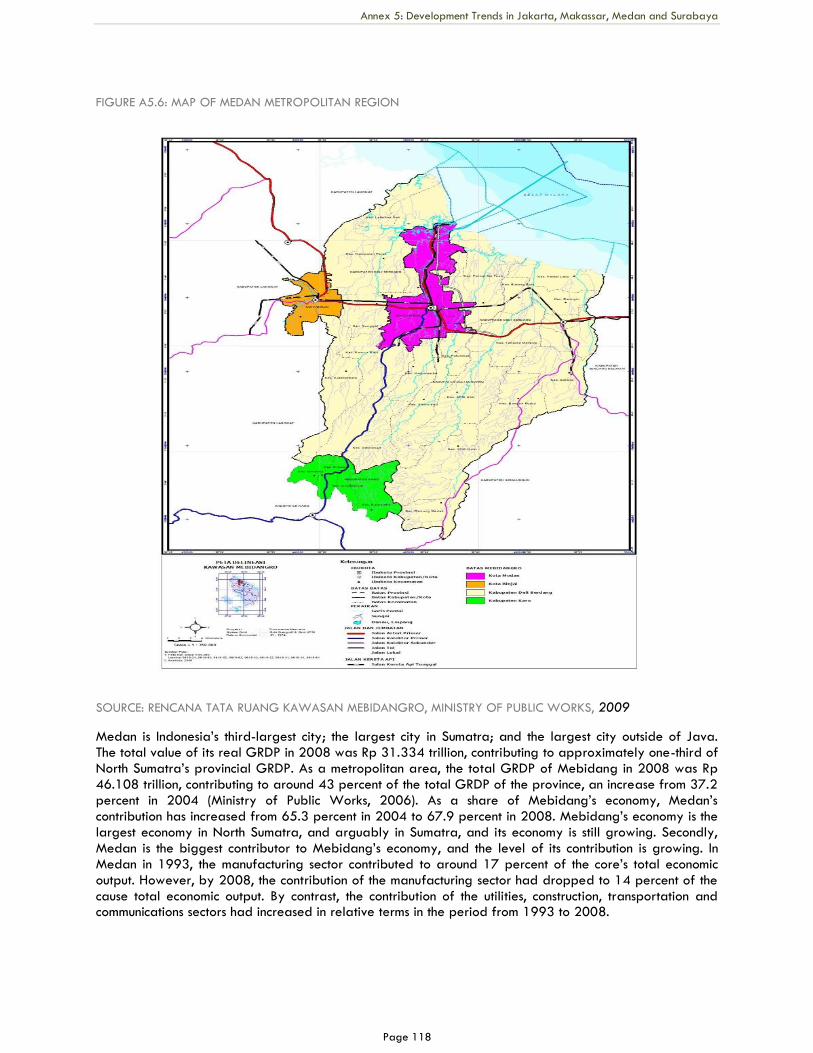

Figure A5. 6 Map of Medan Metropolitan Region 118

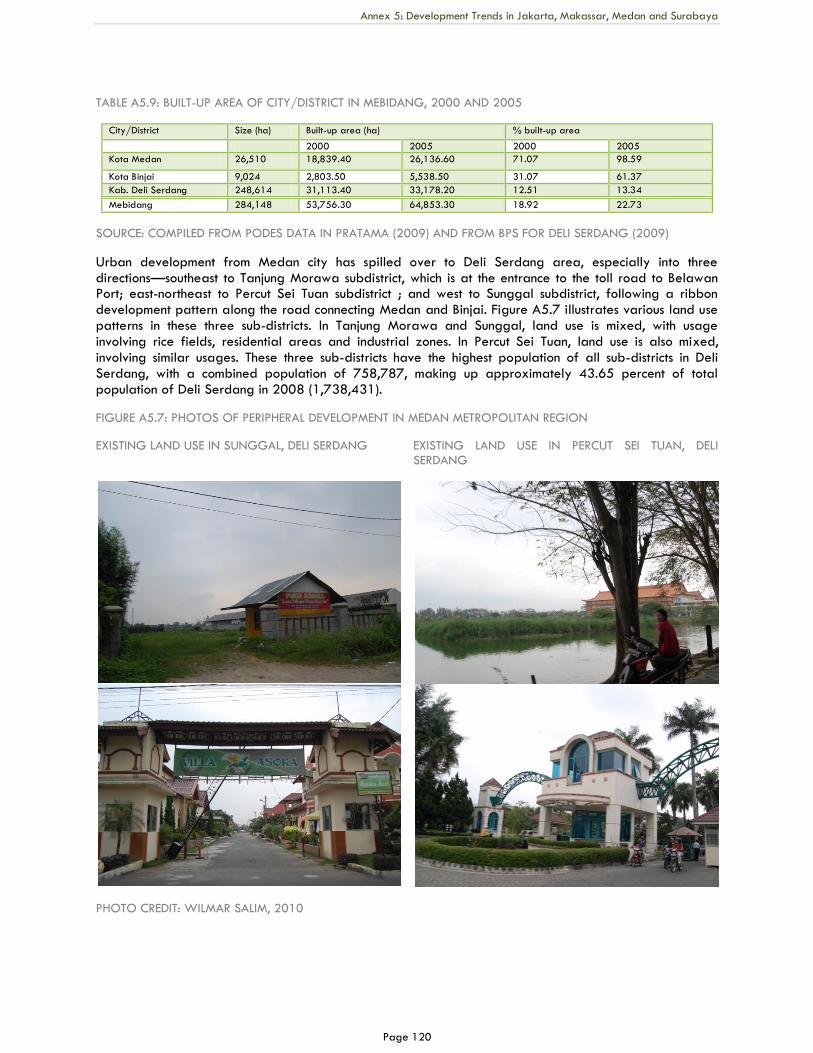

Figure A5. 7 Photos of peripheral development in Medan Metropolitan Region 120

Figure A5. 8 Surabaya Metropolitan Region 121

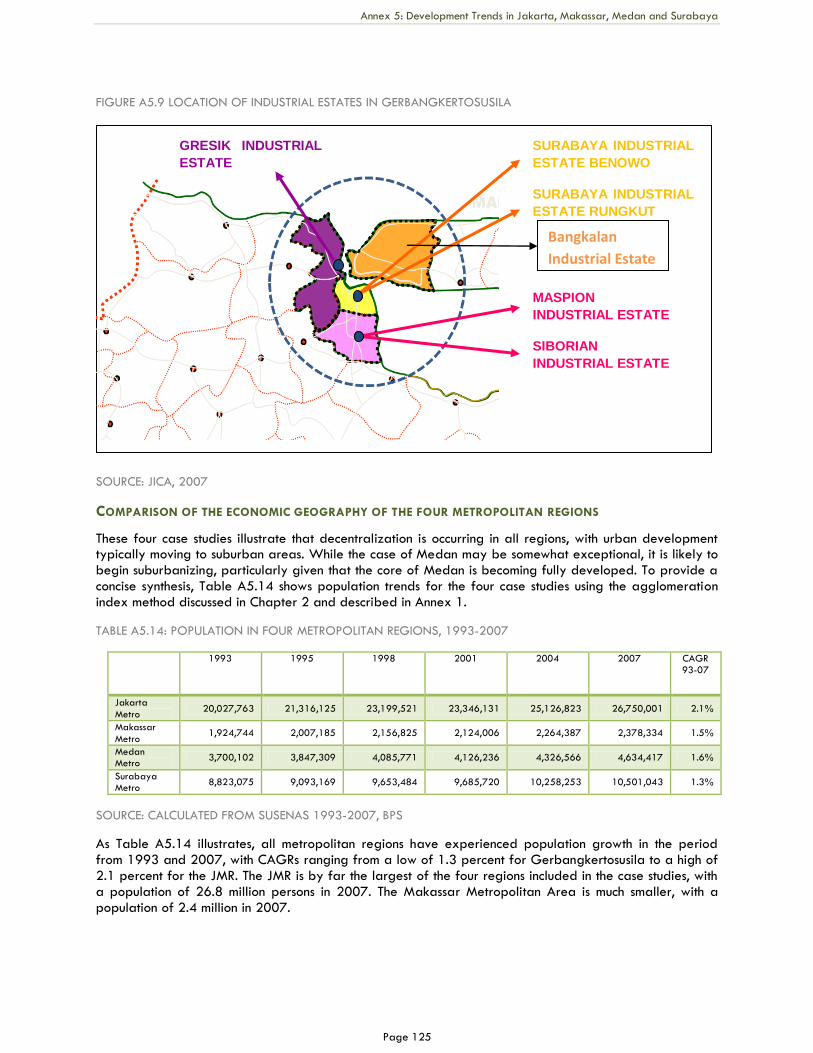

Figure A5. 9 Location of industrial estates in Surabaya Metropolitan Region 125

Page ix

EXECUTIVE SUMMARY

THE RISE OF METROPOLITAN REGIONS: TOWARDS INCLUSIVE AND

SUSTAINABLE REGIONAL DEVELOPMENT

Indonesia has urbanized rapidly and will continue to do so into the mid-term future. By 2025,

approximately 67.5 percent of Indonesia‘s population will live in urban areas. Urbanization is occurring

across the country at varying rates, although at a faster rate in some island regions outside Java-Bali. This

suggests that in the future, urbanization related challenges that have affected Jakarta and Java-Bali will

similarly affect these other regions.

Urbanization creates significant opportunities for Indonesia, with urbanization’s potential to boost

regional economic growth and create vibrant cities and metropolitan areas. Urbanization and the

agglomeration economies that it can generate should be an important element in Indonesia‘s development

as a middle income country. If managed properly, urbanization can generate the productivity gains,

economic opportunities and rising incomes needed to support the increasingly large proportion of

Indonesia‘s middle income earners.

Indonesia has the potential to substantially increase its economic returns from urbanization. Research

in the period over the last 30 years confirms that most countries in the East Asia region experienced growth

in economic output as they become increasingly urbanized. Consider that in the period from 1970 to 2006,

every 1 percent increase in urban population correlated with an average 6 percent increase in per capita

GDP for India and China; an 8 percent increase in per capita GDP for Vietnam; and a 10 percent

increase in per capita GDP for Thailand. However in some Asian countries, including the Philippines and

Indonesia, similar rates of increase in urbanization relate to less than 2 percent increase of per capita

GDP. It is important to consider that each country‘s patterns of urbanization and economic growth have

been unique and contingent on a wide range of variables. In the case of Indonesia, unique challenges

relate, amongst other matters, to the difficulty of connecting growth centers in an archipelagic country,

together with fundamental challenges in spatial planning, metropolitan management and the functioning of

land markets, connective and strategic infrastructure, all of which are underpinned by persistent

institutional challenges. However, similar issues are being addressed successfully in other middle income

countries. Similarly, Indonesia is at a stage of urbanization where it too can take action.

Larger cities in general are more economically productive and competitive than smaller cities and rural

areas because of positive externalities known as agglomeration. There are broadly two types of

agglomeration economies: urbanization economies and localization economies. Large cities create

opportunities for the establishment of localization economies through the clustering of related activities,

while urbanization economies may emerge in dense urban areas where the transaction cost of doing

business are lower and opportunities for knowledge spillover is high. With the benefits of agglomeration,

Page x

businesses within such economies tend to be more economically productive, as demonstrated by a faster

rate of growth in GRDP than in smaller cities and rural areas.

Using the Agglomeration Index method, this study identifies 44 agglomeration areas in Indonesia. The

majority of these agglomeration areas are located in Java, Bali and Sumatra, in which islands most of the

urban population now resides. In other islands, the study identifies only a limited numbers of agglomeration

areas. There is only one agglomeration (Jayapura) on the vast island of Papua and also only one in the

Maluku archipelago, while Kalimantan and Sulawesi have five and six agglomeration areas, respectively.

In terms of size of population, Indonesia has two megacities with populations of more than 10 million

population (Jakarta and Surabaya), four metropolitan areas with populations in the range of 5 – 10

million, 13 metropolitans with populations in the range of 1 – 5 million and eight medium-sized

metropolitan areas with populations in the range of 0.5 – 1 million.

Medium-sized metropolitan areas (those with populations in the range of 0.5 – 1 million) have

performed better than cities in any other size class in terms of generating benefits from agglomeration

economies. Over the last 20 years, the medium-sized cities have seen the strongest per capita growth in

GRDP. This has been accompanied by strong to moderate population growth. The megacities (Jakarta and

Surabaya) have performed well, despite a continuing influx of newcomers and serious infrastructure

challenges. However, their economies grew at lower rates than those of the medium-sized cities relative to

their rates of growth in population. Among cities of all size categories, the small cities have performed

least well, experiencing declines in population and per capita GRDPs. Analysis of trends in land,

population, infrastructure, investment climate, and economic sector data indicate that the medium-sized

cities have been able to leverage urbanization for economic growth.

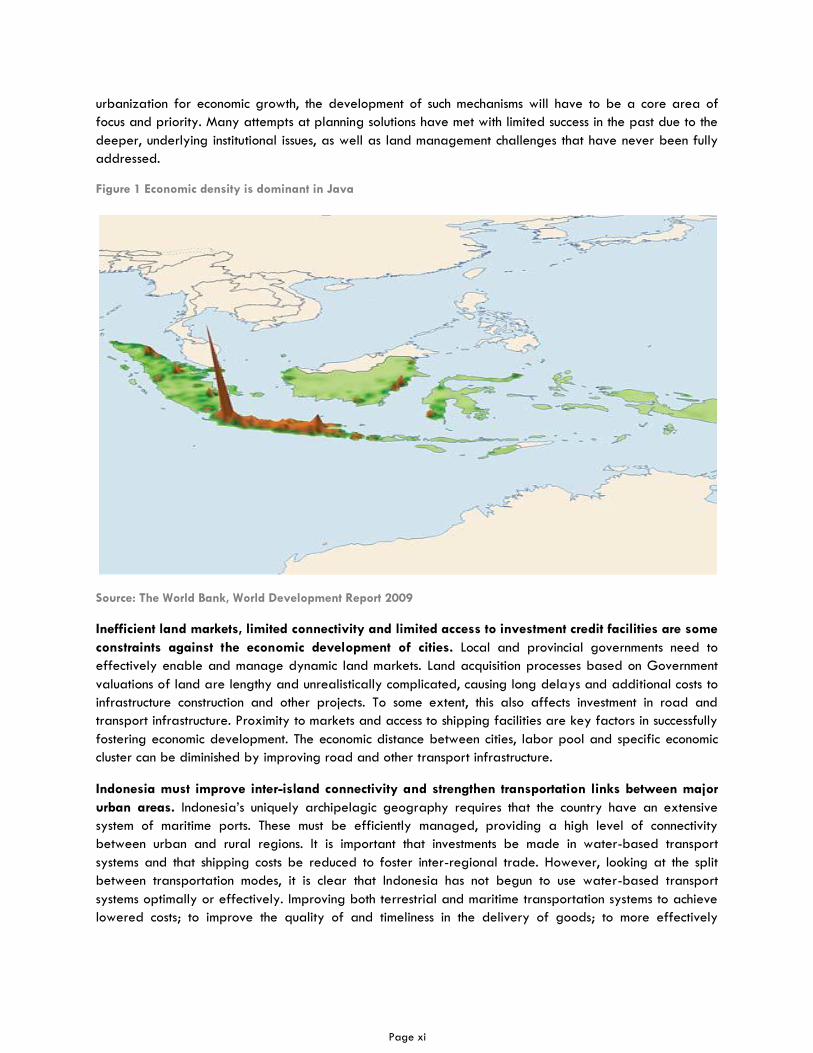

The Jakarta Metropolitan Region (JMR) in particular, and the Java-Bali regions in general, will

continue to play an important role in economic development. Figure 1 shows the high demographic and

economic concentration across Java and on Bali, especially in the country‘s two largest metropolitan

regions, Jakarta and Surabaya. Despite the relatively high levels of productivity Jakarta and Surabaya,

these metro areas urgently need to improve their economic efficiency and to develop facilities to ensure

the quality of life of their residents. Their economies face a number of constraints, including congestion,

poor spatial planning at the regional level, poorly functioning land markets, inadequate transportation

systems, a massive infrastructure backlog, pollution.

The core cities lead in economic output; however the urban periphery should also play an important

role as a driver of growth and agglomeration. Research shows that cities that rely to a greater degree

on their peripheries for the location of productive facilities generate higher rates of GRDP per capita and

a faster rate of economic growth. This fact points to three phenomena:

a) Many metro regions are gradually de-concentrating their centers as they grow into their

peripheries;

b) Periphery areas need to be prepared to receive industry; and

c) This expansion spans across multiple jurisdictions, often with conflicting interests.

These phenomena call urgent attention to the need for mechanisms that optimize and coordinate

development at a scale more complex and much larger than a city: rather, these mechanisms must operate

at the scale of metropolitan areas that may include one or more cities. If Indonesia is to leverage

Page xi

urbanization for economic growth, the development of such mechanisms will have to be a core area of

focus and priority. Many attempts at planning solutions have met with limited success in the past due to the

deeper, underlying institutional issues, as well as land management challenges that have never been fully

addressed.

Figure 1 Economic density is dominant in Java

Source: The World Bank, World Development Report 2009

Inefficient land markets, limited connectivity and limited access to investment credit facilities are some

constraints against the economic development of cities. Local and provincial governments need to

effectively enable and manage dynamic land markets. Land acquisition processes based on Government

valuations of land are lengthy and unrealistically complicated, causing long delays and additional costs to

infrastructure construction and other projects. To some extent, this also affects investment in road and

transport infrastructure. Proximity to markets and access to shipping facilities are key factors in successfully

fostering economic development. The economic distance between cities, labor pool and specific economic

cluster can be diminished by improving road and other transport infrastructure.

Indonesia must improve inter-island connectivity and strengthen transportation links between major

urban areas. Indonesia‘s uniquely archipelagic geography requires that the country have an extensive

system of maritime ports. These must be efficiently managed, providing a high level of connectivity

between urban and rural regions. It is important that investments be made in water-based transport

systems and that shipping costs be reduced to foster inter-regional trade. However, looking at the split

between transportation modes, it is clear that Indonesia has not begun to use water-based transport

systems optimally or effectively. Improving both terrestrial and maritime transportation systems to achieve

lowered costs; to improve the quality of and timeliness in the delivery of goods; to more effectively

Page xii

facilitate people movement will generate manifold benefits related to the increased economic integration

between regions and the opportunities to develop supply chains between small, medium and large cities.

Indonesia’s surface transportation network is inadequate. Highway construction and maintenance has

not kept pace with the country‘s need to develop strong linkages between regions. In the case of Java and

Sumatra, the GOI should consider the construction and further development of trans-Java and trans-

Sumatra highways to increase the efficiency of surface transportation. On Java, a trans-Java corridor

would create strong linkages between Jakarta and Surabaya, as well as with and between the secondary

cities, such as Bandung, Semarang and Yogyakarta.

Capital expenditure on infrastructure is insufficient in the metropolitan areas. Local governments in

rapidly urbanizing areas need to increase both the level and effectiveness of their capital expenditures.

Otherwise, they risk facing severe constraints to economic growth in the future. Capital expenditure on

infrastructure by local governments has a significant and positive influence on district economic growth. At

present, local governments that are relatively more urbanized and/or that have relatively larger urban

populations spend less on capital projects than other local governments. Capital expenditure needs to be

increased in more urbanized local districts.

The Master Plan for Acceleration and Expansion of Indonesia’s Economic Development (MP3EI) was

formulated on the assumption that each region needs to be treated differently in terms of policy and

investment. For example, in Java, the plan promotes improvements to intra-island connectivity through

improved road networks and other strategies intended to support greater development of higher valued

manufacturing. In Sumatra, the plan supports the development of the natural resource economy and

processing capacities for natural resources. In Sulawesi, the plan supports improvements to maritime

connectivity, with the primary focus of economic development being on agribusiness and fisheries.

In summary, Indonesia needs to leverage the positive impacts from its rapid pace of urbanization to a

far greater degree than it has so far. Indonesia has come to a significant turning point: the manner in which

the country urbanizes over the next 15 to 20 years is of crucial long term significance to the country‘s

socio-economic development. Urbanization is a path dependant process. Once a city is built, the

constructed area of the city, together with the institutional relations that develop and define the systems of

management of the city, become increasingly locked-in. In such situations the most important task is to

ensure that initial conditions are correct and implemented in the right sequence, as these conditions will

either powerfully enable or constrain the future growth of that city and its economy. This underscores the

need to take the necessary and appropriate action before the opportunity passes.

PROPOSED POLICY ACTIONS

The GOI needs a multi-faceted strategy for managing urbanization to further leverage regional

growth. Indonesia‘s urban development strategy needs to focus on two main points: (i) ensuring greater

consistency between spatial planning and investment priorities between the different tiers of government

(national, provincial and local); and (ii) the stratification of local governments according to size

characteristics (two largest metropolitan regions; second tier metropolitan areas, rapidly agglomerating

medium-sized cities, and small cities).

The GOI needs to link urbanization trends with the Economic Transformation Master Plan (MP3EI).

Agglomerations are areas of economic activity that the Government can support to boost regional growth.

Supporting such agglomerations would be much more effective and less risky than endeavors to create

Page xiii

new growth poles. The Master Plan for Regional Development has already identified many existing growth

centers and should focus on encouraging local economic initiatives to support these centers.

The GOI needs to improve consistency between spatial plans and investments. Spatial planning must

be coordinated between different levels of government and between districts into which metropolitan

areas fall, so that plans and investment priorities are more closely aligned with investment priorities.

Investment plans for large-scale infrastructure also need to be developed, with these plans needing to take

into account impacts on urban land markets. A higher level of investment is needed in critical infrastructure

(electrical power, transit, surface and maritime transportation networks and basic services). For example,

industrial and business and consumer services districts need to be developed and provided with better

transportation facilities to ensure accessibility to residential zones.

Investment must be increased in Indonesia’s two largest cities, Jakarta and Surabaya. In this report,

cities are defined on the basis of the Agglomeration Index. The Jakarta and Surabaya metropolitan

regions need to promote agglomeration economies. Priorities must include institutional reforms and

investments to improve spatial structure through metropolitan level planning that spans multiple jurisdictions;

support better functioning land markets; improve resilience to natural disasters, such as flooding; and

enhance the quality of life through greater environmental sustainability. Industrial policies to attract a

greater proportion of higher value added activities are needed. To ensure the availability of the human

resources required to these activities, higher quality educational and training institutions are also required.

Major attention needs to be focused on the second tier of metropolitan cities, which are currently

stagnating. Some of Indonesia‘s major second tier cities, including Bandung, Yogyakarta, Cirebon and

Semarang, have not experienced increases in real per capita GRDP over the last 15 years. In the period

from 1993 to 2007, productivity in the cities declined by an average of 10 percent, which is equal to 0.7

percent Compound Annual Growth Rate (CAGR). Central, provincial and district governments need to

upgrade and expand physical and social infrastructure and urban services; to improve the spatial

efficiency (higher densities, industrial and business services centers); to ensure that urban land markets

function more efficiently; and to implement measures to achieve better intra-metropolitan connectivity and

better coordination in the development of metropolitan regions. Importantly, these large metropolitan

areas need to be better linked with larger city regions. Institutional reforms are also needed to improve

the business climate and to reduce the costs of doing business in Indonesia.

The GOI should promote growth in rapidly agglomerating metropolitan and medium-sized cities. In

general, these cities have adequate infrastructure and do not suffer from poor spatial structure. However,

they need higher quality and more expensive infrastructure, particularly infrastructure that supports

connectivity with major centers and ports. As these cities continue to agglomerate, they should maintain

their capital investment programs. Maintaining sound spatial planning and land management can help

these cities enhance productivity, while investment in regional transportation facilities can provide an

additional boost for these cities.

Within small cities the focus should be on the delivery of basic services. These small urban areas have

inadequate infrastructure, inadequate supply of skilled labor and low level of access to markets in major

metropolitan regions, impeding their ability to compete. Rural and lagging regions need to be better

connected to large and medium-sized metropolitan centers. The small cities also need to invest more

heavily in basic infrastructure and to ensure more effective inter-governmental coordination and

management. These cities need to improve their level of access to larger and more prosperous regions; to

improve land market performance; and to create a more positive business climate.

Page xiv

Urbanization presents an opportunity for Indonesia. Urban areas are major contributors to and key

drivers of growth in non-oil GDP. Linking the patterns of urban development to the MP3EI presents on

opportunity to focus on ensuring that existing growth centers perform even better and play an even more

significant role. This is much more likely to be successful than endeavors to establish new growth poles,

which is a very risky and potentially very expensive strategy. Differentiating policy approaches on the

basis of variations in city size will also help the GOI to ensure that its support to different cities is

appropriate to their needs.

Page 1

CHAPTER 1

OVERVIEW AND METHODOLOGY

The objective of this report is to analyze Indonesia‘s regional and urban economic development. The report

will analyze the role of urbanization in shaping agglomeration economies, along with the determinants of

competitiveness in affecting the development of urban (metropolitan) areas, particularly large urban

areas. The report is part of an ongoing engagement and partnership between the World Bank and the

Government of Indonesia (GOI), represented primarily by Bappenas (THE NATIONAL DEVELOPMENT PLANNING

AGENCY). The report is intended to assist and provide input for GOI institutions and agencies as these

institutions and agencies develop a more comprehensive framework for regional and urban economic

development. It will achieve this by defining the role of large cities as centers of economic growth. The

report will be an important contribution to improved understanding of the constraints and steps needed to

improve urban and regional economic growth, competitiveness and service delivery.

The aim of this report is to describe and outline issues related to the major priorities for Indonesia‘s

national urban development strategy. It includes:

(i) An overall descriptive assessment of spatial urban and regional development trends over time;

(ii) An analysis of the relative impact of factors such as location, industrial concentration and

scale, diversity of economic activities, as well as governance and institutional performance on

metropolitan area economic development;

(iii) An identification of the critical constraints to regional and urban economic development based

on the analytical work; and

(iv) A series of policy suggestions for promoting balanced and sustainable urban and regional

development across Indonesia.

One of the major contributions of the research that supports this report is the development of an integrated

and consistent time series database of regional and urban development indicators disaggregated to the

district (kabupaten/kota) level. This database aggregates data from a variety of sources and covering the

period from 1993 to 2007. This allows us to explore spatial and sectoral trends during the pre-1997 crisis

period and the post-crisis ―big bang‖ decentralization period.

The analysis relies on descriptive statistics, multivariate econometric analysis and qualitative case studies.

The report begins with a description of urbanization and economic development trends across Indonesia.

The descriptive analysis examines the range of city-region agglomerations over time, in terms of urban

and total population change; migration; economic activity; access to basic urban infrastructure services;

and institutional performance. Using the results of both the multivariate analysis and the case studies, we

proceed to assess the performance of cities and urban regions over time in terms of population growth,

urbanization, economic output, income, service access and attempt to link this performance with government

policy actions and the structural characteristics of respective local economies. Our intent is to identify

constraints to regional and urban development that are the result of structural characteristics and/or

government policies, programs and investments. Based on the results of the analysis, we will make policy

recommendations for local and central governments on how major urban areas can be enhanced to

improve their competitiveness and prosperity. The remainder of this chapter outlines the structure of the

report.

Chapter One: Overview and Methodology

Page 2

Chapter 2 (“Urbanization and Metropolitan Growth”) provides an overview of the urbanization process.

The data shows that urbanization is occurring across Indonesia and that, in some instances, Outer Island

regions are urbanizing faster than Java-Bali, where most of the urban population currently resides. In terms

of the rate of incidence of poverty, the data shows that poverty rates are typically higher in rural areas,

particularly remote rural areas, than in cities in most regions of Indonesia. This chapter also explores likely

future trends in urbanization, providing estimates of the population growth in 11 large cities. These

projections show that between 2010 and 2025, the population of these cities is expected to increase by

an average of 309,000 persons per year.

Chapter 3 (“Leveraging Urbanization and Agglomeration”) explores the extent to which Indonesia‘s

cities are leveraging the benefits that might be derived from agglomeration economies. The

agglomerations are functionally-defined urban metropolitan areas, with this definition being used in

recognition of the fact that urbanization in Indonesia extends beyond the seven GOI-defined metropolitan

regions. We employ the Agglomeration Index (AI) framework developed by Uchida and Nelson (2008) to

cluster districts into metropolitan agglomerations, using this framework to identify 44 metropolitan regions

in Indonesia. The AI allows us to define metropolitan agglomerations meaningfully and to analyze spatial,

demographic, and economic trends at the metropolitan scale.

Chapter 4 (“Economic Performance of Metropolitan Regions”) reviews the economic performance of

existing metropolitan regions. Using a gravity model, we compute spatial accessibility to population

centers and to manufacturing locations for selected industries. The gravity indices provide a measure of the

proximity of a district to regional attractions. This chapter shows that while Indonesia as a whole has not

fully leveraged the economic benefits of rapid urbanization, mid-sized cities have performed best in terms

of deriving these benefits.

Chapter 5 (“Infrastructure Investments and Urban Development”) analyzes the relationship between

public capital expenditures and economic productivity. We explore the role of investment in infrastructure

in boosting metropolitan economic growth. There is emerging evidence in Indonesia that increased

infrastructure spending at the local level contributes to economic growth. Recent analysis shows that as

district capital spending rises as a proportion of GRDP, its rate of economic growth also increases.

Chapter 6 (“Spatial Drivers of Metropolitan Development”) examines the spatial drivers of metropolitan

development. Here we examine how well Indonesian metropolitan regions are planned and how planning

is enforced. We also examine the role of inter-governmental coordination to manage urban development

that straddles district or provincial boundaries. The chapter shows the urban planning in Indonesia needs to

be strengthened, particularly in large metropolitan areas. In the conclusion, we identify a range of critical

urban planning challenges and recommendations on how these challenges should be addressed.

Chapter 7 (“Conclusion”) summarizes the report‘s main findings and recommendations for leveraging

urbanization to support metropolitan economic growth and to improve the quality of life of Indonesia‘s

urban and non-urban community members. This chapter draws conclusions on the urbanization trends across

the country and sets out policy recommendations for the central government. It also sets out recommended

policy actions for metropolitan areas and policy initiatives for smaller metropolitan areas.

Technical Annexes explain the main analytic tools used in the report. In particular, it explains the use of

the Agglomeration Index to define metropolitan regions (Annex 1); Gravity Indices to explore the link

between metropolitan areas and surrounding districts (see Annex 2 for a description of the gravity

models); PRODY and EXPY to assess the degree of sophistication of a metropolitan area‘s manufacturing

Chapter One: Overview and Methodology

Page 3

sector(Annex 3); and the Barro-style growth model to explain the relationship between public capital

expenditure, district growth, and urbanization (Annex 5).

Annex 6 provides an assessment of development trends in four major metropolitan areas of Jakarta,

Makassar, Medan and Surabaya. The two largest metro areas (Jakarta Metro Area and Surabaya Metro

Area) are developing polycentric spatial structures with multiple nodes surrounding the traditional city

center. Overall, the trends for four metropolitan areas indicate that spatial economic transformation is

underway in all of them, with suburbanization and economic transformation pushing development outward.

QUANTITATIVE DATA

Quantitative data used in this analysis were drawn largely from surveys conducted and compiled by

Statistics Indonesia (Badan Pusat Statistik/BPS).In general, we draw on surveys which provide

representative samples for each district and which are conducted annually. In some cases, however,

databases are available every few years. The National Socio-Economic Survey (SUSENAS) is conducted

annually by BPS. Since 1993, it has been a nationally-representative sample. For our study, Susenas

provides population and demographic data, including data related to the incidence of poverty. The

Village Potential Statistics (PODES) are drawn from a census conducted approximately every three years,

with these sensors measuring village demographics; access to infrastructure; and economic status and

performance. Where necessary, we trend-extrapolate data for intercensal years. Industrial Statistics

(Statistik Industri, a census of large and medium-scale manufacturing operations) provides annual

establishment-level data on all manufacturing establishments with more than twenty registered employees.

The Regional Finance Information System (SIKD) provides data related to public investment in infrastructure

development. We also use the United Nations‘ national accounts for international comparisons and draw

on multiple reports for secondary data. These sources are cited appropriately throughout the report.

We also use data on Gross Regional Domestic Product (GRDP). There are a number of issues with the

GRDP data. District-level GRDP data are estimated from provincial totals, which are produced by BPS

offices at the national, provincial, and district levels. Although all offices are required to follow common

procedures to produce the estimations of GRDP, this dispersion of responsibility does raise some questions

regarding the reliability of the outputs. Between 1993 and 2005, for instance, sub-totals produced by

summing district GRDPs within a province did not match provincial totals, with variations ranging from

between 91 and 105 percent of the published provincial totals (McCulloch and Sjahrir 2008).Values in

2006 and 2007 also fit into this range. Despite these issues, the GRDP district-level data is still used in the

analysis, since it is necessary to include indicators of economic activity at this level in order to study

agglomeration economies. In addition to using BPS-prepared statistics, we compute several spatial

indicators using BPS GIS data and the datasets described immediately above.

QUALITATIVE DATA

To analyze institutional patterns and constraints, we employ an extensive qualitative research framework

relying on a series of qualitative surveys of national and local laws, regulations and practices. We also

conduct detailed case studies in the Jakarta, Medan, Surabaya and Makassar metropolitan regions. The

surveys and case studies focus on local, national and provincial urban planning and administrative laws,

policies, and practices to better understand how current legislation and institutional practices affect trans-

district urbanization. We examine these issues through a review of applicable laws, decrees and policies

pertaining to spatial planning, inter-governmental coordination, business climate, infrastructure planning

and finance, and access to private financial capital. Combined with extensive literature reviews, we use

these surveys and case studies to identify constraints to agglomeration across the country and to frame

Chapter One: Overview and Methodology

Page 4

recommendations on how to address these constraints and to leverage opportunities to boost

agglomeration.

Page 5

CHAPTER 2

URBANIZATION AND METROPOLITAN GROWTH

This chapter reviews past and future trends related to Indonesia‘s urbanization and the development of its metropolitan regions. First, we examine historical urbanization trends on the basis of United Nations tabulations of urban, rural and total populations from 1971 to 2010. Next, we explore population and urbanization trends in each of the country‘s seven major metropolitan regions. Finally, we develop an Agglomeration Index (AI) for Indonesia in order to define functionally-based metropolitan regions.

Indonesia, like other rapidly developing economies, is going through a process of significant urbanization. While Indonesia‘s geographical situation as a complex archipelago of more than 17,000 islands create special challenges, other developing countries have also had to attempt to grapple with spatially uneven development. As the World Development Report of 2009 states:

“No country has grown to middle income without industrializing and urbanizing. None has grown to high income without

vibrant cities.”

Spatially concentrated urbanization and economic development go hand-in-hand. High levels of population density and low-cost access to factor inputs have facilitated the transformation of economies from agrarian to industrial and to service activities. Regions that can manage rural to urban transition successfully are able to rapidly expand their economies and to experience increased average incomes and improved living standards.

According to a 2005 survey of developing countries, almost 75 percent of the responding nations expressed a strong desire to implement policies to reduce migration to urban areas or to reverse migration flows from urban to rural areas (United Nations, 2007). While cities face challenges of congestion, pollution and higher costs, the creation of agglomeration economies and rising incomes means that the benefits of size outweigh the perceived costs. Through investments in infrastructure, better urban planning and more efficient spatial structure, cities can mitigate the effects of these adverse conditions and become more competitive. In East Asia, there are numerous examples of such positive reversals, including the cases of Bangkok, Beijing, Seoul and Tokyo. The success of these cities implies that making cities more productive and efficient is more feasible than attempting to stop or redirect urban growth.

The stopping or limitation of urbanization is commonly proposed or discussed in many developing countries (Renaud, 1981). Such proposals and ideas are driven primarily by the rapid rates of urbanization in low and middle-income developing countries; the proliferation of ―mega-cities‖ with populations over 10 million; widespread urban pollution and congestion; limited urban services; and the perception that cities are economically and socially dysfunctional and draw resources away from rural areas. These concerns frequently prompt policy-makers to call for policies to limit the growth of large cities; stem migration flows to cities; and to seek options for building new towns, growth poles and new special economic zones.

REGIONAL DEVELOPMENT POLICY: PEOPLE VS. PLACE PROSPERITY

Designing and implementing effective forms of regional development is a complex process. In many cases, policy-makers are not fully aware of the drivers that shape urban and regional development. Consequently, these policymakers frame policy initiatives that are ineffective or counterproductive. As many management and policy experts have commented: If you cannot explain, understand or measure performance, you cannot possibly hope to shape it in ways that achieve desired outcomes.

The Government of Indonesia has stressed the importance of spatial equity among the seven Island regions, as mentioned in the Master Plan for Expansion and Acceleration of Indonesia‘s Economic

Chapter Two: Urban and Metropolitan Growth

Page 6

Development (MP3EI). In turn, this has sparked great interest among central and sub-national government decision-makers to consider how to promote development of strategic locations to ―reduce the dominance of Island of Java and increase growth of the rest of Indonesia.‖ One option discussed is moving the capital city out of Jakarta, although the experience from other countries (Brazil, Nigeria, and Pakistan, to name a few, Baskoro, 2010) show that moving the capital had very little, if any, impact on urban development in the former capital cities.

One useful way to characterize regional development policy is to think of it in terms of the promotion of people prosperity versus place prosperity. The question implied by this distinction is: Should governments spend scarce resources to attempt to build up lagging regions (a focus on place)? Or should they consider policy instruments to enhance ―people prosperity‖ through education and human capital development or through the promotion of labor mobility and migration? An underlying theme that cuts across these questions and debates is the notion that the Indonesian Government should foster place prosperity over people prosperity. The dilemma implied by the distinction between people versus place prosperity is not unique to Indonesia, nor is it new. It is a longstanding question that regional development planners and economists have debated for years. Governments have launched hundreds of initiatives to promote either people prosperity or place prosperity, without resolving or settling the distinction.

In terms of promoting both people and place prosperity, the Indonesian Government has launched the ―Master Plan for Acceleration and Expansion of Indonesia‘s Economic Development‖ (MP3EI). The MP3EI Plan combines both sector and regional development approaches, which in turn are integrated with the development of Economic Corridors. The objective of this initiative is to boost economic development by clustering and sharpening economic activities in certain regions. It provides strategic direction for investors, guiding these investors to targeted investment locations where the Government will concentrate on providing major support and guidance. The main strategy of the economic transformation is to develop centers of growth in each region through the promotion of Economic Corridors, strengthening connectivity and integration between regions to lower logistics cost and building synergy between centers of growth in different regions. The development of Economic Corridors is based on the spatial conditions of each of Indonesia‘s major islands, with each Economic Corridor leveraging its specific advantages (see Table 2.1 below).

The master plan will spur growth in some development corridors, such as the east coast of Sumatra; the northern regions of Java, Bali and Nusa Tenggara; the west and east coasts of Kalimantan; and the west coast of Sulawesi. Economic centers, such as Special Economic Zones (SEZ) and Free Trade Zones (FTZ), will be developed alongside the corridor to support investment and to boost the economic attractiveness of the region. They will also facilitate the subsequent development of massive infrastructure projects to support the economic activities of these corridors. The flow of resources, goods and services will foster urbanization in areas adjacent to each corridor. Moreover, the proposed programs for the development of transportation infrastructure, such as the trans-Java expressway, the trans-Java railway, and the trans-Sumatra highway, will connect regions and integrate economic activities throughout Indonesia.

Chapter Two: Urban and Metropolitan Growth

Page 7

TABLE 2.1: ECONOMIC CORRIDORS IN THE MASTER PLAN FOR ACCELERATION AND EXPANSION OF INDONESIA’S ECONOMIC DEVELOPMENT (MP3EI)

Economic Corridor Master Plan‘s Direction Highlights

Sumatra Plantations production, processing center and national energy reserve

Located along global major sea lines of Malacca Strait, also proximity with growth center in Java, Singapore and Malaysia

Abundant natural resources, such as oil and gas

Java National industry and services booster High quality of human resources

Most developed region to date

Kalimantan Mining production, processing center and national energy reserve

Located along Indonesian major sea lines of Makassar Strait and South China Sea

Abundant natural resources such as oil and gas

Sulawesi-North Maluku Plantation, agriculture, fisheries production and processing center

Located along Indonesian major sea lines of Makassar Strait and Pacific Ocean

Most developed region in East Indonesia

Bali-Nusa Tenggara National tourism gate and national food support

Benefited from location next to Java

Long-time popular tourism destination

Maluku-Papua Natural resources processing and human resource

Abundant natural resources

Low population density

SOURCE: MASTER PLAN FOR ACCELERATION AND EXPANSION OF INDONESIA’S ECONOMIC DEVELOPMENT, 2011

Indonesia can promote sustainable growth across regions by supporting the comparative advantage of each region, which is also supported by MP3EI. In Java and Bali, growth has been driven mostly by the manufacturing and services sectors. High economic growth is concentrated in densely populated regions such as Java and Bali, where the sub-national growth of these regions are generating almost two-thirds of the total growth in national output. As a result of these economic disparities, imbalances in rates of regional growth remain a challenge. In particular, the growth rates in output per capita in Java, Bali and Kalimantan are considerably higher than the national average. Even adjusted for population, the regional growth of Java and Bali stands out as the largest contributor to national output. Thus, there are still some challenges for Indonesia to achieve higher growth overall. Specifically, Indonesia needs to move up the value chain and gradually shift from exporting raw materials to processed products.

In rich natural commodity producing islands such as Sumatra and Kalimantan, growth has been driven by the export of commodities of raw natural resources, such as oil and natural gas. However, the exploitation of natural resources in these rich regions has not been managed well. In general, natural commodity sectors have expanded because of increases in global market prices. This expansion therefore remains highly dependent on volatile global market conditions and will not lead to sustained growth. While the rate of growth in the services sector remains high and is continuing to increase, there has been a decline in the growth of the manufacturing sector since the crisis.

The World Bank‘s trade development report (2010b) suggests that commodity growth has not kept pace with inflation. Four fifths of the growth in the total value of commodity exports from 2005 to 2007 resulted from an increase in prices on global markets rather than from an increase in the volume of production. Most of the revenues derived from the commodities sector were utilized to support subsidies, including fuel subsidies, rather than on productive investments. This is in contrast to the situation in the 1970s, when the

Chapter Two: Urban and Metropolitan Growth

Page 8

Indonesian Government used the commodity windfall to improve infrastructure and to revamp its agricultural sector.

As Indonesia‘s decentralization and regional autonomy reforms of 2001 assumes that a large part of growth policy will be made at the district (kabupaten/kota) level, it is crucial to ensure that sub-national policy-making supports the promotion of dynamic sectors in the regions. Besides the promotion of economic corridors, government policies also focus on economic integration to encourage inclusive growth. To improve spatial equity, the Government has attempted to develop a limited number of dispersed centers of economic activity across the country. However, international experience suggests that growth poles should be carefully located based on rigorous economic analysis, as the record of such initiatives is mixed, with a significant proportion of both successes and failures.

Many countries have tried some very aggressive measures to foster more inclusive and spatially balanced growth. The range of policy tools is wide, including: attempts to control internal migration (China and the former Soviet Union); the formation of growth poles (Brazil, Venezuela, France and Canada); offering financial incentives for firms to locate in lagging regions (the Tennessee Valley Authority, Canada‘s Department of Regional Economic Expansion); the creation of economic zones (Malaysia, India, Thailand,

BOX 2.1: “GO WEST”: CHINA’S EFFORTS TO DEVELOP ITS LAGGING WESTERN REGION

The large western region of China has historically lagged behind the coastal East, despite its mineral and energy resources. This has largely been the result of its harsh climate and difficult terrain. The Western region is very large, covering more than 70 percent of China‘s total land area and consisting of 13 provinces. However, it is sparsely populated, With less than 30 percent of China‘s population. The GDP per capita in Western China is less than half of that in the East. Although the West has a larger absolute number of towns and cities, due to its large size, the density of urban centers across the region is far lower. The private sector is also less dynamic than in the East, which has around 3.5 times the number of private enterprises per town than the West and North-East.

In 1999, the Chinese government announced its China Western Development or ―Go West‖ policy, targeting the Western region for development with the intention of reducing economic disparity between the coast and the interior; promoting national unity; and utilizing natural resources more efficiently. The Government‘s emphasis was on encouraging private investment in the West, using only limited public funds. The long-term strategy was to target existing metropolitan centers with established economic bases, which were intended to act as engines of growth, providing employment that would attract rural migrants.

The key policies outlined by the Government to promote regional growth included:

Infrastructure development: Transport, including national and provincial highways, rail systems, and airports;

communications; energy; irrigation; and urban infrastructure

Environmental protection: Controlling floods, draughts, and sandstorms

Sectoral and economic adjustment: Promoting sectors that take advantage of the West‘s comparative advantage,

e.g., minerals and tourism, and encouraging high-tech industries to locate in the West

Human capital and R&D: Improving funding and support for research facilities, technical training, and college

education, and using incentives such as higher compensation to attract talent to the West

Foreign Direct Investment and trade: Preferential treatment and incentives to encourage FDI and private investment

to the West, and opening up more areas for FDI investment; and

Targeted poverty alleviation.

The policy has had mixed results so far. Economic and population growth has increased in the West since the policy was implemented, but growth rates in the East continue to exceed the West, resulting in a larger gap between the two regions.

As Indonesia attempts to develop its own lagging region in the East, it can draw lessons from China‘s ―Go West‖ experience. As

in Western China, established urban agglomerations in Eastern Indonesia present an opportunity to boost regional development,

acting as strategic points of entry that can lead to economic growth in surrounding areas.

Chapter Two: Urban and Metropolitan Growth

Page 9

and Vietnam); or the establishment of new towns (the UK, the United States and India).

URBANIZATION PATTERN AND TRAJECTORY

Urban population data in this section are based on traditional estimates of urbanization trends using Government‘s definitions and administrative boundaries. In the case of Indonesia, BPS defines urban areas as follows: 1) in areas that have a population density of 5,000 persons per square kilometer; 2) areas in which 25 percent or less of the households work in the agricultural sector; and 3) areas in which there are eight or more specific kinds of urban facilities, including primary schools or equivalent; junior high schools or equivalent; senior high schools or equivalent; cinemas; hospitals, maternity hospitals/mother-child hospitals; primary health care centers; roads that can accommodate three and four wheeled motorized vehicles; telephones; post offices; markets with buildings; shopping centers; banks; factories; restaurants; public electricity; and part equipment rental services.

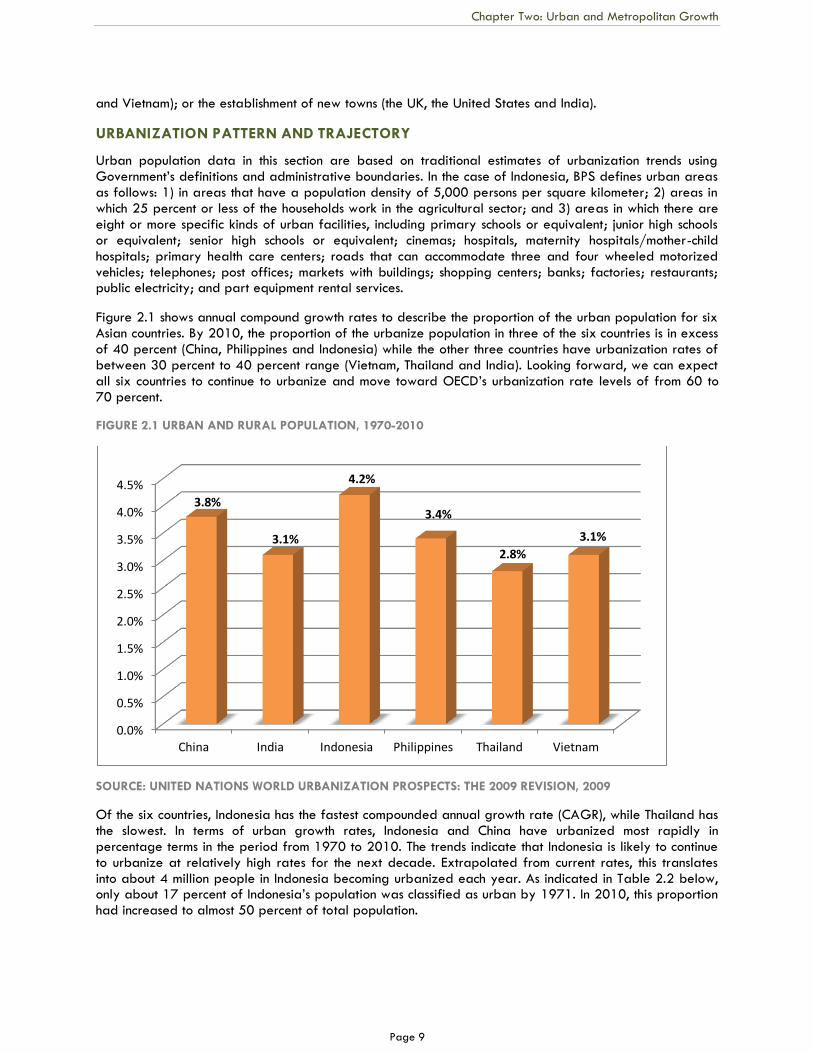

Figure 2.1 shows annual compound growth rates to describe the proportion of the urban population for six Asian countries. By 2010, the proportion of the urbanize population in three of the six countries is in excess of 40 percent (China, Philippines and Indonesia) while the other three countries have urbanization rates of between 30 percent to 40 percent range (Vietnam, Thailand and India). Looking forward, we can expect all six countries to continue to urbanize and move toward OECD‘s urbanization rate levels of from 60 to 70 percent.

FIGURE 2.1 URBAN AND RURAL POPULATION, 1970-2010

SOURCE: UNITED NATIONS WORLD URBANIZATION PROSPECTS: THE 2009 REVISION, 2009

Of the six countries, Indonesia has the fastest compounded annual growth rate (CAGR), while Thailand has the slowest. In terms of urban growth rates, Indonesia and China have urbanized most rapidly in percentage terms in the period from 1970 to 2010. The trends indicate that Indonesia is likely to continue to urbanize at relatively high rates for the next decade. Extrapolated from current rates, this translates into about 4 million people in Indonesia becoming urbanized each year. As indicated in Table 2.2 below, only about 17 percent of Indonesia‘s population was classified as urban by 1971. In 2010, this proportion had increased to almost 50 percent of total population.

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

China India Indonesia Philippines Thailand Vietnam

3.8%

3.1%

4.2%

3.4%

2.8%

3.1%

Chapter Two: Urban and Metropolitan Growth

Page 10

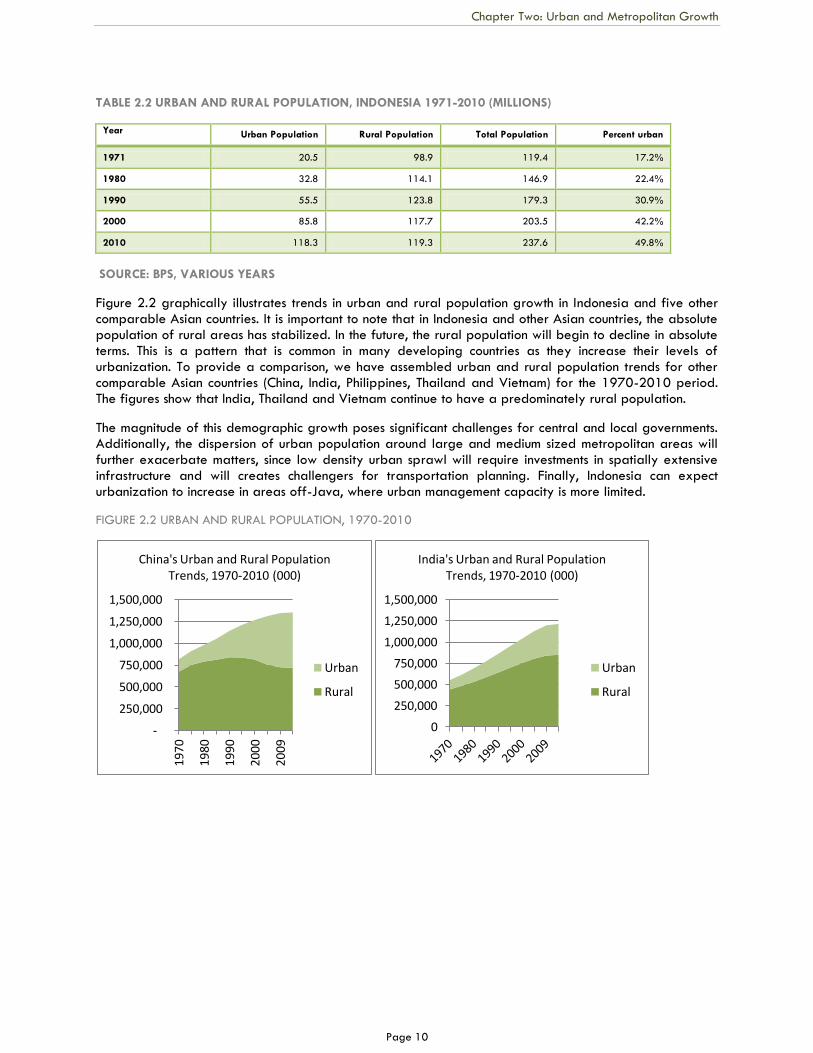

TABLE 2.2 URBAN AND RURAL POPULATION, INDONESIA 1971-2010 (MILLIONS)

Year Urban Population Rural Population Total Population Percent urban

1971 20.5 98.9 119.4 17.2%

1980 32.8 114.1 146.9 22.4%

1990 55.5 123.8 179.3 30.9%

2000 85.8 117.7 203.5 42.2%

2010 118.3 119.3 237.6 49.8%

SOURCE: BPS, VARIOUS YEARS

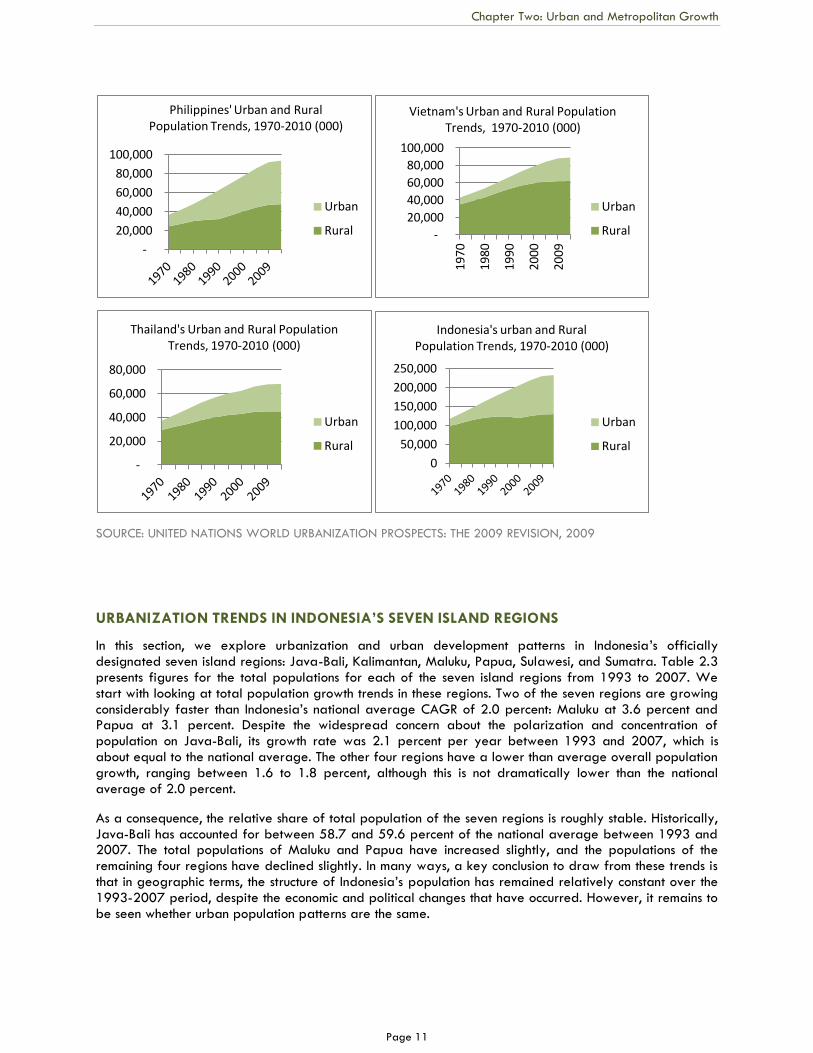

Figure 2.2 graphically illustrates trends in urban and rural population growth in Indonesia and five other comparable Asian countries. It is important to note that in Indonesia and other Asian countries, the absolute population of rural areas has stabilized. In the future, the rural population will begin to decline in absolute terms. This is a pattern that is common in many developing countries as they increase their levels of urbanization. To provide a comparison, we have assembled urban and rural population trends for other comparable Asian countries (China, India, Philippines, Thailand and Vietnam) for the 1970-2010 period. The figures show that India, Thailand and Vietnam continue to have a predominately rural population.

The magnitude of this demographic growth poses significant challenges for central and local governments. Additionally, the dispersion of urban population around large and medium sized metropolitan areas will further exacerbate matters, since low density urban sprawl will require investments in spatially extensive infrastructure and will creates challengers for transportation planning. Finally, Indonesia can expect urbanization to increase in areas off-Java, where urban management capacity is more limited.

FIGURE 2.2 URBAN AND RURAL POPULATION, 1970-2010

-

250,000

500,000

750,000

1,000,000

1,250,000

1,500,000

1970

1980

1990

2000

2009

China's Urban and Rural Population Trends, 1970-2010 (000)

Urban

Rural

0

250,000

500,000

750,000

1,000,000

1,250,000

1,500,000

India's Urban and Rural Population Trends, 1970-2010 (000)

Urban

Rural

Chapter Two: Urban and Metropolitan Growth

Page 11

SOURCE: UNITED NATIONS WORLD URBANIZATION PROSPECTS: THE 2009 REVISION, 2009

URBANIZATION TRENDS IN INDONESIA’S SEVEN ISLAND REGIONS

In this section, we explore urbanization and urban development patterns in Indonesia‘s officially designated seven island regions: Java-Bali, Kalimantan, Maluku, Papua, Sulawesi, and Sumatra. Table 2.3 presents figures for the total populations for each of the seven island regions from 1993 to 2007. We start with looking at total population growth trends in these regions. Two of the seven regions are growing considerably faster than Indonesia‘s national average CAGR of 2.0 percent: Maluku at 3.6 percent and Papua at 3.1 percent. Despite the widespread concern about the polarization and concentration of population on Java-Bali, its growth rate was 2.1 percent per year between 1993 and 2007, which is about equal to the national average. The other four regions have a lower than average overall population growth, ranging between 1.6 to 1.8 percent, although this is not dramatically lower than the national average of 2.0 percent.

As a consequence, the relative share of total population of the seven regions is roughly stable. Historically, Java-Bali has accounted for between 58.7 and 59.6 percent of the national average between 1993 and 2007. The total populations of Maluku and Papua have increased slightly, and the populations of the remaining four regions have declined slightly. In many ways, a key conclusion to draw from these trends is that in geographic terms, the structure of Indonesia‘s population has remained relatively constant over the 1993-2007 period, despite the economic and political changes that have occurred. However, it remains to be seen whether urban population patterns are the same.

-

20,000

40,000

60,000

80,000

100,000

Philippines' Urban and Rural Population Trends, 1970-2010 (000)

Urban

Rural -

20,000

40,000

60,000

80,000

100,000

1970

1980

1990

2000

2009

Vietnam's Urban and Rural Population Trends, 1970-2010 (000)

Urban

Rural

-

20,000

40,000

60,000

80,000

Thailand's Urban and Rural Population Trends, 1970-2010 (000)

Urban

Rural

0

50,000

100,000

150,000

200,000

250,000

Indonesia's urban and Rural Population Trends, 1970-2010 (000)

Urban

Rural

Chapter Two: Urban and Metropolitan Growth

Page 12

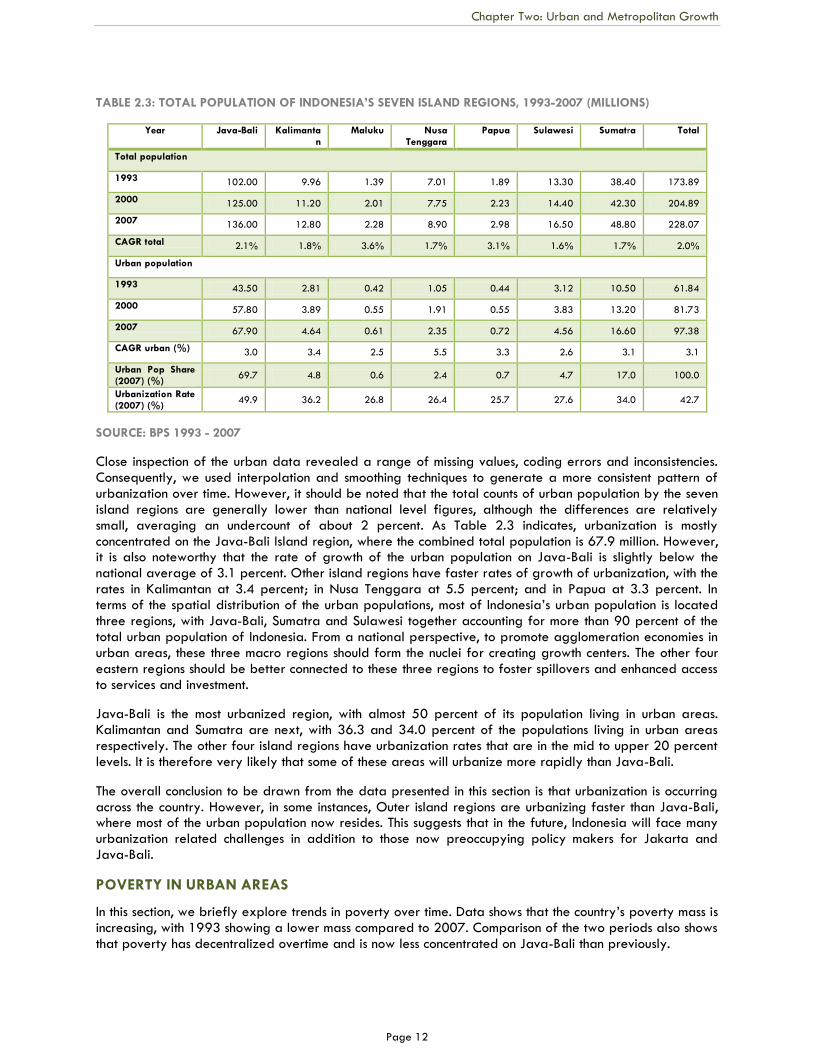

TABLE 2.3: TOTAL POPULATION OF INDONESIA’S SEVEN ISLAND REGIONS, 1993-2007 (MILLIONS)

Year Java-Bali Kalimantan

Maluku Nusa Tenggara

Papua Sulawesi Sumatra Total

Total population

1993 102.00 9.96 1.39 7.01 1.89 13.30 38.40 173.89

2000 125.00 11.20 2.01 7.75 2.23 14.40 42.30 204.89

2007 136.00 12.80 2.28 8.90 2.98 16.50 48.80 228.07

CAGR total 2.1% 1.8% 3.6% 1.7% 3.1% 1.6% 1.7% 2.0%

Urban population

1993 43.50 2.81 0.42 1.05 0.44 3.12 10.50 61.84

2000 57.80 3.89 0.55 1.91 0.55 3.83 13.20 81.73

2007 67.90 4.64 0.61 2.35 0.72 4.56 16.60 97.38

CAGR urban (%) 3.0 3.4 2.5 5.5 3.3 2.6 3.1 3.1

Urban Pop Share (2007) (%)

69.7 4.8 0.6 2.4 0.7 4.7 17.0 100.0

Urbanization Rate (2007) (%)

49.9 36.2 26.8 26.4 25.7 27.6 34.0 42.7

SOURCE: BPS 1993 - 2007

Close inspection of the urban data revealed a range of missing values, coding errors and inconsistencies. Consequently, we used interpolation and smoothing techniques to generate a more consistent pattern of urbanization over time. However, it should be noted that the total counts of urban population by the seven island regions are generally lower than national level figures, although the differences are relatively small, averaging an undercount of about 2 percent. As Table 2.3 indicates, urbanization is mostly concentrated on the Java-Bali Island region, where the combined total population is 67.9 million. However, it is also noteworthy that the rate of growth of the urban population on Java-Bali is slightly below the national average of 3.1 percent. Other island regions have faster rates of growth of urbanization, with the rates in Kalimantan at 3.4 percent; in Nusa Tenggara at 5.5 percent; and in Papua at 3.3 percent. In terms of the spatial distribution of the urban populations, most of Indonesia‘s urban population is located three regions, with Java-Bali, Sumatra and Sulawesi together accounting for more than 90 percent of the total urban population of Indonesia. From a national perspective, to promote agglomeration economies in urban areas, these three macro regions should form the nuclei for creating growth centers. The other four eastern regions should be better connected to these three regions to foster spillovers and enhanced access to services and investment.

Java-Bali is the most urbanized region, with almost 50 percent of its population living in urban areas. Kalimantan and Sumatra are next, with 36.3 and 34.0 percent of the populations living in urban areas respectively. The other four island regions have urbanization rates that are in the mid to upper 20 percent levels. It is therefore very likely that some of these areas will urbanize more rapidly than Java-Bali.

The overall conclusion to be drawn from the data presented in this section is that urbanization is occurring across the country. However, in some instances, Outer island regions are urbanizing faster than Java-Bali, where most of the urban population now resides. This suggests that in the future, Indonesia will face many urbanization related challenges in addition to those now preoccupying policy makers for Jakarta and Java-Bali.

POVERTY IN URBAN AREAS

In this section, we briefly explore trends in poverty over time. Data shows that the country‘s poverty mass is increasing, with 1993 showing a lower mass compared to 2007. Comparison of the two periods also shows that poverty has decentralized overtime and is now less concentrated on Java-Bali than previously.

Chapter Two: Urban and Metropolitan Growth

Page 13

While the total number of Indonesians living in poverty increased from 26.0 million persons in 1993 to 37.3 million persons in 2007, the proportion of those living in poverty declined from 17.8 percent of the population in 1993 to 16.6 percent of the population in 2007 (these counts and percentages are tentative, as many districts did not report poverty data in 1993; the 1993 percentage is adjusted for un-reporting). Poverty rates are generally lower in urban areas for both 1993 and 2007.

Figure 2.3 illustrates the patterns of poverty rates and the proportion of the population classified as poor in urban and suburban hinterland areas. As it shows, poverty rates are typically higher in the hinterlands than in cities for most regions of Indonesia.

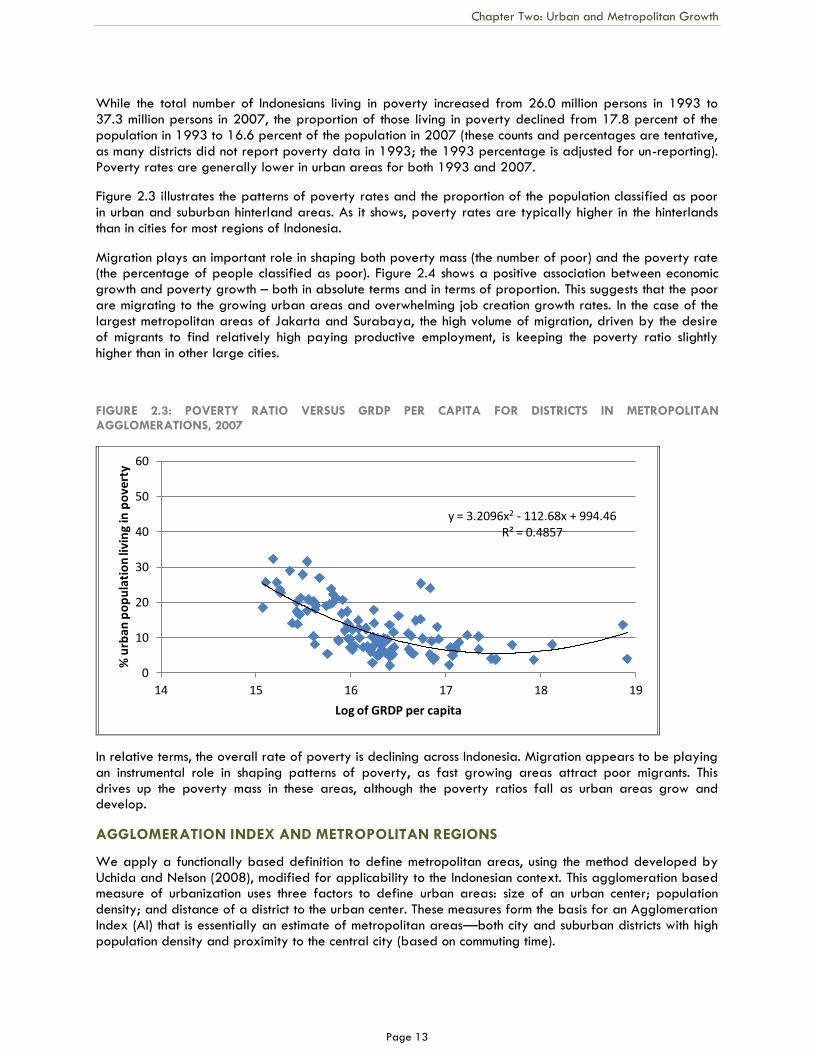

Migration plays an important role in shaping both poverty mass (the number of poor) and the poverty rate (the percentage of people classified as poor). Figure 2.4 shows a positive association between economic growth and poverty growth – both in absolute terms and in terms of proportion. This suggests that the poor are migrating to the growing urban areas and overwhelming job creation growth rates. In the case of the largest metropolitan areas of Jakarta and Surabaya, the high volume of migration, driven by the desire of migrants to find relatively high paying productive employment, is keeping the poverty ratio slightly higher than in other large cities.

FIGURE 2.3: POVERTY RATIO VERSUS GRDP PER CAPITA FOR DISTRICTS IN METROPOLITAN AGGLOMERATIONS, 2007

In relative terms, the overall rate of poverty is declining across Indonesia. Migration appears to be playing an instrumental role in shaping patterns of poverty, as fast growing areas attract poor migrants. This drives up the poverty mass in these areas, although the poverty ratios fall as urban areas grow and develop.

AGGLOMERATION INDEX AND METROPOLITAN REGIONS

We apply a functionally based definition to define metropolitan areas, using the method developed by Uchida and Nelson (2008), modified for applicability to the Indonesian context. This agglomeration based measure of urbanization uses three factors to define urban areas: size of an urban center; population density; and distance of a district to the urban center. These measures form the basis for an Agglomeration Index (AI) that is essentially an estimate of metropolitan areas—both city and suburban districts with high population density and proximity to the central city (based on commuting time).

y = 3.2096x2 - 112.68x + 994.46 R² = 0.4857

0

10

20

30

40

50

60

14 15 16 17 18 19

% u

rba

n p

op

ula

tio

n li

vin

g in

po

vert

y