CHAPTER- 1 COMPANY PROFILE OF JAI PRAKASH ASSOCIATION 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CHAPTER- 1

COMPANY PROFILEOF

JAI PRAKASH ASSOCIATION

1

JAYPEE ASSOCIATES LTD.

Shri Jaiprakash Gaur(Founder Of Jaypee Group)

“Growth with a Human Face”

The group is well diversified conglomerate with active interest in the

areas of civil engineering, design & construction for hydropower & river

valley projects, development of private hydro power projects, cement

manufacturing, hospitality, Business development and management of golf

resort, expressways and highways, real estate development information

technology and educational institutes.

2

VISION OF THE COMPANY :-

“To be amongst most trusted power utility company by providing

environment friendly power on most cost effective basis, ensuring

prosperity for its stakeholders and growth with human face.”

MISSION OF THE COMPANY: -

To achieve excellence in every activity we undertake.

To ensure most cost effective power for sustained growth of India.

To inculcate value system across the organization for ensuring

trustworthy relationship with associates and stake holders.

To be committed towards the safety and health of employees and the

public. The main motto of the company is Work for Safe, Healthy,

and Clean & Green Environment.

MAJOR AREAS OF OPERATION

CEMENT

CIVIL CONSTRUCTION

HYDRO POWER CONSTRUCTION

HOTEL AND TOURISM

INFORMATION TECHNOLOGY

EDUCATION & WELFARE

JAIPRAKASH VENTURES LTD.

3

Jaypee Cement

Jaiprakash Associates ltd.

Jaypee Korcham Hydro Corporation

JIL Information Technology Ltd.

Jaiprakash Power Ventures

Jaypee Hotels Ltd.

Jaypee Greens Ltd.

Jaypee Cements Ltd

Jaypee Ventures Ltd.

Jaiprakash Sewa Sansthan

Jaypee Cement

Jaypee Korcham Hydro Corporation

JIL Information Technology Ltd.

Jaiprakash Power Ventures

Jaypee Hotels Ltd.

Jaypee Greens Ltd.

Jaypee Cements Ltd

Jaypee Ventures Ltd.

Jaiprakash Sewa Sansthan

JAYPEE GROUP

CORPORATE PHILOSOPHY

Any corporate entity needs to be dynamic and vibrant, responsive to

the changing economic scenario and flexible enough to absorb

environmental and physical fluctuations. It must harness the inherent

strengths of available resources and must possess the capacity to learn

from success. More than anything else, it should ensure growth with a

humane face.

Today Jaypee Group is a well-diversified infrastructure industrial group

with a turnover of over 15000 crores.

OVERVIEW OF CEMENT INDUSTRY

4

Cement is one of the core industries, which plays a vital role

in the growth of a nation. India ranks fifth among the cement

producing countries in the world. The present per capita cement

consumption is around 84kg, which is much lower than the per

capita consumption of the developed countries. During the last

couple of years, cement industry has been one of the main

beneficiaries of the infrastructure boom. While on the one hand

several big and small cement companies are actively considering

expansion plans in anticipation of further growth in demand for

cement, on the other, a phase of acquisitions and mergers among

the existing players is also not being ruled out in the immediate

future.

The present scenario of cement industry is very good in

terms of demand and with the prices going above Rs 170 - Rs 180

5

per bag everywhere and in some pockets even reaching Rs 200 per

bag. Most importantly, the gap between the demand and supply does

not exist any longer in any part of the country. Domestic

consumption with 11 per cent increase and exports keeping up with

the last year levels, the Indian cement industry is expected to cross

150 million tones in dispatches, including domestic consumption , and

exports during 2005-06 from all plants put together.

The Indian cement industry has a capacity to produce nearly 152

million tonnes a year and the demand has been growing by almost 10 per

cent annually, it has driven most of the cement companies to operate at

their full capacity or peak production levels. The consumption demand

for cement has risen substantially in states like Andhra Pradesh,

Karnataka, Rajasthan, Himachal Pradesh, West Bengal and Chattishgarh.

Moreover, healthy demand from Middle East Asian countries has helped

to push up the demand for cement export. The cement dispatches in the

last one year rose by a robust 11 percent aided by 10 per cent growth in

domestic dispatches. The exports have risen by 48 percent as against

clinker exports which are down by 43 per cent. As the demand has far

outstripped supply the cement companies’ capacities are at full throttle

with almost 94 percent utilization. A glance at the table below shows the

production and dispatches and more importantly the capacity utilization

levels of major Indian companies for the period April 05 to Feb 06.

JAYPEE: CEMENT DIVISION

6

Jaypee group is the 3rd largest cement producer in the country. The groups

cement facilities are located in the Satna Cluster (M.P.), which has one of

the highest cement production growth rates in India.

The group produces special blend of Portland Pozzolana Cement under the

brand name ‘Jaypee Cement’ (PPC). Its cement division currently operates

modern, computerized process control cement plants with an aggregate

installed capacity of 28 MnTPA. The company is in the midst of capacity

expansion of its cement business in Northern, Southern, Central, Eastern

and Western parts of the country and is slated to be a 35.90 MnTPA by

FY13 (expected) with Captive Thermal Power plants totaling 672 MW.

7

Keeping pace with the advancements in the IT industry, all the 260 cement

dumps are networked using TDM/TDMA VSATs along with a dedicated

hub to provide 24/7 connectivity between the plants and all the 120 points

of cement distribution in order to ensure “track – the – truck” initiative and

provide seamless integration. This initiative is the first of its kind in the

cement industry in India.

In the near future, the group plans to expand its cement capacities via

acquisition and greenfield additions to maximize economies of scale and

build on vision to focus on large size plants from inception. The Group is

committed towards the safety and health of employees and the public. Our

motto is.

‘Work For Safe, Healthy,

Clean & Green Environment'.

Mining

The cement manufacturing process starts from the mining of limestone,

which is the main raw material for making cement. Limestone is excavated

from open cast mines after drilling and blasting and loaded on to dumpers

8

which transport the material and unload into hoppers of the limestone

crushers.

Crushing Stacking & Reclaiming of Limestone

The LS Crushers crush the limestone to minus 80 mm size and discharge the

material onto a belt conveyor which takes it to the stacker via the Bulk

material analyzer. The material is stacked in longitudinal stockpiles.

Limestone is extracted transversely from the stockpiles by the declaimers

and conveyed to the Raw Mill hoppers for grinding of raw meal.

Crushing Stacking & Reclaiming of Coal

The process of making cement clinker requires heat. Coal is used as the fuel

for providing heat. Raw Coal received from the collieries is stored in a coal

yard. Raw Coal is dropped on a belt conveyor from a hopper and is taken to

and crushed in a crusher. Crushed coal discharged from the Coal Crusher is

stored in a longitudinal stockpile from where it is reclaimed by a reclaimer

and taken to the coal mill hoppers for grinding of fine coal.

Raw Meal Drying/Grinding & Homogenization

Reclaimed limestone along with some laterite stored in their respective

hoppers is fed to the Raw Mill for fine grinding. The hot gasses coming

from the clinkerisation section are used in the raw mill for drying and

transport of the ground raw meal to the Electrostatic Precipitator / Bag

House, where it is collected and then stored and homogenised in the

9

concrete silo. Raw Meal extracted from the silo (now called Kiln feed) is

fed to the top of the Preheater for Pyroprocessing.

Clinkerisation

Cement Clinker is made by pyroprocessing of Kiln feed in the preheater and

the rotary kiln. Fine coal is fired as fuel to provide the necessary heat in the

kiln and the Precalciner located at the bottom of the 5/6 stage preheater. Hot

clinker discharged from the Kiln drops on the grate cooler and gets cooled.

The cooler discharges the clinker onto the pan / bucket conveyor and it is

transported to the clinker stockpiles / silos. The clinker is taken from the

stockpile / silo to the ball mill hoppers for cement grinding.

Cement Grinding & Storage

Clinker and Gypsum (for OPC) and also Pozzolana (for PPC) are extracted

from their respective hoppers and fed to the Cement Mills. These Ball Mills

grind the feed to a fine powder and the Mill discharge is fed to an elevator,

which takes the material to a separator, which separates fine product and the

coarse. The latter is sent to the mill inlet for regrinding and the fine product

is stored in concrete silos.

Packing

Cement extracted from silos is conveyed to the automatic electronic packers

where it is packed in 50 Kgs. Polythene bags and dispatched in trucks.

Recent Achievements of Jai Prakash Associations

10

Year 2012 300 MW Baspa – II Hydropower project has been awarded the “Gold

Shield for 2009-10” and “Silver Shield for 2010-11” by the Ministry of

Power, Government of India in the category of “performance of

hydropower stations”.

Mr. Manoj Gaur, Executive Chairman, Jaypee Group and Mr.

Sameer Gaur, MD & CEO, Jaypee Sports International Ltd won the

Global Standards Award at NDTV Profit Business Leadership Awards

2011. The award was presented by Mr. Pranab Mukherjee, Union Finance

Minister of India on 7th January, 2012 at Mumbai.

Year 2011

Dalla Cement Factory (A unit of Jaiprakash Associates Ltd.) is

11

awarded first prize in the cement sector for the National Energy

Conservation Awards, 2011.

Chunar Cement Factory (A unit of Jaiprakash Associates Ltd.) is

awarded the Certificate of Merit in the cement sector for the National

Energy Conservation Awards, 2011.

Jaypee Rewa Cement Plant and Jaype Bela Cement Plant in Madhya

Pradesh of the Group have been awarded with the most prestigious “SWORD

OF HONOUR” award by the British Safety Council, UK in the field of Health

and Safety management system.

Year 2010

Jaypee Rewa Cement Plant and Jaype Bela Cement Plant in

Madhya Pradesh of the Group have been awarded with renowned and most

prestigious “SWORD OF HONOUR” award by the British Safety Council, UK. This

is a well acclaimed and celebrated international award in the field of

12

Health and Safety management system. 3.00 MnTPA Rewa and 2.40

MnTPA Bela are the only cement plants to be bestowed with this honour in

India.(For Details)

The garbage processing plant of Jaiprakash Associates Ltd.

located in Dadumajra, Chandigarh was awarded “Excellence for the best

solid waste management plant in the country” by Confederation of Indian

Industry (CII).

"Lifetime Achievement Award" being conferred to Shri Jaiprakash

Gaur, Founder Chairman by Merchants’ Chamber of Uttar Pradesh,

Kanpur for creating new milestones in Infrastructure development and his

achievement in Corporate Social Responsibility for the year 2010.

13

“Infrastructure Leader of the Year ” award being conferred to Shri

Jaiprakash Gaur, Founder Chairman by Shri Kamal Nath, the Union

Minister of Road Transport and Highways during the Essar Steel

Infrastructure Excellence Awards 2010 in association with CNBC TV18.

(For Details)

400 MW Vishnuprayag Hydropower Project of Jaiprakash Power

Ventures Ltd (JPVL) was awarded 1st Prize in the category “Energy &

Power’’ by the Essar Steel Infrastructure Excellence Awards 2010 in

association with CNBC TV18. (For Details)

300 MW Baspa – II Hydropower project being awarded with “Silver

Shield” by Shri Sushil Kumar Shinde, Union Minister of Power along with

Shri Bharatsinh Solanki, Union Minister of State for Power in the

prestigious National Awards for Meritorious Performance in Power Sector

by the Ministry of Power for 2008-09.

14

CHAPTER-2

INTRODUCTION

OF

WORKING CAPITAL

MANAGEMENT

What is Working Capital?

15

Working capital is how much in liquid assets that a company has on hand.

Working capital is needed to pay for planned and unexpected expenses,

meet the short-term obligations of the business, and to build the business.

A lack of working capital makes it hard to attract investors or to get

business loans or obtain credit.

Working capital is the money a business has available to sustain its

operations. It's the capital available to purchase inventory, pay employees,

keep the lights on, and finance other short term expenditures. This makes

managing working capital a critical business skill. If there is no working

capital, there is no business.

Thousands of companies fail each year due to poor working capital

management practices. Entrepreneurs often don't account for short term

disruptions to cash flow and are forced to close their operations. Many of

these companies have viable business models, and would have otherwise

succeeded had they better managed their working capital.

Working Capital is Required to Start and Grow a Business :-

When you first start a business you need start-up working capital since the

business is not yet making money to sustain itself. The number one reason

most businesses fail during their first two years of operation is due to a lack

of working capital.

Having ample working capital not only helps you to meet your obligations,

it is vital to growing your business.

16

Types of working capital:-

The operating cycle creates the need for current assets (working

capital).However the need does not come to an end after the cycle is

completed to explain this continuing need of current assets a destination

should be drawn between permanent and temporary working capital.

Permanent working capital:

The need for current assets arises, as already observed, because of the cash

cycle. To carry on business certain minimum level of working capital is

necessary on continues and uninterrupted basis. For all practical purpose,

this requirement will have to be met permanent as with other fixed assets.

This requirement refers to as permanent or fixed working capita.

Temporary working capital:

Any amount over and above the permanent level of working capital is

temporary, fluctuating or variable, working capital. This portion of the

required working capital is needed to meet fluctuation in demand

consequent upon changes in production and sales as result of seasonal

changes.

Sources of Working Capital:

1) Long- term sources: -

a) Issue of shares

b) Issue of debentures

c) Long –term loans

d) Retained earning

e) Sale of any old asset

17

2) Short –Term Sources: -

a) Internal sources: -

i) Provision for tax

ii) Depreciation funds

iii) Outstanding expanses

b) External sources: -

i) Normal trade credit

ii) Bills payable

iii) Overdraft

iv) Public deposit

v) Advance from customers

FACTORS AFFECTING THE REQUIREMENT OF

WORKING CAPITAL

1) Size of business:

This is very clear that if there is any big concern means it need

maximum of working capital to run the business smoothly but the

requirement of working capital will be reduced if we will reduced the

size of business as we do not have the sufficient long operating cycle

to invest the higher rate of working capital.

2) Nature of business:

Here we will discuss on the major part of firms -

i) The manufacturing unit

ii) The trading unit

Means we can easily understand that in case of manufacturing unit

the firm required maximum working capital to complete its

operating cycle.

18

3) Seasonal operation

The seasonal operation also effect the requirement of working capital

because the sale can be increased or decreased if they is any concern which

is manufacturing the seasonal goods.

4) Credit policy:

This policy normally takes an important place to impact on the

requirement of working capital means any company having a good credit

policy for a shorter period may required the less working capital on the

other hand the lenient credit policy may generate the risk of doubtful debts.

In this case the company requires more working capital during this period

this takes place to convert the credit into cash.

5) Marketable competition:

As per the present synerio of the market we can find the toughest

competition between every two company which are dealing with the same

time of product to reduce the competitiveness and to win the gain the

company gives or provides the some special offers to the buyer and to the

seller and these offers are not related with the operating cycle of the

company so the company needs exist amount of working capital to manage

the amount of these offers.

6) Growth and expansion:

As for as the growth and expansion is concerned it is very clear it will

increase the size of business we require some extra money for this purpose.

In the same condition if any company going to launch a new product they

again required exist amount of working capital to complete the operating

cycle of that particular product. The increment in the size is known as

growth and the establishment in the new sector or segment is called

expansion.

19

7) Shortage of raw material:

The requirement of working capital is also depends on the viability of

the raw material in the market. At the time of shortage of raw material

the price may also be high due to higher demand and less viability in this

case the firm has to purchase the raw material on higher price and required

some extra amount for the increment of cost. It means the company has to

invest more money for purchasing.

8) Dividend policy:

This factor is important because it is directly impact on the

financial position of the firm because the higher dividend rate makes the

company enable to get as strong position in the market. So to fulfill the

requirement of the dividend the company may use the retained earning or

profit or they have to generate the funds for dividend from other sources. So

this will impact on the operating cycle as well as this will degrees the cash

balance of the company, which the company is used to fulfill requirement

of temporary working capital.

9) Depreciation policy:

Depreciation policy also is treated as a source of working

capital because we can use the depreciation funds for the timing of fulfill the

requirement of temporary working capital. If the company is not

maintaining the depreciation policy in this case the company has to generate

the funds from the long term sources or any other source which can be

increase the liability of the firm.

20

Management of working capital:

Working capital management involves the relationship between a

firm's short-term assets and its short-term liabilities. The goal of working

capital management is to ensure that a firm is able to continue its operations

and that it has sufficient ability to satisfy both maturing short-term debt and

upcoming operational expenses. The management of working capital

involves managing inventories, accounts receivable and payable, and cash.

Working capital management will use a combination of policies and

techniques for the management of working capital. The policies aim at

managing the current assets (generally cash and cash equivalents,

inventories and debtors) and the short term financing, such that cash flows

and returns are acceptable.

• Cash management

• Inventory management

-Work in Process (WIP), Finished Goods, Supply chain

management, Just In Time, Economic order quantity, Economic

quantity.

• Debtors management

- Credit policy vice versa Discounts and allowances

• Short term financing

- Loan factoring

21

Working capital operating cycle

Investment in working capital is influenced by four key events in the

production and sales cycle. These events are: purchase of raw materials,

payment for their purchase, the sale of finished goods, and collection of

cash for the sales made.

Operating cycle and cash cycle are two important components of working

capital management. Together they determine the efficiency of a firm

regarding working capital management. While the operating cycle is the

time period from inventory purchase until the receipt of cash, the cash cycle

is the time period from when cash is paid out, to when cash is received.

The cash cycle is interpreted as the number of days between the payment for

inputs and getting cash by sales of commodities manufactured from that

input

Operating cycle of the company

The entire sequence of operations in a company can be summarized as

follows:

• The operating cycle for a company primarily begins with the purchase

of raw materials, which are paid for after a delay representing the

creditor's payable period.

• These purchased raw materials are then converted by the production

unit into finished goods and then sold. The time lag between the

purchase of raw materials and the sale of finished goods is known as

the inventory period.

22

• Upon sale of finished goods on credit terms, there exists a time lag

between the sale of finished goods and the collection of cash on sale.

This period is known as the accounts receivables period.

The operating cycle can be depicted as:

• The stage between purchase of raw materials and their payment is

known as the creditors’ payables period.

• The period between purchase of raw materials and production of

finished goods is known as the inventory period.

23

The following ratios will help in managing debtors, creditors and

inventories

1. Stock Turnover ratio = Cost of goods sold / Average Stock

2. Debtors Turnover ratio = [(Debtors+ Bills receivable*365] /

Net credit sales.

3. Debtors Turnover rate = Credit sales / (Average Debtors +

Bills receivable)

4. Creditors Turnover ratio = [(Creditors + Bills

payable)*365] / Credit purchases

5. Creditors Turnover rate = Credit purchases / Average

Creditors

24

CHAPTER- 3

INVENTORY MANAGEMENT

25

IN VENTORY MANAGEMENT :-

Material Management is concept which aims at a company wide,

integrated approach towards the management of materials in an Industrial

undertaking-Its objective is primarily cost reduction and efficient handling

of materials at all stages and in all parts of the undertaking.

Improving the capital turnover ratio covers the whole range of

functions involved in converting raw materials and ancillary supplies into

finished products.

IMPORTANCE OF MATERIALS MANAGEMENT :

1. Materials account for 60 to 64% fo the sales value of a production

hence small change in material costs can result in large sum of money

saved or lost.

The balance 36% accounts for wages and salaries, overheads and

profits.

2. Inventory carrying costs, briefly comprises of, interest charges on the

cost of inventory, storage and handling costs, cost of insurance, and

physical deterioration and obsolescence costs.

All these amounts to atleast 20% of the materials costs. These are

hidden costs generally covered by overheads.

3. So the total material cost will amount to be :

64% + ( 20% of 64 or 12.8%) = 76.8 say 77% of the sales revenue.

Hence, the inventories should be controlled to the minimum possible.

26

ADVANTAGES IN INTEGRATED MATERIALS MANAGEMENT

Organizations which have gone in a big way for the integrated

materials management usually enjoy the following advantages:

1. Better Accountability

2. Better Coordination

3. Better Performance

TOOLS AND TECHNIQUES OF INVENTORY MANAGEMENT

A-B-C Analysis (Applied in JRP based on consumption level):

The materials are divided into a number of categories for adopting a

selective approach for material control. It is generally seen that in

manufacturing concerns, a small percentage of items contribute a large

percentage of value of consumption and a large percentage of items of

material contribute a small percentage of value. In between these two

limits there are some items which have almost equal percentage of value

of materials. Under A-B-C analysis, the materials are divided into three

categories viz., A, B and C. Past experience has shown that almost 10

per cent of the items contribute to 70 per cent of value of consumption

and this category is called "A" Category. About 20 per cent of the items

contribute about 20 per cent of value of consumption and this is known

as category 'B' materials. Category 'C' covers about 70 per cent of items

of materials which contribute only 10 per cent of value of consumption.

There may be some variations in different organizations and an

adjustment can be made in these percentages.

27

PROCEDURE

1. RECEIPT OF STORES:

1. On arrival of consignment on visual inspection, if any damage is

found in packing of consignments of item/equipments, a damage

certificate is obtained from transporting agency and same is

forwarded to insurance Section for lodging transit insurance claim.

2. On receipt of the purchased product at the Stores, the delivery

documents are verified with corresponding purchase

orders/requisitions.

3. If purchased product is required CENVAT claim, handover

"Duplicate for Transporter copy" to Taxation Department

representative visiting Stores in morning hours of every working day.

4. Receipt of codified goods are recorded in goods receipt register as

and unique goods receipt number is allotted to each lot/consignment.

5. Physical verification of the quantities is carried out by counting

weight, measurement, etc.

6. An identification tag is affixed to one of the items, Bulk materials like

Steel, Grinding media, Casting, Refractory items, Lubricants, etc. are

directly unloaded at the designated place after due verification. Fuel

oils are directly taken into designated fuel tanks. Explosives are

directly unloaded at magazine located in the vicinity of mines after

due verification.

7. Fuel oils and explosive materials are unloaded, separately in separate

location i.e. HSD/Furnace Oil Tanks.

8. Inspection record generated accordingly.

9. Inspection of material being done within 07 days receipt to indenting

department with respect to the specifications in purchase orders and

actual receipts.

28

10. Non-confirming materials are documented in to Discrepancies Report

One copy of the same is forwarded to the supplies along with material

for appropriate action.

11. Bill of party, indicating the GR no. is forwarded to Accounts

Department for processing supplier payment.

12. All the non-conforming materials like returned to supplier supported

by Challan-cum gate pass.

2. STORAGE AND ISSUE OF STORES:

1. All items are issued to User Dept. against requisition slip as per

(Stores requisition slip)/ or reservation against SAP system.

2. Before issuing the materials necessary issue entries are made in

computer on line basis.

3. The items which require special storage condition like bearings,

instrumentation cards, vulcanizing materials, etc. are identified and

stored appropriately and special precautions are taken where

necessary.

4. All items which have a shelf-life are identified and first in first out

(FIFO) systems is followed for issue of such items, to ensure no

material with expiry date is stocked.

5. All shelf life items in stock are physically checked every month to

detect any deterioration. Expired material is being used with

permission of the indenter/user, in unproductive area or it is written

off and disposed off from the inventory after due approval of

Honorable MD.

6. All the items which gets surplus with user departments and further

usable can be returned to Stores through Stores Return Voucher

29

CHAPTER – 4

CASH MANAGEMENT

30

Cash management:

The corporate process of collecting, managing and (short-term)

investing cash. A key component of ensuring a company's financial stability

and solvency. Frequently corporate treasurers or a business manager is

responsible for overall cash management.

Successful cash management involves not only avoiding insolvency

(and therefore bankruptcy), but also reducing days in account

receivables(AR), increasing collection rates, selecting appropriate short-

term investment vehicles, and increasing days cash on hand all in order to

improve a company's overall financial profitability

CASH IS GENERALLY MAINTAINED FOR FOLLOWING

MOTIVES:

A. Transaction motive:

Transaction motive refer to the holding of cash to meet routine cash

requirements to finance the transactions which a firm carries on in a

variety of transactions to accomplish its objectives which have to be

paid for in the form of cash. E.g. payment for purchases, wages,

operating expenses, financial charges like interest, taxes, dividends

etc. Thus requirement of cash balances to meet routine need is known

as the transaction motive and such motive refers to the holding of

cash to meet anticipated obligations whose timing is not perfectly

synchronized with cash receipts.

B. Precautionary motive:

A firm has to pay cash for the purposes which can not be predicted or

anticipated. The unexpected cash needs at the short notice may be due

31

to:Floods, strikes & failure of customer Slow down in collection of

current receivables Increase in cost of raw material Collection of

some order of goods as customer is not satisfied The cash balance

held in reserves for such random and unforeseen fluctuations in cash

flows are called as precautionary balance. Thus, precautionary cash

provides a cushion to meet unexpected contingencies. The more

unpredictable are the cash flows, the larger is the need for such

balance.

C. Speculative motive:

It refers to the desire of the firm to take advantage of opportunities

which present themselves at unexpected moment & which are

typically outside the normal course of business. If the precautionary

motive is defensive in nature, in that firms must make provisions to

tide over unexpected contingencies, the speculative motive represents

a positive and aggressive approach. The speculative motive helps to

take advantages of: An opportunity to purchase raw material at

reduced price on payment of immediate cash. A chance to speculate

on interest rate movements by buying securities when interest rates

are expected to decline. Make purchases at favourable price. Delay

purchase of raw material on the anticipation of decline in prices.

D. Transaction motive:

Transaction motive refer to the holding of cash to meet routine cash

requirements to finance the transactions which a firm carries on in a

variety of transactions to accomplish its objectives which have to be

paid for in the form of cash. E.g. payment for purchases, wages,

operating expenses, financial charges like interest, taxes, dividends

32

etc. Thus requirement of cash balances to meet routine need is known

as the transaction motive and such motive refers to the holding of

cash to meet anticipated obligations whose timing is not perfectly

synchronized with cash receipts.

E. Precautionary motive:

A firm has to pay cash for the purposes which can not be predicted or

anticipated. The unexpected cash needs at the short notice may be due

to:Floods, strikes & failure of customer Slow down in collection of

current receivables Increase in cost of raw material Collection of

some order of goods as customer is not satisfied The cash balance

held in reserves for such random and unforeseen fluctuations in cash

flows are called as precautionary balance. Thus, precautionary cash

provides a cushion to meet unexpected contingencies. The more

unpredictable are the cash flows, the larger is the need for such

balance.

F. Speculative motive:

It refers to the desire of the firm to take advantage of opportunities

which present themselves at unexpected moment & which are

typically outside the normal course of business. If the precautionary

motive is defensive in nature, in that firms must make provisions to

tide over unexpected contingencies, the speculative motive represents

a positive and aggressive approach. The speculative motive helps to

take advantages of: An opportunity to purchase raw material at

reduced price on payment of immediate cash. A chance to speculate

on interest rate movements by buying securities when interest rates

are expected to decline. Make purchases at favourable price. Delay

purchase of raw material on the anticipation of decline in prices.

33

CHAPTER- 5

CREDIT MANAGEMENT

34

Credit management:

Credit means delaying payment for goods or services you have

already received until a later date.

Credit management is concerned with making sure that organisation,

who buy goods or services on credit, or individuals who borrow money, can

afford to do so and that they pay their debts on time.

Credit jobs exist within any industry sector e.g. manufacturing,

distribution, retail, telecoms, utilities, local authority, financial services, and

within any size company from SMEs (Small, Medium Enterprises) to large

corporate. You could also work for a company specialising in credit

management services e.g. debt collection agency, credit insurance company,

credit reference agency.

Credit policy:

The credit policy of the firm affects the working capital by

influencing the level of debtors. The credit terms to be granted to customers

may depend upon the norms of the industry to which the firm belongs. But a

firm has the flexibility of shaping its credit policy within the constraint of

35

industry norms and practices. The firm should be discretion in granting

credit terms to its customers. Depending upon the individual case, different

terms may be given to different customers. A liberal credit policy, without

rating the creditworthiness of customers, will be detrimental to the firm and

will create a problem of collections. A high collection period will mean tie-

up of large funds in book debts. Slack collection procedures can increase the

chance of bad debts. In order to ensure that unnecessary funds are not tied

up in debtors, the firm should follow a rationalized credit policy based on

the credit standing of customers and periodically review the

creditworthiness of the exiting customers. The case of delayed payments

should be thoroughly investigated.

36

CHAPTER- 6

RATIo ANAlysIs

AND

INTERpRETATIoN

37

RATIO ANALYSIS

Definition of 'Ratio Analysis'

Ratio Analysis is a form of Financial Statement Analysis that is used to

obtain a quick indication of a firm's financial performance in several key

areas. The ratios are categorized as Short-term Solvency Ratios, Debt

Management Ratios, Asset Management Ratios, Profitability Ratios, and

Market Value Ratios.

Ratio Analysis as a tool possesses several important features. The data,

which are provided by financial statements, are readily available. The

computation of ratios facilitates the comparison of firms which differ in

size. Ratios can be used to compare a firm's financial performance with

industry averages. In addition, ratios can be used in a form of trend analysis

to identify areas where performance has improved or deteriorated over time.

Because Ratio Analysis is based upon accounting information, its

effectiveness is limited by the distortions which arise in financial statements

due to such things as Historical Cost Accounting and inflation. Therefore,

Ratio Analysis should only be used as a first step in financial analysis, to

obtain a quick indication of a firm's performance and to identify areas which

need to be investigated further.

38

ADVANTAGE OF RATIO ANALYSIS

1. Helpful in analysis of Financial Statements.

2. Helpful in comparative Study.

3. Helpful in locating the weak spots of the business.

4. Helpful in Forecasting.

5. Estimate about the trend of the business.

6. Fixation of ideal Standards.

7. Effective Control.

8. Study of Financial Soundness.

39

SOLVENCY RATIOS

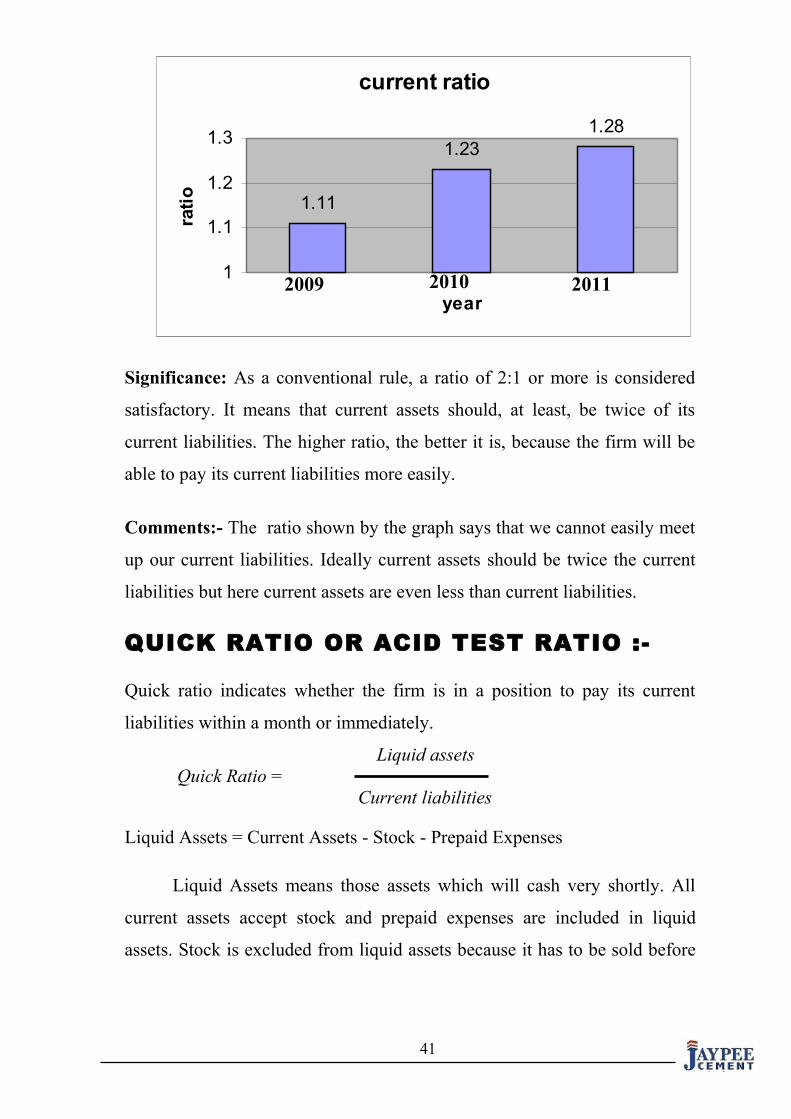

CURRENT RATIO

This ratio explains the relationship between current assets and current

liabilities of a business. The formula of calculating the ratio is:-

Current Assets

Current ratio = Current Liabilities

Current Assets include those assets which can be converted into cash within

a year’s time and current liabilities include those liabilities which are

repayable in a year’s time. This ratio indicates the availability of current

assets in rupees for every one rupee of current liability.

Current Assets = Cash in hand + Cash at Bank + Short term investments +

Debtors +Stock +Prepaid expenses.

Current Liabilities = Bank overdraft + B/P + Creditors + Provision for

Taxation + Proposed dividend + Unclaimed dividend + Outstanding

dividend + Loans payable within a year.

14,684,085,101.69For the year 2011-2010 = = 1.11:1

13,215,999,829.69

12929562027.36For the year 2009 - 2010 = = 1.23 : 1

10441716877.19

8707767112.25For the year 2008 – 2009 = = 1.28 : 1

6759523242.53

40

Significance: As a conventional rule, a ratio of 2:1 or more is considered

satisfactory. It means that current assets should, at least, be twice of its

current liabilities. The higher ratio, the better it is, because the firm will be

able to pay its current liabilities more easily.

Comments:- The ratio shown by the graph says that we cannot easily meet

up our current liabilities. Ideally current assets should be twice the current

liabilities but here current assets are even less than current liabilities.

QUICK RATIO OR ACID TEST RATIO :-

Quick ratio indicates whether the firm is in a position to pay its current

liabilities within a month or immediately.

Liquid assets Quick Ratio = Current liabilities

Liquid Assets = Current Assets - Stock - Prepaid Expenses

Liquid Assets means those assets which will cash very shortly. All

current assets accept stock and prepaid expenses are included in liquid

assets. Stock is excluded from liquid assets because it has to be sold before

41

current ratio

1.11

1.231.28

1

1.1

1.2

1.3

year

rati

o

2009 2010 2011

it converted into cash. Prepaid expenses are also excluded from it because

they are not expected to be converted into cash.

6081371899For the year 2009 - 2010 = = 0.60 : 1

10207269054

5868747252For the year 2008-2009 = = 0.90 :1 6504483042

Significance: Generally, the quick ratio of 1:1 is considered to be

satisfactory. Quick ratio thus more rigorous test of liquidity than the current

ratio and, when used together with current ratio, it gives a better picture of

short term financial position of the firm.

Comments:-

Since quick ratio is decreasing over the years [from 2009(0.90)-

2011(0.47)], it not gives a good picture of firm’ s short term financial

position so firm is not in the position to pay its current liabilities

immediately..

42

CASH RATIO

Since cash is the most liquid asset, a financial analyst may examine

cash ratio and its equivalent to current liabilities. Trade investments and

marketable securities equivalent to cash; so they may be included in cash

ratio.

Cash + Marketable securities Cash ratio = Current Liabilities

4943394564For the year 2010-2011 = = 0.38

12944132188

5344821803For the year 2009 - 2010 = = 0.52

10207269054

5578794627For the year 2008-2009 = = 0.86

6504483042

43

Significance:- Cash ratio generally helps in finding out whether the cash is

being proper utilised in the business or not and to check that whether or not

cash is lying ideal in the firm, if yes then to make proper utilisation of cash.

Comments:-As we can see that circulation of cash has decreased over the

past years. It shows that debtors are not making prompt payments and

company is not able to make better utilization of cash

ACTIVITY RATIO

INVENTORY TURNOVER RATIO

Inventory turnover indicates the efficiency of the firm in producing and

selling its products. It is calculated by dividing the cost of goods sold by the

average inventory.

Cost of Goods Sold Inventory Turnover Ratio = Average Inventory

Cost of Goods Sold = Opening Stock + Purchases + Direct Charges –

Closing Stock.

Or

Cost of Goods Sold = Net Sales – Gross Profit.

25344343015For the year 2010-2011 = = 7.78 times.

3256557159

15967226548For the year 2009-2010 = = 11.19 times.

1426463513

12521318155For the year 2008- 2009 = = 22.45 times

557573769

44

Significance:-

This ratio indicates whether or not the stock has been efficiently utilized. It

shows the speed with which the stock is rotated into sales. The higher the

ratio, the better it is, since it indicates that the stock is selling quickly. In

business where stock turnover is high goods can be sold at low margin of

profit and even then the profitability can be high.

Comments:

Inventory turnover ratio of the company is quite good earlier it means that

there is proper outflow of the stock and goods do not remain in the godown

for a long time. As we can see that the inventory turnover is decreasing

which shows that there is overspending in stock which is left unused .

TOTAL ASSETS TURNOVER RATIO

Assets are used to generate sales. Therefore, a firm should manage its assets

efficiently to maximize sales. The relationship between sales and assets is

called assets turnover.

45

Cost of goods sold / sales Total Assets turnover ratio = Total Assets

Total Assets = Fixed Assets + current assets

48520571504For the year ending (2010-2011) = = 0.29 times.

165871014877

35403563785For the year ending (2009-2010) = = 0.26. times.

134611476656

21958565843For the year ending (2008-2009) = = 0.206 times.

106429370209

.

Significance: This ratio is of particular importance in manufacturing

concerns where the investment in assets is quite high. This ratio reveals how

effectively the assets are being utilised, compared with previous year.

46

Comments:-

The graph clearly depicts that the total asset ratio was 0.20 times in 2008-

2009 which shows a gradual increase. The ratio gain momentum which

currently stood at 0.299 times which depicts efficient use of fixed assets

than earlier.

PROFITABILITY RATIO

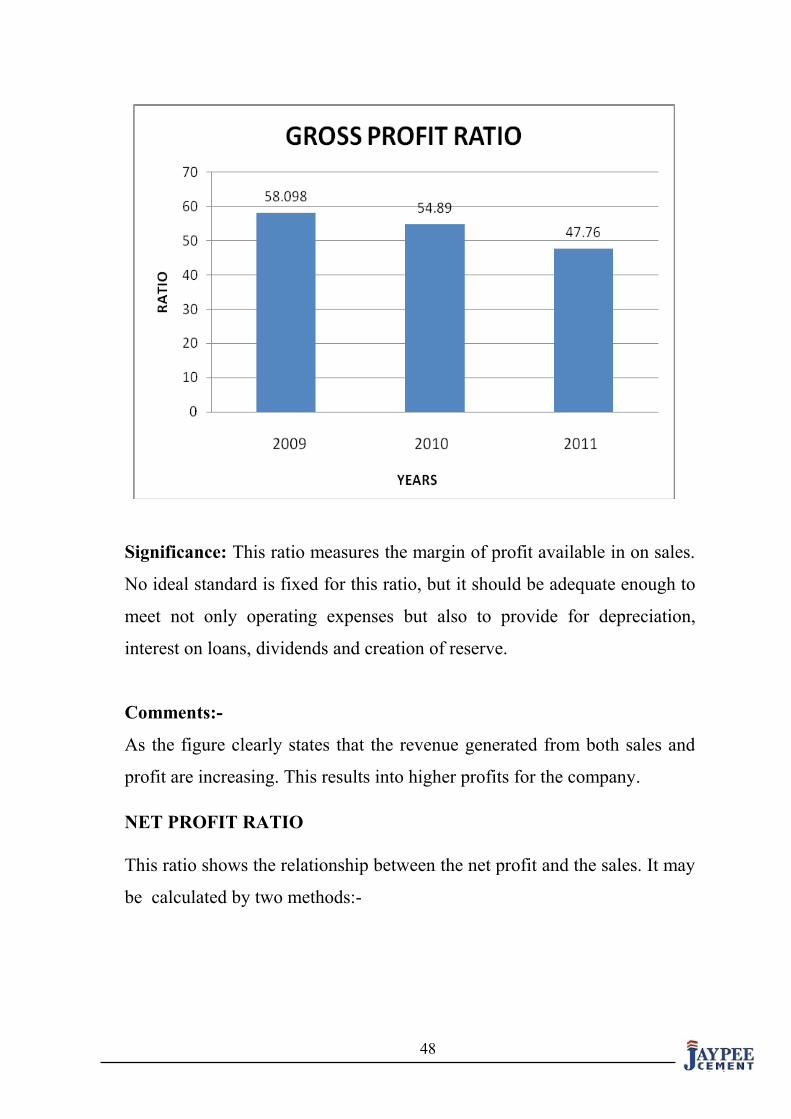

GROSS PROFIT RATIO

The ratio shows the relationship between gross profit and sales.

Gross ProfitGross Profit Ratio = * 100

Net Sales

Net Sales = Gross revenue – Excise duty

23176228489For the year ending (2010-2011) = *100 = 47.76 %

48520571504

19436337237For the year ending (2009-2010) = *100 = 54.89 %

35403563785

12757686068For the year ending (2008-2009) = *100 = 58.098 %

21958565845

47

Significance: This ratio measures the margin of profit available in on sales.

No ideal standard is fixed for this ratio, but it should be adequate enough to

meet not only operating expenses but also to provide for depreciation,

interest on loans, dividends and creation of reserve.

Comments:-

As the figure clearly states that the revenue generated from both sales and

profit are increasing. This results into higher profits for the company.

NET PROFIT RATIO

This ratio shows the relationship between the net profit and the sales. It may

be calculated by two methods:-

48

Net Profit(a) Net Profit Ratio = * 100

Net Sales

3144921045For the year ending (2010-2011) = * 100 = 6.48 % 48520571504

7482523916For the year ending (2009-2010) = *100 = 21.1 %

35403563785

6143316501For the year ending (2008-2009) = *100 = 27.95 %

21958565485

helps in determining the overall efficiency of the business operations. An

increase in the ratio over the previous shows improvement in the overall

efficiency and profitability of the business.

49

Comments:-

The net profit ratio shows a decrease because the operating expenses have

increased in comparison to past year. So they should keep a watch on their

operating activities and try to reduce the expenditure incurred on them.

As the figure clearly states that the revenue generated from sales is

increasing but the profit is going down by few digits because of increase in

operational activities. But still the ratio of the current year is quite

significant but this continuous decrease in the ratio might be problematic.

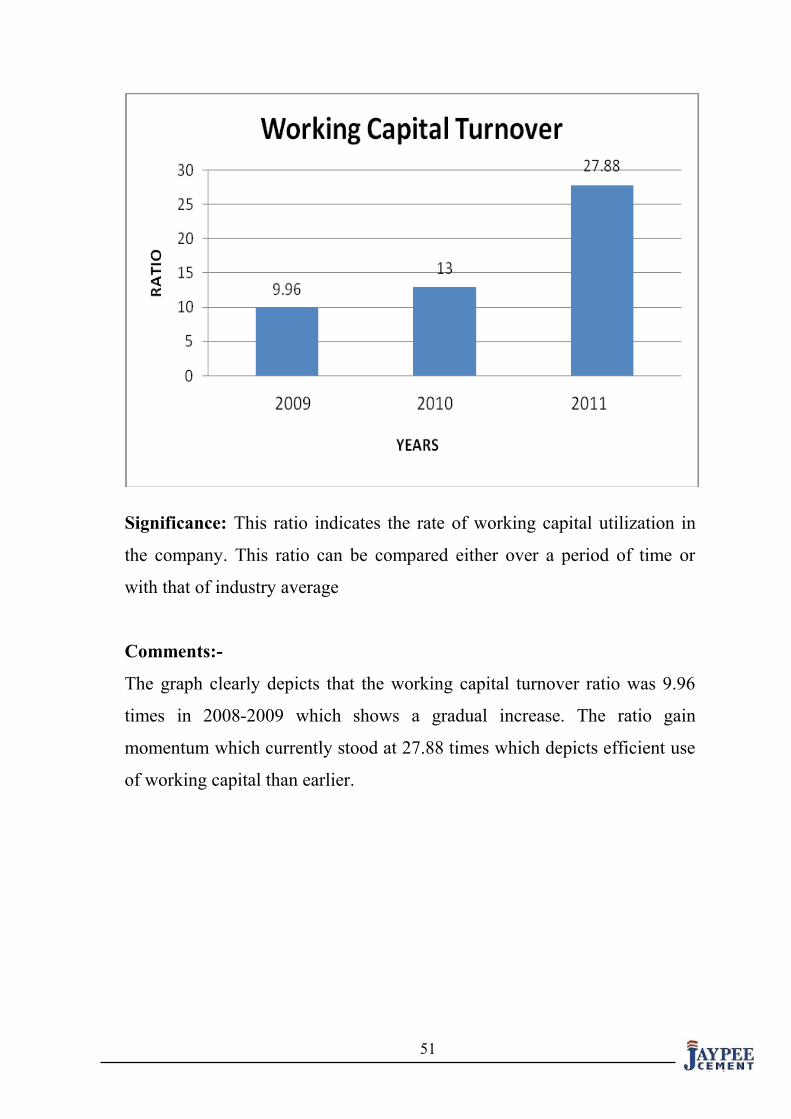

WORKING CAPITAL TURNOVER RATIO

Working capital turnover indicates the rate of working capital utilization in

the company. This ratio can be compared either over a period of time or

with that of industry average

Net sales Working capital turnover ratio = Working capital

Working capital = Current Assets - Current Liabilities

21958565845For the year ending (2008-2009) = = 9.96 times.

2203284070

35403563785For the year ending (2009-2010) = = 13 times.

2722292973

48520571504For the year ending (2010-2011) = = 27.88 times.

1739952913

.

50

Significance: This ratio indicates the rate of working capital utilization in

the company. This ratio can be compared either over a period of time or

with that of industry average

Comments:-

The graph clearly depicts that the working capital turnover ratio was 9.96

times in 2008-2009 which shows a gradual increase. The ratio gain

momentum which currently stood at 27.88 times which depicts efficient use

of working capital than earlier.

51

Ratios of operating cycle:

Operating cycle of the company

The entire sequence of operations in a company can be

summarized as follows:

• The operating cycle for a company primarily begins with the purchase

of raw materials, which are paid for after a delay representing the

creditor's payable period.

• These purchased raw materials are then converted by the production

unit into finished goods and then sold. The time lag between the

purchase of raw materials and the sale of finished goods is known as

the inventory period.

• Upon sale of finished goods on credit terms, there exists a time lag

between the sale of finished goods and the collection of cash on sale.

This period is known as the accounts receivables period.

52

RAW MATERIAL CONVERSION PERIOD

11.71

21.06

13.03

0

5

10

15

20

25

1 2 3

YEAR

RA

TIO

SRaw material conversion period: Raw material inventory * 365 Raw material conversion period = Raw material consumption

70710592.77 * 360For the year ending (2008-2009) = = 11.8 days

2173747305

239033379* 360For the year ending (2009-2010) = = 21.06 days

2722292973 229265138* 360

For the year ending (2010-2011) = = 13.03 days. 6330718841.

Comments:-

The graph clearly depicts that the raw material conversion period was

11.71 days in 2008-2009 which shows a gradual increase. The ratio gain

momentum which currently stood at 13.03 days.

53

2009 2010 2011

Work in process conversion period:

Work in progress inventory * 360 Work in progress = Cost of goods sold

975694875*360

For the year ending (2008-2009) = = 28.44 days 12521318155

975694875*360For the year ending (2009-2010) = = 18.35 days

19135687722 2364032473* 360

For the year ending (2010-2011) = = 34.04 days. 25344343016

Comments:-

The graph clearly depicts that the work in process was 28.44 days in 2008-

2009 and then it declines to 18.35. The ratio gain momentum which

currently stood at 34.04 days.

Finished goods inventory conversion period:

54

WORK IN PROCESS

28.44

18.35

34.04

0

1020

30

40

1 2 3

YEAR

RA

TIO

S

2009 2010 2011

FINISHED GOODS INVENTORY

9.23

24.98 26.21

0

10

20

30

1 2 3

YEAR

RA

TIO

S Finished goods inventory * 360 Finished goods = Cost of goods sold

316863358*360For the year ending (2008-2009) = = 9.23 days

12521318155

1327961605*360For the year ending (2009-2010) = = 24.98 days

19135687722

1845425365* 360For the year ending (2010-2011) = = 26.21 days.

25344343016

Comments:-

The graph clearly depicts that the finished goods inventory was 9.23 days in

2008-2009 and then it comes to 24.98 which shows a gradual increase. The

ratio gain momentum which currently stood at 26.21 days.

Debtor conversion period:

debtors * 360

55

2009 2010 2011

DEBTORS CONVERSION PERIOD

5.287.68

10.89

0

5

10

15

1 2 3

YEAR

RA

TIO

S

Debtor conversion period = Credit sales

317844444*360For the year ending (2008-2009) = = 5.28 days

21958565845

841866444*360For the year ending (2009-2010) = = 7.68 days

39430701026

1448699776* 360For the year ending (2010-2011) = = 10.89 days. 48520571504

.

Comments:-

The graph clearly depicts that the debtors’ conversion period was 5.28 days

in 2008-2009 and then it comes to 7.68 which shows a gradual increase. The

ratio gain momentum which currently stood at 10.89 days.

Gross operating cycle:

56

2009 2010 2011

GROSS OPERATING CYCLE

49.3

64.873.3

0

20

40

60

80

1 2 3

YEAR

DA

YS

Gross operating cycle= raw material conversion period + work in

process + finished goods conversion period.

2008-2009= 11.7 + 28.4 + 9.23 = 49.3

2009-2010= 21.6+ 18.3 +24.9= 64.8

2010-2011=13.03+ 34.04+26.21= 73.28

GRAPH PPRESENTATION

Comments- The graph clearly depicts that the gross operating cycle was

49.3 days in 2008-2009 and then it comes to 64.8 days which shows a

gradual increase. The ratio gain momentum which currently stood at 73.3

days.

Net operating cycle-

57

2009 2010 2011

NET OPERATING CYCLE

4457.1 62.4

0

20

40

60

80

1 2 3

YEAR

DA

YS

Net operating cycle also referred as cash conversion cycle.

Operating cycle is the time duration required to convert sales, after

the conversion of resources into inventories, into cash.

Net operating cycle= gross operating cycle- debtors

conversion period

2008-2009= 49.3 -5.3= 44 days

2009-2010= 64.8- 7.7= 57.1 days

201-2011= 73.3- 10.9=62.4 days

GRAPH PPRESENTATION

Comments- The graph clearly depicts that the net operating cycle was 44

days in 2008-2009 and then it comes to 57.1 days which shows a gradual

increase. The ratio gain momentum which currently stood at 62.4 days.

58

2009 2010 2011

SUGGESTIONS AND

RECOMMENDATIONS

• The Liquidity Ratio shows that the liquidator’s position of the

company is quite satisfactory. All the ratios such as the current ratio,

quick ratio and cash ratio show a satisfactory position of the

company. The company has to make full utilization of its assets.

• Leverage position of the company is good as we can see that the ratio

continuously decreases and lastly the firm is able to pay all its debt in

current year. So the firm should try to maintain it and should invest its

money in some profitable activities.

• Gross Profit ratio of the company is declining, this could be due to :-

Increase in the prices of raw material.

Increase in the manufacturing expenses.

There is fall in prices of unsold goods, there by reducing

the value of unsold goods.

• Focused attention should be paid by initiating a special drive to

expedite recoveries from sundry debtors.

59

• The Net Profit Ratio of the firm also decreases. It shows the

inefficiency and unpredictability of the business. This decline is

because of increase in expenses borne by operating activities.

CONCLUSION

Finance is the basic pillar on which the structure of industrial

undertaking is based. This pillar should be properly placed. A

good working environment and attractive incentives for the

achievement of targets has obviously created ideal conditions in

Jaypee cements for the both management and workers. Not a

single day of production has been lost this shows efficiency in

management.

In my report I have calculated some of the ratio that was very

regularly used at Jaypee group for the necessary analysis activities

performed by it from time to time. Jaypee group uses this

technique usually to check out its current functioning and to

compare its performance on regular basis with the past years.

60

This technique is useful in inter-firm analysis and to judge

once performance standard as ratio helps to set some standard

marks which the firm target to achieve in the given span of time.

BIBLIOGRAPHY

I. I. M. Pandey - Financial Management Vikas-2003

II. Annual reports – Jaypee Associates Ltd. (Cement division)

III. Company website - www.jalindia.com

IV. Websites - www.google.com

61

62

Related Documents