www.pwc.pl Work in the European Union – taxes and social security contributions April 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

www.pwc.pl

Work in the European Union – taxes and social security contributions

April 2016

PwC

Top destinations for economic migration

in Europe: 1,901,000 people (mainly European Union countries)

Source: GUS (Polish Office of National Statistics) information on destinations and levels of temporary migration from Poland in the years 2004 to 2014

In 2004, a million people were temporary migrants: up by 132%

2,320,000 Polish people are temporary economic migrants, including:

86%

Top migration destinations:

• United Kingdom (685,000)

• Germany (614,000)

• Ireland (113,000)

• Netherlands (109,000)

• Italy (96,000)

2

PwC

Taxation of income from work – changes

• Estonia: from 21% to 20% (2015)

• Latvia: from 24% to 23% (2015)

• Hungary: from 16% to 15% (2016)

• Austria (2016): a reduction in the lowest tax rate from 36.5% to 25%; a new (temporary – until 2020) 55% tax rate for the

richest (income > EUR 1m)

• Spain (2015 and 2016): a reduction in the rates from 20-47% (in 2014) to 19-45% (in 2016)

• Netherlands (2015 and 2016): a reduction in the rates (both income tax and social security contributions) from

37%/42%/52% (in 2014) to 36.55%/40.40%/52% (in 2016)

• Ireland (2015): a reduction in the lowest rate from 41% to 40%

• Portugal (2015): the introduction of a family quotient modelled on the French tax system (with each child corresponding to

0.3)

• Greece (2015): an increase in the highest solidarity tax rate from 2.8% to 8% (for incomes > EUR 500,000)

• Estonia – an increase from EUR 1,848 EUR to EUR 2,040 (further gradual increase expected by 2018 - the tax-free

threshold is to be EUR 2,460)

• Finland – an increase from EUR 16,500 to EUR 16,700

• Germany – an increase from EUR 8,354 to EUR 8,652

• United Kingdom – an increase from about EUR 13,500 to EUR 14,100

Tax rate changes

Changes in tax-free

thresholds (2016)

Most of the changes in Europe are beneficial to taxpayers – mainly tax rate cuts (in the first instance, flat rates

or tax rates for the poorest taxpayers) and tax-free threshold increases

3

PwC

Taxation of income from work – changes (cont.)

Tax thresholds – examples of changes

Interesting facts

United Kingdom – the first tax threshold was lowered in the tax years 2014/2015 and 2015/2016 (from GBP 32,010 to GBP 31,865 and from GBP 31,865 to

GBP 31,785), only to be increased to GBP 32,000 in the tax year 2016/2017 (whereas the second tax threshold remains unchanged).

There are 18 income tax rates in place in Luxembourg!

Country The highest threshold 2015 The lowest threshold 2016 Tax rate* (%)

Sweden EUR 68,527 EUR 67,170 57

Austria EUR 60,000 EUR 90,000 50

Belgium EUR 37,300 EUR 38,080 50

Finland* EUR 90,000 EUR 72,300 31.75 (+ local district tax)

Netherlands EUR 57,585 EUR 66,421 52

Germany EUR 250,731 EUR 254,447 45

* However, the other thresholds were raised

4

PwC

Reporting of income from work – interesting facts

Ireland: it’s permitted to pay tax in 12 instalments (the total tax liability due is 105% of the original tax

liability)

Sweden: a tax return may by accepted by phone or a text message

The Provisional Tax Return is becoming more and more popular – more than a half of the member

states; Croatia (since 2015), Poland

Popularization of electronic tax returns: available in most European countries; in Greece, taxpayers

who submit their tax returns electronically are entitled to a tax allowance of 1.5% (up to EUR 118);

in Portugal, a person who submits their tax return online may do that by the end of April (rather than by

the end of March); similar arrangements are in place in the United Kingdom and Italy

Austria: late filing of a tax return may carry a penalty of 10% of the tax due

5

PwC

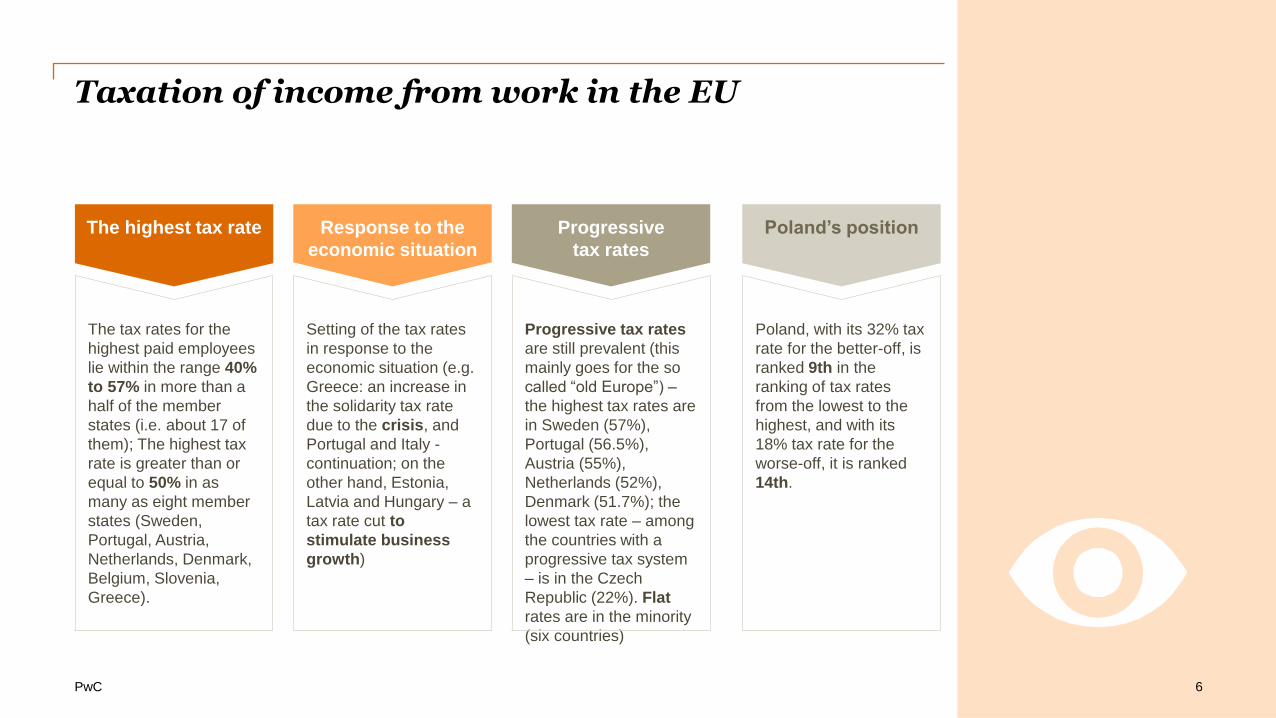

Taxation of income from work in the EU

The highest tax rate

The tax rates for the

highest paid employees

lie within the range 40%

to 57% in more than a

half of the member

states (i.e. about 17 of

them); The highest tax

rate is greater than or

equal to 50% in as

many as eight member

states (Sweden,

Portugal, Austria,

Netherlands, Denmark,

Belgium, Slovenia,

Greece).

Response to the

economic situation

Setting of the tax rates

in response to the

economic situation (e.g.

Greece: an increase in

the solidarity tax rate

due to the crisis, and

Portugal and Italy -

continuation; on the

other hand, Estonia,

Latvia and Hungary – a

tax rate cut to

stimulate business

growth)

Progressive

tax rates

Progressive tax rates

are still prevalent (this

mainly goes for the so

called “old Europe”) –

the highest tax rates are

in Sweden (57%),

Portugal (56.5%),

Austria (55%),

Netherlands (52%),

Denmark (51.7%); the

lowest tax rate – among

the countries with a

progressive tax system

– is in the Czech

Republic (22%). Flat

rates are in the minority

(six countries)

Poland’s position

Poland, with its 32% tax

rate for the better-off, is

ranked 9th in the

ranking of tax rates

from the lowest to the

highest, and with its

18% tax rate for the

worse-off, it is ranked

14th.

6

PwC

Taxation of income from work – allowances

No option for couples to file jointly: Austria, Netherlands, Cyprus, Czech Republic, Denmark, Lithuania

(with certain exceptions), Latvia, Romania, Slovenia, Hungary, Italy. Whereas in Greece, joint filing of tax

returns is (in principle) mandatory for couples

Family tax allowances (mainly child tax allowances or, to a lesser extent, joint filing for couples) are in

place in most of the countries; moreover, many countries use a wide range of other allowances (e.g.

educational, medical, commuter allowances, etc.)

Poland looks good in terms of family tax allowances (children’s allowance, joint filing for couples, joint

filing for single parents and their children), however, far worse in terms of other allowances

7

PwC

Taxation of income from work – preferences for mobile employees

8

An option to exclude a relocation package from tax (up to a certain limit: private

Austrian school tuition benefit, double-household benefit, travel to and from the

home country)

No taxation of amounts involved in travel to and from the home country and

visits paid by the spouse

We have noticed a practice of tax revenue authorities which is beneficial to

mobile employees, in respect of mobility-related income – for instance,

interpretations are issued to confirm that a refund of the employee’s travel from

the home country to the country of secondment by the employer is excluded

from the employee’s income. The same applies to a refund of housing costs,

school for children, etc.

Poland

France

Macron’s Law

(France) – seconded

employees have the

right to retain the

benefits granted to

them under the home

country’s laws even if

they change their

employer (within the

same group)

Austria

PwC

Social security contributions on remuneration

Ireland: 11 social security rates, depending on remuneration (8.50% to 10.75% for the employer and nil to 4% for the

employee)

United Kingdom: any income below GBP 7,775 a year is excluded from social security contributions; there are two social

security thresholds depending on income: in total, 25.8% and 15.8% (the lower social security contribution is applicable to

higher incomes)

Poland is positioned in the middle of the cost of labour (i.e. the employer’s contribution) ranking (it is ranked 14th from the

lowest cost to the highest cost), with the employer’s contribution of up to 22.67%.

Luxembourg: some of the lowest social security contributions (16% in total) - offset by high taxes

Social security contribution raises / cuts (2016) Belgium – a raise in the employer’s contribution from

27% to 30% (in 2015, there was a cut from 33% to 27%), Slovakia – a cut in the employer’s contribution

from 35.2% to 34.4%; Spain – a slight cut in the employer’s contribution (from 30.15% to 29.9%)

In most of the countries: total social security contributions between 30% and 40% (in a couple of them above 40%, e.g.

Slovakia, Czech Republic, Belgium; France even 60%), of which the employer’s contribution lies usually in the range 20%

to 35%

France: the employer’s contribution is as much as 45%

Usually, the employer’s contribution is higher than the employee’s contribution, the contribution basis is capped in

absolute terms, and contributions are deductible from income – this is also the case in Poland

9

PwC

Retirement age in the EU

The lowest retirement age is in Slovenia at the moment (58.4 years for women and 58.8 years for men)

The highest retirement age in the Czech Republic – even 68.4 years (in the future). The retirement age

in the United Kingdom is to be raised to 68 years.

A pension reform is also under way in Poland – the retirement age of 67 years will be reached in 2020

for men, and in 2040 for women

Retirement age: continued gradual increase in most of the countries – to 65 or 67 years

10

PwC

Conclusions Characteristics shared by most EU countries

Income tax

rates

Popular tax

allowances

Income tax

tendencies

Social security

contributions

Progressive tax rates are prevalent in European countries (with the highest tax rate usually in

the range of 40% to 50%)

There are child allowances in most of the countries, also joint filing of tax returns for couples in

about a half of the countries, many countries employ other tax allowances

Tax cuts, tax-free threshold raises and tax threshold indexation in a couple of countries

On average, about 30% to 40% of the employees remuneration; the retirement age gradually

being increased to 65 to 67 years in many countries

11

PwC

Personal income taxes are not all there is… CIT and VAT – changes (1/2)

The reduced VAT rate was raised for certain goods from 10% to 13% (effective from

1 January 2016) Austria

The CIT rate is reduced

2013 – 25%

2014 – 24.5%

2015 – 23.5%

Denmark

In January 2014, the main VAT rate was raised from 18% to 19%, and one of the reduced

rates was raised from 8% to 9% Cyprus

In 2015, a second reduced VAT rate of 10% was introduced Czech

Republic

In 2015, the CIT rate was reduced from 21% to 20% Estonia

12

PwC

Personal income taxes are not all there is… CIT and VAT – changes (2/2)

CIT rate cut: before 31 March 2015, the CIT rate was 21%. Now: 20% United

Kingdom

In 2014, the CIT rate was reduced from 24.5% to 20% Finland

Effective from 1 January 2014, the main VAT rate was raised from 19.6% to 20%, and the

reduced rate was raised from 7% to 10% France

Raise of three VAT rates: before 1 January 2015, the VAT rates was: 15%, 12%, 6%, 3%,

0%. Now: 17%, 14%, 8%, 3%, 0%. Luxembourg

The CIT rate was reduced from 30% to 25% (for the periods starting 1 January 2016 or

later) Spain

13

Romania 2016 change of VAT rates: from 24 to 20%; another

decrease planned in 2017

PwC

Tax revenue as a percentage of GDP

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Source: Taxation trends in the European Union, 2015 Edition

14

PwC

Selected taxes as a percentage of total taxation (in alphabetical order) (1/2)

Country

Indirect taxes

(VAT, excise duty, customs

duty, etc.) CIT PIT Social security contributions

Austria 34.4 5.5 23.5 34.6

Belgium 29.4 6.8 28.0 32.2

Bulgaria 55.3 6.8 10.6 25.8

Croatia 50.8 5.6 10.3 32.1

Cyprus 42.7 17.8 11.3 25.9

Czech Republic 35 9.5 10.8 44.5

Denmark 35 6.3 50.9 1.9

Estonia 43.7 4.5 16.5 35.3

Finland 33.3 5 29.4 29.8

France 34.9 5 18.8 37.9

Greece 37.6 3.3 20.6 32.1

Spain 32.9 6.6 23.8 36.8

Netherlands 30.4 5.4 19.6 41

Ireland 39.1 8.5 33.8 15.3

Source: Taxation trends in the European Union, 2015 Edition

15

PwC

Selected taxes as a percentage of total taxation (in alphabetical order) (2/2)

Country

Indirect taxes

(VAT, excise duty, customs

duty, etc.) CIT PIT Social security contributions

Lithuania 41.9 4.8 12.9 40.3

Luxembourg 33 13.4 22 29.3

Latvia 42.2 5.7 20.4 30.2

Malta 40.7 18.7 20.1 18

Germany 29.2 6.9 22.5 39.8

Poland 40.4 6.6 14.1 37.7

Portugal 42.9 8.7 18.3 28

Romania 47.2 7.6 12.3 31.2

Slovakia 36.1 8.5 9.2 44.2

Slovenia 38.8 3.4 15.6 40.5

Sweden 42.3 6.5 34.4 16.2

Hungary 47.1 3.3 13.8 33.8

United Kingdom 38.5 8.1 27.1 18.8

Italy 34.5 5.1 27.8 30.8

Source: Taxation trends in the European Union, 2015 Edition

16

Thank you!

Tomasz Barańczyk

Managing Partner

PwC, Tax and Legal Services

Phone: + 48 22 746 4852

Joanna Narkiewicz-Tarłowska

Director

PwC, Tax and Legal Services

Phone: 502 184 764

© 2016 PwC Poland Sp. z o.o.

This presentation has been prepared for general guidance only and it does not

constitute advice within the meaning of the relevant Polish laws and regulations.

You should not rely on the information contained in this presentation in your

actions/decisions without first obtaining professional advice. No warranty

(express or implied) is given as to the correctness or accuracy of the information

contained in our presentation. Moreover, to the extent permitted by the laws of

Poland, PwC Polska Sp. z o.o., its partners, employees and agents do not

assume any liability to you or accept any responsibility, contractual or otherwise,

for any losses, damage or expenditure which may be a direct or indirect

consequence of any action taken on the basis of the information contained in our

presentation or decisions taken on the basis of this presentation.

Mikołaj Woźniak

Vice Director

PwC, Tax and Legal Services

Phone: 519 507 449

PwC

Annex 1 – Personal income tax rates in the EU

18

PwC

Ranking of countries by tax rates (the highest tax bracket)*

Rank Country Tax rate (%)

1. Bulgaria 10 (flat rate)

2. Lithuania 15 (flat rate)

3. Hungary 16 (flat rate)/ from 2016 – 15

4. Romania 16 (flat rate)

5. Estonia 20

6. Czech

Republic

22

7. Latvia 23 (flat rate)

8. Slovakia 25

9. Poland 32

10. Cyprus 35

11. Malta 35

12. Croatia 40

13. Luxembourg 40

14. Ireland 40

Rank Country Tax rate (%)

15. Italy 43 (+ regional, local district and solidarity taxes depending

on income)

16. United

Kingdom

45

17. Germany 45 (plus solidarity tax at 5.5% of the tax)

18. Spain 47 / from 2016: 45

19. Finland 48 (including state and local district tax)

20. France 49

21. Greece 50 (including solidarity tax of 8%)

22. Slovenia 50

23. Belgium 50

24. Denmark 51.7 (including state and local district tax)

25. Netherlands 52

26. Austria 50 / from 2016: 55

27. Portugal 56.5 (including solidarity tax of 8.5%)

28. Sweden 57 (including state and local district tax)

* It should be borne in mind that, in addition to the tax rates themselves, what should be taken into account in fully identifying personal income tax charge on remunerations in each country are also tax thresholds,

the tax-free threshold, tax exemptions and allowances available, etc.

19

PwC

Ranking of countries by tax rates (the lowest tax bracket)

Rank Country Tax rate (%)

1. France 5,5

2. Luxembourg 8

3. Netherlands 8,4

4. Bulgaria 10 (flat rate)

5. Croatia 12

6. Germany 14 (plus solidarity tax at 5.5% of the tax)

7. Malta 15

8. Lithuania 15 (flat rate)

9. Czech

Republic

15

10. Romania 16 (flat rate)

11. Slowenia 16

12. Hungary 16 (flat rate)/ from 2016 – 15

13. Portugal 18 (including 3,5% solidarity tax)

14. Poland 18

Rank Country Tax rate (%)

15. Slovakia 19

16. Cyprus 20

17. Spain 20 / from 2016: 19

18. Ireland 20

19. United

Kingdom

20

20. Estonia 20 (flat rate)

21. Greece 22.7 (including solidarity tax of 0.7%)

22. Finland 22.75 (including state and local district tax)

23. Italy 23 (+ regional, local and solidarity taxes depending on

income)

24. Latvia 23 (flat rate)

25. Belgium 25

26. Sweden Ca. 32 (in the first tax bracket – municipial tax only)

27. Denmark Ok. 32 (including state and municipial tax)

28. Austria 36,5/ from 2016: 25

20

PwC

Annex 2: Tax-free (income tax) thresholds in EU member states

21

PwC

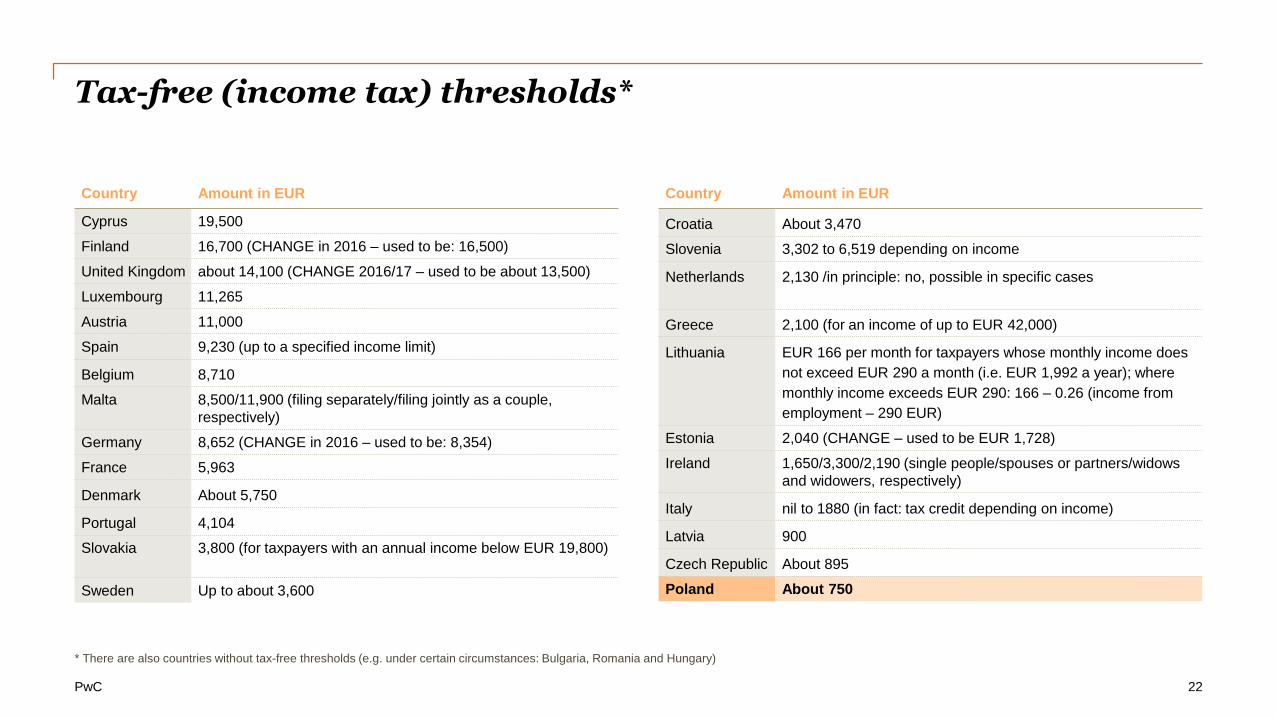

Tax-free (income tax) thresholds*

Country Amount in EUR

Cyprus 19,500

Finland 16,700 (CHANGE in 2016 – used to be: 16,500)

United Kingdom about 14,100 (CHANGE 2016/17 – used to be about 13,500)

Luxembourg 11,265

Austria 11,000

Spain 9,230 (up to a specified income limit)

Belgium 8,710

Malta 8,500/11,900 (filing separately/filing jointly as a couple,

respectively)

Germany 8,652 (CHANGE in 2016 – used to be: 8,354)

France 5,963

Denmark About 5,750

Portugal 4,104

Slovakia 3,800 (for taxpayers with an annual income below EUR 19,800)

Sweden Up to about 3,600

Country Amount in EUR

Croatia About 3,470

Slovenia 3,302 to 6,519 depending on income

Netherlands 2,130 /in principle: no, possible in specific cases

Greece 2,100 (for an income of up to EUR 42,000)

Lithuania EUR 166 per month for taxpayers whose monthly income does

not exceed EUR 290 a month (i.e. EUR 1,992 a year); where

monthly income exceeds EUR 290: 166 – 0.26 (income from

employment – 290 EUR)

Estonia 2,040 (CHANGE – used to be EUR 1,728)

Ireland 1,650/3,300/2,190 (single people/spouses or partners/widows

and widowers, respectively)

Italy nil to 1880 (in fact: tax credit depending on income)

Latvia 900

Czech Republic About 895

Poland About 750

* There are also countries without tax-free thresholds (e.g. under certain circumstances: Bulgaria, Romania and Hungary)

22

PwC

Annex 3: Examples of tax thresholds in the EU

23

PwC

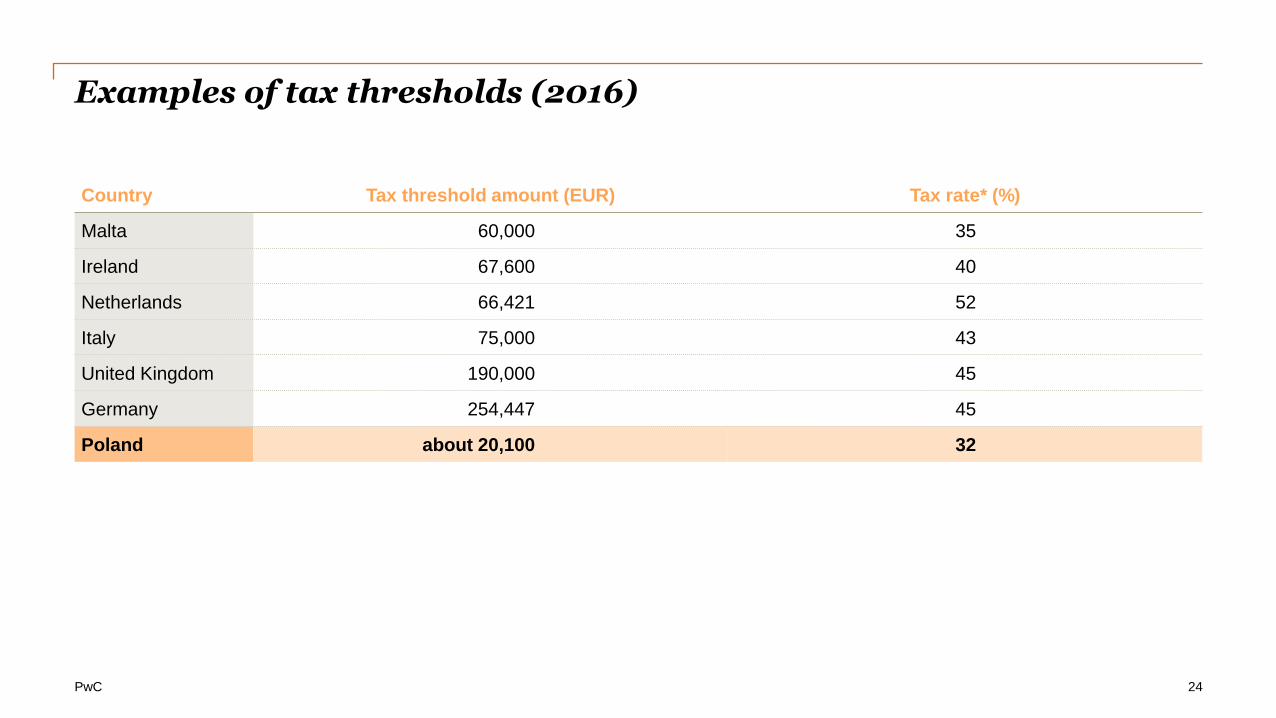

Examples of tax thresholds (2016)

Country Tax threshold amount (EUR) Tax rate* (%)

Malta 60,000 35

Ireland 67,600 40

Netherlands 66,421 52

Italy 75,000 43

United Kingdom 190,000 45

Germany 254,447 45

Poland about 20,100 32

24

PwC

Annex 4 – Social security contributions in the EU

25

PwC

Social security contributions on remuneration – ranking by the cost to the employer (1/2)*

Rank Country Cost to employer (%) Cost to employee (%) Total social security contribution (%)

1. Luxembourg 8 8 16

2. Slowenia 8,85 15,5 24,35

3. Denmark 10 5 15

4. Malta 10 (+ additional state

funds

of 50% of the

contribution)

10 20 (+ additional state funds

of 50% of the contribution)

5. Ireland 10,75 0 (4) 14,75

6. Cyprus 11,5 7,8 15,6

7. United Kingdom 13,8 2 (12) 15,8 (25,8)

8. Croatia 17,2 20 37,2

9. Finland 17,35 5,7 (7,2) 23,05 (24,55)

10. Bulgaria 17,8-18,5 12,9 30,7-31,4

11. Netherlands 18,81 28,15 46,96

12. Germany 19,32 18,32 42,6

13. Austria 21,63 18,07 39,7

14. Polska 22,67 14.96 (including the non-

deductible portion of the

health insurance

conribution)

37,63

26

*At the highest rate in each category

PwC

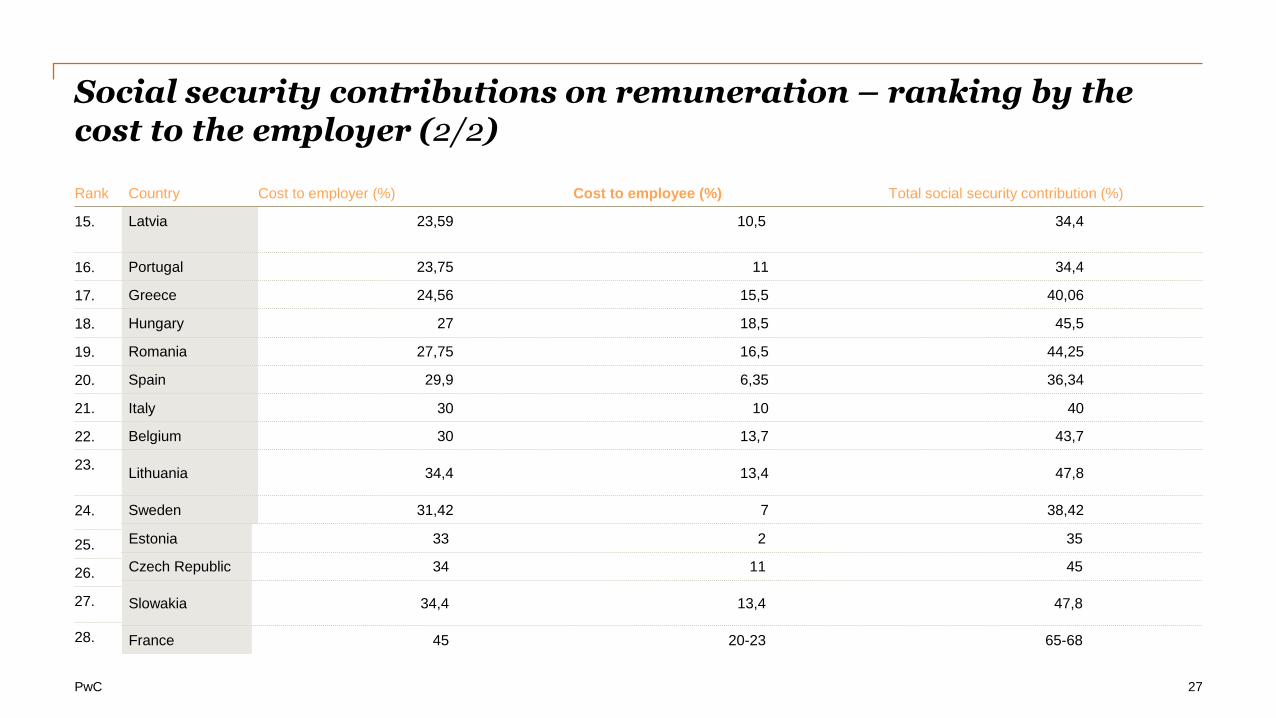

Social security contributions on remuneration – ranking by the cost to the employer (2/2) Rank Country Cost to employer (%) Cost to employee (%) Total social security contribution (%)

15. Latvia 23,59 10,5 34,4

16. Portugal 23,75 11 34,4

17. Greece 24,56 15,5 40,06

18. Hungary 27 18,5 45,5

19. Romania 27,75 16,5 44,25

20. Spain 29,9 6,35 36,34

21. Italy 30 10 40

22. Belgium 30 13,7 43,7

23. Lithuania 34,4 13,4 47,8

24. Sweden 31,42 7 38,42

27

25.

26.

27.

28.

Estonia 33 2 35

Czech Republic 34 11 45

Slowakia 34,4 13,4 47,8

France 45 20-23 65-68

PwC

Annex 5 – retirement age in the EU

28

PwC

Retirement age in each country (in alphabetical order) (1/2)

Country Women Men Notes

Austria 60 65 Over the years 2024 to 2033, the retirement age of women will be raised to 65 years

Belgium 65 65

Bulgaria 60.8 63.8 A pension reform is being discussed

Croatia 65 65

Cyprus 65 65

Czech Republic 67 67 For a person born in 1977 (for those born after that date: a special formula whereby the

retirement age may be higher, e.g. for a person born in 1985: 68.4 years)

Denmark 65-67 65-67 Depending on the date of birth

Estonia 60 63 2016: equal retirement age planned

Finland 63-68 63-68 Discretion to choose

France 60-67 60-67 Depending on the date of birth

Greece 62-67 62-67 Depending on the number of days of service

Spain 65 65 Raising to 67 years planned

Netherlands 65.3 65.3 Raising to 67 years planned by 2021

29

PwC

Retirement age in each country (in alphabetical order) (2/2)

Country Women Men Notes

Ireland 65 65

Lithuania 61.4 63.2 Raising to 65 years planned by 2026

Luxembourg 65 65

Latvia 62 62

Malta 65 65

Germany 65 65 Raising to 67 years planned by 2029

Portugal 66 66

Romania 63 65

Slovakia 62 62

Slovenia 58.4-65 58.8-65 Depending on the insurance period

Sweden 65 65

Hungary 62 62 Raising to 65 years planned by 2022

United Kingdom 60 65 Raising to 68 years planned for both sexes

Italy 63.9 66.3

30

PwC

Annex 6: CIT and VAT rates in each country

31

PwC

VAT and CIT rates in each country (in alphabetical order) (1/2)

Country VAT rate CIT rate

Austria 20%, 13% 25%

Belgium 21%, 12%, 6%, 0% 33.99%

Bulgaria 20%, 9%, 0% 10%

Croatia 25%, 13%, 5% 20%

Cyprus 19%, 9%, 5%, 0% 12.5%

Czech Republic 21%, 15%, 10%, 0% 19%

Denmark 25%, 0% 22%

Estonia 20%, 9%, 0% 20%

Finland 24%, 14%, 10%, 0% 20%

France 20%, 10%, 5%, 2.1%, 0% 33.33%

Greece 23%, 13%, 6.5%, 0% 26%

Spain 21%, 10%, 4% 25%

Netherlands 21%, 6%, 0% 25%, 20%

Ireland 23%, 13.5%, 9%, 0% 12.5%

32

PwC

VAT and CIT rates in each country (in alphabetical order) (2/2)

Country VAT rate CIT rate

Lithuania 21%, 9%, 6%, 5%, 0% 15%, 5% (small enterprises and farmers)

Luxembourg 17%, 14%, 8%, 3%, 0% 20%, 21%

Latvia 21%, 12%, 0% 15%

Malta 18%, 7%, 5%, 0% 35%

Germany 19%, 7% 15%

Poland 23%, 8%, 5%, 0% 19%

Portugal 23%, 13%, 6%, 0% 21%, 17%

Romania 24%, 9%, 0% 16%

Slovakia 20%, 10%, 0% 22%

Slovenia 22%, 9.5% 17%

Sweden 25%, 12%, 6%, 0% 22%

Hungary 27%, 18%, 5% 10%, 19%

United Kingdom 20%, 5%, 0% 20%

Italy 22%, 10%, 4% 27.5%

33

Related Documents