Consulting WHITE PAPER Supplier Finance: An alternative source of financing?

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Consulting

WHite PAPeRSupplier Finance: An alternative source of financing?

Co

nsu

ltin

g

The Consulting teams from Mazars assist and advise the actors from public and private sector, in order to help them comply their organizations with their strategies and to succeed in their transformations, for a better global performance.

Composed of professionals dedicated to financial, strategic and operational consulting, they combine sharpened domain expertise and meticulous understanding of the actual issues the organizations have to face.

Over 350 consultants over the world, intervening within 20 offices, in the United-States, in South America, in Africa, in Europe, in the Middle-East, in Russia and in Asia, offer a collaborative approach, global and oriented towards the resolutions of the clients issues.

b-process, an ARIBA Company, is a European electronic invoicing leader, with a network of nearly 30,000 interconnected companies on its billManager platform. Based on an unrivalled technological experience in secured P2P exchanges, b-process has created Invoice2CASH, the first Supplier Finance collaborative platform. ARIBA, b-process’ mother company, is a worldwide leader in collaborative commerce solutions.

Mazars is an international, integrated and independent organisation, specialising in audit, accountancy, tax, legal and advisory services.

Mazars can rely on the skills of 13,000 professionals in the 68 countries which make up its integrated partnership on the five continents. Mazars also has correspondents and joint ventures in 15 additional countries.

Mazars is also one of the founding members of the Praxity alliance, which gathers 79 independent organisations and 28,000 professionals in 82 countries.

3

For the past twenty years or so, most international corporations have developed optimization programs

in conjunction with supply chain. Considerable attention has been given to management procedures relating to suppliers and the flow of supply, where many opportunities existed for improvement and concurrent savings. This has produced results, so that today physical transactions between large buyers and their suppliers are organized in a highly efficient manner. This streamlining has brought about a significant increase in collaborative platforms linking buyers with their suppliers, in connection with electronic billing programs and, more generally, “spend management” programs.

That is the context in which the notion of supply chain finance has emerged. Since the flow of goods, services and information with suppliers was streamlined, corporations have naturally sought to create value from the implied financial transactions.

Following a detailed study, and based on our combined expertise in financial consulting and in billing flows, we now believe that Supplier Finance stands out as one of the best supply chain finance practices.

Supplier Finance systems have successfully adapted to new business and financial conditions and, today, offer an appropriate response to the problems of both buyers and suppliers.

Accordingly, we have felt that it would be pertinent to propose a detailed analysis of the principles and many opportunities of Supplier Finance as a worthy supply chain finance application, as well as to share our experience regarding key factors that must be taken into consideration in order to take full advantage of these ambitious and promising practices.

We invite you to examine this paper, which we trust contains replies to all of your questions.

Alexis RenardVP Ariba, General Manager b-process

Hervé BlazejewskiConsulting Partner, Mazars

Editorial

4

Summary

Supplier Finance: An alternative source of financing?Combining optimized working capital financing with improved security for suppliers by means of a collaborative Supplier Finance approach

The objective of Supply Chain Finance has long been to take advantage of discounting potential not used by buyers. Today, corporations have found another use for it. What are the purposes of these new forms of Supplier Finance? First, corporations are looking for alternative sources of financing that do not impact their working capital needs. Second, they are most often called upon to help finance their suppliers’ needs, in a period of seemingly lasting economic instability.

With cash scarce and costly, and in a period of structural change when banks tend to have increasingly restrictive prudential standards, can this new form of Supplier Finance help provide greater supply security and improve corporate resilience?

the purpose of this white paper, which does not claim to be exhaustive, is to present a general outline of a financing system that deserves serious consideration in light of its potential contributions in terms of supply chain finance and purchasing policy by: (i) reducing risks in order to obtain better financial terms; (ii) offering an attractive financing option to all suppliers; and (iii) dividing benefits among all parties, based on the Supplier Finance program’s objectives.

Reducing risks, which is the underlying principle in Supplier Finance programs, makes it possible to significantly lower the cost of financing. That is why two essential factors must be taken into consideration, i.e. the financial health of the buyer and its ability to undertake to pay its bills. The program’s financing costs accordingly become nearly equal to those of the buyer.

Hence, the buyer can offer its suppliers financial terms that may be highly favorable if the suppliers’ borrowing rate is significantly higher. It goes without saying that interest rate differentials do not in and of themselves make the system compelling. The buyer must undertake to rapidly validate its invoices so as to provide for the earliest possible pre-financing. This in turn has an impact on management practices, processes and tools likely to accelerate the approval of invoices.

The last principle undoubtedly is a key to the structuring process, as it gives the buyer the possibility of making its program equally effective in generating financial gains for the buyer and securing its supplies by helping its suppliers obtain financing at a reduced cost.

5

Summary

One thing must be clear, however: a buyer cannot gain from both ends! therefore, all Supplier Finance systems must be specially designed to satisfy the needs and expectation of buyers while at the same time limiting the risks inherent in this type of arrangement, such as the reclassification of trade payables to debt.

Lastly, it should be noted that, thanks to significant technological advances, Supplier Finance arrangements are becoming fully collaborative. The increased popularity of automated electronic billing systems now makes it possible to take advantage of the instant availability of secure billing data. With the real-time validation of receivables and purchase-to-pay networks connecting buyers to their suppliers, they provide incentives for programs and extend the potential financing periods by automating the process of invoice recording and validation.

6

ContentsIntroduction ��������������������������������������������������������������������������������������������������������� 7

1. Supplier Finance, a system originally invented to generate financial gains ..........................7

2. In reaction to the recession, Supplier Finance becomes collaborative ..................................7

3. Supplier Finance is an increasingly attractive source of financing ........................................8

Supplier Finance principles and prerequisites ���������������������������������������������������� 101. Supplier Finance is a simple concept ...................................................................................10

2. Transferring risks from the supplier to the buyer ..................................................................10

3. The Supplier Finance life cycle ................................................................................................11

4. The two prerequisites for Supplier Finance ........................................................................... 12

5. Interest-rate and revenue-sharing model .............................................................................. 13

Essential technological support for Supplier Finance ����������������������������������������� 151. Features required to operate a Supplier Finance program ................................................... 15

2. The three ages of Supplier Finance platforms ...................................................................... 16

A promising market for collaborative Supplier Finance: ����������������������������������� 191. Payment delays, worsening in the recession, continue to be common in most

European countries ............................................................................................................... 19

2. Increased restrictions on bank credit leave corporations without the means to finance their working capital needs .................................................................................... 20

3. The financing of trade receivables no longer provides a fully adequate solution to current needs ......................................................................................................................... 21

4. The growth of Supplier Finance in Europe ............................................................................22

Supplier Finance, a collaborative approach to cash flows ����������������������������������� 231. Supplier Finance: A strategy for optimizing working capital or for securing suppliers? ..... 23

2. Collaborative Supplier Finance: the benefits of a collaborative approach to cash flows ....24

Setting up a Supplier Finance program ��������������������������������������������������������������� 271. Setting objectives for the Supplier Finance program ............................................................27

2. Carrying out the Supplier Finance project .............................................................................29

3. Securing the Supplier Finance arrangement .........................................................................30

4. Rolling out of the Supplier Finance system ...........................................................................30

5. Expanding the Supplier Finance arrangement .......................................................................31

6. Managing a Supplier Finance program’s technological aspects ..........................................31

Conclusion ��������������������������������������������������������������������������������������������������������� 33

Methodology ������������������������������������������������������������������������������������������������������ 34

Bibliography ������������������������������������������������������������������������������������������������������� 35

7

introduction

Economic conditions that favor creative financial solutions 1. Supplier Finance, a system originally invented to generate

financial gains

Supplier Finance arrangements first came into being more than twenty years ago and were primarily intended to maximize discounting gains by major buyers of goods and services. The first Supplier Finance arrangements were aimed at maximizing the discounts extended by selected suppliers in consideration for the buyer’s ability to rapidly approve payment for the goods and services supplied to it.

Supplier Finance arrangements were first initiated in part for that essentially practical reason by major manufacturers (FIAT) and distributors (Carrefour), whose procure-to-pay processes are highly advanced and structured.

Used mostly in Southern European countries, this kind of arrangement accounts for about 30% of aggregate factoring volume in Italy and 25% in Spain, two countries where payment periods are longer than in France.

Starting in 2006, certain buyers saw Supplier Finance as a potential way of having their suppliers finance their own working capital needs, by significantly lengthening payment periods in return for financial “collaboration” negotiated by the buyer (payment of suppliers’ invoices in 90 or 120 days instead of 45 days).

In France, such practices ceased in 2008 with the implementation of the Act on the Modernization of the Economy (LME), which limited the time allowed for paying suppliers. Paradoxically, interest in Supplier Finance did not diminish, as it provided buyers with a real opportunity to reexamine their organization and make it more efficient.

Nevertheless, buyers in France initiated relatively few Supplier Finance arrangements aimed at stabilizing their working capital requirements, mainly because of the the risk that their trade payables might be reclassified to debt in the case of financing with longer terms than those allowed by the LME Act.

2. In reaction to the recession, Supplier Finance becomes collaborative

The emergence of a new form of Supplier Finance has its source in the recession and the LME Act. Collaborative Supplier Finance no longer seeks just to maximize gains from discounting.

This new form of Supplier Finance relies on the same technical approach, namely the negotiation with suppliers of a factoring arrangement. However, its purpose is now primarily collaborative. It seeks to secure the buyer’s supplies, in particular from firms that are the most exposed to the effects of the recession.

Introduction

8

This shift in the nature of Supplier Finance makes it now possible to consider the arrangement as a new component of supply chain finance, which adds a collaborative dimension to the financing of working capital by the buyer and its suppliers, through improved control of purchase-to-pay processes.

The first collaborative Supplier Finance programs have now come into being, and differ from their predecessors in part by:

• the eligibility of a significantly larger number of suppliers;

• the discretionary right of suppliers to choose to join in the arrangement and to use the financing options as they see fit.

Although there are still only a few of those new collaborative Supplier Finance programs, they are of increasing interest to major corporations that seek to improve their resilience under the prevailing economic circumstances.

3. Supplier Finance is an increasingly attractive source of financing

For the past several years, banks have made it harder for businesses to obtain credit facilities. Bank prudential regulations, even more stringent since Basel III, are going to make it more and more difficult for the most exposed suppliers to have access to financing and further increase the cost of credit.

Payment delays, which have remained relatively stable in France over the past six years, have considerably increased in Europe since 2008, causing the short-term working capital needs of businesses to worsen. Having to wait longer before they are paid and unable to obtain funds from the banks, corporations have been looking for alternative financing methods.

In this context, collaborative Supplier Finance arrangements offering sufficiently attractive interest rates will become valuable sources of financing for economically sensitive businesses or those that can no longer increase their conventional credit facilities.

Because they offer attractive rates, collaborative Supplier Finance arrangements are going to make it possible for both banks and buyers to make use of potential discounting sources, including middle market companies and small businesses.

Financed by interest-rate differentials, effective collaborative Supplier Finance programs will primarily rely on:

• the use of technological platforms ensuring rapid execution and favoring collaboration between buyers and their suppliers; in this connection, existing electronic networks for the transmission of electronic invoices between buyers and suppliers can play a significant collaborative role;

• the requisite fair sharing of gains between the participating parties (buyer, financial institutions, suppliers and technological platform).

Buyers who make use of this novel alternative payment system, and respect this fair sharing, will acquire an unquestionable and probably essential competitive advantage. It will help them get through the recession on better conditions and will lastingly improve the effectiveness and resilience of their supply chain.

9

introduction

Based on the notion that collaborative Supplier Finance can be a source of financial innovation and a practical way of improving corporate resilience during the recession, this white paper seeks to throw light on this innovative and still too little-known practice.

The purpose of this white paper is not merely to simply explain Supplier Finance. It also seeks to suggest new areas that could be investigated to optimize the financing of working capital, bolster collaboration between buyers and suppliers and enhance corporate supply security.

10

Supplier Finance principles and prerequisites

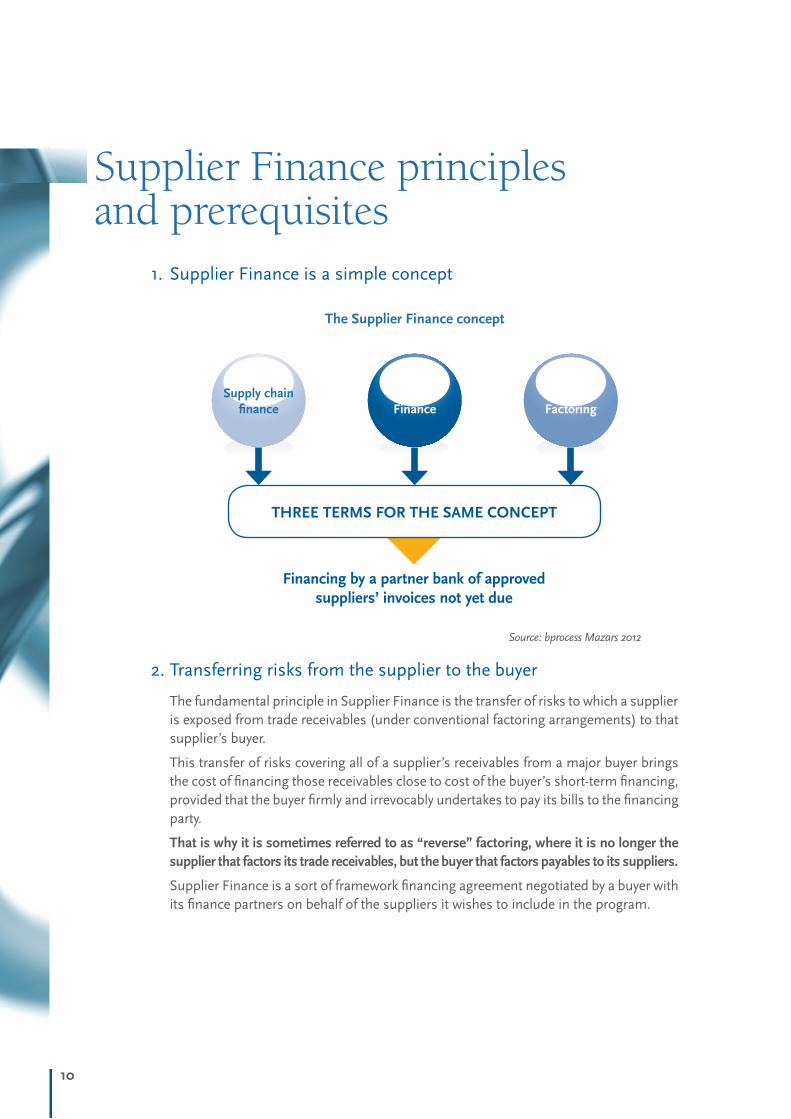

1. Supplier Finance is a simple concept

the Supplier Finance concept

Source: bprocess Mazars 2012

Supply chain finance

Supplier Finance

Reverse Factoring

tHRee teRMS FOR tHe SAMe COnCePt

Financing by a partner bank of approved suppliers’ invoices not yet due

2. Transferring risks from the supplier to the buyer

The fundamental principle in Supplier Finance is the transfer of risks to which a supplier is exposed from trade receivables (under conventional factoring arrangements) to that supplier’s buyer.

This transfer of risks covering all of a supplier’s receivables from a major buyer brings the cost of financing those receivables close to cost of the buyer’s short-term financing, provided that the buyer firmly and irrevocably undertakes to pay its bills to the financing party.

that is why it is sometimes referred to as “reverse” factoring, where it is no longer the supplier that factors its trade receivables, but the buyer that factors payables to its suppliers.

Supplier Finance is a sort of framework financing agreement negotiated by a buyer with its finance partners on behalf of the suppliers it wishes to include in the program.

11

Supplier Finance principles and prerequisites

3. The Supplier Finance life cycle

Supplier Finance life cycle

Source: Mazars 2011

Buyer

Supplier Bank

52

3

4

1

issuance of invoiceDue date: 60 days from billing date (Exclusive of immediate payments, Perben Act limits, etc.)

Payment on due date

Validation of invoice with payment approval

Prepayment of the invoice

Request to assign a receivable

Supplier Finance steps

Conventional steps

1. The supplier sends the buyer an invoice.

2. The buyer makes its invoices from suppliers firmly and irrevocably available on a technological exchange platform as soon as it approves their payment.

3. The supplier may, at any time, ask the bank to pay the buyer’s invoices.

4. The bank prepays the invoices assigned by the supplier.

5. The buyer pays the bank on the due date shown in sales contracts with the suppliers enrolled in the Supplier Finance program.

Flowchart of a receivable under Supplier Finance

Source: Mazars 2011

Receipt of invoices

Retrieval from the buyer’s IT system

Request for prepayment

Payment by the bank to the supplier

Payment by the buyer to the bank

Processing of invoices

Period in which invoices are available on the platform

Payment approval

D1 D10

D10 + x

D60D57

12

4. The two prerequisites for Supplier Finance

The transfer of risks makes it possible for the buyer to benefit from close to its own financing terms if it firmly and irrevocably undertakes to pay the invoices included in the Supplier Finance program.

In order for suppliers to be paid as promptly as possible, the buyer must be in a position to make a firm commitment to settle invoices very shortly after receiving them from suppliers. In the absence of such a commitment, the prepayment terms may no longer be of interest to the suppliers.

The first prerequisite therefore concerns the process from the delivery of purchased goods and services to the approval of payment, which must be rapid and dependable. In fact, certain kinds of purchases are less suited to Supplier Finance, such as when acceptance procedures are very complex or require time-consuming approvals.

The second prerequisite concerns the difference between the discount rate applied to the Supplier Finance by the buyer and the rate at which suppliers can borrow funds:

• In France and elsewhere in Europe, the rate differential will essentially depend on the buyer’s creditworthiness;

• In emerging markets, the differential no longer depends on the buyer’s credit rating but on other market-related factors (e.g. the inflation rate).

Whenever there is a wide spread between the rates charged to the buyer and the supplier, the arrangement will produce significant savings. Those savings may be divided among the parties, depending on the gains sought by the buyer.

interest rate spread between the buyer and the supplier

bprocess - Mazars 2012

Rate at which the supplier can borrow

Rate applicable to the Supplier

Finance program

Value opportunity

Rate at which the buyer can

borrow

In the event that some suppliers do not satisfy the above prerequisites, it would of course be possible to limit the program’s scope to specific suppliers or to adapt the terms to various purchase segments.

13

Supplier Finance principles and prerequisites

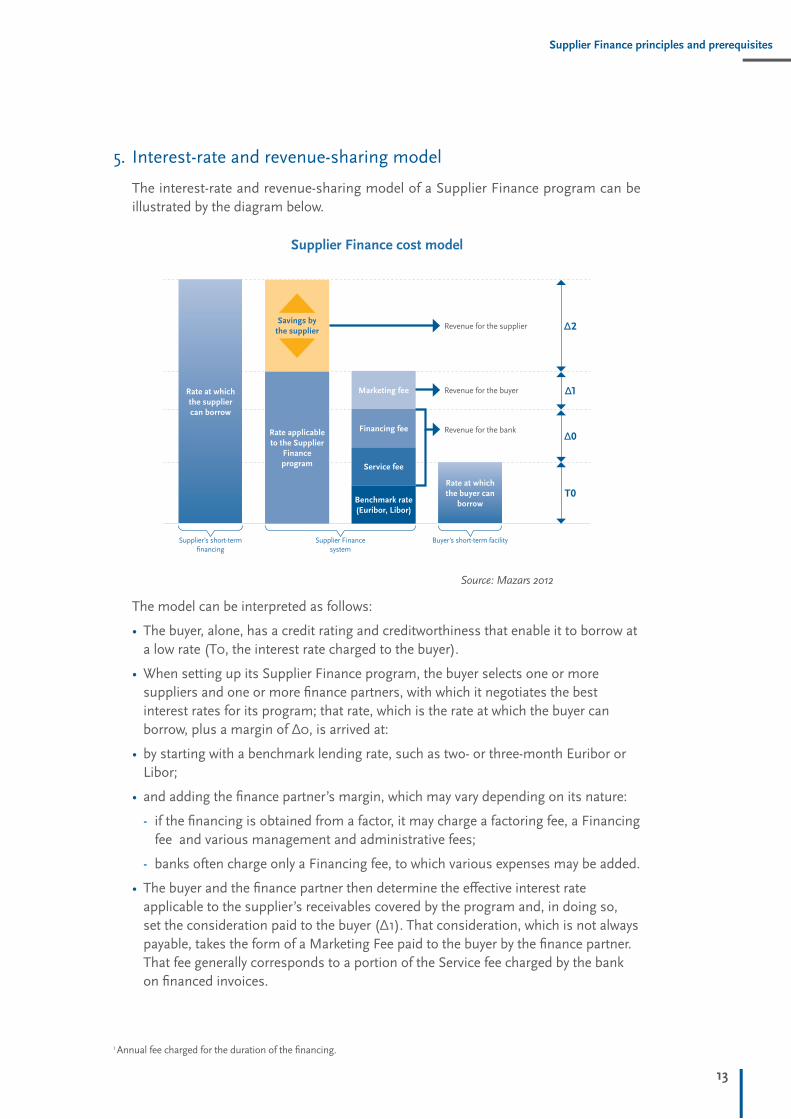

5. Interest-rate and revenue-sharing model

The interest-rate and revenue-sharing model of a Supplier Finance program can be illustrated by the diagram below.

Supplier Finance cost model

Source: Mazars 2012

Rate at which the supplier can borrow

Marketing fee

Service fee

Financing fee

Benchmark rate (euribor, Libor)

Rate applicable to the Supplier

Finance program

Savings by the supplier

Rate at which the buyer can

borrow

Revenue for the supplier

Revenue for the buyer

Revenue for the bank

Supplier’s short-term financing

Supplier Finance system

Buyer’s short-term facility

Δ2

Δ1

Δ0

The model can be interpreted as follows:

• The buyer, alone, has a credit rating and creditworthiness that enable it to borrow at a low rate (T0, the interest rate charged to the buyer).

•When setting up its Supplier Finance program, the buyer selects one or more suppliers and one or more finance partners, with which it negotiates the best interest rates for its program; that rate, which is the rate at which the buyer can borrow, plus a margin of Δ0, is arrived at:

• by starting with a benchmark lending rate, such as two- or three-month Euribor or Libor;

• and adding the finance partner’s margin, which may vary depending on its nature:

- if the financing is obtained from a factor, it may charge a factoring fee, a Financing fee and various management and administrative fees;

- banks often charge only a Financing fee, to which various expenses may be added.

• The buyer and the finance partner then determine the effective interest rate applicable to the supplier’s receivables covered by the program and, in doing so, set the consideration paid to the buyer (Δ1). That consideration, which is not always payable, takes the form of a Marketing Fee paid to the buyer by the finance partner. That fee generally corresponds to a portion of the Service fee charged by the bank on financed invoices.

1 Annual fee charged for the duration of the financing.

t0

14

• The effective rate applicable to the suppliers is therefore T0+Δ0+Δ1, and the gain for the supplier is equal to the amount by which that rate differs from TF, the rate at which it could borrow from its own banks, and T0+Δ0+Δ1, i.e. Δ2.

Under a collaborative Supplier Finance arrangement, it should be noted that interest expenses incurred by the program are paid to the financing party only if the supplier decides to finance the receivables it has elected to assign.

The challenge consists in setting the cursor between Δ1 and Δ2:

• a minimum Δ2 would produce the highest benefits for the buyer but the arrangement would be of only relative interest for the supplier;

• a minimum Δ1 corresponds to a situation where the buyer forgoes benefits in favor of the suppliers it wishes to support during a difficult business period;

• finally, the cursor may of course be moved up or down depending on the kind of suppliers or the purchasing segments concerned.

It should be noted, however, that there really is no standard interest-rate model. It is better to opt for an “all inclusive” rate, which is added to the benchmark money-market rate applicable to the program. This makes it easier for the buyer to compare offers by several financing parties, and is easier for the suppliers to understand.

Concerning the fee paid to the technology provider, it is generally paid by the buyer and is most often a flat fee. However, it can vary depending on the number of suppliers in the program and the amount of financing provided.

15

essential technological support for Supplier Finance

There can be no Supplier Finance without technological support that provides for the flow of information between the parties.

1. Features required to operate a Supplier Finance program

The principal purpose of a Supplier Finance platform is to connect the parties and provide for the free flow of information among them. Ideally, it should therefore include the following features:

• loading of the buyer’s payment orders;

• automatic calculation of available financing;

• finance request screen for use by suppliers and for calculating financing charges;

• submission of finance requests to the bank and monitoring of replies;

• automatic issuance of transfer orders on the buyer’s behalf, with all of the invoices coming due, whether or not they have been financed.

However, the growing complexity of programs and the more frequent requests by buyers for transparence and independence make the following features increasingly necessary:

• tools for promoting the program with suppliers and following through on their enrollment;

• loading of all of the buyer’s trade receivable documents, whether or not the invoices have been validated, in order to let each supplier access the complete records of its receivables from the buyer;

• availability of reporting statements that contain data usable by all parties;

• consolidated management of programs involving several banks (“multi-bank”) and automatic issuing of statistical data for monitoring the program.

Lastly, electronic data acquisition services for invoices and the automatic validation of invoices play a key role in ensuring that the due date of factored invoices is sufficiently distant to make financing of interest to the supplier.

In this connection, older Supplier Finance platforms may not include some or all of these features.

Essential technological support for Supplier Finance

16

2. The three ages of Supplier Finance platforms

Bank platforms

Historically, banks have been the first to offer technological platforms to their buying customers and suppliers enrolled in programs. The features they provide, which are generally minimal, are used to share information required to operate and oversee Supplier Finance programs.

The cost of operating those platforms is generally included in financial service fees charged to suppliers when they assign receivables.

Bank platforms have limited flexibility, however. Thus, if the buyer wishes to work with a different finance partner or add new lenders, it is in principle charged extra fees for connecting to the platforms of those other entities and for applying the changes to its previously enrolled suppliers.

The banks have become increasingly aware of the important role that of multi-bank platforms are being called upon to play in the future development of large Supplier Finance programs.

Accordingly, they are seeking to make their technical solutions more accessible.

third-party multi-bank platforms

In spite of the prevalence of bank platforms, the current growth of credit and the expansion of the geographical area covered by new Supplier Finance programs are giving rise to multi-bank arrangements. Under such programs, several banks participate in the effort to enroll suppliers and share the concerned buyer’s risk exposure as well as the revenue generated by programs.

Under the circumstances, it seems difficult to ask a buyer to connect to a different proprietary platform for each bank with which it does business. Doing so would make it impossible to effectively monitor the program as a whole.

It would probably be unnecessarily complicated to envisage a syndication approach, in which the partner banks would agree to channel all transactions between the program participants through a single platform operated by the lead bank.

On the other hand, it makes sense to have a multi-bank platform operated by a third party on behalf of all of the participants:

• The buyer is not tied to proprietary bank platforms. It can replace or add a finance partner at its discretion without having to change platforms. Furthermore, by fostering competition among the finance partners, the platform can sometimes help obtain more favorable financing terms. It also gives the buyer an exclusive link through which it can access all programs operated by the various banks retained by it.

• For the finance partner, a hub-type of platform can replace a costly system of point-to-point connections with each buyer, so that a single link can be used by the bank to communicate with all of its buyers, provided they are in turn connected to the hub.

• For all of the parties, a third-party platform means that rates can be posted in a clear and unambiguous manner. Costs are known from the start by the participating

17

essential technological support for Supplier Finance

parties. Compared with the bank platform system, this method involves a new party, who must be compensated, although that additional cost may have a very limited impact on the ability of the platform to attract suppliers, as:

- its cost merely offsets the operating cost of the bank platform; and

- it can contribute additional savings resulting from competitive bidding or the complimentarity sought by the banks.

In actual fact, multi-bank platforms have been in existence for several years, although they have been a consequence of the market’s growth rather than contributors to it.

Three factors have combined to account for this unremarkable performance:

• The platforms have not helped deal with the two root causes of failure by Supplier Finance programs, i.e. the slow pace of enrollment by suppliers and validation of income by buyers.

• The promise made to banks that this would create value has thus far been insufficient to convince them to give up their proprietary platform model and use hubs that, still today, connect only a very limited number of buyers and suppliers.

• In order to remain profitable in a tight market, they charge high fees or sometimes conceal their charges by seeking to act as intermediaries in the relationship between the buyer and its banks.

Purchase-to-pay platforms (P2P)

A new type of third-party multi-bank platform seems to combine the features of its predecessors while limiting their shortcomings.

First and foremost, a P2P platform offers a set of features that provide for the electronic and automatic processing of some or all of the steps leading up to the actual Supplier Finance transactions: orders, acceptances, billing and validation of invoices.

These platforms have proved effective, with the largest among them being used by thousands of buyers and hundreds of thousands of suppliers and handling transactions totaling hundreds of billions of euros.

Besides their multi-bank nature, the platforms can provide answers for all of the objections raised concerning conventional third-party platforms:

• A buyer’s suppliers are already enrolled insofar as certain P2P features are concerned. It is therefore easy to notify each of them of a Supplier Finance program when they connect to the online account. For example, if a supplier issues invoices via the platform, it can be informed of the amount of financing that is theoretically available and the interest charged on it whenever it links up to verify the validation of its invoices by its buyer.

• The tools for accelerating the validation of invoices by the buyer are often already in place, including the automatic integration of billing data (paper invoices in digital format or tax-compliant electronic invoices), with the use of automated reconciliation engines combining the order, receipt and invoice, the implementation of manual invoice validation workflows, including for invoices not related to orders, etc.

18

• The promises made to the bank regarding the hub are fulfilled because of the intrinsic size of the network of connected firms.

• Lastly, overhead costs are amortized over the full range of P2P services, so that it is possible to charge interest and fees that protect the interests of all of the parties and the economic fairness of the Supplier Finance system.

19

A promising market for collaborative Supplier Finance:

increase in payment periods and drying up of bank credit1. Payment delays, worsening in the recession, continue to be

common in most European countries

The European authorities have long sought to regulate late payments for commercial transactions (European Directive 2000/35 of June 29, 2000 revised October 20, 2010).

There is little coordination regarding the transposition of the Directive into the domestic law of various countries, although some progress is being made toward more uniform practices.

Still, those regulations have not prevented payment periods from worsening sharply, with a peak reached in 2008-2009, and from continuing to be of major concern to all parties concerned.

Figure 6: Changes in payment periods – comparison of France and europe (in days’ delay)

Source: DFCG financial industry newsletter of 2/16/12

16,0

15,5

15,0

14,5

14,0

13,5

13,0

12,5

12,0

11,5

11,0

16,0

15,5

15,0

14,5

14,0

13,5

13,0

12,5

12,0

11,5

11,0

dec-06 dec-08dec-07 dec-09 jun-11jun-07 jun-09 dec-10jun-08 jun-10 dec-11

europe France

A promising market for collaborative Supplier Finance:

20

According to data published by Altares, payments in Europe were 13.5 days late on average in 2011. The trend in Europe is driven by Germany and the Netherlands, where delays are the shortest (8 days), and by Great Britain, where payment practices have been improving (from 19 days at the end of 2009 to 15.7 days at the end of 2011). The average in Spain and Portugal is 20 days.

In France, payment deferrals have been relatively stable over the past six years. However, at the end of 2011, Belgium overtook France in third place, with both countries reporting average payment delays of about 12 days.

Thus, regardless of payment terms, on average, only 40% of all firms pay their bills on time.

Comparison of average payment terms in europe – third quarter of 2011

Source: Altares “First quarter 2011 analysis: Payment patterns of European firms”

0 - 30 8,1

8,5

12,4

20,8

12,1

18,3

15,5

16,4

26,3

GermanyContractual DPO (days)

Delay in payment (days)

A noterContractual DPO’s are the number of days theoretically in place. Practically, average DPO’s without delay are generally over 70 days in Southern Europe and 30 to 50 days in the other countries.

Belgium

Spain

France

ireland

italy

netherlands

Portugal

United Kingdom

30 - 90

90 - 120

30 - 60

30 - 60

30 - 120

0 - 90

90 - 120

30 - 60

The business view is that payment delays are primarily due to buyers having financial problems.

It is acknowledged, however, that lateness may be deliberate and reflect a unilateral “optimizing” attempt, at the expense of the industrial or commercial supplier affected by the delay.

2. Increased restrictions on bank credit leave corporations without the means to finance their working capital needs

As the above overview indicates, businesses in Europe continue to be in a difficult financial position: payment delays remain significant.

21

A promising market for collaborative Supplier Finance:

The banks must, for their part, deal with an increase in risks (the worsening of the economic environment means an increase in loss experience) as well as the stricter prudential rules imposed on them (Basel II and III).

Access to credit automatically became more restricted throughout the economy as an increasing number of companies were having ever more unmanageable cash shortage problems.

The European Payment Index 2010, an Intrum Justitia survey of more than 6000 businesses in 25 European countries, shows that companies have been feeling the impact of credit restrictions. The survey’s conclusions show the presence in 2010, more than previously, of “companies finding little support from their banks and having to work harder than ever before to implement efficient credit management processes to avoid liquidity problems.”

Accordingly, businesses must deal with these problems (access to credit, collection of receivables) by developing new solutions to have easier access to cash, without putting themselves at risk financially.

3. The financing of trade receivables no longer provides a fully adequate solution to current needs

Short-term financing solutions sometimes used by small businesses to finance their operations have considerably evolved in recent years, partly due to demands by lenders that financing be backed by in rem securities.

As a result, unsecured credit facilities (i.e. not secured by a specific asset) such as bank overdrafts have been gradually replaced by asset-backed financing, such as assignments of receivables by way of security.

There has been an increase in the discounting of notes and trade receivables, and subsequently in factoring.

Factoring, also known as invoice discounting, began to grow faster in Europe at the start of the millennium, when it began to be viewed as an instrument for managing receivables that could also provide enforceable guarantees in the event that the business using it should run into trouble.

Nevertheless, while factoring can help companies gain rapid access to cash, it can also be a costly and, at times, restrictive solution to implement or access.

Collaborative Supplier Finance, which provides for secure transactions and is, at the same time, simple to use and flexible, therefore seems to be an innovative financing alternative that has its legitimate place in the array of financing solutions available today.

22

Diagram showing the main current financing and payment solutions

Source: Mazars 2012

Methods

inte

rest

ed p

artie

sB

uyer

sSu

pplie

rs

Simple Complex

Conventional Supplier FinanceDynamic

Discounting

Discounting

VCOM

Dailly Act assignments

Conventional factoring

Confidential factoring

Securitization

Collaborative Supplier Finance

4. The growth of Supplier Finance in Europe

It is difficult to estimate the number and value of Supplier Finance programs operating in continental Europe, although some large programs are indicative of the growth of this practice.

Over the past few years, large corporations have confirmed their interest in this kind of arrangement. Feasibility studies have become more frequent and are expected to produce concrete results in coming months.

Several opposing factors account for this trend.

Tensions resulting from the worsening economic environment create incentives for buyers to hold on to or rebuild their cash balances. It thus becomes more tempting to defer payments to suppliers.

However, such a practice – which is prohibited by domestic regulations (see the LME Act in France) – can place suppliers at risk and threaten the operation of the supply chain, in particular in sectors where suppliers are considered strategic.

Growth prospects are therefore very promising for supply chain finance solutions in general and Supplier Finance in particular.

In France, for example, where the aggregate factoring volume was 153 billion euros in 2010, it is estimated that about 10% of that total corresponds to financing by means of Supplier Finance programs.

The implementation of new programs and the growth of existing ones suggest that volume may have increased by close to 30%, or about twice as much as for conventional factoring (which was up 15% at the end of September 20111 – Source ASF).

23

Supplier Finance, a collaborative approach to cash flows

For corporate treasurers, Supplier Finance is nothing new. It is perfectly consistent with payment methods used for more than ten years. Why then has it remained so little known and is it not more frequently used by businesses?

The first reason simply has to do with the fact that the arrangements, because of their nature, have only involved a limited number of suppliers.

A second reason, which is related to the 2008 recession and the so-called subprime crisis, is that credit has become more selective. The gap between the rates at which highly-rated firms can borrow and the rates charged to average companies has widened and become more closely dependent on credit rating. Before 2008, lending rates had become disconnected from risks.

The third reason is structural. Prior the current liquidity crisis, buyers and suppliers had easier access to credit at competitive rates, with interest rates frequently more favorable that those charged under existing Supplier Finance programs.

The current economic environment has therefore favored the emergence of a new form of Supplier Finance to complement the collaborative supply chain. This new form of Supplier Finance was a natural financial extension of the supply chain and has become one of the primary factors in the development of supply chain finance. Collaborative Supplier Finance thus appears to be the missing link between the security of supplies and the management of working capital.

1. Supplier Finance: a strategy for optimizing working capital or for securing suppliers?

Supplier Finance: a single term covering two separate objectives

The primarily purpose of conventional Supplier Finance is to use and generate substantial funds in the form of discounts offered by suppliers, while having the least possible impact on the buyer’s working capital requirements. The programs generally concern a small number of suppliers, for which discounting is a normal commercial practice, and they mainly seek to maximize benefits for the buyer.

The fact that conventional Supplier Finance is essentially financial in scope and represents a payment practice that is often strongly promoted by buyers has given it a somewhat negative image among suppliers.

What collaborative Supplier Finance seeks to do is to make prepayment on favorable terms available to suppliers. This in turn allows a buyer, if necessary, to negotiate longer payment terms without impacting the working capital of its suppliers and, in any event, to make its supplies from companies enrolled in the program more secure.

Supplier Finance, a collaborative approach to cash flows

24

Because collaborative Supplier Finance is by definition collaborative, the benefits that buyers can expect are of a more operational than purely financial nature.

Programs described as Supplier Finance can accordingly have two different but perfectly complementary objectives.

Conventional and collaborative Supplier Finance approaches are not mutually exclusive

A buyer seeking to obtain direct financial gains and operational benefits would have to place the cursor halfway between the two objectives in its Supplier Finance system.

Balance between reserve factoring approaches

Source: Mazars 2012

Marketing fee

Bank fees

Collaborative SF

Marketing fee

Bank fees

traditional SF

Search for operational gains

Search for financial gains

If the buyer cannot achieve its objectives with a single Supplier Finance program, setting up two programs – one conventional and the other collaborative – may be contemplated.

In this connection, certain buyers with conventional Supplier Finance programs are now developing more collaborative programs but are not terminating their previous arrangements.

2. Collaborative Supplier Finance: the benefits of a collaborative approach to cash flows

Recent events (the financial crisis, the recession, the liquidity crisis, natural disasters, etc.) have raised the awareness of the economic and industrial system’s fragility. Corporations have responded by seeking to intensify collaboration between their own departments and with their customers and suppliers. This collaborative effort often focuses exclusively on operational issues and neglects the cash flow dimension.

25

Supplier Finance, a collaborative approach to cash flows

By including cash flow management in this collaborative effort, companies are better able to operate in an increasingly volatile and demanding environment. Collaborative Supplier Finance is an effective way of combining physical transactions with financial transactions and bringing about the emergence of a supply chain finance approach that is often still at the conceptual stage.

improved corporate resilience

A corporation’s capacity to adapt, innovate and grow in a complex or difficult sector does not only depend on its know-how, processes or financial health. It is also essential for it to develop strong relationships with its customers and suppliers.

When used in a fair manner, a collaborative Supplier Finance program can reinforce a corporation’s economic ecosystem at little cost and give it a long-term competitive advantage.

As an illustration of the foregoing, the observation has been made that suppliers with a limited ability to deliver their services tend to favor buyers with collaborative Supplier Finance programs over others, primarily because they are paid earlier and their collection costs are lower.

Thus, buyers can improve their resilience by limiting the risk of a break in supply or failure by their suppliers.

Optimized working capital

In an environment where access to cash is becoming more problematic, even for large corporations, the efficient use of overdraft facilities extended by banks has become more critical for business.

This also holds true for short-term credit facilities, and it has therefore become crucial for treasurers to find alternative sources of funds, so that existing bank overdraft facilities can be used with a certain degree of flexibility.

In practical terms, a buyer that has negotiated specific short-term facilities in order to have the resources needed to pay for its purchases from suppliers in cash would arrive at the same result with a Supplier Finance program that significantly lightens its debt burden (by doing away with the initial short-term credit facilities).

Likewise, a cash-rich buyer financing the same type of program with its available cash could use the Supplier Finance to refinance its working capital by reclaiming excess cash.

As for collaborative Supplier Finance programs, they provide buyers with additional leverage when negotiating improved payment terms in return for low-cost short-term financing for its suppliers.

However, this optimization approach can be hampered by certain specific domestic regulations (e.g. the LME Act in France, which sets the maximum permitted contractual payment period at 60 days), and particular attention must be placed on ensuring that trade payables are not reclassified to debt.

26

Secured supplies

Collaborative Supplier Finance is a natural outcome of collaborative measures initiated by corporations with their suppliers, including in the field of logistics. One of the major benefits of collaborative Supplier Finance is that it provides security for the company’s suppliers by ensuring efficient cash flow management.

The greater the share of savings from a collaborative Supplier Finance program set aside by a buyer for its suppliers, the more secure that buyer’s supplies – and, ultimately, its suppliers – will be, as suppliers will become partly independent of financial market conditions, which are often highly volatile for suppliers affected by fluctuations in the economy.

Through collaborative Supplier Finance, a buyer can, if it wishes, be a responsible economic participant in a sustainable development strategy for its business ecosystem.

An improved purchase mix

“Fully aware of the limits imposed by environmental conditions, a client can try and give its company more discretion in its choices by the addition of ‘purchase marketing’” (Cova, 1992).

Now more than before, buyers find it absolutely necessary to include in the purchase mix conditions relating to the environment, especially the economic environment. Collaborative Supplier Finance can provide security for a purchasing policy or procurement strategy by fostering continued sound, value-creating competition, with prices based on the products or services sold rather than on the suppliers’ available financing terms.

Beyond these strategic considerations, collaborative Supplier Finance simply provides significant leverage for optimizing the total cost of ownership (TCO).

By relying on the transparency of financial relationships with suppliers, the buyer can lower its purchasing costs, as the prices of products and services it buys no longer have to reflect:

• the former financing cost, which was sometimes very high;

• the average payment period, as the supplier can now keep track of invoices coming due and optimize its cash flow without needing to add further markups.

Lower purchase prices represent an important potential direct financial return from collaborative Supplier Finance, even though that part of the financial benefits is more difficult to measure when arranging the program.

27

Setting up a Supplier Finance program

The setting up of a Supplier Finance program is a project that involves several parties, both within the company (financial and accounting management, purchasing, operating departments, etc.) and outside it (suppliers, finance partners, technological service providers, etc.).

Planning for this kind of project is a necessary step that, over time, will make it possible for both the buyer and its suppliers to take full advantage of Supplier Finance arrangements.

The next part of this document provides brief explanations of all of the steps involved in a project to set up a conventional or collaborative Supplier Finance program.

the successive steps in a Supplier Finance project

Source: Mazars 2012

Defining the program’s

objective

Carrying out the program

Securing the program

Rolling out the program

expanding the program

1. Setting objectives for the Supplier Finance program

Objectives and strategy

Following validation of the prerequisites, as set forth in the section “Two prerequisites for Supplier Finance,” it is essential to first define the objective underlying the Supplier Finance project. Based on the feedback received about this type of program, it seems evident that it is one of the critical phases of the project.

Supplier Finance is not a miracle solution that will produce a maximum of net EBIDTA increases along with financing at very attractive rates for suppliers. Furthermore, the business model must include the cost of bank and technological services charged, without which the program cannot operate.

Setting up a Supplier Finance program

28

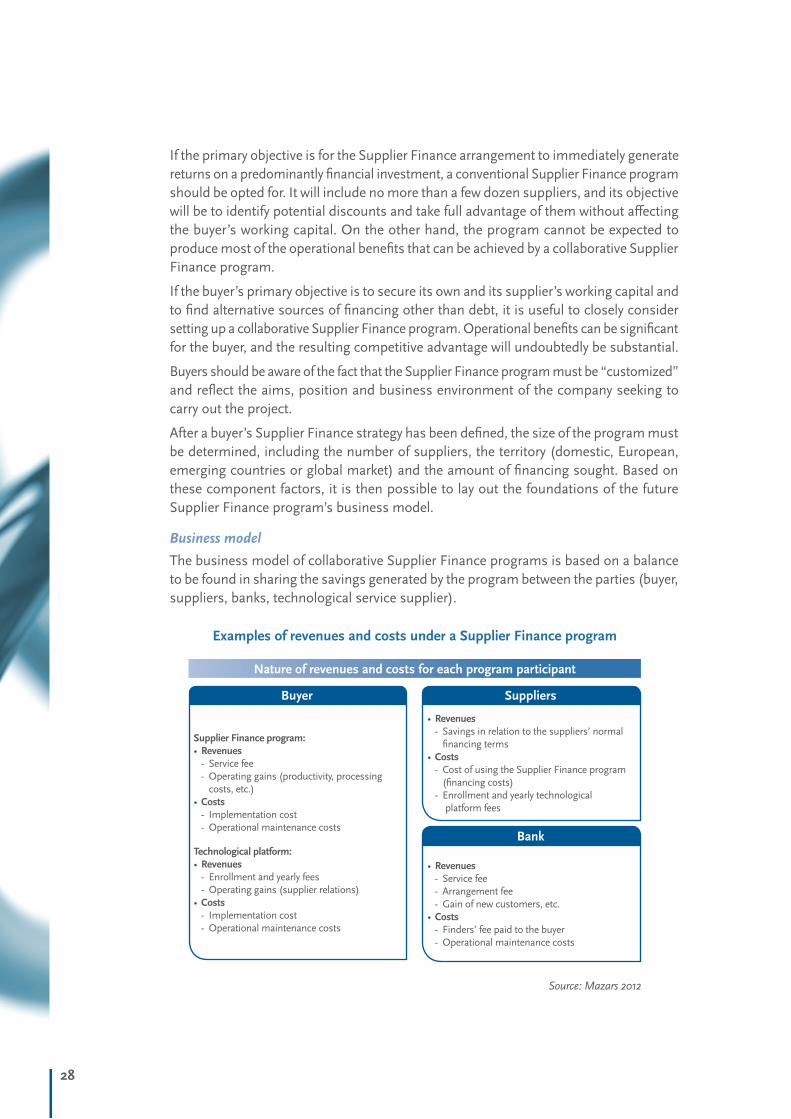

If the primary objective is for the Supplier Finance arrangement to immediately generate returns on a predominantly financial investment, a conventional Supplier Finance program should be opted for. It will include no more than a few dozen suppliers, and its objective will be to identify potential discounts and take full advantage of them without affecting the buyer’s working capital. On the other hand, the program cannot be expected to produce most of the operational benefits that can be achieved by a collaborative Supplier Finance program.

If the buyer’s primary objective is to secure its own and its supplier’s working capital and to find alternative sources of financing other than debt, it is useful to closely consider setting up a collaborative Supplier Finance program. Operational benefits can be significant for the buyer, and the resulting competitive advantage will undoubtedly be substantial.

Buyers should be aware of the fact that the Supplier Finance program must be “customized” and reflect the aims, position and business environment of the company seeking to carry out the project.

After a buyer’s Supplier Finance strategy has been defined, the size of the program must be determined, including the number of suppliers, the territory (domestic, European, emerging countries or global market) and the amount of financing sought. Based on these component factors, it is then possible to lay out the foundations of the future Supplier Finance program’s business model.

Business model

The business model of collaborative Supplier Finance programs is based on a balance to be found in sharing the savings generated by the program between the parties (buyer, suppliers, banks, technological service supplier).

examples of revenues and costs under a Supplier Finance program

Source: Mazars 2012

nature of revenues and costs for each program participant

Buyer Suppliers

Bank

Supplier Finance program:•Revenues

- Service fee - Operating gains (productivity, processing costs, etc.)

•Costs - Implementation cost - Operational maintenance costs

technological platform:•Revenues

- Enrollment and yearly fees - Operating gains (supplier relations)

•Costs - Implementation cost - Operational maintenance costs

•Revenues - Savings in relation to the suppliers’ normal financing terms

•Costs - Cost of using the Supplier Finance program (financing costs)

- Enrollment and yearly technological platform fees

•Revenues - Service fee - Arrangement fee - Gain of new customers, etc.

•Costs - Finders’ fee paid to the buyer - Operational maintenance costs

29

Setting up a Supplier Finance program

In order to select the business model best suited to the buyer’s strategy, it is essential to rely on statistical models to:

• draw up a dependable, accurate business model that can be successfully defended before the project’s sponsor or the company’s executive board

• provide for the neutrality of the arrangement, in which the parties may have conflicting interests.

At the end of the first step, it is important to obtain the executive board’s support for the project and to remove any ambiguity regarding the program’s objectives.

2. Carrying out the Supplier Finance project

Once the buyer’s objectives have been defined and the size of its program determined in accordance with an approved business model, an operating strategy must be adopted and the Supplier Finance program must be put in place.

This development phase will rely on a detailed analysis, followed by a an operating action plan in two areas:

• the organization of the buyer and its processes;

• the finance and technological partners participating in the program.

When putting into place a Supplier Finance system, special attention must be given to building the scenarios. They must take into consideration:

• the strategic and tactical aspects of choosing finance and technological partners;

• the program’s operational, technical, legal and accounting risks (e.g. reclassification of trade payable to debt in the case of publicly-traded companies).

Four critical areas of concern when launching a Supplier Finance program

Source: Mazars 2012

Supplier Finance program

Market

Maturity

• Interested finance partners•Reported and quantified suppliers’ interests•Buyer’s stated objective

•Sufficiently large purchase base•Controlled and rapid payment approval procedure•Access to data from IT systems

improvement margins• Increase in eligible purchases•Purchasing department’s support•Extension of the program’s reach

(internationalization, corporate subsidiaries, etc.)

Arrangement•Defined business model•Rising volume strategy •Legal frameworks•Control of risks, including

reclassification of payables to debt

• Improved EBITDA and operating benefits from payment procedures to identified suppliers

30

Briefly stated, at the end of this project phase, it is necessary to:

• update the model in light of an analysis of the buyer’s business processes and environment and, where applicable, observations by the other parties;

• draw up a detailed timetable for the project and the related operational action plan;

• secure the project sponsors’ agreement for an operational pilot project to verify the scenarios contained in the business plan;

• prepare a request for proposals to be sent to potential financial and technological partners for the pilot project and its practical realization, where applicable.

3. Securing the Supplier Finance arrangement

Buyers generally focus their attention mainly on outside obstacles to their Supplier Finance project, such as the applicable interest rates relative to those of the market, their suppliers’ confidence or hesitations regarding the program, etc.

While it is true that those outside factors should not be disregarded, there can also be considerable internal obstacles to overcome. They generally have to do with a lack of comprehension regarding the purpose of the program and, at times, with a lack of support from the supplier relations or purchasing departments, generally based on operational considerations.

Lastly, in the case of publicly-traded corporations or their subsidiaries, making the system secure will necessarily require a detailed analysis so as to limit the risk that trade payables be reclassified to debt.

4. Rolling out of the Supplier Finance system

For all of the foregoing reasons, prudence must be used when seeking to set up a Supplier Finance program with the help of an operational pilot project.

There is a special observation period during which the processes can be tried out, the organization tested and the relationship with partners strengthened. It is essential to examine how the suppliers are going to use the new system, so that the program can be adjusted to reflect the buyer’s specific circumstances. It is advisable to rely on the program’s predefined operating indicators to make all statistical evaluations required to optimize its effectiveness when it becomes fully operational.

Ideally, there should be a six-month pilot observation period during which the behavior of suppliers can be monitored over a full accounting cycle. In the case of collaborative Supplier Finance programs, where the buyer initiates the request for financing, it has been observed that requests for funds are often submitted on certain days of the month and coincide sometimes closely with the end of accounting periods. If this is the case, the suppliers should be encouraged to opt for a systematic financing of their receivables. This would result in a more efficient use of the facilities extended to the program by the finance partners.

31

Setting up a Supplier Finance program

5. Expanding the Supplier Finance arrangement

At this point in the project, an implementing strategy must be adopted for the selected Supplier Finance program. The extension of the program to a larger number of suppliers, buyers (e.g. a corporation’s subsidiaries) and countries, if any, can require that the number of finance partners working with the program be increased.

The buyer now has the choice between at least two strategies:

• dealing with a bank syndicate, which would increase the financing available under the arrangement, while leaving a single finance partner in charge of the program; this approach has the advantage of facilitating the everyday management of the Supplier Finance program, but is often difficult to arrange, and costly, with any additional expenses reducing the appeal of the program;

• adding new finance partners to the program, which entails a new competitive bidding procedure; this approach promotes healthy competition between banks and broadens the choice of partners for the buyer. It is easier to use when the program relies on a non-bank technological platform; however, in response to the growing demand, banks have recently started to give other bank partners access to their Supplier Finance services.

The purpose of this phase is to ensure the long-term future of the buyer’s Supplier Finance program, so as to accomplish the objectives set by the buyer in its business model. In the case of collaborative Supplier Finance programs, their long-term survival depends on whether all of the parties derive an economic benefit over time, in particular the finance partners, which otherwise will seek a way out, probably at the expense of the suppliers.

6. Managing a Supplier Finance program’s technological aspects

The integration, configuration, rollout and operation of the platform are the essential phases of its utilization. The credibility and success of a Supplier Finance program can depend on how well they are managed.

integration and configuration

During this project stage, the characteristics and users of the legal entities of all stakeholders (buyers, suppliers, banks) and the program’s features (currencies, ceilings, eligible suppliers, etc.) are defined on the platform. The data can be loaded and updated either manually or automatically.

For data flows (invoices, payment forms, financing requests, transfer orders, etc.), interfaces are created between the platform and the buyer and the banks’ IT systems so that information may be retrieved, securely shared and automatically integrated.

This can be achieved rapidly if there are existing links between the buyer’s IT system and the platform (originally established for the purpose of an electronic billing project, for example).

32

Rollout

This step in the project concerns the enrollment of suppliers in the Supplier Finance program. To be truly effective, it must cover the promotion and facilitation of the finance partner’s contracting procedures, and the activation of the program for each supplier.

Promotion can be facilitated if a supplier is already connected to the platform for other purchase-to-pay transactions, or as part of a simulation process using its actual data.

In order to facilitate the work of the finance partners’ sales representatives, assistance with contracting procedures must involve a clear explanation of prerequisites for enrolling in the program and the easy downloading of the banks’ contractual documents.

Operation

This program’s operation entails the automatic processing of all data flows between the platform and the participants, the availability of online services to apply for financing, and access to both the overall and detailed monitoring of the programs’ performance.

This operation must obviously entail commitments regarding the level of service in terms of the platform’s availability andthe time needed to process shared files, eliminate bugs and respond to requests for changes.

The most critical aspects of the technological platform’s operating phase are its scalability (the ability to handle a growing volume of data and users), security (identification of the users, confidentiality and integrity of the data) and, of course, its traceability (audit trail).

33

In the current economic environment, and with liquidity restrictions, companies seek to be economically creative in order to continue improving their competitiveness, resilience and flexibility. In this endeavor, traditional Supplier Finance arrangements have evolved to become more open, attractive and, in the end, collaborative, thus helping finance management to become an in-house business partner in the same way as operation management.

This new mode of collaborative Supplier Finance now occupies an important place among supply chain finance instruments and, hence, complements measures carried out by business over the past ten years that are aimed at optimizing physical flows.

Other financing solutions are likely to be developed at an even earlier point along the supply chain, based on the experience accumulated in conjunction with future collaborative Supplier Finance programs.

By tracking commercial transactions between parties from start to finish, keeping a record of those relations and facilitating the production of data shared by all parties along the supply chain, collaborative platforms will enable banks to back loans with underlying instruments (order forms, receipts, invoices, payment approvals) that remain little used today, thus improving the security of their financing.

Greater harmonization and synchronization of physical and financial information flows is what is ultimately needed to give the supply chain the necessary visibility that will facilitate and reinforce the relationship among its various participants.

Conclusion

Conclusion

34

The above analyses are based on consulting work done by Mazars in France and elsewhere, in both the manufacturing and service sectors. The result reflects the combined expertise of Mazars and b-process regarding Supplier Finance arrangements.

The findings of this white paper have been verified through observations made in the course of our work with our customers or discussions with our partners.

We have improved our knowledge and our analyses with the help of feedback by buyers and banks who agreed to talk to us in connection with the drafting of this white paper, in particular:

Mr. CROUZET, Auchan / Mr. LEVENES, Conforama / Mrs DESTOMBES and Mr. LABBE, EDF / MM. BORA and DRAY, ABN Amro / Mrs DOURIEZ-SOROVIC and SURMELY, BNP Paribas Factor / MM. BARONE, LEPOUTRE and VILLEBRUN, CGA / Mr. AMBROSINO, Crédit Agricole / Mr. BLAS, Deutsche Bank / Mrs MOSSER and Mr. PORTE, Euler-Hermes / Mr. GUERARD, ING.

Methodology

The content of this White Paper is provided for information use only.

Neither Mazars, b-process nor any other contributor to this content shall be held responsible for its further utilization.

Propriety of Mazars and b-process – All rights reserved, March 2012.

Doc

umen

t pri

nted

on

60%

rec

ycle

d pa

per,

40%

unr

ecyc

led

pape

r w

ith a

n ec

o-fr

iend

ly d

esig

n w

hich

red

uces

env

iron

men

tal i

mpa

ct

Bibliography “Comportement de paiement des entreprises en Europe” Third quarter of 2011 analysis - Altares

“European Payment Index 2011” Intrum Justitia

“Rapport 2010” Le Médiateur des Ministères de l’Economie et du budget

“Trends in Lending – July 2011” Bank of England

“2010 – Rapport Annuel” Observatoire des délais de Paiement

“Les affactureurs s’inquiètent des effets de Bâle 3 sur leur secteur” Agefi Hebdo, 8/11/2011

“Le reverse factoring: un outil au service de la LME et des délais de paiement” La Lettre du Trésorier 02/2009

“Les grandes entreprises séduites par les atouts du "reverse factoring"“ Agefi Hebdo , 03/2009

“Supply Chain finance: What’s it worth?” IMD International, 2009

“Supply chain finance: From myth to reality” - Mc Kinsey on Payments 10/2010

“Supply chain on Swift – Issue 6” Swift, Q2 2011

“Supply Chain finance: comment préparer le futur ?” Mazars, 2011

Contacts:

Mazars

Miguel de FontenayManaging Partner Global ConsultingTel.: +33 (0) 1 49 97 65 55E-mail: [email protected]

Hervé BlazejewskiManaging Partner ConsultingTel.: +33 (0) 1 49 97 62 69E-mail: [email protected]

Philippe BourdonManaging Partner ConsultingTel.: +33 (0) 1 49 97 66 69E-mail: [email protected]

b-process

Alexis RenardVice President Ariba, General Manager b-process Tel.: +33 (0) 55 50 48 48E-mail: [email protected]

Jean-Cyril SchütterléBusiness Development DirectorTel.: +33 (0) 1 55 50 48 58 E-mail: [email protected]

Cyril Broutin Supply Chain Finance ManagerTel.: +33 (0) 1 55 50 48 58 [email protected]

Mazars61, rue Henri Regnault92075 Paris - La Défense CedexTel.: +33 (0) 1 49 97 60 00Fax: +33 (0) 1 49 97 00 01

b-process4, rue de Ventadour75001 ParisTel.: +33 (0) 55 50 48 48Fax: +33 (0) 1 55 50 48 49

www.mazars.fr www.b-process.com

Con

cept

ion:

Maz

ars,

Com

mun

icat

ion

-Bro

ch 7

2 - E

N 0

5/12

Related Documents