Why, who, when and how? An empirical view of the UK construction industry’s decision making process

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Why, who, when and how?

An empirical view of the UK construction industry’s

decision making process

Tony Williams

Building Value Ltd

the independent strategic advisor to the building materials, construction

& support services sectors

11 June 2004

UK construction industry is the focus of the study

Number three market in Europe

Accounts for 8% of GDP (below average)

Largest single domestic industry

Some 1.5 million employees

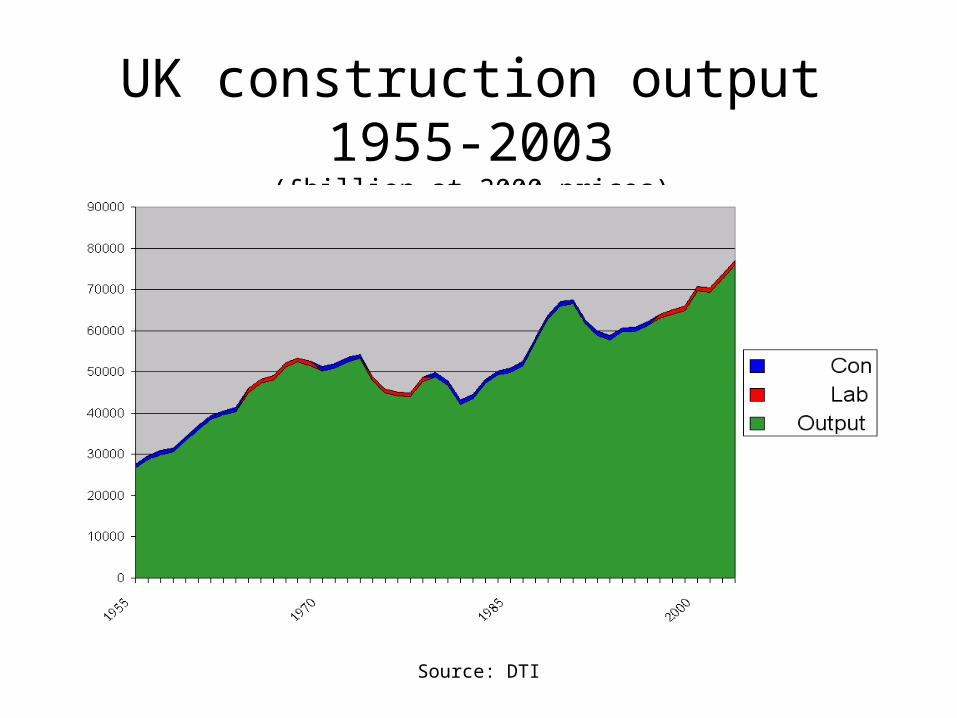

Source: DTI

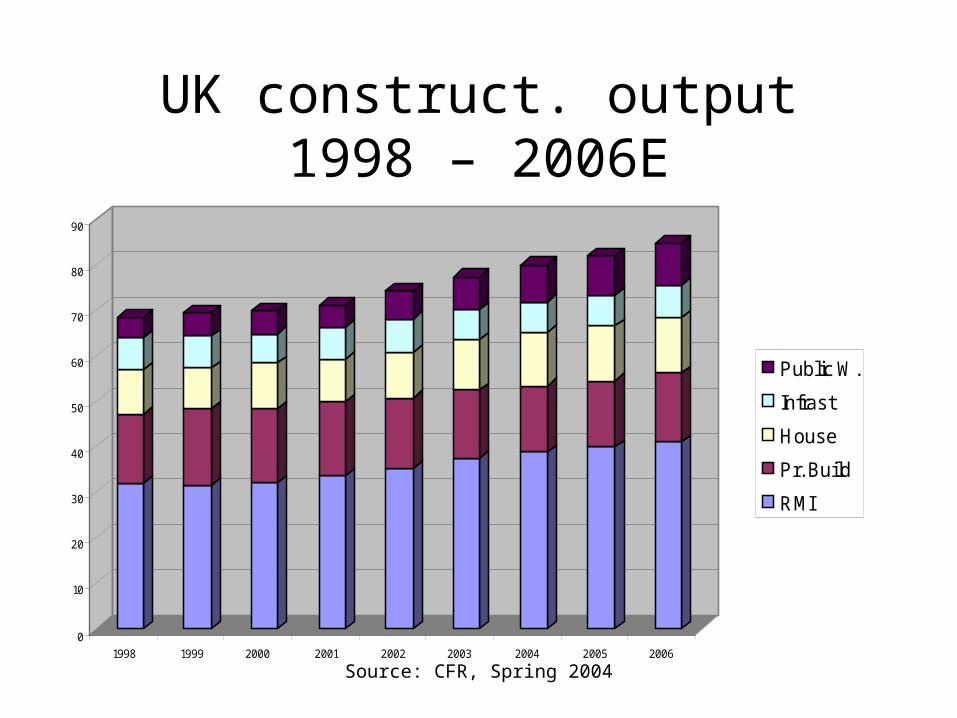

UK construction output 1955-2003

(£billion at 2000 prices)

UK construction - history

Sustained growth since 1994

Relatively impervious to politics, aside from mid-1970s

Three major collapses in 1974-7; 1980-1; and 1991-3

Source: CFR, Spring 2004

UK construct. output 1998 – 2006E

0

10

20

30

40

50

60

70

80

90

1998 1999 2000 2001 2002 2003 2004 2005 2006

Public W.

Infrast

House

Pr. Build

RMI

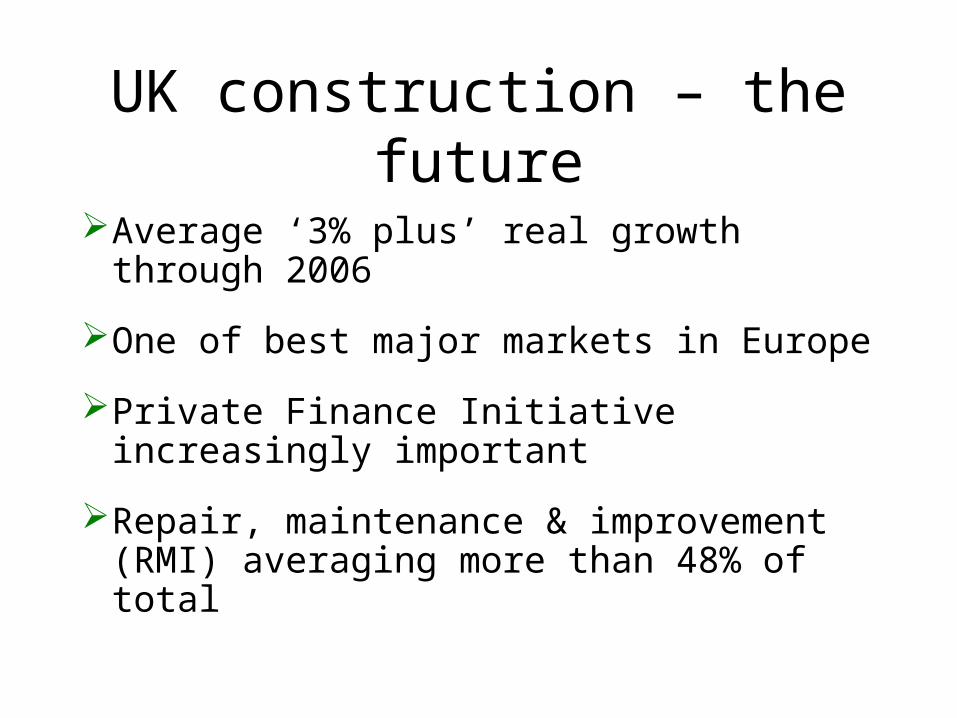

UK construction – the future

Average ‘3% plus’ real growth through 2006

One of best major markets in Europe

Private Finance Initiative increasingly important

Repair, maintenance & improvement (RMI) averaging more than 48% of total

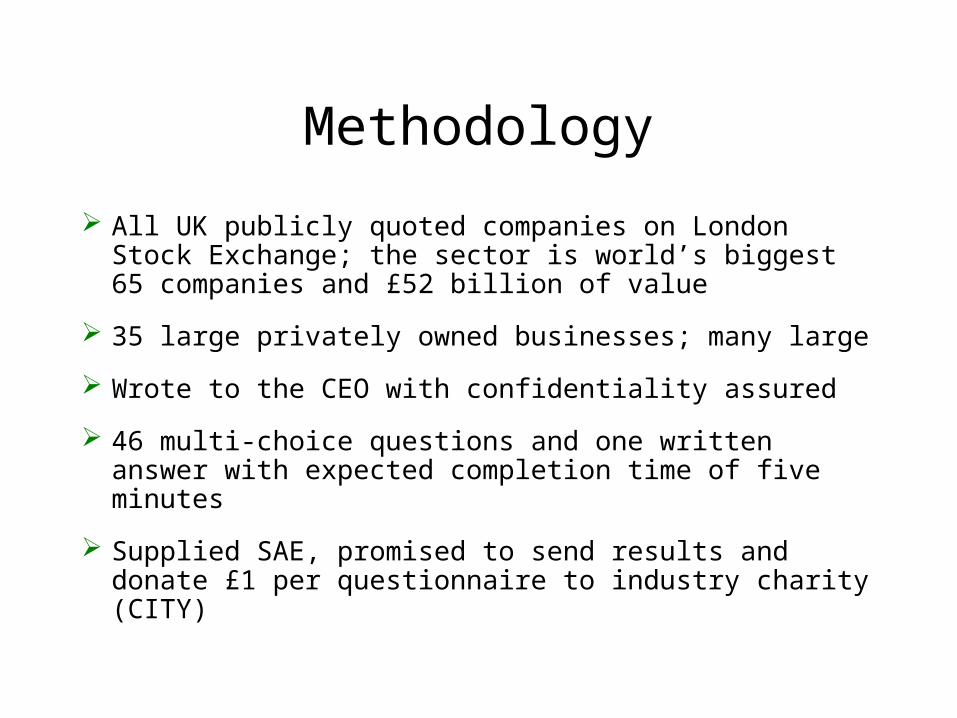

Methodology

All UK publicly quoted companies on London Stock Exchange; the sector is world’s biggest 65 companies and £52 billion of value

35 large privately owned businesses; many large

Wrote to the CEO with confidentiality assured

46 multi-choice questions and one written answer with expected completion time of five minutes

Supplied SAE, promised to send results and donate £1 per questionnaire to industry charity (CITY)

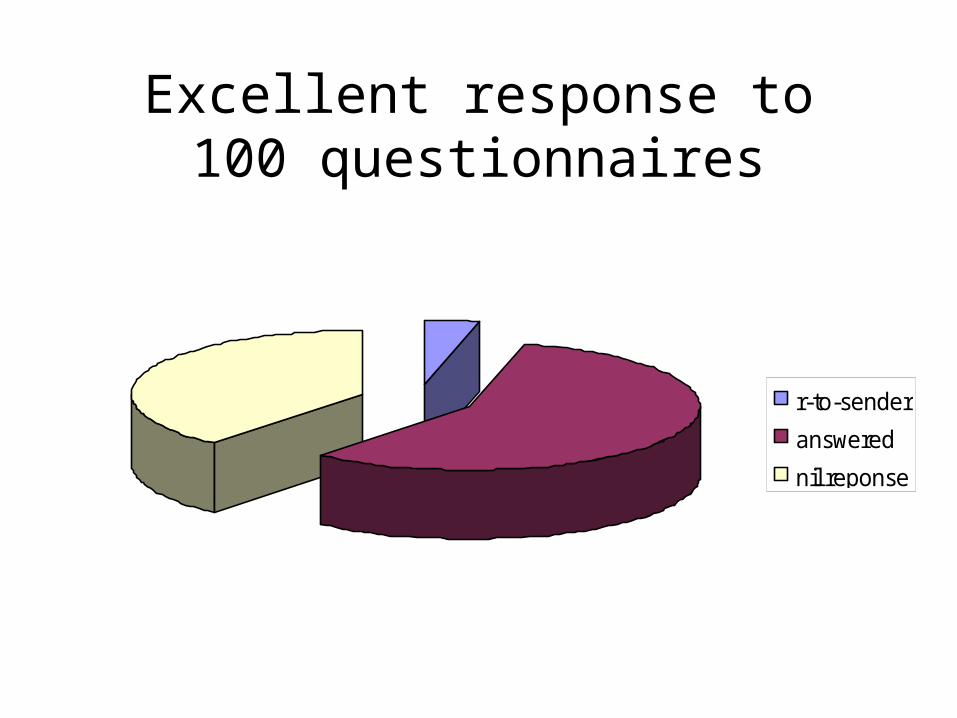

Excellent response to 100 questionnaires

r-to-sender

answered

nil reponse

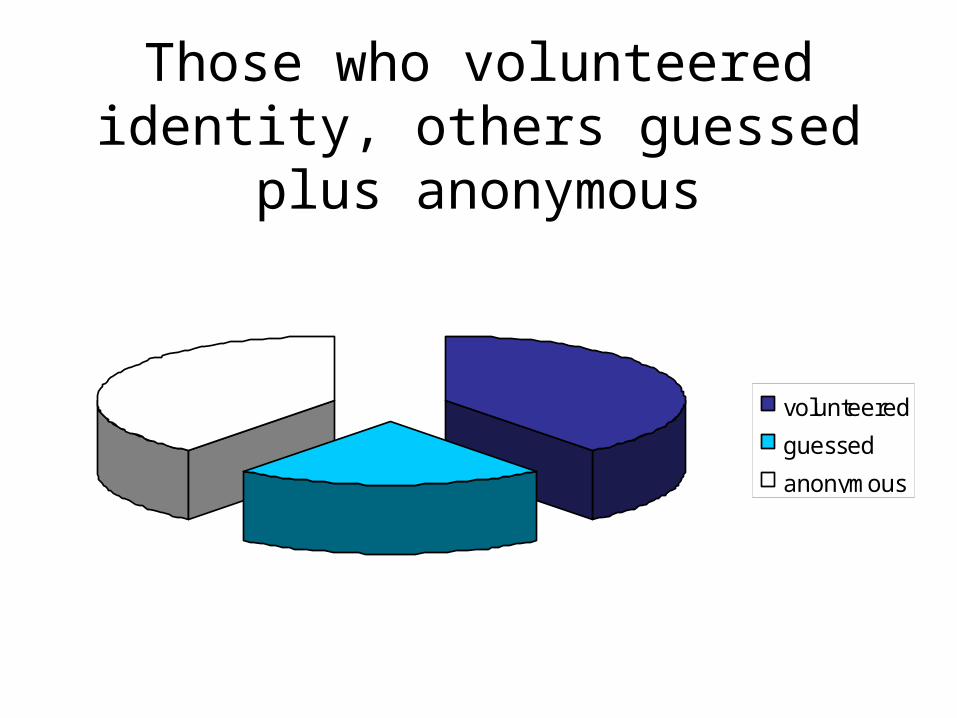

Those who volunteered identity, others guessed plus anonymous

volunteered

guessed

anonymous

Questionnaire idiosyncrasies

90% of respondents used ticks in the question boxes; with 5% each employing crosses or slashes

Two thirds used black pen, 30% blue and 3% red

The PA of one CEO called, emailed and wrote to say he didn’t have time to fill it in; another declined my invitation to the conference

5% eschewed the SAE and one send it back empty

40% of companies identified themselves

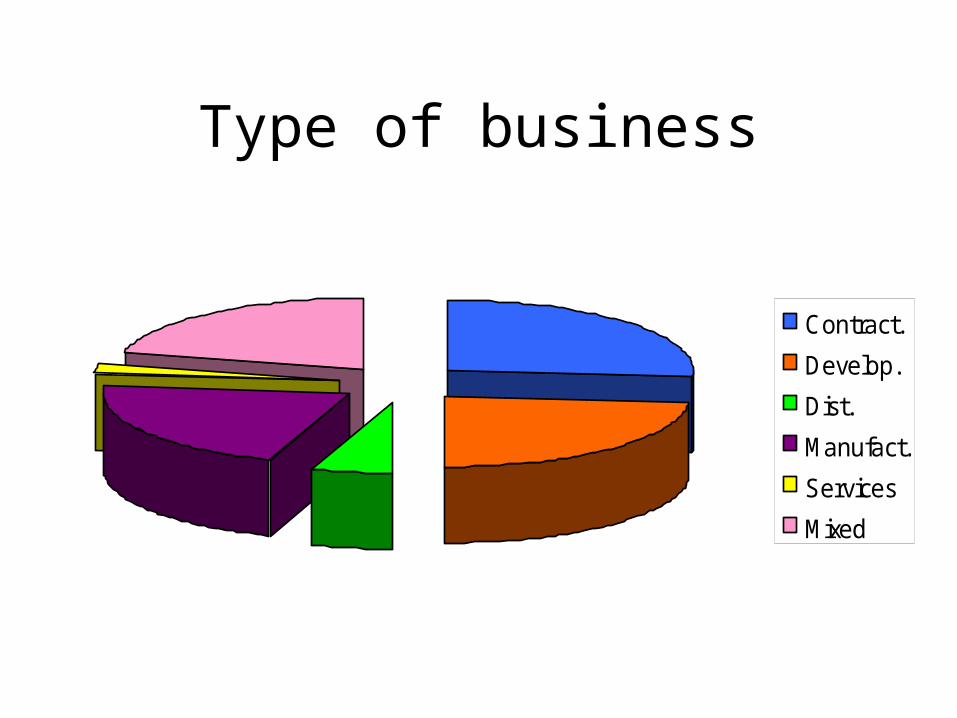

Type of business

Contract.

Develop.

Dist.

Manufact.

Services

Mixed

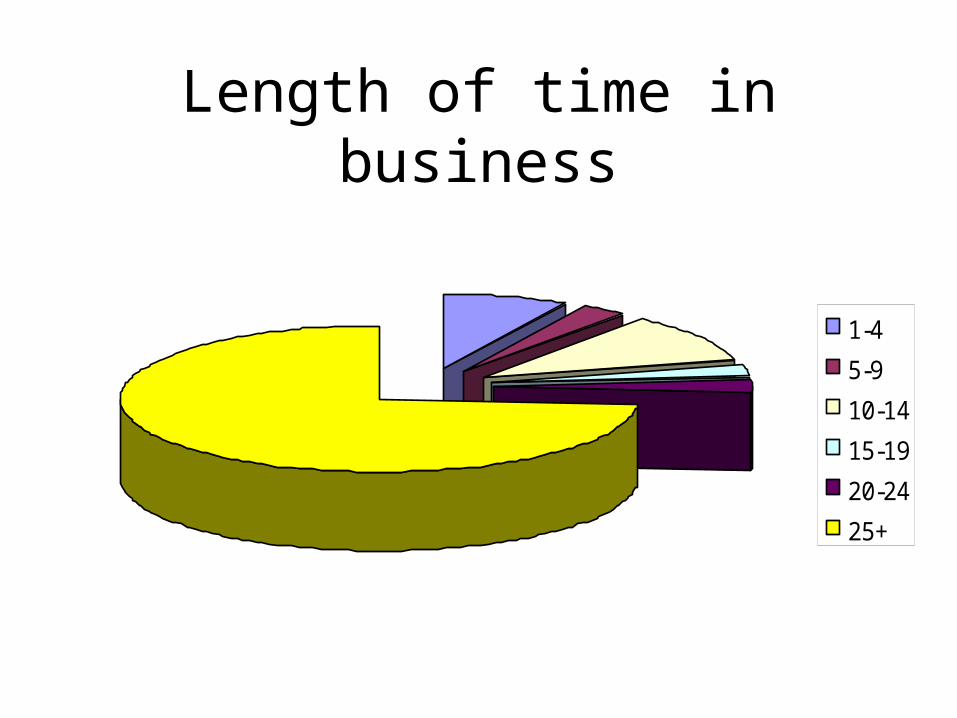

Length of time in business

1-4

5-9

10-14

15-19

20-24

25+

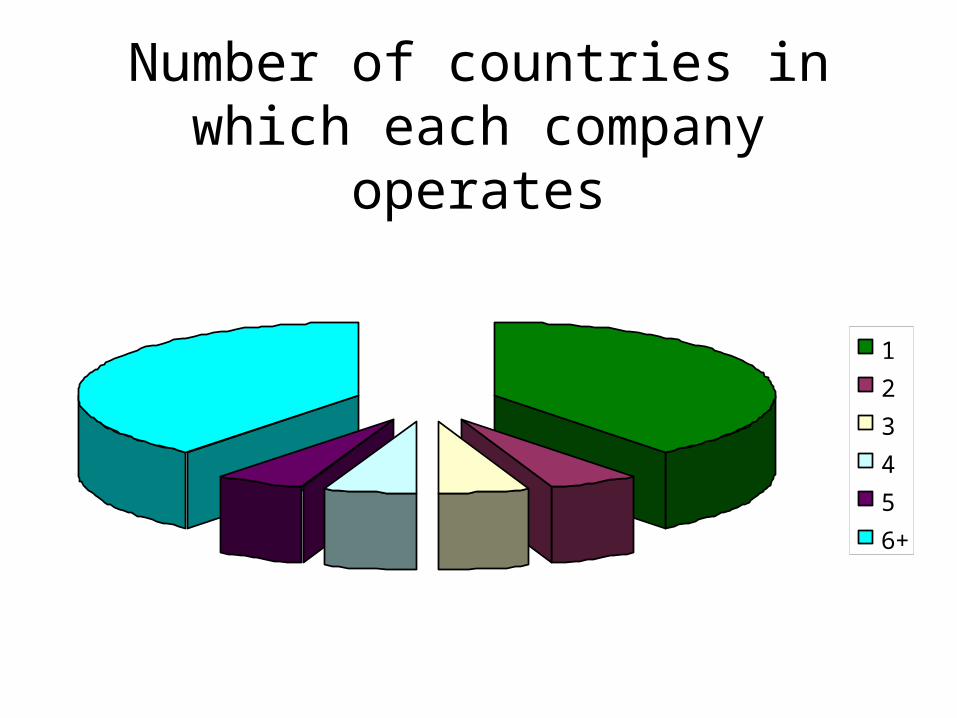

Number of countries in which each company operates

1

2

3

4

5

6+

“Those who run international businesses do so because they like to

travel. Very few construction companies make more from overseas operations than at home; so why do

they stay there?

UK contractor, 2004

Distribution of employees % in each band

0

5

10

15

20

25

30

1 - 99

100 - 499

500 - 999

1,000 - 2,499

2,500 - 4,999

5,000 - 9,999

10,000-19,999

20,000+

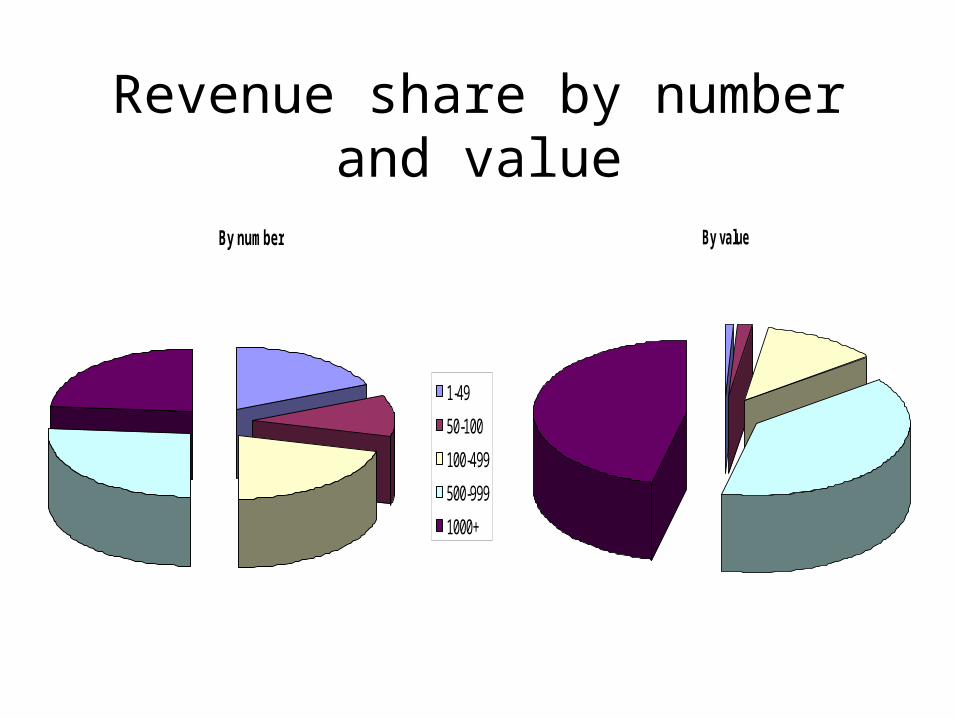

Revenue share by number and value

By valueBy number

1-49

50-100

100-499

500-999

1000+

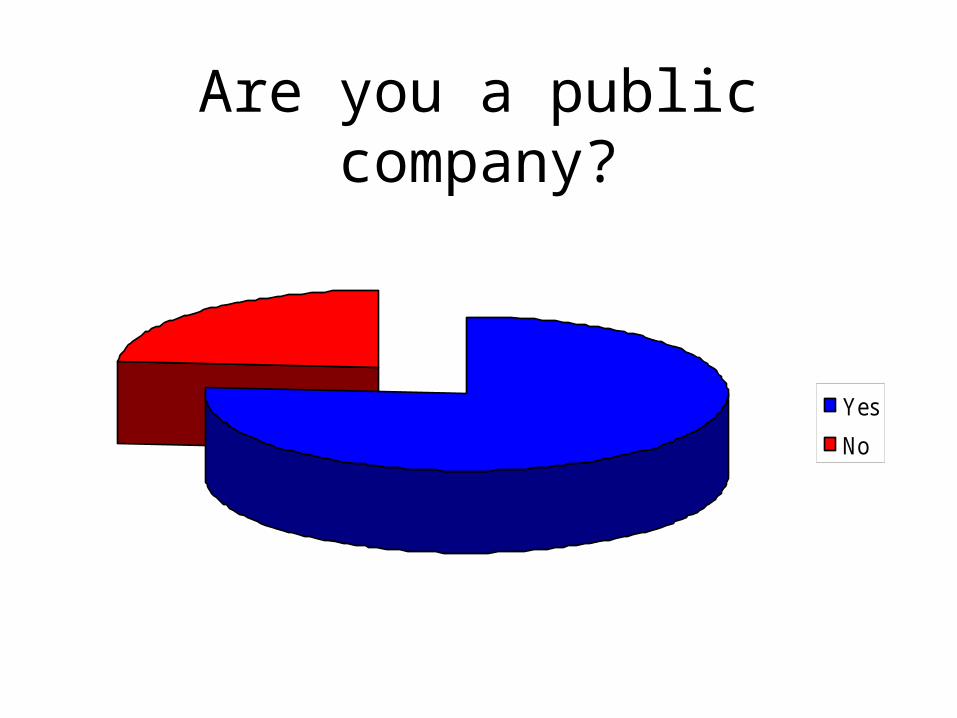

Are you a public company?

Yes

No

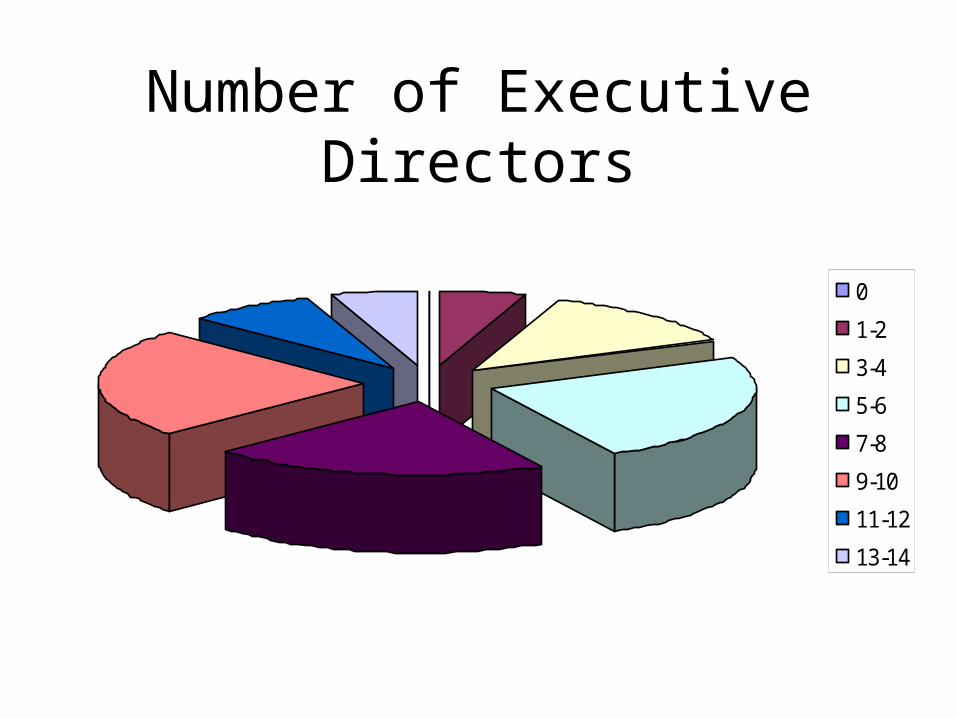

Number of Executive Directors

0

1-2

3-4

5-6

7-8

9-10

11-12

13-14

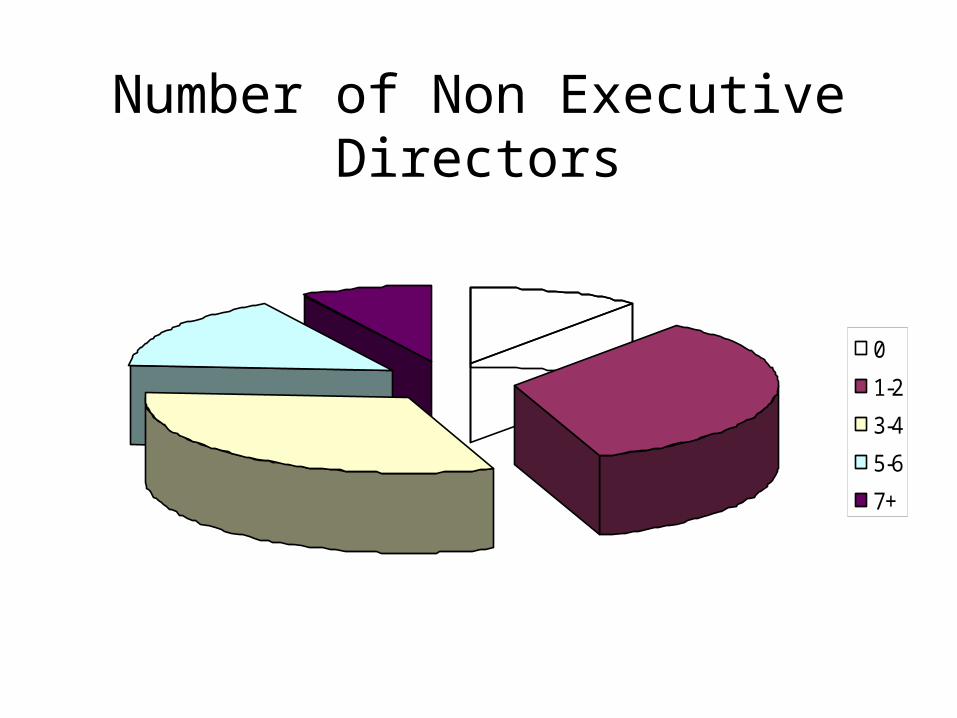

Number of Non Executive Directors

0

1-2

3-4

5-6

7+

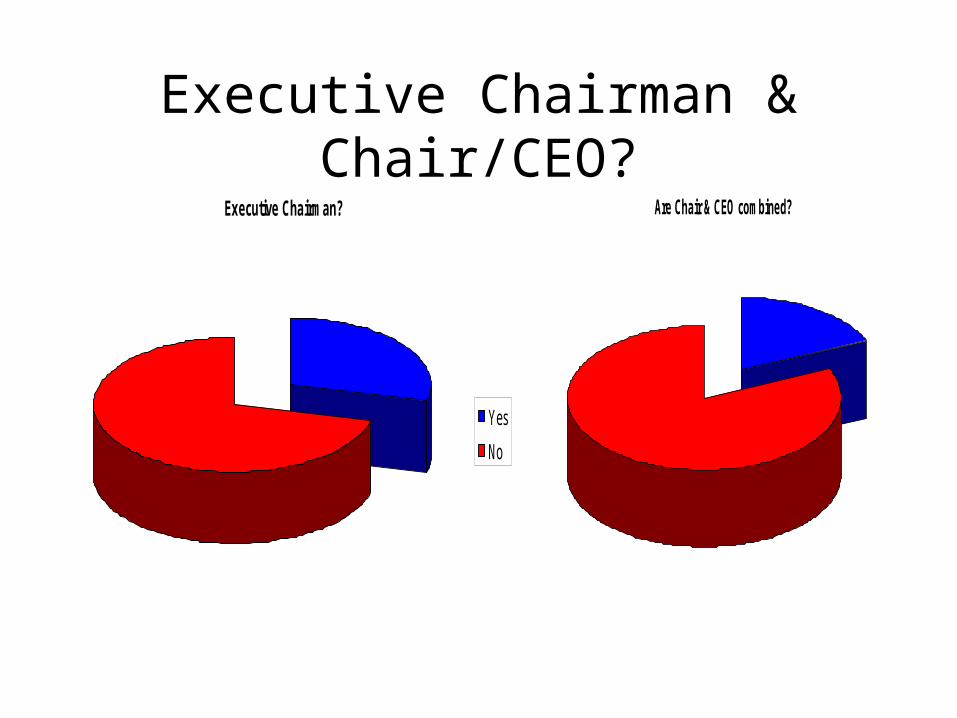

Executive Chairman & Chair/CEO?Executive Chairman?

Yes

No

Are Chair & CEO combined?

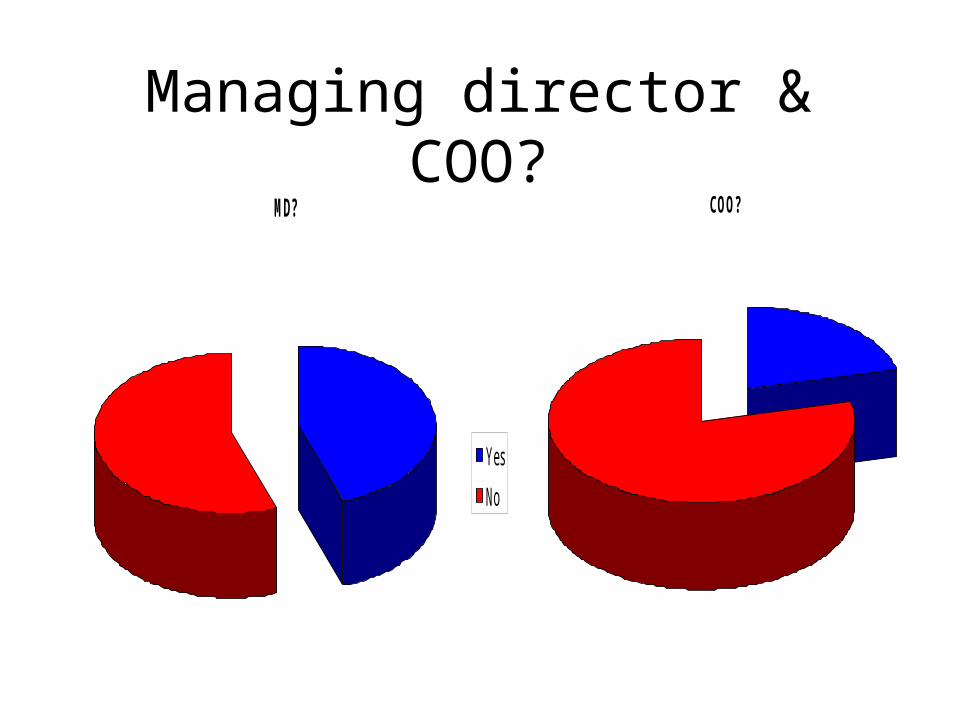

Managing director & COO?MD?

Yes

No

COO?

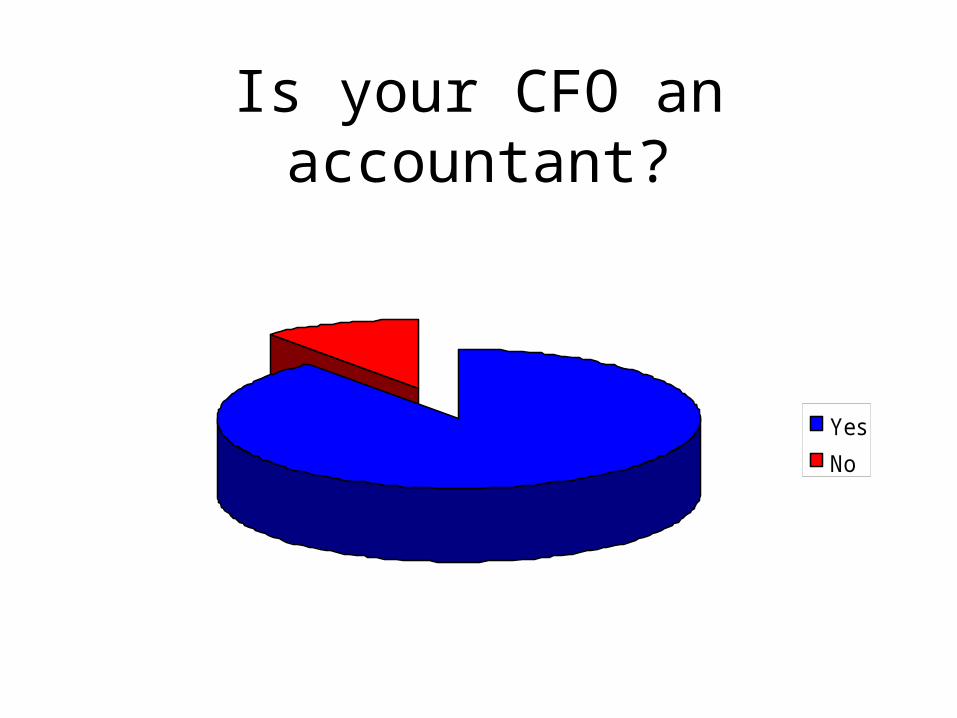

Is your CFO an accountant?

Yes

No

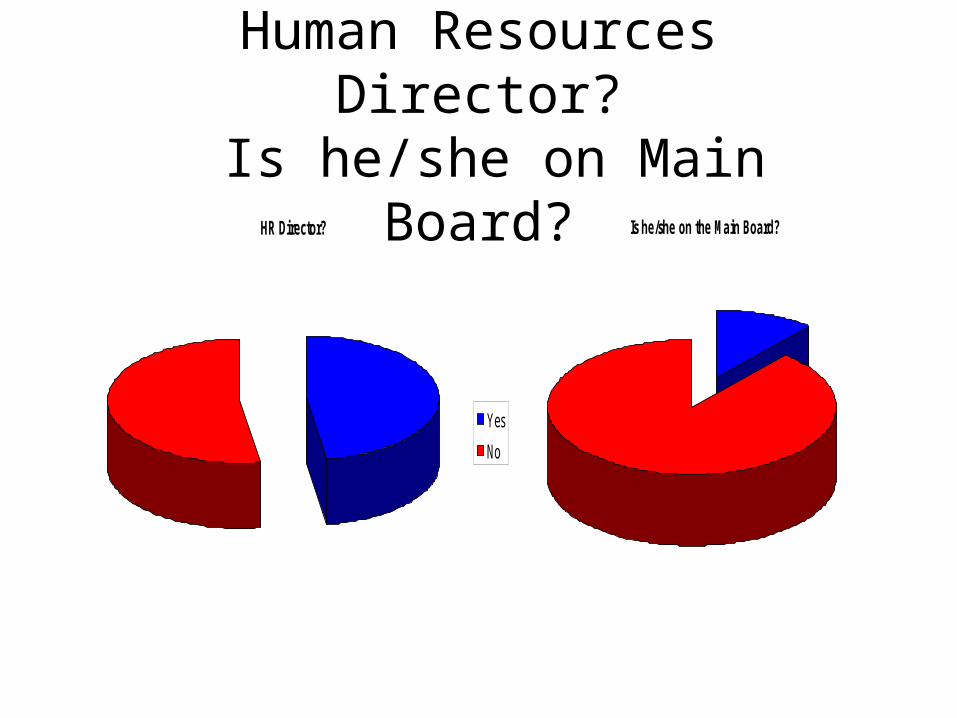

Human Resources Director? Is he/she on Main Board?

HR Director?

Yes

No

Is he/she on the Main Board?

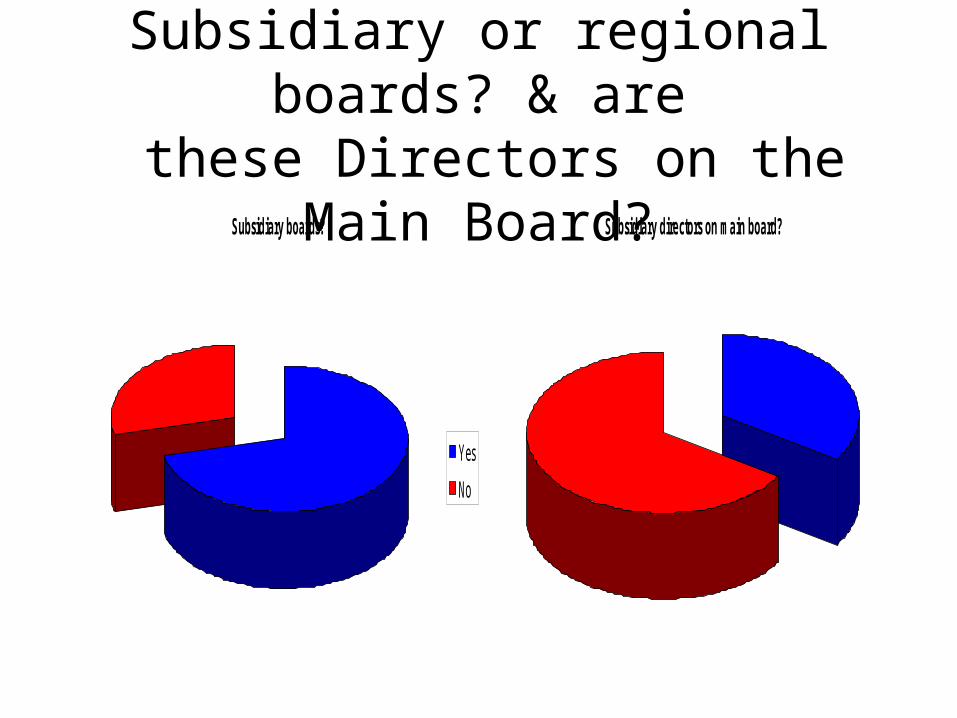

Subsidiary or regional boards? & are

these Directors on the Main Board?Subsidiary boards?

Yes

No

Subsidiary directors on main board?

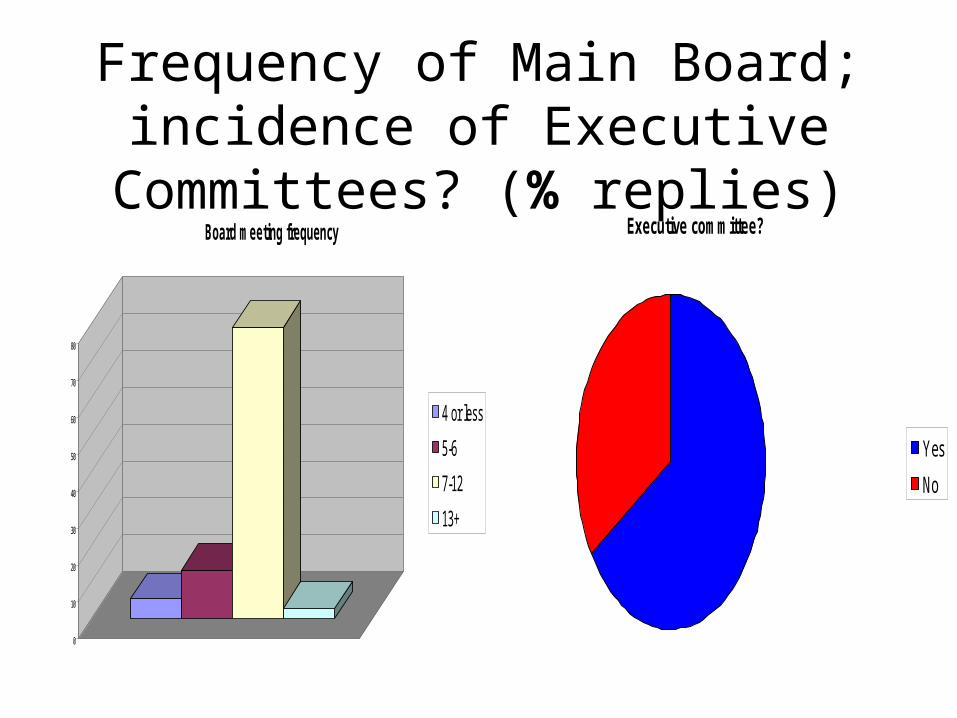

Frequency of Main Board; incidence of Executive

Committees? (% replies)Executive committee?

Yes

No

0

10

20

30

40

50

60

70

80

Board meeting frequency

4 or less

5-6

7-12

13+

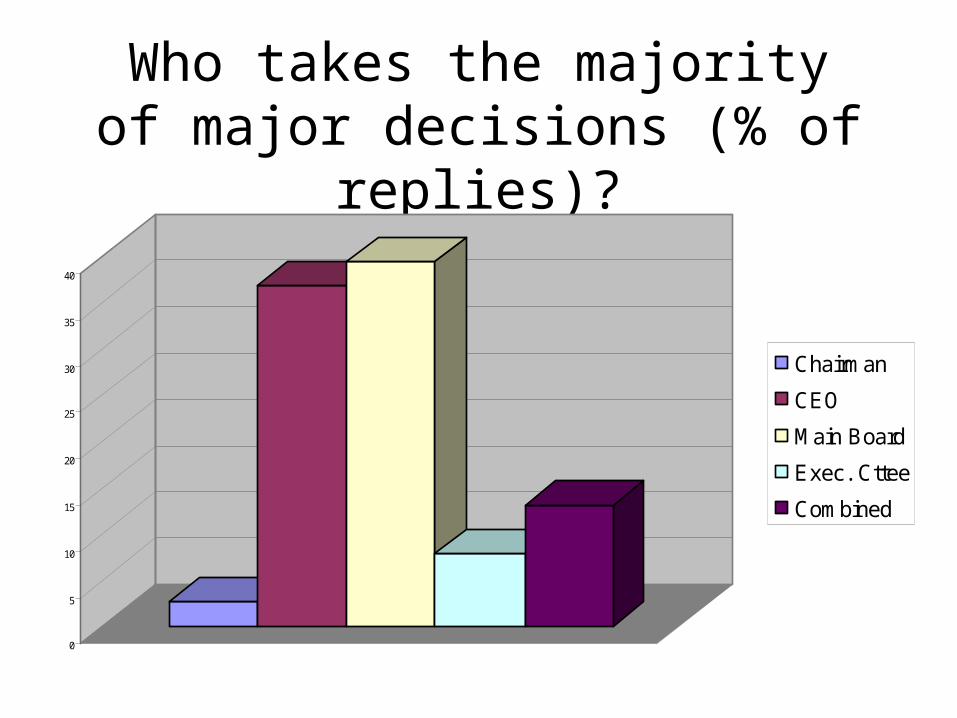

Who takes the majority of major decisions (% of replies)?

0

5

10

15

20

25

30

35

40

Chairman

CEO

Main Board

Exec. Cttee

Combined

“A poorly controlled area at large corporate level is strategic decision making that doesn’t hold firm for the medium term. This means subsidiary

managers never get to understand how they can be part of group-wide

goals......

“…The lack of political will ‘to stick to one’s knitting’, even if market

conditions change, means that a lot of second tier decision making is in

vain”

UK construction CEO, 2004

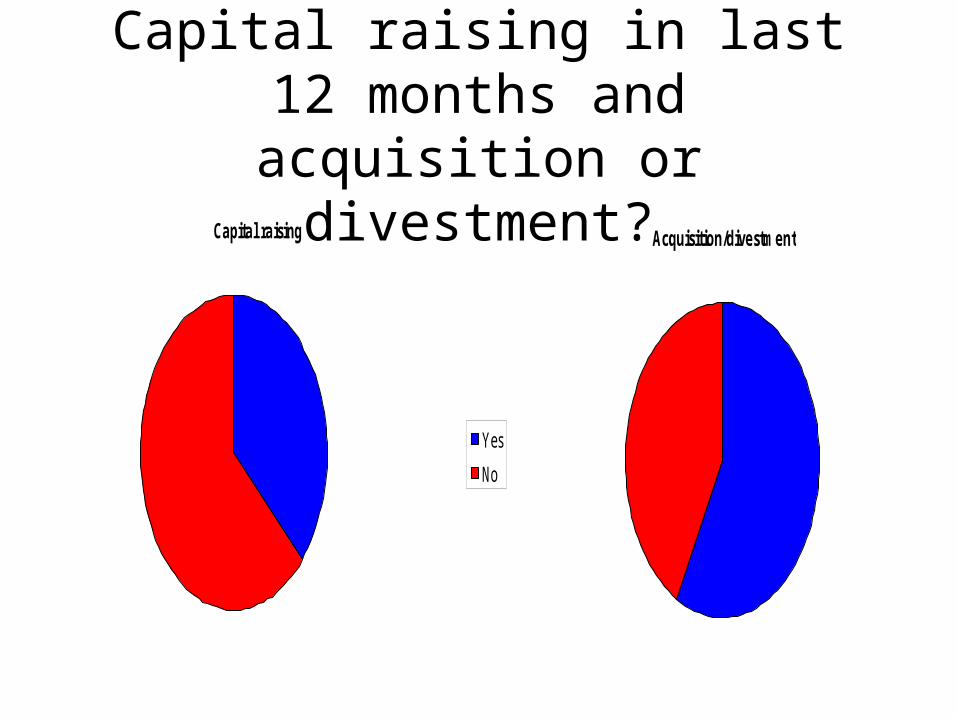

Capital raising in last 12 months and acquisition or

divestment?Capital raising

Yes

No

Acquisition/divestment

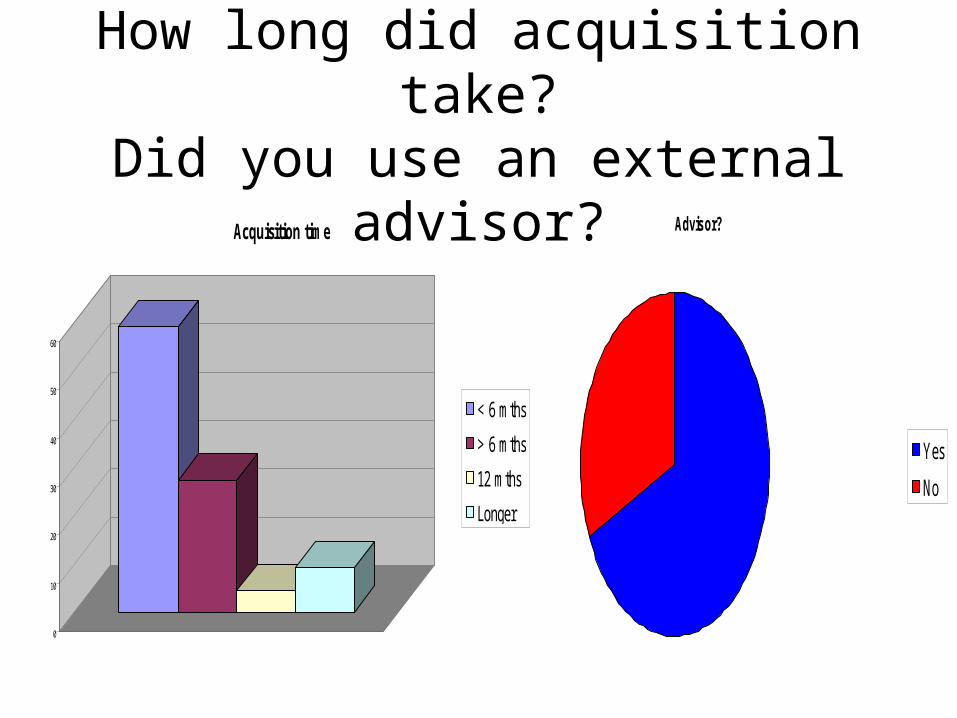

How long did acquisition take?

Did you use an external advisor? Advisor?

Yes

No

0

10

20

30

40

50

60

Acquisition time

< 6 mths

> 6 mths

12 mths

Longer

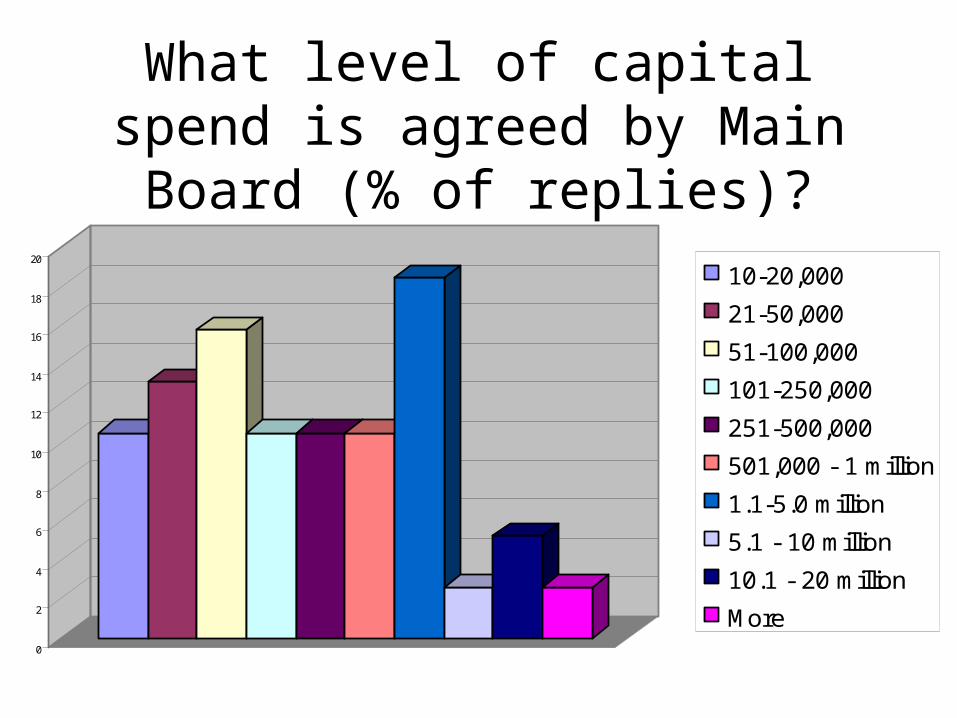

What level of capital spend is agreed by Main Board (% of replies)?

0

2

4

6

8

10

12

14

16

18

20

10-20,000

21-50,000

51-100,000

101-250,000

251-500,000

501,000 - 1 million

1.1-5.0 million

5.1 - 10 million

10.1 - 20 million

More

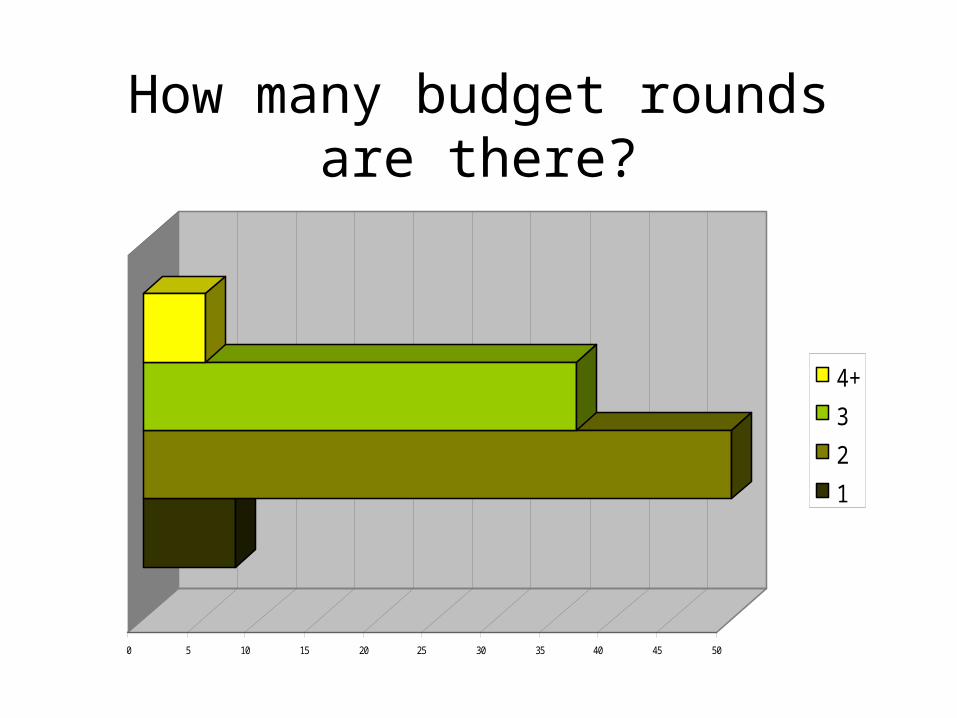

How many budget rounds are there?

0 5 10 15 20 25 30 35 40 45 50

4+

3

2

1

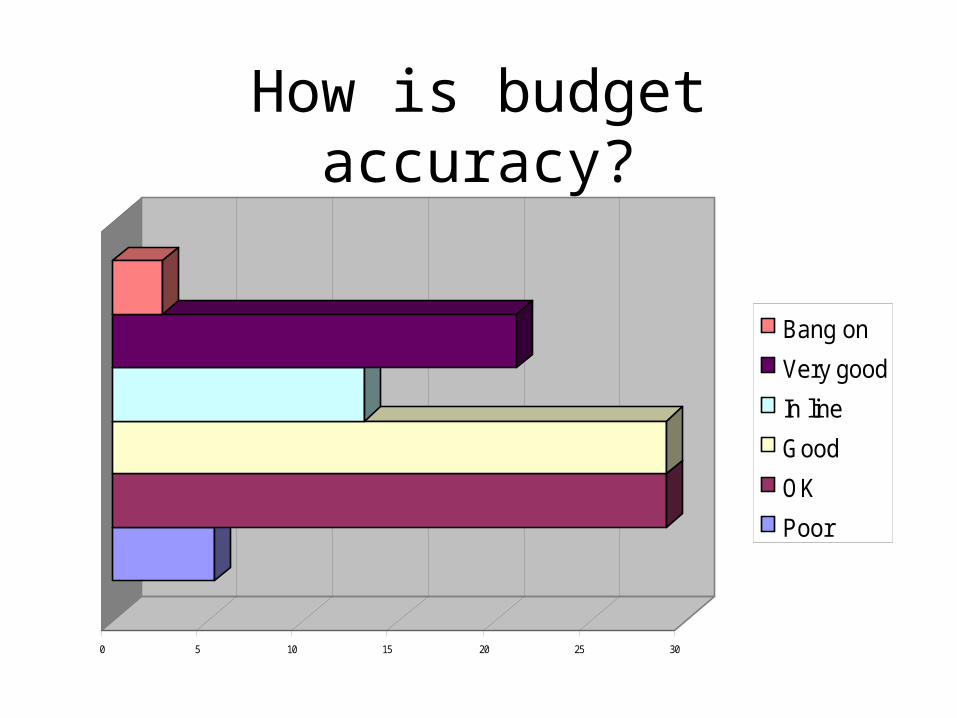

How is budget accuracy?

0 5 10 15 20 25 30

Bang on

Very good

In line

Good

OK

Poor

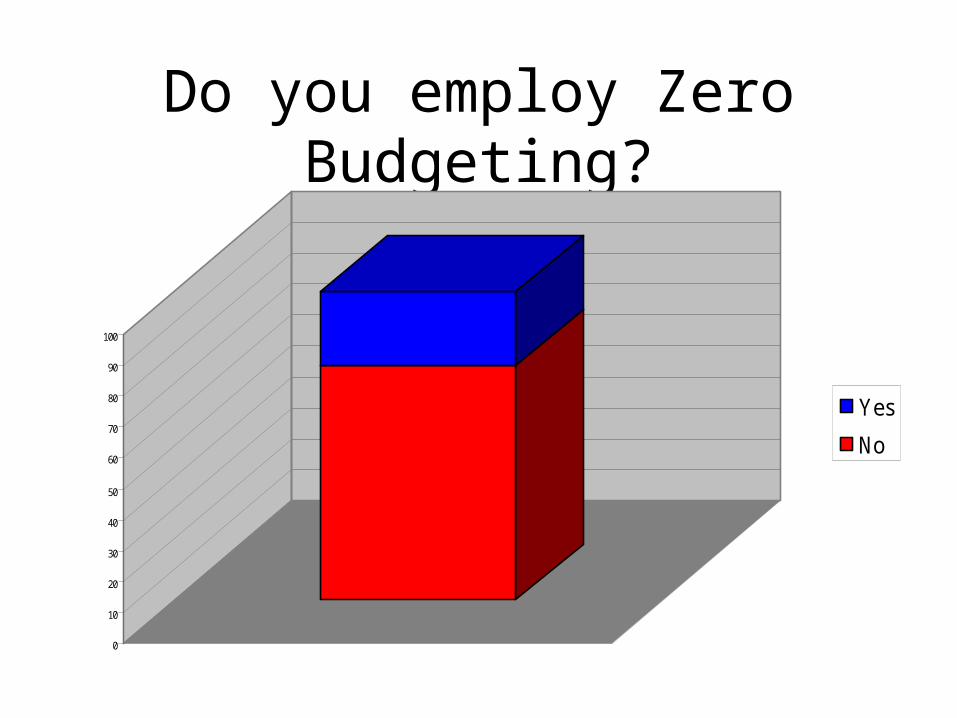

Do you employ Zero Budgeting?

0

10

20

30

40

50

60

70

80

90

100

Yes

No

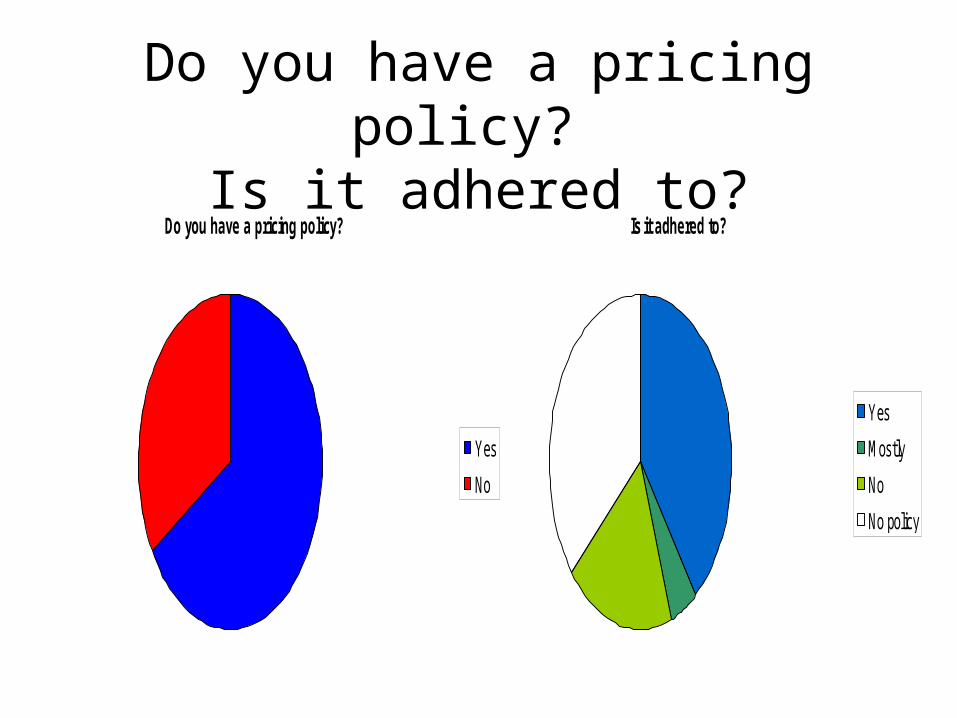

Do you have a pricing policy?

Is it adhered to?Is it adhered to?

Yes

Mostly

No

No policy

Do you have a pricing policy?

Yes

No

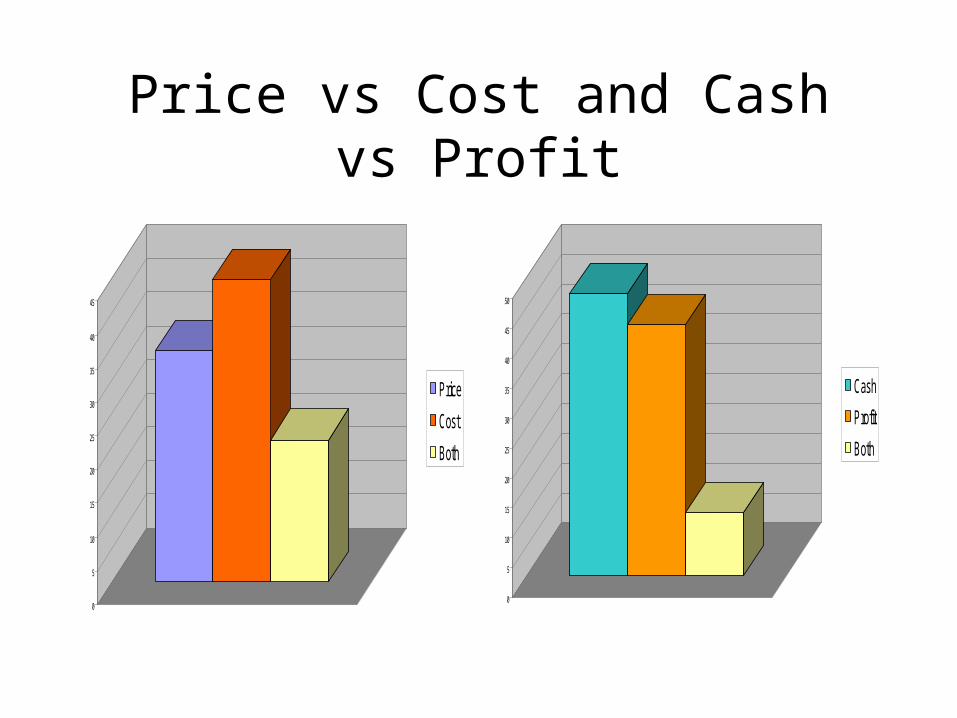

Price vs Cost and Cash vs Profit

0

5

10

15

20

25

30

35

40

45

50

Cash

Profit

Both

0

5

10

15

20

25

30

35

40

45

Price

Cost

Both

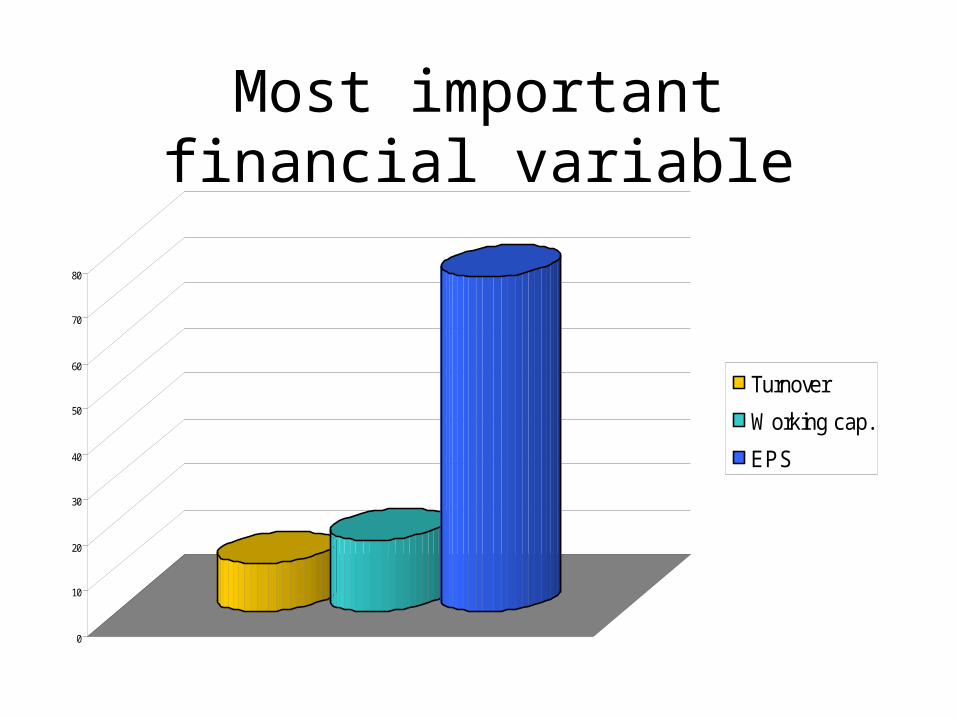

Most important financial variable

0

10

20

30

40

50

60

70

80

Turnover

Working cap.

EPS

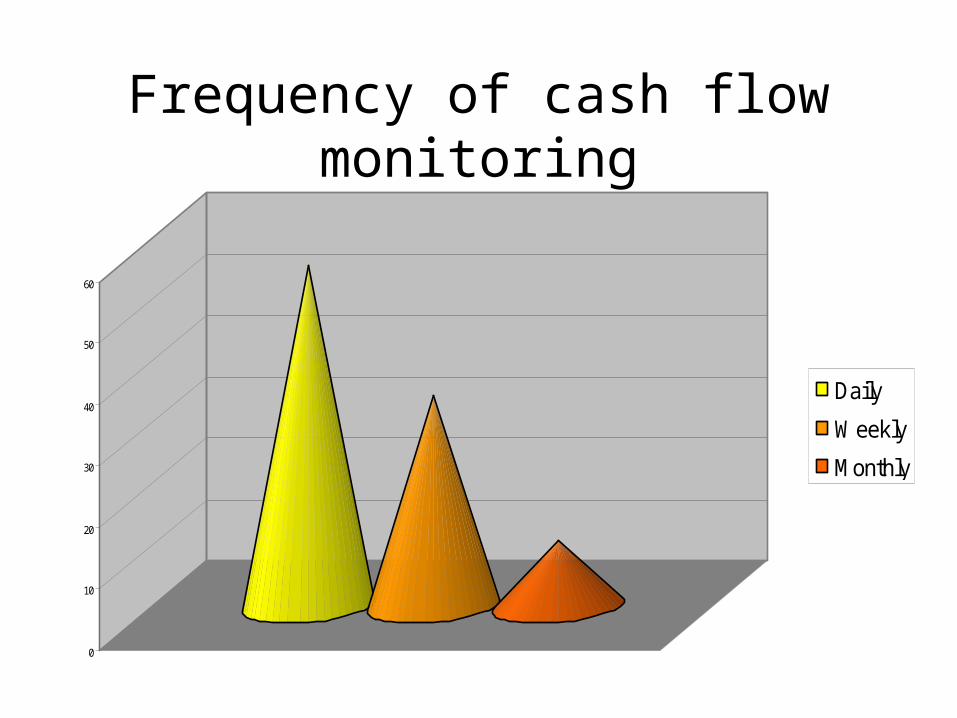

Frequency of cash flow monitoring

0

10

20

30

40

50

60

Daily

Weekly

Monthly

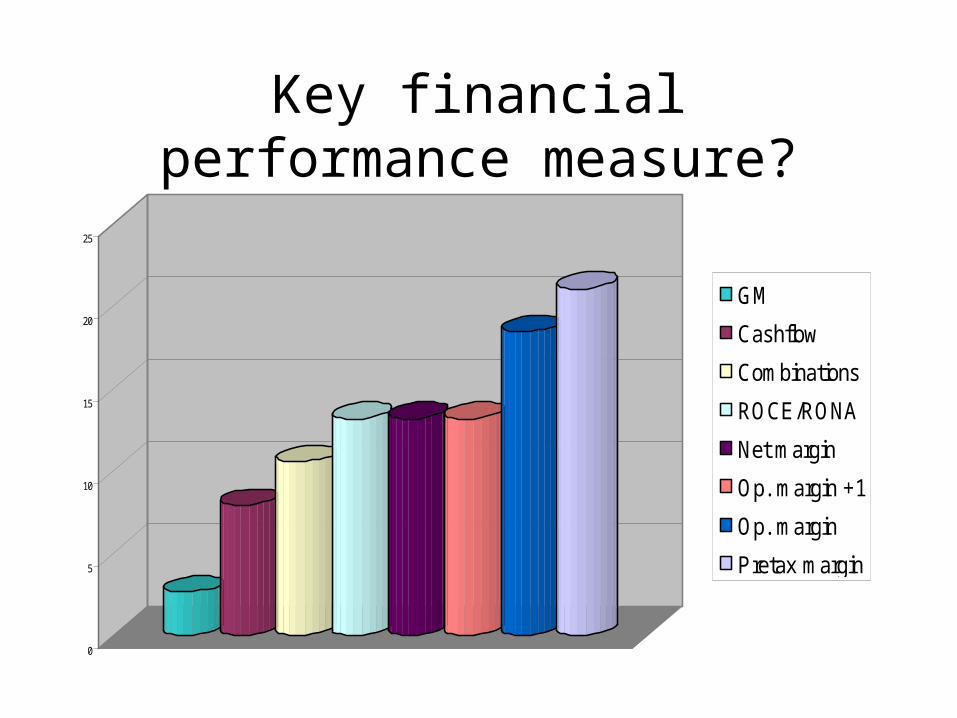

Key financial performance measure?

0

5

10

15

20

25

GM

Cashflow

Combinations

ROCE/RONA

Net margin

Op. margin +1

Op. margin

Pretax margin

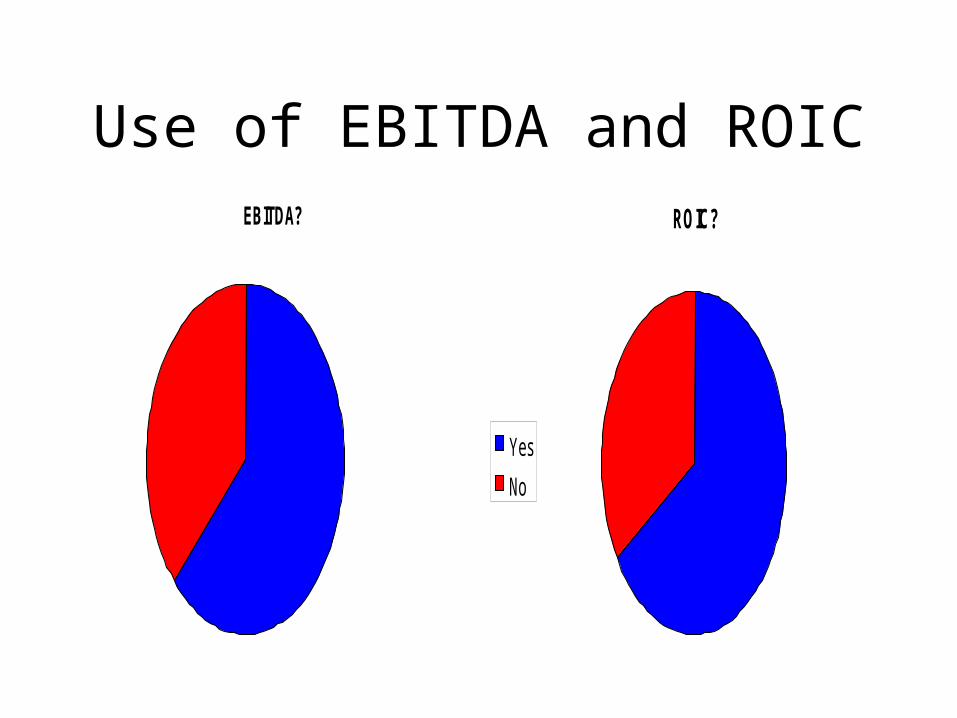

Use of EBITDA and ROICEBITDA?

Yes

No

ROIC?

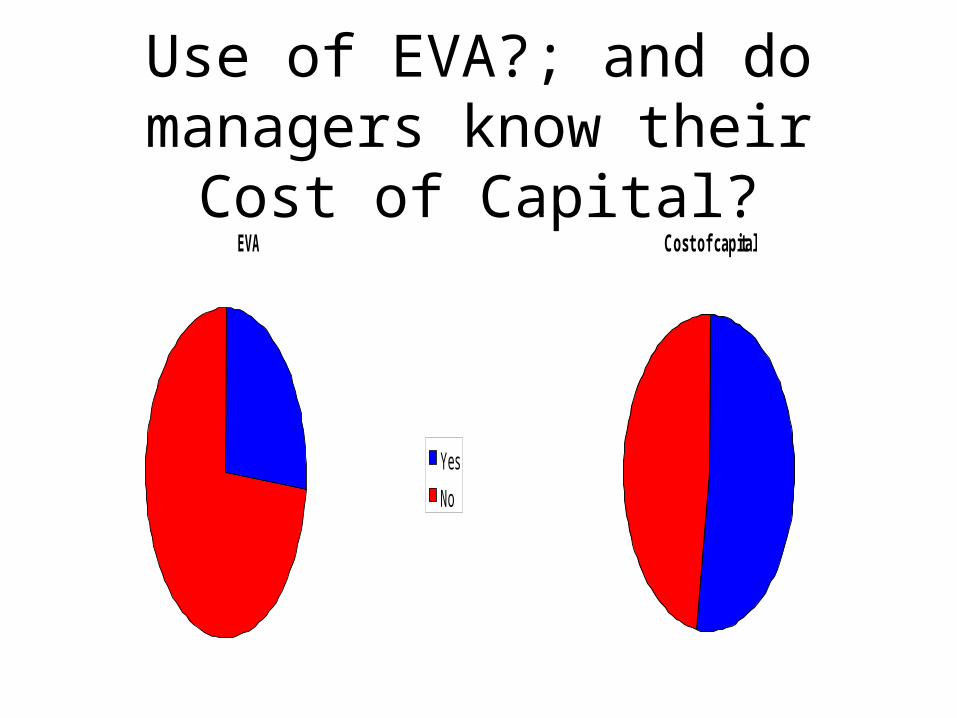

Use of EVA?; and do managers know their Cost of Capital?

EVA

Yes

No

Cost of capital

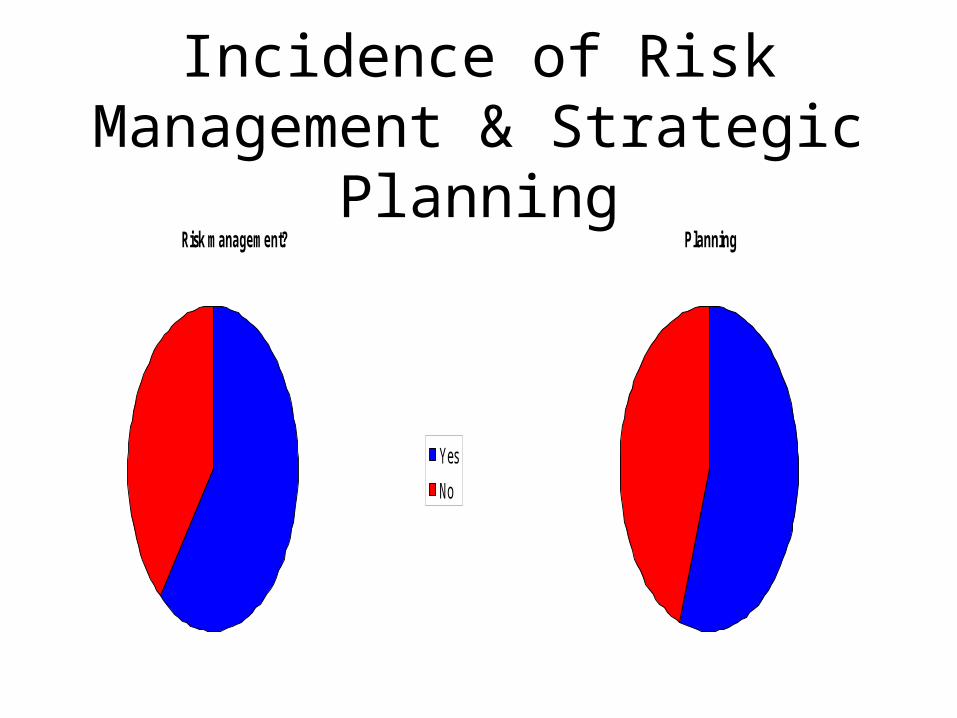

Incidence of Risk Management & Strategic Planning

Risk management?

Yes

No

Planning

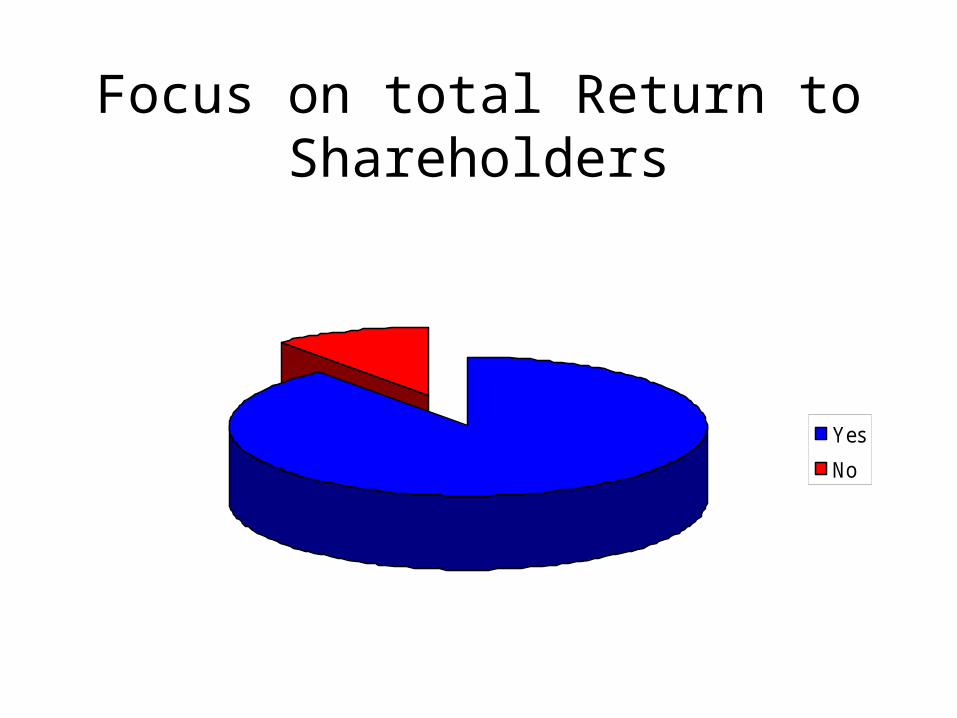

Focus on total Return to Shareholders

Yes

No

“What surprises me about construction is that decisions are

taken without a proper review of the facts, particularly the risks, which many refuse to quantify by arguing that such issues are subjective or

even emotive…

“…Not pricing for a known exposure at the bidding stage is very blinkered

indeed – to say the very least”

Development company CEO, 2004

“Risk is not related to size. You could just as easily lose £1 million on a £5 million job as one that is

worth £50 million”

Construction CEO, 2004

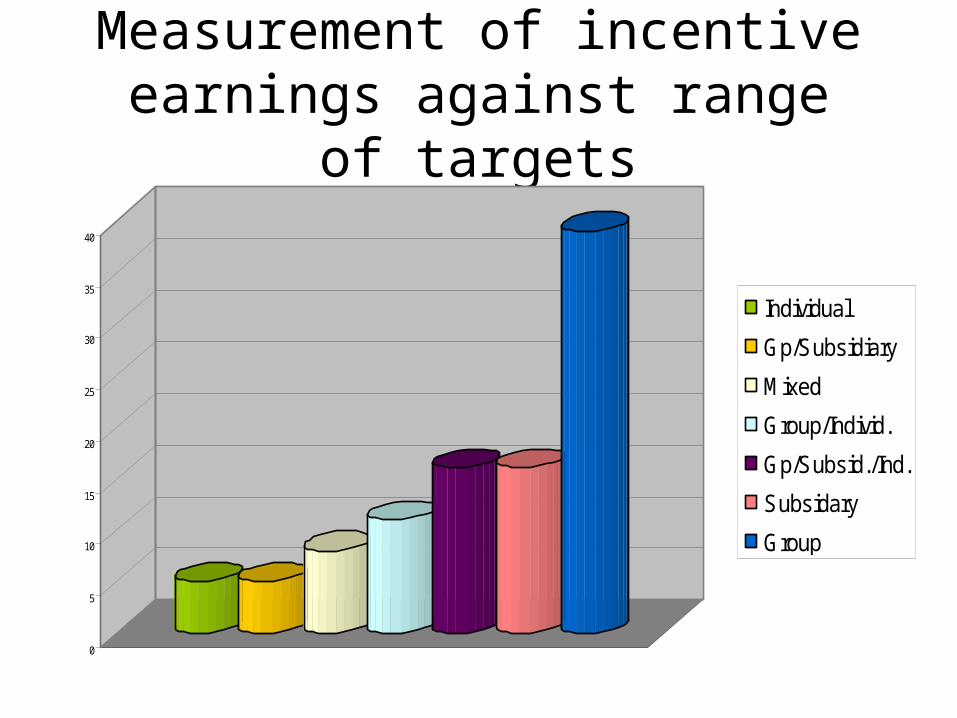

Measurement of incentive earnings against range of targets

0

5

10

15

20

25

30

35

40

Individual

Gp/Subsidiary

Mixed

Group/Individ.

Gp/Subsid./Ind.

Subsidary

Group

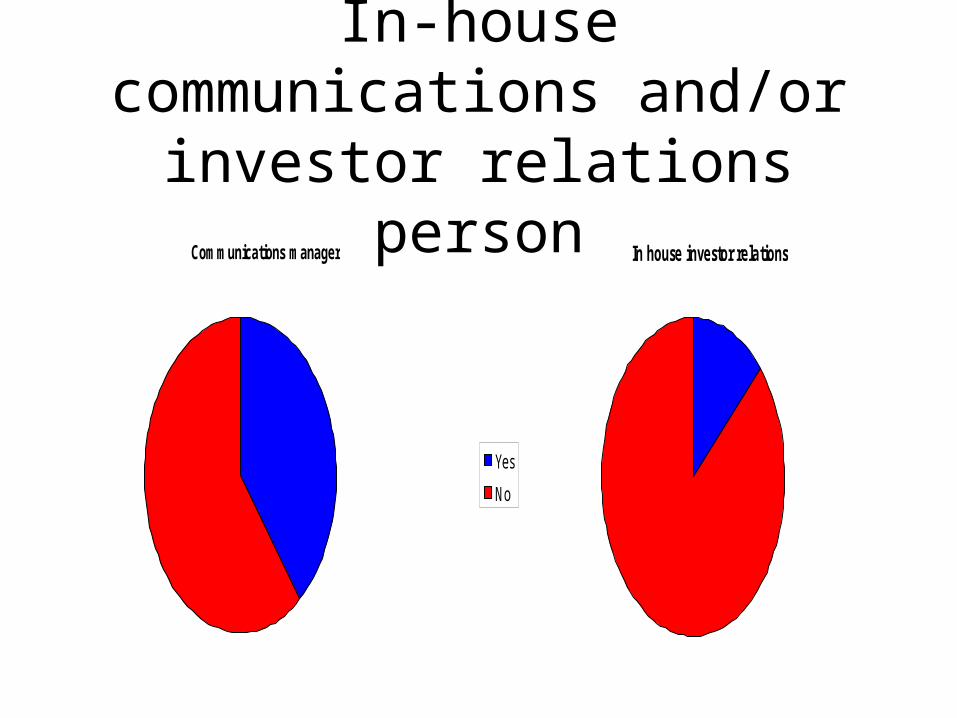

In-house communications and/or investor relations personCommunications manager

Yes

No

In house investor relations

“Construction is a long term business and trying to make

decisions to satisfy shareholders on a quarterly basis can be inconsistent

with the strategic plan.......

…and if decision making favours one group of stakeholders at the expense of others, for a prolonged period, the

business is virtually guaranteed to under perform”

Construction CEO, 2004

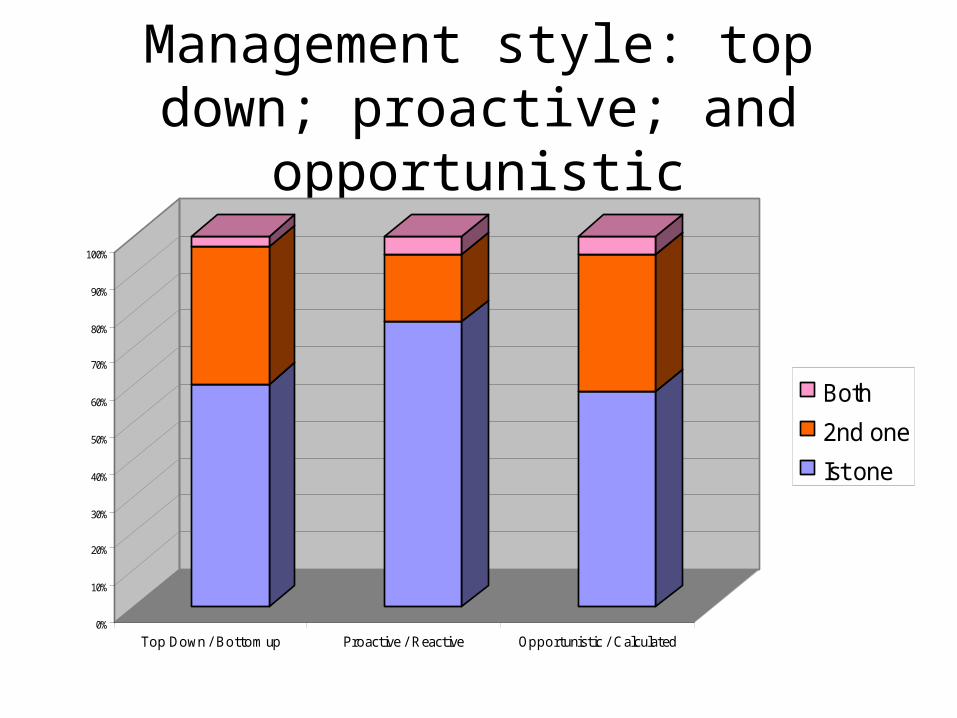

Management style: top down; proactive; and opportunistic

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Top Down / Bottom up Proactive / Reactive Opportunistic / Calculated

Both

2nd one

Ist one

Summary and conclusions

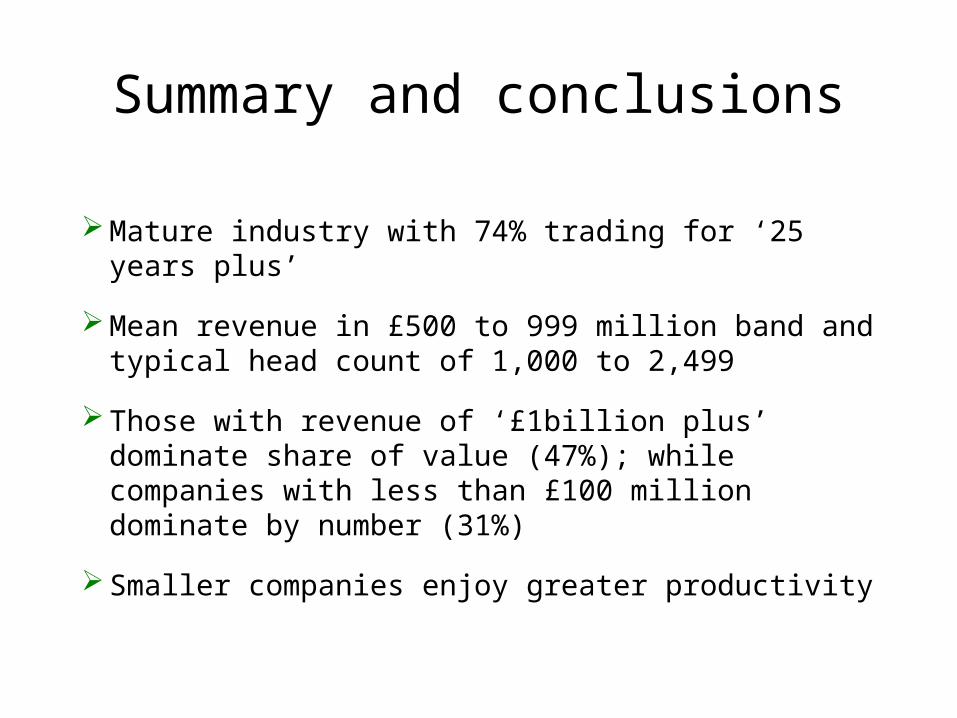

Mature industry with 74% trading for ‘25 years plus’

Mean revenue in £500 to 999 million band and typical head count of 1,000 to 2,499

Those with revenue of ‘£1billion plus’ dominate share of value (47%); while companies with less than £100 million dominate by number (31%)

Smaller companies enjoy greater productivity

Summary and conclusions

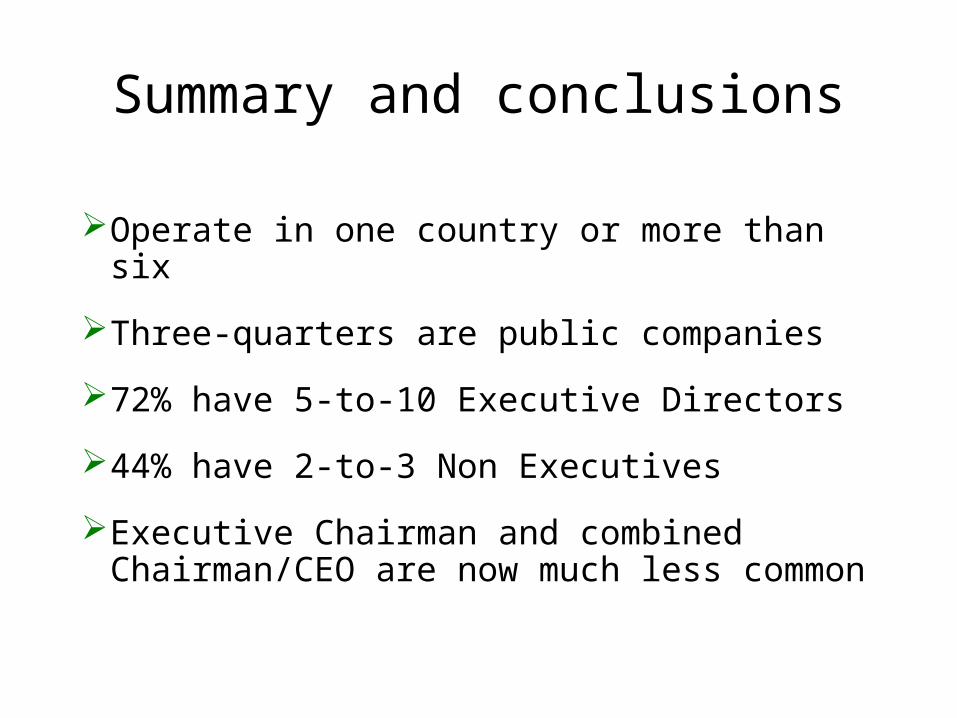

Operate in one country or more than six

Three-quarters are public companies

72% have 5-to-10 Executive Directors

44% have 2-to-3 Non Executives

Executive Chairman and combined Chairman/CEO are now much less common

Summary and conclusions

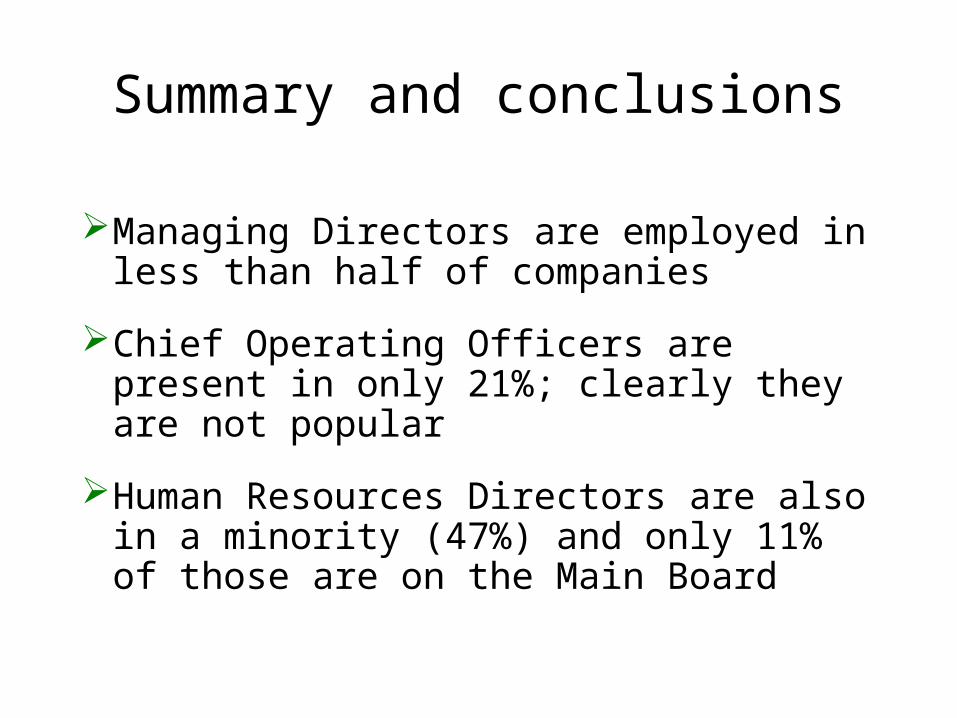

Managing Directors are employed in less than half of companies

Chief Operating Officers are present in only 21%; clearly they are not popular

Human Resources Directors are also in a minority (47%) and only 11% of those are on the Main Board

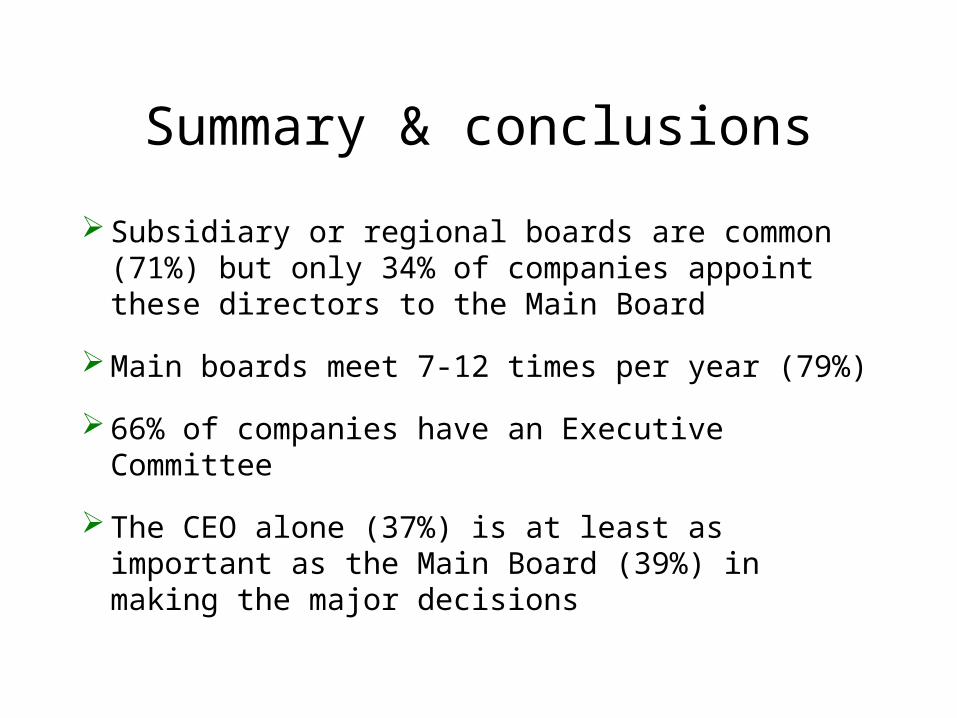

Summary & conclusions

Subsidiary or regional boards are common (71%) but only 34% of companies appoint these directors to the Main Board

Main boards meet 7-12 times per year (79%)

66% of companies have an Executive Committee

The CEO alone (37%) is at least as important as the Main Board (39%) in making the major decisions

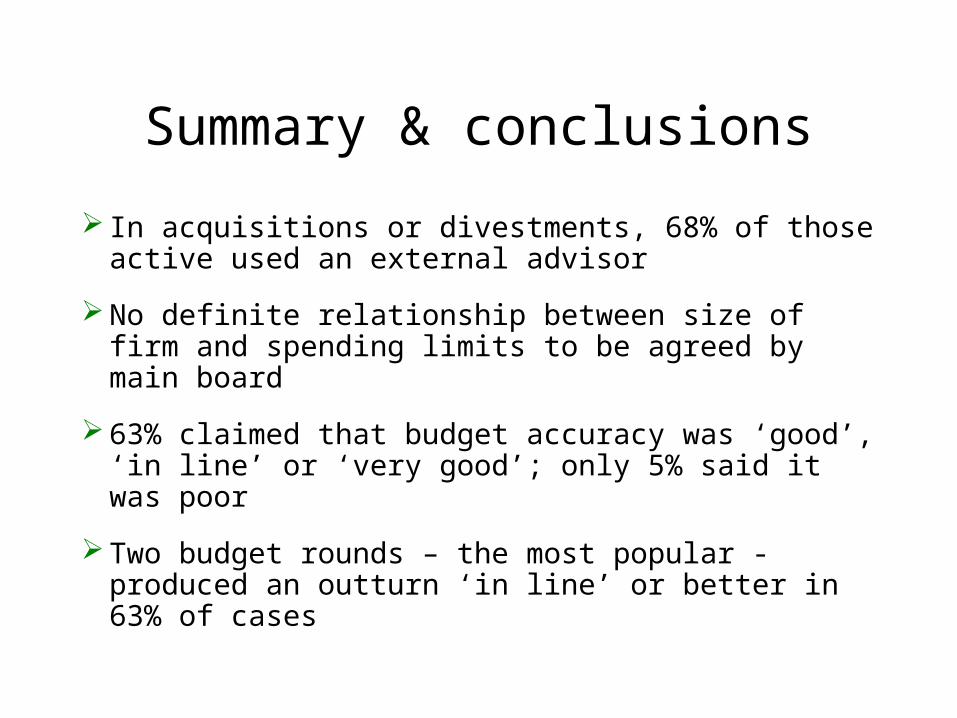

Summary & conclusions

In acquisitions or divestments, 68% of those active used an external advisor

No definite relationship between size of firm and spending limits to be agreed by main board

63% claimed that budget accuracy was ‘good’, ‘in line’ or ‘very good’; only 5% said it was poor

Two budget rounds – the most popular - produced an outturn ‘in line’ or better in 63% of cases

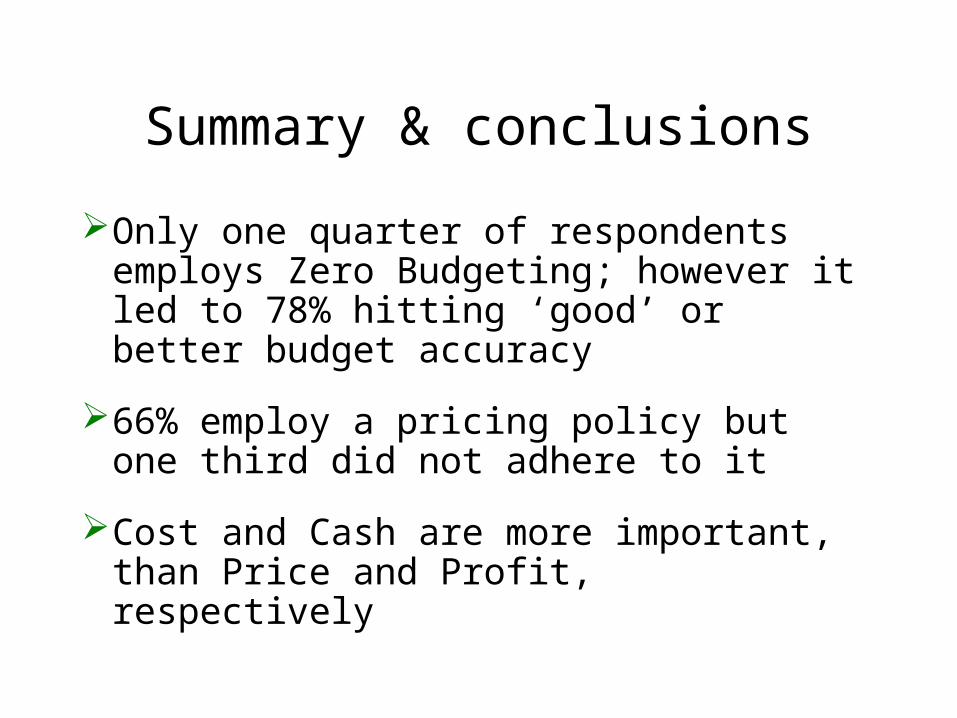

Summary & conclusions

Only one quarter of respondents employs Zero Budgeting; however it led to 78% hitting ‘good’ or better budget accuracy

66% employ a pricing policy but one third did not adhere to it

Cost and Cash are more important, than Price and Profit, respectively

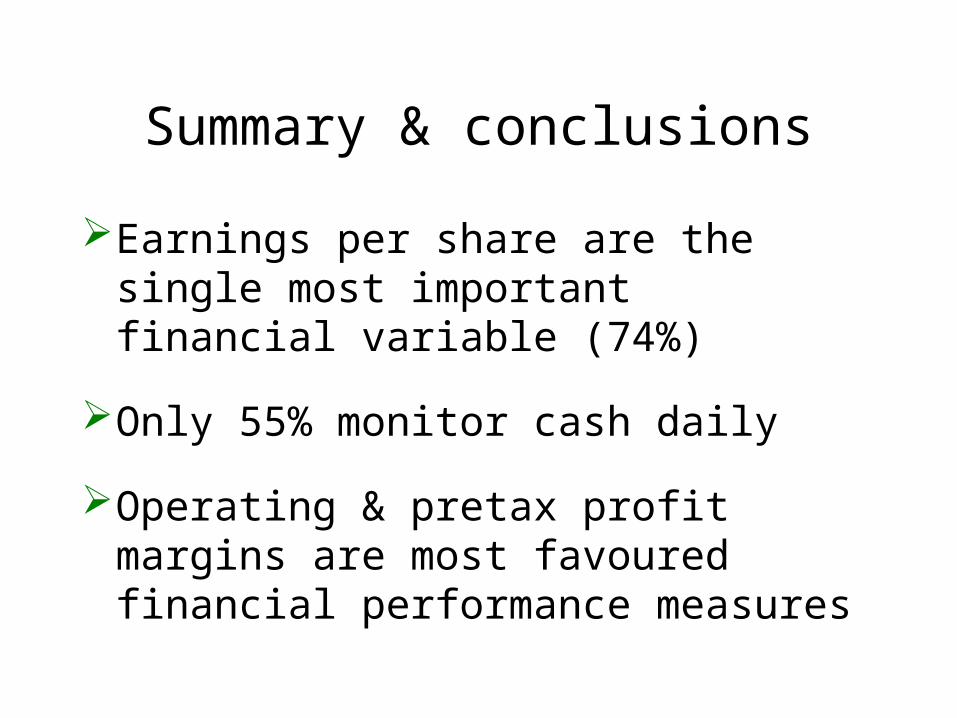

Summary & conclusions

Earnings per share are the single most important financial variable (74%)

Only 55% monitor cash daily

Operating & pretax profit margins are most favoured financial performance measures

Summary & conclusions

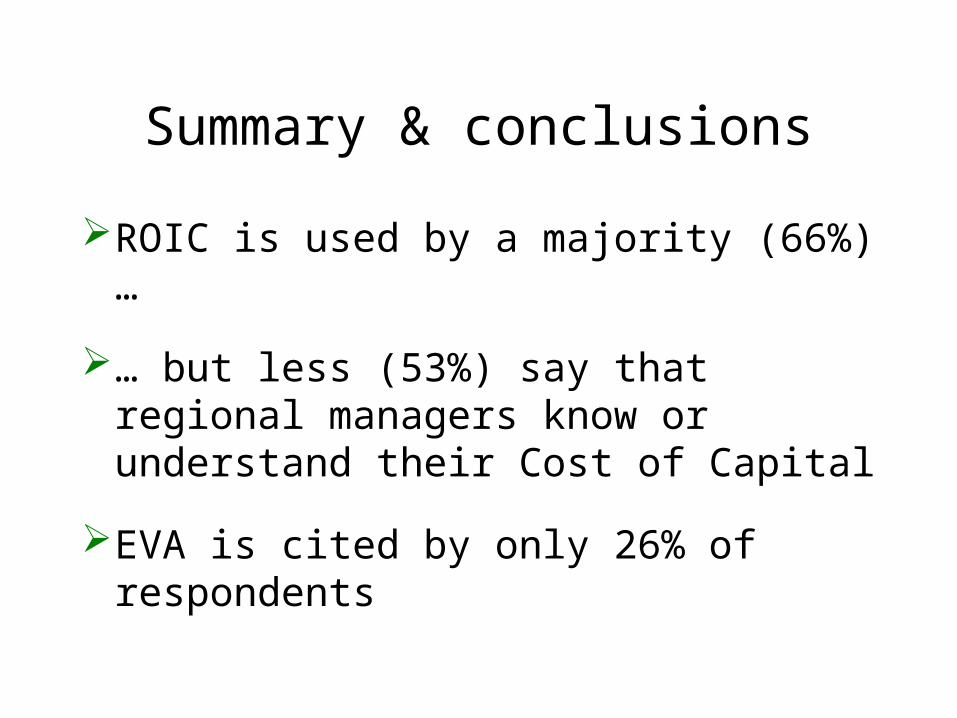

ROIC is used by a majority (66%)…

… but less (53%) say that regional managers know or understand their Cost of Capital

EVA is cited by only 26% of respondents

Summary & conclusions

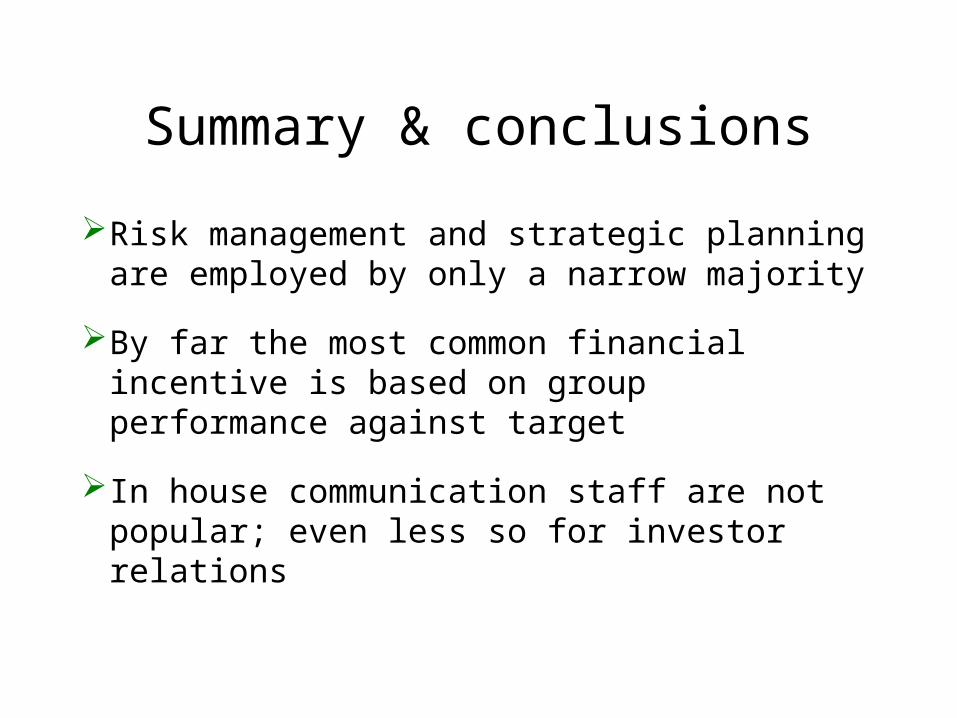

Risk management and strategic planning are employed by only a narrow majority

By far the most common financial incentive is based on group performance against target

In house communication staff are not popular; even less so for investor relations

Summary & conclusions

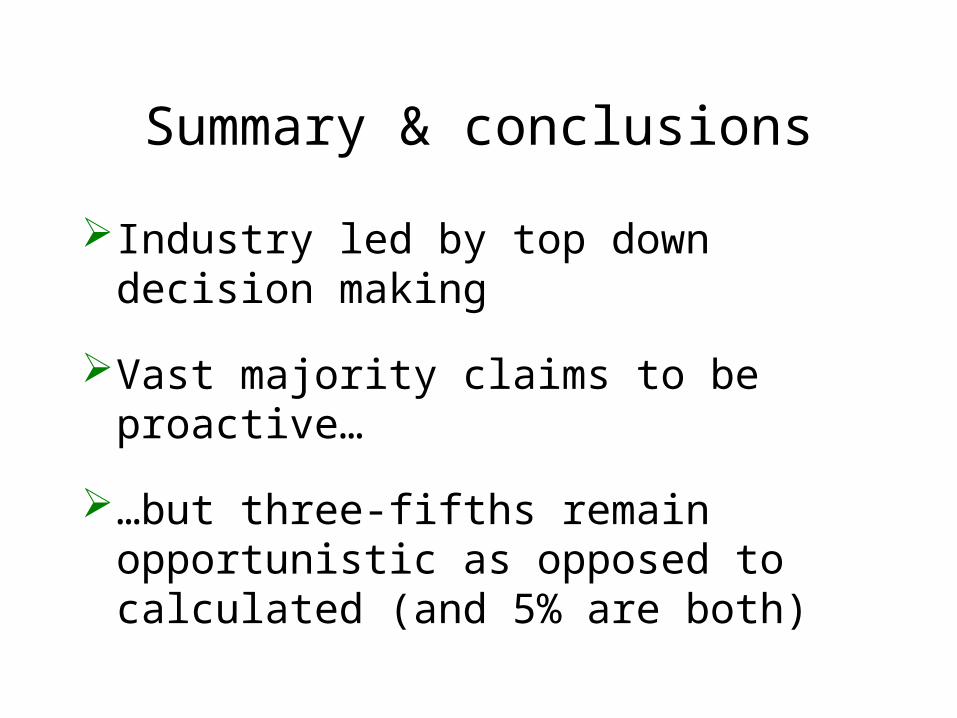

Industry led by top down decision making

Vast majority claims to be proactive…

…but three-fifths remain opportunistic as opposed to calculated (and 5% are both)

Final word

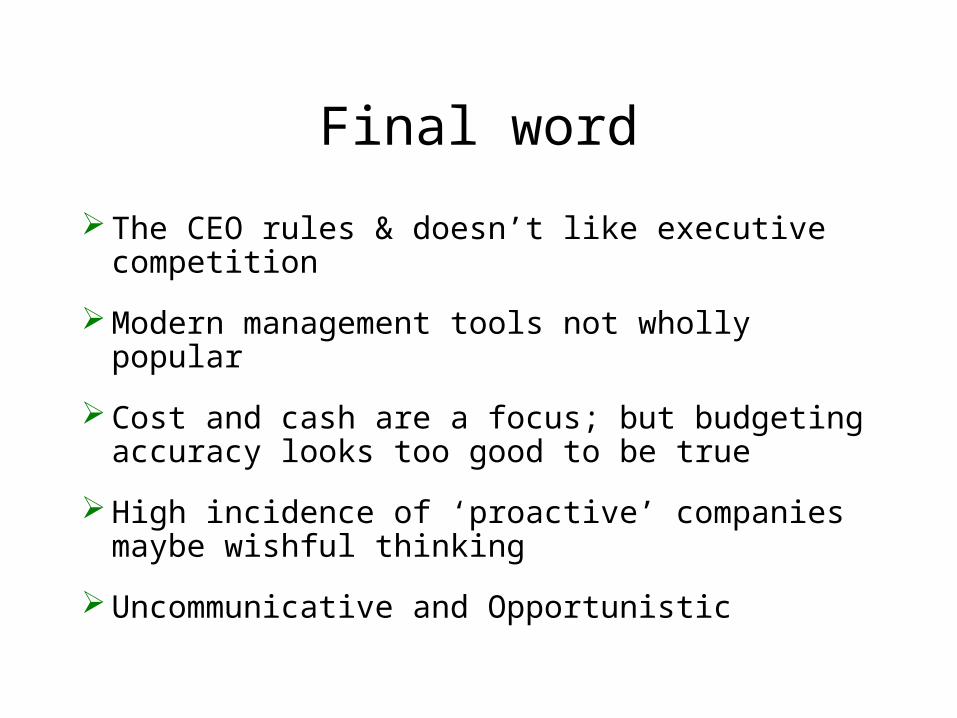

The CEO rules & doesn’t like executive competition

Modern management tools not wholly popular

Cost and cash are a focus; but budgeting accuracy looks too good to be true

High incidence of ‘proactive’ companies maybe wishful thinking

Uncommunicative and Opportunistic

“Prevarication is the bane of British management: a bad decision is

better than no decision”

Building materials CEO, 2004

Related Documents