MAY THE JOYOUS SEASON BRING YOU A FULFILLING HARVEST, SOARING HAPPINESS AND RYTHMIC CELEBRATIONS HAPPY LOHRI & MAKAR SANKRANTI 2016 : Issue 509, Week : 11th - 14th January A Weekly Update from SMC (For private circulation only) WISE M NEY Brand smc 333

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

MAY THE JOYOUS SEASONBRING YOU A FULFILLING HARVEST,SOARING HAPPINESS AND RYTHMIC CELEBRATIONS

HAPPY LOHRI &MAKAR SANKRANTI

2016 : Issue 509, Week : 11th - 14th JanuaryA Weekly Update from SMC

(For private circulation only)

WISE M NEY

Bra

nd

sm

c 333

Contents

Equity 4-7

Derivatives 8-9

Commodity 10-13

Currency 14

IPO 15

FD Monitor 16

Insurance 17

Mutual Fund 18

SMC RESEARCH TEAMREGISTERED OFFICES:

11 / 6B, Shanti Chamber, Pusa Road, New Delhi 110005.

Tel: 91-11-30111000, Fax: 91-11-25754365

MUMBAI OFFICE:

Dheeraj Sagar, 1st Floor, Opp. Goregaon sports Club, Link Road

Malad (West), Mumbai 400064

Tel: 91-22-67341600, Fax: 91-22-28805606

KOLKATA OFFICE:

18,Rabindra Sarani, Poddar Court, Gate No-4,5th Floor, Kolkata-700001

Tel : 91-33-39847000 Fax No : 91-33-39847004

AHMEDABAD OFFICE :

10/A, 4th Floor, Kalapurnam Building, Near Municipal Market,

C G Road, Ahmedabad-380009, Gujarat

Tel : 91-79-26424801 - 05, 40049801 - 03

CHENNAI OFFICE:

Salzburg Square, Flat No.1, III rd Floor, Door No.107, Harrington Road,

Chetpet, Chennai - 600031.

Tel: 044-39109100, Fax -044- 39109111

SECUNDERABAD OFFICE:

206, 3rd Floor, above CMR Exclusive, Bhuvana Towers, S.D.Road,

Secunderabad - 500003

Tel: 91-40-30780298/99, 39109536

DUBAI OFFICE:

312, Belshalat Building, Al Karama, Dubai, P.O. Box 117210, U.A.E.

Tel: 97143963120, Mobile : 971502612483

Fax : 9714 3963122

Email ID : [email protected]

Printed and Published on behalf of

Mr. Saurabh Jain @ Publication Address

11/6B, Shanti Chamber, Pusa Road, New Delhi-110005

Website: www.smcindiaonline.com

Investor Grievance : [email protected]

Printed at: S&S MARKETING

102, Mahavirji Complex LSC-3, Rishabh Vihar, New Delhi - 110092 (India)

Ph.: +91-11- 43035012, 43035014, Email: [email protected]

ith the onset of the New Year, global stock markets rattled with a sinking

Yuan adding to concern about the strength of China's economy as it shifts Waway from investment and manufacturing toward consumption and

services. Investors turn risk averse with regards to growing concern over the health of

the Asia's largest economy i.e. China, selling stocks all over the globe. China-fueled

selloff in mining and energy shares spooked sentiments in the European stocks too, that

fell mirroring declines that shook global equities in August. U.S. markets too came off in

tandem with other markets as investors sensed that the global growth engine is starting

to slow. The World Bank on Wednesday cut its global growth forecasts for this year and

2017, citing concerns over China's economy and its impact on commodities that have

been at the forefront of traders' minds since 2016 got under way.

Back at home, Indian markets tumbled down by more than 4 percent, reflecting the

weakness in the global markets. Foreign institutional investors remained on the sell side

of the markets. It seems that slowing China is widely expected to spell trouble for world

markets. On the macro front, data on industrial production for November 2015 and the

data on inflation based on the consumer price index (CPI) for December 2015 will be

announced by the government after market hours on Tuesday, 12 January 2016. Recently,

the World Bank forecast that India is likely to grow by a robust 7.8 percent this year and

7.9 percent in the next two years on the back of stronger domestic policy reforms.

Macroeconomic data, Q3 results of India Inc., trend in global markets, investment by

foreign portfolio investors (FPIs) and domestic institutional investors (DIIs), the

movement of rupee against the dollar and crude oil price movement will dictate trend on

the bourses in the near term.

On the commodity front, some tensions in the Middle East and rout in the Chinese market

influenced the commodity prices significantly. It gave a negative impact on the base

metal and energy prices. Investors may jump back to gold to hedge some of the

uncertainties over global growth, over China, with positioning in gold. Gold can move in

the range of 25500-26700 while Silver can move in the range of 32000-36000. Crude oil

may remain on a volatile path with some short covering at lower levels can be seen after

the recent slide amid global supply glut. Crude oil can move in the range of 2050-2600 in

MCX. New Yuan Loans, Unemployment Rate of Australia, German GDP, BOE Asset

Purchase Target, Bank of England Rate Decision, Advance Retail Sales, U. of Michigan

Confidence are some data and events, which should be taken care of while trading in

commodities.

From The Desk Of Editor

(Saurabh Jain)

SMC Global Securities Limited is proposing, subject to receipt of requisite approvals, market conditions and other considerations, a further public offering of its equity shares and has filed the Draft Red Herring Prospectus with the Securities and Exchange Board of India (“SEBI”) and the Stock Exchanges. The Draft Red Herring Prospectus is available on the website of SEBI at www.sebi.gov.in and on the websites of the Book Running Lead Manager i.e., ICICI Securities Limited at www.icicisecurities.com and the Co- Book Running Lead Manager i.e., Elara Capital (India) Private Limited at www.elaracapital.com . Investors should note that investment in equity shares involves a high degree of risk and for details relating to the same, please see the section titled “Risk Factors” of the aforementioned offer document.

SMC Global Securities Ltd. (hereinafter referred to as “SMC”) is a registered Member of National Stock Exchange of India Limited, Bombay Stock Exchange Limited and its associate is member of MCX stock Exchange Limited. It is also registered as a Depository Participant with CDSL and NSDL. Its associates merchant banker and Portfolio Manager are registered with SEBI and NBFC registered with RBI. It also has registration with AMFI as a Mutual Fund Distributor.

SMC has applied with SEBI for registering as a Research Entity in terms of SEBI (Research Analyst) Regulations, 2014. SMC or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing /dealing in securities Market.

SMC or its associates including its relatives/analyst do not hold any financial interest/beneficial ownership of more than 1% in the company covered by Analyst. SMC or its associates and relatives does not have any material conflict of interest. SMC or its associates/analyst has not received any compensation from the company covered by Analyst during the past twelve months. The subject company has not been a client of SMC during the past twelve months. SMC or its associates has not received any compensation or other benefits from the company covered by analyst or third party in connection with the research report. The Analyst has not served as an officer, director or employee of company covered by Analyst and SMC has not been engaged in market making activity of the company covered by Analyst.

The views expressed are based solely on information available publicly available/internal data/ other reliable sources believed to be true.

SMC does not represent/ provide any warranty express or implied to the accuracy, contents or views expressed herein and investors are advised to independently evaluate the market conditions/risks involved before making any investment decision.

NEWS

DOMESTIC NEWSEconomy• India will likely grow by a robust 7.8 percent this year and 7.9 percent in

the next two years on the back of stronger domestic policy reforms, the World Bank forecast, even as it cut its global economic growth forecast for 2016, citing weak growth among emerging markets.

• The Indian Cabinet approved conversion of MUDRA Ltd, an NBFC, into MUDRA Bank and also setting up of a Credit Guarantee Fund for loans disbursed under the Pradhan Mantri Micro Units Development Refinance Agency (MUDRA) Yojana.

Pharmaceutical• Glenmark Pharmaceuticals Inc., USA has been granted tentative approval

by the United States Food & Drug Administration for its Dronedarone Tablets, 400 mg, the generic version of Multaq Tablets, 400 mg of Sanofi- Aventis U.S., LLC.

• Lupin has launched its Tri-Lo-Marzia tablets, an oral contraceptive drug, in the US market after getting approval from the American health regulator. The company's US subsidiary Lupin Pharmaceutical Inc has launched Tri-Lo-Marzia tablets after receiving approval from the United States Food and Drug Administration (USFDA).

• Cipla has inked a pact with US-based BioQ Pharma for registration and commercialisation of latter's Ropivacaine infusion system, used in treating post-operative pain, in India.

Realty/ Construction• NBCC has bagged orders worth `8,523 crore in the month gone by. The

company was awarded ̀ 8195 crore worth of orders for project management consultancy (PMC) during December. It also managed to fetch engineering procurement and construction (EPC) orders worth ̀ 328 crore.

• National Buildings Construction Corporation announced that Indian Institute of Technology, Mandi has awarded the work of construction of Academic Building, Guest House, Gymnasium, Hospital and Auditorium at IIT Mandi Campus for ̀ 294.78 crore.

• Punj Lloyd has won four highway projects worth `1,555 crore in Bihar, Chhattisgarh, Odisha and Punjab from the central government. The engineering, procurement and construction projects in Bihar, Chhattisgarh and Odisha have been awarded to Punj Lloyd by the National Highways Authority of India while the order in Punjab has been won from the Ministry of Road Transport and Highways (MORTH).

• IRB Infrastructure Developers has bagged a `10,050-crore order to construct the Zozila pass tunnel in Jammu & Kashmir. It is the biggest national highway project awarded in India in terms of project cost with a tunnel length spanning 14.08 km.

Automobile• Mahindra & Mahindra launched Imperio, a premium pick-up priced at

`6.25 lakh (ex-showroom, Thane, BS III variant). The new M&M vehicle will compete against Tata Xenon and Isuzu D-Max pick-ups. The Imperio will replace the existing Genio pick-up.

INTERNATIONAL NEWS• The World Bank trimmed its global growth outlook, citing anemic recovery

in major emerging markets, although it suggested that overall growth will improve from last year, underpinned by advanced economies. Global economic growth is forecast to be 2.9 percent this year, instead of the 3.3 percent projected in June, the Washington-based lender said in its bi-annual Global Economic Prospects.

• US factory orders edged down by 0.2 percent in November after jumping by 1.3 percent in October. The modest decrease matched economist estimates. The pullback partly reflected a continued decrease in orders for non-durable goods, which fell by 0.4 percent in November after dipping by 0.2 percent in October.

• US non-manufacturing index edged down to 55.3 in December from 55.9 in November, although a reading above 50 continues to point to growth in the service sector. The modest decrease came as a surprise to economists, who had expected the non-manufacturing index to inch up to 56.2.

• US trade deficit shrank to $42.4 billion in November from a revised $44.6 billion in October. Economists had expected the deficit to widen to $44.4 billion in November from the $43.9 billion originally reported for the previous month.

• US construction spending fell 0.4 percent to an annual rate of $1.123 trillion in November from the revised October estimate of $1.127 trillion. Economists had expected spending to rise by 0.7 percent. The unexpected drop was partly due to a steep decline in spending on public construction, which slumped 1.0 percent to annual rate of $294.3 billion.

• US initial jobless claims fell to 277,000, a decrease of 10,000 from the previous week's unrevised level of 287,000. Economists had expected jobless claims to drop to 272,000.

• Eurozone producer prices decreased at a stable pace for the second straight month in November, in line with expectations. The producer price index fell 3.2 percent year-over-year in November, the same rate of decrease as in the previous month, which was revised from a 3.1 percent drop reported earlier. The figure was also matched with consensus estimate.

Ex-Date Company Purpose

11-Jan-16 JMC Projects (India) Rights 2:7

19-Jan-16 Oil India Interim Dividend

21-Jan-16 Siemens Final Dividend Rs 6/- Plus Special Dividend Rs 4/- Per Share

25-Jan-16 MindTree Interim Dividend

2-Feb-16 Persistent Systems Interim Dividend (Record Date Revised)

3-Feb-16 Godrej Consumer Products Third Interim Dividend

Meeting Date Company Purpose

12-Jan-16 DCB BANK Results

12-Jan-16 Tata Consultancy Ser. Results/Dividend

12-Jan-16 Oil India Dividend

12-Jan-16 IndusInd Bank Results

12-Jan-16 The Federal Bank Results

13-Jan-16 Reliance Industrial

Infrastructure Results

13-Jan-16 Karur Vysya Bank Results

14-Jan-16 Infosys Results

15-Jan-16 Hindustan Unilever Results

15-Jan-16 Zee Entertainment Ent. Results

15-Jan-16 Pipavav Defence and

Offshore Engineering Com. Results

15-Jan-16 NIIT Technologies Results

16-Jan-16 The Karnataka Bank Results

16-Jan-16 Wipro Results/Dividend

16-Jan-16 LIC Housing Finance Results

18-Jan-16 Asian Paints Results

18-Jan-16 MindTree Results/Dividend

18-Jan-16 Kotak Mahindra Bank Results

19-Jan-16 HCL Technologies Results/Dividend

FORTHCOMING EVENTS

NOTES:1) These levels should not be confused with the daily trend sheet, which is sent every morning by e-mail in the name

of "Morning Mantra ".2) Sometimes you will find the stop loss to be too far but if we change the stop loss once, we will find more strength

coming into the stock. At the moment, the stop loss will be far as we are seeing the graphs on weekly basis and taking a long-term view and not a short-term view.

TREND SHEET

Stocks *Closing Trend Date Rate SUPPORT RESISTANCE Closing

Price Trend Trend

Changed Changed

SENSEX 24934 DOWN 13.11.15 25610 26000 27000

S&P NIFTY 7601 DOWN 13.11.15 7762 7990 8120

CNX IT 10990 DOWN 24.04.15 11132 11400 11600

CNX BANK 16143 DOWN 11.12.15 16343 17000 17300

ACC 1296 DOWN 20.03.15 1570 1370 1400

BHARTIAIRTEL 324 DOWN 04.12.15 322 335 345

BHEL 154 DOWN 13.08.15 259 170 175

CIPLA 622 DOWN 03.09.15 691 660 680

DLF 112 DOWN 13.11.15 110 120 126

HINDALCO 77 DOWN 12.12.14 154 85 90

ICICI BANK 245 DOWN 06.02.15 329 270 275

INFOSYS 1063 DOWN 20.11.15 1052 1100 1120

ITC 314 DOWN 08.01.16 314 330 340

L&T 1179 DOWN 27.08.15 1620 1320 1350

MARUTI 4215 DOWN 08.01.16 4215 4450 4500

NTPC 140 UP 06.11.15 136 130 124

ONGC 230 DOWN 17.10.14 397 240 250

RELIANCE 1026 UP 23.10.15 955 960 940

TATASTEEL 254 UP 24.12.15 263 240 230

S/l

4

®

Closing as on 08-01-2016

BSE SENSEX GAINERS & LOSERS TOP (% Change) NSE NIFTY GAINERS TOP & LOSERS (% Change)

SECTORAL INDICES (% Change)

SMC Trend

FMCGHealthcare

Auto BankRealty

Cap GoodsCons Durable

Oil & GasPower

ITMetal

Down SidewaysUp

GLOBAL INDICES (% Change)

INDIAN INDICES (% Change)

5

®

SMC Trend

Nifty BSE Midcap S&P CNX 500BSE SmallcapSensex Nifty Junior

SMC Trend

FTSE 100CAC 40

NasdaqDow jonesS&P 500

NikkeiStrait times

Hang SengShanghai

280.54

8.70

-574.88

-245.06

-113.69-49.10 -72.90

357.60

-800.00

-600.00

-400.00

-200.00

0.00

200.00

400.00

600.00

Friday Monday Tuesday Wednesday Thursday

FII / FPI Activity MF Activity

0.23

-14.52

-12.29-11.46

-10.67-10.04

-16.00

-14.00

-12.00

-10.00

-8.00

-6.00

-4.00

-2.00

0.00

2.00

GAIL (India) Tata Motors Bank of Baroda

Vedanta Punjab Natl.Bank

B H E L

-4.96 -5.00

-3.52 -3.61 -3.77

-4.54

-6.00

-5.00

-4.00

-3.00

-2.00

-1.00

0.00

Nifty Sensex BSE Midcap BSE Smallcap

Nifty Junior S&P CNX 500

-7.22

-5.99-6.27

-0.93

-4.42-4.29

-3.32

-4.27

-1.66

-4.23

-5.95

-8.00

-7.00

-6.00

-5.00

-4.00

-3.00

-2.00

-1.00

0.00

Auto Index Bankex Cap Goods Index

Cons Durable Index

FMCG Index Healthcare Index

IT Index Metal Index Oil & Gas Index

Power Index Realty Index

-6.35

-5.23-4.93

-6.65

-5.30

-7.21

-11.70

-4.62-5.04

-14.00

-12.00

-10.00

-8.00

-6.00

-4.00

-2.00

0.00

Nasdaq Comp. Dow Jones S&P 500 Nikkei Strait Times Hang Seng Shanghai Comp.

FTSE 100 CAC 40

0.11

-14.55

-10.03

-8.99-8.58

-7.95

-16.00

-14.00

-12.00

-10.00

-8.00

-6.00

-4.00

-2.00

0.00

2.00

GAIL (India) Tata Motors B H E L Axis Bank Adani Ports St Bk of India

INSTITUTIONAL ACTIVITY (Equity) (` Crore)

Closing as on 22.10.15

Closing as on 21.10.15

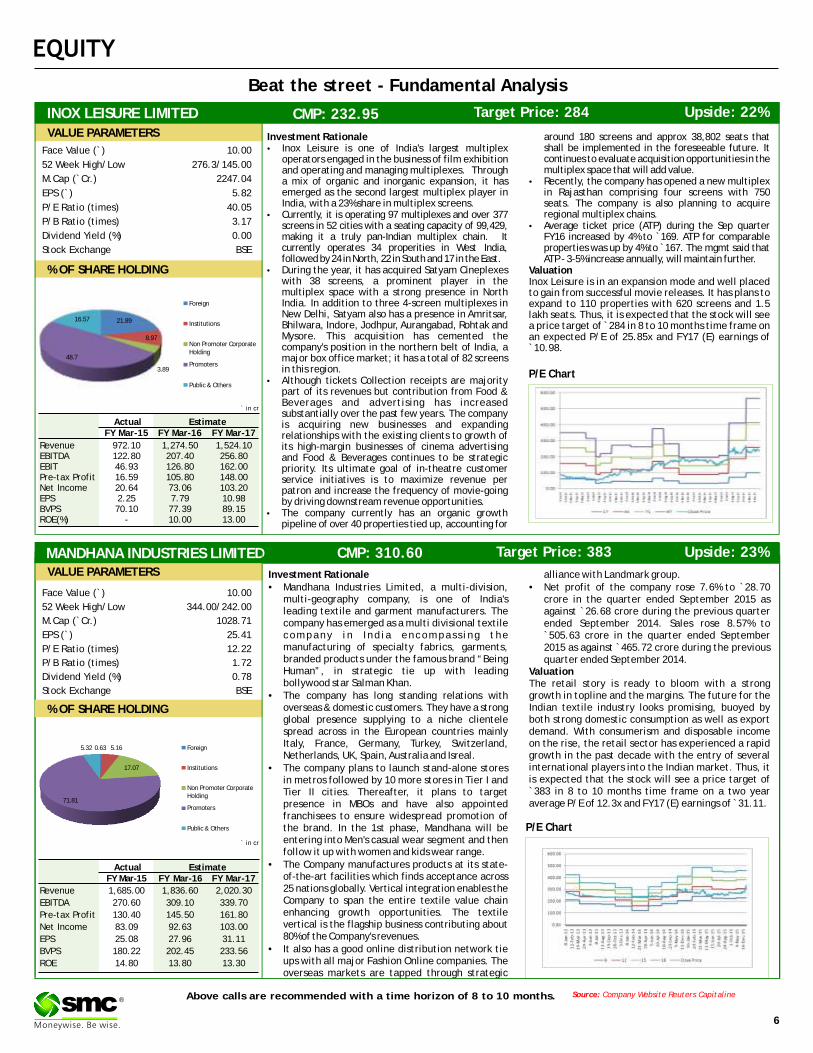

Beat the street - Fundamental Analysis

Above calls are recommended with a time horizon of 8 to 10 months. Source: Company Website Reuters Capitaline

6

®

Investment Rationale alliance with Landmark group.•Mandhana Industries Limited, a multi-division, •Net profit of the company rose 7.6% to `28.70

multi-geography company, is one of India's crore in the quarter ended September 2015 as leading textile and garment manufacturers. The against `26.68 crore during the previous quarter company has emerged as a multi divisional textile ended September 2014. Sales rose 8.57% to company in Ind ia encompass ing the `505.63 crore in the quarter ended September manufacturing of specialty fabrics, garments, 2015 as against `465.72 crore during the previous branded products under the famous brand “Being quarter ended September 2014.Human”, in strategic tie up with leading Valuationbollywood star Salman Khan. The retail story is ready to bloom with a strong

•The company has long standing relations with growth in topline and the margins. The future for the overseas & domestic customers. They have a strong Indian textile industry looks promising, buoyed by global presence supplying to a niche clientele both strong domestic consumption as well as export spread across in the European countries mainly demand. With consumerism and disposable income Italy, France, Germany, Turkey, Switzerland, on the rise, the retail sector has experienced a rapid Netherlands, UK, Spain, Australia and Isreal. growth in the past decade with the entry of several

international players into the Indian market. Thus, it •The company plans to launch stand-alone stores is expected that the stock will see a price target of in metros followed by 10 more stores in Tier I and `383 in 8 to 10 months time frame on a two year Tier II cities. Thereafter, it plans to target average P/E of 12.3x and FY17 (E) earnings of ̀ 31.11.presence in MBOs and have also appointed

franchisees to ensure widespread promotion of the brand. In the 1st phase, Mandhana will be entering into Men's casual wear segment and then follow it up with women and kids wear range.

•The Company manufactures products at its state-of-the-art facilities which finds acceptance across 25 nations globally. Vertical integration enables the Company to span the entire textile value chain enhancing growth opportunities. The textile vertical is the flagship business contributing about 80% of the Company's revenues.

•It also has a good online distribution network tie ups with all major Fashion Online companies. The overseas markets are tapped through strategic

P/E Chart

MANDHANA INDUSTRIES LIMITED CMP: 310.60 Upside: 23%Target Price: 383

Face Value (`) 10.00

52 Week High/Low 344.00/242.00

M.Cap (`Cr.) 1028.71

EPS (`) 25.41

P/E Ratio (times) 12.22

P/B Ratio (times) 1.72

Dividend Yield (%) 0.78

Stock Exchange BSE

` in cr

% OF SHARE HOLDING

VALUE PARAMETERS

Actual EstimateFY Mar-15 FY Mar-16 FY Mar-17

Revenue 1,685.00 1,836.60 2,020.30

EBITDA 270.60 309.10 339.70

Pre-tax Profit 130.40 145.50 161.80

Net Income 83.09 92.63 103.00

EPS 25.08 27.96 31.11

BVPS 180.22 202.45 233.56

ROE 14.80 13.80 13.30

INOX LEISURE LIMITED CMP: 232.95 Upside: 22%Target Price: 284

Investment Rationale around 180 screens and approx 38,802 seats that •Inox Leisure is one of India's largest multiplex shall be implemented in the foreseeable future. It

operators engaged in the business of film exhibition continues to evaluate acquisition opportunities in the and operating and managing multiplexes. Through multiplex space that will add value.a mix of organic and inorganic expansion, it has •Recently, the company has opened a new multiplex emerged as the second largest multiplex player in in Rajasthan comprising four screens with 750 India, with a 23% share in multiplex screens. seats. The company is also planning to acquire

•Currently, it is operating 97 multiplexes and over 377 regional multiplex chains. screens in 52 cities with a seating capacity of 99,429, •Average ticket price (ATP) during the Sep quarter making it a truly pan-Indian multiplex chain. It FY16 increased by 4% to `169. ATP for comparable currently operates 34 properities in West India, properties was up by 4% to ̀ 167. The mgmt said that followed by 24 in North, 22 in South and 17 in the East. ATP - 3-5% increase annually, will maintain further.

•During the year, it has acquired Satyam Cineplexes Valuationwith 38 screens, a prominent player in the Inox Leisure is in an expansion mode and well placed multiplex space with a strong presence in North to gain from successful movie releases. It has plans to India. In addition to three 4-screen multiplexes in expand to 110 properties with 620 screens and 1.5 New Delhi, Satyam also has a presence in Amritsar, lakh seats. Thus, it is expected that the stock will see Bhilwara, Indore, Jodhpur, Aurangabad, Rohtak and a price target of ̀ 284 in 8 to 10 months time frame on Mysore. This acquisition has cemented the an expected P/E of 25.85x and FY17 (E) earnings of company's position in the northern belt of India, a `10.98.major box office market; it has a total of 82 screens in this region.

•Although tickets Collection receipts are majority part of its revenues but contribution from Food & Beverages and advertising has increased substantially over the past few years. The company is acquiring new businesses and expanding relationships with the existing clients to growth of its high-margin businesses of cinema advertising and Food & Beverages continues to be strategic priority. Its ultimate goal of in-theatre customer service initiatives is to maximize revenue per patron and increase the frequency of movie-going by driving downstream revenue opportunities.

•The company currently has an organic growth pipeline of over 40 properties tied up, accounting for

Face Value (`) 10.00

52 Week High/Low 276.3/145.00

M.Cap (`Cr.) 2247.04

EPS (`) 5.82

P/E Ratio (times) 40.05

P/B Ratio (times) 3.17

Dividend Yield (%) 0.00

Stock Exchange BSE

% OF SHARE HOLDING

P/E Chart

` in cr

Actual EstimateFY Mar-15 FY Mar-16 FY Mar-17

Revenue 972.10 1,274.50 1,524.10EBITDA 122.80 207.40 256.80EBIT 46.93 126.80 162.00Pre-tax Profit 16.59 105.80 148.00Net Income 20.64 73.06 103.20EPS 2.25 7.79 10.98BVPS 70.10 77.39 89.15ROE(%) - 10.00 13.00

21.89

8.97

3.89

48.7

16.57

Foreign

Institutions

Non Promoter Corporate Holding

Promoters

Public & Others

0.63 5.16

17.07

71.81

5.32 Foreign

Institutions

Non Promoter Corporate Holding

Promoters

Public & Others

VALUE PARAMETERS

Charts by Spider Software India Ltd

7

EQUITY

Above calls are recommended with a time horizon of 1-2 months

Disclaimer : research. The analysis contained in the analyst research is based on numerous assumptions. Different assumptions could result in materially different results.The analyst, not any of its affiliated companies, not any of their members, directors, employees or agents accepts any liability for any loss or damage arising out of the use of all or any part of the analysis research.

The analyst and its affiliates companies make no representation or warranty in relation to the accuracy, completeness or reliability of the information contained in its

SOURCE: CAPITAL LINE

®

The stock closed at `387.45 on 08th January 2016. It made a 52-week low at

`272.95 on 06th January 2015 and a 52-week high at `412 on 10th August 2015.

The 200 days Exponential Moving Average (EMA) of the stock on the daily chart is

currently at ̀ 363.23.

After falling marginally from higher levels, it managed to hold its price by

rebounding from its crucial support of 280 levels, which is clear on the charts.

Moreover, oscillators are also supporting this particular scrip so we anticipate

that in coming days it will remain on higher note and reach our targets. One can

buy in range of 377-380 levels for the target of 405-415 levels with SL of 365

levels.

Godrej Industries Limited

The stock closed at `887.55 on 08th January 2016. It made a 52-week low at

`543.10 on 05th January 2015 and a 52-week high of `990.95 on 10th August

2015. The 200 days Exponential Moving Average (EMA) of the stock on the daily

chart is currently at ̀ 756.88.

As we can see on the charts, it has maintained its uptrend with marginal

retracements. Last week there was steep decline in broader index but it was still

on higher side. We anticipate that in the coming days it will manage to hold its

upward rally and may reach our desired targets. One can buy in range of 875-880

levels for the target of 915-925 levels with SL of 858 levels.

Hindustan Petroleum Corporation Limited

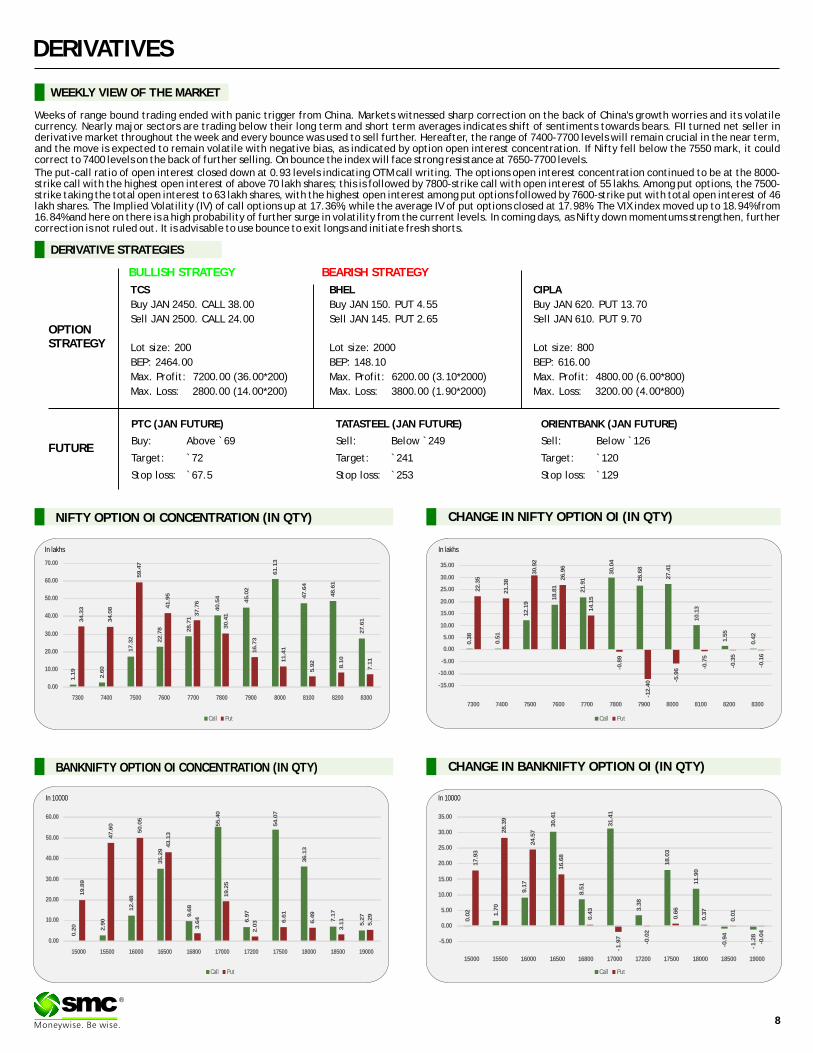

DERIVATIVES

CHANGE IN NIFTY OPTION OI (IN QTY)

WEEKLY VIEW OF THE MARKET

NIFTY OPTION OI CONCENTRATION (IN QTY)

CHANGE IN BANKNIFTY OPTION OI (IN QTY)BANKNIFTY OPTION OI CONCENTRATION (IN QTY)

®

PTC (JAN FUTURE)

Buy: Above `69

Target: `72

Stop loss: `67.5

CIPLA

Buy JAN 620. PUT 13.70

Sell JAN 610. PUT 9.70

Lot size: 800

BEP: 616.00

Max. Profit: 4800.00 (6.00*800)

Max. Loss: 3200.00 (4.00*800)

OPTIONSTRATEGY

FUTURE

TCS

Buy JAN 2450. CALL 38.00

Sell JAN 2500. CALL 24.00

Lot size: 200

BEP: 2464.00

Max. Profit: 7200.00 (36.00*200)

Max. Loss: 2800.00 (14.00*200)

BHEL

Buy JAN 150. PUT 4.55

Sell JAN 145. PUT 2.65

Lot size: 2000

BEP: 148.10

Max. Profit: 6200.00 (3.10*2000)

Max. Loss: 3800.00 (1.90*2000)

DERIVATIVE STRATEGIES

TATASTEEL (JAN FUTURE)

Sell: Below `249

Target: `241

Stop loss: `253

ORIENTBANK (JAN FUTURE)

Sell: Below `126

Target: `120

Stop loss: `129

BULLISH STRATEGY BEARISH STRATEGY

Weeks of range bound trading ended with panic trigger from China. Markets witnessed sharp correction on the back of China's growth worries and its volatile currency. Nearly major sectors are trading below their long term and short term averages indicates shift of sentiments towards bears. FII turned net seller in derivative market throughout the week and every bounce was used to sell further. Hereafter, the range of 7400-7700 levels will remain crucial in the near term, and the move is expected to remain volatile with negative bias, as indicated by option open interest concentration. If Nifty fell below the 7550 mark, it could correct to 7400 levels on the back of further selling. On bounce the index will face strong resistance at 7650-7700 levels. The put-call ratio of open interest closed down at 0.93 levels indicating OTM call writing. The options open interest concentration continued to be at the 8000-strike call with the highest open interest of above 70 lakh shares; this is followed by 7800-strike call with open interest of 55 lakhs. Among put options, the 7500-strike taking the total open interest to 63 lakh shares, with the highest open interest among put options followed by 7600-strike put with total open interest of 46 lakh shares. The Implied Volatility (IV) of call options up at 17.36%, while the average IV of put options closed at 17.98%. The VIX index moved up to 18.94% from 16.84% and here on there is a high probability of further surge in volatility from the current levels. In coming days, as Nifty down momentums strengthen, further correction is not ruled out. It is advisable to use bounce to exit longs and initiate fresh shorts.

In lakhs

In 10000 In 10000

Call Put

0.3

8

0.5

1

12

.19

18

.81

21

.91

30

.04

26

.68

27

.41

10

.13

1.5

5

0.4

2

22

.35

21

.38

30

.92

26

.96

14

.15

-0.8

9

-12

.40 -5

.96 -0

.75

-0.3

5

-0.1

6

-15.00

-10.00

-5.00

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

7300 7400 7500 7600 7700 7800 7900 8000 8100 8200 8300

Call Put

1.1

9

2.6

0

17

.32 22

.78 28

.71

40

.54

45

.02

61

.13

47

.64

48

.61

27

.613

4.3

3

34

.08

59

.47

41

.95

37

.76

30

.41

16

.73

11

.41

5.9

2

8.1

0

7.1

1

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

7300 7400 7500 7600 7700 7800 7900 8000 8100 8200 8300

Call Put

0.2

0

2.9

0

12

.48

35

.29

9.6

8

55

.40

6.9

7

54

.07

36

.13

7.1

7

5.2

7

19

.89

47

.60

50

.05

43

.13

3.6

4

19

.25

2.0

3 6.6

1

6.4

9

3.1

1

5.2

9

0.00

10.00

20.00

30.00

40.00

50.00

60.00

15000 15500 16000 16500 16800 17000 17200 17500 18000 18500 19000

Call Put

0.0

2 1.7

0

9.1

7

30

.41

8.5

1

31

.41

3.3

8

18

.03

11

.90

-0.9

4

-1.2

8

17

.93

28

.39

24

.57

16

.68

0.4

3

-1.9

7

-0.0

2

0.6

6

0.3

7

0.0

1

-0.0

4

-5.00

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

15000 15500 16000 16500 16800 17000 17200 17500 18000 18500 19000

8

In lakhs

9

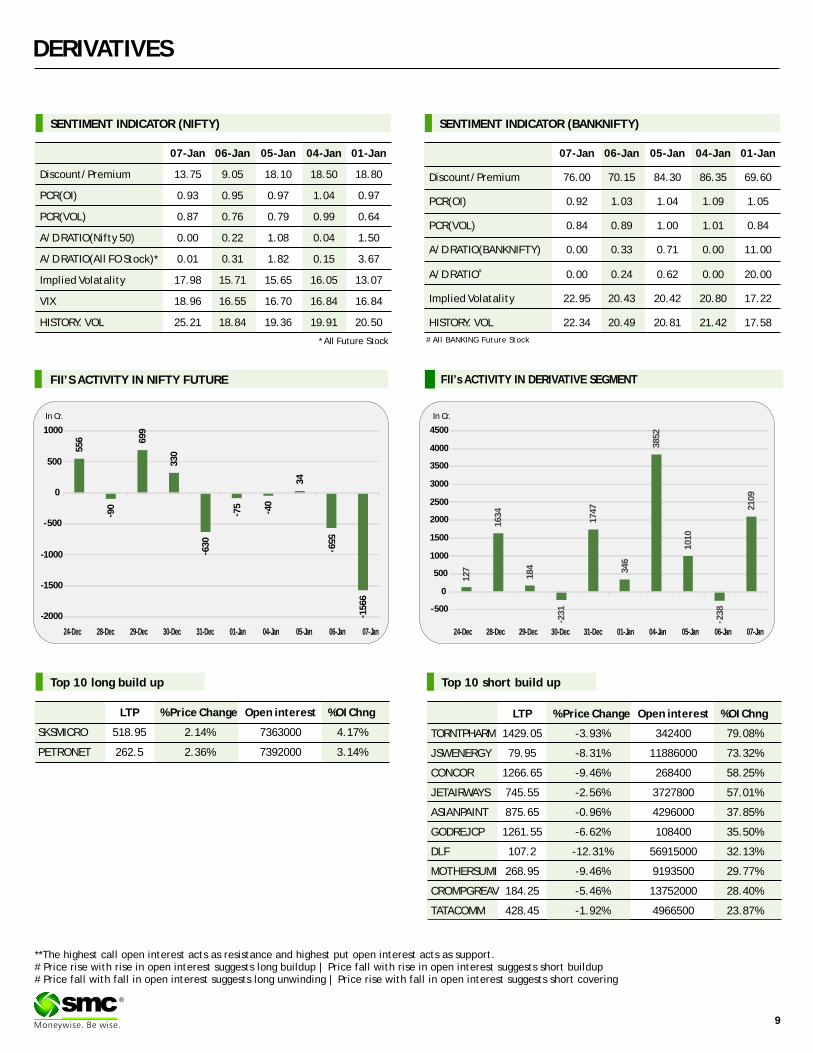

DERIVATIVES

®

FII’s ACTIVITY IN DERIVATIVE SEGMENT

SENTIMENT INDICATOR (NIFTY)

07-Jan 06-Jan 05-Jan 04-Jan 01-Jan

Discount/Premium 13.75 9.05 18.10 18.50 18.80

PCR(OI) 0.93 0.95 0.97 1.04 0.97

PCR(VOL) 0.87 0.76 0.79 0.99 0.64

A/D RATIO(Nifty 50) 0.00 0.22 1.08 0.04 1.50

A/D RATIO(All FO Stock)* 0.01 0.31 1.82 0.15 3.67

Implied Volatality 17.98 15.71 15.65 16.05 13.07

VIX 18.96 16.55 16.70 16.84 16.84

HISTORY. VOL 25.21 18.84 19.36 19.91 20.50

*All Future Stock

SENTIMENT INDICATOR (BANKNIFTY)

07-Jan 06-Jan 05-Jan 04-Jan 01-Jan

Discount/Premium 76.00 70.15 84.30 86.35 69.60

PCR(OI) 0.92 1.03 1.04 1.09 1.05

PCR(VOL) 0.84 0.89 1.00 1.01 0.84

A/D RATIO(BANKNIFTY) 0.00 0.33 0.71 0.00 11.00

#A/D RATIO 0.00 0.24 0.62 0.00 20.00

Implied Volatality 22.95 20.43 20.42 20.80 17.22

HISTORY. VOL 22.34 20.49 20.81 21.42 17.58

FII’S ACTIVITY IN NIFTY FUTURE

**The highest call open interest acts as resistance and highest put open interest acts as support.# Price rise with rise in open interest suggests long buildup | Price fall with rise in open interest suggests short buildup # Price fall with fall in open interest suggests long unwinding | Price rise with fall in open interest suggests short covering

# All BANKING Future Stock

Top 10 short build up

In Cr. In Cr.

Top 10 long build up

LTP % Price Change Open interest %OI Chng

SKSMICRO 518.95 2.14% 7363000 4.17%

PETRONET 262.5 2.36% 7392000 3.14%

LTP % Price Change Open interest %OI Chng

TORNTPHARM 1429.05 -3.93% 342400 79.08%

JSWENERGY 79.95 -8.31% 11886000 73.32%

CONCOR 1266.65 -9.46% 268400 58.25%

JETAIRWAYS 745.55 -2.56% 3727800 57.01%

ASIANPAINT 875.65 -0.96% 4296000 37.85%

GODREJCP 1261.55 -6.62% 108400 35.50%

DLF 107.2 -12.31% 56915000 32.13%

MOTHERSUMI 268.95 -9.46% 9193500 29.77%

CROMPGREAV 184.25 -5.46% 13752000 28.40%

TATACOMM 428.45 -1.92% 4966500 23.87%

55

6

- 90

69

9

33

0

- 63

0

- 75

- 40

34

-

55

9

- 15

66

-2000

-1500

-1000

-500

0

500

1000

24-Dec 28-Dec 29-Dec 30-Dec 31-Dec 01-Jan 04-Jan 05-Jan 06-Jan 07-Jan

12

7

16

34

18

4

- 23

1

17

47

34

6

38

52

10

10

- 23

8

21

09

-500

0

500

1000

1500

2000

2500

3000

3500

4000

4500

24-Dec 28-Dec 29-Dec 30-Dec 31-Dec 01-Jan 04-Jan 05-Jan 06-Jan 07-Jan

Turmeric futures (Apr) is expected to consolidate in the range of 9600-10400 levels. The upside may remain capped as the selling pressure will perhaps catch pace in the days to come. It is reported that in Sangli, the new crop has started entering the market. Secondly, at Erode spot markets, the sentiments are bearish as only 50% of the arrivals are getting sold due to lack of upcountry demand. The market participants are waiting for the fresh crop to hit as prices are expected to go down, before making any bulk purchase. Cardamom futures (Jan) is likely to take support near 790 levels & trade higher towards 835-850 levels. At the spot markets, exporters are buying as the prices of exportable grade material continued to stay at affordable levels. On the international market, in the current crop season, Guatemala expects a production of 28,000 tonnes, lower than the 4-year average production of 34,250 tonnes due to dry spell in the flowering and fruit setting season. Jeera futures (Feb) will possibly take an attempt to break the support near 14000 levels & fall further in days to come on the back of weak export as well as domestic demand. Moreover, favourable weather with higher sowing has made the sentiments bearish in spot market. At Unjha mandi of Gujarat, the best quality jeera quoted near ̀ 2,600-2,850 per 20 kg and medium jeera stood at ̀ 2,400-2,600. Coriander futures (April) would possibly consolidate in the range of 7400-8400 levels. The fundamental factors of lower sowing area reported in Gujarat and Andhra Pradesh may support the prices. Farmers revealed that, current weather is not favourable for Coriander crop & may reduce the yield.

SPICES

Soybean futures (Feb) will probably fall further & test 3600 levels. The sentiments attached to this counter on the domestic as well as in the international markets are bearish owing to contracting Chinese economy. Furthermore, on CBOT, U.S soybeans are under pressure on expectations of bumper South American production. It is reported that soybean harvesting has started in Brazil's top two growing states Mato Grosso and Parana. At home, the major crushing giants are refraining themselves from aggressive buying and crushing in Madhya Pradesh, Maharashtra and Rajasthan. The crushing units in these states are running at much lower crushing capacity (below 30%) while some are closed due to unviable crushing. Mustard futures (Jan) may trade in the range of 4150-4320 levels. In the current scenario, the crop is under pod formation stage & in good condition. The weather temperature is conducive in key mustard seed growing belts of Rajasthan, Uttar Pradesh, Madhya Pradesh, Haryana and West Bengal. Refined soy oil futures (Feb) is expected to drop towards 585 levels, while CPO futures (Jan) may continue to consolidate in the range of 400-420 levels. The factors that are capping the upside are low refining margins, seasonal slowdown of demand and high stocks at ports as well as in pipelines. Malaysian palm oil futures on the Bursa Malaysia Derivatives Exchange are under pressure due to weak export demand and a narrowing spread between the tropical oil and soyoil. On the international market, the market participants will remain cautious ahead of the release of palm oil export data by Cargo surveyor ITS & SGS accompanied with Malaysia's December 2015 data to be released by Malaysian palm oil Board on January 11, 2016.

OIL AND OILSEEDS

OTHER COMMODITIES

Sugar futures (Mar) is likely to trade range bound within 3140-3250 levels. The upside may get limited due to rise in the domestic prices of the sweetener, the prospects of exports are fading out & Indian parity is facing stiff competition against Brazilian supplies in key export markets. Secondly, the supplies in the domestic market are getting stronger as crushing season is in its full pace. As on 31st December, 2015 sugar production is 6.5% higher as compared to last season's production for the corresponding period. Kapas futures (Apr) is expected to trade in the range of 850-875 levels, with a downside bias. The fundamentals of cotton on the international market are bearish amid concerns about the economy in top consumer China. Secondly, the U.S. producer selling has picked up as farmers who had held off until the New Year for tax reasons entered the market. Back at home, many of the textile mills in country are willing to import cotton from African region rather than buying it from local traders. Wheat futures (Feb) may consolidate in the range of 1650-1720 levels. The downside may remain capped as the total production is expected to be lower this season. In the current scenario, sowing is on and would continue till 15th January-2016. Recovery in coverage is expected now to some extent with decreasing temperature in central, east and western parts of India. However, overall acreage may decrease due to late sowing. As per latest update from Ministry of Agriculture Indian wheat growing States have covered 271.46 lakh ha area till 1st Jan, 2016.It is almost 7.4 % lower (293.16 lakh ha) in comparison to area covered in the corresponding time of last year.

Bullion counter may remain on positive path as global stock markets meltdown amid china slowdown concerns is creating safe haven demand for the yellow metal. Furthermore the movement of dollar index will give direction to the bullion counter as it can move in range of 97-100 in near term. On domestic bourses, movement in local currency rupee has affected the prices which can move in range of 65.50 -67.50 in near term. Gold can move in range of 25500-26700 while Silver can move in range of 32000-36000. Recently global stock markets fell on major exchanges fell for a sixth straight day and crude oil prices touched multi-year lows as investors fretted over the state of China's economy and its ability to stabilize its stock market. In a sign of improving investor sentiment, assets of SPDR Gold Trust, the top gold-backed exchange-traded fund, rose 0.65 percent to 645.13 tonnes last week which was the first increase in three weeks. Escalating tension in West Saia, led by Iran severing ties with a number of Gulf countries, plus the hydrogen bomb tests by North Korea, have raised geopolitical uncertainty. With South Korea seeking support from America in terms of installation of nuclear missiles at its border with North Korea, tension is likely to continue. Gold is considered as safe haven in times of geopolitical uncertainty. With China's growth dropping, as seen from falling equity markets and the Yuan's devaluation, investors park their money in gold as alternative asset.

BULLIONS

Crude oil may remain on volatile path with some short covering at lower levels can be seen after the recent slide amid global supply glut. Crude oil can move in range of 2050-2600 in MCX. The global benchmark oil prices fell to nearly 32 levels which were last seen in 2004, hammered by the market turmoil in China, the world's second-biggest consumer of the fuel. Worries about slowing economic growth, especially in China, are helping to drive the sharp drop in crude prices. With producers in the U.S. and Mideast still pumping oil at a fast clip, a drop-off in demand would add to the global supply glut that has shaved about 70% off prices over the past 18 months. In the near term, though, the prospect of more barrels from Iran is looming over the market. Sanctions on the Persian Gulf producer could be lifted this quarter, giving Iranian producers the green light to ship more crude into an already oversupplied market. OPEC hasn't agreed to any output cuts since prices started falling in mid-2014, and the group's production rose sharply last year. OPEC's next meeting is scheduled for June 2016. Natural gas prices may continue its recovery due to colder weather in US. Overall natural gas can move in range of test 145-175 in MCX. Moderate weather-driven demand and robust production has pushed the natural-gas market into oversupply in recent months. Stockpiles usually start drawing in early winter as more consumers use natural gas for indoor heating, but mild temperatures this winter meant that inventories kept growing until late November.

ENERGY COMPLEX

Base metals counter may continue to remain on volatile path with some short covering at current levels can be seen after the recent fall amid China concerns. In a move that deepened concerns over China's economic health, the People's Bank of China set the yuan midpoint rate lower for an eighth consecutive day last week. The 0.5 percent decline was the biggest between daily fixings since August. China's central bank is under increasing pressure from policy advisers to let the yuan currency fall quickly and sharply, by as much as 10-15 percent, as its recent gradual softening is thought to be doing more harm than good. Copper may move in the range of 285-320. Copper prices tumbled last week, hitting their lowest in nearly seven years, as plunging China equities highlighted the country's economic problems and reinforced concern about demand for industrial metals. Lead can move in the range of 107-117 and Zinc can hover in range of 97-105. Chinese refined zinc production growth is expected to slow down in 2016 due to decreased concentrate supply from major overseas miners and planned production cuts by China's top smelters. Zinc concentrate supply will become much tighter in 2016 given the closure of several overseas mines in 2015 and the production cuts by Glencore and Nyrstar. Aluminum can move in range of 95-102 in MCX. Japan's aluminium premiums for January-March shipments were set at $110 per tonne, up 22 percent from the previous quarter. Nickel may move in range of 520-620 in MCX.

BASE METALS

10

®

11

TECHNICAL RECOMMENDATIONS

COMMODITY

ALUMINIUM MCX (JANUARY) contract closed at `98.50 on 07th Jan'16. The contract made its high of

`103.60 on 24th Dec'15 and a low of ̀ 97 on 24th Nov'15. The 18-day Exponential Moving Average of the

commodity is currently at ̀ 99.98.

On the daily chart, the commodity has Relative Strength Index (14-day) value of 45.One can buy in the

range of ̀ 98.60-97.50 with the stop loss of ̀ 96 for a target of ̀ 100.

COTTON SEED OIL NCDEX (FEBRUARY) contract closed at 2092 on 07th Jan'16. The contract made its

high of ̀ 2147 on 01st Jan'16 and a low of ̀ 1542 on 5th Aug'15. The 18-day Exponential Moving Average of

the commodity is currently at ̀ 2019.

On the daily chart, the commodity has Relative Strength Index (14-day) value of 79. One can buy in the

range of ̀ 2080-2070 with the stop loss of ̀ 2050 for a target of ̀ 2150.

`

CORIENDER NCDEX (APRIL) contract closed at 7989 on 07th Jan'16. The contract made its high of

`9948 on 19th Nov'15 and a low of ̀ 7365 on 30th Dec'15. The 18-day Exponential Moving Average of the

commodity is currently at ̀ 8037.8.

On the daily chart, the commodity has Relative Strength Index (14-day) value of 36. One can buy in the

range of ̀ 7900-7870 with the stop loss of ̀ 7800 for a target of ̀ 8100.

`

®

ALUMINIUM MCX (JANUARY)

COTTON SEED OIL NCDEX (FEBRUARY)

CORIENDER NCDEX (APRIL)

NOTES : 1) These levels should not be confused with the daily trend sheet, which is sent every morning by e-mail in the name of Daily report- commodities (Morning Mantra).

2) Sometimes you will find the stop loss to be too far but if we change the stop loss once, we will find more strength coming into the commodity. At the moment, the stop loss will be far as we are seeing the graphs on weekly basis and taking a long-term view and not a short-term view.

EXCHANGE COMMODITY CONTRACT CLOSING DATE TREND TREND RATE TREND SUPPORT RESISTANCE CLOSING

PRICE CHANGED CHANGED STOP/LOSS

NCDEX SOYABEAN JAN 3640.00 03.12.15 Down 3680.00 - 3750.00 3800.00

NCDEX JEERA JAN 13985.00 23.12.15 Down 14595.00 - 15200.00 15700.00

NCDEX CHANA JAN 4880.00 23.12.15 UP 4954.00 4500.00 - 4300.00

NCDEX RM SEEDS JAN 4242.00 10.12.15 SIDEWAYS

MCX MENTHA OIL JAN 880.70 05.11.15 UP 956.60 870.00 - 850.00

MCX CARDAMOM FEB 818.50 07.01.16 SIDEWAYS

MCX SILVER MAR 34531.00 12.11.15 Down 33889.00 - 35500.00 36500.00

MCX GOLD FEB 26100.00 12.11.15 Down 25329.00 - 26200.00 26500.00

MCX COPPER FEB 300.80 04.06.15 Down 381.35 - 325.00 340.00

MCX LEAD JAN 110.20 31.12.15 Up 118.05 108.00 - 105.00

MCX ZINC JAN 99.45 04.06.15 Down 137.15 - 106.00 110.00

MCX NICKEL JAN 562.90 21.05.15 Down 827.90 - 640.00 660.00

MCX ALUMINUM JAN 98.50 22.10.15 Down 94.50 - 103.00 104.00

MCX CRUDE OIL JAN 2254.00 12.11.15 Down 2876.00 - 2600.00 2800.00

MCX NATURAL GAS JAN 160.90 22.10.15 Down 154.70 - 163.00 168.00

TREND SHEET

*Closing as on 07.01.16

COMMODITY

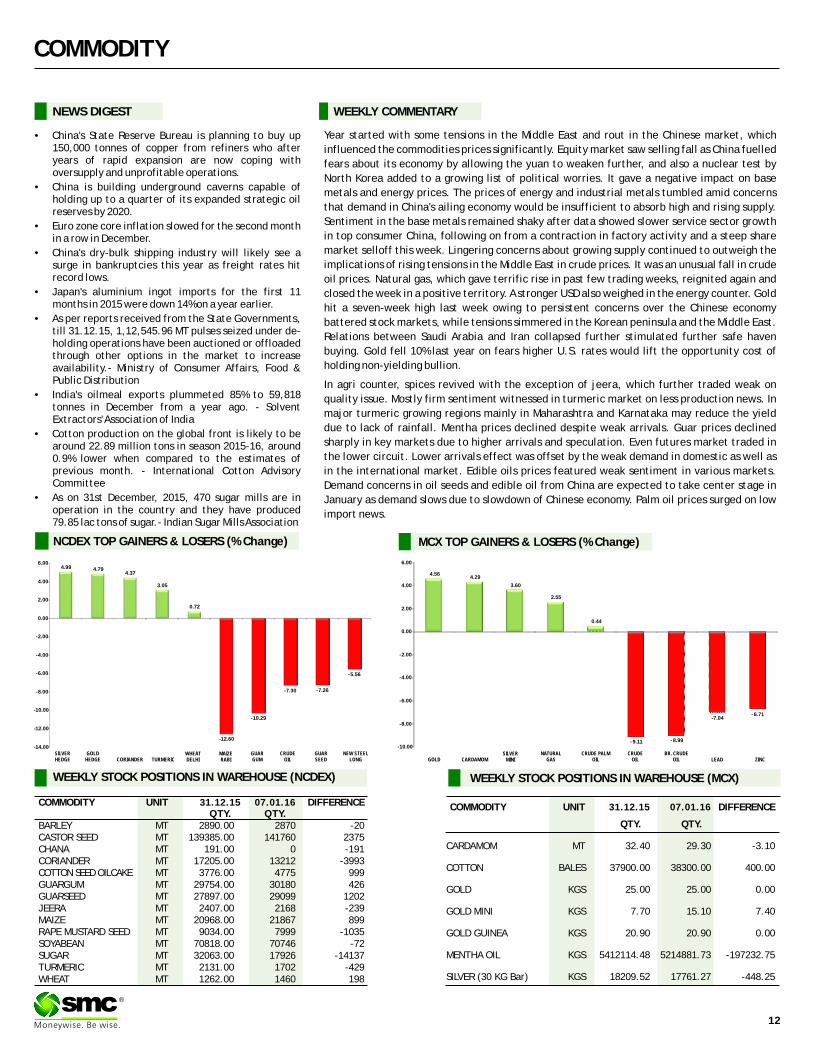

NEWS DIGEST

Year started with some tensions in the Middle East and rout in the Chinese market, which

influenced the commodities prices significantly. Equity market saw selling fall as China fuelled

fears about its economy by allowing the yuan to weaken further, and also a nuclear test by

North Korea added to a growing list of political worries. It gave a negative impact on base

metals and energy prices. The prices of energy and industrial metals tumbled amid concerns

that demand in China's ailing economy would be insufficient to absorb high and rising supply.

Sentiment in the base metals remained shaky after data showed slower service sector growth

in top consumer China, following on from a contraction in factory activity and a steep share

market selloff this week. Lingering concerns about growing supply continued to outweigh the

implications of rising tensions in the Middle East in crude prices. It was an unusual fall in crude

oil prices. Natural gas, which gave terrific rise in past few trading weeks, reignited again and

closed the week in a positive territory. A stronger USD also weighed in the energy counter. Gold

hit a seven-week high last week owing to persistent concerns over the Chinese economy

battered stock markets, while tensions simmered in the Korean peninsula and the Middle East.

Relations between Saudi Arabia and Iran collapsed further stimulated further safe haven

buying. Gold fell 10% last year on fears higher U.S. rates would lift the opportunity cost of

holding non-yielding bullion.

In agri counter, spices revived with the exception of jeera, which further traded weak on

quality issue. Mostly firm sentiment witnessed in turmeric market on less production news. In

major turmeric growing regions mainly in Maharashtra and Karnataka may reduce the yield

due to lack of rainfall. Mentha prices declined despite weak arrivals. Guar prices declined

sharply in key markets due to higher arrivals and speculation. Even futures market traded in

the lower circuit. Lower arrivals effect was offset by the weak demand in domestic as well as

in the international market. Edible oils prices featured weak sentiment in various markets.

Demand concerns in oil seeds and edible oil from China are expected to take center stage in

January as demand slows due to slowdown of Chinese economy. Palm oil prices surged on low

import news.

WEEKLY COMMENTARY

COMMODITY UNIT 07.01.16 DIFFERENCEQTY. QTY.

BARLEY MT 2890.00 2870 -20CASTOR SEED MT 139385.00 141760 2375CHANA MT 191.00 0 -191CORIANDER MT 17205.00 13212 -3993COTTON SEED OILCAKE MT 3776.00 4775 999GUARGUM MT 29754.00 30180 426GUARSEED MT 27897.00 29099 1202JEERA MT 2407.00 2168 -239MAIZE MT 20968.00 21867 899RAPE MUSTARD SEED MT 9034.00 7999 -1035SOYABEAN MT 70818.00 70746 -72SUGAR MT 32063.00 17926 -14137TURMERIC MT 2131.00 1702 -429WHEAT MT 1262.00 1460 198

31.12.15 COMMODITY UNIT 07.01.16 DIFFERENCE

QTY. QTY.

CARDAMOM MT 32.40 29.30 -3.10

COTTON BALES 37900.00 38300.00 400.00

GOLD KGS 25.00 25.00 0.00

GOLD MINI KGS 7.70 15.10 7.40

GOLD GUINEA KGS 20.90 20.90 0.00

MENTHA OIL KGS 5412114.48 5214881.73 -197232.75

SILVER (30 KG Bar) KGS 18209.52 17761.27 -448.25

31.12.15

•China's State Reserve Bureau is planning to buy up 150,000 tonnes of copper from refiners who after years of rapid expansion are now coping with oversupply and unprofitable operations.

•China is building underground caverns capable of holding up to a quarter of its expanded strategic oil reserves by 2020.

•Euro zone core inflation slowed for the second month in a row in December.

•China's dry-bulk shipping industry will likely see a surge in bankruptcies this year as freight rates hit record lows.

•Japan's aluminium ingot imports for the first 11 months in 2015 were down 14% on a year earlier.

•As per reports received from the State Governments, till 31.12.15, 1,12,545.96 MT pulses seized under de-holding operations have been auctioned or offloaded through other options in the market to increase availability.- Ministry of Consumer Affairs, Food & Public Distribution

•India's oilmeal exports plummeted 85% to 59,818 tonnes in December from a year ago. - Solvent Extractors' Association of India

•Cotton production on the global front is likely to be around 22.89 million tons in season 2015-16, around 0.9% lower when compared to the estimates of previous month. - International Cotton Advisory Committee

•As on 31st December, 2015, 470 sugar mills are in operation in the country and they have produced 79.85 lac tons of sugar.- Indian Sugar Mills Association

WEEKLY STOCK POSITIONS IN WAREHOUSE (MCX)

12

®

NCDEX TOP GAINERS & LOSERS (% Change) MCX TOP GAINERS & LOSERS (% Change)

WEEKLY STOCK POSITIONS IN WAREHOUSE (NCDEX)

4.99 4.794.37

3.05

0.72

-12.60

-10.29

-7.30 -7.26

-5.56

-14.00

-12.00

-10.00

-8.00

-6.00

-4.00

-2.00

0.00

2.00

4.00

6.00

SILVERHEDGE

GOLD HEDGE CORIANDER TURMERIC

WHEATDELHI

MAIZERABI

GUARGUM

CRUDEOIL

GUARSEED

NEW STEELLONG

4.564.29

3.60

2.55

0.44

- 9.11 -8.99

-7.04- 6.71

-10.00

-8.00

-6.00

-4.00

-2.00

0.00

2.00

4.00

6.00

GOLD CARDAMOMSILVER

MININATURAL

GASCRUDE PALM

OILCRUDE

OILBR. CRUDE

OIL LEAD ZINC

Price movement of commodities in December 2015

In last month of the year 2015, highest gainer and highest loser, both were from

agri commodity complex. Cotton oilseed cake was the highest gainer in December

2015 due to increased mill use amid expectation of lower production of cotton in

India and expectation of falling World ending stocks. Kapas prices also moved up

with same reason. Sugar prices rose the highest monthly gain in December last year

on the estimates of higher export amid deficit in the international market. Oilseed

counters moved down on the multiple reasons. The high price of soybean in the

domestic market against the lower realization for meal and oil resulted in to

drastic fall in demand and export of soybean meal. RM Seed slipped on expectation

of higher yield and lower rapemeal export.

In spices counter, jeera and dhaniya prices dragged down whereas steady to firm

sentiment was witnessed in cardamom market. Jeera prices declined due to lower

export and domestic demand. Coriander prices plunged the most due to lower

quality supply in the spot market and possibility of a rise in sowing acreage in the

current season.

All the base metals, except nickel, witnessed its first monthly gain since April as lead

led the rally. Lead and zinc rose on worries short supply. Copper climbed on

speculation of production cuts in China will help reduce a supply glut. Nine of the

biggest copper producers have agreed to cut sales by 200,000 metric tonnes in the

first three months of 2016. Nickel continued to trade lower on higher stock position.

Bearish sentiments continued in bullion counters as the Federal Reserve rose

interest rates mid-December, making precious metals less attractive to those

investors seeking yield-bearing assets. Silver closed down too.

COMMODITY

COMMODITY EXCHANGE CONTRACT 07.01.16 CHANGE%

ALUMINIUM LME 3 MONTHS 1473.00 1475.00 0.14

COPPER LME 3 MONTHS 4609.50 4524.00 -1.85

LEAD LME 3 MONTHS 1745.50 1659.50 -4.93

NICKEL LME 3 MONTHS 8505.00 8505.00 0.00

ZINC LME 3 MONTHS 1568.00 1506.00 -3.95

GOLD COMEX FEB 1075.60 1107.80 2.99

SILVER COMEX MAR 13.84 14.34 3.63

LIGHT CRUDE OIL NYMEX FEB 36.76 33.27 -9.49

NATURAL GAS NYMEX FEB 2.33 2.38 2.06

01.01.16

PRICES OF METALS IN LME/ COMEX/ NYMEX (in US $)

WEEKLY STOCK POSITIONS IN LME (IN TONNES)

COMMODITY STOCK POSITION STOCK POSITION DIFFERENCE

31.12.15 07.01.16

ALUMINIUM 2901200 2882800 -18400

COPPER 236975 235850 -1125

NICKEL 444702 440358 -4344

LEAD 191675 190900 -775

ZINC 465975 457325 -8650

INTERNATIONAL COMMODITY PRICES

COMMODITY EXCHANGE CONTRACT UNIT 01.01.16 07.01.16 CHANGE(%)

Soya CBOT MAR Cent per Bushel 856.00 864.25 0.96

Maize CBOT MAR Cent per Bushel 351.50 353.00 0.43

CPO BMD MAR MYR per MT 2436.00 2422.00 -0.57

Sugar LIFFE MAR 10 cents per MT 419.20 428.80 2.29

13

®

SPOT PRICES (% change)

-7.64

-4.83

-2.76

-2.53

-1.60

-1.41

-1.26

-1.07

-0.83

-0.63

-0.56

-0.04

0.00

0.07

0.25

0.28

1.37

1.53

2.08

3.54

-10.00 -8.00 -6.00 -4.00 -2.00 0.00 2.00 4.00 6.00

GUAR GUM (JODHPUR)

GUAR SEED (JODHPUR)

SOYABEAN (INDORE)

MUSTARD (JAIPUR)

REFINED SOYA OIL (INDORE)

SUGAR (KOLKATA)

CHILLI (GUNTUR)

CORIANDER (KOTA)

BARLEY (JAIPUR)

JEERA (UNJHA)

GUR (MUZAFFARNGR.)

WHEAT (DELHI)

CRUDE PALM OIL (KANDLA)

COTTON (KADI)

COTTON SEED OIL CAKE (AKOLA)

TURMERIC (NIZAMABAD)

PEPPER MALABAR GAR (KOCHI)

SILVER 5 KG (DELHI)

CHANA (DELHI )

RAW JUTE (KOLKATA)

CURRENCY

Currency Table

Currency Pair Open High Low Close

USD/INR 66.49 67.15 66.46 67.10

EUR/INR 72.45 73.16 71.80 72.87

GBP/INR 97.94 99.44 97.59 97.75

JPY/INR 55.54 57.74 55.54 57.06

(Source: Reliable Software, Open: Monday 9.00 AM IST, Close: Thursday (5.00 PM IST)

News Flows of last week

06th Jan U.S. services sector growth slowed in December

06th Jan Euro zone economic sentiment improved as unemployment falls

06th Jan China forex reserves fall $512.66 billion in 2015, biggest drop on record

07th Jan U.S. jobs market holding firmer despite slowing growth

07th Jan Yuan hit weakest since Feb 2011 on fresh low midpoint

07th Jan The Canadian dollar's plunged to a 12-year low

07th Jan U.S. jobs market seen fairly healthy, despite slowing economy

EUR/INR (JAN) contract closed at 72.87 on 07th January'16. The contract made its

high of ̀ 73.16 on 04th January'16 and a low of ̀ 71.80 on 06th January '16 (Weekly

Basis). The 14-day Exponential Moving Average of the EUR/INR is currently at

`72.51

On the daily chart, EUR/INR has Relative Strength Index (14-day) value of 54.24.

One can buy above 73.00 for a target of 74.00 with the stop loss of 72.45.

JPY/NR (JAN) contract closed at 57.06 on 07th January'16. The contract made its high of `57.74 on 07th January'16 and a low of `55.54 on 04th January'16 (Weekly Basis). The 14-day Exponential Moving Average of the JPY/INR is currently at ̀ 55.66

On the daily chart, JPY/INR has Relative Strength Index (14-day) value of 74.65. One can buy above 57.05 for a target of 58.10 with the stop loss of 56.45

Market Stance

Indian rupee has some shaky starts during last week trading session as it

weakened to a three week low as against the dollar on persistent demand for

the American currency from banks and importers amid sharp fall in equities. In

a surprise move, China's central bank lowered the Yuan's value against the US

dollar, sending the domestic stock markets tumbling. In worldwide trade, the

dollar edged higher against the other major currencies, as heightened

concerns over global geopolitical tensions continued to dampen demand for

riskier assets after North Korea confirmed that it had conducted a nuclear

test. In other currencies Sterling fell to its weakest since April against the

dollar. Moreover, China's foreign exchange reserves, the world's largest,

posted their biggest annual drop on record in 2015. Nearly two-thirds of the

drop came between August and December, hinting at the scope of the central

bank's attempts to stabilise the Yuan after its surprise devaluation in August

panicked markets.

EUR/INR

USD/INR (JAN) contract closed at `67.10 on 07th January'16. The contract made

its high of `67.15 on 07th January'16 and a low of `66.46 on 04th January'16

(Weekly Basis). The 14-day Exponential Moving Average of the USD/INR is

currently at ̀ 66.71.

On the daily chart, the USD/INR has Relative Strength Index (14-day) value of

61.36. One can buy 67.10 for the target of 67.80 with the stop loss of 66.75.

GBP/INR (JAN) contract closed at 97.75 on 07th January'16. The contract made its high of `99.44 on 04th January'16 and a low of `97.58 on 07th January'16 (Weekly Basis). The 14-day Exponential Moving Average of the GBP/INR is currently at ̀ 98.80

On the daily chart, GBP/INR has Relative Strength Index (14-day) value of 35.06. One can buy above 98.50 for a target of 99.50 with the stop loss of 98.00

`

USD/INRTechnical Recommendation

Economic gauge for the next week

Date Currency Event Previous

12th Jan GBP NIESR GDP Estimate (3M) 0.6

13th Jan EUR Non-monetary policy's ECB meeting

14th Jan GBP BoE Asset Purchase Facility 375

14th Jan GBP BoE Interest Rate Decision 0.5

14th Jan GBP Monetary Policy Summary

14th Jan GBP BOE MPC Vote Cut 0

14th Jan GBP BOE MPC Vote Unchanged 8

14th Jan EUR ECB Monetary Policy Meeting Accounts

15th Jan USD Retail Sales ex Autos (MoM) 0.4

15th Jan USD Retail Sales (MoM) 0.2

GBP/INR JPY/INR

14

®

IPO

IPO NEWSIPO NEWS

VLCC gets Sebi nod for ̀ 400 crore IPO Capital markets regulator Sebi has given clearance to beauty and wellness firm VLCC Health Care to raise at least `400 crore through IPO to fund its expansion in domestic as well as international markets. The firm, which had filed draft red herring prospectus (DRHP) with Sebi on September 23, seeking permission for an IPO, obtained clearance from Sebi on December 29. As per the draft papers, the initial public offer (IPO) comprises fresh issue of shares worth Rs 400 crore and an offer for sale of up to 37.67 lakh equity shares by the existing shareholders - Indivision India Partners and Leon International. The company plans to sell up to 18 lakh equity shares for ̀ 100 crore through a pre-IPO placement of its shares to the institutional investors. The proceeds of the issue will be utilised for setting up VLCC Wellness Centres in India and abroad. Besides, the firm plans to establish VLCC Institutes in the country. In addition, funds will also be used for payment of loans, brand development and general corporate purpose, among others. Founded by Vandana Luthra in 1989, the company has operations in India, Sri Lanka, Bangladesh, Nepal, Malaysia, Singapore, the UAE, Oman, Bahrain, Qatar, Kuwait, Saudi Arabia and Kenya. ICICI Securities, Citigroup Global Markets India and Axis Capital are the merchant bankers for the proposed IPO. The shares are proposed to be listed on BSE and NSE.

L&T Infotech Gets Sebi Clearance For ̀ 2,000-crore IPOL&T Infotech, a subsidiary of engineering giant Larsen & Toubro, has received capital markets regulator Securities and Exchange Board of India's (Sebi) approval to float an initial public offering worth ̀ 2,000 crore. The issue comprises an offer for sale of up to 1,75,00,000 equity shares of face value of Rs 1 each by Larsen & Toubro. The firm, which had filed draft red herring prospectus (DRHP) with Sebi on September 28 seeking permission for an IPO, obtained clearance from capital markets regulator on December 31. Last month, a company official had said that L&T Infotech is looking to raise over ̀ 2,000 crore through the initial public offer (IPO) and the public issue is expected to hit the capital markets in the last quarter of 2015-16. Citigroup Global Markets India, Kotak Mahindra Capital Company, Barclays Bank Plc and ICICI Securities are stated to manage to issue. Equity shares offered through the issue are proposed to be listed on BSE and NSE. L&T Infotech will be the second unit of the parent company to go public. Company's financial arm L&T Finance Holdings Ltd was listed in 2011. L&T Infotech currently has a headcount of more than 20,000 people and has Chevron Corp., Hitachi Ltd and Lafarge SA as its top clients.

International Tractors plans to raise ̀ 1,200 crore via IPO in 2016International Tractors Ltd (ITL), the makers of Sonalika tractors, is planning to raise as much as ̀ 1,200 crore through an initial public offering (IPO), according to three people aware of the development, who spoke on condition of anonymity. The Delhi-based company is the third largest maker of tractors in the country. Global private equity major Blackstone Group Lp, which invested $100 million for a 12.5% stake in the company in 2012, is looking to make a partial exit through the IPO, said a second person aware of the development. A large portion of the IPO will be an offer for sale from Blackstone. The 20-year-old firm had sales close to ̀ 4,000 crore in 2014-15, according to the third person cited above. The company is about to start a new production facility with a capacity of 40,000 units, taking its total production capacity to 100,000 units a year. Though most tractor makers were hit by this year's weak monsoon, ITL has performed relatively better because of robust exports. During April-September, ITL's tractor sales fell 16.7% to 30,209 units from 36,279 units a year ago. Mahindra and Mahindra group saw its tractor sales decline 21.8% to 101,289 units and TAFE's sales declined 21.2% to 58,828 units.

SP Apparels files IPO papers with SebiJoining the IPO bandwagon, Coimbatore-based SP Apparels has filed draft papers with capital markets regulator Sebi to raise at least `215 crore through its initial public offer. The company intends to garner up to ̀ 215 crore through fresh issue of shares, while its existing shareholders will offload 9,00,000 equity shares, as per the Draft Red Herring Prospectus (DRHP) filed with Sebi. Established in 1989, the company manufactures and exports knitted garments for infants and children. The firm also manufactures and retails menswear in India under the brand 'Crocodile'. The company said that proceeds from the fresh issue will be utilised for repayment of debt, expansion and modernisation of manufacturing facility at Salem in Tamil Nadu and opening of new stores for the sale of 'Crocodile' products. The funds raised will be also used for addition of balancing machineries for its existing dyeing unit at Sipcot, Perundurai in Tamil Nadu and other general corporate purposes. The company intends to list its shares on BSE and NSE. The book running lead manager to the issue is Motilal Oswal Investment Advisors and Centrum Capital.

SME watch: Fourth Dimension's IPO sees slow startThe initial public offering (IPO) of Fourth Dimension Solutions on the NSE's SME platform Emerge had seen a slow start, with total bids for just 28,000 shares so far, which represents 0.01 times of the 28,92,000 shares up for sale. The IPO price was fixed at ̀ 30 apiece, which represents a premium of ̀ 20 on the face value of ̀ 10 per share. The market lot was fixed at ̀ 4,000 equity shares and in multiples thereafter, suggesting any investor interested in the IPO will have to make a bid worth at least `1,20,000. For retail investors, there was a ceiling of `2,00,000 on bids for SME IPOs. The limit for bids by market makers was set at 1,48,000 equity shares. Sarthi Capital Advisors is the leading managers of the issue. The company, which had generated negative cash flow in the past four years, intends to use the proceeds to meet its working capital requirements.

Sebi asks two firms to repay investor money Markets regulator Sebi has ordered two firms - Sunplant Constructions and Krutibibha Corporation - to refund the money they had raised illegally from investors. Besides barring the firms and their directors from capital markets for four years, Securities and Exchange Board of India (Sebi) also directed them to pay 15 per cent interest annually along with the refund amount. A Sebi probe found Sunplant Constructions had raised about ̀ 24 crore by way of issuance of Redeemable Preference Shares (RPS) to 3,212 investors without complying with the public issue norm, while Krutibibha collected `3.84 crore by issuing preference shares to 2,081 people. Krutibibha claimed to have paid back around ̀ 2.57 crore to investors. Since the shares were issued to more than 50 persons by each company, they were required to list these securities on stock exchanges. However, the companies failed to comply with this norm. Accordingly, Sebi said the companies and their directors will refund the money "through the issuance of RPS...with an interest of 15 per cent per annum... from the date when the repayments became due to the investors till the date of actual payment." Besides, they will also have to issue public notice in all editions of two National Dailies (one English and one Hindi) and in one local daily with wide circulation, detailing the modalities for refund, including details of contact persons within 15 days. After completing the repayments, the firms will have to file a report of such completion with Sebi within a period of three months, certified by two independent Chartered Accountants. In case the firms fail to comply with the orders, Sebi will initiate attachment and recovery proceedings, besides registering a civil/criminal case against Sunplant Constructions and Krutibibha, among others. Besides, Sebi has barred the firms and their directors from the capital markets and said such debarment will be in place for four years from "the date of completion of refunds to investors" .

Thyrocare Technologies Limited files draft IPO papers Indian diagnostic company Thyrocare Technologies Ltd said on Thursday it had filed draft red herring prospectus with the country's market regulator for an initial public offering (IPO) of 10.7 million shares. Thyrocare said it plans to list on both the BSE and NSE exchanges. JM Financial, Edelweiss Financial and ICICI Securities are lead managers for the issue.

Narayana Hrudaya Pharma 6801.13 613.00 6-Jan-16 250.00 291.00 330.70 32.28

Dr Lal Pathlabs Pharma 4450.94 638.00 23-Dec-15 550.00 717.00 803.80 46.15

Alkem Lab Pharma 17863.01 1349.61 23-Dec-15 1050.00 1380.00 1467.35 39.75

S H Kelkar & Co. FMCG 3702.29 200.00 16-Nov-15 180.00 222.00 250.75 39.31

IPO TRACKER

Company Sector M.Cap(In `Cr.) Issue Size(in `Cr.) List Date Issue Price List Price Last Price %Gain/Loss(from Issue price)

*

*Closing prices as on 07-01-2016®

15

®

16

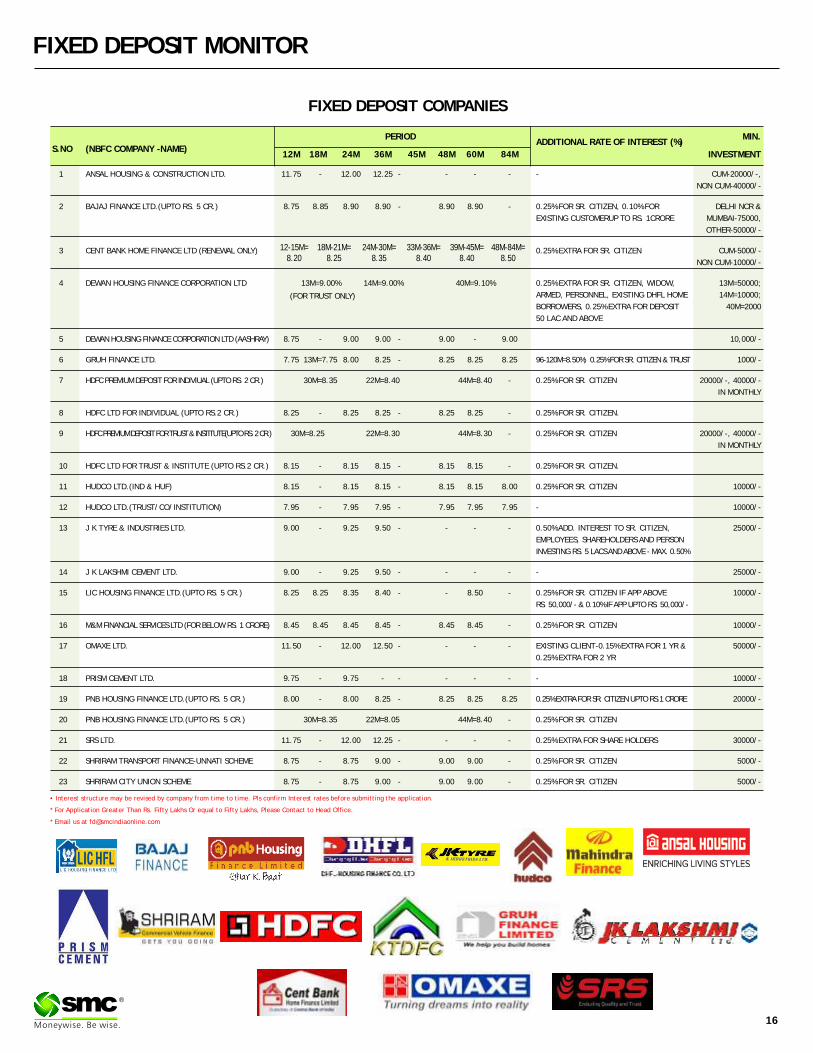

FIXED DEPOSIT MONITOR

• Interest structure may be revised by company from time to time. Pls confirm Interest rates before submitting the application.

* For Application Greater Than Rs. Fifty Lakhs Or equal to Fifty Lakhs, Please Contact to Head Office.

* Email us at [email protected]

FIXED DEPOSIT COMPANIES

PERIOD MIN.ADDITIONAL RATE OF INTEREST (%)

S.NO (NBFC COMPANY -NAME)12M 18M 24M 36M 45M 48M 60M 84M INVESTMENT

1 ANSAL HOUSING & CONSTRUCTION LTD. 11.75 - 12.00 12.25 - - - - - CUM-20000/-,

NON CUM-40000/-

2 BAJAJ FINANCE LTD.(UPTO RS. 5 CR.) 8.75 8.85 8.90 8.90 - 8.90 8.90 - 0.25% FOR SR. CITIZEN, 0.10% FOR DELHI NCR &

EXISTING CUSTOMERUP TO RS. 1CRORE MUMBAI-75000,

OTHER-50000/-

3 CENT BANK HOME FINANCE LTD (RENEWAL ONLY) 0.25% EXTRA FOR SR. CITIZEN CUM-5000/-

NON CUM-10000/-

4 DEWAN HOUSING FINANCE CORPORATION LTD 13M=9.00% 14M=9.00% 40M=9.10% 0.25% EXTRA FOR SR. CITIZEN, WIDOW, 13M=50000;

ARMED, PERSONNEL, EXISTING DHFL HOME 14M=10000;

BORROWERS, 0.25% EXTRA FOR DEPOSIT 40M=2000

50 LAC AND ABOVE

5 DEWAN HOUSING FINANCE CORPORATION LTD (AASHRAY) 8.75 - 9.00 9.00 - 9.00 - 9.00 10,000/-

6 GRUH FINANCE LTD. 7.75 13M=7.75 8.00 8.25 - 8.25 8.25 8.25 96-120M=8.50%; 0.25% FOR SR. CITIZEN & TRUST 1000/-

7 HDFC PREMIUM DEPOSIT FOR INDIVIUAL (UPTO RS. 2 CR.) 30M=8.35 22M=8.40 44M=8.40 - 0.25% FOR SR. CITIZEN 20000/-, 40000/-

IN MONTHLY

8 HDFC LTD FOR INDIVIDUAL (UPTO RS.2 CR.) 8.25 - 8.25 8.25 - 8.25 8.25 - 0.25% FOR SR. CITIZEN.

9 HDFC PREMIUM DEPOSIT FOR TRUST & INSTITUTE(UPTO RS. 2 CR.) 30M=8.25 22M=8.30 44M=8.30 - 0.25% FOR SR. CITIZEN 20000/-, 40000/-

IN MONTHLY

10 HDFC LTD FOR TRUST & INSTITUTE (UPTO RS.2 CR.) 8.15 - 8.15 8.15 - 8.15 8.15 - 0.25% FOR SR. CITIZEN.

11 HUDCO LTD.(IND & HUF) 8.15 - 8.15 8.15 - 8.15 8.15 8.00 0.25% FOR SR. CITIZEN 10000/-

12 HUDCO LTD.(TRUST/CO/INSTITUTION) 7.95 - 7.95 7.95 - 7.95 7.95 7.95 - 10000/-

13 J K TYRE & INDUSTRIES LTD. 9.00 - 9.25 9.50 - - - - 0.50% ADD. INTEREST TO SR. CITIZEN, 25000/-

EMPLOYEES, SHAREHOLDERS AND PERSON

INVESTING RS. 5 LACS AND ABOVE - MAX. 0.50%

14 J K LAKSHMI CEMENT LTD. 9.00 - 9.25 9.50 - - - - - 25000/-

15 LIC HOUSING FINANCE LTD.(UPTO RS. 5 CR.) 8.25 8.25 8.35 8.40 - - 8.50 - 0.25% FOR SR. CITIZEN IF APP ABOVE 10000/-

RS. 50,000/- & 0.10% IF APP UPTO RS. 50,000/-

16 M&M FINANCIAL SERVICES LTD (FOR BELOW RS. 1 CRORE) 8.45 8.45 8.45 8.45 - 8.45 8.45 - 0.25% FOR SR. CITIZEN 10000/-

17 OMAXE LTD. 11.50 - 12.00 12.50 - - - - EXISTING CLIENT-0.15% EXTRA FOR 1 YR & 50000/-

0.25% EXTRA FOR 2 YR

18 PRISM CEMENT LTD. 9.75 - 9.75 - - - - - - 10000/-

19 PNB HOUSING FINANCE LTD.(UPTO RS. 5 CR.) 8.00 - 8.00 8.25 - 8.25 8.25 8.25 0.25% EXTRA FOR SR. CITIZEN UPTO RS.1 CRORE 20000/-

20 PNB HOUSING FINANCE LTD.(UPTO RS. 5 CR.) 30M=8.35 22M=8.05 44M=8.40 - 0.25% FOR SR. CITIZEN

21 SRS LTD. 11.75 - 12.00 12.25 - - - - 0.25% EXTRA FOR SHARE HOLDERS 30000/-

22 SHRIRAM TRANSPORT FINANCE-UNNATI SCHEME 8.75 - 8.75 9.00 - 9.00 9.00 - 0.25% FOR SR. CITIZEN 5000/-

23 SHRIRAM CITY UNION SCHEME 8.75 - 8.75 9.00 - 9.00 9.00 - 0.25% FOR SR. CITIZEN 5000/-

(FOR TRUST ONLY)

12-15M=8.20

18M-21M=8.25

24M-30M=8.35

33M-36M=8.40

39M-45M=8.40

48M-84M=8.50

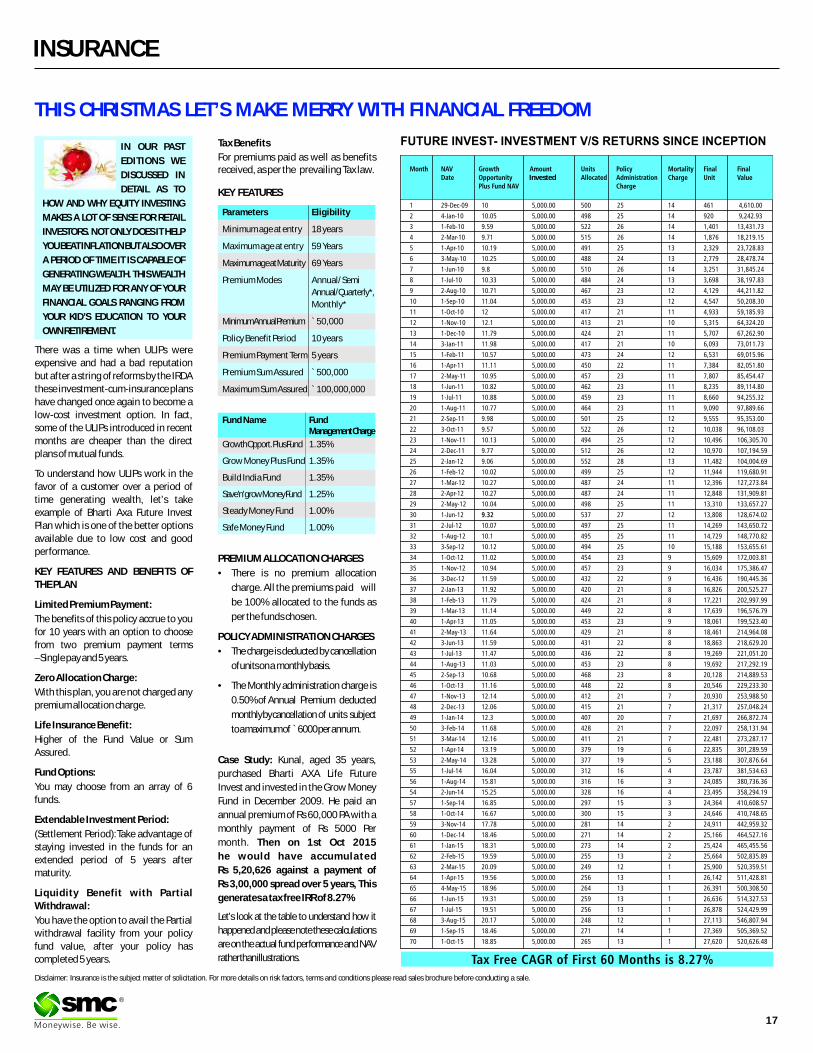

INSURANCE

®

THIS CHRISTMAS LET’S MAKE MERRY WITH FINANCIAL FREEDOM

17

PREMIUM ALLOCATION CHARGES

• There is no premium allocation

charge. All the premiums paid will

be 100% allocated to the funds as

per the funds chosen.

POLICY ADMINISTRATION CHARGES

• The charge is deducted by cancellation

of units on a monthly basis.

• The Monthly administration charge is

0.50% of Annual Premium deducted

monthly by cancellation of units subject

to a maximum of ̀ 6000 per annum.

Case Study: Kunal, aged 35 years,

purchased Bharti AXA Life Future

Invest and invested in the Grow Money

Fund in December 2009. He paid an

annual premium of Rs 60,000 PA with a

monthly payment of Rs 5000 Per

month. Then on 1st Oct 2015

he would have accumulated

Rs 5,20,626 against a payment of

Rs 3,00,000 spread over 5 years, This

generates a tax free IRR of 8.27%

Let’s look at the table to understand how it

happened and please note these calculations

are on the actual fund performance and NAV

rather than illustrations.

KEY FEATURES

There was a time when ULIPs were

expensive and had a bad reputation

but after a string of reforms by the IRDA

these investment-cum-insurance plans

have changed once again to become a

low-cost investment option. In fact,

some of the ULIPs introduced in recent

months are cheaper than the direct

plans of mutual funds.

To understand how ULIPs work in the

favor of a customer over a period of

time generating wealth, let’s take

example of Bharti Axa Future Invest

Plan which is one of the better options

available due to low cost and good

performance.

KEY FEATURES AND BENEFITS OF

THE PLAN

Limited Premium Payment:

The benefits of this policy accrue to you

for 10 years with an option to choose

from two premium payment terms

–Single pay and 5 years.

Zero Allocation Charge:

With this plan, you are not charged any

premium allocation charge.

Life Insurance Benefit:

Higher of the Fund Value or Sum

Assured.

Fund Options:

You may choose from an array of 6

funds.

Extendable Investment Period:

(Settlement Period):Take advantage of

staying invested in the funds for an

extended period of 5 years after

maturity.

Liquidity Benefit with Partial

Withdrawal:

You have the option to avail the Partial

withdrawal facility from your policy

fund value, after your policy has

completed 5 years.

IN OUR PAST

EDITIONS WE

DISCUSSED IN

DETAIL AS TO

HOW AND WHY EQUITY INVESTING

MAKES A LOT OF SENSE FOR RETAIL

INVESTORS. NOT ONLY DOES IT HELP

YOU BEAT INFLATION BUT ALSO OVER

A PERIOD OF TIME IT IS CAPABLE OF

GENERATING WEALTH. THIS WEALTH

MAY BE UTILIZED FOR ANY OF YOUR

FINANCIAL GOALS RANGING FROM

YOUR KID’S EDUCATION TO YOUR

OWN RETIREMENT.

Tax Benefits

For premiums paid as well as benefits received, as per the prevailing Tax law.

Disclaimer: Insurance is the subject matter of solicitation. For more details on risk factors, terms and conditions please read sales brochure before conducting a sale.

Parameters Eligibility

Minimum age at entry 18 years

Maximum age at entry 59 Years

Maximum age at Maturity 69 Years

Premium Modes Annual/ Semi

Annual/ Quarterly*,

Monthly*

Minimum Annual Premium `50,000

Policy Benefit Period 10 years

Premium Payment Term 5 years

Premium Sum Assured `500,000

Maximum Sum Assured `100,000,000

Fund Name Fund Management Charge

Growth Opport. Plus Fund 1.35%

Grow Money Plus Fund 1.35%

Build India Fund 1.35%

Save'n' grow Money Fund 1.25%

Steady Money Fund 1.00%

Safe Money Fund 1.00%

Invested

18

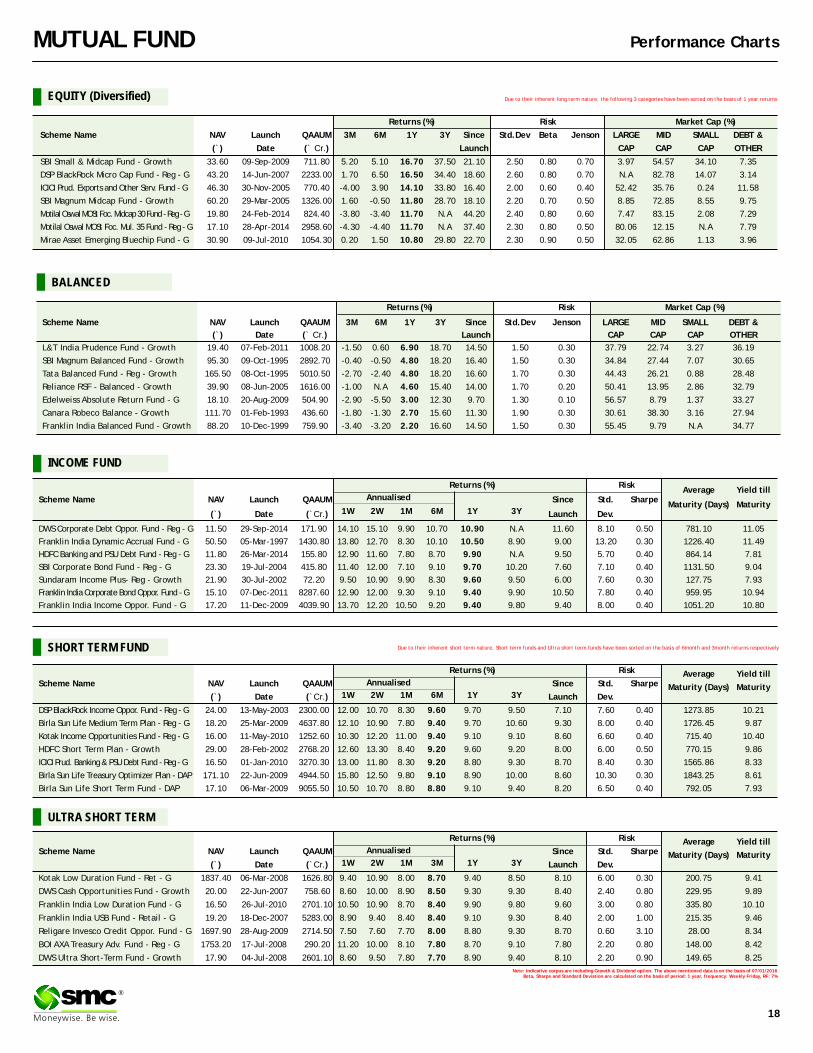

MUTUAL FUND Performance Charts

Returns (%) Risk Market Cap (%)

Scheme Name NAV Launch QAAUM 3M 6M 1Y 3Y Since Std.Dev Beta Jenson LARGE MID SMALL DEBT &

(`) Date (` Cr.) Launch CAP CAP CAP OTHER

SBI Small & Midcap Fund - Growth 33.60 09-Sep-2009 711.80 5.20 5.10 16.70 37.50 21.10 2.50 0.80 0.70 3.97 54.57 34.10 7.35