A Project Report on “WORKING CAPITAL MANAGEMENT” At Submitted in the partial fulfillment of the requirements of Post Graduate Diploma in Management At Indus Business Academy, Bangalore Under the guidance of Dr. Ramesh. S Mr. Niranjan Nanda Mentor Senior Manager (Finance) Indus Business Academy NALCO Bangalore-560062 Bhubaneswar-751001 Submitted By Shubhransu Kumar Patel (FPB1214/137)

Working Capital Management at NALCO

Oct 23, 2015

This report is made for education purpose

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

A

Project Report on

“WORKING CAPITAL MANAGEMENT”

At

Submitted in the partial fulfillment of the requirements of

Post Graduate Diploma in Management

At

Indus Business Academy, Bangalore

Under the guidance of

Dr. Ramesh. S Mr. Niranjan Nanda

Mentor Senior Manager (Finance)

Indus Business Academy NALCO

Bangalore-560062 Bhubaneswar-751001

Submitted By

Shubhransu Kumar Patel (FPB1214/137)

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 2

Director’s Certificate

This is to certify that Mr. Shubhransu Kumar Patel is a bonafied student of

Indus Business Academy, Bangalore and is presently pursuing his Post Graduate

Diploma in Management.

Under my guidance he has submitted his Project titled “Working Capital

Management” at National Aluminium Company Limited in partial fulfillment of the

requirement during the Post Graduate Diploma in Management.

This project has not been previously submitted as part of another degree or

diploma of another Business School or University.

Dr. Subhash Sharma (Dean)

Indus Business Academy

Lakshmipura, Thataguni Post,

Kanakapura Main Road,

Bangalore-560062

Tel: +91-80-28435931/2/3/4

Fax: +91-80-28435935

Email: [email protected]

URL: www.ibainternational.org

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 3

Guide’s Certificate

This is to certify that the project entitled “Working Capital Management” at

National Aluminium Company Limited (NALCO) Corporate Office; Bhubaneswar has

been carried out by Mr. Shubhransu Kumar Patel from 05th Aug 2013 to 14th Oct

2013, under my Supervision in partial fulfillment of the requirement for the Post

Graduate Diploma in Management at Indus Business Academy, Bangalore. I am

satisfied with his sincere performance and study.

I wish his all success in life.

Mr. Niranjan Nanda

Sr. Manager (Finance)/Project Guide

National Aluminium Company Limited

Bhubaneswar

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 4

Mentor’s Certificate

This is to certify that Mr. Shubhransu Kumar Patel is a bonafied student of

Indus Business Academy, Bangalore and is presently pursuing his Post Graduate

Diploma in Management.

Under my guidance he has submitted his project titled “Working Capital

Management” at National Aluminium Company Limited in partial fulfillment of the

requirement during the Post Graduate Diploma in Management.

This paper has not been previously submitted as part of another degree or

diploma of another Business School or University.

Dr. Ramesh. S (Mentor)

Indus Business Academy

Lakshmipura, Thataguni Post,

Kanakapura Main Road,

Bangalore-560062

Tel: +91-80-28435931/2/3/4

Fax: +91-80-28435935

Email:[email protected]

URL:-www.ibainternational.org

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 5

Declaration

I Mr. Shubhransu Kumar Patel the undersigned, a student of Indus Business

Academy, Bangalore, declare that this project report titled “Working Capital

Management” in partial fulfillment of the requirement for the Summer Internship

Program during the Post-Graduation Diploma in Management.

This work has not been previously submitted by me as a part of any other

degree or diploma of another school or University.

Shubhransu Kumar Patel

FPB1214/137

PGDM 2012-2014

Indus Business Academy

Lakshmipura, Thataguni Post,

Kanakpura Main Road,

Bangalore- 560062

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 6

Acknowledgement

I take this opportunity to thank my college, Indus Business Academy, Bangalore

and Mr. Manish Jain (CEO) for giving me a chance to do a summer internship project,

adding the experience of practical knowledge so important to understand and to try and

bridge the gap between theoretical and practical knowledge.

I also express my sincere gratitude to Dr. Subhash Sharma, Director, Indus

Business Academy and Dr. Ramesh. S Faculty of Indus Business Academy for their

valuable inputs.

I am thankful to “National Aluminium Company Limited” for giving me an

opportunity to undertake a project on “Working Capital Management” and also for

providing me all the information required.

I express my gratitude to Mr. Niranjan Nanda, Senior Manager (Finance) at to

National Aluminium Company Limited, who through his vast experience and knowledge

has been able to guide me, both ably and successfully towards the completion of my

summer internship project.

I am sincerely grateful for the assistance of several individuals, who have

contributed towards fulfillment of this report. The knowledge, experience, guidance and

the most important factors – support from these people are indeed valuable.

Shubhransu Kumar Patel

Indus Business Academy,

Bangalore

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 7

Table of Contents:

Director’s Certificate................................................................................................................ 2

Guide’s Certificate ................................................................................................................... 3

Mentor’s Certificate ................................................................................................................. 4

Declaration ............................................................................................................................... 5

Acknowledgement ................................................................................................................... 6

Executive Summary: ............................................................................................................... 9

Introduction: ........................................................................................................................... 10

Definition of Working Capital: .......................................................................................... 10

Important things about Working Capital: ....................................................................... 11

Importance of Working Capital ........................................................................................ 11

Concept of Working Capital: ............................................................................................ 12

Operating Cycle Concept of Working Capital: .............................................................. 11

Importance of Cash flow Management in Working Capital Management: ............... 15

Consequences of Under Assessment of Working Capital: ......................................... 16

Consequences of Over Assessment of Working Capital: ........................................... 16

Industry Profile ....................................................................................................................... 17

History: ................................................................................................................................ 17

Introduction: ....................................................................................................................... 18

Major producing countries: .............................................................................................. 19

Major Consuming Countries: ........................................................................................... 19

Top Aluminum Companies in India: ............................................................................... 20

Porter's Five Force Model Analysis: ............................................................................... 23

Company Profile .................................................................................................................... 25

NALCO: ............................................................................................................................... 25

Vision: ................................................................................................................................. 25

Mission: ............................................................................................................................... 25

Achievements: ................................................................................................................... 26

Organizational Structure: ................................................................................................. 27

General Information about NALCO: ............................................................................... 28

Balance Sheet as on 31.3.2013: ..................................................................................... 29

Statement of Profit and Loss account as on 31.3.2013: ............................................. 30

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 8

Last Five Year Performance of NALCO: ....................................................................... 31

Comparisons of NALCO with Hindalco: ......................................................................... 32

Projects under Planning: .................................................................................................. 33

Brownfield Projects: ...................................................................................................... 33

Vertical Integration Projects: ........................................................................................ 33

Diversification Projects (Power): ................................................................................. 34

Diversification Projects (Other): .................................................................................. 34

Greenfield Projects: ...................................................................................................... 35

SWOT Analysis: ................................................................................................................ 36

Analysis and Interpretation: ................................................................................................. 38

Objective of the Study: ..................................................................................................... 38

Ratio Analysis: ................................................................................................................... 38

Role of Ratio Analysis: ..................................................................................................... 38

Financial ratio analysis: .................................................................................................... 39

Liquidity Ratios: ............................................................................................................. 39

Activity or Efficiency Ratio: .......................................................................................... 44

Profitability Ratio: .......................................................................................................... 49

Findings: ................................................................................................................................. 53

Suggestions: .......................................................................................................................... 53

Conclusion: ............................................................................................................................. 54

Bibliography: .......................................................................................................................... 55

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 9

Executive Summary:

Cash is the life line of a company understanding a company’s cash flow is

essential for making essential decisions. A good way to judge a company’s cash flow

prospects is to look at its Working Capital Management. Working capital is also

known as operational capital. It represents the day to day liquidity available to a

business. The goal of working capital management is to ensure that a firm is able to

continue its operations and has sufficient ability to satisfy both maturing short term

debt and upcoming operational expenses.

Every start up business need funds for two purposes for its establishment and

for its day to day operations but the success of that business entirely depends on the

proper management of the day-today finance and the management of this short term

capital of the business is called Working Capital Management.

Working Capital is the money used to pay for the everyday trading activities

carried out by the business- stationary needs, staff salaries and wages, rent, energy

bills, payments for suppliers and so on.

This report is showing the financial performance of company through ratio

analysis related to working capital management.

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 10

Introduction:

Definition of Working Capital:

“Working capital is an excess of current assets over current liabilities. In other

words, the amount of current assets which is more than current liabilities is known as

Working Capital. If current liabilities are nil then, working capital will equal to current

assets. Working capital shows strength of business in short period of time. If a

company have some amount in the form of working capital, it means Company have

liquid assets, with this money company can face every crises position in market."

Formula of Calculating Working Capital

Working Capital = Current Assets - Current Liabilities

Current Assets

Current assets are those assets which can be converted into cash within One

year or less than one year. Current assets include cash, bank, debtors, bill

receivables, prepaid expenses, outstanding incomes.

Current Liabilities

Current Liabilities are those liabilities which can be paid to respective parties

within one year or less than one year at their maturity. Current liabilities include

creditors, outstanding bills, bank overdraft, bills payable and short term loans,

outstanding expenses, advance income.

Other names of Working Capital

Some Professional accountants know working capital as operating capital,

operating liquidity, positive working capital.

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 11

Important things about Working Capital:

1. Working Capital can be negative. At that time, we add one word “deficiency" in the

back of working capital. It means if Current Liabilities are more than current assets, it

is known as working capital deficiency or inverse working capital or negative working

capital.

2. Working capital can be easily adjusted, if Accounts manager knows different

techniques of managing working capital. He can try to get short term loan or he can

increase working capital by proper management of inventory and outstanding

incomes and debtors.

3. Working capital can also change by Changing in Cash Conversion period. Cash

conversion period is a period in which company changes current assets into cash or

bank.

4. Working capital can also positive by increasing growth rate of company. If

company does not invest more money and increase profit, the same amount will

increase in the cash position of company and with cash company can increase their

working capital position.

Importance of Working Capital

Some times, if creditors demand their money from company, at that time

company's high working capital saves company from that situation. You know that

selling of current assets is easy in small period of time but Company cannot sell their

fixed assets with in small period of time. So, if Company has sufficient working

capital, Company can easily pay off the creditors and create his reputation in market.

But if a company has zero working capital and then company cannot pay creditors in

emergency time and either company becomes bankrupt or takes loan at higher rate

of Interest. In both condition, it is very dangerous and always Company's Account

Manager tries to keep some amount of working capital for creating goodwill in

market.

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 12

Positive working capital also enables to pay day to day expenses like wages,

salaries, overheads and other operating expenses. Because sufficient working capital

can not only pay maturity liabilities but also outstanding liabilities without any more

delay.

One of the advantage of positive working capital that Company can do every risky

work without any tension of self-security.

Concept of Working Capital:

1. Gross Working Capital

In this concept of working capital, we study gross working capital. We do not deduct

current liabilities in this concept but we use current liabilities as source of fund.

Suppose, if we buy goods on credit, it means we save our cash and we can use this

as working capital for paying other expenses.

2. Net Working Capital

Under this concept we use net working capital. For this, we first deduct all our current

liabilities from our current assets. Excess of current assets over current liabilities will

be current assets. We have to maintain minimum level of working capital in our

business for operation of business activities. This concept is also used for

preparation of balance sheet. In the vertical form of balance sheet, we show excess

of current assets over current liabilities.

Operating Cycle Concept of Working Capital:

In this concept of working capital, we make the operating cycle. In this cycle,

we calculate inventory conversion period. To know this, we can estimate when we

need cash for buying our inventory. We also calculate debtor or receivable

conversion period. To know this, we can estimate when we receive cash from our

debtors.

If inventory conversion period is less than debtor conversion period, we have

to manage other sources for buying our inventories. If we buy good on credit, we also

take care creditors' conversion period.

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 13

(Operation cycle of Working Capital Management)

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 14

Factors affecting Working Capital Management:

The working capital needs of a business are influenced by numerous factors.

The important parts are discussed in brief as given below:

Nature of Enterprise

The nature and the working capital requirements of an enterprise are interlinked.

While a manufacturing industry has a long cycle of operation of the working capital,

the same would be short in an enterprise involved in providing services. The required

amount is also varies as per the nature; an enterprise involved in production would

require more working capital than a service sector enterprise.

Manufacturing/Production Policy

Each enterprise in the manufacturing sector has its own production policy, some

follow the policy of uniform production even if the demand varies from time to time,

and others may follow the principle of 'demand-based production' in which production

is based on the demand during that particular phase of time. Accordingly, the working

capital requirements vary for both of them.

Operations

The requirement of working capital fluctuates for seasonal business. The working

capital needs of such businesses may increase considerably during the busy season

and decrease during the slack season. Ice creams and cold drinks have a great

demand during summer, while in winter the sales are negligible.

Market Condition

If there is high competition in the chosen product category, then one shall need to

offer shops like credit, immediate delivery of goods etc. for which the working capital

requirement will be high. Otherwise, if there is no competition or less competition in

the market then the working capital requirements will be low.

Availability of Raw Material

If raw material is readily available then one need not maintain a large stock of the

same, thereby reducing the working capital investment in raw material stock. On the

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 15

other hand, if raw material is not readily available then a large inventory/stock needs

to be maintained, thereby calling for substantial investment in the same.

Growth and Expansion

Growth and expansion in the volume of business results is enhancement of the

working capital requirement. As business grows and expands, it needs a larger

amount of working capital. Normally, the need for increased working capital funds

precedes growth in business activities.

Price Level Changes

Generally, rising price level requires a higher investment in the working capital. With

increasing prices, the same level of current assets needs enhanced investment.

Manufacturing Cycle

The manufacturing cycle starts with the purchase of raw material and is completed

with the production of finished goods. If the manufacturing cycle involves a longer

period, the need for working capital would be more.

Importance of Cash flow Management in Working

Capital Management:

A company with healthy operating cash flow is in a position to plough this cash into

its projects/working capital projects/working capital cycle.. It can thus grow at a

steady pace, compared to the companies that mostly rely on external sources to fund

their growth. This was on display during the credit crisis last year, which put the

future of companies with poor cash flows in doubt.

It may be possible that company reports very good earnings but it may not be

generating sufficient cash. Cash flow can be negative while profitability is positive.

Income statement and cash flow statement should be analyzed to assess the

operational efficiency of the company.

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 16

Consequences of Under Assessment of Working

Capital:

Growth may be stunted. It may become difficult for the enterprise to

undertake profitable projects due to non-availability of working capital.

Implementation of operating plans may become difficult and consequently the

profit goals may not be achieved.

Cash crisis may emerge due to paucity of working funds.

Optimum capacity utilization of fixed assets may not be achieved due

to non-availability of the working capital.

The business may fail to honors its commitment in time, thereby adversely

affecting its credibility. This situation may lead to business closure.

The business may be compelled to buy raw materials on credit and sell

finished goods on cash. In the process it may end up with increasing cost of

purchases and reducing selling prices by offering discounts. Both these

situations would affect profitability adversely.

Non-availability of stocks due to non-availability of funds may result in

production stoppage.

While underassessment of working capital has disastrous implications on

business, over assessment of working capital also has its own danger.

Consequences of Over Assessment of Working

Capital:

Excess of working capital may result in unnecessary accumulation of

inventories.

It may lead to offer too liberal credit terms to buyers and very poor recovery

system and cash management.

It may make management complacent leading to its inefficiency.

Over-investment in working capital makes capital less productive and may

reduce return on investment.

Working capital is very essential for success of a business and, therefore,

Need efficient management and control. Each of the components of the

working capital needs proper management to optimize the profit.

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 17

Industry Profile

History:

Indian Aluminium Industry was first established in the year 1808 and it took

almost 46 years to make its production commercially viable. The research work of the

country took several years and resulted in extracting the Aluminium from the ore. On

earth Aluminium is third most available element constituting almost 7.3% by mass.

Currently Aluminium is also the second most used metal in the world after steel. Due

to the fact that consistent growth of Indian economy at a rate of 8%, the demand for

metals, used for various sectors, is also on the higher side. As a result, the Indian

Aluminium Industry is also growing consistently as in the year 2009 the aluminium

industry in India saw a growth of about 9%.

In the year 1938 the production of Aluminium started in India when the

Aluminum Corporation of India's plant was commissioned. The plant was set up with

a financial and technical collaboration with Alcan, Canada which had a capacity of

producing 2,500 tons per annum. In the year 1959 the Hindustan Aluminum

Corporation (Hindalco) was set up; which had a capacity of producing 20,000 tons

per annum. A public sector enterprise Malco which had a capacity of 10,000 tons per

annum was commissioned in 1965. Then later in the year 1987, National Aluminium

Company (NALCO) was commissioned to produce Aluminium with a capacity of

producing 0.218 million tons.

Indian Aluminium Industry Government started regulating and controlling

during the 1970's. Restrictions in entry and price distribution controls were common

in the Aluminium Industry. Aluminium Control Order has been implemented where

the aluminium producers had to sell 50% of their products for electrical usages in the

country. Later in 1989, the order was removed as the government decontrolling was

revoked. In the year 1991 with de-licensing of industry, the liberal import of

technologies and capital goods was started. The liberalization resulted in a growth

rate of 12% of the industry, comparing to the growth rate of 6% during the 1980.

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 18

Introduction:

India was the second largest consumer of aluminium in Asia during the year

2012, with the electrical sector being the main driver of demand. As the largest

producer of aluminium in India, we are well positioned to cater to its growing demand

for aluminium.

In addition to the electrical sector, the automotive and construction sectors also

contribute a major share for the aluminium market in India. As per forecast, the

primary aluminium demand in India is expected to reach 6 million tonnes by 2025,

which equates to about 4.1kg of per capita aluminium consumption in 2025.

When compared to the current per capita aluminium

consumption of around 1.5 kg and aluminium

demand of 1.8 million tonnes, this underscores the

immense potential for demand growth in India.

Aluminium continues to outpace other base metals

in 2012-13, despite softer demand according to a

study. However the Indian aluminium industry would be affected by probable slower

Chinese growth in the years to come.

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 19

Major producing countries:

Major Consuming Countries:

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 20

Top Aluminum Companies in India:

Aluminum industry is one of the highly concentrated industry in India and the

top five companies in this sector offers a great share towards the production of the

country. With the increasing demand for aluminum in India, the top players in this

sector are also growing at a faster pace. The fact is that production of Aluminum in

India has presently outpaced the demand for aluminum in the country.

India holds second place in aluminum production after China and the country

has a competence of producing 3.95 million tons, which is nearly 8% of the total

aluminum production all over the world. The names of top players in the aluminum

industry in India are given below:

Top players in Aluminum Industry in India:

• HINDALCO

• Sterlite Industries

• NALCO

• BALCO

• MALCO

• INDAL

• Kennametal India

• Hindustan Zinc

• Sujana Metal Products

Some of the details regarding these top players in the aluminum industry in

India are given in next page.

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 21

HINDALCO:

HINDALCO has a market share of 39% in the aluminum industry in India and

this company is a flagship of Aditya Birla Group. They have their aluminum plant in

the state of Uttar Pradesh and they are dealing with different types of aluminum

products like foils, wheels, rolled products, extrusions and primary aluminum.

Sterlite Industries:

This company’s aluminum production comprises of MALCO and BALCO, who

are two giants in the aluminum industry in India. MALCO is a wholly integrated

producer of aluminum, while BALCO is partially integrated. Sterlite industries have a

market share of 32% in the Indian aluminum industry.

NALCO:

The Indian Government has a stake of 87.15% in this company and they have

their aluminum plant at Damanjodi, which is located in the state of Orissa. The

present production capacity of the company if 345000 tons of aluminum and to

increase it to 460000 tons, the company is concentrating on a capex programme.

BALCO:

Bharat Aluminum Company Limited came into existence in the year 1965 as a

public sector undertaking. Nearly 51% of the equity share of this company is held by

Stertile industries. This is an ISO 9001:2000 company with ownership over smelters,

refineries, captive power plants, captive bauxite mines and of course, aluminum

mines.

MALCO:

MALCO stands for Madras Aluminum Company and this company is a

subsidiary of Vedanta Resources. They have their power plant at Salem in Tamil

Nadu and they are engaged in different activities like mining, refining and smelting in

the aluminum industry.

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 22

INDAL:

INDAL stands for Indian Aluminum Company Limited and they are now

merged with Hindalco Industries Limited, who is the top player in the aluminum

industry in India. INDAL is operating from the state of West Bengal.

Kennametal India:

Kennametal India came into existence in the year 1964 and their former name

was Widia India Limited. They are dealing with the manufacture of different products

like products made out of hard metals, machines for special purposes, forming, jigs

and fixtures, metal castings and mining tools in the aluminum industry in India.

Hindustan Zinc:

ZL and the company came into existence in the year 1966 as public sector

undertaking. In the year 2002, government of India disinvested its stock holding with

HZL and this company became a part of Sterlite industries.

Sujana Metal Products:

This company came into existence in the year 2000 and they are gaining

popularity as the largest manufacturer aluminum products in the whole of south India.

They are dealing with four major division’s namely international trade, TMT bars,

structural steels and tower manufacturing.

Thus, the aluminum sector is growing by every means in India and this sector

is also contributing to the development of the country through offering employment

opportunities to a number of deserving people.

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 23

Porter's Five Force Model Analysis:

Threat of New Entry:

Time and cost of entry

Specialist in Knowledge

Economies of Scale

Cost Advantages

Technology Perfection

Barriers to Entry

Porter's Five Force

Model

Threat of New Entry

Buyer Power

Threat of Substitution

Supplier Power

Competitive Rivalry

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 24

Buyer Power:

Number of customer

Size of each order

Differences between competitors

Price sensitivity

Ability to substitute

Threat of Substitution:

Substitute performance

Cost of change

Supplier Power:

Number of suppliers

Size of suppliers

Uniqueness of service

Your ability to substitute

Cost of changing

Competitive Rivalry:

Number of competitors

Quality differences

Customer’s loyalty

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 25

Company Profile

NALCO:

Incorporated in 1981, as a public sector enterprise of the Government of India

National Aluminium Company Limited (Nalco) is Asia's largest integrated aluminium

complex, encompassing bauxite mining, alumina refining, aluminium smelting and

casting, power generation, rail and port operations. Commissioned during 1985-87,

Nalco has emerged to be a star performer in production, export of alumina and

aluminium, and more significantly, in propelling a self-sustained growth.

Vision:

To be reputed global Company in the Metals and Energy Sectors.

Mission:

To continuously develop human resources, create safe working conditions,

improve productivity and quality and reduce cost and waste.

To be a good corporate citizen, protecting and enhancing the environment as

well as discharging social responsibility in order to ensure sustainable growth.

To intensify R&D for technology development.

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 26

Achievements:

First Mines Safety Award-1988 by DGMS

Indira Priyadarshini Vrikshamitra (IPVM) Award-1994 from MOEF, Govt. of

India, for afforestation and wasteland development

Best Eco-friendly Factory Award 1994-95 to the Mines and Refinery Complex

by Orissa State Factory Inspectrate

State Award-1995 to Captive Power Plant from state Factory inspectorate for

Environment Management

FICCI Environment Award for Environment Conservation and Pollution

Control- 1996-97

WEC-IIEE-IAEWP Environment award -1997 for contributing towards

environment protection

Gem Granite Environment Award for -1997-98 by FIMI, New Delhi for Mines

Shri Sita Ram Rungta Memorial Social Awareness Award-1997-98 by FIMI,

New Delhi

Pollution Control Excellence Award - 1998 by Orissa State Pollution Control

Board for Mines

Special Commendation under Golden Peacock Environment Management

Award 1998 Scheme by World Environment Foundation

State Award for Best Occupational Health Centre to S&P Complex`-1998

Best Safety Performance Award to CPP by CII (ER)- 1999-2000

2nd Best Practice in Environment, Safety & Health in industries of Orissa

award by CII-ER to CPP -2006-07.

Best Environment Management Award to CPP for 2006-07.

Best Performance in Accident Prevention, Safety management &

communication System to CPP for 2006-07.

Pollution Control Excellent Award 2008 to Panchpatmali Bauxite Mines from

State Pollution Control Board, Bhubaneswar.

2nd Best Practice in Environment Management instituted by Confederation of

Indian Industry (CII) to Alumina Refinery for 2008-09.

Pollution Control Excellence Award 2009 by OSPCB to Alumina Refinery.

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 27

Organizational Structure:

NALCO has an effective organizational structure Headed by Shri Ansuman

Das (Chairman cum Managing Director) along with seven full time and part time

official Directors, Eight Independent Directors (appointed by Govt. of India) and Eight

Executive Directors with total 7555 No. of Permanent Employees.

DIRECTOR

EXECUTIVE DIRECTOR

GENERAL MANAGER

D. GENERAL MANAGER

ASST. GENERAL MANAGER

SENIOR MANAGER

MANAGER

D. MANAGER

ASST. MANAGER

JUNIOR MANAGER

ASST. OFFICER

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 28

General Information about NALCO:

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 29

Balance Sheet as on 31.3.2013:

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 30

Statement of Profit and Loss account as on 31.3.2013:

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 31

Last Five Year Performance of NALCO:

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 32

Comparisons of NALCO with Hindalco:

The major competitor of NALCO is Hindalco in Aluminium production in India.

…………….Rs in Cr……………..

Name Market Capital Sales Turnover Net Profit Total Assets

NALCO 8,272.94 6,916.48 592.83 11,932.45

Hindalco 23,521.13 26,056.93 1,699.20 58,117.16

The above table shows the comparative study of NALCO against its biggest rivalry

Hindalco in terms of aluminium production in India.

Above table indicates ₹8.57 profit against the sales of ₹100.00 each as compared to

Hindalco ₹6.52. Nalco is generating ₹2.02 more profit then Hindalco.

……………..Rs in Cr…………….

Name NALCO Hindalco

Mar '13 Mar '13

Sources Of Funds

Total Share Capital 1,288.62 191.48

Equity Share Capital 1,288.62 191.48

Share Application Money 0 541.31

Preference Share Capital 0 0

Reserves 10,643.83 33,239.60

Revaluation Reserves 0 0

Networth 11,932.45 33,972.39

Secured Loans 0 20,521.01

Unsecured Loans 0 3,623.76

Total Debt 0 24,144.77

Total Liabilities 11,932.45 58,117.16

This table shows the details related to companies Debt and Equity.

NALCO is having 672.98% more Share Capital of Hindalco, whereas Hindalco is

having 312.80% more Reserves of NALCO.

In terms of Debt NALCO has zero debt as compare to Hindalco ₹24,144.77 Cr.

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 33

Projects under Planning:

Brownfield Projects:

Vertical Integration Projects:

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 34

Diversification Projects (Power):

Diversification Projects (Other):

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 35

Greenfield Projects:

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 36

SWOT Analysis:

Strengths:

Nalco has achieved the “Zero Debt’ status. It has its own strong financial

resources. Due to effective implements of ‘state of the art’ technology its image in the

Global Market is excellent and in Indian Market it is the leader in Aluminum

market/sector.

The company has its own fully mechanized open cast mines along with its

own Aluminum plant. It has its own microprocessor-based burner at its own power

plant having automatic turbine run up system.

Skilled and committed manpower, good quality bauxite reserves, efficient

technology, efficient operations, production of quality alumina and aluminium

products at competitive cost, excellent customer service, prudential financial

management and sound corporate Governance practices in all facets of operations

are some of the key strengths of NALCO.

Weakness:

Due to present scenario of industrial development, there is an exodus of

experienced personnel from the company. The company work culture is poor due to

strong trade union activities and political interferences. Average age of workmen is

high which has becomes a hindrance of effective working.

Now a day’s coal supply has become a major problem for the company. As

the company is dependent upon imported coal is the major weakness. Exchange

rates are some of the weaknesses that continue to affect the profitability of the

company.

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 37

Opportunities:

The company has commenced its project activities for the second phase

expansion and shall precede its own resources to a considered extent. The

availability of surplus Alumina with the company after 2nd phase expansion and the

sustaining demand for Alumina in the global market has put it in a demanding stage

and offers attractive opportunities for entering into creative business deals and for

participating in the JVS of overseas smelter.

The continuation of reform process focus on second generation liberalization

process and the ongoing globalization trend may bring ample opportunities for the

company in playing a key role in metal trading, hedging, tolling, capacity addition,

technology collaboration and in redefining new areas for application of its value

added rolled products and chemical business.

Threats:

Continuous rising of crude oil in global market, developments of fragmented

geopolitical scenario, slowdown in the economic activities across the global, possible

halt to the peace initiatives with neighboring countries, terrorism, reversal in global

economic scenario, hardening of interest rates, natural calamities, erratic monsoon,

poaching of its man power by competitors for their green field projects and levy of

anti-dumping duties on its raw material import are the major threats of NALCO.

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 38

Analysis and Interpretation:

Objective of the Study:

To understand the practical aspects of working capital management.

To understand the role of ratios in working capital management.

To understand the day to day income and expenses of the organization.

Research Type:

This Research is purely based on Secondary Research.

Data Referred for Analysis:

Annual Reports of NALCO (Last 5 Years)

Ratio Analysis:

Ratio analysis is the powerful tool of financial statements analysis. A ratio is

define as “the indicated quotient of two mathematical expressions” and as “the

relationship between two or more things”. The absolute figures reported in the

financial statement do not provide meaningful understanding of the performance and

financial position of the firm. Ratio helps to summaries large quantities of financial

data and to make qualitative judgment of the firm’s financial performance.

Role of Ratio Analysis:

Ratio analysis helps to appraise the firms in the term of their profitability and

efficiency of performance, either individually or in relation to other firms in same

industry. Ratio analysis is one of the best possible technique available to manage for

impart the basic functions like planning and control. As future is closely related to the

immediately past, ratio calculated on the basis historical financial data may be of

good assistance to predict the future. E.g. On the basis of inventory turnover ratio or

debtor’s turnover ratio in the past, the level of inventory and debtors can be easily

ascertained for any given amount of sales. Similarly, the ratio analysis may be able to

locate the point out the various areas which need the management attention in order

to improve the situation. E.g. Current ratio which shows a constant decline trend may

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 39

be indicate the need for further introduction of long term finance in order to increase

the liquidity position. As the ratio analysis is concerned with all the aspect of the

firm’s financial analysis liquidity, solvency, activity, profitability and overall

performance, it enables the interested persons to know the financial and operational

characteristics of an organization and take suitable decisions.

Financial ratio analysis:

Financial ratio analysis involves calculating certain standardized relationship

between figures appearing in the financial statements and then using those

relationships called ratios to analyze the business' financial position and financial

performance. Due to varying size of businesses different comparison of two

businesses is not possible. Certain techniques have to be applied in simplifying the

financial statements and making them comparable. These include financial ratio

analysis and common-size financial statements.

Ratios are divided into different categories such as liquidity ratios, Activity

ratio, profitability ratios, etc.

Liquidity Ratios:

Liquidity is the ability of a business to pay its current liabilities using its current

assets. Information about liquidity of a company is relevant to its creditors,

employees, banks, etc. current ratio, quick ratio, cash ratio and cash conversion

cycle are key measures of liquidity.

Current Ratio:

Current ratio is the ratio of current assets of a business to its current liabilities.

It is the most widely used test of liquidity of a business and measures the ability of a

business to repay its debts over the period of next 12 months.

Formula:

Current ratio is calculated using the following formula:

Current Ratio = Current Assets/Current Liabilities

Both the above figures can be obtained from the balance sheet of the

business. Current assets are the assets of a business expected to be converted to

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 40

cash or used up in next 12 months or within the normal operating cycle of the

business. Current liabilities on the other hand are the obligations of a business which

need to be settled within next 12 months or within the normal operating cycle.

Graphical Representation of Current Ratio:

Analysis:

Current ratio matches current assets with current liabilities and tells us

whether the current assets are enough to settle current liabilities. Current ratio below

1 shows critical liquidity problems because it means that total current liabilities

exceed total current assets. General rule is that higher the current ratio better it is but

there is a limit to this. Abnormally high value of current ratio may indicate existence of

idle or underutilized resources in the company.

1.90

2.00

2.10

2.20

2.30

2.40

2.50

2.60

2.70

FY2012-13 FY2011-12 FY2010-11 FY2009-10 FY2008-09

YEARS

Current Ratio

Current Ratio

YEARS

(Amounts in

Crore)

FY2012-

13 FY2011-12

FY2010-

11 FY2009-10

FY2008-

09

Current Assets 7075.81 7022.33 6045.17 5209.64 4528.81

Current

Liabilities 3211.93 2676.89 2740.95 2219.93 1933.24

Current Ratio 2.20 2.62 2.21 2.35 2.34

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 41

Quick Ratio or Acid Test Ratio:

Quick ratio or Acid Test ratio is the ratio of the sum of cash and cash

equivalents, marketable securities and accounts receivable to the current liabilities of

a business. It measures the ability of a company to pay its debts by using its cash

and near cash current assets (i.e. accounts receivable and marketable securities).

Formula

Quick ratio is calculated using the following formula:

Quick Ratio = (Cash +Marketable Securities +Receivables)/Current Liabilities

Marketable securities are those securities which can be converted into cash

quickly. Examples of marketable securities are treasury bills, saving bills, shares of

stock-exchange, etc. Receivables refer to accounts receivable. Alternatively, quick

ratio can also be calculated using the following formula:

Formula:

Quick / Acid Test Ratio = (Current Asset-Inventory)/Current Liabilities

YEARS

(Amounts in

Crore)

FY2012-

13

FY2011-

12

FY2010-

11

FY2009-

10

FY2008-

09

Current Assets 7075.81 7022.33 6045.17 5209.64 4528.81

Inventories 1380.64 1212.7 1058.47 944.92 841.9

Current

Liabilities 3211.93 2676.89 2740.95 2219.93 1933.24

Quick Ratio 1.77 2.17 1.82 1.92 1.91

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 42

Graphical Representation of Quick Ratio:

Analysis:

Quick ratio measures the liquidity of a business by matching its cash and near

cash current assets with its total liabilities. It helps us to determine whether a

business would be able to pay off all its debts by using its most liquid assets (i.e.

cash, marketable securities and accounts receivable).

A quick ratio of 1.00 means that the most liquid assets of a business are

equal to its total debts and the business will just manage to repay all its debts by

using its cash, marketable securities and accounts receivable. A quick ratio of more

than one indicates that the most liquid assets of a business exceed its total debts. On

the opposite side, a quick ratio of less than one indicates that a business would not

be able to repay all its debts by using its most liquid assets.

Thus we conclude that, generally, a higher quick ratio is preferable because it

means greater liquidity. However a quick ratio which is quite high, say 4.00 is not

favorable to a business as whole because this means that the business has idle

current assets which could have been used to create additional projects thus

increasing profits. In other words, very high value of quick ratio may indicate

inefficiency.

0.00

0.50

1.00

1.50

2.00

2.50

FY2012-13 FY2011-12 FY2010-11 FY2009-10 FY2008-09

YEARS

Quick Ratio

Quick Ratio

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 43

Cash Ratio:

Cash ratio is the ratio of cash and cash equivalents of a company to its

current liabilities. It is an extreme liquidity ratio since only cash and cash equivalents

are compared with the current liabilities. It measures the ability of a business to repay

its current liabilities by only using its cash and cash equivalents and nothing else.

Formula:

Cash ratio is calculated using the following formula:

Cash Ratio = Cash +Cash Equivalents/Current Liabilities

Cash equivalents are assets which can be converted into cash quickly

whereas current liabilities are those liabilities which are to be settled within 12

months or the business cycle.

YEARS

(Amounts in Crore)

FY2012-

13

FY2011-

12

FY2010-

11

FY2009-

10

FY2008-

09

Cash and Cash

Equivalents 3504.38 4168.35 3795.23 3125.35 2869.04

Current Liabilities 3211.93 2676.89 2740.95 2219.93 1933.24

Cash Ratio 1.09 1.56 1.38 1.41 1.48

Graphical Representation of Cash Ratio:

0.00

0.50

1.00

1.50

2.00

FY2012-13 FY2011-12 FY2010-11 FY2009-10 FY2008-09

YEARS

Cash Ratio

Cash Ratio

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 44

Analysis:

Cash ratio of NALCO is1.00 it means, that the business will be able to pay all

its current liabilities in immediate short term. Therefore, creditors usually prefer high

cash ratio. But businesses usually do not plan to keep their cash and cash equivalent

at level with their current liabilities because they can use a portion of idle cash to

generate profits. This means that a normal value of cash ratio is somewhere below

1.00.

Activity or Efficiency Ratio:

Inventory Turnover Ratio:

Inventory turnover is the ratio of cost of goods sold by a business to its

average inventory during a given accounting period. It is an activity ratio measuring

the number of times per period; a business sells and replaces its entire batch of

inventory again.

Formula:

Inventory turnover ratio is calculated using the following formula:

Inventory Turnover Ratio = Net Sales/Inventories

Cost of goods sold figure is obtained from the income statement of a business

whereas the values of inventory are obtained from the balance sheets.

YEARS

(Amounts in

Crore)

FY2012-

13

FY2011-

12

FY2010-

11

FY2009-

10

FY2008-

09

Net Sales 6809.00 6500.00 5958.98 5055.66 5094.52

Inventories 1380.64 1212.7 1058.47 944.92 841.9

Inventory Turnover

Ratio 4.93 5.35 5.62 5.35 6.05

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 45

Graphical Representation of Inventory Turnover Ratio:

Analysis:

Inventory turnover ratio is used to measure the inventory management

efficiency of a business. In general, a higher value of inventory turnover indicates

better performance and lower value means inefficiency in controlling inventory levels.

A lower inventory turnover ratio may be an indication of over-stocking which may

pose risk of obsolescence and increased inventory holding costs. However, a very

high value of this ratio may be accompanied by loss of sales due to inventory

shortage.

Inventory turnover is different for different industries. Businesses which trade

perishable goods have very higher turnover compared to those dealing in durables.

Hence a comparison would only be fair if made between businesses of same

industry.

Working Capital Turnover Ratio:

The working capital turnover ratio measures how well a company is utilizing

its working capital to support a given level of sales. Working capital is current assets

minus current liabilities. A high turnover ratio indicates that management is being

extremely efficient in using a firm's short-term assets and liabilities to support sales.

Conversely, a low ratio indicates that a business is investing in too many accounts

receivable and inventory assets to support its sales, which could eventually lead to

an excessive amount of bad debts and obsolete inventory.

0.001.002.003.004.005.006.007.00

FY2

01

2-1

3

FY2

01

1-1

2

FY2

01

0-1

1

FY2

00

9-1

0

FY2

00

8-0

9

YEARS

Inventory Turnover Ratio

Inventory Turnover Ratio

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 46

Formula:

The working capital turnover ratio is calculated using the following formula:

The working capital turnover ratio = Net Sales/Working Capital

YEARS

(Amounts in

Crore)

FY2012-

13

FY2011-

12

FY2010-

11

FY2009-

10

FY2008-

09

Net Sales 6809 6500 5958.98 5055.66 5094.52

Working Capital 3863.88 4345.44 3304.22 2989.71 2595.57

Working Capital

Turnover Ratio 1.76 1.50 1.80 1.69 1.96

Graphical Representation of Working capital Turnover Ratio:

Analysis:

An extremely high working capital turnover ratio can indicate that a company

does not have enough capital to support it sales growth; collapse of the company

may be imminent. This is a particularly strong indicator when the accounts

payable component of working capital is very high, since it indicates that

management cannot pay its bills as they come due for payment.

0.00

0.50

1.00

1.50

2.00

FY2

01

2-1

3

FY2

01

1-1

2

FY2

01

0-1

1

FY2

00

9-1

0

FY2

00

8-0

9

YEARS

Working Capital Turnover Ratio

Working Capital TurnoverRatio

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 47

An excessively high turnover ratio can be spotted by comparing the ratio for a

particular business to those reported elsewhere in its industry, to see if the business

is reporting outlier results.

Asset turnover ratio:

Asset turnover ratio is the ratio of a company's sales to its assets. It is an

efficiency ratio which tells how successfully the company is using its assets to

generate revenue.

There are a number of variants of the ratio like total asset turnover ratio, fixed

asset turnover ratio and working capital turnover ratio. In all cases the numerator is

the same i.e. net sales (both cash and credit) but denominator is average total

assets, average fixed assets and average working capital respectively.

Formula:

Following formulas are used to calculate each of the asset turnover ratios:

Total Asset Turnover Ratio=Net Sales/Total Assets

Fixed Asset Turnover Ratio = Net Sales/Fixed Assets

YEARS

(Amounts in

Crore) FY2012-13 FY2011-12 FY2010-11 FY2009-10 FY2008-09

Net Sales 6809 6500 5958.98 5055.66 5094.52

Total Assets 16326.95 15520.78 11872.95 11056.17 10391.16

Fixed Assets 6523.8 6498.98 7237.06 7079.71 6899.66

Total Assets

Turnover Ratio 0.42 0.42 0.50 0.46 0.49

Fixed Assets

Turnover Ratio 1.04 1.00 0.82 0.71 0.74

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 48

Graphical Representation of Total Assets Turnover Ratio :

Analysis

If a company can generate more sales with fewer assets it has a higher

turnover ratio which tells it is a good company because it is using its assets

efficiently. A lower turnover ratio tells that the company is not using its assets

optimally. Total asset turnover ratio is a key driver of return on equity.

0.000.100.200.300.400.500.60

FY2

01

2-1

3

FY2

01

1-1

2

FY2

01

0-1

1

FY2

00

9-1

0

FY2

00

8-0

9

YEARS

Total Assets Turnover Ratio

Total Assets Turnover Ratio

0.000.200.400.600.801.001.20

FY2

01

2-1

3

FY2

01

1-1

2

FY2

01

0-1

1

FY2

00

9-1

0

FY2

00

8-0

9

YEARS

Fixed Assets Turnover Ratio

Fixed Assets Turnover Ratio

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 49

Profitability Ratio:

Every firm is most concerned with its profitability. One of the most frequently

used tools of financial ratio analysis is profitability ratios which are used to determine

the company's bottom line and its return to its investors. Profitability measures are

important to company managers and owners alike. If a small business has outside

investors who have put their own money into the company, the primary owner

certainly has to show profitability to those equity investors.

Profitability ratios show a company's overall efficiency and performance. We

can divide profitability ratios into two types: margins and returns. Ratios that show

margins represent the firm's ability to translate sales dollars into profits at various

stages of measurement. Ratios that show returns represent the firm's ability to

measure the overall efficiency of the firm in generating returns for its shareholders.

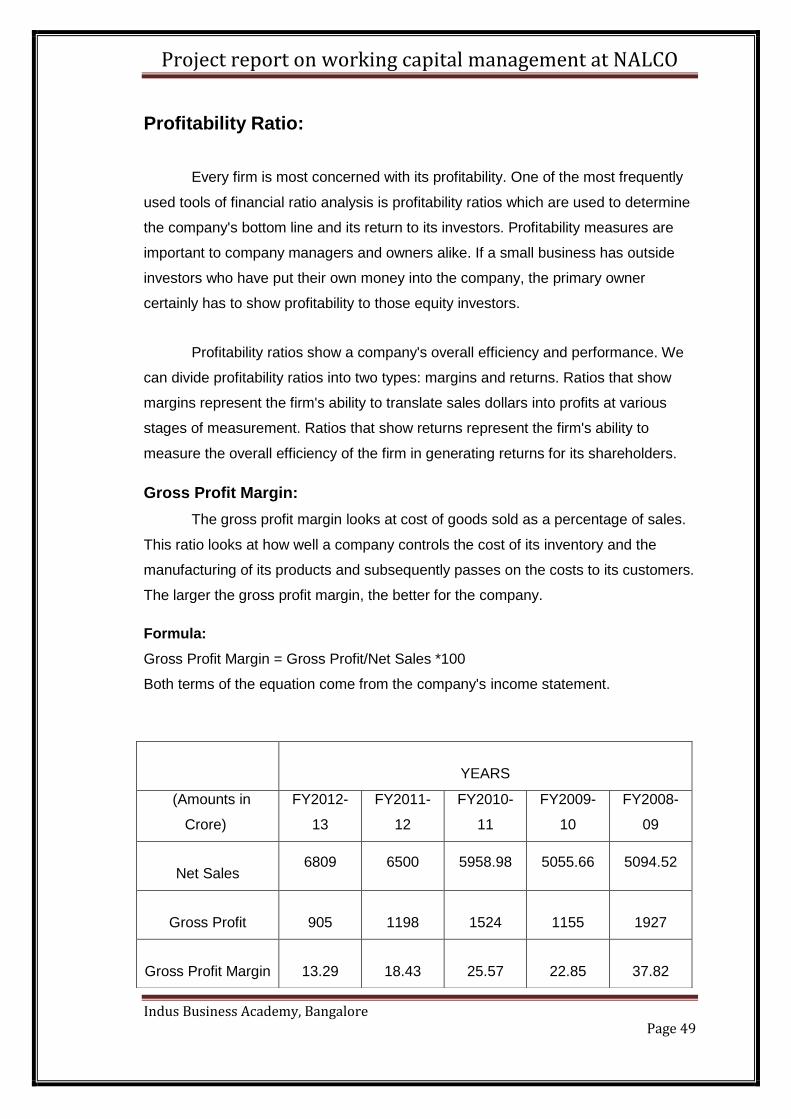

Gross Profit Margin:

The gross profit margin looks at cost of goods sold as a percentage of sales.

This ratio looks at how well a company controls the cost of its inventory and the

manufacturing of its products and subsequently passes on the costs to its customers.

The larger the gross profit margin, the better for the company.

Formula:

Gross Profit Margin = Gross Profit/Net Sales *100

Both terms of the equation come from the company's income statement.

YEARS

(Amounts in

Crore)

FY2012-

13

FY2011-

12

FY2010-

11

FY2009-

10

FY2008-

09

Net Sales 6809 6500 5958.98 5055.66 5094.52

Gross Profit 905 1198 1524 1155 1927

Gross Profit Margin 13.29 18.43 25.57 22.85 37.82

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 50

Graphical Representation of Gross Profit Margin:

Operating Profit Margin:

Operating profit is also known as EBIT and is found on the company's income

statement. EBIT is earnings before interest and taxes. The operating profit margin

looks at EBIT as a percentage of sales. The operating profit margin ratio is a

measure of overall operating efficiency, incorporating all of the expenses of ordinary,

daily business activity.

Formula:

Operating Profit Margin = Operating Profit/Net Sales*100

Both terms of the equation come from the company's income statement.

YEARS

(Amounts in Crore)

FY2012-

13

FY2011-

12

FY2010-

11

FY2009-

10

FY2008-

09

Operating Profit 906 1145 1593 1102 1804

Net Sales 6809 6500 5958.98 5055.66 5094.52

Operating Profit Margin 13.31 17.62 26.73 21.8 35.32

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

FY2012-13 FY2011-12 FY2010-11 FY2009-10 FY2008-09

YEARS

Gross Profit Margin

Gross Profit Margin

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 51

Graphical Representation of Operating Profit Margin:

Analysis

Operating margin ratio of 9% means that a net profit of ₹9.00 is made on

each ₹100.00 of sales. Thus a higher value of operating margin ratio is favorable

which indicates that more proportion of revenue is converted to operating income. An

increase in operating margin ratio overtime means that the profitability is improving. It

is also important to compare the gross margin ratio of a business to the average

gross profit margin of the industry. In general, a business which is more efficient is

controlling its overall costs will have higher operating margin ratio.

Net Profit Margin:

When doing a simple profitability ratio analysis, net profit margin is the most

often margin ratio used. The net profit margin shows how much of each sales shows

up as net income after all expenses are paid. For example, if the net profit margin is

5%, which means that ₹5.00 of every ₹100.00 is profit.

The net profit margin measures profitability after consideration of all expenses

including taxes, interest, and depreciation.

0.005.00

10.0015.0020.0025.0030.0035.0040.00

FY2

01

2-1

3

FY2

01

1-1

2

FY2

01

0-1

1

FY2

00

9-1

0

FY2

00

8-0

9

YEARS

Operating Profit Margin

Operating Profit Margin

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 52

Formula:

Net Profit Margin = Net Income/Net Sales*100

Both terms of the equation come from the income statement.

YEARS

(Amounts in

Crore)

FY2012-

13

FY2011-

12

FY2010-

11

FY2009-

10

FY2008-

09

Net Sales 6809 6500 5958.98 5055.66 5094.52

Net Income 593 1050 1069 814 1272

Net Profit Margin 8.71 16.15 17.94 16.10 24.97

Graphical Representation of Net Profit Margin:

Analysis

Net profit margin shows the actual profit generated by company after paid all the

taxes and duties to Govt. As compare to FY 2011-12 this year it drastically reduce from

16.15% to 8.71% this year.

0.00

5.00

10.00

15.00

20.00

25.00

FY2012-13 FY2011-12 FY2010-11 FY2009-10 FY2008-09

YEARS

Net Profit Margin

Net Profit Margin

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 53

Findings:

Current ratio of NALCO is 2.20 and it shows that company has enough

Current Assets to settle its Current Liability.

Quick ratio of NALCO is 1.70 it means for each ₹1.00 of Liability Company

has ₹1.70 to repay.

Working capital turnover ratio is 1.76 in the year 2012-13; it shows that

company has enough money to support its sales growth.

Asset turnover ratio is 0.42 which indicate that NALCO is not making the

optimum utilization its assets towards production.

Operating profit margin is decreased as compare to its previous year, mainly

due to the bad economy condition, shortage of domestic coal, high cost of

imported coking coal(six times cost more as compared to domestic coal)

NALCO has followed a very good investment strategy for its surplus amounts

as they are not keeping their surplus amount idle.

Suggestions:

Company should try to start production in Rolled product unit of NALCO

which is not operating and being idle since long.

The Debt-Equity ratio is 0:1 now, it means NALCO is presently a zero debt

company. It should try to reduce its equity and increase its debt component in

order to leverage its position.

The company should try and extend credit sales so that their sale increases.

Since NALCO has a sellers’ market, it can take advantages of this position

and expand its production to grow its sales further.

Company should try to take another coal block to overcome the problems

related to shortage of coal to improve their production.

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 54

Conclusion:

The management of Working Capital deals with determination, maintenance,

control and monitoring of level of all the individual current assets. For the efficient

and optimal use of fixed assets, the existence and necessity of current assets is

implied. Working Capital is the amount necessary to cover the cost of operating the

enterprise which means to carry out the day to day operations. After studying the

components of working capital management system of NALCO, It is found that the

company has a sound and effective policy and its performance is very good even in

this bad recession situation company has managed to post good profit. Declining

cost of the products due to stiff competition from China accompanied with the rising

cost of inputs, particularly that of imported coking coal is likely to erode the profit

margin of Nalco in the current financial year. Company is competing well at the

domestic as well as the international level and it is among the low cost producers of

aluminium in the world only because of its proper management of finance, specially

the short term finance known as the working capital. The company is a matured one

and it has contributed well in the countries growth and development and will also

continue to perform and contribute to the whole nation. In conclusion, we can say

that the company’s management is an effective one and knows well the management

of finance, its working capital management system is very good because of which

only the company has got the status of NAVRATNA Company. The management

would try to make up for the loss by technology up gradation, improvement in

manufacturing rate and reduction in the cost of production ,the company’s exports

have perceptually increased and it has bright potential to carry on its endeavors to

achieve excellence in its field. Research and Development Endeavour of NALCO

have been product and process developments of value added products, waste

utilization, indigenization of improvement technology to the extent possible.

Project report on working capital management at NALCO

Indus Business Academy, Bangalore Page 55

Bibliography:

NALCO Annual Report 2008-09, 2009-10, 2010-11, 2011-12 & 2012-13

http://wirc-icai.org/material/sanjay%20kothari.pdf

http://www.ediindia.org/doc/SpecialPDF/chp-14.pdf

http://www.indianmirror.com/indian-industries/2013/aluminium-2013.html

http://www.nalcoindia.com

http://finance.toolbox.com/blogs/business-borrowing/how-to-read-a-ratio-

financial-statement-analysis-41501

http://accountingexplained.com/financial/ratios//

Related Documents