Workers Compensation Insurance: The Role of State Funds, Market Trends and Economic Influences October 12, 2010 Robert P. Hartwig, Ph.D., CPCU, President & Economist Insurance Information Institute 110 William Street New York, NY 10038 Tel: 212.346.5520 Cell: 917.453.1885 [email protected]

Workers Compensation Insurance: The Role of State Funds, Market Trends and Economic Influences October 12, 2010 Robert P. Hartwig, Ph.D., CPCU, President.

Jan 02, 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Workers Compensation Insurance: The Role of State Funds, Market

Trends and Economic Influences

October 12, 2010

Robert P. Hartwig, Ph.D., CPCU, President & EconomistInsurance Information Institute 110 William Street New York, NY 10038

Tel: 212.346.5520 Cell: 917.453.1885 [email protected] www.iii.org

2

Presentation Outline

The Role of Workers Compensation State Funds History Organizational Structure and Evolution Market Share Analysis Performance

Property Casualty Insurance and Workers Compensation Market Overview &Outlook Financial Overview Underwriting Trends

State of the Economy and Impacts on Employers and Workers Compensation Insurance Impacts of the “Great Recession” on Exposure & Growth

A Brief History: The Role of Workers

Compensation State Funds

3

Social Policy, History, Economics, Insurance Market Forces and Politics

All Played Important Roles in the Development of Modern WC Systems,

State Funds and Their Structure

4

Workers Compensation Timeline

Industrialization of US in the Late 19th/Early 20th Century Led to Increasing & Unacceptably High Number of Deaths and Injuries Among Workers

In 1912, an estimated 18,000 to 23,000 workers were killed on the job (compared to 5,071 in 2008) and approximately 4.7 million (12% or workforce) suffered a nonfatal illness or injury (compared to 3.7 million 2008)

The 1912 death/injury rates would imply 75,600 deaths and 17 million injuries today

More awareness of broader impacts on families of injured/killed workers

Workers Could Seek Redress Under Tort Law, But Seldom Prevailed

Employers usually won suits filed by injured workers by arguing:– Contributory Negligence: Employee was at least partially to blame for the accident– Assumed Risk: By taking the job, the employee understood the hazards involved– Fellow Servant Rule: A fellow worker caused the accident, so the employer was not at fault

European Countries Began to Implement Workers Compensation Programs

Germany (1884); England (1897)

Insurers Began to Sell Commercial Liability Coverage in the Late 1800s

Coverage for inadvertent errors became more commonplace

In the workforce, such policies became the first employer liability policies

Source: Insurance Information Institute.

5

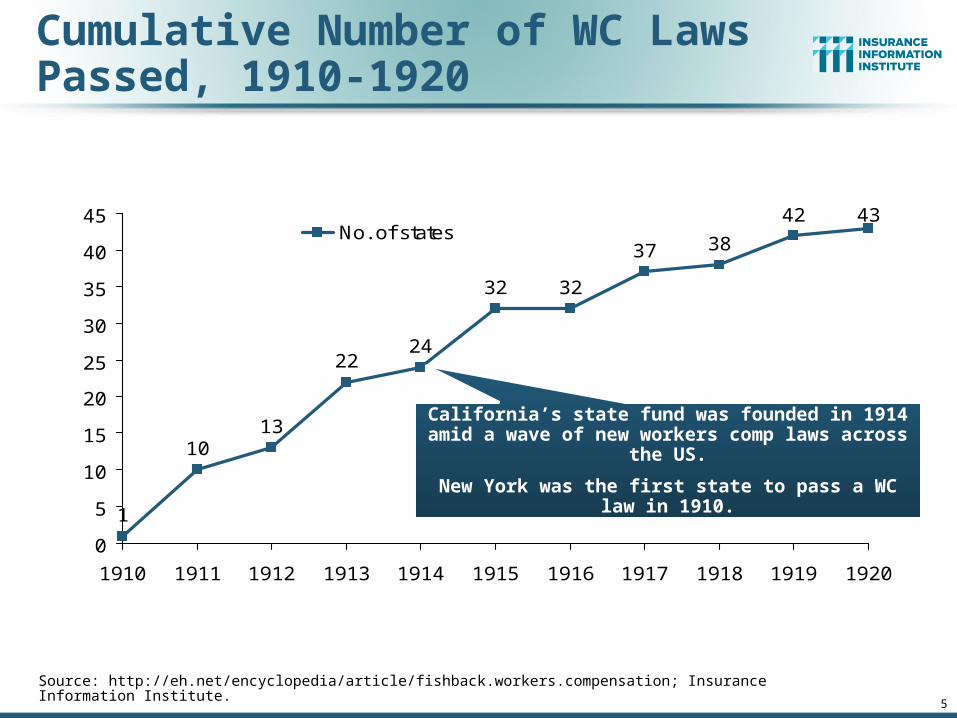

Cumulative Number of WC Laws Passed, 1910-1920

1

1013

2224

32 32

37 38

42 43

0

5

10

15

20

25

30

35

40

45

1910 1911 1912 1913 1914 1915 1916 1917 1918 1919 1920

No. of states

Source: http://eh.net/encyclopedia/article/fishback.workers.compensation; Insurance Information Institute.

California’s state fund was founded in 1914 amid a wave of new workers comp laws across the US.

New York was the first state to pass a WC law in 1910.

6

The Role of Workers Compensation State Funds: Public Policy & Economic Missions

The Core Public Policy Mission of WC State Funds is to Assure the Availability of Affordable Workers Compensation Coverage to Employers The original catalyst for WC was the recognition that the rapidly increasing number of occupational

injuries and deaths were exacting a high and unfair physical and financial toll on injured workers and their families

Prior to 1920, there was some question whether the private insurance sector could meet the demand and affordably supply this new type of coverage on its own. State funds were a tool for meeting this new public policy objective.

States adopted differing strategies for assuring this obligation was met: competitive and monopolistic state funds whereas others allowed the private sector to satisfy demand (subject to state oversight and regulation)

For the state funds formed in the late 1980s and 1990s, states sought to bring stability to a market where costs were rising rapidly and residual market shares exploding

Secondary Core Public Policy Mission: Reduce Workplace Injuries/Deaths Provision of loss control services and loss sensitive pricing help achieve this goal

Core Economic Mission: Support of the State Economy The availability of affordable WC coverage is a key consideration in many business location and

expansion decisions

This issue is likely increase in importance in the job-starved 2010s

To Operate Self-Sufficiently (i.e., Minimal Public Financial Support)

Source: Insurance Information Institute; Conning.

7

Number of Workers Comp State Funds Formed by Decade, 1910–2010

01

9

01

001

0

13

0

2

4

6

8

10

12

14

1910s 1920s 1930s 1940s 1950s 1960s 1970s 1980s 1990s 2000s**

* Nevada’s monopolistic state fund, founded in 1913, was privatized in 1999. There is currently no state fund in the state.**West Virginia’s original (monopolistic) state fund was formed in 1915. Its successor, BrickStreet Mutual, became a competitive state fund in 2006. Oregon’s original (monopolistic) fund, formed in 1914, adopted a competitive structure in 1980.Sources: Insurance Information Institute research.

Number of State Funds Formed

All But Three of the 26 State Funds Ever Formed Were Founded in the 1910s (the Decade in which Workers Comp Laws Were Put on

the Books in Most States) and the 1990s (During a Period of Massive Reform of WC Systems Countrywide)

California’s state fund was founded in 1914 amid a wave of new workers comp laws across the US. At that time, state’s were experimenting with different

systems: private, monopolistic state funds and competitive state funds

CACOID

MDNV*NYNDOH

OR**PAUTWA

WV**WY OK AZ MN

HIKYLAMEMOMTNMRITX

8

Monopolistic State Funds: Where Are they Today?

State Date started StatusOhio 1911 Still monopolistic

Washington 1911 Monopolistic; referendum sought in 2010

Nevada 1913 State fund privatized in 1999

Oregon 1913 Allowed competition in 1980

West Virginia 1913 Allowed competition in 2008

Wyoming 1915 Still monopolistic

North Dakota 1919 Still monopolistic

Source: Economic History Association, http://eh.net/encyclopedia/article/fishback.workers.compensation, Insurance Information Institute research.

9

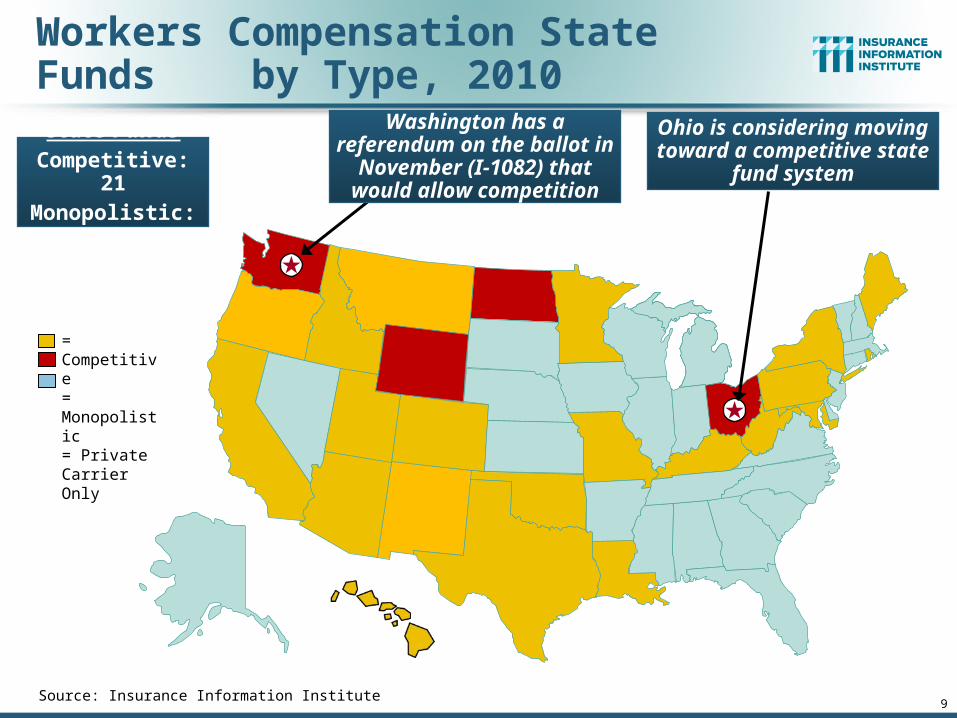

Workers Compensation State Funds by Type, 2010

Source: Insurance Information Institute

Ohio is considering moving toward a competitive state

fund systemState Funds

Competitive: 21Monopolistic: 4

= Competitive= Monopolistic= Private Carrier Only

Washington has a referendum on the ballot in

November (I-1082) that would allow competition

10

Identity Crisis: The Role of State Funds in 2010 and Beyond

The Role and Need for State Funds Is Being Questioned from Within and from Without

Two monopolistic state funds have disappeared in recent years (NV and WV); OH and WA are being challenged.

AZ will convert to a mutual structure by 2013

A number of state funds can write WC risk for companies domiciled in their home state

Several state funds now own subsidiaries that allow them to write risks with no ties to their home state (breach of core mission?)

Factors that Can Lead to Questioning of the Role of WC State Funds

Shrinking Residual Markets

Intense Private Insurer Competition

Prolonged Soft Market

Increasing Options (e.g., Captives, Large Deductible Programs)

Passage of Time Since Last WC Crisis (early 1990s)

State Budget Woes

Source: Insurance Information Institute.

11

The Curious Case of Arizona: Conversion of State Fund to a Mutual Insurer

Arizona Seems to Have Decided it Doesn’t Need a State Fund (As Did NV)

Excerpts from Arizona Senate Bill 1045 (2010 Second Regular Session)

On or before January 1, 2013, the state compensation fund board of directors, which terminates on July 1, 2012 pursuant to section 41-3012.19, Arizona Revised Statutes, shall perform all acts necessary to establish a successor mutual insurer corporation. The successor mutual insurer corporation shall operate to the same extent as any mutual casualty insurer that is licensed and authorized to write insurance in this state, subject to the authority and regulation by the department of insurance pursuant to title 28 20, chapter 4, article 1, Arizona Revised Statutes, and with all the powers and subject to all the laws, rules and requirements of a mutual insurer corporation that is organized under the laws of this state.

The successor mutual insurer corporation is not an agency of this state or a public entity of this state. The successor mutual insurer corporation shall not use the term "state compensation fund" or "SCF" in its new name or logo from and after June 30, 2014.

Source: State of Arizona; Insurance Information Institute.

Workers Compensation Premium Continues Its Sharp DeclineNet Written Premium

$ Billions

Calendar Yearp Preliminary

Source: 1990–2008 Private Carriers, Best's Aggregates & Averages; 2009p, NCCI1996–2009p State Funds: AZ, CA, CO, HI, ID, KY, LA, MD, MO, MT, NM, OK, OR, RI, TX, UT Annual Statements

State Funds available for 1996 and subsequent

13

WC Competitive State Fund Market Share,1996 – 2009p

22.4%

26.4% 25.4%

21.0%

16.9%15.2%

14.1%12.7%

18.7%

12.9%10.8%10.2%10.0%10.6%

0%

5%

10%

15%

20%

25%

30%

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Market Share (%) Private insurance markets are highly competitive. State

fund market shares have been falling steadily since 2003.

Competition, favorable underwriting trends, coverage options, private insurer innovations in risk management have all helped to make the private

sector WC insurance the most attractive option in most cases

Source: 1990–2008 Private Carriers, Best's Aggregates & Averages; 2009p, NCCI, Insurance Information Institute Market Share calculations1996–2009p State Funds: AZ, CA, CO, HI, ID, KY, LA, MD, MO, MT, NM, OK, OR, RI, TX, UT Annual Statements

State Funds available for 1996 and subsequent; p: Preliminary

14

Workers Compensation State Fund Market Shares, 2008

100.

0

100.

0

100.

0

100.

0

87.4

67.2

65.4

61.3

60.8

58.3

56.4

52.2

47.4

38.7

35.1

31.5

29.2

26.5

24.9

24.3

22.6

22.3

14.4

11.0

10.9

0

20

40

60

80

100

ND OH WA WY WV MT CO ME RI ID OR UT AZ NY OK NM TX LA MD KY CA HI MO MN PA

Sta

te F

und

Mar

ket S

hare

(%)

Source: Conning; Insurance Information Institute.

State funds market shares among the 21 competitive state funds vary widely, from nearly 90% in WV (in transition from a monopolistic to a competitive

fund market) to barely 10% in PA

15

Workers Compensation State Fund Incurred Loss Ratio, 2008

120.

6%

111.

9% 120.

6%

61.6

%

81.2

%

111.

9%

46.2

%

63.2

%

96.0

%

81.8

%

61.6

%

92.2

%

83.2

%

87.0

%

91.9

% 103.

8%

117.

1%

72.4

%

64.8

% 72.1

%

46.2

%

77.1

%

20%

40%

60%

80%

100%

120%

140%

AZ CA CO HI ID KY LA ME MD MN MO MT NM NY OK OR PA RI TX UT WV US*

Incu

rred

Los

s R

atio

(%)

Yellow bars = states where the state fund is also the market of last resort

Source: Conning; A.M. Best; Insurance Information Institute.

The average competitive workers comp state fund ran a

loss ratio of 84.2% in 2008 compared to 77.1% for the US

WC market overall

13 of the 21 competitive state funds also serve as the market of last resort

16

Comparison of State WC rates

Source: Oregon Workers’ Compensation Premium Rate Ranking 2008. Rates weighted by Oregon’s distribution of exposures by classification

WC rates, on average, do not appear to be significantly higher or lower in states with workers comp state funds

California’s WC rates are about average

P-C Insurance and Workers Compensation Overview &

Outlook

17

A Slow Motion Cyclical Turn is Underway

18

Profitability

Historically Volatile

P/C Net Income After Taxes1991–2010:H1 ($ Millions)

$1

4,1

78

$5

,84

0

$1

9,3

16

$1

0,8

70

$2

0,5

98

$2

4,4

04 $3

6,8

19

$3

0,7

73

$2

1,8

65

$3

,04

6

$3

0,0

29

$6

2,4

96

$3

,04

3

$1

6,5

31$2

8,3

11

-$6,970

$6

5,7

77

$4

4,1

55

$2

0,5

59

$3

8,5

01

-$10,000

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10:H1

2005 ROE*= 9.6% 2006 ROE = 12.7% 2007 ROE = 10.9% 2008 ROE = 0.3% 2009 ROAS1 = 5.8% 2010:H1 ROAS = 6.3%

* ROE figures are GAAP; 1Return on avg. surplus. Excluding Mortgage & Financial Guaranty insurers yields a 7.5% ROAS for 2010:H1 and 4.6% for 2009. 2009:H1 net income was $19.2 billion and $10.2 billion in 2008:H1 excluding M&FG.Sources: A.M. Best, ISO, Insurance Information Institute

P-C Industry 2010:H1 profits rose $10.6B from $6.0B in 2009:H1, due mainly to $2.2B in realized

capital gains vs. -$11.1B in previous realized capital losses

20

ROE: P/C vs. All Industries1987–2009*

* Excludes Mortgage & Financial Guarantee in 2008 and 2009.Sources: ISO, Fortune; Insurance Information Institute.

-5%

0%

5%

10%

15%

20%

87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

US P/C Insurers All US Industries

P/C Profitability IsCyclical and Volatile

Hugo

Andrew

Northridge

Lowest CAT Losses in 15 Years

Sept. 11

Katrina, Rita, Wilma

4 Hurricanes

Financial Crisis*

(Percent)

A 100 Combined Ratio Isn’t What ItOnce Was: 90-95 Is Where It’s At Now

Combined Ratio / ROE

* 2009 and 2010:Q1 figures are return on average statutory surplus. 2008, 2009 and 2010:H1figures exclude mortgage and financial guaranty insurersSource: Insurance Information Institute from A.M. Best and ISO data.

97.5

100.6 100.1 100.7

92.6

99.5 100.1101.0

7.5%7.3%

9.6%

15.9%

14.3%

12.7%

4.4%

8.9%

80

85

90

95

100

105

110

1978 1979 2003 2005 2006 2008* 2009* 2010:H1*0%

3%

6%

9%

12%

15%

18%

Combined Ratio ROE*

Combined Ratios Must Be Lower in Today’s DepressedInvestment Environment to Generate Risk Appropriate ROEs

A combined ratio of about 100 generated a 7% ROE in 2009,10% in 2005 and 16% in 1979

P/C Insurer Impairments, 1969–20098

15

12

71

19

34

91

31

21

99

16

14

13

36

49

31 3

45

04

85

56

05

84

12

91

61

23

11

8 19

49 50

47

35

18

14 15

7 65

0

10

20

30

40

50

60

70

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

00

01

02

03

04

05

06

07

08

09

Source: A.M. Best; Insurance Information Institute.

The Number of Impairments Varies Significantly Over the P/C Insurance Cycle, With Peaks Occurring Well into Hard Markets

5 of the 11 are Florida companies (1 of these

5 is a title insurer)

24

Reasons for US P/C Insurer Impairments, 1969–2008

38.1%

14.3%8.1%

7.6%

7.9%

7.0%

9.1%

4.2%

3.7%

Source: A.M. Best: 1969-2008 Impairment Review, Special Report, Apr. 6, 2009

Deficient Loss Reserves and Inadequate Pricing Are the Leading Cause of Insurer Impairments, Underscoring the Importance of Discipline.

Investment Catastrophe Losses Play a Much Smaller Role

Deficient Loss Reserves/In-adequate Pricing

Reinsurance Failure

Rapid GrowthAlleged Fraud

Catastrophe Losses

Affiliate Impairment

Investment Problems

Misc.

Sig. Change in Business

P/C Premium Growth Primarily Driven by the

Industry’s Underwriting Cycle, Not the Economy

25

26

-5%

0%

5%

10%

15%

20%

25%

71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

10F

Soft Market Appears to Persist in 2010 but May Be Easing: Relief in 2011?

(Percent)1975-78 1984-87 2000-03

Shaded areas denote “hard market” periodsSources: A.M. Best (historical and forecast), ISO, Insurance Information Institute.

Net Written Premiums Fell 0.7% in 2007 (First Decline Since 1943) by 2.0% in 2008, and 4.2% in 2009, the First 3-Year Decline Since 1930-33.

NWP was flat with 0.0% growth in 10:H1 vs. -4.4% in 09:H1

27

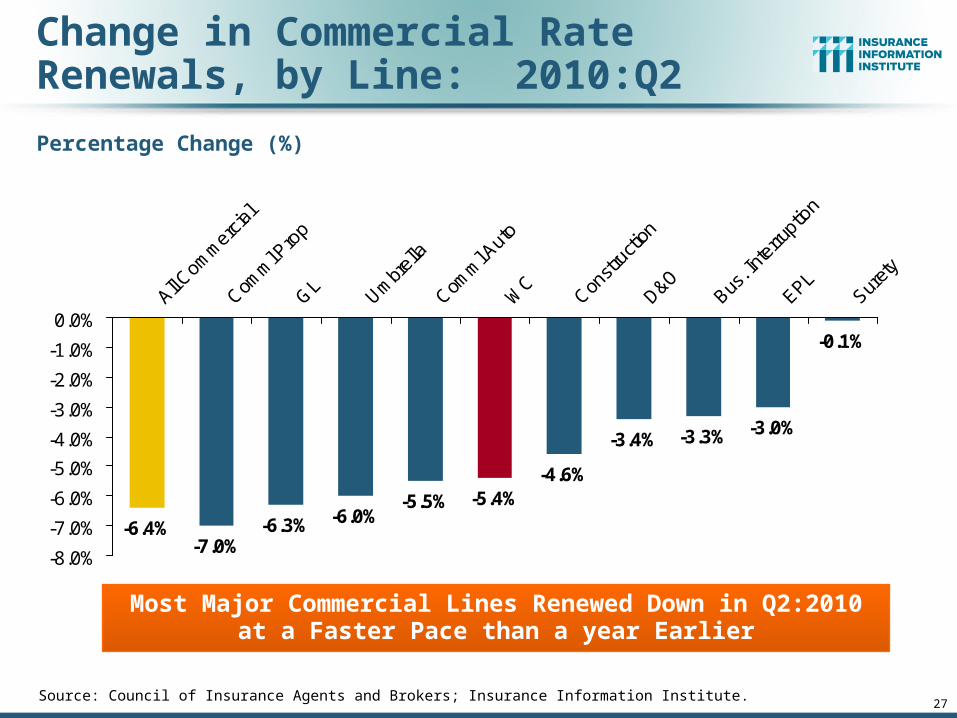

Change in Commercial Rate Renewals, by Line: 2010:Q2

Source: Council of Insurance Agents and Brokers; Insurance Information Institute.

Most Major Commercial Lines Renewed Down in Q2:2010 at a Faster Pace than a year Earlier

Percentage Change (%)

-4.6%

-3.4% -3.3% -3.0%

-0.1%

-6.4%-7.0%

-6.3% -6.0%-5.5% -5.4%

-8.0%

-7.0%

-6.0%

-5.0%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%All C

omm

ercia

l

Comm

l Pro

p

GL

Umbr

ella

Comm

l Aut

o

WC

Const

ructi

on

D&OBus

. Int

erru

ptio

n

EPLSur

ety

28

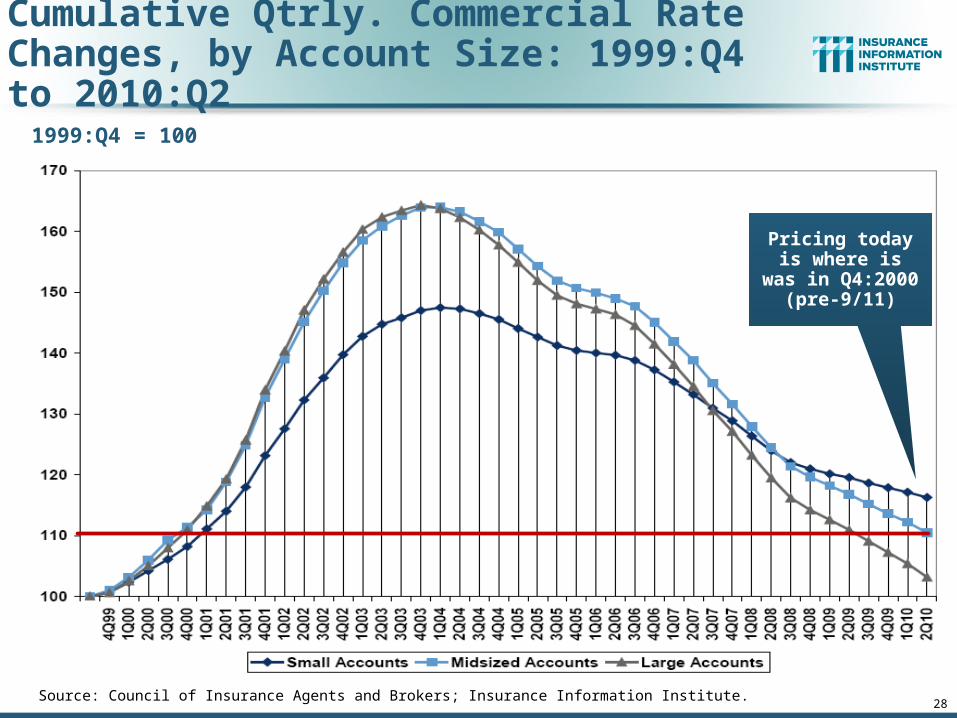

Cumulative Qtrly. Commercial Rate Changes, by Account Size: 1999:Q4 to 2010:Q2

Source: Council of Insurance Agents and Brokers; Insurance Information Institute.

1999:Q4 = 100

Pricing today is where is was in

Q4:2000 (pre-9/11)

Net Written Premium Growth Forcasts by Line: 2010 - 2012

Source: Conning, Second Quarter 2010 forecast.

Line 2010F 2011F 2012FAll Lines 1.8% 5.0% 5.4%

Personal Auto 3.1 5.2 5.0

Homeowners 4.7 5.2 5.0

Workers Comp -4.0 5.5 10.0

Commercial Auto 1.5 8.1 6.9

Commercial Multiperil 1.5 6.3 7.3

General Liability 1.3 5.8 5.8

Inland Marine 2.0 4.5 5.0

Capital/PolicyholderSurplus (US)

30

Shrinkage, but Not Enoughto Trigger Hard Market

31

Policyholder Surplus, 2006:Q4–2010:Q2

Sources: ISO, A.M .Best.

($ Billions)

$487.1$496.6

$512.8$521.8

$478.5

$455.6

$437.1

$463.0

$490.8

$511.5

$540.7$530.5

$505.0$515.6$517.9

$420

$440

$460

$480

$500

$520

$540

$560

06:Q4 07:Q1 07:Q2 07:Q3 07:Q4 08:Q1 08:Q2 08:Q3 08:Q4 09:Q1 09:Q2 09:Q3 09:Q4 10:Q1 10:Q2

2007:Q3Previous Surplus Peak

Quarterly Surplus Changes Since 2009:Q1 Trough

09:Q1: -$84.7B (-16.2%) 09:Q2: -$58.8B (-11.2%)09:Q3: -$31.8B (-5.9%)09:Q4: -$10.3B (-2.0%)

10:Q1: +$18.9B (+3.6%)10:Q2: -$10.2B (-1.9%)

Surplus set a new record in 2010:Q1*

*Includes $22.5B of paid-in capital from a holding company parent for one insurer’s investment in a non-insurance business

Investment Performance

32

Investments Are a PrincipleSource of Declining Profitability

Property/Casualty Insurance Industry Investment Gain: 1994–2010:H11

$35.4

$42.8$47.2

$52.3

$44.4

$36.0

$45.3$48.9

$59.4$55.7

$64.0

$31.7

$39.0

$25.8

$58.0

$51.9$56.9

$0

$10

$20

$30

$40

$50

$60

$70

94 95 96 97 98 99 00 01 02 03 04 05* 06 07 08 09 10:H1In 2008, Investment Gains Fell by 50% Due to Lower Yields and

Nearly $20B of Realized Capital Losses 2009 Saw Smaller Realized Capital Losses But Declining Investment Income

Investment Gains Are Recovering So Far in 20101 Investment gains consist primarily of interest, stock dividends and realized capital gains and losses.* 2005 figure includes special one-time dividend of $3.2B.Sources: ISO; Insurance Information Institute.

($ Billions) 2009:H1 gain was $12.5B

Investment gains in 2010 are on track to be their best since 2007

34

-1.8

%

-1.8

%

-2.0

%

-3.6

%

-3.3

%

-3.3

%

-3.7

%

-4.3

%

-5.2

%

-5.7

%

-7.3%

-1.9

%

-2.1

%

-3.1

%

-8%-7%-6%-5%-4%-3%-2%-1%0%

Perso

nal L

ines

Pvt Pass

Aut

o

Pers P

rop

Comm

ercia

l

Comm

l Auto

Credit

Comm

Pro

p

Comm

Cas

Fidelity

/Sure

ty

War

rant

y

Surplu

s Line

s

Med

Mal

WC

Reinsu

ranc

e**

Lower Investment Earnings Place a Greater Burden on Underwriting and Pricing Discipline

*Based on 2008 Invested Assets and Earned Premiums**US domestic reinsurance onlySource: A.M. Best; Insurance Information Institute.

Reduction in Combined Ratio Necessary to Offset 1% Decline in Investment Yield to Maintain Constant ROE, by Line*

35

Underwriting Trends – Financial Crisis Does Not

Directly Impact Underwriting Performance: Cycle, Catastrophes

Were 2008’s Drivers

36

P/C Insurance Industry Combined Ratio, 2001–2010:H1*

* Excludes Mortgage & Financial Guaranty insurers in 2008, 2009 and 2010. Including M&FG, 2008=105.1, 2009=100.7, 2010:H1=101.7 Sources: A.M. Best, ISO.

95.7

99.3 100.1101.0

92.6

100.898.4

100.1

107.5

115.8

90

100

110

120

2001 2002 2003 2004 2005 2006 2007 2008 2009* 2010:H1

Best Combined

Ratio Since 1949 (87.6)

As Recently as 2001, Insurers Paid Out

Nearly $1.16 for Every $1 in Earned

Premiums

Relatively Low CAT Losses, Reserve Releases

Cyclical Deterioration

Heavy Use of Reinsurance Lowered Net

Losses

Relatively Low CAT Losses, Reserve Releases

Lower CAT

Losses, More

Reserve Releases

37

2.3

-2.1

-8.3

-2.6-6.6

-9.9 -9.8

-4.1

1

11.7

23.2

13.79.9

7.3

-6.7-9.5

-14.6-16 -15

-5

-$20

-$15

-$10

-$5

$0

$5

$10

$15

$20

$25

$309

2

93

94

95

96

97

98

99

00

01

02

03

04

05

06

07

08

09

10

E

11

E

Pri

or

Yr.

Re

se

rve

Re

lea

se

($

B)

-6

-4

-2

0

2

4

6

8 Imp

ac

t on

Co

mb

ine

d R

atio

(Po

ints

)

Prior Yr. ReserveDevelopment ($B)

Impact onCombined Ratio(Points)

P/C Reserve Development, 1992–2011E

Reserve Releases Are Continuing Strong in 2010 But Should Begin to Taper Off in 2011

Note: 2005 reserve development excludes a $6 billion loss portfolio transfer between American Re and Munich Re. Including this transaction, total prior year adverse development in 2005 was $7 billion. The data from 2000 and subsequent years excludes development from financial guaranty and mortgage insurance. Sources: Barclay’s Capital; A.M. Best.

Prior year reserve releases totaled $8.8 billion in the

first half of 2010, up from $7.1 billion in

the first half of 2009

Workers Compensation Operating Environment

38

The Weak Economy and Soft Market Have Made the Workers Comp Operating

Increasingly Challenging

Workers Compensation Combined Ratio: 1973–2012P

96

.8 99

.91

01

.1 10

4.2

10

3.6

99

.49

6.4

10

1.4

10

2.8

10

3.9

11

2.5

12

1.9

11

8.8

12

1.1

11

7.6

11

8.4

11

8.2

11

7.4 12

2.6

12

1.5

10

9.1

10

2.0

97

.0 10

0.0

10

1.0

10

7.0

11

5.3 11

8.2

12

1.7

11

0.9

11

0.0

10

7.0

10

2.7

98

.41

03

.51

04

.31

09

.81

16

.01

17

.01

17

.0

80

85

90

95

100

105

110

115

120

125

73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11P

Workers Comp Underwriting Results Are Deteriorating Markedly

Sources: A.M. Best; Insurance Information Institute.

$ Billions

Calendar Year

2

5

10

15

1820

21

18

15

12

6

99

42

0

5

10

15

20

25

30

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

2009 Tabular Discount Is $5.3 Billion

Considers all reserve discounts as deficienciesLoss and LAE figures are based on NAIC Annual Statement data for each valuation date and NCCI latest selectionsSource: NCCI analysis

WC Loss and LAE Reserve Deficiency: Private Carriers

Calendar Year Reserve Deficiency Increased in 2009

Workers Compensation Medical & Indemnity Claim Cost Trends

41

Rising Medical Costs Exert Pressure While Indemnity Costs Rise Well Ahead of

Wage Inflation

$8.5 $8.6 $8.4$9.2 $9.6$10.3

$11.4$12.3

$13.6$14.6

$16.6$18.0

$19.2$20.3

$21.9$23.0

$24.3$25.9

$27.2

$5

$10

$15

$20

$25

$30

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09p

Annual Change 1991–1993: +1.9%Annual Change 1994–2001: +8.9%Annual Change 2002-2009: +6.6%

Accident Year

MedicalClaim Cost ($000s)

2009p: Preliminary based on data valued as of 12/31/20091991-2008: Based on data through 12/31/2008, developed to ultimateBased on the states where NCCI provides ratemaking services; Excludes the effects of deductible policies

Cumulative Change = 224%(1993-2009p)

Workers Comp Medical Claim Costs Continue to Rise

4.5%

3.5%2.8%

3.2% 3.5%4.1%

4.6% 4.7%4.0%

4.4% 4.2% 4.0%4.4%

3.7% 3.4%

5.1%

7.4%

10.1%

8.3%

10.6%

7.3%

13.5%

8.8%

7.3%

5.6%

7.4%

5.4% 5.4%

6.7%

5.0%

0%

2%

4%

6%

8%

10%

12%

14%

16%

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Change in Medical CPI

Change Med Cost per Lost Time Claim

WC Medical Severity Risingat Twice the Medical CPI Rate

Sources: Med CPI from US Bureau of Labor Statistics, WC med severity from NCCI based on NCCI states.

Average annual increase in WC medical severity form 1995 through 2009 was nearly twice the medical CPI (7.6% vs.

3.9%). New healthcare reform legislation is unlikely to have any

impact on the gap.

WC Insurers Experience Inflation More Intensely than 2009 CPI Suggests

Source: Bureau of Labor Statistics; Insurance Information Institute.

2.7%

1.8%

6.9%

3.0% 3.0%3.4%

3.1%3.4%

0%

2%

4%

6%

8%

Overall CPI "Core" CPI HospitalServices

Physicians'Services

DentalServices

PrescriptionDrugs

Medical CareCommodities

Medical CPI

(Percent increase Dec 08 to Dec 09)

Healthcare Costs Are a Major WC Insurance Cost Driver. They AreLikely to Increase Faster than the CPI for the Next Few Years, at Least

44

Excludes Food and Energy

Inpatient Services Rose 6.7%;

Outpatient Services Rose 7.4%

45

Workers Compensation Lost-Time Claim Frequency Continues to Decline*

-4.4

%

0.3

%

-6.5

%

-4.5

%

0.5

%

-3.9

%

-2.3

%

-4.5

%

-6.9

%

-4.5

%

-4.1

%

-3.7

%

-6.6

%

-6.2

%

-3.0

%

-3.4

%

-4.0

%

-9.2

%

-4.2

%

-10%

-8%

-6%

-4%

-2%

0%

2%

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09P

(Percent) Lost-Time Claims

Claim frequency fell in 4.0% in 2009, in part due to the recession

Cumulative Change of -54.7%

(1991 – 2008)

2009p: Preliminary based on data valued as of 12/31/2009; *Frequency is defined as the number of lost-time claims per 100,000 workers.1991-2008: Based on data through 12/31/2008, developed to ultimateBased on the states where NCCI provides ratemaking services including state funds; Excludes the effects of deductible policies

Med Costs Share of Total Costs is Increasing Steadily

Indemnity53%

Medical47%

Source: NCCI (based on states where NCCI provides ratemaking services).

Indemnity48%

Medical52%

Indemnity42%

Medical58%1989

1999

2009p

WC Med Cost Will Equal 2/3 of Total by 2019 if Trends Hold

Source: Insurance Information Institute.

Indemnity33%

Medical67%

2019 Estimate

This trend will likely be

supported by the increased labor

force participation of workers age 55

and older.

Indemnity Claim Cost Trends

48

Indemnity Costs Continue to Rise at a Pace Above Wage Inflation

$1

0.0

$9

.7

$9

.4

$9

.9

$1

0.1

$1

0.7

$1

1.5

$1

2.5

$1

3.8

$1

5.3

$1

6.7

$1

7.3

$1

8.0

$2

2.0

$2

3.0

$2

0.8

$1

9.8

$1

8.3

$1

8.8

+5.0%

+1.0%-3.1% -2.8%+4.9%+1.7%+5.9%

+7.7%+9.0%

+10.1%

+10.1%

+9.2%+3.1%+4.1%+1.7%

+3.1%+5.0%

5

7

9

11

13

15

17

19

21

23

25

1991 1993 1995 1997 1999 2001 2003 2005 2007 2009p

IndemnityClaim Cost ($ 000s)

Annual Change 1991–1993: -1.7%Annual Change 1994–2001: +7.3%Annual Change 2002–2008: +4.0%

2009p: Preliminary based on data valued as of 12/31/20091991–2008: Based on data through 12/31/2008, developed to ultimateBased on the states where NCCI provides ratemaking servicesExcludes the effects of deductible policies

Accident Year

+4.5

Workers Comp Indemnity Claim Costs Continue to Grow

+5.8

4.2%

5.2%5.6%

4.7%

6.3%

2.3%

1.1%

2.7%

1.7%

4.7% 4.6%

2.3%

5.9%

7.7%

9.0%

10.1%

4.1%

1.7%

3.1%

5.0% 5.0%5.8%

4.5%

-1.0%

3.5%

3.6%

1.7%

10.1%

9.2%

3.1%

-2%

0%

2%

4%

6%

8%

10%

12%

1995 1997 1999 2001 2003 2005 2007 2009p

Change in CPS Wage Change in Indemnity Cost per Lost-Time Claim

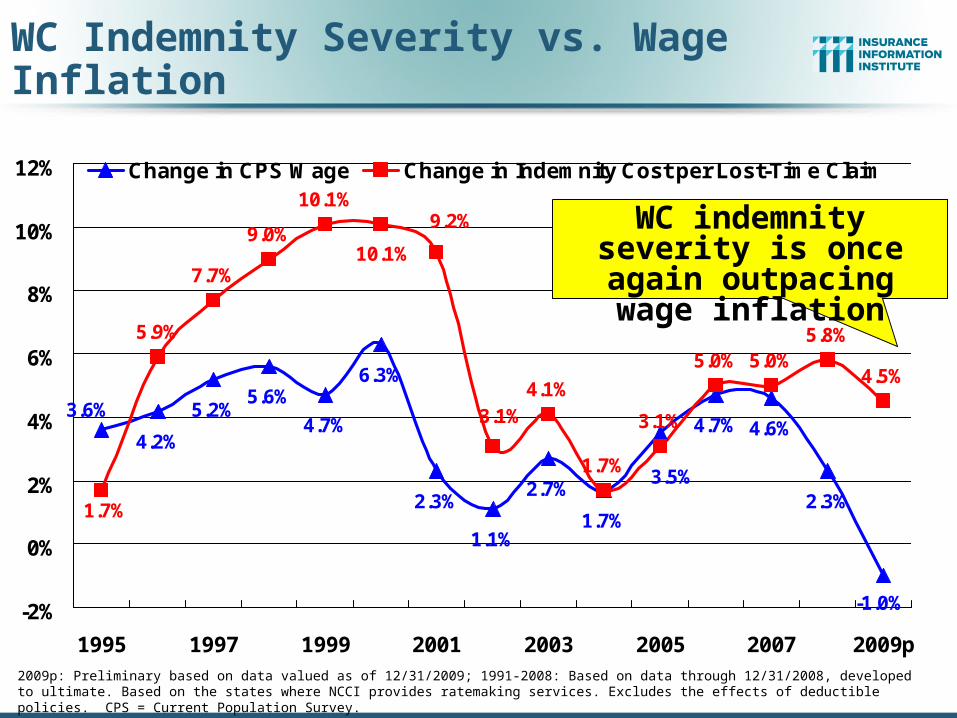

WC Indemnity Severity vs. Wage Inflation

2009p: Preliminary based on data valued as of 12/31/2009; 1991-2008: Based on data through 12/31/2008, developed to ultimate. Based on the states where NCCI provides ratemaking services. Excludes the effects of deductible policies. CPS = Current Population Survey.Source: NCCI

WC indemnity severity is once again outpacing

wage inflation

51

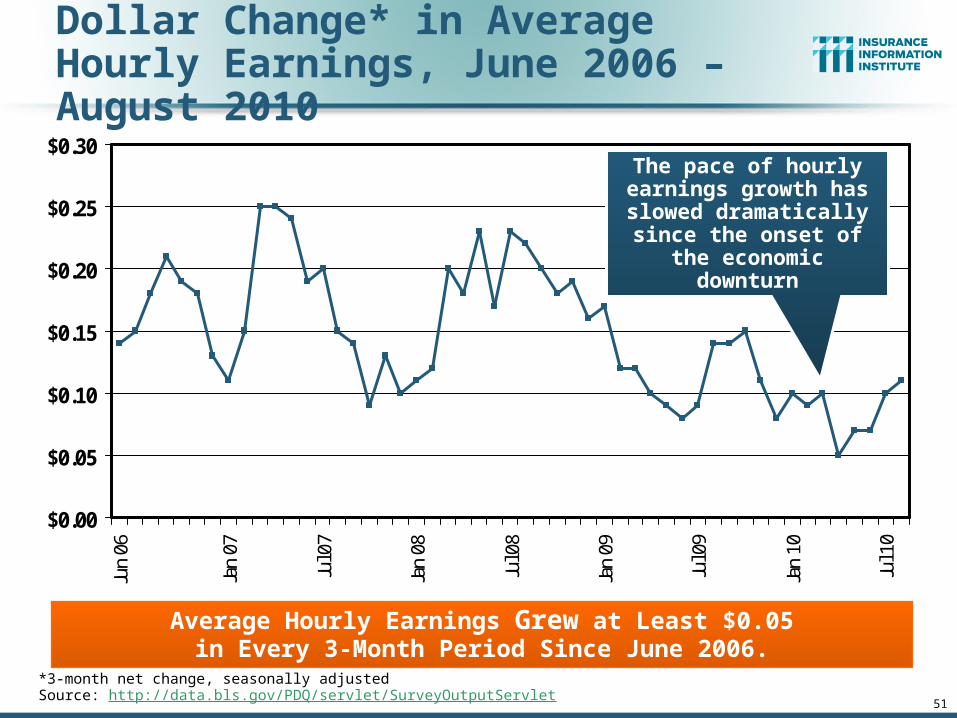

Dollar Change* in Average Hourly Earnings, June 2006 – August 2010

$0.00

$0.05

$0.10

$0.15

$0.20

$0.25

$0.30Ju

n 06

Jan

07

Jul 0

7

Jan

08

Jul 0

8

Jan

09

Jul 0

9

Jan

10

Jul 1

0

*3-month net change, seasonally adjustedSource: http://data.bls.gov/PDQ/servlet/SurveyOutputServlet

Average Hourly Earnings Grew at Least $0.05in Every 3-Month Period Since June 2006.

The pace of hourly earnings growth has

slowed dramatically since the onset of the

economic downturn

52

Total Wages, California2001-2009

$619.15 $614.54$630.69

$667.52

$703.99

$749.50

$790.44 $797.79

$753.97

$518

.60

$508

.16

$521

.08

$555

.40

$588

.32

$627

.54

$659

.99

$661

.15

$618

.17

$400

$450

$500

$550

$600

$650

$700

$750

$800

$850

2001 2002 2003 2004 2005 2006 2007 2008 2009p

All Employers Private Employers

Source: http://data.bls.gov

Recessions Cause Payrolls to Shrink. The 2001 Recession Saw a 2.0% Decline in Private Wages; the 2008-09 Dropoff was 6.3%.

Billions

Wages fallen sharply in hard hit

states like California

Where Will the Growth in WC Exposure Come From?

53

Industry and Occupation Growth Analysis

54

Fastest Growing Occupations, 2008–2018:Health/Science/Tech Dominate

Sources: US Bureau of Labor Statistics: Occupational Outlook Handbook, 2010-2011 Edition; Insurance Information Institute

OccupationsPercent change

Number of

new jobs(in thousands)

Wages (May 2008 median) Education/training category

Biomedical engineers 72 11.6 $ 77,400 Bachelor's degree

Network systems and data communications analysts

53 155.8 71,100 Bachelor's degree

Home health aides 50 460.9 20,460 Short-term on-the-job training

Personal and home care aides 46 375.8 19,180 Short-term on-the-job training

Financial examiners 41 11.1 70,930 Bachelor's degree

Medical scientists, except epidemiologists

40 44.2 72,590 Doctoral degree

Physician assistants 39 29.2 81,230 Master's degree

Skin care specialists 38 14.7 28,730 Postsecondary vocational award

Biochemists and biophysicists 37 8.7 82,840 Doctoral degree

Athletic trainers 37 6.0 39,640 Bachelor's degree

Physical therapist aides 36 16.7 23,760 Short-term on-the-job training

Dental hygienists 36 62.9 66,570 Associate degree

Veterinary technologists and technicians

36 28.5 28,900 Associate degree

Dental assistants 36 105.6 32,380 Moderate-term on-the-job training

Computer software engineers, applications

34 175.1 85,430 Bachelor's degree

Medical assistants 34 163.9 28,300 Moderate-term on-the-job training

Physical therapist assistants 33 21.2 46,140 Associate degree

Veterinarians 33 19.7 79,050 First professional degree

Self-enrichment education teachers

32 81.3 35,720 Work experience in a related occupation

Compliance officers, except agriculture, construction, health and safety, and transportation

31 80.8 48,890 Long-term on-the-job training

SOURCE: BLS Occupational Employment Statistics and Division of Occupational Outlook

WC exposure growth the fastest in the health, science and tech areas

55

Occupations with Largest Numerical Growth, 2008–2018: Health, Services Dominate

Sources: US Bureau of Labor Statistics: Occupational Outlook Handbook, 2010-2011 Edition; Insurance Information Institute

Dollar growth in WC exposures should grow the most (at current rate levels) in the health and services industries

Occupations

Number of

new jobs(in thousands) Percent change

Wages (May 2008 median) Education/training category

Registered nurses 581.5 22 $ 62,450 Associate degree

Home health aides 460.9 50 20,460 Short-term on-the-job training

Customer service representatives 399.5 18 29,860 Moderate-term on-the-job training

Combined food preparation and serving workers, including fast food

394.3 15 16,430 Short-term on-the-job training

Personal and home care aides 375.8 46 19,180 Short-term on-the-job training

Retail salespersons 374.7 8 20,510 Short-term on-the-job training

Office clerks, general 358.7 12 25,320 Short-term on-the-job training

Accountants and auditors 279.4 22 59,430 Bachelor's degree

Nursing aides, orderlies, and attendants

276.0 19 23,850 Postsecondary vocational award

Postsecondary teachers 256.9 15 58,830 Doctoral degree

Construction laborers 255.9 20 28,520 Moderate-term on-the-job training

Elementary school teachers, except special education

244.2 16 49,330 Bachelor's degree

Truck drivers, heavy and tractor-trailer

232.9 13 37,270 Short-term on-the-job training

Landscaping and groundskeeping workers

217.1 18 23,150 Short-term on-the-job training

Bookkeeping, accounting, and auditing clerks

212.4 10 32,510 Moderate-term on-the-job training

Executive secretaries and administrative assistants

204.4 13 40,030 Work experience in a related occupation

Management analysts 178.3 24 73,570 Bachelor's or higher degree, plus work experience

Computer software engineers, applications

175.1 34 85,430 Bachelor's degree

Receptionists and information clerks

172.9 15 24,550 Short-term on-the-job training

Carpenters 165.4 13 38,940 Long-term on-the-job trainingSOURCE: BLS Occupational Employment Statistics and Division of Occupational Outlook

56

Occupations With Largest Numerical Growth Across the States, 2006–2016

Sources: State Occupational Projections (Long-term), http://www.projectionscentral.com/

State Occupations

Number of

new jobs Percent Change

California Retail salespersons 109,300 22

TexasCombined food preparation and serving workers, incl. fast food

88,520 33

Texas Retail salespersons 78,600 24

California Personal and home care aides 76,900 27

Texas Personal and home care aides 74,800 56

TexasCustomer service representatives

65,630 31

California Office clerks, general 63,100 15

TexasElementary school teachers, except special education

62,280 43

California Registered nurses 59,600 25

Texas Registered nurses 59,590 38

Florida Retail salespersons 55,930 20

CaliforniaCustomer service representatives

55,600 28

Texas Waiters and waitresses 53,650 31

CaliforniaCombined food preparation and serving workers, incl. fast food

53,200 25

California Waiters and waitresses 52,800 23

New York Home health aides 52,320 38

FloridaCustomer service representatives

51,830 32

California Postsecondary teachers 51,300 30

CaliforniaElementary school teachers, except special education

51,300 27

Texas Child care workers 44,230 30

Texas and California will see the most job growth through 2016, much of it

in health and retail occupations

57

The Economic Storm

What the Financial Crisis and Recession Mean for the Industry’s

Exposure Base, Growth and Profitability

58

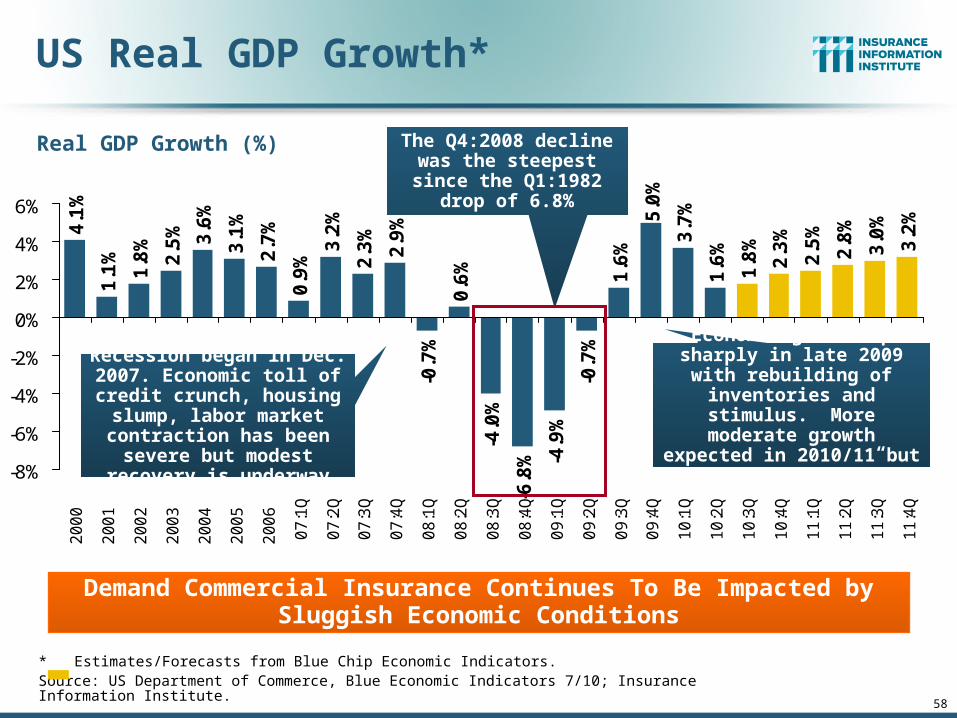

US Real GDP Growth*

* Estimates/Forecasts from Blue Chip Economic Indicators.Source: US Department of Commerce, Blue Economic Indicators 7/10; Insurance Information Institute.

2.7

%

0.9

%

3.2

%

2.3

%

2.9

%

-0.7

%

0.6

%

-4.0

%

-6.8

% -4.9

%

-0.7

%

1.6

%

5.0

%

3.7

%

1.6

%

1.8

%

2.3

%

2.5

%

2.8

%

3.0

%

3.2

%

4.1

%

1.1

%

1.8

%

2.5

% 3.6

%

3.1

%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

2

00

0

2

00

1

2

00

2

2

00

3

2

00

4

2

00

5

2

00

6

07

:1Q

07

:2Q

07

:3Q

07

:4Q

08

:1Q

08

:2Q

08

:3Q

08

:4Q

09

:1Q

09

:2Q

09

:3Q

09

:4Q

10

:1Q

10

:2Q

10

:3Q

10

:4Q

11

:1Q

11

:2Q

11

:3Q

11

:4Q

Demand Commercial Insurance Continues To Be Impacted by Sluggish Economic Conditions

Real GDP Growth (%)

Recession began in Dec. 2007. Economic toll of credit

crunch, housing slump, labor market contraction has

been severe but modest recovery is underway

The Q4:2008 decline was the steepest since the Q1:1982 drop of 6.8%

Economic growth up sharply in late 2009 with rebuilding

of inventories and stimulus. More moderate growth

expected in 2010/11 but no “double dip”

59

Length of US Business Cycles,1929–Present*

10 1116

6

168 8

19

50

80

3745

39

24

106

36

58

12

92

120

73

13

43

138 11 10 8

0

10

20

30

40

50

60

70

80

90

100

110

120

Aug1929

May1937

Feb1945

Nov1948

Jul1953

Aug1957

Apr1960

Dec1969

Nov1973

Jan1980

Jul1981

Jul1990

Mar2001

Dec2007

Month Recession Started

Contraction Expansion Following

* Through July 2010. Assumes “official” end of recession was June 2009. ** Post-WW II period through end of most recent expansion. Sources: National Bureau of Economic Research; Insurance Information Institute.

Average Duration**Recession = 10.4 MosExpansion = 60.5 Mos

Length of Expansions Greatly Exceeds

Contractions

Duration (Months)

60

State Economic Growth Varied Tremendously in 2008

US Bureau of Economic Analysis

Highest Quintile

Fourth Quintile

Third Quintile

Second Quintile

Lowest Quintile

Far West0.6

Rocky Mountain2.2

Southwest1.7

Plains2.0 Great Lakes

-0.4

New England1.0

Mideast1.3

Southeast0.0

US = 0.7

WA2.0

OR1.6

CA0.4

NV-0.6

ID0.0

MT1.8

WY4.4

UT1.4 CO

2.9

AZ-0.6 NM

2.0

TX2.0

OK2.7

KS2.2

NE1.3

SD3.5

ND7.3 MN

2.0

IA2.1

MO1.3

WI0.7

IL0.3

MI-1.5

IN-0.6

OH-0.7

NY1.6

PA1.1

NJ0.6

MD1.3

DE-1.6

DC3.0VA

1.3

WV2.5

KY-0.1

NC0.1

SC0.6

TN0.5

AR0.7

LA0.3

MS1.7

AL0.7

GA-0.6

FL-1.6

AK-2.0

HI0.7

ME1.4

NH1.8

VT1.7 MA

1.9

RI-0.9CT

-0.4

Mountain, Plains States Growing the Fastest

Percent Change in Real GDP by State, 2007–2008

61

Labor Market Trends

Massive Job Losses Sapped the Economy and Commercial/Workers

Comp Exposure, But Trend is Improving

62

Unemployment and Underemployment Rates: Rocketed Up in 2008-09; Stabilizing in 2010?

2

4

6

8

10

12

14

16

18

Jan 00 Jan 01 Jan 02 Jan 03 Jan 04 Jan 05 Jan 06 Jan 07 Jan 08 Jan 09 Jan 10

Traditional Unemployment Rate U-3

Unemployment + Underemployment Rate U-6

Aug10

Unemployment rate was 9.6% in

July

Unemployment peaked at 10.1%

in Oct. 2009, highest monthly rate since 1983.

Peak rate in the last 30 years: 10.8% in Nov -

Dec 1982

Source: US Bureau of Labor Statistics; Insurance Information Institute.

U-6 went from 8.0% in March

2007 to 17.5% in Oct 2009; Stood at 16.7% in July

2010

January 2000 through August 2010, Seasonally Adjusted (%)

Recession ended in

November 2001

Unemployment kept rising for

19 more months

Recession began in

December 2007

63

US Unemployment Rate

4.5

%

4.5

%

4.6

%

4.8

%

4.9

% 5.4

% 6.1

%

6.9

%

8.1

%

9.3

%

9.6

% 10

.0%

9.7

%

9.7

%

9.6

%

9.5

%

9.4

%

9.2

%

9.0

%9.6

%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

07

:Q1

07

:Q2

07

:Q3

07

:Q4

08

:Q1

08

:Q2

08

:Q3

08

:Q4

09

:Q1

09

:Q2

09

:Q3

09

:Q4

10

:Q1

10

:Q2

10

:Q3

10

:Q4

11

:Q1

11

:Q2

11

:Q3

11

:Q4

Rising unemployment eroded payrolls

and workers comp’s exposure base.

Unemployment likely peaked at 10% in late 2009.

* = actual; = forecastsSources: US Bureau of Labor Statistics; Blue Chip Economic Indicators (9/10); Insurance Information Institute

2007:Q1 to 2011:Q4F*

Unemployment forecasts remain stubbornly high

through 2011

64

Unemployment Rates Vary Widelyby State and Region: July 2010*

14.3

%

13.1

%

6.5%

4.7%

4.4%

3.6%

8.9%

10.6

%12.3

%

10.2

%7.

8%

6.8%

10.3

%

6.8%

9.2%

10.3

%

8.0%

6.7%7.

3%7.

2%

8.8%

8.2%

8.2%

6.9%

9.6%

0%

3%

6%

9%

12%

15%

AZ

NM TX OK ID CO UT

MT

WY

NV

CA

OR

WA MI IL O

H IN WI

MO

MN IA KS NE

SD

ND

Une

mpl

oym

ent R

ate

(%)

*Provisional figures for July 2010, seasonally adjusted.

Sources: US Bureau of Labor Statistics; Insurance Information Institute.

Southwest Mountain

Far West

Great Plains

Great Lakes

65

Unemployment Rates Vary Widelyby State and Region: July 2010* (cont’d)

11.5

%10

.8%

10.8

%9.

9%9.

9%9.

8%9.

8%9.

7%8.

6%7.

4%7.

2%7.

0%

9.7%

9.3%

8.4%

8.2%

7.1%

11.9

%9.

0%8.

9%8.

1%6.

0%5.

8%

7.7%

6.3%

0%

3%

6%

9%

12%

15%

FL MS

SC

GA KY

TN NC AL

WV AR LA VA NJ

PA DE

NY

MD RI

MA CT

ME

VT

NH

AK HI

Une

mpl

oym

ent R

ate

(%)

*Provisional figures for July 2010, seasonally adjusted.

Sources: US Bureau of Labor Statistics; Insurance Information Institute.

Southeast Mid-Atlantic New England

66

Monthly Change Employment*-7

2-1

44

-12

2-1

60

-13

7-1

61

-12

8-1

75

-32

1-3

80

-59

7-6

81

-77

9-7

26

-75

3-5

28 -3

87

-51

5 -34

6 -21

2-2

25

-22

46

4-1

09

14 39

20

8 31

3 43

2-1

75 -5

4-5

4

-1,000

-800

-600

-400

-200

0

200

400

600

Jan

08

Fe

b 0

8M

ar

08

Ap

r 0

8M

ay

08

Jun

08

Jul 0

8A

ug

08

Se

p 0

8O

ct 0

8N

ov

08

De

c 0

8Ja

n 0

9F

eb

09

Ma

r 0

9A

pr

09

Ma

y 0

9Ju

n 0

9Ju

l 09

Au

g 0

9S

ep

09

Oct

09

No

v 0

9D

ec

09

Jan

10

Fe

b 1

0M

ar

10

Ap

r 1

0M

ay

10

Jun

10

Jul 1

0A

ug

10

Monthly Losses in Dec. 08–Mar. 09 Were

the Largest in the Post-WW II Period

*Estimate based on Reuters poll of economists.Source: US Bureau of Labor Statistics: http://www.bls.gov/ces/home.htm; Insurance Information Institute

Job Losses Since the Recession Began in Dec. 2007 Peaked at 8.4 Mill in Dec. 09; Stands at 7.7 Million Through August 2010;

14.9 Million People are Now Defined as Unemployed

January 2008 through August 2010* (Thousands)

The job gain and loss figures in 2010 are severely distorted by the hiring and

termination of temporary Census workers. So far in 2010, 763,000 private sector jobs

have been created.

Estimated Effect of Recessions* on Payroll (Workers Comp Exposure)

*Data represent maximum recorded decline over 12-month period using annualized quarterly wage and salary accrual dataSource: Insurance Information Institute research; Federal Reserve Bank of St. Louis (wage and salary data); National Bureau of Economic Research (recession dates).

-4.4%

-2.0%-1.1%

1.1%

3.7%4.6%

8.5%

3.5%

2.1%

-0.5%

-3.6%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

1948-1949

1953-1954

1957-1958

1960-1961

1969-1970

1973-1975

1980 1981-1982

1990-1991

2001 2007-2009

Recessions in the 1970s and 1980s saw smaller exposure impacts

because of continued wage inflation, a factor not present

during the 2007-2009 recession

The Dec. 2007 to mid-2009 recession

caused the largest impact on WC

exposure in 60 years

(Percent Change)

(All Post WWII Recessions)

Recession Dates (Beginning/Ending Years)

68

Frequency: 1926–2009A Long-Term Drift Downward

Note: Recessions indicated by gray bars.Sources: NCCI from US Bureau of Labor Statistics; National Bureau of Economic Research.

Manufacturing – Total Recordable CasesRate of Injury and Illness Cases per 100 Full-Time Workers

Crisis-Driven Exposure Drivers

69

Economic Obstaclesto Growth in P/C Insurance,

Including Workers Compensation

70

43,6

9448

,125

69,3

0062

,436

64,0

04 71,2

77 81,2

3582

,446

63,8

5363

,235

64,8

5371

,549

70,6

4362

,304

52,3

7451

,959

53,5

4954

,027

44,3

6737

,884

35,4

7240

,099

38,5

4035

,037

34,3

1739

,201

19,6

95 28,3

2243

,546

60,8

3729

,059

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 0910

:H1

Business Bankruptcy Filings,1980-2010:H1

Source: American Bankruptcy Institute; Insurance Information Institute

Significant Exposure Implications for All Commercial Lines. There Are Some Preliminary Indications that Business

Bankruptcies Are Beginning to Decline.

There were 60,837 business bankruptcies in 2009, up 40% from 2008 and the most since 1993. 2010:H1

bankruptcies totaled 29,059, down 4% from H1:2009, but still very high by historical standards.

% Change Surrounding Recessions

1980-82 58.6%1980-87 88.7%1990-91 10.3%2000-01 13.0%2006-09 208.9%*

71

Private Sector Business Starts,1993:Q2 – 2009:Q4*

175

186

174

180

186

192

188

187 18

918

6 190 19

419

119

9 204

202

195

196

196

206

206

201

192

198

206

206

203

211

205

212

200 20

520

420

419

720

320

920

1

192

192

193

201 20

420

221

0 212

209

216 22

0 223

220

220

210

221

212

204

218

209

207

199

191 19

317

117

716

918

0

203

150

160

170

180

190

200

210

220

230

93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

Business Starts Are Down Nearly 20% in the Current Downturn, Holding Back Most Types of Commercial Insurance Exposure

*Latest available as of September 12, 2010, seasonally adjustedSource: Bureau of Labor Statistics, http://www.bls.gov/news.release/cewbd.t07.htm.

(Thousands)

180,000 businesses started in 2009:Q4, the best quarter in 2009. 2009 was the slowest year for new

business starts since 1993.

66%

68%

70%

72%

74%

76%

78%

80%

82%

Ma

r 0

1

Ju

n 0

1

Se

p 0

1

De

c 0

1

Ma

r 0

2

Ju

n 0

2

Se

p 0

2

De

c 0

2

Ma

r 0

3

Ju

n 0

3

Se

p 0

3

De

c 0

3

Ma

r 0

4

Ju

n 0

4

Se

p 0

4

De

c 0

4

Ma

r 0

5

Ju

n 0

5

Se

p 0

5

De

c 0

5

Ma

r 0

6

Ju

n 0

6

Se

p 0

6

De

c 0

6

Ma

r 0

7

Ju

n 0

7

Se

p 0

7

De

c 0

7

Ma

r 0

8

Ju

n 0

8

Se

p 0

8

De

c 0

8

Ma

r 0

9

Ju

n 0

9

Se

p 0

9

De

c 0

9

Ma

r 1

0

Ju

n 1

0

Recovery in Capacity Utilization is a Positive Sign for Insurance Exposure

Source: Federal Reserve Board statistical releases at http://www.federalreserve.gov/releases/g17/Current/default.htm. 72

Percent of Capacity Utilized (Manufacturing, Mining, Utilities)

Hurricane Katrina

March 2001-November 2001

recession

“Full Capacity”

The closer the economy is to operating at “full

capacity,” the greater the demand for insurance

Manufacturing capacity stood at

74.8% in July 2010, above the June 2009 low of 68.2% but well below the pre-crisis

peak of 80%+

Recession began December 2007

www.iii.org

Thank you for your timeand your attention!

Twitter: twitter.com/bob_hartwig

Insurance Information Institute Online:

Related Documents