Working Capital Management Presented by: In a Basel III World Jennifer S. Komar James L. Graves September 21, 2015 Date:

Working Capital Management Presented by: In a Basel III World Jennifer S. Komar James L. Graves September 21, 2015 Date:

Dec 30, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Working Capital Management

Presented by:

In a Basel III World

Jennifer S. Komar

James L. Graves

September 21, 2015

Date:

Today’s presenters

Jennifer S. Komar, NCPProduct ManagerKeyBank Enterprise Commercial Payments

James L. GravesSVP, Liquidity StrategistKeyBank Enterprise Commercial Payments

KeyCorp Public 2

G

Agenda

I. What is Basel?

o The Basel Committee on Banking Supervision (BCBS)

• Basel I

• Basel II

II. What is Basel III?

o Key Aspects of the regulation

o Who are the players?

o What is LCR and how is it calculated?

o Value of Deposits to Financial Institutions

o Operating Deposit Definition

III. What does it mean to me?

o From the Corporate perspective

o From the Bank perspective

IV. Wrap up

KeyCorp Public 3

G

KeyCorp Public 4

What is Basel?

K

KeyCorp Public 5

Are we talking about … ?

The name of the English actor, best known for playing Sherlock Holmes?

(Basil Rathbone, born 1892)

K

KeyCorp Public 6

Are we talking about … ?

A versatile herb used to make pesto sauce?

K

KeyCorp Public 7

Are we talking about … ?

Birthplace of the former #1 ranked tennis player in the world, Roger Federer?

Well, sort of …

K

KeyCorp Public 8

Are we talking about … ?

A set of international banking regulations put forth by the Basel Committee on Bank Supervision?

K

KeyCorp Public

Basel and the Committee on Banking

The Basel Committee on Banking Supervision (BCBS) is a committee of banking supervisory authorities that was established by the central bank governors of the Group of Ten countries in 1974. It provides a forum for regular cooperation on banking supervisory matters.

The Basel accords are a series of recommendations on banking laws and regulations issued by the Basel Committee on Banking Supervision (BSBS).

The name for the accords is derived from Basel, Switzerland, where the committee that maintains the accords meets.

Its objective is to enhance understanding of key supervisory issues and improve the quality of banking supervision worldwide.

9

G

KeyCorp Public

Basel I

Basel I was a document written in 1988 by the Basel Committee on Banking Supervision, which recommends certain standards and regulations for banks. The main recommendation of this document is that in order to lower credit risk, banks should hold enough capital to equal at least 8% if its risk-weighted assets. Most countries have implemented some version of this regulation.

*Group of Ten (have become 11) are: Belgium, Canada, France, Germany, Italy, Japan, the Netherlands, Sweden, Switzerland, the United Kingdom

and the United States.

10

G

KeyCorp Public

Basel II

Basel II, written in 2004, recommended that banks should maintain enough cash reserves to cover risks incurred by investment and lending practices. It improved on Basel I by offering more complex models for calculating regulatory capital, including credit risk, operational risk and market risk.

Implementation of Basel II by United States regulators was in 2008, so it was not in place prior to the Global Financial Crisis of 2007-08. Unlike European regulators, those in the U.S. made Basel II optional for non “core” banks (i.e. assets >$250b).

The full title of the accord is Basel II: The International Convergence of

Capital Measurement and

Capital Standards – A Revised Framework

11

G

KeyCorp Public

So …

Unlike the first accord, where focus was mainly on credit risk, the purpose of Basel II was to create standards and regulations on how much capital financial institutions must have put aside.

12

G

KeyCorp Public

Enter Basel III

13

K

KeyCorp Public

Why B3?

Unlike Basel I and Basel II, which are primarily related to the required level of bank loss reserves that must be held by banks for various classes of loans and other investments and assets that they have, Basel III is primarily related to the risks for the banks of a run on the bank by requiring differing levels of reserves for different forms of bank deposits and other borrowings.

Therefore contrary to what might be expected by the name, Basel III rules do not for the most part supersede the guidelines known as Basel I and Basel II but work alongside them.

14

K

KeyCorp Public

Why B3?

15

G

KeyCorp Public

Key aspects of Basel III

The overall goal of Basel III is to address and to improve the banking sector’s ability to absorb shocks arising from financial and economic stress.

New regulation going into effect 2015-2017, phased implementation Addresses financial stability over a 30 day stress period

A stricter definition of capital to increase the quality, consistency and transparency of the capital base

U.S. regulation does not apply to all banks

A new global liquidity standard : LCR (Liquidity Coverage Ratio)

Specific types of liquid assets - cash and securities

Specific amounts of liquid assets based on type of deposits and credit

commitments

Requirements differ based on size of institution

16

G

The regulatory playing field

KeyCorp Public 17

U.S. financial institutions are classified into three groups, based on asset size. $250b+ Standard treatment $50b - $250b Modified treatment < $50b LCR does not apply

K

High Quality Liquid Assets (HQLA)

KeyCorp Public 18

Three levels defined• Level 1 – highest quality, easily and immediately convertible

to cash with no loss of value, all with zero risk weight• Reserve bank balances, foreign reserves, U.S. government

securities, sovereign and multilateral organization securities• Level 2a – U.S. government sponsored enterprises, 20% risk

weight• Federal Home Loan Mortgage Corp, Federal National

Mortgage Association, Farm Credit System, Federal Home Loan Bank

• Level 2b – publicly traded corporate debt and common stock

What’s excluded• Assets issued by financial sector entities• Bonds and securities issued by public sector entities – state,

local, other subdivisions below level of sovereign

Must be unencumbered,

and not held as a client pooled

security.

G

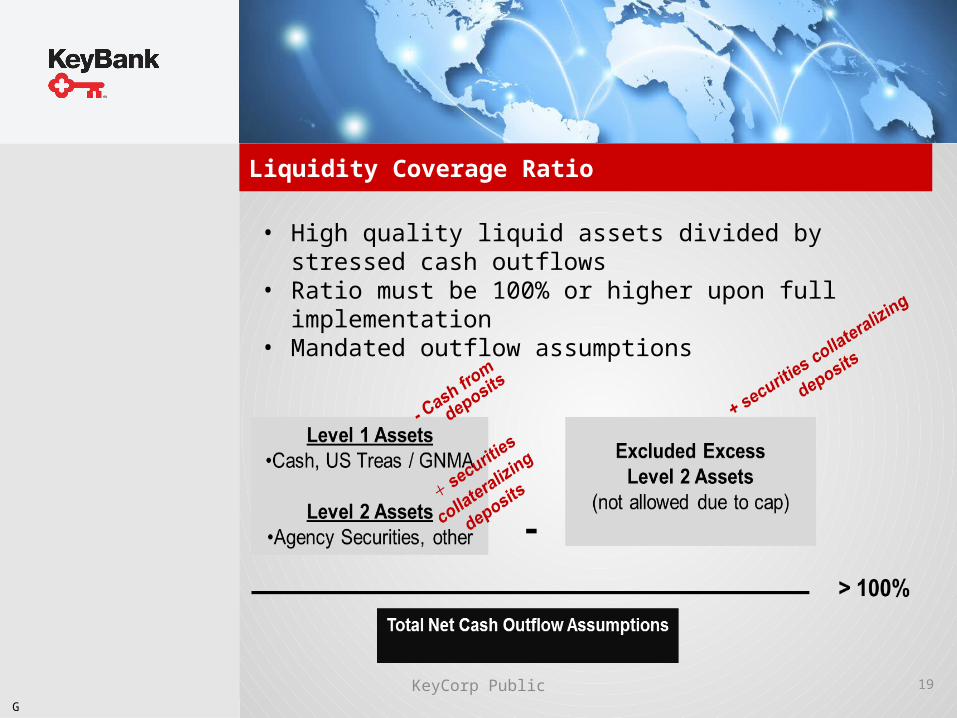

Liquidity Coverage Ratio

KeyCorp Public 19

• High quality liquid assets divided by stressed cash outflows• Ratio must be 100% or higher upon full implementation• Mandated outflow assumptions

G

KeyCorp Public

Outflow Assumptions - Deposits

20

In calculating LCR, the regulation requires that covered banks assume certain outflows from deposit accounts (funds will be withdrawn at these rates) based on the classifications shown below.

Outflow assumptions are different for the two classes of banks that are subject to this regulation (explained on the following slide).

Mandated Outflow Assumptions Balance Classification Full LCR

BankModified LCR

BankStable Retail Deposits 3% 2.1%Other Retail Deposits 10% 7%Operational Commercial Deposits 25% 17.5%Non Operational Commercial Deposits 40% 28%Financial Entities and Correspondent Banks 100% 70%Secured Deposits 100+% 100+%

K

KeyCorp Public

Draw Assumptions - Credit

21

Outflow assumptions also include credit. Unused commitments have draw assumptions based on the commitment categories shown below.

Outflow assumptions are different for the two classes of banks that are subject to this regulation.

Full LCR Modified

LCRBank Bank

Retail Facilities 5.0% 3.5%Commercial Credit 10.0% 7.0%Commercial Liquidity 30.0% 21.0%Financial Entity Credit 40.0% 28.0%Bank Credit & Liquidity 50.0% 35.0%Financial Entity Liquidity 100.0% 70.0%

Mandated Draw Assumptions

Commitment Category

K

KeyCorp Public

Revised View of Deposits

22

G

KeyCorp Public

Operating Deposit Definition

“…a deposit that is necessary to provide operational services as an independent third-party intermediary, agent, or administrator…”

Requires: Operational services provided pursuant to a written

agreement Subject to a 30 calendar day termination notice No economic incentive to attract excess deposits

“Corporate treasurers have

historically valued banks for the

liquidity banks can provide.

Soon, banks will value corporate

treasuries for the KIND of liquidity corporates can

provide…”

Treasury Strategies Inc.Basel III Spring Update, 2015

23

G

KeyCorp Public

What does it mean to me?

24

K

KeyCorp Public

The “Cost” of Regulation

Profitability

Some relationships are more profitable and valuable than others.

Pricing/Rate Actions Most banks that are repricing are doing so at the client level. Some are keeping much narrower bands in their pricing.

• Limiting repricing duration, guaranteeing rates for only one year.

Provides better visibility to the overall value of the relationship, not just a decision

based on deposits.

• Economic incentive

• Section l.4(b)(5) of the proposed rule would have required that “an operational

deposit account not be designed to incent customers to maintain excess funds

therein through increased revenue, reduction in fees, or other economic incentives.”

• Documentation

• Account and/or relationship level documentation may change based on legislation

25

G

KeyCorp Public

The Value of Deposits

Banks have set their strategy to focus on the profitability of the relationship rather than to set targets for the entire segment.

Banks are reviewing their clients on an individual basis to identify whether the overall relationship is worth keeping.

Some will make minor concessions, such as not lowering rates for specific clients, if the overall relationship is profitable. At the same time, they are more willing to drop large deposits if the overall profitability of the relationship is not attractive.

Banks all accept that the deposits on their own are not valuable, however, they often are a necessary component to ultimately achieve profits, e.g., through loans and fee-generating services.

Banks have divergent strategies for their public sector/government lines of business, i.e.: some have continued to grow their public sector business because they are looking ahead to a more favorable interest rate environment.

26

G

KeyCorp Public

So what do I do with my cash?

Corporates need a solid understanding of daily cash requirements (Operational balances) versus long term investments (excess funds)

Some banks are offering or are evaluating offering product alternatives, including: Sweeps Term/Time Deposits Alternative Investments

Several banks are developing programs to help clients better optimize or forecast their operating cash as a method to reposition deposit alternatives.

27

G

KeyCorp Public

Call to Action

What does this mean to me (the Corporate) specifically?

Talk to your banker about: Your operating needs versus investments What pricing or rate impacts will I see? What investment options do you offer?

What does this mean to me (the Banker) specifically? Is it BAU for your clients? Are you discussing LCR with your clients? Are you monitoring the competitive landscape?

28

K

KeyCorp Public

Reality is …

All market participants, including financial institutions, rating analysts, financial journalists and regulators are learning that we now live in an environment where new rules will continue to appear as markets evolve. The Basel banking committee never intended for the first Basel to be set in stone.

In our lifetime, it is more than likely that we could see a Basel V or even a Basel VIII. That reality and its impact, not only to the banking industry, needs to be communicated to the market, i.e.: what do these changes mean for you?

29

G

QuestionsQuestions

Questions

Questions

Questions

Questions

Questions

Questions

KeyBank is Member FDIC.KeyCorp Public 30

Related Documents