When and How will the Global Economy Recover ? Philip Suttle IIF, Director of Global Macroeconomic Analysis Garanti Masters Private Banking Conference Istanbul, Turkey April 17, 2009

When and How will the Global Economy Recover ?

Jan 01, 2016

When and How will the Global Economy Recover ?. Philip Suttle IIF, Director of Global Macroeconomic Analysis Garanti Masters Private Banking Conference Istanbul, Turkey April 17, 2009. An Organizing Framework. - PowerPoint PPT Presentation

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

When and How will the Global Economy Recover ?

Philip SuttleIIF, Director of Global Macroeconomic Analysis

Garanti Masters Private Banking Conference Istanbul, Turkey

April 17, 2009

2

An Organizing Framework

A different kind of global business cycle, driven by private credit, not public (monetary and fiscal) policy

The private credit cycle is global in nature, albeit with some sector, country and regional concentration

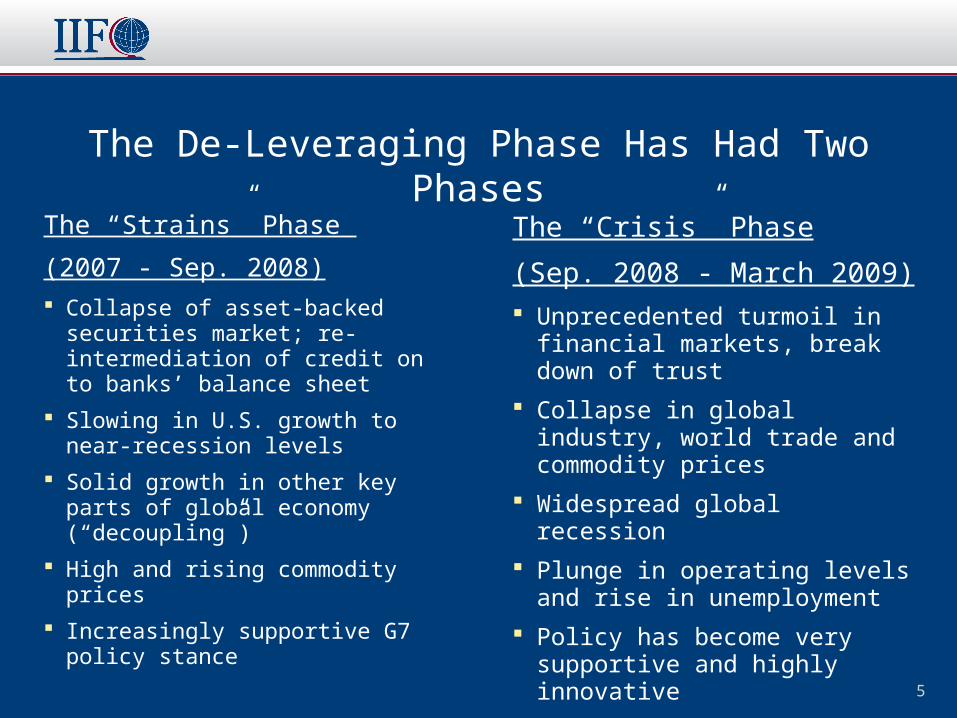

The downleg of this cycle (“the de-leveraging phase”) has come in two parts: the “strains” phase (early 2007 – Sept 2008) and the “crisis” phase (Sept 2008 – Mar 2009)

The best way to characterize our global outlook is that we are projecting a return to conditions more consistent with the “strains” phase in the months ahead

3

Global Capital Flows and the Global Business Cycle

0

4

8

12

16

20

1969 1973 1977 1981 1985 1989 1993 1997 2001 2005 2009

-20

-15

-10

-5

0

5

10

15

20

Fed Funds Rate

Manufacturing Output

Pre-1992 Post-1992

Rates drive the cycle Rates driven by the cycle

percent percent change oya, inverted scale

4

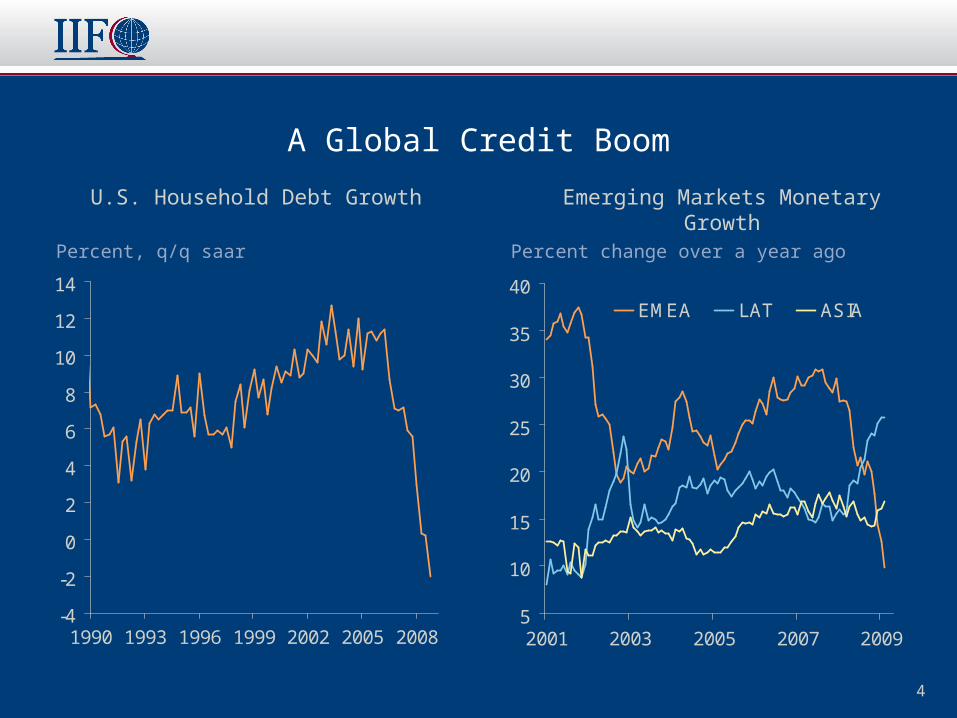

A Global Credit Boom

-4

-2

0

2

4

6

8

10

12

14

1990 1993 1996 1999 2002 2005 2008

Percent, q/q saar

U.S. Household Debt Growth Emerging Markets Monetary Growth

Percent change over a year ago

5

10

15

20

25

30

35

40

2001 2003 2005 2007 2009

EMEA LAT ASIA

5

The De-Leveraging Phase Has Had Two Phases

The “Strains” Phase

(2007 - Sep. 2008) Collapse of asset-backed securities

market; re-intermediation of credit on to banks’ balance sheet

Slowing in U.S. growth to near-recession levels

Solid growth in other key parts of global economy (“decoupling”)

High and rising commodity prices

Increasingly supportive G7 policy stance

The “Crisis” Phase

(Sep. 2008 - March 2009) Unprecedented turmoil in financial

markets, break down of trust

Collapse in global industry, world trade and commodity prices

Widespread global recession

Plunge in operating levels and rise in unemployment

Policy has become very supportive and highly innovative

6

The Current Global Slump is Unprecedented: Deep and Synchronized

-30

-25

-20

-15

-10

-5

0

5

10

15

20

06 07 08 09-35

-30

-25

-20

-15

-10

-5

0

5

10

Emerging Markets (left axis)

G3 (right axis)

Percent, 3m/3m, saar (both axes)

Global Exports and Manufacturing Production

Percent, 3m/3m, saar (nominal terms)

-60

-50

-40

-30

-20

-10

0

10

20

30

40

2006 2007 2008 2009-35

-30

-25

-20

-15

-10

-5

0

5

10

Goods Exports(left axis)

Mfg. Production(right axis)

Manufacturing Production

Percent, 3m/3m, saar

7

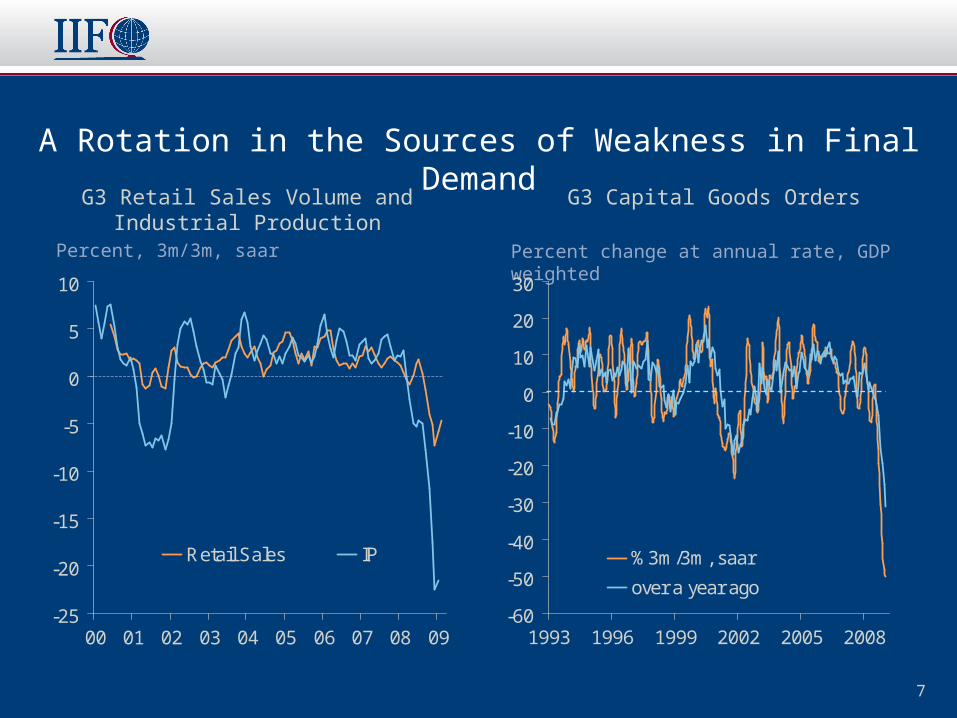

A Rotation in the Sources of Weakness in Final Demand

-25

-20

-15

-10

-5

0

5

10

00 01 02 03 04 05 06 07 08 09

Retail Sales IP

Percent, 3m/3m, saar

G3 Capital Goods Orders

Percent change at annual rate, GDP weighted

-60

-50

-40

-30

-20

-10

0

10

20

30

1993 1996 1999 2002 2005 2008

%3m/3m, saar

over a year ago

G3 Retail Sales Volume and Industrial Production

8

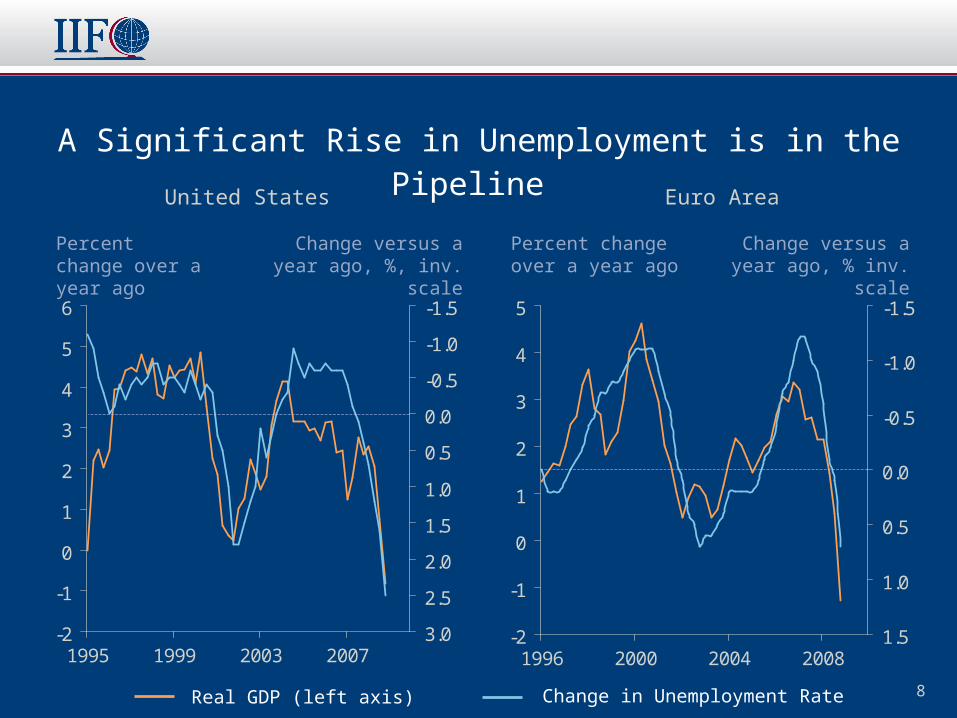

A Significant Rise in Unemployment is in the Pipeline

-2

-1

0

1

2

3

4

5

6

1995 1999 2003 2007

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Percent change over a year ago

Euro Area

Percent change over a year ago

-2

-1

0

1

2

3

4

5

1996 2000 2004 2008

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

United States

Change versus a year ago, % inv. scale

Change versus a year ago, %, inv. scale

Real GDP (left axis) Change in Unemployment Rate

9

A Significant Rise in Unemployment is in the Pipeline (2)

-5

-4

-3

-2

-1

0

1

2

3

4

5

1995 1999 2003 2007

-0.8

-0.4

0.0

0.4

0.8

1.2

Percent change over a year ago

Emerging Asia

Percent change over a year ago

1

3

5

7

9

11

1996 2000 2004 2008

-0.4

-0.2

0.0

0.2

0.4

0.6

Japan

Change versus a year ago, % inv. scale

Change versus a year ago, %, inv. scale

Real GDP (left axis) Change in Unemployment Rate

10

A Significant Rise in Unemployment is in the Pipeline (3)

0

1

2

3

4

5

6

7

8

9

1996 2000 2004 2008

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

Percent change over a year ago

Latin America

Percent change over a year ago

-2

0

2

4

6

8

1996 2000 2004 2008

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

Emerging Markets

Change versus a year ago, % inv. scale

Change versus a year ago, %, inv. scale

Real GDP (left axis) Change in Unemployment Rate

11

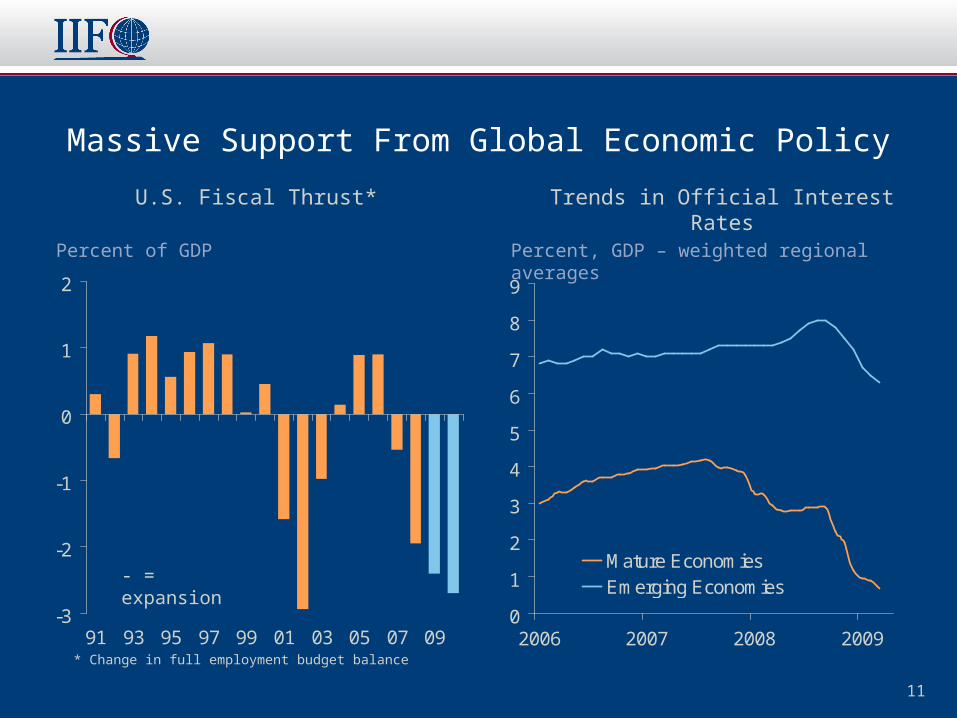

Massive Support From Global Economic Policy

-3

-2

-1

0

1

2

91 93 95 97 99 01 03 05 07 09

Percent of GDP

U.S. Fiscal Thrust* Trends in Official Interest Rates

Percent, GDP – weighted regional averages

0

1

2

3

4

5

6

7

8

9

2006 2007 2008 2009

Mature EconomiesEmerging Economies

* Change in full employment budget balance

- = expansion

12

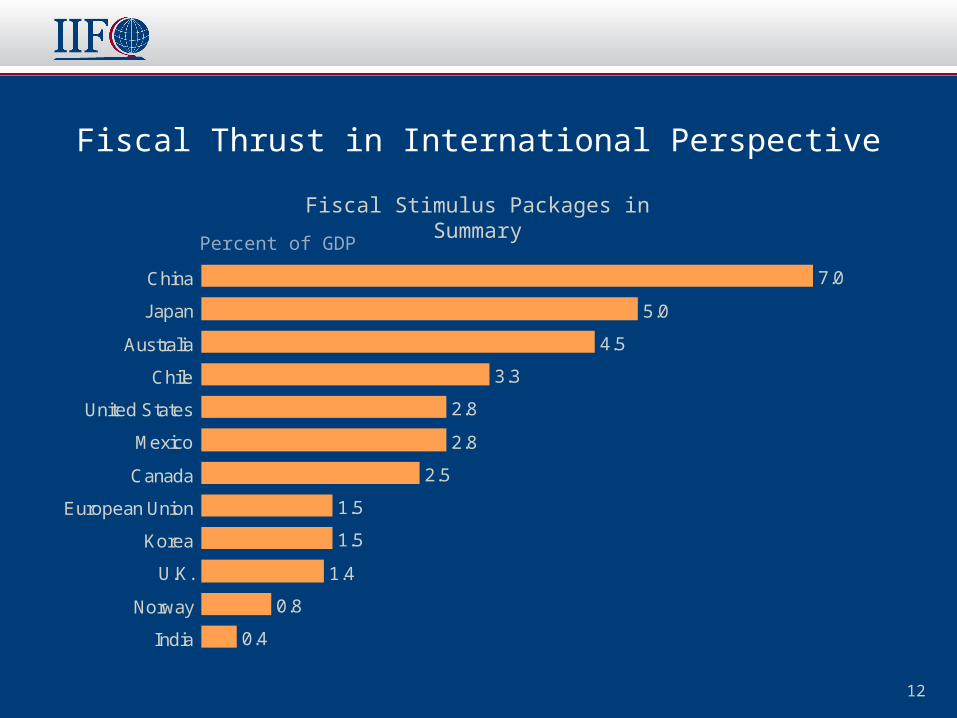

Fiscal Thrust in International Perspective

7.0

5.0

4.5

3.3

2.8

2.8

2.5

1.5

1.5

1.4

0.8

0.4

China

Japan

Australia

Chile

United States

Mexico

Canada

European Union

Korea

U.K.

Norway

India

Fiscal Stimulus Packages in Summary

Percent of GDP

13

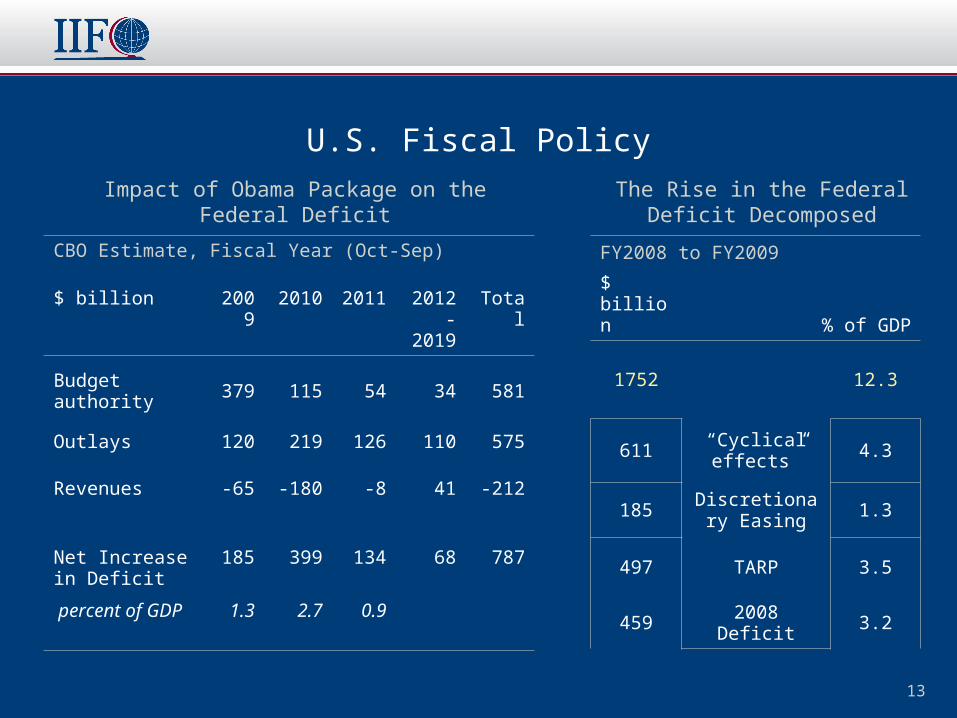

U.S. Fiscal Policy

Impact of Obama Package on the Federal Deficit

CBO Estimate, Fiscal Year (Oct-Sep)

$ billion 2009 2010 2011 2012-2019

Total

Budget authority 379 115 54 34 581

Outlays 120 219 126 110 575

Revenues -65 -180 -8 41 -212

Net Increase in Deficit

185 399 134 68 787

percent of GDP 1.3 2.7 0.9

FY2008 to FY2009

$ billion % of GDP

1752 12.3

611“Cyclical effects”

4.3

185Discretionary

Easing1.3

497 TARP 3.5

459 3.22008 Deficit

The Rise in the Federal Deficit Decomposed

14

Quantitative Easing is the New “New Thing”

50

100

150

200

250

300

350

Jul 07 Nov 07 Mar 08 Jul 08 Nov 08 Mar 09

Fed ECB

BoE BoJ

Central Bank Balance Sheets: Total Assets

Index, end-June 2007=100

BoE 12.6%

Fed 14.5%

ECB 19.7%

BoJ 24.1%

Current Level of Assets (% GDP)

15

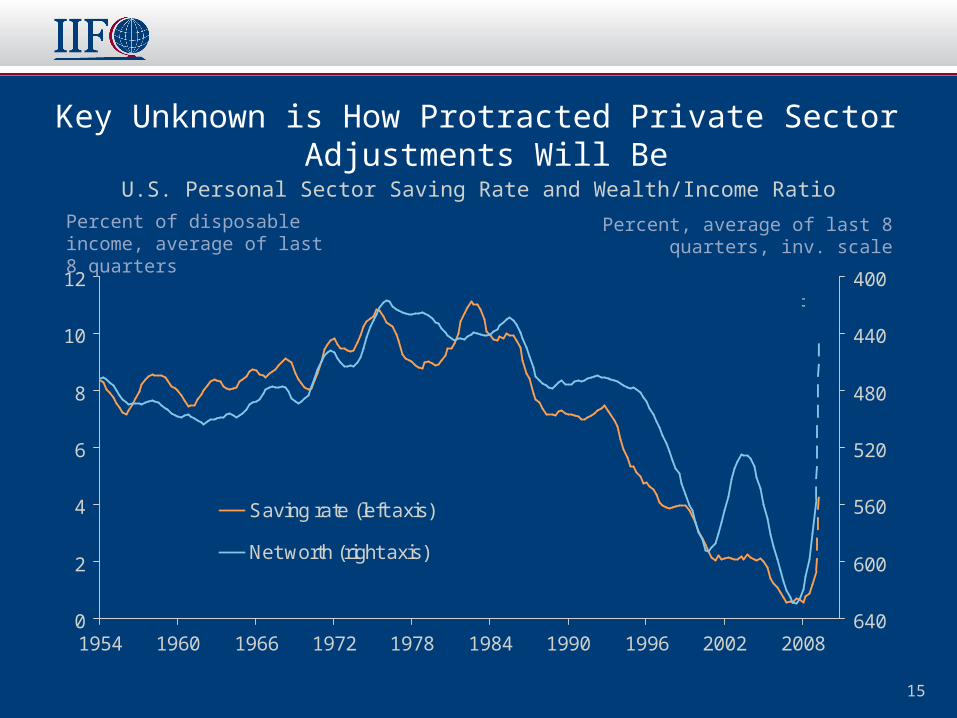

Key Unknown is How Protracted Private Sector Adjustments Will Be

0

2

4

6

8

10

12

1954 1960 1966 1972 1978 1984 1990 1996 2002 2008

400

440

480

520

560

600

640

Saving rate (left axis)

Net worth (right axis)

Dotted lines denote latest estimate (09Q1)

U.S. Personal Sector Saving Rate and Wealth/Income Ratio

Percent of disposable income, average of last 8 quarters

Percent, average of last 8 quarters, inv. scale

16

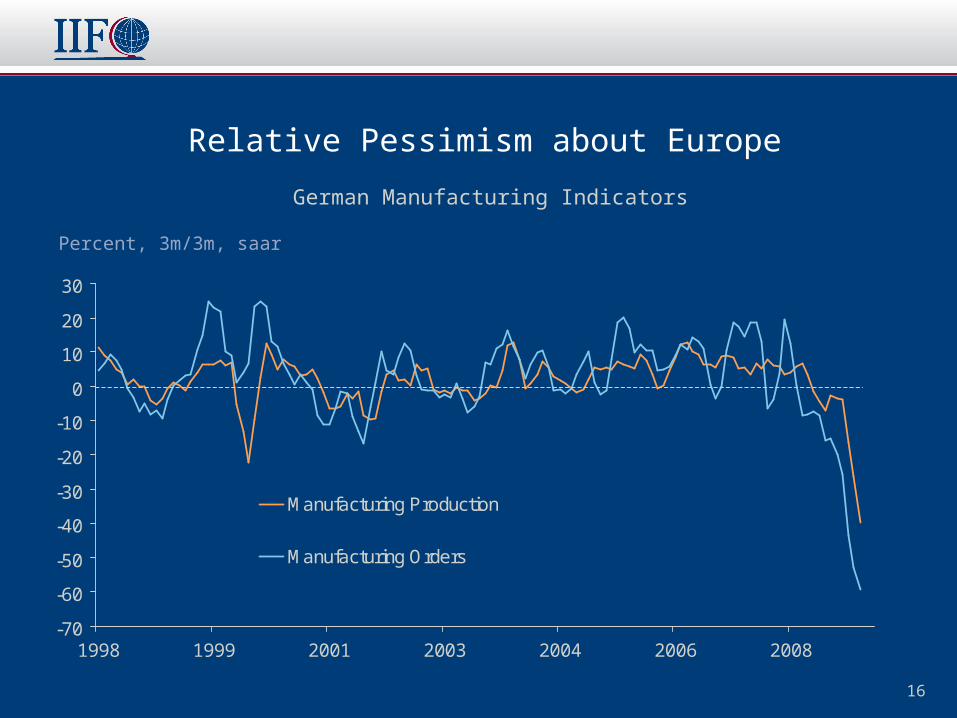

Relative Pessimism about Europe

-70

-60

-50

-40

-30

-20

-10

0

10

20

30

1998 1999 2001 2003 2004 2006 2008

Manufacturing Production

Manufacturing Orders

Percent, 3m/3m, saar

German Manufacturing Indicators

17

Areas of Concern in Europe

Lack of economic flexibility

Lack of policy coordination

Extent of deleveraging ahead in banking systems remains significant

Growing public debt problems in many countries

Over-extended housing markets

Difficulties in Emerging Europe

18

Emerging Europe: The Epicenter of the Third EM Capital Flows Slump since 1980

-1

0

1

2

3

4

5

6

7

1980 1985 1990 1995 2000 2005-2

0

2

4

6

8

10

12

14

Latin America Emerging Asia Emerging Europe (right axis)

Net Private Capital Flows by Major Region

Percent of emerging market GDP Percent of emerging market GDP

19

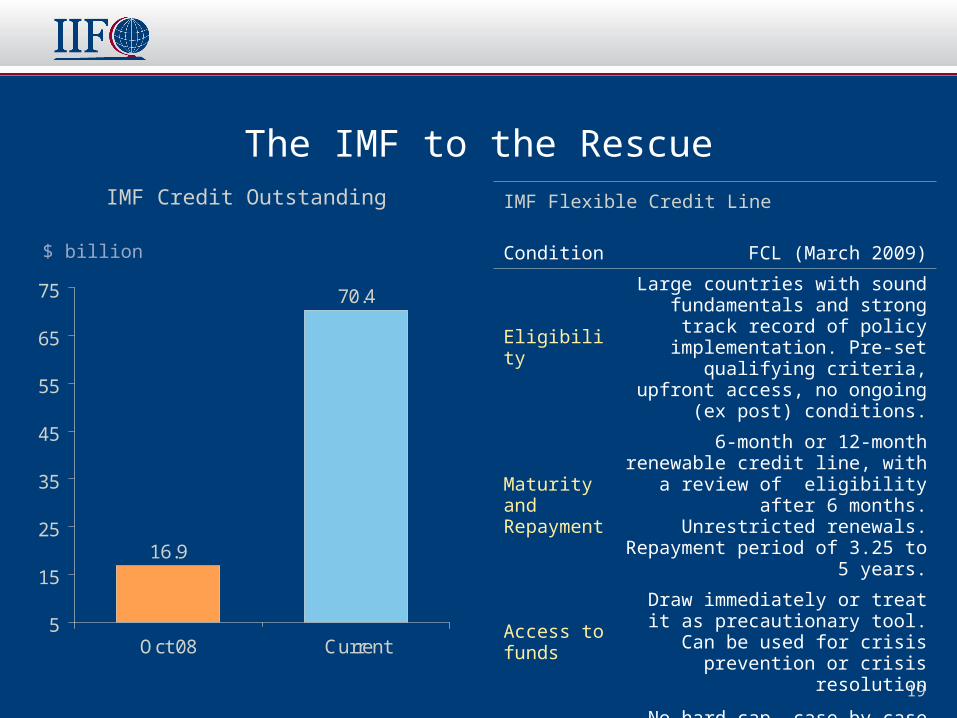

The IMF to the Rescue

16.9

70.4

5

15

25

35

45

55

65

75

Oct 08 Current

$ billion

IMF Credit Outstanding IMF Flexible Credit Line

Condition FCL (March 2009)

Eligibility

Large countries with sound fundamentals and strong track

record of policy implementation. Pre-set qualifying criteria, upfront

access, no ongoing (ex post) conditions.

Maturity and Repayment

6-month or 12-month renewable credit line, with a review of eligibility

after 6 months. Unrestricted renewals. Repayment period of 3.25

to 5 years.

Access to funds

Draw immediately or treat it as precautionary tool. Can be used for crisis prevention or crisis resolution

AmountNo hard cap, case-by-case

assessment

20

There Are Encouraging Signs from China

12

14

16

18

20

22

24

26

2005 2006 2007 2008 2009

Total Loans

M2

China: Monetary Growth

Percent change over a year ago

21

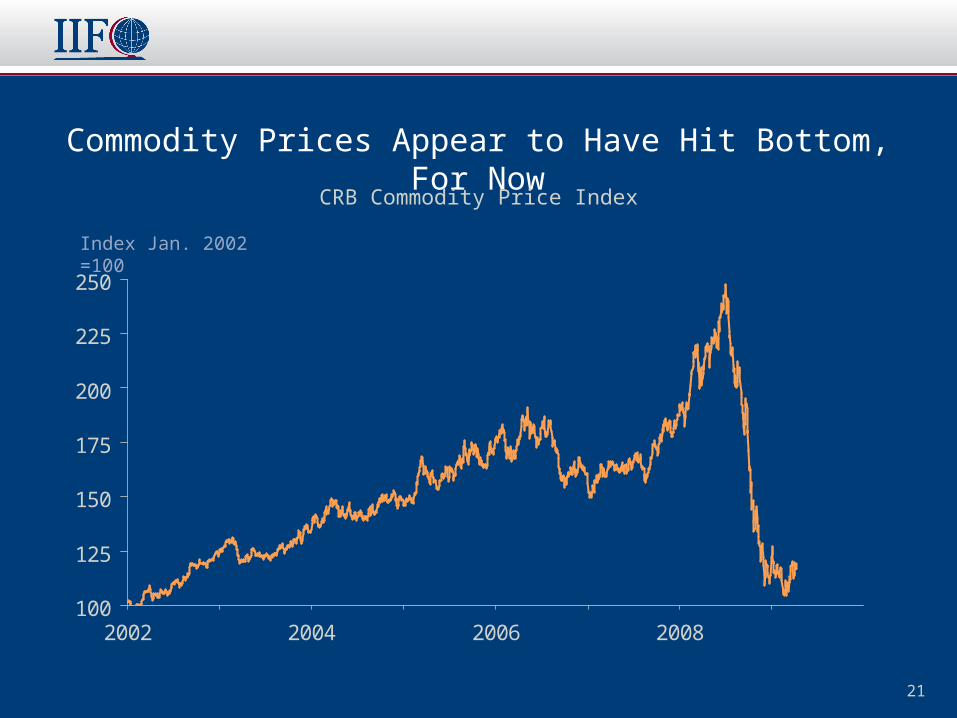

Commodity Prices Appear to Have Hit Bottom, For Now

100

125

150

175

200

225

250

2002 2004 2006 2008

CRB Commodity Price Index

Index Jan. 2002 =100

22

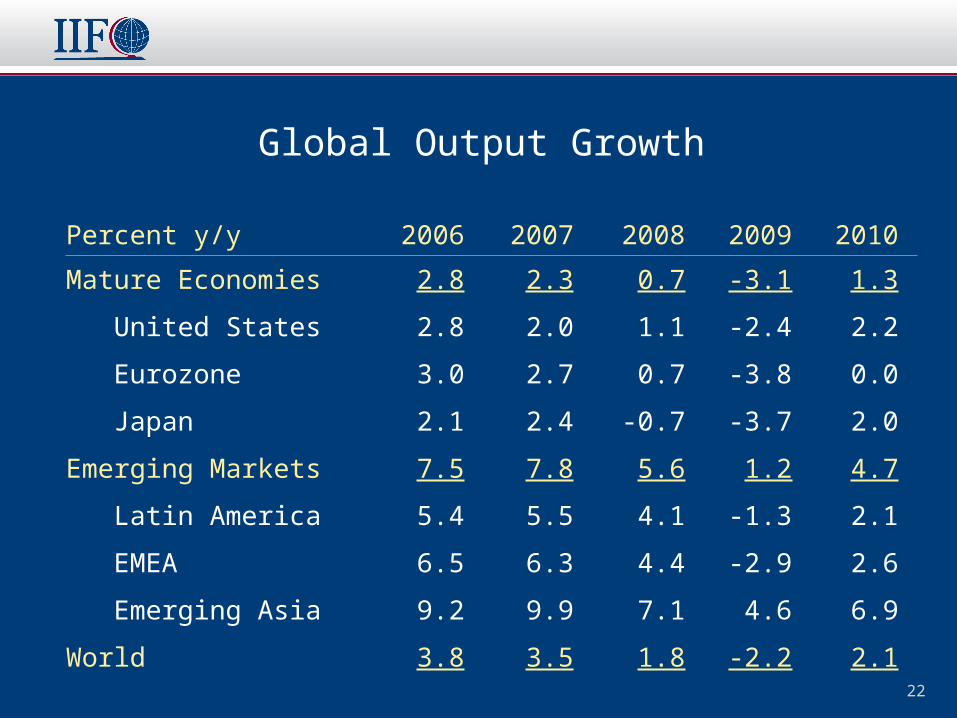

Global Output Growth

Percent y/y 2006 2007 2008 2009 2010

Mature Economies 2.8 2.3 0.7 -3.1 1.3

United States 2.8 2.0 1.1 -2.4 2.2

Eurozone 3.0 2.7 0.7 -3.8 0.0

Japan 2.1 2.4 -0.7 -3.7 2.0

Emerging Markets 7.5 7.8 5.6 1.2 4.7

Latin America 5.4 5.5 4.1 -1.3 2.1

EMEA 6.5 6.3 4.4 -2.9 2.6

Emerging Asia 9.2 9.9 7.1 4.6 6.9

World 3.8 3.5 1.8 -2.2 2.1

23

Concluding Messages

The global economy has been in free-fall for six months, but there are some tentative signs that this is moderating.

In the months ahead, a return to a desynchronized global economy is likely.

A significant increase in global unemployment is now underway, however.

Massive, unprecedented, global policy easing is now underway, the long-term implications of which are somewhat unclear.

Major challenges lie ahead in Europe.

The global backdrop for Asia and Latin America remains very tough, but has improved slightly in the past few months.

When and How will the Global Economy Recover ?

Philip SuttleIIF, Director of Global Macroeconomic Analysis

Garanti Masters Private Banking Conference Istanbul, Turkey

April 17, 2009

Related Documents